Copyright 2015 The Ins4tutes

|

|

|

- Mitchell Griffin

- 6 years ago

- Views:

Transcription

1

2 ARM 56 Review CAD004 Speaker: Michael Elliott, CPCU, AIAF, The Institutes

3 Learning Objectives At the end of this session, you will: Dissect the most challenging ARM 56 course topics. Practice ARM 56 exam questions. Familiarize yourself with the ARM 56 exam format.

4 What to Expect on the Exam Educational Objectives Balanced Exam Pretest Items

5 Test-Taking Tips Get the easy ones Don t get bogged down early Use the mark for later review feature Eliminate the obviously wrong answers Use your scratch paper to keep track

6 Assignment 1 IntroducCon to Risk Financing

7

8

9 Risk Financing Goals Pay for negative consequences of an event Maintain liquidity Manage uncertainty Comply with legal and regulatory requirements Minimize the cost of risk

10 Cost of Risk Retained losses Risk transfer costs Loss control expenses Risk management administrative costs

11

12

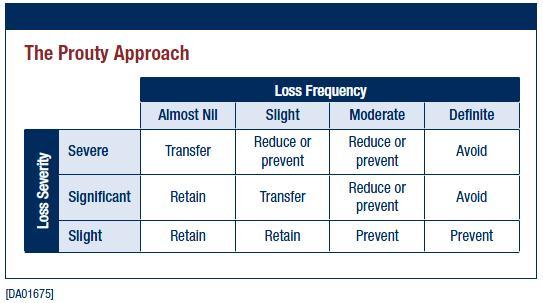

13 The Prouty Approach suggests that losses with low severity and low frequency should be A. Transferred B. Avoided C. Retained D. Prevented

14

15 Assignment 2 Estimating Hazard Risk

16 EsCmaCng Hazard Losses Collect and organize past data Limit individual losses Apply loss development and trend factors Forecast losses

17 One step in forecasting expected losses based on historical data is to limit individual losses. Which one of the following occurs as a result of limiting individual losses? A B C D There is a reduction in the size of the sample that can be used for forecasting. The variability of forecast losses increases. The forecaster is better able to match losses to the layer that is being forecast. The organization will be able to reduce or eliminate losses.

18

19

20

21 In developing its loss forecast, HCB Company's risk management professional prepares the following loss triangle: Months from Beginning of Accident Year Accident Year X2 $105,231 $157,003 $176,771 $188,676 $194,678 20X3 $101,137 $165,780 $189,083 $199,440 20X4 $115,781 $178,912 $192,801 20X5 $120,980 $167,413 20X6 $118,605 What is the 30- to 42-month period-to-period loss development factor for HCB Company for year 20X4? A: 1.08 B: 1.15 C: 1.43 D: 1.67

22

23

24 Applying Increased Limits Factors

25 Assume total losses, limited to $100,000 per loss, equal $3,000,000. Based on the factors in the table above, estimated losses limited to $500,000 per loss equal A. $1,364,000 B. $2,114,000 C. $4,258,000 D. $4,650,000

26 Probability Interval (of a Total Loss Probability Distribution) Representation that shows the probability of outcomes falling within certain ranges of a probability distribution. The probability interval is determined by the areas underneath a probability distribution curve. 26

27 VariaCon from Expected Losses 27

28 Assignment 3 Transferring Hazard Risk Through Insurance

29 Ideally Insurable Loss Exposure Pure risk Accidental loss Definite in time and measurable Large number of similar, independent exposures Not simultaneous and not catastrophic Economically feasible to insure

30 Excess Liability Insurance Excess liability insurance is insurance coverage for losses that exceed the limits of underlying insurance or a retention amount. It is not an umbrella and most often takes one of three basic forms, which are: Following form Self-contained form Combination form 30

31 One form of excess liability insurance incorporates provisions of the underlying policy and then modifies the provisions with additional conditions or exclusions. This type of coverage is called A: A self-contained excess liability policy. B: An umbrella excess liability policy. C: A following-form excess liability policy. D: A combination excess liability policy.

32 Assignment 5 Retrospective Rating Plans

33 Retrospective Rating Plan Premium (Basic Premium + Converted Losses + Excess Loss Premium) x Tax Multiplier Subject to maximum and minimum premium amounts 33

34 1. Basic Premium covers the insurer acquisition costs, overhead, and profit. Basic premium is expressed as a percentage of the standard premium. Standard premium is calculated by using state rating classifications and rates, applying them to an insured s estimated exposures (for example, sales for a CGL policy or payroll for workers compensation policy) for the policy period. 34

35 2. Converted Losses incurred losses multiplied by a loss conversion factor, which is a factor used to account for the unallocated portion of loss adjustment expenses (which includes, for example, rent for the office space of the claims department that cannot be allocated to a specific claim.) 3. Excess Loss Premium compensates the insurer for the risk that an individual loss will exceed the loss limit, which is the limit or cap on a single loss that the insurer will apply to the loss when calculating the retrospective premium (that way an insured is not subject to the maximum premium just because of a single bad claim when otherwise the loss experience during the coverage period was good). Excess loss premium is expressed as a percentage of the standard premium and is multiplied by the loss conversion factor. 35

36 4. Tax Multiplier adds an amount for state premium taxes, license fees, service bureau charges, and residual market loadings. It is expressed as a factor that is multiplied by the other components of the retrospective formula. 5. Maximum Premium amount that the retrospective rating plan premium will not exceed. Maximum premium is expressed as a percentage of the standard premium. 6. Minimum Premium amount that the retrospective rating plan premium will not fall below. Minimum premium is expressed as a percentage of the standard premium. 36

37 Example of a RetrospecCve RaCng Plan Premium CalculaCon Assume that Cranston Manufacturing Company (Cranston) has the following cost factors for its incurred loss retrospeccve racng plan: Policy Limit $1,000,000 per occurrence Standard Premium $700,000 Basic Premium 20% Loss Conversion Factor 1.10 Loss Limit $500,000 per occurrence Excess Loss Premium 5% Tax MulCplier 1.04 Maximum Premium 150% Minimum Premium 40% Group 1 - $300,000 incurred losses Group 3 - $700,000 incurred losses Group 2 - $400,000 incurred losses Group 4 - $800,000 incurred losses 37

38 Analysis: The basic premium is 20% of the $700,000 standard premium, which is $140,000. The excess loss premium is 5% of the $700,000 standard premium, which is $35,000, mulcplied by the loss conversion factor of 1.10, for a total of $38,500. The maximum premium is 150% of the $700,000 standard premium, which is $1,050,000, and the minimum premium is 40% of the $700,000 standard premium, which is $280,000. We now have all we need to determine the retrospeccve racng plan premium as a funccon of incurred loss by applying the retrospeccve racng formula. [$140,000 + (Level of Incurred Losses x 1.10) + ($35,000 X 1.10)] x

39 Incurred Losses Premium $ 50,000 $ 280,000 minimum premium applies 100, , , , , , , , , , , , , , ,000 1,050,000 maximum premium applies 39

40 Comparison of Incurred Loss with Paid Loss RetrospecCve RaCng Plans Incurred loss retrospeccve racng plan Insured organizacon pays premium based on incurred losses. Benefit from taking a larger tax deduccon on premium based on incurred rather than paid losses. Paid loss retrospeccve racng plan Insured organizacon pays basic premium, excess loss premium, and contributes to an escrow fund for paid losses. Cash flow benefit from paying premium as losses are paid rather than incurred. Basic premium increased to compensate insurer for loss of cash flow. 40

41 Assignment 6 Reinsurance

42 Reinsurance FuncCons Increase large line capacity Provide catastrophe proteccon Stabilize loss experience Provide surplus relief Facilitate withdrawal from a market segment Provide underwricng guidance 42

43 Surplus Relief Premium revenue earned over time Acquisition expenses charged immediately For a growing insurance company, mismatch creates a drain on policyholders surplus Assets Liabili4es Surplus + premium revenue - acquisi4on expenses (not matched with revenue) 43

44 Facilitate Withdrawal From a Market Segment When withdrawing from a market segment the primary insurer has several options, which include: Stop selling new policies Cancel all policies Purchase porsolio reinsurance 44

45 Portfolio reinsurance is a reinsurance agreement that reinsures the loss exposures of an entire type of insurance, class of business, or geographic area. Important points to remember: 1. It is an excep4on to the rule that reinsurers do not accept all the liability for specified loss exposures of a primary insurer. 2. While reinsured, the primary insurer retains direct obliga4ons to insureds (not a nova4on). 3. OYen requires approval from the state insurance department. 45

