Implementing Revenue Recognition for Health Care Organizations M A R C H 1 8,

|

|

|

- Evan Moore

- 5 years ago

- Views:

Transcription

1 Implementing Revenue Recognition for Health Care Organizations M A R C H 1 8,

2 Background & Key Principles

3 ASU REVENUE FROM CONTRACTS WITH CUSTOMERS Effective for Public Business Entities (& not-for-profit entities that are conduit debt obligors) in fiscal years & interim periods beginning after December 15, 2017 Effective for all other entities in fiscal years beginning after December 15, 2018 Principles-based approach instead of a rules-based approach

4 OBJECTIVES OF THE NEW REVENUE STANDARD Remove inconsistencies & weaknesses in existing requirements to improve comparability Provide a more robust framework for addressing revenue issues FASB/IASB* converged standard Provide more useful information through improved disclosure requirements Simplify the preparation of financial statements by reducing the number of requirements by having one revenue framework *IASB: International Accounting Standards Board/FASB: Financial Accounting Standards Board

5 ASU REVENUE FROM CONTRACTS WITH CUSTOMERS This ASU superseded health care industry-specific guidance & substantially all existing revenue recognition guidance & added significant interim & annual disclosures PROMISED GOODS OR SERVICES TO CUSTOMERS CORE PRINCIPLE recognizing revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services CONSIDERATION TO WHICH THE ENTITY EXPECTS TO BE ENTITLED

6 NEW REVENUE RECOGNITION PROCESS Identify contract with a customer Identify performance obligations Determine the transaction price Allocate the transaction price Recognize revenue when/as a performance obligation is satisfied

7 ASU REVENUE FROM CONTRACTS WITH CUSTOMERS SCOPE OF NEW STANDARD All entities that enter into contracts with customers Public, private, not-for-profit Regardless of industry EXCEPTIONS Lease contracts Insurance contracts Financial instruments Guarantees Nonmonetary exchanges in the same line of business to facilitate sales to customers EXCLUSIONS Contributions Collaborative agreements 7

8 ASU REVENUE FROM CONTRACTS WITH CUSTOMERS Insurance Contract Exception Entities that fall under ASC 944: Financial Services Insurance Entities are excluded However Entities that fall under ASC 954: Health Care Entities are in scope & so their insurance-related revenues need to be considered Arrangements seen within health care entities that are in-scope include the following examples Claims handling/aso arrangements Capitation & prepaid arrangements 8

9 ASU REVENUE FROM CONTRACTS WITH CUSTOMERS Contributions & Grants Exclusion While excluded from ASU , new guidance was issued recently On June 21, 2018, the FASB Issued ASU , Clarifying the Scope & the Accounting Guidance for Contributions Received & Contributions Made 9

10 Transition Methods & Guidance

11 TRANSITION APPROACHES *assumes a public entity with a December 31 year-end Transition Approach Date of Cumulative Effect Adjustment* Full Retrospective Full Retrospective Using One or More Practical Expedients Modified Retrospective Restate for all contracts Restate for all contracts except contracts covered by practical expedients No contracts restated; reported based on legacy guidance Apply to all contracts January 1, 2017 Apply to all contracts January 1, 2017 Apply to all contracts January 1,

12 12 TRANSITION ELECTIONS PUBLIC COMPANIES

13 TRANSITION HELP FASB/IASB AICPA SEC TRG Advises the Boards Does not have standard-setting authority AICPA Financial Reporting Executive Committee (FinREC) AICPA Revenue Recognition Working Group AICPA 16 Industry Task Forces (RRTF) Focus on consistent application Focus on accounting questions that may require standard setting Focus on internal controls, systems & processes

14 AICPA REVENUE RECOGNITION TASK FORCES Aerospace & Defense Airlines Asset Management Broker-Dealers Construction Contractors Depository Institutions Gaming Health Care Hospitality Insurance Not-for-profit Oil & Gas Power & Utility Software Telecommunications Timeshare

15 AICPA REVENUE RECOGNITION TASK FORCES Develop a new Accounting Guide on Revenue Recognition Guide to provide helpful hints & illustrative examples on how to apply the standard Guidance will not be prescriptive but instead is intended to be a resource Full implementation issues are posted for comment after review from the overall Revenue Recognition Working Group & FinREC List of issues for the health care industry is posted on the AICPA website

16 HEALTH CARE ISSUES IDENTIFIED BY THE AICPA REVENUE RECOGNITION TASK FORCE Issues identified & finalized Revenue recognition for self-pay patients Application of Steps 1 & 3 Application of the portfolio approach Disclosure requirements Performance obligations (other than CCRCs) Third-party estimates Contract acquisition costs Risk sharing arrangements Identifying the performance obligation & recognition of refundable & nonrefundable entrance fees for CCRCs, including significant financing component considerations & future service obligations

17 HEALTH CARE ISSUES BEING CONSIDERED BY HFMA PRINCIPLES & PRACTICES BOARD Capitation revenue Update of HFMA Statement 15 on Bad Debt & Charity Care Medicaid supplemental payment programs The effect of revenue recognition on Medicare cost reporting

18 Common Industry Implementation Challenges

19 1 STEP 1 IDENTIFY CONTRACT(S) WITH A CUSTOMER A legally enforceable contract can be written, oral or implied by an entity s customary business practices, & needs to meet all of the following requirements It has commercial substance The parties have approved the contract & are committed to their obligations The entity can identify each party s rights regarding goods or services The entity can identify the payment terms for the goods or services It is probable the entity will collect the amount of consideration to which it will be entitled

20 COLLECTIBILITY CONSIDERATIONS Before applying the model in the standard to a contract, it must be probable that the entity will collect substantially all of the consideration to which it is entitled in exchange for the goods & services that will be transferred to the customer If this collectability threshold is not met, a contract with a patient does not exist within the scope of the standard A health care entity may make this determination based on past experience with that patient or class of similar patients Assessment is based on both the customer s ability & intent to pay as amounts become due May be difficult for entities to assess No such thing as cash basis

21 PROVIDER CONSIDERATIONS Do I have a contract and collectability threshold Insurance supports probability of collection Patient portion varies which impacts collectability Patients often present without insurance (EMTALA) Medicaid pending Insurance coverage identified later in process Changes in responsible party (MVA, TPL) System operational differences EMTALA vs. Other revenue streams (clinics, urgent-care, retail, home care) New patients vs. recurring patients Is a credit risk assessment performed

22 3 Transaction price is the amount of consideration an entity expects to be entitled to STEP 3 IDENTIFYING THE TRANSACTION PRICE Variable consideration Significant financing component Consideration payable to a customer Explicit & implicit price concessions Constraint of revenue

23 IMPLICIT PRICE CONCESSION CONSIDERATIONS What should we consider? Customary business practice of not performing a credit assessment prior to providing services Continues to provide services to a patient (or patient class) even when historical experience indicates that it is not probable that the entity will collect substantially all of the discounted charges (gross or standard charges less any contractual adjustments or discounts) in the contract

24 If one is present FinREC believes that the health care entity has implicitly provided a price concession to the patient (or patients in the patient class), even if it will continue to attempt to collect the full amount of discounted charges

25 BAD DEBT EXPENSE So when would there be bad debt expense? When a health care entity performs a credit assessment prior to providing services to a patient & expects to collect substantially all of the discounted charges For example, an elective procedure in which historical experience supports collection of substantially all of the discounted charges What s the impact?

26 What s the expected effect? Many health care providers expect a significant decrease in the provision for bad debts for services provided to uninsured & insured patients with co-payments & deductibles, in comparison to what is currently recorded under U.S. GAAP

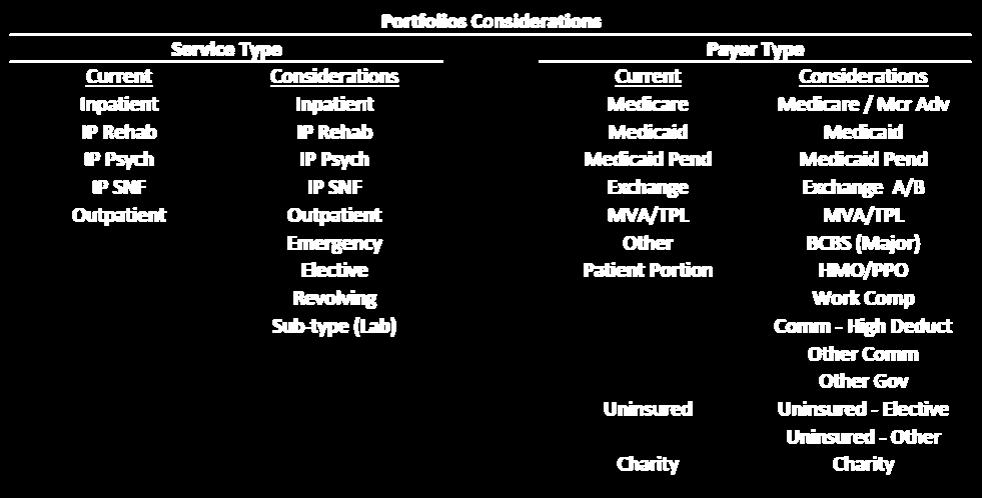

27 PORTFOLIO APPROACH Entities can apply the standard to a portfolio of contracts or performance obligations with similar characteristics Entities must reasonably expect that the financial statement effect of using the portfolio approach will not differ materially from applying the standard on a contract-by-contract basis Key considerations How to apply a portfolio approach How to establish portfolios How to determine effect would not differ materially

