Navigating the Indirect Cost Rate Maze. Chad Braley Marie Salamone

|

|

|

- Blake Lloyd

- 5 years ago

- Views:

Transcription

1 Navigating the Indirect Cost Rate Maze Chad Braley Marie Salamone

2 Value Proposition Capital Edge is the country s largest independent consulting firm focusing solely on the U.S. Government contracting market. 2

3 Who We Work With All entities receiving Federal funding 3

4 The Solution Model 4

5 Contract Life Cycle Support *The graphic above is a sampling of services offered. 5

6 Course Outline Indirect Rates The Basics Indirect Rate Composition Options Indirect Rates throughout Contract Life Cycle Establishing and Understanding Corporate Strategic Objectives Challenges Developing Indirect Cost Rates Mergers and Acquisitions Indirect Rate Changes under CAS Covered Contracts To Silo or Not to Silo Decentralized Organizations Corporate Culture Hurdles 6

7 Indirect Rates The Basics

8 Three Questions Direct What is Cost? Indirect What is Cost Allocation? Pools Allocation Base What is Cost Allowability? Reasonable Allowable Allocable 8

9 Composition of Total Cost FAR Direct Costs Costs directly associated with production of a product or service (aka Variable Costs ) + Indirect Costs Costs required to support production and/or normal business operations (aka Fixed Costs ) + Cost of Money The imputed cost of investment in the business - Applicable Credits = Total Cost 9

10 Typical Direct & Indirect Costs Material Direct Labor Utilities Indirect Labor Subcontracts Rent Direct Costs Indirect Costs 10

11 Direct & Indirect Costs The regulations do not provide explicit criteria for the types of direct and indirect costs It is up to your company to define the costs that are direct vs. indirect as long as company parameters: can meet direct/indirect regulatory definitions, and ensure that costs are treated consistently as direct/indirect in like circumstances (CAS 402 Guidance) Depending on industry type, make-up of company costs, company size, etc., costs that are treated as direct by one company may be treated as indirect by another 11

12 Major Concepts Indirect Cost Pools Homogeneous Pools Beneficial or Causal Relationships Homogeneous Indirect pools must contain costs with common links Base used to allocate those pooled cost must benefit from or demonstrate to have caused the indirect costs to be incurred Allocability FAR Normally expressed as a percentage (i.e., Pool Expenses is the numerator and Allocation Base is the denominator) 12

13 Typical Indirect Pools and Allocation Bases Fringe Pool Health Insurance Vacation Total Labor Retirement Overhead Pool Indirect Labor Utilities Direct Labor Rent G&A Human Resources Total Cost Input Finance or CEO Value Added Input Base 13

14 Full Absorption Costing Material / Subcontracts General Direct Labor Overhead Selling Administrative Product Cost Period Cost Total Project Costs 14

15 Allowable Cost Criteria FAR What is Cost Allowability? Costs the Government is willing to pay for! CAS/GAAP Compliant Reasonable Allocable A cost is allowable only when the cost complies with all of the following requirements FAR 31.2 criteria and limitations Complies with terms of the contract Risks of double and treble damages, plus interest for failure to comply! 15

16 Indirect Rate Composition Options

17 Common Indirect Cost Pools Common Indirect Cost Pools Overhead Company Site Overhead Customer Site General & Administrative (G&A) Material Handling (typical when a value added G&A base is used) Fringe Benefits 17

18 Intermediate Cost Pools Typical Intermediate Cost Pools & Bases Fringe benefits -- Total labor Facilities Square footage or headcount IT Service Center -- Usage or headcount Payroll Service Center -- Paychecks or headcount Overhead Service Center -- Direct Labor & Fringe Human Resources -- Headcount These can be found in Schedule D of the ICS 18

19 Two Tiers vs. Three Tiers Two Tiers Fringe is considered an intermediate pool, allocated based on direct labor Allocated out to G&A and Overhead pools as part of their rates Overhead includes fringe on direct labor Overhead is applied on direct labor only G&A applied to the total cost input Three Tiers Fringe is a final indirect rate pool, applied to total labor Applied first before Overhead and G&A rates applied Overhead is applied on Direct Labor plus fringe on Direct Labor G&A is applied to the total cost input 19

20 Two Tiers vs. Three Tiers Fringe (allocated based on % of Total labor) Two Tier Indirect Rate Structure Overhead direct labor G&A total cost input 20

21 Two Tiers vs. Three Tiers Three Tier Indirect Rate Structure Fringe Overhead G&A Total Labor Direct Labor + Direct Labor Fringe Direct Labor + DL Fringe + Overhead + ODC s +Subcontracts 21

22 Two Tiers vs. Three Tiers Similarities The G&A rate will always be the same, because it is applied to the same base (total cost input) regardless of the structure Differences Overhead rate will be higher using two-tier system, because fringe costs are in the pool instead of the base *How to decide: How many times have you heard a customer say your O/H rate is too high? How many times have you heard a customer say to cut benefits b/c your fringe is too high? Definitely worth consideration. 22

23 G&A Allocation Bases Companies can choose between three types of G&A allocation bases: Total Cost Input includes all contract costs except G&A, including direct labor, fringe, overhead, subcontracts, materials, and other ODC s Method used most often Value-Added does not include direct material and subcontracts costs Useful when there is a significant amount of subcontract costs and/or materials Single Input Base Typically direct labor and less frequently used 23

24 Strategy Considerations What is important to your organization? Want a Lower Pass Thru on SubK? Want a Lower Overhead Rate? High number of subcontractors / material costs? Consider moving from a 2 Tier to a 3 Tier Fringe Structure Consider a Material Handling Rate Review costs which could be claimed as Fringe rather than Overhead 24

25 Common Pitfalls to Avoid When changing G&A allocation bases, you must consider the impact of rate changes on existing contracts When creating a customer site O/H, be aware of the impact to your contractor site work Creating new O/H pools for new contracts or new work sites can be very dangerous The administrative and systemic burdens often outweigh the benefits This process can also create numerous small pools and bases that may fluctuate significantly Be wary of your contract type mix when making changes How will this effect the entire contract population? 25

26 Indirect Rates Throughout Contract Life Cycle

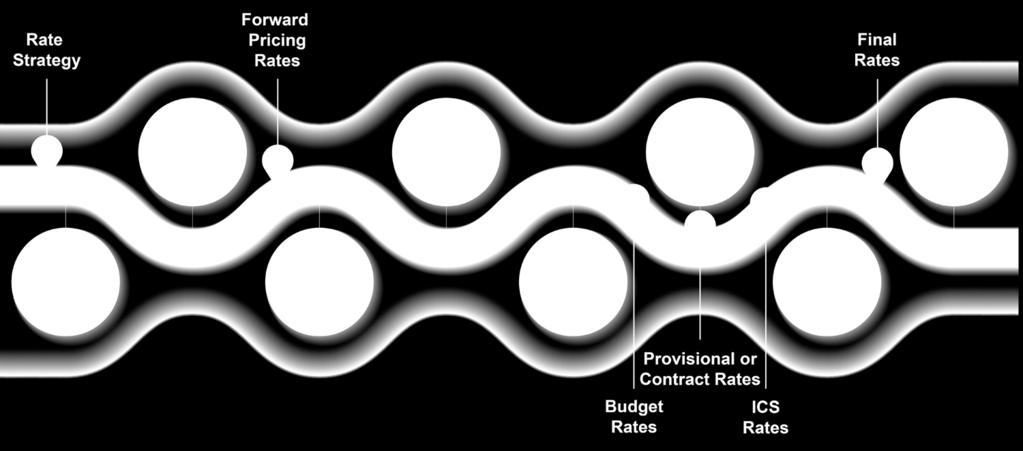

27 Types of Indirect Rates 27

28 Types of Indirect Rates (Cont.) Forward Pricing Rates - FAR allows for the establishment of mutually agreed to Forward Pricing Rates between the Contracting Officer and Contractor Established long-term rates for use in contractor pricing efforts Based on the Contractor s long range plans and budgets May be continuously negotiated/updated based on availability of most current, accurate, and complete data Adequacy Check List available at DCAA.mil Budgeted Rates Approved internally for management purposes and as a basis for pricing products and services DCAA expects rates are prepared annually 28

