How to Develop Indirect Cost Rates For Nonprofit Organizations

|

|

|

- Derek Holt

- 6 years ago

- Views:

Transcription

1 How to Develop Indirect Cost Rates For Nonprofit Organizations 2010 Government and Not-For-Profit Conference UMD University College Adelphi, Maryland April 30, 2010 Presenter: Paul H. Calabrese Rubino & McGeehin, CPAs & Consultants Senior Manager Tel:

2 Basic Indirect Rate Principles Documentation to ensure: Uniform measurement Consistency year to year comparison Cost accounting period - accrual Concept of ALLOCABILITY 3 Importance of Federal Rates Example of service firms Government contractors FAR Pt. 31 Cost Accounting Standards Board Service and Not For Profit (NFP) Non-Profit org s OMB Circular A-122 Dept. of Labor & DHHS models Outside forces on NFPs IRS 990 SFE, FASB 117 SFE 4

3 Cost Accounting Definitions Adequate project costing Segregate cost for each government grant Distinguish between direct and indirect cost Consistent cost allocation of indirect cost Identify unallowable, non-recoverable cost Assign cost to the appropriate accounting period Sufficient accounting controls to ensure compliance with federal grant regulations OMB Circular A-122 for Non-Profit Organizations Capable of performance measurement, such as provisional vs. actuals for indirect burden rates Facilitate the development of indirect cost rates 6

4 Direct Expenses Direct Cost are costs specifically identified or traceable to a final cost objective (program service group, activity, cost center, department, or grant). Examples: direct labor, direct material, supplies, consultants, sub-awards, and travel. 7 Reasons for Indirect Rates Develop cost estimates for grant proposals used in the SF 424a Manage within cost measurement and performance requirements Full Cost Recovery Comply with government regulations, i.e. OMB Circular A-122 8

5 Indirect Rates Indirect rates synonymous with: Burdens Loading Overhead Types Fringe G&A (Indirect, Management & General from IRS Form 990) 9 Indirect Cost Definitions Indirect Cost are costs not directly identified with a single final cost objective (grant), but rather relates to two or more final cost objectives, or a service center, like occupancy department. Indirect costs cannot be economically traced to each grant so they must be placed in a cost pool to be allocated on a causal-beneficial basis to the final cost objective or grant. 10

6 Indirect Cost Allocations Period for allocating and accumulating incurred indirect cost to grants Base period equals the org s fiscal year Grants cross over two fiscal years Two different indirect rates 11 Indirect Rate Administration Negotiation and Approval of Indirect Rates per OMB Circular A-122 Agency with largest dollar value = cognizant agency Indirect rate proposal submitted 90 days after new award to an organization May not happen if you have earmarked funds, HRSA Part B, CFDA limits adm. to 10% Issues when agency is not proactive in the negotiation and settlement of indirect rates 12

7 Indirect Rate Administration Negotiation and Approval of Indirect Rates Existing org s submit new rate proposals within 6 months after the end of their fiscal year Pre-determined (forecasted) rate is established when the org. is not expected to exceed the rate based on actual cost 13 Indirect Rate Administration Fixed (ceiling) rates negotiated when predetermined are not appropriate Fixed rate is not subject to adjustment Final rate Based on actual cost for period Once negotiated, not subject to adjustment 14

8 Indirect Rate Administration Provisional or Billing Rate Forecasted indirect cost rate Used for funding, interim billing or cost reporting The results of any negotiation is distributed to other participating agencies Many clients complain they cannot find the office for negotiating indirect rate Look at conditions clauses attached to grant 15 Designing a Cost Accounting System to Compute Indirect Rates

9 Rate System Mechanisms Use service centers: fringe, occupancy Isolate administration for G&A (w/o facility) Identify direct functional areas Allocate as much direct (DAL method) Large enough to have administration built into functional areas for Overhead 17 Fringe as a Service Center For example, fringe cost includes pension, medical insurance and payroll taxes for direct personnel, working on multiple programs, that cannot be economically assigned to each of those grants. 18

10 Fringe Cost Pool & Base Each of the fringe expenses reside in a cost pool to be allocated on a causal-beneficial basis to the final cost objective or grant. Fringe expenses is the numerator and total labor dollars (including PTO) is the denominator to develop a % via a fraction. Total labor has a functional relationship with fringe expense where total labor is the independent variable and fringe is the dependent variable. 19 Fringe Rate Computation Fringe Pool & Base Example: Fringe Indirect Cost Pool: $1,500 Pension 1,500 Medical Insurance 500 Payroll Tax $3,500 Total Fringe * $ 2,000 Direct Labor (D/L) Grant A 8,000 D/L Grant B $10,000 Total Grant D/L* (Allocation Base) * $3,500/$10,000 = 35% Fringe Indirect Burden Rate *Missing indirect labor applied to G&A. 20

11 Fringe Applied to Grants Fringe Application Example: Grant A: $ 2,000 D/L 700 Fringe ($2,000 D/L x 35% fringe rate) 1,400 Other Direct Costs (ODCs) $ 4,100 Total cost for Grant A-final cost objective Grant B: $ 8,000 D/L 2,800 Fringe ($8,000 D/L x 35% fringe rate) 9,600 ODC $20,400 Total cost for Grant B-final cost objective 21 Indirect Cost Example General fund = administrative costs Executive director s office Finance, HR, IT, Purchasing, Facility Mgmt. Office Space, Utilities, Audits, Insurance Value = $150,000 (A) Programs, Value = $1,000,000 (B) $900,000 in non-federal: programs, fundraising, membership, promotion, P/R $100,000 federal grant Fractional relationship between general fund (M&G) and Programs = 15% 22

12 Indirect Cost Example Total Cost of Grant $100,000 direct costs $ 15,000 applied indirect (15% x $100,000) $115,000 = total value of grant 23 Analysis of Indirect Expenses

13 Indirect Rate Multiplier Indirect Rate Loading Factor: Fringe (1.35) x G&A (1.25) = For every D/L $1.00 spent, there will be an additional cost of 69 in burden cost. 25 Percent of Base Analysis Fringe Pool Example: FY 2009 FY 2010 Account $1,500 15% $1,500 20% Pension 1,500 15% 2,500 33% Medical 500 5% 500 7% Payroll $3,500 35% $4,500 60% Fringe Pool $10,000 $7,500 Total Labor Base 26

14 Fringe as a Percent of the Base 27 Isolate G&A (numerator) Indirect cost classified into two broad activities Facilities: buildings, equipment and capital investments, maintenance and operation expenses Administration: general administration, director s office, accounting, HR, library expenses and other types of expenditures not mentioned under facility 28

15 Isolate Admin. From Facility If an organization has more than $10 Million in federal funding of direct costs in a fiscal year, a breakout of indirect cost into two components: facility and administration, having indirect cost rates. Private grants limit indirect rate to 9% 29 Is there an ideal indirect rate? 15% Total G&A includes: 10% Administrative Functions 5% Occupancy Private Foundation Grant permits: 9% Total G&A Limitation Occupancy is a direct line item cost What is the best allocation base? What is the best rate, low or high?

16 G&A Bases (denominator) General & Administrative MTDC Base Allocate on Modified Total Direct Cost (MTDC) Direct labor, applied fringe, non-labor direct Exclusions from MTDC base shown on next slide G&A Salaries and Fringe Base Direct labor and applied fringe only G&A Salary Base Only direct labor 31 Distribution Basis for MTDC Salaries and wages (direct labor) Fringe benefits on direct labor Materials and supplies, services & travel Sub-grants and subcontracts up to the first $25,000 of each sub-grant or subcontract, regardless of period covered by sub-grant Amounts excluded from MTDC: Sub-grants/subcontracts > $25,000 Equipment, capital expenditures Participant support cost, generally excluded 32

17 Direct Cost under A-122/SFE Cost of Certain Activities Direct Programs Fundraising Salaries, fringes and space cost In direct cost base because these items receive a benefit from the indirect infrastructure Treated as unallowable on federal awards Membership Promotion, lobbying, & public relations Some agencies interpret that some indirect unallowables should be treated as direct 33 Allocate occupancy direct

