PPACA Implementation and the Marketplaces aka Exchanges. Presented by: Cathy Cooper November 15, 2013

|

|

|

- Roy Flowers

- 6 years ago

- Views:

Transcription

1 PPACA Implementation and the Marketplaces aka Exchanges Presented by: Cathy Cooper November 15, 2013

2 Today s Agenda 2014 Provisions Groups over 50 in 2014 Groups under 50 in 2014 Marketplaces aka Exchanges

3 2014 Provisions

4 2014 Provisions Effective on Plan Year Metal Level/Actuarial Value (AV) Non grandfathered individual & small group plans must have a minimum actuarial value AV is the way to express a plans overall level of financial protection in one number For example, if a plan has an AV of 70% on average, a participant would be responsible for 30% of the cost of all covered benefits In the Exchanges, AV is represented as metal levels 60% for a bronze plan, 70% for a silver plan, 80% for a gold plan, 90% for a platinum plan

5 2014 Provisions Effective on Plan Year Essential Benefits Non grandfathered individual & small group plans Must include services in the following 10 categories: Ambulatory patient services Emergency services Hospitalization Maternity & newborn care Mental health & substance use disorder services, including behavioral health treatment Prescription drugs Rehabilitative and habilitative services and devices Laboratory services Preventive and wellness services and chronic disease mgmt Pediatric services, including oral and vision care

6 2014 Provisions Effective on Plan Year All applicable plans must include the essential benefits package and must comply with limitations on annual costsharing for plans that are sold in the exchanges Michigan s essential benefit package is a Priority Health HMO package PPACA limits the amount of out of pocket cost sharing (deductible, coinsurance, copayments) for essential benefits only Includes OV and RX copayments which are typically not included in the out of pocket maximum Does not include non essential benefit charges, out of network charges and services not covered by the plan $6,350 single/$12,700 family in 2014 After 2014, amount will be indexed based by the change in the cost of health insurance

7 2014 Provisions Effective on Plan Year Annual deductibles are limited to $2,000 single/$4,000 family coverage A deductible may exceed the limit if the plan cannot reasonably reach the actuarial value (AV) of a given level of coverage without exceeding the limit HHS may increase this amount in future years An employer may offer a higher deductible plan, i.e. $3,000/$6,000, as long as that employer reimburses the deductible down to the allowable limit of $2,000/$4,000 Carriers struggled with AV of these plans

8 2014 Provisions Effective on Plan Year Annual Limits (grandfathered and non grandfathered) Insurers may not impose annual limits on the dollar value of essential benefits Reporting of Health Insurance Coverage Any group that provides minimum essential coverage to an individual during a calendar year must report certain information to the IRS and provide a written statement to the individual Waiting Periods (grandfathered and non grandfathered) Group health plans cannot require any waiting periods in excess of 90 days

9 2014 Provisions Effective on Plan Year Elimination of all pre existing condition limitations (all plans) Guaranteed renewability and availability Insurers have to renew coverage at the option of the group and accept every group that applies for coverage Wellness Programs The maximum reward for participation in a wellness program will increase to 30% of cost of applicable coverage

10 Groups over 50

11 Employer Responsibility Delayed until January 1, 2015 Employer must count all full time employees and part time employees on a full time equivalent basis in determining if they have 50 or more employees Certain seasonal workers are not counted in determining if employer has 50 workers Full time = 30 or more hours per week, determined on a monthly basis Penalties assessed for no coverage or coverage that doesn t meet a minimum value standard or is not affordable

12 Employer Responsibility Minimum value standard (plans share of costs is at least 60%) will determine adequacy of coverage Affordable coverage is coverage where the employee s share is less than 9.5% of household income However, employers don t need to use that standard to determine if their plan is adequate The premium employers use to calculate affordability is the single employee rate for the lowest tier plan, regardless of how many dependents employee has covered on the employer plan or what plan the employee elects The employer uses the employee s W2 wage to calculate income, not the household income

13 Rate & Plan Expectations for 2014 Insurers estimate there will be a 6 7% increase in rates due to new PPACA taxes alone Does not include trend or change in base rates Some groups are looking at self funding to avoid compliance with state mandates, ERISA taxes, essential benefits, and medical loss ratio requirements

14 Groups Under 50

15 What About Groups Under 50? Groups under 50 in size have to comply with: Essential Benefits Lifetime limits Deductible cap Out of pocket maximums Only exception to the rule is for grandfathered plans Check with your carrier to make sure they honor grandfathered plans Groups under 50 FTE s are also eligible to purchase coverage on the SHOP Exchange

16 The Good News No employer mandate No penalties No coverage at all Unaffordable coverage

17 The Bad News Plans will have to change to meet the new essential benefits guidelines Renewals will be mapped to compliant plan Policies can only be rated using the following: Area, Age (3:1) and tobacco status (1.5:1) most carriers are not charging a tobacco surcharge for small groups Applies to all fully insured plans inside and outside of the exchange, both group and individual Health status and industry can no longer be used to determine rates

18 Rates in 2014 Rates will be per person based on ages of enrolling members and area of group headquarters, with a maximum of 3 oldest children under age 21 There are 16 rating areas that were chosen by the state No longer Single, Two person or Family rates Contribution strategy may have to change to contribution by tier i.e. Today an employer pays 70% and the employee pays 30%, in 2014, the 70% will not be the same for all singles, two person, and families, which will be a budget challenge Additional taxes will apply on top of these changes

19 Rate & Plan Expectations for 2014 Insurers estimate there will be a 7 8% increase in rates due to new PPACA taxes alone Does not include trend or change in base rates Some groups are looking at self funding to avoid compliance with state mandates, ERISA taxes, essential benefits, and medical loss ratio requirements Insurers are determining how Small Group Reform law fits since participation rules can be enforced Impacts to renewal questionnaire??? Some insurers are renewing groups in December 2013 to avoid compliance with these rules until December, 2014, however, taxes will still be applied January, 2014

20 Marketplaces aka Exchanges

21 The Marketplace, aka Exchange HHS decided that Exchanges will now become Marketplaces because the word exchange does not translate to Spanish Coverage is available January 1, 2014 with enrollment beginning October 1, 2013 through healthcare.gov many technical glitches have caused access problems Coverage meets minimum value, essential benefits and metal standards, i.e. Gold, Silver, Bronze All plans are subject to a 3.5% service fee that is sent directly to the Federal government

22 Individual Marketplace Individuals purchase coverage here Subsidies are only available to qualified individuals purchasing coverage through health insurance exchanges after January 1, 2014 Individuals with family incomes between % of the federal poverty level are eligible for a premium tax credit Individuals with family incomes at or below 250% of the FPL also qualify for reduced cost sharing Individuals and their dependents who have been offered coverage through an employer that meets an affordability and minimum value test are not eligible to purchase coverage through an exchange and get a subsidy

23 Individual Coverage Subsidies The premium subsidy will come in the form of a refundable and advanceable tax credit paid directly to the individual s insurer The amount of the refundable premium tax credit received is based on the premium for the second lowest cost qualified health plan in the exchange (the silver plan) and in the rating area where the individual is eligible to purchase coverage Exchange subsidies do no mean free coverage and they will benefit lower income individuals and families very differently Plan decision makers and their families generally will not qualify for subsidies

24 The PPACA Premium Tax Credit s Varying Impact Individual 30 year old with qualified employer coverage Family Status Married, two children Income Percentage of income that may be spent on health insurance $35, % of household income Estimated value of the employee s annual tax credit in 2014 No one in the family qualified to buy coverage in the exchange or get a subsidy 30 year old with no employer coverage 30 year old with no employer coverage 45 Year old with qualified employer coverage Single $35, % of household income Married, two children Married, three children $35, % of household income $55, % of household income $155 (based on Kaiser Family Foundation s projection of a $3440 annual single premium in 2014) Individual s annual premium costs would be $3325 $8,720 (based on Kaiser Family Foundation s projection of a $10,108 annual family premium in 2014) Family s annual premium costs would be $1,388 $0 No one in the family is qualified to buy coverage in the exchange or get a subsidy 45 year old with no employer coverage 45 year old with no employer coverage Single $55,000 N/A $0 Individual may buy coverage in the exchange but would not qualify for subsidy Individual s annual premium payments would be $5,609 based on Kaiser Family Foundation s projection of 2014 single premium Married, two children $55, % of household income $10, 100 (based on Kaiser Family Foundation s projection of a $14, 250 annual family premium in 2014) Family s annual premium costs would be $4,135