46 Types of Reinsurance Faculta4ve Treaty Pro rata Excess of loss

47 Quota Share (pro rata)

48 Surplus Share (pro rata)

49 XYZ Insurance Company has a 9-line surplus share treaty with a retention $100,000 and a maximum cession of $900,000. Policy A insures a building for $500,000. If there is a $50,000 loss under Policy A, how much of it will XYZ retain? A: $0 B: $5,000 C: $10,000 D: $50,000

50 Excess of Loss Reinsurance

51 Assignment 7 Captive Insurance

52 52

53 Types of Cap4ves Single- parent (pure) Group Associa4on cap4ve Risk reten4on group Rent- a- CapCve Segregated Cell Cap4ve

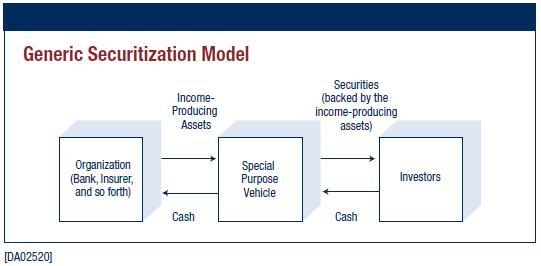

54 Advantages of a Captive 1. Reducing the cost of risk 2. Benefiting from cash flow 3. Obtaining insurance not otherwise available 4. Direct access to reinsurers 5. Negotiating with insurers 6. Centralizing loss retention 7. Tax advantages 8. Controlling losses 9. Obtaining rate equity 54

55 Disadvantages of a Captive 1. Capital and start-up costs 2. Sensitivity to losses 3. Pressure from parent 4. Premium taxes and residual market loadings 55

56 For which one of the following types of captives must the owners be from the same industry? A. Group captive B. Protected cell captive C. Rent-a-captive D. Risk Retention Group

57 Assignment 9 Transferring Financial Risk

58 Types of Financial Risk Market Risk Interest rate risk Exchange rate risk Liquidity risk Credit Risk Price Risk

59 DerivaCves Forward contracts Options Swaps

60 Which one of the following gives the holder the right to buy or sell an asset for a specific price? A. Forward B. Option C. Security D. Swap

61 SecuriCzaCon

62 With a securitization, income-producing assets, such as mortgage receivables, are transferred to a special purpose vehicle (SPV) in exchange for cash. These assets are A. Converted into forward contracts. B. Sold to investors. C. Traded on an open exchange. D. Used to collateralize securities sold to investors.

63 Assignment 10 Transferring Hazard Risk to the Financial Markets

64 64

65 With an insurance securitization, the special purpose vehicle (SPV) is often called a transformer because it tranforms A. A loss index into indemnity. B. Cash into securities. C. Insurable risk into investment risk. D. Primary insurance into reinsurance.

66 Contingent Capital Standby credit is an arrangement whereby a bank or another financial institution agrees to provide a loan to an organization in the event the organization suffers a loss. Contingent surplus notes are surplus notes that have been designed so that an insurer, at its option, can immediately obtain funds by issuing surplus notes at a pre-arranged rate of interest. Catastrophe equity puts are rights to sell equity (stock) at a predetermine price in the event of a catastrophic loss. 66

67 Assignment 11 Allocating Costs of Managing Hazard Risk

68 Allocating risk management costs Costs of accidental losses not reimbursed by insurance or other outside sources 2. Insurance premiums 3. Costs of risk control techniques 4. Costs of administering risk management activities 68

69 1. Incurred loss basis keep track of incurred losses, just as an insurance company would; including IBNR 2. Claims-made basis keep track of losses for claims made, just as an insurance company would; does not include IBNR 3. Claims-paid basis keep track of amounts paid on losses during the accounting period, regardless of when the losses occurred 69

70 Prospective cost allocation cost fixed at beginning of accounting period Retrospective cost allocation cost estimated at beginning of accounting period an adjusted as loss costs are known 70

71

72

73

74 Q & A 74

75 EO 6.04 Describe the administration of retrospective rating plans. Collateral requirements for paid loss retrospective rating plans For financial accounting purposes an organization must recognize its retained losses as they are incurred. The additional premium owed (as determined by the retrospective rating formula) must be recognized as a liability on the organization s next balance sheet and as an expense on the organization s next income statement. With a paid loss retrospective rating plan, premium payments are based on when losses are paid, not when they are incurred. But for financial accounting purposes, an organization must recognize additional premium owed when the losses are incurred, not when they are paid. Incurred but not reported (IBNR) losses must also be recognized if they can be estimated with reasonable accuracy. 75

76 EO 9.02 Explain how finite risk insurance plans operate, including: Types of risks covered Experience fund terms and calculation guidelines Variations in the terms of plans Common Characteristics of Finite Risk Plans The limits of coverage apply on an aggregate basis. The term of coverage is usually for five to ten years. The premium is usually 50% or more of the policy limits. The insurer shares profit with the insured, including investment income. The insured is allowed to commute the policy. 76

77 Types of Risk Covered 1. Underwri4ng risk is the risk that an insurer s losses and expenses will be greater than the premiums and the investment income it expects to earn under the insurance contract. 2. Investment risk is the risk that an insurer s investment income will be lower than it expects and includes 4ming risk and interest rate risk. Timing risk is the risk, under an insurance contract, that the insured s losses will be paid faster or more slowly than expected. Interest rate risk is the risk that interest rates will be below the expected rate during the term of the insurance contract. 3. Credit risk is the risk that an insurer will not collect the premiums owed by its insured. 77

78 Prospective versus Retroactive Plans Prospective plan is a risk financing plan arranged to cover losses from events that have not yet occurred Retroactive plan is a risk financing plan arranged to cover losses from events that have already occurred 78

79 Loss Portfolio Transfers Loss portfolio transfer is a type of retroactive plan that applies to an entire portfolio of losses. The losses usually have established reserves, but uncertainty exists as to the timing of the loss payments and the potential for further loss development. 79

80 EO Analyze the concerns of organizations transferring risk and investors supplying capital. Important DefiniCons Financial security of the par4es supplying the risk capital (the credit risk). Basis risk: the risk that the amount an organiza4on receives to offset its losses might be greater than or less than its actual losses. 80

81 EO Describe the practical considerations of selecting a cost allocation basis. An organiza4on s accoun4ng system can influence alloca4on. An organiza4on s opera4ons may be subject to more than one tax system. Each department should be charged at least a minimum amount for risk management services regardless of exposure or loss experience. If an organiza4on is highly decentralized, each department may be purchasing its own insurance. Cost alloca4on should penalize or reward each department according to its risk management costs. Use of computerized risk management informa4on systems (RMIS) has become standard in many industries. Cost alloca4on systems should remain as consistent as possible from year to year. 81

Supplemental Background Material. Course CFE 3. Reinsurance. (Passing grade for this exam is 74%)

") Supplemental Background Material Course (Passing grade for this exam is 74%) Please note that this study guide is a tool for learning the materials you need to effectively study for this examination. As

Supplemental Background Material Course (Passing grade for this exam is 74%) Please note that this study guide is a tool for learning the materials you need to effectively study for this examination. As

Reinsurance 101: an Overview Session 107

Reinsurance 101: an Overview Session 107 Monday, June 9, 2014 1:30pm 3:00pm IASA 86 TH ANNUAL EDUCATIONAL CONFERENCE & BUSINESS SHOW Introductions Tim Corley Tim is a Senior Solutions Executive for Inpoint

Reinsurance 101: an Overview Session 107 Monday, June 9, 2014 1:30pm 3:00pm IASA 86 TH ANNUAL EDUCATIONAL CONFERENCE & BUSINESS SHOW Introductions Tim Corley Tim is a Senior Solutions Executive for Inpoint

The Reinsurance Placement Cycle

The Reinsurance Placement Cycle Session 507 Tuesday, June 9, 2015 1:30pm Overview Interactive session among four parties: Insurance Company Reinsurance Company Reinsurance Broker Audience Panel Members

The Reinsurance Placement Cycle Session 507 Tuesday, June 9, 2015 1:30pm Overview Interactive session among four parties: Insurance Company Reinsurance Company Reinsurance Broker Audience Panel Members

Strategies for Controlling your Cost of Risk

Strategies for Controlling your Cost of Risk 1 controlling cost of risk is a learning process 2 which direction will you go to control your cost of risk 3 understanding your industry is crucial to creating

Strategies for Controlling your Cost of Risk 1 controlling cost of risk is a learning process 2 which direction will you go to control your cost of risk 3 understanding your industry is crucial to creating

Reinsurance (Passing grade for this exam is 74)

") Supplemental Background Material NAIC Examiner Project Course CFE 3 (Passing grade for this exam is 74) Please note that this study guide is a tool for learning the materials you need to effectively study

Supplemental Background Material NAIC Examiner Project Course CFE 3 (Passing grade for this exam is 74) Please note that this study guide is a tool for learning the materials you need to effectively study

SOCIETY OF ACTUARIES Introduction to Ratemaking & Reserving Exam GIIRR MORNING SESSION. Date: Wednesday, April 29, 2015 Time: 8:30 a.m. 11:45 a.m.