28 PORTFOLIO APPROACH More on key considerations Portfolio approach may be applied to all aspects of the model or only to certain steps If establishing portfolios, an entity will need to use judgment to determine the size, composition & number of portfolios Health care entities may consider segregating by payor class, type of service & other categories An entity also will need to consider materiality & documentation requirements How to establish portfolios

29 PORTFOLIO APPROACH Considerations for a health care entity to determine in grouping contracts with similar characteristics for inclusion in a portfolio Type of service, e.g., inpatient, outpatient, skilled nursing, home health Type of payors, e.g., insurance, governmental program, self-pay Whether contracts are entered into at or near the same time A health care entity may include some or a combination of the above considerations in its determination of a portfolio A health care entity may reclassify the remaining self pay balance (co-pay or deductibles) into a separate portfolio after insurance company has paid How to establish portfolios How to determine effect would not differ materially

30 PORTFOLIO APPROACH PROVIDER CONSIDERATIONS

31 COMMON QUESTIONS IN ADOPTION 1 Do we need any new systems? Will our general ledger change? 2 Will we have any bad debt expense? 3 What about patients in-house at period end? 4 Who should be involved in the implementation process? 5 How does this standard change the IRS Form 990, community benefit reporting & the cost report requirements?

32 COMMON INDUSTRY IMPLEMENTATION CHALLENGES Contracts Identify contract(s) with a patient Transaction Price Portfolio approach Special considerations for self pay & Medicaid-pending Changes to estimation methodologies Analysis of service lines for any true credit risk assessments at or prior to service Disclosures Updating systems & processes to accumulate data Implicit price concessions Other Reimbursement Third-party settlements Bundled payment arrangements Risk-sharing arrangements

33 PROVIDER CONSIDERATIONS Implementation approach Planning Portfolio approach Practical expedients selected Financial impact of adoption Changes to internal processes Internal control documentation Data for disclosures Revenue Recognition Issues Medicaid pending patients Self pay Bundled payments State Medicaid programs Third party settlements

34 Lessons Learned Medicaid pending May not have historical information to see how patients are resolved May need to look at a conversion rate based on materiality Self-pay revenue May have multiple self-pay portfolios Geographically Co-insurance and deductibles, high deductible plans, true self pay, etc Use judgment on when credit risk is performed Bundled payments Determine if additional care coordination after discharge is a separate performance obligation Reconciliation process estimate true up

35 Lessons Learned Control changes Monthly control to calculate variable consideration Annual control to review portfolio approach Analyze new programs/agreements under ASC 606 Change Allowance Methodology Run dual methodology until comfortable with changes Average daily method to be used May still consider aging as a secondary look but this could mean variable consideration was not accurate Create an implementation group Involve IT early for data mining Need a project manager Engage auditors during implementation process Understand disclosures and data needed to be gathered Determine impact on internal operations

36 Lessons Learned Educate stakeholders Management Board of Directors Debt holders Contributors May include adoption of ASU on the NFP reporting model changes

37 Disclosure Considerations

38 DISCLOSURE REQUIREMENTS both qualitative & quantitative information Performance obligations Contract balances Significant judgments Disaggregation of revenue Understand nature, amount, timing & uncertainty of revenue & cash flows Costs to obtain or fulfill a contract 38

39 DISAGGREGATION OF REVENUE FOR HEALTH CARE Timing of transfer of goods or service Type of customer, e.g., Medicare, Medicaid, Self-Pay Example categories Type of service, e.g., independent living, assisted living, nursing home Type of contract, e.g., type A, B, C Geographical location

40 DISCLOSURE REQUIREMENTS Disaggregation of revenue considerations What is presented in annual reports, investor presentations, EMMA filings? What information is regularly reviewed by the chief decision makers for evaluating financial performance of operating segments? What other information would users of the financial statements find helpful in evaluating financial performance? Industry comparisons

41 DISAGGREGATION OF REVENUE FOR HEALTH CARE Revenue Disaggregation by Payor The composition of patient care service revenue by primary payor for the years ended December 31 is as follows: 20x2 20x1 Medicare $ 16,000 $ 15,000 Medicaid 6,000 5,000 Managed care 11,000 10,500 Commercial insurers 4,000 3,500 Uninsured 1,800 1,900 Other 1,000 1,000 $ 39,800 $ 36,900

42 DISAGGREGATION OF REVENUE FOR HEALTH CARE Revenue Disaggregation by Region, Service Line, Reimbursement & Timing Services lines: Hospital-inpatient Hospital-outpatient 20x2 Northeast Central Southeast Total $ 3,500 4,500 $ 1,000 2,000 $ 3,000 2,000 $ 7,500 8,500 Physician services 3,000 3,000 5,000 11,000 Home health & hospice Retail sales Other Method of reimbursement: Fee for service Capitation & risk sharing Other Timing of revenue & recognition: 1,000 2, , ,000 4, ,800 8,000 1,000 $ 14,400 $ 9,000 $ 16,400 $ 39,800 $ 8,900 3,100 2,400 $ 14,400 $ 5,300 1,500 2,200 $ 9,000 $ 6,000 6,000 4,400 $ 16,400 $ 20,200 10,600 9,000 $ 39,800 Health care services transferred over time $ 12,400 $ 7,000 $ 12,400 $ 31,800 Retail pharmacy & equipment sales at point in time 2,000 2,000 4,000 8,000 $ 14,400 $ 9,000 $ 16,400 $ 39,800

43 DISCLOSURE REQUIREMENTS Quantitative & qualitative disclosures Contracts with customers Significant judgements Assets recognized Level of detail Need enough to explain, not so much it confuses Performance obligations Over time or a point in time Transaction price Allocation & subsequent changes Optional disclosures Implicit price concessions

44 Public Company Disclosure Excerpts from Second Quarter Q s AICPA Health Care Industry Conference #AICPAhealth

45 Tenet Healthcare Corporation 10Q Second Quarter 2018 ASU was issued to clarify the principles for recognizing revenue, to remove inconsistencies and weaknesses in revenue recognition requirements, and to provide a more robust framework for addressing revenue issues. Our adoption of ASU was accomplished using a modified retrospective method of application, and our accounting policies related to revenues were revised accordingly effective January 1, 2018, as discussed below. AICPA Health Care Industry Conference

46 Tenet Healthcare Corporation 10Q Second Quarter 2018 Net Patient Service Revenues We report net patient service revenues at the amounts that reflect the consideration to which we expect to be entitled in exchange for providing patient care. These amounts are due from patients, third-party payers (including managed care payers and government programs) and others, and they include variable consideration for retroactive revenue adjustments due to settlement of audits, reviews and investigations. Generally, we bill our patients and third-party payers several days after the services are performed or shortly after discharge. Revenues are recognized as performance obligations are satisfied. We determine performance obligations based on the nature of the services we provide. We recognize revenues for performance obligations satisfied over time based on actual charges incurred in relation to total expected charges. We believe that this method provides a faithful depiction of the transfer of services over the term of performance obligations based on the inputs needed to satisfy the obligations. Generally, performance obligations satisfied over time relate to patients in our hospitals receiving inpatient acute care services. We measure performance obligations from admission to the point when there are no further services required for the patient, which is generally the time of discharge. AICPA Health Care Industry Conference

47 Tenet Healthcare Corporation 10Q Second Quarter 2018 Because our patient service performance obligations relate to contracts with a duration of less than one year, we have elected to apply the optional exemption provided in FASB Accounting Standards Codification ( ASC ) (a) and, therefore, we are not required to disclose the aggregate amount of the transaction price allocated to performance obligations that are unsatisfied or partially unsatisfied at the end of the reporting period. The unsatisfied or partially unsatisfied performance obligations referred to above are primarily related to inpatient acute care services at the end of the reporting period. The performance obligations for these contracts are generally completed when the patients are discharged, which generally occurs within days or weeks of the end of the reporting period. We determine the transaction price based on gross charges for services provided, reduced by contractual adjustments provided to third-party payers, discounts provided to uninsured patients in accordance with our Compact, and implicit price concessions provided primarily to uninsured patients. We determine our estimates of contractual adjustments and discounts based on contractual agreements, our discount policies and historical experience. We determine our estimate of implicit price concessions based on our historical collection experience with these classes of patients using a portfolio approach as a practical expedient to account for patient contracts as collective groups rather than individually. The financial statement effects of using this practical expedient are not materially different from an individual contract approach. AICPA Health Care Industry Conference

