INDIVIDUAL SHARED RESPONSIBILITY PROVISION

|

|

|

- Amelia Byrd

- 5 years ago

- Views:

Transcription

1 UNIVERSAL HEALTHCARE COUNCIL 2013 The Affordable Care Act s (ACA) shared responsibility provisions fall on two groups: individuals and employers. INDIVIDUAL SHARED RESPONSIBILITY PROVISION Overview The Individual Shared Responsibility provision of the Affordable Care Act (ACA) (aka Individual Mandate), requires most U.S. residents to obtain health insurance that meets minimum essential coverage (MEC) guidelines or pay a penalty, beginning in Individuals Subject to the Mandate With some exceptions, individuals will be required to maintain minimum essential coverage for themselves and their dependents, per federal income tax guidelines. Certain individuals and their dependents are exempt from the individual mandate, including: Undocumented immigrants; Those for whom coverage is unaffordable (i.e., premiums exceed 8% of household income); Those who are very low income (i.e., household income is below the minimum threshold for filing a tax return); Those with a short coverage gap (i.e. without coverage for less than three consecutive months during the year, which may only be claimed once in a year); Jail and prison inmates; Those experiencing certain hardships (e.g., natural disaster, or significant, unexpected increase in essential expenses if the expense of complying with ACA would have caused deprivation of food, shelter, clothing or other necessities); Native Americans eligible for care through the Indian Health Care service; and Those with religious exemptions. 10/10/2013 Page 1

2 Complying with the Mandate Non-exempt individuals may choose to comply by participating in a health insurance plan that meets minimum essential coverage (MEC) guidelines or pay a penalty. Qualifying MEC is broadly defined and includes: Employer-sponsored coverage (including COBRA coverage and retiree coverage) Coverage purchased in the individual market, including a qualified health plan offered through Covered California Medicare Part A coverage and Medicare Advantage plans Most Medicaid coverage Children's Health Insurance Program (CHIP) coverage Certain types of veterans health coverage administered by the Veterans Administration TRICARE Coverage provided to Peace Corps volunteers Coverage under the Nonappropriated Fund Health Benefit Program Refugee Medical Assistance supported by the Administration for Children and Families Self-funded health coverage offered to students by universities for plan or policy years that begin on or before Dec. 31, 2014 (for later plan or policy years, sponsors of these programs may apply to HHS to be recognized as minimum essential coverage) State high risk pools for plan or policy years that begin on or before Dec. 31, 2014 (for later plan or policy years, sponsors of these program may apply to HHS to be recognized as minimum essential coverage) The individual shared responsibility provision goes into effect in An individual will not have to account for coverage or exemptions or to make any payments until the individual files their 2014 federal income tax return in Information is forthcoming via the IRS regarding how the income tax return will take account of coverage and exemptions. Insurers will be required to provide everyone that they cover each year with information that will help them demonstrate they had coverage beginning with the 2015 tax year. Excepted benefit plans, which offer only limited benefits (e.g., vision, dental, hospital, accident, Medicaid covering only certain benefits such as family planning, workers' compensation, or disability policies), do not qualify as minimum essential coverage, and, if this is the only coverage an individual obtains, would leave the individual subject to penalty. Potential Financial Assistance for Low Income Individuals ACA provides financial assistance to non-exempt individuals to help them meet the individual mandate. As of 2014, the lowest income California adults with incomes up to 133% FPL ($15,856 for a single individual; $26,951 for a family of three) will be 10/10/2013 Page 2

3 eligible for Medi-Cal (California s Medicaid program). Medi-Cal was previously available only to low-income children, seniors, people with disabilities, and families. California adopted the ACA option to extend Medi-Cal to all non-exempt adults. Also effective beginning in 2014, those with incomes above the Medi-Cal threshold up to 400% FPL ($45,960/individual; $78,120/family of three) will be eligible on a sliding scale basis for subsidies to help pay for the premiums and cost-sharing requirements of health plans offered through Covered California. While these subsidies do not cover the entire cost of health care faced by individuals and families, they help to defray the costs of purchasing insurance. The chart below shows the expanded health insurance eligibility options for low-income individuals. In its first week, Covered California received nearly one million hits to its website and fielded 59,000 calls, and determined 28,699 individuals eligible for health care coverage. As information regarding location of eligibility and enrollment and uptake rate become available, these data can be used to further inform projections of insured/uninsured in our area. 10/10/2013 Page 3

4 Penalties for Noncompliance Penalties for not complying with individual mandate will be assessed on individuals through their income tax returns. The annual penalties are as follows: YEAR After 2016 Flat Rate $95/adult $47.50/child $285 maximum/family $325/adult $162.50/child $975 maximum/family $695/adult $347.50/child $2,085 maximum/family PENALTY OR Percentage of Family Income 1 1% 2% 2.5% Increases annually by cost of living 2.5% The following chart from the Congressional Research Service shows how the penalties for noncompliance with the individual mandate would affect a family of four with incomes up to $125,000 (530% of FPL). 1 Family income is defined as total income in excess of the filing threshold ($10,000 for an individual and $20,000 for a family in /10/2013 Page 4

5 The penalty is pro-rated by the number of months without coverage, though there is no penalty for a single gap in coverage of less than three months in a year. The penalty cannot be greater than the national average premium for Bronze coverage in the exchange. The chart below, from the Kaiser Family Foundation, depicts the individual shared responsibility provisions of the ACA. 10/10/2013 Page 5

6 EMPLOYER SHARED RESPONSIBILITY PROVISION Overview The ACA does not explicitly mandate that employers offer their employees acceptable health insurance. However, it does provide tax benefits for certain small businesses that offer affordable health insurance coverage and imposes penalties on certain large employers that do not offer affordable health insurance coverage. Determining Employer Size The ACA counts full-time equivalent employees (FTEs) to determine business size. FTEs are calculated as follows: Full-time employees (working at least 30 hours per week in any month): Counted as one FTE. Part-time employees: Calculated by taking the hours worked by all part-time employees in a month and dividing that amount by 120. Seasonal: Not counted in the calculation for those working up to 120 days in a year. As an example, consider a business with 35 full-time employees (those who work 30 or more hours). Assume the firm also has 20 part-time employees who each work 24 hours per week (96 hours in a month). These part-time employees hours would be treated as equivalent to 16 full-time employees for the month, based on the following calculation: 20 employees x 96 hours/120 = 1920/120 = 16. Thus, in this example, the firm would be considered a large employer, based on a total FTE count of 51 that is, 35 full-time employees plus 16 FTEs based on the number of part-time hours worked. Small Employer Provisions Beginning in 2014, small businesses, defined as those with fewer than 50 full-time equivalent employees (FTEs), are eligible to purchase small group health plans through Covered California s Small Business Health Options Program (SHOP). Certain small businesses that purchase this coverage through SHOP will be eligible for a federal health care tax credit if they have fewer than 25 full-time-equivalent employees for the tax year, pay employees an average of less than $50,000 per year, and contribute at least 50 percent of their employees premium cost. Employers with 10 or fewer full-time-equivalent employees with wages averaging $25,000 or less per year are eligible for the maximum amount of tax credits. The tax credit employers receive will depend on a number of factors, including the 10/10/2013 Page 6