SOCIETY OF ACTUARIES Exam GIIRR MORNING SESSION Date: Wednesday, April 29, 2015 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 100 points.

SOCIETY OF ACTUARIES Exam GIIRR MORNING SESSION Date: Wednesday, April 29, 2015 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 100 points.

The old Exam 6 Second Edition G. Stolyarov II,

The Actuary s Free Study GUIDE for The old Exam 6 Second Edition G. Stolyarov II, ASA, ACAS, MAAA, CPCU, ARe, ARC, API, AIS, AIE, AIAF First Edition Published in July-October 2010 Second Edition Published

The Actuary s Free Study GUIDE for The old Exam 6 Second Edition G. Stolyarov II, ASA, ACAS, MAAA, CPCU, ARe, ARC, API, AIS, AIE, AIAF First Edition Published in July-October 2010 Second Edition Published

Cell Company Overview and Innovative Applications

Cell Company Overview and Innovative Applications 2018 World Captive Forum January 31 February 2, 2018 Fort Lauderdale, FL #WorldCaptiveForum Presenters: Les Boughner Chairman Advantage Insurance Management

Cell Company Overview and Innovative Applications 2018 World Captive Forum January 31 February 2, 2018 Fort Lauderdale, FL #WorldCaptiveForum Presenters: Les Boughner Chairman Advantage Insurance Management

The Reinsurance Placement Cycle

Session 507 Tuesday, June 10, 2014 1:45pm 3:15pm IASA 86 TH ANNUAL EDUCATIONAL CONFERENCE & BUSINESS SHOW Overview This will be an interactive session describing the placement of a reinsurance program

Session 507 Tuesday, June 10, 2014 1:45pm 3:15pm IASA 86 TH ANNUAL EDUCATIONAL CONFERENCE & BUSINESS SHOW Overview This will be an interactive session describing the placement of a reinsurance program

P&C Reinsurance Pricing 101 Ohio Chapter IASA. Prepared by Aon Benfield Inpoint Operations

P&C Reinsurance Pricing 101 Ohio Chapter IASA Prepared by Aon Benfield Inpoint Operations Agenda Focus on Treaty, P&C Reinsurance Certain concepts apply to Facultative and/or LYH Reinsurance Pro-Rata Reinsurance

P&C Reinsurance Pricing 101 Ohio Chapter IASA Prepared by Aon Benfield Inpoint Operations Agenda Focus on Treaty, P&C Reinsurance Certain concepts apply to Facultative and/or LYH Reinsurance Pro-Rata Reinsurance

Risk Management in Insurance

University of Cologne Department of Risk Management and Insurance Risk Management in Insurance Value and risk based management with special consideration of Solvency II Salzburg University April / Thursday

University of Cologne Department of Risk Management and Insurance Risk Management in Insurance Value and risk based management with special consideration of Solvency II Salzburg University April / Thursday

CVS CAREMARK INDEMNITY LTD. NOTES TO THE FINANCIAL STATEMENTS DECEMBER 31, 2017 AND 2016 (expressed in United States dollars) 1. Operations CVS Carema

1. Operations CVS Carema") NOTES TO THE FINANCIAL STATEMENTS 1. Operations CVS Caremark Indemnity Ltd. ("The Company"), formerly known as Twinsurance Limited, was incorporated in Bermuda on March 27, 1980, and is a wholly owned

NOTES TO THE FINANCIAL STATEMENTS 1. Operations CVS Caremark Indemnity Ltd. ("The Company"), formerly known as Twinsurance Limited, was incorporated in Bermuda on March 27, 1980, and is a wholly owned

SYLLABUS OF BASIC EDUCATION 2018 Basic Techniques for Ratemaking and Estimating Claim Liabilities Exam 5

The syllabus for this four-hour exam is defined in the form of learning objectives, knowledge statements, and readings. Exam 5 is administered as a technology-based examination. set forth, usually in broad

The syllabus for this four-hour exam is defined in the form of learning objectives, knowledge statements, and readings. Exam 5 is administered as a technology-based examination. set forth, usually in broad

Foundations of Reinsurance

Foundations of Reinsurance Monday, September 23, 2013, 1:30 p.m. Marsha A. Cohen Senior Vice President & Director of Education Reinsurance Association of America Washington, D.C. Marsha A. Cohen is senior

Foundations of Reinsurance Monday, September 23, 2013, 1:30 p.m. Marsha A. Cohen Senior Vice President & Director of Education Reinsurance Association of America Washington, D.C. Marsha A. Cohen is senior

Lesson 6 Risk Financing

Lesson 6 Risk Financing Lesson 6 Intro p1 (ELR) An organization s risks have been identified and analyzed. For those risks that cannot be avoided, risk control techniques have been implemented to either

Lesson 6 Risk Financing Lesson 6 Intro p1 (ELR) An organization s risks have been identified and analyzed. For those risks that cannot be avoided, risk control techniques have been implemented to either

Finance 160:163 Insurance Operations Fall 2009 Dr. A. Frank Thompson Exam 1

Finance 160:163 Insurance Operations Fall 2009 Dr. A. Frank Thompson Exam 1 Directions: Please answer the following 25 multiple choice questions and 2 short essay questions designed to test your knowledge

Finance 160:163 Insurance Operations Fall 2009 Dr. A. Frank Thompson Exam 1 Directions: Please answer the following 25 multiple choice questions and 2 short essay questions designed to test your knowledge

GI IRR Model Solutions Spring 2015

GI IRR Model Solutions Spring 2015 1. Learning Objectives: 1. The candidate will understand the key considerations for general insurance actuarial analysis. Learning Outcomes: (1l) Adjust historical earned

GI IRR Model Solutions Spring 2015 1. Learning Objectives: 1. The candidate will understand the key considerations for general insurance actuarial analysis. Learning Outcomes: (1l) Adjust historical earned

DRAFT 2011 Exam 5 Basic Ratemaking and Reserving

2011 Exam 5 Basic Ratemaking and Reserving The CAS is providing this advanced copy of the draft syllabus for this exam so that candidates and educators will have a sense of the learning objectives and

2011 Exam 5 Basic Ratemaking and Reserving The CAS is providing this advanced copy of the draft syllabus for this exam so that candidates and educators will have a sense of the learning objectives and

Reinsurance Contracts: Clause and Effect

Reinsurance Contracts: Clause and Effect Session #607 Panel Members Pat Larsen, CPCU, ARe Vice President, Ceded Reinsurance/Account Executive American Agricultural Insurance Company Paul Poston, CPCU,

Reinsurance Contracts: Clause and Effect Session #607 Panel Members Pat Larsen, CPCU, ARe Vice President, Ceded Reinsurance/Account Executive American Agricultural Insurance Company Paul Poston, CPCU,

Topics in Risk Management. Agenda 27/05/56. Sarayut Nathaphan

Topics in Risk Management Sarayut Nathaphan 1 Agenda The Changing Scope of Risk Management Enterprise Risk Management Insurance Market Dynamics Loss Forecasting Financial Analysis in Risk Management Decision

Topics in Risk Management Sarayut Nathaphan 1 Agenda The Changing Scope of Risk Management Enterprise Risk Management Insurance Market Dynamics Loss Forecasting Financial Analysis in Risk Management Decision

GIIRR Model Solutions Fall 2015

GIIRR Model Solutions Fall 2015 1. Learning Objectives: 1. The candidate will understand the key considerations for general insurance actuarial analysis. Learning Outcomes: (1k) Estimate written, earned

GIIRR Model Solutions Fall 2015 1. Learning Objectives: 1. The candidate will understand the key considerations for general insurance actuarial analysis. Learning Outcomes: (1k) Estimate written, earned

Energy Insurance Mutual Limited. Audited Financial Statements. Years ended December 31, 2017 and 2016 with Report of Independent Auditors

Audited Financial Statements Years ended December 31, 2017 and 2016 with Report of Independent Auditors Audited Financial Statements Years ended December 31, 2017 and 2016 Contents Report of Independent

Audited Financial Statements Years ended December 31, 2017 and 2016 with Report of Independent Auditors Audited Financial Statements Years ended December 31, 2017 and 2016 Contents Report of Independent

Metropolitan Direct Property and Casualty Insurance Company ASSETS

ASSETS Current Year Prior Year 1 2 3 4 Net Admitted Nonadmitted Assets Net Assets Assets (Cols. 1-2) Admitted Assets 1. Bonds (Schedule D)......29,421,421...0...29,421,421...28,718,306 2. Stocks (Schedule

ASSETS Current Year Prior Year 1 2 3 4 Net Admitted Nonadmitted Assets Net Assets Assets (Cols. 1-2) Admitted Assets 1. Bonds (Schedule D)......29,421,421...0...29,421,421...28,718,306 2. Stocks (Schedule

California Joint Powers Insurance Authority

An Actuarial Analysis of the Self-Insurance Program as of June 30, 2018 October 26, 2018 Michael L. DeMattei, FCAS, MAAA Jonathan B. Winn, FCAS, MAAA Table of Contents INTRODUCTION... 1 Purpose of Report...

