UNIVERSAL HEALTHCARE COUNCIL 2013 OVERVIEW OF THE AFFORDABLE CARE ACT

|

|

|

- Noah Russell Cunningham

- 6 years ago

- Views:

Transcription

1 UNIVERSAL HEALTHCARE COUNCIL 2013 OVERVIEW OF THE AFFORDABLE CARE ACT Introduction The Patient Protection and Affordable Care Act (ACA) was signed into federal law on March 23, While many reforms and provisions have taken effect gradually over the past three years and some are not effective until as late as 2018, January 2014 marks the start of an important year for ACA implementation at the local level. This document provides a brief background on Affordable Care Act provisions relevant to the work of the Universal Healthcare Council. ACA Overview ACA provisions aimed at decreasing the number of uninsured and increasing affordability of health care fall under the categories of shared responsibility, coverage expansion, and insurance market reforms. Shared responsibility falls on two groups: individuals and employers. Individuals Starting January 1 st, 2014, most Americans are required to carry health insurance that meets Minimum Essential Coverage (MEC) requirements. Qualifying coverage includes certain government-sponsored plans, employer-sponsored plans, grandfathered plans, plans in the individual market, and plans sold through health insurance exchanges. Coverage that provides only dental or vision benefits does not qualify as MEC. o Shared responsibility payment: Individuals choosing not to enroll in MEC, and any dependents without MEC, are subject to an annual penalty when filing taxes. For 2014, the penalty is 1% of taxable income or $95, increasing to 2% of taxable income or $325 in 2015, and 2.5% of taxable income or $695 in After 2016, the payment will be increased and adjusted for cost of living. o Exemptions: The penalty is waived for individuals who are without qualified coverage for no more than three consecutive months and those who are exempt from the requirement to carry insurance. Exemptions are granted for undocumented immigrants, economic hardship, incarcerated persons, members of Indian tribes, religious beliefs, persons for whom the lowest cost 9/26/2013 Page 1

2 Overview of the Affordable Care Act plan exceeds 8% of household income, and persons below the federal income tax filing threshold. Employers Beginning January 1, 2015, ACA imposes a penalty on employers with 50 or more full-time equivalent (FTE) employees that fail to insure their employees in certain circumstances. Noncompliant employers face penalties, also known as shared responsibility payments, for either failing to offer coverage or for offering unaffordable coverage: o No coverage is defined as an employer that offers coverage for fewer than 95% of FTEs. The penalty is imposed if at least employee receives a low income subsidy through Covered California. The penalty is equal to $2,000 multiplied by the number of FTEs beyond the first 30. o Unaffordable coverage is defined as health insurance that pays for less than 60% of covered health care expenses OR health insurance that pays for 60% of covered health care expenses but the employee would have to pay >9.5% of their family income for coverage. The penalty is imposed if at least employee receives a low income subsidy through Covered California. The penalty is the greater of $3,000 multiplied by the number of FTEs receiving a subsidy, OR $2,000 multiplied by the number of FTEs beyond the first 30. o At a minimum, large employers that offer insurance that covers at least 60% of health expenses at a cost to employees of no more than 9.5% of family income would avoid penalties. Coverage expansion is achieved through Medicaid reforms and the creation of Health Insurance Exchanges. Medicaid reforms With coverage beginning January 1, 2014, states may expand their Medicaid programs to cover individuals earning less than 133% of the Federal Poverty Level (FPL; $15,282 per year for an individual and $31,322 for a family of four). This provision streamlines Medicaid eligibility guidelines and allows states to cover previously ineligible populations comprised of non-disabled, childless adults. The federal government will 9/26/2013 Page 2

3 Overview of the Affordable Care Act bear the cost of covering the newly eligible population at 100% for the first three years, tapering down to 90% in 2020 and beyond. California has chosen to expand Medi-Cal and expects to cover 1.6 million new enrollees statewide, with open enrollment beginning in October Health Insurance Exchanges Beginning January 1st, 2014, the ACA requires the establishment and operation of an online marketplace in each state, where individuals and small businesses may compare and purchase health insurance plans. Covered California, California s Exchange, will begin open enrollment in October 2013 for plans effective January Five health insurers will have plans on Covered California that will be available for San Franciscans: Anthem Blue Cross, Blue Shield, Chinese Community Health Plan, Kaiser, and HealthNet. o o Individual consumers will have a choice of plans from tiers that vary by actuarial value (the percentage of benefit costs covered by the plan), ranging from 60% in the Bronze tier to 90% in the Platinum. If eligible, certain persons may also enroll in a low-premium, high-deductible catastrophic coverage plan. All plans offered on Covered California must offer a set of minimum benefits and comply with annual out-of-pocket cost limits based on individual or family income. Qualified persons earning between % of FPL (up to $45,960 per year for an individual and $94,200 for a family of four) will be eligible for federal tax credits and out-of-pocket cost sharing subsidies to help afford coverage through the Exchange. Small businesses, defined as those with fewer than 50 full-time employees, will also be able to purchase plans through Covered California. Businesses with fewer than 25 employees will be eligible for tax subsidies. Insurance market reforms, some of which are already in effect, include: Guaranteed Issue (insurers may not deny coverage to anyone seeking it) Elimination of annual limits on covered benefits Elimination of pre-existing condition exclusions Extended coverage for adults younger than 26 under their parents insurance Elimination of premium rating based on gender or health status Coverage of preventive and primary care services without cost-sharing 9/26/2013 Page 3

4 Overview of the Affordable Care Act Requirement for insurers to spend at least 80% of premiums on medical services or make rebates to consumers Effective January 1 st, 2014, requirement for all non-grandfathered individual and small group plans to provide an essential health benefits package from defined benefit categories, while covering at least 60% of plan costs and maintaining limits on cost-sharing 9/26/2013 Page 4

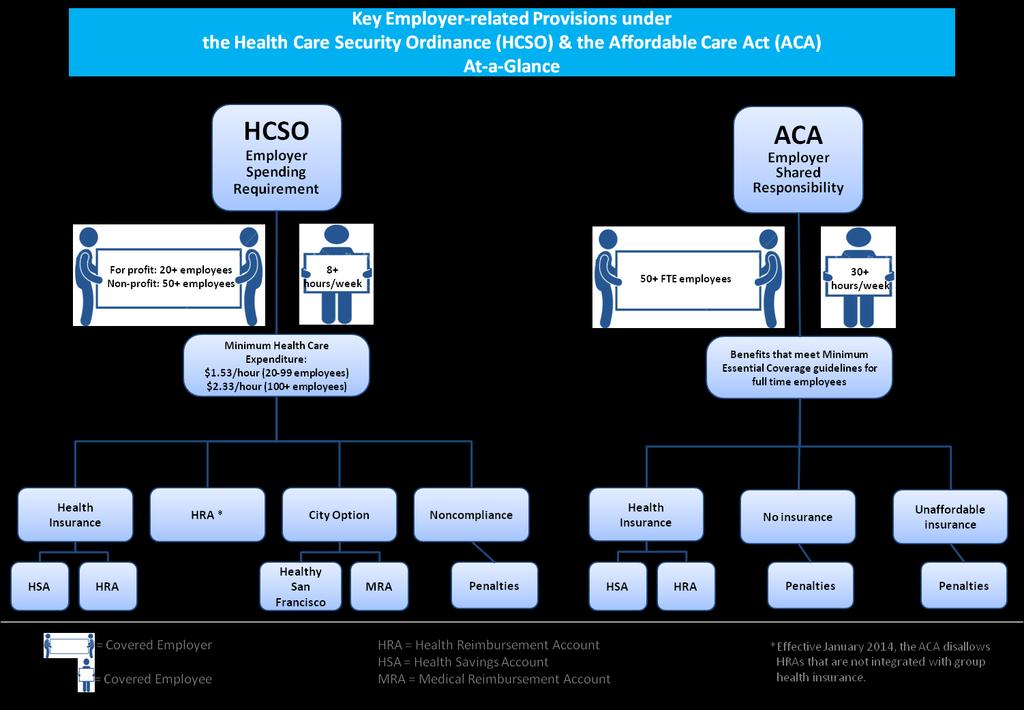

5 UNIVERSAL HEALTHCARE COUNCIL 2013 HEALTH CARE ACCESS PROGRAMS IN SAN FRANCISCO Introduction The City and County of San Francisco has a long-standing commitment to providing access to health care for all San Franciscans. This document provides background on local programs and policies seeking to extend coverage to San Franciscans without access to or eligibility for commercial insurance and state/federal public programs. Health Care Security Ordinance (HCSO): As a result of the work of the previous Universal Healthcare Council, the Health Care Security Ordinance was passed in In addition to creating the Healthy San Francisco Program, the HCSO established employer responsibilities toward employees health care costs. Effective 2008, the Employer Spending Requirement (ESR) under the HCSO obligates all for-profit San Francisco employers with 20 or more employees to make health care expenditures on behalf of employees working a minimum of 8 hours per week. Non-profit employers with 50 or more employees are also subject to the ESR. In 2013, the minimum health care expenditure rates are $1.55/hour per covered employee for small/medium employers and $2.33/hour for large employers. Employers may comply with the ESR by choosing any, or any combination of, the following: Offer health insurance if plan expenditures do not satisfy minimum health care expenditure rates, employer must also establish a health reimbursement account Establish individual Health Reimbursement Accounts (HRA) these funds must be irrevocably allocated for the employee s use and available for a minimum of 24 months after the date of allocation. Effective January 1 st, 2014, HRAs that are not coupled with a health insurance plan are disallowed under the Affordable Care Act. Contribute to City Option if the employer elects to make payments to the City, employees have the option to enroll in Healthy San Francisco or to have the money deposited in a medical reimbursement account (MRA) 9/26/2013 Page 1