18 Charge Rent Direct & Indirect Rent example of allocability: 1. Rent charged directly for a separate office devoted to one grant 2. Rent (G&A) applied via square footage (SF) to various departments/programs based on SF or some other basis (next slide) 3. Allocating rent for executive director or director of finance, no direct relationship to grant or direct activities 35 Charge Rent Direct & Indirect Rent example of allocability: 2. Rent (G&A) applied via square footage (SF) to various departments/programs based on SF or P/R $ a. If site devoted to grant is 1,000/10,000 SF for 10% of total rental cost ($5,000 = $500) b. If $5,000 in total rent is allocated via D/L dollars over $20,000/$80,000 = 25% for this program/grant (total rent = $1,250), i.e. Direct Allocation Method 36

19 Direct Allocation Method Joint costs depreciation, rental cost, repair & maintenance, telephone, and the like (utility, property insurance, etc) Prorate on a base that accurately measures benefits provided to each direct award and indirect departments Direct and indirect FTE positions Hours worked direct and indirect Direct and indirect labor dollars 37 Direct Allocation Method Square footage for direct and G&A areas is difficult to measure and keep up to date In order to use the Direct Allocation Method, make sure the grant proposal has a line item for joint costs or occupancy Set up a separate department to track and allocate joint costs to direct and indirect cost objectives OMB Circular A-122, Attachment A, D.4. 38

20 When is Overhead necessary Grouping administrative costs for cost centers under a department or functional area Departmental executive or VP Receptionist or other admin personnel Functional work benefits local cost centers Governmental group w/ multiple grants Burden is necessary to recover adm. 39 Overhead Service Centers Functional Groupings (slide 41) Example of Intermediate Cost Pool Rock n roll college radio worksheet (42) Intermediate functions Technical Production Cost Pool (slide 43) Intermediate cost pool receives applied fringe, overhead and G&A (slide 43) Allocated to Rock n Roll cost center (44) 40

21 College Radio Station - Functional Areas 41 College Radio: Applied Burdens 42

22 Service Center: Technical Production 43 College Radio: Allocated Tech. Prod. 44

23 Designing a NFP Rate System 1. Utilize existing reference materials 2. Develop Cost Accounting Matrix 3. Specialized cost accounting reports 4. ICRP document rate to DHHS 45 Utilize Existing Documents

24 Requested Item List Last FY & current YTD Trial Balance Current Chart of Accounts IRS Form 990 Last FY audit/financials Statement of Functional Expenses Annual Budget Grant documents cost limitations Previous negotiated rates w/ an agency 47 Trial Balances (T/B) Last year and current YTD T/B Need historical data for full accounting period/year Need YTD if at least 6 months More relevant at 9 month intervals Actual cost data can be combined with budget to provide full year forecast Prior account structure may not be too useful for rate development 48

25 Chart of Accounts (COA) Goal of new COA S-I-M-P-L-I-F-Y Reduce work for accounting staff Develop a matrix of G/L and Departments Standardize for consistency - ease of use Basis for new cost accounting system Integrate with annual budget updates Fit report data on ONE page 49 IRS Form 990 Part II Statement of Functional Expenses See how organization currently views their overall (matrix) structure Columnar approach Program Services Management and General Fundraising Rows represent expense accounts 50

26 51 Exhibit 2.4 from Not-For-Profit Accounting Made Easy by Warren Ruppel, Published John Wiley & Sons, Inc. New York 2002

27 Annual Budget Format Should be similar to schedule of functional expenses for integration Budget used for this year s projected indirect cost rate Budget may be modified to include impact of management and general on each program s bottom line 53 Prior Rate Agreements Prior agency indirect cost rate agreements provide the basis for: How the rate is computed, i.e. allocation base Cognizant agency and contacts Any special limitations Applicable historical fiscal year(s) New provisional rate How long ago may be out of date 54

28 Cost Accounting Matrix Cost Accounting Matrix Framework for cost accounting system & indirect rate computations Facilitate an adequate job cost system Separate cost/funds between grants, or programs services Distinguish between direct and indirect cost Identify and segregate unallowable cost, direct or indirect 56

29 Cost Accounting Matrix G/L Expenses Salaries Fringe line Sub-awards: 2 accts < $25k + > $25K Supplies Communication Occupancy line Equipment maintenance & repair Travel Depreciation/amortization 57 Sample Natural Accounts Revenue & Expense Structure 4000 Revenue (Income) 5000 Direct cost (COGS) 6000 Fringe benefits (Expense) 7000 Overhead (Reserved) 8000 G&A (Expense) 9000 Unallowable expenses (Expense) Facilitates indirect rate development 58

30 Specialized Reports Grant Cost Report / Multi-Year Beyond fiscal year Inception-To-Date Prior fiscal years Current month Performance period Budget funding Burn rate, backlog, months left 60

31 61 Labor Distribution by Project Sorts first by grant Shows all employees charging to a grant/job/program Shows hours and cost, usually their pay rate is suppressed Used to validate time charged to grant by program manager 62

32 Project Time Report from SYMPAQ SQL software, Aldebaron Financial Solutions 63 Templates for ICRP U.S. Department of Labor Indirect Cost Rate Determination Guide oc/costdeterminationguide/main.htm#t oc DHHS ICRP Template 64

33 Components of Agency Indirect Cost Rate Submission DHHS

34

35

36

37

38

39 Any Questions 78

Developing Indirect Cost Rates for Non Profits: Practical Approaches

Presenting a live 110 minute teleconference with interactive Q&A Developing Indirect Cost Rates for Non Profits: Practical Approaches WEDNESDAY, JUNE 6, 2012 1pm Eastern 12pm Central 11am Mountain 10am

Presenting a live 110 minute teleconference with interactive Q&A Developing Indirect Cost Rates for Non Profits: Practical Approaches WEDNESDAY, JUNE 6, 2012 1pm Eastern 12pm Central 11am Mountain 10am

Indirect Cost Rates For Nonprofit Organizations

Indirect Cost Rates For Nonprofit Organizations Bag Lunch Webinar May 8, 2013 All slides and handouts copyright 2013, Rubino & Company, Chartered Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants

Indirect Cost Rates For Nonprofit Organizations Bag Lunch Webinar May 8, 2013 All slides and handouts copyright 2013, Rubino & Company, Chartered Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants

Indirect Cost Rates For Nonprofit Organizations

Indirect Cost Rates For Nonprofit Organizations Bag Lunch Webinar October 10, 2012 All slides and handouts copyright 2012, Rubino & Company, Chartered Presenter: Paul H. Calabrese Rubino & Company, CPAs

Indirect Cost Rates For Nonprofit Organizations Bag Lunch Webinar October 10, 2012 All slides and handouts copyright 2012, Rubino & Company, Chartered Presenter: Paul H. Calabrese Rubino & Company, CPAs

Indirect Cost Rates & What Happens Under. Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager

Indirect Cost Rates & What Happens Under the New Super Circular Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager Tel: 301-214-4137 pcalabrese@rubino.com www.linkedin.com/pub/paul-calabrese/20/293/645/

Indirect Cost Rates & What Happens Under the New Super Circular Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager Tel: 301-214-4137 pcalabrese@rubino.com www.linkedin.com/pub/paul-calabrese/20/293/645/

What Happens to Indirect Rates under the Uniform Guidance Bag Lunch Webinar November 19, 2015

What Happens to Indirect Rates under the Uniform Guidance Bag Lunch Webinar November 19, 2015 Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager Tel: 301-214-4137 pcalabrese@rubino.com

What Happens to Indirect Rates under the Uniform Guidance Bag Lunch Webinar November 19, 2015 Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager Tel: 301-214-4137 pcalabrese@rubino.com

How to Develop Indirect Rates Under the New Super Circular. Part 1 Webinar 1 or 2 Slide Decks Rubino & Company, Chartered May 8, 2014

How to Develop Indirect Rates Under the New Super Circular Part 1 Webinar 1 or 2 Slide Decks Rubino & Company, Chartered May 8, 2014 Click Update to / Impact edit Master of Super Circular text styles Definitions

How to Develop Indirect Rates Under the New Super Circular Part 1 Webinar 1 or 2 Slide Decks Rubino & Company, Chartered May 8, 2014 Click Update to / Impact edit Master of Super Circular text styles Definitions

Indirect Cost Rate Development for Non-Profits Navigating Accounting Standards and Best Practices to Calculate and Assign Expenses

Presenting a live 110-minute teleconference with interactive Q&A Indirect Cost Rate Development for Non-Profits Navigating Accounting Standards and Best Practices to Calculate and Assign Expenses TUESDAY,

Presenting a live 110-minute teleconference with interactive Q&A Indirect Cost Rate Development for Non-Profits Navigating Accounting Standards and Best Practices to Calculate and Assign Expenses TUESDAY,