An Actuarial Analysis of the Self-Insurance Program as of June 30, 2018 October 26, 2018 Michael L. DeMattei, FCAS, MAAA Jonathan B. Winn, FCAS, MAAA Table of Contents INTRODUCTION... 1 Purpose of Report...

American International Reinsurance Company, Ltd. and Subsidiary Audited GAAP Consolidated Financial Statements. December 31, 2017 and 2016

American International Reinsurance Company, Ltd. and Subsidiary Audited GAAP Consolidated Financial Statements December 31, 2017 and 2016 Table of Contents FINANCIAL STATEMENTS Page Independent Auditor

American International Reinsurance Company, Ltd. and Subsidiary Audited GAAP Consolidated Financial Statements December 31, 2017 and 2016 Table of Contents FINANCIAL STATEMENTS Page Independent Auditor

2015 Statutory Combined Annual Statement Schedule P Disclosure

2015 Statutory Combined Annual Statement Schedule P Disclosure This disclosure provides supplemental facts and methodologies intended to enhance understanding of Schedule P reserve data. It provides additional

2015 Statutory Combined Annual Statement Schedule P Disclosure This disclosure provides supplemental facts and methodologies intended to enhance understanding of Schedule P reserve data. It provides additional

Pennsylvania Professional Liability Joint Underwriting Association

MAZARS USA LLP Pennsylvania Professional Liability Joint Underwriting Association Statutory Financial Statements and Supplementary Information December 31, 2017 and 2016 MAZARS USA LLP IS AN INDEPENDENT

MAZARS USA LLP Pennsylvania Professional Liability Joint Underwriting Association Statutory Financial Statements and Supplementary Information December 31, 2017 and 2016 MAZARS USA LLP IS AN INDEPENDENT

Years ended December 31, 2017 and 2016 with Report of Independent Auditors

Audited Financial Statements Years ended December 31, 2017 and 2016 with Report of Independent Auditors Audited Financial Statements Years ended December 31, 2017 and 2016 Contents Report of Independent

Audited Financial Statements Years ended December 31, 2017 and 2016 with Report of Independent Auditors Audited Financial Statements Years ended December 31, 2017 and 2016 Contents Report of Independent

Metropolitan Group Property and Casualty Insurance Company ASSETS

ASSETS Current Year Prior Year 1 2 3 4 Net Admitted Nonadmitted Assets Net Assets Assets (Cols. 1-2) Admitted Assets 1. Bonds (Schedule D)......351,261,854...0...351,261,854...369,773,387 2. Stocks (Schedule

ASSETS Current Year Prior Year 1 2 3 4 Net Admitted Nonadmitted Assets Net Assets Assets (Cols. 1-2) Admitted Assets 1. Bonds (Schedule D)......351,261,854...0...351,261,854...369,773,387 2. Stocks (Schedule

SCHEDULE P: MEMORIZE ME!!!

SCHEDULE P: MEMORIZE ME!!! NOTE: This skips all the prior years row calculation stuff, since it is covered pretty well by TIA (and I m sure any other manual). What are the cross-checks performed by the

SCHEDULE P: MEMORIZE ME!!! NOTE: This skips all the prior years row calculation stuff, since it is covered pretty well by TIA (and I m sure any other manual). What are the cross-checks performed by the

Tuesday, March 17, 2015 Houston, TX. 3:45 5:00 p.m. CAPTIVATING RISK: ART MARKET AND CAPTIVE SOLUTIONS

Tuesday, March 17, 2015 Houston, TX 3:45 5:00 p.m. : ART MARKET AND CAPTIVE SOLUTIONS Presented by Michael O Neill, CPCU, ARM President and CEO American Contractors Insurance Group Many companies look

Tuesday, March 17, 2015 Houston, TX 3:45 5:00 p.m. : ART MARKET AND CAPTIVE SOLUTIONS Presented by Michael O Neill, CPCU, ARM President and CEO American Contractors Insurance Group Many companies look

COURSE 5 MORNING SESSION APPLICATION OF BASIC ACTUARIAL PRINCIPLES SECTION A-WRITTEN ANSWER

COURSE 5 MORNING SESSION APPLICATION OF BASIC ACTUARIAL PRINCIPLES SECTION A-WRITTEN ANSWER **BEGINNING OF EXAMINATION** COURSE 5 MORNING SESSION 1. (4 points) Describe the reasons an individual or a business

COURSE 5 MORNING SESSION APPLICATION OF BASIC ACTUARIAL PRINCIPLES SECTION A-WRITTEN ANSWER **BEGINNING OF EXAMINATION** COURSE 5 MORNING SESSION 1. (4 points) Describe the reasons an individual or a business

Daniel Keough & Martin Brauch, CFA Innovative Captive Strategies, Inc. (ICS)

") Daniel Keough & Martin Brauch, CFA Innovative Captive Strategies, Inc. (ICS) Alternative Insurance Markets: Assessing New Risk Management Tools Agenda 1. Introduction to Innovative Captive Strategies (ICS)

Daniel Keough & Martin Brauch, CFA Innovative Captive Strategies, Inc. (ICS) Alternative Insurance Markets: Assessing New Risk Management Tools Agenda 1. Introduction to Innovative Captive Strategies (ICS)

SOCIETY OF ACTUARIES Advanced Topics in General Insurance. Exam GIADV. Date: Friday, April 27, 2018 Time: 2:00 p.m. 4:15 p.m.

SOCIETY OF ACTUARIES Exam GIADV Date: Friday, April 27, 2018 Time: 2:00 p.m. 4:15 p.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 40 points. This exam consists of

SOCIETY OF ACTUARIES Exam GIADV Date: Friday, April 27, 2018 Time: 2:00 p.m. 4:15 p.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 40 points. This exam consists of

Reinsurance Structures and Pricing Pro-Rata Treaties. Care Reinsurance Boot Camp Josh Fishman, FCAS, MAAA August 12, 2013

Reinsurance Structures and Pricing Pro-Rata Treaties Care Reinsurance Boot Camp Josh Fishman, FCAS, MAAA August 12, 2013 Motivations for Purchasing Reinsurance 1) Limiting Liability [on specific risks]

Reinsurance Structures and Pricing Pro-Rata Treaties Care Reinsurance Boot Camp Josh Fishman, FCAS, MAAA August 12, 2013 Motivations for Purchasing Reinsurance 1) Limiting Liability [on specific risks]

The Feasibility Process

The Feasibility Process Moderator: Derek Freihaut Principal and Consulting Actuary; Pinnacle Actuarial Resources Panelists: Patrick Theriault Managing Director; Michael Meehan Consultant; Milliman Strategic

The Feasibility Process Moderator: Derek Freihaut Principal and Consulting Actuary; Pinnacle Actuarial Resources Panelists: Patrick Theriault Managing Director; Michael Meehan Consultant; Milliman Strategic

Exam ERM-GC. Date: Tuesday, October 30, 2018 Time: 8:30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES. Recognized by the Canadian Institute of Actuaries.

Enterprise Risk Management General Corporate ERM Extension Exam ERM-GC Date: Tuesday, October 30, 2018 Time: 8:30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has

Enterprise Risk Management General Corporate ERM Extension Exam ERM-GC Date: Tuesday, October 30, 2018 Time: 8:30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has

The objectives of the chapter are to provide an understanding of:

Insurance Companies The objectives of the chapter are to provide an understanding of: o o o o o o Why individuals buy insurance. The regulatory issues affecting insurance and the accounting system insurance

Insurance Companies The objectives of the chapter are to provide an understanding of: o o o o o o Why individuals buy insurance. The regulatory issues affecting insurance and the accounting system insurance

DELAWARE COMPENSATION RATING BUREAU, INC.