25 Individual Mandate Requirement that all individuals obtain private health insurance or pay a penalty Exemptions are members of certain faiths, health care sharing ministries, those with income restraints or hardships Additional exemptions: native americans, those who haven t had coverage for up to 90 days, undocumented immigrants, and imprisoned people Penalty is assessed by the IRS and collected upon tax filing Due to problems with marketplace site, there is much political pressure to delay the individual mandate

26

27 SHOP Exchange Groups (2 50 only) can purchase coverage here Groups over 50 will be eligible in Jan. 1, 2016 Groups over 100 will be eligible in Jan. 1, 2017 Only place the Small Business Tax Credit is available in 2014 Fewer than 25 full time employees Pay an average wage of less than $50,000/year Pay at least 50% of employee premiums

28 Eligibility Requirements SHOP Employer s business must: Be located in a SHOP s service area Have at least one eligible employee on payroll Have no more than 50 full time equivalent (FTE)* employees on payroll Offer coverage to all full time** employees *Part time workers must be counted as fractions of an FTE when determining employer size, even if part time workers are not offered coverage. **Full time is defined as working an average of 30 or more hours per week.

29 Process to Enroll in the SHOP Beginning this fall, employers can created their own My Accounts at healthcare.gov and go through the application process as follows: Step 1: Employers registers basic information about their businesses. Step 2: Next, employer inputs an employee roster with basic information about each employee. Step 3: The SHOP will generate information about the range of premiums for plans, and, at the employer s request, detailed descriptions of specific plans at different price points. In 2014, employers can provide health insurance coverage to their employees by offering a single Qualified Health Plan (QHP) option.

30 Process to Enroll in the SHOP Step 4: In 2014, after the employer selects one QHP, that QHP will be the default reference plan. Step 5: Once the employer has selected a reference plan, they choose a defined percentage of the reference plan to contribute for each employee. The employer also decides if and at what percentage they will contribute towards dependent and dental coverage. (Like contributions to employee coverage, employer contributions to dependent insurance coverage and dental coverage are optional under the Affordable Care Act for small employers.) Step 6: Next, the employer decides whether all employees will contribute the same amount for coverage or will pay a premium based on age.

31 Process to Enroll in the SHOP Step 7: The employer views a summary of choices and has an opportunity to explore what if scenarios. Step 8: The employer can also help each eligible employee enroll in SHOP. Step 9: The employer reviews the completed application and determines if he or she has provided all the required information and met the minimum participation rate (in most states at least 70% of employees must participate*). Last, the employer establishes a waiting period policy for newly eligible employees, and submits the first month s premium.

32 Private Exchanges: An Alternative Like the public exchanges, private exchanges offer an organized market place for health insurance plans with multiple designs and price points Unlike public exchanges, private exchanges: Are managed in the private sector Are not eligible for government subsidies Private exchanges are generally based on defined contribution models

33 Why Employers are Looking at DC To reset how the employer and employee share the cost of coverage To connect employees to their health care and its costand be a catalyst for employees to make better choices To improve financial predictability in medical program budgeting To parallel retirement plans transition from DB to DC Source: Mercer March 6,2013

34 DC Tax Treatment Tax treatment of medical plans can continue as is with a qualified Sect. 125 plan Pre tax for employee Deductible expense for employer Tax treatment of voluntary benefits Employer chooses one medical carrier and signs group contract no penalty

35 Private Exchange Models Single Carrier: BCBSM Glide Path open to all certified agents Single Distributor: AON, Hewitt closed to all agents Multi carrier, Multi product, Multi distributor: iselect Custom Benefits Store open to all certified agents

Carrier Partners -HAP -Priority Health -Met-Life -Guardian -Allstate -Symetra Employers Choose the Carriers, the employee chooses the")

36 iselect Portfolio Employee Offerings- Health (min 8-10 plan options) Dental ( 3 options) Vision (4 options) Life Disability Worksite Voluntary coverage Health Savings Accounts Pet Insurance Telemedicine FSA (optional) Carrier Partners -HAP -Priority Health -Met-Life -Guardian -Allstate -Symetra Employers Choose the Carriers, the employee chooses the plan

37 The Ultimate ACA Pain Reliever SMALL GROUP Set up defined contribution now avoid member level pricing issues Enrollment tool will do the pricing work from the employee Products offered PPACA ready Plan documents, reports and process easy for compliance LARGE GROUP PPACA Actuarial Value Assurance with the suites Contribution strategy allowing for split funding solutions.. Affordability Voluntary Products Available for Part timers Compliance documents all stored on the tool Fully insured or self insured options

38 Why Offer Employer Sponsored Coverage? Employers can provide substantial economic value and financial peace of mind to employees by offering group health insurance coverage A healthy workforce is directly linked to productivity Offering benefits can allow employers to attract the best workers and remain competitive Tax deductibility for employers Employees pay for coverage pre tax and generally receive employer contributions

39 Considerations for Small Groups To offer coverage or not offer coverage, a few reminders: Public exchanges are new and untested many problems Coverage will be available for purchase outside the exchange, however, new rating factors and plan designs will apply does early renewal strategy make sense? Coverage may be available through a private exchange that allows the employee to have choice but generally through a more manageable number of carriers If the employer drops coverage, then everyone has to go to the exchange to get coverage determine how many of your employees would be eligible for subsidies Consult your insurance agent on these decisons

40 Questions? Cathy Cooper (248)

THE AFFORDABLE CARE ACT...2

Table of Contents THE AFFORDABLE CARE ACT...2 Health Insurance Marketplace (Exchange)...3 Metallic Levels...4 Catastrophic Plans...4 Individual Mandate...5 Subsidies...5 Open Enrollment Period...6 Special

Table of Contents THE AFFORDABLE CARE ACT...2 Health Insurance Marketplace (Exchange)...3 Metallic Levels...4 Catastrophic Plans...4 Individual Mandate...5 Subsidies...5 Open Enrollment Period...6 Special

Health Care Reform under the Patient Protection and Affordable Care Act ( PPACA ) provisions effective January 1, 2014

provisions effective January 1, 2014") The New Health Care Landscape Today s Agenda Health Care Reform under the Patient Protection and Affordable Care Act ( PPACA ) provisions effective January 1, 2014 Exchanges and Qualified Health Plans

The New Health Care Landscape Today s Agenda Health Care Reform under the Patient Protection and Affordable Care Act ( PPACA ) provisions effective January 1, 2014 Exchanges and Qualified Health Plans

Health Care Reform. PPACA Compliance Overview

Health Care Reform PPACA Compliance Overview Agenda 1 2 What Healthcare Reform Is How the ACA is Affecting Employers 3 4 5 What the Employer Delay Means For Your Business Factors Affecting Your Premiums

Health Care Reform PPACA Compliance Overview Agenda 1 2 What Healthcare Reform Is How the ACA is Affecting Employers 3 4 5 What the Employer Delay Means For Your Business Factors Affecting Your Premiums

ACA and The Marketplace. Also known as the (Federal) Exchange

Exchange") ACA and The Marketplace Also known as the (Federal) Exchange 1 Qualified Health Plan and Minimum Essential Coverage (Indiv., Small Group & Large Group Coverage) Needs to Meet the Following (At a Minimum):

ACA and The Marketplace Also known as the (Federal) Exchange 1 Qualified Health Plan and Minimum Essential Coverage (Indiv., Small Group & Large Group Coverage) Needs to Meet the Following (At a Minimum):

The Affordable Care Act: A Summary on Healthcare Reform. The Wyoming Department of Insurance

The Affordable Care Act: A Summary on Healthcare Reform The Wyoming Department of Insurance The ACA is a federal law that impacts Wyoming and its citizens. The State of Wyoming has filed a lawsuit against

The Affordable Care Act: A Summary on Healthcare Reform The Wyoming Department of Insurance The ACA is a federal law that impacts Wyoming and its citizens. The State of Wyoming has filed a lawsuit against

The Patient Protection and Affordable Care Act

The Patient Protection and Affordable Care Act 2015 marks the beginning of the fifth full year of the Patient Protection and Affordable Care Act (ACA). We want to take the opportunity to look ahead and

The Patient Protection and Affordable Care Act 2015 marks the beginning of the fifth full year of the Patient Protection and Affordable Care Act (ACA). We want to take the opportunity to look ahead and

4/22/2014. Health Care Reform. Disclosure. Health Care Reform. How Will it Change Your Business Strategy?