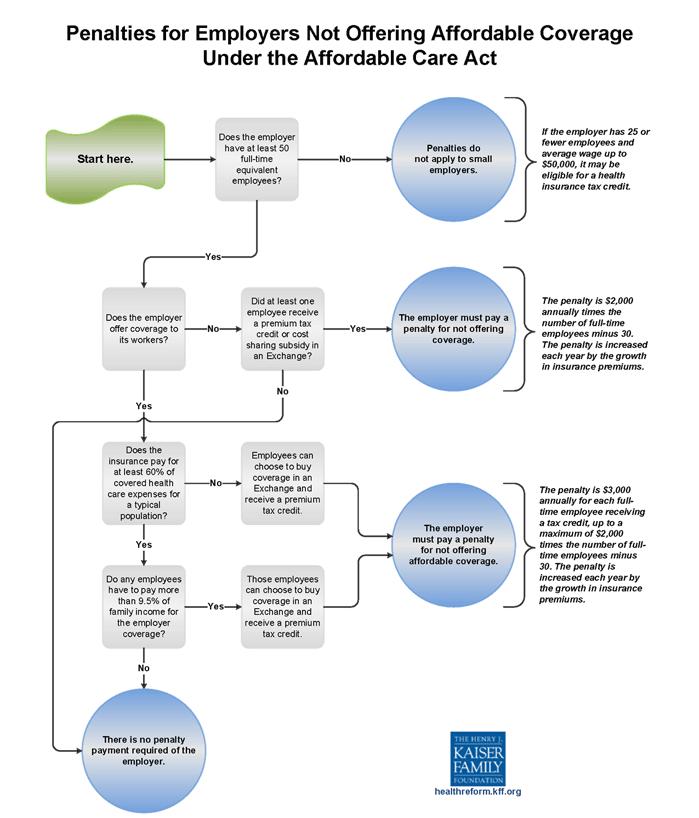

7 number of full-time-equivalent employees and the amount the employer contributes toward insurance premiums. The table below provides an overview: Small Business Tax Credits on Covered California Business Type Business Size Average FTE Salary Tax Credit For-profit <10 FTE <$25,000 For-profit < 25 FTE < $50,000 35% of employer Sliding scale, up to 35% of employer 50% of employer Sliding scale, up to 50% of employer Non-profit or Tax-Exempt <10 FTE < $25,000 25% of employer 35% of employer Non-profit or Tax-Exempt <25 FTE < $50,000 Sliding scale, up to 25% of employer Sliding scale, up to 35% of employer Tax credits are available for tax year 2013 and become more generous starting in Tax credits are available for a total of two consecutive years. SHOP health plans will be sold through licensed agents who are trained and certified by Covered California. Large Employer Provisions Large employers are defined as those with at least 50 FTEs. Beginning in 2015, a large employer may be subject to a penalty if it does not offer affordable health insurance to its employees and one or more of its full-time employees obtains a premium tax credit through Covered California. (An individual may be eligible for a premium tax credit if his or her income is below 400 percent of the federal poverty level and the individual s employer either does not offer health coverage, or offers insurance that is not affordable.) The ACA s guidelines for what qualifies as affordable insurance are as follows: The offered coverage must provide minimum value, meaning that the plan covers at least 60% of the beneficiary s health-related expenses. The employee s annual premiums for self-only coverage may not exceed 9.5% of the employee s household income If a large employer offers no coverage, then the penalty is equal to $2,000 multiplied by the number of full-time employees beyond the first /10/2013 Page 7

8 As an example, consider the large employer with the 51 FTEs, calculated in the example above. This employer had 35 full-time employees and 20 part-time. If this employer did not offer coverage, the penalty calculation would be as follows: 35 full-time employees first 30 full-time employees x $2,000 = 5 x $2,000 = $10,000. If a large employer offers unaffordable coverage then the penalty is the lesser of: $3,000 multiplied by the number of full-time employees receiving a subsidy, OR $2,000 multiplied by the number of full-time employees beyond the first 30. For this example, consider again the same 51 FTE employer with 35 full-time employees and 20 part-time employees. Assume for this example that three full-time employees received a subsidy on Covered California. This employer would be subject to a $9,000 penalty, which is the lesser of the following two calculations: 3 full-time employees receiving a subsidy x $3,000 = $9, full-time employees first 30 full-time employees x $2,000 = 5 x $2,000 = $10,000. The chart on the next page, from the Kaiser Family Foundation, depicts the penalties for employer noncompliance. 10/10/2013 Page 8

9 10/10/2013 Page 9

10 Duty to Notify All employers subject to the Fair Labor Standards Act (which prescribes standards for the basic minimum wage and overtime pay and affects most private and public employment) also have a duty to notify their employees about health insurance options available under the ACA, though there is no fine or penalty for noncompliance. These notices must be provided by October 1, 2013 and must: Provide a description of services provided by Covered California and Covered California contact information; Inform employees they could be eligible for federal tax credits if they purchase an insurance plan through the exchange; and Inform employees that if they purchase insurance through the exchange, they could lose the employer contribution to any health plan offered by the employer. INSURANCE AND EMPLOYMENT STATUS IN SF Unless otherwise stated the data below represent San Franciscans ages only. This age group represents those most likely to be uninsured and also those most likely to benefit under the provision of the ACA. The source of the citywide data is the U.S. Census Bureau s 2011 American Community Survey, which estimated approximately 588,200 San Franciscans ages 18-64, representing 73% of the total San Francisco population. Current Status Insurance Currently, the majority (72%) of San Franciscans have private health insurance, and 14% (~84,700) are uninsured. 10/10/2013 Page 10

are enrolled in coordinated health access programs for the uninsured operated by the")

11 Full-time v. Part-time Employment While most year olds work full-time year round, almost one third work part-time. Employment and Insurance Status Among those who are in the labor force, the large majority are employed and, among the employed, most have private health insurance. Rates of uninsurance are highest among the unemployed. Health Insurance Transitions Post ACA Implementation Of the 84,700 uninsured, 60,000 (71%) are enrolled in coordinated health access programs for the uninsured operated by the Department of Public Health (DPH). DPH s health access programs Healthy San Francisco and SF PATH provide a comprehensive array of health care services for low-income, uninsured San 10/10/2013 Page 11

12 Franciscans. The participation of nearly three quarters of San Francisco s uninsured in these programs provides DPH with a significant amount of information about the impact of the ACA in San Francisco. Transitions among Healthy San Francisco & SF PATH Participants As of January 1 st, 2014, 40,500 (67)% of the 60,000 uninsured San Franciscans enrolled in Healthy San Francisco and SF PATH will be eligible for ACA coverage. Of this population, 25,000 participants are expected to successfully enroll in coverage. Expected Transitions among Healthy San Francisco (HSF)/SF PATH Participants Who is eligible for insurance? What are they eligible for? Who will enroll? Transitions among Uninsured not Enrolled in Healthy San Francisco or SF PATH Among San Francisco s total uninsured are 24,700 persons not enrolled in Healthy San Francisco or SF PATH. As this group is not in the system, little is known about its health care related behavior. Based on demographic data on San Francisco from the American Community Survey, this population is more likely than the insured population to work part-time and earn less than $50,000 per year. Income data further indicates that 42 percent of this group is likely to qualify for Medi-Cal under 10/10/2013 Page 12

13 the ACA, although it is difficult to distinguish the newly eligible from those who were eligible before the ACA but did not enroll. Another 39 percent is likely to be eligible for subsidized coverage on the Exchange. However, these estimates do not reflect other ACA eligibility criteria, such as citizenship status. Residually Uninsured The ACA does not extend insurance to everyone. Not everyone will not be eligible for new options available under the ACA (e.g., the undocumented) and some will be eligible but will not enroll for any number of reasons (e.g., coverage is unaffordable, they are unaware of their options, cultural or linguistic barriers, they choose the penalty over the coverage). As a result of its experience with the Healthy San Francisco Program, DPH identified the following populations as having large number of uninsured people who would be most in need of intensive outreach and education to successfully convince them to enroll in an insurance plan: Residents of San Francisco s Southeast sector; Latino adults in the Mission District and other bordering communities with a high concentration of Latino families; Asian Americans, with a primary focus on Chinese Americans and Samoan and Pacific Islander communities; Small businesses, including sole proprietors and employees of small businesses (those with under 20 employees) in the manufacturing, retail, and service industries; and Young people who are years old. The following table illustrates the total number of all San Franciscans remaining potentially uninsured after full ACA implementation (likely 2019), using the current number of uninsured and different insurance uptake scenarios among eligible populations. The applied uptake rates come from the UC Berkeley CalSIM model, and reflect a number of factors including income, eligibility for Medi-Cal or subsidies, and whether or not the person has had previous offers of insurance. Generally, uptake rates decrease as income increases and with previous decisions not to enroll in coverage. For example, those who are eligible for exchange subsidies ( % of FPL) are more likely to enroll than those who do not (400% FPL +). The small range of the residually uninsured estimates (from 58-63%) reflects the large number of persons estimated to be ineligible for ACA coverage, as well as the fact that a majority of the eligible are expected to qualify for Medi-Cal or exchange subsidies. 10/10/2013 Page 13

