Key to Profitability

|

|

|

- Oswin McBride

- 5 years ago

- Views:

Transcription

1 Key to Profitability Understanding Indirect Cost Allocation Rates Sam Davidson President, GovConConsulting2013, LLC

2 Do you REALLY know what your products or services cost?

3 If You Don t Know What They Cost How do you know what to sell them for?

4 Or if you want to sell them at all!

5 We All Understand Direct Costs Those costs that can be identified specifically with a particular contract, customer order or final cost objective But for cost would not be incurred but for the existence of a specific contract, customer order or final cost objective Anticipated to be recoverable from the customer

6 And Probably Understand Indirect Costs Incurred for the common good of the organization or its employees Benefits more that one contract, customer order or final cost objective Cannot be specifically identified to a particular cost objective Impractical to identify and split

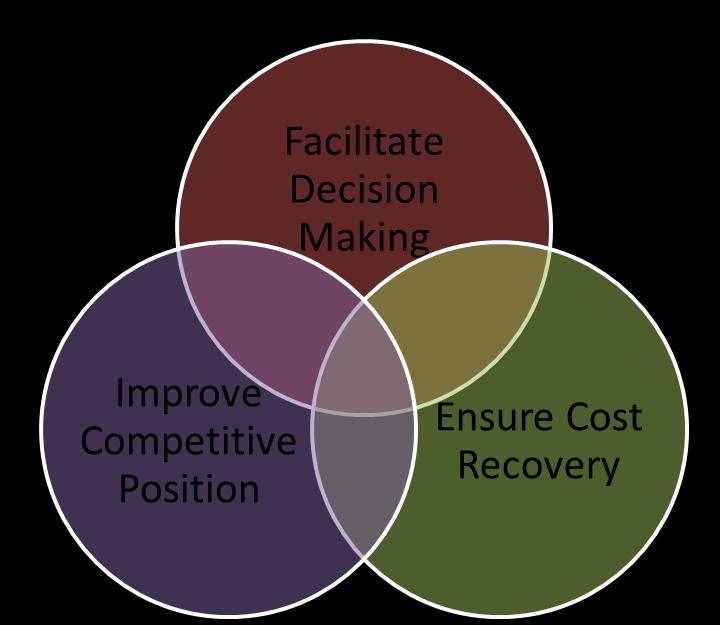

7 Benefits of Comprehensive Indirect Cost Allocation

8 Need For a Thorough Budgeting Process Projecting Costs Associated With: Existing business New business Transom business Planned Changes Personnel Operating changes Organizational changes Economic and Political Impacts

9 Indirect Rate Calculation

10 Homogeneous Cost Pools Costs included in the pool must have a similar beneficial causal relationship to cost objectives Allocation can not be materially different than if the costs were allocated separately Shall include all of the homogeneous indirect costs identified with the activity to which the pool relates

11 Cost Allocation Base Best suited for assigning the particular expense pool to the cost objective (contract, customer order, product or service line, etc.) Must have a cause and effect relationship to the expense pool being allocated Must produce equitable results to all parties involved Must include all expenses (allowable or unallowable)

12 Lifecycle of Indirect Rates

13 Types of Indirect Rates Budget Rates approved internally for management purposes and as a basis for pricing products and/or services Billing, Provisional or Contractual Rates approved by your customer Actual Rates supported by your accounting system and subject to audit

14 Your Indirect Rate Structure Must Your Organization (NOT to be dictated by your accounting software, your customer or by the government)

15 Keep in Mind Regulations do not dictate what costs are to be considered direct or indirect (contract might) Regulations do not dictate how many cost pools you must have More detail generally leads to more accurate allocation of costs

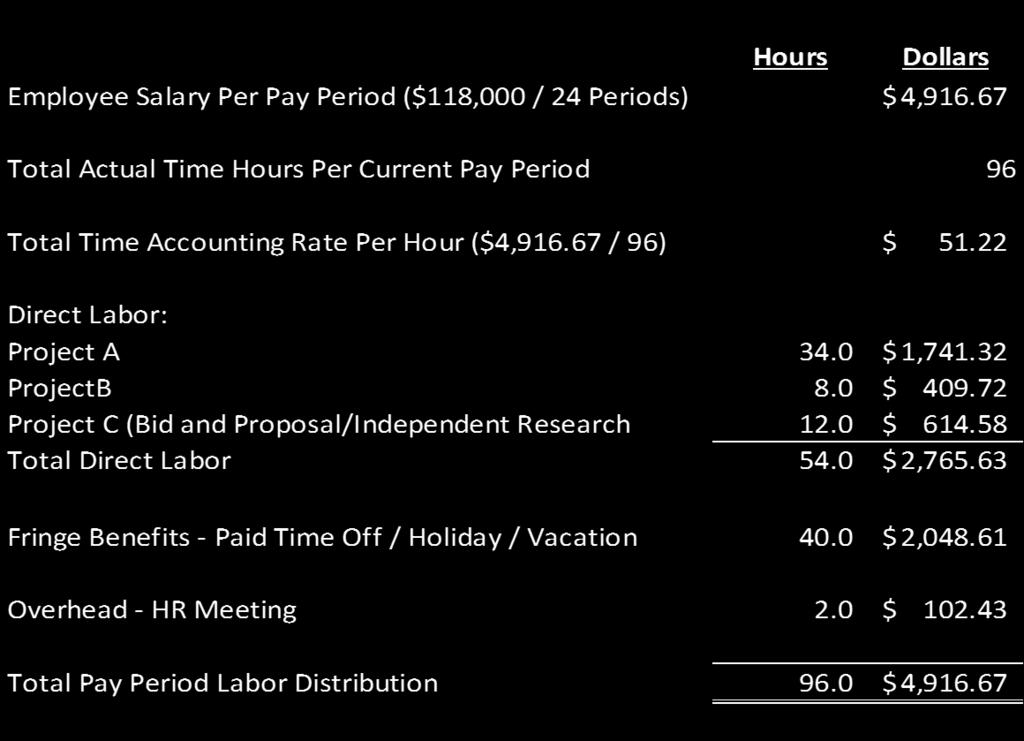

16 Also Keep in Mind Must be able to maintain consistency period to period Less detail leads to more period to period fluctuations in rates Costs are allocated over a fiscal year not a contract performance period Keep it simple easier to understand and audit

17 Accounting for Unallowable Costs Defined in FAR Part 31.2, Contract Cost Principles or in the contract itself Must be excluded from any billing, claim or proposal to the Government (FAR Subpart )

18 Establish an Organized Chart of Accounts Can be anything that fits your organization Make it simple to be able to recognize type of costs included Example: 5000 = Direct Costs 6000 = Fringe Benefit Costs 7000 = Overhead Costs 8000 = General and Administrative Costs 9000 = Unallowable Costs

19 Common Indirect Rate Application

20 Wrap Rate Calculation Defines the needed price for every dollar of direct labor Can be calculated to include or exclude profit Used in quick pricing calculations Allows competitive cost comparison

21 #1 Direct Labor Costs Represents salary or hourly cost per labor hour for An average rate per individual Homogeneous grouping of individuals Average rate for individuals performing similar tasks and with similar qualifications Weighted average rate for individuals performing disparate tasks requiring disparate qualifications as a team

22 Calculation of Standard Rates / Hour

23 Total Time Accounting Utilizes an effective hourly rate vs. a standard hourly rate Effective hourly rate can vary from pay period to pay period Salary amount paid remains constant Hours worked can vary as documented by employees time recording

24 Total Time Accounting (Cont d) Does not include any bonus amounts paid Not required if salary employee is paid for additional hours (salary paid increases to match additional hours) Preferred by DCAA/Required by FAR

25 Labor Cost Per Hour

26 Misallocated Overtime Labor

27 Labor Distribution

28 #2 Fringe Benefits Expenses incurred for the benefit of the employees Apply to both direct and indirect personnel

29 Fringe Costs Fringe Costs include but are not limited to: Employer federal, state and local payroll taxes (FUTA, SUTA, FICA, etc.) Workers compensation Holidays, vacations and sick or lost time Jury duty, military or bereavement Medical, dental and vision Short and log-term disability Pensions Health club dues Tuition Company contributions to 401(k) or 403(b) plans ESOP Stock incentive awards (options) Parking (at facility) Severance Life insurance

30 Fringe Rate Calculation

31 Fringe Benefit Rate Consideration Customize benefits for categories of employees (retirees, part-time, etc.) Benefit packages by division or geographic location Bonuses Yes! No! Maybe! Do they apply equally to all employees Are they a continuing, repetitive costs awarded based on established policy Depending on what impact they have on the rate

32 #3 Operating / Overhead (O/H) Costs Costs associated with assisting direct labor employees in doing their jobs Personnel, machinery, supplies, etc.

