Revenue Recognition PREPARE NOW. Presented By Mary Jalbert, Principal Michael Whitten, Senior Manager October 3, 2017

|

|

|

- Adelia Price

- 6 years ago

- Views:

Transcription

1 Revenue Recognition PREPARE NOW Presented By Mary Jalbert, Principal Michael Whitten, Senior Manager October 3, 2017

2 Agenda TODAY S OBJECTIVE: A meaningful discussion and exchange of ideas resulting in tangible steps to apply in the revenue recognition implementation process 1. AICPA task force guidance (issued & pending) 2. Start preparing now 3. Examples 2

3 AICPA Task Force REVENUE RECOGNITION FIVE-STEP PROCESS UNDER THE NEW STANDARD 1. Identify the contract with the patient: Can be written, oral, or implied. Written or oral contracts could include: Signed patient responsibility forms Consent of service forms Patient scheduled appointments (online, in-person, telephone, etc.) Establishment of an implied contract: Required by law or regulation to treat emergency conditions (through the ED) and often provide services to uninsured or underinsured patients regardless of their ability to pay Not-for-profit entities (501(c)(3)) are charitable organizations and have certain requirements to maintain their tax-exempt status, charitable mission, or both. 3

4 AICPA Task Force REVENUE RECOGNITION FIVE-STEP PROCESS UNDER THE NEW STANDARD 2. Identify separate performance obligations (if applicable) 3. Determine the transaction price: For hospitals and clinics, the transaction price is ultimately the amount they will record as net patient service revenue for services provided to a patient or portfolio of patients. The transaction price includes the effects of variable consideration (explicit or implicit) and the consideration of other constraints. Example of explicit Example of implicit 4

5 AICPA Task Force REVENUE RECOGNITION FIVE-STEP PROCESS UNDER THE NEW STANDARD 3. Determine the transaction price (continued): Even after considering variable price concessions, entities should incorporate any other constraints that may exist related to the patient s (or patients in the patient class) ability to pay that may result in a significant revenue reversal at some point in the future. 4. Allocate the transaction price to the separate performance obligations in the contract (if applicable) 5. Recognize revenue when the entity satisfies the performance obligation What is not changing significantly under the new standard? 5

6 AICPA Task Force APPLICATION OF THE PORTFOLIO APPROACH APPLICATION OF THE PORTFOLIO APPROACH The new standard allows entities to use the portfolio approach, a practical expedient to account for patient contracts as a collective group, rather than individually, if the financial statement effects are not expected to materially differ from an individual contract approach. Entities will be required to use judgment when determining the size and composition of portfolios. The new standard specifies the need for similar characteristics among contracts to be grouped together; however, it does permit the application of a reasonable approach to determine the portfolios that would be appropriate for its types of contracts. 6

7 AICPA Task Force APPLICATION OF THE PORTFOLIO APPROACH APPLICATION OF THE PORTFOLIO APPROACH Healthcare entities may consider some of the following to determine the grouping of contracts with similar characteristics within a portfolio: TYPE OF SERVICE inpatient, outpatient, emergency room, physician practice, elective versus non-elective procedures, etc. TYPE OF PAYORS full coverage insurance contract (Anthem, Aetna, etc.), insurance contract with patient responsibility (deductible, co-pay), governmental programs (Medicare, Medicaid), uninsured self-pay, etc. Entities may also consider the size of the co-pay or deductible as a further consideration (high deductible plans) UNINSURED SELF-PAY may consider uninsured self-pay patients with whom the entity has no previous history, uninsured self-pay patients with a positive payment history, and uninsured self-pay patients with a history of making no payments TIMING of when the contracts are entered into (same quarter) 7

8 Revenue Recognition BE PREPARED START PREPARING NOW Consider conducting a readiness assessment of your organization: Review the current service offerings to determine when a contract may exist with a patient Review the current process for estimating the transaction price (determining net patient service revenue) and consider what changes may need to be made to record net patient service revenue under the new standard 8

9 Revenue Recognition BE PREPARED START PREPARING NOW It will be important for your organization to determine what type(s) of data it has or can derive from its revenue cycle system to support the following: Historical collections on patients with coinsurance and deductibles compared to patients with no insurance Historical success rate for qualifying patients for Medicare and Medicaid benefits Historical rate of patients who qualify for your organization s financial assistance policy Other types of historical data that your organization may require based on the services it provides WHAT IS THE EFFECTIVE DATE? Fiscal years ending 9/30/2019 for conduit debt obligors It will be one year before the lease implementation 9

10 Examples IMPLICIT PRICE CONCESSION UNINSURED SELF-PAY PATIENT (SINGLE CONTRACT) Patient is treated through the ED, the hospital does not assess their ability to pay at the time of service. Patient is uninsured and does not qualify for any type of financial assistance (charity care or uninsured discount under the hospital s policies, or government entitlement programs). Total gross charges for the services provided were $10,000 which the hospital intends to pursue collection of and may engage a collection agency to do so. However, the hospital has a collection history with similar types of patients and expects to collect only $1,000 from the patient. The hospital has provided an implicit price concession to this patient because (a) the hospital is required to provide emergency services regardless of the patient s ability to pay under the Social Security Act, and (b) the hospital continues to provide services to uninsured self-pay patients even when historical experience indicates it is not probable that they will collect substantially all of the charges. Thus, $1,000 is determined to be the transaction price and the hospital concludes that it is probable it will collect this amount and records patient revenue and accounts receivable of $1,000. The new standard requires the hospital to update the estimated transaction price, including the assessment of whether variable consideration is constrained at the end of each reporting period. Subsequent adjustments (positive or negative) are made to patient revenue and accounts receivable (adjustments to the contractual allowance). 10

11 Examples IMPLICIT PRICE CONCESSION UNINSURED SELF-PAY PATIENT WITH UNINSURED DISCOUNT (SINGLE CONTRACT) Patient is treated through the ED. The hospital is required to provide emergency services regardless of the patient s ability to pay and based on its stated mission. In addition, based on the requirements of IRC Section 501(r), the hospital makes reasonable efforts to determine whether patients are eligible for assistance under its financial assistance policy. During the patient s stay and before discharge, the hospital determines the patient qualifies for its financial assistance policy (uninsured discount) and grants the patient a 75% discount (this is an explicit price concession). Total charges for the services provided were $40,000. Thus, upon billing a $30,000 discount (contractual allowance) is applied resulting in net charges of $10,000 being billed to the patient, which the hospital intends to pursue collection of. The hospital has a collection history with similar types of patients and expects to collect only $1,000 from the patient which is determined to be the transaction price and the hospital concludes that it is probable it will collect this amount and records patient revenue and accounts receivable of $1,000. The facts and circumstances indicate the hospital's intention when entering into the contract with the patient was to provide a price concession because (a) the hospital is required to provide emergency services regardless of the patient's ability to pay under the Social Security Act; (b) as per its stated mission and in accordance with IRC Section 501(r), the hospital is required to limit amounts charged for emergency services to individuals eligible for assistance under the hospital's financial assistance policy; and (c) the hospital continues to provide services to uninsured self-pay patients even when historical experience indicates that it is not probable that the entity will collect substantially all of the discounted charges. 11

12 Examples IMPLICIT PRICE CONCESSION INSURED PATIENT WITH HIGH DEDUCTIBLE PLAN (SINGLE CONTRACT) Patient is treated at an urgent care clinic but, prior to providing service, does not determine whether or not the patient has a patient responsibility (for example, whether or not the patient has met his or her deductible for the period) and, if so, whether the patient has the ability to pay it. The charges for the services provided to the patient are $5,000. After services are provided, the patient presents proof of coverage with a commercial insurance company. Based on its contract with the commercial payor, the clinic determines there is a contractual adjustment of $3,000 (that is, an explicit price concession). Therefore, the discounted charges for services provided to the patient are $2,000. The clinic has a history of providing services to insured patients with high deductible plans and collecting amounts that are substantially less than its discounted charges. The clinic considered that the services were provided early in the calendar year and, therefore, patients with high deductible plans may not have met their deductible. Based on its historical experience with patients with high deductible plans during similar time periods in prior years, the clinic estimates that it only expects to collect $200 for the contract. The clinic intends to pursue collection of the $2,000 and may engage the use of external collection agencies to do so. That is, the clinic does not intend to give up collecting the discounted charges. The facts and circumstances indicate that the clinic's intention, when entering into the contract with the patient, was to provide an implicit price concession, it concludes that $200 is the transaction price. The clinic concludes that it is probable that it will collect the $200 and records patient service revenue and accounts receivable of $

