Endogenous risk in a DSGE model with capital-constrained financial intermediaries

|

|

|

- Cleopatra Carroll

- 5 years ago

- Views:

Transcription

1 Endogenous risk in a DSGE model with capital-constrained financial intermediaries Hans Dewachter (NBB-KUL) and Raf Wouters (NBB) NBB-Conference, Brussels, October 2012 PP 1

2 motivation/objective introduce endogenous financial risk in a standard DSGE macromodel: Mendoza (2010), Br&Sa (2012) and He&Kr (2012) use specific, small-scale models common framework for analysing traditional monetary policy questions (inflation, output gap) and financial stability concerns (risk, volatility, asset pricing, credit supply) financial risk is priced by financial intermediaries that are occasionally capital- constrained (following He and Krishnamurthy (2012)): see also Gilchrist Zakrajeck (2012) and Adrian et al. (2012) use local third-order perturbation approach to solve the model: evaluate the trade-off between approximation errors and computational efficiency of the solution that is also applicable to models with a larger state vector PP 2

3 outline of the paper/presentation start from a simplified version of He and Krishnamurthy (2012): continuous-time, global solution with occasionally-binding capital constraint main mechanism behind endogenous risk channel local third-order approximation of this simple model: occasionally-binding constraint => non-linear but continuous approximation global dynamics => local solution with third-order perturbation method application of this methododology in a standard DSGE macromodel: evaluate the risk channel in a model with additional real and nominal frictions counterfactual simulation illustrating the potential role of the risk channel interaction with monetary policy behavior: risk and risk-free interest rate PP 3

4 Simplified version of He and Krishnamurthy (2012) simplification: only productive capital stock (no housing stock) households: maximize expected utility of consumption and allocate their wealth between risk-free deposits and equity of financial intermediaries financial intermediaries: maximize expected utility of reputation (function of past return performance) subject to their balance sheet => mean-variance portfolio optimization production: simple AK production technology (Y=AK) and quadratic adjustment costs in capital accumulation financial frictions: households have no direct access to the capital market (financial intermediary is the marginal investor in capital), and their equity holdings in FI are restricted by the reputation of the intermediary => FI occasionally capital-constrained PP 4

5 Simplified version of He and Krishnamurthy (2012) PP 5

6 Simplified version of He and Krishnamurthy (2012) V e = min(,(1- )W) PP 6

7 Simplified version of He and Krishnamurthy (2012) optimal leverage of financial intermediaries: capital market equilibrium: occasional constraint on HH equity position: reputation dynamics: => equilibrium required return on capital: with both time-varying coefficients and dependent on the volatility of reputation and the sensitivity of the asset price to reputation PP 7

8 Simplified version of He and Krishnamurthy (2012) optimal leverage of financial intermediaries: capital market equilibrium: occasional constraint on HH equity position: reputation dynamics: => equilibrium required return on capital: => endogenous risk channel: exog. shock to the efficiency of capital => PP 8

9 Simplified version of He and Krishnamurthy (2012) optimal leverage of financial intermediaries: capital market equilibrium: occasional constraint on HH equity position: reputation dynamics: => equilibrium required return on capital: => endogenous risk channel: exog. shock to the efficiency of capital => => => PP 9

10 Simplified version of He and Krishnamurthy (2012) optimal leverage of financial intermediaries: capital market equilibrium: occasional constraint on HH equity position: reputation dynamics: => equilibrium required return on capital: => endogenous risk channel: exog. shock to the efficiency of capital => => => => PP 10

11 Simplified version of He and Krishnamurthy (2012) optimal leverage of financial intermediaries: capital market equilibrium: occasional constraint on HH equity position: reputation dynamics: => equilibrium required return on capital: => endogenous risk channel: exog. shock to the efficiency of capital => => => => => PP 11

12 Simplified version of He and Krishnamurthy (2012) optimal leverage of financial intermediaries: capital market equilibrium: occasional constraint on HH equity position: reputation dynamics: => equilibrium required return on capital: => endogenous risk channel: exog. shock to the efficiency of capital => => => => => => PP 12

13 Simplified version of He and Krishnamurthy (2012) optimal leverage of financial intermediaries: capital market equilibrium: occasional constraint on HH equity position: reputation dynamics: => equilibrium required return on capital: => endogenous risk channel: exog. shock to the efficiency of capital => => => => => => => PP 13

14 Simplified version of He and Krishnamurthy (2012) optimal leverage of financial intermediaries: capital market equilibrium: occasional constraint on HH equity position: reputation dynamics: => equilibrium required return on capital: => endogenous risk channel: exog. shock to the efficiency of capital => => => => => => => => => PP 14

15 Simplified version of He and Krishnamurthy (2012) calibration similar to He and Krishnamurthy (2012) but with lower volatility for the exogenous shock to the efficiency of capital (2% instead of 5%): PP 15

16 40 Leverage ( FI ) 0.8 Equity (V) Non-binding constraint Risk premium (EdR-rdt) 0.05 Non-binding constraint I/K Non-binding constraint Scaled intermediary reputation (e) 0.2 Non-binding constraint Asset price (Q) Capital price 0.6 Wealth of equity household Non-binding constraint C/K Non-binding constraint Scaled intermediary reputation (e) PP 16

17 Simple version of He and Krishnamurthy (2012) PP 17

18 Simplified version of He and Krishnamurthy (2012) this model generates an important risk channel: "endogenous" risk and volatility in asset prices >> fundamental exogenous productivity risk the role of risk is particular striking when the capital constraint on financial intermediaries becomes binding two useful extensions: the interaction and feedback between financial and real variables can be reinforced with a more complex transmission mechanism from asset prices on production or consumption decisions (e.g. credit contraint on working capital) occasionally-binding minimum constraint in HH risk position can be replaced by a non-linear but continuous function => necessary step for local perturbation PP 18

19 Local approximation He and Krishnamurthy specify their model in continuous time and solve the global dynamics with shifts between regimes with a binding and non-binding capital constraint By replacing the minimum constraint on HH risky position by a continuous portfolio rule, we can solve the model locally with a much more efficient perturbation approach: ==> The model, more precisly the reputation of the FI, is indeterminate under a first-order approximation but with a third-order approximation the risk channel generates a stable outcome:. The approximation is taken around the center of the stochastic distribution. and are selected to approximate the minconstraint. PP 19

20 S-HeKr local approximation of S-HeKr PP 20

21 Local approximation PP 21

22 Local approximation the local approximation can reproduce quite precisely the dynamics of the leverage and the equity of the FI risk aversion and the risk premium are time-varying and linear functions of the reputation-state of the FI the convex relation between risk premium and reputation is lost in the approximation => we retain a first-order approximation of the risk channel with our local approximation the amount of risk (vol) and the price of risk are relatively small because the exogenous volatility is small and because the model has a very weak internal propagation mechanism => apply this methodology in a standard DSGE macromodel with real and nominal frictions that reinforces the propagation of the exogenous shock PP 22

23 Application in DSGE model model extentions with a more realistic production and distribution specification: endogenous labor supply, habit in preferences and GHH utility function for HH CD production problem with fixed costs that correspond to the price markup monopolistic competition in good and labor markets nominal price and wage stickiness monetary policy rule: simple inflation targeting strategy => many of these frictions increase the propagation of exogenous shocks and, important for asset pricing, increase the volatility of dividend returns for the FI PP 23

24 Application in DSGE model Calibration and estimation of the productivity shock as single fundamental shock estimation with four US-data Y, C, I and W/P growth over the period 1955q1-2011q2 PP 24

