Calibrating Macroprudential Policy to Forecasts of Financial Stability

|

|

|

- Cassandra Alexander

- 5 years ago

- Views:

Transcription

1 Calibrating Macroprudential Policy to Forecasts of Financial Stability Scott Brave (FRB Chicago) Jose A. Lopez (FRBSF) EBA Policy Research Workshop London, UK November 29, 2017 The views expressed here are those of the authors and do not necessarily represent the views of the Board of Governors of the Federal Reserve System, the Federal Reserve Bank of Chicago, or the Federal Reserve Bank of San Francisco.

2 Overview Since the financial crisis, the introduction of explicit macroprudential responsibilities at central banks and financial regulatory agencies has created a need for new measures of financial stability. Many have been proposed, but they require further transformation / calibration to become policy indicators. We propose a transformation into transition probabilities between states of higher and lower financial stability. Forecasts of these probabilities can then be used within the decision theoretic framework of Kahn and Stinchcombe (AER, 2015) to provide countercyclical capital buffer suggestions calibrated to current circumstances.

3 Countercyclical capital buffers The CCyB would increase regulatory capital requirements for select firms when policymakers judge that systemic risk is elevated. Ranges from 0% to 2.5% depending on the deliberations of the relevant national regulatory authority. As a macroprudential tool, the setting of its level is most directly linked to the condition of the overall financial environment. Depends on analysis of current macroeconomic, financial, and supervisory information, including measures of financial stability. BCBS advocates the use of a country s detrended ratio of private, nonfinancial credit to nominal GDP, as a key reference variable.

4 Credit-to-GDP ratio Drehmann et al. (2011) propose one-sided HP filtering using the λ parameter of 400,000. Edge & Meisenzahl (2011) present challenges to this choice. Jim Hamilton (2016) wrote a paper entitled: Why You Should Never Use the Hodrick-Prescott Filter (1) The HP filter produces series with spurious dynamic relations that have no basis in the underlying data-generating process. (2) The one-sided filter produces series that do not have the properties sought by most potential users of the HP filter. (3) A statistical formalization of the problem produces values for the smoothing parameter far below 1600 for quarterly data. Building on Brave and Butters (2012), we examine the quarterly log first differences of real private credit and real GDP instead.

5 Markov-switching model ln GDP ln GDP, ln C, ln C t S S t1 t t1 t 2 states: higher and lower degrees of financial stability; i.e., S +, S - i j Pr S S S S,X, ijt t t 1 t ijt Our first specification is that the transition probabilities are constant; i.e., δ ijt = δ As per Diebold et al. (1994), we examine time-varying probabilities that are functions of FSIs, denoted as X. t X 1 X t 1 Xt X t t

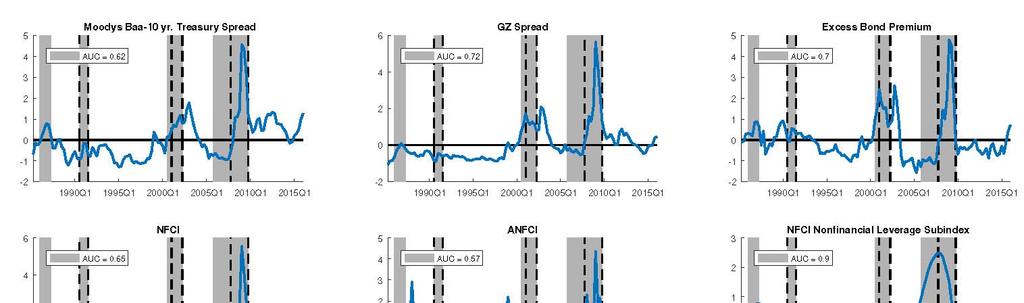

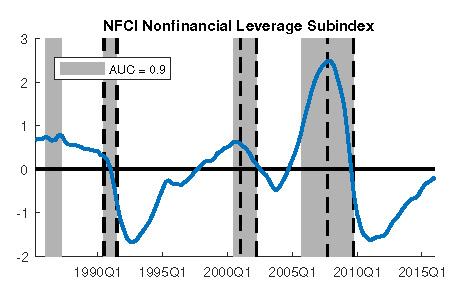

6 Financial stability indicators We examine a focused subset of FSI based on previous literature. FSI reflecting conditions in the corporate bond market and correlated with near-term economic growth: (1) The spread between yields on seasoned long-term Baa-rated industrial bonds and Treasuries of comparable maturities - As per Lopez-Salido, Stein, and Zakrajsek (2015) (2)(3) Spread and excess bond premium measures developed by Gilchrist and Zakrajsek (2012) FSI reflecting conditions in the banking system: (4) Leverage Ratio FSI by Brave & Butters (2012) reflecting conditions more broadly: - Constructed using an unbalanced panel of 105 mixed-frequency indicators of financial activity (5) The National Financial Conditions Index (NFCI) (6) The NFCI adjusted for current economic conditions (ANFCI) (7) NFCI Nonfinancial leverage subcomponent

7 Markov-switching model (cont.) 8 models are combined with Bayesian model averaging techniques. Two states are defined according to the estimated model parameters, so they vary somewhat across specifications. States are distinguished primarily by differences in the estimated constants and the contemporaneous coefficients on credit growth. S+ : Average real GDP growth>0, Minimal co-movement with credit - estimated at +2.5% annualized growth rate - near-zero coefficient on Δln(C t ) S- : Average real GDP growth<0, Strong co-movement with credit - estimated at -2.7% annualized growth rate - coefficient of +0.7 on Δln(C t )

8 Markov-switching model (cont.) Model-implied states of financial instability: Probability>0.5 Adverse Events: 1986Q1-1986Q4, 1990Q3-1991Q1, 2000Q3-2001Q4, 2005Q4-2009Q2 Recessions: 1990Q3-1991Q1, 2001Q1-2001Q4, 2007Q4-2009Q2

9 Markov-switching model (cont.)

10 Markov-switching model (cont.)

11 Forecasting state probabilities To forecast the state probabilities up to k periods ahead, define and such that E S, T T T T1 T Pr ST pt Pr S p p p P, p p k E P Tk T T and the hazard function for the negative state is k 2,1 H (k) EPr S P T T k T T

12 Forecasting state probabilities (cont.) A single quarter of the financial instability state is likely insufficient to warrant policy action. For CCyB, capital increase must be completed within 12 months. - Intuition for event of interest as 4 quarters in the negative state. We consider this event over 8 projection quarters T+k, kϵ[1,8]. With 3 in-sample quarters, we have 2,048(=2 11 ) paths to consider. - With 8(=2 3 ) sets of initial conditions, we can aggregate the cumulative likelihood of the 4-quarter event across the projection quarters and weight by likelihood.

