REVENUE RECOGNITION ASU /8/2016. CPAs & ADVISORS ACCOUNTING AND AUDITING UPDATE FOR ARKANSAS HFMA

|

|

|

- Lindsey Paul

- 6 years ago

- Views:

Transcription

1 CPAs & ADVISORS experience clarity // ACCOUNTING AND AUDITING UPDATE FOR ARKANSAS HFMA Tracy Young, CPA Partner, BKD Health Care Group Little Rock REVENUE RECOGNITION ASU

2 FASB/IASB ORIGINAL REVENUE RECOGNITION TIMELINE EFFECTIVE DATE DELAYED ONE YEAR 2

3 WHO S IMPACTED All entities that enter into contracts with customers Public, private, not-for-profit Regardless of industry Contracts with customers, except Lease contracts Insurance contracts Financial instruments Certain guarantees (other than product warranties) Certain nonmonetary exchanges ASU SUMMARY Principle based approach versus rule based Core principle is to recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services Guidance specifies the accounting for an individual contract with a customer; however, as a practical expedient, an entity may apply guidance to a portfolio of contracts (or performance obligations) with similar characteristics if the entity reasonably expects that the effects on the financial statements would not differ materially from applying guidance to individual contracts 3

4 FIVE-STEP MODEL Step 1 Step 2 Step 3 Step 4 Step 5 Identify contract(s) with customer Identify performance obligations Determine transaction price Allocate transaction price to performance obligations Recognize revenue when (or as) performance obligation is satisfied TRANSITION APPROACHES Transition Approach Date of Cumulative Effect Adjustment Full Retrospective Restate for all contracts Apply to all contracts January 1, 2017 Retrospective Using One or More Practical Expedients Cumulative Effect at Date of Adoption Restate for all contracts except contracts covered by practical expedients No contracts restated; reported based on legacy guidance Apply to all contracts January 1, 2017 Apply to all contracts January 1,

5 AICPA REVENUE RECOGNITION TASK FORCES Aerospace and Defense Airlines Asset Management Broker-Dealers Construction Contractors Depository Institutions Gaming Health Care Hospitality Insurance Not-for-profit Oil and Gas Power and Utility Software Telecommunications Timeshare 10// experience clarity 5

6 AICPA REVENUE RECOGNITION TASK FORCES Develop a new Accounting Guide on Revenue Recognition Guide to provide helpful hints and Illustrative examples on how to apply the standard Guidance will not be prescriptive but instead intended to be a resource Full implementation issues will be posted for comment after review from the overall Revenue Recognition Working Group and FinREC List of issues by industry is posted on the AICPA website HEALTH CARE ISSUES IDENTIFIED Revenue recognition for self-pay patients Application of Steps 1 and 3 Application of the portfolio approach Identifying the performance obligation and recognition of refundable and non-refundable entrance fees for CCRC s Significant Financing Components Disclosure requirements as compared to ASU Contract acquisition costs Determination of the transaction price as it relates to thirdparty estimates 6

7 HEALTH CARE IMPLEMENTATION ISSUES SELF-PAY REVENUE Current practice Gross charges, net of self-pay discounts recorded as contractual adjustments Bad debt expense recorded and presented separately as a reduction to net patient service revenue if an entity does not assess collectability New guidance Record revenue at amount entity expects to be entitled to Bad debt expense presented as operating expense Use of judgment in determining what constitutes bad debt versus implicit price concessions No change in charity care guidance STEP 1 IDENTIFY CONTRACT(S) WITH A CUSTOMER 7

8 COLLECTIBILITY Collectibility will be explicit threshold that must be assessed before applying revenue recognition model to contract. Entity must evaluate customer credit risk & conclude that it is probable that it will collect amount of consideration due in exchange for goods or services Assessment is based on both customer s ability & intent to pay as amounts become due Difficult for health care entities to assess CONSIDERATION RECEIVED BEFORE STEP 1 IS MET 8

9 HEALTH CARE IMPLEMENTATION ISSUES STEP 3 OF THE MODEL Transaction price is the amount of consideration an entity expects to be entitled to Transaction price reflects the effects of the following: Variable consideration Significant financing component Consideration payable to a customer Noncash consideration Consideration is variable if explicitly stated, or if Customer has valid expectation arising from entity s customary business practices that entity will accept an amount that is less than the stated contract price Other facts and circumstances indicate that the entity s intention is to offer a price concession to the customer HEALTH CARE IMPLEMENTATION ISSUES PORTFOLIO APPROACH Entities can apply the standard or aspects of it to a portfolio of contracts or performance obligations with similar characteristics (i.e., portfolio approach) Entities must reasonably expect that the financial statement effect of using the portfolio approach will not differ materially from applying the standard on a contract-by-contract basis Key considerations How to apply a portfolio approach How to establish portfolios How to determine effect would not differ materially 9

10 HEALTH CARE IMPLEMENTATION ISSUES PORTFOLIO APPROACH (CONT.) Portfolio approach may be applied to all aspects of the model or only to certain steps If establishing portfolios, an entity will need to use judgment to determine the size, composition and number of portfolios Health care entities may consider segregating by payor class, type of service and other categories An entity also will need to consider materiality and documentation requirements IDENTIFYING THE CONTRACT EXAMPLE Background Hospital provides services to uninsured (self pay) patient in emergency room Hospital has not previously provided medical services to this patient After providing services to patient, Hospital obtains information about the patient s ability and intention to pay Hospital designates the patient to a customer class The standard rate for the services provided are $10,000 Hospital expects to accept a lower amount of consideration for the services provided as such the promised consideration is variable Based on historical cash collections from this customer class and other relevant information about the patient, Hospital determines that it expects to be entitled to $1,000 10

11 IDENTIFYING THE CONTRACT - EXAMPLE Evaluation On the basis of its collection history from patients in this customer class, Hospital concludes it is probable it will collect $1,000 (estimate of variable consideration) Therefore, the contract with the patient has met the requirements of Step 1 and will be accounted for under the model This example is from ASC to 105 SELF PAY REVENUE RECOGNITION ISSUES HC entities need to consider specific facts and circumstances to determine if an enforceable contract exists Currently, there is no concept of cash basis in the standard Medicaid pending status patients Use of historical information Use of portfolio approach Explicit versus Implicit price concessions Day 1 versus Day 2 accounting Where do subsequent changes to variable consideration get reported? Practical implementation 11

12 CONTINUING CARE RETIREMENT COMMUNITIES CCRC CONSIDERATIONS Type A, or Lifecare Contract Includes housing and healthcare services at little or no increase in the monthly fee; these contracts typically provide for the highest entrance and monthly fees as the CCRC absorbs the healthcare risk Type B, or Modified Lifecare Contract Limits the amount of healthcare services that may be accessed without an increase in the monthly fee, e.g., resident may be allowed to access healthcare services at little or no increase in the monthly fee for 60 days, after which the resident would be required to pay a higher fee for healthcare services Type C, or Fee-for-service Contract Requires resident to pay market rates for healthcare services; these contracts typically provide for the lowest entrance and monthly fees as the resident absorbs the healthcare risk Type D, or Rental Contract No entrance fee requirement 12

13 CCRC SPECIFIC CONSIDERATIONS The AICPA Healthcare Revenue Recognition Task Force is analyzing the following primary issues as they relate to CCRCs Accounting for monthly / periodic fees and nonrefundable entrance fees under the different contract types (A, B, C, D), including portfolio versus individual contract approach to revenue recognition Significant financing component considerations for refundable and nonrefundable entrance fees Obligation to provide future services and use of facilities Contract acquisition costs CCRC SPECIFIC CONSIDERATIONS Entrance Fees Determining the performance obligations Allocating the transaction price to multiple performance obligations Consideration of the variable consideration for maintenance fees Satisfying the performance obligation Amortization over the pattern of transfer of goods and services Consideration of Significant Financing component 13

14 OTHER MATTERS DISCLOSURES Disclosures to enable the users to understand the nature, amount, timing and uncertainty of revenue and cash flows from customers An entity shall disaggregate revenue recognized from contracts with customers depending on the nature of that revenue Aggregated amount of the transaction price allocated to performance obligations that are unsatisfied, including methods, inputs and assumptions Timing and satisfaction of performance obligations Entity to disclose both qualitative and quantitative information 14

15 DISCLOSURES Per ASC entities to disclose: Revenue from contracts with customers, including the disaggregation of revenue into appropriate categories Contract balances, including the opening and closing balances of receivables, contract assets and contract liabilities Revenue recognized in the reporting period that was included in the contract liability at the beginning of the period Revenue recognized in the reporting period from performance obligations satisfied Significant judgments and changes in judgments, made in applying the requirements to those contracts FINANCIAL REPORTING 15