25 S-HeKr local approximation of S-HeKr DSGE-model PP 25

26 Application in DSGE model PP 26

27 Application in DSGE model the impulse response analysis helps to understand the transmission of the productivity shocks: the IRFs are state-dependent: impact is different in states with high, medium and low reputation compare also with the effect under certainty equivalence (first-order approximation): the difference between the third-order and the first-order solution is a proxy for the risk channel in the economy graphs plot the IRFs for a one standard error decline in the productivity shock (0.75%) PP 27

28 PP 28

29 PP 29

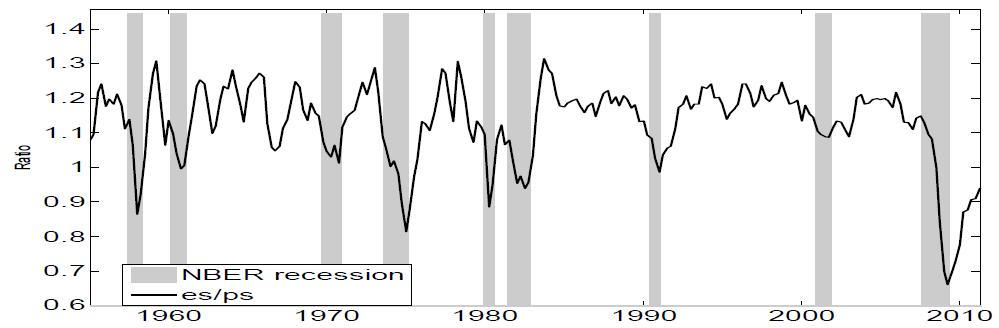

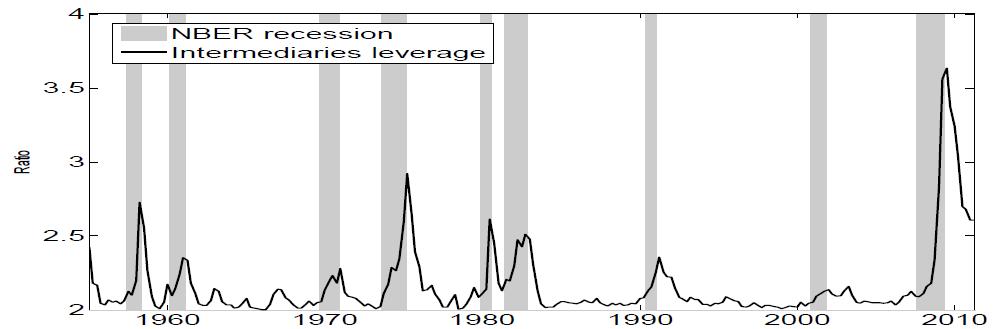

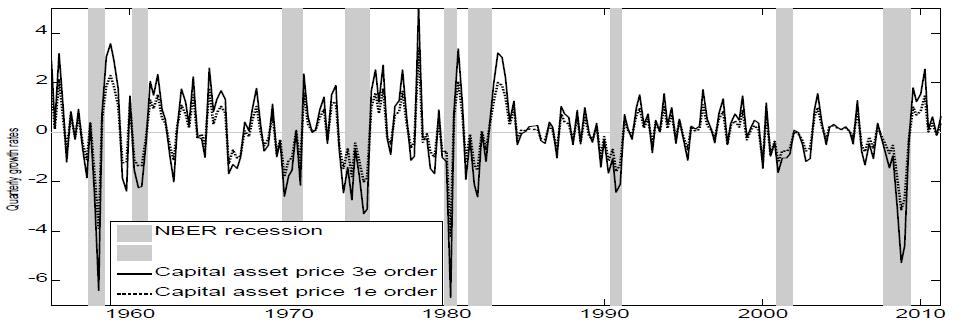

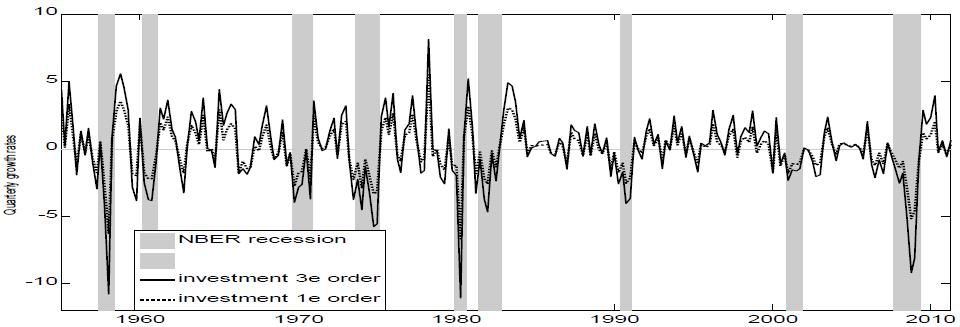

30 Application in DSGE model historical counterfactual simulation: using the model-consistent estimate for the productivity process and the implied transmission mechanism, we obtain an estimate of the potential contribution of the risk channel to the historical macroeconomic realisations by comparing the outcomes under third-order and first-order: important contribution of the risk channel in the transmission of fundamental shocks strong interaction between monetary policy and risk premium PP 30

31 PP 31

32 PP 32

33 PP 33

34 PP 34

35 PP 35

36 PP 36

37 PP 37

38 Application in DSGE model historical counterfactual simulation: using the model-consistent estimate for the productivity process and the implied transmission mechanism, we obtain an estimate of the potential contribution of the risk channel to the historical macroeconomic realisations by comparing the outcomes under third-order and first-order: important contribution of the risk channel in the transmission of fundamental shocks strong interaction between monetary policy and risk premium with only fundamental productivity shocks, the financial cycle and the business cycle have a synchronous development: => specific shocks to FI, e.g. subprime mortgage shock, can make the financial sector much more vulnerable with important spillover risks to the real economy PP 38

39 Sensitivity analysis PP 39

40 Concluding remarks our local perturbation approach delivers a first-order approximation to the risk channel implied by the global dynamics of the model: substantial approximation errors but interesting insights on the risk channel in larger models full gain from computational efficiency only realized in empirical validation FI are confronted with more complex constraints and firms can also finance themselves directly on the capital market => many extensions are necessary many interesting policy applications are possible with this setup: evaluate the traditional inflation objective together with objectives in terms of risk, volatility and strength of the FI introduce specific instruments of macro-prudential regulation PP 40

41 PP 41

Non-standard monetary policy, asset prices and macroprudential policy in a monetary union. L. Burlon, A. Gerali, A. Notarpietro and M.

Non-standard monetary policy, asset prices and macroprudential policy in a monetary union L. Burlon, A. Gerali, A. Notarpietro and M. Pisani Discussion by Raf Wouters (NBB) Unconventional monetary policy:

Non-standard monetary policy, asset prices and macroprudential policy in a monetary union L. Burlon, A. Gerali, A. Notarpietro and M. Pisani Discussion by Raf Wouters (NBB) Unconventional monetary policy:

Working Paper Research. Endogenous risk in a DSGE model with capital-constrained financial intermediaries. October 2012 No 235

Endogenous risk in a DSGE model with capital-constrained financial intermediaries Working Paper Research by H. Dewachter and R. Wouters October 2012 No 235 Editorial Director Jan Smets, Member of the Board

Endogenous risk in a DSGE model with capital-constrained financial intermediaries Working Paper Research by H. Dewachter and R. Wouters October 2012 No 235 Editorial Director Jan Smets, Member of the Board

A Macroeconomic Framework for Quantifying Systemic Risk. June 2012

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He Arvind Krishnamurthy University of Chicago & NBER Northwestern University & NBER June 212 Systemic Risk Systemic risk: risk (probability)

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He Arvind Krishnamurthy University of Chicago & NBER Northwestern University & NBER June 212 Systemic Risk Systemic risk: risk (probability)

Overborrowing, Financial Crises and Macro-prudential Policy

Overborrowing, Financial Crises and Macro-prudential Policy Javier Bianchi University of Wisconsin Enrique G. Mendoza University of Maryland & NBER The case for macro-prudential policies Credit booms are

