Annex III OUTLINE OF INVESTMENT EFFICIENCY INDICA TORS AND SIMULATION MODEL

|

|

|

- Marion Summers

- 5 years ago

- Views:

Transcription

1 project. Annex III OUTLINE OF INVESTMENT EFFICIENCY INDICA TORS AND SIMULATION MODEL The following four parameters are usually utilized for measuring the profitability of a Payback period Benefit ratio Net present value Internal rate of return (a) Payback neriod The payback period measures the time taken for the net cash flow generated by an investment to pay back the of its initial investment. The shorter the payback period, the better the investment. With this method of investment appraisal, a project will be approved if its payback period is shorter than a limit that was set up previously. If it is a question of choosing between projects, then the one with the shorter payback period will be chosen. Payback period criterion has the merit of being simple to calculate and gives a rough measure of the amount of time that the capital is at risk. It may be the most frequently utilized method of appraisal in the industry at present. However, it has a number of serious disadvantages, for example: (a) Neglect of income after paxback The payback criterion completely ignores any cash proceeds after the payback date. These may be nil or many thousands of dollars, but the same value is indicated by the payback period. (b) Neglect of timing of cash flows It also ignores the timing of the cash flows within the payback period, which is very important. For example, with a 4-year payback period, in a quickly changing market there would be considerable advantage in having the majority of income in the first year offset the relatively high risk. However, if the same investment with the same payback period were being made where changes are relatively few and the risk is consequently less, there might be considerable advantage in having a rising trend of net income. Both cases have the same payback periods, but very different characteristics which may influence the total amounts of discounted cash flow depending on the level of interest rate. However, the payback period indicator cannot show such differences.

2 The 56 (c) No indication on Qrofitabilitx Payback period gives no indication of the profitability of a project or even of whether it will ever be profitable. It assumes that once the capital outlay has been recovered, the investment proves while. It completely ignores the of raising capital as well as the opportunity investing elsewhere. Payback analysis, however, is in some circumstances a useful tool. Because it is simple and easy to calculate, it can be used as an initial screening device to save time in the followingways: Projects with a very long payback of more than, for example, 1 to 15 years are unlikely to be profitable even in mor~ conservative sectors, and are probably therefore not analyzing further.. Projects involving a relatively small capital outlay and with a short payback either absolutely or in relation to their likely lives are probably. undertaking without detailed analysis other than a payback calculation. This may be the case for various kinds of office machines. However, payback analysis is a very dangerous method of investment appraisal on whichto rely for decisions involving large amounts of capital. Itis as likely to give the wrong answeras to give the right one.. (b) Benefit ratio Benefit ratio is defined as follows: Benefit ratio = Present of benefits Present of In this method, a ration of" 1" or above will indicate a project with discounted benefits greater than discounted s, and the project is therefore acceptable. A higher benefit - ratiois usually construed to mean greater profitability. To compute the ratio, it is necessary to decide on a discount rate. The best discount rate to use is probably the opportunity of capital, whichis the rate of return (or profitability) of the least possible investment in an economy given thetotal available capital. However, in practice it is very difficult to obtain the value of opportunity of capital. In most developing countries this is assumed to be somewhere between 8 and 15 per cent. Another value that is sometimes used is the market rate of interest. This is, as a matter of fact, subject to error because of distortions that may occur in the market. benefit- ratio method suffers from the following disadvantages: (1) A common netting out convention is required to derive and benefit streamsto avoid misleading results in ranking projects using benefit ratios.

3 (2) The value of the benefit ratio depends on the discount rate used. Since selection of the right discount rate is always a problem, some doubt always exists as to the relevance of the calculated benefit- ratio. (c) Net uresent Net present is defined as follows: Net present = Present of benefits- Present of s = Present of net benefits In the above, net benefits is defined as the algebraic difference of benefit and in each year of the benefit and streams. The net benefit stream is also known as the cash flow. A positive value of the net present indicates a project where discounted benefits are greater than discounted s. The net present method has the following disadvantages: Although the net present is a measure of the profitability of a project, the measures is not tied to the amount of investment required. Two projects having the same net present may thus have widely different investment requirements. The value of net present depends on the discount rate used, and therefore suffers the disadvantage of having to select the right discount rate prior to the analysis. (3) It is necessary to ensure that all discounting is done to the same base year to allow proper comparison of alternative projects. (d) Internal rate of return Internal rate of return is defined as "the discount rate which will cause the net present of the project to be equal to zero". In other words, the internal rate of return could be called "break-even discount rate" for the project. For normal projects where benefits follow an initial investment, the net present decreases as the discount rate is increased. There is one value of the discount rate at which the net present becomes zero as shown in Figure A-I. This discount rate is known as the internal rate of return. ~'7

18 2 22 24 26 Figure A-I: Internal rate of return The internal rate of return")

of 2 in each year of the life of the project.")

of 1. This project then has an IRR of 2 per cent (2 divided by 1).")

4 ~1-,,I~ :::::j ~ -+-i N~--+-, =j==j::~ ~ t 6 ~ -2, I I I I -1 ),...,.1 ""'" -..;;J J -i -I -1 -i Discount rate (%) Figure A-I: Internal rate of return The internal rate of return (IRR) is a measure of the return on and of capital for a project. The following illustration provides a simple definition of the IRR. Investment (1) Return of capital (1) Return on capital Year In this project, the original investment of 1 produces a return (profit) of 2 in each year of the life of the project. At the end of the project life, the project also generated sufficient additional profit to provide for the return of the capital (original investment) of 1. This project then has an IRR of 2 per cent (2 divided by 1). Of course, in practice, the investment sums and profits will not take on such a simple pattern, and a different method to compute the IRR is required. Although manual computation of internal rate of return is possible, it involves a trial-anderror procedure and consequently is a little bit troublesome. However, standard computer programmes are available in many spread sheet software forms for personal computer, from which the IRR can be computed rapidly for any given cash flow (net benefit) stream as explained below. 58

and l-iii(b) respectively.")

Payback period, (c) Benefit ration and (d) Net present will be automatically returned for tables l-iii(a) and (b) when the above-mentioned")

and (b) respectively. The user may utilize only one table if two are not needed.")