Health Care Reform How Will it Change Your Business Strategy? OHCA Educational Session April 29 th, 2014 Presented by: Roderick S. Wood, CHRS Huntington Insurance, Inc. Disclosure This presentation contains

Health Care Reform How Will it Change Your Business Strategy? OHCA Educational Session April 29 th, 2014 Presented by: Roderick S. Wood, CHRS Huntington Insurance, Inc. Disclosure This presentation contains

Navajo County Schools EBT

Navajo County Schools EBT Affordable Care Act (ACA) Update Aaron Polkoski Segal Consulting January 31st, 2014 Copyright 2013 by The Segal Group, Inc., parent of The Segal Company. All rights reserved.

Navajo County Schools EBT Affordable Care Act (ACA) Update Aaron Polkoski Segal Consulting January 31st, 2014 Copyright 2013 by The Segal Group, Inc., parent of The Segal Company. All rights reserved.

Frequently Asked Questions about Health Care Reform and the Affordable Care Act

Frequently Asked Questions about Health Care Reform and the Affordable Care Act HEALTH CARE REFORM OVERVIEW Q 1: What ACA changes are already in place? There are no lifetime dollar limits on essential

Frequently Asked Questions about Health Care Reform and the Affordable Care Act HEALTH CARE REFORM OVERVIEW Q 1: What ACA changes are already in place? There are no lifetime dollar limits on essential

Affordable Care Act HEALTHCARE.GOV. Marketplace Implementation Briefing Loudon County Chamber of Commerce July 12, 2013

HEALTHCARE.GOV Affordable Care Act Marketplace Implementation Briefing Loudon County Chamber of Commerce July 12, 2013 Joanne Corte Grossi, MIPP Regional Director U.S. Department of Health & Human Services,

HEALTHCARE.GOV Affordable Care Act Marketplace Implementation Briefing Loudon County Chamber of Commerce July 12, 2013 Joanne Corte Grossi, MIPP Regional Director U.S. Department of Health & Human Services,

HEALTH INSURANCE MARKETPLACE. May 21,

HEALTH INSURANCE MARKETPLACE May 21, 2013 Agenda Introduction and Welcome Health Insurance Marketplaces Market Reforms Overview Enrollment Process The Marketplace and Small Businesses Applying for Small

HEALTH INSURANCE MARKETPLACE May 21, 2013 Agenda Introduction and Welcome Health Insurance Marketplaces Market Reforms Overview Enrollment Process The Marketplace and Small Businesses Applying for Small

Washington Health Benefit Exchange

Washington Health Benefit Exchange HEALTHCARE REFORM SEMINAR November 25th, 2013 ACA INFORMATIONAL SESSION FOR SMALL BUSINESS OWNERS The Affordable Care Act Exchange Basics Today s Agenda Exchange Functions

Washington Health Benefit Exchange HEALTHCARE REFORM SEMINAR November 25th, 2013 ACA INFORMATIONAL SESSION FOR SMALL BUSINESS OWNERS The Affordable Care Act Exchange Basics Today s Agenda Exchange Functions

The Affordable Care Act and the Essential Health Benefits Package

October 24, 2011 The Affordable Care Act and the Essential Health Benefits Package A. Background Under the Affordable Care Act (the ACA or the Act ), and starting in 2014, certain low to moderate income

October 24, 2011 The Affordable Care Act and the Essential Health Benefits Package A. Background Under the Affordable Care Act (the ACA or the Act ), and starting in 2014, certain low to moderate income

Chapter 1: What is the Affordable Care Act?

Chapter 1: What is the Affordable Care Act? The Affordable Care Act (ACA), also known as Obamacare, is a law that aims to help millions of Americans secure health insurance. Many individuals still are

Chapter 1: What is the Affordable Care Act? The Affordable Care Act (ACA), also known as Obamacare, is a law that aims to help millions of Americans secure health insurance. Many individuals still are

Rehmann Live! ACA Impact: Addressing the

Rehmann Live! ACA Impact: Addressing the Affordable Insert Care Presentation Act s effect on the Title public Here sector Presented by: Don McAnelly, CPA, ABV, CGMA Michael P. James, JD, MBA, CSSGB Don

Rehmann Live! ACA Impact: Addressing the Affordable Insert Care Presentation Act s effect on the Title public Here sector Presented by: Don McAnelly, CPA, ABV, CGMA Michael P. James, JD, MBA, CSSGB Don

What is The Affordable Care Act and how does it affect me?

What is The Affordable Care Act and how does it affect me? November 2013 Patient Protection and Affordable Care Act (PPACA) Overview The federal Patient Protection and Affordable Care Act signed by President

What is The Affordable Care Act and how does it affect me? November 2013 Patient Protection and Affordable Care Act (PPACA) Overview The federal Patient Protection and Affordable Care Act signed by President

Health Care Reform Frequently Asked Questions

Health Care Reform Frequently Asked Questions What are health exchanges, or marketplaces, and when are they going to be available? Health insurance exchanges, now called health insurance marketplaces,

Health Care Reform Frequently Asked Questions What are health exchanges, or marketplaces, and when are they going to be available? Health insurance exchanges, now called health insurance marketplaces,

Affordable Care Act A Broker s Perspective. Jeffrey M. Barry Barry Insurance Group

Affordable Care Act A Broker s Perspective Jeffrey M. Barry Barry Insurance Group What Is So Expensive? Is it health insurance? Is it the increased cost of healthcare? Essential Health Benefits Ambulatory

Affordable Care Act A Broker s Perspective Jeffrey M. Barry Barry Insurance Group What Is So Expensive? Is it health insurance? Is it the increased cost of healthcare? Essential Health Benefits Ambulatory

AFFORDABLE CARE ACT: SMALL EMPLOYER HEALTH REFORM CHECKLIST

White Paper AFFORDABLE CARE ACT: SMALL EMPLOYER HEALTH REFORM CHECKLIST White Paper AFFORDABLE CARE ACT: SMALL EMPLOYER HEALTH REFORM CHECKLIST Employers that offer health care coverage to employees are

White Paper AFFORDABLE CARE ACT: SMALL EMPLOYER HEALTH REFORM CHECKLIST White Paper AFFORDABLE CARE ACT: SMALL EMPLOYER HEALTH REFORM CHECKLIST Employers that offer health care coverage to employees are

Simple answers to health reform s complex issues facing every employer, and what you can do now to protect your business and your future.

