THE ECONOMICS OF BANK CAPITAL

|

|

|

- Ginger Paul

- 5 years ago

- Views:

Transcription

1 THE ECONOMICS OF BANK CAPITAL Edoardo Gaffeo Department of Economics and Management University of Trento

2 OUTLINE What we are talking about, and why Banks are «special», and their capital is «special» as well Skin in the game Braking distance to avoid a crash Capital requirements as VaR Perverse regulation? The drivers of endogenous risk The risk-taking channel of monetary policy What have we learned? Edoardo Gaffeo INET YSI Trento, june 3 rd 2017

3 CAPITAL WHAT? Assets Total Assets (A) Low-risk assets (A1) High-risk assets (A2) Deposits (D) Non-core liabilities (B) Capital (C) Tier 1 Equity (E) Tier 2 Hybrid instruments (H) Liabilities Edoardo Gaffeo INET YSI Trento, june 3 rd 2017

4 CAPITAL WHAT? Capital adequacy ratio = + Φ Φ = minimum CAR specified in RW banking regulation Leverage ratio = Δ = minimum LR specified in banking regulation (from 2018) Edoardo Gaffeo INET YSI Trento, june 3 rd 2017

5 A HOT RESEARCH TOPIC Google Scholar items found per year searching for «bank capital» Edoardo Gaffeo INET YSI Trento, june 3 rd 2017

3. Contagion (green) 4.")

6 THAT SPURS A LOT OF RESEARCH IN SEVERAL AREAS Benoit et al. (2017) Survey of 220 papers on: 1. Systemic risk-taking (blue) 2. Amplification mechanisms (red) 3. Contagion (green) 4. Systemic risk measures (yellow) Edoardo Gaffeo INET YSI Trento, june 3 rd 2017

7 BANKS ARE «SPECIAL»

8 RECAPITALIZATION: A TRANSATLANTIC VIEW

9 CAPITAL REQUIREMENTS

10 HOW DOES BANK CAPITAL RELATE TO RISK?

11 A TOUGH THEORETICAL ISSUE Key point: banks optimal capital structure is strictly related to the theory of financial intermediation: Why do banks exists? In the presence of transaction costs (e.g., asymmetric information), FIs increase social welfare by providing QAT services: Maturity transformation Liquidity transformation Volume transformation Risk pooling In classical theories of FI, none role for capital!

12 BANKS AS DELEGATED MONITORS Diamond (1984): investment projects of a larger scale than individual savings, and project cash flows unobservable to investors. Information can be retrieved by costly ex-post auditing (costly state verification), or a pre-commitment to pay a fixed amount (D) with a non-pecuniary penalty (P) in case of default. A bank acts a filter: it audits projects on behalf of investors, and pre-commits to repay them a fixed amount D with a penalty P for default. The latter is equivalent to a demand deposit contract. Due to the LLN, intermediation is Pareto improving if the bank is large enough, so that its probability of default goes to zero and deposits are riskless.

13 BANKS AS LIQUIDITY INSURERS Diamond and Dybvig (1983): investment projects can be of two types: i) an asset that matures in the long-run, but interim liquidation comes with a cost (illiquidity); ii) a short-run asset. Risk-averse investors can be of two types: i) early or ii) late. Type is i.i.d. and private information (shock), while in the aggregate fractions are public information (LLN). As long as shocks are not perfectly correlated across individuals, banks may efficiently invest savings on long-term projects, providing depositors with insurance against idiosyncratic consumption shocks.

14 BANKS AS LIQUIDITY INSURERS The game has a second (bad) Nash equilibrium. If depositors believe that only early consumers withdraw in t = 1, the bank can satisfy both early and late depositors by exploiting the law of large numbers. If depositors hold different beliefs, however, the bank can be subject to a run and forced to bankruptcy. Remedies: find an institutional arrangement preserving the good equilibrium but suppressing the bad one. Example: deposit insurance.

15 A ROLE FOR CAPITAL Why does bank capital play none role in these theories? Delegated monitoring: perfect diversification. Liquidity provision: deposit insurance affects incentives to take risk, but the issue is neglected. Different rationales for bank capital.

16 BANK CAPITAL IN THE MONITORING-THE-MONITOR PROBLEM Holstrom and Tirole (1997): moral hazard generates limited pledgeability and borrowing constraints. Firms are endowed with net worth N and want to invest I > N. They can choose between direct and bank financing: Direct financing does not monitor: cheap but low pledgeability. Bank financing monitors: increases pledgeability at some cost. Each firm can privately choose one of three projects: Good Bad 1 Bad 2 Private benefits 0 b B with B > b > 0 Prob. success p H p L p L with p H > p L socially efficient

17 BANK CAPITAL IN THE MONITORING-THE-MONITOR PROBLEM Bank monitoring can prevent choice of Bad 1, but not of Bad 2 (social inefficiency). Firm capital acts as a signal: skin in the game. Firms need to have at least N bank to make it IC to choose Good instead of Bad 1, assuming banks monitor. Firms need to have at least N direct > N bank to make it IC to choose Good when approaching direct financing. But bank monitoring is only privately observable. Banks must hold enough capital to make it IC for them to monitor. Banks exist only if they have equity capital. In this case, they allow a larger amount of investment (Pareto improvement).

18 BANK CAPITAL IN THE MONITORING-THE-MONITOR PROBLEM Several implications: Capital in firms and capital in banks play complementary roles. High enough capital in banks expand firms debt capacity, as bank loans makes direct financing cheaper (banks and markets are complements). A negative shock to bank capital causes a credit crunch and an increase of the cost of external finance for firms. Poorly capitalized firms are affected the most.