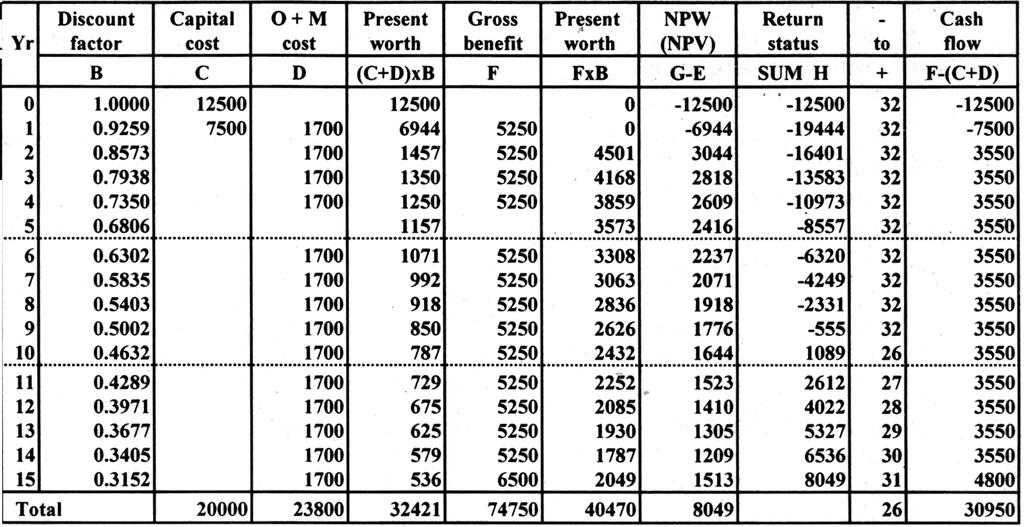

5 Adjustable Constraints: The +H=O+H=O +E4>+4> (e) Simulation model of.investment efficienc~ indicators A printout of a simulation model which is designed to compute the four investment efficiency indicators simultaneously for two cases is contained in tables 1-III(a) and (b). The model which is programmed on the basis of Lotus can compare the respective indicators of two cases for deciding their priority. It consists of three parts, namely the head panel, table 1- lii(a) and table 1-III(b) of one case and Table 2 of the other case. In the head panel, the entry of discount rates should be made to cells E4 and G4 for tables l-iii(a) and l-iii(b) respectively. In each table, capital s, operating and maintenance s and gross benefits should be entered to Column C, 9 and F respectively. Be careful not to enter values to any other parts, since these cells contain formulas which will return values in accordance with the independent variables. Three indicators, vis. (B) Payback period, (c) Benefit ration and (d) Net present will be automatically returned for tables l-iii(a) and (b) when the above-mentioned values are duly entered. The attached printout shows such indicators at discount rates of8. and 12. per cent on the same cash flow in tables l-iii(a) and (b) respectively. The user may utilize only one table if two are not needed. The last item in the head panel, ( e) Result indicates internal rates of return of Tables 1 and 2. The user must supply an initial estimate-of the 'internal rate of return. When it is too far from the correct rate, the function will return ERR: If that occurs, enter another estimate to recalculate the fonnula. Note also that if the range contains multiple negative may return inconsistent or inaccurate results. The user may easily verify the accuracyof a returned internal rate of return by copyingcommands the value to cell E4 and/or G4. In this case, the are:/,range, Value, press Enter, up 4 rows, press Enter. If the value was correct, the: net present value in E7 and G7 will turn to Zero. The internal rate of return will also be calculated by using the "Solver" function of Lotus-2-3 under the following definition: cells: E4 and 4 (discount rate) total net present value (H and H ) shall be zero, viz. and discount rates shall be negative, viz. 59

TABLE2~ 8.% ~.i.~.~f!;.~~.~.:':~.")

Benefit d) Net e) Result")

Yrl Discount")

xB F FxB G-E SUM H Pre;sent")

xB 1.")

26 27 28 29 3")

125 2 I -75 48 (' US$)")

6 Table B Tables I-ill: (a) and (b) Investment efficiency indicators (simulation model) IT~~LE1.~2 b) TABLE2~ 8.% ~.i.~.~f!;.~~.~.:':~.~.e.: Payback period (year): 12.% 1 c) Benefit d) Net e) Result ratio: present : of (Q}IRR: Enter estimated IRR in 18 and/or K , % 2, % 'TABLE I 11 'TABLE 2.%1 I Table I-III (a) Yrl Discount factor B 1. III Capital O+M D C Total Gross benefit NPW NPV Return (C+D)xB F FxB G-E SUM H Pre;sent Present ~==:~~ , ' status , ~ ~ to + Discount factor Capital C (C+D)xB Total D Present O+M ~ Gross benefit F Cash flow F-(C+D) l-iii(b) Yr~ 2.%1 (' US$) I (' US$) Present FxB NPW NPV Return - status to G-E SUM H Cash flow F-(C+D)

University 18 Lessons Financial Management. Unit 2: Capital Budgeting Decisions

University 18 Lessons Financial Management Unit 2: Capital Budgeting Decisions Nature of Investment Decisions The investment decisions of a firm are generally known as the capital budgeting, or capital

University 18 Lessons Financial Management Unit 2: Capital Budgeting Decisions Nature of Investment Decisions The investment decisions of a firm are generally known as the capital budgeting, or capital

Capital Budgeting CFA Exam Level-I Corporate Finance Module Dr. Bulent Aybar

Capital Budgeting CFA Exam Level-I Corporate Finance Module Dr. Bulent Aybar Professor of International Finance Capital Budgeting Agenda Define the capital budgeting process, explain the administrative

Capital Budgeting CFA Exam Level-I Corporate Finance Module Dr. Bulent Aybar Professor of International Finance Capital Budgeting Agenda Define the capital budgeting process, explain the administrative

Describe the importance of capital investments and the capital budgeting process

Chapter 20 Making capital investment decisions Affects operations for many years Requires large sums of money Describe the importance of capital investments and the capital budgeting process 3 4 5 6 Operating

Chapter 20 Making capital investment decisions Affects operations for many years Requires large sums of money Describe the importance of capital investments and the capital budgeting process 3 4 5 6 Operating

Chapter 10 The Basics of Capital Budgeting: Evaluating Cash Flows ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS

Chapter 10 The Basics of Capital Budgeting: Evaluating Cash Flows ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS 10-1 a. Capital budgeting is the whole process of analyzing projects and deciding whether

Chapter 10 The Basics of Capital Budgeting: Evaluating Cash Flows ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS 10-1 a. Capital budgeting is the whole process of analyzing projects and deciding whether

Commercestudyguide.com Capital Budgeting. Definition of Capital Budgeting. Nature of Capital Budgeting. The process of Capital Budgeting

Commercestudyguide.com Capital Budgeting Capital Budgeting decision is considered the most important and most critical decision for a finance manager. It involves decisions related to long-term investments

Commercestudyguide.com Capital Budgeting Capital Budgeting decision is considered the most important and most critical decision for a finance manager. It involves decisions related to long-term investments

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing)

") Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Introduction A long term view of benefits and costs must be taken when reviewing a capital expenditure project.

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Introduction A long term view of benefits and costs must be taken when reviewing a capital expenditure project.

CAPITAL BUDGETING AND THE INVESTMENT DECISION

C H A P T E R 1 2 CAPITAL BUDGETING AND THE INVESTMENT DECISION I N T R O D U C T I O N This chapter begins by discussing some of the problems associated with capital asset decisions, such as the long

C H A P T E R 1 2 CAPITAL BUDGETING AND THE INVESTMENT DECISION I N T R O D U C T I O N This chapter begins by discussing some of the problems associated with capital asset decisions, such as the long

Global Financial Management

Global Financial Management Valuation of Cash Flows Investment Decisions and Capital Budgeting Copyright 2004. All Worldwide Rights Reserved. See Credits for permissions. Latest Revision: August 23, 2004

Global Financial Management Valuation of Cash Flows Investment Decisions and Capital Budgeting Copyright 2004. All Worldwide Rights Reserved. See Credits for permissions. Latest Revision: August 23, 2004

The nature of investment decision

The nature of investment decision Investment decisions must be consistent with the objectives of the particular organization. In private-sector business, maximizing the wealth of the owners is normally

The nature of investment decision Investment decisions must be consistent with the objectives of the particular organization. In private-sector business, maximizing the wealth of the owners is normally

Session 02. Investment Decisions

Session 02 Investment Decisions Programme : Executive Diploma in Accounting, Business & Strategy (EDABS 2017) Course : Corporate Financial Management (EDABS 202) Lecturer : Mr. Asanka Ranasinghe MBA (Colombo),

Session 02 Investment Decisions Programme : Executive Diploma in Accounting, Business & Strategy (EDABS 2017) Course : Corporate Financial Management (EDABS 202) Lecturer : Mr. Asanka Ranasinghe MBA (Colombo),

CA. Sonali Jagath Prasad ACA, ACMA, CGMA, B.Com.