48 Tenet Healthcare Corporation 10Q Second Quarter 2018 We have a system and estimation process for recording Medicare net patient revenue and estimated cost report settlements. As a result, we record accruals to reflect the expected final settlements on our cost reports. For filed cost reports, we record the accrual based on those cost reports and subsequent activity, and record a valuation allowance against those cost reports based on historical settlement trends. The accrual for periods for which a cost report is yet to be filed is recorded based on estimates of what we expect to report on the filed cost reports, and a corresponding valuation allowance is recorded as previously described. Cost reports generally must be filed within five months after the end of the annual cost reporting period. After the cost report is filed, the accrual and corresponding valuation allowance may need to be adjusted. Settlements with third-party payers for retroactive revenue adjustments due to audits, reviews or investigations are considered variable consideration and are included in the determination of the estimated transaction price for providing patient care using the most likely outcome method. These settlements are estimated based on the terms of the payment agreement with the payer, correspondence from the payer and our historical settlement activity, including an assessment to ensure that it is probable that a significant reversal in the amount of cumulative revenue recognized will not occur when the uncertainty associated with the retroactive adjustment is subsequently resolved. Estimated settlements are adjusted in future periods as adjustments become known (that is, new information becomes available), or as years are settled or are no longer subject to such audits, reviews and investigations AICPA Health Care Industry Conference

49 Tenet Healthcare Corporation 10Q Second Quarter 2018 Revenues under managed care plans are based primarily on payment terms involving predetermined rates per diagnosis, per-diem rates, discounted fee-forservice rates and/or other similar contractual arrangements. These revenues are also subject to review and possible audit by the payers, which can take several years before they are completely resolved. The payers are billed for patient services on an individual patient basis. An individual patient s bill is subject to adjustment on a patient-by-patient basis in the ordinary course of business by the payers following their review and adjudication of each particular bill. We estimate the discounts for contractual allowances at the individual hospital level utilizing billing data on an individual patient basis. At the end of each month, on an individual hospital basis, we estimate our expected reimbursement for patients of managed care plans based on the applicable contract terms. Contractual allowance estimates are periodically reviewed for accuracy by taking into consideration known contract terms, as well as payment history. We believe our estimation and review process enables us to identify instances on a timely basis where such estimates need to be revised. We do not believe there were any adjustments to estimates of patient bills that were material to our revenues. In addition, on a corporate-wide basis, we do not record any general provision for adjustments to estimated contractual allowances for managed care plans. Managed care accounts, net of contractual allowances recorded, are further reduced to their net realizable value through implicit price concessions based on historical collection trends for these payers and other factors that affect the estimation process. AICPA Health Care Industry Conference

50 Tenet Healthcare Corporation 10Q Second Quarter 2018 Generally, patients who are covered by third-party payers are responsible for related co-pays, co-insurance and deductibles, which vary in amount. We also provide services to uninsured patients and offer uninsured patients a discount from standard charges. We estimate the transaction price for patients with co-pays, co-insurance and deductibles and for those who are uninsured based on historical collection experience and current market conditions. Under our Compact and other uninsured discount programs, the discount offered to certain uninsured patients is recognized as a contractual allowance, which reduces net operating revenues at the time the self-pay accounts are recorded. The uninsured patient accounts, net of contractual allowances recorded, are further reduced to their net realizable value at the time they are recorded through implicit price concessions based on historical collection trends for self-pay accounts and other factors that affect the estimation process. There are various factors that can impact collection trends, such as changes in the economy, which in turn have an impact on unemployment rates and the number of uninsured and underinsured patients, the volume of patients through our emergency departments, the increased burden of co-pays, co-insurance amounts and deductibles to be made by patients with insurance, and business practices related to collection efforts. These factors continuously change and can have an impact on collection trends and our estimation process. Subsequent changes to the estimate of the transaction price are generally recorded as adjustments to net patient revenues in the period of the change. AICPA Health Care Industry Conference

51 Tenet Healthcare Corporation 10Q Second Quarter 2018 We have provided implicit price concessions, primarily to uninsured patients and patients with co-pays, co-insurance and deductibles. The implicit price concessions included in estimating the transaction price represent the difference between amounts billed to patients and the amounts we expect to collect based on our collection history with similar patients. Although outcomes vary, our policy is to attempt to collect amounts due from patients, including co-pays, co-insurance and deductibles due from patients with insurance, at the time of service while complying with all federal and state statutes and regulations, including, but not limited to, the Emergency Medical Treatment and Active Labor Act ( EMTALA ). Generally, as required by EMTALA, patients may not be denied emergency treatment due to inability to pay. Therefore, services, including the legally required medical screening examination and stabilization of the patient, are performed without delaying to obtain insurance information. In non-emergency circumstances or for elective procedures and services, it is our policy to verify insurance prior to a patient being treated; however, there are various exceptions that can occur. Such exceptions can include, for example, instances where (1) we are unable to obtain verification because the patient s insurance company was unable to be reached or contacted, (2) a determination is made that a patient may be eligible for benefits under various government programs, such as Medicaid or Victims of Crime, and it takes several days or weeks before qualification for such benefits is confirmed or denied, and (3) under physician orders we provide services to patients that require immediate treatment.. AICPA Health Care Industry Conference

52 Tenet Healthcare Corporation 10Q Second Quarter 2018 We also provide charity care to patients who are financially unable to pay for the healthcare services they receive. Most patients who qualify for charity care are charged a per-diem amount for services received, subject to a cap. Except for the per-diem amounts, our policy is not to pursue collection of amounts determined to qualify as charity care; therefore, we do not report these amounts in net operating revenues. Patient advocates from Conifer s Medical Eligibility Program screen patients in the hospital to determine whether those patients meet eligibility requirements for financial assistance programs. They also expedite the process of applying for these government programs.. AICPA Health Care Industry Conference

53 Tenet Healthcare Corporation 10Q Second Quarter 2018 Net operating revenues for our Hospital Operations and other and Ambulatory Care segments primarily consist of net patient service revenues, principally for patients covered by Medicare, Medicaid, managed care and other health plans, as well as certain uninsured patients under our Compact and other uninsured discount and charity programs. Net operating revenues for our Conifer segment primarily consist of revenues from providing revenue cycle management services to healthcare systems, as well as individual hospitals, physician practices, self-insured organizations, health plans and other entities.. AICPA Health Care Industry Conference

54 Tenet Healthcare Corporation 10Q Second Quarter 2018 The table below shows our sources of net operating revenues from continuing operations: Three Months Ended June 30, Six Months Ended June 30, Hospital Operations and other: Net patient service revenues less provision for doubtful accounts from hospitals and related outpatient facilities Medicare $ 701 $ 820 $ 1,483 $ 1,682 Medicaid Managed care 2,273 2,451 4,641 4,884 Self-pay Indemnity and other Total 3,443 3,719 7,086 7,447 Physician practices revenues less provision for doubtful accounts Health plans Revenue from other sources Hospital Operations and other total prior to inter-segment eliminations 3,733 4,085 7,680 8,200 Ambulatory Care , Conifer Inter-segment eliminations (144) (155) (294) (314) Net operating revenues $ 4,506 $ 4,802 $ 9,205 $ 9,615 AICPA Health Care Industry Conference

55 HCA Healthcare Inc. 10Q Second Quarter 2018 In May 2014, the Financial Accounting Standards Board ( FASB ) issued a new standard related to revenue recognition. We adopted the new standard effective January 1, 2018, using the full retrospective method. The adoption of the new standard did not have an impact on our recognition of net revenues for any periods prior to adoption. The most significant impact of adopting the new standard is to the presentation of our consolidated income statements, where we no longer present the Provision for doubtful accounts as a separate line item and our Revenues are presented net of estimated implicit price concession revenue deductions. We also have eliminated the related presentation of allowances for doubtful accounts on our consolidated balance sheets as a result of the adoption of the new standard. AICPA Health Care Industry Conference

56 HCA Healthcare Inc. 10Q Second Quarter 2018 Our revenues generally relate to contracts with patients in which our performance obligations are to provide health care services to the patients. Revenues are recorded during the period our obligations to provide health care services are satisfied. Our performance obligations for inpatient services are generally satisfied over periods that average approximately five days, and revenues are recognized based on charges incurred in relation to total expected charges. Our performance obligations for outpatient services are generally satisfied over a period of less than one day. The contractual relationships with patients, in most cases, also involve a third-party payer (Medicare, Medicaid, managed care health plans and commercial insurance companies, including plans offered through the health insurance exchanges) and the transaction prices for the services provided are dependent upon the terms provided by (Medicare and Medicaid) or negotiated with (managed care health plans and commercial insurance companies) the third-party payers. AICPA Health Care Industry Conference

57 HCA Healthcare Inc. 10Q Second Quarter 2018 Our revenues are based upon the estimated amounts we expect to be entitled to receive from patients and third-party payers. Estimates of contractual allowances under managed care and commercial insurance plans are based upon the payment terms specified in the related contractual agreements. Revenues related to uninsured patients and uninsured copayment and deductible amounts for patients who have health care coverage may have discounts applied (uninsured discounts and contractual discounts). We also record estimated implicit price concessions (based primarily on historical collection experience) related to uninsured accounts to record self-pay revenues at the estimated amounts we expect to collect. AICPA Health Care Industry Conference