13 KS policy objective function These hazard function projections are an input into the objective function of the macroprudential policymaker, but what does that function look like? Kahn-Stinchcombe (AER, 2015) present an analytical framework for decisions based on hesitating to take a costly action in order to gather more information on the current state of the situation. - At issue is the optimal timing of a costly precautionary measure: an evacuation before a hurricane landfall; or a politically painful reform of a banking system before the next financial crisis. Closed-form first order condition for optimal time to act t * : * rc h t u 1 u /rc Balancing the benefit of waiting in the numerator (i.e., saving from not incurring cost) and the policy cost (i.e., NPV of gains minus C)

14 KS policy objective function (cont.) Define t w as the waiting time until the defined adverse event arrives. f(t w ) is its pdf; F(t w ) is its cdf; h(t w ) = f(t w )/(1-F(t w )) is its hazard When to act balances the costs and benefits of the policy with the probabilistic arrival of the adverse event. u is the present utility flow, and u is the flow after enacting the policy such that u u 0 C is the cost of enacting the policy (current cost, but can be expanded) The policy also affects the probability of the event occurring: f t ;t w 1 f t if t t w w 1 1 f tw if tw t1

15 Calibration: KS policy objective function (cont.) The discount rate r is the 2-year Treasury rate since the government policymaker is working over a two-year event horizon. The narrow cost C of the policy is the dollar cost to the affected firms of raising the equity capital needed to meet a 0.25% CCyB increase. Θ is calibrated as [0, 0.25, 0.50, 0.75, 1]. How do we calibrate the current and adverse utility flows? - External calibration: - Set u as expected GDP growth (from professional forecasts) - Set u as reduction based on decreased GDP growth after increase in capital requirements - MAG (2010) study: [20%,80%] range from [-17, -4] bp - Internal calibration: - Set using estimated model parameters u,u

16 External calibration results: 0.25% buffer u,u Small difference between leads to narrow KS band Q4 policymaker is behind and should act immediately Q4/2015.Q4 policymaker can wait since the hazard function is below the KS band that would signal the need to act.

17 u,u Internal calibration Set using estimated model parameters: - Calculate the state-dependent expected GDP growth rate from the model, which includes expected credit growth - Set u g and u b - The larger difference leads to lower, wider KS band.

18 Internal calibration results: 0.25% buffer 2007.Q4 policymaker is behind and should act immediately Q4/2015.Q4 policymaker can wait until PQ8/PQ7 to act since the hazard function is just then touching the lower bound of the KS band that would signal the need to act.

19 Internal calibration results: optimal buffer - Free the CCyB policy from a strict +0.25% to a range of values; i.e., for current conditions, what CCyB value is most reasonable? Dashed line represents a 0.25% capital buffer

20 Conclusion Macroprudential policy responsibilities have become important elements for maintaining financial stability. Given a set of policy tools, policymakers need (1) ways to measure the degree of financial stability, (2) translate those measurements into policy projections, and (3) decide if and when to implement their policy tools. We propose a methodology that (1) can incorporate a wide variety of financial stability indicators, (2) translates financial stability measures into probability forecasts of better or worse states of financial stability over an event horizon, and (3) presents a closed-form solution for when to act that can be calibrated to the cost, benefits, and effectiveness of the policy tool to be implemented. (4) allows for a flexible calibration exercise that can be expanded

Calibrating Macroprudential Policy to Forecasts of Financial Stability

FEDERAL RESERVE BANK OF SAN FRANCISCO WORKING PAPER SERIES Calibrating Macroprudential Policy to Forecasts of Financial Stability Scott A. Brave Federal Reserve Bank of Chicago Jose A. Lopez Federal Reserve

FEDERAL RESERVE BANK OF SAN FRANCISCO WORKING PAPER SERIES Calibrating Macroprudential Policy to Forecasts of Financial Stability Scott A. Brave Federal Reserve Bank of Chicago Jose A. Lopez Federal Reserve

Calibrating Macroprudential Policy to Forecasts of Financial Stability. S.A. Brave, J.A. Lopez

Calibrating Macroprudential Policy to Forecasts of Financial Stability S.A. Brave, J.A. Lopez Discussant: Valerio Pesic University La Sapienza, Rome (Italy) valerio.pesic@uniroma1.it This paper deals on

Calibrating Macroprudential Policy to Forecasts of Financial Stability S.A. Brave, J.A. Lopez Discussant: Valerio Pesic University La Sapienza, Rome (Italy) valerio.pesic@uniroma1.it This paper deals on

Economics Letters 108 (2010) Contents lists available at ScienceDirect. Economics Letters. journal homepage:

Contents lists available at ScienceDirect. Economics Letters. journal homepage:") Economics Letters 108 (2010) 167 171 Contents lists available at ScienceDirect Economics Letters journal homepage: www.elsevier.com/locate/ecolet Is there a financial accelerator in US banking? Evidence

Economics Letters 108 (2010) 167 171 Contents lists available at ScienceDirect Economics Letters journal homepage: www.elsevier.com/locate/ecolet Is there a financial accelerator in US banking? Evidence

1 DIRECTIVE 2013/36/EU OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 26 June 2013 on access to the

Methodology underlying the determination of the benchmark countercyclical capital buffer rate and supplementary indicators signalling the build-up of cyclical systemic financial risk The application of

Methodology underlying the determination of the benchmark countercyclical capital buffer rate and supplementary indicators signalling the build-up of cyclical systemic financial risk The application of

Growth Opportunities, Investment-Specific Technology Shocks and the Cross-Section of Stock Returns

Growth Opportunities, Investment-Specific Technology Shocks and the Cross-Section of Stock Returns Leonid Kogan 1 Dimitris Papanikolaou 2 1 MIT and NBER 2 Northwestern University Boston, June 5, 2009 Kogan,

Growth Opportunities, Investment-Specific Technology Shocks and the Cross-Section of Stock Returns Leonid Kogan 1 Dimitris Papanikolaou 2 1 MIT and NBER 2 Northwestern University Boston, June 5, 2009 Kogan,

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

R-Star Wars: The Phantom Menace

R-Star Wars: The Phantom Menace James Bullard President and CEO 34th Annual National Association for Business Economics (NABE) Economic Policy Conference Feb. 26, 2018 Washington, D.C. Any opinions expressed

R-Star Wars: The Phantom Menace James Bullard President and CEO 34th Annual National Association for Business Economics (NABE) Economic Policy Conference Feb. 26, 2018 Washington, D.C. Any opinions expressed

Note on Countercyclical Capital Buffer Methodology

Note on Countercyclical Capital Buffer Methodology Prepared by Financial Stability Department December 2018 1 1. Background and Legal Basis Following the recent financial crisis, the Basel Committee on

Note on Countercyclical Capital Buffer Methodology Prepared by Financial Stability Department December 2018 1 1. Background and Legal Basis Following the recent financial crisis, the Basel Committee on

COUNTERCYCLICAL CAPITAL BUFFER

} COUNTERCYCLICAL CAPITAL BUFFER 9 June 18 Pursuant to a decision of the Board of Directors of 7 June 18, the countercyclical buffer rate for credit exposures to the domestic private non-financial sector

} COUNTERCYCLICAL CAPITAL BUFFER 9 June 18 Pursuant to a decision of the Board of Directors of 7 June 18, the countercyclical buffer rate for credit exposures to the domestic private non-financial sector

Predicting Turning Points in the South African Economy

289 Predicting Turning Points in the South African Economy Elna Moolman Department of Economics, University of Pretoria ABSTRACT Despite the existence of macroeconomic models and complex business cycle

289 Predicting Turning Points in the South African Economy Elna Moolman Department of Economics, University of Pretoria ABSTRACT Despite the existence of macroeconomic models and complex business cycle