13 Examples NO IMPLICIT PRICE CONCESSION UNINSURED SELF-PAY PATIENT (SINGLE CONTRACT) An uninsured self-pay patient schedules an elective cosmetic surgery at an outpatient surgery center that has a policy of performing a credit assessment prior to providing elective surgery to its patients. The gross charges for the procedure are $4,000. Prior to surgery, the outpatient surgery center assesses the patient's ability to pay and grants the patient special pricing of $3,000 (that is, an explicit price concession or discount of $1,000), which is similar to what it would charge an insured patient. The outpatient surgery center collects $1,500 upfront and agrees to bill the patient the remaining $1,500 after the surgery. Based on its credit assessment, the outpatient surgery center determines that it is probable that it will collect the remaining $1,500 due from the patient and does not intend to provide a further price concession or discount. The outpatient surgery center records patient service revenue of $3,000, accounts receivable of $1,500, and cash of $1,500. Based on a subsequent change in facts and circumstances, the surgery center determines that it only expects to collect $500 of the $1,500 billed to the patient. Therefore, the remaining $1,000 that it does not expect to collect represents an impairment loss (bad debt expense). 13

14 Examples IMPLICIT PRICE CONCESSION INSURED PATIENTS WITH CO-PAYMENT (PORTFOLIO APPROACH) A hospital provides services to patients during a reporting period and determines that they are covered by insurance carrier B and that each patient has a patient responsibility (co-payment). Because of its not-for-profit mission, the hospital does not have a policy of assessing patients' intent and ability to pay their patient responsibility portion prior to providing service. Because of the similar characteristics of the patients (that is, each patient is covered by insurance carrier B and has a similar co-payment), the hospital applies a portfolio approach. This portfolio of contracts is identified based on qualitative and quantitative factors, and the hospital concludes the expected outcome from using a portfolio approach is not expected to materially differ from an individual contract approach. Its insurance carrier B portfolio includes both the insurance and co-payment amounts. The charges for services provided to patients in this portfolio total $1,000,000 for the reporting period. Based on its contractual agreement with insurance carrier B, the hospital applies contractual adjustments of 50%, or $500,000. The contractual adjustments represent explicit price concessions. The contractual adjustments are recognized as a reduction to the transaction price. The remaining charges of $500,000 include $475,000 in amounts due from insurance carrier B and $25,000 in co-payment amounts due from the patients. 14

15 Examples IMPLICIT PRICE CONCESSION INSURED PATIENTS WITH CO-PAYMENT (PORTFOLIO APPROACH) - CONTINUED Based on its historical experience, the hospital expects to collect all of the amounts due from insurance carrier B ($475,000) but only expects to collect 40% or $10,000 of the co-payment amounts due from the patients. In total, the hospital expects to collect $485,000. Because the hospital has a business practice of providing services to patients regardless of their ability to pay, it determines that the $15,000 it does not expect to collect of patient copayments represents an implicit price concession. Therefore, the hospital determines that the transaction price is $485,000 (gross charges of $1,000,000, less contractual adjustments of $500,000, less the implicit price concessions of $15,000) and that collection of substantially all of the transaction price is probable. The hospital determines the criteria in the standard have been met because it has legally enforceable contracts with the patients, the contracts have commercial substance, the services provided and payment terms can be identified, and the parties have approved the contracts. Based on its expectation of payment from insurance carrier B, the hospital concludes that it is probable that a significant revenue reversal in the cumulative amount of revenue recognized ($485,000) will not occur as the uncertainty is resolved (that is, as payments are received). The hospital recognizes patient revenue and accounts receivable of $485,

16 Examples IMPLICIT PRICE CONCESSION INSURED PATIENTS WITH CO-PAYMENT (PORTFOLIO APPROACH) - CONCLUDED If the hospital subsequently determines it will only collect $475,000, instead of $485,000 it initially estimated, it will need to evaluate whether it has obtained any adverse information regarding the financial condition of the patients in the portfolio to determine if an impairment exists. If no adverse information regarding the patients' financial condition has been obtained, the Task Force believes the hospital should generally account for the difference as an increase to the implicit price concession (that is, a reduction to the estimate of the transaction price through contractual allowances) because the hospital determined that it intended to provide an implicit price concession. If the hospital experiences frequent subsequent adjustments that result in decreases to patient revenue, the hospital should re-assess whether its estimation process, including its application of the constraint, is appropriate. 16

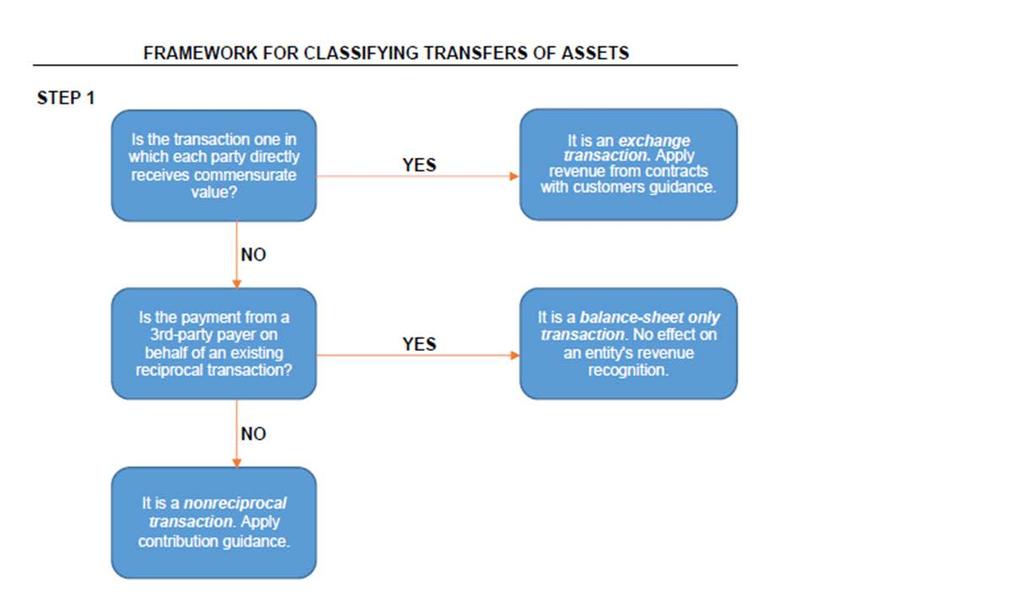

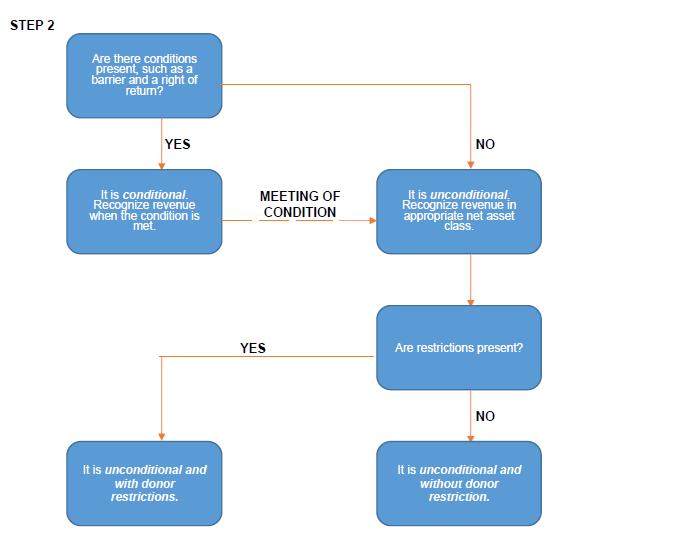

17 Contributions PROPOSED ASU TO CLARIFY GUIDANCE FOR CONTRIBUTIONS RECEIVED AND MADE BY NOT-FOR-PROFITS ISSUE 1: Reciprocal (Exchange) vs. Nonreciprocal (nonexchange/contribution) Who receives the benefit ISSUE 2: Conditional vs. Unconditional Contributions Right of return must exist Agreement must include a barrier Comment period deadline November 1,

18 18

19 19

20 Contact Us MARY JALBERT Principal MICHAEL WHITTEN Senior Manager

Revenue Recognition PREPARE NOW. Presented By Michael Whitten, Senior Manager April 23, 2018

Revenue Recognition PREPARE NOW Presented By Michael Whitten, Senior Manager April 23, 2018 Agenda TODAY S OBJECTIVE: A meaningful discussion and exchange of ideas resulting in tangible steps to apply