Basics of F&A: A University Perspective. Alex Weekes Principal ML Weekes & Company, PC

Basics of F&A: A University Perspective Alex Weekes Principal ML Weekes & Company, PC 203-458-0872 alex.weekes@mlweekes.com Agenda Accountant s reconciliation of the old to new rules Overview of F&A General

Basics of F&A: A University Perspective Alex Weekes Principal ML Weekes & Company, PC 203-458-0872 alex.weekes@mlweekes.com Agenda Accountant s reconciliation of the old to new rules Overview of F&A General

Cost Pools, Indirect Rates & Allocation Plans: Demystified

Cost Pools, Indirect Rates & Allocation Plans: Demystified Maryland Workforce Association 2017 Raising the Bar Conference: Preconference Workshop May 3, 2017 1:00-2:30pm Baker Tilly refers to Baker Tilly

Cost Pools, Indirect Rates & Allocation Plans: Demystified Maryland Workforce Association 2017 Raising the Bar Conference: Preconference Workshop May 3, 2017 1:00-2:30pm Baker Tilly refers to Baker Tilly

T-203 F&A Cost Rates and the Uniform Guidance, A Non-Profit Perspective

T-203 F&A Cost Rates and the Uniform Guidance, A Non-Profit Perspective Alex Weekes Principal ML Weekes & Company, PC 203-458-0872 alex.weekes@mlweekes.com Agenda Regulations (Current and New) Rate Types

T-203 F&A Cost Rates and the Uniform Guidance, A Non-Profit Perspective Alex Weekes Principal ML Weekes & Company, PC 203-458-0872 alex.weekes@mlweekes.com Agenda Regulations (Current and New) Rate Types

Allocating Direct and Indirect Costs for Nonprofits

Allocating Direct and Indirect Costs for Nonprofits Carol Barnard April 18, 2018 Agenda Allocating Indirect Cost Why allocating costs is important to nonprofits Identifying indirect costs Different methods

Allocating Direct and Indirect Costs for Nonprofits Carol Barnard April 18, 2018 Agenda Allocating Indirect Cost Why allocating costs is important to nonprofits Identifying indirect costs Different methods

Administrative Procedure

Division of Finance and Administration AP F&A-02 Administrative Procedure Title: Responsible Office: Adopted: June 1, 2017 Revised: Effective: June 1, 2017 Indirect Cost Rate Instructions for DEO Subrecipients

Division of Finance and Administration AP F&A-02 Administrative Procedure Title: Responsible Office: Adopted: June 1, 2017 Revised: Effective: June 1, 2017 Indirect Cost Rate Instructions for DEO Subrecipients

Indirect Cost Allocation

Indirect Cost Allocation FGFOA School of Governmental Finance November 2, 2015 2:00pm 2:50pm 1 Agenda Why Perform Cost Allocation? Terminology & Definitions Types of Cost Allocation Plans Cost Allocation

Indirect Cost Allocation FGFOA School of Governmental Finance November 2, 2015 2:00pm 2:50pm 1 Agenda Why Perform Cost Allocation? Terminology & Definitions Types of Cost Allocation Plans Cost Allocation

6/5/2014. Cost Allocation Overview. Overview (continued) Overview. Overview (continued) Overview (continued)

Overview. Overview (continued) Overview (continued)") Cost Allocation Overview OHIO ASSOCIATION OF PUBLIC TREASURERS Public Finance Officer Training Institute June 2014 MAXIMUS Robert Fink, Sheri Smith, & Linda Hlebak Learning Objectives Cost Allocation Plan

Cost Allocation Overview OHIO ASSOCIATION OF PUBLIC TREASURERS Public Finance Officer Training Institute June 2014 MAXIMUS Robert Fink, Sheri Smith, & Linda Hlebak Learning Objectives Cost Allocation Plan

Effective Cost Allocation Strategies

Effective Cost Allocation Strategies Kay Sohl Head Start Fiscal Conference April 5, 2011 kay@kaysohlconsulting.net Cost Allocation Systematic method for determining the portion of specific costs which

Effective Cost Allocation Strategies Kay Sohl Head Start Fiscal Conference April 5, 2011 kay@kaysohlconsulting.net Cost Allocation Systematic method for determining the portion of specific costs which

THE ART OF COST ALLOCATIONS FOR BETTER MANAGEMENT

THE ART OF COST ALLOCATIONS FOR BETTER MANAGEMENT cliftonlarsonallen.com Jacqueline Eckman, CPA Principal, Public Sector Group AGENDA 1 Introductions 2 3 4 5 6 3 allocation types Functional allocations

THE ART OF COST ALLOCATIONS FOR BETTER MANAGEMENT cliftonlarsonallen.com Jacqueline Eckman, CPA Principal, Public Sector Group AGENDA 1 Introductions 2 3 4 5 6 3 allocation types Functional allocations

U.S. Department of Housing and Urban Development Office of Housing Counseling

U.S. Department of Housing and Urban Development Office of Housing Counseling Understanding Indirect Cost Rates, De Minimis Rate, and Cost Allocation Plans Booth Management Consulting 7230 Lee Deforest

U.S. Department of Housing and Urban Development Office of Housing Counseling Understanding Indirect Cost Rates, De Minimis Rate, and Cost Allocation Plans Booth Management Consulting 7230 Lee Deforest

Indirect Cost Rates A Non-Profit Perspective. Alex Weekes Principal ML Weekes & Company, PC

Indirect Cost Rates A Non-Profit Perspective Alex Weekes Principal ML Weekes & Company, PC 203-458-0872 alex.weekes@mlweekes.com Agenda Old School versus new regulations Review of 2CFR 200 (not so new

Indirect Cost Rates A Non-Profit Perspective Alex Weekes Principal ML Weekes & Company, PC 203-458-0872 alex.weekes@mlweekes.com Agenda Old School versus new regulations Review of 2CFR 200 (not so new

Introduction to Indirect Costs

Introduction to Indirect Costs GMS Summit St. Petersburg, FL June 12 16, 2016 Presented by: Jason D. Brooks, CPA 1 About the Author Jason D. Brooks, CPA is a partner with Watkins, Ward and Stafford, PLLC

Introduction to Indirect Costs GMS Summit St. Petersburg, FL June 12 16, 2016 Presented by: Jason D. Brooks, CPA 1 About the Author Jason D. Brooks, CPA is a partner with Watkins, Ward and Stafford, PLLC

Uniform Guidance vs. OMB Circulars

Cost Allocation 101 Uniform Guidance vs. OMB Circulars Prior to the Uniform Guidance, requirements Designed for governing DOL-ETA cost direct principles, recipients and administrative their subrecipients

Cost Allocation 101 Uniform Guidance vs. OMB Circulars Prior to the Uniform Guidance, requirements Designed for governing DOL-ETA cost direct principles, recipients and administrative their subrecipients

How Much Does It Cost?

How Much Does It Cost? Eileen G. McLoughlin, Assistant Vice President of Finance and Budgeting, Rensselaer Polytechnic Institute Charles Tegen, Associate Vice President for Finance and Comptroller, Clemson

How Much Does It Cost? Eileen G. McLoughlin, Assistant Vice President of Finance and Budgeting, Rensselaer Polytechnic Institute Charles Tegen, Associate Vice President for Finance and Comptroller, Clemson

ONR Guidance for Indirect Cost Rate Proposals for Non-Profits with less than $10M Federal Funding of Direct Costs in a Fiscal Year

ONR Guidance for Indirect Cost Rate Proposals for Non-Profits with less than $10M Funding of Direct Costs in a Fiscal Year A non-profit organization will submit an indirect cost rate proposal primarily

ONR Guidance for Indirect Cost Rate Proposals for Non-Profits with less than $10M Funding of Direct Costs in a Fiscal Year A non-profit organization will submit an indirect cost rate proposal primarily

International Dark-Sky Association Cost Allocation Plan

International Dark-Sky Association Cost Allocation Plan Adopted 15 September 2014 1 Purpose The purpose of the cost allocation plan is to summarize, in writing, the methods and procedures that this International

International Dark-Sky Association Cost Allocation Plan Adopted 15 September 2014 1 Purpose The purpose of the cost allocation plan is to summarize, in writing, the methods and procedures that this International

Welcome! Understanding Facilities and Administration (F&A) Costs. Matt Michener

Costs. Matt Michener") Understanding Facilities and Administration (F&A) Costs Also known as Overhead Costs, or Indirect Costs. Revised April 2017 1 Welcome! Presenters: Matt Michener matthew.michener@wsu.edu Grant and Contract

Understanding Facilities and Administration (F&A) Costs Also known as Overhead Costs, or Indirect Costs. Revised April 2017 1 Welcome! Presenters: Matt Michener matthew.michener@wsu.edu Grant and Contract

December Facilities and Administrative Costs Primer The Research Foundation for The State University of New York

December 2014 Facilities and Administrative Costs Primer The Research Foundation for The State University of New York Table of Contents Introduction... 3 Direct vs. Facilities and Administrative (F&A)...