Overborrowing, Financial Crises and Macro-prudential Policy Javier Bianchi University of Wisconsin Enrique G. Mendoza University of Maryland & NBER The case for macro-prudential policies Credit booms are

A Macroeconomic Framework for Quantifying Systemic Risk

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Northwestern University and NBER December 2013 He and Krishnamurthy (Chicago, Northwestern)

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Northwestern University and NBER December 2013 He and Krishnamurthy (Chicago, Northwestern)

Credit Shocks and the U.S. Business Cycle. Is This Time Different? Raju Huidrom University of Virginia. Midwest Macro Conference

Credit Shocks and the U.S. Business Cycle: Is This Time Different? Raju Huidrom University of Virginia May 31, 214 Midwest Macro Conference Raju Huidrom Credit Shocks and the U.S. Business Cycle Background

Credit Shocks and the U.S. Business Cycle: Is This Time Different? Raju Huidrom University of Virginia May 31, 214 Midwest Macro Conference Raju Huidrom Credit Shocks and the U.S. Business Cycle Background

A Macroeconomic Framework for Quantifying Systemic Risk

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Stanford University and NBER Bank of Canada, August 2017 He and Krishnamurthy (Chicago,

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Stanford University and NBER Bank of Canada, August 2017 He and Krishnamurthy (Chicago,

Discussion of. Commodity Price Movements in a General Equilibrium Model of Storage. David M. Arsenau and Sylvain Leduc

Discussion of Commodity Price Movements in a General Equilibrium Model of Storage David M. Arsenau and Sylvain Leduc by Raf Wouters (NBB) "Policy Responses to Commodity Price Movements", 6-7 April 2012,

Discussion of Commodity Price Movements in a General Equilibrium Model of Storage David M. Arsenau and Sylvain Leduc by Raf Wouters (NBB) "Policy Responses to Commodity Price Movements", 6-7 April 2012,

Monetary Policy in Pakistan: Confronting Fiscal Dominance and Imperfect Credibility

Monetary Policy in Pakistan: Confronting Fiscal Dominance and Imperfect Credibility Ehsan Choudhri Carleton University Hamza Malik State Bank of Pakistan Background State Bank of Pakistan (SBP) has been

Monetary Policy in Pakistan: Confronting Fiscal Dominance and Imperfect Credibility Ehsan Choudhri Carleton University Hamza Malik State Bank of Pakistan Background State Bank of Pakistan (SBP) has been

A Macroeconomic Framework for Quantifying Systemic Risk

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Northwestern University and NBER May 2013 He and Krishnamurthy (Chicago, Northwestern)

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Northwestern University and NBER May 2013 He and Krishnamurthy (Chicago, Northwestern)

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

Booms and Banking Crises

Booms and Banking Crises F. Boissay, F. Collard and F. Smets Macro Financial Modeling Conference Boston, 12 October 2013 MFM October 2013 Conference 1 / Disclaimer The views expressed in this presentation

Booms and Banking Crises F. Boissay, F. Collard and F. Smets Macro Financial Modeling Conference Boston, 12 October 2013 MFM October 2013 Conference 1 / Disclaimer The views expressed in this presentation

A Macroeconomic Framework for Quantifying Systemic Risk

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Stanford University and NBER March 215 He and Krishnamurthy (Chicago, Stanford) Systemic

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Stanford University and NBER March 215 He and Krishnamurthy (Chicago, Stanford) Systemic

Monetary Theory and Policy. Fourth Edition. Carl E. Walsh. The MIT Press Cambridge, Massachusetts London, England

Monetary Theory and Policy Fourth Edition Carl E. Walsh The MIT Press Cambridge, Massachusetts London, England Contents Preface Introduction xiii xvii 1 Evidence on Money, Prices, and Output 1 1.1 Introduction

Monetary Theory and Policy Fourth Edition Carl E. Walsh The MIT Press Cambridge, Massachusetts London, England Contents Preface Introduction xiii xvii 1 Evidence on Money, Prices, and Output 1 1.1 Introduction

Operationalizing the Selection and Application of Macroprudential Instruments

Operationalizing the Selection and Application of Macroprudential Instruments Presented by Tobias Adrian, Federal Reserve Bank of New York Based on Committee for Global Financial Stability Report 48 The

Operationalizing the Selection and Application of Macroprudential Instruments Presented by Tobias Adrian, Federal Reserve Bank of New York Based on Committee for Global Financial Stability Report 48 The

To explore and to clarify

To explore and to clarify CPB Ministry of Finance, Oslo October 2016 Albert van der Horst To explore and to clarify To explore macroeconomic questions macroeconomic developments => projections impact of

To explore and to clarify CPB Ministry of Finance, Oslo October 2016 Albert van der Horst To explore and to clarify To explore macroeconomic questions macroeconomic developments => projections impact of

A Macroeconomic Model with Financial Panics

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 218 1 The views expressed in this paper are those of the authors

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 218 1 The views expressed in this paper are those of the authors

Macroeconomic Modelling at the Central Bank of Brazil. Angelo M. Fasolo Research Department

Macroeconomic Modelling at the Central Bank of Brazil Angelo M. Fasolo Research Department Introduction Economic analysis at the BCB based on three type of models: Small-scale semi-structural models, focused

Macroeconomic Modelling at the Central Bank of Brazil Angelo M. Fasolo Research Department Introduction Economic analysis at the BCB based on three type of models: Small-scale semi-structural models, focused

Macroprudential Policies in a Low Interest-Rate Environment

Macroprudential Policies in a Low Interest-Rate Environment Margarita Rubio 1 Fang Yao 2 1 University of Nottingham 2 Reserve Bank of New Zealand. The views expressed in this paper do not necessarily reflect

Macroprudential Policies in a Low Interest-Rate Environment Margarita Rubio 1 Fang Yao 2 1 University of Nottingham 2 Reserve Bank of New Zealand. The views expressed in this paper do not necessarily reflect

II.3. Rising sovereign risk premia and the profile of fiscal consolidation ( 35 )

") II.3 Rising sovereign risk premia and the profile of fiscal consolidation II.3. Rising sovereign risk premia and the profile of fiscal consolidation ( 35 ) Higher sovereign risk premia can have important

II.3 Rising sovereign risk premia and the profile of fiscal consolidation II.3. Rising sovereign risk premia and the profile of fiscal consolidation ( 35 ) Higher sovereign risk premia can have important

Financial Amplification, Regulation and Long-term Lending

Financial Amplification, Regulation and Long-term Lending Michael Reiter 1 Leopold Zessner 2 1 Instiute for Advances Studies, Vienna 2 Vienna Graduate School of Economics Barcelona GSE Summer Forum ADEMU,

Financial Amplification, Regulation and Long-term Lending Michael Reiter 1 Leopold Zessner 2 1 Instiute for Advances Studies, Vienna 2 Vienna Graduate School of Economics Barcelona GSE Summer Forum ADEMU,

Should Unconventional Monetary Policies Become Conventional?

