AGA Accounting Principles Committee

|

|

|

- Janel Blankenship

- 5 years ago

- Views:

Transcription

1 AGA Accounting Principles Committee ASU : REVENUE FROM CONTRACTS WITH CUSTOMERS (TOPIC 606)

2 Presenter and Agenda Presenter: Lucas Carpenter U.S. Power & Utilities Practice Senior Manager Agenda: Basics of new standard Update on standard setting activities The Five Steps and Industry focus areas Disclosures and SEC reporting matters Implementation 2

3 Basics of the new standard Overview Impacts Standard could significantly change how most entities recognize revenue Standard is intended to be principle based Will remove existing industryspecific guidance Expanded qualitative and quantitative disclosures (annual and interim) Transition Resource Group AICPA industry working groups Achieve a single, comprehensive revenue recognition model Core principle is that revenue recognition depicts transfer of control to customer in an amount that reflects consideration to which entity expects to be entitled 3

4 Basics of the new standard Scope Scope set to improve consistency and comparability within industries, across industries, and across capital markets Scope of the standard Contracts with customers of all entities and industries within scope with only certain transactions excluded Specifically excluded Lease contracts Insurance contracts Financial instruments Guarantees (other than product warranties) Certain nonmonetary exchanges Contracts with other than customers (e.g., collaborations) 4

5 Basics of the new standard Effective dates Effective date Early adoption permitted? Method of adoption U.S. GAAP Public U.S. GAAP Non-public Beginning after Beginning after Beginning on December 15, 2017 December 15, 2018 January 1, calendar year 2019 calendar year 2018 calendar year Yes Yes Yes No earlier than the No earlier than the original effective date for original effective date for public entities public entities 2017 calendar year 2017 calendar year Retrospective (with certain practical expedients allowed) or modified retrospective IFRS 5

6 Basics of the new standard Five-step model 1: Identify the contract(s) with a customer 2: Identify the performance obligations in the contract 3: Determine the transaction price 4: Allocate the transaction price to the performance obligations in the contract 5: Recognize revenue when (or as) the entity satisfies a performance obligation 6

7 Update on standard setting activities 7

8 Revenue from contracts with customers Update on standard setting activities Recent FASB standard setting activities related to the new revenue standard Standard Status Impact on P&U sector Deferral of effective date Identifying performance obligations and licenses Principle versus agent considerations Narrow scope improvements and practical expedients Technical corrections and provide additional relief from certain disclosure requirements Final ASU High (but don t delay implementation efforts!!) Final ASU Performance obligations (moderate) Licenses (low) Final ASU Low Final ASU Collectibility (high) ED issued in Q (comment period ends on July 2, 2016) Non-cash consideration (low) Presentation of sales taxes (moderate) Transition expedients (moderate) Pre-production activities (low) Disclosure of remaining performance obligation (moderate) Loss provisions for onerous contracts (low) 8

9 Standard setting process in the U.S. (AICPA) AICPA P&U Revenue Recognition Task Force AICPA Revenue Recognition Working Group FinRec AICPA Revenue Recognition Guide AICPA Sector Task Forces TRG, SEC and FASB 9

10 The Five Steps and Industry Focus Areas 10

11 Comparison to existing guidance Step 1 1: Identify the contract(s) with a customer Existing guidance Contract is an agreement between parties that creates legally enforceable rights and obligations New guidance Generally consistent with existing practice Little guidance on accounting for contract modifications Explicit guidance provided on accounting for contract modifications 11

12 Step 1 Industry impacts (continued) Accounting for contract modifications 1 New contract: distinct goods or services at stand-alone selling price 2 Continuation of contract: remaining goods or services distinct from existing contract 3 Continuation of contract: goods or services not distinct from existing contract Prospective, impacting new goods or services only Prospective, impacting both remaining and new goods Cumulative catch up 4 If combination of above Apply principles above 12

13 Step 1 Industry impacts Focus areas Industry focus areas include Are sales to regulated customers within the scope of the new standard? Are contributions in aid of construction within the scope of the new standard? Revenue cannot be recognized if collectability is not probable does this impact revenue recognition for certain hardship customers and how should company's consider regulatory recovery mechanisms in place? How to apply the contract modification guidance to blend and extend and other common contractual arrangements? 13

14 Tariff-based sales Are revenues from sales under a regulated utility s tariff (other than alternative revenue program) within the scope of Topic 606? View A In scope Utility service is distinguishable from alternative revenue programs Represent a contract between the utility and its customers View B Out of scope Not distinguishable from alternative revenue programs Tariff sales are not a contract between the utility and its customers Task force consensus that tariff-based sales are in scope Disclosure consideration for alternative revenue programs 14

15 Contributions in aid of construction (CIAC) Key focus issue for the Power & Utilities AICPA Task Force Two views currently being debated: View A CIAC is out of scope View B CIAC is in scope; performance obligation represents stand-ready obligation to serve customer over the life of the asset Potential impact to the balance sheet and income statement Challenges of implementing if in scope Next steps 15

16 Contributions in aid of construction (CIAC) (continued) Simplified example: Customer contributes $100 to extend an electric line to their home Current model Utility collects cash and records a CIAC Liability for $100 Utility constructs asset and records as PP&E; cash is spent on construction For financial statement purposes: 1. PP&E and the CIAC Liability are presented net on the balance sheet (net balance sheet impact is $0) 2. Amortization of the PP&E and CIAC Liability are presented net on the income statement 3. Net income impact is $0 ASC 606 model (View B) Utility collects cash and records Deferred Revenue (a liability) for $100 Utility constructs asset and records as PP&E; cash is spent on construction For financial statement purposes: 1. PP&E and the Deferred Revenue are presented gross on the balance sheet (i.e., impact is a $100 balance sheet gross-up) 2. Amortization of the PP&E is reflected within Depreciation Expense; amortization of Deferred Revenue is shown as Revenue from Contracts with Customers (i.e., impact is an income statement gross-up of $100) 3. Net income impact is $0 16

17 Collectibility Step 1 (Identify the Contract) of ASU 606 ( ) stipulates that an entity will only apply the revenue guidance to contracts when it is probable that the entity will collect substantially all of the consideration it is entitled to in exchange for the goods or services it transfers to the customer. Key considerations Application of the portfolio approach Constraint on recognition if required to provide additional goods / services 17

18 Collectibility (continued) Utility bills customer $100 and assumes 20 percent chance of collection ($80 reserve requirement). Assume there is no bad debt tracker and ignore recoveries embedded in current rates. (Current model) Dr. AR $100 Cr. Revenue $100 Dr. Bad Debt Expense $80 Cr. Allowance for Bad Debts $80 (Under ASC 606 not in scope) Dr. AR $0 Cr. Revenue $0 Dr. Bad Debt Expense $0 Cr. Allowance for Bad Debts $0 18

19 Blend-and-extend contract modifications Two views under discussion View A A blend-and-extend contract modification should be accounted for as a separate contract Additional deliveries are distinct Price of the contract increases by an amount of consideration that reflects the entity s standalone selling price for the additional deliveries View B A blend-and-extend contract modification should be accounted for as if it were the termination of the existing contract and the creation of a new contract - Additional deliveries are distinct - Price of the contract does not increase by an amount of consideration that reflects the entity s standalone selling price for the additional deliveries 19

20 Blend-and-extend contract modifications Example Background On January 1, 2012, Ivy Power Producers executed a 5-year power sales contract with Rosemary Electric & Gas at a fixed price of $50/MWh for a contract term through 2016 (assume no financing component) On January 1, 2015, Ivy Power Producers and Rosemary Electric & Gas agreed to (1) extend the contract for another 2 years (through 2018) and (2) amend the contract pricing as follows: Current existing contract price: $50/MWh Forward market price at modification date ( ): $40/MWh Modified price to be billed ( ): $45/MWh 20

21 Blend-and-extend contract modifications (continued) Example View A (Separate contract) Year 4 & 5 Dr. AR $45 Dr. Contract Asset $5 Cr. Revenue $50 Year 6 & 7 Dr. AR $45 Cr. Revenue $40 Cr. Contract Asset $5 View B (Termination of existing contract) Dr. AR $45 Cr. Revenue $45 21

22 Comparison to existing guidance Step 2 2: Identify the performance obligations in the contract Existing guidance Deliverables must have standalone value to be accounted for separately New guidance Performance obligations and distinct replace deliverable and standalone value in assessing multiple element arrangements 22