33 Operating / Overhead Costs O/H Costs include but are not limited to: Automobile expenses Books and subscriptions Professional memberships Consulting fees Licenses and fees Parking and taxi Professional meetings/seminars Computer supplies Computer equipment and maintenance Training Supporting labor (including applicable fringe benefits) Recruiting Travel expenses (unless an ODC) Depreciation of buildings and equipment Utilities Facility maintenance Overtime premium Office supplies Communications/telephone Postage and shipping

34 O/H Rate Calculation

35 Client-Site vs. Company-Site Not to be confused with on-site and off-site rates Client-site rates do not carry the same level of support Expense pool should be analyzed to determine equitable allocation between the two rates Document rationale used for allocation

36 Client-Site vs. Company-Site

37 Operating / General Overhead Rate Considerations May be pooled or accumulated by Geographic area Product line or service provided Facility Company-site vs. Customer-site Function Assembly, Test, Machining, Installation, Design, etc. Government vs. commercial

38 #4 Selling, General & Administrative Costs associated with the general administration and overall management of the company Not assignable to any one final cost objective

39 SG&A vs. SG/A SG/A Costs include, but are not limited to: Executive management (CEO, COO, CFO, CIO, President, etc.) Finance and accounting Business planning Sales and marketing Information technology Human resources and recruiting Applicable fringe benefits associated with all indirect labor included) Market research Dues and subscriptions Auto expense Board of Directors Stockholder/investor relations Professional fees (legal counsel, accounting firm, management consultants, etc.) Bid and proposal efforts Independent research and development efforts Travel General business insurance Payroll processing Business licenses and fees

40 SG&A vs. SG/A Calculation

41 Total Cost vs. Value-Added Input Allocation Base Total cost input base includes all costs incurred except SG&A Value-added input base only includes those costs that you incurred Not purchased materials or services Not major subcontractor efforts

42 Total Cost vs. Value-Added Input Allocation Base

43 SG&A Rate Alternatives Multiple business unit SG&A rates Business unit specific costs SG&A vs. G&A Each unit has its own G&A rate Some units with total cost input (TCI) allocation bases Some units with value-added allocation bases

44 More SG&A Rate Alternatives Create a home office expense pool to be charged/allocated to the segments Direct charge Surrogate allocation (e.g., headcount, square feet, etc.) Three-factor formula Composite allocation of RESIDUAL costs based on Average Net Book Value of Assets, Payroll and Revenue

45 Material Handling Rate Costs incurred in the overall administration of materials acquisition and utilization Includes, but not limited to: Purchasing (vendor selection, negotiation and management of purchase orders) Stockroom and stocking Warehouse facility costs Material movement/handling Receiving and inspection/quality control Incoming freight costs Segregates material handling costs from the overhead cost pool Lowers the overhead rate Allocates overhead costs applicable to material only Must remain in the allocation base for SG&A

46 Major Subcontracts Rate Subcontracted efforts to support direct contract performance Includes, but not limited to: Subcontractor selection and negotiation Contract management Technical evaluation and monitoring Performance management Contract reporting Removes subcontracted efforts from the SG&A allocation base Removes applicable support expenses contained in the SG&A expense pool Provides a lower adder to subcontract efforts than the full SG&A rate SG&A rate will increase on all other efforts

47 Other Direct Costs (ODC s) Direct items generally not defined in the contract SOW In addition to direct labor and material Includes such items as: airfares, lodging and subsistence, mileage, relocation costs, schooling tuition allowances, shipping costs, freight costs, storage fees, etc. Gov t. sometimes provides fixed amount to level the proposal playing field

48 Utilize Service Centers Easier way to account for common indirect costs Manage costs between benefiting indirect cost pools Common examples include facilities, IT, telephone, communications, accounting, HR, administration, etc.

49 Utilize Service Centers (Cont d) Allocated based on surrogate (e.g., square footage, headcount, usage, etc.) All costs allocated out by end of accounting period = zero balance

50 Job Cost Ledger

51 Rate Variance Analysis

52 Difference Between Cost vs. Price Cost = Facts Price = Reality

53 Profit on Cost-Type Government Contracts Experimental, development and research contracts limited to 15% of cost Architect and engineering services contracts limited to 6% of estimated cost of construction All other cost-type contracts limited to 10% of cost NO percentage of cost contracts

54 Profit on Fixed-Price Government Contracts Unlimited profit level taking into consideration Contractor efforts Cost risk Socio-economic directives Capital investment Cost control and other past accomplishments Independent development efforts Additional factors Use of Weighted Guidelines for negotiation

55 Profit on Commercial Contracts Sky is the Limit! Subject to COMPETITION!

56 Questions?

303-2701 Visit www.pbmares.")

57 Contact Sam Davidson GovConConsulting2013, LLC Phone: (703) Visit to read our blog and learn of upcoming events.

Contract Pricing Reference Guides Volume 3 Chapter 9 Analysis of Indirect Costs

Contract Pricing Reference Guides Volume 3 Chapter 9 Analysis of Indirect Costs 9.0 - Chapter Introduction 9.1 - Identifying Pools And Bases For Rate Development o 9.1.1 - Identifying Indirect Cost Pools

Contract Pricing Reference Guides Volume 3 Chapter 9 Analysis of Indirect Costs 9.0 - Chapter Introduction 9.1 - Identifying Pools And Bases For Rate Development o 9.1.1 - Identifying Indirect Cost Pools

Navigating the Indirect Cost Rate Maze. Chad Braley Marie Salamone

Navigating the Indirect Cost Rate Maze Chad Braley Marie Salamone Value Proposition Capital Edge is the country s largest independent consulting firm focusing solely on the U.S. Government contracting

Navigating the Indirect Cost Rate Maze Chad Braley Marie Salamone Value Proposition Capital Edge is the country s largest independent consulting firm focusing solely on the U.S. Government contracting

Indirect Cost Recovery: What You Need to Consider. August 2017

Indirect Cost Recovery: What You Need to Consider August 2017 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee,

Indirect Cost Recovery: What You Need to Consider August 2017 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee,

Railroad Audit Circular Training Supplement # 1

ODOT Railroad Audit Circular Attachment 1-1: Sample Overhead Schedule Sample Railroad Company, Inc. Statement of Labor, Fringe Benefits, and Liability Insurance: Maintenance of Way For the Year Ended December

ODOT Railroad Audit Circular Attachment 1-1: Sample Overhead Schedule Sample Railroad Company, Inc. Statement of Labor, Fringe Benefits, and Liability Insurance: Maintenance of Way For the Year Ended December

Capital Area Council of Governments FY 2018 Cost Policy Statement and Cost Allocation Plan

Capital Area Council of Governments FY 2018 Cost Policy Statement and Cost Allocation Plan The Capital Area Council of Governments uses the cost allocation method prescribed in OMB Uniform Administrative

Capital Area Council of Governments FY 2018 Cost Policy Statement and Cost Allocation Plan The Capital Area Council of Governments uses the cost allocation method prescribed in OMB Uniform Administrative

VIP Presents. Indirect Rates What you need to know!

