Basic Statistical and Financial Tools: What Can They Reveal About Your Risks? (RIF001)

|

|

|

- Daisy Owens

- 6 years ago

- Views:

Transcription

1 Basic Statistical and Financial Tools: What Can They Reveal About Your Risks? (RIF001) Speakers: Laura Langone, Senior Director, Global Risk & Insurance, PayPal, Inc. Michael Elliott, Senior Director of Knowledge Resources, The Institutes

2 Basic Statistical and Financial Tools: What Can They Reveal About Your Risks? Introduction How do you evaluate insurance program options? Do you find yourself asking Should my company change deductibles from $250,000 to $500,000 or $1 million? What criteria do you use to evaluate these questions? There a various tools and analyses that may be used: Providing a process for companies to determine their risk tolerance and risk appetite Estimating a company s exposure to loss (expected loss, worst case scenarios) Comparing the company s insurance program options to other company capital investment options

3 Learning Objectives At the end of this session, you will: Explore basic statistical and financial tools available for risk management. Use these tools to analyze organizational risks and select appropriate risk financing solutions. Communicate to top management statistical and financial justifications for chosen risk financing techniques.

4 Overview Financial Tools Available Loss triangles Loss forecasting Retention analysis Understanding key financial concepts Total cost of risk Cash flow analysis Comparing financial options Risk-adjusted return on capital Engaging your broker and obtaining buy-in from management

5 Scenario Workers compensation line of business Current retention = $250,000 per accident Trying to decide whether to increase the retention to $500,000, or even $1,000,000 per accident Develop losses Look at premiums and other costs at alternative retention levels Analyze cash flow

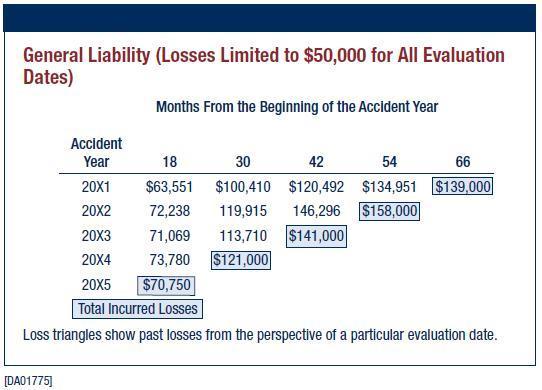

6 Reported Claims Paid Amounts Plus Case Reserves (Incurred Losses) (Losses limited to $250,000 per accident) Evaluation (months after beginning of accident year) Accident Year $1,400,000 $1,960,000 $2,380,000 $2,660,000 $2,800, $1,650,000 $2,310,000 $2,805,000 $3,135, $1,115,000 $1,561,000 $1,895, $1,400,000 $1,960, $1,600,000

7

8 $3,000, Accident Year IBNR $2,500,000 $2,000,000 $1,500,000 $1,000,000 $500,000 $ IBNR Reserves $1,400,000 $840,000 $420,000 $140,000 $0 Case Reserves $1,120,000 $1,260,000 $1,120,000 $840,000 $420,000 Paid Losses $280,000 $700,000 $1,260,000 $1,820,000 $2,380,000

9 $3,500, Accident Year Projections $3,000,000 $2,500,000 $2,000,000 $1,500,000 $1,000,000 $500,000 $ IBNR Reserves $1,600,000 $960,000 $480,000 $160,000 $0 Case Reserves $1,280,000 $1,440,000 $1,280,000 $960,000 $480,000 Paid Losses $320,000 $800,000 $1,440,000 $2,080,000 $2,720,000

10 2016 Per Accident Retentions $250,000 Retention $500,000 Retention $3,000,000 $3,200,000 $3,400,000 $3,200,000 $3,500,000 $3,800,000 $1,000,000 Retention $3,350,000 $3,600,000 $3,950,000

11 2016 Estimated Total Cost of Risk (TCOR) Per Accident Retention $250,000 $500,000 $1,000,000 Retained Claims (expected) $3,200,000 $3,500,000 $3,600,000 Risk transfer expense 900, , ,000 Loss control expense 50,000 50,000 50,000 RM administrative expense 40,000 40,000 40,000 Total cost of risk (expected) 4,190,000 4,090,000 3,940,000 Total cost of risk (high) 4,390,000 4,390,000 4,290,000 Total cost of risk (low) 3,990,000 3,790,000 3,690,000 Add one full-retention loss: $4,440,000 $4,590,000 $4,940,000

12 Cash Flow Analysis of 2016 Expected Claim Amounts Total cost of risk - $250,000 retention - Expected Amount Estimated Percentage Paid Claims Claim Payments 320, , , , , ,000 3,200,000 Risk transfer expense 900, ,000 Loss control expense 50,000 50,000 RM administrative expense 40,000 40,000 Total cash outflow 1,310, , , , , ,000 4,190,000 PV Factor (6.9% per annum) Net Present Value TCOR $1,267,017 $434,285 $541,671 $506,708 $474,002 $332,555 $3,556,239

13 Another Approach The typical approach ignores the capital charge and capital at risk Retention level options can be evaluated using three metrics: Economic Cost of Risk Risk Adjusted Return Risk Adjusted Return on Capital Economic Cost of Risk = L+P+C where L = Discounted Retained Losses P = Discounted Premiums C = Capital Charge What is the capital charge? It is the charge related to holding capital to support the insurance program What is the company s cost of setting aside additional capital to support the insurance program Higher retentions have a higher capital charge and lower retentions have a lower capital charge

14 Economic Cost of Risk Optimality Defined as Minimum Economic Cost $40,000,000 $35,000,000 ECOR = L+P+C Economic Cost of Risk $30,000,000 $25,000,000 $20,000,000 $15,000,000 where L = Disc. Ret. Losses P = Premiums C = Capital Charge $10,000,000 $5,000,000 $0 <null> 2,500,000 $5,000,000 $10,000,000 $25,000,000 $35,000,000 $50,000,000 $100,000,000 Per-Claim Retention The capital charge can be interpreted in various ways whether or not funds are actually segregated from working capital. This approach typically identifies the optimal retention option.

15 Maximizing Risk Adjusted Return Value Generation Through Risk Management $ ECOR ECOR + RAR RAR Option <n> <n> <n> Economic savings from <no insurance> (RAR) is interpreted as the value generated for the firm through the purchase of insurance.

16 Maximizing RAROC 15.0% RAROC = Risk Adjusted Return On Capital Economic Return Economic Capital Risk Adjusted Return on Capital 10.0% 5.0% 0.0% -5.0% -10.0% <null> $2,500,000 $5,000,000 $10,000,000 $25,000,000 $35,000,000 $50,000,000 Per-Occurrence Retention RAROC provides a means to compare treatments of different risks and across lines of business - i.e. a tool to implement true Enterprise Risk Management.

17 Capacity Does Not Imply Desirability 100 Just because a company may have the capacity to bear substantial risk, does not mean that it s in the firm s best interest to do so. Capacity to Bear Additional Risk (millions) Working Capital Pre-Tax Earnings Cashflow Surplus Cashflow Earnings per Share Stockholder's Equity Net Sales Total Assets tolerable range for maximum unexpected losses A firm s capacity to bear risk can be thought of as a pain threshold above which the decision makers do not wish to experience. Capacity is often found through an analysis of the firm s financials, and application of rules of thumb. Wall Street s expectations often play a significant role. By definition, capacity goes across all sources of risk, not just insurable risks. Also, as expected losses are budgeted for, expected losses do not erode capacity. A large strong organization with many investment opportunities should not retain large amounts of fortuitous risk, as its capital base may be better employed.