Simple answers to health reform s complex issues facing every employer, and what you can do now to protect your business and your future. If you have any questions, please contact: Health Reform: A Guide

Simple answers to health reform s complex issues facing every employer, and what you can do now to protect your business and your future. If you have any questions, please contact: Health Reform: A Guide

Affordable Care Act: What Employers Need to Know to be in Compliance in 2014

Affordable Care Act: What Employers Need to Know to be in Compliance in 2014 October 2013 Stacy H. Barrow sbarrow@proskauer.com 1 Agenda Initial Observations Compliance Calendar Checklist: Important dates,

Affordable Care Act: What Employers Need to Know to be in Compliance in 2014 October 2013 Stacy H. Barrow sbarrow@proskauer.com 1 Agenda Initial Observations Compliance Calendar Checklist: Important dates,

Affordable Care Act HEALTHCARE.GOV

HEALTHCARE.GOV Affordable Care Act Marketplace Implementation Briefing Pennsylvania Breast Cancer Coalition 2014 Conference October 13, 2014 Joanne Corte Grossi, MIPP Regional Director U.S. Department

HEALTHCARE.GOV Affordable Care Act Marketplace Implementation Briefing Pennsylvania Breast Cancer Coalition 2014 Conference October 13, 2014 Joanne Corte Grossi, MIPP Regional Director U.S. Department

OVERVIEW OF THE AFFORDABLE CARE ACT. September 23, 2013

OVERVIEW OF THE AFFORDABLE CARE ACT September 23, 2013 Outline The New Continuum of Coverage Medicaid and CHIP Are Changing The New Marketplaces Insurance Affordability Programs Shared Responsibility Requirement

OVERVIEW OF THE AFFORDABLE CARE ACT September 23, 2013 Outline The New Continuum of Coverage Medicaid and CHIP Are Changing The New Marketplaces Insurance Affordability Programs Shared Responsibility Requirement

Health Care Reform. Navigating The Maze Of. What s Inside

Navigating The Maze Of Health Care Reform What s Inside Questions and Answers on Health Care Reform Health Care Reform Timeline Health Care Reform Glossary Questions and Answers on Health Care Reform I

Navigating The Maze Of Health Care Reform What s Inside Questions and Answers on Health Care Reform Health Care Reform Timeline Health Care Reform Glossary Questions and Answers on Health Care Reform I

A special look at health care reform. Helping members make informed decisions. Special Edition 2013

Special Edition 2013 SM Helping members make informed decisions A special look at health care reform. Changes ahead 3 How health care reform will impact rates 6 Five ways health care reform may affect

Special Edition 2013 SM Helping members make informed decisions A special look at health care reform. Changes ahead 3 How health care reform will impact rates 6 Five ways health care reform may affect

Presentation by: Champaign County Health Care Consumers (CCHCC) October 26, Welcome!

October 26, Welcome!") The Affordable Care Act (ACA): The Health Insurance Marketplace and Medicaid Presentation by: Champaign County Health Care Consumers (CCHCC) October 26, 2017 Welcome! Goals of the Affordable Care Act (ACA)

The Affordable Care Act (ACA): The Health Insurance Marketplace and Medicaid Presentation by: Champaign County Health Care Consumers (CCHCC) October 26, 2017 Welcome! Goals of the Affordable Care Act (ACA)

The Affordable Care Act

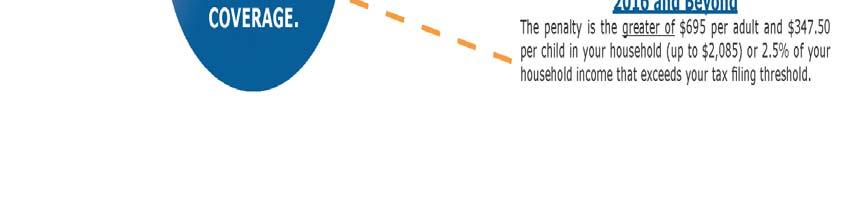

The Affordable Care Act Employers Guide to 2015 and Beyond For Small Groups Summary Jan. 1, 2014, ushered in new Affordable Care Act (ACA) health insurance market reforms. These changes are impacting the

The Affordable Care Act Employers Guide to 2015 and Beyond For Small Groups Summary Jan. 1, 2014, ushered in new Affordable Care Act (ACA) health insurance market reforms. These changes are impacting the

Thursday, December 19, 2013 Celeste Richards Erin Malone

Thursday, December 19, 2013 Celeste Richards Erin Malone Agenda Structure of ACA health Exchange and Mandated Elements of Plan Design Georgia Regions Alliant Health Plans Exchange Products and Provider

Thursday, December 19, 2013 Celeste Richards Erin Malone Agenda Structure of ACA health Exchange and Mandated Elements of Plan Design Georgia Regions Alliant Health Plans Exchange Products and Provider

AN INDIVIDUAL S guide to THE. Right Health Insurance

AN INDIVIDUAL S guide to THE Right Health Insurance TURN TO The right health insurance. Right now. To find the health insurance that s right for you, begin by asking yourself one simple question: What

AN INDIVIDUAL S guide to THE Right Health Insurance TURN TO The right health insurance. Right now. To find the health insurance that s right for you, begin by asking yourself one simple question: What

AFFORDABLE CARE ACT SMALL EMPLOYER HEALTH REFORM CHECKLIST. Edition: November 2014

AFFORDABLE CARE ACT Employers that offer health care coverage to employees are responsible for complying with many of the provisions of the Affordable Care Act (ACA). Most health reform changes apply regardless

AFFORDABLE CARE ACT Employers that offer health care coverage to employees are responsible for complying with many of the provisions of the Affordable Care Act (ACA). Most health reform changes apply regardless

Subsidized Health Coverage through MNsure

INFORMATION BRIEF Research Department Minnesota House of Representatives 600 State Office Building St. Paul, MN 55155 Randall Chun, Legislative Analyst 651-296-8639 Updated: October 2018 Subsidized Health

INFORMATION BRIEF Research Department Minnesota House of Representatives 600 State Office Building St. Paul, MN 55155 Randall Chun, Legislative Analyst 651-296-8639 Updated: October 2018 Subsidized Health

The New Responsibility to Secure Coverage: Frequently Asked Questions

The New Responsibility to Secure Coverage: Frequently Asked Questions Introduction The Patient Protection and Affordable Care Act (PPACA) includes a much-discussed requirement that people secure health

The New Responsibility to Secure Coverage: Frequently Asked Questions Introduction The Patient Protection and Affordable Care Act (PPACA) includes a much-discussed requirement that people secure health

2014 Hill, Chesson & Woody

Topics for Today Healthcare Reform s Mandates Regulations, Taxes and Fees. Oh my!!! Key Trends What s next? Healthcare Reform s Employer Mandate Background The Employer Mandate portion (4980H) of the Patient

Topics for Today Healthcare Reform s Mandates Regulations, Taxes and Fees. Oh my!!! Key Trends What s next? Healthcare Reform s Employer Mandate Background The Employer Mandate portion (4980H) of the Patient

Health Care Reform Update:

Health Care Reform Update: The Employer Mandate and Other Considerations for 2013 February 13, 2013 Today s Agenda Health Care Reform three new concepts Strategic Decisions for Employers in 2013 - Will

Health Care Reform Update: The Employer Mandate and Other Considerations for 2013 February 13, 2013 Today s Agenda Health Care Reform three new concepts Strategic Decisions for Employers in 2013 - Will

FREQUENTLY ASKED QUESTIONS (FAQ) ABOUT THE ACA:

ABOUT THE ACA:") FREQUENTLY ASKED QUESTIONS (FAQ) ABOUT THE ACA: Full implementation of the Patient Protection and Affordable Care Act (ACA) is less than a year away. Regulations impacting school districts have been issued

FREQUENTLY ASKED QUESTIONS (FAQ) ABOUT THE ACA: Full implementation of the Patient Protection and Affordable Care Act (ACA) is less than a year away. Regulations impacting school districts have been issued

By Larry Grudzien Attorney at Law

By Larry Grudzien Attorney at Law 1 What is a small employer? Fees and Taxes 90 day Waiting Period Pre-existing condition Out-of Pocket Limits Wellness Programs Approved Clinical Trials Cafeteria Plans