58 HCA Healthcare Inc. 10Q Second Quarter 2018 Our revenues from third-party payers and others (including uninsured patients) for the quarters and six months ended June 30, 2018 and 2017 are summarized in the following table (dollars in millions): Quarter 2018 Ratio 2017 Ratio Medicare $ 2, % $ 2, % Managed Medicare 1, , Medicaid Managed Medicaid Managed care and insurers 5, , International (managed care and insurers) Other Revenues $ 11, % $ 10, % Six Months 2018 Ratio 2017 Ratio Medicare $ 4, % $ 4, % Managed Medicare 2, , Medicaid Managed Medicaid 1, , Managed care and insurers 12, , International (managed care and insurers) Other Revenues $ 22, % $ 21, % AICPA Health Care Industry Conference

59 HCA Healthcare Inc. 10Q Second Quarter 2018 Laws and regulations governing the Medicare and Medicaid programs are complex and subject to interpretation. As a result, there is at least a reasonable possibility recorded estimates will change by a material amount. Estimated reimbursement amounts are adjusted in subsequent periods as cost reports are prepared and filed and as final settlements are determined (in relation to certain government programs, primarily Medicare, this is generally referred to as the cost report filing and settlement process). AICPA Health Care Industry Conference

60 HCA Healthcare Inc. 10Q Second Quarter 2018 The collection of outstanding receivables for Medicare, Medicaid, managed care payers, other third-party payers and patients is our primary source of cash and is critical to our operating performance. The primary collection risks relate to uninsured patient accounts, including patient accounts for which the primary insurance carrier has paid the amounts covered by the applicable agreement, but patient responsibility amounts (deductibles and copayments) remain outstanding. Implicit price concessions relate primarily to amounts due directly from patients. Estimated implicit price concessions are recorded for all uninsured accounts, regardless of the aging of those accounts. Accounts are written off when all reasonable internal and external collection efforts have been performed. AICPA Health Care Industry Conference

61 HCA Healthcare Inc. 10Q Second Quarter 2018 The estimates for implicit price concessions are based upon management s assessment of historical writeoffs and expected net collections, business and economic conditions, trends in federal, state and private employer health care coverage and other collection indicators. Management relies on the results of detailed reviews of historical writeoffs and collections at facilities that represent a majority of our revenues and accounts receivable (the hindsight analysis ) as a primary source of information in estimating the collectability of our accounts receivable. We perform the hindsight analysis quarterly, utilizing rolling twelve-months accounts receivable collection and writeoff data. We believe our quarterly updates to the estimated implicit price concession amounts at each of our hospital facilities provide reasonable estimates of our revenues and valuations of our accounts receivable. These routine, quarterly changes in estimates have not resulted in material adjustments to the valuations of our accounts receivable or period-to-period comparisons of our results of operations. At June 30, 2018 and December 31, 2017, estimated implicit price concessions of $5.736 billion and $5.488 billion, respectively, had been recorded as reductions to our accounts receivable balances to enable us to record our revenues and accounts receivable at the estimated amounts we expect to collect. AICPA Health Care Industry Conference

62 HCA Healthcare Inc. 10Q Second Quarter 2018 To quantify the total impact of the trends related to uninsured accounts, we believe it is beneficial to view total uncompensated care, which is comprised of charity care, uninsured discounts and implicit price concessions. A summary of the estimated cost of total uncompensated care for the quarters and six months ended June 30, 2018 and 2017 follows (dollars in millions): Quarter Six Months Patient care costs (salaries and benefits, supplies, other operating expenses and depreciation and amortization) $ 9,871 $ 9,177 $ 19,738 $ 18,326 Cost-to-charges ratio (patient care costs as percentage of gross patient charges) 12.6% 13.0% 12.5% 12.9 % Total uncompensated care $ 6,486 $ 5,721 $ 12,738 $ 11,048 Multiply by the cost-to-charges ratio 12.6% 13.0% 12.5% 12.9 % Estimated cost of total uncompensated care $ 817 $ 743 $ 1,592 $ 1,425 AICPA Health Care Industry Conference

63 Genesis Healthcare, Inc. 10Q Second Quarter 2018 In May 2014, the FASB issued ASU No , Revenue from Contracts with Customers and all related amendments (ASC 606), which serves to supersede most existing revenue recognition guidance, including guidance specific to the healthcare industry. ASC 606 provides a principles-based framework for recognizing revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services and requires enhanced disclosures to enable users of financial statements to understand the nature, amount, timing, and uncertainty of revenue and cash flows arising from contracts with customers. The Company adopted ASC 606 effective January 1, 2018 using the modified retrospective transition method. There was no cumulative effect on the opening balance of accumulated deficit as a result of adopting the standard as of January 1, Results for reporting periods beginning after January 1, 2018 are presented under ASC 606, while comparative information has not been restated and continues to be reported under the accounting standards in effect for those periods. See Note 4 Net Revenues and Accounts Receivable. AICPA Health Care Industry Conference

64 Genesis Healthcare, Inc. 10Q Second Quarter 2018 The Company receives revenues from Medicare, Medicaid, private insurance, self-pay residents, other third-party payors and longterm care facilities that utilize its rehabilitation therapy and other services. The Company s inpatient services segment derives approximately 78% of its revenue from Medicare and various state Medicaid programs. The following table depicts the Company s inpatient services segment revenue by source for the three and six months ended June 30, 2018 and Three months ended June 30, Six months ended June 30, Medicare 22 % 23 % 22 % 23 % Medicaid 57 % 55 % 56 % 55 % Insurance 12 % 12 % 13 % 12 % Private 8 % 9 % 8 % 9 % Other 1 % 1 % 1 % 1 % Total 100 % 100 % 100 % 100 % AICPA Health Care Industry Conference

65 Genesis Healthcare, Inc. 10Q Second Quarter 2018 The sources and amounts of the Company s revenues are determined by a number of factors, including licensed bed capacity and occupancy rates of inpatient facilities, the mix of patients and the rates of reimbursement among payors. Likewise, payment for ancillary medical services, including services provided by the Company s rehabilitation therapy services business, varies based upon the type of payor and payment methodologies. Changes in the case mix of the patients as well as payor mix among Medicare, Medicaid and private pay can significantly affect the Company s profitability. AICPA Health Care Industry Conference

66 Genesis Healthcare, Inc. 10Q Second Quarter 2018 The Company generates revenues, primarily by providing healthcare services to its customers. Revenues are recognized when control of the promised good or service is transferred to our customers, in an amount that reflects the consideration the Company expects to be entitled from patients, third-party payers (including government programs and insurers) and others, in exchange for those goods and services. Performance obligations are determined based on the nature of the services provided. The majority of the Company s healthcare services represent a bundle of services that are not capable of being distinct and as such, are treated as a single performance obligation satisfied over time as services are rendered. The Company also provides certain ancillary services which are not included in the bundle of services, and as such, are treated as separate performance obligations satisfied at a point in time, if and when, those services are rendered. AICPA Health Care Industry Conference

67 Genesis Healthcare, Inc. 10Q Second Quarter 2018 The Company determines the transaction price based on contractually agreed-upon amounts or rates, adjusted for estimates of variable consideration, such as implicit price concessions. The Company utilizes the expected value method to determine the amount of variable consideration that should be included to arrive at the transaction price, using contractual agreements and historical reimbursement experience within each payor type. Variable consideration also exists in the form of settlements with Medicare and Medicaid as a result of retroactive adjustments due to audits and reviews. The Company applies constraint to the transaction price, such that net revenues are recorded only to the extent that it is probable that a significant reversal in the amount of the cumulative revenue recognized will not occur in the future. If actual amounts of consideration ultimately received differ from the Company s estimates, the Company adjusts these estimates, which would affect net revenues in the period such variances become known. Adjustments arising from a change in the transaction price were not significant for the three and six months ended June 30, The Company has elected a practical expedient to not adjust the promised amount of consideration for the effects of a significant financing component due to its expectation that the period between the time the service is provided and the time payment is received will be one year or less. AICPA Health Care Industry Conference

68 Genesis Healthcare, Inc. 10Q Second Quarter 2018 The Company s adoption of ASC 606 primarily impacts the presentation of revenues due to the inclusion of variable consideration in the form of implicit price concessions contained in certain of its contracts with customers. Under ASC 606, amounts estimated to be uncollectable are generally considered implicit price concessions that are a direct reduction to net revenues. Prior to adoption of ASC 606, such amounts were classified as provision for losses on accounts receivable. For the three and six months ended June 30, 2018, the Company recorded approximately $22.0 million and $46.8 million, respectively, of implicit price concessions as a direct reduction of net revenues that would have been recorded as operating expenses prior to the adoption of ASC 606. The adoption of ASC 606 is not expected to have a material impact on net income on an ongoing basis. To the extent there are material subsequent events that affect the payor's ability to pay, such amounts are recorded within operating expenses. At June 30, 2018, the remaining balance of allowance for doubtful accounts previously disclosed on the consolidated balance sheets relating to accounts receivable with December 31, 2017 and prior service dates is $277.4 million. AICPA Health Care Industry Conference