MANAGEMENT OF FINANCIAL RESOURCES AND PERFORMANCE SESSIONS 3& 4 INVESTMENT APPRAISAL METHODS June 10 to 24, 2013 CA. Sonali Jagath Prasad ACA, ACMA, CGMA, B.Com. WESTFORD 2008 Thomson SCHOOL South-Western

MANAGEMENT OF FINANCIAL RESOURCES AND PERFORMANCE SESSIONS 3& 4 INVESTMENT APPRAISAL METHODS June 10 to 24, 2013 CA. Sonali Jagath Prasad ACA, ACMA, CGMA, B.Com. WESTFORD 2008 Thomson SCHOOL South-Western

Profitability Estimates

CH2404 Process Economics Unit III Profitability Estimates Dr. M. Subramanian Associate Professor Department of Chemical Engineering Sri Sivasubramaniya Nadar College of Engineering Kalavakkam 603 110,

CH2404 Process Economics Unit III Profitability Estimates Dr. M. Subramanian Associate Professor Department of Chemical Engineering Sri Sivasubramaniya Nadar College of Engineering Kalavakkam 603 110,

The formula for the net present value is: 1. NPV. 2. NPV = CF 0 + CF 1 (1+ r) n + CF 2 (1+ r) n

n + CF 2 (1+ r) n") Lecture 6: Capital Budgeting 1 Capital budgeting refers to an investment into a long term asset. It must be noted that all investments have a cost and that investments should always have benefits such

Lecture 6: Capital Budgeting 1 Capital budgeting refers to an investment into a long term asset. It must be noted that all investments have a cost and that investments should always have benefits such

CAPITAL BUDGETING TECHNIQUES (CHAPTER 9)

") CAPITAL BUDGETING TECHNIQUES (CHAPTER 9) Capital budgeting refers to the process used to make decisions concerning investments in the long-term assets of the firm. The general idea is that a firm s capital,

CAPITAL BUDGETING TECHNIQUES (CHAPTER 9) Capital budgeting refers to the process used to make decisions concerning investments in the long-term assets of the firm. The general idea is that a firm s capital,

INVESTMENT APPRAISAL TECHNIQUES FOR SMALL AND MEDIUM SCALE ENTERPRISES

SAMUEL ADEGBOYEGA UNIVERSITY COLLEGE OF MANAGEMENT AND SOCIAL SCIENCES DEPARTMENT OF BUSINESS ADMINISTRATION COURSE CODE: BUS 413 COURSE TITLE: SMALL AND MEDIUM SCALE ENTERPRISE MANAGEMENT SESSION: 2017/2018,

SAMUEL ADEGBOYEGA UNIVERSITY COLLEGE OF MANAGEMENT AND SOCIAL SCIENCES DEPARTMENT OF BUSINESS ADMINISTRATION COURSE CODE: BUS 413 COURSE TITLE: SMALL AND MEDIUM SCALE ENTERPRISE MANAGEMENT SESSION: 2017/2018,

WEEK 7 Investment Appraisal -1

WEEK 7 Investment Appraisal -1 Learning Objectives Understand the nature and importance of investment decisions. Distinguish between discounted cash flow (DCF) and nondiscounted cash flow (non-dcf) techniques

WEEK 7 Investment Appraisal -1 Learning Objectives Understand the nature and importance of investment decisions. Distinguish between discounted cash flow (DCF) and nondiscounted cash flow (non-dcf) techniques

CHAPTER 9 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA

CHAPTER 9 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA Learning Objectives LO1 How to compute the net present value and why it is the best decision criterion. LO2 The payback rule and some of its shortcomings.

CHAPTER 9 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA Learning Objectives LO1 How to compute the net present value and why it is the best decision criterion. LO2 The payback rule and some of its shortcomings.

Chapter 7. Net Present Value and Other Investment Rules

Chapter 7 Net Present Value and Other Investment Rules Be able to compute payback and discounted payback and understand their shortcomings Understand accounting rates of return and their shortcomings Be

Chapter 7 Net Present Value and Other Investment Rules Be able to compute payback and discounted payback and understand their shortcomings Understand accounting rates of return and their shortcomings Be

Capital Budgeting Process and Techniques 93. Chapter 7: Capital Budgeting Process and Techniques

Capital Budgeting Process and Techniques 93 Answers to questions Chapter 7: Capital Budgeting Process and Techniques 7-. a. Type I error means rejecting a good project. Payback could lead to Type errors

Capital Budgeting Process and Techniques 93 Answers to questions Chapter 7: Capital Budgeting Process and Techniques 7-. a. Type I error means rejecting a good project. Payback could lead to Type errors

Disclaimer: This resource package is for studying purposes only EDUCATION

Disclaimer: This resource package is for studying purposes only EDUCATION Chapter 6: Valuing stocks Bond Cash Flows, Prices, and Yields - Maturity date: Final payment date - Term: Time remaining until

Disclaimer: This resource package is for studying purposes only EDUCATION Chapter 6: Valuing stocks Bond Cash Flows, Prices, and Yields - Maturity date: Final payment date - Term: Time remaining until

International Project Management. prof.dr MILOŠ D. MILOVANČEVIĆ

International Project Management prof.dr MILOŠ D. MILOVANČEVIĆ Project Evaluation and Analysis Project Financial Analysis Project Evaluation and Analysis The important aspects of project analysis are:

International Project Management prof.dr MILOŠ D. MILOVANČEVIĆ Project Evaluation and Analysis Project Financial Analysis Project Evaluation and Analysis The important aspects of project analysis are:

Investment Appraisal

Investment Appraisal Introduction to Investment Appraisal Whatever level of management authorises a capital expenditure, the proposed investment should be properly evaluated, and found to be worthwhile

Investment Appraisal Introduction to Investment Appraisal Whatever level of management authorises a capital expenditure, the proposed investment should be properly evaluated, and found to be worthwhile

Capital investment decisions: 1

Capital investment decisions: 1 Solutions to Chapter 13 questions Question 13.24 (i) Net present values: Year 0% 10% 20% NPV Discount NPV Discount NPV ( ) Factor ( ) Factor ( ) 0 (142 700) 1 000 (142 700)

Capital investment decisions: 1 Solutions to Chapter 13 questions Question 13.24 (i) Net present values: Year 0% 10% 20% NPV Discount NPV Discount NPV ( ) Factor ( ) Factor ( ) 0 (142 700) 1 000 (142 700)

Copyright Disclaimer under Section 107 of the Copyright Act 1976, allowance is made for "fair use" for purposes such as criticism, comment, news

Copyright Disclaimer under Section 107 of the Copyright Act 1976, allowance is made for "fair use" for purposes such as criticism, comment, news reporting, teaching, scholarship, and research. Fair use