December 2014 Facilities and Administrative Costs Primer The Research Foundation for The State University of New York Table of Contents Introduction... 3 Direct vs. Facilities and Administrative (F&A)...

Mark W. Stout, MBA DOI Interior Business Center Indirect Cost Services - Sacramento April 2017

Mark W. Stout, MBA DOI Interior Business Center Indirect Cost Services - Sacramento April 2017 About ICS General Principles Uniform Guidance Direct, Indirect, Unallowable, Exclusions Distribution Base

Mark W. Stout, MBA DOI Interior Business Center Indirect Cost Services - Sacramento April 2017 About ICS General Principles Uniform Guidance Direct, Indirect, Unallowable, Exclusions Distribution Base

Indirect Cost Recovery: What You Need to Consider. August 2017

Indirect Cost Recovery: What You Need to Consider August 2017 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee,

Indirect Cost Recovery: What You Need to Consider August 2017 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee,

GCS 224 Surviving DCAA Audits with GCS Premier. Presented by: Nicole Mitchell, Aronson & Company

GCS 224 Surviving DCAA Audits with GCS Premier Presented by: Nicole Mitchell, Aronson & Company Agenda Government Contract Audits and the Role of DCAA and DCMA Basic Attributes of a Government Approved

GCS 224 Surviving DCAA Audits with GCS Premier Presented by: Nicole Mitchell, Aronson & Company Agenda Government Contract Audits and the Role of DCAA and DCMA Basic Attributes of a Government Approved

Facilities & Administrative Costs: Balancing Sponsor Requirements and Institutional Needs

Facilities & Administrative Costs: Balancing Sponsor Requirements and Institutional Needs Kimberly Read, PhD, CRA Assistant Director Florida Center for Inclusive Communities University of South Florida

Facilities & Administrative Costs: Balancing Sponsor Requirements and Institutional Needs Kimberly Read, PhD, CRA Assistant Director Florida Center for Inclusive Communities University of South Florida

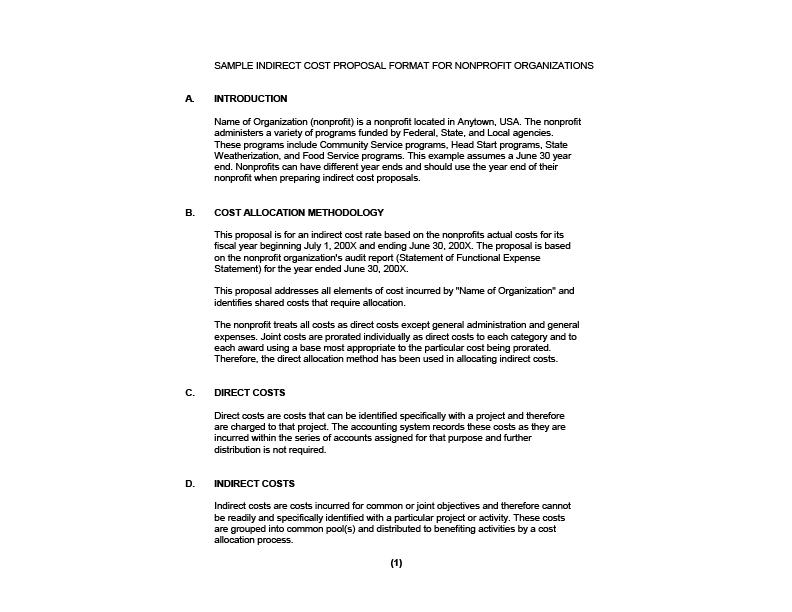

SAMPLE ORGANIZATION Model Cost Allocation Plan

SAMPLE ORGANIZATION Model Cost Allocation Plan Use the following model Cost Allocation Plan (CAP) as guidance for Non-profit organizations. The CAP should be tailored to fit the specific policies of each

SAMPLE ORGANIZATION Model Cost Allocation Plan Use the following model Cost Allocation Plan (CAP) as guidance for Non-profit organizations. The CAP should be tailored to fit the specific policies of each

Introduction to Indirect Costs

Introduction to Indirect Costs Questions to be Answered What are indirect costs? How are they documented? How are they recovered? Points to Keep in Mind Indirect costs tend to be support costs (e.g., telephone,

Introduction to Indirect Costs Questions to be Answered What are indirect costs? How are they documented? How are they recovered? Points to Keep in Mind Indirect costs tend to be support costs (e.g., telephone,

Everything You ve Always Wanted to Know. About Indirect Costs. But Were Too Confused to Ask.

Everything You ve Always Wanted to Know About Indirect Costs But Were Too Confused to Ask. Presentation to RADG Harry W. Orf, PhD 10 June 2014 Page 1 2 What We Will Cover Federal Statutes That Govern Indirect

Everything You ve Always Wanted to Know About Indirect Costs But Were Too Confused to Ask. Presentation to RADG Harry W. Orf, PhD 10 June 2014 Page 1 2 What We Will Cover Federal Statutes That Govern Indirect

Understanding the Cost Accounting Standards. Bag Lunch Webinar May 9, 2018

Understanding the Cost Accounting Standards Bag Lunch Webinar May 9, 2018 1 Co-Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager n Tel: 301-214-4137 n pcalabrese@rubino.com

Understanding the Cost Accounting Standards Bag Lunch Webinar May 9, 2018 1 Co-Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager n Tel: 301-214-4137 n pcalabrese@rubino.com

FLORIDA DEPARTMENT OF ECONOMIC OPPORTUNITY WEATHERIZATION ASSISTANCE PROGRAM

FLORIDA DEPARTMENT OF ECONOMIC OPPORTUNITY WEATHERIZATION ASSISTANCE PROGRAM NON-PROFIT GUIDANCE FOR DOCUMENTATION AND SUPPORT OF PROGRAM SUPPORT AND ADMINISTRATION EXPENDITURES Version 1 March 2013 NON-PROFIT

FLORIDA DEPARTMENT OF ECONOMIC OPPORTUNITY WEATHERIZATION ASSISTANCE PROGRAM NON-PROFIT GUIDANCE FOR DOCUMENTATION AND SUPPORT OF PROGRAM SUPPORT AND ADMINISTRATION EXPENDITURES Version 1 March 2013 NON-PROFIT

Florida MIECHV Initiative Provider Fiscal Policy Manual

2018 Florida MIECHV Initiative Provider Fiscal Policy Manual Florida MIECHV Initiative This project is supported by the Health Resources and Services Administration (HRSA) of the U.S. Department of Health

2018 Florida MIECHV Initiative Provider Fiscal Policy Manual Florida MIECHV Initiative This project is supported by the Health Resources and Services Administration (HRSA) of the U.S. Department of Health

GENERAL INSTRUCTIONS--Continuation Sheet... COVER SHEET AND CERTIFICATION... C-1. PART I General Information... I-1. Indirect Costs...

Revision Number 1 Effective Date June 30, 2006 INDEX GENERAL INSTRUCTIONS--Continuation Sheet.............. (i) COVER SHEET AND CERTIFICATION................... C-1 PART I General Information..................

Revision Number 1 Effective Date June 30, 2006 INDEX GENERAL INSTRUCTIONS--Continuation Sheet.............. (i) COVER SHEET AND CERTIFICATION................... C-1 PART I General Information..................