23 Bundled arrangements (e.g. PPAs) In April 2016, FASB updated revenue standard on performance obligations Clarification of distinct Is the objective to transfer individual goods or a combined item? Immaterial promises Is the promised good or service immaterial in the context of the contract? Shipping and handling activities Do shipping and handling activities occur after control of the goods is transferred to the customer? Industry Focus Areas: Level of integration of products / services Separate analysis of RECs and capacity Elements on a customer s bill (e.g., transmission, distribution, basic service) Next steps 23

24 Comparison to existing guidance Step 3 3: Determine the transaction price Existing guidance Arrangement s fee must be fixed or determinable for revenue to be recognized New guidance Variable consideration must be estimated subject to a constraint (exception for licenses of intellectual property involving sales- or usage- based royalties) Discounting of revenues required in limited circumstances Entities must assess whether a significant financing component exists 24

25 Variable consideration vs. Optional purchases Key focus issue for the Power & Utilities AICPA Task Force (in the context of requirements contracts ) Optional purchases Customer has a right to choose to purchase additional goods or services Each is a separate purchase decision Prior to customer s exercise of the option, the vendor is not obligated to provide those goods or services and the customer is not obligated to pay for those goods or services Variable consideration The contract obligates the vendor to transfer promised goods or services The ultimate quantity of good or services is not known and is outside the control of the vendor and customer Customer is obligated to pay for each good or service transferred Determining the nature of the promise (including pricing) is key Next steps 25

26 Comparison to existing guidance Step 4 4: Allocate the transaction price to the performance obligations in the contract Existing guidance Allocate transaction price to multiple deliverables based on relative selling price New guidance Generally consistent with existing practice 26

27 Step 4 Industry impacts Focus areas Industry focus areas include How should you allocate the transaction price to each performance obligation (e.g., PPA with energy, capacity, and RECs) - How should you allocate variable consideration? - How should you allocate a discount that a customer receives for purchasing a bundle of goods or services (e.g., PPA with energy, capacity, and RECs) How should you determine standalone selling price? 27

28 Comparison to existing guidance Step 5 5: Recognize revenue when (or as) the entity satisfies a performance obligation Existing guidance Recognition based on transfer of the risks and rewards of ownership New guidance Revenue recognized when or as control of good or service transfers to the customer Criteria identified for assessing whether performance obligation is satisfied at a point in time or over time 28

29 Step 5 Industry impacts Focus areas Industry focus areas include When does control of a commodity transfer to the customer over time or at a point in time? If control transfers over time, how should progress toward complete satisfaction be measured? - When is it appropriate to use the practical expedient (i.e., recognize revenue in the amount to which the entity has a right to invoice) to measure progress? - What does the concept of value to customer mean in the standard? 29

30 Application of series guidance Series of goods and services Separately account for performance obligations if a series of goods or services are homogenous and meet both of the following criteria: Each distinct good or service in the series would be a performance obligation satisfied over time, and A single method used to measure the entity s progress toward satisfaction of the performance obligation A performance obligation is satisfied over time if any of the following criteria are met The customer receives and consumes the benefits of the entity s performance as the entity performs, or Entity s performance creates or enhances an asset (work in process) that the customer controls, or Entity s performance does not create an asset with an alternative use to the entity and the customer does not have control over the asset created, but the entity has a right to payment for performance completed to date 30

31 Application of series guidance to storable commodities and capacity Key considerations Consideration of immediate consumption criterion Capacity Would stand ready = service? Next steps 31

32 Step vs. Strip pricing Step pricing Stated, but changing, prices per unit for a fixed quantity Judgment in selecting method of measurement of progress Significant financing component May apply the invoice practical expedient Strip pricing Constant fixed price (i.e. the price per unit is identical for all units) Straight line over the contract period May apply the invoice practical expedient Potential to lead to different revenue profiles for contracts that deliver the same goods Next steps 32

33 Disclosures & Other SEC Reporting Matters 33

34 Annual disclosure requirements Disclosure type Disaggregated revenue Reconciliation of contract balances Performance obligations Significant judgments Practical expedients Required information Disaggregation of revenue into categories that show how economic factors affect the nature, amount, timing, and uncertainty of revenue and cash flows Opening and closing balances and revenue recognized during the period from changes in contract balances Qualitative and quantitative information about significant changes in contract balances Descriptive information about an entity s performance obligations Method used to recognize revenue for performance obligations satisfied over time and why the method is appropriate Significant judgments related to transfer of control for performance obligations satisfied at a point in time Information about the methods, inputs, and assumptions used to determine and allocate transaction price Existence of a significant financing component Expensing certain costs of obtaining contract 34

35 Other SEC matters Reporting issues related to adoption of new Revenue Recognition Standard - Selected financial data - Ratio of earnings to fixed charges 35

36 Registration statements Prior-period annual audited financial statements that are incorporated by reference in registration statements must be revised if: - The interim financial statements that are incorporated in the registration statements reflect an accounting change that requires retrospective application, and - The change is considered material SEC FRM OCA is available for consultation if a registrant believes that, based on its facts and circumstances, a retrospective application of the new revenue recognition standard to all periods required to be presented in a Form S-3 is impracticable. Wesley R. Bricker Deputy Chief Accountant May

37 Impact of registration statement filing on revenue adoption Example Company adopts the new revenue standard under the full-retrospective transition approach in Q Company files its 10Q with the SEC on April 16, 2018 On May 2, 2018, the Company files Form S-3 registration statement with the SEC The Form S-3 incorporates by reference the Company s K and 2018 Q1 10Q Impact Company must revise prior-period annual audited financial statements that are incorporated by reference in registration statements to reflect accounting change for the revenue standard Company will be required to restate an additional year in its Form S-3 to show the effect of the new revenue standard 37