Revenue Recognition PREPARE NOW Presented By Michael Whitten, Senior Manager April 23, 2018 Agenda TODAY S OBJECTIVE: A meaningful discussion and exchange of ideas resulting in tangible steps to apply

Revenue Recognition ASU No

Revenue Recognition ASU No. 2014 09 April 19, 2018 Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC registered investment advisor. CliftonLarsonAllen LLP

Revenue Recognition ASU No. 2014 09 April 19, 2018 Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC registered investment advisor. CliftonLarsonAllen LLP

d. 8-4, Recognizing a CCRC s performance obligation(s) to provide future services and use of facilities to residents

to provide future services and use of facilities to residents") June 1, 2017 Financial Reporting Center Revenue Recognition Working Draft: Health Care Entities Revenue Recognition Implementation Issue Issue #8-6 Presentation and Disclosure Expected Overall Level of

June 1, 2017 Financial Reporting Center Revenue Recognition Working Draft: Health Care Entities Revenue Recognition Implementation Issue Issue #8-6 Presentation and Disclosure Expected Overall Level of

Implementing Revenue Recognition for Health Care Organizations J A N U A R Y

Implementing Revenue Recognition for Health Care Organizations J A N U A R Y 2 0 1 9 AGENDA 1 Introductions & Objectives 2 Background, Key Principles, & Transition 3 Common Industry Implementation Challenges

Implementing Revenue Recognition for Health Care Organizations J A N U A R Y 2 0 1 9 AGENDA 1 Introductions & Objectives 2 Background, Key Principles, & Transition 3 Common Industry Implementation Challenges

Revenue Recognition: A Comprehensive Review for Health Care Entities

Revenue Recognition: A Comprehensive Review for Health Care Entities Table of Contents INTRODUCTION... 4 THE MODEL... 5 SCOPE... 5 CONTRIBUTIONS/GRANTS... 5 COLLABORATIVE ARRANGEMENTS... 6 CHARITY CARE...

Revenue Recognition: A Comprehensive Review for Health Care Entities Table of Contents INTRODUCTION... 4 THE MODEL... 5 SCOPE... 5 CONTRIBUTIONS/GRANTS... 5 COLLABORATIVE ARRANGEMENTS... 6 CHARITY CARE...

Implementing Revenue Recognition for Health Care Organizations M A R C H 1 8,

Implementing Revenue Recognition for Health Care Organizations M A R C H 1 8, 2 0 1 8 Background & Key Principles ASU 2014-09 REVENUE FROM CONTRACTS WITH CUSTOMERS Effective for Public Business Entities

Implementing Revenue Recognition for Health Care Organizations M A R C H 1 8, 2 0 1 8 Background & Key Principles ASU 2014-09 REVENUE FROM CONTRACTS WITH CUSTOMERS Effective for Public Business Entities

Implementing Revenue Recognition for Health Care Organizations S E P T E M B E R 2 1,

Implementing Revenue Recognition for Health Care Organizations S E P T E M B E R 2 1, 2 0 1 8 INTRODUCTIONS Kimberly McKay, CPA Managing Partner kmckay@bkd.com Implementing Revenue Recognition for Health

Implementing Revenue Recognition for Health Care Organizations S E P T E M B E R 2 1, 2 0 1 8 INTRODUCTIONS Kimberly McKay, CPA Managing Partner kmckay@bkd.com Implementing Revenue Recognition for Health

New Jersey Chapter of HFMA Spring Education Event April 2016 ASC 606, Revenue from Contracts with Customers Overview for Healthcare Providers

New Jersey Chapter of HFMA Spring Education Event April 2016 ASC 606, Revenue from Contracts with Customers Overview for Healthcare Providers How Will Revenue be Recognized Under Contracts? Albert Deana,

New Jersey Chapter of HFMA Spring Education Event April 2016 ASC 606, Revenue from Contracts with Customers Overview for Healthcare Providers How Will Revenue be Recognized Under Contracts? Albert Deana,

Implementing Revenue Recognition for Health Care Organizations

Implementing Revenue Recognition for Health Care Organizations AUGUST 6, 2018 TO RECEIVE CPE CREDIT Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader is

Implementing Revenue Recognition for Health Care Organizations AUGUST 6, 2018 TO RECEIVE CPE CREDIT Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader is

Revenue for healthcare providers

Revenue for healthcare providers The new standard s effective date is coming. US GAAP November 2016 kpmg.com/us/frn b Revenue for healthcare providers Revenue viewed through a new lens Again and again,

Revenue for healthcare providers The new standard s effective date is coming. US GAAP November 2016 kpmg.com/us/frn b Revenue for healthcare providers Revenue viewed through a new lens Again and again,

FASB ASU NO REVENUE FROM CONTRACTS WITH CUSTOMERS (TOPIC 606)

") CPAs & ADVISORS experience clarity // REVENUE RECOGNITION FOR HEALTH CARE PROVIDERS Kimberly McKay, CPA Managing Partner BKD. LLP - Houston FASB ASU NO. 2014-09 REVENUE FROM CONTRACTS WITH CUSTOMERS (TOPIC

CPAs & ADVISORS experience clarity // REVENUE RECOGNITION FOR HEALTH CARE PROVIDERS Kimberly McKay, CPA Managing Partner BKD. LLP - Houston FASB ASU NO. 2014-09 REVENUE FROM CONTRACTS WITH CUSTOMERS (TOPIC

2016 Revenue Recognition Session Parts 1 & 2

2016 AICPA Healthcare Conference 2016 Revenue Recognition Session Parts 1 & 2 Speaker Biographies 25-1 Mike Breen, CPA Mike is an audit partner in KPMG s New York Office. He has experience performing financial

2016 AICPA Healthcare Conference 2016 Revenue Recognition Session Parts 1 & 2 Speaker Biographies 25-1 Mike Breen, CPA Mike is an audit partner in KPMG s New York Office. He has experience performing financial

Accounting Standard Updates

Accounting Standard Updates HFMA Spring Conference 2018 Presented by: Kimberly Sokoloff, Health Care Assurance Services Senior Manager Elizabeth Lasnier, Health Care Assurance Services Manager Presenters

Accounting Standard Updates HFMA Spring Conference 2018 Presented by: Kimberly Sokoloff, Health Care Assurance Services Senior Manager Elizabeth Lasnier, Health Care Assurance Services Manager Presenters

COMPLEXITIES FOR LONG-TERM CARE

The New World of Revenue Recognition, ASC 606 COMPLEXITIES FOR LONG-TERM CARE June 27, 2018 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK

The New World of Revenue Recognition, ASC 606 COMPLEXITIES FOR LONG-TERM CARE June 27, 2018 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK

Revenue Recognition, Including Implicit Price Concession and Bad Debt Considerations, for Healthcare Organizations: Accounting Issues and Trends

Revenue Recognition, Including Implicit Price Concession and Bad Debt Considerations, for Healthcare Organizations: Accounting Issues and Trends Principles and Practices Board Issue Analysis January 2019

Revenue Recognition, Including Implicit Price Concession and Bad Debt Considerations, for Healthcare Organizations: Accounting Issues and Trends Principles and Practices Board Issue Analysis January 2019

REVENUE RECOGNITION FOR HEALTH CARE PROVIDERS

REVENUE RECOGNITION FOR HEALTH CARE PROVIDERS Tracy Young, CPA Partner -BKD, LLP Brent Beaulieu, CPA VP Finance Baptist Health ASU 2014-09 REVENUE FROM CONTRACTS WITH CUSTOMERS Effective for Public Business

REVENUE RECOGNITION FOR HEALTH CARE PROVIDERS Tracy Young, CPA Partner -BKD, LLP Brent Beaulieu, CPA VP Finance Baptist Health ASU 2014-09 REVENUE FROM CONTRACTS WITH CUSTOMERS Effective for Public Business

Revenue from contracts with customers. Health care services industry supplement

Note: Since issuing the new revenue standard in May 2014, the FASB and IASB have proposed various amendments to the guidance. This In depth supplement has not been updated to reflect all of the proposed

Note: Since issuing the new revenue standard in May 2014, the FASB and IASB have proposed various amendments to the guidance. This In depth supplement has not been updated to reflect all of the proposed

AUDIT AND ACCOUNTING UPDATE

AUDIT AND ACCOUNTING UPDATE HFMA FL Regional Education Session - Clearwater November 11, 2016 Presenter Carlos Hernandez Southeast Assurance Leader Carlos.hernandez@rsmus.com 2 Agenda Topic Recent accounting

AUDIT AND ACCOUNTING UPDATE HFMA FL Regional Education Session - Clearwater November 11, 2016 Presenter Carlos Hernandez Southeast Assurance Leader Carlos.hernandez@rsmus.com 2 Agenda Topic Recent accounting