16 CONTRACT ACQUISITION COSTS Incremental costs of obtaining a contract Costs the entity incurs that would have not been incurred if the contract was not obtained - Recognize as an asset if the entity to expects to recover those costs Costs that would have been incurred regardless of whether the contract was obtained Expense as incurred Costs to fulfill a contract Costs related directly to a contract (i.e. costs of renewal of an existing contract) Recognize as an asset if costs are expected to be recovered Direct labor, Direct materials, costs charged under a contract CONTRACT ACQUISITION COSTS Costs to fulfill a contract Costs to be expensed as incurred Administrative and General costs unless explicitly chargeable to the customer under the contract Costs of wasted materials, labor or other resources to fulfill the contract Costs related to past performance Costs for which an entity cannot distinguish whether it relates to a performance obligation Practical Expedient recognize as an expense when incurred if the amortization period of the asset is one year or less 16

17 CONTRACT ACQUISITION COSTS Amortization and Impairment Asset should be amortized consistent with the pattern of transfer of the customer services Entity shall update the amortization for significant changes in the pattern of transfer Asset should be evaluated for impairment THIRD PARTY SETTLEMENTS Determination of the transaction price for third party settlements Medicare/Medicaid cost report settlements RAC accruals Risk adjustments for Prepaid Health plans Other Use method which entity expects to better predict the amount of consideration to which it will be entitled Use of Expected Value (probability-weighted amount) Use of Most Likely Amount (single most likely amount in a range of possible considerations) 17

18 STEP 3 OF THE MODEL (CONTINUED) Expected value Sum of the probability-weighted amounts in a range of possible outcomes Most predictive when the transaction has a large number of possible outcomes Most likely amount The single most likely amount in a range of possible outcomes Most predictive when the transaction has two possible outcomes Required to evaluate whether to constrain amounts of variable consideration included in transaction price Objective of the constraint include variable consideration in the transaction price only to the extent it is probable that a significant revenue reversal will not occur Estimates must be updated each reporting period (Proposed ASU with comment date of October 4) 36// experience clarity 18

When another entity is involved in providing goods or services to a customer, an entity that is a principalobtains control of: (a) a good or another asset from the other party")

19 37// experience clarity PRINCIPAL VS. AGENT (ASU ) When another entity is involved in providing goods or services to a customer, an entity that is a principalobtains control of: (a) a good or another asset from the other party that it then transfers to the customer; (b) a right to a service that will be performed by another party, which gives the entity the ability to direct that party to provide the service to the customer on the entity s behalf; or (c) a good or service from the other party that it combines with other goods or services to provide the specified good or service to the customer. 38// experience clarity 19

20 PRINCIPAL VS. AGENT EXAMPLE Entity sells discount vouchers allowing customers discounts at various restaurants. Entity gets 30% of voucher price when sold to a customer and is not obligated to purchase vouchers in advance. Entity assists in resolving customer complaints, but restaurants are responsible for fulfilling obligations Entity concludes that it is an agent Entity records revenue for 30% commission only and not the amount paid by the customer for the voucher. 39// experience clarity PERFORMANCE OBLIGATIONS/LICENSING -ASU An entity s promise to grant a customer a license to intellectual property that has significant standalone functionality (e.g., the ability to process a transaction, perform a function or task, or be played or aired) does not include supporting or maintaining that intellectual property during the license period. REVENUE RECOGNIZED AT POINT IN TIME 2. An entity s promise to grant a customer a license to symbolic intellectual property (that is, intellectual property that does not have significant standalone functionality) includes supporting or maintaining that intellectual property during the license period. REVENUE RECOGNIZED OVER TIME. 40// experience clarity 20

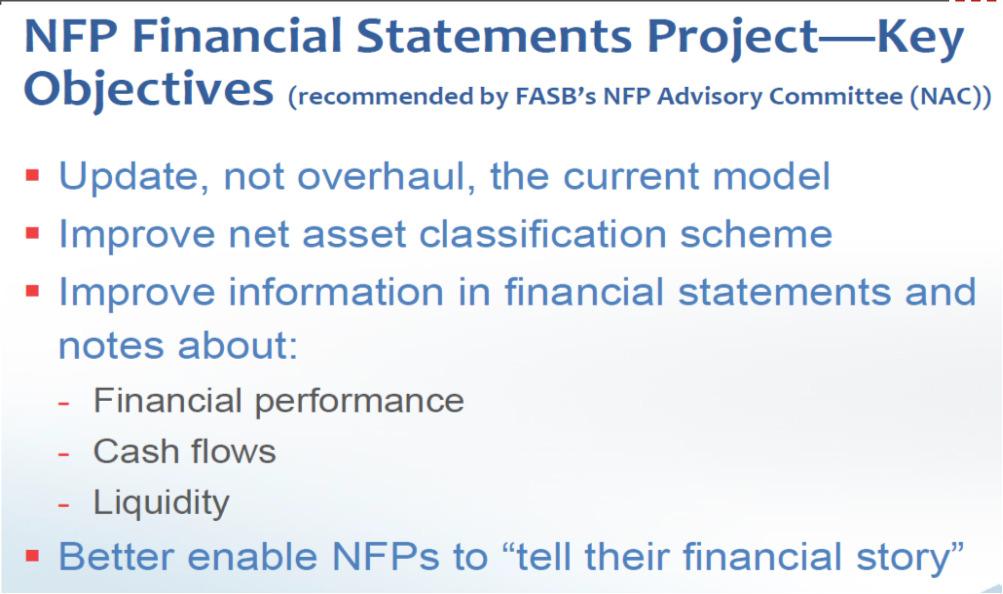

21 NOT-FOR-PROFIT FINANCIAL REPORTING PROJECT (ASU ) 41// experience clarity PERCEIVED WEAKNESSES IN NFP REPORTING Complexity with three net asset classes Confusion regarding statement of cash flows Donors, creditors & other users Difficulty in assessing an entity s liquidity Inconsistent reporting of expenses No clear operating measure defined 21

22 43 44// experience clarity 22

23 45// experience clarity 46// experience clarity 23

24 CURRENT STATEMENT OF FINANCIAL POSITION Not-for-Profit Entity A Statements of Financial Position Years Ended June 30, 20X5 and 20X4 (in thousands) 20X5 20X4 Net Assets Unrestricted $ 115,000 $ 104,000 Temporarily Restricted (Note B) 24,000 25,000 Permanently Restricted (Note C) 142, ,000 Total net assets 282, , PROPOSED STATEMENT OF FINANCIAL POSITION Not-for-Profit Entity A Statements of Financial Position Years Ended June 30, 20X5 and 20X4 (in thousands) 20X5 20X4 Net Assets Without donor restrictions (Note DDD) $ 93,000 $ 74,000 With donor restrictions (Note B) 193, ,000 Total net assets 286, ,

25

26 51 REPORTING OF EXPENSES All NFPs required to report operating expenses by nature & function Options: include in SOA, separate statement or notes Require investment expenses to be netted with investment return Netting limited to external & direct internal expenses 26

27 REPORTING OF EXPENSES Example: F U N C T I O N N A T U R E * Example obtained from FASB EFFECTIVE DATE/TRANSITION-PRIVATE CO. New Lease Accounting Standard 54 27

28 55 NEW VS. EXISTING GUIDANCE: LEASE CLASSIFICATION The lack of explicit bright lines will increase the level of judgment required when classifying a lease particularly for certain highly structured transactions. However, the basis for conclusions acknowledges that one reasonable approach would be to use the bright-line tests Transition reliefs permit an entity to avoid reassessment of lease classification for existing leases at the day of adoption & avoid reassessment of initial direct costs previously capitalized (some of which may no longer qualify for capitalization) 56 28

29 COMPARISON OF LESSEE ACCOUNTING MODELS 57 EFFECT ON BALANCE SHEET 58 29

30 EFFECT ON BALANCE SHEET 59 EFFECT ON INCOME STATEMENT 60 30

31 NEW VS. EXISTING GUIDANCE: SALE-LEASEBACK TRANSACTIONS 61 SALE & LEASEBACK - IMPLICATIONS 62 31

32 63 64// experience clarity 32

33 OVERVIEW OF ASU // experience clarity OVERVIEW OF ASU (CONTINUED) 66// experience clarity 33

")

34 OVERVIEW OF ASU (CONTINUED) 67// experience clarity 68// experience clarity 34

35 ASU HEALTHCARE IMPACT 69// experience clarity ASU HEALTHCARE IMPACT 70// experience clarity 35

36 OVERVIEW OF ASU (CONTINUED) Effective Date & Transition For public business entities for fiscal years, including interim periods within, beginning after December 15, 2017 For all other entities (including NFPs & EBPs) for fiscal years beginning after December 15, 2018 and interim periods within fiscal years beginning after December 15, 2019 Early adoption of certain amendments is permitted, including within an interim period Cumulative-effect adjustment to the BS as of the beginning of the fiscal year of adoption 71// experience clarity 72// experience clarity 36

37 OVERVIEW OF ASU // experience clarity AUDIT STANDARD/GAAP DIFFERENCES 74// experience clarity 37

38 ASU EFFECTIVE DATE 75// experience clarity 76// experience clarity 38

39 ASU // experience clarity ASU // experience clarity 39

40 79// experience clarity ASU FAIR VALUE MEASUREMENT (TOPIC 820): DISCLOSURES FOR INVESTMENTS IN CERTAIN ENTITIES THAT CALCULATE NET ASSET VALUE PER SHARE (OR ITS EQUIVALENT) Issued- April 2015 Summary Remove requirement to categorize within fair value hierarchy all investments for which fair value is measured using net asset value per share practical expedient Remove requirement to make certain disclosures for all investments eligible to be measured at fair value using net asset value per share practical expedient (those disclosures are limited to investments for which entity has elected to measure fair value) 80// experience clarity 40