Exhibit 28 Amended DELAWARE COMPENSATION RATING BUREAU, INC. DECEMBER 1, 201 RESIDUAL MARKET RATE AND VOLUNTARY MARKET LOSS COST FILING INDEX TO CLASSIFICATION EXHIBITS 1 Composite Pure Premium Multipliers

Exhibit 28 Amended DELAWARE COMPENSATION RATING BUREAU, INC. DECEMBER 1, 201 RESIDUAL MARKET RATE AND VOLUNTARY MARKET LOSS COST FILING INDEX TO CLASSIFICATION EXHIBITS 1 Composite Pure Premium Multipliers

OHIO PLAN RISK MANAGEMENT, INC. Columbus, Ohio. FINANCIAL STATEMENTS December 31, 2015 and 2014

OHIO PLAN RISK MANAGEMENT, INC. Columbus, Ohio FINANCIAL STATEMENTS Columbus, Ohio FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR S REPORT... 1 MANAGEMENT S DISCUSSION AND ANALYSIS (UNAUDITED)... 3

OHIO PLAN RISK MANAGEMENT, INC. Columbus, Ohio FINANCIAL STATEMENTS Columbus, Ohio FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR S REPORT... 1 MANAGEMENT S DISCUSSION AND ANALYSIS (UNAUDITED)... 3

SOCIETY OF ACTUARIES Introduction to Ratemaking & Reserving Exam GIIRR MORNING SESSION. Date: Wednesday, April 25, 2018 Time: 8:30 a.m. 11:45 a.m.

SOCIETY OF ACTUARIES Exam GIIRR MORNING SESSION Date: Wednesday, April 25, 2018 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 100 points.

SOCIETY OF ACTUARIES Exam GIIRR MORNING SESSION Date: Wednesday, April 25, 2018 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 100 points.

SOCIETY OF ACTUARIES Introduction to Ratemaking & Reserving Exam GIIRR MORNING SESSION. Date: Wednesday, April 30, 2014 Time: 8:30 a.m. 11:45 a.m.

SOCIETY OF ACTUARIES Exam GIIRR MORNING SESSION Date: Wednesday, April 30, 2014 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 100 points.

SOCIETY OF ACTUARIES Exam GIIRR MORNING SESSION Date: Wednesday, April 30, 2014 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 100 points.

SOCIETY OF ACTUARIES Financial and Regulatory Environment U.S. Exam GIFREU AFTERNOON SESSION. Date: Thursday, April 30, 2015 Time: 1:30 p.m. 3:45 p.m.

SOCIETY OF ACTUARIES Financial and Regulatory Environment U.S. Exam GIFREU AFTERNOON SESSION Date: Thursday, April 30, 2015 Time: 1:30 p.m. 3:45 p.m. INSTRUCTIONS TO CANDIDATES General Instructions 1.

SOCIETY OF ACTUARIES Financial and Regulatory Environment U.S. Exam GIFREU AFTERNOON SESSION Date: Thursday, April 30, 2015 Time: 1:30 p.m. 3:45 p.m. INSTRUCTIONS TO CANDIDATES General Instructions 1.

IASB /FASB Meeting 10 February A. Reinsurance. Purpose of this paper

IASB /FASB Meeting 10 February 2010 IASB agenda reference FASB memo reference 1A 38A Project Topic Insurance Contracts Reinsurance Purpose of this paper 1. An insurance contract involves purchase by a

IASB /FASB Meeting 10 February 2010 IASB agenda reference FASB memo reference 1A 38A Project Topic Insurance Contracts Reinsurance Purpose of this paper 1. An insurance contract involves purchase by a

MANILA BANKERS LIFE INSURANCE CORPORATION. NOTES TO FINANCIAL STATEMENTS December 31, 2015 and 2014

MANILA BANKERS LIFE INSURANCE CORPORATION NOTE 1 CORPORATE INFORMATION NOTES TO FINANCIAL STATEMENTS December 31, 2015 and 2014 Manila Bankers Life Insurance Corporation (MB Life) is a company formed and

MANILA BANKERS LIFE INSURANCE CORPORATION NOTE 1 CORPORATE INFORMATION NOTES TO FINANCIAL STATEMENTS December 31, 2015 and 2014 Manila Bankers Life Insurance Corporation (MB Life) is a company formed and

Notice about the 2 nd Edition

Notice about the 2 nd Edition 2 nd Edition: /CA1, 2 nd Edition, is the current version that was effective on September 1, 2014. Exams on this content were offered for the first time on January 15, 2015.

Notice about the 2 nd Edition 2 nd Edition: /CA1, 2 nd Edition, is the current version that was effective on September 1, 2014. Exams on this content were offered for the first time on January 15, 2015.

ACE INA Overseas Insurance Company and its subsidiaries (Incorporated in Bermuda)

") ACE INA Overseas Insurance Company and its subsidiaries (Incorporated in Bermuda) Consolidated GAAP Financial Statements (in thousands of U.S. dollars) Report of Independent Auditors To the Board of Directors

ACE INA Overseas Insurance Company and its subsidiaries (Incorporated in Bermuda) Consolidated GAAP Financial Statements (in thousands of U.S. dollars) Report of Independent Auditors To the Board of Directors

Basic Reinsurance Concepts

Basic Reinsurance Concepts OVERVIEW What is Reinsurance Insurance/Reinsurance Similarities Parties to the Reinsurance Agreement Why Insurers Buy Reinsurance Types of Reinsurance Agreements How Reinsurance

Basic Reinsurance Concepts OVERVIEW What is Reinsurance Insurance/Reinsurance Similarities Parties to the Reinsurance Agreement Why Insurers Buy Reinsurance Types of Reinsurance Agreements How Reinsurance

FINANCIAL STATEMENT REVIEW. Frontier Pacific Estate Conservation & Liquidation Office For the Period January 1, 2015

FINANCIAL STATEMENT REVIEW Frontier Pacific Estate Conservation & Liquidation Office For the Period January 1, 2015 through December 31, 2015 Prepared By: Office of State Audits and Evaluations Department

FINANCIAL STATEMENT REVIEW Frontier Pacific Estate Conservation & Liquidation Office For the Period January 1, 2015 through December 31, 2015 Prepared By: Office of State Audits and Evaluations Department

CPCU 500 Study Guide and Practice Exam. Presented by: AssociatePI

CPCU 500 Study Guide and Practice Exam Presented by: AssociatePI CPCU 500 Study Guide CPCU 500 Study Guide Your study guide contains: Breakdown of each CPCU 500 chapter List of the most important topics

CPCU 500 Study Guide and Practice Exam Presented by: AssociatePI CPCU 500 Study Guide CPCU 500 Study Guide Your study guide contains: Breakdown of each CPCU 500 chapter List of the most important topics

OHIO PLAN RISK MANAGEMENT, INC. Columbus, Ohio. FINANCIAL STATEMENTS December 31, 2016 and 2015

OHIO PLAN RISK MANAGEMENT, INC. Columbus, Ohio FINANCIAL STATEMENTS Columbus, Ohio FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR S REPORT... 1 MANAGEMENT S DISCUSSION AND ANALYSIS (UNAUDITED)... 3

OHIO PLAN RISK MANAGEMENT, INC. Columbus, Ohio FINANCIAL STATEMENTS Columbus, Ohio FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR S REPORT... 1 MANAGEMENT S DISCUSSION AND ANALYSIS (UNAUDITED)... 3

COMBINED ANNUAL STATEMENT FOR THE YEAR ENDED DECEMBER 31, 2017 OF THE CONDITION AND AFFAIRS OF THE

*00000000* PROPERTY AND CASUALTY COMPANIES - ASSOCIATION EDITION COMBINED ANNUAL STATEMENT FOR THE YEAR ENDED DECEMBER, 0 OF THE CONDITION AND AFFAIRS OF THE AMERICAN INTERNATIONAL GROUP, INC. its affiliated

*00000000* PROPERTY AND CASUALTY COMPANIES - ASSOCIATION EDITION COMBINED ANNUAL STATEMENT FOR THE YEAR ENDED DECEMBER, 0 OF THE CONDITION AND AFFAIRS OF THE AMERICAN INTERNATIONAL GROUP, INC. its affiliated

COMBINED ANNUAL STATEMENT FOR THE YEAR ENDED DECEMBER 31, 2017 OF THE CONDITION AND AFFAIRS OF THE

PROPERTY AND CASUALTY COMPANIES - ASSOCIATION EDITION COMBINED ANNUAL STATEMENT FOR THE YEAR ENDED DECEMBER, 0 OF THE CONDITION AND AFFAIRS OF THE ALLSTATE INSURANCE GROUP its affiliated property casualty