18 Risk-adjusted Return on Capital Example: Worker s Compensation Analysis What retentions are optimal for the economic cost of capital to insure this risk? Inputs: Premium at various retentions Loss forecasts at various confidence levels Understand maximum probable loss worse case scenario Modeling by Oliver Wyman

19 Risk-adjusted Return on Capital Example: Medical Stop Loss Analysis Should HR self-insure this risk? Inputs: Premium at various retentions Loss forecasts at various confidence levels Understand maximum probable loss worse case scenario Modeling by Oliver Wyman

20 Summary Objectives Learned: There are various solid financial tools available for risk managers to make better risk-based decisions If used correctly, a risk retention analysis framework will provide risk managers a process for quantifying and optimizing the insurance purchase on an annual basis Next steps: Engage your broker and actuary Build time into your insurance renewal process Enhance decision making with senior management Add value to other internal stakeholders on these approaches

21 Questions

22 Developing Losses Collect and organize past data Limit individual losses Apply loss development factors

23

24

25

26 Predictive Modeling Training Data Test Data Production

27 Instances Predictive Modeling Data WC Claims Fraud Attributes Class Label Name Age Body part previously injured Attorney involvement Witness Fraudulent Claim Anna 35 Y Y N Y Carlos 42 N N Y N David 53 N N N N Jason 27 Y Y N Y Sonia 32 N Y Y N New Instance Gregory 45 Y Y Y?

28 Information Gain from Various Attributes Prev. Injured Body Part Age Attorney involvement Days to Report Claim Day of week Witness

29 Classification Tree WC Claim Fraud No Previously Injured Body Part Yes Age Attorney involvement < 40 => 40 No Yes Number of Medical Visits Day of week < 3 > 3 Monday Other than Monday Days to Report Claim < 1 > 1 No Witness Yes Prob. Fraud =.02 Prob. Fraud =.80

30 Classification as a Set of Rules If (body part previously injured) AND (an attorney is involved) AND (day of week is Monday) AND (no witness) THEN Class = Fraud Likely Refer for Further Investigation If (body part not previously injured) AND (age less than 40) AND (number of medical visits less than 3) AND (claim reported within 1 day) THEN Class = Fraud Highly Unlikely

THIS SESSION WILL USE POLLING!

THIS SESSION WILL USE POLLING! (To access in an internet browser, go to vcia.cnf.io) Click on the Polling Icon on the VCIA app Click on your session Respond to the Polls HOW TO USE SOCIAL Q&A! (To access

THIS SESSION WILL USE POLLING! (To access in an internet browser, go to vcia.cnf.io) Click on the Polling Icon on the VCIA app Click on your session Respond to the Polls HOW TO USE SOCIAL Q&A! (To access

RISK FINANCING FOR THE LOSS CONTROL PROFESSIONAL

RISK FINANCING FOR THE LOSS CONTROL PROFESSIONAL Session 561 Mark D. Oldham, CSP Lockton Companies Denver, Colorado Learning Outcomes Impact of, and opportunities presented, by loss sensitive risk financing

RISK FINANCING FOR THE LOSS CONTROL PROFESSIONAL Session 561 Mark D. Oldham, CSP Lockton Companies Denver, Colorado Learning Outcomes Impact of, and opportunities presented, by loss sensitive risk financing

Optimal Retention Levels How to get in the Zone

Optimal Retention Levels How to get in the Zone Panelists: James Evans, Albert Risk Management Consultants Stephen DiCenso, Milliman, Inc. Matthew Byrne, Cathedral Indemnity Company Moderator: Michael

Optimal Retention Levels How to get in the Zone Panelists: James Evans, Albert Risk Management Consultants Stephen DiCenso, Milliman, Inc. Matthew Byrne, Cathedral Indemnity Company Moderator: Michael

RISK MANAGEMENT. Budgeting, d) Timing, e) Risk Categories,(RBS) f) 4. EEF. Definitions of risk probability and impact, g) 5. OPA

Timing, e) Risk Categories,(RBS) f) 4. EEF. Definitions of risk probability and impact, g) 5. OPA") RISK MANAGEMENT 11.1 Plan Risk Management: The process of DEFINING HOW to conduct risk management activities for a project. In Plan Risk Management, the remaining FIVE risk management processes are PLANNED

RISK MANAGEMENT 11.1 Plan Risk Management: The process of DEFINING HOW to conduct risk management activities for a project. In Plan Risk Management, the remaining FIVE risk management processes are PLANNED

Insurance Contracts for 831(b) Enterprise Risk Captives Policies and Pooling Agreements

Enterprise Risk Captives Policies and Pooling Agreements") Insurance Contracts for 831(b) Enterprise Risk Captives Policies and Pooling Agreements Jeffrey K. Simpson John R. Capasso Brian Johnson Gordon, Fournaris & Mammarella, P.A. Captive Planning Associates,

Insurance Contracts for 831(b) Enterprise Risk Captives Policies and Pooling Agreements Jeffrey K. Simpson John R. Capasso Brian Johnson Gordon, Fournaris & Mammarella, P.A. Captive Planning Associates,

ก ก Tools and Techniques for Enterprise Risk Management (ERM)

") ก ก Tools and Techniques for Enterprise Risk Management (ERM) COSO ERM ISO ERM 31 2554 10:45 12:15.. 301, 302, 307 ก ก COSO Internal Control ERM Integrated Framework Application Technique ISO 31000 Guide

ก ก Tools and Techniques for Enterprise Risk Management (ERM) COSO ERM ISO ERM 31 2554 10:45 12:15.. 301, 302, 307 ก ก COSO Internal Control ERM Integrated Framework Application Technique ISO 31000 Guide

The Role of ERM in Reinsurance Decisions

The Role of ERM in Reinsurance Decisions Abbe S. Bensimon, FCAS, MAAA ERM Symposium Chicago, March 29, 2007 1 Agenda A Different Framework for Reinsurance Decision-Making An ERM Approach for Reinsurance

The Role of ERM in Reinsurance Decisions Abbe S. Bensimon, FCAS, MAAA ERM Symposium Chicago, March 29, 2007 1 Agenda A Different Framework for Reinsurance Decision-Making An ERM Approach for Reinsurance

Presentation by: Nasumba Kizito Kwatukha CPA,CIA, CISA,CFE,CISSP,CRMA,CISM,IIK 6 th JULY 2017

ENTERPRISE RISK MANAGEMENT SEMINAR Enterprise Risk Management in case of Financial Institutions Presentation by: Nasumba Kizito Kwatukha CPA,CIA, CISA,CFE,CISSP,CRMA,CISM,IIK 6 th JULY 2017 Uphold public

ENTERPRISE RISK MANAGEMENT SEMINAR Enterprise Risk Management in case of Financial Institutions Presentation by: Nasumba Kizito Kwatukha CPA,CIA, CISA,CFE,CISSP,CRMA,CISM,IIK 6 th JULY 2017 Uphold public

Subject CA1 Actuarial Risk Management

Institute of Actuaries of India Subject CA1 Actuarial Risk Management For 2018 Examinations Subject CA1 Actuarial Risk Management Syllabus Aim The aim of the Actuarial Risk Management subject is that upon

Institute of Actuaries of India Subject CA1 Actuarial Risk Management For 2018 Examinations Subject CA1 Actuarial Risk Management Syllabus Aim The aim of the Actuarial Risk Management subject is that upon

The Only Withdrawal Plan You Will Ever Need

The Only Withdrawal Plan You Will Ever Need November 14, 2016 by Ken Steiner Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The Only Withdrawal Plan You Will Ever Need November 14, 2016 by Ken Steiner Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

