Help your constituents gain the most from the Affordable Care Act

|

|

|

- Randell Garrison

- 5 years ago

- Views:

Transcription

1 1

2 Help your constituents gain the most from the Affordable Care Act Quick refresher course on Covered California: your destination for affordable, quality health care, including Medi-Cal Help your constituents with three big questions: 1. What s in it for me? 2. What do I need to consider in making a decision? 3. How do I enroll? Get ready for enrollment on October 1,

3 Eligible if: A U.S. Citizen, U.S. National, or a non-citizen who is Lawfully Present in the U.S.; For Medi-Cal, immigration status only effects the scope of service (e.g. emergency room only or pregnancy only ) A California Resident; AND Not incarcerated, other than incarceration pending the disposition (judgment) of charges. Except Medi-Cal Inmate Eligibility Program 3

4 Eligible for Premium Assistance and Cost-Sharing Subsidies in Covered California if: Purchase coverage through Covered California; Under certain income requirements; AND Not eligible for Minimum Essential Coverage (i.e. Medi-Cal, Medicare, or coverage through an employer that is affordable). 4

5 Quick summary of income ranges Cost Sharing + Premium Assistance Premium Assistance Only Medi-Cal Medi-Cal for Children (up to 266%) Number Up to or at 138% Over 138% 150% 200% 250% 400% 1 $15,856 $15,857 $17,235 $22,980 $28,725 $45,960 2 $21,403 $21,404 $23,265 $31,020 $38,775 $62,040 3 $26,951 $26,952 $29,295 $39,060 $48,825 $78,120 4 $32,499 $32,500 $35,325 $47,100 $58,875 $94,200 5

6 What are you eligible for? 138% FPL Low or No Cost Medi-Cal Covered California Over 138% FPL to 400% FPL Over 138% FPL to 250% FPL Over 250% FPL to 400% FPL Adults: Covered California Premium Assistance + Enhanced Benefits* *Must enroll in a Silver-level plan to receive enhanced benefits Covered California Premium Assistance with Standard Benefits Children: Low or No Cost Medi-Cal* Up to 266% FPL Over 400% FPL Option for Covered California with Standard Benefits and Prices 6

7 Modified Adjusted Gross Income (MAGI) is a driver of eligibility Take your: Adjusted Gross Income + Non-taxable Social Security benefits (Line 20a minus 20b on a Form 1040) Tax-exempt interest (Line on 8b on a Form 1040) Foreign earned income & housing expenses for Americans living abroad (calculated on a Form 2555) _ For Medi-Cal Eligibility, Exclude From Income: Scholarships, awards, or fellowship grants used for education purposes (not living expenses) Certain American Indian and Alaska Native income derived from distributions, payments, ownership interests, real property usage rights, and student financial assistance An amount received as a lump sum is counted as income only in the month received 7

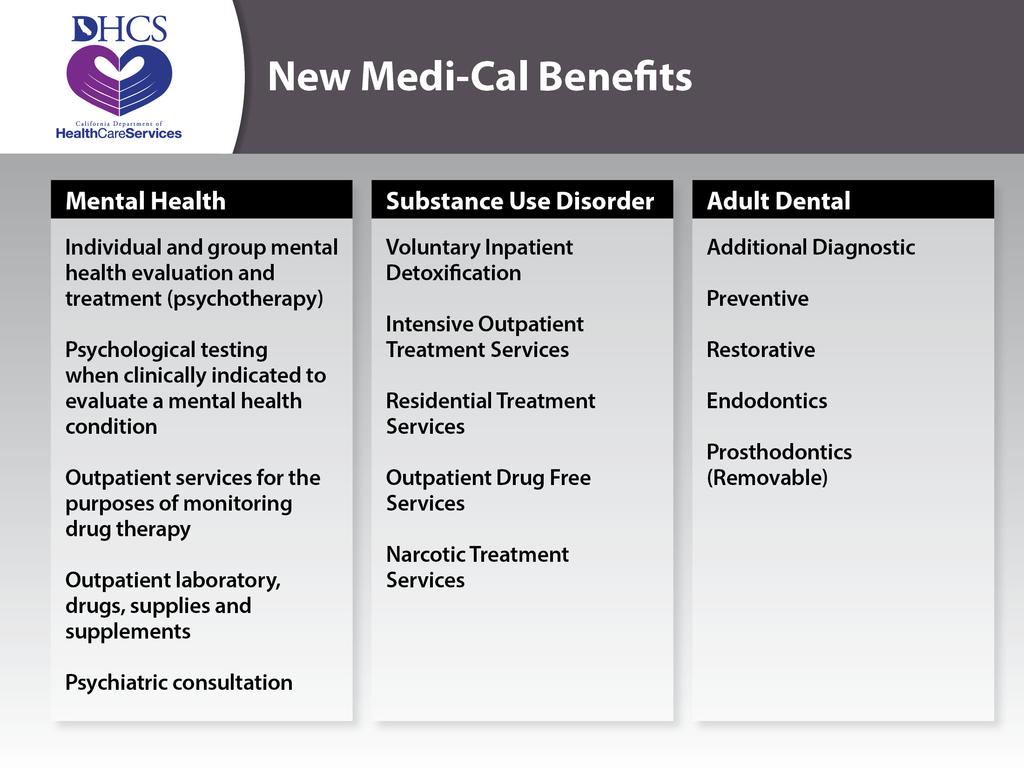

8 The Essential Health Benefits 8

9 Medi-Cal 9

10 10

11 We ve Streamlined the Application Process Applying at Covered California, lets you know if your income makes you eligible for affordable coverage Enrolling: Service Center: We ll help you find your local Medi-Cal county office for quick help. Certified Enrollment Counselor or Certified Insurance Agent: Our counselors and agents will let applicants know their status. County Social Services Office: Where applicants can get their full Medi-Cal eligibility determination using MAGI and Non-MAGI income eligibility rules. 11

12 We ve Simplified Eligibility and How We Verify Information We allow self-attestation & reasonably compatible reviews We have access to a federal electronic verification hub We ll use the MAGI income standard We ve made verifying state residency easier 12

13 Medi-Cal Eligibility by Population Medi-Cal Populations Old Eligibility New Eligibility Adult Population, N/A Up to 138% Parents/Caretaker Relatives Up to 125% Up to 138% Pregnant Women Up to 200% Up to 213% Access for Infants and Mothers Up to 300% Up to 322% Children Up to 250% Up to 266% Over age 65, Blind, or have a disability SSI/SSP recipients and those deemed to be SSI/SSP recipients 1915 home and community-based waivers participants Nursing facility level of care beneficiaries Medicare Savings Program recipients Foster Care/Adoption Assistance and those for whom the State relies on an Express Lane Agency finding of income Medically Needy 13

14 Medi-Cal Eligibility: MAGI Population Medi-Cal Populations Old Eligibility New Eligibility Adult Population, N/A Up to 138% Parents/Caretaker Relatives Up to 125% Up to 138% Pregnant Women Up to 200% Up to 213% Access for Infants and Mothers Up to 300% Up to 322% Children Up to 250% Up to 266% Over age 65, Blind, or have a disability SSI/SSP recipients and those deemed to be SSI/SSP recipients 1915 home and community-based waivers participants MAGI Population Nursing facility level of care beneficiaries Medicare Savings Program recipients Foster Care/Adoption Assistance and those for whom the State relies on an Express Lane Agency finding of income Medically Needy 14

15 Medi-Cal Eligibility: Non-MAGI Population Medi-Cal Populations Old Eligibility New Eligibility Adult Population, N/A Up to 138% Parents/Caretaker Relatives Up to 125% Up to 138% Pregnant Women Up to 200% Up to 213% Non-MAGI Population Access for Infants and Mothers Up to 300% Up to 322% Children Up to 250% Up to 266% Over age 65, Blind, or have a disability SSI/SSP recipients and those deemed to be SSI/SSP recipients 1915 home and community-based waivers participants Nursing facility level of care beneficiaries Medicare Savings Program recipients Foster Care/Adoption Assistance and those for whom the State relies on an Express Lane Agency finding of income Medically Needy 15

16 Medi-Cal Eligible: NOW Medi-Cal Populations Old Eligibility New Eligibility Adult Population, N/A Up to 138% Parents/Caretaker Relatives Up to 125% Up to 138% Pregnant Women Up to 200% Up to 213% Access for Infants and Mothers Up to 300% Up to 322% Children Up to 250% Up to 266% Over age 65, Blind, or have a disability SSI/SSP recipients and those deemed to be SSI/SSP recipients 1915 home and community-based waivers participants Medi-Cal Eligible NOW! Nursing facility level of care beneficiaries Medicare Savings Program recipients Foster Care/Adoption Assistance and those for whom the State relies on an Express Lane Agency finding of income Medically Needy 16