Ins and Outs of Indirect Costs Under the Super Circular Webinar Series

Ins and Outs of In Costs Under the Super Circular Webinar Series March 4: Does Our CAA Effectively Estimate and Reconcile In Costs? Miss a webinar? View it On Demand www.caplaw.org/conferencesandtrainings/webinars.html

Ins and Outs of In Costs Under the Super Circular Webinar Series March 4: Does Our CAA Effectively Estimate and Reconcile In Costs? Miss a webinar? View it On Demand www.caplaw.org/conferencesandtrainings/webinars.html

SANILAC COUNTY, MICHIGAN

SANILAC COUNTY, MICHIGAN FISCAL 2017 COST ALLOCATION PLAN FOR THE PERIOD ENDING December 31, 2017 MGT Consulting Group Michigan Office 2343 Delta Road Bay City, Michigan 48706 989-316-2220 www.mgtconsulting.com

SANILAC COUNTY, MICHIGAN FISCAL 2017 COST ALLOCATION PLAN FOR THE PERIOD ENDING December 31, 2017 MGT Consulting Group Michigan Office 2343 Delta Road Bay City, Michigan 48706 989-316-2220 www.mgtconsulting.com

The Basics of F&A and How the Uniform Guidance Impacts Indirect Costs

The Basics of F&A and How the Uniform Guidance Impacts Indirect Costs Alex Weekes Principal ML Weekes & Company, PC 203-458-0872 alex.weekes@mlweekes.com Indirect Costs / Facilities and Admistrative Cost

The Basics of F&A and How the Uniform Guidance Impacts Indirect Costs Alex Weekes Principal ML Weekes & Company, PC 203-458-0872 alex.weekes@mlweekes.com Indirect Costs / Facilities and Admistrative Cost

OCONTO COUNTY, WISCONSIN

A CENTRAL SERVICES COST ALLOCATION PLAN FISCAL 2010 ACTUAL COSTS FOR THE YEAR ENDED DECEMBER 31, 2010 COUNTY-WIDE COST ALLOCATION PLAN CERTIFICATION OF COST ALLOCATION PLAN This is to certify that I have

A CENTRAL SERVICES COST ALLOCATION PLAN FISCAL 2010 ACTUAL COSTS FOR THE YEAR ENDED DECEMBER 31, 2010 COUNTY-WIDE COST ALLOCATION PLAN CERTIFICATION OF COST ALLOCATION PLAN This is to certify that I have

ONR SUBMISSION REQUIREMENTS FOR NONPROFIT INDIRECT COST RATE PROPOSALS - INITIAL CHECKLIST

ONR SUBMISSION REQUIREMENTS FOR NONPROFIT INDIRECT COST RATE PROPOSALS - INITIAL CHECKLIST 1. Transmittal Letter: State the type of rate requested (e.g. predetermined, fixed, provisional, or final) and

ONR SUBMISSION REQUIREMENTS FOR NONPROFIT INDIRECT COST RATE PROPOSALS - INITIAL CHECKLIST 1. Transmittal Letter: State the type of rate requested (e.g. predetermined, fixed, provisional, or final) and

Project Managers are expected to apply this guidance document when charging direct or indirect costs to grants.

HOW TO DISTINGUISH BETWEEN DIRECT AND INDIRECT CHARGES Vincennes University Purpose As a recipient of federal funds, the Office of Management and Budget (OMB) Circular A-21, Cost Principles for Educational

HOW TO DISTINGUISH BETWEEN DIRECT AND INDIRECT CHARGES Vincennes University Purpose As a recipient of federal funds, the Office of Management and Budget (OMB) Circular A-21, Cost Principles for Educational

Ins and Outs of Indirect Costs Under the Super Circular Webinar Series

Ins and Outs of In Costs Under the Super Circular Webinar Series Miss a webinar? View it On Demand www.caplaw.org/conferencesandtrainings/webinars.html What Impact Does the New Guidance Have on the Treatment

Ins and Outs of In Costs Under the Super Circular Webinar Series Miss a webinar? View it On Demand www.caplaw.org/conferencesandtrainings/webinars.html What Impact Does the New Guidance Have on the Treatment

Implementation Guidelines for Establishing Service Centers and Recharge Centers Charging Sponsored Projects

Responsible University Official: AVP & Comptroller Responsible Office: Financial Reporting Services Implementation Guidelines for Establishing Service Centers and Recharge Centers Charging Sponsored Projects

Responsible University Official: AVP & Comptroller Responsible Office: Financial Reporting Services Implementation Guidelines for Establishing Service Centers and Recharge Centers Charging Sponsored Projects

F&A Methodologies- Short Form Schools with Long Form Consideration. August 15, 2017

F&A Methodologies- Short Form Schools with Long Form Consideration August 15, 2017 1 Agenda Overview of F&A Short Form (SF) Methodology Long Form (LF) Methodology Differences between Short Form & Long

F&A Methodologies- Short Form Schools with Long Form Consideration August 15, 2017 1 Agenda Overview of F&A Short Form (SF) Methodology Long Form (LF) Methodology Differences between Short Form & Long

Contract Support Cost 101

Contract Support Cost 101 May 2014 Vickie Hanvey, CPA, MBA Cost Classification Administrative Direct CSC Indirect CSC Indirect Admin Direct Admin Start up Indirect Program Direct Program Indirect Program

Contract Support Cost 101 May 2014 Vickie Hanvey, CPA, MBA Cost Classification Administrative Direct CSC Indirect CSC Indirect Admin Direct Admin Start up Indirect Program Direct Program Indirect Program

Section 5.4: Completing AFR Schedule B Indirect Administrative Support and Occupancy Valuation. Introduction

Section 5.4: Completing AFR Schedule B Indirect Administrative Support and Occupancy Valuation Introduction Indirect administrative support is that portion of the licensee's general and administrative

Section 5.4: Completing AFR Schedule B Indirect Administrative Support and Occupancy Valuation Introduction Indirect administrative support is that portion of the licensee's general and administrative

GENERAL INSTRUCTIONS COVER SHEET AND CERTIFICATION C-1

INDEX GENERAL INSTRUCTIONS (i) COVER SHEET AND CERTIFICATION C-1 Part I General Information I-1 Part II Direct Costs II-1 Part III Indirect Costs III-1 Part IV Depreciation and Use Allowances IV-1 Part

INDEX GENERAL INSTRUCTIONS (i) COVER SHEET AND CERTIFICATION C-1 Part I General Information I-1 Part II Direct Costs II-1 Part III Indirect Costs III-1 Part IV Depreciation and Use Allowances IV-1 Part

Capital Area Council of Governments FY 2018 Cost Policy Statement and Cost Allocation Plan

Capital Area Council of Governments FY 2018 Cost Policy Statement and Cost Allocation Plan The Capital Area Council of Governments uses the cost allocation method prescribed in OMB Uniform Administrative

Capital Area Council of Governments FY 2018 Cost Policy Statement and Cost Allocation Plan The Capital Area Council of Governments uses the cost allocation method prescribed in OMB Uniform Administrative

Administrative Policy

Administrative Policy POLICY NUMBER 86 Title: Program: Indirect Cost Rate Proposal Preparation for Local Workforce Development Boards Division of Finance and Administration, Bureau of Financial Management

Administrative Policy POLICY NUMBER 86 Title: Program: Indirect Cost Rate Proposal Preparation for Local Workforce Development Boards Division of Finance and Administration, Bureau of Financial Management

Illinois Coalition Against Domestic Violence. Understanding the Uniform Guidance and Indirect Cost Rate March 16, 2016

Illinois Coalition Against Domestic Violence Understanding the Uniform Guidance and Indirect Cost Rate March 16, 2016 1 Understanding the Uniform Guidance and Indirect Cost Rate Presented by: Teri L. Taylor,

Illinois Coalition Against Domestic Violence Understanding the Uniform Guidance and Indirect Cost Rate March 16, 2016 1 Understanding the Uniform Guidance and Indirect Cost Rate Presented by: Teri L. Taylor,

Cost Allocation and Federal Compliance

Cost Allocation and Federal Compliance Fiscal Training March 20 th, 2008 10:00 a.m. 4:00 p.m. Why is Cost Allocation Important? What are the Federal requirements governing the funding received? What are

Cost Allocation and Federal Compliance Fiscal Training March 20 th, 2008 10:00 a.m. 4:00 p.m. Why is Cost Allocation Important? What are the Federal requirements governing the funding received? What are

A Cost Allocation Plan For RACINE COUNTY, WISCONSIN

A Cost Allocation Plan For Actual FY 2011 Submitted by MAXIMUS Consulting Services, Inc. One West Old State Capitol Plaza Suite 502 Springfield, IL 62701 217-789-0041 2012 MAXIMUS, Inc. INTRODUCTION A

A Cost Allocation Plan For Actual FY 2011 Submitted by MAXIMUS Consulting Services, Inc. One West Old State Capitol Plaza Suite 502 Springfield, IL 62701 217-789-0041 2012 MAXIMUS, Inc. INTRODUCTION A

Today s Topics. Cost Principles. Federal Guidance. Guidance Resources. Purpose of Cost Principles. Cost Principles Overview 5/7/2015

Cost Principles Presented by: Contracts and Grants Accounting James Ringo Today s Topics Making good decisions about costs Allowable Allocable Reasonable, necessary Consistent Distinguishing direct vs.