41 ASU FAIR VALUE MEASUREMENT (TOPIC 820): DISCLOSURES FOR INVESTMENTS IN CERTAIN ENTITIES THAT CALCULATE NET ASSET VALUE PER SHARE (OR ITS EQUIVALENT) Effective Date & Transition Effective for public business entities for fiscal years beginning after December 15, 2015, & interim periods within those fiscal years For all other entities, effective for fiscal years beginning after December 15, 2016, & interim periods within those years Earlier application is permitted Amendments should be applied retrospectively Resources A&A Memo: Not available (remove for external presentations) BKD Thoughtware : FASB Simplifies Fair Value Disclosures 81// experience clarity ASU DEFINED BENEFIT PENSION PLANS (TOPIC 960), DEFINED CONTRIBUTION PENSION PLANS (TOPIC 962), HEALTH AND WELFARE BENEFIT PLANS (TOPIC 965): (PART I) FULLY BENEFIT-RESPONSIVE INVESTMENT CONTRACTS, (PART II) PLAN INVESTMENT DISCLOSURES, (PART III) MEASUREMENT DATE PRACTICAL EXPEDIENT Issued-July 2015 Summary Part I -Fully benefit-responsive Investment Contracts: FBICs would be measured, presented & disclosed only at contract value Part II -Investment Plan Disclosures: (a) Eliminates requirements to disclose (i) individual investments that represent 5 percent or more of net assets available for benefits and (ii) net appreciation or depreciation for investments by general type for both participant-directed investments & nonparticipant-directed investments 82// experience clarity 41

42 ASU DEFINED BENEFIT PENSION PLANS (TOPIC 960), DEFINED CONTRIBUTION PENSION PLANS (TOPIC 962), HEALTH AND WELFARE BENEFIT PLANS (TOPIC 965): (PART I) FULLY BENEFIT-RESPONSIVE INVESTMENT CONTRACTS, (PART II) PLAN INVESTMENT DISCLOSURES, (PART III) MEASUREMENT DATE PRACTICAL EXPEDIENT Effective Date & Transition All amendments are effective for fiscal years beginning after December 15, 2015 Earlier application is permitted Part I & II amendments should be applied retrospectively; Part III amendments should be applied prospectively Resources A&A Memo: Not available (remove for external presentations) BKD Thoughtware : Pending 83// experience clarity 84// experience clarity 42

43 ASU // experience clarity ASU // experience clarity 43

44 ASU // experience clarity 88// experience clarity 44

45 ASU // experience clarity 90// experience clarity 45

46 DONATED PERSONNEL SERVICES (ASU ) Requires recording of all services received from personnel of an affiliate. Services are to be recorded at the cost recorded by the affiliate providing the services (or at fair value of the services if recording at cost overstates the value of the services. Does not apply where recipient entity is charged for the services (at least the direct costs or fair value) HCEs should report expense of services received and an equity transfer below the line for the contribution of the services Effective for years beginning after 6/15/14. 91// experience clarity DISCONTINUED OPERATIONS ASU Reduces the number of disposals that will qualify for discontinued operations treatment New guidance: disposal of a component or group of components that represents a strategic shift that has a major effect on an entity s operations New disclosures for individually material disposals that do NOT qualify for DO treatment. Effective for // experience clarity 46

47 FEDERAL SINGLE AUDIT REQUIREMENT CHANGES Several OMB Circulars replaced with Uniform Guidance in Title 2 CFR Part 200 Single audit threshold increased to $750,000 Major program threshold increased to $750,000 Hospital cost principles not superseded by Uniform Guidance Effective for years beginning after December 31, // experience clarity THANK YOU FOR MORE INFORMATION// For a complete list of our offices and subsidiaries, visit bkd.com or contact: Tracy Young, CPA Partner BKD Health Care Group pyoung@bkd.com 47

REVENUE RECOGNITION ASU /23/2016. CPAs & ADVISORS ACCOUNTING AND AUDITING UPDATE FOR ARKANSAS HFMA

CPAs & ADVISORS experience clarity // ACCOUNTING AND AUDITING UPDATE FOR ARKANSAS HFMA Drew Speed, CPA Partner, Accounting and Auditing Director, Little Rock REVENUE RECOGNITION ASU 2014-09 1 FASB/IASB

CPAs & ADVISORS experience clarity // ACCOUNTING AND AUDITING UPDATE FOR ARKANSAS HFMA Drew Speed, CPA Partner, Accounting and Auditing Director, Little Rock REVENUE RECOGNITION ASU 2014-09 1 FASB/IASB

FASB ASU NO REVENUE FROM CONTRACTS WITH CUSTOMERS (TOPIC 606)

") CPAs & ADVISORS experience clarity // REVENUE RECOGNITION FOR HEALTH CARE PROVIDERS Kimberly McKay, CPA Managing Partner BKD. LLP - Houston FASB ASU NO. 2014-09 REVENUE FROM CONTRACTS WITH CUSTOMERS (TOPIC

CPAs & ADVISORS experience clarity // REVENUE RECOGNITION FOR HEALTH CARE PROVIDERS Kimberly McKay, CPA Managing Partner BKD. LLP - Houston FASB ASU NO. 2014-09 REVENUE FROM CONTRACTS WITH CUSTOMERS (TOPIC

Implementing Revenue Recognition for Health Care Organizations S E P T E M B E R 2 1,

Implementing Revenue Recognition for Health Care Organizations S E P T E M B E R 2 1, 2 0 1 8 INTRODUCTIONS Kimberly McKay, CPA Managing Partner kmckay@bkd.com Implementing Revenue Recognition for Health

Implementing Revenue Recognition for Health Care Organizations S E P T E M B E R 2 1, 2 0 1 8 INTRODUCTIONS Kimberly McKay, CPA Managing Partner kmckay@bkd.com Implementing Revenue Recognition for Health

Implementing Revenue Recognition for Health Care Organizations

Implementing Revenue Recognition for Health Care Organizations AUGUST 6, 2018 TO RECEIVE CPE CREDIT Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader is

Implementing Revenue Recognition for Health Care Organizations AUGUST 6, 2018 TO RECEIVE CPE CREDIT Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader is

REVENUE RECOGNITION FOR HEALTH CARE PROVIDERS

REVENUE RECOGNITION FOR HEALTH CARE PROVIDERS Tracy Young, CPA Partner -BKD, LLP Brent Beaulieu, CPA VP Finance Baptist Health ASU 2014-09 REVENUE FROM CONTRACTS WITH CUSTOMERS Effective for Public Business

REVENUE RECOGNITION FOR HEALTH CARE PROVIDERS Tracy Young, CPA Partner -BKD, LLP Brent Beaulieu, CPA VP Finance Baptist Health ASU 2014-09 REVENUE FROM CONTRACTS WITH CUSTOMERS Effective for Public Business

Implementing Revenue Recognition for Health Care Organizations J A N U A R Y

Implementing Revenue Recognition for Health Care Organizations J A N U A R Y 2 0 1 9 AGENDA 1 Introductions & Objectives 2 Background, Key Principles, & Transition 3 Common Industry Implementation Challenges

Implementing Revenue Recognition for Health Care Organizations J A N U A R Y 2 0 1 9 AGENDA 1 Introductions & Objectives 2 Background, Key Principles, & Transition 3 Common Industry Implementation Challenges

Implementing Revenue Recognition for Health Care Organizations M A R C H 1 8,

Implementing Revenue Recognition for Health Care Organizations M A R C H 1 8, 2 0 1 8 Background & Key Principles ASU 2014-09 REVENUE FROM CONTRACTS WITH CUSTOMERS Effective for Public Business Entities

Implementing Revenue Recognition for Health Care Organizations M A R C H 1 8, 2 0 1 8 Background & Key Principles ASU 2014-09 REVENUE FROM CONTRACTS WITH CUSTOMERS Effective for Public Business Entities

2016 Revenue Recognition Session Parts 1 & 2

2016 AICPA Healthcare Conference 2016 Revenue Recognition Session Parts 1 & 2 Speaker Biographies 25-1 Mike Breen, CPA Mike is an audit partner in KPMG s New York Office. He has experience performing financial

2016 AICPA Healthcare Conference 2016 Revenue Recognition Session Parts 1 & 2 Speaker Biographies 25-1 Mike Breen, CPA Mike is an audit partner in KPMG s New York Office. He has experience performing financial

HFMA Great Lakes Chapter Accounting and Auditing Update February 16, 2018

HFMA Great Lakes Chapter Accounting and Auditing Update February 16, 2018 Who We Are CAROLYN BIELAWSKI, CPA ASSOCIATE Education: Bachelor of Arts in Accounting, Master of Science in Accounting, Michigan