38 Implementation 38

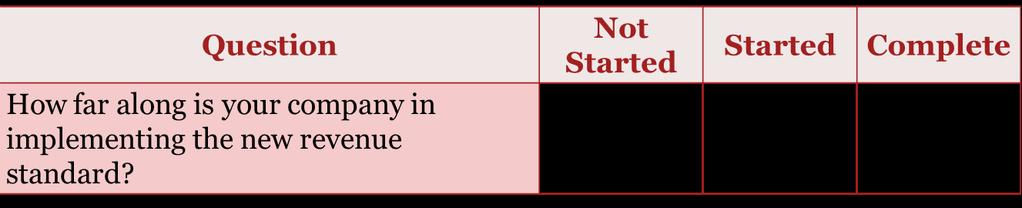

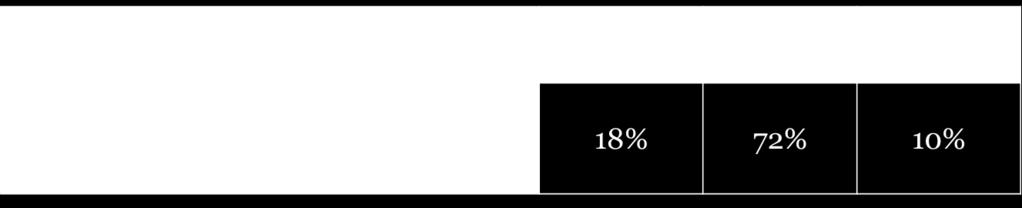

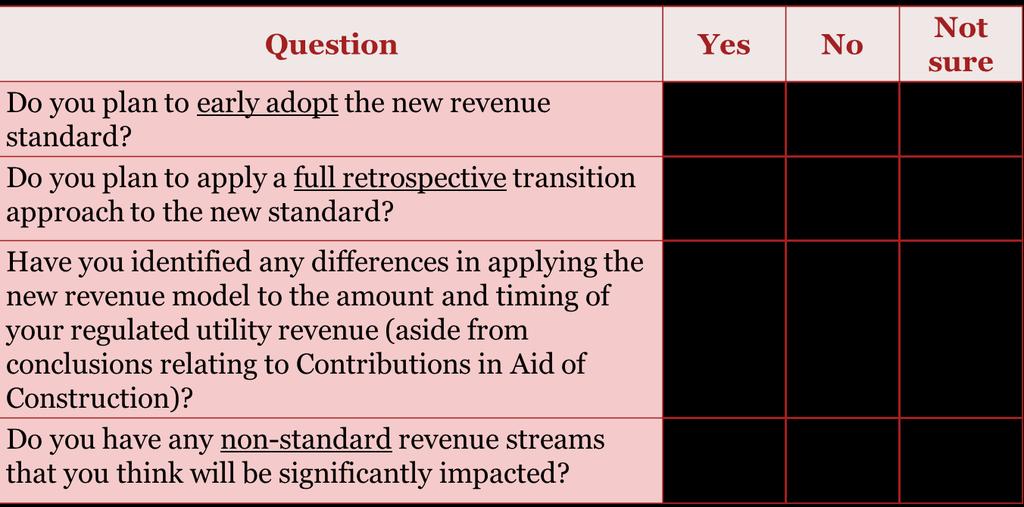

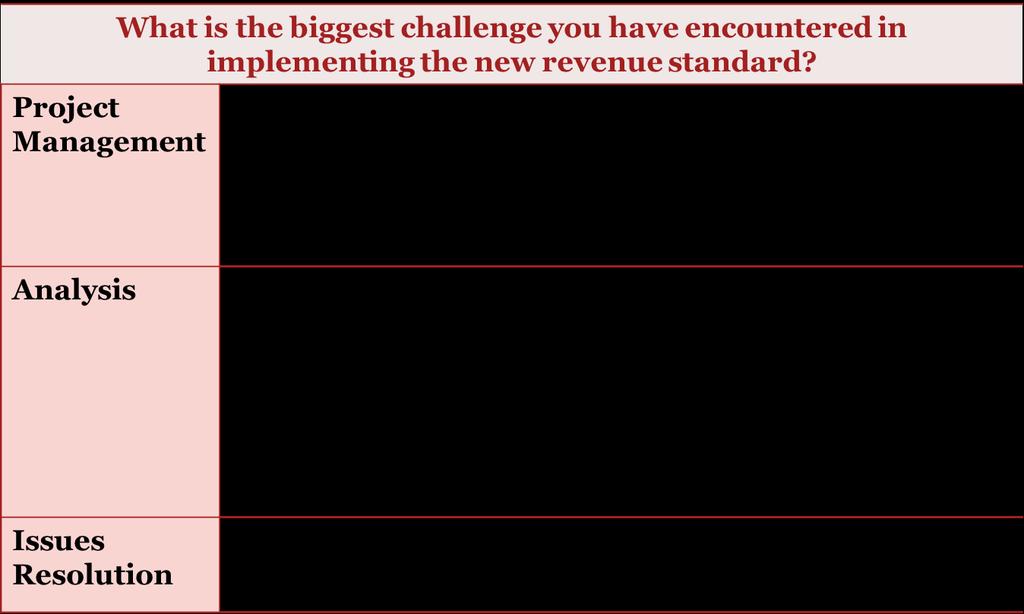

39 Implementation survey results 39

40 Implementation survey - results 40

41 Implementation survey - results 41

42 Implementation Top 5 recommendations 42

43 Save the Date Revenue Seminar Power & Utilities EEI/AGA Revenue Seminar When: November 9 th & November 10 th 2016 Where: Hilton Chicago O Hare Airport What: In depth case studies and more visibility to open issues 43

44 Q&A 44

45 Thank you Contact me to discuss further: Lucas Carpenter U.S. Power & Utilities Practice Senior Manager 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved. refers to the United States member firm, and may sometimes refer to the network. Each member firm is a separate legal entity. Please see for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors. United States helps organizations and individuals create the value they re looking for. We re a member of the network of firms in 157 countries with more than 195,000 people who are committed to delivering quality in assurance, tax and advisory services. Find out more and tell us what matters to you by visiting us at

Revenue Recognition issues Implementation status update

www.pwc.com/us/utilities Revenue Recognition issues Implementation status update EEI-AGA-PwC Revenue Recognition Workshop Sept. 26-27, 2017 Dallas, TX ASC 606 implementation in the U.S. () P&U Revenue

www.pwc.com/us/utilities Revenue Recognition issues Implementation status update EEI-AGA-PwC Revenue Recognition Workshop Sept. 26-27, 2017 Dallas, TX ASC 606 implementation in the U.S. () P&U Revenue

NARUC: REVENUE RECOGNITION JULIE PETIT AUDIT SENIOR MANAGER BRIAN JONES AUDIT SENIOR MANAGER MONDAY, SEPTEMBER 11 TH, 2017

NARUC: REVENUE RECOGNITION JULIE PETIT AUDIT SENIOR MANAGER BRIAN JONES AUDIT SENIOR MANAGER MONDAY, SEPTEMBER 11 TH, 2017 Mazars USA LLP is an independent member firm of Mazars Group. Mazars USA LLP is

NARUC: REVENUE RECOGNITION JULIE PETIT AUDIT SENIOR MANAGER BRIAN JONES AUDIT SENIOR MANAGER MONDAY, SEPTEMBER 11 TH, 2017 Mazars USA LLP is an independent member firm of Mazars Group. Mazars USA LLP is

Picture to be changed

Picture to be changed EVOLUTION DEMANDS SPEED AND FLEXIBILITY Dolphins are some of the most successful hunters in the animal kingdom. Their speed, intelligence and adaptability give them a crucial edge.

Picture to be changed EVOLUTION DEMANDS SPEED AND FLEXIBILITY Dolphins are some of the most successful hunters in the animal kingdom. Their speed, intelligence and adaptability give them a crucial edge.

2017 Deloitte Renewable Energy Seminar Innovating for tomorrow November 13-15, 2017

2017 Deloitte Renewable Energy Seminar Innovating for tomorrow November 13-15, 2017 Teresa Thomas, Partner, Deloitte & Touche LLP Jody Force, Managing Director, Deloitte & Touche LLP Accounting for ASC

2017 Deloitte Renewable Energy Seminar Innovating for tomorrow November 13-15, 2017 Teresa Thomas, Partner, Deloitte & Touche LLP Jody Force, Managing Director, Deloitte & Touche LLP Accounting for ASC

Power & Utilities Spotlight Generating a Discussion About the FASB s New Revenue Standard

August 2014 Power & Utilities Spotlight Generating a Discussion About the FASB s New Revenue Standard In This Issue: Background Key Accounting Issues Effective Date and Transition Implementation Challenges

August 2014 Power & Utilities Spotlight Generating a Discussion About the FASB s New Revenue Standard In This Issue: Background Key Accounting Issues Effective Date and Transition Implementation Challenges

Agenda. Overview of technical standard Amendments to date Impact on construction accounting Implementation action plan Industry initiatives Q&A

Agenda Overview of technical standard Amendments to date Impact on construction accounting Implementation action plan Industry initiatives Q&A Five Step Model Step 1 Step 2 Step 3 Step 4 Step 5 Identify

Agenda Overview of technical standard Amendments to date Impact on construction accounting Implementation action plan Industry initiatives Q&A Five Step Model Step 1 Step 2 Step 3 Step 4 Step 5 Identify

Revenue for power and utilities companies

Revenue for power and utilities companies New standard. New challenges. US GAAP March 2018 kpmg.com/us/frv b Revenue for power and utilities companies Revenue viewed through a new lens Again and again,

Revenue for power and utilities companies New standard. New challenges. US GAAP March 2018 kpmg.com/us/frv b Revenue for power and utilities companies Revenue viewed through a new lens Again and again,

Revenue from Contracts with Customers: The Final Standard

Revenue from Contracts with Customers: The Final Standard 1 TABLE OF CONTENTS Overview and effective date.... 3 Key provisions of the standard.... 3 Transition.... 12 Planning.... 13 How Experis Finance

Revenue from Contracts with Customers: The Final Standard 1 TABLE OF CONTENTS Overview and effective date.... 3 Key provisions of the standard.... 3 Transition.... 12 Planning.... 13 How Experis Finance

Revenue Recognition. Jaime Dordik. Assistant Project Manager, FASB March 26, 2017

Revenue Recognition Jaime Dordik Assistant Project Manager, FASB March 26, 2017 Agenda Overview of New Revenue Standard 5 Steps to Apply the Standard Disclosure Requirements Transition Example Transition

Revenue Recognition Jaime Dordik Assistant Project Manager, FASB March 26, 2017 Agenda Overview of New Revenue Standard 5 Steps to Apply the Standard Disclosure Requirements Transition Example Transition

Revenue from contracts with customers (ASC 606)

") Financial reporting developments A comprehensive guide Revenue from contracts with customers (ASC 606) Revised August 2017 To our clients and other friends The Financial Accounting Standards Board (FASB

Financial reporting developments A comprehensive guide Revenue from contracts with customers (ASC 606) Revised August 2017 To our clients and other friends The Financial Accounting Standards Board (FASB

Recognition Transition Resource Group 2015 Update

BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company BDO KNOWLEDGE limited by guarantee, Webinar Series and forms Revenue part of the Recognition

BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company BDO KNOWLEDGE limited by guarantee, Webinar Series and forms Revenue part of the Recognition

The New Revenue Standard State of the Industry and Prevailing Approaches for Adoption Where are we today and what s to come?