Copyright Disclaimer under Section 107 of the Copyright Act 1976, allowance is made for "fair use" for purposes such as criticism, comment, news reporting, teaching, scholarship, and research. Fair use

Chapter 6 Making Capital Investment Decisions

Making Capital Investment Decisions Solutions to Even-Numbered Problems and Cases 6.2 Manitoba Railroad Limited (MRL) (a) Discount Rate 7% Cash Cash Net Cash Cumulative Year Outflows Inflows Flows Cash

Making Capital Investment Decisions Solutions to Even-Numbered Problems and Cases 6.2 Manitoba Railroad Limited (MRL) (a) Discount Rate 7% Cash Cash Net Cash Cumulative Year Outflows Inflows Flows Cash

Chapter 14 Solutions Solution 14.1

Chapter 14 Solutions Solution 14.1 a) Compare and contrast the various methods of investment appraisal. To what extent would it be true to say there is a place for each of them As capital investment decisions

Chapter 14 Solutions Solution 14.1 a) Compare and contrast the various methods of investment appraisal. To what extent would it be true to say there is a place for each of them As capital investment decisions

Unit-2. Capital Budgeting

Unit-2 Capital Budgeting Unit Structure 2.0. Objectives. 2.1. Introduction. 2.2. Presentation of subject matter. 2.2.1 Meaning of capital budgeting. 2.2.2 Capital expenditure. 2.2.3 Definitions. 2.2.4

Unit-2 Capital Budgeting Unit Structure 2.0. Objectives. 2.1. Introduction. 2.2. Presentation of subject matter. 2.2.1 Meaning of capital budgeting. 2.2.2 Capital expenditure. 2.2.3 Definitions. 2.2.4

Lecture 6 Capital Budgeting Decision

Lecture 6 Capital Budgeting Decision The term capital refers to long-term assets used in production, while a budget is a plan that details projected inflows and outflows during some future period. Thus,

Lecture 6 Capital Budgeting Decision The term capital refers to long-term assets used in production, while a budget is a plan that details projected inflows and outflows during some future period. Thus,

ACCT 102 Fundamentals of Accounting II Chapter 24 Capital Budgeting and Investment Analysis

ACCT 102 Fundamentals of Accounting II Chapter 24 Capital Budgeting and Investment Analysis METHOD ADVANTAGES DISADVANTAGES Average Rate of Return Cash Payback Net Present Value Internal Rate of Return

ACCT 102 Fundamentals of Accounting II Chapter 24 Capital Budgeting and Investment Analysis METHOD ADVANTAGES DISADVANTAGES Average Rate of Return Cash Payback Net Present Value Internal Rate of Return

Chapter What are the important administrative considerations in the capital budgeting process?

Chapter 12 Discussion Questions 12-1. What are the important administrative considerations in the capital budgeting process? Important administrative considerations relate to: the search for and discovery

Chapter 12 Discussion Questions 12-1. What are the important administrative considerations in the capital budgeting process? Important administrative considerations relate to: the search for and discovery

The Mathematics of Interest An Example Assume a bank pays 8% interest on a $100 deposit made today. How much

The Mathematics of Interest An Example CAPITAL BUDGETING Assume a bank pays 8% interest on a $100 deposit made today. How much will the $100 be worth in one year? F n = P(1 + r) n 1 3 Typical Capital Budgeting

The Mathematics of Interest An Example CAPITAL BUDGETING Assume a bank pays 8% interest on a $100 deposit made today. How much will the $100 be worth in one year? F n = P(1 + r) n 1 3 Typical Capital Budgeting

CAPITAL BUDGETING. John D. Stowe, CFA Athens, Ohio, U.S.A. Jacques R. Gagné, CFA Quebec City, Quebec, Canada

CHAPTER 2 CAPITAL BUDGETING John D. Stowe, CFA Athens, Ohio, U.S.A. Jacques R. Gagné, CFA Quebec City, Quebec, Canada LEARNING OUTCOMES After completing this chapter, you will be able to do the following:

CHAPTER 2 CAPITAL BUDGETING John D. Stowe, CFA Athens, Ohio, U.S.A. Jacques R. Gagné, CFA Quebec City, Quebec, Canada LEARNING OUTCOMES After completing this chapter, you will be able to do the following:

AFM 271. Midterm Examination #2. Friday June 17, K. Vetzal. Answer Key

AFM 21 Midterm Examination #2 Friday June 1, 2005 K. Vetzal Name: Answer Key Student Number: Section Number: Duration: 1 hour and 30 minutes Instructions: 1. Answer all questions in the space provided.

AFM 21 Midterm Examination #2 Friday June 1, 2005 K. Vetzal Name: Answer Key Student Number: Section Number: Duration: 1 hour and 30 minutes Instructions: 1. Answer all questions in the space provided.

J ohn D. S towe, CFA. CFA Institute Charlottesville, Virginia. J acques R. G agn é, CFA

CHAPTER 2 CAPITAL BUDGETING J ohn D. S towe, CFA CFA Institute Charlottesville, Virginia J acques R. G agn é, CFA La Société de l assurance automobile du Québec Quebec City, Canada LEARNING OUTCOMES After

CHAPTER 2 CAPITAL BUDGETING J ohn D. S towe, CFA CFA Institute Charlottesville, Virginia J acques R. G agn é, CFA La Société de l assurance automobile du Québec Quebec City, Canada LEARNING OUTCOMES After

Financial Management Bachelors of Business Administration Study Notes & Tutorial Questions Chapter 1: Investment & Project Appraisal

Financial Management Bachelors of Business Administration Study Notes & Tutorial Questions Chapter 1: Investment & Project Appraisal Ibrahim Sameer AVID College Page 1 INTRODUCTION Capital budgeting is

Financial Management Bachelors of Business Administration Study Notes & Tutorial Questions Chapter 1: Investment & Project Appraisal Ibrahim Sameer AVID College Page 1 INTRODUCTION Capital budgeting is

CAPITAL BUDGETING. Key Terms and Concepts to Know

CAPITAL BUDGETING Key Terms and Concepts to Know Capital budgeting: The process of planning significant investments in projects that have long lives and affect more than one future period, such as the

CAPITAL BUDGETING Key Terms and Concepts to Know Capital budgeting: The process of planning significant investments in projects that have long lives and affect more than one future period, such as the

(a) (i) Year 0 Year 1 Year 2 Year 3 $ $ $ $ Lease Lease payment (55,000) (55,000) (55,000) Borrow and buy Initial cost (160,000) Residual value 40,000

(i) Year 0 Year 1 Year 2 Year 3 $ $ $ $ Lease Lease payment (55,000) (55,000) (55,000) Borrow and buy Initial cost (160,000) Residual value 40,000") Answers Applied Skills, FM Financial Management (FM) September/December 2018 Sample Answers Section C 31 Melanie Co (a) (i) Year 0 Year 1 Year 2 Year 3 $ $ $ $ Lease Lease payment (55,000) (55,000) (55,000)

Answers Applied Skills, FM Financial Management (FM) September/December 2018 Sample Answers Section C 31 Melanie Co (a) (i) Year 0 Year 1 Year 2 Year 3 $ $ $ $ Lease Lease payment (55,000) (55,000) (55,000)