19 EXCESSIVE RISK TAKING Merton (1977): deposit insurance as a put option. In DD (1983), the cash flow distribution of investments is given. What if the bank can make unobservable project choices with different riskiness after deposits are received? Incentive for banks to take the riskiest project, if this carries higher repayments to the bank. Risk-taking can be tamed if depositors discipline bank managers by threatening withdrawal as they receive adverse information on the amount of risk the bank is taking. Deposit insurance reduces incentives for information acquisition and control by depositors. Regulatory restrictions is necessary to limit risk taking: capital requirements.

20 A COMPLEX DANCE Bank capital affects the quality of assets, monitoring efforts, distribution of cash flows. Capital requirements are needed to restrain the appetite for risk. They act as a lower bound: once you bang against it it s too late. Shareholders might be expropriated even if their stake is still positive. The (excess-)capital buffer is an endogenous variable. Risk management is valuable (Froot and Stein, 1998). Bank risk management takes the form of VaR (Adrian and Shin, 2007).

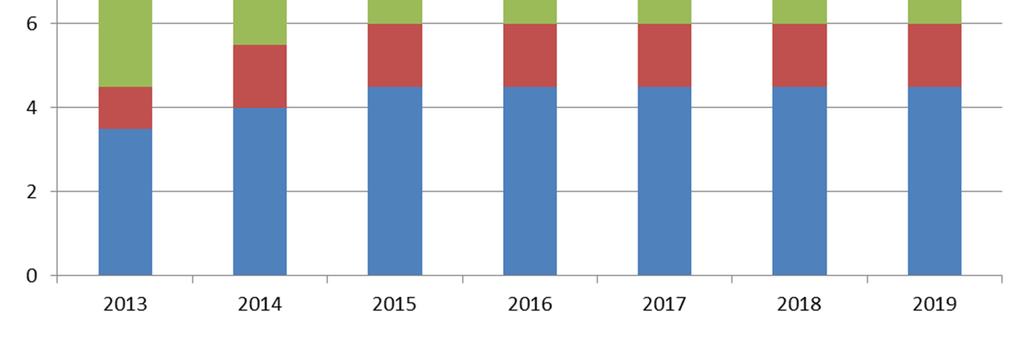

21 THE HISTORICAL EXPERIENCE Jorda et al. (2017). Composition of liabilities for the banking sector, averages by year for 17 countries.

22 THE HISTORICAL EXPERIENCE The capital ratio provides virtually no information about the probability of a systemic financial crisis. Loan growth (asset side of the balance sheet) is the single most useful indicator of financial crisis risk among several other potential predictors (Schularick and Taylor, 2012). The amount of bank capital affects the cost of a crisis: a more highly levered financial sector at the start of a financial-crisis recession is associated with slower subsequent output growth and a significantly weaker cyclical recovery. Do we have a theory of bank capital explaining these stylized facts?

23 BASEL-BASED CAPITAL REQUIREMENTS The regulator sets a probability of solvency α (ex. α = 99.9%). A default occurs whenever the value of losses is larger than equity. Let x i the exposure to obligor i, and u i the random loss (in excess of that provisioned). Thus, the total portfolio loss of n different assets is = #! "!!$. For given capital K, bankruptcy occurs when L > K.

24 BASEL-BASED CAPITAL REQUIREMENTS The same as setting a loss ratio l = & ) (*+ ' ( larger than, = - Prudential regulation imposes a level of capital K such that./01 l, = 1 4. ) (*+ ' ( In a perfectly diversified portfolio with uncorrelated credit risk, the LLN implies that the required capital is zero. Capital requirements are concerned with correlated risks and imperfect diversification..

25 MANAGING RISK IN BANKS

26 BANK CAPITAL AS A VAR PROBLEM Banks assess the risk to which they are exposed by recurring to statistical calculations measuring the Value-at-Risk (VaR) of their assets as returns vary. The urge to action coming from price movements generates an externality: in an attempt to mitigate its own risk exposure, a bank contributes to spread the risk all over the financial system. Systemic risk is endogenous: price changes and balance-sheet adjustments reinforce each other to amplify small shocks.

27 BANK CAPITAL UNDER A VAR CONSTRAINT A two-period economy, (t, t + 1) An investor decides an asset allocation by choosing between: an amount y t of risky security, which costs p t cash, c t The price of the risky security at time (t + 1) is 5 67 = 1+/ where/ 67 is the outcome of a stochastic process, with /9 67 ~ ;;< Ω >,@, µ > 0

28 BANK CAPITAL AS A VAR PROBLEM The investor has an initial capital endowment e t. The time t balance sheet is p t y t + c t = e t, and it is consistent with either short or long positions on the risky security. For a Leveraged investor (i.e., a financial intermediary) Assets Liabilities Securities p t y t Equity e t Debt c t The leverage is 6 = A BC B D B.

29 BANK CAPITAL UNDER A VAR CONSTRAINT Let α be the VaRconfidence level, so that (1 - α) represents the maximum probability to go bankrupt the following period. Bankruptcy occurs whenever e t+1 0, occurring if: that is / E 6 +F 6 0 /9 67 F E 6

30 BANK CAPITAL UNDER A VAR CONSTRAINT Define φ as a constant such that./01 / 67 > I@ = 1 4 φσ is the VaR associated to the stochastic return/ 67 at the confidence level α, when the expected return is µ. The problem is that of choosing an asset allocation with an amount of risky asset y such that the probability to become insolvent at time (t + 1) is not higher that (1 - α).