PROPERTY AND CASUALTY COMPANIES - ASSOCIATION EDITION COMBINED ANNUAL STATEMENT FOR THE YEAR ENDED DECEMBER, 0 OF THE CONDITION AND AFFAIRS OF THE ALLSTATE INSURANCE GROUP its affiliated property casualty

Reinsurance Symposium 2016

Reinsurance Symposium 2016 MAY 10 12, 2016 GEN RE HOME OFFICE, STAMFORD, CT A Berkshire Hathaway Company Reinsurance Symposium 2016 MAY 10 12, 2016 GEN RE HOME OFFICE, STAMFORD, CT Developing a Treaty

Reinsurance Symposium 2016 MAY 10 12, 2016 GEN RE HOME OFFICE, STAMFORD, CT A Berkshire Hathaway Company Reinsurance Symposium 2016 MAY 10 12, 2016 GEN RE HOME OFFICE, STAMFORD, CT Developing a Treaty

Ratemaking for Captives and Alternative Market Vehicles

Ratemaking for Captives and Alternative Market Vehicles Ann M. Conway, FCAS, MAAA Abstract: Although captives represent a significant part of the insurance market, there is relatively little information

Ratemaking for Captives and Alternative Market Vehicles Ann M. Conway, FCAS, MAAA Abstract: Although captives represent a significant part of the insurance market, there is relatively little information

SANDELL HOLDINGS LTD. CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEARS ENDED DECEMBER 31, 2016 AND 2015

CONSOLIDATED FINANCIAL STATEMENTS (AND INDEPENDENT AUDITOR S REPORT THEREON) FOR THE YEARS ENDED DECEMBER 31, 2016 AND 2015 CONSOLIDATED FINANCIAL STATEMENTS AS AT CONTENTS Independent Auditor s Report...

CONSOLIDATED FINANCIAL STATEMENTS (AND INDEPENDENT AUDITOR S REPORT THEREON) FOR THE YEARS ENDED DECEMBER 31, 2016 AND 2015 CONSOLIDATED FINANCIAL STATEMENTS AS AT CONTENTS Independent Auditor s Report...

COMBINED ANNUAL STATEMENT FOR THE YEAR ENDED DECEMBER 31, 2017 OF THE CONDITION AND AFFAIRS OF THE

PROPERTY AND CASUALTY COMPANIES - ASSOCIATION EDITION COMBINED ANNUAL STATEMENT FOR THE YEAR ENDED DECEMBER, 0 OF THE CONDITION AND AFFAIRS OF THE CINCINNATI INSURANCE GROUP its affiliated property casualty

PROPERTY AND CASUALTY COMPANIES - ASSOCIATION EDITION COMBINED ANNUAL STATEMENT FOR THE YEAR ENDED DECEMBER, 0 OF THE CONDITION AND AFFAIRS OF THE CINCINNATI INSURANCE GROUP its affiliated property casualty

THIS SESSION WILL USE POLLING!

THIS SESSION WILL USE POLLING! (To access in an internet browser, go to vcia.cnf.io) Click on the Polling Icon on the VCIA app Click on your session Respond to the Polls HOW TO USE SOCIAL Q&A! (To access

THIS SESSION WILL USE POLLING! (To access in an internet browser, go to vcia.cnf.io) Click on the Polling Icon on the VCIA app Click on your session Respond to the Polls HOW TO USE SOCIAL Q&A! (To access

CAPTIVE INSURANCE TAXES: Is the Strike Zone Narrowing. GARY BOWERS Johnson Lambert LLP Raleigh, NC

CAPTIVE INSURANCE TAXES: Is the Strike Zone Narrowing GARY BOWERS Johnson Lambert LLP Raleigh, NC 919.719.6411 gbowers@johnsonlambert.com Preview We are breaking this into three parts: 1) Brief Tax Review

CAPTIVE INSURANCE TAXES: Is the Strike Zone Narrowing GARY BOWERS Johnson Lambert LLP Raleigh, NC 919.719.6411 gbowers@johnsonlambert.com Preview We are breaking this into three parts: 1) Brief Tax Review

IASB Educational Session Non-Life Claims Liability

IASB Educational Session Non-Life Claims Liability Presented by the January 19, 2005 Sam Gutterman and Martin White Agenda Background The claims process Components of claims liability and basic approach

IASB Educational Session Non-Life Claims Liability Presented by the January 19, 2005 Sam Gutterman and Martin White Agenda Background The claims process Components of claims liability and basic approach

Financial Statements For the Year Ended December 31, 2018

Financial Statements For the Year Ended Financial Statements For the year ended Table of Contents Page Independent Auditor's Report 2 Statement of Financial Position 4 Statement of Comprehensive Income

Financial Statements For the Year Ended Financial Statements For the year ended Table of Contents Page Independent Auditor's Report 2 Statement of Financial Position 4 Statement of Comprehensive Income

NEW JERSEY COMPENSATION RATING & INSPECTION BUREAU HOW TO DETERMINE THE COST OF A WORKERS COMPENSATION INSURANCE POLICY

NEW JERSEY COMPENSATION RATING & INSPECTION BUREAU HOW TO DETERMINE THE COST OF A WORKERS COMPENSATION INSURANCE POLICY 2018 INTRODUCTION This booklet provides a basic explanation of how the cost of a

NEW JERSEY COMPENSATION RATING & INSPECTION BUREAU HOW TO DETERMINE THE COST OF A WORKERS COMPENSATION INSURANCE POLICY 2018 INTRODUCTION This booklet provides a basic explanation of how the cost of a

ABR REINSURANCE LTD. Financial Statements. December 31, 2017 and 2016

Financial Statements December 31, 2017 and 2016 Index to Financial Statements Independent Auditor s Report...1 Balance Sheets as of December 31, 2017 and 2016...3 Statements of Income for the years ended

Financial Statements December 31, 2017 and 2016 Index to Financial Statements Independent Auditor s Report...1 Balance Sheets as of December 31, 2017 and 2016...3 Statements of Income for the years ended

Revised Educational Note. Premium Liabilities. Committee on Property and Casualty Insurance Financial Reporting. March 2015.

Revised Educational Note Premium Liabilities Committee on Property and Casualty Insurance Financial Reporting March 2015 Document 215017 Ce document est disponible en français 2015 Canadian Institute of

Revised Educational Note Premium Liabilities Committee on Property and Casualty Insurance Financial Reporting March 2015 Document 215017 Ce document est disponible en français 2015 Canadian Institute of

SOCIETY OF ACTUARIES Individual Life & Annuities United States Company/Sponsor Perspective Exam CSP-IU MORNING SESSION

SOCIETY OF ACTUARIES Exam CSP-IU MORNING SESSION Date: Friday, May 9, 2008 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 120 points. It consists

SOCIETY OF ACTUARIES Exam CSP-IU MORNING SESSION Date: Friday, May 9, 2008 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 120 points. It consists

Response to Barron s Article

Response to Barron s Article In its June 2, 2014 edition, Barron s published an article by Bill Alpert which is replete with significant factual inaccuracies, which are set forth in Part A below, notwithstanding

Response to Barron s Article In its June 2, 2014 edition, Barron s published an article by Bill Alpert which is replete with significant factual inaccuracies, which are set forth in Part A below, notwithstanding

Insurance Chapter ALABAMA DEPARTMENT OF INSURANCE ADMINISTRATIVE CODE CHAPTER LIFE AND HEALTH REINSURANCE AGREEMENTS

Insurance Chapter 482-1-085 ALABAMA DEPARTMENT OF INSURANCE ADMINISTRATIVE CODE CHAPTER 482-1-085 LIFE AND HEALTH REINSURANCE AGREEMENTS TABLE OF CONTENTS 482-1-085-.01 Authority 482-1-085-.02 Preamble

Insurance Chapter 482-1-085 ALABAMA DEPARTMENT OF INSURANCE ADMINISTRATIVE CODE CHAPTER 482-1-085 LIFE AND HEALTH REINSURANCE AGREEMENTS TABLE OF CONTENTS 482-1-085-.01 Authority 482-1-085-.02 Preamble

Analysis of Uses for Surplus Equity and the Concept of Mid-Layer Pooling. Associate in Risk Pool Management 602 Research Project

Analysis of Uses for Surplus Equity and the Concept of Mid-Layer Pooling Associate in Risk Pool Management 602 Research Project Submitted by Adrienne Beatty, ARM, AINS December 2012 Revised May 2013 Executive

Analysis of Uses for Surplus Equity and the Concept of Mid-Layer Pooling Associate in Risk Pool Management 602 Research Project Submitted by Adrienne Beatty, ARM, AINS December 2012 Revised May 2013 Executive

DELAWARE COMPENSATION RATING BUREAU, INC.