REVENUE RECOGNITION ASU /8/2016. CPAs & ADVISORS ACCOUNTING AND AUDITING UPDATE FOR ARKANSAS HFMA

CPAs & ADVISORS experience clarity // ACCOUNTING AND AUDITING UPDATE FOR ARKANSAS HFMA Tracy Young, CPA Partner, BKD Health Care Group Little Rock REVENUE RECOGNITION ASU 2014-09 1 FASB/IASB ORIGINAL REVENUE

CPAs & ADVISORS experience clarity // ACCOUNTING AND AUDITING UPDATE FOR ARKANSAS HFMA Tracy Young, CPA Partner, BKD Health Care Group Little Rock REVENUE RECOGNITION ASU 2014-09 1 FASB/IASB ORIGINAL REVENUE

HFMA Great Lakes Chapter Accounting and Auditing Update February 16, 2018

HFMA Great Lakes Chapter Accounting and Auditing Update February 16, 2018 Who We Are CAROLYN BIELAWSKI, CPA ASSOCIATE Education: Bachelor of Arts in Accounting, Master of Science in Accounting, Michigan

HFMA Great Lakes Chapter Accounting and Auditing Update February 16, 2018 Who We Are CAROLYN BIELAWSKI, CPA ASSOCIATE Education: Bachelor of Arts in Accounting, Master of Science in Accounting, Michigan

PATIENT ASSISTANCE PROGRAM

Policy: ADM30.00, v.10 Category: Administrative/Patient Accounts PATIENT ASSISTANCE PROGRAM Effective: 08/10/2016 Origination Date: 05/02/2003 I. PURPOSE: The purpose of this policy is to further the charitable

Policy: ADM30.00, v.10 Category: Administrative/Patient Accounts PATIENT ASSISTANCE PROGRAM Effective: 08/10/2016 Origination Date: 05/02/2003 I. PURPOSE: The purpose of this policy is to further the charitable

REVENUE RECOGNITION ASU /23/2016. CPAs & ADVISORS ACCOUNTING AND AUDITING UPDATE FOR ARKANSAS HFMA

CPAs & ADVISORS experience clarity // ACCOUNTING AND AUDITING UPDATE FOR ARKANSAS HFMA Drew Speed, CPA Partner, Accounting and Auditing Director, Little Rock REVENUE RECOGNITION ASU 2014-09 1 FASB/IASB

CPAs & ADVISORS experience clarity // ACCOUNTING AND AUDITING UPDATE FOR ARKANSAS HFMA Drew Speed, CPA Partner, Accounting and Auditing Director, Little Rock REVENUE RECOGNITION ASU 2014-09 1 FASB/IASB

Advocate Health Care Network and Subsidiaries FINANCIAL REPORT

Advocate Health Care Network and Subsidiaries FINANCIAL REPORT For the First Quarter Ended March 31, 2018 Cautionary Statement Regarding Forward Looking Statements in this Quarterly Financial Report This

Advocate Health Care Network and Subsidiaries FINANCIAL REPORT For the First Quarter Ended March 31, 2018 Cautionary Statement Regarding Forward Looking Statements in this Quarterly Financial Report This

Changes to revenue recognition in the health care industry

Changes to revenue recognition in the health care industry Prepared by: Dan Vandenberghe, Partner, RSM US LLP dan.vandenberghe@rsmus.com, +1 612 376 9267 Jay Adkisson, Partner, RSM US LLP jay.adkisson@rsmus.com,

Changes to revenue recognition in the health care industry Prepared by: Dan Vandenberghe, Partner, RSM US LLP dan.vandenberghe@rsmus.com, +1 612 376 9267 Jay Adkisson, Partner, RSM US LLP jay.adkisson@rsmus.com,

Banner Health and Subsidiaries Years Ended December 31, 2017 and 2016 With Report of Independent Auditors

C ONSOLIDATED F INANCIAL S TATEMENTS Banner Health and Subsidiaries Years Ended December 31, 2017 and 2016 With Report of Independent Auditors Ernst & Young LLP Consolidated Financial Statements Years

C ONSOLIDATED F INANCIAL S TATEMENTS Banner Health and Subsidiaries Years Ended December 31, 2017 and 2016 With Report of Independent Auditors Ernst & Young LLP Consolidated Financial Statements Years

Mayo Clinic. Unaudited Condensed Consolidated Financial Statements Quarter Ended June 30, 2018

Mayo Clinic Unaudited Condensed Consolidated Financial Statements Quarter Ended June 30, 2018 Mayo Clinic Contents Unaudited Financial Statements Condensed consolidated statements of financial 1 position

Mayo Clinic Unaudited Condensed Consolidated Financial Statements Quarter Ended June 30, 2018 Mayo Clinic Contents Unaudited Financial Statements Condensed consolidated statements of financial 1 position

F I N A N C I A L S T A T E M E N T S. Banner Health and Subsidiaries Years Ended December 31, 2018 and 2017 With Report of Independent Auditors

C O N S O L I D A T E D F I N A N C I A L S T A T E M E N T S Years Ended December 31, 2018 and 2017 With Report of Independent Auditors Ernst & Young LLP Consolidated Financial Statements Years Ended

C O N S O L I D A T E D F I N A N C I A L S T A T E M E N T S Years Ended December 31, 2018 and 2017 With Report of Independent Auditors Ernst & Young LLP Consolidated Financial Statements Years Ended

RWJ BARNABAS HEALTH, INC. Consolidated Financial Statements. December 31, 2017 and (With Independent Auditors Report Thereon)

") Consolidated Financial Statements (With Independent Auditors Report Thereon) Table of Contents Page Independent Auditors Report 1 Consolidated Financial Statements: Consolidated Balance Sheets 2 Consolidated

Consolidated Financial Statements (With Independent Auditors Report Thereon) Table of Contents Page Independent Auditors Report 1 Consolidated Financial Statements: Consolidated Balance Sheets 2 Consolidated

Mount Sinai Medical Center of Florida, Inc. and Subsidiaries

Mount Sinai Medical Center of Florida, Inc. and Subsidiaries Consolidated Financial Statements as of and for the Years Ended December 31, 2013 and 2012, Supplemental Information as of and for the Year

Mount Sinai Medical Center of Florida, Inc. and Subsidiaries Consolidated Financial Statements as of and for the Years Ended December 31, 2013 and 2012, Supplemental Information as of and for the Year

JUPITER MEDICAL CENTER, INC. AND AFFILIATED COMPANIES. Jupiter, Florida. CONSOLIDATED FINANCIAL STATEMENTS September 30, 2014 and 2013

JUPITER MEDICAL CENTER, INC. AND AFFILIATED COMPANIES Jupiter, Florida CONSOLIDATED FINANCIAL STATEMENTS Jupiter, Florida CONSOLIDATED FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR S REPORT... 1 FINANCIAL

JUPITER MEDICAL CENTER, INC. AND AFFILIATED COMPANIES Jupiter, Florida CONSOLIDATED FINANCIAL STATEMENTS Jupiter, Florida CONSOLIDATED FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR S REPORT... 1 FINANCIAL

Laurel Lake Retirement Community, Inc. and Subsidiary YEARS ENDED DECEMBER 31, 2018 AND 2017

Laurel Lake Retirement Community, Inc. and Subsidiary CONSOLIDATED FINANCIAL STATEMENTS CONTENTS Independent auditor s report 1 Financial statement: Consolidated statements of financial position 2 Consolidated

Laurel Lake Retirement Community, Inc. and Subsidiary CONSOLIDATED FINANCIAL STATEMENTS CONTENTS Independent auditor s report 1 Financial statement: Consolidated statements of financial position 2 Consolidated

MANAGEMENT S DISCUSSION OF FINANCIAL AND OPERATING PERFORMANCE

MANAGEMENT S DISCUSSION OF FINANCIAL AND OPERATING PERFORMANCE Utilization Trends The Corporation has experienced an increase in utilization from the end of 2015 through fiscal year 2017. Occupancy of

MANAGEMENT S DISCUSSION OF FINANCIAL AND OPERATING PERFORMANCE Utilization Trends The Corporation has experienced an increase in utilization from the end of 2015 through fiscal year 2017. Occupancy of

Mayo Clinic. Unaudited Condensed Consolidated Financial Statements Quarter Ended March 31, 2018

Mayo Clinic Unaudited Condensed Consolidated Financial Statements Quarter Ended March 31, 2018 Mayo Clinic Contents Unaudited Financial Statements Condensed consolidated statements of financial 1 position