REDUCING TOTAL COST OF RISK THROUGH ANALYTICS

REDUCING TOTAL COST OF RISK THROUGH ANALYTICS Jessica Wacek, Senior Vice President, Marsh Jaci Mennenga, Risk Manager, COUNTRY Financial W W W. C H I C A G O L A N D R I S K F O R U M. O R G Risk Has a

REDUCING TOTAL COST OF RISK THROUGH ANALYTICS Jessica Wacek, Senior Vice President, Marsh Jaci Mennenga, Risk Manager, COUNTRY Financial W W W. C H I C A G O L A N D R I S K F O R U M. O R G Risk Has a

Session 4, Monday, April 3 rd (4:00-5:00)

") Session 4, Monday, April 3 rd (4:00-5:00) Applied Statistical Tools: Risk and Capital Budgeting v2.0 2014 Association for Financial Professionals. All rights reserved. Session 12-1 Chapters Covered Risk

Session 4, Monday, April 3 rd (4:00-5:00) Applied Statistical Tools: Risk and Capital Budgeting v2.0 2014 Association for Financial Professionals. All rights reserved. Session 12-1 Chapters Covered Risk

ENTERPRISE RISK AND STRATEGIC DECISION MAKING: COMPLEX INTER-RELATIONSHIPS

ENTERPRISE RISK AND STRATEGIC DECISION MAKING: COMPLEX INTER-RELATIONSHIPS By Mark Laycock The views and opinions expressed in this paper are those of the authors and do not necessarily reflect the official

ENTERPRISE RISK AND STRATEGIC DECISION MAKING: COMPLEX INTER-RELATIONSHIPS By Mark Laycock The views and opinions expressed in this paper are those of the authors and do not necessarily reflect the official

THE COMIC-CON OF RISK FINANCING

THE COMIC-CON OF RISK FINANCING RIF006 Speakers: Barbara Benson, VP Risk Solution, Willis Towers Watson Scott Silitsky, VP Risk Management, thyssenkrupp Elevator Corporation Learning Objectives At the

THE COMIC-CON OF RISK FINANCING RIF006 Speakers: Barbara Benson, VP Risk Solution, Willis Towers Watson Scott Silitsky, VP Risk Management, thyssenkrupp Elevator Corporation Learning Objectives At the

ALM processes and techniques in insurance

ALM processes and techniques in insurance David Campbell 18 th November. 2004 PwC Asset Liability Management Matching or management? The Asset-Liability Management framework Example One: Asset risk factors

ALM processes and techniques in insurance David Campbell 18 th November. 2004 PwC Asset Liability Management Matching or management? The Asset-Liability Management framework Example One: Asset risk factors

ALM as a tool for Malaysian business

Actuarial Partners Consulting Sdn Bhd Suite 17-02 Kenanga International Jalan Sultan Ismail 50250 Kuala Lumpur, Malaysia +603 2161 0433 Fax +603 2161 3595 www.actuarialpartners.com ALM as a tool for Malaysian

Actuarial Partners Consulting Sdn Bhd Suite 17-02 Kenanga International Jalan Sultan Ismail 50250 Kuala Lumpur, Malaysia +603 2161 0433 Fax +603 2161 3595 www.actuarialpartners.com ALM as a tool for Malaysian

Subject SP1 Health and Care Specialist Principles Syllabus

Subject SP1 Health and Care Specialist Principles Syllabus for the 2019 exams 1 June 2018 Health and Care Specialist Principles Aim The aim of the Health and Care Principles subject is to instil in successful

Subject SP1 Health and Care Specialist Principles Syllabus for the 2019 exams 1 June 2018 Health and Care Specialist Principles Aim The aim of the Health and Care Principles subject is to instil in successful

INSTITUTE OF BANKING STUDIES

INSTITUTE OF BANKING STUDIES Accredited by: Website: www.kibs.edu.kw Ibselearning: wwwibselearning.com email: training@kibs.edu.kw email: ibslearn@kibs.edu.kw Risk Management is a Process of Taking Calculated

INSTITUTE OF BANKING STUDIES Accredited by: Website: www.kibs.edu.kw Ibselearning: wwwibselearning.com email: training@kibs.edu.kw email: ibslearn@kibs.edu.kw Risk Management is a Process of Taking Calculated

WHAT IS CAPITAL BUDGETING?

WHAT IS CAPITAL BUDGETING? Capital budgeting is a required managerial tool. One duty of a financial manager is to choose investments with satisfactory cash flows and rates of return. Therefore, a financial

WHAT IS CAPITAL BUDGETING? Capital budgeting is a required managerial tool. One duty of a financial manager is to choose investments with satisfactory cash flows and rates of return. Therefore, a financial

P1 Performance Operations

Operational Level Paper P1 Performance Operations Examiner s Answers SECTION A Answer to Question One 1.1 The correct answer is D. 1.2 $40,000 x 3.791 = $151,640 $50,000 / $151,640 = 0.3297 = 33.0% The

Operational Level Paper P1 Performance Operations Examiner s Answers SECTION A Answer to Question One 1.1 The correct answer is D. 1.2 $40,000 x 3.791 = $151,640 $50,000 / $151,640 = 0.3297 = 33.0% The

Business Auditing - Enterprise Risk Management. October, 2018

Business Auditing - Enterprise Risk Management October, 2018 Contents The present document is aimed to: 1 Give an overview of the Risk Management framework 2 Illustrate an ERM model Page 2 What is a risk?

Business Auditing - Enterprise Risk Management October, 2018 Contents The present document is aimed to: 1 Give an overview of the Risk Management framework 2 Illustrate an ERM model Page 2 What is a risk?

NAIC ORSA: A Practical Guide to the DOI s First Year Reviews

ZZ NAIC ORSA: A Practical Guide to the DOI s First Year Reviews Eli Russo Sherry Flippo NAIC 2 Attention APIR, PIR, or SPIR Designees This presentation is pre-qualified for NAIC Designation Renewal Credits

ZZ NAIC ORSA: A Practical Guide to the DOI s First Year Reviews Eli Russo Sherry Flippo NAIC 2 Attention APIR, PIR, or SPIR Designees This presentation is pre-qualified for NAIC Designation Renewal Credits

Life under Solvency II Be prepared!

Life under Solvency II Be prepared! Moderator: Hugh Rosenbaum, Towers Watson Speakers: Tomas Wittbjer, Global Head of Insurance, IKANO SA Lorraine Stack, Marsh Management Services Dublin Session Overview

Life under Solvency II Be prepared! Moderator: Hugh Rosenbaum, Towers Watson Speakers: Tomas Wittbjer, Global Head of Insurance, IKANO SA Lorraine Stack, Marsh Management Services Dublin Session Overview

How to Improve the Value of Your Bank

How to Improve the Value of Your Bank Philip K. Smith, President Gerrish Smith Tuck, Consultants and Attorneys Independent Bankers of Colorado 44 th Annual Convention September 20-22, 2017 Increase earnings

How to Improve the Value of Your Bank Philip K. Smith, President Gerrish Smith Tuck, Consultants and Attorneys Independent Bankers of Colorado 44 th Annual Convention September 20-22, 2017 Increase earnings

Total Cost of Risk: The Captive Focus

Total Cost of Risk: The Captive Focus Hugh Rosenbaum, Retired Principal, Towers Watson Jim Blinn, Executive Editor of RIMS Benchmark Survey and EVP of Advisen Ltd. Joel Chansky, Principal, Milliman James

Total Cost of Risk: The Captive Focus Hugh Rosenbaum, Retired Principal, Towers Watson Jim Blinn, Executive Editor of RIMS Benchmark Survey and EVP of Advisen Ltd. Joel Chansky, Principal, Milliman James

Value of Dynamic Financial Analysis for Insurance Companies.