VIP Presents Indirect Rates What you need to know! The VIP Program Accelerating the Growth of Veteran Owned Small Businesses in the Federal Marketplace Powered By 971 Graduates and Growing From 45 States,

VIP Presents Indirect Rates What you need to know! The VIP Program Accelerating the Growth of Veteran Owned Small Businesses in the Federal Marketplace Powered By 971 Graduates and Growing From 45 States,

GCS 224 Surviving DCAA Audits with GCS Premier. Presented by: Nicole Mitchell, Aronson & Company

GCS 224 Surviving DCAA Audits with GCS Premier Presented by: Nicole Mitchell, Aronson & Company Agenda Government Contract Audits and the Role of DCAA and DCMA Basic Attributes of a Government Approved

GCS 224 Surviving DCAA Audits with GCS Premier Presented by: Nicole Mitchell, Aronson & Company Agenda Government Contract Audits and the Role of DCAA and DCMA Basic Attributes of a Government Approved

Capital Area Council of Governments FY 2019 Cost Policy Statement and Cost Allocation Plan

Capital Area Council of Governments FY 2019 Cost Policy Statement and Cost Allocation Plan The Capital Area Council of Governments uses the cost allocation method prescribed in OMB Uniform Administrative

Capital Area Council of Governments FY 2019 Cost Policy Statement and Cost Allocation Plan The Capital Area Council of Governments uses the cost allocation method prescribed in OMB Uniform Administrative

International Dark-Sky Association Cost Allocation Plan

International Dark-Sky Association Cost Allocation Plan Adopted 15 September 2014 1 Purpose The purpose of the cost allocation plan is to summarize, in writing, the methods and procedures that this International

International Dark-Sky Association Cost Allocation Plan Adopted 15 September 2014 1 Purpose The purpose of the cost allocation plan is to summarize, in writing, the methods and procedures that this International

OHIO DEPARTMENT OF TRANSPORTATION CENTRAL OFFICE, 1980 W. Broad St., 4 th Floor, COLUMBUS, OHIO 43223

RAILROAD AUDIT CIRCULAR No. 4V7-Draft OHIO DEPARTMENT OF TRANSPORTATION CENTRAL OFFICE, 1980 W. Broad St., 4 th Floor, COLUMBUS, OHIO 43223 SUBJECT: Subcontracted Costs (DRAFT FOR COMMENT PERIOD 2) Last

RAILROAD AUDIT CIRCULAR No. 4V7-Draft OHIO DEPARTMENT OF TRANSPORTATION CENTRAL OFFICE, 1980 W. Broad St., 4 th Floor, COLUMBUS, OHIO 43223 SUBJECT: Subcontracted Costs (DRAFT FOR COMMENT PERIOD 2) Last

Howland Tax Services

Howland Tax Services 2007 Self-Employment Checklist (United States) What is your main product or service? Name of business Business address Fiscal year end (usually Dec. 31) Do you use the Cash or Accrual

Howland Tax Services 2007 Self-Employment Checklist (United States) What is your main product or service? Name of business Business address Fiscal year end (usually Dec. 31) Do you use the Cash or Accrual

CAS - Part II. The Cost Allocation Standards Dixon Hughes Goodman, LLP

CAS - Part II The Cost Allocation Standards 1 Agenda Session I Administration: CAS Overview Applicability Types of Coverage CAS Administration Part II - The Cost Allocation Standards Part III - The Cost

CAS - Part II The Cost Allocation Standards 1 Agenda Session I Administration: CAS Overview Applicability Types of Coverage CAS Administration Part II - The Cost Allocation Standards Part III - The Cost

Howland Tax Services International

Howland Tax Services International 2010 Self-Employment Checklist (United States) Identification What is your main product or service? Name of business Business address Fiscal year end (usually Dec. 31)

Howland Tax Services International 2010 Self-Employment Checklist (United States) Identification What is your main product or service? Name of business Business address Fiscal year end (usually Dec. 31)

AIA 2017 Compensation Survey Survey Questions

Contact Info AIA 2017 Compensation Survey Survey Questions Contact Info *1. I currently work for a firm that has at least 1 domestic office with 3 or more architecture, at least 1 of whom is full-time.

Contact Info AIA 2017 Compensation Survey Survey Questions Contact Info *1. I currently work for a firm that has at least 1 domestic office with 3 or more architecture, at least 1 of whom is full-time.

Government Contracts Pricing Strategies and Rate Structures

Government Contracts Pricing Strategies and Rate Structures Presented By: Brandon Smith bsmith@anglincpa.com Jon Levin jlevin@maynardcooper.com Provisional Billing Rates Provisional, Target, Budget, Billing,

Government Contracts Pricing Strategies and Rate Structures Presented By: Brandon Smith bsmith@anglincpa.com Jon Levin jlevin@maynardcooper.com Provisional Billing Rates Provisional, Target, Budget, Billing,

City of Cleveland Professional Services Contracts Reimbursables Policy 01/01/2014

City of Cleveland Professional Services Contracts Reimbursables Policy 01/01/2014 The following constitutes the City of Cleveland s Reimbursables policies to be used in the City s Professional Services

City of Cleveland Professional Services Contracts Reimbursables Policy 01/01/2014 The following constitutes the City of Cleveland s Reimbursables policies to be used in the City s Professional Services

N o w h e r e t o R u n, N o w h e r e t o H i d e : D i s c l o s u r e S t a t e m e n t s a n d C o s t A c c o u n t i n g S t a n d a r d s

N o w h e r e t o R u n, N o w h e r e t o H i d e : D i s c l o s u r e S t a t e m e n t s a n d C o s t A c c o u n t i n g S t a n d a r d s Presented by Darrell Hineman, CPA, CFE, Director Jeff Shapiro,

N o w h e r e t o R u n, N o w h e r e t o H i d e : D i s c l o s u r e S t a t e m e n t s a n d C o s t A c c o u n t i n g S t a n d a r d s Presented by Darrell Hineman, CPA, CFE, Director Jeff Shapiro,

Indirect Cost Rates For Nonprofit Organizations

Indirect Cost Rates For Nonprofit Organizations Bag Lunch Webinar October 10, 2012 All slides and handouts copyright 2012, Rubino & Company, Chartered Presenter: Paul H. Calabrese Rubino & Company, CPAs

Indirect Cost Rates For Nonprofit Organizations Bag Lunch Webinar October 10, 2012 All slides and handouts copyright 2012, Rubino & Company, Chartered Presenter: Paul H. Calabrese Rubino & Company, CPAs

FLORIDA DEPARTMENT OF ECONOMIC OPPORTUNITY WEATHERIZATION ASSISTANCE PROGRAM

FLORIDA DEPARTMENT OF ECONOMIC OPPORTUNITY WEATHERIZATION ASSISTANCE PROGRAM NON-PROFIT GUIDANCE FOR DOCUMENTATION AND SUPPORT OF PROGRAM SUPPORT AND ADMINISTRATION EXPENDITURES Version 1 March 2013 NON-PROFIT

FLORIDA DEPARTMENT OF ECONOMIC OPPORTUNITY WEATHERIZATION ASSISTANCE PROGRAM NON-PROFIT GUIDANCE FOR DOCUMENTATION AND SUPPORT OF PROGRAM SUPPORT AND ADMINISTRATION EXPENDITURES Version 1 March 2013 NON-PROFIT

SAMPLE ORGANIZATION Model Cost Allocation Plan

SAMPLE ORGANIZATION Model Cost Allocation Plan Use the following model Cost Allocation Plan (CAP) as guidance for Non-profit organizations. The CAP should be tailored to fit the specific policies of each

SAMPLE ORGANIZATION Model Cost Allocation Plan Use the following model Cost Allocation Plan (CAP) as guidance for Non-profit organizations. The CAP should be tailored to fit the specific policies of each

Community Partnerships Program Eligible Costing Rules and Financial Management Guidelines

Community Partnerships Program Eligible Costing Rules and Financial Management Guidelines Top tips when preparing your budget... 2 What are eligible costs?... 3 I. Personnel, Payroll and other Compensation...