By Larry Grudzien Attorney at Law 1 What is a small employer? Fees and Taxes 90 day Waiting Period Pre-existing condition Out-of Pocket Limits Wellness Programs Approved Clinical Trials Cafeteria Plans

Affordable Care Act HEALTHCARE.GOV

HEALTHCARE.GOV Affordable Care Act Marketplace Implementation Briefing Pennsylvania Breast Cancer Coalition 2013 Conference October 15, 2013 Joanne Corte Grossi, MIPP Regional Director U.S. Department

HEALTHCARE.GOV Affordable Care Act Marketplace Implementation Briefing Pennsylvania Breast Cancer Coalition 2013 Conference October 15, 2013 Joanne Corte Grossi, MIPP Regional Director U.S. Department

Health Care Reform - Understanding the ACA Pediatric Essential Health Benefit

Health Care Reform - Understanding the ACA Pediatric Essential Health Benefit Presented by: John Lee DC Metro Sales Manager Agenda About Dominion Dental Services Health Care Reform Overview o When is Your

Health Care Reform - Understanding the ACA Pediatric Essential Health Benefit Presented by: John Lee DC Metro Sales Manager Agenda About Dominion Dental Services Health Care Reform Overview o When is Your

The New Healthcare Law and Its Impact on Small Business

U. S. Small Business Administration Washington Metropolitan Area District Office The New Healthcare Law and Its Impact on Small Business Julie C. Verratti Advisor U.S. Small Business Administration Julie.Verratti@sba.gov

U. S. Small Business Administration Washington Metropolitan Area District Office The New Healthcare Law and Its Impact on Small Business Julie C. Verratti Advisor U.S. Small Business Administration Julie.Verratti@sba.gov

What s on the Horizon for Health Care and Public Benefits. May 8, 2013

What s on the Horizon for Health Care and Public Benefits. May 8, 2013 1 Overview Individual Mandate Federal Exchange Changes to Badgercare Changes to MAPP Future of HIRSP Changes to employer group health

What s on the Horizon for Health Care and Public Benefits. May 8, 2013 1 Overview Individual Mandate Federal Exchange Changes to Badgercare Changes to MAPP Future of HIRSP Changes to employer group health

An Employer s Guide to Health Care Reform. Important details to navigate employer-provided benefits amidst a changing health care landscape.

An Employer s Guide to Health Care Reform Important details to navigate employer-provided benefits amidst a changing health care landscape. Navigating a new health care landscape Health care reform, also

An Employer s Guide to Health Care Reform Important details to navigate employer-provided benefits amidst a changing health care landscape. Navigating a new health care landscape Health care reform, also

Health Care Reform Provision (effective January 1, 2014) School City of Hobart Medical Plan

School City of Hobart Medical Plan") Health Care Reform: We ve Got You Covered The health care reform law officially called the Patient Protection and Affordable Care Act of 2010 (ACA for short) is here to stay. Additional changes resulting

Health Care Reform: We ve Got You Covered The health care reform law officially called the Patient Protection and Affordable Care Act of 2010 (ACA for short) is here to stay. Additional changes resulting

COVERED CALIFORNIA: THE GOOD, THE BAD & THE UNDEFINED FOR CHILDREN WITH SPECIAL HEALTH CARE NEEDS

1 COVERED CALIFORNIA: THE GOOD, THE BAD & THE UNDEFINED FOR CHILDREN WITH SPECIAL HEALTH CARE NEEDS Ann-Louise Kuhns President & CEO California Children s Hospital Association Health Care Reform: The Basics

1 COVERED CALIFORNIA: THE GOOD, THE BAD & THE UNDEFINED FOR CHILDREN WITH SPECIAL HEALTH CARE NEEDS Ann-Louise Kuhns President & CEO California Children s Hospital Association Health Care Reform: The Basics

Healthcare Reform for Small Employers Presented by: Larry Grudzien

Healthcare Reform for Small Employers Presented by: Larry Grudzien We re proud to offer a full-circle solution to your HR needs. BASIC offers collaboration, flexibility, stability, security, quality service

Healthcare Reform for Small Employers Presented by: Larry Grudzien We re proud to offer a full-circle solution to your HR needs. BASIC offers collaboration, flexibility, stability, security, quality service

Affordable Care Act Title 1: Employer Mandate. MAJ Philip Durando CPT Elvis Gonzalez CPT Stephanie Kessinger

Affordable Care Act Title 1: Employer Mandate MAJ Philip Durando CPT Elvis Gonzalez CPT Stephanie Kessinger Agenda Employer Mandate Tax Penalties and Credits Components defined Full Time Employee Affordability

Affordable Care Act Title 1: Employer Mandate MAJ Philip Durando CPT Elvis Gonzalez CPT Stephanie Kessinger Agenda Employer Mandate Tax Penalties and Credits Components defined Full Time Employee Affordability

Evaluating Your Nonprofit s Options under the Affordable Care Act: The Pros and Cons of Health Insurance Alternatives for Your Employees

Evaluating Your Nonprofit s Options under the Affordable Care Act: The Pros and Cons of Health Insurance Alternatives for Your Employees Tuesday, July 23, 2013, 12:30 p.m. 2:00 p.m. EDT Venable LLP, Washington,

Evaluating Your Nonprofit s Options under the Affordable Care Act: The Pros and Cons of Health Insurance Alternatives for Your Employees Tuesday, July 23, 2013, 12:30 p.m. 2:00 p.m. EDT Venable LLP, Washington,

TO UNDERSTANDING THE AFFORDABLE CARE ACT

3 STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT What s Inside Step 1: What Understand what you re buying 4 Step 2: How How can you buy health insurance? 20 STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT

3 STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT What s Inside Step 1: What Understand what you re buying 4 Step 2: How How can you buy health insurance? 20 STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT

Health Care Reform

Health Care Reform 2013-14 The Individual Mandate Via the Exchange may qualify for subsidy or premium tax credit Other source - most likely from the employer An employee ONLY receives a premium subsidy

Health Care Reform 2013-14 The Individual Mandate Via the Exchange may qualify for subsidy or premium tax credit Other source - most likely from the employer An employee ONLY receives a premium subsidy

Health Policy Essentials: Private Health Insurance. Bernadette Fernandez, Annie Mach, Janemarie Mulvey March 1, 2013

Health Policy Essentials: Private Health Insurance Bernadette Fernandez, Annie Mach, Janemarie Mulvey March 1, 2013 Private Health Insurance Insurance provides protection from economic loss Risk likelihood

Health Policy Essentials: Private Health Insurance Bernadette Fernandez, Annie Mach, Janemarie Mulvey March 1, 2013 Private Health Insurance Insurance provides protection from economic loss Risk likelihood

Affordable Care Act Survival Kit

Affordable Care Act Survival Kit The Affordable Care Act (ACA) stands poised to usher in sweeping changes for many businesses. Multiple regulations and shifting timetables, however, make it difficult to

Affordable Care Act Survival Kit The Affordable Care Act (ACA) stands poised to usher in sweeping changes for many businesses. Multiple regulations and shifting timetables, however, make it difficult to

AFFORDABLE CARE ACT LARGE EMPLOYER HEALTH REFORM CHECKLIST. Edition: October 2017

AFFORDABLE CARE ACT Employers that offer health care coverage to employees are responsible for complying with many of the provisions of the Affordable Care Act (ACA). Most health reform changes apply regardless

AFFORDABLE CARE ACT Employers that offer health care coverage to employees are responsible for complying with many of the provisions of the Affordable Care Act (ACA). Most health reform changes apply regardless

6/20/13 Presented By: Mike Marchini, Beckie Lewis, & Liz Logsdon or

CBIZ PRESENTS Affordable Care Act: The Impact on Your Business & Your Employees 6/20/13 Presented By: Mike Marchini, Beckie Lewis, & Liz Logsdon 301-777-1500 or 800-624-0954 Determine Which PPACA Provisions