Cost Principles Presented by: Contracts and Grants Accounting James Ringo Today s Topics Making good decisions about costs Allowable Allocable Reasonable, necessary Consistent Distinguishing direct vs.

Cost Allocation Plan

Cost Allocation Plan Western States Air Resources Council (WESTAR) 1218 3 rd Avenue, Suite 1518 Seattle, WA Contact Person: Dan Johnson, Executive Director Email: djohnson@westar.org A. INTRODUCTION The

Cost Allocation Plan Western States Air Resources Council (WESTAR) 1218 3 rd Avenue, Suite 1518 Seattle, WA Contact Person: Dan Johnson, Executive Director Email: djohnson@westar.org A. INTRODUCTION The

TEDDY BEARS AGAINST VIOLENCE

COST ALLOCATION PLAN Purpose/General Statements The purpose of this cost allocation plan is to summarize, in writing, the methods and procedures that this organization will use to allocate costs to Administrative/General,

COST ALLOCATION PLAN Purpose/General Statements The purpose of this cost allocation plan is to summarize, in writing, the methods and procedures that this organization will use to allocate costs to Administrative/General,

Capital Area Council of Governments FY 2019 Cost Policy Statement and Cost Allocation Plan

Capital Area Council of Governments FY 2019 Cost Policy Statement and Cost Allocation Plan The Capital Area Council of Governments uses the cost allocation method prescribed in OMB Uniform Administrative

Capital Area Council of Governments FY 2019 Cost Policy Statement and Cost Allocation Plan The Capital Area Council of Governments uses the cost allocation method prescribed in OMB Uniform Administrative

VIP Presents. Indirect Rates What you need to know!

VIP Presents Indirect Rates What you need to know! The VIP Program Accelerating the Growth of Veteran Owned Small Businesses in the Federal Marketplace Powered By 971 Graduates and Growing From 45 States,

VIP Presents Indirect Rates What you need to know! The VIP Program Accelerating the Growth of Veteran Owned Small Businesses in the Federal Marketplace Powered By 971 Graduates and Growing From 45 States,

A Cost Allocation Plan For RACINE COUNTY, WISCONSIN

A Cost Allocation Plan For Actual FY 2010 Submitted by MAXIMUS Consulting Services, Inc. One West Old State Capitol Plaza Suite 502 Springfield, IL 62701 217-789-0041 2011 MAXIMUS, Inc. INTRODUCTION A

A Cost Allocation Plan For Actual FY 2010 Submitted by MAXIMUS Consulting Services, Inc. One West Old State Capitol Plaza Suite 502 Springfield, IL 62701 217-789-0041 2011 MAXIMUS, Inc. INTRODUCTION A

Demystifying Cost Allocation. Steve Zimmerman Spectrum Nonprofit Services, LLC. Our Conversation Today. What goes into the price?

Demystifying Cost Allocation Steve Zimmerman Spectrum Nonprofit Services, LLC This project was supported by Grant No. 2010 ET S6 K008 awarded by the Office on Violence Against Women, U.S. Department of

Demystifying Cost Allocation Steve Zimmerman Spectrum Nonprofit Services, LLC This project was supported by Grant No. 2010 ET S6 K008 awarded by the Office on Violence Against Women, U.S. Department of

Unrelated Business Income Taxes (UBIT)

") CORNELL UNIVERSITY POLICY LIBRARY Unrelated Business Income Taxes (UBIT) POLICY 3.15 Chapter 15, Unrelated Business Income Taxes Tax Office POLICY STATEMENT Units of the university that have activities

CORNELL UNIVERSITY POLICY LIBRARY Unrelated Business Income Taxes (UBIT) POLICY 3.15 Chapter 15, Unrelated Business Income Taxes Tax Office POLICY STATEMENT Units of the university that have activities

Keys to Submitting an Adequate Incurred Cost Proposal

Keys to Submitting an Adequate Incurred Cost Proposal Presented By: Kiran Pinto, Senior Manager, Watkins Meegan Keith Romanowski, Compliance Director, WJ Technologies March 20, 2013 Agenda Who Needs to

Keys to Submitting an Adequate Incurred Cost Proposal Presented By: Kiran Pinto, Senior Manager, Watkins Meegan Keith Romanowski, Compliance Director, WJ Technologies March 20, 2013 Agenda Who Needs to

Understanding F&A Rates. OPTIONAL SUBHEAD HERE Sara Tarkington January 23 rd, 2018

OPTIONAL SUBHEAD HERE Sara Tarkington January 23 rd, 2018 Why an F&A Cost Rate? It is federal policy to provide for the reimbursement of F&A costs except when specific limitations and prohibitions exist

OPTIONAL SUBHEAD HERE Sara Tarkington January 23 rd, 2018 Why an F&A Cost Rate? It is federal policy to provide for the reimbursement of F&A costs except when specific limitations and prohibitions exist

Indirect Rates for Cost Plus Contracting Jenny W Clark. Jenny Clark

Indirect Rates for Cost Plus Contracting Jenny W Clark Jenny Clark jwclark@solvability.com Jenny W Clark The Oprah of Federal Contracting Solvability, Inc. www.solvability.com Phone 256-882-6276 E-mail

Indirect Rates for Cost Plus Contracting Jenny W Clark Jenny Clark jwclark@solvability.com Jenny W Clark The Oprah of Federal Contracting Solvability, Inc. www.solvability.com Phone 256-882-6276 E-mail

Preparing your AAA Area Plan Budget & Cost Allocation Plan. Fiscal Track AM Workshop Session May 29, :30 AM - Noon

Preparing your AAA Area Plan Budget & Cost Allocation Plan Fiscal Track AM Workshop Session May 29, 2014 10:30 AM - Noon 1 Why is Cost Allocation Important? What are the State and Federal requirements

Preparing your AAA Area Plan Budget & Cost Allocation Plan Fiscal Track AM Workshop Session May 29, 2014 10:30 AM - Noon 1 Why is Cost Allocation Important? What are the State and Federal requirements

INDIRECT COSTS IN THE SCHOOL NUTRITION PROGRAMS (SNP) School Nutrition Association Annual National Conference Philadelphia, Pennsylvania July 20,

School Nutrition Association Annual National Conference Philadelphia, Pennsylvania July 20,") INDIRECT COSTS IN THE SCHOOL NUTRITION PROGRAMS (SNP) School Nutrition Association Annual National Conference Philadelphia, Pennsylvania July 20, 2008 SNA 2006 INDIRECT COST STUDY What Are They? How Are

INDIRECT COSTS IN THE SCHOOL NUTRITION PROGRAMS (SNP) School Nutrition Association Annual National Conference Philadelphia, Pennsylvania July 20, 2008 SNA 2006 INDIRECT COST STUDY What Are They? How Are

BUDGETING AND ALLOCATION

BUDGETING AND PROPOSED COST ALLOCATION Session Objectives Differentiate between direct, shared and indirect costs Reflecting costs in budgets & proposals Understand accounting for expenses and allocations

BUDGETING AND PROPOSED COST ALLOCATION Session Objectives Differentiate between direct, shared and indirect costs Reflecting costs in budgets & proposals Understand accounting for expenses and allocations

JOHNS HOPKINS UNIVERSITY COST ACCOUNTING STANDARDS BOARD DISCLOSURE STATEMENT FOR EDUCATIONAL INSTITUTIONS CASB DS-2

COST ACCOUNTING STANDARDS BOARD FOR CASB DS-2 March 23, 2010 INDEX JOHNS HOPKINS UNIVERISTY GENERAL INSTRUCTIONS... Continuation Sheet... i COVER SHEET AND CERTIFICATION...... ii PART I... General Information...

COST ACCOUNTING STANDARDS BOARD FOR CASB DS-2 March 23, 2010 INDEX JOHNS HOPKINS UNIVERISTY GENERAL INSTRUCTIONS... Continuation Sheet... i COVER SHEET AND CERTIFICATION...... ii PART I... General Information...