69 Genesis Healthcare, Inc. 10Q Second Quarter 2018 The Company has reclassified the provision for losses on accounts receivable of $24.0 million and $47.5 million for the three and six months ended June 30, 2017, respectively, to other operating expenses in the consolidated statements of operations. These reclassifications had no effect on the reported results of operations. Under ASC 606, the Company recognizes revenue in the statements of operations and contract assets on the consolidated balance sheets only when services have been provided. Since the Company has performed its obligation under the contract, it has unconditional rights to the consideration recorded as contract assets and therefore classifies those billed and unbilled contract assets as accounts receivable. Under ASC 606, payments that the Company receives from customers in advance of providing services represent contract liabilities. Such payments primarily relate to private pay patients, which are billed monthly in advance. The Company had no material contract liabilities or activity as of and for the three and six months ended June 30, AICPA Health Care Industry Conference

70 Genesis Healthcare, Inc. 10Q Second Quarter 2018 The Company disaggregates revenue from contracts with customers by reportable operating segments and payor type. The Company notes that disaggregation of revenue into these categories achieves the disclosure objectives to depict how the nature, amount, timing and uncertainty of revenue and cash flows are affected by economic factors. The payment terms and conditions within the Company's revenue-generating contracts vary by contract type and payor source. Payments are generally received within 30 to 60 days after billed. See Note 6 Segment Information. AICPA Health Care Industry Conference

71 Other Considerations

72 THIRD-PARTY SETTLEMENTS Determination of the transaction price for third-party settlements Medicare/Medicaid cost report settlements RAC accruals Risk adjustments for prepaid health plans Other Use method which entity expects to better predict the amount of consideration to which it will be entitled Use of Expected Value (probability-weighted amount) Use of Most Likely Amount (single most likely amount in a range of possible considerations)

73 THIRD-PARTY SETTLEMENTS EXPECTED VALUE Sum of the probability-weighted amounts in a range of possible outcomes Most predictive when the transaction has a large number of possible outcomes MOST LIKELY AMOUNT The single most likely amount in a range of possible outcomes Most predictive when the transaction has two possible outcomes Required to evaluate whether to constrain amounts of variable consideration included in transaction price Objective of the constraint include variable consideration in the transaction price only to the extent it is probable that a significant revenue reversal will not occur Estimates must be updated each reporting period

74 THIRD-PARTY SETTLEMENTS Transition guidance for modified retrospective approach Evaluate contracts to determine if substantially all of the revenue was recognized under legacy GAAP (before the date of initial application) If all or substantially all of the revenue has not been recognized, the contracts with patients subject to retroactive settlement by that payor for the open cost report year would be considered open contracts & FASB ASC 606 will need to be applied to those contracts for purposes of determining the cumulative effect adjustment at the date of initial application

75 BUNDLED PAYMENT ARRANGEMENTS Step 1 Identification of the contract FinREC believes the contract is with the patient not the third-party payor Step 2 Performance obligation Care Coordination is not necessarily a performance obligation. Need to assess each contract & in addition consider implied promises & if so are they a distinct performance obligation Step 3 Transaction price considerations Variable consideration Constraint of revenue Use of portfolios Significant financing component Do you have historical information to estimate the variable consideration Exposed an example for CJR

76 CCRC SPECIFIC CONSIDERATIONS Accounting for monthly/periodic fees Accounting for nonrefundable entrance fees under the different contract types (focus has been primarily on Type A Contracts) Significant financing component considerations for refundable & nonrefundable entrance fees Obligation to provide future services & use of facilities Contract acquisition costs Want more in depth training on CCRC-specific implications? Visit bkd.com/thelink to access our on-demand presentation.

77 WHAT TO DO NOW? 1 Read the standard & related resources 2 Identify a champion or task force to study the new standard 3 4 Determine if resource bandwidth & competencies exist within the organization or if outside assistance is needed Engage reimbursement, IT & finance staff (& third party, if deemed necessary) 5 Identify revenue streams & the related portfolios 6 7 Concentrate on disclosures & if any changes are needed to gather the information Educate audit committees, boards & other stakeholders

78 Accounting Guidance for Contributions Received & Contributions Made

79 ASU CLARIFYING THE SCOPE & ACCOUNTING GUIDANCE FOR CONTRIBUTIONS RECEIVED & CONTRIBUTIONS MADE Contributions & Grants One June 21, 2018, the FASB Issued ASU , Clarifying the Scope & the Accounting Guidance for Contributions Received & Contributions Made The ASU clarifies Whether an asset transfer is a contribution or an exchange transaction The criteria for determining whether contributions are unconditional (& recognized immediately into income) or conditional (& deferred) 79

80 ASU CLARIFYING THE SCOPE & ACCOUNTING GUIDANCE FOR CONTRIBUTIONS RECEIVED & CONTRIBUTIONS MADE Background Issued as a result of seeing diversity in practice among NFP entities, even after considering the issuance of ASC 606 Scope Guidance applies to all NFPs & business entities. The rules do not apply to transfers of assets from the government to a business entity

81 ASU , CLARIFYING THE SCOPE & THE ACCOUNTING GUIDANCE FOR CONTRIBUTIONS RECEIVED & CONTRIBUTIONS MADE Effective Date & Transition The final standard should be applied on a modified prospective basis following the effective date to agreements that are either (a) incomplete as of the effective date or (b) entered into after the effective date. Retrospective application is permitted Resource providers have an additional year to implement the provisions on the standard 1 Public entities include NFPs with conduit debt obligations

Implementing Revenue Recognition for Health Care Organizations S E P T E M B E R 2 1,

Implementing Revenue Recognition for Health Care Organizations S E P T E M B E R 2 1, 2 0 1 8 INTRODUCTIONS Kimberly McKay, CPA Managing Partner kmckay@bkd.com Implementing Revenue Recognition for Health

Implementing Revenue Recognition for Health Care Organizations S E P T E M B E R 2 1, 2 0 1 8 INTRODUCTIONS Kimberly McKay, CPA Managing Partner kmckay@bkd.com Implementing Revenue Recognition for Health

Implementing Revenue Recognition for Health Care Organizations

Implementing Revenue Recognition for Health Care Organizations AUGUST 6, 2018 TO RECEIVE CPE CREDIT Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader is

Implementing Revenue Recognition for Health Care Organizations AUGUST 6, 2018 TO RECEIVE CPE CREDIT Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader is

Implementing Revenue Recognition for Health Care Organizations J A N U A R Y

Implementing Revenue Recognition for Health Care Organizations J A N U A R Y 2 0 1 9 AGENDA 1 Introductions & Objectives 2 Background, Key Principles, & Transition 3 Common Industry Implementation Challenges

Implementing Revenue Recognition for Health Care Organizations J A N U A R Y 2 0 1 9 AGENDA 1 Introductions & Objectives 2 Background, Key Principles, & Transition 3 Common Industry Implementation Challenges

FASB ASU NO REVENUE FROM CONTRACTS WITH CUSTOMERS (TOPIC 606)

") CPAs & ADVISORS experience clarity // REVENUE RECOGNITION FOR HEALTH CARE PROVIDERS Kimberly McKay, CPA Managing Partner BKD. LLP - Houston FASB ASU NO. 2014-09 REVENUE FROM CONTRACTS WITH CUSTOMERS (TOPIC

CPAs & ADVISORS experience clarity // REVENUE RECOGNITION FOR HEALTH CARE PROVIDERS Kimberly McKay, CPA Managing Partner BKD. LLP - Houston FASB ASU NO. 2014-09 REVENUE FROM CONTRACTS WITH CUSTOMERS (TOPIC

REVENUE RECOGNITION FOR HEALTH CARE PROVIDERS

REVENUE RECOGNITION FOR HEALTH CARE PROVIDERS Tracy Young, CPA Partner -BKD, LLP Brent Beaulieu, CPA VP Finance Baptist Health ASU 2014-09 REVENUE FROM CONTRACTS WITH CUSTOMERS Effective for Public Business

REVENUE RECOGNITION FOR HEALTH CARE PROVIDERS Tracy Young, CPA Partner -BKD, LLP Brent Beaulieu, CPA VP Finance Baptist Health ASU 2014-09 REVENUE FROM CONTRACTS WITH CUSTOMERS Effective for Public Business

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC Form 10-Q

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 Form 10-Q Quarterly report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the quarterly period ended 2018

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 Form 10-Q Quarterly report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the quarterly period ended 2018

REVENUE RECOGNITION ASU /8/2016. CPAs & ADVISORS ACCOUNTING AND AUDITING UPDATE FOR ARKANSAS HFMA

CPAs & ADVISORS experience clarity // ACCOUNTING AND AUDITING UPDATE FOR ARKANSAS HFMA Tracy Young, CPA Partner, BKD Health Care Group Little Rock REVENUE RECOGNITION ASU 2014-09 1 FASB/IASB ORIGINAL REVENUE

