Understanding the Cost Accounting Standards. Bag Lunch Webinar May 9, 2018

|

|

|

- Gervais Lloyd

- 5 years ago

- Views:

Transcription

1 Understanding the Cost Accounting Standards Bag Lunch Webinar May 9,

2 Co-Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager n Tel: n pcalabrese@rubino.com n

3 Co-Presenter: G. Chris Brown Aldebaron, Inc. d/b/a SYMPAQ Vice President n Tel: , Ext n n Cbrown@sympaq.com

4 Co-Presenter: Steven Shamlian, CPA Government Contract Compliance Management, LLC Founder n Tel: n sshamlian@gccm-llc.com n Firm Bio:

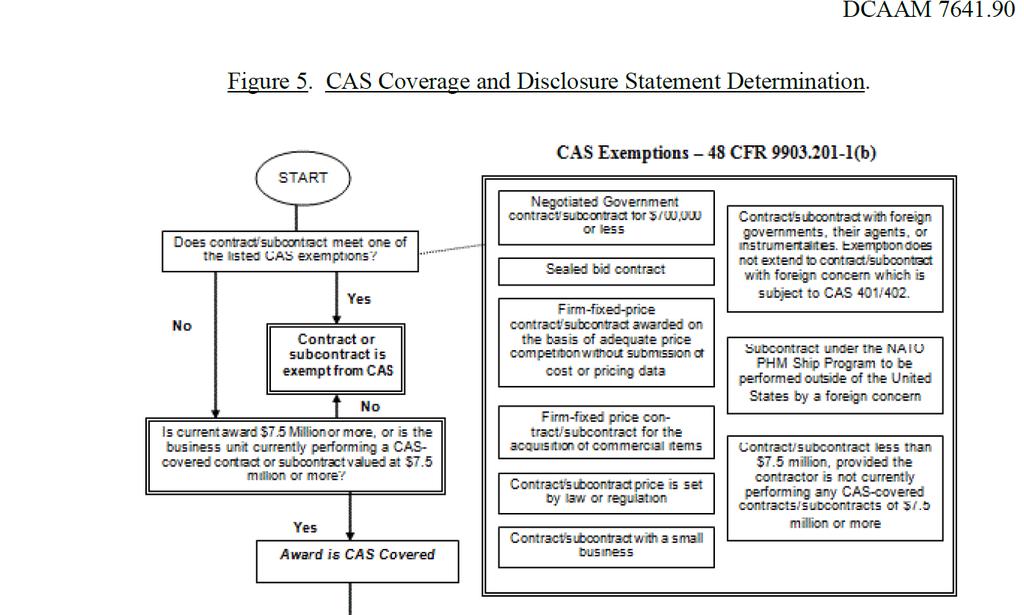

5 Sources q The Cost Accounting Standards (CAS) in FAR 9903 and 9904 q DCAAM , Figure 5

6 6

7 Overview n CAS Applicability n Significance of CAS Thresholds n Application of CAS Thresholds 7

8 CAS Applicability 8

9 Purpose of CAS n Achieve uniformity and consistency in cost accounting practices among contractors and subcontractors n Prerequisite to contracting n Disclose cost accounting practices n Agree to downward price adjustment if non-compliance w/standard, disclosed or established practice 9

10 Contracts Exempt from CAS n Sealed Bid n Award values less than $750,000 n Small Business n Foreign Governments n Price set by law or regulation n FFP & FPEconomicPriceAdjustment, T&M, fixed labor hour contracts for acquisition of commercial items n Award value less than $7.5 million if not performing on CAS covered contracts valued at $7.5 million n Executed and performed entirely outside US n FFP with price competition and with no cost or 10 pricing data submitted

11 Exemption from CAS n Price or Costing Data Threshold n FAR (a1) n $750,000 n Exemption to CAS Coverage n $750,000 11

12 Exemption from CAS n Contracts or subcontracts having an awarded value of less than $7,500,000 n Provided that, at the time of award, the business unit of the contractor or subcontractor is not currently performing any CAS-covered contract or subcontract with a value > = $750,000 12

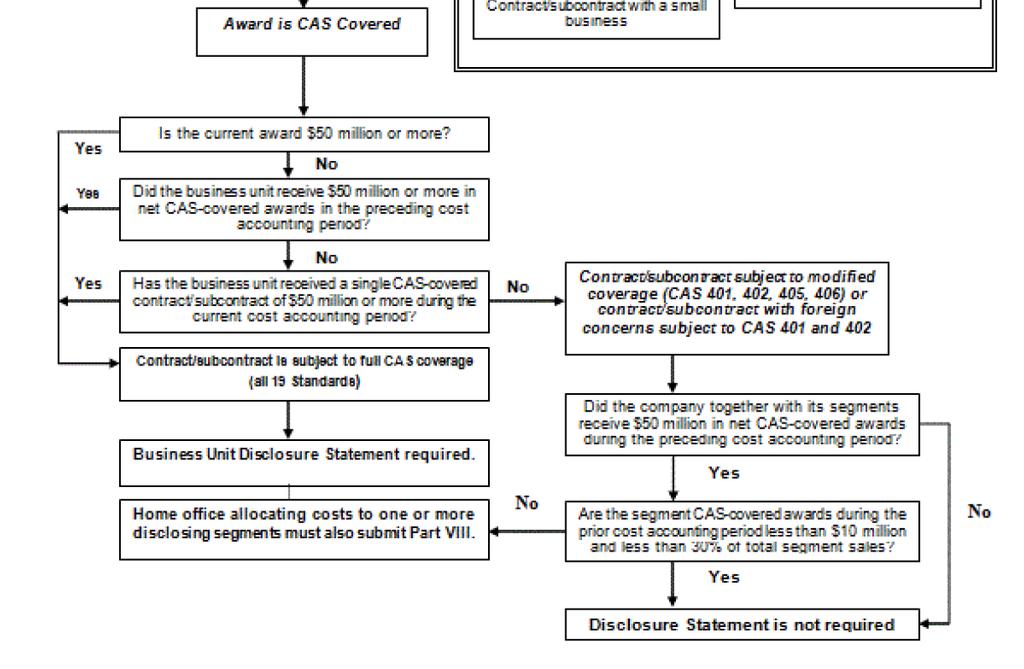

13 Exemption from CAS Definition of currently performing n a contractor has been awarded a contract, but has not yet received notification of final acceptance of all supplies, services, and data deliverable under the contract (including options) 13

14 Exemption from CAS n Initial $750,000 trigger n negotiated contracts and subcontracts not in excess of $750,000 tied to TINA threshold (Truthful Cost or Pricing Data) n The $7.5 million threshold applies only if there is not one, single CAS-covered contract currently being performed 14

15 15

16 16

17 What is the significance of the CAS thresholds?

18 Assessing Cost Impact Complex Matrix n n n n n Contract by contract basis: exempt from CAS, modified or full CAS coverage Measure the potential value of applicable modified and/or full CAS contracts Compute impact from point of noncompliance or change to end of contract(s) Determine impact on a Business Unit by Business Unit basis (if more than one) CAS status (modified or full) may change from fiscal year to fiscal year 18

19 Definition of Business Unit n n Business unit means any segment of an organization, or an entire business organization which is not divided into segments. Segment means one of two or more divisions, product departments, plants, or other subdivisions of an organization reporting directly to a home office, usually identified with responsibility for profit and/or producing a product or service. The terms include Government-owned contractor-operated (GOCO) facilities, and joint ventures and subsidiaries (domestic and foreign) in which the organization has a majority ownership. 19

20 Application of Coverages n Types of CAS Coverage n FAR (b), Modified, (1) (3) n Modified status for a Business Unit (BU) that receives less than $50 Million (M) in net awards in the previous accounting period where no one contract award was greater than $50 M. n Modified coverage involves only 4 CAS standards 401, 402, 405 and 406, and not the entire 19 CAS standards 20

21 Application of Coverages n If one contract is awarded as modified CAS than all CAS contracts awarded thereafter during that fiscal period awarded to that B.U. have Modified coverage n Exception to prior rule n If B.U. receives one CAS covered contract that is greater than $50 M, then that contract and all other contracts thereafter receive Full CAS coverage during the same fiscal year. n Note: the contracts awarded with modified coverage before the $50 M award remain as having modified coverage 21

22 Application of Coverages n Principal regarding CAS Coverage n Once a contract has modified coverage, it will not change its coverage regardless if the B.U. has a change of status (type of CAS coverage) in subsequent accounting periods. n Likewise, once a contract is full covered, it is always fully covered. n Likewise, once a contract is exempt from CAS coverage, it is always exempt from CAS. 22