6 Health Care Access Programs in San Francisco Healthy San Francisco (HSF) Healthy San Francisco was created at the recommendation of the 2006 Universal Healthcare Council and began enrollment in While HSF is administered by the San Francisco Health Plan, it is not insurance. Rather, it is an access program that connects enrollees with a citywide network of medical and behavioral health care providers. San Francisco residents with incomes up to 500% of FPL, and who are not eligible for other public insurance programs, are eligible to participate in Healthy San Francisco. Since 2007, HSF has provided access to care for over 116,000 uninsured residents. City residents may enroll in Healthy San Francisco by one of three avenues: Their employer chooses the City Option to comply with the Employer Spending Requirement under the Health Care Security Ordinance. During FY , 1,429 employers contributed to the City Option, and 40,479 HSF enrollees received some employer contribution. They do not qualify for any state or federal health insurance programs. This category generally covers undocumented persons. Their incomes fall below 500% of FPL. Healthy Kids (HK) Healthy Kids provides insurance for medical, dental, vision, and behavioral health services for children aged To be eligible, a child must be from a family earning less than 300% of the federal poverty level (FPL), and must not be eligible for any other public insurance program (Medi-Cal or Healthy Families). Healthy Kids is administered by the San Francisco Health Plan, with annual premiums ranging from $48 - $189 per child. Under the Affordable Care Act, all citizen and legally present children currently eligible for HK will transition to Medi-Cal. Healthy Workers (HW) Healthy Workers provides group health insurance to registered In-Home Supportive Services (IHSS) workers, as well as certain temporary, exempt as-needed employees of the City and County of San Francisco. Plan enrollees have access to a full range of medical, vision, and mental health care. Administered by the San Francisco Health Plan, Healthy Workers is funded by a combination of City and County General Fund and federal/state reimbursement. 12/16/2013 Page 2

7 Health Care Access Programs in San Francisco Health Care Accountability Ordinance (HCAO) Effective July 1, 2001, the Health Care Accountability Ordinance obligates all City contractors with annual contracts of over $25,000 ($50,000 for non-profits) and some tenants at city air and sea ports to provide health coverage for their employees. Covered contractors, defined as those with 20 or more employees, and any covered subcontractors, must offer health plan benefits to their employees. The health plan benefits must meet Minimum Standards, set by the Department of Public Health, and the contractor must pay 100% of employees premiums. Contractors who do not offer a health plan may choose instead to make payments to the City for use by the Department of Public Health. The current rate of expenditure for this option is $4.00/hour per covered employee, not to exceed $160/week per covered employee. 12/16/2013 Page 3

8 18-64 State and Federal Programs Available in San Francisco At-a-Glance Current 2014

9

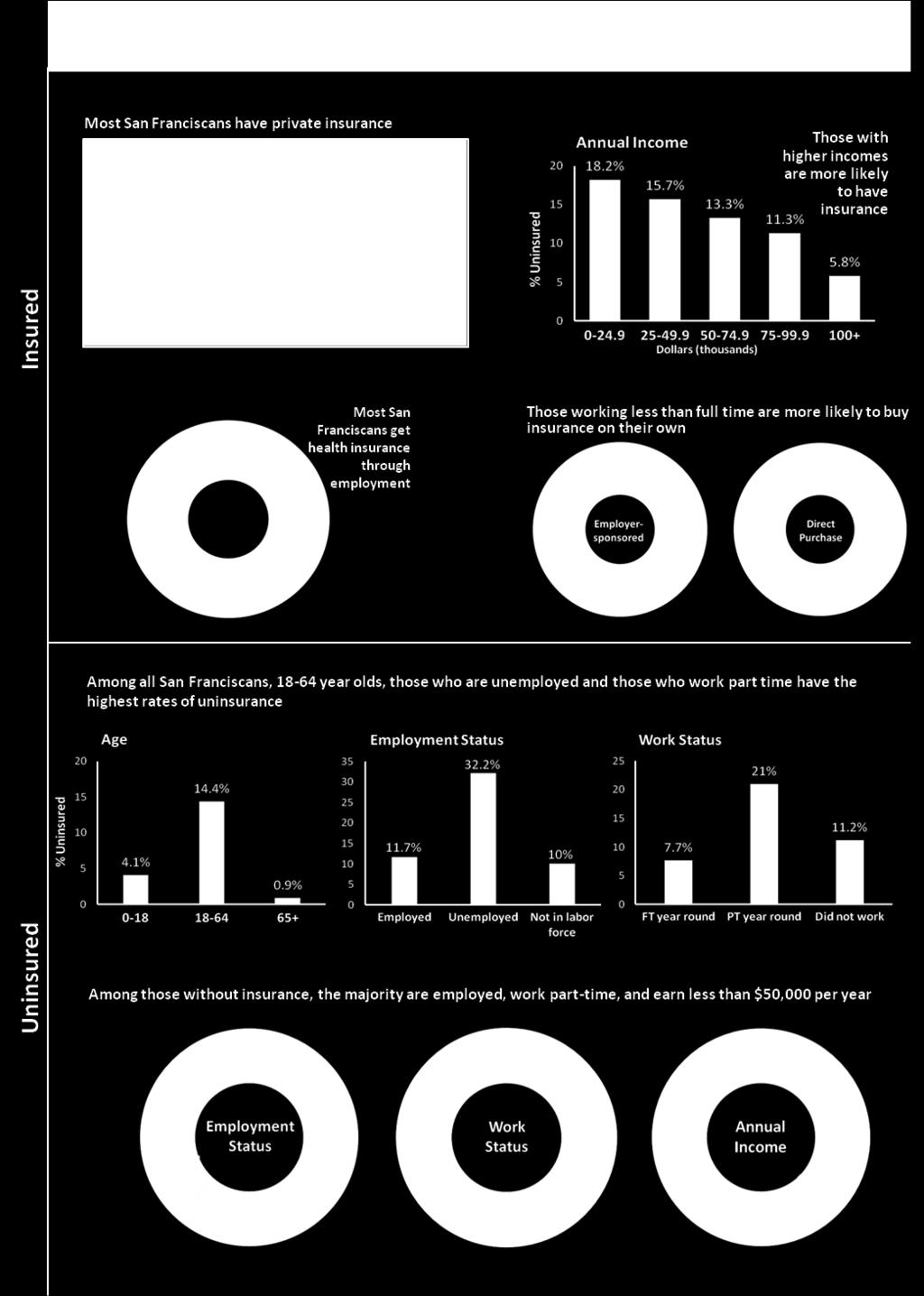

10 UNIVERSAL HEALTHCARE COUNCIL 2013 INSURANCE STATUS IN SAN FRANCISCO Introduction Close to 90% of San Franciscans have some form of health insurance through private or public coverage. Using the latest available data 1, this document provides a snapshot of how San Franciscans get health care coverage and who remains uninsured. Insured The major factors delineating how people get health insurance are age, income, and employment. Age Children under 18 years of age are covered by their parents insurance or by state and federal low-income health programs, depending on household income. California law extends Medi-Cal coverage to eligible young adults under 21, and the Affordable Care Act (ACA) allows young adults under 26 to remain on their parents private insurance. Persons aged 65 and older are covered by Medicare, and in the case of lowincome or disabled seniors, also by Medi-Cal. The large majority of San Francisco s population (72%) falls within the age range; this group also accounts for the majority of the City s workforce and is the group that would be most impacted by ACA implementation. Exhibit 1: San Franciscans Insurance Status by Type and Age Type of insurance Age % of San Franciscans Under Private 65.2% 72.4% 71.4% 2.9% Public 26.4% 8.4% 14.1% 51.9% Public & Private 4.3% 1.1% 2.7% 44.3% None 4.1% 18.1% 11.8% 0.9% 1 Data source: American Community Survey, 1 Year Estimates, /26/2013 Page 1

, Healthy Kids (up to 300% of FPL), and Healthy San")

will be eligible for subsidized coverage on the Exchange.")