29 Types of Indirect Rates (Cont.) Provisional or Contract Rates (FAR ) Approval by the contracting officer or CFAO Rates established based on information from recent review, previous rate audits or experience Auditor assurance that rates are as close as possible to final indirect cost rates anticipated Revision by mutual agreement (AT ANY TIME), to prevent substantial over/underpayment Typically based on a contractor s budget rates 29

30 Types of Indirect Rates (Cont.) ICS Rates (Final Indirect Cost Rate Proposal) Unaudited year end rates based on actual costs incurred Subject to audit by DCAA or Contracting Officer s designee Required within six months of Contractor s fiscal year end FAR (d)(2)(i) - Allowable Cost and Payment FAR (b)(4) & (b)(5) - Payments under T&M and Labor- Hour Contracts FAR allows for ICS rates to become provisional rates for the fiscal period until the Contractor s ICS can be audit and rates finalized 30

31 Types of Indirect Rates (Cont.) Final Rates - FAR requires final determination of rates by either the Contractor officer or his assigned representative (auditor) Adjusted for questioned/unallowable costs identified by the auditor and Subject to Negotiation 31

32 Life Cycle of Indirect Rates 32

33 Acquisition Cycle - Indirect Rates 33

34 Establishing and Understanding Corporate Strategic Objectives

35 Organizational Considerations What type of industry? Goods Services How large is your organization? Small Medium Large Does your organization have many people and facilities in multiple locations? Do you have a large number of subcontractors? 35

36 Considerations Industry (Cont.) Goods Do you have multiple product lines requiring differing support functions? Do you have manufacturing facilities in multiple locations? Services Do you have a large number of employees working at client/customer sites? Do you have different service offerings requiring different support functions? Are your employee s located both domestically and internationally? 36

37 Compliant Rate Structure Benefits Facilitates Decision Making How is the company structured? Is the company structure changing? Improves Competitive Advantage in Market Place Indirect Rate Structure positioned to win the work Capitalizes on Thorough Budgeting Process Hopefully already in existence Ensures Allowable Cost Recovery And maybe even some profit! Rate Structure MUST mirror the Organization, not limited by accounting software, customer or govt. 37

38 Indirect Cost Rate Challenges

39 Challenge No. 1 Mergers and Acquisitions Due Diligence Has proper due diligence been performed on existing government contracts? Are there rate caps? Are there CAS covered contracts? Are there unsubmitted/late incurred cost submission years? Are there inadequate incurred cost submissions? Are costs owed to the government on flexibly priced contracts? Incorporate or Segregate Will the acquired company be folded into the existing company? How will the acquisition impact the existing rate structure? Allowable vs. Unallowable Costs Are M&A costs captured to properly segregate allowable from unallowable? 39

40 Challenge No. 2 Rate Changes under CAS Covered Contracts Fully CAS Covered Contracts require disclosure to accounting practices including indirect rate structures Changes to disclosed practices (including changes to rates) require cost impact proposals Two types of cost impact proposals General Dollar Magnitude (GDM) Proposal (FAR d) Detailed Cost Impact (DCI) Proposal (FAR e) For Companies without CAS Covered Contracts: 1. Keep changes to a minimum - makes good business sense 2. Change rates to maintain compliance with standards 3. Cost become material because of change in business 4. If changes are necessary, change ahead of anticipation of receiving a CAS covered contract 40

41 Challenge No. 3 To Silo or Not to Silo Advantages Limits Compliance to Government Business Limits Audits and Oversight to Government Business Disadvantages Disruption to current operations Corporate culture resistance to change Sometimes difficult to get buy in until work volume increases 41

42 Challenge No. 4 Decentralized Organizations Lines of business can analyze profitability in a vacuum Bid on new work using rates which are not the most current, accurate and complete Win contracts with significantly low rate caps Bill contracts with unapproved provisional rates resulting High contract overbillings resulting in paying $$ back to the government OR High contract underbillings resulting in poor cash flow to the organization 42

43 Challenge No. 5 Corporate Culture Hurdles Establishing or changing allocation bases can impact lines of businesses differently Example: Use of headcount for IT vs. Use of No. of Licenses Allocating costs on budgeted data without using actual base data Actual data is difficult to obtain or no longer tracked Communication Challenges Between Departments Contracts and Accounting/Finance Business Development and Compliance 43

44

45

46 CONTACT US CORPORATE HEADQUARTERS 8200 Greensboro Drive Suite 401 McLean, Virginia National Coverage in Satellite Offices Phoenix, AZ Los Angeles, CA San Diego, CA San Francisco, CA Denver, CO Melbourne, FL Tampa, FL Dayton, OH Pittsburgh, PA Philadelphia, PA

Key to Profitability

Key to Profitability Understanding Indirect Cost Allocation Rates Sam Davidson President, GovConConsulting2013, LLC govconconsulting2013@gmail.com/703-303-2701 Do you REALLY know what your products or

Key to Profitability Understanding Indirect Cost Allocation Rates Sam Davidson President, GovConConsulting2013, LLC govconconsulting2013@gmail.com/703-303-2701 Do you REALLY know what your products or

Indirect Rates for Cost Plus Contracting Jenny W Clark. Jenny Clark

Indirect Rates for Cost Plus Contracting Jenny W Clark Jenny Clark jwclark@solvability.com Jenny W Clark The Oprah of Federal Contracting Solvability, Inc. www.solvability.com Phone 256-882-6276 E-mail

Indirect Rates for Cost Plus Contracting Jenny W Clark Jenny Clark jwclark@solvability.com Jenny W Clark The Oprah of Federal Contracting Solvability, Inc. www.solvability.com Phone 256-882-6276 E-mail

GCS 224 Surviving DCAA Audits with GCS Premier. Presented by: Nicole Mitchell, Aronson & Company

GCS 224 Surviving DCAA Audits with GCS Premier Presented by: Nicole Mitchell, Aronson & Company Agenda Government Contract Audits and the Role of DCAA and DCMA Basic Attributes of a Government Approved

GCS 224 Surviving DCAA Audits with GCS Premier Presented by: Nicole Mitchell, Aronson & Company Agenda Government Contract Audits and the Role of DCAA and DCMA Basic Attributes of a Government Approved

Click to edit Master title style

Click to edit Master title style Fourth level The Cost Accounting Standards and Consequences of Noncompliance Click to edit Master text styles Click to edit Master title style Breakout Third Session level

Click to edit Master title style Fourth level The Cost Accounting Standards and Consequences of Noncompliance Click to edit Master text styles Click to edit Master title style Breakout Third Session level

Government Contracts Pricing Strategies and Rate Structures

Government Contracts Pricing Strategies and Rate Structures Presented By: Brandon Smith bsmith@anglincpa.com Jon Levin jlevin@maynardcooper.com Provisional Billing Rates Provisional, Target, Budget, Billing,

Government Contracts Pricing Strategies and Rate Structures Presented By: Brandon Smith bsmith@anglincpa.com Jon Levin jlevin@maynardcooper.com Provisional Billing Rates Provisional, Target, Budget, Billing,

Indirect Cost Recovery: What You Need to Consider. August 2017

Indirect Cost Recovery: What You Need to Consider August 2017 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee,

Indirect Cost Recovery: What You Need to Consider August 2017 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee,

CAS - Part II. The Cost Allocation Standards Dixon Hughes Goodman, LLP

CAS - Part II The Cost Allocation Standards 1 Agenda Session I Administration: CAS Overview Applicability Types of Coverage CAS Administration Part II - The Cost Allocation Standards Part III - The Cost

CAS - Part II The Cost Allocation Standards 1 Agenda Session I Administration: CAS Overview Applicability Types of Coverage CAS Administration Part II - The Cost Allocation Standards Part III - The Cost