Value of Dynamic Financial Analysis for Insurance Companies www.ultirisk.com Main Applications of DFA 1. Ceded Reinsurance Evaluation and Optimisation 2. Risk-Adjusted Capital Allocation and Pricing 3.

Value of Dynamic Financial Analysis for Insurance Companies www.ultirisk.com Main Applications of DFA 1. Ceded Reinsurance Evaluation and Optimisation 2. Risk-Adjusted Capital Allocation and Pricing 3.

Copyright 2015 The Ins4tutes

ARM 56 Review CAD004 Speaker: Michael Elliott, CPCU, AIAF, The Institutes Learning Objectives At the end of this session, you will: Dissect the most challenging ARM 56 course topics. Practice ARM 56 exam

ARM 56 Review CAD004 Speaker: Michael Elliott, CPCU, AIAF, The Institutes Learning Objectives At the end of this session, you will: Dissect the most challenging ARM 56 course topics. Practice ARM 56 exam

Performance-Based Engineering and Resilience Management for Your Risk Control Program

Performance-Based Engineering and Resilience Management for Your Risk Control Program Speakers: (RIC010) Jamie Bloom - Insurance Manager, Sonoma County, California Evan Reis - Co-founder, US Resiliency

Performance-Based Engineering and Resilience Management for Your Risk Control Program Speakers: (RIC010) Jamie Bloom - Insurance Manager, Sonoma County, California Evan Reis - Co-founder, US Resiliency

LAURENTIDE INSURANCE AND MORTGAGE COMPANY LIMITED 2017 AUDITED FINANCIAL STATEMENTS

LAURENTIDE INSURANCE AND MORTGAGE COMPANY LIMITED 2017 AUDITED FINANCIAL STATEMENTS INDEPENDENT AUDITORS REPORT Independent auditors report To the Shareholder of Laurentide Insurance and Mortgage Company

LAURENTIDE INSURANCE AND MORTGAGE COMPANY LIMITED 2017 AUDITED FINANCIAL STATEMENTS INDEPENDENT AUDITORS REPORT Independent auditors report To the Shareholder of Laurentide Insurance and Mortgage Company

AMERICAN INTERNATIONAL GROUP, INC. ECONOMIC CAPITAL MODELING INITIATIVE & APPLICATIONS

AMERICAN INTERNATIONAL GROUP, INC. ECONOMIC CAPITAL MODELING INITIATIVE & APPLICATIONS November 2007 Update INTRODUCTION AIG has made significant progress to date on its economic capital modeling initiative

AMERICAN INTERNATIONAL GROUP, INC. ECONOMIC CAPITAL MODELING INITIATIVE & APPLICATIONS November 2007 Update INTRODUCTION AIG has made significant progress to date on its economic capital modeling initiative

Project Theft Management,

Project Theft Management, by applying best practises of Project Risk Management Philip Rosslee, BEng. PrEng. MBA PMP PMO Projects South Africa PMO Projects Group www.pmo-projects.co.za philip.rosslee@pmo-projects.com

Project Theft Management, by applying best practises of Project Risk Management Philip Rosslee, BEng. PrEng. MBA PMP PMO Projects South Africa PMO Projects Group www.pmo-projects.co.za philip.rosslee@pmo-projects.com

Exam ERM-GI. Date: Tuesday, October 30, 2018 Time: 8:30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES. Recognized by the Canadian Institute of Actuaries.

Enterprise Risk Management General Insurance Extension Exam ERM-GI Date: Tuesday, October 30, 2018 Time: 8:30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total

Enterprise Risk Management General Insurance Extension Exam ERM-GI Date: Tuesday, October 30, 2018 Time: 8:30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total

FIN 435 CAPITAL MARKETS AND FIXED INCOME. Spring :30am 9:45am or 4:00pm 5:15pm. Managing Bond Portfolios

FIN 435 CAPITAL MARKETS AND FIXED INCOME Managing Bond Portfolios WHEN Spring 2017 8:30am 9:45am or 4:00pm 5:15pm WHERE SGMH 2308 INTEGRATE A BROAD SET OF BUSINESS RELATED SKILLS INTO AN EFFECTIVE DECISION

FIN 435 CAPITAL MARKETS AND FIXED INCOME Managing Bond Portfolios WHEN Spring 2017 8:30am 9:45am or 4:00pm 5:15pm WHERE SGMH 2308 INTEGRATE A BROAD SET OF BUSINESS RELATED SKILLS INTO AN EFFECTIVE DECISION

Functions of finance. Investment decision Financing decision Dividend decision Liquidity decision

Functions of finance Investment decision Financing decision Dividend decision Liquidity decision Relationship to accounting Accounting and finance are both forms of managing the money of the business,

Functions of finance Investment decision Financing decision Dividend decision Liquidity decision Relationship to accounting Accounting and finance are both forms of managing the money of the business,

FINANCIAL STATEMENT FRAUD: DETAILED LOOK AT UNCOVERING CREATIVE ACCOUNTING FRAUD: P R E S E N T E D B Y : J O H N E K A D A H

FINANCIAL STATEMENT FRAUD: DETAILED LOOK AT UNCOVERING CREATIVE ACCOUNTING FRAUD: P R E S E N T E D B Y : J O H N E K A D A H Definitions Financial statement frauds is the deliberate misrepresentation

FINANCIAL STATEMENT FRAUD: DETAILED LOOK AT UNCOVERING CREATIVE ACCOUNTING FRAUD: P R E S E N T E D B Y : J O H N E K A D A H Definitions Financial statement frauds is the deliberate misrepresentation

1st Capacity Building Seminar on Enterprise Risk Management

1st Capacity Building Seminar on Enterprise Risk Management Hotel Sea Princess, Mumbai 10 th August 2018 ERM as a Business Enabler N K V Roop Kumar, EVP, Chief of Risk, Info & Cyber Security Management,

1st Capacity Building Seminar on Enterprise Risk Management Hotel Sea Princess, Mumbai 10 th August 2018 ERM as a Business Enabler N K V Roop Kumar, EVP, Chief of Risk, Info & Cyber Security Management,

Institute of Actuaries of India. May 2010 EXAMINATION. Subject ST3 General Insurance Specialist Technical. Indicative Solution

Institute of Actuaries of India May 2010 EXAMINATION Subject ST3 General Insurance Specialist Technical Indicative Solution 1). i) The two main types of proportional reinsurance are quota share and surplus

Institute of Actuaries of India May 2010 EXAMINATION Subject ST3 General Insurance Specialist Technical Indicative Solution 1). i) The two main types of proportional reinsurance are quota share and surplus

Benevolence Assistance Liabilities: A Hidden Risk for CCRC Operators. Session 46-F Tuesday, 430P to 540P October 28, 2003

Benevolence Assistance Liabilities: A Hidden Risk for CCRC Operators Session 46-F Tuesday, 430P to 540P October 28, 2003 Presenters Theory AV Powell Consulting Actuary AV Powell & Associates Case Example

Benevolence Assistance Liabilities: A Hidden Risk for CCRC Operators Session 46-F Tuesday, 430P to 540P October 28, 2003 Presenters Theory AV Powell Consulting Actuary AV Powell & Associates Case Example

Measurable value creation through an advanced approach to ERM

Measurable value creation through an advanced approach to ERM Greg Monahan, SOAR Advisory Abstract This paper presents an advanced approach to Enterprise Risk Management that significantly improves upon

Measurable value creation through an advanced approach to ERM Greg Monahan, SOAR Advisory Abstract This paper presents an advanced approach to Enterprise Risk Management that significantly improves upon

RISK ANALYSIS AND CONTINGENCY DETERMINATION USING EXPECTED VALUE TCM Framework: 7.6 Risk Management