17 Medi-Cal Eligible: Starting January 1, 2014 Medi-Cal Populations Old Eligibility New Eligibility Adult Population, N/A Up to 138% Parents/Caretaker Relatives Up to 125% Up to 138% Pregnant Women Up to 200% Up to 213% Access for Infants and Mothers Up to 300% Up to 322% Children Up to 250% Up to 266% Over age 65, Blind, or have a disability SSI/SSP recipients and those deemed to be SSI/SSP recipients 1915 home and community-based waivers participants Newly Medi-Cal Eligible January 1, 2014 Nursing facility level of care beneficiaries Medicare Savings Program recipients Foster Care/Adoption Assistance and those for whom the State relies on an Express Lane Agency finding of income Medically Needy 17

18 Covered California Marketplace 18

19 Covered California Health Plan Essential Health Benefits Ambulatory patient services Emergency services Hospitalization Maternity and newborn care Mental health and substance use disorder services, including behavioral health treatment Prescription drugs Rehabilitative and habilitative services and devices Laboratory services Preventive and wellness services and chronic disease management Pediatric services Standard Benefit Design All Covered California Health Plans cover the same health care services Benefit plans have different levels of cost sharing with the consumer through copays, deductibles, and coinsurance 19

20 Covered California Does Not Offer Medicare Supplemental Plans Adult Vision Plans Adult Dental Plans (coming plan year 2015!) 20

21 New Rules for Equitable Premium Calculation Premium rate is driven by Age Zip code which drives pricing region Benefit plan selected 138% to 400% of Poverty Consumer pays Fair Share percent of income ranging from 2% to 9.5% Premium assistance (in the form of the advance tax credit) paying the balance 21

22 Premium rate is age sensitive.635 factor for children; 1:3 maximum ratio for adults Monthly Premium per Person $600 $500 $400 $300 $200 $ AGE 22

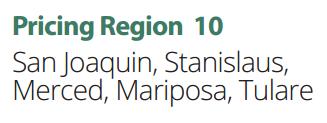

23 Pricing Regions 23

24 Pricing Regions with Average Silver-level Plan Cost 2 nd Lowest Silver-Level Plan Rates for a 40-year-old, by Rating Region 1 $ $322 2 $ $288 Sacramento 3 $ $326 4 $ $396 San Francisco 5 $ $281 6 $ $252 Los Angeles 7 $ $259 San Diego 8 $ $259 9 $ $ $308 24

25 Subsidy Eligible by Region 25

26 Premium rates influenced by benefit plan Plan pays an average percent of health care costs ranging from 60% to 90% 100% 80% Consumer Pays Consumer Pays Consumer Pays Consumer Pays 60% 40% 20% Plan Pays Plan Pays Plan Pays Plan Pays 0% Bronze 60 Silver 70 Gold 80 Platinum 90 Actuarial Value or AV is the expected percent coverage. Gold has an AV of 80% 26

27 The value of premium assistance is sensitive to age $600 $500 Premium assistance is the difference between the actual premium and the consumers fair share payment $400 $300 $200 $100 Premium Assistance Zone Fair Share Payment = % of Household Income 21 years old 64 years old 27

28 Premium assistance eligible consumers pay fair share amounts regardless of age; the premium assistance makes up the difference $600 Fair Share payment + Premium Assistance = Premium for 2 nd Lowest Silver 70 plan Monthly Payment $500 $400 $300 $200 $100 $183 Premium Assistance from IRS $639 $45 Fair Share payment $45 $228 total premium $684 total premium 21 years old 64 years old NOTE: Example reflects 2014 rates for Fresno using 2 nd lowest priced Silver 70 plan 28

29 Premium Assistance as Federal Income Tax Credit Consumers eligible for premium assistance have a choice of how to take advantage of the tax credit: Wait until taxes are filed In Advance Paid monthly directly to health insurer Consumer has risk of over payment or underpayment if income fluctuates If income changes, consumer encouraged to contact Covered California to make adjustment 29

30 Affordability = premium + out of pocket expenses Premium assistance addresses monthly affordability of premium Consumer pays fair share percent of income Cost only goes up if income goes up Out of pocket affordability addressed through enhanced benefits Consumers with income ranging from 138% to 200% of FPL eligible for Platinum level coverage 30

31 Reduced cost sharing improves affordability for many In addition to the premium assistance that helps pay for the monthly premium, many consumers are also eligible for Enhanced Silver plans with very generous benefits to help pay for out-of-pocket costs. 100% 80% 60% 40% Silver 94 Silver 87 Silver 73 Platinum Level Coverage at Silver Level Price Silver 70 20% 0% 140% - 150% 150% - 200% 200% - 250% 250% - 400% Income as Percent of Federal Poverty Level (FPL) 31

32 $1 of income can make a huge difference Medi-Cal Cost Sharing + Premium Assistance Medi-Cal for Children (up to 266%) Premium Assistance Only Number Up to or at 138% Over 138% 150% 200% 250% 400% 1 $15,856 $15,857 $17,235 $22,980 $28,725 $45,960 2 $21,403 $21,404 $23,265 $31,020 $38,775 $62,040 3 $26,951 $26,952 $29,295 $39,060 $48,825 $78,120 4 $32,499 $32,500 $35,325 $47,100 $58,875 $94,200 32

33 What is the definition of family? Under the Affordable Care Act, a family is defined by your Modified Adjust Gross Income (MAGI) household. Family = You (taxpayer) + Spouse (if applicable and must file jointly) + Claimed Dependent(s) (must not be claimed by another) Family Size = Number of individuals in the family Household Income = The sum of the taxpayer s MAGI plus the MAGI of tax dependents in the family if they are required to file 33

34 34

35 How to use the Shop and Compare Tool At home on your computer On your tablet from the Apple or Google app store On your phone from the Apple or Google app store 35

Dependents: None Pricing Region: 13 (Imperial County Zip: 92232) *Modified adjusted gross income")

36 Scenario 1: Eligible for Premium Assistance and Cost-Sharing Subsidies Zachary Age: 55 Marital Status: Single Annual Income*: $22,000 (~190% of the Federal Poverty Level) Dependents: None Pricing Region: 13 (Imperial County Zip: 92232) *Modified adjusted gross income 21

37 37 Scenario 1: Eligible for Premium Assistance and Cost-Sharing Subsidies Zachary ELIGIBLE FOR... Covered California Health Plan: Under 400% FPL Premium Assistance Under 250% FPL Cost-Sharing Assistance Age: 55 Marital Status: Single Annual Income*: $22,000 (~190% of the Federal Poverty Level) Dependents: None Pricing Region: 13 (Imperial County Zip: 92232) *Modified adjusted gross income

38 38 Scenario 1: Eligible for Premium Assistance and Cost-Sharing Subsidies Zachary ELIGIBLE FOR... Covered California Health Plan: Under 400% FPL Premium Assistance Under 250% FPL Cost-Sharing Assistance Age: 55 Marital Status: Single Annual Income*: $22,000 (~190% of the Federal Poverty Level) Dependents: None Pricing Region: 13 (Imperial County Zip: 92232) *Modified adjusted gross income

39 Scenario 1: Eligible for Premium Assistance and Cost-Sharing Subsidies 39 Zachary ELIGIBLE FOR... Covered California Health Plan: Under 400% FPL Premium Assistance Under 250% FPL Cost-Sharing Assistance Age: 55 Marital Status: Single Annual Income*: $22,000 (~190% of the Federal Poverty Level) Dependents: None Pricing Region: 13 (Imperial County Zip: 92232) *Modified adjusted gross income

40 Three Three Takeaways: 1. Must enroll in a Silverlevel health plan to receive cost-sharing subsidies 2. Out-of-pocket costs (including maximum and deductible) become MUCH LOWER when a Silver-level health plan is enhanced with federal cost-sharing subsidies for Zachary, 87% of his outof-pocket costs will be paid by a Silver-level health plan (vs. 60% if selected a Bronzelevel health plan) 3. How much the plan is enhanced is shown by the number next to the metal tier, Enhanced Silver 87 40

41 Minimum Coverage Plan catastrophic coverage plan Offers the same benefits as other plans, but at a much lower monthly premium and much higher out-of-pocket costs (~50/50 AV) If selected, you cannot receive premium assistance or cost-sharing subsidies, even if eligible Eligible for Minimum Coverage Plan if: Under age 30; or Receive a hardship exemption from Health & Human Services because lowest-cost Bronze plan is more than 8% of MAGI income. 41

Eligible for Medi-Cal Under 266% of the federal")

42 Scenario 2: The Martins Multiple Program Family Adult (Diane) Eligible for Premium Assistance Under 400% of the federal poverty level Eligible for Cost-Sharing Subsidies Under 250% of the federal poverty level and enrolls in a Silver-Level Plan Child (Wendy) Eligible for Medi-Cal Under 266% of the federal poverty level 42