23 Application of the CAS thresholds

24 Application of Thresholds n Importance of CAS tracking system n Identifying contracts with CAS clause n FAR

25 Application of Thresholds n CAS tracking system must measure an award n Net awards n the total value of negotiated CAS-covered prime contract and subcontract awards, including the potential value of contract options, received during the reporting period minus cancellations, terminations, and other related credit transactions. 25

26 Example: CAS 418 Non-Compliance in FY 2018 n If B.U. has full CAS coverage in current fiscal period FY 2018 n Previous contracts remain exempt from CAS, such as executed and performed entirely outside the U.S. n Previous year s modified CAS contracts are not impacted by

27 Example: CAS 418 Non-Compliance in FY 2018 n If B.U. has full CAS coverage in fiscal period FY 2018 n Only contracts with full CAS would be impacted by the 418 non-compliance n Consideration of materiality n Compute impact from the date of the proposed change until the completion of each of the identified contracts with FULL CAS Coverage 27

28 Example: CAS 418 Non-Compliance in FY 2018 n Allocation can still be challenged on the modified CAS and exempt contracts n FAR Determining allocability n Cost adjustments would only apply in years with unsettled burden rates via incurred cost package n Cannot adjust FFP, only flexibly priced contracts n Unlike cost impact statements, it would not apply to future years until the end of those contracts, i.e. fiscal periods not yet started 28

29 Example: CAS 401 Non-Compliance in FY 2018 n If B.U. has modified coverage in fiscal period FY 2018 n Contracts with exempt status would remain exempt n Modified CAS contracts awarded would be impacted during FY 2018 n In the above scenario of modified coverage, a non-compliance would only apply to four CAS standards : CAS 401, 402, 405,

30 1/27/2018 Steve Shamlian / GCCM, LLC 30 COST ACCOUNTING STANDARDS A 30,000 Foot Review

31 1/27/2018 Steve Shamlian / GCCM, LLC 31 How many have CAS-covered contracts? How many want CAS-covered contracts? How many want to become successful businesses, with big Government contracts, providing goods and services that no one else can provide? How many want to continue as a small business making good money with little oversight?

32 1/27/2018 Steve Shamlian / GCCM, LLC 32 CAS Coverage Should Be A Strategic Business Decision

33 What could possibly go wrong?

34 1/27/2018 Steve Shamlian / GCCM, LLC 34 What could possibly go wrong. Failure to comply with standards Failure to consistently follow your established cost accounting practices Failure to timely disclose cost accounting practices Failure to appropriately represent your level of CAS coverage Exempt Modified coverage Full coverage DS Digression

35 1/27/2018 Steve Shamlian / GCCM, LLC 35 Consequences Failure to have contracts awarded. Retroactive price adjustments plus interest. Retroactive price adjustments without interest.

36 1/27/2018 Steve Shamlian / GCCM, LLC 36 Computation of Cost Impact (FAR (h)) Include all affected CAS-covered contracts and subcontracts regardless of their status (i.e., open or closed) or the fiscal year(s) in which the costs are incurred (i.e., whether or not the final indirect rates have been established) (FAR (h))

37 1/27/2018 Steve Shamlian / GCCM, LLC 37 Computation of Cost Impact (FAR (h)) Estimating Costs: When the negotiated contract or subcontract price exceeds what the negotiated price would have been had the contractor used a compliant practice, the difference is increased cost to the Government. Accumulating Costs: When the costs that were accumulated under the noncompliant practice exceed the costs that would have been accumulated using a compliant practice (from the time the noncompliant practice was first implemented until the date the noncompliant practice was replaced with a compliant practice), the difference is increased cost to the Government.

38 1/27/2018 Steve Shamlian / GCCM, LLC 38 Computation of Cost Impact (FAR (h)) Increased Cost to the Government: Flexibly-priced contracts the estimated cost to complete using the changed practice exceeds the estimated cost to complete using the current practice Fixed priced contracts the estimated cost to complete using the changed practice is less than the estimated cost to complete using the current practice

39 1/27/2018 Steve Shamlian / GCCM, LLC 39 Avoiding the Consequences - Exempt Exemptions:

40 1/27/2018 Steve Shamlian / GCCM, LLC 40 Avoiding the Consequences - Threshold Not CAS - Covered: Contracts less than $7.5 million prior to award of a CAS-covered contract of at lease $7.5 million Modified CAS Covered: Contracts greater than $750,000 after award of a CAS-covered contract of $7.5 million Full CAS Covered: Upon award of a CAS-covered contract of $50 million The year following $50 million in CAS-covered awards

41 1/27/2018 Steve Shamlian / GCCM, LLC 41 What is award value? a) The contract price the contractor is guaranteed b) The price including unawarded options c) The first year sales resulting from the contract

42 1/27/2018 Steve Shamlian / GCCM, LLC 42 Considering only the thresholds, how large does a contractor have to be to have CAS-covered contracts? a) Only the LockheedMartin, NorthropGrummans, etc. of the world. b) Significant contractors with at lease $100 million of annual sales. c) Contractors that are a lot smaller that the regulators were probably thinking

43 1/27/2018 Steve Shamlian / GCCM, LLC 43 Avoiding the Consequences - Compliance Fundamental Concepts: Cost accounting practices should be followed consistently Cost accounting practice: Measures costs Assigns costs to cost accounting periods Allocates costs to cost objectives (includes direct and indirect allocation) Allocations of costs are based on a causal or beneficial relationship of the costs to the cost objectives Homogeneous costs may be grouped into cost pools The enterprise will continue The life of the enterprise is divided into cost accounting periods Depreciation or amortization of assets or liabilities is over the useful life of the asset or liability

44 1/27/2018 Steve Shamlian / GCCM, LLC 44 Illustration of Consistency Estimating, accumulating, and reporting costs (CAS 401) Allocating costs incurred for the same purpose (CAS 402) Accounting for unallowable costs (CAS 405)

45 1/27/2018 Steve Shamlian / GCCM, LLC 45 Illustration of Homogeneity Costs from a home office (CAS 403) Standard costs (CAS 407) Allocation of G&A expenses (CAS 410) Material (CAS 411) Direct and indirect costs (CAS 418)

46 1/27/2018 Steve Shamlian / GCCM, LLC 46 Illustration of Continuity of the Enterprise Depreciation of capital assets (404 & 409) Cost accounting period (CAS 406) Cost of compensated personal absence (CAS 408) Pension (412 & 413) Cost of money (CAS 414 & 417) Deferred compensation (CAS 415) Insurance (CAS 416) IRAD/B&P (CAS 420)

47 1/27/2018 Steve Shamlian / GCCM, LLC 47 What will happen The Good: Better position to win larger contracts for goods and services only you can provide. The Bad: Increased compliance cost The Ugly: Increased Government oversight

48 1/27/2018 Steve Shamlian / GCCM, LLC 48 A Strategic Decision Anticipate or avoid coverage by knowing the exemptions and thresholds Follow the concepts applicable to your business Internal controls to document cost accounting practices and follow them consistently

49 Any Questions 49

50 The materials contained herein or discussed in the session or shown in the MS Powerpoint slides, are for illustrative and academic purposes only and should not be considered appropriate for your organization without careful adaptation by experts in the appropriate field of endeavor. DISCLAIMER

Indirect Cost Rates For Nonprofit Organizations

Indirect Cost Rates For Nonprofit Organizations Bag Lunch Webinar May 8, 2013 All slides and handouts copyright 2013, Rubino & Company, Chartered Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants

Indirect Cost Rates For Nonprofit Organizations Bag Lunch Webinar May 8, 2013 All slides and handouts copyright 2013, Rubino & Company, Chartered Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants

What Happens to Indirect Rates under the Uniform Guidance Bag Lunch Webinar November 19, 2015

What Happens to Indirect Rates under the Uniform Guidance Bag Lunch Webinar November 19, 2015 Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager Tel: 301-214-4137 pcalabrese@rubino.com

What Happens to Indirect Rates under the Uniform Guidance Bag Lunch Webinar November 19, 2015 Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager Tel: 301-214-4137 pcalabrese@rubino.com

Indirect Cost Rates For Nonprofit Organizations

Indirect Cost Rates For Nonprofit Organizations Bag Lunch Webinar October 10, 2012 All slides and handouts copyright 2012, Rubino & Company, Chartered Presenter: Paul H. Calabrese Rubino & Company, CPAs