AACE International Recommended Practice No. 44R-08 RISK ANALYSIS AND CONTINGENCY DETERMINATION USING EXPECTED VALUE TCM Framework: 7.6 Risk Management Acknowledgments: John K. Hollmann, PE CCE CEP (Author)

AACE International Recommended Practice No. 44R-08 RISK ANALYSIS AND CONTINGENCY DETERMINATION USING EXPECTED VALUE TCM Framework: 7.6 Risk Management Acknowledgments: John K. Hollmann, PE CCE CEP (Author)

Asset Liability Modelling (ALM) Approaches, Techniques, Trends In the Pension Practice

Approaches, Techniques, Trends In the Pension Practice") Asset Liability Modelling (ALM) Approaches, Techniques, Trends In the Pension Practice Chris Brisebois, FSA, FCIA, CFA CIA Investment Seminar Agenda 2 Background ALM in a pension fund context Modeling

Asset Liability Modelling (ALM) Approaches, Techniques, Trends In the Pension Practice Chris Brisebois, FSA, FCIA, CFA CIA Investment Seminar Agenda 2 Background ALM in a pension fund context Modeling

Ingenious Capital Management Limited: Pillar III Disclosure

CONTENTS 1. Introduction 2. Risk Management 3. Capital Resources 4. Internal Capital Adequacy Assessment Process (ICAAP) 5. Remuneration Policy Disclosure 1. INTRODUCTION 1.1 Scope of Application Ingenious

CONTENTS 1. Introduction 2. Risk Management 3. Capital Resources 4. Internal Capital Adequacy Assessment Process (ICAAP) 5. Remuneration Policy Disclosure 1. INTRODUCTION 1.1 Scope of Application Ingenious

CONTROLLING RISING HEALTH CARE COSTS

CONTROLLING RISING HEALTH CARE COSTS Kiplinger's estimates that in 2003, health care costs will increase by an average of 18%. Small and midsized companies may be hit with a 25%-30% hike. So PLA tapped

CONTROLLING RISING HEALTH CARE COSTS Kiplinger's estimates that in 2003, health care costs will increase by an average of 18%. Small and midsized companies may be hit with a 25%-30% hike. So PLA tapped

**BEGINNING OF EXAMINATION** HEALTH, GROUP LIFE & MANAGED CARE MORNING SESSION

**BEGINNING OF EXAMINATION** HEALTH, GROUP LIFE & MANAGED CARE MORNING SESSION 1. (4 points) You are an actuary for a reinsurance company. A business school professor at a local university has invited

**BEGINNING OF EXAMINATION** HEALTH, GROUP LIFE & MANAGED CARE MORNING SESSION 1. (4 points) You are an actuary for a reinsurance company. A business school professor at a local university has invited

PRICING CHALLENGES A CONTINUOUSLY CHANGING MARKET +34 (0) (0)

(0)") PRICING CHALLENGES IN A CONTINUOUSLY CHANGING MARKET Michaël Noack Senior consultant, ADDACTIS Ibérica michael.noack@addactis.com Ming Roest CEO, ADDACTIS Netherlands ming.roest@addactis.com +31 (0)203

PRICING CHALLENGES IN A CONTINUOUSLY CHANGING MARKET Michaël Noack Senior consultant, ADDACTIS Ibérica michael.noack@addactis.com Ming Roest CEO, ADDACTIS Netherlands ming.roest@addactis.com +31 (0)203

TONY MILSOM Specialist Risk Engineering KPC

www.kuwaiterm.com Quantitative Risk Management Methods, Techniques and Tools TONY MILSOM Specialist Risk Engineering KPC w w w. k u w a i t e r m. c o m KPC ERM Objectives: Three key objectives of KPC

www.kuwaiterm.com Quantitative Risk Management Methods, Techniques and Tools TONY MILSOM Specialist Risk Engineering KPC w w w. k u w a i t e r m. c o m KPC ERM Objectives: Three key objectives of KPC

APPENDIX G. Guidelines for Impact Analysis for CCBFC Committees. Definitions. General Issues

APPENDIX G Guidelines for Impact Analysis for CCBFC Committees This document presents 21 guiding principles for the preparation of impact analyses supporting proposed code changes. It is intended to be

APPENDIX G Guidelines for Impact Analysis for CCBFC Committees This document presents 21 guiding principles for the preparation of impact analyses supporting proposed code changes. It is intended to be

SOCIETY OF ACTUARIES Enterprise Risk Management Investment Extension Exam ERM-INV

SOCIETY OF ACTUARIES Exam ERM-INV Date: Tuesday, October 31, 2017 Time: 8:30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 80 points. This exam consists

SOCIETY OF ACTUARIES Exam ERM-INV Date: Tuesday, October 31, 2017 Time: 8:30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 80 points. This exam consists

Date: Tuesday, October 30, 2018 Time: 8:30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES. Recognized by the Canadian Institute of Actuaries.

Enterprise Risk Management Retirement Benefits Extension Exam ERM-RET Date: Tuesday, October 30, 2018 Time: 8:30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has

Enterprise Risk Management Retirement Benefits Extension Exam ERM-RET Date: Tuesday, October 30, 2018 Time: 8:30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has

CA. Sonali Jagath Prasad ACA, ACMA, CGMA, B.Com.

MANAGEMENT OF FINANCIAL RESOURCES AND PERFORMANCE SESSIONS 3& 4 INVESTMENT APPRAISAL METHODS June 10 to 24, 2013 CA. Sonali Jagath Prasad ACA, ACMA, CGMA, B.Com. WESTFORD 2008 Thomson SCHOOL South-Western

MANAGEMENT OF FINANCIAL RESOURCES AND PERFORMANCE SESSIONS 3& 4 INVESTMENT APPRAISAL METHODS June 10 to 24, 2013 CA. Sonali Jagath Prasad ACA, ACMA, CGMA, B.Com. WESTFORD 2008 Thomson SCHOOL South-Western

Exam ERM-ILA. Date: Tuesday, October 30, 2018 Time: 8:30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES

Enterprise Risk Management Individual Life & Annuities Extension Exam ERM-ILA Date: Tuesday, October 30, 2018 Time: 8:30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination

Enterprise Risk Management Individual Life & Annuities Extension Exam ERM-ILA Date: Tuesday, October 30, 2018 Time: 8:30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination

A GUIDE TO UNDERSTANDING, COMMUNICATING, AND INFLUENCING ACTUARIAL RESULTS

A GUIDE TO UNDERSTANDING, COMMUNICATING, AND INFLUENCING ACTUARIAL RESULTS FEBRUARY 9, 2017 Jennifer Price, FCAS, MAAA Amanda Marsh, FCAS, MAAA 2017 Atlanta RIMS Educational Conference Introduction What

A GUIDE TO UNDERSTANDING, COMMUNICATING, AND INFLUENCING ACTUARIAL RESULTS FEBRUARY 9, 2017 Jennifer Price, FCAS, MAAA Amanda Marsh, FCAS, MAAA 2017 Atlanta RIMS Educational Conference Introduction What

Application of ERM to Private Pension

Application of ERM to Private Pension Katsuhiro Yagura Certified Pension Actuary Fellow of the Institute of Actuaries of Japan Session Number: WBR10 Contents 1. Private Pension 2 2. ERM 10 3. Case Studies

Application of ERM to Private Pension Katsuhiro Yagura Certified Pension Actuary Fellow of the Institute of Actuaries of Japan Session Number: WBR10 Contents 1. Private Pension 2 2. ERM 10 3. Case Studies

