The Affordable Care Act Update

|

|

|

- Buck Dixon

- 5 years ago

- Views:

Transcription

1 The Affordable Care Act Update Presented by: The Union Labor Life Insurance Company SOLUTIONS FOR THE UNION WORKPLACE SPECIALTY INSURANCE INVESTMENTS

2 Overview I. Key Provisions II. Major Challenges III. Healthcare Spending Growth IV. ACA Challenges Ø Keeping Grandfathered Status Ø Premium Stabilization Rule Ø Belly Button Tax (Temporary Reinsurance Fee) Ø Transitional Risk Corridors Program Ø Permanent Risk Adjustment Program VI. Impact of Medicaid Expansion Under the ACA VII. Minimum Essential Coverage (MEC) vs. Essential Health Benefits (EHB) VIII. Public and Private Exchanges - What it means for Self Funded Plans IX. Premium Subsidies X. Employer Mandate XI. Cadillac Tax XII. What plan administrators & trustees should look for 2

3 Key ACA Health Plan Provisions Impacting Taft Hartley Plans Ø Belly Button Tax per covered individual Ø Coverage for approved clinical trials Ø Employee notification of access to Exchanges Ø FSA/HSA/HRA limits Ø 90 Day Waiting Period Ø Provide Minimum Essential Coverage (MEC) Ø Removal of Lifetime + Annual Coverage Limits 3

4 Major challenges. Brought to you by the ACA. Unfunded Mandates Health Insurance Marketplace Belly Button Tax in 2014 Self Funded Plan Cadillac Tax in 2018 Unlimited Coverage Maximums Part/Full Time staffing Fluctuations in budgeting Employer Eligibility Waiting Period Requirements Employer Mandate Penalty in 2015 Added complexity with Collective Bargaining Agreement Premium subsidy eligible? Medicaid eligible? (Expanded program) Changes in plan and benefits Plan Member 4

5 Healthcare Spending Growth -- Slowing Down? Ø In 2013 U.S. health care spending increased 3.6 percent to reach $2.9 trillion, or $9,255 per person, the fifth consecutive year of slow growth in the range of 3.6 percent and 4.1 percent. The share of the economy devoted to health spending has remained at 17.4 percent since 2009 as health spending and the Gross Domestic Product increased at similar rates for 2010 to Ø There is no fundamental shift yet in how health care is paid for or delivered. We still have a healthcare spending problem?! ü Physician payment rate reduction for Medicaid. ü Coverage expansion to previously uninsured individuals increases competition among carriers. ü Slower growth in the use of healthcare services. ü Cost sensitivity related to low income growth. ü Employers efforts to control costs Source: downloads/highlights.pdf; September

6 ACA Challenges: Keeping Grandfathered Status Ø Decision to maintain or eliminate Grandfathered Status Grandfathered plans are exempt from offering certain requirements: New patient protection provisions Limits on out-of-pocket maximums Certain preventive services on a first-dollar coverage basis Elimination of deductibles Ø All plans, regardless of whether Grandfathered, must offer unlimited lifetime and annual benefits on medical coverage. Source: 6

7 ACA Challenges: Keeping Grandfathered Status What is the advantage of keeping this status? Plans can avoid many of the ACA s requirements that may result in an increase in plan costs. Yet, it s very easy for Taft Hartley plans to lose this status if deductions or changes are made to premiums, benefits, co-pays and annual limits: Ø Eliminating benefits for certain conditions. Ø Increase in cost sharing by more than 15% (plus medical inflation). Ø Increase in co-payments by more than $5 per member (adjusted for medical inflation) or 15% (plus medical inflation) whichever is greater. Source: 7

2. Transitional Risk Corridors Program 3.")

8 The ACA s Premium Stabilization Rule Ø Standards to addressing problematic risk distribution due to adverse selection and other health care market variations. Ø 3 programs were implemented starting in 2014: 1. Belly Button Tax (Temporary Reinsurance Program) 2. Transitional Risk Corridors Program 3. Permanent Risk Adjustment Program 8

9 1. The Belly Button Tax (Temporary Reinsurance Program) What? Provides payment to plans covering an unhealthier population in the individual exchanges. Why? Who contributes? Who is eligible? How? When? To stabilize individual market premiums during the early years of new market reforms (Guaranteed Issue Provision). All individual & group issuers and Third Party Administrators (fullyinsured & self funded plans). Fee applies to each plan member, spouse and covered dependent (i.e. each belly button). Individual issuers that cover an unhealthier population (inside and outside exchanges) that are subject to ACA market rules are eligible for contributions. When plan s cost of a covered individual exceeds a certain threshold, that plan is eligible for payments. Source: 9

10 1. The Belly Button Tax (Temporary Reinsurance Fee) Year Reinsurance Pool U.S. Treasury Insurance Issuers and TPAs (Individual & Group Market) Status for self-funded/self administered group plans 2014 $10B $2B $5.25/month ($63/year) per member Requires Payment 2015 $6B $2B $3.67/month ($44/year) per member Temporarily Exempt* 2016 $4B $1B $2.25/month ($27/year) per member Temporarily Exempt* *Final rule has narrow definition: Plans must maintain and manage claims processing and adjudication in order to be recognized as self funded/self administered. Additional exemptions for self funded/self administered plans to use TPAs: Uses an unrelated third party to obtain a discount provider network or claim re-pricing services. Outsources core administrative functions for pharmacy or other excluded benefits (limited scope dental/vision) Outsources no more than 5% of core administrative services on non-excluded benefits (major medical). Source: 10

11 2. Transitional Risk Corridors Program What? Why? Sharing gains and losses on allowable costs between HHS and Qualified Health Plans (QHP) to help ensure stable health insurance premium settings in the health insurance marketplace (exchanges). Helps QHPs compete on price, not on plans risk pools. When? How? Works in conjunction with the ACA s Medical Loss Ratio (MLR) provision to distribute risk across health plans (80% MLR in individual market & 85% MLR in large group market). 11

12 2. Transitional Risk Corridors Program Collects HHS Pays Plans with lower than expected claims experience. < 97% of targeted amount set by HHS. ü Charges and payments are on percentage basis, not first dollar basis. ü If issuer's allowable costs are less than 97 percent of its target amount, it pays HHS a percentage of the difference Plans with higher than expected claims experience. > 103% of targeted amount set by HHS. 12

13 3. Permanent Risk Adjustment Program What? Why? Who participates? How? When? ü Shifts funding among insurers based on risk. Plans covering healthier populations in a given state will be assessed a charge. ü The charges will then serve as a source of payment to plans covering unhealthier populations. ü Reduces incentive for plans to avoid providing coverage to unhealthier enrollees. ü Program helps to fund health plans that cover a disproportionately unhealthy population both inside and outside the Health Insurance Marketplace to protect against adverse selection. ü All non-grandfathered plans in the individual and group market. ü Multi-state plans. ü Consumer Operated & Oriented Plans (COOPs). ü States operating their own exchanges (established state exchanges) have the option to operate their own state-based Risk Adjustment Program or to allow the federal government to run the program on Source:

14 How do all 3 programs work together? Permanent Risk Adjustment Program Spreads the risk so insurers don t just focus on covering the healthier population. Temporary Reinsurance Program Helps to reduce premiums by covering the cost for unhealthier enrollees in the individual market. Reinsurance contributions to reinsurance payouts Transitional Risk Corridors Program Limits the extent of health insurers losses and gains. 14

15 Impact of Medicaid Expansion Under the ACA Ø Expanded Medicaid to include individuals between the ages of 19 and 64 with incomes at or below 138% Federal Poverty Level (FPL) as of Individual: $16,243 Family of 3: $27,724 Ø Eligibility for Medicaid and CHIP is now based on new Modified Adjusted Gross Income (MAGI): Taxable wages + other income applicable adjustments = MAGI Ø Standardizes the approach to determining financial eligibility across states and health insurance affordability programs. Ø As part of this transition, states converted their existing Medicaid income limits to MAGI-equivalent limits. Ø Advanced payments of premium subsidies for individuals who purchased coverage on the individual exchanges are also determined using MAGI. Sources:

16 Current Status of State Medicaid Expansion Decisions 16

17 Cost and coverage implications of Medicaid Expansion Ø There is no deadline for states to implement the expansion. Ø States that already implemented the Medicaid Expansion in 2014 will receive 100% federal funding for the first 3 years (2014 to 2016). Ø Beginning in 2017, the federal match rate is as follows: 2017: 95% 2018: 94% 2019: 93% 2020+: 90% Source: 17

: Ø Coverage an individual must have to comply with the individual mandate and avoid the individual mandate penalty tax and that large")

18 Minimum Essential Coverage vs. Essential Health Benefits: Ø Minimum Essential Coverage (MEC): Ø Coverage an individual must have to comply with the individual mandate and avoid the individual mandate penalty tax and that large employers will be required to offer in 2015 to their employees to avoid the employer mandate penalty. Ø Employer s/plan's share of the total allowed costs of benefits provided is 60% or more of costs. The remaining 40% of costs are paid for by the covered individual (i.e.co-pays, deductibles, coinsurance) Source: Source: 18

do not need to provide EHB, but they must meet MEC requirements. Visit: www.")