Community Partnerships Program Eligible Costing Rules and Financial Management Guidelines Top tips when preparing your budget... 2 What are eligible costs?... 3 I. Personnel, Payroll and other Compensation...

Cost Allocation Plan

Cost Allocation Plan Western States Air Resources Council (WESTAR) 1218 3 rd Avenue, Suite 1518 Seattle, WA Contact Person: Dan Johnson, Executive Director Email: djohnson@westar.org A. INTRODUCTION The

Cost Allocation Plan Western States Air Resources Council (WESTAR) 1218 3 rd Avenue, Suite 1518 Seattle, WA Contact Person: Dan Johnson, Executive Director Email: djohnson@westar.org A. INTRODUCTION The

INDIRECT COSTS COST POLICY STATEMENT (CPS) GUIDANCE

GUIDANCE") INDIRECT COSTS COST POLICY STATEMENT (CPS) GUIDANCE The following is an example of the Cost Policy Statement (CPS) which is required if your organization plans to charge indirect costs to a grant awarded

INDIRECT COSTS COST POLICY STATEMENT (CPS) GUIDANCE The following is an example of the Cost Policy Statement (CPS) which is required if your organization plans to charge indirect costs to a grant awarded

Indirect Rates the Basics In Deltek GCS Premier

Indirect Rates the Basics In Deltek GCS Premier COPYRIGHT INFORMATION While NeoSystems has made every attempt to ensure the accuracy of these materials, some errors may exist. NeoSystems is not responsible

Indirect Rates the Basics In Deltek GCS Premier COPYRIGHT INFORMATION While NeoSystems has made every attempt to ensure the accuracy of these materials, some errors may exist. NeoSystems is not responsible

A Guide for Contractors

CFO S TOOLBOX BY KEITH R. FETRIDGE What Is Job Cost? A Guide for Contractors After 20 years of working with hundreds of different contractors, the one question I always hear is: What should be charged

CFO S TOOLBOX BY KEITH R. FETRIDGE What Is Job Cost? A Guide for Contractors After 20 years of working with hundreds of different contractors, the one question I always hear is: What should be charged

Earnings and Deductions Quick Reference

Earnings and Deductions Quick Reference The Earnings and Deductions Quick Reference includes a complete list of the earnings and deductions that are provided in the payroll application. For details on

Earnings and Deductions Quick Reference The Earnings and Deductions Quick Reference includes a complete list of the earnings and deductions that are provided in the payroll application. For details on

Pricing for Services

Pricing for Services 1. Introduction This aid discusses costing and pricing of services to assure that each job earns a reasonable profit. The figures used in the tables and examples do not reflect what

Pricing for Services 1. Introduction This aid discusses costing and pricing of services to assure that each job earns a reasonable profit. The figures used in the tables and examples do not reflect what

F i v e C A S S t a n d a r d s E v e r y G o v e r n m e n t C o n t r a c t o r S h o u l d K n o w a n d F o l l o w

F i v e C A S S t a n d a r d s E v e r y G o v e r n m e n t C o n t r a c t o r S h o u l d K n o w a n d F o l l o w December 17, 2015 Presented by: Darrell Hineman, CPA CFE Director Long Nguyen, CFE

F i v e C A S S t a n d a r d s E v e r y G o v e r n m e n t C o n t r a c t o r S h o u l d K n o w a n d F o l l o w December 17, 2015 Presented by: Darrell Hineman, CPA CFE Director Long Nguyen, CFE

Rocco Sabino MBA, CPA

Rocco Sabino MBA, CPA Rocco.Sabino@Stonybrook.edu Agenda: I. Understanding Financial Information Ø Financial Statements q Income Statement It s all about earning income How does Human Resource (HR) affect

Rocco Sabino MBA, CPA Rocco.Sabino@Stonybrook.edu Agenda: I. Understanding Financial Information Ø Financial Statements q Income Statement It s all about earning income How does Human Resource (HR) affect

Eligible Costing Rules and Financial Management Guidelines

TOP TIPS Alberta Wildfires 2016: Community Organization Partnerships Program Eligible Costing Rules and Financial Management Guidelines WHEN PREPARING YOUR BUDGET For each Budget Category a non-exhaustive

TOP TIPS Alberta Wildfires 2016: Community Organization Partnerships Program Eligible Costing Rules and Financial Management Guidelines WHEN PREPARING YOUR BUDGET For each Budget Category a non-exhaustive

GOVERNMENT CONTRACTING

A GUIDE TO INDIRECT COST RATES IN GOVERNMENT CONTRACTING www.ryansharkey.com TABLE OF CONTENTS Overview Direct vs. Indirect Costs... 3 What are Indirect Rates?... 4 Calculation of Indirect Rates and Impact

A GUIDE TO INDIRECT COST RATES IN GOVERNMENT CONTRACTING www.ryansharkey.com TABLE OF CONTENTS Overview Direct vs. Indirect Costs... 3 What are Indirect Rates?... 4 Calculation of Indirect Rates and Impact

Copyright 2016 INSIDE Public Accounting THE 2016 / INSIDE PUBLIC ACCOUNTING SURVEY & ANALYSIS OF FIRMS

Copyright 2016 THE 2016 / INSIDE PUBLIC ACCOUNTING SURVEY & ANALYSIS OF FIRMS 39-43 Mergers / Acquisitions Do not include lateral hires, professional staff or partners that were hired from another firm

Copyright 2016 THE 2016 / INSIDE PUBLIC ACCOUNTING SURVEY & ANALYSIS OF FIRMS 39-43 Mergers / Acquisitions Do not include lateral hires, professional staff or partners that were hired from another firm

Howland Tax Services

Howland Tax Services 2007 Musician s Checklist (United States) Business name and address (Your name if you don t have a separate business name) Do you use the Cash or Accrual method of accounting? Cash

Howland Tax Services 2007 Musician s Checklist (United States) Business name and address (Your name if you don t have a separate business name) Do you use the Cash or Accrual method of accounting? Cash

Terms. Write down as many payroll terms or payroll taxes that you can think of in 2 minutes. Ready, Set, Go!

Payroll Unit Terms Write down as many payroll terms or payroll taxes that you can think of in 2 minutes. Ready, Set, Go! Payroll Pay Periods Weekly 52 checks a year Biweekly 26 checks a year, every other

Payroll Unit Terms Write down as many payroll terms or payroll taxes that you can think of in 2 minutes. Ready, Set, Go! Payroll Pay Periods Weekly 52 checks a year Biweekly 26 checks a year, every other

Administrative Procedure

Division of Finance and Administration AP F&A-02 Administrative Procedure Title: Responsible Office: Adopted: June 1, 2017 Revised: Effective: June 1, 2017 Indirect Cost Rate Instructions for DEO Subrecipients

Division of Finance and Administration AP F&A-02 Administrative Procedure Title: Responsible Office: Adopted: June 1, 2017 Revised: Effective: June 1, 2017 Indirect Cost Rate Instructions for DEO Subrecipients

U.S. Department of Housing and Urban Development Office of Housing Counseling

U.S. Department of Housing and Urban Development Office of Housing Counseling Understanding Indirect Cost Rates, De Minimis Rate, and Cost Allocation Plans Booth Management Consulting 7230 Lee Deforest

U.S. Department of Housing and Urban Development Office of Housing Counseling Understanding Indirect Cost Rates, De Minimis Rate, and Cost Allocation Plans Booth Management Consulting 7230 Lee Deforest

Attachment 17 RTD Pricing Conditions

Attachment 17 RTD Pricing Conditions 1. General conditions Incurred Costs may be claimed by the Concessionaire under this Agreement only to the extent such Incurred Costs have been incurred in compliance

Attachment 17 RTD Pricing Conditions 1. General conditions Incurred Costs may be claimed by the Concessionaire under this Agreement only to the extent such Incurred Costs have been incurred in compliance

U.S. Department of Housing & Urban Development

U.S. Department of Housing & Urban Development OFFICE OF HOUSING COUNSELING Understanding Billing Methodologies Based on the Cost Principles Required by the Uniform Grant Guidance, 2 CFR Part 200, Subpart

U.S. Department of Housing & Urban Development OFFICE OF HOUSING COUNSELING Understanding Billing Methodologies Based on the Cost Principles Required by the Uniform Grant Guidance, 2 CFR Part 200, Subpart

Bulletin on Payment of Consultant Fees

Bulletin on Payment of Consultant Fees January 22, 2018 Contents Page I. General Information... 3 II. Payment of Services... 5 III. Reimbursable Expenses... 7 IV. Subconsultant Payment Reporting... 13

Bulletin on Payment of Consultant Fees January 22, 2018 Contents Page I. General Information... 3 II. Payment of Services... 5 III. Reimbursable Expenses... 7 IV. Subconsultant Payment Reporting... 13

PANEL E: Costly Mistakes!