The New Revenue Standard Where are we today and what s to come? June 26, 2017 Speaking with you today Grant Casner Grant has been with Deloitte for over 14 years and advises companies on complex accounting

The New Revenue Standard Where are we today and what s to come? June 26, 2017 Speaking with you today Grant Casner Grant has been with Deloitte for over 14 years and advises companies on complex accounting

Revenue From Contracts With Customers

September 2017 Revenue From Contracts With Customers Understanding and Implementing the New Rules An article by Scott Lehman, CPA, and Alex J. Wodka, CPA Audit / Tax / Advisory / Risk / Performance Smart

September 2017 Revenue From Contracts With Customers Understanding and Implementing the New Rules An article by Scott Lehman, CPA, and Alex J. Wodka, CPA Audit / Tax / Advisory / Risk / Performance Smart

Revenue from contracts with customers (ASC 606)

") Financial reporting developments A comprehensive guide Revenue from contracts with customers (ASC 606) August 2015 To our clients and other friends In May 2014, the Financial Accounting Standards Board

Financial reporting developments A comprehensive guide Revenue from contracts with customers (ASC 606) August 2015 To our clients and other friends In May 2014, the Financial Accounting Standards Board

Government Contractors: Are You Prepared for the New Revenue Standard? Presented by CohnReznick s Government Contracting Industry Practice

Government Contractors: Are You Prepared for the New Revenue Standard? Presented by CohnReznick s Government Contracting Industry Practice PLEASE READ This presentation has been prepared for information

Government Contractors: Are You Prepared for the New Revenue Standard? Presented by CohnReznick s Government Contracting Industry Practice PLEASE READ This presentation has been prepared for information

Revenue from contracts with customers (ASC 606)

") Financial reporting developments A comprehensive guide Revenue from contracts with customers (ASC 606) Revised August 2016 To our clients and other friends In May 2014, the Financial Accounting Standards

Financial reporting developments A comprehensive guide Revenue from contracts with customers (ASC 606) Revised August 2016 To our clients and other friends In May 2014, the Financial Accounting Standards

Applying IFRS. IFRS 15 Revenue from Contracts with Customers. A closer look at the new revenue recognition standard (Updated October 2017)

") Applying IFRS IFRS 15 Revenue from Contracts with Customers A closer look at the new revenue recognition standard (Updated October 2017) Overview The International Accounting Standards Board (IASB) and

Applying IFRS IFRS 15 Revenue from Contracts with Customers A closer look at the new revenue recognition standard (Updated October 2017) Overview The International Accounting Standards Board (IASB) and

Revenue from Contracts with Customers

Grant Thornton August 2017 Revenue from Contracts with Customers Navigating the guidance in ASC 606 and ASC 340-40 This publication was created for general information purposes, and does not constitute

Grant Thornton August 2017 Revenue from Contracts with Customers Navigating the guidance in ASC 606 and ASC 340-40 This publication was created for general information purposes, and does not constitute

REVENUE RECOGNITION PROJECT UPDATED OCTOBER 2013 TOPICAL CONTENTS

REVENUE RECOGNITION PROJECT UPDATED OCTOBER 2013 TOPICAL CONTENTS STEP 1: IDENTIFY THE CONTRACT WITH A CUSTOMER... 3 Contracts with Customers that Contain Nonrecourse, Seller-Based Financing... 3 Contract

REVENUE RECOGNITION PROJECT UPDATED OCTOBER 2013 TOPICAL CONTENTS STEP 1: IDENTIFY THE CONTRACT WITH A CUSTOMER... 3 Contracts with Customers that Contain Nonrecourse, Seller-Based Financing... 3 Contract

Revenue Recognition: Manufacturers & Distributors Supplement

Revenue Recognition: Manufacturers & Distributors Supplement Table of Contents BACKGROUND & SUMMARY... 3 SCOPE... 5 THE REVENUE RECOGNITION MODEL... 5 STEP 1 IDENTIFY THE CONTRACT WITH A CUSTOMER... 5

Revenue Recognition: Manufacturers & Distributors Supplement Table of Contents BACKGROUND & SUMMARY... 3 SCOPE... 5 THE REVENUE RECOGNITION MODEL... 5 STEP 1 IDENTIFY THE CONTRACT WITH A CUSTOMER... 5

FINANCIAL INSTITUTIONS REMINDER CHECKLIST. REV REC 606 Implementation

FINANCIAL INSTITUTIONS REMINDER CHECKLIST REV REC 606 Implementation 2 FINANCIAL INSTITUTIONS REMINDER CHECKLIST Reminder Checklist This document is intended to be used as a reminder of ASC 606 requirements

FINANCIAL INSTITUTIONS REMINDER CHECKLIST REV REC 606 Implementation 2 FINANCIAL INSTITUTIONS REMINDER CHECKLIST Reminder Checklist This document is intended to be used as a reminder of ASC 606 requirements

Revenue Recognition: A Comprehensive Look at the New Standard

Revenue Recognition: A Comprehensive Look at the New Standard BACKGROUND & SUMMARY... 3 SCOPE... 4 COLLABORATIVE ARRANGEMENTS... 4 THE REVENUE RECOGNITION MODEL... 5 STEP 1 IDENTIFY THE CONTRACT WITH A

Revenue Recognition: A Comprehensive Look at the New Standard BACKGROUND & SUMMARY... 3 SCOPE... 4 COLLABORATIVE ARRANGEMENTS... 4 THE REVENUE RECOGNITION MODEL... 5 STEP 1 IDENTIFY THE CONTRACT WITH A

Straight Away Special Edition

Straight away Special edition In transition The latest on revenue recognition implementation 23 July 2015 Transition Resource Group debates revenue recognition implementation issues TRG discusses variable

Straight away Special edition In transition The latest on revenue recognition implementation 23 July 2015 Transition Resource Group debates revenue recognition implementation issues TRG discusses variable

The new revenue recognition standard technology

No. 2014-16 26 August 2014 Technical Line FASB final guidance The new revenue recognition standard technology In this issue: Overview... 1 Scope, transition and effective date... 3 Summary of the new model...

No. 2014-16 26 August 2014 Technical Line FASB final guidance The new revenue recognition standard technology In this issue: Overview... 1 Scope, transition and effective date... 3 Summary of the new model...

Annual Nonprofit Accounting and Auditing Update

Annual Nonprofit Accounting and Auditing Update July 21, 2016 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee,

Annual Nonprofit Accounting and Auditing Update July 21, 2016 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee,

Revenue Recognition Media Finance Focus 2016 Denver, Colorado

Revenue Recognition Media Finance Focus 2016 Denver, Colorado 1 Panelists Dwight Delapenha, Deladad Advisory Dan Drobac, PwC Sue Tuxill, Salem Media Group Mike Ruggiero, ATV Broadcast 2 Revenue Recognition

Revenue Recognition Media Finance Focus 2016 Denver, Colorado 1 Panelists Dwight Delapenha, Deladad Advisory Dan Drobac, PwC Sue Tuxill, Salem Media Group Mike Ruggiero, ATV Broadcast 2 Revenue Recognition

Applying IFRS. Joint Transition Resource Group discusses additional revenue implementation issues. July 2015

Applying IFRS Joint Transition Resource Group discusses additional revenue implementation issues July 2015 Contents Overview 2 1. Issues that may require further discussion 2 1.1 Application of the constraint

Applying IFRS Joint Transition Resource Group discusses additional revenue implementation issues July 2015 Contents Overview 2 1. Issues that may require further discussion 2 1.1 Application of the constraint

REVENUE RECOGNITION FOR BROKER-DEALERS AND INVESTMENT ADVISERS

REVENUE RECOGNITION FOR BROKER-DEALERS AND INVESTMENT ADVISERS December 7, 2017 RSM US LLP. All Rights Reserved. Your instructors Tracy Whetstone Partner, National Professional Standards Group Chicago,

REVENUE RECOGNITION FOR BROKER-DEALERS AND INVESTMENT ADVISERS December 7, 2017 RSM US LLP. All Rights Reserved. Your instructors Tracy Whetstone Partner, National Professional Standards Group Chicago,

Applying IFRS IFRS 15 Revenue from Contracts with Customers. A closer look at the new revenue recognition standard

Applying IFRS IFRS 15 Revenue from Contracts with Customers A closer look at the new revenue recognition standard Updated September 2016 Overview In May 2014, the International Accounting Standards Board

Applying IFRS IFRS 15 Revenue from Contracts with Customers A closer look at the new revenue recognition standard Updated September 2016 Overview In May 2014, the International Accounting Standards Board

Revenue Recognition: Construction Industry Supplement

Revenue Recognition: Construction Industry Supplement Table of Contents BACKGROUND & SUMMARY... 4 SCOPE... 5 THE REVENUE RECOGNITION MODEL... 5 STEP 1 IDENTIFY THE CONTRACT WITH A CUSTOMER... 6 Collectibility...