19 Minimum Essential Coverage vs. Essential Health Benefits: Essential Health Benefits (EHB): Ø 10 core benefits that qualified health plans (QHPs) must cover on the public exchanges. Ø Insured plans that are not offered on public exchanges and self insured plan (i.e. self funded and multiemployer plans ) do not need to provide EHB, but they must meet MEC requirements. Visit: for list of EHB 19

20 Public and Private Exchanges: What it means for Self Funded Plans. 20

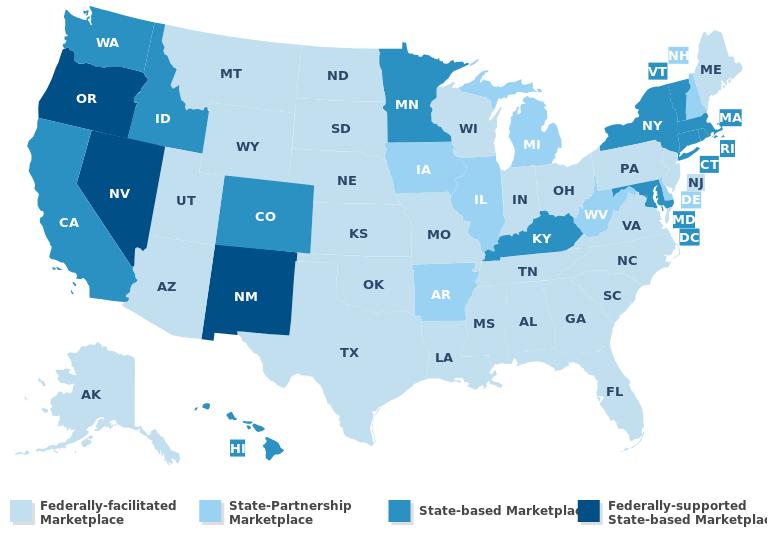

21 Health Insurance Marketplace Continuum of Exchange Options State-based Exchange State operates all exchange activities State-Federal Partnership Exchange State operates plan management and/or consumer assistance activities; may determine Medicaid/CHIP eligibility Federally-Facilitated Exchange HHS operates all exchange activities; state may determine Medicaid/CHIP eligibility Source: The Henry J. Kaiser Family Foundation

22 Health Insurance Marketplace PRIVATE EXCHANGE: v Defined Contribution structure. v Can control employer s overall health costs. v Enrollees can use HRA $$. v Relies on carrier for plan choices. v No premium or cost sharing subsidy available. State Based 2 variants: Ø Marketplace Ø State Partnership Federally Based Private Exchanges Affordable Health Care Public Exchanges PUBLIC EXCHANGE: v Covers Essential Health Benefits (EHB) v Has out of pocket limits for In-Network EHB v Provides Guaranteed Issue and Renewal v Enrollees can use HRA $$ v State & federal government make plan choices v Offers Premium & Cost Sharing subsidies for eligible enrollees. source: 22

$6,600 - individual $13,200 -family Young & Invincible For individuals under 30 yrs old. source: http://heathcare.")

23 Health Insurance Marketplace: Basics of the Public Exchange LEVELS OF COVERAGE Metal Actuarial Value Out of Pocket Platinum 90% 10% Gold 80% 20% Silver 70% 30% Bronze 60% 40% Maximum Out of Pocket for 2015 (excluding Premium) $6,600 - individual $13,200 -family Young & Invincible For individuals under 30 yrs old. source: 23

24 State Health Insurance Marketplace Types, 2015 Source: 24

25 Health Insurance Marketplace: Basics of the Public Exchange - Premium Subsidy Modified Annual Adjusted Gross Income (MAGI) Maximum Annual Premium Contribution % FPL (2015) Individual Family of 4 % of income** Individual Family of 4 100% $11,770 $24,250 2% $235 $ % $23,540 $48, % $1,483 $3, % $35,310 $72, % $3,354 $6, % $47,080 $97, % $4,473 $9,215 Based on premium costs for second lowest cost silver plan (70%) * Based on a sliding scale of caps. Premium subsidy amount is the same, even if enrollee selects a more expensive plan, such as platinum (90%) or gold (80%) or less expensive plan, such as bronze (60%).Young and Invincible level (catastrophic coverage only) does not qualify for premium subsidy eligibility. Source: 25

26 Health Insurance Marketplace: Basics of the Public Exchange - Premium Subsidy Subsidies will vary person to person within any plan and is based on family income and number of dependents. Annual Family Income Age Single (S) or Family of 4 (F) Premium Amount paid by enrollee Subsidy $30, S $3,167 $2,492 $675 $30, F Medicaid $50, S $3,742 $3,742 $0 $50, F $10,776 $3,340 $7,436 $70, S $4,629 $4,629 $0 $70, F $12,548 $6,559 $5,989 $80, S $4,629 $4,629 $0 $80, F $12,548 $7,648 $4,900 $90, S $4,629 $4,629 $0 $90, F $12,548 $8,604 $3,944 Examples of estimated insurance premiums above are based on 2015 incomes and number of dependents. For family of 4, estimates based on 2 adults of same age, and 2 children under age of 21, all with no tobacco use. Source: 26

27 Health Insurance Marketplace: Basics of the Public Exchange- Premium Subsidy To qualify for subsidies, Individual must NOT be: Ø Eligible for coverage through an employer sponsored plan where the employer makes the required contribution toward that coverage. Ø Covered by Medicaid, Medicare, military or veterans' coverage or other coverage recognized by HHS. Ø Subsidy eligibility in states that did not expand Medicaid Individuals with household incomes at or below 138% of FPL are NOT: Ø Eligible for a premium subsidy AND Ø Responsible for paying the individual mandate fee. 27

28 Health Insurance Marketplace: Basics of the Public Exchange-Cost Sharing Reductions What? How? Who is eligible? Why? What does this mean for enrollees? It protects enrollees in silver plans from high out-of-pocket costs by reducing the charges enrollees would have to pay to receive services. Makes it easier for enrollees who are looking to purchase coverage to compare plans in the Health Insurance Marketplace. Automatically reduces the charges for enrollee to receive services. It is not reimbursed to the enrollee and not reconciled at end of year. Individuals enrolled in a silver plan ONLY to ensure that any cost sharing reduction is based on 70% actuarial value (AV). Benefits all people enrolled in a silver plan on the exchanges (those who use very little services & those who use a great deal of service). Source: 28

29 Health Insurance Marketplace: Basics of the Public Exchange-Cost Sharing Reductions Ø People who qualify for the premium subsidy will also be eligible for the cost sharing reduction if they enroll in a silver plan. Ø Cost sharing reductions based on FPL in a silver plan variations that corresponds with their household income. Household Income New Actuarial Value % Annual Out of Pocket Maximums % of FPL For cost sharing reduction Self Only Family 100% 150% 94% $2,250 $4, %-200% 87% $2,250 $4, % 250% 73% $5,200 $10,400 29

.")

30 Health Insurance Marketplace: Basics of the Public Exchange-Cost Sharing Reductions What does this mean for insurance providers offering silver plans on the exchanges? Can use existing cost sharing limits that apply to high deductible health plans (HDHPs) that are qualified to be paired with Health Savings Accounts (HSAs). Health plans that provide cost sharing reductions to enrollees will be eligible for full reimbursement for the reduction amounts from HHS. 30

31 Health Insurance Marketplace: Basics of the Public Exchange Ø Sets the standards for Qualified Health Plans QHPs Ø Determines eligibility for Medicaid, CHIP & premium subsidies Open enrollment period: No enrollment outside this period, except for special circumstances: November 1, 2015 January 31, 2016 Eligibility Requirements: Ø Resident of the state where the exchange is established. Ø Not incarcerated. Ø US Citizen. 31

32 Defining Coverage Affordability Coverage is considered affordable if the cost to the employee of self-only coverage does not exceed 9.5% of that individual employee s household income. The definition of affordability is an issue for multiemployer plan participants. Ø What if employer offers dependent coverage? Ø The employee s cost for coverage may exceed 9.5% of his or her household income. Employee and his/her dependents are NOT eligible for subsidies on the exchanges, even if coverage offered by employer is NOT affordable. Ø Is there a solution for self funded plans? 32

33 The Employer Mandate Also known as the Employer Shared Responsibility Penalty or Employer Penalty of Requires businesses that do not provide affordable coverage to pay a penalty. Mandate was delayed until 2015 for large employers and 2016 for small to medium employers. 33

34 The Employer Mandate Employer has more than 100 employees NO YES Employer offers the opportunity to enroll in minimum essential coverage MEC-under an eligible employer-sponsored plan. If more than 50 employees but fewer than has until 2016 to phase in health care coverage for their full time employees. YES Coverage is at least 60% of covered health care expenses NO Did at least 1 employee receive a premium subsidy or cost sharing subsidy in the Health Insurance Marketplace? YES NO Employer pays penalty for not offering coverage at all OR not offering affordable coverage YES NO There is no penalty payment requirement of the employer 34

X $2,000.")