Vanguard: The yield curve inversion and what it means for investors

Vanguard: The yield curve inversion and what it means for investors December 3, 2018 by Joseph Davis, Ph.D. of Vanguard The U.S. economy has seen a prolonged period of growth without a recession. As the

Vanguard: The yield curve inversion and what it means for investors December 3, 2018 by Joseph Davis, Ph.D. of Vanguard The U.S. economy has seen a prolonged period of growth without a recession. As the

EUROPEAN SYSTEMIC RISK BOARD

2.9.2014 EN Official Journal of the European Union C 293/1 I (Resolutions, recommendations and opinions) RECOMMENDATIONS EUROPEAN SYSTEMIC RISK BOARD RECOMMENDATION OF THE EUROPEAN SYSTEMIC RISK BOARD

2.9.2014 EN Official Journal of the European Union C 293/1 I (Resolutions, recommendations and opinions) RECOMMENDATIONS EUROPEAN SYSTEMIC RISK BOARD RECOMMENDATION OF THE EUROPEAN SYSTEMIC RISK BOARD

Stock Market Cross-Section Skewness and Business Cycle Fluctuations

Stock Market Cross-Section Skewness and Business Cycle Fluctuations Thiago R. T. Ferreira Federal Reserve Board Abstract Using U.S. data from 1926 to 215, I document that the cross-section skewness of

Stock Market Cross-Section Skewness and Business Cycle Fluctuations Thiago R. T. Ferreira Federal Reserve Board Abstract Using U.S. data from 1926 to 215, I document that the cross-section skewness of

Characteristics of the euro area business cycle in the 1990s

Characteristics of the euro area business cycle in the 1990s As part of its monetary policy strategy, the ECB regularly monitors the development of a wide range of indicators and assesses their implications

Characteristics of the euro area business cycle in the 1990s As part of its monetary policy strategy, the ECB regularly monitors the development of a wide range of indicators and assesses their implications

Internet Appendix for: Cyclical Dispersion in Expected Defaults

Internet Appendix for: Cyclical Dispersion in Expected Defaults March, 2018 Contents 1 1 Robustness Tests The results presented in the main text are robust to the definition of debt repayments, and the

Internet Appendix for: Cyclical Dispersion in Expected Defaults March, 2018 Contents 1 1 Robustness Tests The results presented in the main text are robust to the definition of debt repayments, and the

Stock Market Cross-Sectional Skewness and Business Cycle Fluctuations 1

Stock Market Cross-Sectional Skewness and Business Cycle Fluctuations 1 Ninth BIS CCA Research Conference Rio de Janeiro June 2018 1 Previously presented as Cross-Section Skewness, Business Cycle Fluctuations

Stock Market Cross-Sectional Skewness and Business Cycle Fluctuations 1 Ninth BIS CCA Research Conference Rio de Janeiro June 2018 1 Previously presented as Cross-Section Skewness, Business Cycle Fluctuations

Macroeconomic Cycle and Economic Policy

Macroeconomic Cycle and Economic Policy Lecture 1 Nicola Viegi University of Pretoria 2016 Introduction Macroeconomics as the study of uctuations in economic aggregate Questions: What do economic uctuations

Macroeconomic Cycle and Economic Policy Lecture 1 Nicola Viegi University of Pretoria 2016 Introduction Macroeconomics as the study of uctuations in economic aggregate Questions: What do economic uctuations

Properties of the estimated five-factor model

Informationin(andnotin)thetermstructure Appendix. Additional results Greg Duffee Johns Hopkins This draft: October 8, Properties of the estimated five-factor model No stationary term structure model is

Informationin(andnotin)thetermstructure Appendix. Additional results Greg Duffee Johns Hopkins This draft: October 8, Properties of the estimated five-factor model No stationary term structure model is

Optimal Credit Market Policy. CEF 2018, Milan

Optimal Credit Market Policy Matteo Iacoviello 1 Ricardo Nunes 2 Andrea Prestipino 1 1 Federal Reserve Board 2 University of Surrey CEF 218, Milan June 2, 218 Disclaimer: The views expressed are solely

Optimal Credit Market Policy Matteo Iacoviello 1 Ricardo Nunes 2 Andrea Prestipino 1 1 Federal Reserve Board 2 University of Surrey CEF 218, Milan June 2, 218 Disclaimer: The views expressed are solely

Capital regulation and macroeconomic activity

1/35 Capital regulation and macroeconomic activity Implications for macroprudential policy Roland Meeks Monetary Assessment & Strategy Division, Bank of England and Department of Economics, University

1/35 Capital regulation and macroeconomic activity Implications for macroprudential policy Roland Meeks Monetary Assessment & Strategy Division, Bank of England and Department of Economics, University

L 2 Supply and Productivity Tools and Growth Diagnostics

L 2 Supply and Productivity Tools and Growth Diagnostics IMF Singapore Regional Training Institute OT 18.52 Macroeconomic Diagnostics February 26 March 2, 2018 Presenter Reza Siregar This training material

L 2 Supply and Productivity Tools and Growth Diagnostics IMF Singapore Regional Training Institute OT 18.52 Macroeconomic Diagnostics February 26 March 2, 2018 Presenter Reza Siregar This training material

Housing Prices and Growth

Housing Prices and Growth James A. Kahn June 2007 Motivation Housing market boom-bust has prompted talk of bubbles. But what are fundamentals? What is the right benchmark? Motivation Housing market boom-bust

Housing Prices and Growth James A. Kahn June 2007 Motivation Housing market boom-bust has prompted talk of bubbles. But what are fundamentals? What is the right benchmark? Motivation Housing market boom-bust

Household Heterogeneity in Macroeconomics

Household Heterogeneity in Macroeconomics Department of Economics HKUST August 7, 2018 Household Heterogeneity in Macroeconomics 1 / 48 Reference Krueger, Dirk, Kurt Mitman, and Fabrizio Perri. Macroeconomics

Household Heterogeneity in Macroeconomics Department of Economics HKUST August 7, 2018 Household Heterogeneity in Macroeconomics 1 / 48 Reference Krueger, Dirk, Kurt Mitman, and Fabrizio Perri. Macroeconomics

D OES A L OW-I NTEREST-R ATE R EGIME H ARM S AVERS? James Bullard President and CEO

D OES A L OW-I NTEREST-R ATE R EGIME H ARM S AVERS? James Bullard President and CEO Nonlinear Models in Macroeconomics and Finance for an Unstable World Norges Bank Jan. 26, 2018 Oslo, Norway Any opinions

D OES A L OW-I NTEREST-R ATE R EGIME H ARM S AVERS? James Bullard President and CEO Nonlinear Models in Macroeconomics and Finance for an Unstable World Norges Bank Jan. 26, 2018 Oslo, Norway Any opinions

PERU: MACROPRUDENTIAL POLICIES TO ACHIEVE FINANCIAL STABILITY. Renzo Rossini General Manager Central Reserve Bank of Peru

PERU: MACROPRUDENTIAL POLICIES TO ACHIEVE FINANCIAL STABILITY Renzo Rossini General Manager Central Reserve Bank of Peru Dollarization Central Reserve Bank of Peru 2 Russian crisis Reduction of short-term

PERU: MACROPRUDENTIAL POLICIES TO ACHIEVE FINANCIAL STABILITY Renzo Rossini General Manager Central Reserve Bank of Peru Dollarization Central Reserve Bank of Peru 2 Russian crisis Reduction of short-term