Methods of Financial Appraisal

Appendix 2 Methods of Financial Appraisal The of money over time There are a number of financial appraisal techniques, ranging from the simple to the sophisticated, that can be of use as an aid to decision-making

Appendix 2 Methods of Financial Appraisal The of money over time There are a number of financial appraisal techniques, ranging from the simple to the sophisticated, that can be of use as an aid to decision-making

Introduction to Capital

Introduction to Capital What is Capital? Money invested in business to generate income The money, property, and other valuables which collectively represent the wealth of an individual or business The

Introduction to Capital What is Capital? Money invested in business to generate income The money, property, and other valuables which collectively represent the wealth of an individual or business The

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) What is meant by the term 'Net Present Value'? 1) A) The future value of cash flows after netting

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) What is meant by the term 'Net Present Value'? 1) A) The future value of cash flows after netting

Engineering Economics and Financial Accounting

Engineering Economics and Financial Accounting Unit 5: Accounting Major Topics are: Balance Sheet - Profit & Loss Statement - Evaluation of Investment decisions Average Rate of Return - Payback Period

Engineering Economics and Financial Accounting Unit 5: Accounting Major Topics are: Balance Sheet - Profit & Loss Statement - Evaluation of Investment decisions Average Rate of Return - Payback Period

Investment Decision Criteria. Principles Applied in This Chapter. Learning Objectives

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

P. V. V I S W A N A T H W I T H A L I T T L E H E L P F R O M J A K E F E L D M A N F O R A F I R S T C O U R S E I N F I N A N C E

1 P. V. V I S W A N A T H W I T H A L I T T L E H E L P F R O M J A K E F E L D M A N F O R A F I R S T C O U R S E I N F I N A N C E 2 The objective of a manager is to maximize NPV of cash flows and is

1 P. V. V I S W A N A T H W I T H A L I T T L E H E L P F R O M J A K E F E L D M A N F O R A F I R S T C O U R S E I N F I N A N C E 2 The objective of a manager is to maximize NPV of cash flows and is

Part 2 Financial Metrics and Rates of Return

Part 2 Financial Metrics and Rates of Return Christopher Russell Energy PathFINDER www.energypathfinder.com (443) 636-7746 crussell@energypathfinder.com Spare no expense to save money on this one. Samuel

Part 2 Financial Metrics and Rates of Return Christopher Russell Energy PathFINDER www.energypathfinder.com (443) 636-7746 crussell@energypathfinder.com Spare no expense to save money on this one. Samuel

UNIT IV CAPITAL BUDGETING

UNIT IV CAPITAL BUDGETING Capital Budgeting: Capital budgeting is the process of making investment decision in long-term assets or courses of action. Capital expenditure incurred today is expected to bring

UNIT IV CAPITAL BUDGETING Capital Budgeting: Capital budgeting is the process of making investment decision in long-term assets or courses of action. Capital expenditure incurred today is expected to bring

Chapter 8. Ross, Westerfield and Jordan, ECF 4 th ed 2004 Solutions

Ross, Westerfield and Jordan, ECF 4 th ed 2004 Solutions Chapter 8. Answers to Concepts Review and Critical Thinking Questions 1. A payback period less than the project s life means that the NPV is positive

Ross, Westerfield and Jordan, ECF 4 th ed 2004 Solutions Chapter 8. Answers to Concepts Review and Critical Thinking Questions 1. A payback period less than the project s life means that the NPV is positive

8: Economic Criteria

8.1 Economic Criteria Capital Budgeting 1 8: Economic Criteria The preceding chapters show how to discount and compound a variety of different types of cash flows. This chapter explains the use of those

8.1 Economic Criteria Capital Budgeting 1 8: Economic Criteria The preceding chapters show how to discount and compound a variety of different types of cash flows. This chapter explains the use of those

Solutions to Problems

Solutions to Problems 1. The investor would earn income of $2.25 and a capital gain of $52.50 $45 =$7.50. The total gain is $9.75 or 21.7%. $8.25 on a stock that paid $3.75 in income and sold for $67.50.

Solutions to Problems 1. The investor would earn income of $2.25 and a capital gain of $52.50 $45 =$7.50. The total gain is $9.75 or 21.7%. $8.25 on a stock that paid $3.75 in income and sold for $67.50.

Chapter 7: Investment Decision Rules

Chapter 7: Investment Decision Rules-1 Chapter 7: Investment Decision Rules I. Introduction and Review of NPV A. Introduction Q: How decide which long-term investment opportunities to undertake? Key =>

Chapter 7: Investment Decision Rules-1 Chapter 7: Investment Decision Rules I. Introduction and Review of NPV A. Introduction Q: How decide which long-term investment opportunities to undertake? Key =>

Investment Decision Criteria. Principles Applied in This Chapter. Disney s Capital Budgeting Decision

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

The following points highlight the three time-adjusted or discounted methods of capital budgeting, i.e., 1. Net Present Value

Discounted Methods of Capital Budgeting Financial Analysis The following points highlight the three time-adjusted or discounted methods of capital budgeting, i.e., 1. Net Present Value Method 2. Internal

Discounted Methods of Capital Budgeting Financial Analysis The following points highlight the three time-adjusted or discounted methods of capital budgeting, i.e., 1. Net Present Value Method 2. Internal

Introduction to RELCOST. Carolyn Roos, Ph.D. Northwest CHP Technical Assistance Partnerships Washington State University Energy Program

Introduction to RELCOST Carolyn Roos, Ph.D. Northwest CHP Technical Assistance Partnerships Washington State University Energy Program 1 Overview of RELCOST Presentation Outline Program use Results A review

Introduction to RELCOST Carolyn Roos, Ph.D. Northwest CHP Technical Assistance Partnerships Washington State University Energy Program 1 Overview of RELCOST Presentation Outline Program use Results A review

Project Selection Models. The Selection and Prioritisation of Project

DEVELOPMENT PANORAMA RESOURCES Project Selection Models This article discusses the selection and prioritisation of projects and shows how the financial calculations are done. The Selection and Prioritisation

DEVELOPMENT PANORAMA RESOURCES Project Selection Models This article discusses the selection and prioritisation of projects and shows how the financial calculations are done. The Selection and Prioritisation

Financial Management Masters of Business Administration Study Notes & Tutorial Questions Chapter 3: Investment Decisions

Financial Management Masters of Business Administration Study Notes & Tutorial Questions Chapter 3: Investment Decisions 1 INTRODUCTION The word Capital refers to be the total investment of a company of

Financial Management Masters of Business Administration Study Notes & Tutorial Questions Chapter 3: Investment Decisions 1 INTRODUCTION The word Capital refers to be the total investment of a company of

An Analysis Comparing John Hancock Protection UL

White Paper An Analysis Comparing John Hancock Protection UL and MetLife Secure Flex UL updated April 2015 Background & General Comments John Hancock Protection UL is the only UL product without lifetime

White Paper An Analysis Comparing John Hancock Protection UL and MetLife Secure Flex UL updated April 2015 Background & General Comments John Hancock Protection UL is the only UL product without lifetime

Final Course Paper 2 Strategic Financial Management Chapter 2 Part 8. CA. Anurag Singal