X $2,000] or [Total # of employees who receive tax subsidies)")

35 The Employer Mandate: How it s determined Employer drops coverage completely: Employee is eligible to purchase health insurance on the exchanges and receiving a subsidy to cover premium. Employer offers coverage that is not considered affordable or of minimum value: Penalty would only apply if the coverage provided to the employee is more than 9.5% of that employee s individual income. Employer is required to pay penalty (Total # of full time employees minus 80) X $2,000. Employer Penalty Penalty is lesser of: (Total # of full time employees minus 80) X $2,000] or [Total # of employees who receive tax subsidies) X$3,000.] Starting in 2016, the penalty will exempt the first 30 full-time employees, instead of the first

36 The Employer Mandate: 90 Day Waiting Period How will the Employer Mandate impact employers who participate in collectively bargained plans? Ø Limits on waiting periods: Ø Full time, part time, seasonal, intermittent? Ø Setting rules for becoming eligible: Ø Measurement or look-back period in determining eligibility. 36

37 The Employer Mandate: Possible Outcomes Employer : May try to avoid or reduce penalty for not providing MEC &/or offering unaffordable coverage. Potential Result: Employee: Will want to avoid the individual penalty for not purchasing MEC. 1. Rise in employers offering mini-med/skinny plans to employees. These plans do not have annual dollar limits but do have limited categories of coverage. On November 5, 2014, HHS, Department of Treasury, including IRS released a guidance document advising that large employers offering health plans that DO NOT cover inpatient hospital services are NOT offering minimum value health coverage. 2. Rise in Private Exchanges and in offering supplemental insurance products. Critical illness, dental, vision, hospital confinement, short term disability. Sources:

38 The Cadillac Tax What? When? Who Pays? Why? 40% tax on benefits exceeding certain thresholds based on total cost of coverage for: ü The average cost for the health insurance plan (whether insured or self-funded) ü Employer contributions to an HAS, Archer medical spending account or HRA ü Contributions (including employee-elected payroll deductions and non-elective employer contributions) to an FSA ü The value of coverage in certain on-site medical clinics ü The cost for certain limited-benefit plans if they are provided on a tax-preferred basis Scheduled to take effect in 2018 and is permanent. The entity that shall pay the excise tax is (1) the health insurance issuer in the case of applicable coverage provided under an insured plan, (2) the employer if the applicable coverage consists of coverage under which the employer makes contributions to an HAS or Archer MSA, and (3) the person that administers the plan in the case of any other applicable coverage. To help finance component of the ACA, including the creation of low-cost health insurance products on the exchanges. 38

39 The Cadillac Tax How much? Thresholds will be based on: ü Medical inflation between 2010 and 2018 and will increase if the actual growth in healthcare costs exceeds the projected growth. ü In 2019, will go by CPI-U plus 1% point. Cost threshold indexed after 2018: Individual: $10,200 Family: $27,500 Multiemployer Plans can use the family threshold. ü Thresholds can be adjusted for age and gender, qualified retiree and/or high risk profession status. Source:

40 The Cadillac Tax EXAMPLES: Family Coverage Cost of Plan per Family = $32,500 $32,500 - $27,500 = $5,000 over threshold 500 Families x $5,000 = $2,500,000 Excise Tax = $1,000,000 (40% of $2.5M) Self-only Coverage Cost of Plan per Individual = $12,000 $12,000 - $10,200 = $1,800 over threshold 250 covered individuals x $1,800 = $450,000 Excise Tax= $180,000 (40% of 450,000) Source:

41 The Cadillac Tax The cost excludes premiums paid by employers and employees for: Excepted Benefits: Critical illness, hospital indemnity, accident, disability, long term care, etc. Vision and dental under separate policies from medical (considered excepted benefits) Source:

42 What plan administrators & trustees should look for: Ø Minimum Essential Coverage (MEC) and affordability. Ø Is the plan within the 60% minimum value standard and is the coverage intended to be affordable for plan members? Ø Maintaining or losing Grandfathered status. Ø Employer Mandate. Ø Future rules will be issued by the IRS detailing reporting requirements for the Employer Mandate in 2015 and Ø Is the plan in compliance? Ø Preparing for Cadillac Tax in Ø Added complexity to Collective Bargained Agreements. 42

The Affordable Care Act Update

The Affordable Care Act Update Presented by: The Union Labor Life Insurance Company SOLUTIONS FOR THE UNION WORKPLACE SPECIALTY INSURANCE INVESTMENTS Overview of Presentation 1. 2010 2014 Provisions overview

The Affordable Care Act Update Presented by: The Union Labor Life Insurance Company SOLUTIONS FOR THE UNION WORKPLACE SPECIALTY INSURANCE INVESTMENTS Overview of Presentation 1. 2010 2014 Provisions overview

Health Care Reform at-a-glance

Health Care Reform at-a-glance August 2015 Table of Contents Employer mandate...3 Individual mandate...3 Health plan provisions applying to both grandfathered and non-grandfathered employer plans...4 Health

Health Care Reform at-a-glance August 2015 Table of Contents Employer mandate...3 Individual mandate...3 Health plan provisions applying to both grandfathered and non-grandfathered employer plans...4 Health

2014 and Beyond. This timeline explains how and when the Affordable Care Act (ACA) provisions will be implemented over the next few years.

provisions will be implemented over the next few years.") December This timeline explains how and when the Affordable Care Act (ACA) provisions will be implemented over the next few years. Get Covered Illinois, the Official Health Marketplace of Illinois While

December This timeline explains how and when the Affordable Care Act (ACA) provisions will be implemented over the next few years. Get Covered Illinois, the Official Health Marketplace of Illinois While

The Affordable Care Act: A Summary on Healthcare Reform. The Wyoming Department of Insurance

The Affordable Care Act: A Summary on Healthcare Reform The Wyoming Department of Insurance Additional Resources Wyoming Insurance Department: http://doi.wyo.gov/ or toll free at 1-(800)-438-5768 Information

The Affordable Care Act: A Summary on Healthcare Reform The Wyoming Department of Insurance Additional Resources Wyoming Insurance Department: http://doi.wyo.gov/ or toll free at 1-(800)-438-5768 Information

Health Care Reform: Be Prepared for 2014

Health Care Reform: Be Prepared for 2014 Your Health Care Reform Team: Moderator Eboni Britt POMCO Group Marketing Manager Co-presenter Jessica Marabella POMCO Group Account Manager Co-presenter Amy Zell

Health Care Reform: Be Prepared for 2014 Your Health Care Reform Team: Moderator Eboni Britt POMCO Group Marketing Manager Co-presenter Jessica Marabella POMCO Group Account Manager Co-presenter Amy Zell

Health Care Reform: The Financial Impact on the Employer

Health Care Reform: The Financial Impact on the Employer WP&BC August 15, 2012 1 1 Supreme Court Examines Constitutionality U.S. Supreme Court Ruling: June 28, 2012 Individual Mandate - Constitutional

Health Care Reform: The Financial Impact on the Employer WP&BC August 15, 2012 1 1 Supreme Court Examines Constitutionality U.S. Supreme Court Ruling: June 28, 2012 Individual Mandate - Constitutional

H E A L T H C A R E R E F O R M T I M E L I N E

H E A L T H C A R E R E F O R M T I M E L I N E On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act (ACA), into law. The ACA makes sweeping changes to the U.S.

H E A L T H C A R E R E F O R M T I M E L I N E On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act (ACA), into law. The ACA makes sweeping changes to the U.S.

The MC Academy The Employee Benefits and Executive Compensation Series HEALTH CARE REFORM ACT

The MC Academy The Employee Benefits and Executive Compensation Series HEALTH CARE REFORM ACT April 16, 2013 Topics Health Care Reform under the Patient Protection and Affordable Care Act Overview Exchanges

The MC Academy The Employee Benefits and Executive Compensation Series HEALTH CARE REFORM ACT April 16, 2013 Topics Health Care Reform under the Patient Protection and Affordable Care Act Overview Exchanges

Affordable Care Act and Employers

Affordable Care Act and Employers Important Details about Health Care Reform The Affordable Care Act (ACA, i.e., federal health care reform) makes significant changes to health insurance practices nationwide.