The topic of government contract cost accounting is one

The topic of government contract cost accounting is one that is distinguished from accounting for commercial contracts. Not surprisingly, there are requirements unique to U.S. government contracts. Most

The topic of government contract cost accounting is one that is distinguished from accounting for commercial contracts. Not surprisingly, there are requirements unique to U.S. government contracts. Most

PAC B.01/ August 7, PAC-013(R) MEMORANDUM FOR REGIONAL DIRECTORS, DCAA HEADS OF PRINCIPAL STAFF ELEMENTS, HQ, DCAA

MEMORANDUM FOR REGIONAL DIRECTORS, DCAA HEADS OF PRINCIPAL STAFF ELEMENTS, HQ, DCAA") DEFENSE CONTRACT AUDIT AGENCY DEPARTMENT OF DEFENSE 8725 JOHN J. KINGMAN ROAD, SUITE 2135 FORT BELVOIR, VA 22060-6219 IN REPLY REFER TO PAC 730.3.B.01/2013-02 August 7, 2014 MEMORANDUM FOR REGIONAL DIRECTORS,

DEFENSE CONTRACT AUDIT AGENCY DEPARTMENT OF DEFENSE 8725 JOHN J. KINGMAN ROAD, SUITE 2135 FORT BELVOIR, VA 22060-6219 IN REPLY REFER TO PAC 730.3.B.01/2013-02 August 7, 2014 MEMORANDUM FOR REGIONAL DIRECTORS,

GOVERNMENT CONTRACTING

A GUIDE TO INDIRECT COST RATES IN GOVERNMENT CONTRACTING www.ryansharkey.com TABLE OF CONTENTS Overview Direct vs. Indirect Costs... 3 What are Indirect Rates?... 4 Calculation of Indirect Rates and Impact

A GUIDE TO INDIRECT COST RATES IN GOVERNMENT CONTRACTING www.ryansharkey.com TABLE OF CONTENTS Overview Direct vs. Indirect Costs... 3 What are Indirect Rates?... 4 Calculation of Indirect Rates and Impact

N o w h e r e t o R u n, N o w h e r e t o H i d e : D i s c l o s u r e S t a t e m e n t s a n d C o s t A c c o u n t i n g S t a n d a r d s

N o w h e r e t o R u n, N o w h e r e t o H i d e : D i s c l o s u r e S t a t e m e n t s a n d C o s t A c c o u n t i n g S t a n d a r d s Presented by Darrell Hineman, CPA, CFE, Director Jeff Shapiro,

N o w h e r e t o R u n, N o w h e r e t o H i d e : D i s c l o s u r e S t a t e m e n t s a n d C o s t A c c o u n t i n g S t a n d a r d s Presented by Darrell Hineman, CPA, CFE, Director Jeff Shapiro,

Chiu Lee DCAA Financial Liaison Advisor

DCAA SERVICES An Overview of the DCAA Audit Process for Small Businesses Chiu Lee DCAA Financial Liaison Advisor DARPA SBIR Phase I Workshop The views expressed in this presentation are DCAA's views and

DCAA SERVICES An Overview of the DCAA Audit Process for Small Businesses Chiu Lee DCAA Financial Liaison Advisor DARPA SBIR Phase I Workshop The views expressed in this presentation are DCAA's views and

PANEL E: Costly Mistakes!

PANEL E: Costly Mistakes! How to avoid the most common pitfalls that face a growing company. Lessons learned from an operational and legal perspective that may help you make money and stay out of jail!

PANEL E: Costly Mistakes! How to avoid the most common pitfalls that face a growing company. Lessons learned from an operational and legal perspective that may help you make money and stay out of jail!

VIP Presents. Indirect Rates What you need to know!

VIP Presents Indirect Rates What you need to know! The VIP Program Accelerating the Growth of Veteran Owned Small Businesses in the Federal Marketplace Powered By 971 Graduates and Growing From 45 States,

VIP Presents Indirect Rates What you need to know! The VIP Program Accelerating the Growth of Veteran Owned Small Businesses in the Federal Marketplace Powered By 971 Graduates and Growing From 45 States,

Contract Pricing Reference Guides Volume 3 Chapter 9 Analysis of Indirect Costs

Contract Pricing Reference Guides Volume 3 Chapter 9 Analysis of Indirect Costs 9.0 - Chapter Introduction 9.1 - Identifying Pools And Bases For Rate Development o 9.1.1 - Identifying Indirect Cost Pools

Contract Pricing Reference Guides Volume 3 Chapter 9 Analysis of Indirect Costs 9.0 - Chapter Introduction 9.1 - Identifying Pools And Bases For Rate Development o 9.1.1 - Identifying Indirect Cost Pools

government contracting

Policy and Procedures Manual: What s In It and Why Do You Need One? Janet Borjeson Mike Mardesich October 27, 2016 The Fundamentals of Government Contracting Webinar Series 1 Your Presenters Janet Borjeson

Policy and Procedures Manual: What s In It and Why Do You Need One? Janet Borjeson Mike Mardesich October 27, 2016 The Fundamentals of Government Contracting Webinar Series 1 Your Presenters Janet Borjeson

Indirect Rates the Basics In Deltek GCS Premier

Indirect Rates the Basics In Deltek GCS Premier COPYRIGHT INFORMATION While NeoSystems has made every attempt to ensure the accuracy of these materials, some errors may exist. NeoSystems is not responsible

Indirect Rates the Basics In Deltek GCS Premier COPYRIGHT INFORMATION While NeoSystems has made every attempt to ensure the accuracy of these materials, some errors may exist. NeoSystems is not responsible

Keys to Submitting an Adequate Incurred Cost Proposal

Keys to Submitting an Adequate Incurred Cost Proposal Presented By: Kiran Pinto, Senior Manager, Watkins Meegan Keith Romanowski, Compliance Director, WJ Technologies March 20, 2013 Agenda Who Needs to

Keys to Submitting an Adequate Incurred Cost Proposal Presented By: Kiran Pinto, Senior Manager, Watkins Meegan Keith Romanowski, Compliance Director, WJ Technologies March 20, 2013 Agenda Who Needs to

ACCOUNTING SYSTEMS for SBIR/STTR AWARDS. Presented by: Mike Anderson

ACCOUNTING SYSTEMS for SBIR/STTR AWARDS Presented by: Mike Anderson Seminar Objectives What is the Difference Between a Grant and a Contract Accounting Requirements For Cost-Type Awards What are Audit

ACCOUNTING SYSTEMS for SBIR/STTR AWARDS Presented by: Mike Anderson Seminar Objectives What is the Difference Between a Grant and a Contract Accounting Requirements For Cost-Type Awards What are Audit

F i v e C A S S t a n d a r d s E v e r y G o v e r n m e n t C o n t r a c t o r S h o u l d K n o w a n d F o l l o w

F i v e C A S S t a n d a r d s E v e r y G o v e r n m e n t C o n t r a c t o r S h o u l d K n o w a n d F o l l o w December 17, 2015 Presented by: Darrell Hineman, CPA CFE Director Long Nguyen, CFE

F i v e C A S S t a n d a r d s E v e r y G o v e r n m e n t C o n t r a c t o r S h o u l d K n o w a n d F o l l o w December 17, 2015 Presented by: Darrell Hineman, CPA CFE Director Long Nguyen, CFE

COST ACCOUNTING STANDARDS BOARD DISCLOSURE STATEMENT REQUIRED BY PUBLIC LAW EDUCATIONAL INSTITUTIONS

INDEX GENERAL INSTRUCTIONS--Continuation Sheet.............. (i) COVER SHEET AND CERTIFICATION................... C-1 PART I General Information.................. I-1 Part II Part III Part IV Direct Costs......................

INDEX GENERAL INSTRUCTIONS--Continuation Sheet.............. (i) COVER SHEET AND CERTIFICATION................... C-1 PART I General Information.................. I-1 Part II Part III Part IV Direct Costs......................