Indirect Cost Rates For Nonprofit Organizations Bag Lunch Webinar October 10, 2012 All slides and handouts copyright 2012, Rubino & Company, Chartered Presenter: Paul H. Calabrese Rubino & Company, CPAs

Indirect Cost Rates & What Happens Under. Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager

Indirect Cost Rates & What Happens Under the New Super Circular Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager Tel: 301-214-4137 pcalabrese@rubino.com www.linkedin.com/pub/paul-calabrese/20/293/645/

Indirect Cost Rates & What Happens Under the New Super Circular Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager Tel: 301-214-4137 pcalabrese@rubino.com www.linkedin.com/pub/paul-calabrese/20/293/645/

Cost Accounting Standards

Cost Accounting Standards Application of CAS and Modified CAS Coverage September 13, 2016 Agenda Introduction CAS applicability Exceptions to CAS Determining contract value for purposes of CAS Disclosure

Cost Accounting Standards Application of CAS and Modified CAS Coverage September 13, 2016 Agenda Introduction CAS applicability Exceptions to CAS Determining contract value for purposes of CAS Disclosure

COST AND PRICING: NO CONTRACT IS REALLY FINAL. Terry Albertson Skye Mathieson Liz Buehler

COST AND PRICING: NO CONTRACT IS REALLY FINAL Terry Albertson Skye Mathieson Liz Buehler 79 Three Phases Proposal Performance and Billing Final Payment 80 Proposal Forward pricing rates Labor rates Indirect

COST AND PRICING: NO CONTRACT IS REALLY FINAL Terry Albertson Skye Mathieson Liz Buehler 79 Three Phases Proposal Performance and Billing Final Payment 80 Proposal Forward pricing rates Labor rates Indirect

FAR Part 31.2 Cost Principles Impacting Indirect Rates. Bag Lunch Webinar April 26, 2018

FAR Part 31.2 Cost Principles Impacting Indirect Rates Bag Lunch Webinar April 26, 2018 1 Co-Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager Tel: 301-214-4137 pcalabrese@rubino.com

FAR Part 31.2 Cost Principles Impacting Indirect Rates Bag Lunch Webinar April 26, 2018 1 Co-Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager Tel: 301-214-4137 pcalabrese@rubino.com

Introduction to the Cost Accounting Standards Mike Mardesich & Brad Tress April 25, 2017

Introduction to the Cost Accounting Standards Mike Mardesich & Brad Tress April 25, 2017 The Fundamentals of Government Contracting Webinar Series 1 Your Presenters Mike Mardesich Dixon Hughes Goodman

Introduction to the Cost Accounting Standards Mike Mardesich & Brad Tress April 25, 2017 The Fundamentals of Government Contracting Webinar Series 1 Your Presenters Mike Mardesich Dixon Hughes Goodman

How to Develop Indirect Rates Under the New Super Circular. Part 1 Webinar 1 or 2 Slide Decks Rubino & Company, Chartered May 8, 2014

How to Develop Indirect Rates Under the New Super Circular Part 1 Webinar 1 or 2 Slide Decks Rubino & Company, Chartered May 8, 2014 Click Update to / Impact edit Master of Super Circular text styles Definitions

How to Develop Indirect Rates Under the New Super Circular Part 1 Webinar 1 or 2 Slide Decks Rubino & Company, Chartered May 8, 2014 Click Update to / Impact edit Master of Super Circular text styles Definitions

How to Develop Indirect Cost Rates For Nonprofit Organizations

How to Develop Indirect Cost Rates For Nonprofit Organizations 2010 Government and Not-For-Profit Conference UMD University College Adelphi, Maryland April 30, 2010 Presenter: Paul H. Calabrese Rubino

How to Develop Indirect Cost Rates For Nonprofit Organizations 2010 Government and Not-For-Profit Conference UMD University College Adelphi, Maryland April 30, 2010 Presenter: Paul H. Calabrese Rubino

F i v e C A S S t a n d a r d s E v e r y G o v e r n m e n t C o n t r a c t o r S h o u l d K n o w a n d F o l l o w

F i v e C A S S t a n d a r d s E v e r y G o v e r n m e n t C o n t r a c t o r S h o u l d K n o w a n d F o l l o w December 17, 2015 Presented by: Darrell Hineman, CPA CFE Director Long Nguyen, CFE

F i v e C A S S t a n d a r d s E v e r y G o v e r n m e n t C o n t r a c t o r S h o u l d K n o w a n d F o l l o w December 17, 2015 Presented by: Darrell Hineman, CPA CFE Director Long Nguyen, CFE

Presented by CohnReznick s Government Contracting Industry Practice. Kristen Soles, CPA, Partner & Kiran Pinto, CPA, Senior Manager

A u d i t R e a d y : A n I n s i d e r s G u i d e t o G o v e r n m e n t C o n t r a c t A u d i t s & C o m p l i a n c e Presented by CohnReznick s Government Contracting Industry Practice Kristen

A u d i t R e a d y : A n I n s i d e r s G u i d e t o G o v e r n m e n t C o n t r a c t A u d i t s & C o m p l i a n c e Presented by CohnReznick s Government Contracting Industry Practice Kristen

ACCOUNTING SYSTEMS for SBIR/STTR AWARDS. Presented by: Mike Anderson

ACCOUNTING SYSTEMS for SBIR/STTR AWARDS Presented by: Mike Anderson Seminar Objectives What is the Difference Between a Grant and a Contract Accounting Requirements For Cost-Type Awards What are Audit

ACCOUNTING SYSTEMS for SBIR/STTR AWARDS Presented by: Mike Anderson Seminar Objectives What is the Difference Between a Grant and a Contract Accounting Requirements For Cost-Type Awards What are Audit

Challenges of Contracting with the Federal Government November 19 th, 2015

Challenges of Contracting with the Federal Government November 19 th, 2015 The Fundamentals of Government Contracting Webinar Series 1 Your Presenters David King Dixon Hughes Goodman, LLP 703.970.0433

Challenges of Contracting with the Federal Government November 19 th, 2015 The Fundamentals of Government Contracting Webinar Series 1 Your Presenters David King Dixon Hughes Goodman, LLP 703.970.0433

Small. B u s i n e s s, G r o w Y o u r. T o. Y o u M u s t P l a n. f o r G r o w t h

Emerging Businesses: Small T o G r o w Y o u r B u s i n e s s, Y o u M u s t P l a n f o r G r o w t h 18 Contract Management January 2009 Emerging small businesses must plan for growth by ensuring systems

Emerging Businesses: Small T o G r o w Y o u r B u s i n e s s, Y o u M u s t P l a n f o r G r o w t h 18 Contract Management January 2009 Emerging small businesses must plan for growth by ensuring systems

Cost Accounting Standards: Overview and Best Practices

Cost Accounting Standards: Overview and Best Practices Joseph G. Martinez K. Tyler Thomas October 10, 2017 Agenda Introduction to the Cost Accounting Standards ("CAS") Overview/Fundamental Requirements

Cost Accounting Standards: Overview and Best Practices Joseph G. Martinez K. Tyler Thomas October 10, 2017 Agenda Introduction to the Cost Accounting Standards ("CAS") Overview/Fundamental Requirements

CAS - Part II. The Cost Allocation Standards Dixon Hughes Goodman, LLP

CAS - Part II The Cost Allocation Standards 1 Agenda Session I Administration: CAS Overview Applicability Types of Coverage CAS Administration Part II - The Cost Allocation Standards Part III - The Cost

CAS - Part II The Cost Allocation Standards 1 Agenda Session I Administration: CAS Overview Applicability Types of Coverage CAS Administration Part II - The Cost Allocation Standards Part III - The Cost

COST ACCOUNTING STANDARDS NOTICES AND CERTIFICATION

COST ACCOUNTING STANDARDS NOTICES AND CERTIFICATION Introduction The Prime Contract under which this solicitation is issued requires that APL determine the applicability of Cost Accounting Standards Board

COST ACCOUNTING STANDARDS NOTICES AND CERTIFICATION Introduction The Prime Contract under which this solicitation is issued requires that APL determine the applicability of Cost Accounting Standards Board

Chapter 37 Joint Ventures and Teaming Arrangements

Chapter 37 Joint Ventures and Teaming Arrangements Authoritative Sources Cost Accounting Standards FAR Subpart 9.6 Contractor Team Arrangements FASB ASC 323 Investments - Equity Method and Joint Ventures