Affordable Care Act and Employers Important Details about Health Care Reform The Affordable Care Act (ACA, i.e., federal health care reform) makes significant changes to health insurance practices nationwide.

Health Care Reform. Navigating The Maze Of. What s Inside

Navigating The Maze Of Health Care Reform What s Inside Questions and Answers on Health Care Reform Health Care Reform Timeline Health Care Reform Glossary Questions and Answers on Health Care Reform I

Navigating The Maze Of Health Care Reform What s Inside Questions and Answers on Health Care Reform Health Care Reform Timeline Health Care Reform Glossary Questions and Answers on Health Care Reform I

The Affordable Care Act; 2014 and Beyond

The Affordable Care Act; 2014 and Beyond Presented by: Lacey Robinson, ACA Certified Vice President & Senior Benefits Consultant Gregory & Appel December 10, 2013 Agenda 2014 ACA Mandates ACA Intention

The Affordable Care Act; 2014 and Beyond Presented by: Lacey Robinson, ACA Certified Vice President & Senior Benefits Consultant Gregory & Appel December 10, 2013 Agenda 2014 ACA Mandates ACA Intention

The Affordable Care Act: A Summary on Healthcare Reform. The Wyoming Department of Insurance

The Affordable Care Act: A Summary on Healthcare Reform The Wyoming Department of Insurance The ACA is a federal law that impacts Wyoming and its citizens. The State of Wyoming has filed a lawsuit against

The Affordable Care Act: A Summary on Healthcare Reform The Wyoming Department of Insurance The ACA is a federal law that impacts Wyoming and its citizens. The State of Wyoming has filed a lawsuit against

Health Care Reform Overview

Publication date: March 2014 Health Care Reform Overview for Large Group (51+) Plans The following chart provides a breakdown of key Affordable Care Act (ACA) provisions by year for large group plans,

Publication date: March 2014 Health Care Reform Overview for Large Group (51+) Plans The following chart provides a breakdown of key Affordable Care Act (ACA) provisions by year for large group plans,

Fall Health Care Symposium

2014 Fall Health Care Symposium Agenda ACA What s Happening Now Group vs. Individual Coverage Alternative Funding Options Why Wellness Matters Transforming HR Through Technology Understanding Obamacare

2014 Fall Health Care Symposium Agenda ACA What s Happening Now Group vs. Individual Coverage Alternative Funding Options Why Wellness Matters Transforming HR Through Technology Understanding Obamacare

Health Care Reform under the Patient Protection and Affordable Care Act ( PPACA ) provisions effective January 1, 2014

provisions effective January 1, 2014") The New Health Care Landscape Today s Agenda Health Care Reform under the Patient Protection and Affordable Care Act ( PPACA ) provisions effective January 1, 2014 Exchanges and Qualified Health Plans

The New Health Care Landscape Today s Agenda Health Care Reform under the Patient Protection and Affordable Care Act ( PPACA ) provisions effective January 1, 2014 Exchanges and Qualified Health Plans

Patient Protection and Affordable Care Act

September 27, 2010 Patient Protection and Affordable Care Act 1 9020 Stony Point Parkway Suite 200 Richmond, VA 23235 804-267-3100 Agenda Overview Employer Feedback Terms Components of Health Care Reform

September 27, 2010 Patient Protection and Affordable Care Act 1 9020 Stony Point Parkway Suite 200 Richmond, VA 23235 804-267-3100 Agenda Overview Employer Feedback Terms Components of Health Care Reform

The Patient Protection and Affordable Care Act. An In-Depth Analysis of Provisions Directly or Indirectly Affecting Group Health Plans

The Patient Protection and Affordable Care Act An In-Depth Analysis of Provisions Directly or Indirectly Affecting Group Health Plans Table of Contents Section 1 Insurance Plan Provisions Prohibition on

The Patient Protection and Affordable Care Act An In-Depth Analysis of Provisions Directly or Indirectly Affecting Group Health Plans Table of Contents Section 1 Insurance Plan Provisions Prohibition on

Navajo County Schools EBT

Navajo County Schools EBT Affordable Care Act (ACA) Update Aaron Polkoski Segal Consulting January 31st, 2014 Copyright 2013 by The Segal Group, Inc., parent of The Segal Company. All rights reserved.

Navajo County Schools EBT Affordable Care Act (ACA) Update Aaron Polkoski Segal Consulting January 31st, 2014 Copyright 2013 by The Segal Group, Inc., parent of The Segal Company. All rights reserved.

Pennsylvania Association of Health Underwriters Advisors and Advocates for Employers, Employees and Health Care Consumers

Pennsylvania Association of Health Underwriters Advisors and Advocates for Employers, Employees and Health Care Consumers Timeline for Health Care Reform March 26, 2010 The Patient Protection and Affordable

Pennsylvania Association of Health Underwriters Advisors and Advocates for Employers, Employees and Health Care Consumers Timeline for Health Care Reform March 26, 2010 The Patient Protection and Affordable

HEALTHCARE REFORM 2014 AND BEYOND WHAT S NEXT?

HEALTHCARE REFORM 2014 AND BEYOND WHAT S NEXT? Associated Financial Group 1 AFFORDABLE CARE ACT (ACA) WHEN DID IT BECOME LAW? The ACA became law on March 23, 2010. The objective was to expand coverage,

HEALTHCARE REFORM 2014 AND BEYOND WHAT S NEXT? Associated Financial Group 1 AFFORDABLE CARE ACT (ACA) WHEN DID IT BECOME LAW? The ACA became law on March 23, 2010. The objective was to expand coverage,

Health Reform Update. April 1, Presented by: Chip Kerby Liberté Group LLC (202)

") Health Reform Update April 1, 2010 Presented by: Chip Kerby Liberté Group LLC chip@libertegroup.com (202) 756-2459 Agenda Background Key elements Impact on stakeholders 1 Background Sources of Coverage

Health Reform Update April 1, 2010 Presented by: Chip Kerby Liberté Group LLC chip@libertegroup.com (202) 756-2459 Agenda Background Key elements Impact on stakeholders 1 Background Sources of Coverage

The Affordable Care Act: Time to Prepare for 2014 and Beyond

The Affordable Care Act: Time to Prepare for 2014 and Beyond Howard Van Mersbergen Vice President of Employee Benefits, Christian Schools International Brian C. Meekhof Benefits Administrator, Christian

The Affordable Care Act: Time to Prepare for 2014 and Beyond Howard Van Mersbergen Vice President of Employee Benefits, Christian Schools International Brian C. Meekhof Benefits Administrator, Christian

Health Care Reform: Legislative Brief Important Effective Dates for Employers and Health Plans

Health Care Reform: Legislative Brief Important Effective Dates for Employers and Health Plans On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act (ACA), into

Health Care Reform: Legislative Brief Important Effective Dates for Employers and Health Plans On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act (ACA), into

Simple answers to health reform s complex issues facing every employer, and what you can do now to protect your business and your future.

Simple answers to health reform s complex issues facing every employer, and what you can do now to protect your business and your future. If you have any questions, please contact: Health Reform: A Guide

Simple answers to health reform s complex issues facing every employer, and what you can do now to protect your business and your future. If you have any questions, please contact: Health Reform: A Guide

HEALTH CARE REFORM Focus on Group Coverage Blue Cross and Blue Shield of Minnesota. All rights reserved.