CBIZ PRESENTS Affordable Care Act: The Impact on Your Business & Your Employees 6/20/13 Presented By: Mike Marchini, Beckie Lewis, & Liz Logsdon 301-777-1500 or 800-624-0954 Determine Which PPACA Provisions

Marketplace 101. Find health care options that meet your needs and fit your budget

Marketplace 101 Find health care options that meet your needs and fit your budget Objectives This session will help you Explain the Health Insurance Marketplace Define who might be eligible Define options

Marketplace 101 Find health care options that meet your needs and fit your budget Objectives This session will help you Explain the Health Insurance Marketplace Define who might be eligible Define options

AFFORDABLE CARE ACT LARGE EMPLOYER HEALTH REFORM CHECKLIST. Edition: August 2015

AFFORDABLE CARE ACT Employers that offer health care coverage to employees are responsible for complying with many of the provisions of the Affordable Care Act (ACA). Most health reform changes apply regardless

AFFORDABLE CARE ACT Employers that offer health care coverage to employees are responsible for complying with many of the provisions of the Affordable Care Act (ACA). Most health reform changes apply regardless

ACA Regulations: Insurance Exchanges and EHBs

ACA Regulations: Insurance Exchanges and EHBs 1 Insurance Exchanges Insurance Exchanges: Exchanges are online marketplaces More than 20 million individuals and employees of small businesses may purchase

ACA Regulations: Insurance Exchanges and EHBs 1 Insurance Exchanges Insurance Exchanges: Exchanges are online marketplaces More than 20 million individuals and employees of small businesses may purchase

STUDENTS GUIDE TO THE AFFORDABLE CARE ACT Grant Atkinson J.D, NAGPS Legal Concerns Chair, August 25, 2013

STUDENTS GUIDE TO THE AFFORDABLE CARE ACT Grant Atkinson J.D, NAGPS Legal Concerns Chair, August 25, 2013 What do students need to know about the the Affordable Care Act? THE BASICS: 1) It encourages you

STUDENTS GUIDE TO THE AFFORDABLE CARE ACT Grant Atkinson J.D, NAGPS Legal Concerns Chair, August 25, 2013 What do students need to know about the the Affordable Care Act? THE BASICS: 1) It encourages you

Washington Health Benefit Exchange

Washington Health Benefit Exchange AFFORDABLE CARE ACT 101 APRIL 26, 2013 Christine Brown Navigator/In-person Assister Program Today s Agenda History of the Affordable Care Act (ACA) Highlights of the

Washington Health Benefit Exchange AFFORDABLE CARE ACT 101 APRIL 26, 2013 Christine Brown Navigator/In-person Assister Program Today s Agenda History of the Affordable Care Act (ACA) Highlights of the

5/5/2014. The Affordable Care Act* 45 th Annual WMSHP Spring Seminar. The Affordable Care Act (ACA) March 23,2010

March 23,2010") The Affordable Care Act* 45 th Annual WMSHP Spring Seminar Richard Lichtenstein, PhD, MPH S.J. Axelrod Collegiate Professor of Health Management and Policy University of Michigan School of Public Health

The Affordable Care Act* 45 th Annual WMSHP Spring Seminar Richard Lichtenstein, PhD, MPH S.J. Axelrod Collegiate Professor of Health Management and Policy University of Michigan School of Public Health

Affordable Care Act Resource Guide

Affordable Care Act Resource Guide for Businesses with fewer than 50 employees Effective January 22, 2016 Form No. 3-1018 (02-16) The information in this document is a general overview of the rules, regulations

Affordable Care Act Resource Guide for Businesses with fewer than 50 employees Effective January 22, 2016 Form No. 3-1018 (02-16) The information in this document is a general overview of the rules, regulations

Health Insurance Marketplace

Health Insurance Marketplace Briefing on the Affordable Care Act 2014 Ben J. Altheimer Oral Symposium UALR Bowen School of Law February 28, 2014 David Nilasena, MD Centers for Medicare & Medicaid Services

Health Insurance Marketplace Briefing on the Affordable Care Act 2014 Ben J. Altheimer Oral Symposium UALR Bowen School of Law February 28, 2014 David Nilasena, MD Centers for Medicare & Medicaid Services

ACA in Brief 2/18/2014. It Takes Three Branches... Overview of the Affordable Care Act. Health Insurance Coverage, USA, % 16% 55% 15% 10%

Health Insurance Coverage, USA, 2011 16% Uninsured Overview of the Affordable Care Act 55% 16% Medicaid Medicare Private Non-Group Philip R. Lee Institute for Health Policy Studies Janet Coffman, MPP,

Health Insurance Coverage, USA, 2011 16% Uninsured Overview of the Affordable Care Act 55% 16% Medicaid Medicare Private Non-Group Philip R. Lee Institute for Health Policy Studies Janet Coffman, MPP,

Insurance (Coverage) Reform

Reform") Arkansas Health Law Check Up Insurance (Coverage) Reform Create Insurance Marketplaces For individuals & small businesses Expand Medicaid to 138% FPL Arkansas alternative = Private Option, not Arkansas

Arkansas Health Law Check Up Insurance (Coverage) Reform Create Insurance Marketplaces For individuals & small businesses Expand Medicaid to 138% FPL Arkansas alternative = Private Option, not Arkansas

Health Care Reform Information for Employees. Your options under health care reform

Health Care Reform Information for Employees Your options under health care reform Patient Protection and Affordable Care Act (PPACA) September 2013 Contents 1 Your options under health care reform 2 Health

Health Care Reform Information for Employees Your options under health care reform Patient Protection and Affordable Care Act (PPACA) September 2013 Contents 1 Your options under health care reform 2 Health

AFFORDABLE CARE ACT (ACA)

") AFFORDABLE CARE ACT (ACA) Presented By ANDREW H. HOOK, CELA, CFP, AEP 295 Bendix Road, Suite 170, Virginia Beach, VA 23452 5806 Harbour View Blvd., Suite 203, Suffolk, VA 23435 Tel: 757-399-7506 Fax: 757-397-1267

AFFORDABLE CARE ACT (ACA) Presented By ANDREW H. HOOK, CELA, CFP, AEP 295 Bendix Road, Suite 170, Virginia Beach, VA 23452 5806 Harbour View Blvd., Suite 203, Suffolk, VA 23435 Tel: 757-399-7506 Fax: 757-397-1267

IMPLICATIONS OF THE AFFORDABLE CARE ACT FOR COUNTY EMPLOYERS

IMPLICATIONS OF THE AFFORDABLE CARE ACT FOR COUNTY EMPLOYERS Mississippi Association of Supervisors Annual Convention Biloxi, Mississippi June 20, 2013 Presented by Leslie Scott MAS General Counsel Group

IMPLICATIONS OF THE AFFORDABLE CARE ACT FOR COUNTY EMPLOYERS Mississippi Association of Supervisors Annual Convention Biloxi, Mississippi June 20, 2013 Presented by Leslie Scott MAS General Counsel Group

Employer Obligations and Coverage Options under the Affordable Care Act in 2014/2015

Employer Obligations and Coverage Options under the Affordable Care Act in 2014/2015 C H I C A G O S O U T H L A N D C H A M B E R O F C O M M E R C E J U L Y 1 5, 2 0 1 3 L A U R A M I N Z E R E X E C

Employer Obligations and Coverage Options under the Affordable Care Act in 2014/2015 C H I C A G O S O U T H L A N D C H A M B E R O F C O M M E R C E J U L Y 1 5, 2 0 1 3 L A U R A M I N Z E R E X E C

The MC Academy The Employee Benefits and Executive Compensation Series HEALTH CARE REFORM ACT

The MC Academy The Employee Benefits and Executive Compensation Series HEALTH CARE REFORM ACT April 16, 2013 Topics Health Care Reform under the Patient Protection and Affordable Care Act Overview Exchanges