14 Healthy San Francisco Uninsured + non-healthy San Francisco Uninsured Total Residually Uninsured Estimates Insurance Uptake Scenario Among Non-HSF Uninsured Population Low Mid High Total Eligible for ACA 58,722 58,722 58,722 Eligible--Expected to Enroll 31,395 33,607 35,362 Eligible--Likely not to Enroll 27,327 25,115 23,360 Total Ineligible 25,975 25,975 25,975 # of all San Franciscans Residually Uninsured (Ineligible + Eligible Likely not to Enroll) 53,302 51,090 49,335 Residually Uninsured as % of Total Uninsured 63% 60% 58% Residually Uninsured as % of San Francisco Population aged % 8.7% 8.4% FOR CONSIDERATION/DISCUSSION Populations Not Covered by ACA ACA represents comprehensive reform and will expand health insurance to millions of Americans, yet some populations are not included in the health insurance expansions offered under the ACA. These populations include: Individuals exempt from the individual mandate, including undocumented immigrants; Individuals working fewer than 30 hours per week for a single employer; Small business employees; and Working individuals earning low wages for whom even the established affordability thresholds are high. Hard to Reach Populations Several populations within San Francisco are more likely to be uninsured and hard to reach. These are the 15,500 current Healthy San Francisco enrollees who are expected not to transition to health insurance even though they are eligible and the 24,700 uninsured that not currently enrolled in these programs. Among the barriers to enrollment these populations may face is affordability, which will be discussed in a future UHC meeting. In San Francisco, these populations include: Residents of the Southeast sector; 10/10/2013 Page 14

15 Latino adults; Asian Americans; Employees of certain industries or sectors that may have a higher number of undocumented or part-time employees. Small business owners; and Young people ages Residually Uninsured The estimate and make-up of the residually uninsured (both those who are ineligible for insurance and those who are eligible but do not enroll) is important to understand as local programs may transform to fit the needs of this population. An additional factor in this conversation is the city s obligation under Section of the California Health & Welfare Code Section 17000, which requires that [e]very county and every city and county shall relieve and support all incompetent, poor, indigent persons, and those incapacitated by age, disease, or accident, lawfully resident therein, when such persons are not supported and relieved by their relatives or friends, by their own means, or by state hospitals or other state or private institutions. This has been interpreted to apply to essential health services, which in San Francisco have been provided by the Department of Public Health in several ways, including charity care, sliding fee scale for health care services, and Healthy San Francisco. 10/10/2013 Page 15

UNIVERSAL HEALTHCARE COUNCIL 2013 OVERVIEW OF THE AFFORDABLE CARE ACT

UNIVERSAL HEALTHCARE COUNCIL 2013 OVERVIEW OF THE AFFORDABLE CARE ACT Introduction The Patient Protection and Affordable Care Act (ACA) was signed into federal law on March 23, 2010. While many reforms

UNIVERSAL HEALTHCARE COUNCIL 2013 OVERVIEW OF THE AFFORDABLE CARE ACT Introduction The Patient Protection and Affordable Care Act (ACA) was signed into federal law on March 23, 2010. While many reforms

The Affordable Care Act and the Income Tax. By Greg Martinez December 2013

The Affordable Care Act and the Income Tax By Greg Martinez December 2013 Overview Health insurance mandate Individual Shared Responsibility Provision Exemptions Minimum essential coverage Penalties Covered

The Affordable Care Act and the Income Tax By Greg Martinez December 2013 Overview Health insurance mandate Individual Shared Responsibility Provision Exemptions Minimum essential coverage Penalties Covered

The Individual Mandate

The Individual Mandate 2013 Zywave, Inc. All rights reserved. Presented by Johnson, Kendall & Johnson Benefits, Inc. What is Health Care Reform? The Affordable Care Act (ACA) was enacted in March 2010.

The Individual Mandate 2013 Zywave, Inc. All rights reserved. Presented by Johnson, Kendall & Johnson Benefits, Inc. What is Health Care Reform? The Affordable Care Act (ACA) was enacted in March 2010.

FACTS ABOUT THE ACA INDIVIDUAL MANDATE

FACTS ABOUT THE ACA INDIVIDUAL MANDATE Beginning 2014, every U.S. citizen and resident alien must have health insurance (minimum essential coverage). Failure to do so will result in a penalty (an additional

FACTS ABOUT THE ACA INDIVIDUAL MANDATE Beginning 2014, every U.S. citizen and resident alien must have health insurance (minimum essential coverage). Failure to do so will result in a penalty (an additional

2014 AFFORDABLE CARE ACT (OBAMA CARE)

") 2014 AFFORDABLE CARE ACT (OBAMA CARE) Planning for 2014 Tax Return Filings O Beginning 2014, the ACA requires all persons be covered by health insurance O Individuals not covered by Medicare, their employers,

2014 AFFORDABLE CARE ACT (OBAMA CARE) Planning for 2014 Tax Return Filings O Beginning 2014, the ACA requires all persons be covered by health insurance O Individuals not covered by Medicare, their employers,

GENERAL INFORMATION BULLETIN

AFL-CIO California School Employees Association GENERAL INFORMATION BULLETIN March 15, 2013 General Information Bulletin No. 17 13 AFFORDABLE CARE ACT (ACA) QUESTION & ANSWER RESOURCE DOCUMENT Action for

AFL-CIO California School Employees Association GENERAL INFORMATION BULLETIN March 15, 2013 General Information Bulletin No. 17 13 AFFORDABLE CARE ACT (ACA) QUESTION & ANSWER RESOURCE DOCUMENT Action for

ACA & the Tax Season

ACA & the Tax Season Common Cents Tara Straw September 9, 2014 The ACA on the Tax Return 2 Reporting health coverage For every month For everyone on the return Exemptions from the individual responsibility

ACA & the Tax Season Common Cents Tara Straw September 9, 2014 The ACA on the Tax Return 2 Reporting health coverage For every month For everyone on the return Exemptions from the individual responsibility

Compliance Alert. ACA Mandates Different Measures of Affordability

Compliance Alert ACA Mandates Different Measures of Affordability August 29, 2014 Quick Facts: Several Affordable Care Act (ACA) provisions measure the affordability of employersponsored health coverage.

Compliance Alert ACA Mandates Different Measures of Affordability August 29, 2014 Quick Facts: Several Affordable Care Act (ACA) provisions measure the affordability of employersponsored health coverage.

Sales Division Webinar #9

Disclaimer: The information contained in this presentation is a brief overview and should not be construed as tax advice or exhausted coverage of the topic. 1 Sales Division Webinar #9 ALL SERVICE CHANNELS

Disclaimer: The information contained in this presentation is a brief overview and should not be construed as tax advice or exhausted coverage of the topic. 1 Sales Division Webinar #9 ALL SERVICE CHANNELS

Questions and Answers on the. Individual Shared Responsibility Provision. January 30, 2013

Questions and Answers on the Individual Shared Responsibility Provision January 30, 2013 Basic Information 1. What is the individual shared responsibility provision? Under the Affordable Care Act, the

Questions and Answers on the Individual Shared Responsibility Provision January 30, 2013 Basic Information 1. What is the individual shared responsibility provision? Under the Affordable Care Act, the

Basic Information 1. What is the individual shared responsibility provision?

Affordable Care Act Topics Individuals and Families Employers Other Organizations For Tax Pros What's Trending News Health Care Tax Tips Questions and Answers Legal Guidance and Other Resources Affordable

Affordable Care Act Topics Individuals and Families Employers Other Organizations For Tax Pros What's Trending News Health Care Tax Tips Questions and Answers Legal Guidance and Other Resources Affordable

FINANCIAL CONSIDERATIONS FOR INDIVIDUALS, EMPLOYERS, AND THE LOCAL PUBLIC HEALTH SYSTEM

UNIVERSAL HEALTHCARE COUNCIL 2013 FINANCIAL CONSIDERATIONS FOR INDIVIDUALS, EMPLOYERS, AND THE LOCAL PUBLIC HEALTH SYSTEM As San Francisco moves forward with Health Reform, cost considerations will play

UNIVERSAL HEALTHCARE COUNCIL 2013 FINANCIAL CONSIDERATIONS FOR INDIVIDUALS, EMPLOYERS, AND THE LOCAL PUBLIC HEALTH SYSTEM As San Francisco moves forward with Health Reform, cost considerations will play

Key Medicaid, CHIP, and Low-Income Provisions in the Senate Bill Patient Protection and Affordable Care Act (Released November 18, 2009)

") Key Medicaid, CHIP, and Low-Income Provisions in the Senate Bill Patient Protection and Affordable Care Act (Released November 18, 2009) On November 18, 2009, the Senate released its health care reform

Key Medicaid, CHIP, and Low-Income Provisions in the Senate Bill Patient Protection and Affordable Care Act (Released November 18, 2009) On November 18, 2009, the Senate released its health care reform