Mayo Clinic Unaudited Condensed Consolidated Financial Statements Quarter Ended March 31, 2018 Mayo Clinic Contents Unaudited Financial Statements Condensed consolidated statements of financial 1 position

RWJ BARNABAS HEALTH, INC. Consolidated Financial Statements. December 31, (With Independent Auditors Report Thereon)

") Consolidated Financial Statements (With Independent Auditors Report Thereon) Table of Contents Page Independent Auditors Report 1 Consolidated Financial Statements: Consolidated Balance Sheet 3 Consolidated

Consolidated Financial Statements (With Independent Auditors Report Thereon) Table of Contents Page Independent Auditors Report 1 Consolidated Financial Statements: Consolidated Balance Sheet 3 Consolidated

POLK MEDICAL CENTER, INC. ROME, GEORGIA FINANCIAL STATEMENTS. for the years ended June 30, 2016 and 2015

ROME, GEORGIA FINANCIAL STATEMENTS for the years ended C O N T E N T S Pages Independent Auditor s Report 1-2 Financial Statements: Balance Sheets 3-4 Statements of Operations and Changes in Net Assets

ROME, GEORGIA FINANCIAL STATEMENTS for the years ended C O N T E N T S Pages Independent Auditor s Report 1-2 Financial Statements: Balance Sheets 3-4 Statements of Operations and Changes in Net Assets

JUPITER MEDICAL CENTER, INC. AND AFFILIATED COMPANIES. Jupiter, Florida. CONSOLIDATED FINANCIAL STATEMENTS September 30, 2015 and 2014

JUPITER MEDICAL CENTER, INC. AND AFFILIATED COMPANIES Jupiter, Florida CONSOLIDATED FINANCIAL STATEMENTS Jupiter, Florida CONSOLIDATED FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR S REPORT... 1 FINANCIAL

JUPITER MEDICAL CENTER, INC. AND AFFILIATED COMPANIES Jupiter, Florida CONSOLIDATED FINANCIAL STATEMENTS Jupiter, Florida CONSOLIDATED FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR S REPORT... 1 FINANCIAL

GREENWOOD LEFLORE HOSPITAL. Audited Financial Statements Years Ended September 30, 2015 and 2014

Audited Financial Statements CONTENTS Independent Auditor's Report 1 2 Management's Discussion and Analysis 3 10 Financial Statements Statements of Net Position 11 Statements of Revenues, Expenses and

Audited Financial Statements CONTENTS Independent Auditor's Report 1 2 Management's Discussion and Analysis 3 10 Financial Statements Statements of Net Position 11 Statements of Revenues, Expenses and

Atchison Hospital Association, Inc. and Riverbend Regional Healthcare Foundation. Consolidated Financial Report September 30, 2015

Consolidated Financial Report September 30, 2015 Contents Independent Auditor s Report on the Financial Statements 1 2 Financial Statements Consolidated balance sheets 3 4 Consolidated statements of operations

Consolidated Financial Report September 30, 2015 Contents Independent Auditor s Report on the Financial Statements 1 2 Financial Statements Consolidated balance sheets 3 4 Consolidated statements of operations

Mount Nittany Health System and Affiliates d/b/a Mount Nittany Health

Mount Nittany Health System and Affiliates d/b/a Mount Nittany Health Consolidated Financial Statements and Supplementary Information Table of Contents Page Independent Auditors Report 1 Financial Statements

Mount Nittany Health System and Affiliates d/b/a Mount Nittany Health Consolidated Financial Statements and Supplementary Information Table of Contents Page Independent Auditors Report 1 Financial Statements

South Shore Health System, Inc. (Formerly South Shore Health and Educational Corporation) and Subsidiaries

and Subsidiaries") South Shore Health System, Inc. (Formerly South Shore Health and Educational Corporation) and Subsidiaries Consolidated Financial Statements as of and for the Years Ended September 30, 2016 and 2015, Supplemental

South Shore Health System, Inc. (Formerly South Shore Health and Educational Corporation) and Subsidiaries Consolidated Financial Statements as of and for the Years Ended September 30, 2016 and 2015, Supplemental

Subject: FINANCIAL POLICY

and ER Physicians Group At also known as Page 1 of 6 STATEMENT OF PURPOSE; To ensure that (JH) and ER Physicians Group At (ERP Group) has financial stability and can meet its mission and continue to provide

and ER Physicians Group At also known as Page 1 of 6 STATEMENT OF PURPOSE; To ensure that (JH) and ER Physicians Group At (ERP Group) has financial stability and can meet its mission and continue to provide

ACCOUNTING AND AUDIT UPDATE

ACCOUNTING AND AUDIT UPDATE HFMA FL Regional Education Session - Hollywood January 19, 2017 Presenter Carlos Hernandez Southeast Assurance Leader Carlos.hernandez@rsmus.com 2 Agenda Accounting and Auditing

ACCOUNTING AND AUDIT UPDATE HFMA FL Regional Education Session - Hollywood January 19, 2017 Presenter Carlos Hernandez Southeast Assurance Leader Carlos.hernandez@rsmus.com 2 Agenda Accounting and Auditing

Trinity Health Operating Income continues to climb in Q1 FY19

Trinity Health Operating Income continues to climb in Q1 FY19 Summary Highlights for the First Quarter of FY19 (Quarter Ended September 30, 2018) In the first quarter of fiscal year 2019, Trinity Health

Trinity Health Operating Income continues to climb in Q1 FY19 Summary Highlights for the First Quarter of FY19 (Quarter Ended September 30, 2018) In the first quarter of fiscal year 2019, Trinity Health

South Shore Health System, Inc. and Subsidiaries

South Shore Health System, Inc. and Subsidiaries Consolidated Financial Statements as of and for the Years Ended September 30, 2017 and 2016, Supplemental Consolidating Schedules as of and for the Year

South Shore Health System, Inc. and Subsidiaries Consolidated Financial Statements as of and for the Years Ended September 30, 2017 and 2016, Supplemental Consolidating Schedules as of and for the Year

NEBRASKA METHODIST HEALTH SYSTEM, INC. AND AFFILIATES. Consolidated Financial Statements. December 31, 2016 and 2015

Consolidated Financial Statements (With Independent Auditors Report Thereon) and OMB Uniform Guidance Reports December 31, 2016 KPMG LLP Suite 300 1212 N. 96th Street Omaha, NE 68114-2274 Suite 1120 1248

Consolidated Financial Statements (With Independent Auditors Report Thereon) and OMB Uniform Guidance Reports December 31, 2016 KPMG LLP Suite 300 1212 N. 96th Street Omaha, NE 68114-2274 Suite 1120 1248

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC Form 10-Q

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 Form 10-Q Quarterly report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the quarterly period ended 2018

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 Form 10-Q Quarterly report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the quarterly period ended 2018

Financial Statements. Years Ended September 30, 2016 and 2015

The report accompanying these financial statements was issued by BDO USA, LLP, a Delaware limited liability partnership and the U.S. member of BDO International Limited, a UK company limited by guarantee.

The report accompanying these financial statements was issued by BDO USA, LLP, a Delaware limited liability partnership and the U.S. member of BDO International Limited, a UK company limited by guarantee.

Trinity Health Operating Revenue Grows 5.5% to $9.5 billion in the First Half of FY19

Trinity Health Operating Revenue Grows 5.5% to $9.5 billion in the First Half of FY19 Summary Highlights for the First Half of FY19 (Six Months Ended December 31, 2018) During the first six months of fiscal

Trinity Health Operating Revenue Grows 5.5% to $9.5 billion in the First Half of FY19 Summary Highlights for the First Half of FY19 (Six Months Ended December 31, 2018) During the first six months of fiscal

MULTICARE HEALTH SYSTEM. Consolidated Financial Statements. December 31, 2011 and (With Independent Auditors Report Thereon)

") Consolidated Financial Statements (With Independent Auditors Report Thereon) KPMG LLP Suite 900 801 Second Avenue Seattle, WA 98104 Independent Auditors Report The Board of Directors MultiCare Health System:

Consolidated Financial Statements (With Independent Auditors Report Thereon) KPMG LLP Suite 900 801 Second Avenue Seattle, WA 98104 Independent Auditors Report The Board of Directors MultiCare Health System:

Printed copies are for reference only. Please refer to the electronic copy for the latest version.