PANEL E: Costly Mistakes! How to avoid the most common pitfalls that face a growing company. Lessons learned from an operational and legal perspective that may help you make money and stay out of jail!

PANEL E: Costly Mistakes! How to avoid the most common pitfalls that face a growing company. Lessons learned from an operational and legal perspective that may help you make money and stay out of jail!

Cost Allocation Manual

Page 1 of 19 Black Hills Service Company Cost Allocation Manual Effective Date: July 14, 2008 Amended: January 1, 2010 Amended: August 1, 2010 Page 2 of 19 Black Hills Service Company Cost Allocation Manual

Page 1 of 19 Black Hills Service Company Cost Allocation Manual Effective Date: July 14, 2008 Amended: January 1, 2010 Amended: August 1, 2010 Page 2 of 19 Black Hills Service Company Cost Allocation Manual

EXHIBIT D DEPARTMENT PAYMENT PROCESS / VOUCHERS (CHAPTER 7)

") EXHIBIT D DEPARTMENT PAYMENT PROCESS / VOUCHERS (CHAPTER 7) 7-1 CHAPTER 7 PAYMENT PROCESS/ VOUCHERS CHAPTER 7 - PAYMENT PROCESS / VOUCHER 7.10 Voucher Instructions After written notice to proceed is given,

EXHIBIT D DEPARTMENT PAYMENT PROCESS / VOUCHERS (CHAPTER 7) 7-1 CHAPTER 7 PAYMENT PROCESS/ VOUCHERS CHAPTER 7 - PAYMENT PROCESS / VOUCHER 7.10 Voucher Instructions After written notice to proceed is given,

Activity Code Compliance Audit CAS 403 Version 6.23, dated March 2018 B-1 Planning Considerations

Activity Code 19403 Compliance Audit CAS 403 B-1 Planning Considerations Type of Service - Attestation Examination Engagement Audit Specific Independence Determination Members of the audit team and internal

Activity Code 19403 Compliance Audit CAS 403 B-1 Planning Considerations Type of Service - Attestation Examination Engagement Audit Specific Independence Determination Members of the audit team and internal

Change Order Guidelines

Change Order Guidelines ELECTRI International Prof. Matt Syal, Ph.D. Joseph Diffendal Daniel Duah, Ph.D. Construction Management School of Planning, Design and Construction Michigan State University 1

Change Order Guidelines ELECTRI International Prof. Matt Syal, Ph.D. Joseph Diffendal Daniel Duah, Ph.D. Construction Management School of Planning, Design and Construction Michigan State University 1

SRC: Cost Policy Statement

Reviewed08/06/2014 SRC: Cost Policy Statement I. General Accounting Policies A. Basis of Accounting - Accrual Basis B. Fiscal Period - January 1 through December 31 C. Allocation Basis for Individual Cost

Reviewed08/06/2014 SRC: Cost Policy Statement I. General Accounting Policies A. Basis of Accounting - Accrual Basis B. Fiscal Period - January 1 through December 31 C. Allocation Basis for Individual Cost

Review Your Accounting System

Review Your Accounting System What to Expect in Government Construction Contracting Presented by: Maria B. Marston, CPA Witt Mares, PLC mmarston@wittmares.com Today s s Areas of Focus Internal corporate

Review Your Accounting System What to Expect in Government Construction Contracting Presented by: Maria B. Marston, CPA Witt Mares, PLC mmarston@wittmares.com Today s s Areas of Focus Internal corporate

Kallenz. S Corporation Tax Organizer

Kallenz S Corporation Tax Organizer The S Corporation Tax Organizer has been designed to help collect and organize the information that we will need to prepare your business income tax returns in the most

Kallenz S Corporation Tax Organizer The S Corporation Tax Organizer has been designed to help collect and organize the information that we will need to prepare your business income tax returns in the most

Federal Grant Administration Guidelines

Federal Grant Administration Guidelines The following documents internal controls that are required to be in writing for federal grants in accordance with the Uniform Administrative Requirements, Cost

Federal Grant Administration Guidelines The following documents internal controls that are required to be in writing for federal grants in accordance with the Uniform Administrative Requirements, Cost

JOHNS HOPKINS UNIVERSITY COST ACCOUNTING STANDARDS BOARD DISCLOSURE STATEMENT FOR EDUCATIONAL INSTITUTIONS CASB DS-2

COST ACCOUNTING STANDARDS BOARD FOR CASB DS-2 March 23, 2010 INDEX JOHNS HOPKINS UNIVERISTY GENERAL INSTRUCTIONS... Continuation Sheet... i COVER SHEET AND CERTIFICATION...... ii PART I... General Information...

COST ACCOUNTING STANDARDS BOARD FOR CASB DS-2 March 23, 2010 INDEX JOHNS HOPKINS UNIVERISTY GENERAL INSTRUCTIONS... Continuation Sheet... i COVER SHEET AND CERTIFICATION...... ii PART I... General Information...

ONR Guidance for Indirect Cost Rate Proposals for Non-Profits with less than $10M Federal Funding of Direct Costs in a Fiscal Year

ONR Guidance for Indirect Cost Rate Proposals for Non-Profits with less than $10M Funding of Direct Costs in a Fiscal Year A non-profit organization will submit an indirect cost rate proposal primarily

ONR Guidance for Indirect Cost Rate Proposals for Non-Profits with less than $10M Funding of Direct Costs in a Fiscal Year A non-profit organization will submit an indirect cost rate proposal primarily

2017 Small-Business Tax Prep Checklist

220 S. 4th Street Elkhart, IN 46516 Phone 574-298-1634 or 574-849-0788 2017 Small-Business Tax Prep Checklist If you are using QuickBooks or some other form of accounting software, we will need either

220 S. 4th Street Elkhart, IN 46516 Phone 574-298-1634 or 574-849-0788 2017 Small-Business Tax Prep Checklist If you are using QuickBooks or some other form of accounting software, we will need either

ONR SUBMISSION REQUIREMENTS FOR NONPROFIT INDIRECT COST RATE PROPOSALS - INITIAL CHECKLIST

ONR SUBMISSION REQUIREMENTS FOR NONPROFIT INDIRECT COST RATE PROPOSALS - INITIAL CHECKLIST 1. Transmittal Letter: State the type of rate requested (e.g. predetermined, fixed, provisional, or final) and

ONR SUBMISSION REQUIREMENTS FOR NONPROFIT INDIRECT COST RATE PROPOSALS - INITIAL CHECKLIST 1. Transmittal Letter: State the type of rate requested (e.g. predetermined, fixed, provisional, or final) and

PART I - GENERAL INFORMATION No. Description Part I 1.1.0 Description of Your Cost Accounting System for recording expenses charged to Federally sponsored agreements (e.g. contracts, grants and cooperative

PART I - GENERAL INFORMATION No. Description Part I 1.1.0 Description of Your Cost Accounting System for recording expenses charged to Federally sponsored agreements (e.g. contracts, grants and cooperative

Self Employment Income & Single Member LLC Organizer This Organizer belongs to:

This self-employment organizer will assist you with organization of your business information and records. The IRS imposes reporting and record-keeping rules, some of which are described in this Organizer.