Health Care Reform under the Patient Protection and Affordable Care Act ( PPACA ) provisions effective January 1, 2014

provisions effective January 1, 2014") The New Health Care Landscape Today s Agenda Health Care Reform under the Patient Protection and Affordable Care Act ( PPACA ) provisions effective January 1, 2014 Exchanges and Qualified Health Plans

The New Health Care Landscape Today s Agenda Health Care Reform under the Patient Protection and Affordable Care Act ( PPACA ) provisions effective January 1, 2014 Exchanges and Qualified Health Plans

OVERVIEW OF THE AFFORDABLE CARE ACT. September 23, 2013

OVERVIEW OF THE AFFORDABLE CARE ACT September 23, 2013 Outline The New Continuum of Coverage Medicaid and CHIP Are Changing The New Marketplaces Insurance Affordability Programs Shared Responsibility Requirement

OVERVIEW OF THE AFFORDABLE CARE ACT September 23, 2013 Outline The New Continuum of Coverage Medicaid and CHIP Are Changing The New Marketplaces Insurance Affordability Programs Shared Responsibility Requirement

The Affordable Care Act: Information for Wyoming Consumers

The Affordable Care Act: Information for Wyoming Consumers The Wyoming Department of Insurance The Affordable Care Act is a federally-mandated health care and health insurance law. Wyoming citizens and

The Affordable Care Act: Information for Wyoming Consumers The Wyoming Department of Insurance The Affordable Care Act is a federally-mandated health care and health insurance law. Wyoming citizens and

AFFORDABLE CARE ACT INTRODUCTION CAUTION!

AFFORDABLE CARE ACT INTRODUCTION Last summer, the United States Supreme Court upheld the constitutionality of the Affordable Care Act (ACA) removing most of the constitutional issues surrounding health

AFFORDABLE CARE ACT INTRODUCTION Last summer, the United States Supreme Court upheld the constitutionality of the Affordable Care Act (ACA) removing most of the constitutional issues surrounding health

Tennessee Public Health Association. Overview of the Affordable Care Act

Tennessee Public Health Association Overview of the Affordable Care Act Susie Baird Director of Policy Health Care Finance and Administration September 12, 2013 1 Origins of ACA Signed into law on March

Tennessee Public Health Association Overview of the Affordable Care Act Susie Baird Director of Policy Health Care Finance and Administration September 12, 2013 1 Origins of ACA Signed into law on March

Pay or Play Employer Shared Responsibility Penalties

Brought to you by Biggs Insurance Services Pay or Play Employer Shared Responsibility Penalties The Affordable Care Act (ACA) requires certain large employers to offer affordable, minimum value health

Brought to you by Biggs Insurance Services Pay or Play Employer Shared Responsibility Penalties The Affordable Care Act (ACA) requires certain large employers to offer affordable, minimum value health

Presenters Marc J. Smith Mary-Michal Rawling

Presenters Marc J. Smith Mary-Michal Rawling The Affordable Care Act (ACA) Starting in January 1, 2014 it will be Required that most U.S. citizens and legal residents obtain and maintain healthcare coverage

Presenters Marc J. Smith Mary-Michal Rawling The Affordable Care Act (ACA) Starting in January 1, 2014 it will be Required that most U.S. citizens and legal residents obtain and maintain healthcare coverage

What is the Employer s responsibility? Basically, eligible employers must offer affordable coverage to all eligible employees Or pay a penalty.

Guide to the PPACA What is the Employer s responsibility? Basically, eligible employers must offer affordable coverage to all eligible employees Or pay a penalty. Eligible Employers Companies with more

Guide to the PPACA What is the Employer s responsibility? Basically, eligible employers must offer affordable coverage to all eligible employees Or pay a penalty. Eligible Employers Companies with more

The New Responsibility to Secure Coverage: Frequently Asked Questions

The New Responsibility to Secure Coverage: Frequently Asked Questions Introduction The Patient Protection and Affordable Care Act (PPACA) includes a much-discussed requirement that people secure health

The New Responsibility to Secure Coverage: Frequently Asked Questions Introduction The Patient Protection and Affordable Care Act (PPACA) includes a much-discussed requirement that people secure health

Health Care Reform Update. April 2013

Health Care Reform Update April 2013 2013 Compliance Issues Summary of Benefits and Coverage Simple explanation of benefits and costs 4 double sided pages, 12 point or larger font Can provide in paper

Health Care Reform Update April 2013 2013 Compliance Issues Summary of Benefits and Coverage Simple explanation of benefits and costs 4 double sided pages, 12 point or larger font Can provide in paper

Pay or Play Employer Shared Responsibility Penalties

Brought to you by Olson Insurance Pay or Play Employer Shared Responsibility Penalties The Affordable Care Act (ACA) requires applicable large employers (ALEs) to offer affordable, minimum value health

Brought to you by Olson Insurance Pay or Play Employer Shared Responsibility Penalties The Affordable Care Act (ACA) requires applicable large employers (ALEs) to offer affordable, minimum value health

The Affordable Care Act: A Summary on Healthcare Reform. The Wyoming Department of Insurance

The Affordable Care Act: A Summary on Healthcare Reform The Wyoming Department of Insurance Additional Resources Wyoming Insurance Department: http://doi.wyo.gov/ or toll free at 1-(800)-438-5768 Information

The Affordable Care Act: A Summary on Healthcare Reform The Wyoming Department of Insurance Additional Resources Wyoming Insurance Department: http://doi.wyo.gov/ or toll free at 1-(800)-438-5768 Information

HEALTH CARE REFORM 2010 A CHRONOLOGICAL OVERVIEW OF THE LAW'S OBLIGATIONS FOR EMPLOYERS. Henry Smith. Smith & Downey.

HEALTH CARE REFORM 2010 A CHRONOLOGICAL OVERVIEW OF THE LAW'S OBLIGATIONS FOR EMPLOYERS Henry Smith Smith & Downey hsmith@smithdowney.com 410-321-9350 [Note that this presentation is merely a very broad

HEALTH CARE REFORM 2010 A CHRONOLOGICAL OVERVIEW OF THE LAW'S OBLIGATIONS FOR EMPLOYERS Henry Smith Smith & Downey hsmith@smithdowney.com 410-321-9350 [Note that this presentation is merely a very broad

Revisiting the Affordable Care Act

Revisiting the Affordable Care Act Mona Cole Outreach and Sales Distribution Analyst Covered California Nicholas Lujan Outreach and Sales Distribution Analyst Covered California Cristina Collazo Senior

Revisiting the Affordable Care Act Mona Cole Outreach and Sales Distribution Analyst Covered California Nicholas Lujan Outreach and Sales Distribution Analyst Covered California Cristina Collazo Senior

Health care reform update

Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently owned and managed member of Baker Tilly International. Health care reform update Agenda > Recent updates for 2014 and beyond > Individual

Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently owned and managed member of Baker Tilly International. Health care reform update Agenda > Recent updates for 2014 and beyond > Individual

2014 TAX UPDATE RACHELLE R. STYLES, CPA, MACC

2014 TAX UPDATE RACHELLE R. STYLES, CPA, MACC LEARNING OBJECTIVES Gain an understanding of the impact of health reform to the tax system Take a look at this year s Dirty Dozen tax scams presented by the

2014 TAX UPDATE RACHELLE R. STYLES, CPA, MACC LEARNING OBJECTIVES Gain an understanding of the impact of health reform to the tax system Take a look at this year s Dirty Dozen tax scams presented by the

Marketplace 101. Find health care options that meet your needs and fit your budget

Marketplace 101 Find health care options that meet your needs and fit your budget Objectives This session will help you Explain the Health Insurance Marketplace Define who might be eligible Define options

Marketplace 101 Find health care options that meet your needs and fit your budget Objectives This session will help you Explain the Health Insurance Marketplace Define who might be eligible Define options

Open Enrollment is here!