11 Health Care Access Programs in San Francisco Income Household income, as a percentage of the federal poverty level (FPL), determines eligibility for state and local public insurance programs, including Medi-Cal (up to 133% of FPL starting 2014), Healthy Kids (up to 300% of FPL), and Healthy San Francisco (up to 500% of FPL). Under the ACA, people earning between % of FPL (~$15,000 - $46,000 per year) will be eligible for subsidized coverage on the Exchange. Among San Franciscans in each age bracket, those with incomes above 400% of FPL comprise the largest proportion of people with insurance, and those earning between % of FPL account for the smallest. Exhibit 2a: While more than half of San Franciscans earn less than $46,000 per year, those with higher incomes form the majority of those with insurance San Francisco s Population by Federal Poverty Level 12/16/2013 Page 2

12 Health Care Access Programs in San Francisco Employment Private, employer-sponsored coverage accounts for the largest proportion of insured San Franciscans, with 67% of insured year olds participating in employer plans. However, employer-sponsored insurance is generally available only to full-time employees, as indicated by the sharp decrease in the numbers of part-time or unemployed persons with employer-sponsored plans. If they do not qualify for public programs, individuals without an offer of coverage from their employer may purchase directly on the insurance market. Insured San Franciscans working less than full time account for only 23% of those participating in employersponsored plans, but represent 36% of those with direct purchase insurance. Beginning in 2014, individuals who are not eligible for public programs or are not offered affordable employer-sponsored coverage will be able to purchase plans on Covered California. Exhibit 3: Most San Franciscans get insurance through their employers, and full-time employees form the majority of those with insurance Source of Insurance Among San Franciscan Aged Source of Insurance and Employment Status Among Insured San Franciscan Aged /16/2013 Page 3

, of whom 84,679 are aged 18-64, did not have health insurance in 2011.")

13 Health Care Access Programs in San Francisco Uninsured An estimated 90,106 San Franciscans (11.2%), of whom 84,679 are aged 18-64, did not have health insurance in The reasons for not having insurance include ineligibility for state/federal public programs, difficulty understanding or navigating the insurance system, cost, or not feeling the need to have insurance. Exhibit 4a depicts which San Franciscans are most likely to be uninsured, while Exhibit 4b details the characteristics among the uninsured. Exhibit 4a: San Franciscans from the following categories are most likely to be uninsured: year olds, those earning less than $25,000 per year, those who are unemployed, and those who work part-time all year. Exhibit 4b: Among San Franciscans who do not have insurance, 62% are employed, 45% work part-time all year, and 48% earn less than $50,000 per year. 12/16/2013 Page 4

14

INDIVIDUAL SHARED RESPONSIBILITY PROVISION

UNIVERSAL HEALTHCARE COUNCIL 2013 The Affordable Care Act s (ACA) shared responsibility provisions fall on two groups: individuals and employers. INDIVIDUAL SHARED RESPONSIBILITY PROVISION Overview The

UNIVERSAL HEALTHCARE COUNCIL 2013 The Affordable Care Act s (ACA) shared responsibility provisions fall on two groups: individuals and employers. INDIVIDUAL SHARED RESPONSIBILITY PROVISION Overview The

HEALTH REFORM. Presentation to San Francisco Health Commission April 20, 2010

1 HEALTH REFORM Presentation to San Francisco Health Commission April 20, 2010 Tangerine Brigham, Deputy Director of Health and Director of Healthy San Francisco Colleen Chawla, Director of Grants and

1 HEALTH REFORM Presentation to San Francisco Health Commission April 20, 2010 Tangerine Brigham, Deputy Director of Health and Director of Healthy San Francisco Colleen Chawla, Director of Grants and

The Affordable Care Act: A Summary on Healthcare Reform. The Wyoming Department of Insurance

The Affordable Care Act: A Summary on Healthcare Reform The Wyoming Department of Insurance Additional Resources Wyoming Insurance Department: http://doi.wyo.gov/ or toll free at 1-(800)-438-5768 Information

The Affordable Care Act: A Summary on Healthcare Reform The Wyoming Department of Insurance Additional Resources Wyoming Insurance Department: http://doi.wyo.gov/ or toll free at 1-(800)-438-5768 Information

GENERAL INFORMATION BULLETIN

AFL-CIO California School Employees Association GENERAL INFORMATION BULLETIN March 15, 2013 General Information Bulletin No. 17 13 AFFORDABLE CARE ACT (ACA) QUESTION & ANSWER RESOURCE DOCUMENT Action for

AFL-CIO California School Employees Association GENERAL INFORMATION BULLETIN March 15, 2013 General Information Bulletin No. 17 13 AFFORDABLE CARE ACT (ACA) QUESTION & ANSWER RESOURCE DOCUMENT Action for

Key Medicaid, CHIP, and Low-Income Provisions in the Senate Bill Patient Protection and Affordable Care Act (Released November 18, 2009)

") Key Medicaid, CHIP, and Low-Income Provisions in the Senate Bill Patient Protection and Affordable Care Act (Released November 18, 2009) On November 18, 2009, the Senate released its health care reform

Key Medicaid, CHIP, and Low-Income Provisions in the Senate Bill Patient Protection and Affordable Care Act (Released November 18, 2009) On November 18, 2009, the Senate released its health care reform

OVERVIEW OF THE AFFORDABLE CARE ACT. September 23, 2013

OVERVIEW OF THE AFFORDABLE CARE ACT September 23, 2013 Outline The New Continuum of Coverage Medicaid and CHIP Are Changing The New Marketplaces Insurance Affordability Programs Shared Responsibility Requirement

OVERVIEW OF THE AFFORDABLE CARE ACT September 23, 2013 Outline The New Continuum of Coverage Medicaid and CHIP Are Changing The New Marketplaces Insurance Affordability Programs Shared Responsibility Requirement

The Affordable Care Act: A Summary on Healthcare Reform. The Wyoming Department of Insurance

The Affordable Care Act: A Summary on Healthcare Reform The Wyoming Department of Insurance The ACA is a federal law that impacts Wyoming and its citizens. The State of Wyoming has filed a lawsuit against

The Affordable Care Act: A Summary on Healthcare Reform The Wyoming Department of Insurance The ACA is a federal law that impacts Wyoming and its citizens. The State of Wyoming has filed a lawsuit against

Health Care Reform. Navigating The Maze Of. What s Inside

Navigating The Maze Of Health Care Reform What s Inside Questions and Answers on Health Care Reform Health Care Reform Timeline Health Care Reform Glossary Questions and Answers on Health Care Reform I

Navigating The Maze Of Health Care Reform What s Inside Questions and Answers on Health Care Reform Health Care Reform Timeline Health Care Reform Glossary Questions and Answers on Health Care Reform I

FINANCIAL CONSIDERATIONS FOR INDIVIDUALS, EMPLOYERS, AND THE LOCAL PUBLIC HEALTH SYSTEM

UNIVERSAL HEALTHCARE COUNCIL 2013 FINANCIAL CONSIDERATIONS FOR INDIVIDUALS, EMPLOYERS, AND THE LOCAL PUBLIC HEALTH SYSTEM As San Francisco moves forward with Health Reform, cost considerations will play

UNIVERSAL HEALTHCARE COUNCIL 2013 FINANCIAL CONSIDERATIONS FOR INDIVIDUALS, EMPLOYERS, AND THE LOCAL PUBLIC HEALTH SYSTEM As San Francisco moves forward with Health Reform, cost considerations will play

Tennessee Public Health Association. Overview of the Affordable Care Act

Tennessee Public Health Association Overview of the Affordable Care Act Susie Baird Director of Policy Health Care Finance and Administration September 12, 2013 1 Origins of ACA Signed into law on March

Tennessee Public Health Association Overview of the Affordable Care Act Susie Baird Director of Policy Health Care Finance and Administration September 12, 2013 1 Origins of ACA Signed into law on March

Frequently Asked Questions about Health Care Reform and the Affordable Care Act

Frequently Asked Questions about Health Care Reform and the Affordable Care Act HEALTH CARE REFORM OVERVIEW Q 1: What ACA changes are already in place? There are no lifetime dollar limits on essential

Frequently Asked Questions about Health Care Reform and the Affordable Care Act HEALTH CARE REFORM OVERVIEW Q 1: What ACA changes are already in place? There are no lifetime dollar limits on essential

Navigating the New Health Care Law

Navigating the New Health Care Law For Sole Proprietors and Small Businesses (50 employees or less) This presentation is intended for educational purposes only and not intended as a legal, tax, or insurance