CPAs & ADVISORS experience clarity // ACCOUNTING AND AUDITING UPDATE FOR ARKANSAS HFMA Tracy Young, CPA Partner, BKD Health Care Group Little Rock REVENUE RECOGNITION ASU 2014-09 1 FASB/IASB ORIGINAL REVENUE

d. 8-4, Recognizing a CCRC s performance obligation(s) to provide future services and use of facilities to residents

to provide future services and use of facilities to residents") June 1, 2017 Financial Reporting Center Revenue Recognition Working Draft: Health Care Entities Revenue Recognition Implementation Issue Issue #8-6 Presentation and Disclosure Expected Overall Level of

June 1, 2017 Financial Reporting Center Revenue Recognition Working Draft: Health Care Entities Revenue Recognition Implementation Issue Issue #8-6 Presentation and Disclosure Expected Overall Level of

REVENUE RECOGNITION ASU /23/2016. CPAs & ADVISORS ACCOUNTING AND AUDITING UPDATE FOR ARKANSAS HFMA

CPAs & ADVISORS experience clarity // ACCOUNTING AND AUDITING UPDATE FOR ARKANSAS HFMA Drew Speed, CPA Partner, Accounting and Auditing Director, Little Rock REVENUE RECOGNITION ASU 2014-09 1 FASB/IASB

CPAs & ADVISORS experience clarity // ACCOUNTING AND AUDITING UPDATE FOR ARKANSAS HFMA Drew Speed, CPA Partner, Accounting and Auditing Director, Little Rock REVENUE RECOGNITION ASU 2014-09 1 FASB/IASB

New Jersey Chapter of HFMA Spring Education Event April 2016 ASC 606, Revenue from Contracts with Customers Overview for Healthcare Providers

New Jersey Chapter of HFMA Spring Education Event April 2016 ASC 606, Revenue from Contracts with Customers Overview for Healthcare Providers How Will Revenue be Recognized Under Contracts? Albert Deana,

New Jersey Chapter of HFMA Spring Education Event April 2016 ASC 606, Revenue from Contracts with Customers Overview for Healthcare Providers How Will Revenue be Recognized Under Contracts? Albert Deana,

Revenue Recognition: A Comprehensive Review for Health Care Entities

Revenue Recognition: A Comprehensive Review for Health Care Entities Table of Contents INTRODUCTION... 4 THE MODEL... 5 SCOPE... 5 CONTRIBUTIONS/GRANTS... 5 COLLABORATIVE ARRANGEMENTS... 6 CHARITY CARE...

Revenue Recognition: A Comprehensive Review for Health Care Entities Table of Contents INTRODUCTION... 4 THE MODEL... 5 SCOPE... 5 CONTRIBUTIONS/GRANTS... 5 COLLABORATIVE ARRANGEMENTS... 6 CHARITY CARE...

2016 Revenue Recognition Session Parts 1 & 2

2016 AICPA Healthcare Conference 2016 Revenue Recognition Session Parts 1 & 2 Speaker Biographies 25-1 Mike Breen, CPA Mike is an audit partner in KPMG s New York Office. He has experience performing financial

2016 AICPA Healthcare Conference 2016 Revenue Recognition Session Parts 1 & 2 Speaker Biographies 25-1 Mike Breen, CPA Mike is an audit partner in KPMG s New York Office. He has experience performing financial

Revenue Recognition ASU No

Revenue Recognition ASU No. 2014 09 April 19, 2018 Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC registered investment advisor. CliftonLarsonAllen LLP

Revenue Recognition ASU No. 2014 09 April 19, 2018 Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC registered investment advisor. CliftonLarsonAllen LLP

Revenue Recognition PREPARE NOW. Presented By Mary Jalbert, Principal Michael Whitten, Senior Manager October 3, 2017

Revenue Recognition PREPARE NOW Presented By Mary Jalbert, Principal Michael Whitten, Senior Manager October 3, 2017 Agenda TODAY S OBJECTIVE: A meaningful discussion and exchange of ideas resulting in

Revenue Recognition PREPARE NOW Presented By Mary Jalbert, Principal Michael Whitten, Senior Manager October 3, 2017 Agenda TODAY S OBJECTIVE: A meaningful discussion and exchange of ideas resulting in

Revenue from contracts with customers. Health care services industry supplement

Note: Since issuing the new revenue standard in May 2014, the FASB and IASB have proposed various amendments to the guidance. This In depth supplement has not been updated to reflect all of the proposed

Note: Since issuing the new revenue standard in May 2014, the FASB and IASB have proposed various amendments to the guidance. This In depth supplement has not been updated to reflect all of the proposed

Revenue Recognition PREPARE NOW. Presented By Michael Whitten, Senior Manager April 23, 2018

Revenue Recognition PREPARE NOW Presented By Michael Whitten, Senior Manager April 23, 2018 Agenda TODAY S OBJECTIVE: A meaningful discussion and exchange of ideas resulting in tangible steps to apply

Revenue Recognition PREPARE NOW Presented By Michael Whitten, Senior Manager April 23, 2018 Agenda TODAY S OBJECTIVE: A meaningful discussion and exchange of ideas resulting in tangible steps to apply

AUDIT AND ACCOUNTING UPDATE

AUDIT AND ACCOUNTING UPDATE HFMA FL Regional Education Session - Clearwater November 11, 2016 Presenter Carlos Hernandez Southeast Assurance Leader Carlos.hernandez@rsmus.com 2 Agenda Topic Recent accounting

AUDIT AND ACCOUNTING UPDATE HFMA FL Regional Education Session - Clearwater November 11, 2016 Presenter Carlos Hernandez Southeast Assurance Leader Carlos.hernandez@rsmus.com 2 Agenda Topic Recent accounting

COMPLEXITIES FOR LONG-TERM CARE

The New World of Revenue Recognition, ASC 606 COMPLEXITIES FOR LONG-TERM CARE June 27, 2018 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK

The New World of Revenue Recognition, ASC 606 COMPLEXITIES FOR LONG-TERM CARE June 27, 2018 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK

Accounting Standard Updates

Accounting Standard Updates HFMA Spring Conference 2018 Presented by: Kimberly Sokoloff, Health Care Assurance Services Senior Manager Elizabeth Lasnier, Health Care Assurance Services Manager Presenters

Accounting Standard Updates HFMA Spring Conference 2018 Presented by: Kimberly Sokoloff, Health Care Assurance Services Senior Manager Elizabeth Lasnier, Health Care Assurance Services Manager Presenters

Laurel Lake Retirement Community, Inc. and Subsidiary YEARS ENDED DECEMBER 31, 2018 AND 2017

Laurel Lake Retirement Community, Inc. and Subsidiary CONSOLIDATED FINANCIAL STATEMENTS CONTENTS Independent auditor s report 1 Financial statement: Consolidated statements of financial position 2 Consolidated

Laurel Lake Retirement Community, Inc. and Subsidiary CONSOLIDATED FINANCIAL STATEMENTS CONTENTS Independent auditor s report 1 Financial statement: Consolidated statements of financial position 2 Consolidated

JUPITER MEDICAL CENTER, INC. AND AFFILIATED COMPANIES. Jupiter, Florida. CONSOLIDATED FINANCIAL STATEMENTS September 30, 2014 and 2013

JUPITER MEDICAL CENTER, INC. AND AFFILIATED COMPANIES Jupiter, Florida CONSOLIDATED FINANCIAL STATEMENTS Jupiter, Florida CONSOLIDATED FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR S REPORT... 1 FINANCIAL

JUPITER MEDICAL CENTER, INC. AND AFFILIATED COMPANIES Jupiter, Florida CONSOLIDATED FINANCIAL STATEMENTS Jupiter, Florida CONSOLIDATED FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR S REPORT... 1 FINANCIAL

Advocate Health Care Network and Subsidiaries FINANCIAL REPORT

Advocate Health Care Network and Subsidiaries FINANCIAL REPORT For the First Quarter Ended March 31, 2018 Cautionary Statement Regarding Forward Looking Statements in this Quarterly Financial Report This

Advocate Health Care Network and Subsidiaries FINANCIAL REPORT For the First Quarter Ended March 31, 2018 Cautionary Statement Regarding Forward Looking Statements in this Quarterly Financial Report This

JUPITER MEDICAL CENTER, INC. AND AFFILIATED COMPANIES. Jupiter, Florida. CONSOLIDATED FINANCIAL STATEMENTS September 30, 2015 and 2014

JUPITER MEDICAL CENTER, INC. AND AFFILIATED COMPANIES Jupiter, Florida CONSOLIDATED FINANCIAL STATEMENTS Jupiter, Florida CONSOLIDATED FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR S REPORT... 1 FINANCIAL

JUPITER MEDICAL CENTER, INC. AND AFFILIATED COMPANIES Jupiter, Florida CONSOLIDATED FINANCIAL STATEMENTS Jupiter, Florida CONSOLIDATED FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR S REPORT... 1 FINANCIAL