Navigating the Federal Marketplace AFFORDABLE CARE Open Enrollment is here! Reminders On November 20 at 9:30 AM ET, IPHCA is hosting a call with Matt Cesnik from FSSA again. CMS has released guidance on

Navigating the Federal Marketplace AFFORDABLE CARE Open Enrollment is here! Reminders On November 20 at 9:30 AM ET, IPHCA is hosting a call with Matt Cesnik from FSSA again. CMS has released guidance on

Navigating the New Health Care Law

Navigating the New Health Care Law For Sole Proprietors and Small Businesses (50 employees or less) This presentation is intended for educational purposes only and not intended as a legal, tax, or insurance

Navigating the New Health Care Law For Sole Proprietors and Small Businesses (50 employees or less) This presentation is intended for educational purposes only and not intended as a legal, tax, or insurance

VITA/TCE Basic Certification Topics on Affordable Care Act

VITA/TCE Basic Certification Topics on Affordable Care Act What does the ACA require? 2 or or Coverage Exemption SRP Everyone has a Shared Responsibility Individuals Purchase coverage, - Claim an exemption,

VITA/TCE Basic Certification Topics on Affordable Care Act What does the ACA require? 2 or or Coverage Exemption SRP Everyone has a Shared Responsibility Individuals Purchase coverage, - Claim an exemption,

THE AFFORDABLE CARE ACT...2

Table of Contents THE AFFORDABLE CARE ACT...2 Health Insurance Marketplace (Exchange)...3 Metallic Levels...4 Catastrophic Plans...4 Individual Mandate...5 Subsidies...5 Open Enrollment Period...6 Special

Table of Contents THE AFFORDABLE CARE ACT...2 Health Insurance Marketplace (Exchange)...3 Metallic Levels...4 Catastrophic Plans...4 Individual Mandate...5 Subsidies...5 Open Enrollment Period...6 Special

Navajo County Schools EBT

Navajo County Schools EBT Affordable Care Act (ACA) Update Aaron Polkoski Segal Consulting January 31st, 2014 Copyright 2013 by The Segal Group, Inc., parent of The Segal Company. All rights reserved.

Navajo County Schools EBT Affordable Care Act (ACA) Update Aaron Polkoski Segal Consulting January 31st, 2014 Copyright 2013 by The Segal Group, Inc., parent of The Segal Company. All rights reserved.

AFFORDABLE CARE ACT SURVIVAL KIT

AFFORDABLE CARE ACT SURVIVAL KIT This tool was developed to help VITA/TCE volunteers understand the ACA-related tax provisions and how to complete a return in TaxWise. Approaching the ACA Ask each person

AFFORDABLE CARE ACT SURVIVAL KIT This tool was developed to help VITA/TCE volunteers understand the ACA-related tax provisions and how to complete a return in TaxWise. Approaching the ACA Ask each person

Health Insurance Marketplace

Health Insurance Marketplace Briefing on the Affordable Care Act 2014 Ben J. Altheimer Oral Symposium UALR Bowen School of Law February 28, 2014 David Nilasena, MD Centers for Medicare & Medicaid Services

Health Insurance Marketplace Briefing on the Affordable Care Act 2014 Ben J. Altheimer Oral Symposium UALR Bowen School of Law February 28, 2014 David Nilasena, MD Centers for Medicare & Medicaid Services

HCR FAQ. Covered California Individual and Family Coverage. What is Covered California? What is Obamacare? Are they the same?

HCR FAQ Covered California Individual and Family Coverage What is Covered California? What is Obamacare? Are they the same? Covered California is a new, easy-to-use marketplace established for California

HCR FAQ Covered California Individual and Family Coverage What is Covered California? What is Obamacare? Are they the same? Covered California is a new, easy-to-use marketplace established for California

HCR Support Specialist Training Module II

HCR Support Specialist Training Module II The ACA and the Individual Market Your Trainer Today: Constance Starkey Individual Mandate What is the mandate? What are the exceptions? What is the penalty for

HCR Support Specialist Training Module II The ACA and the Individual Market Your Trainer Today: Constance Starkey Individual Mandate What is the mandate? What are the exceptions? What is the penalty for

MARKET STABILITY WORKGROUP 2.0. Tuesday, November 13, :30 10:30 a.m. The United Way of Rhode Island

MARKET STABILITY WORKGROUP 2.0 Tuesday, November 13, 2018 8:30 10:30 a.m. The United Way of Rhode Island 1 UPDATES SINCE OUR LAST MEETING Meeting 3 Follow-ups: 1332 Guidance HRA rule Brief overview of

MARKET STABILITY WORKGROUP 2.0 Tuesday, November 13, 2018 8:30 10:30 a.m. The United Way of Rhode Island 1 UPDATES SINCE OUR LAST MEETING Meeting 3 Follow-ups: 1332 Guidance HRA rule Brief overview of

VITA/TCE Basic Certification Topics on Affordable Care Act. Current as of November 20, 2017

VITA/TCE Basic Certification Topics on Affordable Care Act Current as of November 20, 2017 MEC & SRP REFRESHER What does the ACA require? 3 or or Coverage Exemption SRP Minimum Essential Coverage (MEC)

VITA/TCE Basic Certification Topics on Affordable Care Act Current as of November 20, 2017 MEC & SRP REFRESHER What does the ACA require? 3 or or Coverage Exemption SRP Minimum Essential Coverage (MEC)

VITA Training. Affordable Care Act (ACA)

") VITA Training Affordable Care Act (ACA) Does everyone really have to get health insurance? Yes. A new health care law says that health insurance will be required starting January 1, 2014. That means everyone

VITA Training Affordable Care Act (ACA) Does everyone really have to get health insurance? Yes. A new health care law says that health insurance will be required starting January 1, 2014. That means everyone

Washington Health Benefit Exchange

Washington Health Benefit Exchange AFFORDABLE CARE ACT 101 APRIL 26, 2013 Christine Brown Navigator/In-person Assister Program Today s Agenda History of the Affordable Care Act (ACA) Highlights of the

Washington Health Benefit Exchange AFFORDABLE CARE ACT 101 APRIL 26, 2013 Christine Brown Navigator/In-person Assister Program Today s Agenda History of the Affordable Care Act (ACA) Highlights of the

AFFORDABLE CARE ACT (ACA)

") AFFORDABLE CARE ACT (ACA) Presented By ANDREW H. HOOK, CELA, CFP, AEP 295 Bendix Road, Suite 170, Virginia Beach, VA 23452 5806 Harbour View Blvd., Suite 203, Suffolk, VA 23435 Tel: 757-399-7506 Fax: 757-397-1267

AFFORDABLE CARE ACT (ACA) Presented By ANDREW H. HOOK, CELA, CFP, AEP 295 Bendix Road, Suite 170, Virginia Beach, VA 23452 5806 Harbour View Blvd., Suite 203, Suffolk, VA 23435 Tel: 757-399-7506 Fax: 757-397-1267

Health Care Reform Under the ACA Its Effect on Municipalities and Their Employees

Health Care Reform Under the ACA Its Effect on Municipalities and Their Employees Maine Municipal Employees Health Trust 1-800-852-8300 www.mmeht.org The Difference Is Trust August 2014 1 Today s Agenda

Health Care Reform Under the ACA Its Effect on Municipalities and Their Employees Maine Municipal Employees Health Trust 1-800-852-8300 www.mmeht.org The Difference Is Trust August 2014 1 Today s Agenda

How Minimum Is Your Health Insurance Coverage? IRS Proposes Regulations on Offering and Maintaining Minimum Essential Coverage Starting in 2014

How Minimum Is Your Health Insurance Coverage? IRS Proposes Regulations on Offering and Maintaining Minimum Essential Coverage Starting in 2014 February 2013 Proposed regulations issued by the Treasury

How Minimum Is Your Health Insurance Coverage? IRS Proposes Regulations on Offering and Maintaining Minimum Essential Coverage Starting in 2014 February 2013 Proposed regulations issued by the Treasury

Health Care Reform 2013 Update. Presented by Rachel Cutler Shim

Health Care Reform 2013 Update Presented by Rachel Cutler Shim 2 Agenda Health Care Reform in 2013 and Beyond 2012 Preventive Care for Women Form W-2 Reporting Summary of Benefits and Coverage 2013 Health

Health Care Reform 2013 Update Presented by Rachel Cutler Shim 2 Agenda Health Care Reform in 2013 and Beyond 2012 Preventive Care for Women Form W-2 Reporting Summary of Benefits and Coverage 2013 Health

Affordable Care Act Update

Affordable Care Act Update CLAconnect.com May 19, 2015 Presented by: Anita Baker Session Objectives Identify key definitions impacting employer implementation of the Affordable Care Act Understand the

Affordable Care Act Update CLAconnect.com May 19, 2015 Presented by: Anita Baker Session Objectives Identify key definitions impacting employer implementation of the Affordable Care Act Understand the

HEALTH CARE REFORM: EMPLOYER SHARED RESPONSIBILITY RULES

HEALTH CARE REFORM: EMPLOYER SHARED RESPONSIBILITY RULES The Affordable Care Act (ACA) requires applicable large employers (ALEs) to offer affordable, minimum value health coverage to their full-time employees

HEALTH CARE REFORM: EMPLOYER SHARED RESPONSIBILITY RULES The Affordable Care Act (ACA) requires applicable large employers (ALEs) to offer affordable, minimum value health coverage to their full-time employees

T R U S T E D A D V I S O R S. Providing Outstanding Client Service Boston /Cambridge/Newport / Providence / Waltham

T R U S T E D A D V I S O R S Providing Outstanding Client Service Boston /Cambridge/Newport / Providence / Waltham www.kahnlitwin.com Health Care Reform Overview Applicable Large Employer Determination

T R U S T E D A D V I S O R S Providing Outstanding Client Service Boston /Cambridge/Newport / Providence / Waltham www.kahnlitwin.com Health Care Reform Overview Applicable Large Employer Determination

President Obama speaks about the Affordable Care Act at the White House on May 10.