Navigating the New Health Care Law For Sole Proprietors and Small Businesses (50 employees or less) This presentation is intended for educational purposes only and not intended as a legal, tax, or insurance

The Affordable Care Act and the Income Tax. By Greg Martinez December 2013

The Affordable Care Act and the Income Tax By Greg Martinez December 2013 Overview Health insurance mandate Individual Shared Responsibility Provision Exemptions Minimum essential coverage Penalties Covered

The Affordable Care Act and the Income Tax By Greg Martinez December 2013 Overview Health insurance mandate Individual Shared Responsibility Provision Exemptions Minimum essential coverage Penalties Covered

THE AFFORDABLE CARE ACT Frequently Asked Questions

THE AFFORDABLE CARE ACT Frequently Asked Questions We are providing basic information on the ACA in order for you to best prepare for your tax appointment. While we strive to give you complete and accurate

THE AFFORDABLE CARE ACT Frequently Asked Questions We are providing basic information on the ACA in order for you to best prepare for your tax appointment. While we strive to give you complete and accurate

The Affordable Care Act; 2014 and Beyond

The Affordable Care Act; 2014 and Beyond Presented by: Lacey Robinson, ACA Certified Vice President & Senior Benefits Consultant Gregory & Appel December 10, 2013 Agenda 2014 ACA Mandates ACA Intention

The Affordable Care Act; 2014 and Beyond Presented by: Lacey Robinson, ACA Certified Vice President & Senior Benefits Consultant Gregory & Appel December 10, 2013 Agenda 2014 ACA Mandates ACA Intention

The Patient Protection and Affordable Care Act in Colorado

The Patient Protection and Affordable Care Act in Colorado Colorado Center on Law and Policy 789 Sherman St., Suite 300, Denver, CO 80203 303-573-5669 September 20, 2013 The Problem 50 million uninsured

The Patient Protection and Affordable Care Act in Colorado Colorado Center on Law and Policy 789 Sherman St., Suite 300, Denver, CO 80203 303-573-5669 September 20, 2013 The Problem 50 million uninsured

M E M O R A N D U M. Jim Illig, Health Commission President, and Members of the Health Commission

City and County of San Francisco Gavin Newsom Mayor Department of Public Health Mitchell H. Katz, MD Director of Health M E M O R A N D U M DATE: April 16, 2010 TO: FROM: THRU: RE: Jim Illig, Health Commission

City and County of San Francisco Gavin Newsom Mayor Department of Public Health Mitchell H. Katz, MD Director of Health M E M O R A N D U M DATE: April 16, 2010 TO: FROM: THRU: RE: Jim Illig, Health Commission

Health Insurance Marketplace

Health Insurance Marketplace Briefing on the Affordable Care Act 2014 Ben J. Altheimer Oral Symposium UALR Bowen School of Law February 28, 2014 David Nilasena, MD Centers for Medicare & Medicaid Services

Health Insurance Marketplace Briefing on the Affordable Care Act 2014 Ben J. Altheimer Oral Symposium UALR Bowen School of Law February 28, 2014 David Nilasena, MD Centers for Medicare & Medicaid Services

ACA in Brief 2/18/2014. It Takes Three Branches... Overview of the Affordable Care Act. Health Insurance Coverage, USA, % 16% 55% 15% 10%

Health Insurance Coverage, USA, 2011 16% Uninsured Overview of the Affordable Care Act 55% 16% Medicaid Medicare Private Non-Group Philip R. Lee Institute for Health Policy Studies Janet Coffman, MPP,

Health Insurance Coverage, USA, 2011 16% Uninsured Overview of the Affordable Care Act 55% 16% Medicaid Medicare Private Non-Group Philip R. Lee Institute for Health Policy Studies Janet Coffman, MPP,

The New Responsibility to Secure Coverage: Frequently Asked Questions

The New Responsibility to Secure Coverage: Frequently Asked Questions Introduction The Patient Protection and Affordable Care Act (PPACA) includes a much-discussed requirement that people secure health

The New Responsibility to Secure Coverage: Frequently Asked Questions Introduction The Patient Protection and Affordable Care Act (PPACA) includes a much-discussed requirement that people secure health

Health Care Reform under the Patient Protection and Affordable Care Act ( PPACA ) provisions effective January 1, 2014

provisions effective January 1, 2014") The New Health Care Landscape Today s Agenda Health Care Reform under the Patient Protection and Affordable Care Act ( PPACA ) provisions effective January 1, 2014 Exchanges and Qualified Health Plans

The New Health Care Landscape Today s Agenda Health Care Reform under the Patient Protection and Affordable Care Act ( PPACA ) provisions effective January 1, 2014 Exchanges and Qualified Health Plans

2014 and Beyond. This timeline explains how and when the Affordable Care Act (ACA) provisions will be implemented over the next few years.

provisions will be implemented over the next few years.") December This timeline explains how and when the Affordable Care Act (ACA) provisions will be implemented over the next few years. Get Covered Illinois, the Official Health Marketplace of Illinois While

December This timeline explains how and when the Affordable Care Act (ACA) provisions will be implemented over the next few years. Get Covered Illinois, the Official Health Marketplace of Illinois While

Health Care Reform: General Q&A for Employees

From Health Care Reform: General Q&A for Employees Common questions answered I ve heard a lot about the health care reform law. When do the reforms become effective? The health care reform bill was signed

From Health Care Reform: General Q&A for Employees Common questions answered I ve heard a lot about the health care reform law. When do the reforms become effective? The health care reform bill was signed

Health Care Reform Under the ACA Its Effect on Municipalities and Their Employees

Health Care Reform Under the ACA Its Effect on Municipalities and Their Employees Maine Municipal Employees Health Trust 1-800-852-8300 www.mmeht.org The Difference Is Trust August 2014 1 Today s Agenda

Health Care Reform Under the ACA Its Effect on Municipalities and Their Employees Maine Municipal Employees Health Trust 1-800-852-8300 www.mmeht.org The Difference Is Trust August 2014 1 Today s Agenda

Some Basics on the Individual Mandate, Subsidies, and Medicaid Expansion Lisa Klinger, J.D.

Some Basics on the Individual Mandate, Subsidies, and Medicaid Expansion Lisa Klinger, J.D. www.leavitt.com/healthcarereform.com 10-23- 2013 As of January 1, 2014, the Patient Protection and Affordable

Some Basics on the Individual Mandate, Subsidies, and Medicaid Expansion Lisa Klinger, J.D. www.leavitt.com/healthcarereform.com 10-23- 2013 As of January 1, 2014, the Patient Protection and Affordable

HEALTH CARE REFORM Focus on Group Coverage Blue Cross and Blue Shield of Minnesota. All rights reserved.

HEALTH CARE REFORM Focus on Group Coverage 2011 Blue Cross and Blue Shield of Minnesota. All rights reserved. Current Insurance Coverage Environment Minnesota United States Uninsured 9% Ot her Public 1%

HEALTH CARE REFORM Focus on Group Coverage 2011 Blue Cross and Blue Shield of Minnesota. All rights reserved. Current Insurance Coverage Environment Minnesota United States Uninsured 9% Ot her Public 1%

Aldridge Financial Consultants January 12, 2013

Aldridge Financial Consultants Mark D. Aldridge, CFP, CFA, ChFC 3021 Bethel Road Suite 100 Columbus, OH 43220 614-824-3080 Fax 614 824-3082 mark.aldridge@raymondjames.com www.markaldridge.com Health-Care

Aldridge Financial Consultants Mark D. Aldridge, CFP, CFA, ChFC 3021 Bethel Road Suite 100 Columbus, OH 43220 614-824-3080 Fax 614 824-3082 mark.aldridge@raymondjames.com www.markaldridge.com Health-Care

Complying with Health Care Reform

Complying with Health Care Reform April 17, 2013 1 1 What Happened? In March 2010, Congress passed and the President signed health reform in: The Patient Protection and Affordable Care Act The Health Care

Complying with Health Care Reform April 17, 2013 1 1 What Happened? In March 2010, Congress passed and the President signed health reform in: The Patient Protection and Affordable Care Act The Health Care

Help your constituents gain the most from the Affordable Care Act

1 Help your constituents gain the most from the Affordable Care Act Quick refresher course on Covered California: your destination for affordable, quality health care, including Medi-Cal Help your constituents

1 Help your constituents gain the most from the Affordable Care Act Quick refresher course on Covered California: your destination for affordable, quality health care, including Medi-Cal Help your constituents

FACTS ABOUT THE ACA INDIVIDUAL MANDATE

FACTS ABOUT THE ACA INDIVIDUAL MANDATE Beginning 2014, every U.S. citizen and resident alien must have health insurance (minimum essential coverage). Failure to do so will result in a penalty (an additional