Exhibit 28 As Filed DELAWARE COMPENSATION RATING BUREAU, INC. DECEMBER 1, 2012 RESIDUAL MARKET RATE AND VOLUNTARY MARKET LOSS COST FILING INDEX TO CLASSIFICATION EXHIBITS 1 Composite Pure Premium Multipliers

Exhibit 28 As Filed DELAWARE COMPENSATION RATING BUREAU, INC. DECEMBER 1, 2012 RESIDUAL MARKET RATE AND VOLUNTARY MARKET LOSS COST FILING INDEX TO CLASSIFICATION EXHIBITS 1 Composite Pure Premium Multipliers

Financial Statements and Required Supplementary Information ANNUAL REPORT. June 30, 2018 and 2017 With Independent Auditors Report Thereon

Financial Statements and Required Supplementary Information 2018 ANNUAL REPORT June 30, 2018 and 2017 With Independent Auditors Report Thereon Table of Contents Letter from the President & Director...

Financial Statements and Required Supplementary Information 2018 ANNUAL REPORT June 30, 2018 and 2017 With Independent Auditors Report Thereon Table of Contents Letter from the President & Director...

Captives and the Management of Risk Table of Contents

Captives and the Management of Risk Table of Contents Captives and the Management of Risk (3rd ed.) Preface o Acknowledgement o About the Author o Frequently Asked Questions (CAPFAQs) Addressed in this

Captives and the Management of Risk Table of Contents Captives and the Management of Risk (3rd ed.) Preface o Acknowledgement o About the Author o Frequently Asked Questions (CAPFAQs) Addressed in this

COMBINED ANNUAL STATEMENT FOR THE YEAR ENDED DECEMBER 31, 2016 OF THE CONDITION AND AFFAIRS OF THE

*00000000* PROPERTY AND CASUALTY COMPANIES - ASSOCIATION EDITION COMBINED ANNUAL STATEMENT FOR THE YEAR ENDED DECEMBER, 0 OF THE CONDITION AND AFFAIRS OF THE AMERICAN INTERNATIONAL GROUP, INC. its affiliated

*00000000* PROPERTY AND CASUALTY COMPANIES - ASSOCIATION EDITION COMBINED ANNUAL STATEMENT FOR THE YEAR ENDED DECEMBER, 0 OF THE CONDITION AND AFFAIRS OF THE AMERICAN INTERNATIONAL GROUP, INC. its affiliated

Self Insured Workers Comp vs Group Captives

You Say SIG, I Say Captive Self Insured Workers Comp vs Group Captives Keith Fawcett Brent Re Duke Niedringhaus J.W. Terrill-Marsh & McLennan Agency Similarities of Captives & SIGs Provide a mechanism

You Say SIG, I Say Captive Self Insured Workers Comp vs Group Captives Keith Fawcett Brent Re Duke Niedringhaus J.W. Terrill-Marsh & McLennan Agency Similarities of Captives & SIGs Provide a mechanism

Self-Insuring Worker s Compensation through a Tennessee Captive

Self-Insuring Worker s Compensation through a Tennessee Captive Presented by Keith Fawcett, CPCU, ARe Brentwood Reinsurance Intermediaries, Inc. Norman Chandler, CPA, CPCU Taylor Chandler, LLC New options

Self-Insuring Worker s Compensation through a Tennessee Captive Presented by Keith Fawcett, CPCU, ARe Brentwood Reinsurance Intermediaries, Inc. Norman Chandler, CPA, CPCU Taylor Chandler, LLC New options

Captive Insurance Company Glossary

Captive Insurance Company Glossary All rights reserved. No part of this book may be reproduced in any form or by any means without permission in writing from the publisher. Captive Insurance Company Glossary

Captive Insurance Company Glossary All rights reserved. No part of this book may be reproduced in any form or by any means without permission in writing from the publisher. Captive Insurance Company Glossary

Norfolk Mutual Insurance Company. Financial Statements December 31, 2016

Financial Statements December 31, 2016 Index to Financial Statements December 31, 2016 MANAGEMENT'S RESPONSIBILITY FOR FINANCIAL REPORTING 1 Page INDEPENDENT AUDITORS' REPORT 2 FINANCIAL STATEMENTS Statement

Financial Statements December 31, 2016 Index to Financial Statements December 31, 2016 MANAGEMENT'S RESPONSIBILITY FOR FINANCIAL REPORTING 1 Page INDEPENDENT AUDITORS' REPORT 2 FINANCIAL STATEMENTS Statement

Statutory Financial Statements, Supplementary Information and Report of Independent Certified Public Accountants

Statutory Financial Statements, Supplementary Information and Report of Independent Certified Public Accountants CONNECTICUT ATTORNEYS TITLE INSURANCE COMPANY TABLE OF CONTENTS Page Report of Independent

Statutory Financial Statements, Supplementary Information and Report of Independent Certified Public Accountants CONNECTICUT ATTORNEYS TITLE INSURANCE COMPANY TABLE OF CONTENTS Page Report of Independent

Patrik. I really like the Cape Cod method. The math is simple and you don t have to think too hard.

Opening Thoughts I really like the Cape Cod method. The math is simple and you don t have to think too hard. Outline I. Reinsurance Loss Reserving Problems Problem 1: Claim report lags to reinsurers are

Opening Thoughts I really like the Cape Cod method. The math is simple and you don t have to think too hard. Outline I. Reinsurance Loss Reserving Problems Problem 1: Claim report lags to reinsurers are

Second Revision Educational Note. Premium Liabilities. Committee on Property and Casualty Insurance Financial Reporting. July 2016.

Second Revision Educational Note Premium Liabilities Committee on Property and Casualty Insurance Financial Reporting July 2016 Document 216076 Ce document est disponible en français 2016 Canadian Institute

Second Revision Educational Note Premium Liabilities Committee on Property and Casualty Insurance Financial Reporting July 2016 Document 216076 Ce document est disponible en français 2016 Canadian Institute

CONSOLIDATED CONDENSED BALANCE SHEET Argus International Life Bermuda Limited As at March 31, 2017 expressed in ['000s] Bermuda Dollars

![CONSOLIDATED CONDENSED BALANCE SHEET Argus International Life Bermuda Limited As at March 31, 2017 expressed in ['000s] Bermuda Dollars](/thumbs/78/77807523.jpg "CONSOLIDATED CONDENSED BALANCE SHEET Argus International Life Bermuda Limited As at March 31, 2017 expressed in ['000s] Bermuda Dollars") CONSOLIDATED CONDENSED BALANCE SHEET Argus International Life Bermuda Limited As at March 31, 2017 expressed in ['000s] Bermuda Dollars LINE No. Note 2017 2016 1. CASH AND CASH EQUIVALENTS 3,408 2,714

CONSOLIDATED CONDENSED BALANCE SHEET Argus International Life Bermuda Limited As at March 31, 2017 expressed in ['000s] Bermuda Dollars LINE No. Note 2017 2016 1. CASH AND CASH EQUIVALENTS 3,408 2,714

Rating and Ratemaking

Rating and Ratemaking Ratemaking refers to the pricing of insurance and the calculation of insurance premiums A rate is the price per unit of insurance An exposure unit is the unit of measurement used

Rating and Ratemaking Ratemaking refers to the pricing of insurance and the calculation of insurance premiums A rate is the price per unit of insurance An exposure unit is the unit of measurement used

General Insurance Introduction to Ratemaking & Reserving Exam

Learn Today. Lead Tomorrow. ACTEX Study Manual for General Insurance Introduction to Ratemaking & Reserving Exam Spring 2018 Edition Ke Min, ACIA, ASA, CERA ACTEX Study Manual for General Insurance Introduction

Learn Today. Lead Tomorrow. ACTEX Study Manual for General Insurance Introduction to Ratemaking & Reserving Exam Spring 2018 Edition Ke Min, ACIA, ASA, CERA ACTEX Study Manual for General Insurance Introduction

Successful Captives: Three Case Studies

Successful Captives: Three Case Studies 2018 World Captive Forum January 31 February 2, 2018 Fort Lauderdale, FL #WorldCaptiveForum Presenters: Andrew W. Kush Chief Administrative Officer Healthcare Services

Successful Captives: Three Case Studies 2018 World Captive Forum January 31 February 2, 2018 Fort Lauderdale, FL #WorldCaptiveForum Presenters: Andrew W. Kush Chief Administrative Officer Healthcare Services