HFMA Great Lakes Chapter Accounting and Auditing Update February 16, 2018 Who We Are CAROLYN BIELAWSKI, CPA ASSOCIATE Education: Bachelor of Arts in Accounting, Master of Science in Accounting, Michigan

d. 8-4, Recognizing a CCRC s performance obligation(s) to provide future services and use of facilities to residents

to provide future services and use of facilities to residents") June 1, 2017 Financial Reporting Center Revenue Recognition Working Draft: Health Care Entities Revenue Recognition Implementation Issue Issue #8-6 Presentation and Disclosure Expected Overall Level of

June 1, 2017 Financial Reporting Center Revenue Recognition Working Draft: Health Care Entities Revenue Recognition Implementation Issue Issue #8-6 Presentation and Disclosure Expected Overall Level of

New Jersey Chapter of HFMA Spring Education Event April 2016 ASC 606, Revenue from Contracts with Customers Overview for Healthcare Providers

New Jersey Chapter of HFMA Spring Education Event April 2016 ASC 606, Revenue from Contracts with Customers Overview for Healthcare Providers How Will Revenue be Recognized Under Contracts? Albert Deana,

New Jersey Chapter of HFMA Spring Education Event April 2016 ASC 606, Revenue from Contracts with Customers Overview for Healthcare Providers How Will Revenue be Recognized Under Contracts? Albert Deana,

Revenue from contracts with customers (ASC 606)

") Financial reporting developments A comprehensive guide Revenue from contracts with customers (ASC 606) Revised August 2017 To our clients and other friends The Financial Accounting Standards Board (FASB

Financial reporting developments A comprehensive guide Revenue from contracts with customers (ASC 606) Revised August 2017 To our clients and other friends The Financial Accounting Standards Board (FASB

Changes to revenue recognition in the health care industry

Changes to revenue recognition in the health care industry Prepared by: Dan Vandenberghe, Partner, RSM US LLP dan.vandenberghe@rsmus.com, +1 612 376 9267 Jay Adkisson, Partner, RSM US LLP jay.adkisson@rsmus.com,

Changes to revenue recognition in the health care industry Prepared by: Dan Vandenberghe, Partner, RSM US LLP dan.vandenberghe@rsmus.com, +1 612 376 9267 Jay Adkisson, Partner, RSM US LLP jay.adkisson@rsmus.com,

Revenue Recognition: A Comprehensive Review for Health Care Entities

Revenue Recognition: A Comprehensive Review for Health Care Entities Table of Contents INTRODUCTION... 4 THE MODEL... 5 SCOPE... 5 CONTRIBUTIONS/GRANTS... 5 COLLABORATIVE ARRANGEMENTS... 6 CHARITY CARE...

Revenue Recognition: A Comprehensive Review for Health Care Entities Table of Contents INTRODUCTION... 4 THE MODEL... 5 SCOPE... 5 CONTRIBUTIONS/GRANTS... 5 COLLABORATIVE ARRANGEMENTS... 6 CHARITY CARE...

Revenue from contracts with customers (ASC 606)

") Financial reporting developments A comprehensive guide Revenue from contracts with customers (ASC 606) Revised August 2016 To our clients and other friends In May 2014, the Financial Accounting Standards

Financial reporting developments A comprehensive guide Revenue from contracts with customers (ASC 606) Revised August 2016 To our clients and other friends In May 2014, the Financial Accounting Standards

AUDIT AND ACCOUNTING UPDATE

AUDIT AND ACCOUNTING UPDATE HFMA FL Regional Education Session - Clearwater November 11, 2016 Presenter Carlos Hernandez Southeast Assurance Leader Carlos.hernandez@rsmus.com 2 Agenda Topic Recent accounting

AUDIT AND ACCOUNTING UPDATE HFMA FL Regional Education Session - Clearwater November 11, 2016 Presenter Carlos Hernandez Southeast Assurance Leader Carlos.hernandez@rsmus.com 2 Agenda Topic Recent accounting

Accounting Standard Updates

Accounting Standard Updates HFMA Spring Conference 2018 Presented by: Kimberly Sokoloff, Health Care Assurance Services Senior Manager Elizabeth Lasnier, Health Care Assurance Services Manager Presenters

Accounting Standard Updates HFMA Spring Conference 2018 Presented by: Kimberly Sokoloff, Health Care Assurance Services Senior Manager Elizabeth Lasnier, Health Care Assurance Services Manager Presenters

Revenue Recognition: A Comprehensive Look at the New Standard

Revenue Recognition: A Comprehensive Look at the New Standard BACKGROUND & SUMMARY... 3 SCOPE... 4 COLLABORATIVE ARRANGEMENTS... 4 THE REVENUE RECOGNITION MODEL... 5 STEP 1 IDENTIFY THE CONTRACT WITH A

Revenue Recognition: A Comprehensive Look at the New Standard BACKGROUND & SUMMARY... 3 SCOPE... 4 COLLABORATIVE ARRANGEMENTS... 4 THE REVENUE RECOGNITION MODEL... 5 STEP 1 IDENTIFY THE CONTRACT WITH A

CPAs & ADVISORS. experience clarity // REVENUE RECOGNITION. FASB/IASB Joint Project

CPAs & ADVISORS experience clarity // REVENUE RECOGNITION FASB/IASB Joint Project May 28, 2014 - ASU 2014-09, Revenue from Contracts with Customers, is released Single, converged, comprehensive approach

CPAs & ADVISORS experience clarity // REVENUE RECOGNITION FASB/IASB Joint Project May 28, 2014 - ASU 2014-09, Revenue from Contracts with Customers, is released Single, converged, comprehensive approach

Health Care. A Focus on Financial Reporting. FASB Revenue Recognition for CHCs: 4/16/2018

Health Care FASB Revenue Recognition for CHCs: A Focus on Financial Reporting Helping Community Health Centers Understand the Changes Needed for Financial Statement Presentation & Disclosure Requirements

Health Care FASB Revenue Recognition for CHCs: A Focus on Financial Reporting Helping Community Health Centers Understand the Changes Needed for Financial Statement Presentation & Disclosure Requirements

WELCOME TO THE AUDITING AND ACCOUNTING UPDATE

WELCOME TO THE AUDITING AND ACCOUNTING UPDATE JANUARY 26, 2018 1 Welcome and introduction You say goodbye and I say hello https://youtu.be/rblyskz_vni 2 2 HFMA A&A UpdaTe Presented by: Michael F. Garczynski,

WELCOME TO THE AUDITING AND ACCOUNTING UPDATE JANUARY 26, 2018 1 Welcome and introduction You say goodbye and I say hello https://youtu.be/rblyskz_vni 2 2 HFMA A&A UpdaTe Presented by: Michael F. Garczynski,

Revenue from contracts with customers. Health care services industry supplement

Note: Since issuing the new revenue standard in May 2014, the FASB and IASB have proposed various amendments to the guidance. This In depth supplement has not been updated to reflect all of the proposed

Note: Since issuing the new revenue standard in May 2014, the FASB and IASB have proposed various amendments to the guidance. This In depth supplement has not been updated to reflect all of the proposed

Agenda. Overview of technical standard Amendments to date Impact on construction accounting Implementation action plan Industry initiatives Q&A

Agenda Overview of technical standard Amendments to date Impact on construction accounting Implementation action plan Industry initiatives Q&A Five Step Model Step 1 Step 2 Step 3 Step 4 Step 5 Identify

Agenda Overview of technical standard Amendments to date Impact on construction accounting Implementation action plan Industry initiatives Q&A Five Step Model Step 1 Step 2 Step 3 Step 4 Step 5 Identify

NARUC: REVENUE RECOGNITION JULIE PETIT AUDIT SENIOR MANAGER BRIAN JONES AUDIT SENIOR MANAGER MONDAY, SEPTEMBER 11 TH, 2017

NARUC: REVENUE RECOGNITION JULIE PETIT AUDIT SENIOR MANAGER BRIAN JONES AUDIT SENIOR MANAGER MONDAY, SEPTEMBER 11 TH, 2017 Mazars USA LLP is an independent member firm of Mazars Group. Mazars USA LLP is

NARUC: REVENUE RECOGNITION JULIE PETIT AUDIT SENIOR MANAGER BRIAN JONES AUDIT SENIOR MANAGER MONDAY, SEPTEMBER 11 TH, 2017 Mazars USA LLP is an independent member firm of Mazars Group. Mazars USA LLP is

Revenue Recognition ASU No

Revenue Recognition ASU No. 2014 09 April 19, 2018 Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC registered investment advisor. CliftonLarsonAllen LLP

Revenue Recognition ASU No. 2014 09 April 19, 2018 Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC registered investment advisor. CliftonLarsonAllen LLP

Government Contractors: Are You Prepared for the New Revenue Standard? Presented by CohnReznick s Government Contracting Industry Practice

Government Contractors: Are You Prepared for the New Revenue Standard? Presented by CohnReznick s Government Contracting Industry Practice PLEASE READ This presentation has been prepared for information

Government Contractors: Are You Prepared for the New Revenue Standard? Presented by CohnReznick s Government Contracting Industry Practice PLEASE READ This presentation has been prepared for information

Aerospace & Defense Spotlight The Converged Revenue Recognition Model Has Landed

September 2014 Aerospace & Defense Spotlight The Converged Revenue Recognition Model Has Landed In This Issue: Background Key Accounting Issues Effective Date and Transition Challenges for A&D Entities