FACTS ABOUT THE ACA INDIVIDUAL MANDATE Beginning 2014, every U.S. citizen and resident alien must have health insurance (minimum essential coverage). Failure to do so will result in a penalty (an additional

ObamaCare 101: An Educational Training on Health Reform. Training Workshop

ObamaCare 101: An Educational Training on Health Reform Training Workshop About ITUP ITUP is a non partisan, non profit health policy think tank based in Santa Monica, CA. We are funded by generous grants

ObamaCare 101: An Educational Training on Health Reform Training Workshop About ITUP ITUP is a non partisan, non profit health policy think tank based in Santa Monica, CA. We are funded by generous grants

What s on the Horizon for Health Care and Public Benefits. May 8, 2013

What s on the Horizon for Health Care and Public Benefits. May 8, 2013 1 Overview Individual Mandate Federal Exchange Changes to Badgercare Changes to MAPP Future of HIRSP Changes to employer group health

What s on the Horizon for Health Care and Public Benefits. May 8, 2013 1 Overview Individual Mandate Federal Exchange Changes to Badgercare Changes to MAPP Future of HIRSP Changes to employer group health

HCR Support Specialist Training Module II

HCR Support Specialist Training Module II The ACA and the Individual Market Your Trainer Today: Constance Starkey Individual Mandate What is the mandate? What are the exceptions? What is the penalty for

HCR Support Specialist Training Module II The ACA and the Individual Market Your Trainer Today: Constance Starkey Individual Mandate What is the mandate? What are the exceptions? What is the penalty for

Overview of the ACA and Wisconsin Medicaid Reforms. Covering Kids & Families Wisconsin Wisconsin Primary Health Care Association

Overview of the ACA and Wisconsin Medicaid Reforms Covering Kids & Families Wisconsin Wisconsin Primary Health Care Association Updated September 9, 2013 Topics to be Covered What is the ACA? Wisconsin

Overview of the ACA and Wisconsin Medicaid Reforms Covering Kids & Families Wisconsin Wisconsin Primary Health Care Association Updated September 9, 2013 Topics to be Covered What is the ACA? Wisconsin

THE AFFORDABLE CARE ACT...2

Table of Contents THE AFFORDABLE CARE ACT...2 Health Insurance Marketplace (Exchange)...3 Metallic Levels...4 Catastrophic Plans...4 Individual Mandate...5 Subsidies...5 Open Enrollment Period...6 Special

Table of Contents THE AFFORDABLE CARE ACT...2 Health Insurance Marketplace (Exchange)...3 Metallic Levels...4 Catastrophic Plans...4 Individual Mandate...5 Subsidies...5 Open Enrollment Period...6 Special

AFFORDABLE CARE ACT (ACA) UPDATE JUNE 26, 2013

UPDATE JUNE 26, 2013") AFFORDABLE CARE ACT (ACA) UPDATE JUNE 26, 2013 FREDDY WARNER SYSTEM EXECUTIVE, PUBLIC POLICY & GOVERNMENT RELATIONS MEMORIAL HERMANN HEALTH SYSTEM ACA - REVISITED OBAMA SIGNED INTO LAW 2010 GOALS PROVIDE

AFFORDABLE CARE ACT (ACA) UPDATE JUNE 26, 2013 FREDDY WARNER SYSTEM EXECUTIVE, PUBLIC POLICY & GOVERNMENT RELATIONS MEMORIAL HERMANN HEALTH SYSTEM ACA - REVISITED OBAMA SIGNED INTO LAW 2010 GOALS PROVIDE

Sales Division Webinar #9

Disclaimer: The information contained in this presentation is a brief overview and should not be construed as tax advice or exhausted coverage of the topic. 1 Sales Division Webinar #9 ALL SERVICE CHANNELS

Disclaimer: The information contained in this presentation is a brief overview and should not be construed as tax advice or exhausted coverage of the topic. 1 Sales Division Webinar #9 ALL SERVICE CHANNELS

The Affordable Care Act: Information for Wyoming Consumers

The Affordable Care Act: Information for Wyoming Consumers The Wyoming Department of Insurance The Affordable Care Act is a federally-mandated health care and health insurance law. Wyoming citizens and

The Affordable Care Act: Information for Wyoming Consumers The Wyoming Department of Insurance The Affordable Care Act is a federally-mandated health care and health insurance law. Wyoming citizens and

Open Enrollment is here!

Navigating the Federal Marketplace AFFORDABLE CARE Open Enrollment is here! Reminders On November 20 at 9:30 AM ET, IPHCA is hosting a call with Matt Cesnik from FSSA again. CMS has released guidance on

Navigating the Federal Marketplace AFFORDABLE CARE Open Enrollment is here! Reminders On November 20 at 9:30 AM ET, IPHCA is hosting a call with Matt Cesnik from FSSA again. CMS has released guidance on

Rhode Island League of Cities and Towns. Health Care Reform and the State Exchanges: What Cities and Towns Should Be Doing Now

Rhode Island League of Cities and Towns Health Care Reform and the State Exchanges: What Cities and Towns Should Be Doing Now Rick Johnson Senior Vice President, National Public Sector Health Practice

Rhode Island League of Cities and Towns Health Care Reform and the State Exchanges: What Cities and Towns Should Be Doing Now Rick Johnson Senior Vice President, National Public Sector Health Practice

2014 AFFORDABLE CARE ACT (OBAMA CARE)

") 2014 AFFORDABLE CARE ACT (OBAMA CARE) Planning for 2014 Tax Return Filings O Beginning 2014, the ACA requires all persons be covered by health insurance O Individuals not covered by Medicare, their employers,

2014 AFFORDABLE CARE ACT (OBAMA CARE) Planning for 2014 Tax Return Filings O Beginning 2014, the ACA requires all persons be covered by health insurance O Individuals not covered by Medicare, their employers,

Washington Health Benefit Exchange

Washington Health Benefit Exchange AFFORDABLE CARE ACT 101 APRIL 26, 2013 Christine Brown Navigator/In-person Assister Program Today s Agenda History of the Affordable Care Act (ACA) Highlights of the

Washington Health Benefit Exchange AFFORDABLE CARE ACT 101 APRIL 26, 2013 Christine Brown Navigator/In-person Assister Program Today s Agenda History of the Affordable Care Act (ACA) Highlights of the

Understanding the Impacts of Health Care Reform on Employers : 2014 and beyond

2013 CliftonLarsonAllen LLP Understanding the Impacts of Health Care Reform on Employers : 2014 and beyond cliftonlarsonallen.com Peoria County Bar Association January 25, 2014 Deb Freeland Objectives

2013 CliftonLarsonAllen LLP Understanding the Impacts of Health Care Reform on Employers : 2014 and beyond cliftonlarsonallen.com Peoria County Bar Association January 25, 2014 Deb Freeland Objectives

How Minimum Is Your Health Insurance Coverage? IRS Proposes Regulations on Offering and Maintaining Minimum Essential Coverage Starting in 2014

How Minimum Is Your Health Insurance Coverage? IRS Proposes Regulations on Offering and Maintaining Minimum Essential Coverage Starting in 2014 February 2013 Proposed regulations issued by the Treasury

How Minimum Is Your Health Insurance Coverage? IRS Proposes Regulations on Offering and Maintaining Minimum Essential Coverage Starting in 2014 February 2013 Proposed regulations issued by the Treasury

COVERED CALIFORNIA: THE GOOD, THE BAD & THE UNDEFINED FOR CHILDREN WITH SPECIAL HEALTH CARE NEEDS

1 COVERED CALIFORNIA: THE GOOD, THE BAD & THE UNDEFINED FOR CHILDREN WITH SPECIAL HEALTH CARE NEEDS Ann-Louise Kuhns President & CEO California Children s Hospital Association Health Care Reform: The Basics

1 COVERED CALIFORNIA: THE GOOD, THE BAD & THE UNDEFINED FOR CHILDREN WITH SPECIAL HEALTH CARE NEEDS Ann-Louise Kuhns President & CEO California Children s Hospital Association Health Care Reform: The Basics

4/22/2014. Health Care Reform. Disclosure. Health Care Reform. How Will it Change Your Business Strategy?

Health Care Reform How Will it Change Your Business Strategy? OHCA Educational Session April 29 th, 2014 Presented by: Roderick S. Wood, CHRS Huntington Insurance, Inc. Disclosure This presentation contains

Health Care Reform How Will it Change Your Business Strategy? OHCA Educational Session April 29 th, 2014 Presented by: Roderick S. Wood, CHRS Huntington Insurance, Inc. Disclosure This presentation contains

Presentation by: Champaign County Health Care Consumers (CCHCC) October 26, Welcome!