This self-employment organizer will assist you with organization of your business information and records. The IRS imposes reporting and record-keeping rules, some of which are described in this Organizer.

Introduction to the Cost Accounting Standards Mike Mardesich & Brad Tress April 25, 2017

Introduction to the Cost Accounting Standards Mike Mardesich & Brad Tress April 25, 2017 The Fundamentals of Government Contracting Webinar Series 1 Your Presenters Mike Mardesich Dixon Hughes Goodman

Introduction to the Cost Accounting Standards Mike Mardesich & Brad Tress April 25, 2017 The Fundamentals of Government Contracting Webinar Series 1 Your Presenters Mike Mardesich Dixon Hughes Goodman

Self Employment Income & Single Member LLC Organizer This Organizer belongs to:

Self Employment Income & Single Member LLC Organizer This Organizer belongs to: This self-employment organizer will assist you with organization of your business information and records. The IRS imposes

Self Employment Income & Single Member LLC Organizer This Organizer belongs to: This self-employment organizer will assist you with organization of your business information and records. The IRS imposes

ODOT Railroad Audit Circular No. 1

Definitions, Audit Authority, and Guidance for Computing Overhead Rates for Railroads Release Date: January 1, 2010 Application: Unless and until revised by ODOT, this Circular is effective for actual

Definitions, Audit Authority, and Guidance for Computing Overhead Rates for Railroads Release Date: January 1, 2010 Application: Unless and until revised by ODOT, this Circular is effective for actual

ICANN Staff Remuneration Practices FY2017 (1 July 2016 through 30 June 2017) As of 1 July 2016

As of 1 July 2016") ICANN Staff Remuneration Practices FY2017 (1 July 2016 through 30 June 2017) As of 1 July 2016 The overarching objective of ICANN s remuneration framework is to ensure remuneration provided is competitive

ICANN Staff Remuneration Practices FY2017 (1 July 2016 through 30 June 2017) As of 1 July 2016 The overarching objective of ICANN s remuneration framework is to ensure remuneration provided is competitive

UNIVERSITY OF UTAH COST ACCOUNTING STANDARDS DISCLOSURE STATEMENT

UNIVERSITY OF UTAH COST ACCOUNTING STANDARDS DISCLOSURE STATEMENT COVERSHEET AND CERTIFICATION 0.1 Educational Institution (a) Name UNIVERSITY OF UTAH (b) Street Address 201 S PRESIDENTS CIRCLE RM 408

UNIVERSITY OF UTAH COST ACCOUNTING STANDARDS DISCLOSURE STATEMENT COVERSHEET AND CERTIFICATION 0.1 Educational Institution (a) Name UNIVERSITY OF UTAH (b) Street Address 201 S PRESIDENTS CIRCLE RM 408

The topic of government contract cost accounting is one

The topic of government contract cost accounting is one that is distinguished from accounting for commercial contracts. Not surprisingly, there are requirements unique to U.S. government contracts. Most

The topic of government contract cost accounting is one that is distinguished from accounting for commercial contracts. Not surprisingly, there are requirements unique to U.S. government contracts. Most

Using GCS to Drive Decision Making Susan Smith, WJ Technologies Antoinette Merrill, Summit Consulting

GCS Premier It s Not Just A History Lesson Using GCS to Drive Decision Making Susan Smith, WJ Technologies Antoinette Merrill, Summit Consulting GCS Premier It s Not Just A History Lesson Objective: To

GCS Premier It s Not Just A History Lesson Using GCS to Drive Decision Making Susan Smith, WJ Technologies Antoinette Merrill, Summit Consulting GCS Premier It s Not Just A History Lesson Objective: To

Change Order Guidelines: Quick Reference

ELECTRI International The Foundation for Electrical Construction, Inc. PRODUCTIVITY ENHANCEMENT Change Order Guidelines: Quick Reference ELECTRI International 3 Bethesda Metro Center, Suite 1100 Bethesda,

ELECTRI International The Foundation for Electrical Construction, Inc. PRODUCTIVITY ENHANCEMENT Change Order Guidelines: Quick Reference ELECTRI International 3 Bethesda Metro Center, Suite 1100 Bethesda,

1 Exam Prep Business and Finance Practice Test 5

1 Exam Prep Business and Finance Practice Test 5 1. According to Builder's Guide to Accounting, the most precise ratio used to judge whether the level of the inventory is correct for the volume of work

1 Exam Prep Business and Finance Practice Test 5 1. According to Builder's Guide to Accounting, the most precise ratio used to judge whether the level of the inventory is correct for the volume of work

S-Corporation: EIN Name Date Incorporated Date of S-Election Address: Mailing Address Suite # City State Zip Code

S-Corporation: EIN Name Date Incorporated Date of S-Election Address: Mailing Address Suite # City State Zip Code Contact Name: Email: Contact Phones: (Office) (Home) (Mobile) Contact Mailing Address Suite

S-Corporation: EIN Name Date Incorporated Date of S-Election Address: Mailing Address Suite # City State Zip Code Contact Name: Email: Contact Phones: (Office) (Home) (Mobile) Contact Mailing Address Suite

Chapter 5 Eligible Earnings

IN THIS CHAPTER: PERA-Eligible Salary Compensation that is not Salary Closer Look at Some Types of Pay Workers Compensation Payments Pay while on Personal, Parental or Military Leave Members on Paid Medical

IN THIS CHAPTER: PERA-Eligible Salary Compensation that is not Salary Closer Look at Some Types of Pay Workers Compensation Payments Pay while on Personal, Parental or Military Leave Members on Paid Medical

TRIM PUBLIC HEARING. September 14, :01 p.m.

TRIM PUBLIC HEARING September 14, 2017 5:01 p.m. CHILDREN S SERVICES COUNCIL OF PALM BEACH COUNTY TRIM PUBLIC HEARING, SEPTEMBER 14, 2017 COVER PAGES Agenda & Synopsis of Exhibits EXHIBIT I Certification

TRIM PUBLIC HEARING September 14, 2017 5:01 p.m. CHILDREN S SERVICES COUNCIL OF PALM BEACH COUNTY TRIM PUBLIC HEARING, SEPTEMBER 14, 2017 COVER PAGES Agenda & Synopsis of Exhibits EXHIBIT I Certification

Allocating Direct and Indirect Costs for Nonprofits

Allocating Direct and Indirect Costs for Nonprofits Carol Barnard April 18, 2018 Agenda Allocating Indirect Cost Why allocating costs is important to nonprofits Identifying indirect costs Different methods

Allocating Direct and Indirect Costs for Nonprofits Carol Barnard April 18, 2018 Agenda Allocating Indirect Cost Why allocating costs is important to nonprofits Identifying indirect costs Different methods

CHARGING PRACTICES FOR FEDERALLY FUNDED GRANTS AND CONTRACTS 2009 (Revised) UNIVERSITY OF CALIFORNIA DAVIS

UNIVERSITY OF CALIFORNIA DAVIS") CHARGING PRACTICES FOR FEDERALLY FUNDED GRANTS AND CONTRACTS 2009 (Revised) UNIVERSITY OF CALIFORNIA DAVIS CONTENTS Introduction... 1 Standards for Financial Management... 2 Is the Cost Allowable?... 3

CHARGING PRACTICES FOR FEDERALLY FUNDED GRANTS AND CONTRACTS 2009 (Revised) UNIVERSITY OF CALIFORNIA DAVIS CONTENTS Introduction... 1 Standards for Financial Management... 2 Is the Cost Allowable?... 3

Proposal Pricing Instructions Page 1 of 7 Supplier Proposal Adequacy Checklist Instructions

Proposal Pricing Instructions Page 1 of 7 Supplier Proposal Adequacy Checklist Instructions Unless a valid exemption applies, Cost or Pricing Data is required to support proposals exceeding $750,000. Contractors

Proposal Pricing Instructions Page 1 of 7 Supplier Proposal Adequacy Checklist Instructions Unless a valid exemption applies, Cost or Pricing Data is required to support proposals exceeding $750,000. Contractors

OREGON STATE UNIVERSITY

OREGON STATE UNIVERSITY COST ACCOUNTING STANDARDS BOARD (CASB DS-2) REVISION 5 EFFECTIVE DATE JULY 1, 2008 INDEX DESCRIPTION PAGES REVISION 5 EFFECTIVE DATE JULY 1, 2008 PART I PART II PART III PART IV

OREGON STATE UNIVERSITY COST ACCOUNTING STANDARDS BOARD (CASB DS-2) REVISION 5 EFFECTIVE DATE JULY 1, 2008 INDEX DESCRIPTION PAGES REVISION 5 EFFECTIVE DATE JULY 1, 2008 PART I PART II PART III PART IV

Conformity with GAAP is essential for consistency and comparability in financial reporting.