HFMA Great Lakes Chapter Accounting and Auditing Update February 16, 2018

HFMA Great Lakes Chapter Accounting and Auditing Update February 16, 2018 Who We Are CAROLYN BIELAWSKI, CPA ASSOCIATE Education: Bachelor of Arts in Accounting, Master of Science in Accounting, Michigan

HFMA Great Lakes Chapter Accounting and Auditing Update February 16, 2018 Who We Are CAROLYN BIELAWSKI, CPA ASSOCIATE Education: Bachelor of Arts in Accounting, Master of Science in Accounting, Michigan

Revenue for healthcare providers

Revenue for healthcare providers The new standard s effective date is coming. US GAAP November 2016 kpmg.com/us/frn b Revenue for healthcare providers Revenue viewed through a new lens Again and again,

Revenue for healthcare providers The new standard s effective date is coming. US GAAP November 2016 kpmg.com/us/frn b Revenue for healthcare providers Revenue viewed through a new lens Again and again,

ACCOUNTING AND AUDIT UPDATE

ACCOUNTING AND AUDIT UPDATE HFMA FL Regional Education Session - Hollywood January 19, 2017 Presenter Carlos Hernandez Southeast Assurance Leader Carlos.hernandez@rsmus.com 2 Agenda Accounting and Auditing

ACCOUNTING AND AUDIT UPDATE HFMA FL Regional Education Session - Hollywood January 19, 2017 Presenter Carlos Hernandez Southeast Assurance Leader Carlos.hernandez@rsmus.com 2 Agenda Accounting and Auditing

Hallmark Health Corporation and Affiliates

Hallmark Health Corporation and Affiliates Consolidated Financial Statements as of and for the Years Ended September 30, 2016 and 2015, Schedule of Expenditures of Federal Awards for the Year Ended September

Hallmark Health Corporation and Affiliates Consolidated Financial Statements as of and for the Years Ended September 30, 2016 and 2015, Schedule of Expenditures of Federal Awards for the Year Ended September

Trinity Health Operating Income continues to climb in Q1 FY19

Trinity Health Operating Income continues to climb in Q1 FY19 Summary Highlights for the First Quarter of FY19 (Quarter Ended September 30, 2018) In the first quarter of fiscal year 2019, Trinity Health

Trinity Health Operating Income continues to climb in Q1 FY19 Summary Highlights for the First Quarter of FY19 (Quarter Ended September 30, 2018) In the first quarter of fiscal year 2019, Trinity Health

Changes to revenue recognition in the health care industry

Changes to revenue recognition in the health care industry Prepared by: Dan Vandenberghe, Partner, RSM US LLP dan.vandenberghe@rsmus.com, +1 612 376 9267 Jay Adkisson, Partner, RSM US LLP jay.adkisson@rsmus.com,

Changes to revenue recognition in the health care industry Prepared by: Dan Vandenberghe, Partner, RSM US LLP dan.vandenberghe@rsmus.com, +1 612 376 9267 Jay Adkisson, Partner, RSM US LLP jay.adkisson@rsmus.com,

Mayo Clinic. Unaudited Condensed Consolidated Financial Statements Quarter Ended June 30, 2018

Mayo Clinic Unaudited Condensed Consolidated Financial Statements Quarter Ended June 30, 2018 Mayo Clinic Contents Unaudited Financial Statements Condensed consolidated statements of financial 1 position

Mayo Clinic Unaudited Condensed Consolidated Financial Statements Quarter Ended June 30, 2018 Mayo Clinic Contents Unaudited Financial Statements Condensed consolidated statements of financial 1 position

Atchison Hospital Association, Inc. and Riverbend Regional Healthcare Foundation. Consolidated Financial Report September 30, 2015

Consolidated Financial Report September 30, 2015 Contents Independent Auditor s Report on the Financial Statements 1 2 Financial Statements Consolidated balance sheets 3 4 Consolidated statements of operations

Consolidated Financial Report September 30, 2015 Contents Independent Auditor s Report on the Financial Statements 1 2 Financial Statements Consolidated balance sheets 3 4 Consolidated statements of operations

Revenue Recognition: Construction Industry Supplement

Revenue Recognition: Construction Industry Supplement Table of Contents BACKGROUND & SUMMARY... 4 SCOPE... 5 THE REVENUE RECOGNITION MODEL... 5 STEP 1 IDENTIFY THE CONTRACT WITH A CUSTOMER... 6 Collectibility...

Revenue Recognition: Construction Industry Supplement Table of Contents BACKGROUND & SUMMARY... 4 SCOPE... 5 THE REVENUE RECOGNITION MODEL... 5 STEP 1 IDENTIFY THE CONTRACT WITH A CUSTOMER... 6 Collectibility...

Revenue Recognition, Including Implicit Price Concession and Bad Debt Considerations, for Healthcare Organizations: Accounting Issues and Trends

Revenue Recognition, Including Implicit Price Concession and Bad Debt Considerations, for Healthcare Organizations: Accounting Issues and Trends Principles and Practices Board Issue Analysis January 2019

Revenue Recognition, Including Implicit Price Concession and Bad Debt Considerations, for Healthcare Organizations: Accounting Issues and Trends Principles and Practices Board Issue Analysis January 2019

NARUC: REVENUE RECOGNITION JULIE PETIT AUDIT SENIOR MANAGER BRIAN JONES AUDIT SENIOR MANAGER MONDAY, SEPTEMBER 11 TH, 2017

NARUC: REVENUE RECOGNITION JULIE PETIT AUDIT SENIOR MANAGER BRIAN JONES AUDIT SENIOR MANAGER MONDAY, SEPTEMBER 11 TH, 2017 Mazars USA LLP is an independent member firm of Mazars Group. Mazars USA LLP is

NARUC: REVENUE RECOGNITION JULIE PETIT AUDIT SENIOR MANAGER BRIAN JONES AUDIT SENIOR MANAGER MONDAY, SEPTEMBER 11 TH, 2017 Mazars USA LLP is an independent member firm of Mazars Group. Mazars USA LLP is

Financial Statements. Years Ended September 30, 2016 and 2015

The report accompanying these financial statements was issued by BDO USA, LLP, a Delaware limited liability partnership and the U.S. member of BDO International Limited, a UK company limited by guarantee.

The report accompanying these financial statements was issued by BDO USA, LLP, a Delaware limited liability partnership and the U.S. member of BDO International Limited, a UK company limited by guarantee.

Trinity Health Operating Revenue Grows 5.5% to $9.5 billion in the First Half of FY19

Trinity Health Operating Revenue Grows 5.5% to $9.5 billion in the First Half of FY19 Summary Highlights for the First Half of FY19 (Six Months Ended December 31, 2018) During the first six months of fiscal

Trinity Health Operating Revenue Grows 5.5% to $9.5 billion in the First Half of FY19 Summary Highlights for the First Half of FY19 (Six Months Ended December 31, 2018) During the first six months of fiscal

Consolidated Financial Statements as of and for the Years Ended December 31, 2018 and 2017, and Independent Auditors Report

Consolidated Financial Statements as of and for the Years Ended December 31, 2018 and 2017, and Independent Auditors Report INTENTIONALLY BLANK TABLE OF CONTENTS INDEPENDENT AUDITORS REPORT 1 2 CONSOLIDATED

Consolidated Financial Statements as of and for the Years Ended December 31, 2018 and 2017, and Independent Auditors Report INTENTIONALLY BLANK TABLE OF CONTENTS INDEPENDENT AUDITORS REPORT 1 2 CONSOLIDATED

Henry Mayo Newhall Hospital

Financial Statements Years Ended September 30, 2015 and 2014 The report accompanying these financial statements was issued by BDO USA, LLP, a Delaware limited liability partnership and the U.S. member

Financial Statements Years Ended September 30, 2015 and 2014 The report accompanying these financial statements was issued by BDO USA, LLP, a Delaware limited liability partnership and the U.S. member

CAMC Health System, Inc. and Subsidiaries

CAMC Health System, Inc. and Subsidiaries Consolidated Financial Statements and Other Financial Information as of and for the Years Ended December 31, 2016 and 2015, and Independent Auditors Report CAMC

CAMC Health System, Inc. and Subsidiaries Consolidated Financial Statements and Other Financial Information as of and for the Years Ended December 31, 2016 and 2015, and Independent Auditors Report CAMC

NANTICOKE HEALTH SERVICES, INC. AND SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION YEARS ENDED JUNE 30, 2016 AND 2015

NANTICOKE HEALTH SERVICES, INC. AND SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION YEARS ENDED TABLE OF CONTENTS YEARS ENDED INDEPENDENT AUDITORS' REPORT 1 CONSOLIDATED FINANCIAL

NANTICOKE HEALTH SERVICES, INC. AND SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION YEARS ENDED TABLE OF CONTENTS YEARS ENDED INDEPENDENT AUDITORS' REPORT 1 CONSOLIDATED FINANCIAL

Hunterdon Medical Center

. c o m Financial Statements [Type text] Table of Contents Page Independent Auditors Report 1 Financial Statements Balance Sheet 3 Statement of Operations 4 Statement of Changes in Net Assets 5 Statement