43 Scenario 2: Multiple Program Family Child Eligible for Medi-Cal, Mother Eligible for Covered CA The Martins Age: Diane, 35 Marital Status: Single Dependent Children (Wendy): 1 Annual Income*: $35,000 (~225% of Federal Poverty Level) Pricing Region: 3 (El Dorado Zip: 95762) *Modified adjusted gross income

: 1 Annual Income*:")

*Modified adjusted")

44 Scenario 2: Multiple Program Family Child Eligible for Medi-Cal, Mother Eligible for Covered CA The Martins Age: Diane, 35 Marital Status: Single Dependent Children (Wendy): 1 Annual Income*: $35,000 (~225% of Federal Poverty Level) Pricing Region: 3 (El Dorado Zip: 95762) *Modified adjusted gross income 44

45 Scenario 2: Multiple Program Family Child Eligible for Medi-Cal, Mother Eligible for Covered CA The Martins Diane (Adult) will be eligible for: Covered California Health Plan: Under 400% FPL Premium Assistance Under 250% FPL Cost-Sharing Subsidies Age: Diane, 35 Marital Status: Single Dependent Children (Wendy): 1 Annual Income*: $35,000 (~225% of Federal Poverty Level) Pricing Region: 3 (El Dorado Zip: 95762) *Modified adjusted gross income Not shown: Blue Shield of California PPO, $210; Anthem Blue Cross HMO, $348 Wendy (Child) will be eligible for Medi-Cal 45

: 1 Annual Income*: $35,000 (~225% of Federal Poverty Level) Pricing Region: 3 (El")

46 Scenario 2: Multiple Program Family Child Eligible for Medi-Cal, Mother Eligible for Covered CA The Martins Diane (Adult) will be eligible for: Covered California Health Plan: Under 400% FPL Premium Assistance Under 250% FPL Cost-Sharing Subsidies Age: Diane, 35 Marital Status: Single Dependent Children (Wendy): 1 Annual Income*: $35,000 (~225% of Federal Poverty Level) Pricing Region: 3 (El Dorado Zip: 95762) *Modified adjusted gross income Not shown: Blue Shield of California PPO, $210; Anthem Blue Cross HMO, $348 Wendy (Child) will be eligible for Medi-Cal 46

: 1 Annual Income*: $35,000 (~225% of Federal Poverty Level) Pricing Region: 3 (El Dorado Zip: 95762) *Modified adjusted gross income $13 $13 $13 Through Medi-Cal for Families, Wendy")

47 Scenario 2: Multiple Program Family Child Eligible for Medi-Cal, Mother Eligible for Covered CA The Martins Wendy (Child) will be eligible for Medi-Cal Age: Diane, 35 Marital Status: Single Dependent Children (Wendy): 1 Annual Income*: $35,000 (~225% of Federal Poverty Level) Pricing Region: 3 (El Dorado Zip: 95762) *Modified adjusted gross income $13 $13 $13 Through Medi-Cal for Families, Wendy will also be eligible for: 47

: 1 Annual Income*: $35,000 (~225% of Federal Poverty Level) Pricing Region: 3 (El Dorado Zip: 95762) *Modified adjusted gross")

48 Scenario 2: Multiple Program Family Child Eligible for Medi-Cal, Mother Eligible for Covered CA Covered California Standard Benefits: The Martins Age: Diane, 35 Marital Status: Single Dependent Children (Wendy): 1 Annual Income*: $35,000 (~225% of Federal Poverty Level) Pricing Region: 3 (El Dorado Zip: 95762) *Modified adjusted gross income 48

49 49

50 50

51 51

52 52

53 53

HCR FAQ. Covered California Individual and Family Coverage. What is Covered California? What is Obamacare? Are they the same?

HCR FAQ Covered California Individual and Family Coverage What is Covered California? What is Obamacare? Are they the same? Covered California is a new, easy-to-use marketplace established for California

HCR FAQ Covered California Individual and Family Coverage What is Covered California? What is Obamacare? Are they the same? Covered California is a new, easy-to-use marketplace established for California

What is The Affordable Care Act and how does it affect me?

What is The Affordable Care Act and how does it affect me? November 2013 Patient Protection and Affordable Care Act (PPACA) Overview The federal Patient Protection and Affordable Care Act signed by President

What is The Affordable Care Act and how does it affect me? November 2013 Patient Protection and Affordable Care Act (PPACA) Overview The federal Patient Protection and Affordable Care Act signed by President

ObamaCare 101: An Educational Training on Health Reform. Training Workshop

ObamaCare 101: An Educational Training on Health Reform Training Workshop About ITUP ITUP is a non partisan, non profit health policy think tank based in Santa Monica, CA. We are funded by generous grants

ObamaCare 101: An Educational Training on Health Reform Training Workshop About ITUP ITUP is a non partisan, non profit health policy think tank based in Santa Monica, CA. We are funded by generous grants

Presenters Marc J. Smith Mary-Michal Rawling

Presenters Marc J. Smith Mary-Michal Rawling The Affordable Care Act (ACA) Starting in January 1, 2014 it will be Required that most U.S. citizens and legal residents obtain and maintain healthcare coverage

Presenters Marc J. Smith Mary-Michal Rawling The Affordable Care Act (ACA) Starting in January 1, 2014 it will be Required that most U.S. citizens and legal residents obtain and maintain healthcare coverage

Chapter 1: What is the Affordable Care Act?

Chapter 1: What is the Affordable Care Act? The Affordable Care Act (ACA), also known as Obamacare, is a law that aims to help millions of Americans secure health insurance. Many individuals still are

Chapter 1: What is the Affordable Care Act? The Affordable Care Act (ACA), also known as Obamacare, is a law that aims to help millions of Americans secure health insurance. Many individuals still are

OVERVIEW OF THE AFFORDABLE CARE ACT. September 23, 2013

OVERVIEW OF THE AFFORDABLE CARE ACT September 23, 2013 Outline The New Continuum of Coverage Medicaid and CHIP Are Changing The New Marketplaces Insurance Affordability Programs Shared Responsibility Requirement

OVERVIEW OF THE AFFORDABLE CARE ACT September 23, 2013 Outline The New Continuum of Coverage Medicaid and CHIP Are Changing The New Marketplaces Insurance Affordability Programs Shared Responsibility Requirement

Frequently Asked Questions about Health Care Reform and the Affordable Care Act

Frequently Asked Questions about Health Care Reform and the Affordable Care Act HEALTH CARE REFORM OVERVIEW Q 1: What ACA changes are already in place? There are no lifetime dollar limits on essential

Frequently Asked Questions about Health Care Reform and the Affordable Care Act HEALTH CARE REFORM OVERVIEW Q 1: What ACA changes are already in place? There are no lifetime dollar limits on essential

Understanding the Health Insurance Marketplace. August 2013

Understanding the Health Insurance Marketplace August 2013 Objectives This session will help you Explain the Health Insurance Marketplace Identify who will benefit Define who is eligible Explain the enrollment

Understanding the Health Insurance Marketplace August 2013 Objectives This session will help you Explain the Health Insurance Marketplace Identify who will benefit Define who is eligible Explain the enrollment

Presentation by: Champaign County Health Care Consumers (CCHCC) October 26, Welcome!

October 26, Welcome!") The Affordable Care Act (ACA): The Health Insurance Marketplace and Medicaid Presentation by: Champaign County Health Care Consumers (CCHCC) October 26, 2017 Welcome! Goals of the Affordable Care Act (ACA)

The Affordable Care Act (ACA): The Health Insurance Marketplace and Medicaid Presentation by: Champaign County Health Care Consumers (CCHCC) October 26, 2017 Welcome! Goals of the Affordable Care Act (ACA)

COVERED CALIFORNIA: THE GOOD, THE BAD & THE UNDEFINED FOR CHILDREN WITH SPECIAL HEALTH CARE NEEDS

1 COVERED CALIFORNIA: THE GOOD, THE BAD & THE UNDEFINED FOR CHILDREN WITH SPECIAL HEALTH CARE NEEDS Ann-Louise Kuhns President & CEO California Children s Hospital Association Health Care Reform: The Basics

1 COVERED CALIFORNIA: THE GOOD, THE BAD & THE UNDEFINED FOR CHILDREN WITH SPECIAL HEALTH CARE NEEDS Ann-Louise Kuhns President & CEO California Children s Hospital Association Health Care Reform: The Basics

Marketplace 101. Find health care options that meet your needs and fit your budget

Marketplace 101 Find health care options that meet your needs and fit your budget Objectives This session will help you Explain the Health Insurance Marketplace Define who might be eligible Define options