References: CAM Section 2 - General Audit Guidance for Termination of Negotiated Contracts

References: CAM 12-200 Section 2 - General Audit Guidance for Termination of Negotiated Contracts CAM 12-400 Section 4 - Auditing Terminations of Cost-Type Contracts Audit Program 17100 Termination, Cost

References: CAM 12-200 Section 2 - General Audit Guidance for Termination of Negotiated Contracts CAM 12-400 Section 4 - Auditing Terminations of Cost-Type Contracts Audit Program 17100 Termination, Cost

How to Develop Indirect Cost Rates For Nonprofit Organizations

How to Develop Indirect Cost Rates For Nonprofit Organizations 2010 Government and Not-For-Profit Conference UMD University College Adelphi, Maryland April 30, 2010 Presenter: Paul H. Calabrese Rubino

How to Develop Indirect Cost Rates For Nonprofit Organizations 2010 Government and Not-For-Profit Conference UMD University College Adelphi, Maryland April 30, 2010 Presenter: Paul H. Calabrese Rubino

International Cost Estimating & Analysis Association. Supplier Cost/Price Analyses June 20, 2013

International Cost Estimating & Analysis Association Supplier Cost/Price Analyses June 20, 2013 David Eck and Todd W. Bishop Dixon Hughes Goodman LLP Government Contract Consulting Services Group Agenda

International Cost Estimating & Analysis Association Supplier Cost/Price Analyses June 20, 2013 David Eck and Todd W. Bishop Dixon Hughes Goodman LLP Government Contract Consulting Services Group Agenda

Introduction to the Cost Accounting Standards Mike Mardesich & Brad Tress April 25, 2017

Introduction to the Cost Accounting Standards Mike Mardesich & Brad Tress April 25, 2017 The Fundamentals of Government Contracting Webinar Series 1 Your Presenters Mike Mardesich Dixon Hughes Goodman

Introduction to the Cost Accounting Standards Mike Mardesich & Brad Tress April 25, 2017 The Fundamentals of Government Contracting Webinar Series 1 Your Presenters Mike Mardesich Dixon Hughes Goodman

Incurred Cost Submissions

Incurred Cost Submissions Further information is available in the Information for Contractors Manual under Enclosure 6 The views expressed in this presentation are DCAA's views and not necessarily the

Incurred Cost Submissions Further information is available in the Information for Contractors Manual under Enclosure 6 The views expressed in this presentation are DCAA's views and not necessarily the

ONR SUBMISSION REQUIREMENTS FOR NONPROFIT INDIRECT COST RATE PROPOSALS - INITIAL CHECKLIST

ONR SUBMISSION REQUIREMENTS FOR NONPROFIT INDIRECT COST RATE PROPOSALS - INITIAL CHECKLIST 1. Transmittal Letter: State the type of rate requested (e.g. predetermined, fixed, provisional, or final) and

ONR SUBMISSION REQUIREMENTS FOR NONPROFIT INDIRECT COST RATE PROPOSALS - INITIAL CHECKLIST 1. Transmittal Letter: State the type of rate requested (e.g. predetermined, fixed, provisional, or final) and

ehealth Inventory Report of Major Medical Health Plans Available Off of Government Exchanges

ehealth Inventory Report of Major Medical Health Available Off of Government Exchanges February 2014 Introduction Beginning January 1, 2014, all new major medical health insurance plans were required to

ehealth Inventory Report of Major Medical Health Available Off of Government Exchanges February 2014 Introduction Beginning January 1, 2014, all new major medical health insurance plans were required to

Activity Code Compliance Audit CAS 403 Version 6.23, dated March 2018 B-1 Planning Considerations

Activity Code 19403 Compliance Audit CAS 403 B-1 Planning Considerations Type of Service - Attestation Examination Engagement Audit Specific Independence Determination Members of the audit team and internal

Activity Code 19403 Compliance Audit CAS 403 B-1 Planning Considerations Type of Service - Attestation Examination Engagement Audit Specific Independence Determination Members of the audit team and internal

Accounting System Requirements

Accounting System Requirements Further information is available in the Information for Contractors Manual under Enclosure 2 The views expressed in this presentation are DCAA's views and not necessarily

Accounting System Requirements Further information is available in the Information for Contractors Manual under Enclosure 2 The views expressed in this presentation are DCAA's views and not necessarily

Allocating Direct and Indirect Costs for Nonprofits

Allocating Direct and Indirect Costs for Nonprofits Carol Barnard April 18, 2018 Agenda Allocating Indirect Cost Why allocating costs is important to nonprofits Identifying indirect costs Different methods

Allocating Direct and Indirect Costs for Nonprofits Carol Barnard April 18, 2018 Agenda Allocating Indirect Cost Why allocating costs is important to nonprofits Identifying indirect costs Different methods

COST AND PRICING: NO CONTRACT IS REALLY FINAL. Terry Albertson Skye Mathieson Liz Buehler

COST AND PRICING: NO CONTRACT IS REALLY FINAL Terry Albertson Skye Mathieson Liz Buehler 79 Three Phases Proposal Performance and Billing Final Payment 80 Proposal Forward pricing rates Labor rates Indirect

COST AND PRICING: NO CONTRACT IS REALLY FINAL Terry Albertson Skye Mathieson Liz Buehler 79 Three Phases Proposal Performance and Billing Final Payment 80 Proposal Forward pricing rates Labor rates Indirect

Indirect Cost Rates For Nonprofit Organizations

Indirect Cost Rates For Nonprofit Organizations Bag Lunch Webinar May 8, 2013 All slides and handouts copyright 2013, Rubino & Company, Chartered Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants

Indirect Cost Rates For Nonprofit Organizations Bag Lunch Webinar May 8, 2013 All slides and handouts copyright 2013, Rubino & Company, Chartered Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants

ONR Guidance for Indirect Cost Rate Proposals for Non-Profits with less than $10M Federal Funding of Direct Costs in a Fiscal Year

ONR Guidance for Indirect Cost Rate Proposals for Non-Profits with less than $10M Funding of Direct Costs in a Fiscal Year A non-profit organization will submit an indirect cost rate proposal primarily

ONR Guidance for Indirect Cost Rate Proposals for Non-Profits with less than $10M Funding of Direct Costs in a Fiscal Year A non-profit organization will submit an indirect cost rate proposal primarily

Current Issues in Contractor Incurred Cost Submissions and Government Audits

Current Issues in Contractor Incurred Cost Submissions and Government Audits Breakout Session #: C03 Presented by: Stephen H. Bishop, Accounting Director at CGS Administrators, LLC Steven Masiello, McKenna

Current Issues in Contractor Incurred Cost Submissions and Government Audits Breakout Session #: C03 Presented by: Stephen H. Bishop, Accounting Director at CGS Administrators, LLC Steven Masiello, McKenna

Administrative Procedure

Division of Finance and Administration AP F&A-02 Administrative Procedure Title: Responsible Office: Adopted: June 1, 2017 Revised: Effective: June 1, 2017 Indirect Cost Rate Instructions for DEO Subrecipients

Division of Finance and Administration AP F&A-02 Administrative Procedure Title: Responsible Office: Adopted: June 1, 2017 Revised: Effective: June 1, 2017 Indirect Cost Rate Instructions for DEO Subrecipients

Click to edit Master title style

Click to edit Master title style Click to edit Master text styles Second level Click Indirect to edit Rate Master Cycle title style Factors that Drive Your Indirect Rates and Impact Click to edit Your

Click to edit Master title style Click to edit Master text styles Second level Click Indirect to edit Rate Master Cycle title style Factors that Drive Your Indirect Rates and Impact Click to edit Your

Is Your G&A Base Right for You?