September 2014 Aerospace & Defense Spotlight The Converged Revenue Recognition Model Has Landed In This Issue: Background Key Accounting Issues Effective Date and Transition Challenges for A&D Entities

Up to Speed: Accounting update for Healthcare Providers. David Woodall Assurance Partner - Birmingham, AL

www.pwc.com Up to Speed: Accounting update for Healthcare Providers David Woodall Assurance Partner - Birmingham, AL Sean O Hara Assurance Senior Manager Nashville, TN Agenda FASB update The new revenue

www.pwc.com Up to Speed: Accounting update for Healthcare Providers David Woodall Assurance Partner - Birmingham, AL Sean O Hara Assurance Senior Manager Nashville, TN Agenda FASB update The new revenue

Revenue from Contracts with Customers: The Final Standard

Revenue from Contracts with Customers: The Final Standard 1 TABLE OF CONTENTS Overview and effective date.... 3 Key provisions of the standard.... 3 Transition.... 12 Planning.... 13 How Experis Finance

Revenue from Contracts with Customers: The Final Standard 1 TABLE OF CONTENTS Overview and effective date.... 3 Key provisions of the standard.... 3 Transition.... 12 Planning.... 13 How Experis Finance

REVENUE RECOGNITION IMPLEMENTATION CONSIDERATIONS PRESENTED BY: JASON MYERS

REVENUE RECOGNITION IMPLEMENTATION CONSIDERATIONS PRESENTED BY: JASON MYERS UPDATE ON REVENUE RECOGNITION AICPA Update Technical items Variable consideration Disclosures Examples Implementation Advice

REVENUE RECOGNITION IMPLEMENTATION CONSIDERATIONS PRESENTED BY: JASON MYERS UPDATE ON REVENUE RECOGNITION AICPA Update Technical items Variable consideration Disclosures Examples Implementation Advice

Revenue Recognition: Construction Industry Supplement

Revenue Recognition: Construction Industry Supplement Table of Contents BACKGROUND & SUMMARY... 4 SCOPE... 5 THE REVENUE RECOGNITION MODEL... 5 STEP 1 IDENTIFY THE CONTRACT WITH A CUSTOMER... 6 Collectibility...

Revenue Recognition: Construction Industry Supplement Table of Contents BACKGROUND & SUMMARY... 4 SCOPE... 5 THE REVENUE RECOGNITION MODEL... 5 STEP 1 IDENTIFY THE CONTRACT WITH A CUSTOMER... 6 Collectibility...

ACCOUNTING AND AUDIT UPDATE

ACCOUNTING AND AUDIT UPDATE HFMA FL Regional Education Session - Hollywood January 19, 2017 Presenter Carlos Hernandez Southeast Assurance Leader Carlos.hernandez@rsmus.com 2 Agenda Accounting and Auditing

ACCOUNTING AND AUDIT UPDATE HFMA FL Regional Education Session - Hollywood January 19, 2017 Presenter Carlos Hernandez Southeast Assurance Leader Carlos.hernandez@rsmus.com 2 Agenda Accounting and Auditing

Revenue Recognition: Manufacturers & Distributors Supplement

Revenue Recognition: Manufacturers & Distributors Supplement Table of Contents BACKGROUND & SUMMARY... 3 SCOPE... 5 THE REVENUE RECOGNITION MODEL... 5 STEP 1 IDENTIFY THE CONTRACT WITH A CUSTOMER... 5

Revenue Recognition: Manufacturers & Distributors Supplement Table of Contents BACKGROUND & SUMMARY... 3 SCOPE... 5 THE REVENUE RECOGNITION MODEL... 5 STEP 1 IDENTIFY THE CONTRACT WITH A CUSTOMER... 5

COMPLEXITIES FOR LONG-TERM CARE

The New World of Revenue Recognition, ASC 606 COMPLEXITIES FOR LONG-TERM CARE June 27, 2018 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK

The New World of Revenue Recognition, ASC 606 COMPLEXITIES FOR LONG-TERM CARE June 27, 2018 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK

Accounting and Financial Reporting Developments for Private Companies

Accounting and Financial Reporting Developments for Private Companies THIRD QUARTER 2018 In this update, we highlight some of the more important 2018 third-quarter accounting and financial reporting activities

Accounting and Financial Reporting Developments for Private Companies THIRD QUARTER 2018 In this update, we highlight some of the more important 2018 third-quarter accounting and financial reporting activities

Revenue for healthcare providers

Revenue for healthcare providers The new standard s effective date is coming. US GAAP November 2016 kpmg.com/us/frn b Revenue for healthcare providers Revenue viewed through a new lens Again and again,

Revenue for healthcare providers The new standard s effective date is coming. US GAAP November 2016 kpmg.com/us/frn b Revenue for healthcare providers Revenue viewed through a new lens Again and again,

Revenue Recognition PREPARE NOW. Presented By Mary Jalbert, Principal Michael Whitten, Senior Manager October 3, 2017

Revenue Recognition PREPARE NOW Presented By Mary Jalbert, Principal Michael Whitten, Senior Manager October 3, 2017 Agenda TODAY S OBJECTIVE: A meaningful discussion and exchange of ideas resulting in

Revenue Recognition PREPARE NOW Presented By Mary Jalbert, Principal Michael Whitten, Senior Manager October 3, 2017 Agenda TODAY S OBJECTIVE: A meaningful discussion and exchange of ideas resulting in

Revenue Recognition PREPARE NOW. Presented By Michael Whitten, Senior Manager April 23, 2018

Revenue Recognition PREPARE NOW Presented By Michael Whitten, Senior Manager April 23, 2018 Agenda TODAY S OBJECTIVE: A meaningful discussion and exchange of ideas resulting in tangible steps to apply

Revenue Recognition PREPARE NOW Presented By Michael Whitten, Senior Manager April 23, 2018 Agenda TODAY S OBJECTIVE: A meaningful discussion and exchange of ideas resulting in tangible steps to apply

12/3/2015 UPDATE ON NEW AND PROPOSED FASB AND GASB STANDARDS. Presented by Drew Speed, CPA Partner, BKD, LLP

UPDATE ON NEW AND PROPOSED FASB AND GASB STANDARDS Presented by Drew Speed, CPA Partner, BKD, LLP 1 NEW FASBREPORTING MODEL FOR NON-PROFIT ORGANIZATIONS BACKGROUND Current guidance (FAS 117) issued 20

UPDATE ON NEW AND PROPOSED FASB AND GASB STANDARDS Presented by Drew Speed, CPA Partner, BKD, LLP 1 NEW FASBREPORTING MODEL FOR NON-PROFIT ORGANIZATIONS BACKGROUND Current guidance (FAS 117) issued 20

Revenue Recognition. Task Force. Status of Implementation Issues. AICPA Financial Reporting Center. Revenue Recognition. aicpa.

Task Force of Implementation Issues February, 08 AICPA Financial Reporting Center On May 8, 04, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 04-09, from Contracts

Task Force of Implementation Issues February, 08 AICPA Financial Reporting Center On May 8, 04, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 04-09, from Contracts

REVENUE RECOGNITION PROJECT UPDATED OCTOBER 2013 TOPICAL CONTENTS

REVENUE RECOGNITION PROJECT UPDATED OCTOBER 2013 TOPICAL CONTENTS STEP 1: IDENTIFY THE CONTRACT WITH A CUSTOMER... 3 Contracts with Customers that Contain Nonrecourse, Seller-Based Financing... 3 Contract

REVENUE RECOGNITION PROJECT UPDATED OCTOBER 2013 TOPICAL CONTENTS STEP 1: IDENTIFY THE CONTRACT WITH A CUSTOMER... 3 Contracts with Customers that Contain Nonrecourse, Seller-Based Financing... 3 Contract

Revenue Changes for Franchisors. Revenue Changes for Franchisors

Revenue Changes for Franchisors Table of Contents INTRODUCTION... 4 PORTFOLIO APPROACH... 5 STEP 1: IDENTIFY THE CONTRACT WITH A CUSTOMER... 6 COMBINING CONTRACTS... 7 STEP 2: IDENTIFY PERFORMANCE OBLIGATIONS

Revenue Changes for Franchisors Table of Contents INTRODUCTION... 4 PORTFOLIO APPROACH... 5 STEP 1: IDENTIFY THE CONTRACT WITH A CUSTOMER... 6 COMBINING CONTRACTS... 7 STEP 2: IDENTIFY PERFORMANCE OBLIGATIONS

Defining Issues. Revenue from Contracts with Customers. June 2014, No

Defining Issues June 2014, No. 14-25 Revenue from Contracts with Customers On May 28, 2014, the FASB and the IASB issued a new accounting standard that is intended to improve and converge the financial

Defining Issues June 2014, No. 14-25 Revenue from Contracts with Customers On May 28, 2014, the FASB and the IASB issued a new accounting standard that is intended to improve and converge the financial

Revenue Recognition: A Comprehensive Look at the New Standard for the Construction & Real Estate Industries

Revenue Recognition: A Comprehensive Look at the New Standard for the Construction & Real Estate Industries Table of Contents BACKGROUND & SUMMARY... 3 SCOPE... 4 THE REVENUE RECOGNITION MODEL... 5 STEP

Revenue Recognition: A Comprehensive Look at the New Standard for the Construction & Real Estate Industries Table of Contents BACKGROUND & SUMMARY... 3 SCOPE... 4 THE REVENUE RECOGNITION MODEL... 5 STEP

The new revenue recognition standard technology

No. 2014-16 26 August 2014 Technical Line FASB final guidance The new revenue recognition standard technology In this issue: Overview... 1 Scope, transition and effective date... 3 Summary of the new model...