Optimal Retention Levels How to get in the Zone

Optimal Retention Levels How to get in the Zone Panelists: James Evans, Albert Risk Management Consultants Stephen DiCenso, Milliman, Inc. Matthew Byrne, Cathedral Indemnity Company Moderator: Michael

Optimal Retention Levels How to get in the Zone Panelists: James Evans, Albert Risk Management Consultants Stephen DiCenso, Milliman, Inc. Matthew Byrne, Cathedral Indemnity Company Moderator: Michael

The Role of ERM in Reinsurance Decisions

The Role of ERM in Reinsurance Decisions Abbe S. Bensimon, FCAS, MAAA ERM Symposium Chicago, March 29, 2007 1 Agenda A Different Framework for Reinsurance Decision-Making An ERM Approach for Reinsurance

The Role of ERM in Reinsurance Decisions Abbe S. Bensimon, FCAS, MAAA ERM Symposium Chicago, March 29, 2007 1 Agenda A Different Framework for Reinsurance Decision-Making An ERM Approach for Reinsurance

SAUDI UNITED COOPERATIVE INSURANCE COMPANY (WALA'A) (A Saudi Joint Stock Company)

(A Saudi Joint Stock Company)") FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS' REPORT FOR THE FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS' REPORT Index Independent auditors' report 2 Page Statement of financial position 3 4 Statement

FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS' REPORT FOR THE FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS' REPORT Index Independent auditors' report 2 Page Statement of financial position 3 4 Statement

Exam ERM-ILA. Date: Tuesday, October 30, 2018 Time: 8:30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES

Enterprise Risk Management Individual Life & Annuities Extension Exam ERM-ILA Date: Tuesday, October 30, 2018 Time: 8:30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination

Enterprise Risk Management Individual Life & Annuities Extension Exam ERM-ILA Date: Tuesday, October 30, 2018 Time: 8:30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination

Starr Insurance & Reinsurance Limited and Subsidiaries

Starr Insurance & Reinsurance Limited and Subsidiaries Consolidated Financial Statements Table of Contents Page Independent Auditors Report 1 Financial Statements Consolidated Balance Sheet 3 Consolidated

Starr Insurance & Reinsurance Limited and Subsidiaries Consolidated Financial Statements Table of Contents Page Independent Auditors Report 1 Financial Statements Consolidated Balance Sheet 3 Consolidated

The Wawanesa Mutual Insurance Company. Consolidated Financial Statements December 31, 2011

The Wawanesa Mutual Insurance Company Consolidated Financial Statements February 21, 2012 Independent Auditor s Report To the Directors of The Wawanesa Mutual Insurance Company We have audited the accompanying

The Wawanesa Mutual Insurance Company Consolidated Financial Statements February 21, 2012 Independent Auditor s Report To the Directors of The Wawanesa Mutual Insurance Company We have audited the accompanying

SOCIETY OF ACTUARIES Introduction to Ratemaking & Reserving Exam GIIRR MORNING SESSION. Date: Wednesday, November 1, 2017 Time: 8:30 a.m. 11:45 a.m.

SOCIETY OF ACTUARIES Exam GIIRR MORNING SESSION Date: Wednesday, November 1, 2017 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 100 points.

SOCIETY OF ACTUARIES Exam GIIRR MORNING SESSION Date: Wednesday, November 1, 2017 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 100 points.

He holds the Chartered Property Casualty Underwriter and Associate in Reinsurance designations.

Reinsurance Overview Tuesday, May 9, 2017, 1:00 p.m. Gary Myers, CPCU, ARe Lost Woods Re, LLC Centralia, Mo. Gary Myers is a familiar figure to many in the property/casualty insurance industry. Starting

Reinsurance Overview Tuesday, May 9, 2017, 1:00 p.m. Gary Myers, CPCU, ARe Lost Woods Re, LLC Centralia, Mo. Gary Myers is a familiar figure to many in the property/casualty insurance industry. Starting

FINANCIAL STATEMENT REVIEW. Mission National Estate Conservation & Liquidation Office For the Period January 1, 2013

FINANCIAL STATEMENT REVIEW Mission National Estate Conservation & Liquidation Office For the Period January 1, 2013 through December 31, 2013 Prepared By: Office of State Audits and Evaluations Department

FINANCIAL STATEMENT REVIEW Mission National Estate Conservation & Liquidation Office For the Period January 1, 2013 through December 31, 2013 Prepared By: Office of State Audits and Evaluations Department

Metropolitan Property and Casualty Insurance Company ASSETS

ASSETS 2 Current Year Prior Year 1 2 3 4 Net Admitted Nonadmitted Assets Net Assets Assets (Cols. 1-2) Admitted Assets 1. Bonds (Schedule D)......2,881,506,666...0...2,881,506,666...2,931,285,752 2. Stocks

ASSETS 2 Current Year Prior Year 1 2 3 4 Net Admitted Nonadmitted Assets Net Assets Assets (Cols. 1-2) Admitted Assets 1. Bonds (Schedule D)......2,881,506,666...0...2,881,506,666...2,931,285,752 2. Stocks

Basic Statistical and Financial Tools: What Can They Reveal About Your Risks? (RIF001)

") Basic Statistical and Financial Tools: What Can They Reveal About Your Risks? (RIF001) Speakers: Laura Langone, Senior Director, Global Risk & Insurance, PayPal, Inc. Michael Elliott, Senior Director of

Basic Statistical and Financial Tools: What Can They Reveal About Your Risks? (RIF001) Speakers: Laura Langone, Senior Director, Global Risk & Insurance, PayPal, Inc. Michael Elliott, Senior Director of

Team Members. Final reports are available on our website at You can contact our office at:

Team Members Jennifer Whitaker, Chief Cheryl L. McCormick, CPA, Assistant Chief Rick Cervantes, CPA, Manager Hanzhao Meng, CPA, Supervisor Jack Liu, CPA Blanca Sandoval Dennis Solheim, CPA Final reports

Team Members Jennifer Whitaker, Chief Cheryl L. McCormick, CPA, Assistant Chief Rick Cervantes, CPA, Manager Hanzhao Meng, CPA, Supervisor Jack Liu, CPA Blanca Sandoval Dennis Solheim, CPA Final reports

California Retrospective Rating Plan Effective January 1, 2013 Updated April 2, 2015

Workers Compensation Insurance Rating Bureau of California California Retrospective Rating Plan Effective January 1, 2013 Notice This California Retrospective Rating Plan (Plan) was developed by the Workers

Workers Compensation Insurance Rating Bureau of California California Retrospective Rating Plan Effective January 1, 2013 Notice This California Retrospective Rating Plan (Plan) was developed by the Workers

COMBINED ANNUAL STATEMENT

PROPERTY AND CASUALTY COMPANIES ASSOCIATION EDITION COMBINED ANNUAL STATEMENT FOR THE YEAR ENDING December, 06 OF THE CONDITION AND AFFAIRS OF THE ZENITH INSURANCE COMPANY AND ITS AFFILIATED PROPERTY AND

PROPERTY AND CASUALTY COMPANIES ASSOCIATION EDITION COMBINED ANNUAL STATEMENT FOR THE YEAR ENDING December, 06 OF THE CONDITION AND AFFAIRS OF THE ZENITH INSURANCE COMPANY AND ITS AFFILIATED PROPERTY AND

MORNING SESSION. Date: Friday, May 11, 2007 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES

SOCIETY OF ACTUARIES Exam APMV MORNING SESSION Date: Friday, May 11, 2007 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 120 points. It consists

SOCIETY OF ACTUARIES Exam APMV MORNING SESSION Date: Friday, May 11, 2007 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 120 points. It consists

Haverford (Bermuda) Ltd. Condensed General Purpose Financial Statemets. For the financial year from. January 1, 2017.

Ltd. Condensed General Purpose Financial Statemets. For the financial year from. January 1, 2017.") Haverford (Bermuda) Ltd Condensed General Purpose Financial Statemets For the financial year from January 1, 2017 December 31, 2017 Contents Haverford (Bermuda) Ltd As at December 31, 2017 1 Contents

Haverford (Bermuda) Ltd Condensed General Purpose Financial Statemets For the financial year from January 1, 2017 December 31, 2017 Contents Haverford (Bermuda) Ltd As at December 31, 2017 1 Contents

RESERVEPRO Technology to transform loss data into valuable information for insurance professionals

RESERVEPRO Technology to transform loss data into valuable information for insurance professionals Today s finance and actuarial professionals face increasing demands to better identify trends for smarter

RESERVEPRO Technology to transform loss data into valuable information for insurance professionals Today s finance and actuarial professionals face increasing demands to better identify trends for smarter