Is Your G&A Base Right for You? Presented by CohnReznick s Government Contracting Industry Practice Christine Williamson, Partner and Karen Louis, Member, WJ Technologies PLEASE READ This presentation

Is Your G&A Base Right for You? Presented by CohnReznick s Government Contracting Industry Practice Christine Williamson, Partner and Karen Louis, Member, WJ Technologies PLEASE READ This presentation

Presented by Laura Anne Pray, CPA Audit Manager

Presented by Laura Anne Pray, CPA Audit Manager 1 Construction Industry at a Glance One of the largest contributing segments of the American economy Employees Gross National Product Raw Materials High

Presented by Laura Anne Pray, CPA Audit Manager 1 Construction Industry at a Glance One of the largest contributing segments of the American economy Employees Gross National Product Raw Materials High

Uniform Guidance vs. OMB Circulars

Cost Allocation 101 Uniform Guidance vs. OMB Circulars Prior to the Uniform Guidance, requirements Designed for governing DOL-ETA cost direct principles, recipients and administrative their subrecipients

Cost Allocation 101 Uniform Guidance vs. OMB Circulars Prior to the Uniform Guidance, requirements Designed for governing DOL-ETA cost direct principles, recipients and administrative their subrecipients

New to Cost Reimbursement Contracts? Meet Your New Friends

New to Cost Reimbursement Contracts? Meet Your New Friends Breakout Session #: G07 Brent Calhoon Partner Baker Tilly Shingai Mavengere Director, Government Accounting UnitedHealthcare Military & Veterans

New to Cost Reimbursement Contracts? Meet Your New Friends Breakout Session #: G07 Brent Calhoon Partner Baker Tilly Shingai Mavengere Director, Government Accounting UnitedHealthcare Military & Veterans

ZipRealty, Inc. Supplemental Data Reclassification of Consolidated Statement of Operations

Reclassification of Consolidated Statement of Operations Effective January 1, 2007, for income statement presentation purposes, we have reclassified sales support and marketing expenses from general and

Reclassification of Consolidated Statement of Operations Effective January 1, 2007, for income statement presentation purposes, we have reclassified sales support and marketing expenses from general and

Using GCS to Drive Decision Making Susan Smith, WJ Technologies Antoinette Merrill, Summit Consulting

GCS Premier It s Not Just A History Lesson Using GCS to Drive Decision Making Susan Smith, WJ Technologies Antoinette Merrill, Summit Consulting GCS Premier It s Not Just A History Lesson Objective: To

GCS Premier It s Not Just A History Lesson Using GCS to Drive Decision Making Susan Smith, WJ Technologies Antoinette Merrill, Summit Consulting GCS Premier It s Not Just A History Lesson Objective: To

That seems to be a problematic approach, right? Think about it: Solving Executive Compensation Concerns with Blended Rates. Written by Nick Sanders

The allowability of contractor executive compensation is a complex, tricky, thing made more tricky by recent statutory and regulatory changes. We have written about some of those rece nt changes before.

The allowability of contractor executive compensation is a complex, tricky, thing made more tricky by recent statutory and regulatory changes. We have written about some of those rece nt changes before.

Cost Accounting Standards: Overview and Best Practices

Cost Accounting Standards: Overview and Best Practices Joseph G. Martinez K. Tyler Thomas October 10, 2017 Agenda Introduction to the Cost Accounting Standards ("CAS") Overview/Fundamental Requirements

Cost Accounting Standards: Overview and Best Practices Joseph G. Martinez K. Tyler Thomas October 10, 2017 Agenda Introduction to the Cost Accounting Standards ("CAS") Overview/Fundamental Requirements

Indirect Cost Rates For Nonprofit Organizations

Indirect Cost Rates For Nonprofit Organizations Bag Lunch Webinar October 10, 2012 All slides and handouts copyright 2012, Rubino & Company, Chartered Presenter: Paul H. Calabrese Rubino & Company, CPAs

Indirect Cost Rates For Nonprofit Organizations Bag Lunch Webinar October 10, 2012 All slides and handouts copyright 2012, Rubino & Company, Chartered Presenter: Paul H. Calabrese Rubino & Company, CPAs

Contractor Learns Importance of Having DCAA-Approved Cost Accounting System the Hard Way

NOTE TO READERS: The Apogee Consulting, Inc. website is likely to be updated only sporadically over the next several weeks. This situation arises from the happy problem that we are SWAMPED WITH WORK and

NOTE TO READERS: The Apogee Consulting, Inc. website is likely to be updated only sporadically over the next several weeks. This situation arises from the happy problem that we are SWAMPED WITH WORK and

The Fundamentals of Government Contracting Webinar Series

An Introduction to the Incurred Cost Submission Part II: Preparation and Adequacy Review March 24 th, 2016 The Fundamentals of Government Contracting Webinar Series 1 Your Presenters David King Dixon Hughes

An Introduction to the Incurred Cost Submission Part II: Preparation and Adequacy Review March 24 th, 2016 The Fundamentals of Government Contracting Webinar Series 1 Your Presenters David King Dixon Hughes

Item No. Adequacy Consideration Adequate Notes

References: CAM 12-200 Section 2 - General Audit Guidance for Termination of Negotiated Contracts CAM 12-300 Section 3 - Auditing Terminations of Fixed-Price Contracts Audit Program 17100 Termination,

References: CAM 12-200 Section 2 - General Audit Guidance for Termination of Negotiated Contracts CAM 12-300 Section 3 - Auditing Terminations of Fixed-Price Contracts Audit Program 17100 Termination,

Indirect Cost Rate Development for Non-Profits Navigating Accounting Standards and Best Practices to Calculate and Assign Expenses

Presenting a live 110-minute teleconference with interactive Q&A Indirect Cost Rate Development for Non-Profits Navigating Accounting Standards and Best Practices to Calculate and Assign Expenses TUESDAY,

Presenting a live 110-minute teleconference with interactive Q&A Indirect Cost Rate Development for Non-Profits Navigating Accounting Standards and Best Practices to Calculate and Assign Expenses TUESDAY,

MG-3 - Supplier Cost Price Analyses Best Practices for Evaluating Supplier Proposals and Quotes

International Cost Estimating & Analysis Association - Supplier Cost / Price Analyses June 10-13, 2014 Presented By: David Eck, CPA Director Mike Mardesich, CPA Manager Dixon Hughes Goodman Government

International Cost Estimating & Analysis Association - Supplier Cost / Price Analyses June 10-13, 2014 Presented By: David Eck, CPA Director Mike Mardesich, CPA Manager Dixon Hughes Goodman Government

GOVERNMENT CONTRACT COSTS, PRICING & ACCOUNTING REPORT

Reprinted with permission from Government Contract Costs, Pricing& Accounting Report, Volume 12, Issue 1, K2017 Thomson Reuters. Further reproduction without permission of the publisher is prohibited.

Reprinted with permission from Government Contract Costs, Pricing& Accounting Report, Volume 12, Issue 1, K2017 Thomson Reuters. Further reproduction without permission of the publisher is prohibited.