Should Unconventional Monetary Policies Become Conventional? Dominic Quint and Pau Rabanal Discussant: Annette Vissing-Jorgensen, University of California Berkeley and NBER Question: Should LSAPs be used

Should Unconventional Monetary Policies Become Conventional? Dominic Quint and Pau Rabanal Discussant: Annette Vissing-Jorgensen, University of California Berkeley and NBER Question: Should LSAPs be used

A Macroeconomic Framework for Quantifying Systemic Risk

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Northwestern University and NBER November 2012 He and Krishnamurthy (Chicago, Northwestern)

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Northwestern University and NBER November 2012 He and Krishnamurthy (Chicago, Northwestern)

A DSGE model to assess the post crisis regulation of universal banks

A DSGE model to assess the post crisis regulation of universal banks O. de Bandt 1 M. Chahad 2 1 Banque de France - ACPR and University of Paris Ouest 2 Banque de France 4 th EBA Policy Research Workshop

A DSGE model to assess the post crisis regulation of universal banks O. de Bandt 1 M. Chahad 2 1 Banque de France - ACPR and University of Paris Ouest 2 Banque de France 4 th EBA Policy Research Workshop

The Implications for Fiscal Policy Considering Rule-of-Thumb Consumers in the New Keynesian Model for Romania

Vol. 3, No.3, July 2013, pp. 365 371 ISSN: 2225-8329 2013 HRMARS www.hrmars.com The Implications for Fiscal Policy Considering Rule-of-Thumb Consumers in the New Keynesian Model for Romania Ana-Maria SANDICA

Vol. 3, No.3, July 2013, pp. 365 371 ISSN: 2225-8329 2013 HRMARS www.hrmars.com The Implications for Fiscal Policy Considering Rule-of-Thumb Consumers in the New Keynesian Model for Romania Ana-Maria SANDICA

International Monetary Policy Coordination and Financial Market Integration

An important paper that opens an important conference. In my discussion I will attempt to: cast the paper within the broader context of the current literature and debate on coordination; suggest an interpretation

An important paper that opens an important conference. In my discussion I will attempt to: cast the paper within the broader context of the current literature and debate on coordination; suggest an interpretation

Oil Shocks and the Zero Bound on Nominal Interest Rates

Oil Shocks and the Zero Bound on Nominal Interest Rates Martin Bodenstein, Luca Guerrieri, Christopher Gust Federal Reserve Board "Advances in International Macroeconomics - Lessons from the Crisis," Brussels,

Oil Shocks and the Zero Bound on Nominal Interest Rates Martin Bodenstein, Luca Guerrieri, Christopher Gust Federal Reserve Board "Advances in International Macroeconomics - Lessons from the Crisis," Brussels,

Monetary Policy in Pakistan: The Role of Foreign Exchange and Credit Markets

Monetary Policy in Pakistan: The Role of Foreign Exchange and Credit Markets Ehsan Choudhri Distinguished Research Professor Carleton University ehsan.choudhri@carleton.ca and Hamza Ali Malik Director,

Monetary Policy in Pakistan: The Role of Foreign Exchange and Credit Markets Ehsan Choudhri Distinguished Research Professor Carleton University ehsan.choudhri@carleton.ca and Hamza Ali Malik Director,

Assessing the Spillover Effects of Changes in Bank Capital Regulation Using BoC-GEM-Fin: A Non-Technical Description

Assessing the Spillover Effects of Changes in Bank Capital Regulation Using BoC-GEM-Fin: A Non-Technical Description Carlos de Resende, Ali Dib, and Nikita Perevalov International Economic Analysis Department

Assessing the Spillover Effects of Changes in Bank Capital Regulation Using BoC-GEM-Fin: A Non-Technical Description Carlos de Resende, Ali Dib, and Nikita Perevalov International Economic Analysis Department

Intermediary Balance Sheets Tobias Adrian and Nina Boyarchenko, NY Fed Discussant: Annette Vissing-Jorgensen, UC Berkeley

Intermediary Balance Sheets Tobias Adrian and Nina Boyarchenko, NY Fed Discussant: Annette Vissing-Jorgensen, UC Berkeley Objective: Construct a general equilibrium model with two types of intermediaries:

Intermediary Balance Sheets Tobias Adrian and Nina Boyarchenko, NY Fed Discussant: Annette Vissing-Jorgensen, UC Berkeley Objective: Construct a general equilibrium model with two types of intermediaries:

Lecture 2 General Equilibrium Models: Finite Period Economies

Lecture 2 General Equilibrium Models: Finite Period Economies Introduction In macroeconomics, we study the behavior of economy-wide aggregates e.g. GDP, savings, investment, employment and so on - and

Lecture 2 General Equilibrium Models: Finite Period Economies Introduction In macroeconomics, we study the behavior of economy-wide aggregates e.g. GDP, savings, investment, employment and so on - and

MA Advanced Macroeconomics: 11. The Smets-Wouters Model

MA Advanced Macroeconomics: 11. The Smets-Wouters Model Karl Whelan School of Economics, UCD Spring 2016 Karl Whelan (UCD) The Smets-Wouters Model Spring 2016 1 / 23 A Popular DSGE Model Now we will discuss

MA Advanced Macroeconomics: 11. The Smets-Wouters Model Karl Whelan School of Economics, UCD Spring 2016 Karl Whelan (UCD) The Smets-Wouters Model Spring 2016 1 / 23 A Popular DSGE Model Now we will discuss

Overborrowing, Financial Crises and Macro-prudential Policy. Macro Financial Modelling Meeting, Chicago May 2-3, 2013

Overborrowing, Financial Crises and Macro-prudential Policy Javier Bianchi University of Wisconsin & NBER Enrique G. Mendoza Universtiy of Pennsylvania & NBER Macro Financial Modelling Meeting, Chicago

Overborrowing, Financial Crises and Macro-prudential Policy Javier Bianchi University of Wisconsin & NBER Enrique G. Mendoza Universtiy of Pennsylvania & NBER Macro Financial Modelling Meeting, Chicago

Intermediary Asset Pricing

Intermediary Asset Pricing Z. He and A. Krishnamurthy - AER (2012) Presented by Omar Rachedi 18 September 2013 Introduction Motivation How to account for risk premia? Standard models assume households

Intermediary Asset Pricing Z. He and A. Krishnamurthy - AER (2012) Presented by Omar Rachedi 18 September 2013 Introduction Motivation How to account for risk premia? Standard models assume households

Macroeconometric Modeling (Session B) 7 July / 15

7 July / 15") Macroeconometric Modeling (Session B) 7 July 2010 1 / 15 Plan of presentation Aim: assessing the implications for the Italian economy of a number of structural reforms, showing potential gains and limitations

Macroeconometric Modeling (Session B) 7 July 2010 1 / 15 Plan of presentation Aim: assessing the implications for the Italian economy of a number of structural reforms, showing potential gains and limitations

A Policy Model for Analyzing Macroprudential and Monetary Policies

A Policy Model for Analyzing Macroprudential and Monetary Policies Sami Alpanda Gino Cateau Cesaire Meh Bank of Canada November 2013 Alpanda, Cateau, Meh (Bank of Canada) ()Macroprudential - Monetary Policy

A Policy Model for Analyzing Macroprudential and Monetary Policies Sami Alpanda Gino Cateau Cesaire Meh Bank of Canada November 2013 Alpanda, Cateau, Meh (Bank of Canada) ()Macroprudential - Monetary Policy

Oil Price Shock and Optimal Monetary Policy in a Model of Small Open Oil Exporting Economy - Case of Iran 1

Journal of Money and Economy Vol. 8, No.3 Summer 2013 Oil Price Shock and Optimal Monetary Policy in a Model of Small Open Oil Exporting Economy - Case of Iran 1 Rabee Hamedani, Hasti 2 Pedram, Mehdi 3

Journal of Money and Economy Vol. 8, No.3 Summer 2013 Oil Price Shock and Optimal Monetary Policy in a Model of Small Open Oil Exporting Economy - Case of Iran 1 Rabee Hamedani, Hasti 2 Pedram, Mehdi 3

On the Merits of Conventional vs Unconventional Fiscal Policy

On the Merits of Conventional vs Unconventional Fiscal Policy Matthieu Lemoine and Jesper Lindé Banque de France and Sveriges Riksbank The views expressed in this paper do not necessarily reflect those

On the Merits of Conventional vs Unconventional Fiscal Policy Matthieu Lemoine and Jesper Lindé Banque de France and Sveriges Riksbank The views expressed in this paper do not necessarily reflect those