Marketplace 101 Find health care options that meet your needs and fit your budget Objectives This session will help you Explain the Health Insurance Marketplace Define who might be eligible Define options

Health Insurance Marketplace

Health Insurance Marketplace Briefing on the Affordable Care Act 2014 Ben J. Altheimer Oral Symposium UALR Bowen School of Law February 28, 2014 David Nilasena, MD Centers for Medicare & Medicaid Services

Health Insurance Marketplace Briefing on the Affordable Care Act 2014 Ben J. Altheimer Oral Symposium UALR Bowen School of Law February 28, 2014 David Nilasena, MD Centers for Medicare & Medicaid Services

Understanding the Health Insurance Marketplace. September 2013

Understanding the Health Insurance Marketplace September 2013 1. Health Insurance Marketplace To provide qualified individuals and employers Access to affordable coverage options Ability to buy certain

Understanding the Health Insurance Marketplace September 2013 1. Health Insurance Marketplace To provide qualified individuals and employers Access to affordable coverage options Ability to buy certain

ACA and The Marketplace. Also known as the (Federal) Exchange

Exchange") ACA and The Marketplace Also known as the (Federal) Exchange 1 Qualified Health Plan and Minimum Essential Coverage (Indiv., Small Group & Large Group Coverage) Needs to Meet the Following (At a Minimum):

ACA and The Marketplace Also known as the (Federal) Exchange 1 Qualified Health Plan and Minimum Essential Coverage (Indiv., Small Group & Large Group Coverage) Needs to Meet the Following (At a Minimum):

Health Care Reform. Navigating The Maze Of. What s Inside

Navigating The Maze Of Health Care Reform What s Inside Questions and Answers on Health Care Reform Health Care Reform Timeline Health Care Reform Glossary Questions and Answers on Health Care Reform I

Navigating The Maze Of Health Care Reform What s Inside Questions and Answers on Health Care Reform Health Care Reform Timeline Health Care Reform Glossary Questions and Answers on Health Care Reform I

Insurance (Coverage) Reform

Reform") Arkansas Health Law Check Up Insurance (Coverage) Reform Create Insurance Marketplaces For individuals & small businesses Expand Medicaid to 138% FPL Arkansas alternative = Private Option, not Arkansas

Arkansas Health Law Check Up Insurance (Coverage) Reform Create Insurance Marketplaces For individuals & small businesses Expand Medicaid to 138% FPL Arkansas alternative = Private Option, not Arkansas

AN INDIVIDUAL S guide to THE. Right Health Insurance

AN INDIVIDUAL S guide to THE Right Health Insurance TURN TO The right health insurance. Right now. To find the health insurance that s right for you, begin by asking yourself one simple question: What

AN INDIVIDUAL S guide to THE Right Health Insurance TURN TO The right health insurance. Right now. To find the health insurance that s right for you, begin by asking yourself one simple question: What

The Affordable Care Act: A Summary on Healthcare Reform. The Wyoming Department of Insurance

The Affordable Care Act: A Summary on Healthcare Reform The Wyoming Department of Insurance The ACA is a federal law that impacts Wyoming and its citizens. The State of Wyoming has filed a lawsuit against

The Affordable Care Act: A Summary on Healthcare Reform The Wyoming Department of Insurance The ACA is a federal law that impacts Wyoming and its citizens. The State of Wyoming has filed a lawsuit against

AFFORDABLE CARE ACT FAQ

AFFORDABLE CARE ACT FAQ What is the Healthcare Insurance Marketplace? The Marketplace is a new way to find quality health coverage. It can help if you don t have coverage now or if you have it but want

AFFORDABLE CARE ACT FAQ What is the Healthcare Insurance Marketplace? The Marketplace is a new way to find quality health coverage. It can help if you don t have coverage now or if you have it but want

Overview of the ACA and Wisconsin Medicaid Reforms. Covering Kids & Families Wisconsin Wisconsin Primary Health Care Association

Overview of the ACA and Wisconsin Medicaid Reforms Covering Kids & Families Wisconsin Wisconsin Primary Health Care Association Updated September 9, 2013 Topics to be Covered What is the ACA? Wisconsin

Overview of the ACA and Wisconsin Medicaid Reforms Covering Kids & Families Wisconsin Wisconsin Primary Health Care Association Updated September 9, 2013 Topics to be Covered What is the ACA? Wisconsin

Humana, Healthcare Reform and You What you need to know

Humana, Healthcare Reform and You What you need to know About Humana Headquartered in Louisville, KY Over 50 years experience in the health industry Diverse portfolio of products Over 12.1 million medical

Humana, Healthcare Reform and You What you need to know About Humana Headquartered in Louisville, KY Over 50 years experience in the health industry Diverse portfolio of products Over 12.1 million medical

The Affordable Care Act

The Affordable Care Act Employers Guide to 2015 and Beyond For Small Groups Summary Jan. 1, 2014, ushered in new Affordable Care Act (ACA) health insurance market reforms. These changes are impacting the

The Affordable Care Act Employers Guide to 2015 and Beyond For Small Groups Summary Jan. 1, 2014, ushered in new Affordable Care Act (ACA) health insurance market reforms. These changes are impacting the

THE AFFORDABLE CARE ACT...2

Table of Contents THE AFFORDABLE CARE ACT...2 Health Insurance Marketplace (Exchange)...3 Metallic Levels...4 Catastrophic Plans...4 Individual Mandate...5 Subsidies...5 Open Enrollment Period...6 Special

Table of Contents THE AFFORDABLE CARE ACT...2 Health Insurance Marketplace (Exchange)...3 Metallic Levels...4 Catastrophic Plans...4 Individual Mandate...5 Subsidies...5 Open Enrollment Period...6 Special

ObamaCare What Does the Affordable Care Act Mean For You?

ObamaCare What Does the Affordable Care Act Mean For You? After tonight, you will: Understand key aspects of the ACA Private Health Insurance Consumer Protections Medi-Cal Expansion Health Benefit Exchange

ObamaCare What Does the Affordable Care Act Mean For You? After tonight, you will: Understand key aspects of the ACA Private Health Insurance Consumer Protections Medi-Cal Expansion Health Benefit Exchange

Affordable Care Act A Broker s Perspective. Jeffrey M. Barry Barry Insurance Group

Affordable Care Act A Broker s Perspective Jeffrey M. Barry Barry Insurance Group What Is So Expensive? Is it health insurance? Is it the increased cost of healthcare? Essential Health Benefits Ambulatory

Affordable Care Act A Broker s Perspective Jeffrey M. Barry Barry Insurance Group What Is So Expensive? Is it health insurance? Is it the increased cost of healthcare? Essential Health Benefits Ambulatory

TO UNDERSTANDING THE AFFORDABLE CARE ACT

3 STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT What s Inside Step 1: What Understand what you re buying 4 Step 2: How How can you buy health insurance? 20 STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT

3 STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT What s Inside Step 1: What Understand what you re buying 4 Step 2: How How can you buy health insurance? 20 STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT

The Health Insurance Marketplace 101 August 2013

The Health Insurance Marketplace 101 August 2013 Thursday, September 12, 2013, 7:00 pm Health Insurance Marketplace Elissa Balch is a Management Analyst for the Centers for Medicare & Medicaid Services

The Health Insurance Marketplace 101 August 2013 Thursday, September 12, 2013, 7:00 pm Health Insurance Marketplace Elissa Balch is a Management Analyst for the Centers for Medicare & Medicaid Services

Subsidized Health Coverage through MNsure

INFORMATION BRIEF Research Department Minnesota House of Representatives 600 State Office Building St. Paul, MN 55155 Randall Chun, Legislative Analyst 651-296-8639 Updated: October 2018 Subsidized Health

INFORMATION BRIEF Research Department Minnesota House of Representatives 600 State Office Building St. Paul, MN 55155 Randall Chun, Legislative Analyst 651-296-8639 Updated: October 2018 Subsidized Health

Health Care Reform under the Patient Protection and Affordable Care Act ( PPACA ) provisions effective January 1, 2014

provisions effective January 1, 2014") The New Health Care Landscape Today s Agenda Health Care Reform under the Patient Protection and Affordable Care Act ( PPACA ) provisions effective January 1, 2014 Exchanges and Qualified Health Plans

The New Health Care Landscape Today s Agenda Health Care Reform under the Patient Protection and Affordable Care Act ( PPACA ) provisions effective January 1, 2014 Exchanges and Qualified Health Plans

PPACA Implementation and the Marketplaces aka Exchanges. Presented by: Cathy Cooper November 15, 2013

PPACA Implementation and the Marketplaces aka Exchanges Presented by: Cathy Cooper November 15, 2013 Today s Agenda 2014 Provisions Groups over 50 in 2014 Groups under 50 in 2014 Marketplaces aka Exchanges