Chapter 37 Joint Ventures and Teaming Arrangements

Chapter 37 Joint Ventures and Teaming Arrangements Authoritative Sources Cost Accounting Standards FAR Subpart 9.6 Contractor Team Arrangements FASB ASC 323 Investments - Equity Method and Joint Ventures

Chapter 37 Joint Ventures and Teaming Arrangements Authoritative Sources Cost Accounting Standards FAR Subpart 9.6 Contractor Team Arrangements FASB ASC 323 Investments - Equity Method and Joint Ventures

Regional Snapshot: The Cost of Living in Metro Atlanta

Regional Snapshot: The Cost of Living in Metro Atlanta Photo by rawpixel.com on Unsplash Atlanta Regional Commission, February 2018 For more information, contact: cdegiulio@atlantaregional.org In Summary

Regional Snapshot: The Cost of Living in Metro Atlanta Photo by rawpixel.com on Unsplash Atlanta Regional Commission, February 2018 For more information, contact: cdegiulio@atlantaregional.org In Summary

U.S. Investment Outlook

U.S. Investment Outlook Quarterly Investor Research update Q2 2015 U.S. Investment overview 37% 21% 15% 15% U.S. cities dominating global investment activity Top 20 Cities for Transactional Volumes H1

U.S. Investment Outlook Quarterly Investor Research update Q2 2015 U.S. Investment overview 37% 21% 15% 15% U.S. cities dominating global investment activity Top 20 Cities for Transactional Volumes H1

OHIO DEPARTMENT OF TRANSPORTATION CENTRAL OFFICE, 1980 W. Broad St., 4 th Floor, COLUMBUS, OHIO 43223

RAILROAD AUDIT CIRCULAR No. 4V7-Draft OHIO DEPARTMENT OF TRANSPORTATION CENTRAL OFFICE, 1980 W. Broad St., 4 th Floor, COLUMBUS, OHIO 43223 SUBJECT: Subcontracted Costs (DRAFT FOR COMMENT PERIOD 2) Last

RAILROAD AUDIT CIRCULAR No. 4V7-Draft OHIO DEPARTMENT OF TRANSPORTATION CENTRAL OFFICE, 1980 W. Broad St., 4 th Floor, COLUMBUS, OHIO 43223 SUBJECT: Subcontracted Costs (DRAFT FOR COMMENT PERIOD 2) Last

Item No. Adequacy Consideration Adequate Notes

References: CAM 12-200 Section 2 - General Audit Guidance for Termination of Negotiated Contracts CAM 12-300 Section 3 - Auditing Terminations of Fixed-Price Contracts Audit Program 17100 Termination,

References: CAM 12-200 Section 2 - General Audit Guidance for Termination of Negotiated Contracts CAM 12-300 Section 3 - Auditing Terminations of Fixed-Price Contracts Audit Program 17100 Termination,

ODOT Contract Audit Circular No. 1

Definitions, Audit Authority, and Guidance for Computing Overhead Rates Last Updated: April 15, 2008 CONTRACT AUDIT CIRCULAR No. 1 OHIO DEPARTMENT OF TRANSPORTATION CENTRAL OFFICE, 1980 W. Broad St., 4

Definitions, Audit Authority, and Guidance for Computing Overhead Rates Last Updated: April 15, 2008 CONTRACT AUDIT CIRCULAR No. 1 OHIO DEPARTMENT OF TRANSPORTATION CENTRAL OFFICE, 1980 W. Broad St., 4

FOR IMMEDIATE RELEASE Contact: Ann Marie Gorden/Robert Nihen

cutting through complexity News FOR IMMEDIATE RELEASE Contact: Ann Marie Gorden/Robert Nihen June 24, 2014 KPMG LLP 201-505-6288/201-307-8296 agorden@kpmg.com / rnihen@kpmg.com CINCINNATI, CLEVELAND, ATLANTA

cutting through complexity News FOR IMMEDIATE RELEASE Contact: Ann Marie Gorden/Robert Nihen June 24, 2014 KPMG LLP 201-505-6288/201-307-8296 agorden@kpmg.com / rnihen@kpmg.com CINCINNATI, CLEVELAND, ATLANTA

Adequacy of Proposals for. Global Supply Chain

Adequacy of Proposals for Global Supply Chain 1 Adequacy of Proposals Objectives This resource document covers the following: An overview of the proposal process, including applicable FAR (Federal Acquisition

Adequacy of Proposals for Global Supply Chain 1 Adequacy of Proposals Objectives This resource document covers the following: An overview of the proposal process, including applicable FAR (Federal Acquisition

Cost Accounting Standards

Cost Accounting Standards Application of CAS and Modified CAS Coverage September 13, 2016 Agenda Introduction CAS applicability Exceptions to CAS Determining contract value for purposes of CAS Disclosure

Cost Accounting Standards Application of CAS and Modified CAS Coverage September 13, 2016 Agenda Introduction CAS applicability Exceptions to CAS Determining contract value for purposes of CAS Disclosure

Employee Benefits Alert

Employee Benefits Alert September 2005 Issue No. 48 Health Saving Accounts: Comparability Rules The IRS and Treasury recently published proposed regulations concerning the comparability rules for employer

Employee Benefits Alert September 2005 Issue No. 48 Health Saving Accounts: Comparability Rules The IRS and Treasury recently published proposed regulations concerning the comparability rules for employer

Pricing Subcontracts to Win Work and Make a Profit

Pricing Subcontracts to Win Work and Make a Profit Breakout Session C02 Rita L. Wells, PhD Senior Acquisition Executive, Suntiva Deidre A. Lee Consultant Date: Thursday, March 17, 2016 Time: 3:45pm 5:00pm

Pricing Subcontracts to Win Work and Make a Profit Breakout Session C02 Rita L. Wells, PhD Senior Acquisition Executive, Suntiva Deidre A. Lee Consultant Date: Thursday, March 17, 2016 Time: 3:45pm 5:00pm

Understanding the Cost Accounting Standards. Bag Lunch Webinar May 9, 2018

Understanding the Cost Accounting Standards Bag Lunch Webinar May 9, 2018 1 Co-Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager n Tel: 301-214-4137 n pcalabrese@rubino.com

Understanding the Cost Accounting Standards Bag Lunch Webinar May 9, 2018 1 Co-Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager n Tel: 301-214-4137 n pcalabrese@rubino.com

Presented by CohnReznick s Government Contracting Industry Practice. Kristen Soles, CPA, Partner & Kiran Pinto, CPA, Senior Manager

A u d i t R e a d y : A n I n s i d e r s G u i d e t o G o v e r n m e n t C o n t r a c t A u d i t s & C o m p l i a n c e Presented by CohnReznick s Government Contracting Industry Practice Kristen

A u d i t R e a d y : A n I n s i d e r s G u i d e t o G o v e r n m e n t C o n t r a c t A u d i t s & C o m p l i a n c e Presented by CohnReznick s Government Contracting Industry Practice Kristen

equity advisory services

CAPABILITIES equity advisory services YOUR SINGLE POINT OF CONTACT FOR THE ENTIRE CAPITAL STACK Better relationships. Better results. EQUITY VOLUME BY PROPERTY TYPE Our close relationships with debt providers

CAPABILITIES equity advisory services YOUR SINGLE POINT OF CONTACT FOR THE ENTIRE CAPITAL STACK Better relationships. Better results. EQUITY VOLUME BY PROPERTY TYPE Our close relationships with debt providers

Master Document Audit Program. Activity Code Compliance Audit CAS 414 Version 5.20, dated March 2018 B-1 Planning Considerations

Activity Code 19414 Compliance Audit CAS 414 Version 5.20, dated March 2018 B-1 Planning Considerations Type of Service - Attestation Examination Engagement Audit Specific Independence Determination Members

Activity Code 19414 Compliance Audit CAS 414 Version 5.20, dated March 2018 B-1 Planning Considerations Type of Service - Attestation Examination Engagement Audit Specific Independence Determination Members

Virginia Department of Transportation Indirect Cost Rate Submission and Review Process Effective January 1, 2019

Virginia Department of Transportation Indirect Cost Rate Submission and Review Process Effective January 1, 2019 1. Policy, Regulation and Guidance a) In order to ensure that consultant costs reimbursed

Virginia Department of Transportation Indirect Cost Rate Submission and Review Process Effective January 1, 2019 1. Policy, Regulation and Guidance a) In order to ensure that consultant costs reimbursed

Implementation Guidelines for Establishing Service Centers and Recharge Centers Charging Sponsored Projects

Responsible University Official: AVP & Comptroller Responsible Office: Financial Reporting Services Implementation Guidelines for Establishing Service Centers and Recharge Centers Charging Sponsored Projects

Responsible University Official: AVP & Comptroller Responsible Office: Financial Reporting Services Implementation Guidelines for Establishing Service Centers and Recharge Centers Charging Sponsored Projects

equity advisory services

CAPABILITIES equity advisory services YOUR SINGLE POINT OF CONTACT FOR THE ENTIRE CAPITAL STACK Better relationships. Better results. EQUITY VOLUME BY PROPERTY TYPE Our close relationships with debt providers