Dartmouth College. Service and Recharge Center Policies and Procedures. Dartmouth College Office of the Controller

Dartmouth College Service and Recharge Center Policies and Procedures Dartmouth College Office of the Controller June 2008 CONTENTS I. Introduction...1 II. General Policies...3 III. Service Center Practices

Dartmouth College Service and Recharge Center Policies and Procedures Dartmouth College Office of the Controller June 2008 CONTENTS I. Introduction...1 II. General Policies...3 III. Service Center Practices

Indirect Cost Rate Proposal and Master Schedule of Fees PRESENTATION BY: COUNTY OF FRESNO AUDITOR-CONTROLLER AUGUST 20, 2013

Indirect Cost Rate Proposal and Master Schedule of Fees 1 PRESENTATION BY: COUNTY OF FRESNO AUDITOR-CONTROLLER AUGUST 20, 2013 Background 2 Cost Accounting principles for local governments are codified

Indirect Cost Rate Proposal and Master Schedule of Fees 1 PRESENTATION BY: COUNTY OF FRESNO AUDITOR-CONTROLLER AUGUST 20, 2013 Background 2 Cost Accounting principles for local governments are codified

Navigating the Indirect Cost Rate Maze. Chad Braley Marie Salamone

Navigating the Indirect Cost Rate Maze Chad Braley Marie Salamone Value Proposition Capital Edge is the country s largest independent consulting firm focusing solely on the U.S. Government contracting

Navigating the Indirect Cost Rate Maze Chad Braley Marie Salamone Value Proposition Capital Edge is the country s largest independent consulting firm focusing solely on the U.S. Government contracting

10 Frequently Asked Questions on Indirect Costs

1 10 Frequently Asked Questions on Indirect Costs Bonnie Graham, Esq. bgraham@bruman.com (202) 965-3652 www.bruman.com First, some background 2 Total Cost of Federal Awards Indirect 10% Direct Indirect

1 10 Frequently Asked Questions on Indirect Costs Bonnie Graham, Esq. bgraham@bruman.com (202) 965-3652 www.bruman.com First, some background 2 Total Cost of Federal Awards Indirect 10% Direct Indirect

Creating A Program Budget

Creating A Program Budget Defining a Program Budget ORGANIZATIONAL BUDGET: Applies to an entire organization's activity, including everything that the organization does. Therefore all the programs and

Creating A Program Budget Defining a Program Budget ORGANIZATIONAL BUDGET: Applies to an entire organization's activity, including everything that the organization does. Therefore all the programs and

SRC: Cost Policy Statement

Reviewed08/06/2014 SRC: Cost Policy Statement I. General Accounting Policies A. Basis of Accounting - Accrual Basis B. Fiscal Period - January 1 through December 31 C. Allocation Basis for Individual Cost

Reviewed08/06/2014 SRC: Cost Policy Statement I. General Accounting Policies A. Basis of Accounting - Accrual Basis B. Fiscal Period - January 1 through December 31 C. Allocation Basis for Individual Cost

Working with F&A at UVA. Caroline Beeman

Caroline Beeman By the end of this session you should be able to solve this problem: Your PI is writing a proposal for an $800,000 grant. This is the total amount the sponsor is willing to pay for both

Caroline Beeman By the end of this session you should be able to solve this problem: Your PI is writing a proposal for an $800,000 grant. This is the total amount the sponsor is willing to pay for both

INDIRECT COSTS COST POLICY STATEMENT (CPS) GUIDANCE

GUIDANCE") INDIRECT COSTS COST POLICY STATEMENT (CPS) GUIDANCE The following is an example of the Cost Policy Statement (CPS) which is required if your organization plans to charge indirect costs to a grant awarded

INDIRECT COSTS COST POLICY STATEMENT (CPS) GUIDANCE The following is an example of the Cost Policy Statement (CPS) which is required if your organization plans to charge indirect costs to a grant awarded

Texas Association of Community Action Agencies (TACAA) 2016 Conference. May 18 20, 2016 San Antonio, TX Holiday Inn Riverwalk Hotel.

2016 Conference. May 18 20, 2016 San Antonio, TX Holiday Inn Riverwalk Hotel.") Texas Association of Community Action Agencies (TACAA) 2016 Conference May 18 20, 2016 San Antonio, TX Holiday Inn Riverwalk Hotel Cost Allocation Thursday, May 19, 2016 8:30 am 10:00 am Presented by:

Texas Association of Community Action Agencies (TACAA) 2016 Conference May 18 20, 2016 San Antonio, TX Holiday Inn Riverwalk Hotel Cost Allocation Thursday, May 19, 2016 8:30 am 10:00 am Presented by:

Finance Chapter: Cost Recovery and Invoicing

Finance Chapter: Cost Recovery and Invoicing Last Revised: 2/2019 Table of Contents Definitions... 2 LPA Agreements and Cost Recovery... 3 100% Locally Funded Work in a Federal/State Project... 4 LPA Timekeeping

Finance Chapter: Cost Recovery and Invoicing Last Revised: 2/2019 Table of Contents Definitions... 2 LPA Agreements and Cost Recovery... 3 100% Locally Funded Work in a Federal/State Project... 4 LPA Timekeeping

CORPORATION FOR PUBLIC BROADCASTING OFFICE OF INSPECTOR GENERAL

CORPORATION FOR PUBLIC BROADCASTING OFFICE OF INSPECTOR GENERAL EVALUATION REPORT ON THE VIABILITY OF CPB S INDIRECT ADMINISTRATIVE SUPPORT BASIC METHOD OPTION REPORT NO. L-ACJ1706-1805 June 5, 2018 [This

CORPORATION FOR PUBLIC BROADCASTING OFFICE OF INSPECTOR GENERAL EVALUATION REPORT ON THE VIABILITY OF CPB S INDIRECT ADMINISTRATIVE SUPPORT BASIC METHOD OPTION REPORT NO. L-ACJ1706-1805 June 5, 2018 [This

Be Prepared: Non-Profit Charter School Financial Statements are Changing

Be Prepared: Non-Profit Charter School Financial Statements are Changing Marlen Gomez, CPA Franci Sassin Derrick DeBruyne, CPA, CFE California Charter Schools Conference 2017 AGENDA Introduction How are

Be Prepared: Non-Profit Charter School Financial Statements are Changing Marlen Gomez, CPA Franci Sassin Derrick DeBruyne, CPA, CFE California Charter Schools Conference 2017 AGENDA Introduction How are

Facilities and Administrative (F&A) Rate A Glimpse Inside the Rate Calculation. April 7, 2011

Rate A Glimpse Inside the Rate Calculation. April 7, 2011") Facilities and Administrative (F&A) Rate A Glimpse Inside the Rate Calculation April 7, 2011 Workshop Presenter(s) Melanie Loots Associate Vice Chancellor for Research Phone: 333-0034 Email: mloots@illinois.edu

Facilities and Administrative (F&A) Rate A Glimpse Inside the Rate Calculation April 7, 2011 Workshop Presenter(s) Melanie Loots Associate Vice Chancellor for Research Phone: 333-0034 Email: mloots@illinois.edu

Indirect Cost Allocation. August 22 nd, 2013

Indirect Cost Allocation August 22 nd, 2013 Why is Cost Allocation Important? What are some of the Federal requirements governing indirect cost allocation plans? Allowable and unallowable costs? What is

Indirect Cost Allocation August 22 nd, 2013 Why is Cost Allocation Important? What are some of the Federal requirements governing indirect cost allocation plans? Allowable and unallowable costs? What is

GOVERNMENT CONTRACTING

A GUIDE TO INDIRECT COST RATES IN GOVERNMENT CONTRACTING www.ryansharkey.com TABLE OF CONTENTS Overview Direct vs. Indirect Costs... 3 What are Indirect Rates?... 4 Calculation of Indirect Rates and Impact

A GUIDE TO INDIRECT COST RATES IN GOVERNMENT CONTRACTING www.ryansharkey.com TABLE OF CONTENTS Overview Direct vs. Indirect Costs... 3 What are Indirect Rates?... 4 Calculation of Indirect Rates and Impact

A CENTRAL SERVICES COST ALLOCATION PLAN RACINE COUNTY, WISCONSIN ACTUAL 2008

A CENTRAL SERVICES COST ALLOCATION PLAN RACINE COUNTY, WISCONSIN ACTUAL 2008 ACTUAL COSTS FOR THE YEAR ENDED December 31, 2008 Windsor, WI 2009 MAXIMUS, INC. RACINE COUNTY, WISCONSIN 2008 ORGANIZATION

A CENTRAL SERVICES COST ALLOCATION PLAN RACINE COUNTY, WISCONSIN ACTUAL 2008 ACTUAL COSTS FOR THE YEAR ENDED December 31, 2008 Windsor, WI 2009 MAXIMUS, INC. RACINE COUNTY, WISCONSIN 2008 ORGANIZATION

Facilities and Administration Rate Proposal

Facilities and Administration Rate Proposal Fiscal Year Ending June 30, 2008 Facilities and Administration Rate Proposal Fiscal Year Ending June 30, 2008 Facilities and Administration April 6, 2009 Ms.