PPACA Implementation and the Marketplaces aka Exchanges Presented by: Cathy Cooper November 15, 2013 Today s Agenda 2014 Provisions Groups over 50 in 2014 Groups under 50 in 2014 Marketplaces aka Exchanges

Individual Health Insurance Marketplace FAQs Purdue Pre-65 Retiree

Individual Health Insurance Marketplace FAQs Purdue Pre-65 Retiree Maria Pearson Melva Lowry Q: What is a Health Insurance Marketplace? A: The Health Insurance Marketplace (Marketplace) is a way to find

Individual Health Insurance Marketplace FAQs Purdue Pre-65 Retiree Maria Pearson Melva Lowry Q: What is a Health Insurance Marketplace? A: The Health Insurance Marketplace (Marketplace) is a way to find

Covered California Overview

Covered California Overview David Panush Director, External Affairs Covered California February 1, 2013 Los Angeles Chamber of Commerce Covered California Governance Independent Public Entity with Qualified

Covered California Overview David Panush Director, External Affairs Covered California February 1, 2013 Los Angeles Chamber of Commerce Covered California Governance Independent Public Entity with Qualified

About our plans. Making sense of Anthem Blue Cross new Affordable Care Act-compliant products

About our plans Making sense of Anthem Blue Cross new Affordable Care Act-compliant products The Affordable Care Act (ACA) is transforming the health care marketplace. We re here to help you and your clients

About our plans Making sense of Anthem Blue Cross new Affordable Care Act-compliant products The Affordable Care Act (ACA) is transforming the health care marketplace. We re here to help you and your clients

About our plans. Making sense of Anthem Blue Cross new Affordable Care Act-compliant products

About our plans Making sense of Anthem Blue Cross new Affordable Care Act-compliant products The Affordable Care Act (ACA) is transforming the health care marketplace. We re here to help you and your clients

About our plans Making sense of Anthem Blue Cross new Affordable Care Act-compliant products The Affordable Care Act (ACA) is transforming the health care marketplace. We re here to help you and your clients

GENERAL INFORMATION BULLETIN

AFL-CIO California School Employees Association GENERAL INFORMATION BULLETIN March 15, 2013 General Information Bulletin No. 17 13 AFFORDABLE CARE ACT (ACA) QUESTION & ANSWER RESOURCE DOCUMENT Action for

AFL-CIO California School Employees Association GENERAL INFORMATION BULLETIN March 15, 2013 General Information Bulletin No. 17 13 AFFORDABLE CARE ACT (ACA) QUESTION & ANSWER RESOURCE DOCUMENT Action for

Washington Health Benefit Exchange

Washington Health Benefit Exchange AFFORDABLE CARE ACT 101 APRIL 26, 2013 Christine Brown Navigator/In-person Assister Program Today s Agenda History of the Affordable Care Act (ACA) Highlights of the

Washington Health Benefit Exchange AFFORDABLE CARE ACT 101 APRIL 26, 2013 Christine Brown Navigator/In-person Assister Program Today s Agenda History of the Affordable Care Act (ACA) Highlights of the

What s on the Horizon for Health Care and Public Benefits. May 8, 2013

What s on the Horizon for Health Care and Public Benefits. May 8, 2013 1 Overview Individual Mandate Federal Exchange Changes to Badgercare Changes to MAPP Future of HIRSP Changes to employer group health

What s on the Horizon for Health Care and Public Benefits. May 8, 2013 1 Overview Individual Mandate Federal Exchange Changes to Badgercare Changes to MAPP Future of HIRSP Changes to employer group health

Understand and Enroll in the Affordable Care Act

You deserve quality healthcare, and MHC will help you find the best plan for you and your family. How can Memphis Health Center assist me in enrolling into the affordable healthcare program? Memphis Health

You deserve quality healthcare, and MHC will help you find the best plan for you and your family. How can Memphis Health Center assist me in enrolling into the affordable healthcare program? Memphis Health

Aldridge Financial Consultants January 12, 2013

Aldridge Financial Consultants Mark D. Aldridge, CFP, CFA, ChFC 3021 Bethel Road Suite 100 Columbus, OH 43220 614-824-3080 Fax 614 824-3082 mark.aldridge@raymondjames.com www.markaldridge.com Health-Care

Aldridge Financial Consultants Mark D. Aldridge, CFP, CFA, ChFC 3021 Bethel Road Suite 100 Columbus, OH 43220 614-824-3080 Fax 614 824-3082 mark.aldridge@raymondjames.com www.markaldridge.com Health-Care

ACA in Brief 2/18/2014. It Takes Three Branches... Overview of the Affordable Care Act. Health Insurance Coverage, USA, % 16% 55% 15% 10%

Health Insurance Coverage, USA, 2011 16% Uninsured Overview of the Affordable Care Act 55% 16% Medicaid Medicare Private Non-Group Philip R. Lee Institute for Health Policy Studies Janet Coffman, MPP,

Health Insurance Coverage, USA, 2011 16% Uninsured Overview of the Affordable Care Act 55% 16% Medicaid Medicare Private Non-Group Philip R. Lee Institute for Health Policy Studies Janet Coffman, MPP,

HEALTH CONCEPTS AND TAX CONSIDERATIONS

14 HEALTH CONCEPTS AND TAX CONSIDERATIONS LEARNING OBJECTIVES Upon the completion of this chapter, you will be able to: 1. Recognize the features of health insurance policies that have been mandated by

14 HEALTH CONCEPTS AND TAX CONSIDERATIONS LEARNING OBJECTIVES Upon the completion of this chapter, you will be able to: 1. Recognize the features of health insurance policies that have been mandated by

Health Care Reform. PPACA Compliance Overview

Health Care Reform PPACA Compliance Overview Agenda 1 2 What Healthcare Reform Is How the ACA is Affecting Employers 3 4 5 What the Employer Delay Means For Your Business Factors Affecting Your Premiums

Health Care Reform PPACA Compliance Overview Agenda 1 2 What Healthcare Reform Is How the ACA is Affecting Employers 3 4 5 What the Employer Delay Means For Your Business Factors Affecting Your Premiums

HEALTH INSURANCE MARKETPLACE. May 21,

HEALTH INSURANCE MARKETPLACE May 21, 2013 Agenda Introduction and Welcome Health Insurance Marketplaces Market Reforms Overview Enrollment Process The Marketplace and Small Businesses Applying for Small

HEALTH INSURANCE MARKETPLACE May 21, 2013 Agenda Introduction and Welcome Health Insurance Marketplaces Market Reforms Overview Enrollment Process The Marketplace and Small Businesses Applying for Small

Thursday, December 19, 2013 Celeste Richards Erin Malone

Thursday, December 19, 2013 Celeste Richards Erin Malone Agenda Structure of ACA health Exchange and Mandated Elements of Plan Design Georgia Regions Alliant Health Plans Exchange Products and Provider

Thursday, December 19, 2013 Celeste Richards Erin Malone Agenda Structure of ACA health Exchange and Mandated Elements of Plan Design Georgia Regions Alliant Health Plans Exchange Products and Provider

ACA Regulations: Insurance Exchanges and EHBs

ACA Regulations: Insurance Exchanges and EHBs 1 Insurance Exchanges Insurance Exchanges: Exchanges are online marketplaces More than 20 million individuals and employees of small businesses may purchase

ACA Regulations: Insurance Exchanges and EHBs 1 Insurance Exchanges Insurance Exchanges: Exchanges are online marketplaces More than 20 million individuals and employees of small businesses may purchase

It s more than coverage. It s care. BlueSelect. Individual and Family

It s more than coverage. It s care. BlueSelect Individual and Family STEP ONE Coverage Levels u Understand the differences and find your best fit Gold Plans Plan pays, on average, 80% of your healthcare

It s more than coverage. It s care. BlueSelect Individual and Family STEP ONE Coverage Levels u Understand the differences and find your best fit Gold Plans Plan pays, on average, 80% of your healthcare

A special look at health care reform. Helping members make informed decisions. Special Edition 2013

Special Edition 2013 SM Helping members make informed decisions A special look at health care reform. Changes ahead 3 How health care reform will impact rates 6 Five ways health care reform may affect

Special Edition 2013 SM Helping members make informed decisions A special look at health care reform. Changes ahead 3 How health care reform will impact rates 6 Five ways health care reform may affect

The Affordable Care Act and You. Presented by: Blue Cross and Blue Shield of Kansas

The Affordable Care Act and You Presented by: Blue Cross and Blue Shield of Kansas Agenda Health insurance basics What does the Affordable Care Act mean for you? Shopping on the Marketplace Kansans serving

The Affordable Care Act and You Presented by: Blue Cross and Blue Shield of Kansas Agenda Health insurance basics What does the Affordable Care Act mean for you? Shopping on the Marketplace Kansans serving

Table of Contents. Legend. Coverage Option Overview 6

Modified Adjusted Gross Income (MAGI): Exchange and Medicaid Eligibility Flow Charts Updated per March 2012 Final Rules and June 2012 Supreme Court Decision October 3, 2012 These charts illustrate MAGI

Modified Adjusted Gross Income (MAGI): Exchange and Medicaid Eligibility Flow Charts Updated per March 2012 Final Rules and June 2012 Supreme Court Decision October 3, 2012 These charts illustrate MAGI

Affordable Care Act. Small Businesses with 1-49 Employees. Simplified for. Questions?