31 BANK CAPITAL UNDER A VAR CONSTRAINT The probability of insolvency is exactly equal to (1 - α) when: that is F E 6 = > I@ >+ F E 6 = I@ Given the initial position in equity (e t ), the expected return on the risky asset (µ), its riskiness (σ) and the acceptable threshold for risk (φ), this identifies the total amount of risky asset to be held in the portfolio.

32 BANK CAPITAL UNDER A VAR CONSTRAINT Interesting implication. Desired leverage is equal to: = 5 6E 6 F 6 = F 6 I@ > 1 F 6 = 1 I@ > that is a constant L = L (φ, σ, µ ) +

33 BANK CAPITAL UNDER A VAR CONSTRAINT Adrian and Shin (2010): If the price of the risky asset varies, a bank using a VaR approach in asset allocation wants to keep the leverage constant («leverage targeting»). The demand curve for a risky asset has a positive slope (demand more asset when its price increases), while the supply curve has a negative slope (sell assets if the price decreases). This is a precondition for the amplification of shocks at a systemic level.

34 SIONS BANK CAPITAL UNDER A VAR CONSTRAINT Assets Liabilities Securities py Equity e Debt py e i) Initial balance-sheet ii) After a price increase iii) After the adjustment Mark-to-market higher value Increase in equity Equity Equity Equity Assets Debt Assets Debt Assets Debt New purchases of securities New borrowing Edoardo Gaffeo Lecture notes set #2

35 BANK CAPITAL UNDER A VAR CONSTRAINT

36 PRO-CYCLICAL LEVERAGE? Recall that leverage is: = 5 6E 6 F 6 = 1 I@ > where φσ is the value at risk per euro of assets (unit VaR). Leverage is pro-cyclical if the unit VaR is counter-cyclical (Adrian and Shin, 2014).

37 THE RECENT EXPERIENCE Goel et al. (2014). Leverage for U.S. commercial and investment banks.

38 SYSTEMIC LEVERAGE MARK I Banks engage in highly correlated high leverage choices due to strategic complementarities (Aikman et al., 2015; Vives, 2014). Acharya and Yorumalzer (2007): when the number of bank failures is large, the regulator finds it ex-post optimal to bail them out ( too many to fail ). This gives banks incentives to herd and increases the risk that many banks may fail together. Farhi and Tirole (2012): private leverage choices depend on the anticipated policy reaction to the overall maturity mismatch. Since policy instruments are only imperfectly targeted to the institutions they try to rescue, it is profitable for a bank to adopt a risky balance sheet when others are doing the same.

39 SYSTEMIC LEVERAGE MARK II Systemic leverage increases as a response to monetary policy: bank risk-based channel of monetary transmission (Borio and Zhu, 2008; Dell Ariccia et al., 2014). Policy (risk-free) rates affect bank risk taking depending on how banks are able to pass policy changes onto lending rates (passthrough effect), and on how they optimally adjust their capital structure in response to such changes (leverage effect).

40 SYSTEMIC LEVERAGE MARK II Lower risk-free real interest rates imply a reduction of interest rates on bank loans. This reduces the bank s gross return conditional on its portfolio repaying, reducing its incentive to monitor. The risk-shifting effect works the other way round. Due to agency problems and limited liability, the amount of risk shareholders want to transfer to debtholders falls as deposit rates drop. The strength of the risk-shifting effect is a function of leverage, however. If banks can adjust optimally their capital structure, equilibrium leverage increases in a low interest rate environment since the benefit from holding capital (as a signal) falls.

41 RISK-TAKING CHANNEL Dell Ariccia et al. (2013). Interest rates (Fed Funds) and bank risk taking (Survey of Terms of Business Lending) for U.S. banks.

42 WHAT HAVE WE LEARNED? Tension between micro- and macro-prudential regulation. In a banking system, both systemic risk and individual bank s contribution are endogenous and depend on banks equity capital. Capital requirements should be set to properly capture this coevolution. Ex. Gauthier et al. (2012): properly-designed capital requirements could reduce the probability of a systemic crisis by 25%.

43 WHAT HAVE WE LEARNED? Leaning-against-the-wind: how should monetary respond to financial imbalances? For demand shocks, prices and risk-taking (leverage) move in sync. A monetary restriction is effective in restraining both. For supply shocks, the policy rate cannot deal with both objectives at the same time. In any case, a lot of additional research is needed!

44 THANK YOU ALL Edoardo Gaffeo Department of Economics and Management University of Trento

ECON 4335 The economics of banking Lecture 7, 6/3-2013: Deposit Insurance, Bank Regulation, Solvency Arrangements

ECON 4335 The economics of banking Lecture 7, 6/3-2013: Deposit Insurance, Bank Regulation, Solvency Arrangements Bent Vale, Norges Bank Views and conclusions are those of the lecturer and can not be attributed

ECON 4335 The economics of banking Lecture 7, 6/3-2013: Deposit Insurance, Bank Regulation, Solvency Arrangements Bent Vale, Norges Bank Views and conclusions are those of the lecturer and can not be attributed

Economia Finanziaria e Monetaria

Economia Finanziaria e Monetaria Lezione 11 Ruolo degli intermediari: aspetti micro delle crisi finanziarie (asimmetrie informative e modelli di business bancari/ finanziari) 1 0. Outline Scaletta della