The MC Academy The Employee Benefits and Executive Compensation Series HEALTH CARE REFORM ACT April 16, 2013 Topics Health Care Reform under the Patient Protection and Affordable Care Act Overview Exchanges

Employer Health Small Employer Health

Employer Health Small Employer Health Overview of the ACA and Wisconsin Medicaid Reforms. Covering Kids & Families Wisconsin Wisconsin Primary Health Care Association

Overview of the ACA and Wisconsin Medicaid Reforms Covering Kids & Families Wisconsin Wisconsin Primary Health Care Association Updated September 9, 2013 Topics to be Covered What is the ACA? Wisconsin

Overview of the ACA and Wisconsin Medicaid Reforms Covering Kids & Families Wisconsin Wisconsin Primary Health Care Association Updated September 9, 2013 Topics to be Covered What is the ACA? Wisconsin

Affordable Care Act: Impact on the Indiana Market

1 Affordable Care Act: Impact on the Indiana Market Seema Verma President SVC, Inc 2 Affordable Care Act Key accomplishment is access ~48.6 million uninsured in America* ~800 thousand uninsured in Indiana*

1 Affordable Care Act: Impact on the Indiana Market Seema Verma President SVC, Inc 2 Affordable Care Act Key accomplishment is access ~48.6 million uninsured in America* ~800 thousand uninsured in Indiana*

Health Care Reform: What s In Store for Employer Health Plans?

Health Care Reform: What s In Store for Employer Health Plans? April 21, 2010 Presented by: Sue O. Conway sconway@wnj.com (616) 752-2153 Norbert F. Kugele nkugele@wnj.com (616) 752-2186 Copyright 2010

Health Care Reform: What s In Store for Employer Health Plans? April 21, 2010 Presented by: Sue O. Conway sconway@wnj.com (616) 752-2153 Norbert F. Kugele nkugele@wnj.com (616) 752-2186 Copyright 2010

Healthcare Reform Better Care Reconciliation Act Repeal & Replace

BCRA AHCA American Health Care Act Healthcare Reform Better Care Reconciliation Act Repeal & Replace ACA HCR Affordable Care Act BCRA, AHCA and ACA On June 22, 2017, Senate Republicans released the Better

BCRA AHCA American Health Care Act Healthcare Reform Better Care Reconciliation Act Repeal & Replace ACA HCR Affordable Care Act BCRA, AHCA and ACA On June 22, 2017, Senate Republicans released the Better

Understanding the Health Insurance Marketplace. August 2013

Understanding the Health Insurance Marketplace August 2013 Objectives This session will help you Explain the Health Insurance Marketplace Identify who will benefit Define who is eligible Explain the enrollment

Understanding the Health Insurance Marketplace August 2013 Objectives This session will help you Explain the Health Insurance Marketplace Identify who will benefit Define who is eligible Explain the enrollment

HEALTH CONCEPTS AND TAX CONSIDERATIONS

14 HEALTH CONCEPTS AND TAX CONSIDERATIONS LEARNING OBJECTIVES Upon the completion of this chapter, you will be able to: 1. Recognize the features of health insurance policies that have been mandated by

14 HEALTH CONCEPTS AND TAX CONSIDERATIONS LEARNING OBJECTIVES Upon the completion of this chapter, you will be able to: 1. Recognize the features of health insurance policies that have been mandated by

Help your constituents gain the most from the Affordable Care Act

1 Help your constituents gain the most from the Affordable Care Act Quick refresher course on Covered California: your destination for affordable, quality health care, including Medi-Cal Help your constituents

1 Help your constituents gain the most from the Affordable Care Act Quick refresher course on Covered California: your destination for affordable, quality health care, including Medi-Cal Help your constituents

What s Inside STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT (ACA)

") What s Inside Step 1: What Understand what you re buying 4 Step 2: How How can you buy health insurance? 20 STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT (ACA) Want to know more about the health reform

What s Inside Step 1: What Understand what you re buying 4 Step 2: How How can you buy health insurance? 20 STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT (ACA) Want to know more about the health reform

Impact on the State Health Insurance Program of the Patient Protection and Affordable Care Act

Impact on the State Health Insurance Program of the Patient Protection and Affordable Care Act Adopted August 20, 2012 by the Self-Insurance Estimating Conference Prepared by: Florida Department of Management

Impact on the State Health Insurance Program of the Patient Protection and Affordable Care Act Adopted August 20, 2012 by the Self-Insurance Estimating Conference Prepared by: Florida Department of Management

AFFORDABLE CARE ACT LARGE EMPLOYER HEALTH REFORM CHECKLIST

www.thinkhr.com AFFORDABLE CARE ACT LARGE EMPLOYER HEALTH REFORM CHECKLIST Employers that provide health coverage to employees are responsible for complying with many of the provisions of the Affordable

www.thinkhr.com AFFORDABLE CARE ACT LARGE EMPLOYER HEALTH REFORM CHECKLIST Employers that provide health coverage to employees are responsible for complying with many of the provisions of the Affordable

Affordable Care Act Overview

Affordable Care Act Overview Your guide to health care reform law 208 Edition The foregoing information is general in nature and is intended to keep you apprised of certain important developments. This

Affordable Care Act Overview Your guide to health care reform law 208 Edition The foregoing information is general in nature and is intended to keep you apprised of certain important developments. This

Needs for publicly funded behavioral health services under the Patient Protection and Affordable Care Act (ACA): What gaps will remain?

: What gaps will remain?") Needs for publicly funded behavioral health services under the Patient Protection and Affordable Care Act (ACA): What gaps will remain? February 4, 2014 Stan Dorn (sdorn@urban.org) Senior Fellow, Health

Needs for publicly funded behavioral health services under the Patient Protection and Affordable Care Act (ACA): What gaps will remain? February 4, 2014 Stan Dorn (sdorn@urban.org) Senior Fellow, Health

What s Inside STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT (ACA)

") What s Inside Step 1: What Understand what you re buying 4 Step 2: How How can you buy health insurance? 18 STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT (ACA) Want to know more about the health reform

What s Inside Step 1: What Understand what you re buying 4 Step 2: How How can you buy health insurance? 18 STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT (ACA) Want to know more about the health reform

Health Care Reform: Not Everything Has Been Delayed

Health Care Reform: Not Everything Has Been Delayed HR. Payroll. Benefits. Contents Introduction 3 What Has Been Delayed? 5 Who Is Eligible for a Federal Subsidy? 7 How Much Will Coverage Cost if a Subsidy

Health Care Reform: Not Everything Has Been Delayed HR. Payroll. Benefits. Contents Introduction 3 What Has Been Delayed? 5 Who Is Eligible for a Federal Subsidy? 7 How Much Will Coverage Cost if a Subsidy

8/7/2013 INSURANCE MADE SIMPLE. 1

Presented by: Mark E. Baker Vice President Employee Benefits INSURANCE MADE SIMPLE. 1 Health Care Reform provisions in effect 2010-2012 Large Employer Defined Pay or Play Mandate and Penalties Small Employer

Presented by: Mark E. Baker Vice President Employee Benefits INSURANCE MADE SIMPLE. 1 Health Care Reform provisions in effect 2010-2012 Large Employer Defined Pay or Play Mandate and Penalties Small Employer

Health Care Reform. The Affordable Care Act

1 Health Care Reform The Affordable Care Act House Keeping items.. 1. All phone lines are muted so please send any questions you may have via the chat session during the webinar. 2. All slides will be

1 Health Care Reform The Affordable Care Act House Keeping items.. 1. All phone lines are muted so please send any questions you may have via the chat session during the webinar. 2. All slides will be

AFFORDABLE CARE ACT FAQ

AFFORDABLE CARE ACT FAQ What is the Healthcare Insurance Marketplace? The Marketplace is a new way to find quality health coverage. It can help if you don t have coverage now or if you have it but want

AFFORDABLE CARE ACT FAQ What is the Healthcare Insurance Marketplace? The Marketplace is a new way to find quality health coverage. It can help if you don t have coverage now or if you have it but want

Affordable Care Act. Small Businesses with 1-49 Employees. Simplified for. Questions?