No. 2014-16 26 August 2014 Technical Line FASB final guidance The new revenue recognition standard technology In this issue: Overview... 1 Scope, transition and effective date... 3 Summary of the new model...

Annual Nonprofit Accounting and Auditing Update

Annual Nonprofit Accounting and Auditing Update July 21, 2016 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee,

Annual Nonprofit Accounting and Auditing Update July 21, 2016 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee,

Accounting Update Seminar: New Revenue Recognition and Lease Accounting

Accounting Update Seminar: New Revenue Recognition and Lease Accounting January 23, 2019 Presented by: Mark Hagander, Principal & Matt Cochran, Principal Revenue from Contracts with Customers (FASB ASC

Accounting Update Seminar: New Revenue Recognition and Lease Accounting January 23, 2019 Presented by: Mark Hagander, Principal & Matt Cochran, Principal Revenue from Contracts with Customers (FASB ASC

New Revenue Recognition Framework: Will Your Entity Be Affected?

New Revenue Recognition Framework: Will Your Entity Be Affected? One of the most significant changes to financial accounting and reporting in recent history is soon to be effective. Reporting entities

New Revenue Recognition Framework: Will Your Entity Be Affected? One of the most significant changes to financial accounting and reporting in recent history is soon to be effective. Reporting entities

Revenue Recognition. Task Force. Status of Implementation Issues. Revenue Recognition. aicpa.org/frc

Task Force of Implementation Issues Financial Reporting Center On May 8, 0, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 0-09, from Contracts with Customers.

Task Force of Implementation Issues Financial Reporting Center On May 8, 0, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 0-09, from Contracts with Customers.

Revenue From Contracts With Customers

September 2017 Revenue From Contracts With Customers Understanding and Implementing the New Rules An article by Scott Lehman, CPA, and Alex J. Wodka, CPA Audit / Tax / Advisory / Risk / Performance Smart

September 2017 Revenue From Contracts With Customers Understanding and Implementing the New Rules An article by Scott Lehman, CPA, and Alex J. Wodka, CPA Audit / Tax / Advisory / Risk / Performance Smart

Revenue from contracts with customers (ASC 606)

") Financial reporting developments A comprehensive guide Revenue from contracts with customers (ASC 606) August 2015 To our clients and other friends In May 2014, the Financial Accounting Standards Board

Financial reporting developments A comprehensive guide Revenue from contracts with customers (ASC 606) August 2015 To our clients and other friends In May 2014, the Financial Accounting Standards Board

Advocate Health Care Network and Subsidiaries FINANCIAL REPORT

Advocate Health Care Network and Subsidiaries FINANCIAL REPORT For the First Quarter Ended March 31, 2018 Cautionary Statement Regarding Forward Looking Statements in this Quarterly Financial Report This

Advocate Health Care Network and Subsidiaries FINANCIAL REPORT For the First Quarter Ended March 31, 2018 Cautionary Statement Regarding Forward Looking Statements in this Quarterly Financial Report This

Revenue from Contracts with Customers

Grant Thornton August 2017 Revenue from Contracts with Customers Navigating the guidance in ASC 606 and ASC 340-40 This publication was created for general information purposes, and does not constitute

Grant Thornton August 2017 Revenue from Contracts with Customers Navigating the guidance in ASC 606 and ASC 340-40 This publication was created for general information purposes, and does not constitute

Media & Entertainment Spotlight Navigating the New Revenue Standard

July 2014 Media & Entertainment Spotlight Navigating the New Revenue Standard In This Issue: Background Key Accounting Issues Effective Date and Transition Transition Considerations Thinking Ahead The

July 2014 Media & Entertainment Spotlight Navigating the New Revenue Standard In This Issue: Background Key Accounting Issues Effective Date and Transition Transition Considerations Thinking Ahead The

Technical Line FASB final guidance

No. 2017-14 22 June 2017 Technical Line FASB final guidance How the new revenue standard affects telecommunications entities In this issue: Overview... 1 Contract term... 2 Identifying performance obligations

No. 2017-14 22 June 2017 Technical Line FASB final guidance How the new revenue standard affects telecommunications entities In this issue: Overview... 1 Contract term... 2 Identifying performance obligations

Revenue Recognition: A Comprehensive Update on the Joint Project

The Dbriefs Financial Reporting series presents: Revenue Recognition: A Comprehensive Update on the Joint Project Bob Uhl, Deloitte & Touche LLP Mark Crowley, Deloitte & Touche LLP Bryan Anderson, Deloitte

The Dbriefs Financial Reporting series presents: Revenue Recognition: A Comprehensive Update on the Joint Project Bob Uhl, Deloitte & Touche LLP Mark Crowley, Deloitte & Touche LLP Bryan Anderson, Deloitte

Accounting and financial reporting activities for private companies

Accounting and financial reporting activities for private companies SECOND-QUARTER 2018 In this update, we highlight some of the more important 2018 second-quarter accounting and financial reporting activities

Accounting and financial reporting activities for private companies SECOND-QUARTER 2018 In this update, we highlight some of the more important 2018 second-quarter accounting and financial reporting activities

Implementing the New Revenue Recognition Standards Under ASC 606 Designing an Implementation Plan to Minimize Financial and Operational Upheaval

Implementing the New Revenue Recognition Standards Under ASC 606 Designing an Implementation Plan to Minimize Financial and Operational Upheaval MONDAY, DECEMBER 21, 2015, 1:00-2:50 pm Eastern IMPORTANT

Implementing the New Revenue Recognition Standards Under ASC 606 Designing an Implementation Plan to Minimize Financial and Operational Upheaval MONDAY, DECEMBER 21, 2015, 1:00-2:50 pm Eastern IMPORTANT

Interim Unaudited Consolidated Financial Statements and Other Information

Interim Unaudited Consolidated Financial Statements and Other Information For The Period Ended March 31, 2018 The Cleveland Clinic Foundation d.b.a. Cleveland Clinic Health System INTERIM UNAUDITED CONSOLIDATED

Interim Unaudited Consolidated Financial Statements and Other Information For The Period Ended March 31, 2018 The Cleveland Clinic Foundation d.b.a. Cleveland Clinic Health System INTERIM UNAUDITED CONSOLIDATED

Laurel Lake Retirement Community, Inc. and Subsidiary YEARS ENDED DECEMBER 31, 2018 AND 2017

Laurel Lake Retirement Community, Inc. and Subsidiary CONSOLIDATED FINANCIAL STATEMENTS CONTENTS Independent auditor s report 1 Financial statement: Consolidated statements of financial position 2 Consolidated

Laurel Lake Retirement Community, Inc. and Subsidiary CONSOLIDATED FINANCIAL STATEMENTS CONTENTS Independent auditor s report 1 Financial statement: Consolidated statements of financial position 2 Consolidated

Technical Line FASB final guidance

No. 2017-20 29 June 2017 Technical Line FASB final guidance How the new revenue standard affects asset managers In this issue: Overview... 1 Background... 2 Identifying the contract with a customer...

No. 2017-20 29 June 2017 Technical Line FASB final guidance How the new revenue standard affects asset managers In this issue: Overview... 1 Background... 2 Identifying the contract with a customer...