CAPABILITIES equity advisory services YOUR SINGLE POINT OF CONTACT FOR THE ENTIRE CAPITAL STACK Better relationships. Better results. EQUITY VOLUME BY PROPERTY TYPE Our close relationships with debt providers

Guard Your Investment in Valuable Contracts

Guard Your Investment in Valuable Contracts 1 PRESENTERS Mark Steranka Partner Moss Adams Consulting Robert Gutierrez, CPA, JD Manager Moss Adams Consulting 2 AGENDA Why Audit Contracts Federal Contracts

Guard Your Investment in Valuable Contracts 1 PRESENTERS Mark Steranka Partner Moss Adams Consulting Robert Gutierrez, CPA, JD Manager Moss Adams Consulting 2 AGENDA Why Audit Contracts Federal Contracts

Railroad Audit Circular Training Supplement # 1

ODOT Railroad Audit Circular Attachment 1-1: Sample Overhead Schedule Sample Railroad Company, Inc. Statement of Labor, Fringe Benefits, and Liability Insurance: Maintenance of Way For the Year Ended December

ODOT Railroad Audit Circular Attachment 1-1: Sample Overhead Schedule Sample Railroad Company, Inc. Statement of Labor, Fringe Benefits, and Liability Insurance: Maintenance of Way For the Year Ended December

Proposal Pricing Instructions Page 1 of 7 Supplier Proposal Adequacy Checklist Instructions

Proposal Pricing Instructions Page 1 of 7 Supplier Proposal Adequacy Checklist Instructions Unless a valid exemption applies, Cost or Pricing Data is required to support proposals exceeding $750,000. Contractors

Proposal Pricing Instructions Page 1 of 7 Supplier Proposal Adequacy Checklist Instructions Unless a valid exemption applies, Cost or Pricing Data is required to support proposals exceeding $750,000. Contractors

AUDITING CONSTRUCTION CAPITAL PROJECTS 101

AUDITING CONSTRUCTION CAPITAL PROJECTS 101 January 9, 2018 Adam Rouse Managing Consultant acrouse@bkd.com 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you

AUDITING CONSTRUCTION CAPITAL PROJECTS 101 January 9, 2018 Adam Rouse Managing Consultant acrouse@bkd.com 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you

SPECIALIZED SURETY PRODUCTS

USA SURETY UPDATE FY 2017 A LEADER IN PROVIDING SPECIALIZED SURETY PRODUCTS The Guarantee Company of North America USA Excellence, Expertise, Experience Every time USA Surety Update: 2017 1 TABLE OF CONTENTS

USA SURETY UPDATE FY 2017 A LEADER IN PROVIDING SPECIALIZED SURETY PRODUCTS The Guarantee Company of North America USA Excellence, Expertise, Experience Every time USA Surety Update: 2017 1 TABLE OF CONTENTS

Data Brief. Trends in Employer-Sponsored Health Insurance Premiums and Employee Contributions in Major Metropolitan Areas,

December 2012 Data Brief Trends in Employer-Sponsored Health Insurance Premiums and Employee Contributions in Major Metropolitan Areas, 2003 2011 The mission of The Commonwealth Fund is to promote a high

December 2012 Data Brief Trends in Employer-Sponsored Health Insurance Premiums and Employee Contributions in Major Metropolitan Areas, 2003 2011 The mission of The Commonwealth Fund is to promote a high

Winning Contracts in a Changing Industry. Kristen Soles, CPA, Partner CohnReznick Jacob George, Dir. of Finance Red Team Consulting

Winning Contracts in a Changing Industry Kristen Soles, CPA, Partner CohnReznick Jacob George, Dir. of Finance Red Team Consulting Agenda The Baseline Trends Large, Small & Overall Direct and Indirect

Winning Contracts in a Changing Industry Kristen Soles, CPA, Partner CohnReznick Jacob George, Dir. of Finance Red Team Consulting Agenda The Baseline Trends Large, Small & Overall Direct and Indirect

Copyright Notice. Course Layout & Presentation. Incurred Cost Audits The Process, What to Expect, & How to Survive

Incurred Cost Audits The Process, What to Expect, & How to Survive Presented by Norman J. Lorch, CPA Norman J, Lorch, Copyright Notice The materials presented in this handbook and all of the slides are

Incurred Cost Audits The Process, What to Expect, & How to Survive Presented by Norman J. Lorch, CPA Norman J, Lorch, Copyright Notice The materials presented in this handbook and all of the slides are

PART 31 - CONTRACT COST PRINCIPLES AND PROCEDURES

Appendix 17 - Federal Acquisition Regulation PART 31 - CONTRACT COST PRINCIPLES AND PROCEDURES This appendix contains sections 31.000 to 31.204 of the Federal Acquisition Regulation Section 31 - Contract

Appendix 17 - Federal Acquisition Regulation PART 31 - CONTRACT COST PRINCIPLES AND PROCEDURES This appendix contains sections 31.000 to 31.204 of the Federal Acquisition Regulation Section 31 - Contract

SIGAR JULY. Special Inspector General for Afghanistan Reconstruction

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR Financial Audit 13-6 USDA s Program to Help Advance the Revitalization of Afghanistan s Agricultural Sector: Audit of Costs Incurred

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR Financial Audit 13-6 USDA s Program to Help Advance the Revitalization of Afghanistan s Agricultural Sector: Audit of Costs Incurred

SRC: Cost Policy Statement

Reviewed08/06/2014 SRC: Cost Policy Statement I. General Accounting Policies A. Basis of Accounting - Accrual Basis B. Fiscal Period - January 1 through December 31 C. Allocation Basis for Individual Cost

Reviewed08/06/2014 SRC: Cost Policy Statement I. General Accounting Policies A. Basis of Accounting - Accrual Basis B. Fiscal Period - January 1 through December 31 C. Allocation Basis for Individual Cost

Exploring Unallowable Costs David Eck Mike Mardesich September 22, 2016

Exploring Unallowable Costs David Eck Mike Mardesich September 22, 2016 The Fundamentals of Government Contracting Webinar Series 1 Your Presenters David Eck Dixon Hughes Goodman LLP 214.334.3233 david.eck@dhgllp.com

Exploring Unallowable Costs David Eck Mike Mardesich September 22, 2016 The Fundamentals of Government Contracting Webinar Series 1 Your Presenters David Eck Dixon Hughes Goodman LLP 214.334.3233 david.eck@dhgllp.com

Cost Estimating and Truthful Cost or Pricing Data Requirements

Cost Estimating and Truthful Cost or Pricing Data Requirements Steven M. Masiello Jeremiah J. McIntyre Agenda Cost Estimating FAR cost estimating DFARS cost estimating system rule Government Proposal Analysis

Cost Estimating and Truthful Cost or Pricing Data Requirements Steven M. Masiello Jeremiah J. McIntyre Agenda Cost Estimating FAR cost estimating DFARS cost estimating system rule Government Proposal Analysis

U.S. Department of Housing and Urban Development Office of Housing Counseling

U.S. Department of Housing and Urban Development Office of Housing Counseling Understanding Indirect Cost Rates, De Minimis Rate, and Cost Allocation Plans Booth Management Consulting 7230 Lee Deforest

U.S. Department of Housing and Urban Development Office of Housing Counseling Understanding Indirect Cost Rates, De Minimis Rate, and Cost Allocation Plans Booth Management Consulting 7230 Lee Deforest

AVERAGE HOURLY INCREASES (Including Zero Increases) % 5.1% 3.8%

% 5.1% 3.8%") CCQ Contractor Compensation Quarterly $23.77 is the average hourly rate for Foremen in 2007 Merit Shop Contractors 2007 Merit Shop contractors anticipate skilled craft hourly wage increases of 4.8% in

CCQ Contractor Compensation Quarterly $23.77 is the average hourly rate for Foremen in 2007 Merit Shop Contractors 2007 Merit Shop contractors anticipate skilled craft hourly wage increases of 4.8% in

MY PLAN IS GETTING A REBATE FROM THE INSURER WHAT DO I DO WITH IT?