Optimal monetary and macro-pru policies

Discussion of Kiley and Sim s Optimal monetary and macro-pru policies Oreste Tristani European Central Bank Federal Reserve Bank of San Francisco Conference on Monetary Policy and Financial Markets, 28

Discussion of Kiley and Sim s Optimal monetary and macro-pru policies Oreste Tristani European Central Bank Federal Reserve Bank of San Francisco Conference on Monetary Policy and Financial Markets, 28

Bubble, Bubble Toil and Trouble:

Client Alert December 22, 2015 Bubble, Bubble Toil and Trouble: The Fed Breathes Life into the Countercyclical Capital Buffer Widespread problems in the banking system are often associated with sharp declines

Client Alert December 22, 2015 Bubble, Bubble Toil and Trouble: The Fed Breathes Life into the Countercyclical Capital Buffer Widespread problems in the banking system are often associated with sharp declines

Open Economy Macroeconomics: Theory, methods and applications

Open Economy Macroeconomics: Theory, methods and applications Econ PhD, UC3M Lecture 9: Data and facts Hernán D. Seoane UC3M Spring, 2016 Today s lecture A look at the data Study what data says about open

Open Economy Macroeconomics: Theory, methods and applications Econ PhD, UC3M Lecture 9: Data and facts Hernán D. Seoane UC3M Spring, 2016 Today s lecture A look at the data Study what data says about open

Appendices For Online Publication

Appendices For Online Publication This Online Appendix contains supplementary material referenced in the main text of Credit- Market Sentiment and the Business Cycle, by D. López-Salido, J. C. Stein, and

Appendices For Online Publication This Online Appendix contains supplementary material referenced in the main text of Credit- Market Sentiment and the Business Cycle, by D. López-Salido, J. C. Stein, and

A Macroeconomic Framework for Quantifying Systemic Risk. June 2012

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He Arvind Krishnamurthy University of Chicago & NBER Northwestern University & NBER June 212 Systemic Risk Systemic risk: risk (probability)

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He Arvind Krishnamurthy University of Chicago & NBER Northwestern University & NBER June 212 Systemic Risk Systemic risk: risk (probability)

Occasional Paper Series

Occasional Paper Series Jan Hannes Lang, Cosimo Izzo, Stephan Fahr, Josef Ruzicka Anticipating the bust: a new cyclical systemic risk indicator to assess the likelihood and severity of financial crises

Occasional Paper Series Jan Hannes Lang, Cosimo Izzo, Stephan Fahr, Josef Ruzicka Anticipating the bust: a new cyclical systemic risk indicator to assess the likelihood and severity of financial crises

Oil and macroeconomic (in)stability

stability") Oil and macroeconomic (in)stability Hilde C. Bjørnland Vegard H. Larsen Centre for Applied Macro- and Petroleum Economics (CAMP) BI Norwegian Business School CFE-ERCIM December 07, 2014 Bjørnland and Larsen

Oil and macroeconomic (in)stability Hilde C. Bjørnland Vegard H. Larsen Centre for Applied Macro- and Petroleum Economics (CAMP) BI Norwegian Business School CFE-ERCIM December 07, 2014 Bjørnland and Larsen

WORKING MACROPRUDENTIAL TOOLS

WORKING MACROPRUDENTIAL TOOLS Jesús Saurina Director. Financial Stability Department Banco de España Macro-prudential Regulatory Policies: The New Road to Financial Stability? Thirteenth Annual International

WORKING MACROPRUDENTIAL TOOLS Jesús Saurina Director. Financial Stability Department Banco de España Macro-prudential Regulatory Policies: The New Road to Financial Stability? Thirteenth Annual International

Box 1.3. How Does Uncertainty Affect Economic Performance?

Box 1.3. How Does Affect Economic Performance? Bouts of elevated uncertainty have been one of the defining features of the sluggish recovery from the global financial crisis. In recent quarters, high uncertainty

Box 1.3. How Does Affect Economic Performance? Bouts of elevated uncertainty have been one of the defining features of the sluggish recovery from the global financial crisis. In recent quarters, high uncertainty

Credit Booms, Financial Crises and Macroprudential Policy

Credit Booms, Financial Crises and Macroprudential Policy Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 219 1 The views expressed in this paper are those

Credit Booms, Financial Crises and Macroprudential Policy Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 219 1 The views expressed in this paper are those

Booms and Banking Crises

Booms and Banking Crises F. Boissay, F. Collard and F. Smets Macro Financial Modeling Conference Boston, 12 October 2013 MFM October 2013 Conference 1 / Disclaimer The views expressed in this presentation

Booms and Banking Crises F. Boissay, F. Collard and F. Smets Macro Financial Modeling Conference Boston, 12 October 2013 MFM October 2013 Conference 1 / Disclaimer The views expressed in this presentation

Information aggregation for timing decision making.

MPRA Munich Personal RePEc Archive Information aggregation for timing decision making. Esteban Colla De-Robertis Universidad Panamericana - Campus México, Escuela de Ciencias Económicas y Empresariales

MPRA Munich Personal RePEc Archive Information aggregation for timing decision making. Esteban Colla De-Robertis Universidad Panamericana - Campus México, Escuela de Ciencias Económicas y Empresariales

Fiscal Policy: Ready for The Next Shock?

Fiscal Policy: Ready for The Next Shock? Franziska Ohnsorge December 217 Duration of Global Expansions: Getting Older Although Not Yet Dying of Old Age 18 Global expansions (Number of years) 45 Expansions

Fiscal Policy: Ready for The Next Shock? Franziska Ohnsorge December 217 Duration of Global Expansions: Getting Older Although Not Yet Dying of Old Age 18 Global expansions (Number of years) 45 Expansions

What the Cyclical Response of Advertising Reveals about Markups and other Macroeconomic Wedges

What the Cyclical Response of Advertising Reveals about Markups and other Macroeconomic Wedges Robert E. Hall Hoover Institution and Department of Economics Stanford University Conference in Honor of James

What the Cyclical Response of Advertising Reveals about Markups and other Macroeconomic Wedges Robert E. Hall Hoover Institution and Department of Economics Stanford University Conference in Honor of James

REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL

EUROPEAN COMMISSION Brussels, 9.4.2018 COM(2018) 172 final REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL on Effects of Regulation (EU) 575/2013 and Directive 2013/36/EU on the Economic

EUROPEAN COMMISSION Brussels, 9.4.2018 COM(2018) 172 final REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL on Effects of Regulation (EU) 575/2013 and Directive 2013/36/EU on the Economic

EXPLORING LEADING INDICATORS OF BANKING CRISIS IN CASE OF ALBANIA Odeta Koçillari 1 Financial Stability Department, Bank of Albania

EXPLORING LEADING INDICATORS OF BANKING CRISIS IN CASE OF ALBANIA Odeta Koçillari 1 Financial Stability Department, Bank of Albania Abstract This paper investigates several macro-financial indicators as

EXPLORING LEADING INDICATORS OF BANKING CRISIS IN CASE OF ALBANIA Odeta Koçillari 1 Financial Stability Department, Bank of Albania Abstract This paper investigates several macro-financial indicators as