Chapter 37 Joint Ventures and Teaming Arrangements Authoritative Sources Cost Accounting Standards FAR Subpart 9.6 Contractor Team Arrangements FASB ASC 323 Investments - Equity Method and Joint Ventures

Cost Accounting Standards

Cost Accounting Standards Bill Walter Partner - Government Contract Consulting McLean, Virginia (703) 970-0509 bill.walter@dhgllp.com 1 Agenda Session I Administration: CAS Overview Applicability Types

Cost Accounting Standards Bill Walter Partner - Government Contract Consulting McLean, Virginia (703) 970-0509 bill.walter@dhgllp.com 1 Agenda Session I Administration: CAS Overview Applicability Types

N o w h e r e t o R u n, N o w h e r e t o H i d e : D i s c l o s u r e S t a t e m e n t s a n d C o s t A c c o u n t i n g S t a n d a r d s

N o w h e r e t o R u n, N o w h e r e t o H i d e : D i s c l o s u r e S t a t e m e n t s a n d C o s t A c c o u n t i n g S t a n d a r d s Presented by Darrell Hineman, CPA, CFE, Director Jeff Shapiro,

N o w h e r e t o R u n, N o w h e r e t o H i d e : D i s c l o s u r e S t a t e m e n t s a n d C o s t A c c o u n t i n g S t a n d a r d s Presented by Darrell Hineman, CPA, CFE, Director Jeff Shapiro,

TERMINATION AHEAD SLOW DOWN

Contract Terminations Not So Convenient Presented by Paul Slemons & Darrell M. Hineman TERMINATION AHEAD SLOW DOWN Please Read This presentation has been prepared for information purposes and general guidance

Contract Terminations Not So Convenient Presented by Paul Slemons & Darrell M. Hineman TERMINATION AHEAD SLOW DOWN Please Read This presentation has been prepared for information purposes and general guidance

Lunch n Learn 14 MAR 18 Cost Accounting Standards (CAS) - Applicability

- Applicability") Lunch n Learn 14 MAR 18 Cost Accounting Standards (CAS) - Applicability Session will start at 1230 EDT (1130 CDT). Audio will be through DCS there will be a sound check 30 minutes prior to the session.

Lunch n Learn 14 MAR 18 Cost Accounting Standards (CAS) - Applicability Session will start at 1230 EDT (1130 CDT). Audio will be through DCS there will be a sound check 30 minutes prior to the session.

Are You Subject to the. Standards? Nicole Mitchell, CPA Partner Aronson LLC. June 22, 2011

Are You Subject to the Cost Accounting Standards? Nicole Mitchell, CPA Partner Aronson LLC June 22, 2011 2011 All Rights Reserved 805 King Farm Boulevard Suite 300 Rockville, Maryland 20850 301.231.6200

Are You Subject to the Cost Accounting Standards? Nicole Mitchell, CPA Partner Aronson LLC June 22, 2011 2011 All Rights Reserved 805 King Farm Boulevard Suite 300 Rockville, Maryland 20850 301.231.6200

PANEL E: Costly Mistakes!

PANEL E: Costly Mistakes! How to avoid the most common pitfalls that face a growing company. Lessons learned from an operational and legal perspective that may help you make money and stay out of jail!

PANEL E: Costly Mistakes! How to avoid the most common pitfalls that face a growing company. Lessons learned from an operational and legal perspective that may help you make money and stay out of jail!

Federal Acquisition Regulation: Small Business Subcontracting Improvements

Federal Acquisition Regulation: Small Business Subcontracting Improvements FAC 2005-89, FAR Case 2014-003 Implementation Under Multiple Award Schedules 1 FAR rule (FAC 2005-89/FAR case 2014-003): Subcontracting

Federal Acquisition Regulation: Small Business Subcontracting Improvements FAC 2005-89, FAR Case 2014-003 Implementation Under Multiple Award Schedules 1 FAR rule (FAC 2005-89/FAR case 2014-003): Subcontracting

Allowability of Subcontractor/ Consultant Costs and the Challenges Presented for Procurement System Management

Allowability of Subcontractor/ Consultant Costs and the Challenges Presented for Procurement System Management Breakout Session #: B11 Presented by: Melanie Burgess and Phillip Seckman Date: July 22, 2013

Allowability of Subcontractor/ Consultant Costs and the Challenges Presented for Procurement System Management Breakout Session #: B11 Presented by: Melanie Burgess and Phillip Seckman Date: July 22, 2013

Topics for Discussion

Government Contracting Update September 2010 Presentation By: James W. Thomas LLP PwC New and Proposed Regulations - Cost or Pricing Data - Acquisition Thresholds - Business Systems - Pensions - Security

Government Contracting Update September 2010 Presentation By: James W. Thomas LLP PwC New and Proposed Regulations - Cost or Pricing Data - Acquisition Thresholds - Business Systems - Pensions - Security

Click to edit Master title style

Click to edit Master title style Fourth level The Cost Accounting Standards and Consequences of Noncompliance Click to edit Master text styles Click to edit Master title style Breakout Third Session level

Click to edit Master title style Fourth level The Cost Accounting Standards and Consequences of Noncompliance Click to edit Master text styles Click to edit Master title style Breakout Third Session level

GOVERNMENT CONTRACT COSTS, PRICING & ACCOUNTING REPORT

Reprinted with permission from Government Contract Costs, Pricing& Accounting Report, Volume 12, Issue 1, K2017 Thomson Reuters. Further reproduction without permission of the publisher is prohibited.

Reprinted with permission from Government Contract Costs, Pricing& Accounting Report, Volume 12, Issue 1, K2017 Thomson Reuters. Further reproduction without permission of the publisher is prohibited.

Subcontracting Under USG Contracts. The Differing Viewpoints Prime Contractor Abuses

Subcontracting Under USG Contracts The Differing Viewpoints Prime Contractor Abuses Steve Purcell Senior Contracts Manager ViaSat Inc. Steve.Purcell@viasat.com 1 SUBCONTRACTING UNDER USG CONTRACTS-WHY

Subcontracting Under USG Contracts The Differing Viewpoints Prime Contractor Abuses Steve Purcell Senior Contracts Manager ViaSat Inc. Steve.Purcell@viasat.com 1 SUBCONTRACTING UNDER USG CONTRACTS-WHY

Monitoring Subcontracts

Monitoring Subcontracts The views expressed in this presentation are DCAA's views and not necessarily the views of other DoD organizations Page 1 Subcontracts What should a contractor know about subcontracting:

Monitoring Subcontracts The views expressed in this presentation are DCAA's views and not necessarily the views of other DoD organizations Page 1 Subcontracts What should a contractor know about subcontracting:

Limitations on Pass-Through Charges. Government Contracts Update Volume 2, Nov. 2011

Limitations on Pass-Through Charges Government Contracts Update Volume 2, Nov. 2011 11/22/2011 Vol. 2, Nov 2011 Page 1 of 4 Limitations on Pass-Through Charges Two new clauses were added to the FAR effective

Limitations on Pass-Through Charges Government Contracts Update Volume 2, Nov. 2011 11/22/2011 Vol. 2, Nov 2011 Page 1 of 4 Limitations on Pass-Through Charges Two new clauses were added to the FAR effective

Navigating the Indirect Cost Rate Maze. Chad Braley Marie Salamone

Navigating the Indirect Cost Rate Maze Chad Braley Marie Salamone Value Proposition Capital Edge is the country s largest independent consulting firm focusing solely on the U.S. Government contracting

Navigating the Indirect Cost Rate Maze Chad Braley Marie Salamone Value Proposition Capital Edge is the country s largest independent consulting firm focusing solely on the U.S. Government contracting

Industry Trends from the Trenches

Industry Trends from the Trenches Presented by CohnReznick s Government Contracting Industry Practice Christine Williamson, Partner and Kristen Soles, Partner PLEASE READ This presentation has been prepared

Industry Trends from the Trenches Presented by CohnReznick s Government Contracting Industry Practice Christine Williamson, Partner and Kristen Soles, Partner PLEASE READ This presentation has been prepared

Virginia Department of Transportation Indirect Cost Rate Submission and Review Process Effective January 1, 2019

Virginia Department of Transportation Indirect Cost Rate Submission and Review Process Effective January 1, 2019 1. Policy, Regulation and Guidance a) In order to ensure that consultant costs reimbursed