HUMAN CAPITAL PRACTICE ALERT: HEALTH CARE REFORM BILL August 2012 www.willis.com MY PLAN IS GETTING A REBATE FROM THE INSURER WHAT DO I DO WITH IT? EXECUTIVE SUMMARY All insured employer group medical

HUMAN CAPITAL PRACTICE ALERT: HEALTH CARE REFORM BILL August 2012 www.willis.com MY PLAN IS GETTING A REBATE FROM THE INSURER WHAT DO I DO WITH IT? EXECUTIVE SUMMARY All insured employer group medical

The Consequences of Mortgage Credit Expansion. What is the Nature of the Mortgage Default Crisis?

The Consequences of Mortgage Credit Expansion Atif Mian Amir Sufi University Chicago GSB October 2008 What is the Nature of the Mortgage Default Crisis? 1 Mortgage Defaults, 2005 to 2007 Prime versus Subprime

The Consequences of Mortgage Credit Expansion Atif Mian Amir Sufi University Chicago GSB October 2008 What is the Nature of the Mortgage Default Crisis? 1 Mortgage Defaults, 2005 to 2007 Prime versus Subprime

Understanding Indirect Rates

What Government Contractors Need to Know Understanding Indirect Rates by Robert C. Smith, CPA CEO, ICAT Systems Introduction Indirect Rates can be one of the more confusing accounting concepts for government

What Government Contractors Need to Know Understanding Indirect Rates by Robert C. Smith, CPA CEO, ICAT Systems Introduction Indirect Rates can be one of the more confusing accounting concepts for government

Review Your Accounting System

Review Your Accounting System What to Expect in Government Construction Contracting Presented by: Maria B. Marston, CPA Witt Mares, PLC mmarston@wittmares.com Today s s Areas of Focus Internal corporate

Review Your Accounting System What to Expect in Government Construction Contracting Presented by: Maria B. Marston, CPA Witt Mares, PLC mmarston@wittmares.com Today s s Areas of Focus Internal corporate

Pitfalls Of State And Local Contracting

Pitfalls Of State And Local Contracting Breakout Session #: D16 Mike LaCorte and David Black Date: Tuesday, July 26 Time: 11:15am 12:30pm 1 Mike LaCorte Masters of Science in Taxation Florida Atlantic

Pitfalls Of State And Local Contracting Breakout Session #: D16 Mike LaCorte and David Black Date: Tuesday, July 26 Time: 11:15am 12:30pm 1 Mike LaCorte Masters of Science in Taxation Florida Atlantic

Small. B u s i n e s s, G r o w Y o u r. T o. Y o u M u s t P l a n. f o r G r o w t h

Emerging Businesses: Small T o G r o w Y o u r B u s i n e s s, Y o u M u s t P l a n f o r G r o w t h 18 Contract Management January 2009 Emerging small businesses must plan for growth by ensuring systems

Emerging Businesses: Small T o G r o w Y o u r B u s i n e s s, Y o u M u s t P l a n f o r G r o w t h 18 Contract Management January 2009 Emerging small businesses must plan for growth by ensuring systems

US Hotel Industry Overview. Chris Crenshaw

US Hotel Industry Overview Chris Crenshaw ccrenshaw@str.com July 2014 (12 MMA): All Signs Point To A Sellers Market % Change Room Supply* 1.8 bn 0.8% Room Demand* 1.1 bn 3.4% Occupancy 63 % 2.6% A.D.R.*

US Hotel Industry Overview Chris Crenshaw ccrenshaw@str.com July 2014 (12 MMA): All Signs Point To A Sellers Market % Change Room Supply* 1.8 bn 0.8% Room Demand* 1.1 bn 3.4% Occupancy 63 % 2.6% A.D.R.*

Office. Office. IRR Viewpoint 2015

IRR Viewpoint 05 Above: Designed in 95 in the Art Deco style by architect Timothy Pflueger as the Pacific Telephone and Telegraph Building, 40 New Montgomery Street, San Francisco, CA has been the subject

IRR Viewpoint 05 Above: Designed in 95 in the Art Deco style by architect Timothy Pflueger as the Pacific Telephone and Telegraph Building, 40 New Montgomery Street, San Francisco, CA has been the subject

Europe June Carol Tomé Executive Vice President, Corporate Services & Chief Financial Officer. Diane Dayhoff Vice President, Investor Relations

Europe June 2017 Carol Tomé Executive Vice President, Corporate Services & Chief Financial Officer Diane Dayhoff Vice President, Investor Relations Forward Looking Statements and Non-GAAP Financial Measurements

Europe June 2017 Carol Tomé Executive Vice President, Corporate Services & Chief Financial Officer Diane Dayhoff Vice President, Investor Relations Forward Looking Statements and Non-GAAP Financial Measurements

The Housing Market and the Macroeconomy. Karl E. Case. University of North Carolina February 18, 2010

The Housing Market and the Macroeconomy Karl E. Case University of North Carolina February 18, 2010 Briefly describe some of the connections between the housing market and the Macroeconomy Discuss how

The Housing Market and the Macroeconomy Karl E. Case University of North Carolina February 18, 2010 Briefly describe some of the connections between the housing market and the Macroeconomy Discuss how

FINANCIAL STATEMENTS. The ABC s s of Not-for Financial Reporting

The ABC s s of Not-for for-profit Financial Reporting CAPLAW National Training Conference Minneapolis, Minnesota June 15, 2011 Presented by: Michael A. Zeno, CPA Mary C. Pockl, CPA Wheeling, West Virginia

The ABC s s of Not-for for-profit Financial Reporting CAPLAW National Training Conference Minneapolis, Minnesota June 15, 2011 Presented by: Michael A. Zeno, CPA Mary C. Pockl, CPA Wheeling, West Virginia

VSRA Contract Compliance Seminar August 23, 2011

VSRA Contract Compliance Seminar August 23, 2011 Topics Overview What s new? Defense Federal Acquisition Regulation Supplement; Business Systems Definition and Administration (DFARS Case 2009-D038) Reporting

VSRA Contract Compliance Seminar August 23, 2011 Topics Overview What s new? Defense Federal Acquisition Regulation Supplement; Business Systems Definition and Administration (DFARS Case 2009-D038) Reporting

INDIRECT COSTS COST POLICY STATEMENT (CPS) GUIDANCE

GUIDANCE") INDIRECT COSTS COST POLICY STATEMENT (CPS) GUIDANCE The following is an example of the Cost Policy Statement (CPS) which is required if your organization plans to charge indirect costs to a grant awarded

INDIRECT COSTS COST POLICY STATEMENT (CPS) GUIDANCE The following is an example of the Cost Policy Statement (CPS) which is required if your organization plans to charge indirect costs to a grant awarded

Challenges of Contracting with the Federal Government November 19 th, 2015

Challenges of Contracting with the Federal Government November 19 th, 2015 The Fundamentals of Government Contracting Webinar Series 1 Your Presenters David King Dixon Hughes Goodman, LLP 703.970.0433

Challenges of Contracting with the Federal Government November 19 th, 2015 The Fundamentals of Government Contracting Webinar Series 1 Your Presenters David King Dixon Hughes Goodman, LLP 703.970.0433

Australia/Asia July Diane Dayhoff Vice President, Investor Relations. Lyndsey Burton Senior Manager, Investor Relations

Australia/Asia July 2017 Diane Dayhoff Vice President, Investor Relations Lyndsey Burton Senior Manager, Investor Relations Forward Looking Statements and Non-GAAP Financial Measurements Certain statements

Australia/Asia July 2017 Diane Dayhoff Vice President, Investor Relations Lyndsey Burton Senior Manager, Investor Relations Forward Looking Statements and Non-GAAP Financial Measurements Certain statements