GENERALLY ACCEPTED ACCOUNTING PRINCIPLES (GAAP) & FINANCIAL ACCOUNTING STANDARD BOARD (FASB) The term generally accepted accounting principles refer to the standards, rules, and procedures that serve as

GENERALLY ACCEPTED ACCOUNTING PRINCIPLES (GAAP) & FINANCIAL ACCOUNTING STANDARD BOARD (FASB) The term generally accepted accounting principles refer to the standards, rules, and procedures that serve as

Chart V Expense Codes. Updated 21-MAY-18. Expense Category Category Title

Chart V Expense Codes Updated 21-MAY-18 PE PE Ttile Expense Category Category Title Expense Account Account Title 10 Salaries 4000 Salaries & Wages E4105 Faculty E4106 Staff E4107 Sal-Admin Increment E4108

Chart V Expense Codes Updated 21-MAY-18 PE PE Ttile Expense Category Category Title Expense Account Account Title 10 Salaries 4000 Salaries & Wages E4105 Faculty E4106 Staff E4107 Sal-Admin Increment E4108

Self Employment Income & Single Member LLC Organizer This Organizer belongs to:

Self Employment Income & Single Member LLC Organizer This Organizer belongs to: This self-employment organizer will assist you with organization of your business information and records. The IRS imposes

Self Employment Income & Single Member LLC Organizer This Organizer belongs to: This self-employment organizer will assist you with organization of your business information and records. The IRS imposes

SANILAC COUNTY, MICHIGAN

SANILAC COUNTY, MICHIGAN FISCAL 2017 COST ALLOCATION PLAN FOR THE PERIOD ENDING December 31, 2017 MGT Consulting Group Michigan Office 2343 Delta Road Bay City, Michigan 48706 989-316-2220 www.mgtconsulting.com

SANILAC COUNTY, MICHIGAN FISCAL 2017 COST ALLOCATION PLAN FOR THE PERIOD ENDING December 31, 2017 MGT Consulting Group Michigan Office 2343 Delta Road Bay City, Michigan 48706 989-316-2220 www.mgtconsulting.com

COST ACCOUNTING STANDARDS BOARD DISCLOSURE STATEMENT REQUIRED BY PUBLIC LAW EDUCATIONAL INSTITUTIONS

INDEX GENERAL INSTRUCTIONS--Continuation Sheet.............. (i) COVER SHEET AND CERTIFICATION................... C-1 PART I General Information.................. I-1 Part II Part III Part IV Direct Costs......................

INDEX GENERAL INSTRUCTIONS--Continuation Sheet.............. (i) COVER SHEET AND CERTIFICATION................... C-1 PART I General Information.................. I-1 Part II Part III Part IV Direct Costs......................

In This Issue: Understanding Your Audit: Why It Matters, How It Helps. How to Prepare for and Streamline a Payroll Audit

A workers compensation resource for State Fund policyholders 2010 Issue 1 In This Issue: Understanding Your Audit: Why It Matters, How It Helps How to Prepare for and Streamline a Payroll Audit File This:

A workers compensation resource for State Fund policyholders 2010 Issue 1 In This Issue: Understanding Your Audit: Why It Matters, How It Helps How to Prepare for and Streamline a Payroll Audit File This:

Indirect Cost Rates For Nonprofit Organizations

Indirect Cost Rates For Nonprofit Organizations Bag Lunch Webinar May 8, 2013 All slides and handouts copyright 2013, Rubino & Company, Chartered Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants

Indirect Cost Rates For Nonprofit Organizations Bag Lunch Webinar May 8, 2013 All slides and handouts copyright 2013, Rubino & Company, Chartered Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants

Prevailing Wage Compliance Overview. Presented by Sam Melamed

Prevailing Wage Compliance Overview Presented by Sam Melamed www.contractorsplan.com Session Overview Current enforcement environment Compliance issues related to Davis Bacon Apprenticeship Site of Work

Prevailing Wage Compliance Overview Presented by Sam Melamed www.contractorsplan.com Session Overview Current enforcement environment Compliance issues related to Davis Bacon Apprenticeship Site of Work

Self Employment Income & Single Member LLC Organizer This Organizer belongs to:

Self Employment Income & Single Member LLC Organizer This Organizer belongs to: This self-employment organizer will assist you with organization of your business information and records. The IRS imposes

Self Employment Income & Single Member LLC Organizer This Organizer belongs to: This self-employment organizer will assist you with organization of your business information and records. The IRS imposes

Allowable Costs. Exception to Direct or Indirect Cost Category. Item of Cost Description Normally Direct or Indirect Cost

Allowable Costs The Federal Office of Budget and Management (OMB) 2 CFR Part 200 provides principles to be applied to determine the allowability of certain items of cost on Federal Awards. The principles

Allowable Costs The Federal Office of Budget and Management (OMB) 2 CFR Part 200 provides principles to be applied to determine the allowability of certain items of cost on Federal Awards. The principles

ICANN COMPENSATION JULY 2011

COMPENSATION PRACTICES ICANN COMPENSATION JULY 2011 The overarching objective of ICANN s remuneration framework is to ensure remuneration provided is competitive globally and that it provides staff with

COMPENSATION PRACTICES ICANN COMPENSATION JULY 2011 The overarching objective of ICANN s remuneration framework is to ensure remuneration provided is competitive globally and that it provides staff with

Billing Methodologies and Best Practices

Billing Methodologies and Best Practices Built to Last Built for Change August 9, 2017 OFFICE OF HOUSING COUNSELING 1 Facilitated By Robin L. Booth, CPA Audit Principal Booth Management Consulting OFFICE

Billing Methodologies and Best Practices Built to Last Built for Change August 9, 2017 OFFICE OF HOUSING COUNSELING 1 Facilitated By Robin L. Booth, CPA Audit Principal Booth Management Consulting OFFICE

A CHECKLIST FOR DEVELOPING AND EVALUATING EVALUATION BUDGETS

A CHECKLIST FOR DEVELOPIN AND EVALUATIN EVALUATION BUDETS Jerry Horn December 2001 This checklist is designed to assist evaluators and others think through the many issues that should be considered when

A CHECKLIST FOR DEVELOPIN AND EVALUATIN EVALUATION BUDETS Jerry Horn December 2001 This checklist is designed to assist evaluators and others think through the many issues that should be considered when

Georgia Department of Transportation American Recovery and Reinvestment Act Circular A-87 Synopsis

A grantee/sponsor is responsible for accounting for cost appropriately and maintaining records, including supporting documentation, adequate to demonstrate that costs claimed have been incurred, are allowable,

A grantee/sponsor is responsible for accounting for cost appropriately and maintaining records, including supporting documentation, adequate to demonstrate that costs claimed have been incurred, are allowable,

SANTA CRUZ METROPOLITAN TRANSIT DISTRICT MANAGEMENT COMPENSATION PLAN

SANTA CRUZ METROPOLITAN TRANSIT DISTRICT MANAGEMENT COMPENSATION PLAN Board Adopted August 26, 2016 Effective September 9, 2016 TABLE OF CONTENTS I. MANAGEMENT POSITIONS 1 II. PROBATIONARY STATUS 1 III.