Affordable Care Act Simplified for Small Businesses with 1-49 Employees Questions? Email smallbizhealth@intuit.com @2013 Intuit, Inc. All Rights Reserved. Summary Starting on January 1, 2014, the Affordable

Affordable Care Act Simplified for Small Businesses with 1-49 Employees Questions? Email smallbizhealth@intuit.com @2013 Intuit, Inc. All Rights Reserved. Summary Starting on January 1, 2014, the Affordable

Washington Health Benefit Exchange

Washington Health Benefit Exchange HEALTHCARE REFORM SEMINAR November 25th, 2013 ACA INFORMATIONAL SESSION FOR SMALL BUSINESS OWNERS The Affordable Care Act Exchange Basics Today s Agenda Exchange Functions

Washington Health Benefit Exchange HEALTHCARE REFORM SEMINAR November 25th, 2013 ACA INFORMATIONAL SESSION FOR SMALL BUSINESS OWNERS The Affordable Care Act Exchange Basics Today s Agenda Exchange Functions

Health Care Coverage You Need. A Company You Know.

Health Care Coverage You Need. A Company You Know. 2018 Call 800-477-2000, visit bcbsil.com or contact an independent, authorized agent to get a quote today. When It s Time to Get Health Care Coverage,

Health Care Coverage You Need. A Company You Know. 2018 Call 800-477-2000, visit bcbsil.com or contact an independent, authorized agent to get a quote today. When It s Time to Get Health Care Coverage,

Navajo County Schools EBT

Navajo County Schools EBT Affordable Care Act (ACA) Update Aaron Polkoski Segal Consulting January 31st, 2014 Copyright 2013 by The Segal Group, Inc., parent of The Segal Company. All rights reserved.

Navajo County Schools EBT Affordable Care Act (ACA) Update Aaron Polkoski Segal Consulting January 31st, 2014 Copyright 2013 by The Segal Group, Inc., parent of The Segal Company. All rights reserved.

What s Inside STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT (ACA)

") What s Inside Step 1: What Understand what you re buying 4 Step 2: How How can you buy health insurance? 18 STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT (ACA) Want to know more about the health reform

What s Inside Step 1: What Understand what you re buying 4 Step 2: How How can you buy health insurance? 18 STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT (ACA) Want to know more about the health reform

Affordable Care Act: Impact on the Indiana Market

1 Affordable Care Act: Impact on the Indiana Market Seema Verma President SVC, Inc 2 Affordable Care Act Key accomplishment is access ~48.6 million uninsured in America* ~800 thousand uninsured in Indiana*

1 Affordable Care Act: Impact on the Indiana Market Seema Verma President SVC, Inc 2 Affordable Care Act Key accomplishment is access ~48.6 million uninsured in America* ~800 thousand uninsured in Indiana*

What you need to know

Exploring The Affordable Care Act What you need to know Maternal Child Adolescent Health Advisory Board Meeting August 1, 2013 Vanessa Raditz, vraditz@berkeley.edu Why do we need this training? Many people

Exploring The Affordable Care Act What you need to know Maternal Child Adolescent Health Advisory Board Meeting August 1, 2013 Vanessa Raditz, vraditz@berkeley.edu Why do we need this training? Many people

YOUR BUSINESS, YOUR FUTURE: WHAT YOU NEED TO KNOW ABOUT HEALTHCARE REFORM

YOUR BUSINESS, YOUR FUTURE: WHAT YOU NEED TO KNOW ABOUT HEALTHCARE REFORM Featuring: Gene Marks, The Marks Group, P.C. Decide On Healthcare Is Your Business Affected, And If So What Do You Do? NPCA 1 Still

YOUR BUSINESS, YOUR FUTURE: WHAT YOU NEED TO KNOW ABOUT HEALTHCARE REFORM Featuring: Gene Marks, The Marks Group, P.C. Decide On Healthcare Is Your Business Affected, And If So What Do You Do? NPCA 1 Still

STUDENTS GUIDE TO THE AFFORDABLE CARE ACT Grant Atkinson J.D, NAGPS Legal Concerns Chair, August 25, 2013

STUDENTS GUIDE TO THE AFFORDABLE CARE ACT Grant Atkinson J.D, NAGPS Legal Concerns Chair, August 25, 2013 What do students need to know about the the Affordable Care Act? THE BASICS: 1) It encourages you

STUDENTS GUIDE TO THE AFFORDABLE CARE ACT Grant Atkinson J.D, NAGPS Legal Concerns Chair, August 25, 2013 What do students need to know about the the Affordable Care Act? THE BASICS: 1) It encourages you

Module IV PLAN DESIGN

Module IV PLAN DESIGN Plan Design Benefits Deductible Cost Sharing Out of Pocket Actuarial Value 2 Think about your spreadsheets 3 ESSENTIAL BENEFITS 4 Mandated Benefits Small Group Mandates in Texas Source:

Module IV PLAN DESIGN Plan Design Benefits Deductible Cost Sharing Out of Pocket Actuarial Value 2 Think about your spreadsheets 3 ESSENTIAL BENEFITS 4 Mandated Benefits Small Group Mandates in Texas Source:

Health Care Coverage You Need. A Company You Know.

Health Care Coverage You Need. A Company You Know. 2018 Call 800-531-4456, visit bcbstx.com or contact an independent, authorized agent to get a quote today. When It s Time to Get Health Care Coverage,

Health Care Coverage You Need. A Company You Know. 2018 Call 800-531-4456, visit bcbstx.com or contact an independent, authorized agent to get a quote today. When It s Time to Get Health Care Coverage,

The Affordable Care Act: Implementation in Illinois

The Affordable Care Act: Implementation in Illinois Stephanie F. Altman, J.D. Programs and Policy Director Health & Disability Advocates www.hdadvocates.org www.illinoishealthmatters.org November 2013

The Affordable Care Act: Implementation in Illinois Stephanie F. Altman, J.D. Programs and Policy Director Health & Disability Advocates www.hdadvocates.org www.illinoishealthmatters.org November 2013

FEEL BETTER ABOUT YOUR CHOICES

2015 FEEL BETTER ABOUT YOUR CHOICES CHOOSE WELLCARE. CHOOSE A PLAN TO FIT YOUR NEEDS. Information on individual and family plans inside. Kentucky Boone, Bullitt, Campbell, Clay, Harlan, Jefferson, Jessamine,

2015 FEEL BETTER ABOUT YOUR CHOICES CHOOSE WELLCARE. CHOOSE A PLAN TO FIT YOUR NEEDS. Information on individual and family plans inside. Kentucky Boone, Bullitt, Campbell, Clay, Harlan, Jefferson, Jessamine,

The Affordable Care Act The Bottom Line Facts

The Affordable Care Act The Bottom Line Facts ACA: What Employers Need to Know Presented by: Mike DeMore Managing Director, UnitedAg DEFINITIONS Minimum Essential Coverage (MEC) Very Loose Definition -

The Affordable Care Act The Bottom Line Facts ACA: What Employers Need to Know Presented by: Mike DeMore Managing Director, UnitedAg DEFINITIONS Minimum Essential Coverage (MEC) Very Loose Definition -

What s Inside STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT (ACA)

") What s Inside Step 1: What Understand what you re buying 4 Step 2: How How can you buy health insurance? 20 STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT (ACA) Want to know more about the health reform

What s Inside Step 1: What Understand what you re buying 4 Step 2: How How can you buy health insurance? 20 STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT (ACA) Want to know more about the health reform

UNIVERSAL HEALTHCARE COUNCIL 2013 OVERVIEW OF THE AFFORDABLE CARE ACT

UNIVERSAL HEALTHCARE COUNCIL 2013 OVERVIEW OF THE AFFORDABLE CARE ACT Introduction The Patient Protection and Affordable Care Act (ACA) was signed into federal law on March 23, 2010. While many reforms

UNIVERSAL HEALTHCARE COUNCIL 2013 OVERVIEW OF THE AFFORDABLE CARE ACT Introduction The Patient Protection and Affordable Care Act (ACA) was signed into federal law on March 23, 2010. While many reforms

Affordable Care Act (ACA)

") Affordable Care Act (ACA) The Affordable Care Act: What s Happened So Far, What s Happening, and What s Coming Next Employers Fraud Task Force January 28, 2014 Office of the Regional Director Community

Affordable Care Act (ACA) The Affordable Care Act: What s Happened So Far, What s Happening, and What s Coming Next Employers Fraud Task Force January 28, 2014 Office of the Regional Director Community

Tennessee Public Health Association. Overview of the Affordable Care Act

Tennessee Public Health Association Overview of the Affordable Care Act Susie Baird Director of Policy Health Care Finance and Administration September 12, 2013 1 Origins of ACA Signed into law on March

Tennessee Public Health Association Overview of the Affordable Care Act Susie Baird Director of Policy Health Care Finance and Administration September 12, 2013 1 Origins of ACA Signed into law on March

Health Care Coverage You Need. A Company You Know.