Bennett S. LeBow College of Business

Bennett S. LeBow College of Business Drexel E-Repository and Archive (idea) http://idea.library.drexel.edu/ Drexel University Libraries www.library.drexel.edu The following item is made available as a

Bennett S. LeBow College of Business Drexel E-Repository and Archive (idea) http://idea.library.drexel.edu/ Drexel University Libraries www.library.drexel.edu The following item is made available as a

Which GARCH Model for Option Valuation? By Peter Christoffersen and Kris Jacobs

Online Appendix Sample Index Returns Which GARCH Model for Option Valuation? By Peter Christoffersen and Kris Jacobs In order to give an idea of the differences in returns over the sample, Figure A.1 plots

Online Appendix Sample Index Returns Which GARCH Model for Option Valuation? By Peter Christoffersen and Kris Jacobs In order to give an idea of the differences in returns over the sample, Figure A.1 plots

STRESS TEST MODELLING OF PD RISK PARAMETER UNDER ADVANCED IRB

STRESS TEST MODELLING OF PD RISK PARAMETER UNDER ADVANCED IRB Zoltán Pollák Dávid Popper Department of Finance International Training Center Corvinus University of Budapest for Bankers (ITCB) 1093, Budapest,

STRESS TEST MODELLING OF PD RISK PARAMETER UNDER ADVANCED IRB Zoltán Pollák Dávid Popper Department of Finance International Training Center Corvinus University of Budapest for Bankers (ITCB) 1093, Budapest,

Business cycle volatility and country zize :evidence for a sample of OECD countries. Abstract

Business cycle volatility and country zize :evidence for a sample of OECD countries Davide Furceri University of Palermo Georgios Karras Uniersity of Illinois at Chicago Abstract The main purpose of this

Business cycle volatility and country zize :evidence for a sample of OECD countries Davide Furceri University of Palermo Georgios Karras Uniersity of Illinois at Chicago Abstract The main purpose of this

Fluctuations. Roberto Motto

Financial Factors in Economic Fluctuations Lawrence Christiano Roberto Motto Massimo Rostagno What we do Integrate t financial i frictions into a standard d equilibrium i model and estimate the model using

Financial Factors in Economic Fluctuations Lawrence Christiano Roberto Motto Massimo Rostagno What we do Integrate t financial i frictions into a standard d equilibrium i model and estimate the model using

Internal balance assessment:

Internal balance assessment: Economic activity Macroeconomic Analysis Course Banking Training School, State Bank of Vietnam Martin Fukac 30 October 3 November 2017 Roadmap for macroeconomic assessment

Internal balance assessment: Economic activity Macroeconomic Analysis Course Banking Training School, State Bank of Vietnam Martin Fukac 30 October 3 November 2017 Roadmap for macroeconomic assessment

Bank Capital, Agency Costs, and Monetary Policy. Césaire Meh Kevin Moran Department of Monetary and Financial Analysis Bank of Canada

Bank Capital, Agency Costs, and Monetary Policy Césaire Meh Kevin Moran Department of Monetary and Financial Analysis Bank of Canada Motivation A large literature quantitatively studies the role of financial

Bank Capital, Agency Costs, and Monetary Policy Césaire Meh Kevin Moran Department of Monetary and Financial Analysis Bank of Canada Motivation A large literature quantitatively studies the role of financial

The BCBS proposal for a countercyclical capital buffer : an application to Belgium

The BCBS proposal for a countercyclical capital buffer : an application to Belgium The BCBS proposal for a countercyclical capital buffer : an application to Belgium Joachim Keller Introduction One of

The BCBS proposal for a countercyclical capital buffer : an application to Belgium The BCBS proposal for a countercyclical capital buffer : an application to Belgium Joachim Keller Introduction One of

Global macro matters Rising rates, flatter curve: This time isn t different, it just may take longer

Global macro matters Rising rates, flatter curve: This time isn t different, it just may take longer Vanguard Research Joseph Davis, Ph.D. September 18 Authors: Roger Aliaga-Díaz, Ph.D.; Qian Wang, Ph.D.;

Global macro matters Rising rates, flatter curve: This time isn t different, it just may take longer Vanguard Research Joseph Davis, Ph.D. September 18 Authors: Roger Aliaga-Díaz, Ph.D.; Qian Wang, Ph.D.;

FRBSF Economic Letter

FRBSF Economic Letter 2017-17 June 19, 2017 Research from the Federal Reserve Bank of San Francisco New Evidence for a Lower New Normal in Interest Rates Jens H.E. Christensen and Glenn D. Rudebusch Interest

FRBSF Economic Letter 2017-17 June 19, 2017 Research from the Federal Reserve Bank of San Francisco New Evidence for a Lower New Normal in Interest Rates Jens H.E. Christensen and Glenn D. Rudebusch Interest

D OES A L OW-I NTEREST-R ATE R EGIME P UNISH S AVERS?

D OES A L OW-I NTEREST-R ATE R EGIME P UNISH S AVERS? James Bullard President and CEO Applications of Behavioural Economics and Multiple Equilibrium Models to Macroeconomic Policy Conference July 3, 2017

D OES A L OW-I NTEREST-R ATE R EGIME P UNISH S AVERS? James Bullard President and CEO Applications of Behavioural Economics and Multiple Equilibrium Models to Macroeconomic Policy Conference July 3, 2017

Business Cycle Decomposition and its Determinants: An evidence from Pakistan

Business Cycle Decomposition and its Determinants: An evidence from Pakistan Usama Ehsan Khan* and Syed Monis Jawed* Abstract- The explanation of the potential sources of economic fluctuations has been

Business Cycle Decomposition and its Determinants: An evidence from Pakistan Usama Ehsan Khan* and Syed Monis Jawed* Abstract- The explanation of the potential sources of economic fluctuations has been

Diverse Beliefs and Time Variability of Asset Risk Premia

Diverse and Risk The Diverse and Time Variability of M. Kurz, Stanford University M. Motolese, Catholic University of Milan August 10, 2009 Individual State of SITE Summer 2009 Workshop, Stanford University

Diverse and Risk The Diverse and Time Variability of M. Kurz, Stanford University M. Motolese, Catholic University of Milan August 10, 2009 Individual State of SITE Summer 2009 Workshop, Stanford University

Pushing on a string: US monetary policy is less powerful in recessions

Pushing on a string: US monetary policy is less powerful in recessions Silvana Tenreyro and Gregory Thwaites LSE and Bank of England September 13 Disclaimer This does not represent the views of the Bank

Pushing on a string: US monetary policy is less powerful in recessions Silvana Tenreyro and Gregory Thwaites LSE and Bank of England September 13 Disclaimer This does not represent the views of the Bank

RESPONSES TO SURVEY OF

RESPONSES TO SURVEY OF PRIMARY DEALERS Markets Group, Federal Reserve Bank of New York RESPONSES TO SURVEY OF a v JANUARY Distributed: 1/18/ Received by: 1/22/ The Survey of Primary Dealers is formulated

RESPONSES TO SURVEY OF PRIMARY DEALERS Markets Group, Federal Reserve Bank of New York RESPONSES TO SURVEY OF a v JANUARY Distributed: 1/18/ Received by: 1/22/ The Survey of Primary Dealers is formulated

Enrique Martínez-García. University of Texas at Austin and Federal Reserve Bank of Dallas