Facilities and Administration Rate Proposal Fiscal Year Ending June 30, 2008 Facilities and Administration Rate Proposal Fiscal Year Ending June 30, 2008 Facilities and Administration April 6, 2009 Ms.

Is Your Organization Healthy? : Cost Allocation Methodology, Timesheets and Invoices. Marissa M. Tirona Projects Director April 2, 2009

Is Your Organization Healthy? : Cost Allocation Methodology, Timesheets and Invoices Marissa M. Tirona Projects Director April 2, 2009 Learning Objectives To develop and implement a comprehensive allocation

Is Your Organization Healthy? : Cost Allocation Methodology, Timesheets and Invoices Marissa M. Tirona Projects Director April 2, 2009 Learning Objectives To develop and implement a comprehensive allocation

Cost Allocation Plan. Prepared in compliance with OMB A-87 Guidelines City and County of San Francisco For the Plan Year Ending June 30, 2012

Cost Allocation Plan Prepared in compliance with OMB A-87 Guidelines City and County of San Francisco For the Plan Year Ending June 30, 2012 Revised 6/10/11 per State Audit Prepared by the Office of the

Cost Allocation Plan Prepared in compliance with OMB A-87 Guidelines City and County of San Francisco For the Plan Year Ending June 30, 2012 Revised 6/10/11 per State Audit Prepared by the Office of the

COST ACCOUNTING STANDARDS BOARD DISCLOSURE STATEMENT REQUIRED BY PUBLIC LAW EDUCATIONAL INSTITUTIONS

INDEX GENERAL INSTRUCTIONS--Continuation Sheet.............. (i) COVER SHEET AND CERTIFICATION................... C-1 PART I General Information.................. I-1 Part II Part III Part IV Direct Costs......................

INDEX GENERAL INSTRUCTIONS--Continuation Sheet.............. (i) COVER SHEET AND CERTIFICATION................... C-1 PART I General Information.................. I-1 Part II Part III Part IV Direct Costs......................

Key to Profitability

Key to Profitability Understanding Indirect Cost Allocation Rates Sam Davidson President, GovConConsulting2013, LLC govconconsulting2013@gmail.com/703-303-2701 Do you REALLY know what your products or

Key to Profitability Understanding Indirect Cost Allocation Rates Sam Davidson President, GovConConsulting2013, LLC govconconsulting2013@gmail.com/703-303-2701 Do you REALLY know what your products or

Revised Disclosure Statement. for: Harvard School of Public Health

FORM APPROVED OMB NUMBER 0348-0055 Disclosure Statement for: Harvard School of Public Health Page 1 of 70 INDEX Effective date July 1, 2004 Page COVER SHEET AND CERTIFICATION... C-1 PART I - General Information...

FORM APPROVED OMB NUMBER 0348-0055 Disclosure Statement for: Harvard School of Public Health Page 1 of 70 INDEX Effective date July 1, 2004 Page COVER SHEET AND CERTIFICATION... C-1 PART I - General Information...

BETTY T. YEE California State Controller

UIE BETTY T. YEE California State Controller Division of Accounting and Reporting NEGOTIATION AGREEMENT COUNTYWIDE COST ALLOCATION PLAN City and County of San Francisco Date: June 30, 2016 San Francisco,

UIE BETTY T. YEE California State Controller Division of Accounting and Reporting NEGOTIATION AGREEMENT COUNTYWIDE COST ALLOCATION PLAN City and County of San Francisco Date: June 30, 2016 San Francisco,

Budget Empowerment and Accountability for Nonprofit Organizations

Budget Empowerment and Accountability for Nonprofit Organizations A. Michael Gellman, CPA Rubino & McGeehin Chartered CPAs and Consultants Developed under cooperative agreement with HHS, HRSA, HAB Access

Budget Empowerment and Accountability for Nonprofit Organizations A. Michael Gellman, CPA Rubino & McGeehin Chartered CPAs and Consultants Developed under cooperative agreement with HHS, HRSA, HAB Access

APPENDIX E Additional Accounting Guidance

APPENDIX E Additional Accounting Guidance Table of Contents Page TO-FROM TRANSPORTATION... 1 Identification of Costs... 1 Accounting for Non-To-and-From and Non-Pupil Transportation... 2 Calculating State-Funded

APPENDIX E Additional Accounting Guidance Table of Contents Page TO-FROM TRANSPORTATION... 1 Identification of Costs... 1 Accounting for Non-To-and-From and Non-Pupil Transportation... 2 Calculating State-Funded

THE UNIVERSITY OF TEXAS AT DALLAS

COST ACCOUNTING STANDARDS BOARD COVER SHEET AND CERTIFICATION Revision 3 Date: August 1, 2006 INDEX (FORM APROVED OMB NUMBER 0348-0055) Page Number GENERAL INSTRUCTIONS 1 COVER SHEET AND CERTIFICATION

COST ACCOUNTING STANDARDS BOARD COVER SHEET AND CERTIFICATION Revision 3 Date: August 1, 2006 INDEX (FORM APROVED OMB NUMBER 0348-0055) Page Number GENERAL INSTRUCTIONS 1 COVER SHEET AND CERTIFICATION

Accounting System Requirements

Accounting System Requirements Further information is available in the Information for Contractors Manual under Enclosure 2 The views expressed in this presentation are DCAA's views and not necessarily

Accounting System Requirements Further information is available in the Information for Contractors Manual under Enclosure 2 The views expressed in this presentation are DCAA's views and not necessarily

Copyright Notice. Course Layout & Presentation. Incurred Cost Audits The Process, What to Expect, & How to Survive

Incurred Cost Audits The Process, What to Expect, & How to Survive Presented by Norman J. Lorch, CPA Norman J, Lorch, Copyright Notice The materials presented in this handbook and all of the slides are

Incurred Cost Audits The Process, What to Expect, & How to Survive Presented by Norman J. Lorch, CPA Norman J, Lorch, Copyright Notice The materials presented in this handbook and all of the slides are

INDIRECT COSTS. A Direct Explanation. July 18, What Federal Regulations Govern?

INDIRECT COSTS A Direct Explanation July 18, 2017 What Federal Regulations Govern? Office of Management and Budget (OMB) Uniform Administrative Requirements, Cost Principles, and Audit Requirements for

INDIRECT COSTS A Direct Explanation July 18, 2017 What Federal Regulations Govern? Office of Management and Budget (OMB) Uniform Administrative Requirements, Cost Principles, and Audit Requirements for

M307 Facilities and Administrative Rate Proposal Process at Universities: Guidance for Central/Departmental Administrators

M307 Facilities and Administrative Rate Proposal Process at Universities: Guidance for Central/Departmental Administrators Authors: Hank Kirschenmann - Attain Clay Hester University of Alabama at Birmingham

M307 Facilities and Administrative Rate Proposal Process at Universities: Guidance for Central/Departmental Administrators Authors: Hank Kirschenmann - Attain Clay Hester University of Alabama at Birmingham

Departments will be given credit (or a reduction of allocations) for the following item:

for the following item:") O R E G O N H E A L T H & S C I E N C E U N I V E R S I T Y O V E R H E A D C O S T ( O C A ) M E T H O D O L O G Y D E S C R I P T I O N F O R T H E F I S C A L Y E A R E N D I N G J U N E 3 0, 2 0 1

O R E G O N H E A L T H & S C I E N C E U N I V E R S I T Y O V E R H E A D C O S T ( O C A ) M E T H O D O L O G Y D E S C R I P T I O N F O R T H E F I S C A L Y E A R E N D I N G J U N E 3 0, 2 0 1

Account Management and Transaction Review

Account Management and Transaction Review General Account Management and Transaction Review The use of Account within this document refers to what in Peoplesoft are projects, chart-strings, or Project/grant

Account Management and Transaction Review General Account Management and Transaction Review The use of Account within this document refers to what in Peoplesoft are projects, chart-strings, or Project/grant