Virginia Department of Transportation Indirect Cost Rate Submission and Review Process Effective January 1, 2019 1. Policy, Regulation and Guidance a) In order to ensure that consultant costs reimbursed

Pricing Subcontracts to Win Work and Make a Profit

Pricing Subcontracts to Win Work and Make a Profit Breakout Session C02 Rita L. Wells, PhD Senior Acquisition Executive, Suntiva Deidre A. Lee Consultant Date: Thursday, March 17, 2016 Time: 3:45pm 5:00pm

Pricing Subcontracts to Win Work and Make a Profit Breakout Session C02 Rita L. Wells, PhD Senior Acquisition Executive, Suntiva Deidre A. Lee Consultant Date: Thursday, March 17, 2016 Time: 3:45pm 5:00pm

PAC B.01/ August 7, PAC-013(R) MEMORANDUM FOR REGIONAL DIRECTORS, DCAA HEADS OF PRINCIPAL STAFF ELEMENTS, HQ, DCAA

MEMORANDUM FOR REGIONAL DIRECTORS, DCAA HEADS OF PRINCIPAL STAFF ELEMENTS, HQ, DCAA") DEFENSE CONTRACT AUDIT AGENCY DEPARTMENT OF DEFENSE 8725 JOHN J. KINGMAN ROAD, SUITE 2135 FORT BELVOIR, VA 22060-6219 IN REPLY REFER TO PAC 730.3.B.01/2013-02 August 7, 2014 MEMORANDUM FOR REGIONAL DIRECTORS,

DEFENSE CONTRACT AUDIT AGENCY DEPARTMENT OF DEFENSE 8725 JOHN J. KINGMAN ROAD, SUITE 2135 FORT BELVOIR, VA 22060-6219 IN REPLY REFER TO PAC 730.3.B.01/2013-02 August 7, 2014 MEMORANDUM FOR REGIONAL DIRECTORS,

Winning Contracts in a Changing Industry. Kristen Soles, CPA, Partner CohnReznick Jacob George, Dir. of Finance Red Team Consulting

Winning Contracts in a Changing Industry Kristen Soles, CPA, Partner CohnReznick Jacob George, Dir. of Finance Red Team Consulting Agenda The Baseline Trends Large, Small & Overall Direct and Indirect

Winning Contracts in a Changing Industry Kristen Soles, CPA, Partner CohnReznick Jacob George, Dir. of Finance Red Team Consulting Agenda The Baseline Trends Large, Small & Overall Direct and Indirect

Is Your G&A Base Right for You?

Is Your G&A Base Right for You? Presented by CohnReznick s Government Contracting Industry Practice Christine Williamson, Partner and Karen Louis, Member, WJ Technologies PLEASE READ This presentation

Is Your G&A Base Right for You? Presented by CohnReznick s Government Contracting Industry Practice Christine Williamson, Partner and Karen Louis, Member, WJ Technologies PLEASE READ This presentation

Developing Indirect Cost Rates for Non Profits: Practical Approaches

Presenting a live 110 minute teleconference with interactive Q&A Developing Indirect Cost Rates for Non Profits: Practical Approaches WEDNESDAY, JUNE 6, 2012 1pm Eastern 12pm Central 11am Mountain 10am

Presenting a live 110 minute teleconference with interactive Q&A Developing Indirect Cost Rates for Non Profits: Practical Approaches WEDNESDAY, JUNE 6, 2012 1pm Eastern 12pm Central 11am Mountain 10am

DCAA AUDIT READINESS Understanding Project Accounting and its Impact on Government Contractors

DCAA AUDIT READINESS Understanding Project Accounting and its Impact on Government Contractors JUNE 27, 2018 ABOUT WIPP Founded in 2001, Women Impacting Public Policy (WIPP) is a national, nonpartisan

DCAA AUDIT READINESS Understanding Project Accounting and its Impact on Government Contractors JUNE 27, 2018 ABOUT WIPP Founded in 2001, Women Impacting Public Policy (WIPP) is a national, nonpartisan

Contractor Learns Importance of Having DCAA-Approved Cost Accounting System the Hard Way

NOTE TO READERS: The Apogee Consulting, Inc. website is likely to be updated only sporadically over the next several weeks. This situation arises from the happy problem that we are SWAMPED WITH WORK and

NOTE TO READERS: The Apogee Consulting, Inc. website is likely to be updated only sporadically over the next several weeks. This situation arises from the happy problem that we are SWAMPED WITH WORK and

Cost Estimating and Truthful Cost or Pricing Data Requirements

Cost Estimating and Truthful Cost or Pricing Data Requirements Steven M. Masiello Jeremiah J. McIntyre Agenda Cost Estimating FAR cost estimating DFARS cost estimating system rule Government Proposal Analysis

Cost Estimating and Truthful Cost or Pricing Data Requirements Steven M. Masiello Jeremiah J. McIntyre Agenda Cost Estimating FAR cost estimating DFARS cost estimating system rule Government Proposal Analysis

VIP Presents. Indirect Rates What you need to know!

VIP Presents Indirect Rates What you need to know! The VIP Program Accelerating the Growth of Veteran Owned Small Businesses in the Federal Marketplace Powered By 971 Graduates and Growing From 45 States,

VIP Presents Indirect Rates What you need to know! The VIP Program Accelerating the Growth of Veteran Owned Small Businesses in the Federal Marketplace Powered By 971 Graduates and Growing From 45 States,

International Cost Estimating & Analysis Association. Supplier Cost/Price Analyses June 20, 2013

International Cost Estimating & Analysis Association Supplier Cost/Price Analyses June 20, 2013 David Eck and Todd W. Bishop Dixon Hughes Goodman LLP Government Contract Consulting Services Group Agenda

International Cost Estimating & Analysis Association Supplier Cost/Price Analyses June 20, 2013 David Eck and Todd W. Bishop Dixon Hughes Goodman LLP Government Contract Consulting Services Group Agenda

GCS 224 Surviving DCAA Audits with GCS Premier. Presented by: Nicole Mitchell, Aronson & Company

GCS 224 Surviving DCAA Audits with GCS Premier Presented by: Nicole Mitchell, Aronson & Company Agenda Government Contract Audits and the Role of DCAA and DCMA Basic Attributes of a Government Approved

GCS 224 Surviving DCAA Audits with GCS Premier Presented by: Nicole Mitchell, Aronson & Company Agenda Government Contract Audits and the Role of DCAA and DCMA Basic Attributes of a Government Approved

10/30/2015 OBJECTIVES. CPAs & ADVISORS. Present an overview of the Super Circular. Contents of the Super Circular. Discuss Administrative Requirements

CPAs & ADVISORS experience direction // 2 CFR 200 UNIFORM GRANT GUIDANCE Presented by Andy Richards, CPA, Partner October 30, 2015 OBJECTIVES Present an overview of the Super Circular Contents of the Super

CPAs & ADVISORS experience direction // 2 CFR 200 UNIFORM GRANT GUIDANCE Presented by Andy Richards, CPA, Partner October 30, 2015 OBJECTIVES Present an overview of the Super Circular Contents of the Super

Webinar: Are you Prepared for the Supercircular? February 2014

Webinar: Are you Prepared for the Supercircular? February 2014 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee,

Webinar: Are you Prepared for the Supercircular? February 2014 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee,

Recent Developments in Contract Costs and Accounting. Terry L. Albertson J. Catherine Kunz Linda S. Bruggeman

Recent Developments in Contract Costs and Accounting Terry L. Albertson J. Catherine Kunz Linda S. Bruggeman CAS: Affected Contracts On CAS-covered contracts, Govt is entitled to price adjustments to reflect

Recent Developments in Contract Costs and Accounting Terry L. Albertson J. Catherine Kunz Linda S. Bruggeman CAS: Affected Contracts On CAS-covered contracts, Govt is entitled to price adjustments to reflect

Subcontract Flowdown Best Practices from Both the Prime and Subcontractor Perspective

Subcontract Flowdown Best Practices from Both the Prime and Subcontractor Perspective Breakout Session #: C16 Presented by: Philip R. Seckman Christopher W. Myers Date: July 22, 2013 Time: 4:00-5:15 Agenda

Subcontract Flowdown Best Practices from Both the Prime and Subcontractor Perspective Breakout Session #: C16 Presented by: Philip R. Seckman Christopher W. Myers Date: July 22, 2013 Time: 4:00-5:15 Agenda