Final Course Paper 2 Strategic Financial Management Chapter 2 Part 8 CA. Anurag Singal Internal Rate of Return Miscellaneous Sums Internal Rate of Return (IRR) is the rate at which NPV = 0 XYZ Ltd., an

Final Course Paper 2 Strategic Financial Management Chapter 2 Part 8 CA. Anurag Singal Internal Rate of Return Miscellaneous Sums Internal Rate of Return (IRR) is the rate at which NPV = 0 XYZ Ltd., an

Chapter 7: Investment Decision Rules

Chapter 7: Investment Decision Rules -1 Chapter 7: Investment Decision Rules Note: Read the chapter then look at the following. Fundamental question: What criteria should firms use when deciding which

Chapter 7: Investment Decision Rules -1 Chapter 7: Investment Decision Rules Note: Read the chapter then look at the following. Fundamental question: What criteria should firms use when deciding which

Investment Analysis and Project Assessment

Strategic Business Planning for Commercial Producers Investment Analysis and Project Assessment Michael Boehlje and Cole Ehmke Center for Food and Agricultural Business Purdue University Capital investment

Strategic Business Planning for Commercial Producers Investment Analysis and Project Assessment Michael Boehlje and Cole Ehmke Center for Food and Agricultural Business Purdue University Capital investment

Chapter 9. Capital Budgeting Decision Models

Chapter 9 Capital Budgeting Decision Models Learning Objectives 1. Explain capital budgeting and differentiate between short-term and long-term budgeting decisions. 2. Explain the payback model and its

Chapter 9 Capital Budgeting Decision Models Learning Objectives 1. Explain capital budgeting and differentiate between short-term and long-term budgeting decisions. 2. Explain the payback model and its

Portfolio management strategies:

Portfolio management strategies: Portfolio Management Strategies refer to the approaches that are applied for the efficient portfolio management in order to generate the highest possible returns at lowest

Portfolio management strategies: Portfolio Management Strategies refer to the approaches that are applied for the efficient portfolio management in order to generate the highest possible returns at lowest

SOLUTIONS TO END-OF-CHAPTER QUESTIONS CHAPTER 16

SOLUTIONS TO END-OF-CHAPTER QUESTIONS CHAPTER 16 DEVELOP YOUR UNDERSTANDING Question 16.1 Podcaster University Press Payback Accounting book Economics book Annual Cumulative Annual Cumulative cash flows

SOLUTIONS TO END-OF-CHAPTER QUESTIONS CHAPTER 16 DEVELOP YOUR UNDERSTANDING Question 16.1 Podcaster University Press Payback Accounting book Economics book Annual Cumulative Annual Cumulative cash flows

All In One MGT201 Mid Term Papers More Than (10) BY

BY") All In One MGT201 Mid Term Papers More Than (10) BY http://www.vustudents.net MIDTERM EXAMINATION MGT201- Financial Management (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one Why companies

All In One MGT201 Mid Term Papers More Than (10) BY http://www.vustudents.net MIDTERM EXAMINATION MGT201- Financial Management (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one Why companies

REVIEW MATERIALS FOR REAL ESTATE FUNDAMENTALS

REVIEW MATERIALS FOR REAL ESTATE FUNDAMENTALS 1997, Roy T. Black J. Andrew Hansz, Ph.D., CFA REAE 3325, Fall 2005 University of Texas, Arlington Department of Finance and Real Estate CONTENTS ITEM ANNUAL

REVIEW MATERIALS FOR REAL ESTATE FUNDAMENTALS 1997, Roy T. Black J. Andrew Hansz, Ph.D., CFA REAE 3325, Fall 2005 University of Texas, Arlington Department of Finance and Real Estate CONTENTS ITEM ANNUAL

Six Ways to Perform Economic Evaluations of Projects

Six Ways to Perform Economic Evaluations of Projects Course No: B03-003 Credit: 3 PDH A. Bhatia Continuing Education and Development, Inc. 9 Greyridge Farm Court Stony Point, NY 10980 P: (877) 322-5800

Six Ways to Perform Economic Evaluations of Projects Course No: B03-003 Credit: 3 PDH A. Bhatia Continuing Education and Development, Inc. 9 Greyridge Farm Court Stony Point, NY 10980 P: (877) 322-5800

Jacob: The illustrative worksheet shows the values of the simulation parameters in the upper left section (Cells D5:F10). Is this for documentation?

. Is this for documentation?") PROJECT TEMPLATE: DISCRETE CHANGE IN THE INFLATION RATE (The attached PDF file has better formatting.) {This posting explains how to simulate a discrete change in a parameter and how to use dummy variables

PROJECT TEMPLATE: DISCRETE CHANGE IN THE INFLATION RATE (The attached PDF file has better formatting.) {This posting explains how to simulate a discrete change in a parameter and how to use dummy variables

MGT201 Financial Management All Subjective and Objective Solved Midterm Papers for preparation of Midterm Exam2012 Question No: 1 ( Marks: 1 ) - Please choose one companies invest in projects with negative

MGT201 Financial Management All Subjective and Objective Solved Midterm Papers for preparation of Midterm Exam2012 Question No: 1 ( Marks: 1 ) - Please choose one companies invest in projects with negative

The NPV profile and IRR PITFALLS OF IRR. Years Cash flow Discount rate 10% NPV 472,27 IRR 11,6% NPV

PITFALLS OF IRR J.C. Neves, ISEG, 2018 23 The NPV profile and IRR Years 0 1 2 3 4 5 Cash flow -10000 2000 2500 1000 4000 5000 Discount rate 10% NPV 472,27 IRR 11,6% 5 000,00 NPV 4 000,00 3 000,00 2 000,00

PITFALLS OF IRR J.C. Neves, ISEG, 2018 23 The NPV profile and IRR Years 0 1 2 3 4 5 Cash flow -10000 2000 2500 1000 4000 5000 Discount rate 10% NPV 472,27 IRR 11,6% 5 000,00 NPV 4 000,00 3 000,00 2 000,00

The Process of Modeling

Session #3 Page 1 The Process of Modeling Plan Visualize where you want to finish Do some calculations by hand Sketch out a spreadsheet Build Start with a small-scale model Expand the model to full scale

Session #3 Page 1 The Process of Modeling Plan Visualize where you want to finish Do some calculations by hand Sketch out a spreadsheet Build Start with a small-scale model Expand the model to full scale

Chapter Organization. Net present value (NPV) is the difference between an investment s market value and its cost.

is the difference between an investment s market value and its cost.") Chapter 9 Net Present Value and Other Investment Criteria Chapter Organization 9.1. Net present value 9.2. The Payback Rule 9.3. The Discounted Payback 9.4. The Average Accounting Return 9.6. The Profitability

Chapter 9 Net Present Value and Other Investment Criteria Chapter Organization 9.1. Net present value 9.2. The Payback Rule 9.3. The Discounted Payback 9.4. The Average Accounting Return 9.6. The Profitability

Principles of Managerial Finance Solution Lawrence J. Gitman CHAPTER 10. Risk and Refinements In Capital Budgeting

Principles of Managerial Finance Solution Lawrence J. Gitman CHAPTER 10 Risk and Refinements In Capital Budgeting INSTRUCTOR S RESOURCES Overview Chapters 8 and 9 developed the major decision-making aspects

Principles of Managerial Finance Solution Lawrence J. Gitman CHAPTER 10 Risk and Refinements In Capital Budgeting INSTRUCTOR S RESOURCES Overview Chapters 8 and 9 developed the major decision-making aspects

WHAT IS CAPITAL BUDGETING?