Power & Utilities Spotlight Generating a Discussion About the FASB s New Revenue Standard

August 2014 Power & Utilities Spotlight Generating a Discussion About the FASB s New Revenue Standard In This Issue: Background Key Accounting Issues Effective Date and Transition Implementation Challenges

August 2014 Power & Utilities Spotlight Generating a Discussion About the FASB s New Revenue Standard In This Issue: Background Key Accounting Issues Effective Date and Transition Implementation Challenges

Technical Line FASB final guidance

No. 2017-22 Updated 4 December 2017 Technical Line FASB final guidance How the new revenue standard affects life sciences entities In this issue: Overview... 1 Collaborative arrangements... 2 Effect of

No. 2017-22 Updated 4 December 2017 Technical Line FASB final guidance How the new revenue standard affects life sciences entities In this issue: Overview... 1 Collaborative arrangements... 2 Effect of

LA FAMILIA MEDICAL CENTER FINANCIAL STATEMENTS AND REPORT OF INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS

LA FAMILIA MEDICAL CENTER FINANCIAL STATEMENTS AND REPORT OF INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS June 30, 2016 and 2015 (Restated) CERTIFIED PUBLIC CERTIFIED ACCOUNTANTS PUBLIC ACCOUN CONSULTANTS

LA FAMILIA MEDICAL CENTER FINANCIAL STATEMENTS AND REPORT OF INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS June 30, 2016 and 2015 (Restated) CERTIFIED PUBLIC CERTIFIED ACCOUNTANTS PUBLIC ACCOUN CONSULTANTS

REVENUE RECOGNITION FOR BROKER-DEALERS AND INVESTMENT ADVISERS

REVENUE RECOGNITION FOR BROKER-DEALERS AND INVESTMENT ADVISERS December 7, 2017 RSM US LLP. All Rights Reserved. Your instructors Tracy Whetstone Partner, National Professional Standards Group Chicago,

REVENUE RECOGNITION FOR BROKER-DEALERS AND INVESTMENT ADVISERS December 7, 2017 RSM US LLP. All Rights Reserved. Your instructors Tracy Whetstone Partner, National Professional Standards Group Chicago,

Technical Line FASB final guidance

No. 2016-26 27 July 2017 Technical Line FASB final guidance How the new revenue recognition standard affects automotive OEMs In this issue: Overview... 1 Vehicle sales... 2 Sales incentives... 2 Free goods

No. 2016-26 27 July 2017 Technical Line FASB final guidance How the new revenue recognition standard affects automotive OEMs In this issue: Overview... 1 Vehicle sales... 2 Sales incentives... 2 Free goods

AGA Accounting Principles Committee

www.pwc.com/us/utilities AGA Accounting Principles Committee ASU 2014-09: REVENUE FROM CONTRACTS WITH CUSTOMERS (TOPIC 606) Presenter and Agenda Presenter: Lucas Carpenter U.S. Power & Utilities Practice

www.pwc.com/us/utilities AGA Accounting Principles Committee ASU 2014-09: REVENUE FROM CONTRACTS WITH CUSTOMERS (TOPIC 606) Presenter and Agenda Presenter: Lucas Carpenter U.S. Power & Utilities Practice

A&A UPDATE 2018 RECENTLY ISSUED PRONOUNCEMENTS 10/11/2018. ASU Intangibles Goodwill and Other Internal-Use Software (Subtopic )

") A&A UPDATE 2018 RECENTLY ISSUED PRONOUNCEMENTS Pronouncement ASU 2018-15 Intangibles Goodwill and Other Internal-Use Software (Subtopic 350-40) Effective Date December 31, 2019 public; December 31, 2020

A&A UPDATE 2018 RECENTLY ISSUED PRONOUNCEMENTS Pronouncement ASU 2018-15 Intangibles Goodwill and Other Internal-Use Software (Subtopic 350-40) Effective Date December 31, 2019 public; December 31, 2020

The New Revenue Standard State of the Industry and Prevailing Approaches for Adoption Where are we today and what s to come?

The New Revenue Standard Where are we today and what s to come? June 26, 2017 Speaking with you today Grant Casner Grant has been with Deloitte for over 14 years and advises companies on complex accounting

The New Revenue Standard Where are we today and what s to come? June 26, 2017 Speaking with you today Grant Casner Grant has been with Deloitte for over 14 years and advises companies on complex accounting

ASC Topic 606. Revenue Recognition It s Here. Now What?

It s Here. Now What? By Nancy Rix, Mark F. Wille and Mark Dauberman ASC Topic 606 It took more than 11 years for the Financial Accounting Standards Board and the International Accounting Standards Board

It s Here. Now What? By Nancy Rix, Mark F. Wille and Mark Dauberman ASC Topic 606 It took more than 11 years for the Financial Accounting Standards Board and the International Accounting Standards Board

New Guidance for Recording Contributions, Grants and Contracts

New Guidance for Recording Contributions, Grants and Contracts Trevor W. Williams, CPA Nonprofit Audit Partner Gelman, Rosenberg & Freedman CPAs twilliams@grfcpa.com 301-951-9090 Why? Revenue is a key

New Guidance for Recording Contributions, Grants and Contracts Trevor W. Williams, CPA Nonprofit Audit Partner Gelman, Rosenberg & Freedman CPAs twilliams@grfcpa.com 301-951-9090 Why? Revenue is a key

FASB Revenue Recognition - Deep dive into impact to private institutions. Katie Thornton, Robb Rose

FASB Revenue Recognition - Deep dive into impact to private institutions Katie Thornton, Robb Rose 1 FASB Revenue Recognition FASB ASU 2014-09 Revenue from Contracts with Customers Retrospectively to each

FASB Revenue Recognition - Deep dive into impact to private institutions Katie Thornton, Robb Rose 1 FASB Revenue Recognition FASB ASU 2014-09 Revenue from Contracts with Customers Retrospectively to each

Mount Nittany Health System and Affiliates d/b/a Mount Nittany Health

Mount Nittany Health System and Affiliates d/b/a Mount Nittany Health Consolidated Financial Statements and Supplementary Information Table of Contents Page Independent Auditors Report 1 Financial Statements

Mount Nittany Health System and Affiliates d/b/a Mount Nittany Health Consolidated Financial Statements and Supplementary Information Table of Contents Page Independent Auditors Report 1 Financial Statements

Life Sciences Accounting and Financial Reporting Update Interpretive Guidance on Revenue Recognition Under ASC 606

Life Sciences Accounting and Financial Reporting Update Interpretive Guidance on Revenue Recognition Under ASC 606 March 2017 Revenue Recognition Background In May 2014, the FASB 1 and IASB issued their

Life Sciences Accounting and Financial Reporting Update Interpretive Guidance on Revenue Recognition Under ASC 606 March 2017 Revenue Recognition Background In May 2014, the FASB 1 and IASB issued their

Speaker Bio Cline Comer

AICPA Revision Project Audit and Accounting Guide, Health Care Organizations FICPA Annual Health Care Conference April 28-29, 2011 C. Cline Comer, CPA 1 Speaker Bio Cline Comer Cline Comer is a Partner

AICPA Revision Project Audit and Accounting Guide, Health Care Organizations FICPA Annual Health Care Conference April 28-29, 2011 C. Cline Comer, CPA 1 Speaker Bio Cline Comer Cline Comer is a Partner

OBLIGATED GROUP FINANCIAL STATEMENT (UNAUDITED)

") OBLIGATED GROUP FINANCIAL STATEMENT (UNAUDITED) 3 rd QUARTER JUNE 2018 Obligated Group Financial Statements and Other Financial Information (Unaudited) For the Quarter and Nine Months Ended June 30, 2018

OBLIGATED GROUP FINANCIAL STATEMENT (UNAUDITED) 3 rd QUARTER JUNE 2018 Obligated Group Financial Statements and Other Financial Information (Unaudited) For the Quarter and Nine Months Ended June 30, 2018

Accounting Standards Updates on the Horizon: What You Need to Know

Accounting Standards Updates on the Horizon: What You Need to Know Presenters Frank Jakosz, CPA, CGMA Partner-in-Charge Not-for-Profit and Higher Education Practices Sikich LLP Melisa Galasso, CPA, CGMA

Accounting Standards Updates on the Horizon: What You Need to Know Presenters Frank Jakosz, CPA, CGMA Partner-in-Charge Not-for-Profit and Higher Education Practices Sikich LLP Melisa Galasso, CPA, CGMA

Aurora Health Care, Inc. and Affiliates

Aurora Health Care, Inc. and Affiliates Consolidated Financial Statements as of and for the Years Ended December 31, 2017 and 2016, and Independent Auditors' Report AURORA HEALTH CARE, INC. AND AFFILIATES

Aurora Health Care, Inc. and Affiliates Consolidated Financial Statements as of and for the Years Ended December 31, 2017 and 2016, and Independent Auditors' Report AURORA HEALTH CARE, INC. AND AFFILIATES

Financial Reporting Brief: Roadmap to Understanding the New Revenue Recognition Standards

September 2016 Financial Reporting Center Financial Reporting Brief: Roadmap to Understanding the New Revenue Recognition Standards In May 2014, FASB issued Accounting Standards Update (ASU) 2014-09, Revenue

September 2016 Financial Reporting Center Financial Reporting Brief: Roadmap to Understanding the New Revenue Recognition Standards In May 2014, FASB issued Accounting Standards Update (ASU) 2014-09, Revenue

Agenda / Learning Objectives

Audit and Accounting Update: Navigating Uncharted Waters Tyler Bernier, CPA, CHFP August 18, 2016 Agenda / Learning Objectives Understand significant FASB and GASB Standards changes Consider the effects

Audit and Accounting Update: Navigating Uncharted Waters Tyler Bernier, CPA, CHFP August 18, 2016 Agenda / Learning Objectives Understand significant FASB and GASB Standards changes Consider the effects

Hallmark Health Corporation and Affiliates

Hallmark Health Corporation and Affiliates Consolidated Financial Statements as of and for the Years Ended September 30, 2016 and 2015, Schedule of Expenditures of Federal Awards for the Year Ended September

Hallmark Health Corporation and Affiliates Consolidated Financial Statements as of and for the Years Ended September 30, 2016 and 2015, Schedule of Expenditures of Federal Awards for the Year Ended September

Child Inc. Financial Report and Supplementary Information April 30, 2018

Financial Report and Supplementary Information April 30, 2018 Contents Independent auditor s report 1-2 Financial statements Statements of financial position 3 Statements of activities 4-5 Statements of