Discussion: International Recessions, by Fabrizio Perri (University of Minnesota and FRB of Minneapolis) and Vincenzo Quadrini (University of Southern California) Enrique Martínez-García University of

Discussion: International Recessions, by Fabrizio Perri (University of Minnesota and FRB of Minneapolis) and Vincenzo Quadrini (University of Southern California) Enrique Martínez-García University of

A Macroeconomic Model with Financial Panics

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 218 1 The views expressed in this paper are those of the authors

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 218 1 The views expressed in this paper are those of the authors

Business Cycles. (c) Copyright 1998 by Douglas H. Joines 1

Copyright 1998 by Douglas H. Joines 1") Business Cycles (c) Copyright 1998 by Douglas H. Joines 1 Module Objectives Know the causes of business cycles Know how interest rates are determined Know how various economic indicators behave over the

Business Cycles (c) Copyright 1998 by Douglas H. Joines 1 Module Objectives Know the causes of business cycles Know how interest rates are determined Know how various economic indicators behave over the

UDK : (497.7) POTENTIAL GROWTH, OUTPUT GAP AND THE CYCLICAL FISCAL POSITION OF THE REPUBLIC OF MACEDONIA

POTENTIAL GROWTH, OUTPUT GAP AND THE CYCLICAL FISCAL POSITION OF THE REPUBLIC OF MACEDONIA") UDK 330.34: 330.4 (497.7) POTENTIAL GROWTH, OUTPUT GAP AND THE CYCLICAL FISCAL POSITION OF THE REPUBLIC OF MACEDONIA MSc Misho Nikolov Abstract Economic analysis is becoming more quantitative. Thus the

UDK 330.34: 330.4 (497.7) POTENTIAL GROWTH, OUTPUT GAP AND THE CYCLICAL FISCAL POSITION OF THE REPUBLIC OF MACEDONIA MSc Misho Nikolov Abstract Economic analysis is becoming more quantitative. Thus the

Return to Capital in a Real Business Cycle Model

Return to Capital in a Real Business Cycle Model Paul Gomme, B. Ravikumar, and Peter Rupert Can the neoclassical growth model generate fluctuations in the return to capital similar to those observed in

Return to Capital in a Real Business Cycle Model Paul Gomme, B. Ravikumar, and Peter Rupert Can the neoclassical growth model generate fluctuations in the return to capital similar to those observed in

Overborrowing, Financial Crises and Macro-prudential Policy. Macro Financial Modelling Meeting, Chicago May 2-3, 2013

Overborrowing, Financial Crises and Macro-prudential Policy Javier Bianchi University of Wisconsin & NBER Enrique G. Mendoza Universtiy of Pennsylvania & NBER Macro Financial Modelling Meeting, Chicago

Overborrowing, Financial Crises and Macro-prudential Policy Javier Bianchi University of Wisconsin & NBER Enrique G. Mendoza Universtiy of Pennsylvania & NBER Macro Financial Modelling Meeting, Chicago

Business Cycles. Trends and cycles. Overview. Trends and cycles. Chris Edmond NYU Stern. Spring Start by looking at quarterly US real GDP

Trends and cycles Business Cycles Start by looking at quarterly US real Chris Edmond NYU Stern Spring 2007 1 3 Overview Trends and cycles Business cycle properties does not grow smoothly: booms and recessions

Trends and cycles Business Cycles Start by looking at quarterly US real Chris Edmond NYU Stern Spring 2007 1 3 Overview Trends and cycles Business cycle properties does not grow smoothly: booms and recessions

n n Economic Commentaries

n Economic Commentaries To ensure that the banking sector has enough capital to support the real sector, even during times of stress, it may be efficient to vary the capital requirements over time. With

n Economic Commentaries To ensure that the banking sector has enough capital to support the real sector, even during times of stress, it may be efficient to vary the capital requirements over time. With

Chapter 3. Dynamic discrete games and auctions: an introduction

Chapter 3. Dynamic discrete games and auctions: an introduction Joan Llull Structural Micro. IDEA PhD Program I. Dynamic Discrete Games with Imperfect Information A. Motivating example: firm entry and

Chapter 3. Dynamic discrete games and auctions: an introduction Joan Llull Structural Micro. IDEA PhD Program I. Dynamic Discrete Games with Imperfect Information A. Motivating example: firm entry and

Combining State-Dependent Forecasts of Equity Risk Premium

Combining State-Dependent Forecasts of Equity Risk Premium Daniel de Almeida, Ana-Maria Fuertes and Luiz Koodi Hotta Universidad Carlos III de Madrid September 15, 216 Almeida, Fuertes and Hotta (UC3M)

Combining State-Dependent Forecasts of Equity Risk Premium Daniel de Almeida, Ana-Maria Fuertes and Luiz Koodi Hotta Universidad Carlos III de Madrid September 15, 216 Almeida, Fuertes and Hotta (UC3M)

The U.S. Economy: An Optimistic Outlook, But With Some Important Risks

EMBARGOED UNTIL 8:10 A.M. Eastern Time on Friday, April 13, 2018 OR UPON DELIVERY The U.S. Economy: An Optimistic Outlook, But With Some Important Risks Eric S. Rosengren President & Chief Executive Officer

EMBARGOED UNTIL 8:10 A.M. Eastern Time on Friday, April 13, 2018 OR UPON DELIVERY The U.S. Economy: An Optimistic Outlook, But With Some Important Risks Eric S. Rosengren President & Chief Executive Officer

Idiosyncratic risk, insurance, and aggregate consumption dynamics: a likelihood perspective

Idiosyncratic risk, insurance, and aggregate consumption dynamics: a likelihood perspective Alisdair McKay Boston University June 2013 Microeconomic evidence on insurance - Consumption responds to idiosyncratic

Idiosyncratic risk, insurance, and aggregate consumption dynamics: a likelihood perspective Alisdair McKay Boston University June 2013 Microeconomic evidence on insurance - Consumption responds to idiosyncratic

A Markov switching regime model of the South African business cycle

A Markov switching regime model of the South African business cycle Elna Moolman Abstract Linear models are incapable of capturing business cycle asymmetries. This has recently spurred interest in non-linear

A Markov switching regime model of the South African business cycle Elna Moolman Abstract Linear models are incapable of capturing business cycle asymmetries. This has recently spurred interest in non-linear

Dodd-Frank Act 2014 Mid-Cycle Stress Test. Submitted to the Federal Reserve Bank on July 3, 2014

Dodd-Frank Act 2014 Mid-Cycle Stress Test Submitted to the Federal Reserve Bank on July 3, 2014 Table of Contents Section Pages 1. Requirements for Mid-Cycle Company-Run Stress Test 4 2. Description of

Dodd-Frank Act 2014 Mid-Cycle Stress Test Submitted to the Federal Reserve Bank on July 3, 2014 Table of Contents Section Pages 1. Requirements for Mid-Cycle Company-Run Stress Test 4 2. Description of

APPLICATION OF THE COUNTERCYCLICAL CAPITAL BUFFER IN LITHUANIA

TEMINIŲ STRAIPSNIŲ SERIJA No 5 / 215 TRANSLATION APPLICATION OF THE COUNTERCYCLICAL CAPITAL BUFFER IN LITHUANIA Bank of Lithuania, 215 Reproduction for educational and non-commercial purposes is permitted