POLITICAL LANDSCAPE Washington s political dynamic is fractured House actions are tempered by conservative pressure and tight Democratic majority in the Senate and President Obama GOP is struggling with

POLITICAL LANDSCAPE Washington s political dynamic is fractured House actions are tempered by conservative pressure and tight Democratic majority in the Senate and President Obama GOP is struggling with

THE AFFORDABLE CARE ACT Frequently Asked Questions

THE AFFORDABLE CARE ACT Frequently Asked Questions We are providing basic information on the ACA in order for you to best prepare for your tax appointment. While we strive to give you complete and accurate

THE AFFORDABLE CARE ACT Frequently Asked Questions We are providing basic information on the ACA in order for you to best prepare for your tax appointment. While we strive to give you complete and accurate

Frequently Asked Questions about Health Care Reform and the Affordable Care Act

Frequently Asked Questions about Health Care Reform and the Affordable Care Act HEALTH CARE REFORM OVERVIEW Q 1: What ACA changes are already in place? There are no lifetime dollar limits on essential

Frequently Asked Questions about Health Care Reform and the Affordable Care Act HEALTH CARE REFORM OVERVIEW Q 1: What ACA changes are already in place? There are no lifetime dollar limits on essential

Bringing Health Care Coverage Within Reach

Measuring the Financial Assistance Available through Covered California that is lowering the Cost of Coverage and Care Introduction The Affordable Care Act (ACA) helped cut the rate of the uninsured by

Measuring the Financial Assistance Available through Covered California that is lowering the Cost of Coverage and Care Introduction The Affordable Care Act (ACA) helped cut the rate of the uninsured by

Beyond the Basics of Exemptions and Special Enrollment Periods

Beyond the Basics of Exemptions and Special Enrollment Periods Center on Budget and Policy Priorities March 26, 2014 2 Part I: SPECIAL ENROLLMENT PERIODS 3 Open Enrollment Annual Period When All Eligible

Beyond the Basics of Exemptions and Special Enrollment Periods Center on Budget and Policy Priorities March 26, 2014 2 Part I: SPECIAL ENROLLMENT PERIODS 3 Open Enrollment Annual Period When All Eligible

The Patient Protection and Affordable Care Act in Colorado

The Patient Protection and Affordable Care Act in Colorado Colorado Center on Law and Policy 789 Sherman St., Suite 300, Denver, CO 80203 303-573-5669 September 20, 2013 The Problem 50 million uninsured

The Patient Protection and Affordable Care Act in Colorado Colorado Center on Law and Policy 789 Sherman St., Suite 300, Denver, CO 80203 303-573-5669 September 20, 2013 The Problem 50 million uninsured

Affordable Care Act: Impact on the Indiana Market

1 Affordable Care Act: Impact on the Indiana Market Seema Verma President SVC, Inc 2 Affordable Care Act Key accomplishment is access ~48.6 million uninsured in America* ~800 thousand uninsured in Indiana*

1 Affordable Care Act: Impact on the Indiana Market Seema Verma President SVC, Inc 2 Affordable Care Act Key accomplishment is access ~48.6 million uninsured in America* ~800 thousand uninsured in Indiana*

Covered California Delivering on the Promise of Care. State of Reform Health Policy Conference Anne Price November 6, 2015

Covered California Delivering on the Promise of Care State of Reform Health Policy Conference Anne Price November 6, 2015 Covered California s Promise: Better Care Healthier People Lower Cost How Covered

Covered California Delivering on the Promise of Care State of Reform Health Policy Conference Anne Price November 6, 2015 Covered California s Promise: Better Care Healthier People Lower Cost How Covered

The Affordable Care Act: A Summary on Healthcare Reform. The Wyoming Department of Insurance

The Affordable Care Act: A Summary on Healthcare Reform The Wyoming Department of Insurance The ACA is a federal law that impacts Wyoming and its citizens. The State of Wyoming has filed a lawsuit against

The Affordable Care Act: A Summary on Healthcare Reform The Wyoming Department of Insurance The ACA is a federal law that impacts Wyoming and its citizens. The State of Wyoming has filed a lawsuit against

Individual Mandate and Related Information Requirements under PPACA

Individual Mandate and Related Information Requirements under PPACA Hinda Chaikind Specialist in Health Care Financing September 21, 2010 Congressional Research Service CRS Report for Congress Prepared

Individual Mandate and Related Information Requirements under PPACA Hinda Chaikind Specialist in Health Care Financing September 21, 2010 Congressional Research Service CRS Report for Congress Prepared

AFFORDABLE CARE ACT (ACA) QUESTIONS as of 4/6/15

QUESTIONS as of 4/6/15") AFFORDABLE CARE ACT (ACA) QUESTIONS as of 4/6/15 The PA Association of Health Underwriters (PAHU) whose members are insurance producers specializing in health insurance and employee benefits have prepared

AFFORDABLE CARE ACT (ACA) QUESTIONS as of 4/6/15 The PA Association of Health Underwriters (PAHU) whose members are insurance producers specializing in health insurance and employee benefits have prepared

Washington Health Benefit Exchange

Washington Health Benefit Exchange HEALTHCARE REFORM SEMINAR November 25th, 2013 ACA INFORMATIONAL SESSION FOR SMALL BUSINESS OWNERS The Affordable Care Act Exchange Basics Today s Agenda Exchange Functions

Washington Health Benefit Exchange HEALTHCARE REFORM SEMINAR November 25th, 2013 ACA INFORMATIONAL SESSION FOR SMALL BUSINESS OWNERS The Affordable Care Act Exchange Basics Today s Agenda Exchange Functions

Health Care Reform Update. Michelle VanDellen, CPA Tax Senior Manager

Health Care Reform Update Michelle VanDellen, CPA Tax Senior Manager 1 The material appearing in this presentation is for informational purposes only and is not legal or accounting advice. Communication

Health Care Reform Update Michelle VanDellen, CPA Tax Senior Manager 1 The material appearing in this presentation is for informational purposes only and is not legal or accounting advice. Communication

HEALTH REFORM. Presentation to San Francisco Health Commission April 20, 2010

1 HEALTH REFORM Presentation to San Francisco Health Commission April 20, 2010 Tangerine Brigham, Deputy Director of Health and Director of Healthy San Francisco Colleen Chawla, Director of Grants and

1 HEALTH REFORM Presentation to San Francisco Health Commission April 20, 2010 Tangerine Brigham, Deputy Director of Health and Director of Healthy San Francisco Colleen Chawla, Director of Grants and

Part I: Premium Tax Credits

Part I: Premium Tax Credits Coverage Year 2018 Center on Budget and Policy Priorities September 19, 2017 Overview of Upcoming Open Enrollment Shorter Open Enrollment for OE5 3 Nov 1: Open enrollment begins

Part I: Premium Tax Credits Coverage Year 2018 Center on Budget and Policy Priorities September 19, 2017 Overview of Upcoming Open Enrollment Shorter Open Enrollment for OE5 3 Nov 1: Open enrollment begins

Health Insurance Premium Tax Credits and Cost-Sharing Subsidies: In Brief

Health Insurance Premium Tax Credits and Cost-Sharing Subsidies: In Brief Bernadette Fernandez Specialist in Health Care Financing February 10, 2017 Congressional Research Service 7-5700 www.crs.gov R44425