Economia Finanziaria e Monetaria Lezione 11 Ruolo degli intermediari: aspetti micro delle crisi finanziarie (asimmetrie informative e modelli di business bancari/ finanziari) 1 0. Outline Scaletta della

Global Games and Financial Fragility:

Global Games and Financial Fragility: Foundations and a Recent Application Itay Goldstein Wharton School, University of Pennsylvania Outline Part I: The introduction of global games into the analysis of

Global Games and Financial Fragility: Foundations and a Recent Application Itay Goldstein Wharton School, University of Pennsylvania Outline Part I: The introduction of global games into the analysis of

A Model with Costly Enforcement

A Model with Costly Enforcement Jesús Fernández-Villaverde University of Pennsylvania December 25, 2012 Jesús Fernández-Villaverde (PENN) Costly-Enforcement December 25, 2012 1 / 43 A Model with Costly

A Model with Costly Enforcement Jesús Fernández-Villaverde University of Pennsylvania December 25, 2012 Jesús Fernández-Villaverde (PENN) Costly-Enforcement December 25, 2012 1 / 43 A Model with Costly

The Federal Reserve in the 21st Century Financial Stability Policies

The Federal Reserve in the 21st Century Financial Stability Policies Thomas Eisenbach, Research and Statistics Group Disclaimer The views expressed in the presentation are those of the speaker and are

The Federal Reserve in the 21st Century Financial Stability Policies Thomas Eisenbach, Research and Statistics Group Disclaimer The views expressed in the presentation are those of the speaker and are

Microeconomics of Banking: Lecture 3

Microeconomics of Banking: Lecture 3 Prof. Ronaldo CARPIO Oct. 9, 2015 Review of Last Week Consumer choice problem General equilibrium Contingent claims Risk aversion The optimal choice, x = (X, Y ), is

Microeconomics of Banking: Lecture 3 Prof. Ronaldo CARPIO Oct. 9, 2015 Review of Last Week Consumer choice problem General equilibrium Contingent claims Risk aversion The optimal choice, x = (X, Y ), is

Microeconomics of Banking Second Edition. Xavier Freixas and Jean-Charles Rochet. The MIT Press Cambridge, Massachusetts London, England

Microeconomics of Banking Second Edition Xavier Freixas and Jean-Charles Rochet The MIT Press Cambridge, Massachusetts London, England List of Figures Preface xv xvii 1 Introduction 1 1.1 What Is a Bank,

Microeconomics of Banking Second Edition Xavier Freixas and Jean-Charles Rochet The MIT Press Cambridge, Massachusetts London, England List of Figures Preface xv xvii 1 Introduction 1 1.1 What Is a Bank,

Liquidity and capital: Substitutes or complements?

Marie Hoerova European Central Bank and CEPR Liquidity and capital: Substitutes or complements? Chicago Fed/ECB International Banking Conference November 3, 2016 The views expressed are those of the author

Marie Hoerova European Central Bank and CEPR Liquidity and capital: Substitutes or complements? Chicago Fed/ECB International Banking Conference November 3, 2016 The views expressed are those of the author

Revision Lecture Microeconomics of Banking MSc Finance: Theory of Finance I MSc Economics: Financial Economics I

Revision Lecture Microeconomics of Banking MSc Finance: Theory of Finance I MSc Economics: Financial Economics I April 2005 PREPARING FOR THE EXAM What models do you need to study? All the models we studied

Revision Lecture Microeconomics of Banking MSc Finance: Theory of Finance I MSc Economics: Financial Economics I April 2005 PREPARING FOR THE EXAM What models do you need to study? All the models we studied

Nobel Symposium 2018: Money and Banking

Nobel Symposium 2018: Money and Banking Markus K. Brunnermeier Princeton University Stockholm, May 27 th 2018 Types of Distortions Belief distortions Match belief surveys (BGS) Incomplete markets natural

Nobel Symposium 2018: Money and Banking Markus K. Brunnermeier Princeton University Stockholm, May 27 th 2018 Types of Distortions Belief distortions Match belief surveys (BGS) Incomplete markets natural

The Federal Reserve in the 21st Century Financial Stability Policies

The Federal Reserve in the 21st Century Financial Stability Policies Thomas Eisenbach, Research and Statistics Group Disclaimer The views expressed in the presentation are those of the speaker and are

The Federal Reserve in the 21st Century Financial Stability Policies Thomas Eisenbach, Research and Statistics Group Disclaimer The views expressed in the presentation are those of the speaker and are

Deflation, Credit Collapse and Great Depressions. Enrique G. Mendoza

Deflation, Credit Collapse and Great Depressions Enrique G. Mendoza Main points In economies where agents are highly leveraged, deflation amplifies the real effects of credit crunches Credit frictions

Deflation, Credit Collapse and Great Depressions Enrique G. Mendoza Main points In economies where agents are highly leveraged, deflation amplifies the real effects of credit crunches Credit frictions

Bank Capital, Agency Costs, and Monetary Policy. Césaire Meh Kevin Moran Department of Monetary and Financial Analysis Bank of Canada

Bank Capital, Agency Costs, and Monetary Policy Césaire Meh Kevin Moran Department of Monetary and Financial Analysis Bank of Canada Motivation A large literature quantitatively studies the role of financial

Bank Capital, Agency Costs, and Monetary Policy Césaire Meh Kevin Moran Department of Monetary and Financial Analysis Bank of Canada Motivation A large literature quantitatively studies the role of financial

The lender of last resort: liquidity provision versus the possibility of bail-out