HEALTH CARE REFORM Focus on Group Coverage 2011 Blue Cross and Blue Shield of Minnesota. All rights reserved. Current Insurance Coverage Environment Minnesota United States Uninsured 9% Ot her Public 1%

HEALTH CARE REFORM Focus on Group Coverage 2011 Blue Cross and Blue Shield of Minnesota. All rights reserved. Current Insurance Coverage Environment Minnesota United States Uninsured 9% Ot her Public 1%

Discussion of Key Health Care Reform Provisions Affecting Commercial Health Plans

Discussion of Key Health Care Reform Provisions Affecting Commercial Health Plans Presented by Stuart Rachlin, Alex Cires Milliman Tampa, FL 813-282-9262 SEAC June 2010 Meeting West Palm Beach, FL June

Discussion of Key Health Care Reform Provisions Affecting Commercial Health Plans Presented by Stuart Rachlin, Alex Cires Milliman Tampa, FL 813-282-9262 SEAC June 2010 Meeting West Palm Beach, FL June

The Patient Protection and Affordable Care Act

The Patient Protection and Affordable Care Act 2015 marks the beginning of the fifth full year of the Patient Protection and Affordable Care Act (ACA). We want to take the opportunity to look ahead and

The Patient Protection and Affordable Care Act 2015 marks the beginning of the fifth full year of the Patient Protection and Affordable Care Act (ACA). We want to take the opportunity to look ahead and

Affordable Care Act (ACA) An Overview of Key Provisions

An Overview of Key Provisions") Affordable Care Act (ACA) An Overview of Key Provisions Locey & Cahill, LLC Presentation to the: New York State Association of Management Advocates for School Labor Affairs, Inc. 36 th Annual Summer Conference

Affordable Care Act (ACA) An Overview of Key Provisions Locey & Cahill, LLC Presentation to the: New York State Association of Management Advocates for School Labor Affairs, Inc. 36 th Annual Summer Conference

Monitoring the ACA s. Vital Signs. The Affordable Care Act A Progress Report

Monitoring the ACA s Vital Signs The Affordable Care Act A Progress Report Today s Discussion Affordable Care Act Some Foundational Knowledge Affordable Care Act Compliance Requirements Plan Design Reporting

Monitoring the ACA s Vital Signs The Affordable Care Act A Progress Report Today s Discussion Affordable Care Act Some Foundational Knowledge Affordable Care Act Compliance Requirements Plan Design Reporting

Looking for a Life Vest?

Looking for a Life Vest? November 20 th, 2014 @thomasharte Agenda: Looking for a Life Vest? Health Care Reform: What s new with ACA?? Provisions Already in Effect Preparing for Health Care Reform Primary

Looking for a Life Vest? November 20 th, 2014 @thomasharte Agenda: Looking for a Life Vest? Health Care Reform: What s new with ACA?? Provisions Already in Effect Preparing for Health Care Reform Primary

Health Care Reform Health Plans Overview

Health Care Reform Health Plans Overview Topics Status of health care reform Grandfathered plans Timeline for compliance Health Care Reform What is It? Patient Protection and Affordable Care Act (PPACA)

Health Care Reform Health Plans Overview Topics Status of health care reform Grandfathered plans Timeline for compliance Health Care Reform What is It? Patient Protection and Affordable Care Act (PPACA)

Healthcare Reform Timeline

Healthcare Reform Timeline Provisions That Will Impact Individuals & Employers August 2012 No one sees the direct results of the Patient Protection and Affordable Care Act (PPACA) like the health insurance

Healthcare Reform Timeline Provisions That Will Impact Individuals & Employers August 2012 No one sees the direct results of the Patient Protection and Affordable Care Act (PPACA) like the health insurance

Complying with Health Care Reform

Complying with Health Care Reform April 17, 2013 1 1 What Happened? In March 2010, Congress passed and the President signed health reform in: The Patient Protection and Affordable Care Act The Health Care

Complying with Health Care Reform April 17, 2013 1 1 What Happened? In March 2010, Congress passed and the President signed health reform in: The Patient Protection and Affordable Care Act The Health Care

Crosses the Finish Line. A presentation for the Manufacturer & Business Association

Health Care Reform Crosses the Finish Line A presentation for the Manufacturer & Business Association Background Statement of the problem 50,000,000 uninsured Healthcare costs rising at 2x 4x annual rate

Health Care Reform Crosses the Finish Line A presentation for the Manufacturer & Business Association Background Statement of the problem 50,000,000 uninsured Healthcare costs rising at 2x 4x annual rate

Health Care Reform: What s In Store for Employer Health Plans?

Health Care Reform: What s In Store for Employer Health Plans? April 21, 2010 Presented by: Sue O. Conway sconway@wnj.com (616) 752-2153 Norbert F. Kugele nkugele@wnj.com (616) 752-2186 Copyright 2010

Health Care Reform: What s In Store for Employer Health Plans? April 21, 2010 Presented by: Sue O. Conway sconway@wnj.com (616) 752-2153 Norbert F. Kugele nkugele@wnj.com (616) 752-2186 Copyright 2010

AFFORDABLE CARE ACT: STATUS CHART Health Plans

AFFORDABLE CARE ACT: STATUS CHART Health Plans July 2017 TODD MARTIN, PARTNER 612.335.1409 todd.martin@stinson.com Table of Contents Page ACA Coverage Mandates... 1 ACA Insurance Market Rules... 5 ACA

AFFORDABLE CARE ACT: STATUS CHART Health Plans July 2017 TODD MARTIN, PARTNER 612.335.1409 todd.martin@stinson.com Table of Contents Page ACA Coverage Mandates... 1 ACA Insurance Market Rules... 5 ACA

06/29/2015_830 AM. Healthcare Reform How Will Your Business be Affected in 2015 and Beyond? Introduction

Healthcare Reform How Will Your Business be Affected in 2015 and Beyond? Introduction Overview of ACA Healthcare Reform in 2015 What s on the Horizon Potential Legislative Actions Patient Protection and

Healthcare Reform How Will Your Business be Affected in 2015 and Beyond? Introduction Overview of ACA Healthcare Reform in 2015 What s on the Horizon Potential Legislative Actions Patient Protection and

An Employer s Guide to Health Care Reform. Important details to navigate employer-provided benefits amidst a changing health care landscape.

An Employer s Guide to Health Care Reform Important details to navigate employer-provided benefits amidst a changing health care landscape. Navigating a new health care landscape Health care reform, also

An Employer s Guide to Health Care Reform Important details to navigate employer-provided benefits amidst a changing health care landscape. Navigating a new health care landscape Health care reform, also

8/7/2013 INSURANCE MADE SIMPLE. 1

Presented by: Mark E. Baker Vice President Employee Benefits INSURANCE MADE SIMPLE. 1 Health Care Reform provisions in effect 2010-2012 Large Employer Defined Pay or Play Mandate and Penalties Small Employer

Presented by: Mark E. Baker Vice President Employee Benefits INSURANCE MADE SIMPLE. 1 Health Care Reform provisions in effect 2010-2012 Large Employer Defined Pay or Play Mandate and Penalties Small Employer

Important Effective Dates for Employers and Health Plans

Brought to you by Hipskind Seyfarth Risk Solutions Important Effective Dates for Employers and Health Plans On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act

Brought to you by Hipskind Seyfarth Risk Solutions Important Effective Dates for Employers and Health Plans On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act

Tennessee Public Health Association. Overview of the Affordable Care Act

Tennessee Public Health Association Overview of the Affordable Care Act Susie Baird Director of Policy Health Care Finance and Administration September 12, 2013 1 Origins of ACA Signed into law on March

Tennessee Public Health Association Overview of the Affordable Care Act Susie Baird Director of Policy Health Care Finance and Administration September 12, 2013 1 Origins of ACA Signed into law on March

4/22/2014. Health Care Reform. Disclosure. Health Care Reform. How Will it Change Your Business Strategy?

Health Care Reform How Will it Change Your Business Strategy? OHCA Educational Session April 29 th, 2014 Presented by: Roderick S. Wood, CHRS Huntington Insurance, Inc. Disclosure This presentation contains

Health Care Reform How Will it Change Your Business Strategy? OHCA Educational Session April 29 th, 2014 Presented by: Roderick S. Wood, CHRS Huntington Insurance, Inc. Disclosure This presentation contains

GLOSSARY OF KEY AFFORDABLE CARE ACT AND COMMON HEALTH PLAN TERMS

GLOSSARY OF KEY AFFORDABLE CARE ACT AND COMMON HEALTH PLAN TERMS Note: in the event of any conflict between this glossary and your plan document/summary plan description (SPD) or policy/certificate, the

GLOSSARY OF KEY AFFORDABLE CARE ACT AND COMMON HEALTH PLAN TERMS Note: in the event of any conflict between this glossary and your plan document/summary plan description (SPD) or policy/certificate, the

Patient Protection and Affordable Care Act of 2009: Health Insurance Market Reforms

Patient Protection and Affordable Care Act of 2009: Health Insurance Market Reforms Provision Notes Standards SUBTITLE C Quality Health Insurance Coverage for All Americans PART I HEALTH INSURANCE MARKET

Patient Protection and Affordable Care Act of 2009: Health Insurance Market Reforms Provision Notes Standards SUBTITLE C Quality Health Insurance Coverage for All Americans PART I HEALTH INSURANCE MARKET

THE AFFORDABLE CARE ACT: PAST, PRESENT & FUTURE October 20, 2015

HEALTH WEALTH CAREER THE AFFORDABLE CARE ACT: PAST, PRESENT & FUTURE October 20, 2015 CHERYL RISLEY HUGHES WASHINGTON, DC Key Elements of Health Care Reform for Employers 2010 Accounting impact of change

HEALTH WEALTH CAREER THE AFFORDABLE CARE ACT: PAST, PRESENT & FUTURE October 20, 2015 CHERYL RISLEY HUGHES WASHINGTON, DC Key Elements of Health Care Reform for Employers 2010 Accounting impact of change

2015 Heath Care Reform Compliance Overview

2015 Heath Care Reform Compliance Overview The Affordable Care Act (ACA) has made a number of significant changes to group health plans since the law was enacted over four years ago. Many of these key

2015 Heath Care Reform Compliance Overview The Affordable Care Act (ACA) has made a number of significant changes to group health plans since the law was enacted over four years ago. Many of these key

Health Care Reform: Industry Based Fees and Taxes

Health Care Reform: Industry Based Fees and Taxes The Patient Protection and Affordable Care Act (ACA) imposes a number of broad-based fees and taxes on entities associated with providing health care coverage.