October 26, Welcome!") The Affordable Care Act (ACA): The Health Insurance Marketplace and Medicaid Presentation by: Champaign County Health Care Consumers (CCHCC) October 26, 2017 Welcome! Goals of the Affordable Care Act (ACA)

The Affordable Care Act (ACA): The Health Insurance Marketplace and Medicaid Presentation by: Champaign County Health Care Consumers (CCHCC) October 26, 2017 Welcome! Goals of the Affordable Care Act (ACA)

Health Care Reform Reference Guide

Health Care Reform Reference Guide The Patient Protection and Affordable Care Act (ACA) vs. American Health Care Act (AHCA) May 11, 2017 On May 4, 2017, the House of Representatives voted 217-213 to pass

Health Care Reform Reference Guide The Patient Protection and Affordable Care Act (ACA) vs. American Health Care Act (AHCA) May 11, 2017 On May 4, 2017, the House of Representatives voted 217-213 to pass

SF Covered MRA Update

SF Covered MRA Update Presentation to the Finance and Planning Committee, San Francisco Health Commission Sumi Sousa, Anne Ho and Nimit Ruparel San Francisco Health Plan December 6, 2016 SF City Option

SF Covered MRA Update Presentation to the Finance and Planning Committee, San Francisco Health Commission Sumi Sousa, Anne Ho and Nimit Ruparel San Francisco Health Plan December 6, 2016 SF City Option

The Affordable Care Act Update

The Affordable Care Act Update Presented by: The Union Labor Life Insurance Company SOLUTIONS FOR THE UNION WORKPLACE SPECIALTY INSURANCE INVESTMENTS Overview I. Key Provisions II. Major Challenges III.

The Affordable Care Act Update Presented by: The Union Labor Life Insurance Company SOLUTIONS FOR THE UNION WORKPLACE SPECIALTY INSURANCE INVESTMENTS Overview I. Key Provisions II. Major Challenges III.

H E A L T H C A R E R E F O R M T I M E L I N E

H E A L T H C A R E R E F O R M T I M E L I N E On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act (ACA), into law. The ACA makes sweeping changes to the U.S.

H E A L T H C A R E R E F O R M T I M E L I N E On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act (ACA), into law. The ACA makes sweeping changes to the U.S.

ACA and The Marketplace. Also known as the (Federal) Exchange

Exchange") ACA and The Marketplace Also known as the (Federal) Exchange 1 Qualified Health Plan and Minimum Essential Coverage (Indiv., Small Group & Large Group Coverage) Needs to Meet the Following (At a Minimum):

ACA and The Marketplace Also known as the (Federal) Exchange 1 Qualified Health Plan and Minimum Essential Coverage (Indiv., Small Group & Large Group Coverage) Needs to Meet the Following (At a Minimum):

Affordable Care Act Planning for CPAs. Ben Conley Seyfarth Shaw LLP

Affordable Care Act Planning for CPAs Ben Conley Seyfarth Shaw LLP Overview Background ACA & Taxes Taxes on Employers (and Tax Credits for Employers) Taxes on Individuals (and Tax Credits for Individuals)

Affordable Care Act Planning for CPAs Ben Conley Seyfarth Shaw LLP Overview Background ACA & Taxes Taxes on Employers (and Tax Credits for Employers) Taxes on Individuals (and Tax Credits for Individuals)

Health Care Reform at-a-glance

Health Care Reform at-a-glance August 2015 Table of Contents Employer mandate...3 Individual mandate...3 Health plan provisions applying to both grandfathered and non-grandfathered employer plans...4 Health

Health Care Reform at-a-glance August 2015 Table of Contents Employer mandate...3 Individual mandate...3 Health plan provisions applying to both grandfathered and non-grandfathered employer plans...4 Health

Pennsylvania Association of Health Underwriters Advisors and Advocates for Employers, Employees and Health Care Consumers

Pennsylvania Association of Health Underwriters Advisors and Advocates for Employers, Employees and Health Care Consumers Timeline for Health Care Reform March 26, 2010 The Patient Protection and Affordable

Pennsylvania Association of Health Underwriters Advisors and Advocates for Employers, Employees and Health Care Consumers Timeline for Health Care Reform March 26, 2010 The Patient Protection and Affordable

AFFORDABLE CARE ACT INTRODUCTION CAUTION!

AFFORDABLE CARE ACT INTRODUCTION Last summer, the United States Supreme Court upheld the constitutionality of the Affordable Care Act (ACA) removing most of the constitutional issues surrounding health

AFFORDABLE CARE ACT INTRODUCTION Last summer, the United States Supreme Court upheld the constitutionality of the Affordable Care Act (ACA) removing most of the constitutional issues surrounding health

Compliance Alert. ACA Mandates Different Measures of Affordability

Compliance Alert ACA Mandates Different Measures of Affordability August 29, 2014 Quick Facts: Several Affordable Care Act (ACA) provisions measure the affordability of employersponsored health coverage.

Compliance Alert ACA Mandates Different Measures of Affordability August 29, 2014 Quick Facts: Several Affordable Care Act (ACA) provisions measure the affordability of employersponsored health coverage.

Needs for publicly funded behavioral health services under the Patient Protection and Affordable Care Act (ACA): What gaps will remain?

: What gaps will remain?") Needs for publicly funded behavioral health services under the Patient Protection and Affordable Care Act (ACA): What gaps will remain? February 4, 2014 Stan Dorn (sdorn@urban.org) Senior Fellow, Health

Needs for publicly funded behavioral health services under the Patient Protection and Affordable Care Act (ACA): What gaps will remain? February 4, 2014 Stan Dorn (sdorn@urban.org) Senior Fellow, Health

Patient Protection and Affordable Care Act

September 27, 2010 Patient Protection and Affordable Care Act 1 9020 Stony Point Parkway Suite 200 Richmond, VA 23235 804-267-3100 Agenda Overview Employer Feedback Terms Components of Health Care Reform

September 27, 2010 Patient Protection and Affordable Care Act 1 9020 Stony Point Parkway Suite 200 Richmond, VA 23235 804-267-3100 Agenda Overview Employer Feedback Terms Components of Health Care Reform

kaiser medicaid commission on and the uninsured How Will Health Reform Impact Young Adults? By Karyn Schwartz and Tanya Schwartz Executive Summary

I S S U E P A P E R kaiser commission on medicaid and the uninsured How Will Health Reform Impact Young Adults? By Karyn Schwartz and Tanya Schwartz Executive Summary May 2010 The health reform law that

I S S U E P A P E R kaiser commission on medicaid and the uninsured How Will Health Reform Impact Young Adults? By Karyn Schwartz and Tanya Schwartz Executive Summary May 2010 The health reform law that

Chapter 1: What is the Affordable Care Act?

Chapter 1: What is the Affordable Care Act? The Affordable Care Act (ACA), also known as Obamacare, is a law that aims to help millions of Americans secure health insurance. Many individuals still are

Chapter 1: What is the Affordable Care Act? The Affordable Care Act (ACA), also known as Obamacare, is a law that aims to help millions of Americans secure health insurance. Many individuals still are

Looking for a Life Vest?

Looking for a Life Vest? November 20 th, 2014 @thomasharte Agenda: Looking for a Life Vest? Health Care Reform: What s new with ACA?? Provisions Already in Effect Preparing for Health Care Reform Primary

Looking for a Life Vest? November 20 th, 2014 @thomasharte Agenda: Looking for a Life Vest? Health Care Reform: What s new with ACA?? Provisions Already in Effect Preparing for Health Care Reform Primary

HCR FAQ. Covered California Individual and Family Coverage. What is Covered California? What is Obamacare? Are they the same?