The lender of last resort: liquidity provision versus the possibility of bail-out Rob Nijskens Sylvester C.W. Eijffinger June 24, 2010 The lender of last resort: liquidity versus bail-out 1 /20 Motivation:

The lender of last resort: liquidity provision versus the possibility of bail-out Rob Nijskens Sylvester C.W. Eijffinger June 24, 2010 The lender of last resort: liquidity versus bail-out 1 /20 Motivation:

Supplement to the lecture on the Diamond-Dybvig model

ECON 4335 Economics of Banking, Fall 2016 Jacopo Bizzotto 1 Supplement to the lecture on the Diamond-Dybvig model The model in Diamond and Dybvig (1983) incorporates important features of the real world:

ECON 4335 Economics of Banking, Fall 2016 Jacopo Bizzotto 1 Supplement to the lecture on the Diamond-Dybvig model The model in Diamond and Dybvig (1983) incorporates important features of the real world:

Monetary and Financial Macroeconomics

Monetary and Financial Macroeconomics Hernán D. Seoane Universidad Carlos III de Madrid Introduction Last couple of weeks we introduce banks in our economies Financial intermediation arises naturally when

Monetary and Financial Macroeconomics Hernán D. Seoane Universidad Carlos III de Madrid Introduction Last couple of weeks we introduce banks in our economies Financial intermediation arises naturally when

The Interaction of Monetary and Macroprudential Policies

The Interaction of Monetary and Macroprudential Policies By Stijn Claessens (IMF) Based on an IMF Board Paper Disclaimer! The views presented here are those of the authors and do NOT necessarily reflect

The Interaction of Monetary and Macroprudential Policies By Stijn Claessens (IMF) Based on an IMF Board Paper Disclaimer! The views presented here are those of the authors and do NOT necessarily reflect

Discussion of Liquidity, Moral Hazard, and Interbank Market Collapse

Discussion of Liquidity, Moral Hazard, and Interbank Market Collapse Tano Santos Columbia University Financial intermediaries, such as banks, perform many roles: they screen risks, evaluate and fund worthy

Discussion of Liquidity, Moral Hazard, and Interbank Market Collapse Tano Santos Columbia University Financial intermediaries, such as banks, perform many roles: they screen risks, evaluate and fund worthy

Financial Fragility A Global-Games Approach Itay Goldstein Wharton School, University of Pennsylvania

Financial Fragility A Global-Games Approach Itay Goldstein Wharton School, University of Pennsylvania Financial Fragility and Coordination Failures What makes financial systems fragile? What causes crises

Financial Fragility A Global-Games Approach Itay Goldstein Wharton School, University of Pennsylvania Financial Fragility and Coordination Failures What makes financial systems fragile? What causes crises

LEVERAGE AND LIQUIDITY DRY-UPS: A FRAMEWORK AND POLICY IMPLICATIONS. Denis Gromb LBS, LSE and CEPR. Dimitri Vayanos LSE, CEPR and NBER

LEVERAGE AND LIQUIDITY DRY-UPS: A FRAMEWORK AND POLICY IMPLICATIONS Denis Gromb LBS, LSE and CEPR Dimitri Vayanos LSE, CEPR and NBER June 2008 Gromb-Vayanos 1 INTRODUCTION Some lessons from recent crisis:

LEVERAGE AND LIQUIDITY DRY-UPS: A FRAMEWORK AND POLICY IMPLICATIONS Denis Gromb LBS, LSE and CEPR Dimitri Vayanos LSE, CEPR and NBER June 2008 Gromb-Vayanos 1 INTRODUCTION Some lessons from recent crisis:

Monetary Easing and Financial Instability

Monetary Easing and Financial Instability Viral Acharya NYU-Stern, CEPR and NBER Guillaume Plantin Sciences Po September 4, 2015 Acharya & Plantin (2015) Monetary Easing and Financial Instability September

Monetary Easing and Financial Instability Viral Acharya NYU-Stern, CEPR and NBER Guillaume Plantin Sciences Po September 4, 2015 Acharya & Plantin (2015) Monetary Easing and Financial Instability September

Financial Institutions, Markets and Regulation: A Survey

Financial Institutions, Markets and Regulation: A Survey Thorsten Beck, Elena Carletti and Itay Goldstein COEURE workshop on financial markets, 6 June 2015 Starting point The recent crisis has led to intense

Financial Institutions, Markets and Regulation: A Survey Thorsten Beck, Elena Carletti and Itay Goldstein COEURE workshop on financial markets, 6 June 2015 Starting point The recent crisis has led to intense

Paradox of Prudence & Linkage between Financial & Price Stability

Paradox of Prudence & inkage between Financial & Price Stability Markus Brunnermeier Reserve Bank of South frica Pretoria, South frica, Oct 26 th, 2017 Overview 1. From Risk in Isolation to Systemic Risk

Paradox of Prudence & inkage between Financial & Price Stability Markus Brunnermeier Reserve Bank of South frica Pretoria, South frica, Oct 26 th, 2017 Overview 1. From Risk in Isolation to Systemic Risk

A Baseline Model: Diamond and Dybvig (1983)

") BANKING AND FINANCIAL FRAGILITY A Baseline Model: Diamond and Dybvig (1983) Professor Todd Keister Rutgers University May 2017 Objective Want to develop a model to help us understand: why banks and other

BANKING AND FINANCIAL FRAGILITY A Baseline Model: Diamond and Dybvig (1983) Professor Todd Keister Rutgers University May 2017 Objective Want to develop a model to help us understand: why banks and other