Health Care Coverage You Need. A Company You Know. 2018 Call 855-593-1515, visit www.bcbsmt.com or contact an independent, authorized agent to get a quote today. When It s Time to Get Health Care Coverage,

Health Care Coverage You Need. A Company You Know. 2018 Call 855-593-1515, visit www.bcbsmt.com or contact an independent, authorized agent to get a quote today. When It s Time to Get Health Care Coverage,

Connecting People to Coverage

Connecting People to Coverage Amy Rix Piedmont Health Services Special Projects Manager The Patient Protection and Affordable Care Act was signed March 2010 Open enrollment period runs from October 1,

Connecting People to Coverage Amy Rix Piedmont Health Services Special Projects Manager The Patient Protection and Affordable Care Act was signed March 2010 Open enrollment period runs from October 1,

What s Next for States The Affordable Care Act Post Implementation. Seema Verma, MPH President SVC, Inc

What s Next for States The Affordable Care Act Post Implementation Seema Verma, MPH President SVC, Inc sverma@svcinc.org *Utah, New Mexico & Mississippi will operate a state-base SHOP Exchange but individual

What s Next for States The Affordable Care Act Post Implementation Seema Verma, MPH President SVC, Inc sverma@svcinc.org *Utah, New Mexico & Mississippi will operate a state-base SHOP Exchange but individual

Health Care Reform Frequently Asked Questions

Health Care Reform Frequently Asked Questions What are health exchanges, or marketplaces, and when are they going to be available? Health insurance exchanges, now called health insurance marketplaces,

Health Care Reform Frequently Asked Questions What are health exchanges, or marketplaces, and when are they going to be available? Health insurance exchanges, now called health insurance marketplaces,

4/22/2014. Health Care Reform. Disclosure. Health Care Reform. How Will it Change Your Business Strategy?

Health Care Reform How Will it Change Your Business Strategy? OHCA Educational Session April 29 th, 2014 Presented by: Roderick S. Wood, CHRS Huntington Insurance, Inc. Disclosure This presentation contains

Health Care Reform How Will it Change Your Business Strategy? OHCA Educational Session April 29 th, 2014 Presented by: Roderick S. Wood, CHRS Huntington Insurance, Inc. Disclosure This presentation contains

Federal Health Care Reform

Federal Health Care Reform Presentation to Behavioral Health Collaborative Katie Falls, HSD Secretary May 26, 2010 1 Health Care Reform Areas of Impact Insurance Reforms Medicare Medicaid Quality Improvement

Federal Health Care Reform Presentation to Behavioral Health Collaborative Katie Falls, HSD Secretary May 26, 2010 1 Health Care Reform Areas of Impact Insurance Reforms Medicare Medicaid Quality Improvement

Health Care Reform Provision (effective January 1, 2014) School City of Hobart Medical Plan

School City of Hobart Medical Plan") Health Care Reform: We ve Got You Covered The health care reform law officially called the Patient Protection and Affordable Care Act of 2010 (ACA for short) is here to stay. Additional changes resulting

Health Care Reform: We ve Got You Covered The health care reform law officially called the Patient Protection and Affordable Care Act of 2010 (ACA for short) is here to stay. Additional changes resulting

The Affordable Care Act and the Essential Health Benefits Package

October 24, 2011 The Affordable Care Act and the Essential Health Benefits Package A. Background Under the Affordable Care Act (the ACA or the Act ), and starting in 2014, certain low to moderate income

October 24, 2011 The Affordable Care Act and the Essential Health Benefits Package A. Background Under the Affordable Care Act (the ACA or the Act ), and starting in 2014, certain low to moderate income

The New Responsibility to Secure Coverage: Frequently Asked Questions

The New Responsibility to Secure Coverage: Frequently Asked Questions Introduction The Patient Protection and Affordable Care Act (PPACA) includes a much-discussed requirement that people secure health

The New Responsibility to Secure Coverage: Frequently Asked Questions Introduction The Patient Protection and Affordable Care Act (PPACA) includes a much-discussed requirement that people secure health

THE AFFORDABLE CARE ACT AN OVERVIEW FOR HUMAN RESOURCE & FINANCE PROFESSIONALS AT MID-SIZED COMPANIES

THE AFFORDABLE CARE ACT AN OVERVIEW FOR HUMAN RESOURCE & FINANCE PROFESSIONALS AT MID-SIZED COMPANIES 1 Mid-Sized Retirement & Healthcare Plan Management Conference San Francisco, CA March 17, 2014 GOALS

THE AFFORDABLE CARE ACT AN OVERVIEW FOR HUMAN RESOURCE & FINANCE PROFESSIONALS AT MID-SIZED COMPANIES 1 Mid-Sized Retirement & Healthcare Plan Management Conference San Francisco, CA March 17, 2014 GOALS

HealthCare 201: Essential Updates Before Open Enrollment. Webinar

HealthCare 201: Essential Updates Before Open Enrollment Webinar About ITUP ITUP is a non-partisan, non-profit health policy think tank based in Santa Monica, CA. W e are f unded by generous grants f rom

HealthCare 201: Essential Updates Before Open Enrollment Webinar About ITUP ITUP is a non-partisan, non-profit health policy think tank based in Santa Monica, CA. W e are f unded by generous grants f rom

Affordable Care Act HEALTHCARE.GOV

HEALTHCARE.GOV Affordable Care Act Marketplace Implementation Briefing Pennsylvania Breast Cancer Coalition 2014 Conference October 13, 2014 Joanne Corte Grossi, MIPP Regional Director U.S. Department

HEALTHCARE.GOV Affordable Care Act Marketplace Implementation Briefing Pennsylvania Breast Cancer Coalition 2014 Conference October 13, 2014 Joanne Corte Grossi, MIPP Regional Director U.S. Department

The New Healthcare Law and Its Impact on Small Business

U. S. Small Business Administration Washington Metropolitan Area District Office The New Healthcare Law and Its Impact on Small Business Julie C. Verratti Advisor U.S. Small Business Administration Julie.Verratti@sba.gov

U. S. Small Business Administration Washington Metropolitan Area District Office The New Healthcare Law and Its Impact on Small Business Julie C. Verratti Advisor U.S. Small Business Administration Julie.Verratti@sba.gov

AFFORDABLE CARE ACT (ACA) UPDATE JUNE 26, 2013

UPDATE JUNE 26, 2013") AFFORDABLE CARE ACT (ACA) UPDATE JUNE 26, 2013 FREDDY WARNER SYSTEM EXECUTIVE, PUBLIC POLICY & GOVERNMENT RELATIONS MEMORIAL HERMANN HEALTH SYSTEM ACA - REVISITED OBAMA SIGNED INTO LAW 2010 GOALS PROVIDE

AFFORDABLE CARE ACT (ACA) UPDATE JUNE 26, 2013 FREDDY WARNER SYSTEM EXECUTIVE, PUBLIC POLICY & GOVERNMENT RELATIONS MEMORIAL HERMANN HEALTH SYSTEM ACA - REVISITED OBAMA SIGNED INTO LAW 2010 GOALS PROVIDE

The Patient Protection and Affordable Care Act

The Patient Protection and Affordable Care Act 2015 marks the beginning of the fifth full year of the Patient Protection and Affordable Care Act (ACA). We want to take the opportunity to look ahead and

The Patient Protection and Affordable Care Act 2015 marks the beginning of the fifth full year of the Patient Protection and Affordable Care Act (ACA). We want to take the opportunity to look ahead and

Affordable Care Act HEALTHCARE.GOV. Marketplace Implementation Briefing Loudon County Chamber of Commerce July 12, 2013

HEALTHCARE.GOV Affordable Care Act Marketplace Implementation Briefing Loudon County Chamber of Commerce July 12, 2013 Joanne Corte Grossi, MIPP Regional Director U.S. Department of Health & Human Services,

HEALTHCARE.GOV Affordable Care Act Marketplace Implementation Briefing Loudon County Chamber of Commerce July 12, 2013 Joanne Corte Grossi, MIPP Regional Director U.S. Department of Health & Human Services,

Some Basics on the Individual Mandate, Subsidies, and Medicaid Expansion Lisa Klinger, J.D.