TEMINIŲ STRAIPSNIŲ SERIJA No 5 / 215 TRANSLATION APPLICATION OF THE COUNTERCYCLICAL CAPITAL BUFFER IN LITHUANIA Bank of Lithuania, 215 Reproduction for educational and non-commercial purposes is permitted

The Procyclical Effects of Basel II

9TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 13-14, 2008 The Procyclical Effects of Basel II Rafael Repullo CEMFI and CEPR, Madrid, Spain and Javier Suarez CEMFI and CEPR, Madrid, Spain Presented

9TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 13-14, 2008 The Procyclical Effects of Basel II Rafael Repullo CEMFI and CEPR, Madrid, Spain and Javier Suarez CEMFI and CEPR, Madrid, Spain Presented

On modelling of electricity spot price

, Rüdiger Kiesel and Fred Espen Benth Institute of Energy Trading and Financial Services University of Duisburg-Essen Centre of Mathematics for Applications, University of Oslo 25. August 2010 Introduction

, Rüdiger Kiesel and Fred Espen Benth Institute of Energy Trading and Financial Services University of Duisburg-Essen Centre of Mathematics for Applications, University of Oslo 25. August 2010 Introduction

Financial Frictions Under Asymmetric Information and Costly State Verification

Financial Frictions Under Asymmetric Information and Costly State Verification General Idea Standard dsge model assumes borrowers and lenders are the same people..no conflict of interest. Financial friction

Financial Frictions Under Asymmetric Information and Costly State Verification General Idea Standard dsge model assumes borrowers and lenders are the same people..no conflict of interest. Financial friction

Starting with the measures of uncertainty related to future economic outcomes, the following three sets of indicators are considered:

Box How has macroeconomic uncertainty in the euro area evolved recently? High macroeconomic uncertainty through its likely adverse effect on the spending decisions of both consumers and firms is considered

Box How has macroeconomic uncertainty in the euro area evolved recently? High macroeconomic uncertainty through its likely adverse effect on the spending decisions of both consumers and firms is considered

PRE CONFERENCE WORKSHOP 3

PRE CONFERENCE WORKSHOP 3 Stress testing operational risk for capital planning and capital adequacy PART 2: Monday, March 18th, 2013, New York Presenter: Alexander Cavallo, NORTHERN TRUST 1 Disclaimer

PRE CONFERENCE WORKSHOP 3 Stress testing operational risk for capital planning and capital adequacy PART 2: Monday, March 18th, 2013, New York Presenter: Alexander Cavallo, NORTHERN TRUST 1 Disclaimer

Monetary policy and the asset risk-taking channel

Monetary policy and the asset risk-taking channel Angela Abbate 1 Dominik Thaler 2 1 Deutsche Bundesbank and European University Institute 2 European University Institute Trinity Workshop, 7 November 215

Monetary policy and the asset risk-taking channel Angela Abbate 1 Dominik Thaler 2 1 Deutsche Bundesbank and European University Institute 2 European University Institute Trinity Workshop, 7 November 215

Leverage Restrictions in a Business Cycle Model

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda Disclaimer: The views expressed are those of the authors and do not necessarily reflect those of the Bank of Japan.

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda Disclaimer: The views expressed are those of the authors and do not necessarily reflect those of the Bank of Japan.

Authors: M. Benetton, P. Eckley, N. Garbarino, L. Kirwin, G. Latsi Discussant: Klaus Düllmann*

[Please select] [Please select] Specialisation in mortgage risk under Basel II Authors: M. Benetton, P. Eckley, N. Garbarino, L. Kirwin, G. Latsi Discussant: Klaus Düllmann* EBA Policy Research workshop,

[Please select] [Please select] Specialisation in mortgage risk under Basel II Authors: M. Benetton, P. Eckley, N. Garbarino, L. Kirwin, G. Latsi Discussant: Klaus Düllmann* EBA Policy Research workshop,

Monetary, Fiscal, and Financial Stability Policy Tools: Are We Equipped for the Next Recession?

EMBARGOED UNTIL FRIDAY, MARCH 23, 2018 AT 7:00 P.M.; OR UPON DELIVERY Monetary, Fiscal, and Financial Stability Policy Tools: Are We Equipped for the Next Recession? Eric S. Rosengren President & CEO Federal

EMBARGOED UNTIL FRIDAY, MARCH 23, 2018 AT 7:00 P.M.; OR UPON DELIVERY Monetary, Fiscal, and Financial Stability Policy Tools: Are We Equipped for the Next Recession? Eric S. Rosengren President & CEO Federal

Real Business Cycle Model

Preview To examine the two modern business cycle theories the real business cycle model and the new Keynesian model and compare them with earlier Keynesian models To understand how the modern business

Preview To examine the two modern business cycle theories the real business cycle model and the new Keynesian model and compare them with earlier Keynesian models To understand how the modern business

Escaping the Great Recession 1

Escaping the Great Recession 1 Francesco Bianchi Duke University Leonardo Melosi FRB Chicago ECB workshop on Non-Standard Monetary Policy Measures 1 The views in this paper are solely the responsibility

Escaping the Great Recession 1 Francesco Bianchi Duke University Leonardo Melosi FRB Chicago ECB workshop on Non-Standard Monetary Policy Measures 1 The views in this paper are solely the responsibility

A Brief Report on Norwegian Business Cycles Statistics, Preliminary draft

A Brief Report on Norwegian Business Cycles Statistics, 198-26. 1 - Preliminary draft Hege Marie Gjefsen - hegemgj@student.sv.uio.no Tord Krogh - tskrogh@gmail.com Marie Norum Lerbak lerbak@gmail.com 28.2.28

A Brief Report on Norwegian Business Cycles Statistics, 198-26. 1 - Preliminary draft Hege Marie Gjefsen - hegemgj@student.sv.uio.no Tord Krogh - tskrogh@gmail.com Marie Norum Lerbak lerbak@gmail.com 28.2.28

Fiscal Multipliers in Recessions. M. Canzoneri, F. Collard, H. Dellas and B. Diba

1 / 52 Fiscal Multipliers in Recessions M. Canzoneri, F. Collard, H. Dellas and B. Diba 2 / 52 Policy Practice Motivation Standard policy practice: Fiscal expansions during recessions as a means of stimulating

1 / 52 Fiscal Multipliers in Recessions M. Canzoneri, F. Collard, H. Dellas and B. Diba 2 / 52 Policy Practice Motivation Standard policy practice: Fiscal expansions during recessions as a means of stimulating

Convertible Bonds and Bank Risk-taking

Natalya Martynova 1 Enrico Perotti 2 European Central Bank Workshop June 26, 2013 1 University of Amsterdam, Tinbergen Institute 2 University of Amsterdam, CEPR and ECB In the credit boom, high leverage

Natalya Martynova 1 Enrico Perotti 2 European Central Bank Workshop June 26, 2013 1 University of Amsterdam, Tinbergen Institute 2 University of Amsterdam, CEPR and ECB In the credit boom, high leverage

Speculative Growth and Overreaction to Technology Shocks

Speculative Growth and Overreaction to Technology Shocks Kevin J. Lansing Federal Reserve Bank of San Francisco June 5, 2009 Overview Excess volatility of asset prices may a ect capital accumulation, growth,