Revenue Recognition: Construction Industry Supplement Table of Contents BACKGROUND & SUMMARY... 4 SCOPE... 5 THE REVENUE RECOGNITION MODEL... 5 STEP 1 IDENTIFY THE CONTRACT WITH A CUSTOMER... 6 Collectibility...

Transition Resource Group for Revenue Recognition items of general agreement

Transition Resource Group for Revenue Recognition items of general agreement This table summarizes the issues on which members of the Joint Transition Resource Group for Revenue Recognition (TRG) created

Transition Resource Group for Revenue Recognition items of general agreement This table summarizes the issues on which members of the Joint Transition Resource Group for Revenue Recognition (TRG) created

FASB ASU NO REVENUE FROM CONTRACTS WITH CUSTOMERS (TOPIC 606)

") CPAs & ADVISORS experience clarity // REVENUE RECOGNITION FOR HEALTH CARE PROVIDERS Kimberly McKay, CPA Managing Partner BKD. LLP - Houston FASB ASU NO. 2014-09 REVENUE FROM CONTRACTS WITH CUSTOMERS (TOPIC

CPAs & ADVISORS experience clarity // REVENUE RECOGNITION FOR HEALTH CARE PROVIDERS Kimberly McKay, CPA Managing Partner BKD. LLP - Houston FASB ASU NO. 2014-09 REVENUE FROM CONTRACTS WITH CUSTOMERS (TOPIC

New revenue guidance Implementation in Industrial Products

No. US2017-16 August 17, 2017 What s inside: Overview... 1 Step 1: Identify the contract with the customer... 2 Step 2: Identify performance obligations... 4 Step 3: Determine... 5 Step 4: Allocate...8

No. US2017-16 August 17, 2017 What s inside: Overview... 1 Step 1: Identify the contract with the customer... 2 Step 2: Identify performance obligations... 4 Step 3: Determine... 5 Step 4: Allocate...8

Financial Reporting Brief: Roadmap to Understanding the New Revenue Recognition Standards

September 2016 Financial Reporting Center Financial Reporting Brief: Roadmap to Understanding the New Revenue Recognition Standards In May 2014, FASB issued Accounting Standards Update (ASU) 2014-09, Revenue

September 2016 Financial Reporting Center Financial Reporting Brief: Roadmap to Understanding the New Revenue Recognition Standards In May 2014, FASB issued Accounting Standards Update (ASU) 2014-09, Revenue

The New Era of Revenue Recognition. Chris Harper, CPA, MBA, Senior Manager

The New Era of Revenue Recognition Chris Harper, CPA, MBA, Senior Manager Measuring Temperature What is your level of familiarity with revenue recognition standards that were issued in 2014? I practically

The New Era of Revenue Recognition Chris Harper, CPA, MBA, Senior Manager Measuring Temperature What is your level of familiarity with revenue recognition standards that were issued in 2014? I practically

Aerospace & Defense Spotlight The Converged Revenue Recognition Model Has Landed

September 2014 Aerospace & Defense Spotlight The Converged Revenue Recognition Model Has Landed In This Issue: Background Key Accounting Issues Effective Date and Transition Challenges for A&D Entities

September 2014 Aerospace & Defense Spotlight The Converged Revenue Recognition Model Has Landed In This Issue: Background Key Accounting Issues Effective Date and Transition Challenges for A&D Entities

EEI & AGA Executive Accounting News Flash

EEI & AGA Executive Accounting News Flash Issue XIX Q3 2016 Dear Colleagues: Welcome to the 2016 third quarter edition of the Executive Accounting News Flash. In this quarter s edition we recap the latest

EEI & AGA Executive Accounting News Flash Issue XIX Q3 2016 Dear Colleagues: Welcome to the 2016 third quarter edition of the Executive Accounting News Flash. In this quarter s edition we recap the latest

Effects of the New Revenue Standard: Observations From a Review of First- Quarter 2018 Public Filings by Power and Utilities Companies

Power & Utilities Spotlight July 2018 In This Issue Background Review of Public Disclosure Filings Contacts Effects of the New Revenue Standard: Observations From a Review of First- Quarter 2018 Public

Power & Utilities Spotlight July 2018 In This Issue Background Review of Public Disclosure Filings Contacts Effects of the New Revenue Standard: Observations From a Review of First- Quarter 2018 Public

Revenue for Telecoms. Issues In-Depth. September IFRS and US GAAP. kpmg.com

Revenue for Telecoms Issues In-Depth September 2016 IFRS and US GAAP kpmg.com Contents Facing the challenges 1 Introduction 2 Putting the new standard into context 6 1 Scope 9 1.1 In scope 9 1.2 Out of

Revenue for Telecoms Issues In-Depth September 2016 IFRS and US GAAP kpmg.com Contents Facing the challenges 1 Introduction 2 Putting the new standard into context 6 1 Scope 9 1.1 In scope 9 1.2 Out of

New Revenue Recognition Framework: Will Your Entity Be Affected?

New Revenue Recognition Framework: Will Your Entity Be Affected? One of the most significant changes to financial accounting and reporting in recent history is soon to be effective. Reporting entities

New Revenue Recognition Framework: Will Your Entity Be Affected? One of the most significant changes to financial accounting and reporting in recent history is soon to be effective. Reporting entities

HFMA Great Lakes Chapter Accounting and Auditing Update February 16, 2018

HFMA Great Lakes Chapter Accounting and Auditing Update February 16, 2018 Who We Are CAROLYN BIELAWSKI, CPA ASSOCIATE Education: Bachelor of Arts in Accounting, Master of Science in Accounting, Michigan

HFMA Great Lakes Chapter Accounting and Auditing Update February 16, 2018 Who We Are CAROLYN BIELAWSKI, CPA ASSOCIATE Education: Bachelor of Arts in Accounting, Master of Science in Accounting, Michigan

ED revenue recognition from contracts with customers

ED revenue recognition from contracts with customers An overview of the revised proposals 2 October 2012 Disclaimer This presentation contains information in summary form and is therefore not intended

ED revenue recognition from contracts with customers An overview of the revised proposals 2 October 2012 Disclaimer This presentation contains information in summary form and is therefore not intended

Transition Resource Group for Revenue Recognition Items of general agreement

Applying IFRS Transition Resource Group for Revenue Recognition Items of general agreement Updated March 2019 Contents Overview... 3 1. Step 1: Identify the contract(s) with a customer... 4 1.1 Collectability...

Applying IFRS Transition Resource Group for Revenue Recognition Items of general agreement Updated March 2019 Contents Overview... 3 1. Step 1: Identify the contract(s) with a customer... 4 1.1 Collectability...

Applying the new revenue recognition standard

Applying the new revenue recognition standard On May 28, 24, the FASB and IASB issued their final standard on recognizing revenue from customer contracts. The standard, issued as ASU 24-09 by the FASB

Applying the new revenue recognition standard On May 28, 24, the FASB and IASB issued their final standard on recognizing revenue from customer contracts. The standard, issued as ASU 24-09 by the FASB

Media & Entertainment Spotlight Navigating the New Revenue Standard

July 2014 Media & Entertainment Spotlight Navigating the New Revenue Standard In This Issue: Background Key Accounting Issues Effective Date and Transition Transition Considerations Thinking Ahead The

July 2014 Media & Entertainment Spotlight Navigating the New Revenue Standard In This Issue: Background Key Accounting Issues Effective Date and Transition Transition Considerations Thinking Ahead The

ASC 606 REVENUE RECOGNITION. Everything you need to know now

ASC 606 REVENUE RECOGNITION Everything you need to know now TOPICS 03 04 07 14 21 31 39 48 54 57 61 66 67 Introduction A revenue recognition primer Identifying the contract Identifying performance obligations

ASC 606 REVENUE RECOGNITION Everything you need to know now TOPICS 03 04 07 14 21 31 39 48 54 57 61 66 67 Introduction A revenue recognition primer Identifying the contract Identifying performance obligations

Power & Utility Revenue Recognition Task Force Issue status update August 2017

Power & Utility Revenue Recognition Task Force Issue status update August 2017 Implementation update Tariff-based sales Scope clarification Carve-out of alternative revenue programs led some to question

Power & Utility Revenue Recognition Task Force Issue status update August 2017 Implementation update Tariff-based sales Scope clarification Carve-out of alternative revenue programs led some to question