WHAT IS CAPITAL BUDGETING? Capital budgeting is a required managerial tool. One duty of a financial manager is to choose investments with satisfactory cash flows and rates of return. Therefore, a financial

WHAT IS CAPITAL BUDGETING? Capital budgeting is a required managerial tool. One duty of a financial manager is to choose investments with satisfactory cash flows and rates of return. Therefore, a financial

Businesses will often invest money in order to meet their objectives - markets, relocation or training its existing workforce. Whatever the reason,

Chapter 9 Investment appraisal Businesses will often invest money in order to meet their objectives - these Businesses may will often include invest money sales in growth, order to meet increase their

Chapter 9 Investment appraisal Businesses will often invest money in order to meet their objectives - these Businesses may will often include invest money sales in growth, order to meet increase their

Corporate Finance: Introduction to Capital Budgeting

Corporate Finance: Introduction to Capital Budgeting João Carvalho das Neves Professor of Finance, ISEG jcneves@iseg.ulisboa.pt 2018-2019 1 WHAT IS CAPITAL BUDGETING? Capital budgeting is a formal process

Corporate Finance: Introduction to Capital Budgeting João Carvalho das Neves Professor of Finance, ISEG jcneves@iseg.ulisboa.pt 2018-2019 1 WHAT IS CAPITAL BUDGETING? Capital budgeting is a formal process

Seminar on Financial Management for Engineers. Institute of Engineers Pakistan (IEP)

") Seminar on Financial Management for Engineers Institute of Engineers Pakistan (IEP) Capital Budgeting: Techniques Presented by: H. Jamal Zubairi Data used in examples Project L Project L Project L Project

Seminar on Financial Management for Engineers Institute of Engineers Pakistan (IEP) Capital Budgeting: Techniques Presented by: H. Jamal Zubairi Data used in examples Project L Project L Project L Project

ENG2000 Chapter 16 Evaluating and Comparing Projects: The MARR. ENG2000: R.I. Hornsey CM: 1

ENG2000 Chapter 16 Evaluating and Comparing Projects: The MARR ENG2000: R.I. Hornsey CM: 1 Overview So, we have seen that the act of investing is to sacrifice something of present value in the expectation

ENG2000 Chapter 16 Evaluating and Comparing Projects: The MARR ENG2000: R.I. Hornsey CM: 1 Overview So, we have seen that the act of investing is to sacrifice something of present value in the expectation

1.011Project Evaluation: Comparing Costs & Benefits

1.11Project Evaluation: Comparing Costs & Benefits Carl D. Martland Basic Question: Are the future benefits large enough to justify the costs of the project? Present, Future, and Annual Worth Internal

1.11Project Evaluation: Comparing Costs & Benefits Carl D. Martland Basic Question: Are the future benefits large enough to justify the costs of the project? Present, Future, and Annual Worth Internal

1 INVESTMENT DECISIONS,

1 INVESTMENT DECISIONS, PROJECT PLANNING AND CONTROL THIS CHAPTER INCLUDES Estimation of Project Cash Flow Relevant Cost Analysis for Projects Project Appraisal Methods DCF and Non-DCF Techniques Capital

1 INVESTMENT DECISIONS, PROJECT PLANNING AND CONTROL THIS CHAPTER INCLUDES Estimation of Project Cash Flow Relevant Cost Analysis for Projects Project Appraisal Methods DCF and Non-DCF Techniques Capital

Capital Budgeting Decisions

Capital Budgeting Decisions Chapter 13 PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Copyright 2012

Capital Budgeting Decisions Chapter 13 PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Copyright 2012

BI360 Reporting and Budgeting Examples. A Solver White Paper

BI360 Reporting and Budgeting Examples A Solver White Paper July 2012 solverusa.com Copyright 2012 Table of Contents Solver Templates... 3 Basic Budgeting and Forecasting... 4 Five Year Budget... 4 Forecasting...

BI360 Reporting and Budgeting Examples A Solver White Paper July 2012 solverusa.com Copyright 2012 Table of Contents Solver Templates... 3 Basic Budgeting and Forecasting... 4 Five Year Budget... 4 Forecasting...

10. Estimate the MIRR for the project described in Problem 8. Does it change your decision on accepting this project?

1 CHAPTER 5 Problems and Questions 1. You have been given the following information on a project: It has a five-year lifetime The initial investment in the project will be $25 million, and the investment

1 CHAPTER 5 Problems and Questions 1. You have been given the following information on a project: It has a five-year lifetime The initial investment in the project will be $25 million, and the investment

CMA Part 2. Financial Decision Making

CMA Part 2 Financial Decision Making SU 8.1 The Capital Budgeting Process Capital budgeting is the process of planning and controlling investment for long-term projects. Will affect the company for many

CMA Part 2 Financial Decision Making SU 8.1 The Capital Budgeting Process Capital budgeting is the process of planning and controlling investment for long-term projects. Will affect the company for many

2.1 INTRODUCTION 2.2 PROJECTS: MEANING AND CONCEPT

Management UNIT 2 PROJECT APPRAISAL Structure 2.1 Introduction 2.2 Projects: Meaning and Concept 2.3 Difference Between a Project and a Programme 2.4 Criterion for Project Appraisal 2.5 Project Appraisal

Management UNIT 2 PROJECT APPRAISAL Structure 2.1 Introduction 2.2 Projects: Meaning and Concept 2.3 Difference Between a Project and a Programme 2.4 Criterion for Project Appraisal 2.5 Project Appraisal

MGT201 Lecture No. 11

MGT201 Lecture No. 11 Learning Objectives: In this lecture, we will discuss some special areas of capital budgeting in which the calculation of NPV & IRR is a bit more difficult. These concepts will be

MGT201 Lecture No. 11 Learning Objectives: In this lecture, we will discuss some special areas of capital budgeting in which the calculation of NPV & IRR is a bit more difficult. These concepts will be

Solar is a Bright Investment

Solar is a Bright Investment Investing in a solar system seems like a great idea, but what are the financial implications? How much will it cost and what is the payback? These are common questions that

Solar is a Bright Investment Investing in a solar system seems like a great idea, but what are the financial implications? How much will it cost and what is the payback? These are common questions that

MENG 547 Energy Management & Utilization

MENG 547 Energy Management & Utilization Chapter 4 Economic Decisions for Energy Projects Prof. Dr. Ugur Atikol, cea Director of EMU Energy Research Centre The Need for Economic Analysis The decision on

MENG 547 Energy Management & Utilization Chapter 4 Economic Decisions for Energy Projects Prof. Dr. Ugur Atikol, cea Director of EMU Energy Research Centre The Need for Economic Analysis The decision on

Many decisions in operations management involve large

SUPPLEMENT Financial Analysis J LEARNING GOALS After reading this supplement, you should be able to: 1. Explain the time value of money concept. 2. Demonstrate the use of the net present value, internal

SUPPLEMENT Financial Analysis J LEARNING GOALS After reading this supplement, you should be able to: 1. Explain the time value of money concept. 2. Demonstrate the use of the net present value, internal