THE ROLE OF THE BOARD IN RISK MANAGEMENT

Financial Services THE ROLE OF THE BOARD IN RISK MANAGEMENT PERSPECTIVES FOR INDIAN FINANCIAL INSTITUTIONS AUTHORS David Bergeron Michelle Daisley INTRODUCTION The global financial crisis has exposed deep

Financial Services THE ROLE OF THE BOARD IN RISK MANAGEMENT PERSPECTIVES FOR INDIAN FINANCIAL INSTITUTIONS AUTHORS David Bergeron Michelle Daisley INTRODUCTION The global financial crisis has exposed deep

In physics and engineering education, Fermi problems

A THOUGHT ON FERMI PROBLEMS FOR ACTUARIES By Runhuan Feng In physics and engineering education, Fermi problems are named after the physicist Enrico Fermi who was known for his ability to make good approximate

A THOUGHT ON FERMI PROBLEMS FOR ACTUARIES By Runhuan Feng In physics and engineering education, Fermi problems are named after the physicist Enrico Fermi who was known for his ability to make good approximate

Solvency II. Building an internal model in the Solvency II context. Montreal September 2010

Solvency II Building an internal model in the Solvency II context Montreal September 2010 Agenda 1 Putting figures on insurance risks (Pillar I) 2 Embedding the internal model into Solvency II framework

Solvency II Building an internal model in the Solvency II context Montreal September 2010 Agenda 1 Putting figures on insurance risks (Pillar I) 2 Embedding the internal model into Solvency II framework

WORK INJURY GUIDE WELLS LAW A PROFESSIONAL CORPORATION. WORKERS COMPENSATION Humboldt / Del Norte Counties

WORK INJURY GUIDE WELLS LAW A PROFESSIONAL CORPORATION WORKERS COMPENSATION www.wellswellslaw.com 707-532-4344 Humboldt / Del Norte Counties 530-433-4747 Lassen / Plumas Counties W. HOWARD WELLS*, ATTORNEY

WORK INJURY GUIDE WELLS LAW A PROFESSIONAL CORPORATION WORKERS COMPENSATION www.wellswellslaw.com 707-532-4344 Humboldt / Del Norte Counties 530-433-4747 Lassen / Plumas Counties W. HOWARD WELLS*, ATTORNEY

LICAT Overview. December 1 st, Jacques Tremblay, FCIA, FSA, MAAA

LICAT Overview December 1 st, 2017 Jacques Tremblay, FCIA, FSA, MAAA 1. Introduction Choosing a risk based capital framework Will the new LICAT fit the bill for Caribbean regulators? Versions of MCCSR

LICAT Overview December 1 st, 2017 Jacques Tremblay, FCIA, FSA, MAAA 1. Introduction Choosing a risk based capital framework Will the new LICAT fit the bill for Caribbean regulators? Versions of MCCSR

ROI CASE STUDY SPSS INFINITY PROPERTY & CASUALTY

ROI CASE STUDY SPSS INFINITY PROPERTY & CASUALTY THE BOTTOM LINE Infinity Property & Casualty Corporation (IPACC) deployed SPSS to reduce its payments on fraudulent claims and improve its ability to collect

ROI CASE STUDY SPSS INFINITY PROPERTY & CASUALTY THE BOTTOM LINE Infinity Property & Casualty Corporation (IPACC) deployed SPSS to reduce its payments on fraudulent claims and improve its ability to collect

Enterprise Risk Management (ERM)

") Southeastern Actuaries Conference Enterprise Risk Management (ERM) November 16, 2007 ING. Your future. Made easier. Agenda ERM Are you doing it? Definition of ERM What is it? Industry Overview What is

Southeastern Actuaries Conference Enterprise Risk Management (ERM) November 16, 2007 ING. Your future. Made easier. Agenda ERM Are you doing it? Definition of ERM What is it? Industry Overview What is

Subject SP2 Life Insurance Specialist Principles Syllabus

Subject SP2 Life Insurance Specialist Principles Syllabus for the 2019 exams 1 June 2018 Life Insurance Principles Aim The aim of the Life Insurance Principles subject is to instil in successful candidates

Subject SP2 Life Insurance Specialist Principles Syllabus for the 2019 exams 1 June 2018 Life Insurance Principles Aim The aim of the Life Insurance Principles subject is to instil in successful candidates

POLICY NUMBER: POL 136

Chapter: FINANCE AND ADMINISTRATION Subject: FUNDING POLICY Effective Date: August 6, 2007 Last Update: August 30, 2018 PURPOSE STATEMENT: The purpose of this policy is to explain how the Workers Compensation

Chapter: FINANCE AND ADMINISTRATION Subject: FUNDING POLICY Effective Date: August 6, 2007 Last Update: August 30, 2018 PURPOSE STATEMENT: The purpose of this policy is to explain how the Workers Compensation

ERM-RET Model Solutions Fall 2017

ERM-RET Model Solutions Fall 2017 1. Learning Objectives: 2. The candidate will understand the concepts of risk modeling and be able to evaluate and understand the importance of risk models. 5. The candidate

ERM-RET Model Solutions Fall 2017 1. Learning Objectives: 2. The candidate will understand the concepts of risk modeling and be able to evaluate and understand the importance of risk models. 5. The candidate

Measuring Retirement Plan Effectiveness

T. Rowe Price Measuring Retirement Plan Effectiveness T. Rowe Price Plan Meter helps sponsors assess and improve plan performance Retirement Insights Once considered ancillary to defined benefit (DB) pension

T. Rowe Price Measuring Retirement Plan Effectiveness T. Rowe Price Plan Meter helps sponsors assess and improve plan performance Retirement Insights Once considered ancillary to defined benefit (DB) pension

THE SMART WAY TO ANALYSE YOUR RISKS. DAVID STEBBING Partner, Willis Risk & Analytics

THE SMART WAY TO ANALYSE YOUR RISKS DAVID STEBBING Partner, Willis Risk & Analytics Increasing risks and challenges Commodity market volatility Short-term cashflow planning Profitability of longterm investments

THE SMART WAY TO ANALYSE YOUR RISKS DAVID STEBBING Partner, Willis Risk & Analytics Increasing risks and challenges Commodity market volatility Short-term cashflow planning Profitability of longterm investments

MARSH CAPTIVE SOLUTIONS

MARSH CAPTIVE SOLUTIONS Face a New World of Risk On Your Terms Fluctuating market conditions, unstable regulatory environments, and global economic shifts affect your day-to-day operations and your bottom

MARSH CAPTIVE SOLUTIONS Face a New World of Risk On Your Terms Fluctuating market conditions, unstable regulatory environments, and global economic shifts affect your day-to-day operations and your bottom

DORINCO REINSURANCE COMPANY NAIC GROUP CODE 0000 NAIC COMPANY CODE 33499

DORINCO REINSURANCE COMPANY NAIC GROUP CODE 0000 NAIC COMPANY CODE 33499 MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS - 2015 1. Overview This discussion provides

DORINCO REINSURANCE COMPANY NAIC GROUP CODE 0000 NAIC COMPANY CODE 33499 MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS - 2015 1. Overview This discussion provides

Retirement. Optimal Asset Allocation in Retirement: A Downside Risk Perspective. JUne W. Van Harlow, Ph.D., CFA Director of Research ABSTRACT

Putnam Institute JUne 2011 Optimal Asset Allocation in : A Downside Perspective W. Van Harlow, Ph.D., CFA Director of Research ABSTRACT Once an individual has retired, asset allocation becomes a critical

Putnam Institute JUne 2011 Optimal Asset Allocation in : A Downside Perspective W. Van Harlow, Ph.D., CFA Director of Research ABSTRACT Once an individual has retired, asset allocation becomes a critical

MEMORANDUM. To: From: Metrolinx Board of Directors Robert Siddall Chief Financial Officer Date: September 14, 2017 ERM Policy and Framework

MEMORANDUM To: From: Metrolinx Board of Directors Robert Siddall Chief Financial Officer Date: September 14, 2017 Re: ERM Policy and Framework Executive Summary Attached are the draft Enterprise Risk Management

MEMORANDUM To: From: Metrolinx Board of Directors Robert Siddall Chief Financial Officer Date: September 14, 2017 Re: ERM Policy and Framework Executive Summary Attached are the draft Enterprise Risk Management

Enterprise risk management: How are companies gaining value from their ERM strategies?