Health Insurance Premium Tax Credits and Cost-Sharing Subsidies: In Brief Bernadette Fernandez Specialist in Health Care Financing February 10, 2017 Congressional Research Service 7-5700 www.crs.gov R44425

Health Care Reform. Navigating The Maze Of. What s Inside

Navigating The Maze Of Health Care Reform What s Inside Questions and Answers on Health Care Reform Health Care Reform Timeline Health Care Reform Glossary Questions and Answers on Health Care Reform I

Navigating The Maze Of Health Care Reform What s Inside Questions and Answers on Health Care Reform Health Care Reform Timeline Health Care Reform Glossary Questions and Answers on Health Care Reform I

Affordable Care Act. Introduction. What is the Affordable Care Act? Objectives

Affordable Care Act Introduction This lesson covers some of the tax provisions of the Affordable Care Act (ACA). You will learn how to determine if taxpayers satisfy the individual shared responsibility

Affordable Care Act Introduction This lesson covers some of the tax provisions of the Affordable Care Act (ACA). You will learn how to determine if taxpayers satisfy the individual shared responsibility

Affordable Care Act Planning for CPAs. Ben Conley Seyfarth Shaw LLP

Affordable Care Act Planning for CPAs Ben Conley Seyfarth Shaw LLP Overview Background ACA & Taxes Taxes on Employers (and Tax Credits for Employers) Taxes on Individuals (and Tax Credits for Individuals)

Affordable Care Act Planning for CPAs Ben Conley Seyfarth Shaw LLP Overview Background ACA & Taxes Taxes on Employers (and Tax Credits for Employers) Taxes on Individuals (and Tax Credits for Individuals)

2016 Instructions for Form 8965

Department of the Treasury Internal Revenue Service 2016 Instructions for Form 8965 Health Coverage Exemptions (and Instructions for Figuring Your Shared Responsibility Payment) For each month you must

Department of the Treasury Internal Revenue Service 2016 Instructions for Form 8965 Health Coverage Exemptions (and Instructions for Figuring Your Shared Responsibility Payment) For each month you must

Overview of New Reform Law. Federal Healthcare Reform: Impacts on Employer-Sponsored Plans. Agenda

: Impacts on Employer-Sponsored Plans June 3, 2010 Employee Benefits Planning Association Jack McRae SVP, Congressional and Legislative Affairs Premera Blue Cross Jim Grazko VP and General Manager, Underwriting

: Impacts on Employer-Sponsored Plans June 3, 2010 Employee Benefits Planning Association Jack McRae SVP, Congressional and Legislative Affairs Premera Blue Cross Jim Grazko VP and General Manager, Underwriting

5GBenefits, LLC Your Health Care Reform Partner

5GBenefits, LLC Your Health Care Reform Partner Are you in compliance with health care reform regulations? We can help you stay on top of health care reform in order to avoid penalties from legislative

5GBenefits, LLC Your Health Care Reform Partner Are you in compliance with health care reform regulations? We can help you stay on top of health care reform in order to avoid penalties from legislative

The Affordable Care Act (ACA)

") Life Guide The Affordable Care Act (ACA) The Affordable Care Act, or ACA, is the nation's health insurance reform law, initially enacted in March 2010 and being gradually phased in over a period of years.

Life Guide The Affordable Care Act (ACA) The Affordable Care Act, or ACA, is the nation's health insurance reform law, initially enacted in March 2010 and being gradually phased in over a period of years.

Affordable Care Act. Pub 4012 ACA Tab Pub 4491 Lesson 3

Affordable Care Act Pub 4012 ACA Tab Pub 4491 Lesson 3 ACA IT s The Law Like it or not Repeal or change possible But, Applies to 2016 Deal with it The Good News Most of clients have Medicare 2 ACA Summary

Affordable Care Act Pub 4012 ACA Tab Pub 4491 Lesson 3 ACA IT s The Law Like it or not Repeal or change possible But, Applies to 2016 Deal with it The Good News Most of clients have Medicare 2 ACA Summary

AFFORDABLE CARE ACT FAQ

AFFORDABLE CARE ACT FAQ What is the Healthcare Insurance Marketplace? The Marketplace is a new way to find quality health coverage. It can help if you don t have coverage now or if you have it but want

AFFORDABLE CARE ACT FAQ What is the Healthcare Insurance Marketplace? The Marketplace is a new way to find quality health coverage. It can help if you don t have coverage now or if you have it but want

2018 Instructions for Form 8965

Department of the Treasury Internal Revenue Service 2018 Instructions for Form 8965 Health Coverage Exemptions (and Instructions for Figuring Your Shared Responsibility Payment) Section references are

Department of the Treasury Internal Revenue Service 2018 Instructions for Form 8965 Health Coverage Exemptions (and Instructions for Figuring Your Shared Responsibility Payment) Section references are

Health Care Reform: An Update on California. Kerry Landry, MPH Coverage Programs Specialist February 24 th, 2012

Health Care Reform: An Update on California Kerry Landry, MPH Coverage Programs Specialist February 24 th, 2012 1 Agenda 1. Overview of the Affordable Care Act 2. Focus on Medicaid and Public Coverage

Health Care Reform: An Update on California Kerry Landry, MPH Coverage Programs Specialist February 24 th, 2012 1 Agenda 1. Overview of the Affordable Care Act 2. Focus on Medicaid and Public Coverage

STARTING STRONG FOR COMMUNITY HEALTH! WEBINAR

STARTING STRONG FOR COMMUNITY HEALTH! WEBINAR The ACA and Taxes: Tips for Enrollment Assisters February 26, 2016 Today s Presenters: Alicia Siani, Policy Analyst, EverThrive IL asiani@everthriveil.org

STARTING STRONG FOR COMMUNITY HEALTH! WEBINAR The ACA and Taxes: Tips for Enrollment Assisters February 26, 2016 Today s Presenters: Alicia Siani, Policy Analyst, EverThrive IL asiani@everthriveil.org

Health Care Reform. The Affordable Care Act

1 Health Care Reform The Affordable Care Act House Keeping items.. 1. All phone lines are muted so please send any questions you may have via the chat session during the webinar. 2. All slides will be

1 Health Care Reform The Affordable Care Act House Keeping items.. 1. All phone lines are muted so please send any questions you may have via the chat session during the webinar. 2. All slides will be

Employer Shared Responsibility Glossary of Key Terms

Employer Shared Responsibility Glossary of Key Terms Administrative Period An administrative period is an optional period of up to 90 days following the initial or standard measurement period and ending

Employer Shared Responsibility Glossary of Key Terms Administrative Period An administrative period is an optional period of up to 90 days following the initial or standard measurement period and ending

Overview of the Patient Protection and Affordable Care Act (ACA) Steven Abramson, Marketing Manager Community Health Alliance of Pasadena

Steven Abramson, Marketing Manager Community Health Alliance of Pasadena") Overview of the Patient Protection and Affordable Care Act (ACA) Steven Abramson, Marketing Manager Community Health Alliance of Pasadena What is the Patient Protection and Affordable Care Act (ACA)? When

Overview of the Patient Protection and Affordable Care Act (ACA) Steven Abramson, Marketing Manager Community Health Alliance of Pasadena What is the Patient Protection and Affordable Care Act (ACA)? When

Health Reform: An Overview. Hinda Chaikind February 25, 2011

Health Reform: An Overview Hinda Chaikind February 25, 2011 Introduction Expanded coverage and reform Insurance and subsidies through Exchanges Medicaid expansion CHIP funding (Children s Health Insurance

Health Reform: An Overview Hinda Chaikind February 25, 2011 Introduction Expanded coverage and reform Insurance and subsidies through Exchanges Medicaid expansion CHIP funding (Children s Health Insurance

PPACA Implementation and the Marketplaces aka Exchanges. Presented by: Cathy Cooper November 15, 2013

PPACA Implementation and the Marketplaces aka Exchanges Presented by: Cathy Cooper November 15, 2013 Today s Agenda 2014 Provisions Groups over 50 in 2014 Groups under 50 in 2014 Marketplaces aka Exchanges

PPACA Implementation and the Marketplaces aka Exchanges Presented by: Cathy Cooper November 15, 2013 Today s Agenda 2014 Provisions Groups over 50 in 2014 Groups under 50 in 2014 Marketplaces aka Exchanges

Strategies for Compliance with "Obamacare" for Kathryn B. Solley September 18, 2013

Strategies for Compliance with "Obamacare" for 2014 Kathryn B. Solley September 18, 2013 Mission of Pro Bono Partnership of Atlanta: To maximize the impact of pro bono engagement by connecting a network

Strategies for Compliance with "Obamacare" for 2014 Kathryn B. Solley September 18, 2013 Mission of Pro Bono Partnership of Atlanta: To maximize the impact of pro bono engagement by connecting a network

4/22/2014. Health Care Reform. Disclosure. Health Care Reform. How Will it Change Your Business Strategy?