Speculative Growth and Overreaction to Technology Shocks Kevin J. Lansing Federal Reserve Bank of San Francisco June 5, 2009 Overview Excess volatility of asset prices may a ect capital accumulation, growth,

Financial Frictions in Macroeconomics. Lawrence J. Christiano Northwestern University

Financial Frictions in Macroeconomics Lawrence J. Christiano Northwestern University Balance Sheet, Financial System Assets Liabilities Bank loans Securities, etc. Bank Debt Bank Equity Frictions between

Financial Frictions in Macroeconomics Lawrence J. Christiano Northwestern University Balance Sheet, Financial System Assets Liabilities Bank loans Securities, etc. Bank Debt Bank Equity Frictions between

Credit Shocks and the U.S. Business Cycle. Is This Time Different? Raju Huidrom University of Virginia. Midwest Macro Conference

Credit Shocks and the U.S. Business Cycle: Is This Time Different? Raju Huidrom University of Virginia May 31, 214 Midwest Macro Conference Raju Huidrom Credit Shocks and the U.S. Business Cycle Background

Credit Shocks and the U.S. Business Cycle: Is This Time Different? Raju Huidrom University of Virginia May 31, 214 Midwest Macro Conference Raju Huidrom Credit Shocks and the U.S. Business Cycle Background

A forward-looking model. for time-varying capital requirements. and the New Basel Capital Accord. Chiara Pederzoli Costanza Torricelli

A forward-looking model for time-varying capital requirements and the New Basel Capital Accord Chiara Pederzoli Costanza Torricelli Università di Modena e Reggio Emilia Plan of the presentation: 1) Overview

A forward-looking model for time-varying capital requirements and the New Basel Capital Accord Chiara Pederzoli Costanza Torricelli Università di Modena e Reggio Emilia Plan of the presentation: 1) Overview

US Business Cycle Risk Report

US Business Cycle Risk Report CapitalSpectator.com 15 November 2015 James Picerno, director of research +1.732.710.4750 caps@capitalspectator.com Business Cycle Risk Summary: The Economic Momentum and

US Business Cycle Risk Report CapitalSpectator.com 15 November 2015 James Picerno, director of research +1.732.710.4750 caps@capitalspectator.com Business Cycle Risk Summary: The Economic Momentum and

Macroprudential Policy Analysis for Real Estate Markets in the euro area

Reiner Martin Deputy Head Macroprudential Policies Division European Central Bank Macroprudential Policy Analysis for Real Estate Markets in the euro area Oslo 21 November 2017 Rubric Outline 1 Principles

Reiner Martin Deputy Head Macroprudential Policies Division European Central Bank Macroprudential Policy Analysis for Real Estate Markets in the euro area Oslo 21 November 2017 Rubric Outline 1 Principles

44 ECB HOW HAS MACROECONOMIC UNCERTAINTY IN THE EURO AREA EVOLVED RECENTLY?

Box HOW HAS MACROECONOMIC UNCERTAINTY IN THE EURO AREA EVOLVED RECENTLY? High macroeconomic uncertainty through its likely adverse effect on the spending decisions of both consumers and firms is considered

Box HOW HAS MACROECONOMIC UNCERTAINTY IN THE EURO AREA EVOLVED RECENTLY? High macroeconomic uncertainty through its likely adverse effect on the spending decisions of both consumers and firms is considered

Internet Appendix for: Cyclical Dispersion in Expected Defaults

Internet Appendix for: Cyclical Dispersion in Expected Defaults João F. Gomes Marco Grotteria Jessica Wachter August, 2017 Contents 1 Robustness Tests 2 1.1 Multivariable Forecasting of Macroeconomic Quantities............

Internet Appendix for: Cyclical Dispersion in Expected Defaults João F. Gomes Marco Grotteria Jessica Wachter August, 2017 Contents 1 Robustness Tests 2 1.1 Multivariable Forecasting of Macroeconomic Quantities............

DFAST Modeling and Solution

Regulatory Environment Summary Fallout from the 2008-2009 financial crisis included the emergence of a new regulatory landscape intended to safeguard the U.S. banking system from a systemic collapse. In

Regulatory Environment Summary Fallout from the 2008-2009 financial crisis included the emergence of a new regulatory landscape intended to safeguard the U.S. banking system from a systemic collapse. In

OUTPUT SPILLOVERS FROM FISCAL POLICY

OUTPUT SPILLOVERS FROM FISCAL POLICY Alan J. Auerbach and Yuriy Gorodnichenko University of California, Berkeley January 2013 In this paper, we estimate the cross-country spillover effects of government

OUTPUT SPILLOVERS FROM FISCAL POLICY Alan J. Auerbach and Yuriy Gorodnichenko University of California, Berkeley January 2013 In this paper, we estimate the cross-country spillover effects of government

INTERTEMPORAL ASSET ALLOCATION: THEORY

INTERTEMPORAL ASSET ALLOCATION: THEORY Multi-Period Model The agent acts as a price-taker in asset markets and then chooses today s consumption and asset shares to maximise lifetime utility. This multi-period

INTERTEMPORAL ASSET ALLOCATION: THEORY Multi-Period Model The agent acts as a price-taker in asset markets and then chooses today s consumption and asset shares to maximise lifetime utility. This multi-period

Inflation in the Great Recession and New Keynesian Models

Inflation in the Great Recession and New Keynesian Models Marco Del Negro, Marc Giannoni Federal Reserve Bank of New York Frank Schorfheide University of Pennsylvania BU / FRB of Boston Conference on Macro-Finance

Inflation in the Great Recession and New Keynesian Models Marco Del Negro, Marc Giannoni Federal Reserve Bank of New York Frank Schorfheide University of Pennsylvania BU / FRB of Boston Conference on Macro-Finance

HIGHER CAPITAL IS NOT A SUBSTITUTE FOR STRESS TESTS. Nellie Liang, The Brookings Institution

HIGHER CAPITAL IS NOT A SUBSTITUTE FOR STRESS TESTS Nellie Liang, The Brookings Institution INTRODUCTION One of the key innovations in financial regulation that followed the financial crisis was stress

HIGHER CAPITAL IS NOT A SUBSTITUTE FOR STRESS TESTS Nellie Liang, The Brookings Institution INTRODUCTION One of the key innovations in financial regulation that followed the financial crisis was stress

A Financial Cycle for Albania

A Financial Cycle for Albania Vasilika Kota and Arisa Goxhaj (Saqe) FInancial Stability Department Bank of Albania (First draft) The views expressed herein are of the authors and do not necessarily reflect

A Financial Cycle for Albania Vasilika Kota and Arisa Goxhaj (Saqe) FInancial Stability Department Bank of Albania (First draft) The views expressed herein are of the authors and do not necessarily reflect

RESPONSES TO SURVEY OF

RESPONSES TO SURVEY OF MARKET PARTICIPANTS Markets Group, Federal Reserve Bank of New York RESPONSES TO SURVEY OF a v JANUARY Distributed: 1/18/ Received by: 1/22/ The Survey of Market Participants is

RESPONSES TO SURVEY OF MARKET PARTICIPANTS Markets Group, Federal Reserve Bank of New York RESPONSES TO SURVEY OF a v JANUARY Distributed: 1/18/ Received by: 1/22/ The Survey of Market Participants is