HCR FAQ Covered California Individual and Family Coverage What is Covered California? What is Obamacare? Are they the same? Covered California is a new, easy-to-use marketplace established for California

HCR FAQ Covered California Individual and Family Coverage What is Covered California? What is Obamacare? Are they the same? Covered California is a new, easy-to-use marketplace established for California

The Affordable Care Act: Implementation in Illinois

The Affordable Care Act: Implementation in Illinois Stephanie F. Altman, J.D. Programs and Policy Director Health & Disability Advocates www.hdadvocates.org www.illinoishealthmatters.org November 2013

The Affordable Care Act: Implementation in Illinois Stephanie F. Altman, J.D. Programs and Policy Director Health & Disability Advocates www.hdadvocates.org www.illinoishealthmatters.org November 2013

Addressing Affordability of Health Insurance at the Local Level: San Francisco s Public Benefit Program. CHCF Webinar October 28, 2015

Addressing Affordability of Health Insurance at the Local Level: San Francisco s Public Benefit Program CHCF Webinar October 28, 2015 2 Agenda 10:00-10:05 Introductions Chris Perrone, CHCF 10:05-10:15

Addressing Affordability of Health Insurance at the Local Level: San Francisco s Public Benefit Program CHCF Webinar October 28, 2015 2 Agenda 10:00-10:05 Introductions Chris Perrone, CHCF 10:05-10:15

Washington Health Benefit Exchange

Washington Health Benefit Exchange HEALTHCARE REFORM SEMINAR November 25th, 2013 ACA INFORMATIONAL SESSION FOR SMALL BUSINESS OWNERS The Affordable Care Act Exchange Basics Today s Agenda Exchange Functions

Washington Health Benefit Exchange HEALTHCARE REFORM SEMINAR November 25th, 2013 ACA INFORMATIONAL SESSION FOR SMALL BUSINESS OWNERS The Affordable Care Act Exchange Basics Today s Agenda Exchange Functions

Insurance (Coverage) Reform

Reform") Arkansas Health Law Check Up Insurance (Coverage) Reform Create Insurance Marketplaces For individuals & small businesses Expand Medicaid to 138% FPL Arkansas alternative = Private Option, not Arkansas

Arkansas Health Law Check Up Insurance (Coverage) Reform Create Insurance Marketplaces For individuals & small businesses Expand Medicaid to 138% FPL Arkansas alternative = Private Option, not Arkansas

Overview of the Patient Protection and Affordable Care Act (ACA) Steven Abramson, Marketing Manager Community Health Alliance of Pasadena

Steven Abramson, Marketing Manager Community Health Alliance of Pasadena") Overview of the Patient Protection and Affordable Care Act (ACA) Steven Abramson, Marketing Manager Community Health Alliance of Pasadena What is the Patient Protection and Affordable Care Act (ACA)? When

Overview of the Patient Protection and Affordable Care Act (ACA) Steven Abramson, Marketing Manager Community Health Alliance of Pasadena What is the Patient Protection and Affordable Care Act (ACA)? When

The Affordable Care Act and Covered California. A Guide for Health Care Providers

The Affordable Care Act and Covered California A Guide for Health Care Providers Brought to you by Loma Linda University Institute for Health Policy and Leadership Newest Institute at LLUH To provide the

The Affordable Care Act and Covered California A Guide for Health Care Providers Brought to you by Loma Linda University Institute for Health Policy and Leadership Newest Institute at LLUH To provide the

Navajo County Schools EBT

Navajo County Schools EBT Affordable Care Act (ACA) Update Aaron Polkoski Segal Consulting January 31st, 2014 Copyright 2013 by The Segal Group, Inc., parent of The Segal Company. All rights reserved.

Navajo County Schools EBT Affordable Care Act (ACA) Update Aaron Polkoski Segal Consulting January 31st, 2014 Copyright 2013 by The Segal Group, Inc., parent of The Segal Company. All rights reserved.

Subsidized Health Coverage through MNsure

INFORMATION BRIEF Research Department Minnesota House of Representatives 600 State Office Building St. Paul, MN 55155 Randall Chun, Legislative Analyst 651-296-8639 Updated: October 2018 Subsidized Health

INFORMATION BRIEF Research Department Minnesota House of Representatives 600 State Office Building St. Paul, MN 55155 Randall Chun, Legislative Analyst 651-296-8639 Updated: October 2018 Subsidized Health

Health Care Reform. The Affordable Care Act

1 Health Care Reform The Affordable Care Act House Keeping items.. 1. All phone lines are muted so please send any questions you may have via the chat session during the webinar. 2. All slides will be

1 Health Care Reform The Affordable Care Act House Keeping items.. 1. All phone lines are muted so please send any questions you may have via the chat session during the webinar. 2. All slides will be

Understanding the Health Insurance Marketplace. August 2013

Understanding the Health Insurance Marketplace August 2013 Objectives This session will help you Explain the Health Insurance Marketplace Identify who will benefit Define who is eligible Explain the enrollment

Understanding the Health Insurance Marketplace August 2013 Objectives This session will help you Explain the Health Insurance Marketplace Identify who will benefit Define who is eligible Explain the enrollment

Affordable Care Act and Covered CA: Where We are One Year Later. Wonha Kim, MD, MPH, CPH, FAAP

Affordable Care Act and Covered CA: Where We are One Year Later Wonha Kim, MD, MPH, CPH, FAAP Senior Research Scholar, LLU Institute for Health Policy and Leadership Assistant Professor, Pediatrics, Preventive

Affordable Care Act and Covered CA: Where We are One Year Later Wonha Kim, MD, MPH, CPH, FAAP Senior Research Scholar, LLU Institute for Health Policy and Leadership Assistant Professor, Pediatrics, Preventive

Effects of the Affordable Health Care Act

Effects of the Affordable Health Care Act A Focus on Financial, Administrative and Plan Impacts February 27, 2013 Presented By J.W. Terrill Consulting Services Agenda Introduction: Patient Protection &

Effects of the Affordable Health Care Act A Focus on Financial, Administrative and Plan Impacts February 27, 2013 Presented By J.W. Terrill Consulting Services Agenda Introduction: Patient Protection &

Bringing Health Care Coverage Within Reach

Measuring the Financial Assistance Available through Covered California that is lowering the Cost of Coverage and Care Introduction The Affordable Care Act (ACA) helped cut the rate of the uninsured by

Measuring the Financial Assistance Available through Covered California that is lowering the Cost of Coverage and Care Introduction The Affordable Care Act (ACA) helped cut the rate of the uninsured by

Health Care Reform: The Financial Impact on the Employer

Health Care Reform: The Financial Impact on the Employer WP&BC August 15, 2012 1 1 Supreme Court Examines Constitutionality U.S. Supreme Court Ruling: June 28, 2012 Individual Mandate - Constitutional

Health Care Reform: The Financial Impact on the Employer WP&BC August 15, 2012 1 1 Supreme Court Examines Constitutionality U.S. Supreme Court Ruling: June 28, 2012 Individual Mandate - Constitutional

The Affordable Care Act (ACA)

") Life Guide The Affordable Care Act (ACA) The Affordable Care Act, or ACA, is the nation's health insurance reform law, initially enacted in March 2010 and being gradually phased in over a period of years.

Life Guide The Affordable Care Act (ACA) The Affordable Care Act, or ACA, is the nation's health insurance reform law, initially enacted in March 2010 and being gradually phased in over a period of years.

5/5/2014. The Affordable Care Act* 45 th Annual WMSHP Spring Seminar. The Affordable Care Act (ACA) March 23,2010

March 23,2010") The Affordable Care Act* 45 th Annual WMSHP Spring Seminar Richard Lichtenstein, PhD, MPH S.J. Axelrod Collegiate Professor of Health Management and Policy University of Michigan School of Public Health

The Affordable Care Act* 45 th Annual WMSHP Spring Seminar Richard Lichtenstein, PhD, MPH S.J. Axelrod Collegiate Professor of Health Management and Policy University of Michigan School of Public Health

HEALTH CONCEPTS AND TAX CONSIDERATIONS

14 HEALTH CONCEPTS AND TAX CONSIDERATIONS LEARNING OBJECTIVES Upon the completion of this chapter, you will be able to: 1. Recognize the features of health insurance policies that have been mandated by

14 HEALTH CONCEPTS AND TAX CONSIDERATIONS LEARNING OBJECTIVES Upon the completion of this chapter, you will be able to: 1. Recognize the features of health insurance policies that have been mandated by

The Affordable Care Act: How Will It Help the Uninsured?

The Affordable Care Act: How Will It Help the Uninsured? Kiwon Yoo Insure the Uninsured Project www.itup.org Chapman Law School Symposium October 19, 2012 Insure the Uninsured Project About Us ITUP is

The Affordable Care Act: How Will It Help the Uninsured? Kiwon Yoo Insure the Uninsured Project www.itup.org Chapman Law School Symposium October 19, 2012 Insure the Uninsured Project About Us ITUP is

The Affordable Care Act

The Affordable Care Act Employers Guide to 2015 and Beyond For Small Groups Summary Jan. 1, 2014, ushered in new Affordable Care Act (ACA) health insurance market reforms. These changes are impacting the

The Affordable Care Act Employers Guide to 2015 and Beyond For Small Groups Summary Jan. 1, 2014, ushered in new Affordable Care Act (ACA) health insurance market reforms. These changes are impacting the

THE AFFORDABLE CARE ACT AN OVERVIEW FOR HUMAN RESOURCE & FINANCE PROFESSIONALS AT MID-SIZED COMPANIES

THE AFFORDABLE CARE ACT AN OVERVIEW FOR HUMAN RESOURCE & FINANCE PROFESSIONALS AT MID-SIZED COMPANIES 1 Mid-Sized Retirement & Healthcare Plan Management Conference San Francisco, CA March 17, 2014 GOALS