Milliman Preliminary results The inaugural survey from the Milliman Risk Institute Enterprise risk management: How are companies gaining value from their ERM strategies? Preliminary results Milliman is

Milliman Preliminary results The inaugural survey from the Milliman Risk Institute Enterprise risk management: How are companies gaining value from their ERM strategies? Preliminary results Milliman is

Strategies for Controlling your Cost of Risk

Strategies for Controlling your Cost of Risk 1 controlling cost of risk is a learning process 2 which direction will you go to control your cost of risk 3 understanding your industry is crucial to creating

Strategies for Controlling your Cost of Risk 1 controlling cost of risk is a learning process 2 which direction will you go to control your cost of risk 3 understanding your industry is crucial to creating

Controlling Costs Through Proactive Claims Management

Controlling Costs Through Proactive Claims Management It s no secret that rising medical costs are a serious issue affecting businesses today. Although medical costs associated with healthcare insurance

Controlling Costs Through Proactive Claims Management It s no secret that rising medical costs are a serious issue affecting businesses today. Although medical costs associated with healthcare insurance

Classification of Contracts under International Financial Reporting Standards

Educational Note Classification of Contracts under International Financial Reporting Standards Practice Council June 2009 Document 209066 Ce document est disponible en français 2009 Canadian Institute

Educational Note Classification of Contracts under International Financial Reporting Standards Practice Council June 2009 Document 209066 Ce document est disponible en français 2009 Canadian Institute

Pathfinder Insurance for Robinson Helicopters How Does It Compare to Traditional Placements? By Jeff Rhodes

Pathfinder Insurance for Robinson Helicopters How Does It Compare to Traditional Placements? By Jeff Rhodes Robinson Helicopter Co. has become the leading manufacturer of civil helicopters in the world.

Pathfinder Insurance for Robinson Helicopters How Does It Compare to Traditional Placements? By Jeff Rhodes Robinson Helicopter Co. has become the leading manufacturer of civil helicopters in the world.

Session 61, Overview of Embedded Value. Moderator: Zeeshan Ramzan Ali Rehmani, FSA, MAAA. Presenter: David Lawrence White, Jr.

Session 61, Overview of Embedded Value Moderator: Zeeshan Ramzan Ali Rehmani, FSA, MAAA Presenter: David Lawrence White, Jr., FSA, MAAA Overview of Embedded Value David White, FSA, MAAA KPMG LLP Zeeshan

Session 61, Overview of Embedded Value Moderator: Zeeshan Ramzan Ali Rehmani, FSA, MAAA Presenter: David Lawrence White, Jr., FSA, MAAA Overview of Embedded Value David White, FSA, MAAA KPMG LLP Zeeshan

Years ended December 31, 2017 and 2016 with Report of Independent Auditors

Audited Financial Statements Years ended December 31, 2017 and 2016 with Report of Independent Auditors Audited Financial Statements Years ended December 31, 2017 and 2016 Contents Report of Independent

Audited Financial Statements Years ended December 31, 2017 and 2016 with Report of Independent Auditors Audited Financial Statements Years ended December 31, 2017 and 2016 Contents Report of Independent

Managing your portfolio liability using effective monitoring to change outcomes

Managing your portfolio liability using effective monitoring to change outcomes Prepared by Richard Brookes, Kris Bruckner and David Wright Presented to the Institute of Actuaries of Australia Accident

Managing your portfolio liability using effective monitoring to change outcomes Prepared by Richard Brookes, Kris Bruckner and David Wright Presented to the Institute of Actuaries of Australia Accident

CONTROL COSTS Aastha Trehan, Ritika Grover, Prateek Puri Dronacharya College Of Engineering, Gurgaon

CONTROL COSTS Aastha Trehan, Ritika Grover, Prateek Puri Dronacharya College Of Engineering, Gurgaon Abstract- Project Cost Management includes the processes involved in planning, estimating, budgeting,

CONTROL COSTS Aastha Trehan, Ritika Grover, Prateek Puri Dronacharya College Of Engineering, Gurgaon Abstract- Project Cost Management includes the processes involved in planning, estimating, budgeting,

Demystifying Operational Risk

Demystifying Operational Risk USA 2007 A Comprehensive Two-Day Interactive Seminar Led by Ali Samad-Khan, President, OpRisk Advisory and Special Guest Speaker, Jan Voigts, Federal Reserve Bank of New York

Demystifying Operational Risk USA 2007 A Comprehensive Two-Day Interactive Seminar Led by Ali Samad-Khan, President, OpRisk Advisory and Special Guest Speaker, Jan Voigts, Federal Reserve Bank of New York

11 th Global Conference of Actuaries

CONSTANT PROPORTION PORTFOLIO INSURANCE (CPPI) FOR IMPLEMENTATION OF DYNAMIC ASSET ALLOCATION OF IMMEDIATE ANNUITIES By - Saurabh Khanna 1. Introduction In this paper, we present a strategy of managing

CONSTANT PROPORTION PORTFOLIO INSURANCE (CPPI) FOR IMPLEMENTATION OF DYNAMIC ASSET ALLOCATION OF IMMEDIATE ANNUITIES By - Saurabh Khanna 1. Introduction In this paper, we present a strategy of managing

Exam ERM-GC. Date: Tuesday, October 30, 2018 Time: 8:30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES. Recognized by the Canadian Institute of Actuaries.

Enterprise Risk Management General Corporate ERM Extension Exam ERM-GC Date: Tuesday, October 30, 2018 Time: 8:30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has

Enterprise Risk Management General Corporate ERM Extension Exam ERM-GC Date: Tuesday, October 30, 2018 Time: 8:30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has

What Does a Risk Manager Do? By Keith Wentz, Risk Management and Underwriting Manager, CCAP

What Does a Risk Manager Do? By Keith Wentz, Risk Management and Underwriting Manager, CCAP What is special about risk management in the public sector? Well, this article will provide answers to that question.

What Does a Risk Manager Do? By Keith Wentz, Risk Management and Underwriting Manager, CCAP What is special about risk management in the public sector? Well, this article will provide answers to that question.

Functional document: Asset allocation: plan level, goal level, and scenario level NaviPlan Premium Level 1 R

Functional document: Asset allocation: plan level, goal level, and scenario level NaviPlan Premium Level 1 R Level 2 R functions addressed in this document: How does NaviPlan determine the investor profile

Functional document: Asset allocation: plan level, goal level, and scenario level NaviPlan Premium Level 1 R Level 2 R functions addressed in this document: How does NaviPlan determine the investor profile

EXCELLENCE IN RISK MANAGEMENT XIII Emerging Risks: Anticipating Threats and Opportunities Around the Corner

EXCELLENCE IN RISK MANAGEMENT XIII Emerging Risks: Anticipating Threats and Opportunities Around the Corner World Economic Forum Global Risks 2016 1 Key Themes Definitions Assessing and Modeling Emerging

EXCELLENCE IN RISK MANAGEMENT XIII Emerging Risks: Anticipating Threats and Opportunities Around the Corner World Economic Forum Global Risks 2016 1 Key Themes Definitions Assessing and Modeling Emerging

RECOGNITION OF GOVERNMENT PENSION OBLIGATIONS

RECOGNITION OF GOVERNMENT PENSION OBLIGATIONS Preface By Brian Donaghue 1 This paper addresses the recognition of obligations arising from retirement pension schemes, other than those relating to employee

RECOGNITION OF GOVERNMENT PENSION OBLIGATIONS Preface By Brian Donaghue 1 This paper addresses the recognition of obligations arising from retirement pension schemes, other than those relating to employee

How Do You Measure Which Retirement Income Strategy Is Best?