Illiquidity and Interest Rate Policy

Illiquidity and Interest Rate Policy Douglas Diamond and Raghuram Rajan University of Chicago Booth School of Business and NBER 2 Motivation Illiquidity and insolvency are likely when long term assets

Illiquidity and Interest Rate Policy Douglas Diamond and Raghuram Rajan University of Chicago Booth School of Business and NBER 2 Motivation Illiquidity and insolvency are likely when long term assets

Banking Regulation in Theory and Practice (2)

") Banking Regulation in Theory and Practice (2) Jin Cao (Norges Bank Research, Oslo & CESifo, Munich) November 13, 2017 Universitetet i Oslo Outline 1 Disclaimer (If they care about what I say,) the views

Banking Regulation in Theory and Practice (2) Jin Cao (Norges Bank Research, Oslo & CESifo, Munich) November 13, 2017 Universitetet i Oslo Outline 1 Disclaimer (If they care about what I say,) the views

Bailouts, Bail-ins and Banking Crises

Bailouts, Bail-ins and Banking Crises Todd Keister Rutgers University Yuliyan Mitkov Rutgers University & University of Bonn 2017 HKUST Workshop on Macroeconomics June 15, 2017 The bank runs problem Intermediaries

Bailouts, Bail-ins and Banking Crises Todd Keister Rutgers University Yuliyan Mitkov Rutgers University & University of Bonn 2017 HKUST Workshop on Macroeconomics June 15, 2017 The bank runs problem Intermediaries

Institutional Finance

Institutional Finance Lecture 09 : Banking and Maturity Mismatch Markus K. Brunnermeier Preceptor: Dong Beom Choi Princeton University 1 Select/monitor borrowers Sharpe (1990) Reduce asymmetric info idiosyncratic

Institutional Finance Lecture 09 : Banking and Maturity Mismatch Markus K. Brunnermeier Preceptor: Dong Beom Choi Princeton University 1 Select/monitor borrowers Sharpe (1990) Reduce asymmetric info idiosyncratic

Macroprudential Bank Capital Regulation in a Competitive Financial System

Macroprudential Bank Capital Regulation in a Competitive Financial System Milton Harris, Christian Opp, Marcus Opp Chicago, UPenn, University of California Fall 2015 H 2 O (Chicago, UPenn, UC) Macroprudential

Macroprudential Bank Capital Regulation in a Competitive Financial System Milton Harris, Christian Opp, Marcus Opp Chicago, UPenn, University of California Fall 2015 H 2 O (Chicago, UPenn, UC) Macroprudential

Monetary Economics. Lecture 23a: inside and outside liquidity, part one. Chris Edmond. 2nd Semester 2014 (not examinable)

") Monetary Economics Lecture 23a: inside and outside liquidity, part one Chris Edmond 2nd Semester 2014 (not examinable) 1 This lecture Main reading: Holmström and Tirole, Inside and outside liquidity, MIT

Monetary Economics Lecture 23a: inside and outside liquidity, part one Chris Edmond 2nd Semester 2014 (not examinable) 1 This lecture Main reading: Holmström and Tirole, Inside and outside liquidity, MIT

On the use of leverage caps in bank regulation

On the use of leverage caps in bank regulation Afrasiab Mirza Department of Economics University of Birmingham a.mirza@bham.ac.uk Frank Strobel Department of Economics University of Birmingham f.strobel@bham.ac.uk

On the use of leverage caps in bank regulation Afrasiab Mirza Department of Economics University of Birmingham a.mirza@bham.ac.uk Frank Strobel Department of Economics University of Birmingham f.strobel@bham.ac.uk

The Role of the Net Worth of Banks in the Propagation of Shocks

The Role of the Net Worth of Banks in the Propagation of Shocks Preliminary Césaire Meh Department of Monetary and Financial Analysis Bank of Canada Kevin Moran Université Laval The Role of the Net Worth

The Role of the Net Worth of Banks in the Propagation of Shocks Preliminary Césaire Meh Department of Monetary and Financial Analysis Bank of Canada Kevin Moran Université Laval The Role of the Net Worth

Markets, Banks and Shadow Banks

Markets, Banks and Shadow Banks David Martinez-Miera Rafael Repullo U. Carlos III, Madrid, Spain CEMFI, Madrid, Spain AEA Session Macroprudential Policy and Banking Panics Philadelphia, January 6, 2018

Markets, Banks and Shadow Banks David Martinez-Miera Rafael Repullo U. Carlos III, Madrid, Spain CEMFI, Madrid, Spain AEA Session Macroprudential Policy and Banking Panics Philadelphia, January 6, 2018

Imperfect Transparency and the Risk of Securitization

Imperfect Transparency and the Risk of Securitization Seungjun Baek Florida State University June. 16, 2017 1. Introduction Motivation Study benefit and risk of securitization Motivation Study benefit

Imperfect Transparency and the Risk of Securitization Seungjun Baek Florida State University June. 16, 2017 1. Introduction Motivation Study benefit and risk of securitization Motivation Study benefit

Delegated Monitoring, Legal Protection, Runs and Commitment

Delegated Monitoring, Legal Protection, Runs and Commitment Douglas W. Diamond MIT (visiting), Chicago Booth and NBER FTG Summer School, St. Louis August 14, 2015 1 The Public Project 1 Project 2 Firm

Delegated Monitoring, Legal Protection, Runs and Commitment Douglas W. Diamond MIT (visiting), Chicago Booth and NBER FTG Summer School, St. Louis August 14, 2015 1 The Public Project 1 Project 2 Firm

Microeconomics of Banking: Lecture 2

Microeconomics of Banking: Lecture 2 Prof. Ronaldo CARPIO September 25, 2015 A Brief Look at General Equilibrium Asset Pricing Last week, we saw a general equilibrium model in which banks were irrelevant.