Lecture 5 Present-Worth Analysis

Seg2510 Management Principles for Engineering Managers Lecture 5 Present-Worth Analysis Department of Systems Engineering and Engineering Management The Chinese University of Hong Kong 1 Part I Review

Seg2510 Management Principles for Engineering Managers Lecture 5 Present-Worth Analysis Department of Systems Engineering and Engineering Management The Chinese University of Hong Kong 1 Part I Review

Chapter 9 Net Present Value and Other Investment Criteria. Net Present Value (NPV) Net Present Value (NPV) Konan Chan. Financial Management, Fall 2018

Net Present Value (NPV) Konan Chan. Financial Management, Fall 2018") Chapter 9 Net Present Value and Other Investment Criteria Konan Chan Financial Management, Fall 2018 Topics Covered Investment Criteria Net Present Value (NPV) Payback Period Discounted Payback Average

Chapter 9 Net Present Value and Other Investment Criteria Konan Chan Financial Management, Fall 2018 Topics Covered Investment Criteria Net Present Value (NPV) Payback Period Discounted Payback Average

MULTIPLE-CHOICE QUESTIONS Circle the correct answer on this test paper and record it on the computer answer sheet.

M I M E 3 1 0 E N G I N E E R I N G E C O N O M Y Class Test #2 Thursday, 23 March, 2006 90 minutes PRINT your family name / initial and record your student ID number in the spaces provided below. FAMILY

M I M E 3 1 0 E N G I N E E R I N G E C O N O M Y Class Test #2 Thursday, 23 March, 2006 90 minutes PRINT your family name / initial and record your student ID number in the spaces provided below. FAMILY

FINANCIAL MANAGEMENT V SEMESTER. B.Com FINANCE SPECIALIZATION CORE COURSE. (CUCBCSSS Admission onwards) UNIVERSITY OF CALICUT

UNIVERSITY OF CALICUT") FINANCIAL MANAGEMENT (ADDITIONAL LESSONS) V SEMESTER B.Com UNIVERSITY OF CALICUT SCHOOL OF DISTANCE EDUCATION STUDY MATERIAL Core Course B.Sc. COUNSELLING PSYCHOLOGY III Semester physiological psychology

FINANCIAL MANAGEMENT (ADDITIONAL LESSONS) V SEMESTER B.Com UNIVERSITY OF CALICUT SCHOOL OF DISTANCE EDUCATION STUDY MATERIAL Core Course B.Sc. COUNSELLING PSYCHOLOGY III Semester physiological psychology

UNIT 5 COST OF CAPITAL

UNIT 5 COST OF CAPITAL UNIT 5 COST OF CAPITAL Cost of Capital Structure 5.0 Introduction 5.1 Unit Objectives 5.2 Concept of Cost of Capital 5.3 Importance of Cost of Capital 5.4 Classification of Cost

UNIT 5 COST OF CAPITAL UNIT 5 COST OF CAPITAL Cost of Capital Structure 5.0 Introduction 5.1 Unit Objectives 5.2 Concept of Cost of Capital 5.3 Importance of Cost of Capital 5.4 Classification of Cost

2/9/2010. Investment Appraisal. Investment Appraisal. Investment Appraisal. Investment Appraisal. Investment Appraisal. Investment Appraisal

A means of assessing whether an investment project is worthwhile or not Investment project could be the purchase of a new PC for a small firm, a new piece of equipment in a manufacturing plant, a whole

A means of assessing whether an investment project is worthwhile or not Investment project could be the purchase of a new PC for a small firm, a new piece of equipment in a manufacturing plant, a whole

Topic 1 (Week 1): Capital Budgeting

: Capital Budgeting") 4.2. The Three Rules of Time Travel Rule 1: Comparing and combining values Topic 1 (Week 1): Capital Budgeting It is only possible to compare or combine values at the same point in time. A dollar today

4.2. The Three Rules of Time Travel Rule 1: Comparing and combining values Topic 1 (Week 1): Capital Budgeting It is only possible to compare or combine values at the same point in time. A dollar today

Important questions prepared by Mirza Rafathulla Baig. For B.com & MBA Important questions visit

Financial Management -MBA-II SEM 1. Charm plc, a software company, has developed a new game, Fingo, which it plans to launch in the near future. Sales of the new game are expected to be very strong, following

Financial Management -MBA-II SEM 1. Charm plc, a software company, has developed a new game, Fingo, which it plans to launch in the near future. Sales of the new game are expected to be very strong, following

Net Present Value Q: Suppose we can invest $50 today & receive $60 later today. What is our increase in value? Net Present Value Suppose we can invest

Ch. 11 The Basics of Capital Budgeting Topics Net Present Value Other Investment Criteria IRR Payback What is capital budgeting? Analysis of potential additions to fixed assets. Long-term decisions; involve

Ch. 11 The Basics of Capital Budgeting Topics Net Present Value Other Investment Criteria IRR Payback What is capital budgeting? Analysis of potential additions to fixed assets. Long-term decisions; involve

MBF1223 Financial Management Prepared by Dr Khairul Anuar

MBF1223 Financial Management Prepared by Dr Khairul Anuar L7 - Capital Budgeting Decision Models www.mba638.wordpress.com Learning Objectives 1. Explain capital budgeting and differentiate between short-term

MBF1223 Financial Management Prepared by Dr Khairul Anuar L7 - Capital Budgeting Decision Models www.mba638.wordpress.com Learning Objectives 1. Explain capital budgeting and differentiate between short-term

Chapter 6 Capital Budgeting

Chapter 6 Capital Budgeting The objectives of this chapter are to enable you to: Understand different methods for analyzing budgeting of corporate cash flows Determine relevant cash flows for a project

Chapter 6 Capital Budgeting The objectives of this chapter are to enable you to: Understand different methods for analyzing budgeting of corporate cash flows Determine relevant cash flows for a project

BFC2140: Corporate Finance 1

BFC2140: Corporate Finance 1 Table of Contents Topic 1: Introduction to Financial Mathematics... 2 Topic 2: Financial Mathematics II... 5 Topic 3: Valuation of Bonds & Equities... 9 Topic 4: Project Evaluation

BFC2140: Corporate Finance 1 Table of Contents Topic 1: Introduction to Financial Mathematics... 2 Topic 2: Financial Mathematics II... 5 Topic 3: Valuation of Bonds & Equities... 9 Topic 4: Project Evaluation

Software Economics. Metrics of Business Case Analysis Part 1

Software Economics Metrics of Business Case Analysis Part 1 Today Last Session we covered FV, PV and NPV We started with setting up the financials of a Business Case We talked about measurements to compare

Software Economics Metrics of Business Case Analysis Part 1 Today Last Session we covered FV, PV and NPV We started with setting up the financials of a Business Case We talked about measurements to compare

MANAGEMENT INFORMATION

CERTIFICATE LEVEL EXAMINATION SAMPLE PAPER 3 (90 MINUTES) MANAGEMENT INFORMATION This assessment consists of ONE scenario based question worth 20 marks and 32 short questions each worth 2.5 marks. At least

CERTIFICATE LEVEL EXAMINATION SAMPLE PAPER 3 (90 MINUTES) MANAGEMENT INFORMATION This assessment consists of ONE scenario based question worth 20 marks and 32 short questions each worth 2.5 marks. At least