BENEFITS OF COST ACCOUNTING CONSISTENCY FOR CONTRACTORS AND SUB CONTRATORS - THE APPLES TO APPLES COMPARISON

GLOBAL CONSTRUCTION BENEFITS OF COST ACCOUNTING CONSISTENCY FOR CONTRACTORS AND SUB CONTRATORS - THE APPLES TO APPLES COMPARISON Megan Wells, CMA, Director, Navigant Vanessa Williams, CMA, Associate Director,

GLOBAL CONSTRUCTION BENEFITS OF COST ACCOUNTING CONSISTENCY FOR CONTRACTORS AND SUB CONTRATORS - THE APPLES TO APPLES COMPARISON Megan Wells, CMA, Director, Navigant Vanessa Williams, CMA, Associate Director,

VSRA Contract Compliance Seminar August 23, 2011

VSRA Contract Compliance Seminar August 23, 2011 Topics Overview What s new? Defense Federal Acquisition Regulation Supplement; Business Systems Definition and Administration (DFARS Case 2009-D038) Reporting

VSRA Contract Compliance Seminar August 23, 2011 Topics Overview What s new? Defense Federal Acquisition Regulation Supplement; Business Systems Definition and Administration (DFARS Case 2009-D038) Reporting

Subcontract Pricing Deficiencies. Next Slide

Subcontract Pricing Deficiencies Table of Contents Risk Assessment Research and Planning Risk Assessment Review of Contract and Price Negotiation Memorandum (PNM) Risk Assessment Overrun/Underrun Analysis

Subcontract Pricing Deficiencies Table of Contents Risk Assessment Research and Planning Risk Assessment Review of Contract and Price Negotiation Memorandum (PNM) Risk Assessment Overrun/Underrun Analysis

SINGLE AUDIT UPDATE. Presented By Joel Knopp, CPA

SINGLE AUDIT UPDATE Presented By Joel Knopp, CPA Session Covers Uniform Guidance Circular Components Single Audit Changes Auditee and Auditor Impact Scope of Audit under Uniform Guidance Florida Single

SINGLE AUDIT UPDATE Presented By Joel Knopp, CPA Session Covers Uniform Guidance Circular Components Single Audit Changes Auditee and Auditor Impact Scope of Audit under Uniform Guidance Florida Single

DATA ITEM DESCRIPTION

DATA ITEM DESCRIPTION Title: DD Form 1921, Cost Data Summary Report Number: Approval Date: 20031031 AMSC Number: D7514 DTIC Applicable: Preparing Activity: (D) OSD/PA&E/CAIG Limitation: GIDEP Applicable:

DATA ITEM DESCRIPTION Title: DD Form 1921, Cost Data Summary Report Number: Approval Date: 20031031 AMSC Number: D7514 DTIC Applicable: Preparing Activity: (D) OSD/PA&E/CAIG Limitation: GIDEP Applicable:

August 2, 2017 Illinois State Board of Education. Conference

August 2, 2017 Illinois State Board of Education ISBE School Nutrition Programs Back to School Conference Kristina Shelton, Principal Consultant National School Lunch Program School Meal Services Contracts

August 2, 2017 Illinois State Board of Education ISBE School Nutrition Programs Back to School Conference Kristina Shelton, Principal Consultant National School Lunch Program School Meal Services Contracts

General Procurement. Illinois State Board of Education. Nutrition Programs Back to School Conference. August 7, 2018

General Procurement Illinois State Board of Education Nutrition Programs Back to School Conference August 7, 2018 Primary Contact Kristina Shelton, Principal Consultant School Meal Services Contracts Nutrition

General Procurement Illinois State Board of Education Nutrition Programs Back to School Conference August 7, 2018 Primary Contact Kristina Shelton, Principal Consultant School Meal Services Contracts Nutrition

Contract Compliance and the Federal Acquisition Regulation (FAR) ORA CERTIFICATE PROGRAM (MODULE 11) 20 APRIL 2016

ORA CERTIFICATE PROGRAM (MODULE 11) 20 APRIL 2016") Contract Compliance and the Federal Acquisition Regulation (FAR) ORA CERTIFICATE PROGRAM (MODULE 11) 20 APRIL 2016 Learning Objectives Participants will learn about the history of the Federal Acquisition

Contract Compliance and the Federal Acquisition Regulation (FAR) ORA CERTIFICATE PROGRAM (MODULE 11) 20 APRIL 2016 Learning Objectives Participants will learn about the history of the Federal Acquisition

BEST PRACTICE IN COST ESTIMATION. Presentation by : Dr.-Ing Chris Mbatha

BEST PRACTICE IN COST ESTIMATION Presentation by : Dr.-Ing Chris Mbatha OBJECTIVE The attendee will be able to: Describe a unit price bid Decide when and where the different types of estimates are used

BEST PRACTICE IN COST ESTIMATION Presentation by : Dr.-Ing Chris Mbatha OBJECTIVE The attendee will be able to: Describe a unit price bid Decide when and where the different types of estimates are used

AMENDMENT 1 TO REQUEST FOR PROPOSALS FOR ENGINEERING SERVICES FEBRUARY 21, 2017

AMENDMENT 1 TO REQUEST FOR PROPOSALS FOR ENGINEERING SERVICES FEBRUARY 21, 2017 The City of Huron issued a Request for Proposal for Engineering Services on February 1, 2017 ( RFP ). The following are amendments

AMENDMENT 1 TO REQUEST FOR PROPOSALS FOR ENGINEERING SERVICES FEBRUARY 21, 2017 The City of Huron issued a Request for Proposal for Engineering Services on February 1, 2017 ( RFP ). The following are amendments

Implementation Guidelines for Establishing Service Centers and Recharge Centers Charging Sponsored Projects

Responsible University Official: AVP & Comptroller Responsible Office: Financial Reporting Services Implementation Guidelines for Establishing Service Centers and Recharge Centers Charging Sponsored Projects

Responsible University Official: AVP & Comptroller Responsible Office: Financial Reporting Services Implementation Guidelines for Establishing Service Centers and Recharge Centers Charging Sponsored Projects

Frequently Asked Questions

Frequently Asked Questions Updated: July 2017 For The Office of Management and Budget s Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards At 2 CFR 200 The

Frequently Asked Questions Updated: July 2017 For The Office of Management and Budget s Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards At 2 CFR 200 The

SUMMARY: NASA is proposing to amend the NASA FAR Supplement (NFS) to incorporate a

to incorporate a") This document is scheduled to be published in the Federal Register on 10/29/2013 and available online at http://federalregister.gov/a/2013-25287, and on FDsys.gov NATIONAL AERONAUTICS AND SPACE ADMINISTRATION

This document is scheduled to be published in the Federal Register on 10/29/2013 and available online at http://federalregister.gov/a/2013-25287, and on FDsys.gov NATIONAL AERONAUTICS AND SPACE ADMINISTRATION

On How Not to Draft Agreements

Things I Have Learned As An Arbitrator On How Not to Draft Agreements Barbara Kinosky Centre Law & Consulting Agenda and Sources Agenda 1. Advantages and Risks 2. Key Questions & Considerations 3. Related

Things I Have Learned As An Arbitrator On How Not to Draft Agreements Barbara Kinosky Centre Law & Consulting Agenda and Sources Agenda 1. Advantages and Risks 2. Key Questions & Considerations 3. Related

Policies and Procedures for Federal Contractors

Policies and Procedures for Federal Contractors Presented by CohnReznick s Government Contracting Industry Practice Rebecca Kehoe, Esq., Manager & David Black, Partner, Holland & Knight PLEASE READ This

Policies and Procedures for Federal Contractors Presented by CohnReznick s Government Contracting Industry Practice Rebecca Kehoe, Esq., Manager & David Black, Partner, Holland & Knight PLEASE READ This

Contractor Purchasing System Review (CPSR) Guidebook. October 25, 2016 DEPARTMENT OF DEFENSE (DOD) DEFENSE CONTRACT MANAGEMENT AGENCY (DCMA)

Guidebook. October 25, 2016 DEPARTMENT OF DEFENSE (DOD) DEFENSE CONTRACT MANAGEMENT AGENCY (DCMA)") DEPARTMENT OF DEFENSE (DOD) Contractor Purchasing System Review (CPSR) Guidebook October 25, 2016 DEFENSE CONTRACT MANAGEMENT AGENCY (DCMA) This revision supersedes all previous versions. Table of Contents

DEPARTMENT OF DEFENSE (DOD) Contractor Purchasing System Review (CPSR) Guidebook October 25, 2016 DEFENSE CONTRACT MANAGEMENT AGENCY (DCMA) This revision supersedes all previous versions. Table of Contents