Simulations of the macroeconomic effects of various

VI Investment Simulations of the macroeconomic effects of various policy measures or other exogenous shocks depend importantly on how one models the responsiveness of the components of aggregate demand

VI Investment Simulations of the macroeconomic effects of various policy measures or other exogenous shocks depend importantly on how one models the responsiveness of the components of aggregate demand

Capital regulation and macroeconomic activity

1/35 Capital regulation and macroeconomic activity Implications for macroprudential policy Roland Meeks Monetary Assessment & Strategy Division, Bank of England and Department of Economics, University

1/35 Capital regulation and macroeconomic activity Implications for macroprudential policy Roland Meeks Monetary Assessment & Strategy Division, Bank of England and Department of Economics, University

Self-fulfilling Recessions at the ZLB

Self-fulfilling Recessions at the ZLB Charles Brendon (Cambridge) Matthias Paustian (Board of Governors) Tony Yates (Birmingham) August 2016 Introduction This paper is about recession dynamics at the ZLB

Self-fulfilling Recessions at the ZLB Charles Brendon (Cambridge) Matthias Paustian (Board of Governors) Tony Yates (Birmingham) August 2016 Introduction This paper is about recession dynamics at the ZLB

The Role of Investment Wedges in the Carlstrom-Fuerst Economy and Business Cycle Accounting

MPRA Munich Personal RePEc Archive The Role of Investment Wedges in the Carlstrom-Fuerst Economy and Business Cycle Accounting Masaru Inaba and Kengo Nutahara Research Institute of Economy, Trade, and

MPRA Munich Personal RePEc Archive The Role of Investment Wedges in the Carlstrom-Fuerst Economy and Business Cycle Accounting Masaru Inaba and Kengo Nutahara Research Institute of Economy, Trade, and

General Examination in Macroeconomic Theory. Fall 2010

HARVARD UNIVERSITY DEPARTMENT OF ECONOMICS General Examination in Macroeconomic Theory Fall 2010 ----------------------------------------------------------------------------------------------------------------

HARVARD UNIVERSITY DEPARTMENT OF ECONOMICS General Examination in Macroeconomic Theory Fall 2010 ----------------------------------------------------------------------------------------------------------------

1. Cash-in-Advance models a. Basic model under certainty b. Extended model in stochastic case. recommended)

") Monetary Economics: Macro Aspects, 26/2 2013 Henrik Jensen Department of Economics University of Copenhagen 1. Cash-in-Advance models a. Basic model under certainty b. Extended model in stochastic case

Monetary Economics: Macro Aspects, 26/2 2013 Henrik Jensen Department of Economics University of Copenhagen 1. Cash-in-Advance models a. Basic model under certainty b. Extended model in stochastic case

Transmission of fiscal policy shocks into Romania's economy

THE BUCHAREST ACADEMY OF ECONOMIC STUDIES Doctoral School of Finance and Banking Transmission of fiscal policy shocks into Romania's economy Supervisor: Prof. Moisă ALTĂR Author: Georgian Valentin ŞERBĂNOIU

THE BUCHAREST ACADEMY OF ECONOMIC STUDIES Doctoral School of Finance and Banking Transmission of fiscal policy shocks into Romania's economy Supervisor: Prof. Moisă ALTĂR Author: Georgian Valentin ŞERBĂNOIU

Discussion of Gerali, Neri, Sessa, Signoretti. Credit and Banking in a DSGE Model

Discussion of Gerali, Neri, Sessa and Signoretti Credit and Banking in a DSGE Model Jesper Lindé Federal Reserve Board ty ECB, Frankfurt December 15, 2008 Summary of paper This interesting paper... Extends

Discussion of Gerali, Neri, Sessa and Signoretti Credit and Banking in a DSGE Model Jesper Lindé Federal Reserve Board ty ECB, Frankfurt December 15, 2008 Summary of paper This interesting paper... Extends

Financial Factors in Business Cycles

Financial Factors in Business Cycles Lawrence J. Christiano, Roberto Motto, Massimo Rostagno 30 November 2007 The views expressed are those of the authors only What We Do? Integrate financial factors into

Financial Factors in Business Cycles Lawrence J. Christiano, Roberto Motto, Massimo Rostagno 30 November 2007 The views expressed are those of the authors only What We Do? Integrate financial factors into

Inflation Stabilization and Default Risk in a Currency Union. OKANO, Eiji Nagoya City University at Otaru University of Commerce on Aug.

Inflation Stabilization and Default Risk in a Currency Union OKANO, Eiji Nagoya City University at Otaru University of Commerce on Aug. 10, 2014 1 Introduction How do we conduct monetary policy in a currency

Inflation Stabilization and Default Risk in a Currency Union OKANO, Eiji Nagoya City University at Otaru University of Commerce on Aug. 10, 2014 1 Introduction How do we conduct monetary policy in a currency

A Small Open Economy DSGE Model for an Oil Exporting Emerging Economy

A Small Open Economy DSGE Model for an Oil Exporting Emerging Economy Iklaga, Fred Ogli University of Surrey f.iklaga@surrey.ac.uk Presented at the 33rd USAEE/IAEE North American Conference, October 25-28,

A Small Open Economy DSGE Model for an Oil Exporting Emerging Economy Iklaga, Fred Ogli University of Surrey f.iklaga@surrey.ac.uk Presented at the 33rd USAEE/IAEE North American Conference, October 25-28,

Money and monetary policy in Israel during the last decade

Money and monetary policy in Israel during the last decade Money Macro and Finance Research Group 47 th Annual Conference Jonathan Benchimol 1 This presentation does not necessarily reflect the views of

Money and monetary policy in Israel during the last decade Money Macro and Finance Research Group 47 th Annual Conference Jonathan Benchimol 1 This presentation does not necessarily reflect the views of

Dynamic Macroeconomics

Chapter 1 Introduction Dynamic Macroeconomics Prof. George Alogoskoufis Fletcher School, Tufts University and Athens University of Economics and Business 1.1 The Nature and Evolution of Macroeconomics

Chapter 1 Introduction Dynamic Macroeconomics Prof. George Alogoskoufis Fletcher School, Tufts University and Athens University of Economics and Business 1.1 The Nature and Evolution of Macroeconomics

Aggregate Effects of Collateral Constraints

Thomas Chaney, Zongbo Huang, David Sraer, David Thesmar discussion by Toni Whited 2016 WFA The goal of the paper is to quantify the welfare effects of collateral constraints. Reduced form regressions of

Thomas Chaney, Zongbo Huang, David Sraer, David Thesmar discussion by Toni Whited 2016 WFA The goal of the paper is to quantify the welfare effects of collateral constraints. Reduced form regressions of

ALM Analysis for a Pensionskasse

ALM Analysis for a Pensionskasse Asset Liability Management Study Francesco Sandrini MSc, PhD New Thinking in Finance London, February 14 th 2014 For Internal Use Only. Not to be Distributed to the Public.

ALM Analysis for a Pensionskasse Asset Liability Management Study Francesco Sandrini MSc, PhD New Thinking in Finance London, February 14 th 2014 For Internal Use Only. Not to be Distributed to the Public.