SANTA CRUZ METROPOLITAN TRANSIT DISTRICT MANAGEMENT COMPENSATION PLAN Board Adopted August 26, 2016 Effective September 9, 2016 TABLE OF CONTENTS I. MANAGEMENT POSITIONS 1 II. PROBATIONARY STATUS 1 III.

University of Missouri System Accounting Policies and Procedures

University of Missouri System Accounting Policies and Procedures Policy Number: APM-60.07 Policy Name: Allowable Costs and Cost Principles General Policy and Procedure Overview This policy outlines the

University of Missouri System Accounting Policies and Procedures Policy Number: APM-60.07 Policy Name: Allowable Costs and Cost Principles General Policy and Procedure Overview This policy outlines the

BI360 Reporting and Budgeting Examples. A Solver White Paper

BI360 Reporting and Budgeting Examples A Solver White Paper July 2012 solverusa.com Copyright 2012 Table of Contents Solver Templates... 3 Basic Budgeting and Forecasting... 4 Five Year Budget... 4 Forecasting...

BI360 Reporting and Budgeting Examples A Solver White Paper July 2012 solverusa.com Copyright 2012 Table of Contents Solver Templates... 3 Basic Budgeting and Forecasting... 4 Five Year Budget... 4 Forecasting...

COMPENSATION AND BENEFITS PLAN

COMPENSATION AND BENEFITS PLAN BETWEEN THE CITY OF TRACY AND THE DEPARTMENT HEADS July 1, 2018 through June 30, 2021 Amended March 5, 2019 Human Resources Department 333 Civic Center Plaza Tracy, CA 95376

COMPENSATION AND BENEFITS PLAN BETWEEN THE CITY OF TRACY AND THE DEPARTMENT HEADS July 1, 2018 through June 30, 2021 Amended March 5, 2019 Human Resources Department 333 Civic Center Plaza Tracy, CA 95376

MODULE 26 List and describe fringe benefits provided by the employer.

Student name: Date: MODULE 26 List and describe fringe benefits provided by the employer. Objectives: A. Determine fringe benefits available from some employers. B. List and describe fringe benefits provided

Student name: Date: MODULE 26 List and describe fringe benefits provided by the employer. Objectives: A. Determine fringe benefits available from some employers. B. List and describe fringe benefits provided

Small Business Tax Organizer

EIN Name Date Started Street Address City State Zip Code Please utilize this Tax Organizer to help you gather and organize information relating to preparation of your business income tax returns. Where

EIN Name Date Started Street Address City State Zip Code Please utilize this Tax Organizer to help you gather and organize information relating to preparation of your business income tax returns. Where

How to Prepare Your Taxes

How to Prepare Your Taxes Along with these notes, you will also need to print a copy of the File Folder Quick Reference page, as well as the Tax Organization Labels. It would be helpful to use a 31 pocket

How to Prepare Your Taxes Along with these notes, you will also need to print a copy of the File Folder Quick Reference page, as well as the Tax Organization Labels. It would be helpful to use a 31 pocket

Accounting System Requirements

Accounting System Requirements Further information is available in the Information for Contractors Manual under Enclosure 2 The views expressed in this presentation are DCAA's views and not necessarily

Accounting System Requirements Further information is available in the Information for Contractors Manual under Enclosure 2 The views expressed in this presentation are DCAA's views and not necessarily

Relocation Policy. 01 Policy Statement Reason for Policy Who Needs to Know This Policy Eligibility... 2

Relocation Policy Table of Contents 01 Policy Statement... 2 02 Reason for Policy... 2 03 Who Needs to Know This Policy... 2 04 Eligibility... 2 05 Explanation Reimbursable Relocation Expenses... 2 06

Relocation Policy Table of Contents 01 Policy Statement... 2 02 Reason for Policy... 2 03 Who Needs to Know This Policy... 2 04 Eligibility... 2 05 Explanation Reimbursable Relocation Expenses... 2 06

GUIDELINES FOR BUDGET PREPARATION

CENTERS FOR DISEASE CONTROL AND PREVENTION (CDC) INTRODUCTION Guidance is offered for the preparation of a budget request. Following this guidance will facilitate the review and approval of a requested

CENTERS FOR DISEASE CONTROL AND PREVENTION (CDC) INTRODUCTION Guidance is offered for the preparation of a budget request. Following this guidance will facilitate the review and approval of a requested

ORGANIZER FOR 2018 TAXES

Gerald Hersh EA Page 1 800 Main St Amherst MA 01002 Tel: (413) 256-1663 Fax: (413) 256-1665 Email: gerrystaxhelp@aol.com website: www.amhersttaxpreparation.com ORGANIZER FOR 2018 TAXES Name Social Security

Gerald Hersh EA Page 1 800 Main St Amherst MA 01002 Tel: (413) 256-1663 Fax: (413) 256-1665 Email: gerrystaxhelp@aol.com website: www.amhersttaxpreparation.com ORGANIZER FOR 2018 TAXES Name Social Security

ICANN COMPENSATION JANUARY 2010

COMPENSATION PRACTICES ICANN COMPENSATION JANUARY 2010 The overarching objective of ICANN s remuneration framework is to ensure remuneration provided is competitive globally and that it provides staff

COMPENSATION PRACTICES ICANN COMPENSATION JANUARY 2010 The overarching objective of ICANN s remuneration framework is to ensure remuneration provided is competitive globally and that it provides staff

TRIM PUBLIC HEARING. September 7, :01 p.m.

TRIM PUBLIC HEARING September 7, 2018 5:01 p.m. CHILDREN S SERVICES COUNCIL OF PALM BEACH COUNTY TRIM PUBLIC HEARING, SEPTEMBER 7, 2018 COVER PAGES Agenda & Synopsis of Exhibits EXHIBIT I Certification

TRIM PUBLIC HEARING September 7, 2018 5:01 p.m. CHILDREN S SERVICES COUNCIL OF PALM BEACH COUNTY TRIM PUBLIC HEARING, SEPTEMBER 7, 2018 COVER PAGES Agenda & Synopsis of Exhibits EXHIBIT I Certification

Coversheet. Coversheet. This is a step by step, how to training designed to assist sponsors in completing each sheet of the budget form.

Coversheet Welcome to completing the annual multisite and new center sponsors budget form training presented by the Oregon Department of Education Child Nutrition Programs, referred to as ODE CNP in this

Coversheet Welcome to completing the annual multisite and new center sponsors budget form training presented by the Oregon Department of Education Child Nutrition Programs, referred to as ODE CNP in this

TEXAS SOUTHERN UNIVERSITY MANUAL OF ADMINISTRATIVE POLICIES AND PROCEDURES. SECTION: Fiscal Affairs NUMBER:

TEXAS SOUTHERN UNIVERSITY MANUAL OF ADMINISTRATIVE POLICIES AND PROCEDURES SECTION: Fiscal Affairs NUMBER: 03.04.04 AREA: SUBJECT: Payroll Taxable Fringe Benefits I. PURPOSE AND SCOPE Texas Southern University

TEXAS SOUTHERN UNIVERSITY MANUAL OF ADMINISTRATIVE POLICIES AND PROCEDURES SECTION: Fiscal Affairs NUMBER: 03.04.04 AREA: SUBJECT: Payroll Taxable Fringe Benefits I. PURPOSE AND SCOPE Texas Southern University

SG&A AND EXPENSE CATEGORIZATION POLICY

fjrake,&scull QHSE Ref. No. IMS/FIN/SGA/05Rev. 01 SG&A AND EXPENSE CA TEGORIZA TION 21st May2009 SG&A AND EXPENSE CATEGORIZATION POLICY Rev Date Revision Record 21/05/09 First issue for approval Page 1

fjrake,&scull QHSE Ref. No. IMS/FIN/SGA/05Rev. 01 SG&A AND EXPENSE CA TEGORIZA TION 21st May2009 SG&A AND EXPENSE CATEGORIZATION POLICY Rev Date Revision Record 21/05/09 First issue for approval Page 1