Health Care Reform: Industry Based Fees and Taxes The Patient Protection and Affordable Care Act (ACA) imposes a number of broad-based fees and taxes on entities associated with providing health care coverage.

Affordable Care Act Update

Affordable Care Act Update CLAconnect.com May 19, 2015 Presented by: Anita Baker Session Objectives Identify key definitions impacting employer implementation of the Affordable Care Act Understand the

Affordable Care Act Update CLAconnect.com May 19, 2015 Presented by: Anita Baker Session Objectives Identify key definitions impacting employer implementation of the Affordable Care Act Understand the

Key Elements of Health Care Reform for Employers

Key Elements of Health Care Reform for Employers Change in tax treatment for over-age 2010 dependent coverage Early retiree medical reinsurance Accounting impact of change in Medicare retiree drug subsidy

Key Elements of Health Care Reform for Employers Change in tax treatment for over-age 2010 dependent coverage Early retiree medical reinsurance Accounting impact of change in Medicare retiree drug subsidy

Affordable Care Act Planning for CPAs. Ben Conley Seyfarth Shaw LLP

Affordable Care Act Planning for CPAs Ben Conley Seyfarth Shaw LLP Overview Background ACA & Taxes Taxes on Employers (and Tax Credits for Employers) Taxes on Individuals (and Tax Credits for Individuals)

Affordable Care Act Planning for CPAs Ben Conley Seyfarth Shaw LLP Overview Background ACA & Taxes Taxes on Employers (and Tax Credits for Employers) Taxes on Individuals (and Tax Credits for Individuals)

2016 Compliance Checklist

Brought to you by Risk Management Advisors, Inc. 2016 Compliance Checklist The Affordable Care Act (ACA) has made a number of significant changes to group health plans since the law was enacted over four

Brought to you by Risk Management Advisors, Inc. 2016 Compliance Checklist The Affordable Care Act (ACA) has made a number of significant changes to group health plans since the law was enacted over four

THE AFFORDABLE CARE ACT: 2014 AND BEYOND

THE AFFORDABLE CARE ACT: 2014 AND BEYOND October 28, 2013 Howard Van Mersbergen, Vice President of Employee Benefits, Christian Schools International Julie Sessions, Principal, Mercer Patient Protection

THE AFFORDABLE CARE ACT: 2014 AND BEYOND October 28, 2013 Howard Van Mersbergen, Vice President of Employee Benefits, Christian Schools International Julie Sessions, Principal, Mercer Patient Protection

Health Care Reform Update. April 2013

Health Care Reform Update April 2013 2013 Compliance Issues Summary of Benefits and Coverage Simple explanation of benefits and costs 4 double sided pages, 12 point or larger font Can provide in paper

Health Care Reform Update April 2013 2013 Compliance Issues Summary of Benefits and Coverage Simple explanation of benefits and costs 4 double sided pages, 12 point or larger font Can provide in paper

MYTHS & REALITIES OF HEALTH CARE REFORM

MYTHS & REALITIES OF HEALTH CARE REFORM The Florida Bar Solo & Small Firm Annual Conference January 25, 2014 Presented By: Kirsten Vignec Shareholder Introduction On March 23, 2010, the Patient Protection

MYTHS & REALITIES OF HEALTH CARE REFORM The Florida Bar Solo & Small Firm Annual Conference January 25, 2014 Presented By: Kirsten Vignec Shareholder Introduction On March 23, 2010, the Patient Protection

Affordable Care Act: Evolving Requirements & Compliance Implications

Affordable Care Act: Evolving Requirements & Compliance Implications Peggy Baron Bricker & Eckler LLP 100 South Third Street Columbus, OH 43215 Employer Shared Responsibility Assessable Payments Beginning

Affordable Care Act: Evolving Requirements & Compliance Implications Peggy Baron Bricker & Eckler LLP 100 South Third Street Columbus, OH 43215 Employer Shared Responsibility Assessable Payments Beginning

Health Reform Employer Perspective

Health Reform Employer Perspective Copyright 2008 McGraw Wentworth, Inc. All rights reserved. 1 Government Requirements Expanding Federal requirements effecting employers expanded significantly in 2009

Health Reform Employer Perspective Copyright 2008 McGraw Wentworth, Inc. All rights reserved. 1 Government Requirements Expanding Federal requirements effecting employers expanded significantly in 2009

Understanding the Impacts of Health Care Reform on Employers : 2014 and beyond

2013 CliftonLarsonAllen LLP Understanding the Impacts of Health Care Reform on Employers : 2014 and beyond cliftonlarsonallen.com Peoria County Bar Association January 25, 2014 Deb Freeland Objectives

2013 CliftonLarsonAllen LLP Understanding the Impacts of Health Care Reform on Employers : 2014 and beyond cliftonlarsonallen.com Peoria County Bar Association January 25, 2014 Deb Freeland Objectives

HEALTH CARE REFORM 2010 A CHRONOLOGICAL OVERVIEW OF THE LAW'S OBLIGATIONS FOR EMPLOYERS. Henry Smith. Smith & Downey.

HEALTH CARE REFORM 2010 A CHRONOLOGICAL OVERVIEW OF THE LAW'S OBLIGATIONS FOR EMPLOYERS Henry Smith Smith & Downey hsmith@smithdowney.com 410-321-9350 [Note that this presentation is merely a very broad

HEALTH CARE REFORM 2010 A CHRONOLOGICAL OVERVIEW OF THE LAW'S OBLIGATIONS FOR EMPLOYERS Henry Smith Smith & Downey hsmith@smithdowney.com 410-321-9350 [Note that this presentation is merely a very broad

OVERVIEW OF THE AFFORDABLE CARE ACT. September 23, 2013

OVERVIEW OF THE AFFORDABLE CARE ACT September 23, 2013 Outline The New Continuum of Coverage Medicaid and CHIP Are Changing The New Marketplaces Insurance Affordability Programs Shared Responsibility Requirement

OVERVIEW OF THE AFFORDABLE CARE ACT September 23, 2013 Outline The New Continuum of Coverage Medicaid and CHIP Are Changing The New Marketplaces Insurance Affordability Programs Shared Responsibility Requirement

Questions from Agents/Producers

Questions from Agents/Producers Q. How will income be determined? Will we take the word of the consumer about their income without verifying? A. Incomes will be verified by the data hub on the Federal

Questions from Agents/Producers Q. How will income be determined? Will we take the word of the consumer about their income without verifying? A. Incomes will be verified by the data hub on the Federal

Health Policy Essentials: Private Health Insurance. Bernadette Fernandez, Annie Mach, Janemarie Mulvey March 1, 2013

Health Policy Essentials: Private Health Insurance Bernadette Fernandez, Annie Mach, Janemarie Mulvey March 1, 2013 Private Health Insurance Insurance provides protection from economic loss Risk likelihood

Health Policy Essentials: Private Health Insurance Bernadette Fernandez, Annie Mach, Janemarie Mulvey March 1, 2013 Private Health Insurance Insurance provides protection from economic loss Risk likelihood

January 1, State Notification Regarding Exchanges

January 1, 2013 State Notification Regarding Exchanges While the ACA notes implementation won t begin until January 1, 2013, states must have their health insurance exchange blueprints submitted to the

January 1, 2013 State Notification Regarding Exchanges While the ACA notes implementation won t begin until January 1, 2013, states must have their health insurance exchange blueprints submitted to the

Health Care Reform Update 6/12/2014

Health Care Reform Update 6/12/2014 Disclaimer The information contained herein is for general information only. It is not intended as and does not constitute legal or tax advice. The information should

Health Care Reform Update 6/12/2014 Disclaimer The information contained herein is for general information only. It is not intended as and does not constitute legal or tax advice. The information should

American Health Care Act (House-Passed Bill)

") This chart compares the to provisions of both the House-passed and the Senate Discussion Draft, called the. This chart is current as of June 26, 2017. Individual shared responsibility penalty for not having