. c o m Financial Statements [Type text] Table of Contents Page Independent Auditors Report 1 Financial Statements Balance Sheet 3 Statement of Operations 4 Statement of Changes in Net Assets 5 Statement

Mayo Clinic. Unaudited Condensed Consolidated Financial Statements Quarter Ended March 31, 2018

Mayo Clinic Unaudited Condensed Consolidated Financial Statements Quarter Ended March 31, 2018 Mayo Clinic Contents Unaudited Financial Statements Condensed consolidated statements of financial 1 position

Mayo Clinic Unaudited Condensed Consolidated Financial Statements Quarter Ended March 31, 2018 Mayo Clinic Contents Unaudited Financial Statements Condensed consolidated statements of financial 1 position

PORTER MEDICAL CENTER, INC. AND SUBSIDIARIES

CONSOLIDATED FINANCIAL STATEMENTS with SUPPLEMENTARY INFORMATION With Independent Auditors Report TABLE OF CONTENTS Page Independent Auditors' Report 1 Consolidated Financial Statements Balance Sheets

CONSOLIDATED FINANCIAL STATEMENTS with SUPPLEMENTARY INFORMATION With Independent Auditors Report TABLE OF CONTENTS Page Independent Auditors' Report 1 Consolidated Financial Statements Balance Sheets

Interim Unaudited Consolidated Financial Statements and Other Information

Interim Unaudited Consolidated Financial Statements and Other Information For The Period Ended March 31, 2018 The Cleveland Clinic Foundation d.b.a. Cleveland Clinic Health System INTERIM UNAUDITED CONSOLIDATED

Interim Unaudited Consolidated Financial Statements and Other Information For The Period Ended March 31, 2018 The Cleveland Clinic Foundation d.b.a. Cleveland Clinic Health System INTERIM UNAUDITED CONSOLIDATED

Mount Sinai Medical Center of Florida, Inc. and Subsidiaries

Mount Sinai Medical Center of Florida, Inc. and Subsidiaries Consolidated Financial Statements as of and for the Years Ended December 31, 2013 and 2012, Supplemental Information as of and for the Year

Mount Sinai Medical Center of Florida, Inc. and Subsidiaries Consolidated Financial Statements as of and for the Years Ended December 31, 2013 and 2012, Supplemental Information as of and for the Year

Power & Utilities Spotlight Generating a Discussion About the FASB s New Revenue Standard

August 2014 Power & Utilities Spotlight Generating a Discussion About the FASB s New Revenue Standard In This Issue: Background Key Accounting Issues Effective Date and Transition Implementation Challenges

August 2014 Power & Utilities Spotlight Generating a Discussion About the FASB s New Revenue Standard In This Issue: Background Key Accounting Issues Effective Date and Transition Implementation Challenges

Aurora Health Care, Inc. and Affiliates

Aurora Health Care, Inc. and Affiliates Consolidated Financial Statements as of and for the Years Ended December 31, 2017 and 2016, and Independent Auditors' Report AURORA HEALTH CARE, INC. AND AFFILIATES

Aurora Health Care, Inc. and Affiliates Consolidated Financial Statements as of and for the Years Ended December 31, 2017 and 2016, and Independent Auditors' Report AURORA HEALTH CARE, INC. AND AFFILIATES

Aerospace & Defense Spotlight The Converged Revenue Recognition Model Has Landed

September 2014 Aerospace & Defense Spotlight The Converged Revenue Recognition Model Has Landed In This Issue: Background Key Accounting Issues Effective Date and Transition Challenges for A&D Entities

September 2014 Aerospace & Defense Spotlight The Converged Revenue Recognition Model Has Landed In This Issue: Background Key Accounting Issues Effective Date and Transition Challenges for A&D Entities

Interim Unaudited Consolidated Financial Statements and Other Information

Interim Unaudited Consolidated Financial Statements and Other Information For The Period Ended September 30, 2018 The Cleveland Clinic Foundation d.b.a. Cleveland Clinic Health System INTERIM UNAUDITED

Interim Unaudited Consolidated Financial Statements and Other Information For The Period Ended September 30, 2018 The Cleveland Clinic Foundation d.b.a. Cleveland Clinic Health System INTERIM UNAUDITED

Mount Nittany Health System and Affiliates d/b/a Mount Nittany Health

Mount Nittany Health System and Affiliates d/b/a Mount Nittany Health Consolidated Financial Statements and Supplementary Information Table of Contents Page Independent Auditors Report 1 Financial Statements

Mount Nittany Health System and Affiliates d/b/a Mount Nittany Health Consolidated Financial Statements and Supplementary Information Table of Contents Page Independent Auditors Report 1 Financial Statements

Up to Speed: Accounting update for Healthcare Providers. David Woodall Assurance Partner - Birmingham, AL

www.pwc.com Up to Speed: Accounting update for Healthcare Providers David Woodall Assurance Partner - Birmingham, AL Sean O Hara Assurance Senior Manager Nashville, TN Agenda FASB update The new revenue

www.pwc.com Up to Speed: Accounting update for Healthcare Providers David Woodall Assurance Partner - Birmingham, AL Sean O Hara Assurance Senior Manager Nashville, TN Agenda FASB update The new revenue

Mount Sinai Medical Center of Florida, Inc. and Subsidiaries

Mount Sinai Medical Center of Florida, Inc. and Subsidiaries Consolidated Financial Statements as of and for the Years Ended December 31, 2012 and 2011, Supplemental Information as of and for the Year

Mount Sinai Medical Center of Florida, Inc. and Subsidiaries Consolidated Financial Statements as of and for the Years Ended December 31, 2012 and 2011, Supplemental Information as of and for the Year

UNIVERSITY HOSPITALS HEALTH SYSTEM, INC. Consolidated Financial Statements. December 31, 2016 and (With Independent Auditors Reports Thereon)

") Consolidated Financial Statements (With Independent Auditors Reports Thereon) Table of Contents Page Independent Auditors Report 1 Consolidated Financial Statements Consolidated Balance Sheets 2 Consolidated

Consolidated Financial Statements (With Independent Auditors Reports Thereon) Table of Contents Page Independent Auditors Report 1 Consolidated Financial Statements Consolidated Balance Sheets 2 Consolidated

RWJ BARNABAS HEALTH, INC. Consolidated Financial Statements. December 31, 2017 and (With Independent Auditors Report Thereon)

") Consolidated Financial Statements (With Independent Auditors Report Thereon) Table of Contents Page Independent Auditors Report 1 Consolidated Financial Statements: Consolidated Balance Sheets 2 Consolidated

Consolidated Financial Statements (With Independent Auditors Report Thereon) Table of Contents Page Independent Auditors Report 1 Consolidated Financial Statements: Consolidated Balance Sheets 2 Consolidated

KAISER FOUNDATION HEALTH PLAN, INC. AND SUBSIDIARIES AND KAISER FOUNDATION HOSPITALS AND SUBSIDIARIES. Combined Financial Statements

Combined Financial Statements (Unaudited) Table of Contents Page Financial Statements (Unaudited): Kaiser Foundation Health Plan, Inc. and Subsidiaries and Kaiser Foundation Hospitals and Subsidiaries:

Combined Financial Statements (Unaudited) Table of Contents Page Financial Statements (Unaudited): Kaiser Foundation Health Plan, Inc. and Subsidiaries and Kaiser Foundation Hospitals and Subsidiaries:

RWJ BARNABAS HEALTH, INC. Consolidated Financial Statements. December 31, (With Independent Auditors Report Thereon)

") Consolidated Financial Statements (With Independent Auditors Report Thereon) Table of Contents Page Independent Auditors Report 1 Consolidated Financial Statements: Consolidated Balance Sheet 3 Consolidated

Consolidated Financial Statements (With Independent Auditors Report Thereon) Table of Contents Page Independent Auditors Report 1 Consolidated Financial Statements: Consolidated Balance Sheet 3 Consolidated

Aurora Health Care, Inc. and Affiliates

Aurora Health Care, Inc. and Affiliates Consolidated Financial Statements as of and for the Years Ended December 31, 2016 and 2015, and Independent Auditors' Report AURORA HEALTH CARE, INC. AND AFFILIATES

Aurora Health Care, Inc. and Affiliates Consolidated Financial Statements as of and for the Years Ended December 31, 2016 and 2015, and Independent Auditors' Report AURORA HEALTH CARE, INC. AND AFFILIATES

DECODING CHALLENGES FOR GOVERNMENT REIMBURSEMENT

The New Healthcare World of Revenue Recognition, ASC 606 DECODING CHALLENGES FOR GOVERNMENT REIMBURSEMENT August 1, 2018 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO

The New Healthcare World of Revenue Recognition, ASC 606 DECODING CHALLENGES FOR GOVERNMENT REIMBURSEMENT August 1, 2018 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO

Financial Statements and Report of Independent Certified Public Accountants. Cape Regional Medical Center, Inc. December 31, 2017 and 2016

Financial Statements and Report of Independent Certified Public Accountants Cape Regional Medical Center, Inc. Contents Page Report of Independent Certified Public Accountants 3 Financial statements Balance