1. Money in the utility function (continued)

") Monetary Economics: Macro Aspects, 19/2 2013 Henrik Jensen Department of Economics University of Copenhagen 1. Money in the utility function (continued) a. Welfare costs of in ation b. Potential non-superneutrality

Monetary Economics: Macro Aspects, 19/2 2013 Henrik Jensen Department of Economics University of Copenhagen 1. Money in the utility function (continued) a. Welfare costs of in ation b. Potential non-superneutrality

Chapter 9 Dynamic Models of Investment

George Alogoskoufis, Dynamic Macroeconomic Theory, 2015 Chapter 9 Dynamic Models of Investment In this chapter we present the main neoclassical model of investment, under convex adjustment costs. This

George Alogoskoufis, Dynamic Macroeconomic Theory, 2015 Chapter 9 Dynamic Models of Investment In this chapter we present the main neoclassical model of investment, under convex adjustment costs. This

Comment. The New Keynesian Model and Excess Inflation Volatility

Comment Martín Uribe, Columbia University and NBER This paper represents the latest installment in a highly influential series of papers in which Paul Beaudry and Franck Portier shed light on the empirics

Comment Martín Uribe, Columbia University and NBER This paper represents the latest installment in a highly influential series of papers in which Paul Beaudry and Franck Portier shed light on the empirics

Financial intermediaries in an estimated DSGE model for the UK

Financial intermediaries in an estimated DSGE model for the UK Stefania Villa a Jing Yang b a Birkbeck College b Bank of England Cambridge Conference - New Instruments of Monetary Policy: The Challenges

Financial intermediaries in an estimated DSGE model for the UK Stefania Villa a Jing Yang b a Birkbeck College b Bank of England Cambridge Conference - New Instruments of Monetary Policy: The Challenges

Outline. 1. Overall Impression. 2. Summary. Discussion of. Volker Wieland. Congratulations!

ECB Conference Global Financial Linkages, Transmission of Shocks and Asset Prices Frankfurt, December 1-2, 2008 Discussion of Real effects of the subprime mortgage crisis by Hui Tong and Shang-Jin Wei

ECB Conference Global Financial Linkages, Transmission of Shocks and Asset Prices Frankfurt, December 1-2, 2008 Discussion of Real effects of the subprime mortgage crisis by Hui Tong and Shang-Jin Wei

Idiosyncratic risk, insurance, and aggregate consumption dynamics: a likelihood perspective

Idiosyncratic risk, insurance, and aggregate consumption dynamics: a likelihood perspective Alisdair McKay Boston University June 2013 Microeconomic evidence on insurance - Consumption responds to idiosyncratic

Idiosyncratic risk, insurance, and aggregate consumption dynamics: a likelihood perspective Alisdair McKay Boston University June 2013 Microeconomic evidence on insurance - Consumption responds to idiosyncratic

Commentary: Using models for monetary policy. analysis

Commentary: Using models for monetary policy analysis Carl E. Walsh U. C. Santa Cruz September 2009 This draft: Oct. 26, 2009 Modern policy analysis makes extensive use of dynamic stochastic general equilibrium

Commentary: Using models for monetary policy analysis Carl E. Walsh U. C. Santa Cruz September 2009 This draft: Oct. 26, 2009 Modern policy analysis makes extensive use of dynamic stochastic general equilibrium

Kaplan, Moll and Violante: Unconventional Monetary Policy in HANK

Discussion of Kaplan, Moll and Violante: Unconventional Monetary Policy in HANK Workshop on Current Monetary Policy Challenges Jirka Slacalek European Central Bank www.slacalek.com ECB, December 2016 The

Discussion of Kaplan, Moll and Violante: Unconventional Monetary Policy in HANK Workshop on Current Monetary Policy Challenges Jirka Slacalek European Central Bank www.slacalek.com ECB, December 2016 The

Housing Markets and the Macroeconomy During the 2000s. Erik Hurst July 2016

Housing Markets and the Macroeconomy During the 2s Erik Hurst July 216 Macro Effects of Housing Markets on US Economy During 2s Masked structural declines in labor market o Charles, Hurst, and Notowidigdo

Housing Markets and the Macroeconomy During the 2s Erik Hurst July 216 Macro Effects of Housing Markets on US Economy During 2s Masked structural declines in labor market o Charles, Hurst, and Notowidigdo

An Estimated Two-Country DSGE Model for the Euro Area and the US Economy

An Estimated Two-Country DSGE Model for the Euro Area and the US Economy Discussion Monday June 5, 2006. Practical Issues in DSGE Modelling at Central Banks Stephen Murchison Presentation Outline 1. Paper

An Estimated Two-Country DSGE Model for the Euro Area and the US Economy Discussion Monday June 5, 2006. Practical Issues in DSGE Modelling at Central Banks Stephen Murchison Presentation Outline 1. Paper

Stabilization Policies: Equity Injections into Banks or Purchases of Assets?

Stabilization Policies: Equity Injections into Banks or Purchases of Assets? Michael Kühl 27-28 October 216 Annual Global Conference of the European Banking Institute The presentation represents the personal

Stabilization Policies: Equity Injections into Banks or Purchases of Assets? Michael Kühl 27-28 October 216 Annual Global Conference of the European Banking Institute The presentation represents the personal

Bank Capital, Agency Costs, and Monetary Policy. Césaire Meh Kevin Moran Department of Monetary and Financial Analysis Bank of Canada

Bank Capital, Agency Costs, and Monetary Policy Césaire Meh Kevin Moran Department of Monetary and Financial Analysis Bank of Canada Motivation A large literature quantitatively studies the role of financial

Bank Capital, Agency Costs, and Monetary Policy Césaire Meh Kevin Moran Department of Monetary and Financial Analysis Bank of Canada Motivation A large literature quantitatively studies the role of financial

Principles of Banking (III): Macroeconomics of Banking (1) Introduction

: Macroeconomics of Banking (1) Introduction") Principles of Banking (III): Macroeconomics of Banking (1) Jin Cao (Norges Bank Research, Oslo & CESifo, München) Outline 1 2 Disclaimer (If they care about what I say,) the views expressed in this manuscript

Principles of Banking (III): Macroeconomics of Banking (1) Jin Cao (Norges Bank Research, Oslo & CESifo, München) Outline 1 2 Disclaimer (If they care about what I say,) the views expressed in this manuscript

Have We Underestimated the Likelihood and Severity of Zero Lower Bound Events?

Have We Underestimated the Likelihood and Severity of Zero Lower Bound Events? Hess Chung, Jean Philippe Laforte, David Reifschneider, and John C. Williams 19th Annual Symposium of the Society for Nonlinear

Have We Underestimated the Likelihood and Severity of Zero Lower Bound Events? Hess Chung, Jean Philippe Laforte, David Reifschneider, and John C. Williams 19th Annual Symposium of the Society for Nonlinear

Is the Maastricht debt limit safe enough for Slovakia?

Is the Maastricht debt limit safe enough for Slovakia? Fiscal Limits and Default Risk Premia for Slovakia Moderné nástroje pre finančnú analýzu a modelovanie Zuzana Múčka June 15, 2015 Introduction Aims

Is the Maastricht debt limit safe enough for Slovakia? Fiscal Limits and Default Risk Premia for Slovakia Moderné nástroje pre finančnú analýzu a modelovanie Zuzana Múčka June 15, 2015 Introduction Aims

Credit Crises, Precautionary Savings and the Liquidity Trap October (R&R Quarterly 31, 2016Journal 1 / of19

Credit Crises, Precautionary Savings and the Liquidity Trap (R&R Quarterly Journal of nomics) October 31, 2016 Credit Crises, Precautionary Savings and the Liquidity Trap October (R&R Quarterly 31, 2016Journal

Credit Crises, Precautionary Savings and the Liquidity Trap (R&R Quarterly Journal of nomics) October 31, 2016 Credit Crises, Precautionary Savings and the Liquidity Trap October (R&R Quarterly 31, 2016Journal

Risk Premiums and Macroeconomic Dynamics in a Heterogeneous Agent Model

Risk Premiums and Macroeconomic Dynamics in a Heterogeneous Agent Model F. De Graeve y, M. Dossche z, M. Emiris x, H. Sneessens {, R. Wouters k August 1, 2009 Abstract We analyze nancial risk premiums