This chart compares the to provisions of both the House-passed and the Senate Discussion Draft, called the. This chart is current as of June 26, 2017. Individual shared responsibility penalty for not having

2014 AFFORDABLE CARE ACT (OBAMA CARE)

") 2014 AFFORDABLE CARE ACT (OBAMA CARE) Planning for 2014 Tax Return Filings O Beginning 2014, the ACA requires all persons be covered by health insurance O Individuals not covered by Medicare, their employers,

2014 AFFORDABLE CARE ACT (OBAMA CARE) Planning for 2014 Tax Return Filings O Beginning 2014, the ACA requires all persons be covered by health insurance O Individuals not covered by Medicare, their employers,

Reporting Requirements FAQs

Reporting Requirements - 6055 Frequently Asked Questions Reporting Requirements - 6055 FAQs Summary On March 10, 2014, the U.S. Department of the Treasury and IRS published final rules to implement the

Reporting Requirements - 6055 Frequently Asked Questions Reporting Requirements - 6055 FAQs Summary On March 10, 2014, the U.S. Department of the Treasury and IRS published final rules to implement the

THE AFFORDABLE CARE ACT...2

Table of Contents THE AFFORDABLE CARE ACT...2 Health Insurance Marketplace (Exchange)...3 Metallic Levels...4 Catastrophic Plans...4 Individual Mandate...5 Subsidies...5 Open Enrollment Period...6 Special

Table of Contents THE AFFORDABLE CARE ACT...2 Health Insurance Marketplace (Exchange)...3 Metallic Levels...4 Catastrophic Plans...4 Individual Mandate...5 Subsidies...5 Open Enrollment Period...6 Special

Effects of the Affordable Health Care Act

Effects of the Affordable Health Care Act A Focus on Financial, Administrative and Plan Impacts February 27, 2013 Presented By J.W. Terrill Consulting Services Agenda Introduction: Patient Protection &

Effects of the Affordable Health Care Act A Focus on Financial, Administrative and Plan Impacts February 27, 2013 Presented By J.W. Terrill Consulting Services Agenda Introduction: Patient Protection &

Executive Summary for Benefit Planning

Executive Summary for Benefit Planning Insuring People and Business Since 1868 3 Executive Summary for Benefit Planning 2010 Overview On March 23, 2010, President Obama signed into law the health care

Executive Summary for Benefit Planning Insuring People and Business Since 1868 3 Executive Summary for Benefit Planning 2010 Overview On March 23, 2010, President Obama signed into law the health care

Considering New Options: Navigating the 2014 Health Insurance Marketplace

Considering New Options: Navigating the 2014 Health Insurance Marketplace Indiana Benefits Conference November 19, 2013 Presented by: Katy Stowers, Advisor & General Counsel Agenda What does full implementation

Considering New Options: Navigating the 2014 Health Insurance Marketplace Indiana Benefits Conference November 19, 2013 Presented by: Katy Stowers, Advisor & General Counsel Agenda What does full implementation

Health Reform 101 What You Need to Know

Health Reform 101 What You Need to Know Neil Trautwein Vice President and Employee Benefits Policy Counsel National Retail Federation Health Reform is Here But Not the Reform We Asked For The debate did

Health Reform 101 What You Need to Know Neil Trautwein Vice President and Employee Benefits Policy Counsel National Retail Federation Health Reform is Here But Not the Reform We Asked For The debate did

Hardee s Q4 Franchise System Call. Health Care Reform Update November 5, 2013

Hardee s Q4 Franchise System Call Health Care Reform Update November 5, 2013 Key Elements of Health Care Reform for Employers Change in tax treatment for over-age 2010 dependent coverage Early retiree

Hardee s Q4 Franchise System Call Health Care Reform Update November 5, 2013 Key Elements of Health Care Reform for Employers Change in tax treatment for over-age 2010 dependent coverage Early retiree

6/20/13 Presented By: Mike Marchini, Beckie Lewis, & Liz Logsdon or

CBIZ PRESENTS Affordable Care Act: The Impact on Your Business & Your Employees 6/20/13 Presented By: Mike Marchini, Beckie Lewis, & Liz Logsdon 301-777-1500 or 800-624-0954 Determine Which PPACA Provisions

CBIZ PRESENTS Affordable Care Act: The Impact on Your Business & Your Employees 6/20/13 Presented By: Mike Marchini, Beckie Lewis, & Liz Logsdon 301-777-1500 or 800-624-0954 Determine Which PPACA Provisions

Health Care Reform for Dental Practices

2013 CliftonLarsonAllen LLP Health Care Reform for Dental Practices cliftonlarsonallen.com Nicole O. Fallon Health Care Consultant Manager Sept. 27, 2013 Circular 230 To ensure compliance imposed by IRS

2013 CliftonLarsonAllen LLP Health Care Reform for Dental Practices cliftonlarsonallen.com Nicole O. Fallon Health Care Consultant Manager Sept. 27, 2013 Circular 230 To ensure compliance imposed by IRS

Schools Insurance Group

Contra C t C Costa t C County t Schools Insurance Group p Presented by: Debra DeSpain Senior Account Manager February 8, 2013 Mandate Overview Individual Mandate Full-Time Employees Employer Shared Responsibility

Contra C t C Costa t C County t Schools Insurance Group p Presented by: Debra DeSpain Senior Account Manager February 8, 2013 Mandate Overview Individual Mandate Full-Time Employees Employer Shared Responsibility

PPACA Update: Financial Impact on Leavenworth USD 453

PPACA Update: Financial Impact on Leavenworth USD 453 Health Care Reform Overview What s Next For Employers? Move forward with planning for implementation of all provisions.. In Place Requirements Maintain

PPACA Update: Financial Impact on Leavenworth USD 453 Health Care Reform Overview What s Next For Employers? Move forward with planning for implementation of all provisions.. In Place Requirements Maintain

Health Care Reform Under the ACA Its Effect on Municipalities and Their Employees

Health Care Reform Under the ACA Its Effect on Municipalities and Their Employees Maine Municipal Employees Health Trust 1-800-852-8300 www.mmeht.org The Difference Is Trust August 2014 1 Today s Agenda

Health Care Reform Under the ACA Its Effect on Municipalities and Their Employees Maine Municipal Employees Health Trust 1-800-852-8300 www.mmeht.org The Difference Is Trust August 2014 1 Today s Agenda

9/18/13. The Affordable Care Act and Challenges for Colleges and Universities Legal Issues in Higher Education October 16, 2013.

The Affordable Care Act and Challenges for Colleges and Universities Legal Issues in Higher Education October 16, 2013 Overview The ACA: Here to Stay and Why It Matters 2014: The Known and the Unknown

The Affordable Care Act and Challenges for Colleges and Universities Legal Issues in Higher Education October 16, 2013 Overview The ACA: Here to Stay and Why It Matters 2014: The Known and the Unknown

Gary Bottoms, CLU, ChFC President. David Bottoms, CFP, RHU, REBC, CLU, ChFC Vice President

AN EMPLOYER S GUIDE TO HEALTH CARE REFORM Gary Bottoms, CLU, ChFC President David Bottoms, CFP, RHU, REBC, CLU, ChFC Vice President The Bottoms Group, LLC 180 Cherokee Street NE Marietta, Georgia 30060-1610

AN EMPLOYER S GUIDE TO HEALTH CARE REFORM Gary Bottoms, CLU, ChFC President David Bottoms, CFP, RHU, REBC, CLU, ChFC Vice President The Bottoms Group, LLC 180 Cherokee Street NE Marietta, Georgia 30060-1610

Health Care Reform Update

Health Care Reform Update Presented by David Hayes, FSA, MAAA Consulting Actuary Milliman - Atlanta November 16, 2012 Southeastern Actuaries Conference Fall 2012 Agenda This will be an general session

Health Care Reform Update Presented by David Hayes, FSA, MAAA Consulting Actuary Milliman - Atlanta November 16, 2012 Southeastern Actuaries Conference Fall 2012 Agenda This will be an general session

2013 Miller Johnson. All rights reserved.

Update: How To Prepare For 2014 Tripp W. Vander Wal 1 1 www.millerjohnson.com The materials and information have been prepared for informational purposes only. This is not legal advice, nor intended to

Update: How To Prepare For 2014 Tripp W. Vander Wal 1 1 www.millerjohnson.com The materials and information have been prepared for informational purposes only. This is not legal advice, nor intended to

The Affordable Care Act: Issues for Employers

The Affordable Care Act: Issues for Employers Paul W. Madden Whiteford, Taylor & Preston L.L.P. (401) 347-8742 Direct Fax: (410) 223-4162 pmadden@wtplaw.com Topics Covered Employer Shared Responsibility