Life Sciences Accounting and Financial Reporting Update Interpretive Guidance on Revenue Recognition Under ASC 606

Life Sciences Accounting and Financial Reporting Update Interpretive Guidance on Revenue Recognition Under ASC 606 March 2017 Revenue Recognition Background In May 2014, the FASB 1 and IASB issued their

Life Sciences Accounting and Financial Reporting Update Interpretive Guidance on Revenue Recognition Under ASC 606 March 2017 Revenue Recognition Background In May 2014, the FASB 1 and IASB issued their

The new revenue recognition standard retail and consumer products

Applying IFRS in Retail and Consumer Products The new revenue recognition standard retail and consumer products May 2015 Contents Overview... 3 1. Summary of the new standard... 4 2. Scope, transition

Applying IFRS in Retail and Consumer Products The new revenue recognition standard retail and consumer products May 2015 Contents Overview... 3 1. Summary of the new standard... 4 2. Scope, transition

CPAs & ADVISORS. experience clarity // REVENUE RECOGNITION. FASB/IASB Joint Project

CPAs & ADVISORS experience clarity // REVENUE RECOGNITION FASB/IASB Joint Project May 28, 2014 - ASU 2014-09, Revenue from Contracts with Customers, is released Single, converged, comprehensive approach

CPAs & ADVISORS experience clarity // REVENUE RECOGNITION FASB/IASB Joint Project May 28, 2014 - ASU 2014-09, Revenue from Contracts with Customers, is released Single, converged, comprehensive approach

FASB/IASB Joint Transition Resource Group for Revenue Recognition July 2015 Meeting Summary of Issues Discussed and Next Steps

TRG Agenda ref 44 STAFF PAPER Project Paper topic November 9, 2015 FASB/IASB Joint Transition Resource Group for Revenue Recognition July 2015 Meeting Summary of Issues Discussed and Next Steps CONTACT(S)

TRG Agenda ref 44 STAFF PAPER Project Paper topic November 9, 2015 FASB/IASB Joint Transition Resource Group for Revenue Recognition July 2015 Meeting Summary of Issues Discussed and Next Steps CONTACT(S)

How the new revenue standard will affect media and entertainment entities. February 2017

How the new revenue standard will affect media and entertainment entities February 2017 Agenda Overview Licenses of intellectual property (IP) Other considerations Page 2 Overview New revenue recognition

How the new revenue standard will affect media and entertainment entities February 2017 Agenda Overview Licenses of intellectual property (IP) Other considerations Page 2 Overview New revenue recognition

The new revenue recognition standard - software and cloud services

Applying IFRS in Software and Cloud Services The new revenue recognition standard - software and cloud services January 2015 Overview Software entities may need to change their revenue recognition policies

Applying IFRS in Software and Cloud Services The new revenue recognition standard - software and cloud services January 2015 Overview Software entities may need to change their revenue recognition policies

Defining Issues. Revenue from Contracts with Customers. June 2014, No

Defining Issues June 2014, No. 14-25 Revenue from Contracts with Customers On May 28, 2014, the FASB and the IASB issued a new accounting standard that is intended to improve and converge the financial

Defining Issues June 2014, No. 14-25 Revenue from Contracts with Customers On May 28, 2014, the FASB and the IASB issued a new accounting standard that is intended to improve and converge the financial

by Joe DiLeo and Ermir Berberi, Deloitte & Touche LLP

Heads Up May 11, 2016 Volume 23, Issue 14 In This Issue Collectibility Presentation of Sales Taxes and Similar Taxes Collected From Customers Noncash Consideration Contract Modifications and Completed

Heads Up May 11, 2016 Volume 23, Issue 14 In This Issue Collectibility Presentation of Sales Taxes and Similar Taxes Collected From Customers Noncash Consideration Contract Modifications and Completed

Revenue Recognition: A Comprehensive Look at the New Standard for the Construction & Real Estate Industries

Revenue Recognition: A Comprehensive Look at the New Standard for the Construction & Real Estate Industries Table of Contents BACKGROUND & SUMMARY... 3 SCOPE... 4 THE REVENUE RECOGNITION MODEL... 5 STEP

Revenue Recognition: A Comprehensive Look at the New Standard for the Construction & Real Estate Industries Table of Contents BACKGROUND & SUMMARY... 3 SCOPE... 4 THE REVENUE RECOGNITION MODEL... 5 STEP

Defining Issues. FASB Redeliberates Revenue Guidance on Licensing and Performance Obligations. October 2015, No

Defining Issues October 2015, No. 15-46 FASB Redeliberates Revenue Guidance on Licensing and Performance Obligations On October 5, 2015, the FASB redeliberated and, in general, tentatively decided to adopt

Defining Issues October 2015, No. 15-46 FASB Redeliberates Revenue Guidance on Licensing and Performance Obligations On October 5, 2015, the FASB redeliberated and, in general, tentatively decided to adopt

Observations From a Review of Public Filings by Early Adopters of the New Revenue Standard

Heads Up Volume 25, Issue 1 January 22, 2018 In This Issue Introduction Interim Versus Annual Reporting Considerations Description of Population Disaggregation of Revenue Contract Balances Performance

Heads Up Volume 25, Issue 1 January 22, 2018 In This Issue Introduction Interim Versus Annual Reporting Considerations Description of Population Disaggregation of Revenue Contract Balances Performance

Implementing Revenue Recognition for Health Care Organizations S E P T E M B E R 2 1,

Implementing Revenue Recognition for Health Care Organizations S E P T E M B E R 2 1, 2 0 1 8 INTRODUCTIONS Kimberly McKay, CPA Managing Partner kmckay@bkd.com Implementing Revenue Recognition for Health

Implementing Revenue Recognition for Health Care Organizations S E P T E M B E R 2 1, 2 0 1 8 INTRODUCTIONS Kimberly McKay, CPA Managing Partner kmckay@bkd.com Implementing Revenue Recognition for Health

AUDIT AND ACCOUNTING UPDATE

AUDIT AND ACCOUNTING UPDATE HFMA FL Regional Education Session - Clearwater November 11, 2016 Presenter Carlos Hernandez Southeast Assurance Leader Carlos.hernandez@rsmus.com 2 Agenda Topic Recent accounting

AUDIT AND ACCOUNTING UPDATE HFMA FL Regional Education Session - Clearwater November 11, 2016 Presenter Carlos Hernandez Southeast Assurance Leader Carlos.hernandez@rsmus.com 2 Agenda Topic Recent accounting

FINANCIAL INSTITUTION AND SPECIALTY FINANCE OVERVIEW OF 2014 REVENUE STANDARD

FINANCIAL INSTITUTION AND SPECIALTY FINANCE OVERVIEW OF 2014 REVENUE STANDARD BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited

FINANCIAL INSTITUTION AND SPECIALTY FINANCE OVERVIEW OF 2014 REVENUE STANDARD BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited

Changes to revenue recognition in the health care industry

Changes to revenue recognition in the health care industry Prepared by: Dan Vandenberghe, Partner, RSM US LLP dan.vandenberghe@rsmus.com, +1 612 376 9267 Jay Adkisson, Partner, RSM US LLP jay.adkisson@rsmus.com,

Changes to revenue recognition in the health care industry Prepared by: Dan Vandenberghe, Partner, RSM US LLP dan.vandenberghe@rsmus.com, +1 612 376 9267 Jay Adkisson, Partner, RSM US LLP jay.adkisson@rsmus.com,

Technical Line FASB final guidance

No. 2017-16 29 June 2017 Technical Line FASB final guidance How the new revenue recognition standard affects downstream oil and gas entities In this issue: Overview... 1 Scope and scope exceptions... 2

No. 2017-16 29 June 2017 Technical Line FASB final guidance How the new revenue recognition standard affects downstream oil and gas entities In this issue: Overview... 1 Scope and scope exceptions... 2

Implementing Revenue Recognition for Health Care Organizations J A N U A R Y

Implementing Revenue Recognition for Health Care Organizations J A N U A R Y 2 0 1 9 AGENDA 1 Introductions & Objectives 2 Background, Key Principles, & Transition 3 Common Industry Implementation Challenges

Implementing Revenue Recognition for Health Care Organizations J A N U A R Y 2 0 1 9 AGENDA 1 Introductions & Objectives 2 Background, Key Principles, & Transition 3 Common Industry Implementation Challenges

The new revenue recognition standard mining & metals

Applying IFRS in Mining and Metals The new revenue recognition standard mining & metals June 2015 Contents Overview... 2 1. Summary of the new standard... 3 2. Effective date and transition... 3 3. Scope...