Risk Premiums and Macroeconomic Dynamics in a Heterogeneous Agent Model F. De Graeve y, M. Dossche z, M. Emiris x, H. Sneessens {, R. Wouters k August 1, 2009 Abstract We analyze nancial risk premiums

Was The New Deal Contractionary? Appendix C:Proofs of Propositions (not intended for publication)

") Was The New Deal Contractionary? Gauti B. Eggertsson Web Appendix VIII. Appendix C:Proofs of Propositions (not intended for publication) ProofofProposition3:The social planner s problem at date is X min

Was The New Deal Contractionary? Gauti B. Eggertsson Web Appendix VIII. Appendix C:Proofs of Propositions (not intended for publication) ProofofProposition3:The social planner s problem at date is X min

DSGE model with collateral constraint: estimation on Czech data

Proceedings of 3th International Conference Mathematical Methods in Economics DSGE model with collateral constraint: estimation on Czech data Introduction Miroslav Hloušek Abstract. Czech data shows positive

Proceedings of 3th International Conference Mathematical Methods in Economics DSGE model with collateral constraint: estimation on Czech data Introduction Miroslav Hloušek Abstract. Czech data shows positive

Money and monetary policy in the Eurozone: an empirical analysis during crises

Money and monetary policy in the Eurozone: an empirical analysis during crises Money Macro and Finance Research Group 46 th Annual Conference Jonathan Benchimol 1 and André Fourçans 2 This presentation

Money and monetary policy in the Eurozone: an empirical analysis during crises Money Macro and Finance Research Group 46 th Annual Conference Jonathan Benchimol 1 and André Fourçans 2 This presentation

1 Consumption and saving under uncertainty

1 Consumption and saving under uncertainty 1.1 Modelling uncertainty As in the deterministic case, we keep assuming that agents live for two periods. The novelty here is that their earnings in the second

1 Consumption and saving under uncertainty 1.1 Modelling uncertainty As in the deterministic case, we keep assuming that agents live for two periods. The novelty here is that their earnings in the second

How Costly is External Financing? Evidence from a Structural Estimation. Christopher Hennessy and Toni Whited March 2006

How Costly is External Financing? Evidence from a Structural Estimation Christopher Hennessy and Toni Whited March 2006 The Effects of Costly External Finance on Investment Still, after all of these years,

How Costly is External Financing? Evidence from a Structural Estimation Christopher Hennessy and Toni Whited March 2006 The Effects of Costly External Finance on Investment Still, after all of these years,

Monetary Economics: Macro Aspects, 19/ Henrik Jensen Department of Economics University of Copenhagen

Monetary Economics: Macro Aspects, 19/5 2009 Henrik Jensen Department of Economics University of Copenhagen Open-economy Aspects (II) 1. The Obstfeld and Rogo two-country model with sticky prices 2. An

Monetary Economics: Macro Aspects, 19/5 2009 Henrik Jensen Department of Economics University of Copenhagen Open-economy Aspects (II) 1. The Obstfeld and Rogo two-country model with sticky prices 2. An

Discussion of. Optimal Fiscal and Monetary Policy in a Medium-Scale Macroeconomic Model By Stephanie Schmitt-Grohe and Martin Uribe

Discussion of Optimal Fiscal and Monetary Policy in a Medium-Scale Macroeconomic Model By Stephanie Schmitt-Grohe and Martin Uribe Marc Giannoni Columbia University, CEPR and NBER International Research

Discussion of Optimal Fiscal and Monetary Policy in a Medium-Scale Macroeconomic Model By Stephanie Schmitt-Grohe and Martin Uribe Marc Giannoni Columbia University, CEPR and NBER International Research

Insights on the Greek economy from the 3D macro model

Insights on the Greek economy from the 3D macro model Hiona Balfoussia * and Dimitris Papageorgiou ** This version: April 26 Word count (excluding first page, tables and figures): 274 Abstract The DSGE

Insights on the Greek economy from the 3D macro model Hiona Balfoussia * and Dimitris Papageorgiou ** This version: April 26 Word count (excluding first page, tables and figures): 274 Abstract The DSGE

Lecture Notes in Macroeconomics. Christian Groth

Lecture Notes in Macroeconomics Christian Groth July 28, 2016 ii Contents Preface xvii I THE FIELD AND BASIC CATEGORIES 1 1 Introduction 3 1.1 Macroeconomics............................ 3 1.1.1 The field............................

Lecture Notes in Macroeconomics Christian Groth July 28, 2016 ii Contents Preface xvii I THE FIELD AND BASIC CATEGORIES 1 1 Introduction 3 1.1 Macroeconomics............................ 3 1.1.1 The field............................

Optimal monetary and macro-pru policies

Discussion of Kiley and Sim s Optimal monetary and macro-pru policies Oreste Tristani European Central Bank Federal Reserve Bank of San Francisco Conference on Monetary Policy and Financial Markets, 28

Discussion of Kiley and Sim s Optimal monetary and macro-pru policies Oreste Tristani European Central Bank Federal Reserve Bank of San Francisco Conference on Monetary Policy and Financial Markets, 28

Unemployment (Fears), Precautionary Savings, and Aggregate Demand

, Precautionary Savings, and Aggregate Demand") Unemployment (Fears), Precautionary Savings, and Aggregate Demand Wouter J. Den Haan (LSE/CEPR/CFM) Pontus Rendahl (University of Cambridge/CEPR/CFM) Markus Riegler (University of Bonn/CFM) June 19, 2016

Unemployment (Fears), Precautionary Savings, and Aggregate Demand Wouter J. Den Haan (LSE/CEPR/CFM) Pontus Rendahl (University of Cambridge/CEPR/CFM) Markus Riegler (University of Bonn/CFM) June 19, 2016

GENERAL EQUILIBRIUM ANALYSIS OF FLORIDA AGRICULTURAL EXPORTS TO CUBA

GENERAL EQUILIBRIUM ANALYSIS OF FLORIDA AGRICULTURAL EXPORTS TO CUBA Michael O Connell The Trade Sanctions Reform and Export Enhancement Act of 2000 liberalized the export policy of the United States with

GENERAL EQUILIBRIUM ANALYSIS OF FLORIDA AGRICULTURAL EXPORTS TO CUBA Michael O Connell The Trade Sanctions Reform and Export Enhancement Act of 2000 liberalized the export policy of the United States with

Discussion by J.C.Rochet (SFI,UZH and TSE) Prepared for the Swissquote Conference 2012 on Liquidity and Systemic Risk

Prepared for the Swissquote Conference 2012 on Liquidity and Systemic Risk") Discussion by J.C.Rochet (SFI,UZH and TSE) Prepared for the Swissquote Conference 2012 on Liquidity and Systemic Risk 1 Objectives of the paper Develop a theoretical model of bank lending that allows to

Discussion by J.C.Rochet (SFI,UZH and TSE) Prepared for the Swissquote Conference 2012 on Liquidity and Systemic Risk 1 Objectives of the paper Develop a theoretical model of bank lending that allows to

The Risky Steady State and the Interest Rate Lower Bound

The Risky Steady State and the Interest Rate Lower Bound Timothy Hills Taisuke Nakata Sebastian Schmidt New York University Federal Reserve Board European Central Bank 1 September 2016 1 The views expressed

The Risky Steady State and the Interest Rate Lower Bound Timothy Hills Taisuke Nakata Sebastian Schmidt New York University Federal Reserve Board European Central Bank 1 September 2016 1 The views expressed

Working Paper S e r i e s

Working Paper S e r i e s W P 0-5 M a y 2 0 0 Excessive Volatility in Capital Flows: A Pigouvian Taxation Approach Olivier Jeanne and Anton Korinek Abstract This paper analyzes prudential controls on capital

Working Paper S e r i e s W P 0-5 M a y 2 0 0 Excessive Volatility in Capital Flows: A Pigouvian Taxation Approach Olivier Jeanne and Anton Korinek Abstract This paper analyzes prudential controls on capital