The Affordable Care Act: Issues for Employers Paul W. Madden Whiteford, Taylor & Preston L.L.P. (401) 347-8742 Direct Fax: (410) 223-4162 pmadden@wtplaw.com Topics Covered Employer Shared Responsibility

Healthcare Reform. July 17, 2013

Healthcare Reform July 17, 2013 Agenda Current and Future Requirements for Employers Healthcare Reform Taxes and Fees Individual Mandate and Subsidies Employer Pay or Play Mandate Other Requirements Expanded

Healthcare Reform July 17, 2013 Agenda Current and Future Requirements for Employers Healthcare Reform Taxes and Fees Individual Mandate and Subsidies Employer Pay or Play Mandate Other Requirements Expanded

5GBenefits, LLC Your Health Care Reform Partner

5GBenefits, LLC Your Health Care Reform Partner Are you in compliance with health care reform regulations? We can help you stay on top of health care reform in order to avoid penalties from legislative

5GBenefits, LLC Your Health Care Reform Partner Are you in compliance with health care reform regulations? We can help you stay on top of health care reform in order to avoid penalties from legislative

Employer Mandate: Employer Action Overview

HEALTH CARE REFORM Employer Mandate: Page 2 of 11 Immediatemmediate Employer Action Required Notes Nursing Mothers Employers must provide a reasonable break time for non-exempt employees who are nursing

HEALTH CARE REFORM Employer Mandate: Page 2 of 11 Immediatemmediate Employer Action Required Notes Nursing Mothers Employers must provide a reasonable break time for non-exempt employees who are nursing

By Larry Grudzien Attorney at Law

By Larry Grudzien Attorney at Law 1 What is a small employer? Fees and Taxes 90 day Waiting Period Pre-existing condition Out-of Pocket Limits Wellness Programs Approved Clinical Trials Cafeteria Plans

By Larry Grudzien Attorney at Law 1 What is a small employer? Fees and Taxes 90 day Waiting Period Pre-existing condition Out-of Pocket Limits Wellness Programs Approved Clinical Trials Cafeteria Plans

PRIVATE HEALTH INSURANCE MARKET REFORMS. Presented to AICP, Western Chapter By Kenneth Schnoll May 6, 2010

PRIVATE HEALTH INSURANCE MARKET REFORMS Presented to AICP, Western Chapter By Kenneth Schnoll May 6, 2010 1 OVERVIEW On March 25, 2010 both chambers of Congress passed H.R. 4872, the Health Care Education

PRIVATE HEALTH INSURANCE MARKET REFORMS Presented to AICP, Western Chapter By Kenneth Schnoll May 6, 2010 1 OVERVIEW On March 25, 2010 both chambers of Congress passed H.R. 4872, the Health Care Education

Selected Tax Issues Under Patient Protection and Affordable Care Act (PPACA)

") Selected Tax Issues Under Patient Protection and Affordable Care Act (PPACA) J. Clark Pendergrass Lanier Ford Shaver & Payne P.C. 2101 West Clinton Ave., Suite 102 Huntsville, AL 35805 256-535-1100 jcp@lanierford.com

Selected Tax Issues Under Patient Protection and Affordable Care Act (PPACA) J. Clark Pendergrass Lanier Ford Shaver & Payne P.C. 2101 West Clinton Ave., Suite 102 Huntsville, AL 35805 256-535-1100 jcp@lanierford.com

EXPERT UPDATE. Compliance Headlines from Henderson Brothers:.

EXPERT UPDATE Compliance Headlines from Henderson Brothers:. Health Care Reform Timeline Health Care Reform Timeline This Henderson Brothers Summary provides a timeline of the of key reform provisions

EXPERT UPDATE Compliance Headlines from Henderson Brothers:. Health Care Reform Timeline Health Care Reform Timeline This Henderson Brothers Summary provides a timeline of the of key reform provisions

Health Care Reform: Fact vs. Fiction for Small Business. What employers should be thinking about now to prepare for 2015

Health Care Reform: Fact vs. Fiction for Small Business What employers should be thinking about now to prepare for 2015 Fact vs. Fiction Healthcare is less expensive overall: Fact or fiction? Employers

Health Care Reform: Fact vs. Fiction for Small Business What employers should be thinking about now to prepare for 2015 Fact vs. Fiction Healthcare is less expensive overall: Fact or fiction? Employers

Benefit Strategies and Compliance in a Health Reform Era

2013 CliftonLarsonAllen LLP Benefit Strategies and Compliance in a Health Reform Era CLAconnect.com Nicole Otto Fallon Director/Consultant Aging Services of MN Institute February 5, 2014 Agenda I. Recap

2013 CliftonLarsonAllen LLP Benefit Strategies and Compliance in a Health Reform Era CLAconnect.com Nicole Otto Fallon Director/Consultant Aging Services of MN Institute February 5, 2014 Agenda I. Recap

The ACA: Health Plans Overview

The ACA: Health Plans Overview Agenda What is the legal status of the ACA? Which plans must comply? Reforms currently in place 2013 compliance deadlines 2014 compliance deadlines 2015 compliance deadlines

The ACA: Health Plans Overview Agenda What is the legal status of the ACA? Which plans must comply? Reforms currently in place 2013 compliance deadlines 2014 compliance deadlines 2015 compliance deadlines

Health Care Reform Update

Updated March 9, 2011 Health Care Reform Update Health Care Reform Timeline for Employer-Sponsored Plans This timeline provides some of the key dates associated with the Patient Protection and Affordable

Updated March 9, 2011 Health Care Reform Update Health Care Reform Timeline for Employer-Sponsored Plans This timeline provides some of the key dates associated with the Patient Protection and Affordable

Overview of Health Care Reform

Overview of Health Care Reform Groom Law Group Dial-In January 13, 2010 Overview Landscape Today The Exchange, Multi-State Plans, & CO-OPs Insurance Market Reforms & "Essential" Benefits Employer & Individual

Overview of Health Care Reform Groom Law Group Dial-In January 13, 2010 Overview Landscape Today The Exchange, Multi-State Plans, & CO-OPs Insurance Market Reforms & "Essential" Benefits Employer & Individual

Affordable Care Act: Impact on the Indiana Market

1 Affordable Care Act: Impact on the Indiana Market Seema Verma President SVC, Inc 2 Affordable Care Act Key accomplishment is access ~48.6 million uninsured in America* ~800 thousand uninsured in Indiana*

1 Affordable Care Act: Impact on the Indiana Market Seema Verma President SVC, Inc 2 Affordable Care Act Key accomplishment is access ~48.6 million uninsured in America* ~800 thousand uninsured in Indiana*

HEALTH CARE REFORM: CONSIDERATIONS FOR THE BUSINESS MANAGER

HEALTH CARE REFORM: CONSIDERATIONS FOR THE BUSINESS MANAGER This is only a brief summary that reflects our current understanding of select provisions of the law, often in the absence of regulations. All

HEALTH CARE REFORM: CONSIDERATIONS FOR THE BUSINESS MANAGER This is only a brief summary that reflects our current understanding of select provisions of the law, often in the absence of regulations. All

TO UNDERSTANDING THE AFFORDABLE CARE ACT

3 STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT What s Inside Step 1: What Understand what you re buying 4 Step 2: How How can you buy health insurance? 20 STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT

3 STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT What s Inside Step 1: What Understand what you re buying 4 Step 2: How How can you buy health insurance? 20 STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT

Affordable Care Act. August 20 th, 2013 Stan W. Reynolds Vice President

Affordable Care Act August 20 th, 2013 Stan W. Reynolds Vice President Key Positions in the Affordable Care Act 1. Public Marketplace and available federal subsidies 2. Health insurance availability to

Affordable Care Act August 20 th, 2013 Stan W. Reynolds Vice President Key Positions in the Affordable Care Act 1. Public Marketplace and available federal subsidies 2. Health insurance availability to

Understanding the Value of Self-Insured Health Plans

Understanding the Value of Self-Insured Health Plans SIIA Taft-Hartley Plan Executive Forum April 30, 2015 Copyright 2014 by The Segal Group, Inc. All rights reserved. Discussion Overview The Intent and

Understanding the Value of Self-Insured Health Plans SIIA Taft-Hartley Plan Executive Forum April 30, 2015 Copyright 2014 by The Segal Group, Inc. All rights reserved. Discussion Overview The Intent and

Health Care Reform. Presented by CohnReznick s Government Contracting Industry Practice

Health Care Reform Presented by CohnReznick s Government Contracting Industry Practice Christine Williamson, Partner and Jody Buyalos, Partner, The Insurance Exchange PLEASE READ This presentation has

Health Care Reform Presented by CohnReznick s Government Contracting Industry Practice Christine Williamson, Partner and Jody Buyalos, Partner, The Insurance Exchange PLEASE READ This presentation has