Microeconomics of Banking: Lecture 2 Prof. Ronaldo CARPIO September 25, 2015 A Brief Look at General Equilibrium Asset Pricing Last week, we saw a general equilibrium model in which banks were irrelevant.

Foreign Competition and Banking Industry Dynamics: An Application to Mexico

Foreign Competition and Banking Industry Dynamics: An Application to Mexico Dean Corbae Pablo D Erasmo 1 Univ. of Wisconsin FRB Philadelphia June 12, 2014 1 The views expressed here do not necessarily

Foreign Competition and Banking Industry Dynamics: An Application to Mexico Dean Corbae Pablo D Erasmo 1 Univ. of Wisconsin FRB Philadelphia June 12, 2014 1 The views expressed here do not necessarily

A Macroeconomic Model with Financially Constrained Producers and Intermediaries

A Macroeconomic Model with Financially Constrained Producers and Intermediaries Authors: Vadim, Elenev Tim Landvoigt and Stijn Van Nieuwerburgh Discussion by: David Martinez-Miera ECB Research Workshop

A Macroeconomic Model with Financially Constrained Producers and Intermediaries Authors: Vadim, Elenev Tim Landvoigt and Stijn Van Nieuwerburgh Discussion by: David Martinez-Miera ECB Research Workshop

Intermediary Balance Sheets Tobias Adrian and Nina Boyarchenko, NY Fed Discussant: Annette Vissing-Jorgensen, UC Berkeley

Intermediary Balance Sheets Tobias Adrian and Nina Boyarchenko, NY Fed Discussant: Annette Vissing-Jorgensen, UC Berkeley Objective: Construct a general equilibrium model with two types of intermediaries:

Intermediary Balance Sheets Tobias Adrian and Nina Boyarchenko, NY Fed Discussant: Annette Vissing-Jorgensen, UC Berkeley Objective: Construct a general equilibrium model with two types of intermediaries:

Motivation: Two Basic Facts

Motivation: Two Basic Facts 1 Primary objective of macroprudential policy: aligning financial system resilience with systemic risk to promote the real economy Systemic risk event Financial system resilience

Motivation: Two Basic Facts 1 Primary objective of macroprudential policy: aligning financial system resilience with systemic risk to promote the real economy Systemic risk event Financial system resilience

Implications of Bank regulation for Credit Intermediation and Bank Stability: A Dynamic Perspective Discussion

19 November 2015 4 th EBA Policy Research Workshop Implications of Bank regulation for Credit Intermediation and Bank Stability: A Dynamic Perspective Discussion The opinions expressed in the context of

19 November 2015 4 th EBA Policy Research Workshop Implications of Bank regulation for Credit Intermediation and Bank Stability: A Dynamic Perspective Discussion The opinions expressed in the context of

Aggregate Implications of Credit Market Imperfections (II) By Kiminori Matsuyama. Updated on January 25, 2010

By Kiminori Matsuyama. Updated on January 25, 2010") Aggregate Implications of Credit Market Imperfections (II) By Kiminori Matsuyama Updated on January 25, 2010 Lecture 2: Dynamic Models with Homogeneous Agents 1 Lecture 2: Dynamic Models with Homogeneous

Aggregate Implications of Credit Market Imperfections (II) By Kiminori Matsuyama Updated on January 25, 2010 Lecture 2: Dynamic Models with Homogeneous Agents 1 Lecture 2: Dynamic Models with Homogeneous

Maturity Transformation and Liquidity

Maturity Transformation and Liquidity Patrick Bolton, Tano Santos Columbia University and Jose Scheinkman Princeton University Motivation Main Question: Who is best placed to, 1. Transform Maturity 2.

Maturity Transformation and Liquidity Patrick Bolton, Tano Santos Columbia University and Jose Scheinkman Princeton University Motivation Main Question: Who is best placed to, 1. Transform Maturity 2.

Chapter 8 Liquidity and Financial Intermediation

Chapter 8 Liquidity and Financial Intermediation Main Aims: 1. Study money as a liquid asset. 2. Develop an OLG model in which individuals live for three periods. 3. Analyze two roles of banks: (1.) correcting

Chapter 8 Liquidity and Financial Intermediation Main Aims: 1. Study money as a liquid asset. 2. Develop an OLG model in which individuals live for three periods. 3. Analyze two roles of banks: (1.) correcting

Government Guarantees and Financial Stability

Government Guarantees and Financial Stability F. Allen E. Carletti I. Goldstein A. Leonello Bocconi University and CEPR University of Pennsylvania Government Guarantees and Financial Stability 1 / 21 Introduction

Government Guarantees and Financial Stability F. Allen E. Carletti I. Goldstein A. Leonello Bocconi University and CEPR University of Pennsylvania Government Guarantees and Financial Stability 1 / 21 Introduction

A Macroeconomic Model with Financial Panics

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 218 1 The views expressed in this paper are those of the authors

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 218 1 The views expressed in this paper are those of the authors

Macroeconomics of Bank Capital and Liquidity Regulations

Macroeconomics of Bank Capital and Liquidity Regulations Authors: Frederic Boissay and Fabrice Collard Discussion by: David Martinez-Miera UC3M & CEPR Financial Stability Conference Martinez-Miera (UC3M

Macroeconomics of Bank Capital and Liquidity Regulations Authors: Frederic Boissay and Fabrice Collard Discussion by: David Martinez-Miera UC3M & CEPR Financial Stability Conference Martinez-Miera (UC3M

Do Low Interest Rates Sow the Seeds of Financial Crises?