Policy #: 5146 Version: 3 Page: 1 of 9 Policy: CentraState, and any other substantially related entities (as defined under the Internal Revenue Code ( IRC ) 501(r) final regulations), will comply with

Policy #: 5146 Version: 3 Page: 1 of 9 Policy: CentraState, and any other substantially related entities (as defined under the Internal Revenue Code ( IRC ) 501(r) final regulations), will comply with

The New York and Presbyterian Hospital As of and For the Six Months Ended June 30, 2018

U NAUDITED C ONSOLIDATED F INANCIAL S TATEMENTS AND S UPPLEMENTARY INFORMATION The New York and Presbyterian Hospital As of and For the Six Months Ended June 30, 2018 The New York and Presbyterian Hospital

U NAUDITED C ONSOLIDATED F INANCIAL S TATEMENTS AND S UPPLEMENTARY INFORMATION The New York and Presbyterian Hospital As of and For the Six Months Ended June 30, 2018 The New York and Presbyterian Hospital

Financial Statements and Report of Independent Certified Public Accountants. Cape Regional Medical Center, Inc. December 31, 2017 and 2016

Financial Statements and Report of Independent Certified Public Accountants Cape Regional Medical Center, Inc. Contents Page Report of Independent Certified Public Accountants 3 Financial statements Balance

Financial Statements and Report of Independent Certified Public Accountants Cape Regional Medical Center, Inc. Contents Page Report of Independent Certified Public Accountants 3 Financial statements Balance

Consolidated Financial Statements as of and for the Years Ended December 31, 2018 and 2017, and Independent Auditors Report

Consolidated Financial Statements as of and for the Years Ended December 31, 2018 and 2017, and Independent Auditors Report INTENTIONALLY BLANK TABLE OF CONTENTS INDEPENDENT AUDITORS REPORT 1 2 CONSOLIDATED

Consolidated Financial Statements as of and for the Years Ended December 31, 2018 and 2017, and Independent Auditors Report INTENTIONALLY BLANK TABLE OF CONTENTS INDEPENDENT AUDITORS REPORT 1 2 CONSOLIDATED

news FOR IMMEDIATE RELEASE

news FOR IMMEDIATE RELEASE INVESTOR CONTACT: MEDIA CONTACT: Mark Kimbrough Ed Fishbough 615-344-2688 615-344-2810 HCA Reports First Quarter 2018 Results Nashville, Tenn., May 1, 2018 HCA Healthcare, Inc.

news FOR IMMEDIATE RELEASE INVESTOR CONTACT: MEDIA CONTACT: Mark Kimbrough Ed Fishbough 615-344-2688 615-344-2810 HCA Reports First Quarter 2018 Results Nashville, Tenn., May 1, 2018 HCA Healthcare, Inc.

The Cooper Health System Years Ended December 31, 2015 and 2014 With Report of Independent Auditors

C ONSOLIDATED F INANCIAL S TATEMENTS AND S UPPLEMENTARY I NFORMATION The Cooper Health System Years Ended December 31, 2015 and 2014 With Report of Independent Auditors Ernst & Young LLP Consolidated Financial

C ONSOLIDATED F INANCIAL S TATEMENTS AND S UPPLEMENTARY I NFORMATION The Cooper Health System Years Ended December 31, 2015 and 2014 With Report of Independent Auditors Ernst & Young LLP Consolidated Financial

ATHENS REGIONAL HEALTH SERVICES, INC. AND SUBSIDIARIES. Consolidated Financial Statements and Consolidating Schedules. September 30, 2014 and 2013

Consolidated Financial Statements and Consolidating Schedules (With Independent Auditors Report Thereon) KPMG LLP Suite 2000 303 Peachtree Street, N.E. Atlanta, GA 30308-3210 Independent Auditors Report

Consolidated Financial Statements and Consolidating Schedules (With Independent Auditors Report Thereon) KPMG LLP Suite 2000 303 Peachtree Street, N.E. Atlanta, GA 30308-3210 Independent Auditors Report

Bronson Methodist Hospital. Financial Report December 31, 2014

Financial Report December 31, 2014 Contents Report Letter 1 Financial Statements Balance Sheet 2 Statement of Operations and Changes in Net Assets 3 Statement of Cash Flows 4 5-23 Independent Auditor's

Financial Report December 31, 2014 Contents Report Letter 1 Financial Statements Balance Sheet 2 Statement of Operations and Changes in Net Assets 3 Statement of Cash Flows 4 5-23 Independent Auditor's

MULTICARE HEALTH SYSTEM. Consolidated Financial Statements. December 31, 2016 and 2015

Consolidated Financial Statements (With Independent Auditors Report Thereon) and Independent Auditors Report In Accordance with The Uniform Guidance for Federal Awards Year ended December 31, 2016 Table

Consolidated Financial Statements (With Independent Auditors Report Thereon) and Independent Auditors Report In Accordance with The Uniform Guidance for Federal Awards Year ended December 31, 2016 Table

Hallmark Health Corporation and Affiliates

Hallmark Health Corporation and Affiliates Consolidated Financial Statements as of and for the Years Ended September 30, 2016 and 2015, Schedule of Expenditures of Federal Awards for the Year Ended September

Hallmark Health Corporation and Affiliates Consolidated Financial Statements as of and for the Years Ended September 30, 2016 and 2015, Schedule of Expenditures of Federal Awards for the Year Ended September

Financial Statements and Report of Independent Certified Public Accountants. Cape Regional Medical Center, Inc. December 31, 2016 and 2015

Financial Statements and Report of Independent Certified Public Accountants Cape Regional Medical Center, Inc. Contents Page Report of Independent Certified Public Accountants 3 Financial statements Balance

Financial Statements and Report of Independent Certified Public Accountants Cape Regional Medical Center, Inc. Contents Page Report of Independent Certified Public Accountants 3 Financial statements Balance

Cedars-Sinai Medical Center Years Ended June 30, 2016 and 2015 With Report of Independent Auditors

A UDITED C ONSOLIDATED F INANCIAL S TATEMENTS AND S UPPLEMENTARY I NFORMATION Cedars-Sinai Medical Center Years Ended June 30, 2016 and 2015 With Report of Independent Auditors Ernst & Young LLP Audited

A UDITED C ONSOLIDATED F INANCIAL S TATEMENTS AND S UPPLEMENTARY I NFORMATION Cedars-Sinai Medical Center Years Ended June 30, 2016 and 2015 With Report of Independent Auditors Ernst & Young LLP Audited

BRATTLEBORO MEMORIAL HOSPITAL FINANCIAL STATEMENTS. With Independent Auditors' Report

FINANCIAL STATEMENTS With Independent Auditors' Report TABLE OF CONTENTS Page(s) Independent Auditors' Report 1 Balance Sheets 2 Statements of Operations 3 Statements of Changes in Net Assets 4 Statements

FINANCIAL STATEMENTS With Independent Auditors' Report TABLE OF CONTENTS Page(s) Independent Auditors' Report 1 Balance Sheets 2 Statements of Operations 3 Statements of Changes in Net Assets 4 Statements

Hunterdon Medical Center

. c o m Financial Statements [Type text] Table of Contents Page Independent Auditors Report 1 Financial Statements Balance Sheet 3 Statement of Operations 4 Statement of Changes in Net Assets 5 Statement

. c o m Financial Statements [Type text] Table of Contents Page Independent Auditors Report 1 Financial Statements Balance Sheet 3 Statement of Operations 4 Statement of Changes in Net Assets 5 Statement

Financial Statements and Report of Independent Certified Public Accountants. Cape Regional Medical Center, Inc. December 31, 2015 and 2014

Financial Statements and Report of Independent Certified Public Accountants Cape Regional Medical Center, Inc. Contents Page Report of Independent Certified Public Accountants 3 Financial statements Balance

Financial Statements and Report of Independent Certified Public Accountants Cape Regional Medical Center, Inc. Contents Page Report of Independent Certified Public Accountants 3 Financial statements Balance

I. Policy: Definitions:

Page(s): 1 of 13 Subject: Financial Assistance Policy (Non-Profit Facilities) Formulated: 10/2016 10/2016, Manual: Patient Financial Services Reviewed: 12/2018 Corporate Board Approval Date: Last Revised:

Page(s): 1 of 13 Subject: Financial Assistance Policy (Non-Profit Facilities) Formulated: 10/2016 10/2016, Manual: Patient Financial Services Reviewed: 12/2018 Corporate Board Approval Date: Last Revised:

SELF REGIONAL HEALTHCARE AND AFFILIATES. Combined Financial Statements. September 30, 2013 and ( with Independent Auditors Report thereon )

") Combined Financial Statements September 30, 2013 and 2012 ( with Independent Auditors Report thereon ) Table of Contents September 30, 2013 and 2012 Page(s) Independent Auditors Report... 1 2 Management