Debt Covenants and the Macroeconomy: The Interest Coverage Channel

Debt Covenants and the Macroeconomy: The Interest Coverage Channel Daniel L. Greenwald MIT Sloan EFA Lunch, April 19 Daniel L. Greenwald Debt Covenants and the Macroeconomy EFA Lunch, April 19 1 / 6 Introduction

Debt Covenants and the Macroeconomy: The Interest Coverage Channel Daniel L. Greenwald MIT Sloan EFA Lunch, April 19 Daniel L. Greenwald Debt Covenants and the Macroeconomy EFA Lunch, April 19 1 / 6 Introduction

MACROECONOMIC ANALYSIS OF THE CONFERENCE AGREEMENT FOR H.R. 1, THE TAX CUTS AND JOBS ACT

MACROECONOMIC ANALYSIS OF THE CONFERENCE AGREEMENT FOR H.R. 1, THE TAX CUTS AND JOBS ACT Prepared by the Staff of the JOINT COMMITTEE ON TAXATION December 22, 2017 JCX-69-17 INTRODUCTION Pursuant to section

MACROECONOMIC ANALYSIS OF THE CONFERENCE AGREEMENT FOR H.R. 1, THE TAX CUTS AND JOBS ACT Prepared by the Staff of the JOINT COMMITTEE ON TAXATION December 22, 2017 JCX-69-17 INTRODUCTION Pursuant to section

Business cycle fluctuations Part II

Understanding the World Economy Master in Economics and Business Business cycle fluctuations Part II Lecture 7 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 7: Business cycle fluctuations

Understanding the World Economy Master in Economics and Business Business cycle fluctuations Part II Lecture 7 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 7: Business cycle fluctuations

Credit Frictions and Optimal Monetary Policy. Vasco Curdia (FRB New York) Michael Woodford (Columbia University)

Michael Woodford (Columbia University)") MACRO-LINKAGES, OIL PRICES AND DEFLATION WORKSHOP JANUARY 6 9, 2009 Credit Frictions and Optimal Monetary Policy Vasco Curdia (FRB New York) Michael Woodford (Columbia University) Credit Frictions and

MACRO-LINKAGES, OIL PRICES AND DEFLATION WORKSHOP JANUARY 6 9, 2009 Credit Frictions and Optimal Monetary Policy Vasco Curdia (FRB New York) Michael Woodford (Columbia University) Credit Frictions and

9. Real business cycles in a two period economy

9. Real business cycles in a two period economy Index: 9. Real business cycles in a two period economy... 9. Introduction... 9. The Representative Agent Two Period Production Economy... 9.. The representative

9. Real business cycles in a two period economy Index: 9. Real business cycles in a two period economy... 9. Introduction... 9. The Representative Agent Two Period Production Economy... 9.. The representative

Lecture 23 The New Keynesian Model Labor Flows and Unemployment. Noah Williams

Lecture 23 The New Keynesian Model Labor Flows and Unemployment Noah Williams University of Wisconsin - Madison Economics 312/702 Basic New Keynesian Model of Transmission Can be derived from primitives:

Lecture 23 The New Keynesian Model Labor Flows and Unemployment Noah Williams University of Wisconsin - Madison Economics 312/702 Basic New Keynesian Model of Transmission Can be derived from primitives:

Concerted Efforts? Monetary Policy and Macro-Prudential Tools

Concerted Efforts? Monetary Policy and Macro-Prudential Tools Andrea Ferrero Richard Harrison Benjamin Nelson University of Oxford Bank of England Rokos Capital 20 th Central Bank Macroeconomic Modeling

Concerted Efforts? Monetary Policy and Macro-Prudential Tools Andrea Ferrero Richard Harrison Benjamin Nelson University of Oxford Bank of England Rokos Capital 20 th Central Bank Macroeconomic Modeling

Forward Guidance Under Uncertainty

Forward Guidance Under Uncertainty Brent Bundick October 3 Abstract Increased uncertainty can reduce a central bank s ability to stabilize the economy at the zero lower bound. The inability to offset contractionary

Forward Guidance Under Uncertainty Brent Bundick October 3 Abstract Increased uncertainty can reduce a central bank s ability to stabilize the economy at the zero lower bound. The inability to offset contractionary

State-Dependent Fiscal Multipliers: Calvo vs. Rotemberg *

State-Dependent Fiscal Multipliers: Calvo vs. Rotemberg * Eric Sims University of Notre Dame & NBER Jonathan Wolff Miami University May 31, 2017 Abstract This paper studies the properties of the fiscal

State-Dependent Fiscal Multipliers: Calvo vs. Rotemberg * Eric Sims University of Notre Dame & NBER Jonathan Wolff Miami University May 31, 2017 Abstract This paper studies the properties of the fiscal

Supply-side effects of monetary policy and the central bank s objective function. Eurilton Araújo

Supply-side effects of monetary policy and the central bank s objective function Eurilton Araújo Insper Working Paper WPE: 23/2008 Copyright Insper. Todos os direitos reservados. É proibida a reprodução

Supply-side effects of monetary policy and the central bank s objective function Eurilton Araújo Insper Working Paper WPE: 23/2008 Copyright Insper. Todos os direitos reservados. É proibida a reprodução

What is Cyclical in Credit Cycles?

What is Cyclical in Credit Cycles? Rui Cui May 31, 2014 Introduction Credit cycles are growth cycles Cyclicality in the amount of new credit Explanations: collateral constraints, equity constraints, leverage

What is Cyclical in Credit Cycles? Rui Cui May 31, 2014 Introduction Credit cycles are growth cycles Cyclicality in the amount of new credit Explanations: collateral constraints, equity constraints, leverage

Leverage Restrictions in a Business Cycle Model. March 13-14, 2015, Macro Financial Modeling, NYU Stern.

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda Northwestern University Bank of Japan March 13-14, 2015, Macro Financial Modeling, NYU Stern. Background Wish to address

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda Northwestern University Bank of Japan March 13-14, 2015, Macro Financial Modeling, NYU Stern. Background Wish to address

Optimal Monetary and Macroprudential Policy: Gains and Pitfalls in a Model of Financial Intermediation. March 28, 2014

Optimal Monetary and Macroprudential Policy: Gains and Pitfalls in a Model of Financial Intermediation Michael T. Kiley Jae W. Sim March 28, 2014 THEORETICAL FRAMEWORK Financial intermediation sector in

Optimal Monetary and Macroprudential Policy: Gains and Pitfalls in a Model of Financial Intermediation Michael T. Kiley Jae W. Sim March 28, 2014 THEORETICAL FRAMEWORK Financial intermediation sector in

Aggregate Bank Capital and Credit Dynamics

Aggregate Bank Capital and Credit Dynamics N. Klimenko S. Pfeil J.-C. Rochet G. De Nicolò (Zürich) (Bonn) (Zürich, SFI and TSE) (IMF and CESifo) March 2016 The views expressed in this paper are those of

Aggregate Bank Capital and Credit Dynamics N. Klimenko S. Pfeil J.-C. Rochet G. De Nicolò (Zürich) (Bonn) (Zürich, SFI and TSE) (IMF and CESifo) March 2016 The views expressed in this paper are those of

Exchange Rate Adjustment in Financial Crises

Exchange Rate Adjustment in Financial Crises Michael B. Devereux 1 Changhua Yu 2 1 University of British Columbia 2 Peking University Swiss National Bank June 2016 Motivation: Two-fold Crises in Emerging

Exchange Rate Adjustment in Financial Crises Michael B. Devereux 1 Changhua Yu 2 1 University of British Columbia 2 Peking University Swiss National Bank June 2016 Motivation: Two-fold Crises in Emerging