Financial Report and Supplementary Information April 30, 2018 Contents Independent auditor s report 1-2 Financial statements Statements of financial position 3 Statements of activities 4-5 Statements of

National Insurance Producer Registry. Financial Report December 31, 2017

National Insurance Producer Registry Financial Report December 31, 2017 Contents Independent auditor s report 1 Financial statements Statements of financial position 2 Statements of activities 3 Statements

National Insurance Producer Registry Financial Report December 31, 2017 Contents Independent auditor s report 1 Financial statements Statements of financial position 2 Statements of activities 3 Statements

Hampden-Sydney College and Affiliates. Consolidated Financial and Compliance Report Year Ended June 30, 2016

Hampden-Sydney College and Affiliates Consolidated Financial and Compliance Report Year Ended June 30, 2016 Contents Financial section Independent auditor s report 1-2 Consolidated financial statements

Hampden-Sydney College and Affiliates Consolidated Financial and Compliance Report Year Ended June 30, 2016 Contents Financial section Independent auditor s report 1-2 Consolidated financial statements

I N T E R I M U N A U D I T E D C O N S O L I D A T E D F I N A N C I A L S T A T E M E N T S A N D S U P P L E M E N T A R Y I N F O R M A T I O N

I N T E R I M U N A U D I T E D C O N S O L I D A T E D F I N A N C I A L S T A T E M E N T S A N D S U P P L E M E N T A R Y I N F O R M A T I O N Baptist Health Care Corporation and Subsidiaries For

I N T E R I M U N A U D I T E D C O N S O L I D A T E D F I N A N C I A L S T A T E M E N T S A N D S U P P L E M E N T A R Y I N F O R M A T I O N Baptist Health Care Corporation and Subsidiaries For

Revenue from Contracts with Customers (Topic 606)

") No. 2016-12 May 2016 Revenue from Contracts with Customers (Topic 606) Narrow-Scope Improvements and Practical Expedients An Amendment of the FASB Accounting Standards Codification The FASB Accounting

No. 2016-12 May 2016 Revenue from Contracts with Customers (Topic 606) Narrow-Scope Improvements and Practical Expedients An Amendment of the FASB Accounting Standards Codification The FASB Accounting

The Cooper Health System Years Ended December 31, 2015 and 2014 With Report of Independent Auditors

C ONSOLIDATED F INANCIAL S TATEMENTS AND S UPPLEMENTARY I NFORMATION The Cooper Health System Years Ended December 31, 2015 and 2014 With Report of Independent Auditors Ernst & Young LLP Consolidated Financial

C ONSOLIDATED F INANCIAL S TATEMENTS AND S UPPLEMENTARY I NFORMATION The Cooper Health System Years Ended December 31, 2015 and 2014 With Report of Independent Auditors Ernst & Young LLP Consolidated Financial

SIGNIFICANT ACCOUNTING & REPORTING MATTERS FIRST QUARTER 2017

SIGNIFICANT ACCOUNTING & REPORTING MATTERS FIRST QUARTER 2017 Significant Accounting & Reporting Matters First Quarter 2017 2 TABLE OF CONTENTS Financial Accounting Standards Board (FASB)... 3 Final FASB

SIGNIFICANT ACCOUNTING & REPORTING MATTERS FIRST QUARTER 2017 Significant Accounting & Reporting Matters First Quarter 2017 2 TABLE OF CONTENTS Financial Accounting Standards Board (FASB)... 3 Final FASB

New Developments Summary

June 5, 2014 NDS 2014-06 New Developments Summary A shift in the top line The new global revenue standard is here! Summary After dedicating many years to its development, the FASB and the IASB have issued

June 5, 2014 NDS 2014-06 New Developments Summary A shift in the top line The new global revenue standard is here! Summary After dedicating many years to its development, the FASB and the IASB have issued

ED revenue recognition from contracts with customers

ED revenue recognition from contracts with customers An overview of the revised proposals 2 October 2012 Disclaimer This presentation contains information in summary form and is therefore not intended

ED revenue recognition from contracts with customers An overview of the revised proposals 2 October 2012 Disclaimer This presentation contains information in summary form and is therefore not intended

Aurora Health Care, Inc. and Affiliates

Aurora Health Care, Inc. and Affiliates Consolidated Financial Statements as of and for the Years Ended December 31, 2016 and 2015, and Independent Auditors' Report AURORA HEALTH CARE, INC. AND AFFILIATES

Aurora Health Care, Inc. and Affiliates Consolidated Financial Statements as of and for the Years Ended December 31, 2016 and 2015, and Independent Auditors' Report AURORA HEALTH CARE, INC. AND AFFILIATES

Key Differences Between ASC (Formerly SOP 81-1) and ASC 606

and ASC 606") Aerospace & Defense Spotlight February 2019 Key Differences Between ASC 605-35 (Formerly SOP 81-1) and ASC 606 The Bottom Line In May 2014, the FASB and the International Accounting Standards Board (IASB

Aerospace & Defense Spotlight February 2019 Key Differences Between ASC 605-35 (Formerly SOP 81-1) and ASC 606 The Bottom Line In May 2014, the FASB and the International Accounting Standards Board (IASB

Revenue for the engineering and construction industry

Revenue for the engineering and construction industry The new standard s effective date is coming. US GAAP December 2016 kpmg.com/us/frn b Revenue for the engineering and construction industry Revenue

Revenue for the engineering and construction industry The new standard s effective date is coming. US GAAP December 2016 kpmg.com/us/frn b Revenue for the engineering and construction industry Revenue

I N T E R I M U N A U D I T E D C O N S O L I D A T E D F I N A N C I A L S T A T E M E N T S A N D S U P P L E M E N T A R Y I N F O R M A T I O N

I N T E R I M U N A U D I T E D C O N S O L I D A T E D F I N A N C I A L S T A T E M E N T S A N D S U P P L E M E N T A R Y I N F O R M A T I O N Baptist Health Care Corporation and Subsidiaries For

I N T E R I M U N A U D I T E D C O N S O L I D A T E D F I N A N C I A L S T A T E M E N T S A N D S U P P L E M E N T A R Y I N F O R M A T I O N Baptist Health Care Corporation and Subsidiaries For

Revenue Recognition, Including Implicit Price Concession and Bad Debt Considerations, for Healthcare Organizations: Accounting Issues and Trends

Revenue Recognition, Including Implicit Price Concession and Bad Debt Considerations, for Healthcare Organizations: Accounting Issues and Trends Principles and Practices Board Issue Analysis January 2019

Revenue Recognition, Including Implicit Price Concession and Bad Debt Considerations, for Healthcare Organizations: Accounting Issues and Trends Principles and Practices Board Issue Analysis January 2019

Clarity in financial reporting

A&A Accounting Technical October 2017 Clarity in financial reporting AASB s new income recognition requirements for not-for-profit entities CONTENT 1. Introduction 2. Comparison of income recognition model

A&A Accounting Technical October 2017 Clarity in financial reporting AASB s new income recognition requirements for not-for-profit entities CONTENT 1. Introduction 2. Comparison of income recognition model

The New Health Care Audit Guide And Other Current Topics in Health Care Accounting and Reporting Part 1

The New Health Care Audit Guide And Other Current Topics in Health Care Accounting and Reporting Part 1 FICPA Health Care Conference April 26, 2012 Cline Comer 1 1 Outline Part I AICPA Health Care Audit

The New Health Care Audit Guide And Other Current Topics in Health Care Accounting and Reporting Part 1 FICPA Health Care Conference April 26, 2012 Cline Comer 1 1 Outline Part I AICPA Health Care Audit

SHEPPARD AND ENOCH PRATT FOUNDATION, INC. AND SUBSIDIARIES. June 30, 2016 and (With Independent Auditors Report Thereon)

") Consolidated Financial Statements and Supplementary Information (With Independent Auditors Report Thereon) Table of Contents Page Independent Auditors Report 1 Consolidated Financial Statements: Consolidated

Consolidated Financial Statements and Supplementary Information (With Independent Auditors Report Thereon) Table of Contents Page Independent Auditors Report 1 Consolidated Financial Statements: Consolidated

Not-for-Profit Conference A&A Update for NFPs

Not-for-Profit Conference A&A Update for NFPs James Schmutte July 24, 2014 This session focuses on recent and developing activities of the four standard setters (FASB, AICPA, OMB and GAO) that impact nonprofit

Not-for-Profit Conference A&A Update for NFPs James Schmutte July 24, 2014 This session focuses on recent and developing activities of the four standard setters (FASB, AICPA, OMB and GAO) that impact nonprofit

ASC 606 REVENUE RECOGNITION. Everything you need to know now

ASC 606 REVENUE RECOGNITION Everything you need to know now TOPICS 03 04 07 14 21 31 39 48 54 57 61 66 67 Introduction A revenue recognition primer Identifying the contract Identifying performance obligations

ASC 606 REVENUE RECOGNITION Everything you need to know now TOPICS 03 04 07 14 21 31 39 48 54 57 61 66 67 Introduction A revenue recognition primer Identifying the contract Identifying performance obligations