Combined Financial Statements September 30, 2013 and 2012 ( with Independent Auditors Report thereon ) Table of Contents September 30, 2013 and 2012 Page(s) Independent Auditors Report... 1 2 Management

Mount Sinai Medical Center of Florida, Inc. and Subsidiaries

Mount Sinai Medical Center of Florida, Inc. and Subsidiaries Consolidated Financial Statements as of and for the Years Ended December 31, 2012 and 2011, Supplemental Information as of and for the Year

Mount Sinai Medical Center of Florida, Inc. and Subsidiaries Consolidated Financial Statements as of and for the Years Ended December 31, 2012 and 2011, Supplemental Information as of and for the Year

Definitions: As used in this Policy, the following terms have the meanings as set forth below:

Patient Information for Financial Assistance The Financial Assistance Policy (FAP) of the Medical Center Navicent Health (NAVICENT HEALTH) illustrates our commitment to our patients and the community we

Patient Information for Financial Assistance The Financial Assistance Policy (FAP) of the Medical Center Navicent Health (NAVICENT HEALTH) illustrates our commitment to our patients and the community we

Financial Statements. Years Ended September 30, 2012 and 2011

Financial Statements Years Ended September 30, 2012 and 2011 The report accompanying these financial statements was issued by BDO USA, LLP, a Delaware limited liability partnership and the U.S. member

Financial Statements Years Ended September 30, 2012 and 2011 The report accompanying these financial statements was issued by BDO USA, LLP, a Delaware limited liability partnership and the U.S. member

SAINT BARNABAS CORPORATION d/b/a BARNABAS HEALTH. December 31, 2011 and 2010

Consolidated Financial Statements and Supplementary Information (With Independent Auditors Report Thereon) Table of Contents Independent Auditors Report 1 Consolidated Financial Statements: Consolidated

Consolidated Financial Statements and Supplementary Information (With Independent Auditors Report Thereon) Table of Contents Independent Auditors Report 1 Consolidated Financial Statements: Consolidated

news FOR IMMEDIATE RELEASE

news FOR IMMEDIATE RELEASE INVESTOR CONTACT: MEDIA CONTACT: Mark Kimbrough Ed Fishbough 615-344-2688 615-344-2810 HCA Reports Third Quarter 2018 Results Nashville, Tenn., October 30, 2018 HCA Healthcare,

news FOR IMMEDIATE RELEASE INVESTOR CONTACT: MEDIA CONTACT: Mark Kimbrough Ed Fishbough 615-344-2688 615-344-2810 HCA Reports Third Quarter 2018 Results Nashville, Tenn., October 30, 2018 HCA Healthcare,

Gonzales Healthcare Systems Policy

Gonzales Healthcare Systems Policy Subject: Financial Policy and Healthcare Transparency Purpose: To provide affordable and quality healthcare to our community. Therefore, it is essential that we establish

Gonzales Healthcare Systems Policy Subject: Financial Policy and Healthcare Transparency Purpose: To provide affordable and quality healthcare to our community. Therefore, it is essential that we establish

MultiCare Health System Year End 2012 Results December 31, 2012

MultiCare Health System Year End 2012 Results December 31, 2012 MultiCare Health System (MHS), a Washington nonprofit corporation, is an integrated healthcare delivery system providing inpatient, outpatient,

MultiCare Health System Year End 2012 Results December 31, 2012 MultiCare Health System (MHS), a Washington nonprofit corporation, is an integrated healthcare delivery system providing inpatient, outpatient,

Avita Health System. Consolidated Financial Report with Additional Information June 30, 2016

Consolidated Financial Report with Additional Information June 30, 2016 Contents Report Letter 1-2 Consolidated Financial Statements Balance Sheet 3 Statement of Operations 4 Statement of Changes in Net

Consolidated Financial Report with Additional Information June 30, 2016 Contents Report Letter 1-2 Consolidated Financial Statements Balance Sheet 3 Statement of Operations 4 Statement of Changes in Net

CAMC Health System, Inc. and Subsidiaries

CAMC Health System, Inc. and Subsidiaries Consolidated Financial Statements and Other Financial Information as of and for the Years Ended December 31, 2016 and 2015, and Independent Auditors Report CAMC

CAMC Health System, Inc. and Subsidiaries Consolidated Financial Statements and Other Financial Information as of and for the Years Ended December 31, 2016 and 2015, and Independent Auditors Report CAMC

GREENWOOD LEFLORE HOSPITAL. Audited Financial Statements Years Ended September 30, 2017 and 2016

Audited Financial Statements CONTENTS Independent Auditor's Report 1 2 Management's Discussion and Analysis 3 10 Financial Statements Statements of Net Position 11 Statements of Revenues, Expenses and

Audited Financial Statements CONTENTS Independent Auditor's Report 1 2 Management's Discussion and Analysis 3 10 Financial Statements Statements of Net Position 11 Statements of Revenues, Expenses and

NORTH MISSISSIPPI MEDICAL CENTER, INC., CLAY COUNTY MEDICAL CORPORATION, AND WEBSTER HEALTH SERVICES, INC. (The Obligated Group)

") Combined Financial Statements (With Independent Auditors Report Thereon) KPMG LLP Suite 1100 One Jackson Place 188 East Capitol Street Jackson, MS 39201-2127 Independent Auditors Report The Board of Directors

Combined Financial Statements (With Independent Auditors Report Thereon) KPMG LLP Suite 1100 One Jackson Place 188 East Capitol Street Jackson, MS 39201-2127 Independent Auditors Report The Board of Directors

Mercy Health Years Ended June 30, 2012 and 2011 With Report of Independent Auditors

CONSOLIDATED FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION Mercy Health Years Ended June 30, 2012 and 2011 With Report of Independent Auditors Consolidated Financial Statements and Supplementary Information

CONSOLIDATED FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION Mercy Health Years Ended June 30, 2012 and 2011 With Report of Independent Auditors Consolidated Financial Statements and Supplementary Information

ATHENS REGIONAL HEALTH SERVICES, INC. AND SUBSIDIARIES. Consolidated Financial Statements. September 30, 2012 and 2011

Consolidated Financial Statements (With Independent Auditors Report Thereon) KPMG LLP Suite 2000 303 Peachtree Street, N.E. Atlanta, GA 30308-3210 Independent Auditors Report The Board of Trustees Athens

Consolidated Financial Statements (With Independent Auditors Report Thereon) KPMG LLP Suite 2000 303 Peachtree Street, N.E. Atlanta, GA 30308-3210 Independent Auditors Report The Board of Trustees Athens

C ONSOLIDATED F INANCIAL S TATEMENTS. BJC HealthCare Years Ended December 31, 2017 and 2016 With Report of Independent Auditors.

C ONSOLIDATED F INANCIAL S TATEMENTS BJC HealthCare Years Ended December 31, 2017 and 2016 With Report of Independent Auditors Ernst & Young LLP Consolidated Financial Statements Years Ended December 31,

C ONSOLIDATED F INANCIAL S TATEMENTS BJC HealthCare Years Ended December 31, 2017 and 2016 With Report of Independent Auditors Ernst & Young LLP Consolidated Financial Statements Years Ended December 31,

ALBANY MEDICAL CENTER AND RELATED ENTITIES. Combined Financial Statements and Supplementary Information. December 31, 2014 and 2013

Combined Financial Statements and Supplementary Information (With Independent Auditors Report Thereon) Combined Financial Statements and Supplementary Information Table of Contents Independent Auditors

Combined Financial Statements and Supplementary Information (With Independent Auditors Report Thereon) Combined Financial Statements and Supplementary Information Table of Contents Independent Auditors

0 1 if A Certified Public Accountants

1 : al 0 1 if A Certified Public Accountants Audited Consolidated Financial Statements (Supplemental Schedules and Other Information) Pikeville Medical Center, Inc. and Subsidiaries Years Ended September

1 : al 0 1 if A Certified Public Accountants Audited Consolidated Financial Statements (Supplemental Schedules and Other Information) Pikeville Medical Center, Inc. and Subsidiaries Years Ended September

Patient Financial Assistance Program

Patient Financial Assistance Program Mary Washington Healthcare Level: Supersedes: Hospitals Mary Washington Hospital, Stafford Hospital Patient Financial Assistance Program (corporate); Patient Financial

Patient Financial Assistance Program Mary Washington Healthcare Level: Supersedes: Hospitals Mary Washington Hospital, Stafford Hospital Patient Financial Assistance Program (corporate); Patient Financial

indicates change Entire policy has been updated

Metro Health FINANCIAL ASSISTANCE ELIGIBILITY Section PFS Former Policy Number PFS-D151 Policy Number PFS-03 Original Date June 2004 Effective Date March 2017 Next Review March 2018 indicates change Entire