How Do You Measure Which Retirement Income Strategy Is Best? April 19, 2016 by Michael Kitces Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those

How Do You Measure Which Retirement Income Strategy Is Best? April 19, 2016 by Michael Kitces Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those

The Evolution of ALM in Asia. Some Food For Thought. Mark Saunders, FIA, FASI, FSA

The Evolution of ALM in Asia Some Food For Thought Mark Saunders, FIA, FASI, FSA Principal & Managing Director, Asia Tillinghast Financial Services Business Leader, Asia-Pacific June and July 2005 Joint

The Evolution of ALM in Asia Some Food For Thought Mark Saunders, FIA, FASI, FSA Principal & Managing Director, Asia Tillinghast Financial Services Business Leader, Asia-Pacific June and July 2005 Joint

Subject CP1 Actuarial Practice Core Practices Syllabus

Subject CP1 Actuarial Practice Core Practices Syllabus for the 2019 exams 1 June 2018 Actuarial Practice Aim The aim of the Actuarial Practice subject is to use the technical and business skills learnt

Subject CP1 Actuarial Practice Core Practices Syllabus for the 2019 exams 1 June 2018 Actuarial Practice Aim The aim of the Actuarial Practice subject is to use the technical and business skills learnt

Reinsurance Optimization The Theoretical and Practical Aspects Subhash Chandra Aon Benfield

1 st Capacity Building Seminar Reinsurance Optimization The Theoretical and Practical Aspects Subhash Chandra Aon Benfield Indian Actuarial Profession Serving the Cause of Public Interest 9 th August 2014

1 st Capacity Building Seminar Reinsurance Optimization The Theoretical and Practical Aspects Subhash Chandra Aon Benfield Indian Actuarial Profession Serving the Cause of Public Interest 9 th August 2014

Fundamentals of Project Risk Management

Fundamentals of Project Risk Management Introduction Change is a reality of projects and their environment. Uncertainty and Risk are two elements of the changing environment and due to their impact on

Fundamentals of Project Risk Management Introduction Change is a reality of projects and their environment. Uncertainty and Risk are two elements of the changing environment and due to their impact on

Working Toward Retirement. Building Your Nest Egg: For 1199SEIU Members

Working Toward Retirement Building Your Nest Egg: For 1199SEIU Members Objectives Demonstrate the benefit of starting early (but it s never too late!) Discuss the three-legged stool of retirement (Pension,

Working Toward Retirement Building Your Nest Egg: For 1199SEIU Members Objectives Demonstrate the benefit of starting early (but it s never too late!) Discuss the three-legged stool of retirement (Pension,

LAURENTIDE INSURANCE AND MORTGAGE COMPANY LIMITED 2013 AUDITED FINANCIAL STATEMENTS

LAURENTIDE INSURANCE AND MORTGAGE COMPANY LIMITED 2013 AUDITED FINANCIAL STATEMENTS INDEPENDENT AUDITORS REPORT To the Shareholder of Laurentide Insurance and Mortgage Company Limited: Deloitte & Touche

LAURENTIDE INSURANCE AND MORTGAGE COMPANY LIMITED 2013 AUDITED FINANCIAL STATEMENTS INDEPENDENT AUDITORS REPORT To the Shareholder of Laurentide Insurance and Mortgage Company Limited: Deloitte & Touche

Guidelines for loss reserves. in non-life insurance. Version from August 2006 Approved by the SAA Committee from 1 September 2006.

Guidelines for loss reserves in non-life insurance Version from August 2006 Approved by the SAA Committee from 1 September 2006 Seite 1 1. Object These Guidelines for loss reserves in non-life insurance

Guidelines for loss reserves in non-life insurance Version from August 2006 Approved by the SAA Committee from 1 September 2006 Seite 1 1. Object These Guidelines for loss reserves in non-life insurance

Financial Policies & Procedures for Non-Profit Organizations

Financial Policies & Procedures for Non-Profit Organizations Jefferson A. Holt Presenter Date Mission of Pro Bono Partnership of Atlanta: To maximize the impact of pro bono engagement by connecting a network

Financial Policies & Procedures for Non-Profit Organizations Jefferson A. Holt Presenter Date Mission of Pro Bono Partnership of Atlanta: To maximize the impact of pro bono engagement by connecting a network

MANAGING WORKERS COMPENSATION CLAIMS AND INVESTIGATIONS

MANAGING WORKERS COMPENSATION CLAIMS AND INVESTIGATIONS MANAGING WORKERS COMPENSATION CLAIMS AND INVESTIGATIONS AGENDA: Real Life Scenario Have a Workers Compensation Policy Provide Training to all employees

MANAGING WORKERS COMPENSATION CLAIMS AND INVESTIGATIONS MANAGING WORKERS COMPENSATION CLAIMS AND INVESTIGATIONS AGENDA: Real Life Scenario Have a Workers Compensation Policy Provide Training to all employees

RISK MANAGEMENT STANDARDS FOR P5M

Journal of Engineering Science and Technology Vol. 13, No. 1 (2018) 011-034 School of Engineering, Taylor s University RISK MANAGEMENT STANDARDS FOR P5M PETR ŘEHÁČEK Department of Systems Engineering,

Journal of Engineering Science and Technology Vol. 13, No. 1 (2018) 011-034 School of Engineering, Taylor s University RISK MANAGEMENT STANDARDS FOR P5M PETR ŘEHÁČEK Department of Systems Engineering,

Algorithmic Trading Session 10 Performance Analysis I Performance Measurement. Oliver Steinki, CFA, FRM

Algorithmic Trading Session 10 Performance Analysis I Performance Measurement Oliver Steinki, CFA, FRM Outline Introduction Arithmetic vs. Geometric Mean Why Dollars are More Important Than Percentages

Algorithmic Trading Session 10 Performance Analysis I Performance Measurement Oliver Steinki, CFA, FRM Outline Introduction Arithmetic vs. Geometric Mean Why Dollars are More Important Than Percentages

1. Define risk. Which are the various types of risk?

1. Define risk. Which are the various types of risk? Risk, is an integral part of the economic scenario, and can be termed as a potential event that can have opportunities that benefit or a hazard to an

1. Define risk. Which are the various types of risk? Risk, is an integral part of the economic scenario, and can be termed as a potential event that can have opportunities that benefit or a hazard to an

GIIRR Model Solutions Fall 2015

GIIRR Model Solutions Fall 2015 1. Learning Objectives: 1. The candidate will understand the key considerations for general insurance actuarial analysis. Learning Outcomes: (1k) Estimate written, earned

GIIRR Model Solutions Fall 2015 1. Learning Objectives: 1. The candidate will understand the key considerations for general insurance actuarial analysis. Learning Outcomes: (1k) Estimate written, earned

Information Security Risk Management

Information Security Risk Management Based on ISO/IEC 17799 Houman Sadeghi Kaji Spread Spectrum Communication System PhD., Cisco Certified Network Professional Security Specialist BS7799 LA info@houmankaji.net

Information Security Risk Management Based on ISO/IEC 17799 Houman Sadeghi Kaji Spread Spectrum Communication System PhD., Cisco Certified Network Professional Security Specialist BS7799 LA info@houmankaji.net