Some Basics on the Individual Mandate, Subsidies, and Medicaid Expansion Lisa Klinger, J.D. www.leavitt.com/healthcarereform.com 10-23- 2013 As of January 1, 2014, the Patient Protection and Affordable

Some Basics on the Individual Mandate, Subsidies, and Medicaid Expansion Lisa Klinger, J.D. www.leavitt.com/healthcarereform.com 10-23- 2013 As of January 1, 2014, the Patient Protection and Affordable

Affordable Care Act HEALTHCARE.GOV

HEALTHCARE.GOV Affordable Care Act Marketplace Implementation Briefing Pennsylvania Breast Cancer Coalition 2013 Conference October 15, 2013 Joanne Corte Grossi, MIPP Regional Director U.S. Department

HEALTHCARE.GOV Affordable Care Act Marketplace Implementation Briefing Pennsylvania Breast Cancer Coalition 2013 Conference October 15, 2013 Joanne Corte Grossi, MIPP Regional Director U.S. Department

Health Care Reform

Health Care Reform 2013-14 The Individual Mandate Via the Exchange may qualify for subsidy or premium tax credit Other source - most likely from the employer An employee ONLY receives a premium subsidy

Health Care Reform 2013-14 The Individual Mandate Via the Exchange may qualify for subsidy or premium tax credit Other source - most likely from the employer An employee ONLY receives a premium subsidy

Needs for publicly funded behavioral health services under the Patient Protection and Affordable Care Act (ACA): What gaps will remain?

: What gaps will remain?") Needs for publicly funded behavioral health services under the Patient Protection and Affordable Care Act (ACA): What gaps will remain? February 4, 2014 Stan Dorn (sdorn@urban.org) Senior Fellow, Health

Needs for publicly funded behavioral health services under the Patient Protection and Affordable Care Act (ACA): What gaps will remain? February 4, 2014 Stan Dorn (sdorn@urban.org) Senior Fellow, Health

Bringing Health Care Coverage Within Reach

Measuring the Financial Assistance Available through Covered California that is lowering the Cost of Coverage and Care Introduction The Affordable Care Act (ACA) helped cut the rate of the uninsured by

Measuring the Financial Assistance Available through Covered California that is lowering the Cost of Coverage and Care Introduction The Affordable Care Act (ACA) helped cut the rate of the uninsured by

Premium Tax Credits: Beyond the Basics

Premium Tax Credits: Beyond the Basics Center on Budget and Policy Priorities June 5, 2013 Topics Premium credit basics Determining the amount of the premium credit Factors that affect the amount of the

Premium Tax Credits: Beyond the Basics Center on Budget and Policy Priorities June 5, 2013 Topics Premium credit basics Determining the amount of the premium credit Factors that affect the amount of the

MEDI-CAL 101 T I F F A N Y H U Y E N H - C H O H E A L T H C O N S U M E R C E N T E R B A Y A R E A L E G A L A I D

MEDI-CAL 101 T I F F A N Y H U Y E N H - C H O H E A L T H C O N S U M E R C E N T E R B A Y A R E A L E G A L A I D October 5, 2018 HEALTH CONSUMER CENTER Statewide legal hotline providing free assistance

MEDI-CAL 101 T I F F A N Y H U Y E N H - C H O H E A L T H C O N S U M E R C E N T E R B A Y A R E A L E G A L A I D October 5, 2018 HEALTH CONSUMER CENTER Statewide legal hotline providing free assistance

Health Care Reform: What Changes Are We Facing?

Health Care Reform: What Changes Are We Facing? 1 Health Care Reform: What Changes Are We Facing? A. Care Delivery Accountable Care Organization (ACOs) ACOs are groups of doctors, hospitals, and other

Health Care Reform: What Changes Are We Facing? 1 Health Care Reform: What Changes Are We Facing? A. Care Delivery Accountable Care Organization (ACOs) ACOs are groups of doctors, hospitals, and other

Benefits Report MARCH 2010

Benefits Report MARCH 2010 In this issue 1 Historic Health Care Reform Legislation Signed by President Obama 5 Department of Labor Issues New COBRA Model Notices and COBRA Subsidy Fact Sheet to Reflect

Benefits Report MARCH 2010 In this issue 1 Historic Health Care Reform Legislation Signed by President Obama 5 Department of Labor Issues New COBRA Model Notices and COBRA Subsidy Fact Sheet to Reflect

Implementing the Alternative Benefit Plan

Implementing the Alternative Benefit Plan Carolyn Ingram, Senior Vice President Shannon McMahon, Director of Coverage and Access State Network Medicaid Small Group Convening April 25, 2013 Agenda Alternative

Implementing the Alternative Benefit Plan Carolyn Ingram, Senior Vice President Shannon McMahon, Director of Coverage and Access State Network Medicaid Small Group Convening April 25, 2013 Agenda Alternative

Health Care Reform - Understanding the ACA Pediatric Essential Health Benefit

Health Care Reform - Understanding the ACA Pediatric Essential Health Benefit Presented by: John Lee DC Metro Sales Manager Agenda About Dominion Dental Services Health Care Reform Overview o When is Your

Health Care Reform - Understanding the ACA Pediatric Essential Health Benefit Presented by: John Lee DC Metro Sales Manager Agenda About Dominion Dental Services Health Care Reform Overview o When is Your

The Affordable Care Act in Action. Carla Haddad, MPH The Health Resources and Services Administration Office of Planning, Analysis and Evaluation

The Affordable Care Act in Action Carla Haddad, MPH The Health Resources and Services Administration Office of Planning, Analysis and Evaluation Percent of the Nonelderly Populations who are Eligible Uninsured

The Affordable Care Act in Action Carla Haddad, MPH The Health Resources and Services Administration Office of Planning, Analysis and Evaluation Percent of the Nonelderly Populations who are Eligible Uninsured

ACCESS TO HEALTH CARE FOR YOUNG ADULTS: IMPACT & IMPLICATIONS OF THE AFFORDABLE CARE ACT

ACCESS TO HEALTH CARE FOR YOUNG ADULTS: IMPACT & IMPLICATIONS OF THE AFFORDABLE CARE ACT Abigail English, JD english@cahl.org Young Adult Workshop IOM/NRC Washington, DC May 4, 2013 Special Thanks! M.

ACCESS TO HEALTH CARE FOR YOUNG ADULTS: IMPACT & IMPLICATIONS OF THE AFFORDABLE CARE ACT Abigail English, JD english@cahl.org Young Adult Workshop IOM/NRC Washington, DC May 4, 2013 Special Thanks! M.

GLOSSARY OF KEY AFFORDABLE CARE ACT AND COMMON HEALTH PLAN TERMS

GLOSSARY OF KEY AFFORDABLE CARE ACT AND COMMON HEALTH PLAN TERMS Note: in the event of any conflict between this glossary and your plan document/summary plan description (SPD) or policy/certificate, the

GLOSSARY OF KEY AFFORDABLE CARE ACT AND COMMON HEALTH PLAN TERMS Note: in the event of any conflict between this glossary and your plan document/summary plan description (SPD) or policy/certificate, the

Employment, Insurance & Disability: Understanding the Basics with Congenital Heart Disease

Employment, Insurance & Disability: Understanding the Basics with Congenital Heart Disease By David Highfill, LCSW Ahmanson/UCLA Adult Congenital Heart Disease Center Overview Employment Know your rights

Employment, Insurance & Disability: Understanding the Basics with Congenital Heart Disease By David Highfill, LCSW Ahmanson/UCLA Adult Congenital Heart Disease Center Overview Employment Know your rights

Enrolling in the Health Insurance Marketplace MAINE LOBSTERMEN S ASSOCIATION APRIL GILMORE, NAVIGATOR

Enrolling in the Health Insurance Marketplace MAINE LOBSTERMEN S ASSOCIATION APRIL GILMORE, NAVIGATOR Overview Provide information to help you understand the Health Insurance Marketplace MLA s focus is

Enrolling in the Health Insurance Marketplace MAINE LOBSTERMEN S ASSOCIATION APRIL GILMORE, NAVIGATOR Overview Provide information to help you understand the Health Insurance Marketplace MLA s focus is

Health Insurance Companies for Making the Individual Market in California Affordable

Health Insurance Companies for 2014 Making the Individual Market in California Affordable About Covered California TM Covered California is the state s marketplace for the federal Patient Protection and

Health Insurance Companies for 2014 Making the Individual Market in California Affordable About Covered California TM Covered California is the state s marketplace for the federal Patient Protection and