Metro Health FINANCIAL ASSISTANCE ELIGIBILITY Section PFS Former Policy Number PFS-D151 Policy Number PFS-03 Original Date June 2004 Effective Date March 2017 Next Review March 2018 indicates change Entire

I LJ~LEY MEDICAL CENTER

I LJ~LEY MEDICAL CENTER Consolidated Financial Statement For the Nine Months Ended March 31, 2017 Hurley Medical Center Nine Month Period Ended March 31, 2017 Management Discussion and Analysis For the

I LJ~LEY MEDICAL CENTER Consolidated Financial Statement For the Nine Months Ended March 31, 2017 Hurley Medical Center Nine Month Period Ended March 31, 2017 Management Discussion and Analysis For the

DUKE UNIVERSITY HEALTH SYSTEM, INC. AND AFFILIATES

Consolidated Financial Statements December 31, 2017 and 2016 (Unaudited) Prepared by: Duke University Health System Finance Print Date: January 17, 2018 Consolidated Balance Sheets (Unaudited) December

Consolidated Financial Statements December 31, 2017 and 2016 (Unaudited) Prepared by: Duke University Health System Finance Print Date: January 17, 2018 Consolidated Balance Sheets (Unaudited) December

COMMUNITY HEALTH NETWORK, INC. & AFFILIATED ENTITIES

COMMUNITY HEALTH NETWORK, INC. & AFFILIATED ENTITIES Unaudited Consolidated Financial Statements As of and for the Quarter Ended March 31, 2012 and A-1 Quarterly Financial Information Community Health

COMMUNITY HEALTH NETWORK, INC. & AFFILIATED ENTITIES Unaudited Consolidated Financial Statements As of and for the Quarter Ended March 31, 2012 and A-1 Quarterly Financial Information Community Health

NANTICOKE HEALTH SERVICES, INC. AND SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION YEARS ENDED JUNE 30, 2016 AND 2015

NANTICOKE HEALTH SERVICES, INC. AND SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION YEARS ENDED TABLE OF CONTENTS YEARS ENDED INDEPENDENT AUDITORS' REPORT 1 CONSOLIDATED FINANCIAL

NANTICOKE HEALTH SERVICES, INC. AND SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION YEARS ENDED TABLE OF CONTENTS YEARS ENDED INDEPENDENT AUDITORS' REPORT 1 CONSOLIDATED FINANCIAL

Financial Assistance for Uninsured Patients (Discounted Care or Charity Care)

") Financial Assistance for Uninsured Patients (Discounted Care or Charity Care) Purpose To provide guidelines and procedures for the identification, documentation and application for those needing financial

Financial Assistance for Uninsured Patients (Discounted Care or Charity Care) Purpose To provide guidelines and procedures for the identification, documentation and application for those needing financial

Ashland Hospital Corporation and Subsidiaries d/b/a King s Daughters Medical Center

Consolidated Financial Statements Years Ended September 30, 2013 and 2012 With Independent Auditors Report Consolidated Financial Statements Years Ended September 30, 2013 and 2012 Contents Independent

Consolidated Financial Statements Years Ended September 30, 2013 and 2012 With Independent Auditors Report Consolidated Financial Statements Years Ended September 30, 2013 and 2012 Contents Independent

Baptist Health Care Corporation and Subsidiaries Years Ended September 30, 2017 and 2016 With Report of Independent Certified Public Accountants

C ONSOLIDATED F INANCIAL S TATEMENTS AND S UPPLEMENTARY I NFORMATION Baptist Health Care Corporation and Subsidiaries Years Ended September 30, 2017 and 2016 With Report of Independent Certified Public

C ONSOLIDATED F INANCIAL S TATEMENTS AND S UPPLEMENTARY I NFORMATION Baptist Health Care Corporation and Subsidiaries Years Ended September 30, 2017 and 2016 With Report of Independent Certified Public

Banner Health and Subsidiaries Years Ended December 31, 2015 and 2014 With Report of Independent Auditors

C ONSOLIDATED F INANCIAL S TATEMENTS Banner Health and Subsidiaries Years Ended December 31, 2015 and 2014 With Report of Independent Auditors Ernst & Young LLP Consolidated Financial Statements Years

C ONSOLIDATED F INANCIAL S TATEMENTS Banner Health and Subsidiaries Years Ended December 31, 2015 and 2014 With Report of Independent Auditors Ernst & Young LLP Consolidated Financial Statements Years

Pascack Valley Health System, LLC Consolidated Financial Statements December 31, 2016 and 2015

Pascack Valley Health System, LLC Consolidated Financial Statements Index Page(s) Report of Independent Auditors... 1 Consolidated Financial Statements Balance Sheets... 2 Statements of Operations... 3

Pascack Valley Health System, LLC Consolidated Financial Statements Index Page(s) Report of Independent Auditors... 1 Consolidated Financial Statements Balance Sheets... 2 Statements of Operations... 3

GREENWOOD LEFLORE HOSPITAL. Audited Financial Statements Years Ended September 30, 2016 and 2015

Audited Financial Statements CONTENTS Independent Auditor's Report 1 2 Management's Discussion and Analysis 3 10 Financial Statements Statements of Net Position 11 Statements of Revenues, Expenses and

Audited Financial Statements CONTENTS Independent Auditor's Report 1 2 Management's Discussion and Analysis 3 10 Financial Statements Statements of Net Position 11 Statements of Revenues, Expenses and

Catawba Valley Medical Center and Affiliate (Component Unit of Catawba County) Combined Financial Statements and Supplementary Information

Combined Financial Statements and Supplementary Information") Catawba Valley Medical Center and Affiliate (Component Unit of Catawba County) Combined Financial Statements and Supplementary Information Years Ended June 30, 2016 and 2015 Table of Contents Independent

Catawba Valley Medical Center and Affiliate (Component Unit of Catawba County) Combined Financial Statements and Supplementary Information Years Ended June 30, 2016 and 2015 Table of Contents Independent

Consolidated Financial Statements and Report of Independent Certified Public Accountants

Consolidated Financial Statements and Report of Independent Certified Public Accountants H. Lee Moffitt Cancer Center & Research Institute, Inc. and Subsidiaries June 30, 2017 and 2016 H. Lee Moffitt Cancer

Consolidated Financial Statements and Report of Independent Certified Public Accountants H. Lee Moffitt Cancer Center & Research Institute, Inc. and Subsidiaries June 30, 2017 and 2016 H. Lee Moffitt Cancer

Signs are posted throughout the facility to provide education about charity/fap policies.

Page 1 of 12 I. PURPOSE UC Irvine Medical Center strives to provide quality patient care and high standards for the communities we serve. This policy demonstrates UC Irvine Medical Center s commitment

Page 1 of 12 I. PURPOSE UC Irvine Medical Center strives to provide quality patient care and high standards for the communities we serve. This policy demonstrates UC Irvine Medical Center s commitment

Insider. Health Care. Form 990 Schedule H Updates. In This Issue. Insights & Observations for the Health Care Industry Volume 3 :: Issue 3

Health Care Insider Insights & Observations for the Health Care Industry Volume 3 :: Issue 3 In This Issue Form 990 Schedule H Updates... 1,2 Presentation and Disclosure of Patient Service Revenue... 3,4,5

Health Care Insider Insights & Observations for the Health Care Industry Volume 3 :: Issue 3 In This Issue Form 990 Schedule H Updates... 1,2 Presentation and Disclosure of Patient Service Revenue... 3,4,5

Definitions: As used in this Policy, the following terms have the meanings as set forth below:

Al IN" Nit, 4, Nun, NavicentHealth Patient Information for Financial Assistance The Financial Assistance Policy (FAP) of Navicent Health illustrates our commitment to our patients and the community we

Al IN" Nit, 4, Nun, NavicentHealth Patient Information for Financial Assistance The Financial Assistance Policy (FAP) of Navicent Health illustrates our commitment to our patients and the community we

DUKE UNIVERSITY HEALTH SYSTEM, INC. AND AFFILIATES

Consolidated Financial Statements March 31, 2018 and 2017 (Unaudited) Prepared by: Duke University Health System Finance Print Date: April 24, 2018 Consolidated Balance Sheets (Unaudited) March 31, 2018

Consolidated Financial Statements March 31, 2018 and 2017 (Unaudited) Prepared by: Duke University Health System Finance Print Date: April 24, 2018 Consolidated Balance Sheets (Unaudited) March 31, 2018