Health Care Reform How Will it Change Your Business Strategy? OHCA Educational Session April 29 th, 2014 Presented by: Roderick S. Wood, CHRS Huntington Insurance, Inc. Disclosure This presentation contains

Health Care Reform How Will it Change Your Business Strategy? OHCA Educational Session April 29 th, 2014 Presented by: Roderick S. Wood, CHRS Huntington Insurance, Inc. Disclosure This presentation contains

Rhode Island League of Cities and Towns. Health Care Reform and the State Exchanges: What Cities and Towns Should Be Doing Now

Rhode Island League of Cities and Towns Health Care Reform and the State Exchanges: What Cities and Towns Should Be Doing Now Rick Johnson Senior Vice President, National Public Sector Health Practice

Rhode Island League of Cities and Towns Health Care Reform and the State Exchanges: What Cities and Towns Should Be Doing Now Rick Johnson Senior Vice President, National Public Sector Health Practice

Federal Subsidies for Health Insurance Coverage for People Under Age 65: Tables from CBO s September 2017 Projections

Federal Subsidies for Health Insurance Coverage for People Under Age 65: Tables from CBO s September 2017 Projections Table 1. Health Insurance Coverage for People Under Age 65 Table 2. Net Federal Subsidies

Federal Subsidies for Health Insurance Coverage for People Under Age 65: Tables from CBO s September 2017 Projections Table 1. Health Insurance Coverage for People Under Age 65 Table 2. Net Federal Subsidies

VITA/TCE Basic Certification Topics on Affordable Care Act. Current as of November 20, 2017

VITA/TCE Basic Certification Topics on Affordable Care Act Current as of November 20, 2017 Agenda 2 Webinar #1 Basic Certification Topics Minimum essential coverage Shared responsibility payment Exemptions

VITA/TCE Basic Certification Topics on Affordable Care Act Current as of November 20, 2017 Agenda 2 Webinar #1 Basic Certification Topics Minimum essential coverage Shared responsibility payment Exemptions

Figure ES-1. Major Features of Health Insurance Expansion Bills and Impact on Uninsured, National Expenditures

Figure ES-1. Major Features of Health Insurance Expansion Bills and Impact on, National Expenditures President Bush s Tax Reform Plan Healthy Americans Act 2 Federal/State Partnership 15 States AmeriCare

Figure ES-1. Major Features of Health Insurance Expansion Bills and Impact on, National Expenditures President Bush s Tax Reform Plan Healthy Americans Act 2 Federal/State Partnership 15 States AmeriCare

Health Care Reform: General Q&A for Employees

From Health Care Reform: General Q&A for Employees Common questions answered I ve heard a lot about the health care reform law. When do the reforms become effective? The health care reform bill was signed

From Health Care Reform: General Q&A for Employees Common questions answered I ve heard a lot about the health care reform law. When do the reforms become effective? The health care reform bill was signed

Complying with Health Care Reform

Complying with Health Care Reform April 17, 2013 1 1 What Happened? In March 2010, Congress passed and the President signed health reform in: The Patient Protection and Affordable Care Act The Health Care

Complying with Health Care Reform April 17, 2013 1 1 What Happened? In March 2010, Congress passed and the President signed health reform in: The Patient Protection and Affordable Care Act The Health Care

ISSUE BRIEF. Massachusetts-Style Coverage Expansion: What Would it Cost in California? Introduction. Examining the Massachusetts Model

Massachusetts-Style Coverage Expansion: What Would it Cost in California? Introduction Massachusetts enactment of legislation (H 4850) to extend coverage to all residents has received much attention in

Massachusetts-Style Coverage Expansion: What Would it Cost in California? Introduction Massachusetts enactment of legislation (H 4850) to extend coverage to all residents has received much attention in

UPDATE ON THE AFFORDABLE CARE ACT: EMPLOYER MANDATE

Bill Enck, CPA, CPC, APA Roger Prince, JD, APA UPDATE ON THE AFFORDABLE CARE ACT: EMPLOYER MANDATE berrydunn.com GAIN CONTROL INDIVIDUAL MANDATE 1/1/2014 Individual mandate effective 1/1/2014 Code 5000A

Bill Enck, CPA, CPC, APA Roger Prince, JD, APA UPDATE ON THE AFFORDABLE CARE ACT: EMPLOYER MANDATE berrydunn.com GAIN CONTROL INDIVIDUAL MANDATE 1/1/2014 Individual mandate effective 1/1/2014 Code 5000A

Affordable Care Act Implementation for Employers

Affordable Care Act Implementation for Employers 2014 League of California Cities City Attorneys' Spring Conference May 9, 2014 Click icon to add picture Anne Hydorn, Partner ahydorn@hansonbridgett.com

Affordable Care Act Implementation for Employers 2014 League of California Cities City Attorneys' Spring Conference May 9, 2014 Click icon to add picture Anne Hydorn, Partner ahydorn@hansonbridgett.com

AFORDABLE CARE ACT (ACA)

") AFORDABLE CARE ACT (ACA) The Patient Protection and Affordable Care Act of 2010, commonly known as the Affordable Care Act (ACA), contain several key programs and mandates for employers and individuals.

AFORDABLE CARE ACT (ACA) The Patient Protection and Affordable Care Act of 2010, commonly known as the Affordable Care Act (ACA), contain several key programs and mandates for employers and individuals.

VITA/TCE Basic Certification Topics on Affordable Care Act. Current as of November 15, 2018

VITA/TCE Basic Certification Topics on Affordable Care Act Current as of November 15, 2018 Agenda 2 The Individual Mandate Penalty Was Repealed Everyone is Exempt Not Quite Shared Responsibility Payment

VITA/TCE Basic Certification Topics on Affordable Care Act Current as of November 15, 2018 Agenda 2 The Individual Mandate Penalty Was Repealed Everyone is Exempt Not Quite Shared Responsibility Payment

What s on the Horizon for Health Care and Public Benefits. May 8, 2013

What s on the Horizon for Health Care and Public Benefits. May 8, 2013 1 Overview Individual Mandate Federal Exchange Changes to Badgercare Changes to MAPP Future of HIRSP Changes to employer group health

What s on the Horizon for Health Care and Public Benefits. May 8, 2013 1 Overview Individual Mandate Federal Exchange Changes to Badgercare Changes to MAPP Future of HIRSP Changes to employer group health

The New Healthcare Law and Its Impact on Small Business

U. S. Small Business Administration Washington Metropolitan Area District Office The New Healthcare Law and Its Impact on Small Business Julie C. Verratti Advisor U.S. Small Business Administration Julie.Verratti@sba.gov

U. S. Small Business Administration Washington Metropolitan Area District Office The New Healthcare Law and Its Impact on Small Business Julie C. Verratti Advisor U.S. Small Business Administration Julie.Verratti@sba.gov

Aldridge Financial Consultants January 12, 2013

Aldridge Financial Consultants Mark D. Aldridge, CFP, CFA, ChFC 3021 Bethel Road Suite 100 Columbus, OH 43220 614-824-3080 Fax 614 824-3082 mark.aldridge@raymondjames.com www.markaldridge.com Health-Care

Aldridge Financial Consultants Mark D. Aldridge, CFP, CFA, ChFC 3021 Bethel Road Suite 100 Columbus, OH 43220 614-824-3080 Fax 614 824-3082 mark.aldridge@raymondjames.com www.markaldridge.com Health-Care

NFIB v. Kathleen Sebelius and its Impact on Employers: Healthcare Reform Revisited

July 5, 2012 NFIB v. Kathleen Sebelius and its Impact on Employers: Healthcare Reform Revisited The Patient Protection and Affordable Care Act (the Affordable Care Act ) imposes new requirements on individuals

July 5, 2012 NFIB v. Kathleen Sebelius and its Impact on Employers: Healthcare Reform Revisited The Patient Protection and Affordable Care Act (the Affordable Care Act ) imposes new requirements on individuals