THE AFFORDABLE CARE ACT AN OVERVIEW FOR HUMAN RESOURCE & FINANCE PROFESSIONALS AT MID-SIZED COMPANIES 1 Mid-Sized Retirement & Healthcare Plan Management Conference San Francisco, CA March 17, 2014 GOALS

AFFORDABLE CARE ACT FAQ

AFFORDABLE CARE ACT FAQ What is the Healthcare Insurance Marketplace? The Marketplace is a new way to find quality health coverage. It can help if you don t have coverage now or if you have it but want

AFFORDABLE CARE ACT FAQ What is the Healthcare Insurance Marketplace? The Marketplace is a new way to find quality health coverage. It can help if you don t have coverage now or if you have it but want

Covered California Training Webinar. September 23 rd, 2014

Covered California Training Webinar September 23 rd, 2014 What is the Affordable Care Act? The Patient Protection and Affordable Care Act, also known as the Affordable Care Act (ACA), was signed into law

Covered California Training Webinar September 23 rd, 2014 What is the Affordable Care Act? The Patient Protection and Affordable Care Act, also known as the Affordable Care Act (ACA), was signed into law

The Affordable Care Act (ACA) Health Insurance Exchanges

Health Insurance Exchanges") The Affordable Care Act (ACA) Health Insurance Exchanges Dave Chandra Senior Policy Analyst Center on Budget and Policy Priorities March 11, 2013 Linking Americans to Coverage (2014) FPL Unsubsidized 400%

The Affordable Care Act (ACA) Health Insurance Exchanges Dave Chandra Senior Policy Analyst Center on Budget and Policy Priorities March 11, 2013 Linking Americans to Coverage (2014) FPL Unsubsidized 400%

8/7/2013 INSURANCE MADE SIMPLE. 1

Presented by: Mark E. Baker Vice President Employee Benefits INSURANCE MADE SIMPLE. 1 Health Care Reform provisions in effect 2010-2012 Large Employer Defined Pay or Play Mandate and Penalties Small Employer

Presented by: Mark E. Baker Vice President Employee Benefits INSURANCE MADE SIMPLE. 1 Health Care Reform provisions in effect 2010-2012 Large Employer Defined Pay or Play Mandate and Penalties Small Employer

Monitoring the ACA s. Vital Signs. The Affordable Care Act A Progress Report

Monitoring the ACA s Vital Signs The Affordable Care Act A Progress Report Today s Discussion Affordable Care Act Some Foundational Knowledge Affordable Care Act Compliance Requirements Plan Design Reporting

Monitoring the ACA s Vital Signs The Affordable Care Act A Progress Report Today s Discussion Affordable Care Act Some Foundational Knowledge Affordable Care Act Compliance Requirements Plan Design Reporting

Presented by: Jim Gilbert Registered Health Underwriter & Registered Employee Benefits Consultant

Healthcare Reform Update 18 th Annual Update for Accountants Presented by: Jim Gilbert Registered Health Underwriter & Registered Employee Benefits Consultant Thursday, December 5 th, 2013 What is Health

Healthcare Reform Update 18 th Annual Update for Accountants Presented by: Jim Gilbert Registered Health Underwriter & Registered Employee Benefits Consultant Thursday, December 5 th, 2013 What is Health

California ARCA / MCA Health Care Reform Presentation

Mark Straus Dee Shaw Disclaimer: The ACA is constantly being revised and updated and the information contained in these slides was based on best information available to date. Atlanta Cleveland Los Angeles

Mark Straus Dee Shaw Disclaimer: The ACA is constantly being revised and updated and the information contained in these slides was based on best information available to date. Atlanta Cleveland Los Angeles

ACA & the Tax Season

ACA & the Tax Season Common Cents Tara Straw September 9, 2014 The ACA on the Tax Return 2 Reporting health coverage For every month For everyone on the return Exemptions from the individual responsibility

ACA & the Tax Season Common Cents Tara Straw September 9, 2014 The ACA on the Tax Return 2 Reporting health coverage For every month For everyone on the return Exemptions from the individual responsibility

Quantifying Tax Credits for People Now Buying Insurance on Their Own

issue brief Quantifying Tax Credits for People Now Buying Insurance on Their Own August 2013 A number of states have recently released information on what premiums will be in the individual insurance market

issue brief Quantifying Tax Credits for People Now Buying Insurance on Their Own August 2013 A number of states have recently released information on what premiums will be in the individual insurance market

Health Insurance Webinar Series: The Affordable Care Act Updates for 2017

Health Insurance Webinar Series: The Affordable Care Act Updates for 2017 What is the Affordable Care Act (ACA)? The Patient Protection and Affordable Care Act (PPACA) of 2010 or Affordable Care Act (ACA),

Health Insurance Webinar Series: The Affordable Care Act Updates for 2017 What is the Affordable Care Act (ACA)? The Patient Protection and Affordable Care Act (PPACA) of 2010 or Affordable Care Act (ACA),

Health Insurance Premium Tax Credits and Cost-Sharing Subsidies

Health Insurance Premium Tax Credits and Cost-Sharing Subsidies Bernadette Fernandez Specialist in Health Care Financing April 24, 2018 Congressional Research Service 7-5700 www.crs.gov R44425 Summary

Health Insurance Premium Tax Credits and Cost-Sharing Subsidies Bernadette Fernandez Specialist in Health Care Financing April 24, 2018 Congressional Research Service 7-5700 www.crs.gov R44425 Summary

STUDENTS GUIDE TO THE AFFORDABLE CARE ACT Grant Atkinson J.D, NAGPS Legal Concerns Chair, August 25, 2013

STUDENTS GUIDE TO THE AFFORDABLE CARE ACT Grant Atkinson J.D, NAGPS Legal Concerns Chair, August 25, 2013 What do students need to know about the the Affordable Care Act? THE BASICS: 1) It encourages you

STUDENTS GUIDE TO THE AFFORDABLE CARE ACT Grant Atkinson J.D, NAGPS Legal Concerns Chair, August 25, 2013 What do students need to know about the the Affordable Care Act? THE BASICS: 1) It encourages you

Summary of House Discussion Draft, February 10, 2017

Summary of House Discussion Draft, February 10, 2017 This summary describes key provisions of House Discussion Draft, dated February 10, 2017, reported in the media as a plan to repeal and replace the

Summary of House Discussion Draft, February 10, 2017 This summary describes key provisions of House Discussion Draft, dated February 10, 2017, reported in the media as a plan to repeal and replace the

AFFORDABLE CARE ACT (ACA)

") AFFORDABLE CARE ACT (ACA) Presented By ANDREW H. HOOK, CELA, CFP, AEP 295 Bendix Road, Suite 170, Virginia Beach, VA 23452 5806 Harbour View Blvd., Suite 203, Suffolk, VA 23435 Tel: 757-399-7506 Fax: 757-397-1267

AFFORDABLE CARE ACT (ACA) Presented By ANDREW H. HOOK, CELA, CFP, AEP 295 Bendix Road, Suite 170, Virginia Beach, VA 23452 5806 Harbour View Blvd., Suite 203, Suffolk, VA 23435 Tel: 757-399-7506 Fax: 757-397-1267

Overview of the Federal Affordable Care Act (ACA)

") Overview of the Federal Affordable Care Act (ACA) Catherine Teare, MPP Senior Program Officer Health Reform and Public Programs February 15, 2013 The Status Quo Health spending represents a growing share

Overview of the Federal Affordable Care Act (ACA) Catherine Teare, MPP Senior Program Officer Health Reform and Public Programs February 15, 2013 The Status Quo Health spending represents a growing share

THE PATIENT PROTECTION AND AFFORDABLE CARE ACT UPDATE

THE PATIENT PROTECTION AND AFFORDABLE CARE ACT UPDATE February 21, 2013 Jonathan Alexander, Esq. Compliance Counsel Pinnacle Claims Management, Inc. Copyright 2013 Pinnacle Claims Management, Inc. Reproduction

THE PATIENT PROTECTION AND AFFORDABLE CARE ACT UPDATE February 21, 2013 Jonathan Alexander, Esq. Compliance Counsel Pinnacle Claims Management, Inc. Copyright 2013 Pinnacle Claims Management, Inc. Reproduction

Overview of New Reform Law. Federal Healthcare Reform: Impacts on Employer-Sponsored Plans. Agenda

: Impacts on Employer-Sponsored Plans June 3, 2010 Employee Benefits Planning Association Jack McRae SVP, Congressional and Legislative Affairs Premera Blue Cross Jim Grazko VP and General Manager, Underwriting

: Impacts on Employer-Sponsored Plans June 3, 2010 Employee Benefits Planning Association Jack McRae SVP, Congressional and Legislative Affairs Premera Blue Cross Jim Grazko VP and General Manager, Underwriting