Applying IFRS in Mining and Metals The new revenue recognition standard mining & metals June 2015 Contents Overview... 2 1. Summary of the new standard... 3 2. Effective date and transition... 3 3. Scope...

IASA Conference US GAAP Technical Update. Deloitte & Touche LLP September 14, 2016

IASA Conference 2016 US GAAP Technical Update Deloitte & Touche LLP September 14, 2016 Insurance project update Copyright 2016 Deloitte Development LLC. All rights reserved. 2 Insurance contracts Overview

IASA Conference 2016 US GAAP Technical Update Deloitte & Touche LLP September 14, 2016 Insurance project update Copyright 2016 Deloitte Development LLC. All rights reserved. 2 Insurance contracts Overview

Applying IFRS. Joint Transition Resource Group for Revenue Recognition - items of general agreement. Updated June 2016

Applying IFRS Joint Transition Resource Group for Revenue Recognition - items of general agreement Updated June 2016 Contents Overview...3 1. Step 1: Identify the contract(s) with a customer... 4 1.1 Collectability...

Applying IFRS Joint Transition Resource Group for Revenue Recognition - items of general agreement Updated June 2016 Contents Overview...3 1. Step 1: Identify the contract(s) with a customer... 4 1.1 Collectability...

Revenue Changes for Insurance Brokers

Insurance brokers will see a change in revenue recognition after adopting Accounting Standards Update (ASU) 2014-09, Revenue from Contracts with Customers (Topic 606), which is now effective for public

Insurance brokers will see a change in revenue recognition after adopting Accounting Standards Update (ASU) 2014-09, Revenue from Contracts with Customers (Topic 606), which is now effective for public

Revenue Changes for Franchisors. Revenue Changes for Franchisors

Revenue Changes for Franchisors Table of Contents INTRODUCTION... 4 PORTFOLIO APPROACH... 5 STEP 1: IDENTIFY THE CONTRACT WITH A CUSTOMER... 6 COMBINING CONTRACTS... 7 STEP 2: IDENTIFY PERFORMANCE OBLIGATIONS

Revenue Changes for Franchisors Table of Contents INTRODUCTION... 4 PORTFOLIO APPROACH... 5 STEP 1: IDENTIFY THE CONTRACT WITH A CUSTOMER... 6 COMBINING CONTRACTS... 7 STEP 2: IDENTIFY PERFORMANCE OBLIGATIONS

Ihre Ansprechpartner

Ihre Ansprechpartner Sehr geehrte Damen und Herren, für Rückfragen zur beigefügten Ergänzung Power and Utilities industry supplement zu unserer Publikation In depth zur Thematik Revenue from contracts

Ihre Ansprechpartner Sehr geehrte Damen und Herren, für Rückfragen zur beigefügten Ergänzung Power and Utilities industry supplement zu unserer Publikation In depth zur Thematik Revenue from contracts

Technical Line FASB final guidance

No. 2017-22 Updated 4 December 2017 Technical Line FASB final guidance How the new revenue standard affects life sciences entities In this issue: Overview... 1 Collaborative arrangements... 2 Effect of

No. 2017-22 Updated 4 December 2017 Technical Line FASB final guidance How the new revenue standard affects life sciences entities In this issue: Overview... 1 Collaborative arrangements... 2 Effect of

COMPLEXITIES FOR LONG-TERM CARE

The New World of Revenue Recognition, ASC 606 COMPLEXITIES FOR LONG-TERM CARE June 27, 2018 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK

The New World of Revenue Recognition, ASC 606 COMPLEXITIES FOR LONG-TERM CARE June 27, 2018 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK

FINANCIAL REPORTING GUIDE TO IFRS 15. Revenue from contracts with customers

FINANCIAL REPORTING GUIDE TO IFRS 15 Revenue from contracts with customers CONTENTS Section 1 Applying the changes in IFRS 15 6 Step 1: Identify the contract(s) with a customer 6 Step 2: Identify the performance

FINANCIAL REPORTING GUIDE TO IFRS 15 Revenue from contracts with customers CONTENTS Section 1 Applying the changes in IFRS 15 6 Step 1: Identify the contract(s) with a customer 6 Step 2: Identify the performance

Technical Line FASB final guidance

No. 2017-20 29 June 2017 Technical Line FASB final guidance How the new revenue standard affects asset managers In this issue: Overview... 1 Background... 2 Identifying the contract with a customer...

No. 2017-20 29 June 2017 Technical Line FASB final guidance How the new revenue standard affects asset managers In this issue: Overview... 1 Background... 2 Identifying the contract with a customer...

Accounting Guidance of Special Importance to Electric Cooperatives. Russ Wasson Senior Director of Tax, Finance and Accounting Policy NRECA

Accounting Guidance of Special Importance to Electric Cooperatives Russ Wasson Senior Director of Tax, Finance and Accounting Policy NRECA Agenda Leases (ASC 842) Revenue from Contracts With Customers

Accounting Guidance of Special Importance to Electric Cooperatives Russ Wasson Senior Director of Tax, Finance and Accounting Policy NRECA Agenda Leases (ASC 842) Revenue from Contracts With Customers

Revenue Recognition: A Comprehensive Review for Health Care Entities

Revenue Recognition: A Comprehensive Review for Health Care Entities Table of Contents INTRODUCTION... 4 THE MODEL... 5 SCOPE... 5 CONTRIBUTIONS/GRANTS... 5 COLLABORATIVE ARRANGEMENTS... 6 CHARITY CARE...

Revenue Recognition: A Comprehensive Review for Health Care Entities Table of Contents INTRODUCTION... 4 THE MODEL... 5 SCOPE... 5 CONTRIBUTIONS/GRANTS... 5 COLLABORATIVE ARRANGEMENTS... 6 CHARITY CARE...

Revenue Recognition: A Comprehensive Update on the Joint Project

The Dbriefs Financial Reporting series presents: Revenue Recognition: A Comprehensive Update on the Joint Project Bob Uhl, Deloitte & Touche LLP Mark Crowley, Deloitte & Touche LLP Bryan Anderson, Deloitte

The Dbriefs Financial Reporting series presents: Revenue Recognition: A Comprehensive Update on the Joint Project Bob Uhl, Deloitte & Touche LLP Mark Crowley, Deloitte & Touche LLP Bryan Anderson, Deloitte

2016 Revenue Recognition Session Parts 1 & 2

2016 AICPA Healthcare Conference 2016 Revenue Recognition Session Parts 1 & 2 Speaker Biographies 25-1 Mike Breen, CPA Mike is an audit partner in KPMG s New York Office. He has experience performing financial

2016 AICPA Healthcare Conference 2016 Revenue Recognition Session Parts 1 & 2 Speaker Biographies 25-1 Mike Breen, CPA Mike is an audit partner in KPMG s New York Office. He has experience performing financial

Implementing Revenue Recognition for Health Care Organizations

Implementing Revenue Recognition for Health Care Organizations AUGUST 6, 2018 TO RECEIVE CPE CREDIT Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader is

Implementing Revenue Recognition for Health Care Organizations AUGUST 6, 2018 TO RECEIVE CPE CREDIT Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader is

NEW REVENUE RECOGNITION GUIDANCE WHAT NONPROFITS NEED TO KNOW!

NEW REVENUE RECOGNITION GUIDANCE WHAT NONPROFITS NEED TO KNOW! March 8, 2018 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited

NEW REVENUE RECOGNITION GUIDANCE WHAT NONPROFITS NEED TO KNOW! March 8, 2018 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited

FASB/IASB Update Part I

American Accounting Association FASB/IASB Update Part I Tom Linsmeier FASB Member August 3, 2014 The views expressed in this presentation are those of the presenter. Official positions of the FASB are

American Accounting Association FASB/IASB Update Part I Tom Linsmeier FASB Member August 3, 2014 The views expressed in this presentation are those of the presenter. Official positions of the FASB are

Technical Line FASB final guidance

No. 2016-26 27 July 2017 Technical Line FASB final guidance How the new revenue recognition standard affects automotive OEMs In this issue: Overview... 1 Vehicle sales... 2 Sales incentives... 2 Free goods

No. 2016-26 27 July 2017 Technical Line FASB final guidance How the new revenue recognition standard affects automotive OEMs In this issue: Overview... 1 Vehicle sales... 2 Sales incentives... 2 Free goods

REVENUE RECOGNITION ASU /8/2016. CPAs & ADVISORS ACCOUNTING AND AUDITING UPDATE FOR ARKANSAS HFMA

CPAs & ADVISORS experience clarity // ACCOUNTING AND AUDITING UPDATE FOR ARKANSAS HFMA Tracy Young, CPA Partner, BKD Health Care Group Little Rock REVENUE RECOGNITION ASU 2014-09 1 FASB/IASB ORIGINAL REVENUE