Contract Types and Associated Risks December 20 th, 2016

Contract Types and Associated Risks December 20 th, 2016 The Fundamentals of Government Contracting Webinar Series 1 Your Presenters Mike Mardesich Dixon Hughes Goodman LLP 703.970.0508 mike.mardesich@dhgllp.com

Contract Types and Associated Risks December 20 th, 2016 The Fundamentals of Government Contracting Webinar Series 1 Your Presenters Mike Mardesich Dixon Hughes Goodman LLP 703.970.0508 mike.mardesich@dhgllp.com

Click to edit Master title style

Click to edit Master title style Click to edit Master text styles Second level Click Indirect to edit Rate Master Cycle title style Factors that Drive Your Indirect Rates and Impact Click to edit Your

Click to edit Master title style Click to edit Master text styles Second level Click Indirect to edit Rate Master Cycle title style Factors that Drive Your Indirect Rates and Impact Click to edit Your

Proposal Adequacy Checklist

The offeror shall complete the following checklist, providing location of requested information, or an explanation of why the requested information is not provided. In preparation of the offeror s checklist,

The offeror shall complete the following checklist, providing location of requested information, or an explanation of why the requested information is not provided. In preparation of the offeror s checklist,

Frenemies: The Story of a Prime Contract/Subcontract Relationship

Frenemies: The Story of a Prime Contract/Subcontract Relationship Breakout Session # B-13 William Weisberg Partner Law Offices of William Weisberg PLLC Date: July 28, 2014 Time: 2:30 p.m. 3:45 p.m. Agenda

Frenemies: The Story of a Prime Contract/Subcontract Relationship Breakout Session # B-13 William Weisberg Partner Law Offices of William Weisberg PLLC Date: July 28, 2014 Time: 2:30 p.m. 3:45 p.m. Agenda

Downloaded from UNITED STATES DEPARTMENT OF ENERGY EARNED VALUE MANAGEMENT APPLICATION GUIDE

UNITED STATES DEPARTMENT OF ENERGY EARNED VALUE MANAGEMENT APPLICATION GUIDE VERSION 1.6 JANUARY 1, 2005 FORWARD Standards seldom can stand alone and always require interpretation and discussion. ANSI/EIA

UNITED STATES DEPARTMENT OF ENERGY EARNED VALUE MANAGEMENT APPLICATION GUIDE VERSION 1.6 JANUARY 1, 2005 FORWARD Standards seldom can stand alone and always require interpretation and discussion. ANSI/EIA

University of Delaware Service Center/Recharge Centers/Core Facilities. June 13, 2017

University of Delaware Service Center/Recharge Centers/Core Facilities June 13, 2017 Agenda 1. Purpose 2. Policy 3. Types 4. Federal Guidelines 5. Accounting for Service Centers 6. Capital Equipment and

University of Delaware Service Center/Recharge Centers/Core Facilities June 13, 2017 Agenda 1. Purpose 2. Policy 3. Types 4. Federal Guidelines 5. Accounting for Service Centers 6. Capital Equipment and

Government Contracts Pricing Strategies and Rate Structures

Government Contracts Pricing Strategies and Rate Structures Presented By: Brandon Smith bsmith@anglincpa.com Jon Levin jlevin@maynardcooper.com Provisional Billing Rates Provisional, Target, Budget, Billing,

Government Contracts Pricing Strategies and Rate Structures Presented By: Brandon Smith bsmith@anglincpa.com Jon Levin jlevin@maynardcooper.com Provisional Billing Rates Provisional, Target, Budget, Billing,

That seems to be a problematic approach, right? Think about it: Solving Executive Compensation Concerns with Blended Rates. Written by Nick Sanders

The allowability of contractor executive compensation is a complex, tricky, thing made more tricky by recent statutory and regulatory changes. We have written about some of those rece nt changes before.

The allowability of contractor executive compensation is a complex, tricky, thing made more tricky by recent statutory and regulatory changes. We have written about some of those rece nt changes before.

Current Issues in Contractor Incurred Cost Submissions and Government Audits

Current Issues in Contractor Incurred Cost Submissions and Government Audits Breakout Session #: C03 Presented by: Stephen H. Bishop, Accounting Director at CGS Administrators, LLC Steven Masiello, McKenna

Current Issues in Contractor Incurred Cost Submissions and Government Audits Breakout Session #: C03 Presented by: Stephen H. Bishop, Accounting Director at CGS Administrators, LLC Steven Masiello, McKenna

New to Cost Reimbursement Contracts? Meet Your New Friends

New to Cost Reimbursement Contracts? Meet Your New Friends Breakout Session #: G07 Brent Calhoon Partner Baker Tilly Shingai Mavengere Director, Government Accounting UnitedHealthcare Military & Veterans

New to Cost Reimbursement Contracts? Meet Your New Friends Breakout Session #: G07 Brent Calhoon Partner Baker Tilly Shingai Mavengere Director, Government Accounting UnitedHealthcare Military & Veterans

Indirect Rates for Cost Plus Contracting Jenny W Clark. Jenny Clark

Indirect Rates for Cost Plus Contracting Jenny W Clark Jenny Clark jwclark@solvability.com Jenny W Clark The Oprah of Federal Contracting Solvability, Inc. www.solvability.com Phone 256-882-6276 E-mail

Indirect Rates for Cost Plus Contracting Jenny W Clark Jenny Clark jwclark@solvability.com Jenny W Clark The Oprah of Federal Contracting Solvability, Inc. www.solvability.com Phone 256-882-6276 E-mail

Navigating Your NIH Budget Pre- and Post-Award

The FreeMind Group and Jameson & Co. Present: Navigating Your NIH Budget Pre- and Post-Award Meytal Waiss, M.Sc. Director, Business Development FreeMind Group Ed Jameson, CPA Managing Member Jameson &

The FreeMind Group and Jameson & Co. Present: Navigating Your NIH Budget Pre- and Post-Award Meytal Waiss, M.Sc. Director, Business Development FreeMind Group Ed Jameson, CPA Managing Member Jameson &

Pitfalls Of State And Local Contracting

Pitfalls Of State And Local Contracting Breakout Session #: D16 Mike LaCorte and David Black Date: Tuesday, July 26 Time: 11:15am 12:30pm 1 Mike LaCorte Masters of Science in Taxation Florida Atlantic

Pitfalls Of State And Local Contracting Breakout Session #: D16 Mike LaCorte and David Black Date: Tuesday, July 26 Time: 11:15am 12:30pm 1 Mike LaCorte Masters of Science in Taxation Florida Atlantic

OMB Uniform Guidance Hot Topics and Implementation. July 18, 2014: The University of Alabama in Huntsville

Special attention will be paid to those sections of the that carry the most uncertainty and that may require significant institutional planning and preparation. The purpose of this session is not to provide

Special attention will be paid to those sections of the that carry the most uncertainty and that may require significant institutional planning and preparation. The purpose of this session is not to provide

Frequently Asked Questions Updated: November 2014

Frequently Asked Questions Updated: November 2014 For The Office of Management and Budget s Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards At 2 CFR 200

Frequently Asked Questions Updated: November 2014 For The Office of Management and Budget s Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards At 2 CFR 200

Growing Pains: The Art of Subcontract Management for Small Business

Growing Pains: The Art of Subcontract Management for Small Business Breakout Session # B02 Jeffery A. White, C.P.M, President/CEO J.A. White & Associates, Inc. Date: March 17, 2016 Time: 2:00pm 3:15pm

Growing Pains: The Art of Subcontract Management for Small Business Breakout Session # B02 Jeffery A. White, C.P.M, President/CEO J.A. White & Associates, Inc. Date: March 17, 2016 Time: 2:00pm 3:15pm

MG-3 - Supplier Cost Price Analyses Best Practices for Evaluating Supplier Proposals and Quotes

International Cost Estimating & Analysis Association - Supplier Cost / Price Analyses June 10-13, 2014 Presented By: David Eck, CPA Director Mike Mardesich, CPA Manager Dixon Hughes Goodman Government

International Cost Estimating & Analysis Association - Supplier Cost / Price Analyses June 10-13, 2014 Presented By: David Eck, CPA Director Mike Mardesich, CPA Manager Dixon Hughes Goodman Government

Key Issues in Business Valuation and Their Implication for Financial Advisors

Key Issues in Business Valuation and Their Implication for Financial Advisors A Presentation to the Private Business Group Partners Financial Fall 2008 Conference by Roger Winsby President, Axiom Valuation