Affordable Care Act Simplified for Small Businesses with 1-49 Employees Questions? Email smallbizhealth@intuit.com @2013 Intuit, Inc. All Rights Reserved. Summary Starting on January 1, 2014, the Affordable

Affordable Care Act Simplified for Small Businesses with 1-49 Employees Questions? Email smallbizhealth@intuit.com @2013 Intuit, Inc. All Rights Reserved. Summary Starting on January 1, 2014, the Affordable

Health Care Reform: Fact vs. Fiction for Small Business. What employers should be thinking about now to prepare for 2015

Health Care Reform: Fact vs. Fiction for Small Business What employers should be thinking about now to prepare for 2015 Fact vs. Fiction Healthcare is less expensive overall: Fact or fiction? Employers

Health Care Reform: Fact vs. Fiction for Small Business What employers should be thinking about now to prepare for 2015 Fact vs. Fiction Healthcare is less expensive overall: Fact or fiction? Employers

What s Next for States The Affordable Care Act Post Implementation. Seema Verma, MPH President SVC, Inc

What s Next for States The Affordable Care Act Post Implementation Seema Verma, MPH President SVC, Inc sverma@svcinc.org *Utah, New Mexico & Mississippi will operate a state-base SHOP Exchange but individual

What s Next for States The Affordable Care Act Post Implementation Seema Verma, MPH President SVC, Inc sverma@svcinc.org *Utah, New Mexico & Mississippi will operate a state-base SHOP Exchange but individual

YOUR BUSINESS YOUR FUTURE: How The Affordable Care Act Will Affect Your Business in 2014 and 2015

YOUR BUSINESS YOUR FUTURE: www.genemarks.com How The Affordable Care Act Will Affect Your Business in 2014 and 2015 FALSE TRUE TRUE TRUE The Latest Projections House 435 Members Right Now Projected Results

YOUR BUSINESS YOUR FUTURE: www.genemarks.com How The Affordable Care Act Will Affect Your Business in 2014 and 2015 FALSE TRUE TRUE TRUE The Latest Projections House 435 Members Right Now Projected Results

An Update on Commercial Exchanges. Myra Weisfeld, Senior Managing Consultant

An Update on Commercial Exchanges Myra Weisfeld, Senior Managing Consultant Agenda Introduction & overview ACA Changes to insurance coverage Insurance exchange update Summary & questions 2 3 4 Payment

An Update on Commercial Exchanges Myra Weisfeld, Senior Managing Consultant Agenda Introduction & overview ACA Changes to insurance coverage Insurance exchange update Summary & questions 2 3 4 Payment

11/14/2013. Overview. Employer Mandate Exchanges Medicaid Expansion Funding. Medicare Taxes & Fees. Discussion

Michael A. Morrisey, Ph.D. Lister Hill Center for Health Policy University of Alabama at Birmingham Atlanta Federal Reserve Bank November 14, 2013 Individual Mandate Employer Mandate Exchanges Medicaid

Michael A. Morrisey, Ph.D. Lister Hill Center for Health Policy University of Alabama at Birmingham Atlanta Federal Reserve Bank November 14, 2013 Individual Mandate Employer Mandate Exchanges Medicaid

Complying with Health Care Reform

Complying with Health Care Reform April 17, 2013 1 1 What Happened? In March 2010, Congress passed and the President signed health reform in: The Patient Protection and Affordable Care Act The Health Care

Complying with Health Care Reform April 17, 2013 1 1 What Happened? In March 2010, Congress passed and the President signed health reform in: The Patient Protection and Affordable Care Act The Health Care

Presenters Marc J. Smith Mary-Michal Rawling

Presenters Marc J. Smith Mary-Michal Rawling The Affordable Care Act (ACA) Starting in January 1, 2014 it will be Required that most U.S. citizens and legal residents obtain and maintain healthcare coverage

Presenters Marc J. Smith Mary-Michal Rawling The Affordable Care Act (ACA) Starting in January 1, 2014 it will be Required that most U.S. citizens and legal residents obtain and maintain healthcare coverage

AFFORDABLE CARE ACT SMALL EMPLOYER HEALTH REFORM CHECKLIST

www.thinkhr.com AFFORDABLE CARE ACT SMALL EMPLOYER HEALTH REFORM CHECKLIST Small Employer Health Employers that provide health coverage to employees are responsible for complying with many of the provisions

www.thinkhr.com AFFORDABLE CARE ACT SMALL EMPLOYER HEALTH REFORM CHECKLIST Small Employer Health Employers that provide health coverage to employees are responsible for complying with many of the provisions

Affordable Care Act Resource Guide

Affordable Care Act Resource Guide for Businesses with 50 or more employees Effective January 22, 2015 Form No. 3-1019 (02-16) The information in this document is a general overview of the rules, regulations

Affordable Care Act Resource Guide for Businesses with 50 or more employees Effective January 22, 2015 Form No. 3-1019 (02-16) The information in this document is a general overview of the rules, regulations

Understanding the Health Insurance Marketplace. September 2013

Understanding the Health Insurance Marketplace September 2013 1. Health Insurance Marketplace To provide qualified individuals and employers Access to affordable coverage options Ability to buy certain

Understanding the Health Insurance Marketplace September 2013 1. Health Insurance Marketplace To provide qualified individuals and employers Access to affordable coverage options Ability to buy certain

The Affordable Care Act: Time to Prepare for 2014 and Beyond

The Affordable Care Act: Time to Prepare for 2014 and Beyond Howard Van Mersbergen Vice President of Employee Benefits, Christian Schools International Brian C. Meekhof Benefits Administrator, Christian

The Affordable Care Act: Time to Prepare for 2014 and Beyond Howard Van Mersbergen Vice President of Employee Benefits, Christian Schools International Brian C. Meekhof Benefits Administrator, Christian

Module IV PLAN DESIGN

Module IV PLAN DESIGN Plan Design Benefits Deductible Cost Sharing Out of Pocket Actuarial Value 2 Think about your spreadsheets 3 ESSENTIAL BENEFITS 4 Mandated Benefits Small Group Mandates in Texas Source:

Module IV PLAN DESIGN Plan Design Benefits Deductible Cost Sharing Out of Pocket Actuarial Value 2 Think about your spreadsheets 3 ESSENTIAL BENEFITS 4 Mandated Benefits Small Group Mandates in Texas Source:

The Affordable Care Act: A Summary on Healthcare Reform. The Wyoming Department of Insurance

The Affordable Care Act: A Summary on Healthcare Reform The Wyoming Department of Insurance Additional Resources Wyoming Insurance Department: http://doi.wyo.gov/ or toll free at 1-(800)-438-5768 Information

The Affordable Care Act: A Summary on Healthcare Reform The Wyoming Department of Insurance Additional Resources Wyoming Insurance Department: http://doi.wyo.gov/ or toll free at 1-(800)-438-5768 Information

AFFORDABLE CARE ACT (ACA) UPDATE JUNE 26, 2013

UPDATE JUNE 26, 2013") AFFORDABLE CARE ACT (ACA) UPDATE JUNE 26, 2013 FREDDY WARNER SYSTEM EXECUTIVE, PUBLIC POLICY & GOVERNMENT RELATIONS MEMORIAL HERMANN HEALTH SYSTEM ACA - REVISITED OBAMA SIGNED INTO LAW 2010 GOALS PROVIDE

AFFORDABLE CARE ACT (ACA) UPDATE JUNE 26, 2013 FREDDY WARNER SYSTEM EXECUTIVE, PUBLIC POLICY & GOVERNMENT RELATIONS MEMORIAL HERMANN HEALTH SYSTEM ACA - REVISITED OBAMA SIGNED INTO LAW 2010 GOALS PROVIDE