CPAs & ADVISORS experience clarity // ACCOUNTING AND AUDITING UPDATE FOR ARKANSAS HFMA Tracy Young, CPA Partner, BKD Health Care Group Little Rock REVENUE RECOGNITION ASU 2014-09 1 FASB/IASB ORIGINAL REVENUE

IFRS IN PRACTICE IFRS 15 Revenue from Contracts with Customers

IFRS IN PRACTICE 2018 IFRS 15 Revenue from Contracts with Customers 2 IFRS IN PRACTICE 2018 IFRS 15 REVENUE FROM CONTRACTS WITH CUSTOMERS IFRS IN PRACTICE 2018 IFRS 15 REVENUE FROM CONTRACTS WITH CUSTOMERS

IFRS IN PRACTICE 2018 IFRS 15 Revenue from Contracts with Customers 2 IFRS IN PRACTICE 2018 IFRS 15 REVENUE FROM CONTRACTS WITH CUSTOMERS IFRS IN PRACTICE 2018 IFRS 15 REVENUE FROM CONTRACTS WITH CUSTOMERS

Revenue Recognition Principles

Revenue Recognition Principles 4 CPE Hours d PDH Academy PO Box 449 Pewaukee, WI 53072 www.pdhacademy.com pdhacademy@gmail.com 888-564-9098 CONTINUING EDUCATION for Certified Public Accountants REVENUE

Revenue Recognition Principles 4 CPE Hours d PDH Academy PO Box 449 Pewaukee, WI 53072 www.pdhacademy.com pdhacademy@gmail.com 888-564-9098 CONTINUING EDUCATION for Certified Public Accountants REVENUE

Implementing the new revenue guidance in the technology industry

Grant Thornton January 2019 Implementing the new revenue guidance in the technology industry A supplement This publication was created for general information purposes, and does not constitute professional

Grant Thornton January 2019 Implementing the new revenue guidance in the technology industry A supplement This publication was created for general information purposes, and does not constitute professional

New Developments Summary

June 5, 2014 NDS 2014-06 New Developments Summary A shift in the top line The new global revenue standard is here! Summary After dedicating many years to its development, the FASB and the IASB have issued

June 5, 2014 NDS 2014-06 New Developments Summary A shift in the top line The new global revenue standard is here! Summary After dedicating many years to its development, the FASB and the IASB have issued

Revenue recognition: A whole new world

Revenue recognition: A whole new world Prepared by: Brian H. Marshall, Partner, National Professional Standards Group, RSM US LLP brian.marshall@rsmus.com, +1 203 312 9329 June 2014 UPDATE: To help address

Revenue recognition: A whole new world Prepared by: Brian H. Marshall, Partner, National Professional Standards Group, RSM US LLP brian.marshall@rsmus.com, +1 203 312 9329 June 2014 UPDATE: To help address

Up to Speed: Accounting update for Healthcare Providers. David Woodall Assurance Partner - Birmingham, AL

www.pwc.com Up to Speed: Accounting update for Healthcare Providers David Woodall Assurance Partner - Birmingham, AL Sean O Hara Assurance Senior Manager Nashville, TN Agenda FASB update The new revenue

www.pwc.com Up to Speed: Accounting update for Healthcare Providers David Woodall Assurance Partner - Birmingham, AL Sean O Hara Assurance Senior Manager Nashville, TN Agenda FASB update The new revenue

IFRS 15 Revenue from Contracts with Customers Guide

February 2017 Introduction... 5 Key Differences Between IFRS 15 and IAS 18/IAS 11... 6 Key Differences Between IFRS 15 and ASC 606... 7 Purpose and Scope... 9 Overview of the Five-Step Model... 10 Step

February 2017 Introduction... 5 Key Differences Between IFRS 15 and IAS 18/IAS 11... 6 Key Differences Between IFRS 15 and ASC 606... 7 Purpose and Scope... 9 Overview of the Five-Step Model... 10 Step

Applying IFRS. Joint Transition Group for Revenue Recognition items of general agreement. Updated December 2015

Applying IFRS Joint Transition Group for Revenue Recognition items of general agreement Updated December 2015 Contents Overview... 3 1. Step 1: Identify the contract(s) with a customer... 4 1.1 Collectability...

Applying IFRS Joint Transition Group for Revenue Recognition items of general agreement Updated December 2015 Contents Overview... 3 1. Step 1: Identify the contract(s) with a customer... 4 1.1 Collectability...

Technical Line FASB final guidance

No. 2017-14 22 June 2017 Technical Line FASB final guidance How the new revenue standard affects telecommunications entities In this issue: Overview... 1 Contract term... 2 Identifying performance obligations

No. 2017-14 22 June 2017 Technical Line FASB final guidance How the new revenue standard affects telecommunications entities In this issue: Overview... 1 Contract term... 2 Identifying performance obligations

FASB/IASB Joint Transition Resource Group for Revenue Recognition Application of the Series Provision and Allocation of Variable Consideration

TRG Agenda ref 39 STAFF PAPER Project Paper topic July 13, 2015 FASB/IASB Joint Transition Resource Group for Revenue Recognition Application of the Series Provision and Allocation of Variable Consideration

TRG Agenda ref 39 STAFF PAPER Project Paper topic July 13, 2015 FASB/IASB Joint Transition Resource Group for Revenue Recognition Application of the Series Provision and Allocation of Variable Consideration

Revenue from contracts with customers. Health care services industry supplement

Note: Since issuing the new revenue standard in May 2014, the FASB and IASB have proposed various amendments to the guidance. This In depth supplement has not been updated to reflect all of the proposed

Note: Since issuing the new revenue standard in May 2014, the FASB and IASB have proposed various amendments to the guidance. This In depth supplement has not been updated to reflect all of the proposed

Implementing the New Revenue Recognition Standard for Technology Companies

October 2017 Implementing the New Revenue Recognition Standard for Technology Companies An article by Glenn E. Richards, CPA; Scott G. Sachs, CPA; and Kevin V. Wydra, CPA www.crowe.com 1 Implementing the

October 2017 Implementing the New Revenue Recognition Standard for Technology Companies An article by Glenn E. Richards, CPA; Scott G. Sachs, CPA; and Kevin V. Wydra, CPA www.crowe.com 1 Implementing the

A QUICK TOUR OF THE NEW REVENUE ACCOUNTING STANDARD

A QUICK TOUR OF THE NEW REVENUE ACCOUNTING STANDARD DISCLAIMER: Iconixx does not provide accounting advice. This material has been prepared for informational purposes only, and is not intended to provide,

A QUICK TOUR OF THE NEW REVENUE ACCOUNTING STANDARD DISCLAIMER: Iconixx does not provide accounting advice. This material has been prepared for informational purposes only, and is not intended to provide,

Accounting Standard Updates

Accounting Standard Updates HFMA Spring Conference 2018 Presented by: Kimberly Sokoloff, Health Care Assurance Services Senior Manager Elizabeth Lasnier, Health Care Assurance Services Manager Presenters

Accounting Standard Updates HFMA Spring Conference 2018 Presented by: Kimberly Sokoloff, Health Care Assurance Services Senior Manager Elizabeth Lasnier, Health Care Assurance Services Manager Presenters

Ind AS 115: Revenue from Contracts with Customers

Bringing expert global and local knowledge to your reporting environment www.rsmindia.in Ind AS 115: Revenue from Contracts with Customers - Overview and Impact on Key Sectors 1.0 INTRODUCTION On 29 March

Bringing expert global and local knowledge to your reporting environment www.rsmindia.in Ind AS 115: Revenue from Contracts with Customers - Overview and Impact on Key Sectors 1.0 INTRODUCTION On 29 March

BDO KNOWS: REVENUE RECOGNITION TOPIC 606, REVENUE FROM CONTRACTS WITH CUSTOMERS - PRESENTATION AND DISCLOSURE. 1. Introduction CONTENTS

OCTOBER 2017 www.bdo.com BDO KNOWS: REVENUE RECOGNITION CONTENTS INTRODUCTION... 1 DISCLOSURE OBJECTIVE...2 PRESENTATION...2 Statement of Financial Position...2 Statement of Comprehensive Income (Statement

OCTOBER 2017 www.bdo.com BDO KNOWS: REVENUE RECOGNITION CONTENTS INTRODUCTION... 1 DISCLOSURE OBJECTIVE...2 PRESENTATION...2 Statement of Financial Position...2 Statement of Comprehensive Income (Statement