Key Issues in Business Valuation and Their Implication for Financial Advisors A Presentation to the Private Business Group Partners Financial Fall 2008 Conference by Roger Winsby President, Axiom Valuation

National Contract Management Association of Boston 57th Annual March Workshop

National Contract Management Association of Boston 57th Annual March Workshop Pricing and estimating March 7, 2018 Agenda Introductions Overview and background of the pricing and estimating process Certified

National Contract Management Association of Boston 57th Annual March Workshop Pricing and estimating March 7, 2018 Agenda Introductions Overview and background of the pricing and estimating process Certified

GOVERNMENT CONTRACTING

A GUIDE TO INDIRECT COST RATES IN GOVERNMENT CONTRACTING www.ryansharkey.com TABLE OF CONTENTS Overview Direct vs. Indirect Costs... 3 What are Indirect Rates?... 4 Calculation of Indirect Rates and Impact

A GUIDE TO INDIRECT COST RATES IN GOVERNMENT CONTRACTING www.ryansharkey.com TABLE OF CONTENTS Overview Direct vs. Indirect Costs... 3 What are Indirect Rates?... 4 Calculation of Indirect Rates and Impact

Cost Recovery Issues After A Termination For Convenience

Cost Recovery Issues After A Termination For Convenience Breakout Session # C15 Leslie Anderson, Program Manager, BAE Systems Greg Bingham, Vice President, The Kenrich Group Chelsea Taylor, Manager, The

Cost Recovery Issues After A Termination For Convenience Breakout Session # C15 Leslie Anderson, Program Manager, BAE Systems Greg Bingham, Vice President, The Kenrich Group Chelsea Taylor, Manager, The

Webinar: Making the Right Choices in Government Contracting Part 2

Public Contracting Institute LLC Webinar: Making the Right Choices in Government Contracting Part 2 Presented by Richard D. Lieberman, FAR Consultant, Website: www.richarddlieberman.com, Email rliebermanconsultant@gmail.com.

Public Contracting Institute LLC Webinar: Making the Right Choices in Government Contracting Part 2 Presented by Richard D. Lieberman, FAR Consultant, Website: www.richarddlieberman.com, Email rliebermanconsultant@gmail.com.

Contractor Purchasing System Review (CPSR) Guidebook. October 2, 2017 DEPARTMENT OF DEFENSE (DOD) DEFENSE CONTRACT MANAGEMENT AGENCY (DCMA)

Guidebook. October 2, 2017 DEPARTMENT OF DEFENSE (DOD) DEFENSE CONTRACT MANAGEMENT AGENCY (DCMA)") DEPARTMENT OF DEFENSE (DOD) Contractor Purchasing System Review (CPSR) Guidebook October 2, 2017 DEFENSE CONTRACT MANAGEMENT AGENCY (DCMA) This revision supersedes all previous versions. Table of Contents

DEPARTMENT OF DEFENSE (DOD) Contractor Purchasing System Review (CPSR) Guidebook October 2, 2017 DEFENSE CONTRACT MANAGEMENT AGENCY (DCMA) This revision supersedes all previous versions. Table of Contents

Review Your Accounting System

Review Your Accounting System What to Expect in Government Construction Contracting Presented by: Maria B. Marston, CPA Witt Mares, PLC mmarston@wittmares.com Today s s Areas of Focus Internal corporate

Review Your Accounting System What to Expect in Government Construction Contracting Presented by: Maria B. Marston, CPA Witt Mares, PLC mmarston@wittmares.com Today s s Areas of Focus Internal corporate

Terminations: How to Cope with the Premature Death of Your Contract Presented By:

Terminations: How to Cope with the Premature Death of Your Contract Presented By: Cheryl Anderson canderson@redstonegci.com Jon Levin jlevin@maynardcooper.com Topics Covered Overview of Terminations Terminations

Terminations: How to Cope with the Premature Death of Your Contract Presented By: Cheryl Anderson canderson@redstonegci.com Jon Levin jlevin@maynardcooper.com Topics Covered Overview of Terminations Terminations

The Uniform Guidance: Changes and Strategies for Implementation

The Uniform Guidance: Changes and Strategies for Implementation Mark Davis Attain LLC Cindy Hope University of Alabama Kim Moreland University of Wisconsin Madison Jeffrey Silber Cornell University Topics

The Uniform Guidance: Changes and Strategies for Implementation Mark Davis Attain LLC Cindy Hope University of Alabama Kim Moreland University of Wisconsin Madison Jeffrey Silber Cornell University Topics

Executive orders and federal contractors: What you need to know now

Executive orders and federal contractors: What you need to know now 1 3 Agenda Background & Status Executive Order 13658 (Minimum Wages) Presidential Memo (Pay Equality) Executive Order 13665 (Non-retaliation)

Executive orders and federal contractors: What you need to know now 1 3 Agenda Background & Status Executive Order 13658 (Minimum Wages) Presidential Memo (Pay Equality) Executive Order 13665 (Non-retaliation)

General Federal Acquisition Regulation (FAR) Clauses and Negotiation Tactics-NCURA Region II, May 2011

Clauses and Negotiation Tactics-NCURA Region II, May 2011") General Federal Acquisition Regulation (FAR) Clauses and Negotiation Tactics-NCURA Region II, May 2011 Stacey Bucha Senior Negotiator Office of Sponsored Programs The Pennsylvania State University sxg9@psu.edu

General Federal Acquisition Regulation (FAR) Clauses and Negotiation Tactics-NCURA Region II, May 2011 Stacey Bucha Senior Negotiator Office of Sponsored Programs The Pennsylvania State University sxg9@psu.edu

Using GCS to Drive Decision Making Susan Smith, WJ Technologies Antoinette Merrill, Summit Consulting

GCS Premier It s Not Just A History Lesson Using GCS to Drive Decision Making Susan Smith, WJ Technologies Antoinette Merrill, Summit Consulting GCS Premier It s Not Just A History Lesson Objective: To

GCS Premier It s Not Just A History Lesson Using GCS to Drive Decision Making Susan Smith, WJ Technologies Antoinette Merrill, Summit Consulting GCS Premier It s Not Just A History Lesson Objective: To

NCDA 2018 Winter Conference Procurement under Part 200

NCDA 2018 Winter Conference Procurement under Part 200 PROCUREMENT STANDARDS 2 CFR PART 200 Slide 2 Regulatory Requirements 200.317-200.326 of 2 CFR part 200, Uniform Administrative Requirements, Cost

NCDA 2018 Winter Conference Procurement under Part 200 PROCUREMENT STANDARDS 2 CFR PART 200 Slide 2 Regulatory Requirements 200.317-200.326 of 2 CFR part 200, Uniform Administrative Requirements, Cost

S M A L L B U S I N E S S R E G U L A T O R Y U P D A T E. A Lunch & Learn Presentation by CohnReznick s Government Contracting Industry Practice

S M A L L B U S I N E S S R E G U L A T O R Y U P D A T E A Lunch & Learn Presentation by CohnReznick s Government Contracting Industry Practice P L E A S E R E A D This presentation has been prepared

S M A L L B U S I N E S S R E G U L A T O R Y U P D A T E A Lunch & Learn Presentation by CohnReznick s Government Contracting Industry Practice P L E A S E R E A D This presentation has been prepared

Keys to Submitting an Adequate Incurred Cost Proposal

Keys to Submitting an Adequate Incurred Cost Proposal Presented By: Kiran Pinto, Senior Manager, Watkins Meegan Keith Romanowski, Compliance Director, WJ Technologies March 20, 2013 Agenda Who Needs to

Keys to Submitting an Adequate Incurred Cost Proposal Presented By: Kiran Pinto, Senior Manager, Watkins Meegan Keith Romanowski, Compliance Director, WJ Technologies March 20, 2013 Agenda Who Needs to

CONTRACT ADMINISTRATION AND AUDIT SERVICES

CHAPTER 3042 CONTRACT ADMINISTRATION AND AUDIT SERVICES Subchapter 3042.002 Interagency agreements. Subchapter 3042.1 Contract Audit Services 3042.102 Assignment of contract audit services. 3042.170 Contract

CHAPTER 3042 CONTRACT ADMINISTRATION AND AUDIT SERVICES Subchapter 3042.002 Interagency agreements. Subchapter 3042.1 Contract Audit Services 3042.102 Assignment of contract audit services. 3042.170 Contract