Do Low nterest Rates Sow the Seeds of Financial Crises? Simona Cociuba, University of Western Ontario Malik Shukayev, Bank of Canada Alexander Ueberfeldt, Bank of Canada Second Boston University-Boston

Do Low nterest Rates Sow the Seeds of Financial Crises? Simona Cociuba, University of Western Ontario Malik Shukayev, Bank of Canada Alexander Ueberfeldt, Bank of Canada Second Boston University-Boston

Revision Lecture. MSc Finance: Theory of Finance I MSc Economics: Financial Economics I

Revision Lecture Topics in Banking and Market Microstructure MSc Finance: Theory of Finance I MSc Economics: Financial Economics I April 2006 PREPARING FOR THE EXAM ² What do you need to know? All the

Revision Lecture Topics in Banking and Market Microstructure MSc Finance: Theory of Finance I MSc Economics: Financial Economics I April 2006 PREPARING FOR THE EXAM ² What do you need to know? All the

A Model of Shadow Banking: Crises, Central Banks and Regulation

A Model of Shadow Banking: Crises, Central Banks and Regulation Giovanni di Iasio (Bank of Italy) Zoltan Pozsar (Credit Suisse) The Role of Liquidity in the Financial System Atlanta Federal Reserve, November

A Model of Shadow Banking: Crises, Central Banks and Regulation Giovanni di Iasio (Bank of Italy) Zoltan Pozsar (Credit Suisse) The Role of Liquidity in the Financial System Atlanta Federal Reserve, November

Introduction and road-map for the first 6 lectures

1 ECON 4335 Economics of Banking, Fall 2016 Jacopo Bizzotto; 1 Introduction and road-map for the first 6 lectures 1. Introduction This course covers three sets of topic: (I) microeconomics of banking,

1 ECON 4335 Economics of Banking, Fall 2016 Jacopo Bizzotto; 1 Introduction and road-map for the first 6 lectures 1. Introduction This course covers three sets of topic: (I) microeconomics of banking,

Central bank liquidity provision, risktaking and economic efficiency

Central bank liquidity provision, risktaking and economic efficiency U. Bindseil and J. Jablecki Presentation by U. Bindseil at the Fields Quantitative Finance Seminar, 27 February 2013 1 Classical problem:

Central bank liquidity provision, risktaking and economic efficiency U. Bindseil and J. Jablecki Presentation by U. Bindseil at the Fields Quantitative Finance Seminar, 27 February 2013 1 Classical problem:

Capital Adequacy and Liquidity in Banking Dynamics

Capital Adequacy and Liquidity in Banking Dynamics Jin Cao Lorán Chollete October 9, 2014 Abstract We present a framework for modelling optimum capital adequacy in a dynamic banking context. We combine

Capital Adequacy and Liquidity in Banking Dynamics Jin Cao Lorán Chollete October 9, 2014 Abstract We present a framework for modelling optimum capital adequacy in a dynamic banking context. We combine

Interest Rates, Market Power, and Financial Stability

Interest Rates, Market Power, and Financial Stability Rafael Repullo (joint work with David Martinez-Miera) Conference on Financial Stability Banco de Portugal, 17 October 2017 Introduction (i) Session

Interest Rates, Market Power, and Financial Stability Rafael Repullo (joint work with David Martinez-Miera) Conference on Financial Stability Banco de Portugal, 17 October 2017 Introduction (i) Session

Regulatory Arbitrage and Systemic Liquidity Crises

Regulatory Arbitrage and Systemic Liquidity Crises Stephan Luck & Paul Schempp Princeton University and MPI for Research on Collective Goods Federal Reserve Bank of Atlanta The Role of Liquidity in the

Regulatory Arbitrage and Systemic Liquidity Crises Stephan Luck & Paul Schempp Princeton University and MPI for Research on Collective Goods Federal Reserve Bank of Atlanta The Role of Liquidity in the

A Theory of Bank Liquidity Requirements

A Theory of Bank Liquidity Requirements Charles Calomiris Florian Heider Marie Hoerova Columbia GSB ECB ECB IAES Meetings Washington, D.C., October 15, 2016 The views expressed are solely those of the

A Theory of Bank Liquidity Requirements Charles Calomiris Florian Heider Marie Hoerova Columbia GSB ECB ECB IAES Meetings Washington, D.C., October 15, 2016 The views expressed are solely those of the

DETERMINANTS OF DEBT CAPACITY. 1st set of transparencies. Tunis, May Jean TIROLE

DETERMINANTS OF DEBT CAPACITY 1st set of transparencies Tunis, May 2005 Jean TIROLE I. INTRODUCTION Adam Smith (1776) - Berle-Means (1932) Agency problem Principal outsiders/investors/lenders Agent insiders/managers/entrepreneur

DETERMINANTS OF DEBT CAPACITY 1st set of transparencies Tunis, May 2005 Jean TIROLE I. INTRODUCTION Adam Smith (1776) - Berle-Means (1932) Agency problem Principal outsiders/investors/lenders Agent insiders/managers/entrepreneur

Intermediate Macroeconomics

Intermediate Macroeconomics Lecture 10 - Consumption 2 Zsófia L. Bárány Sciences Po 2014 April Last week Keynesian consumption function Kuznets puzzle permanent income hypothesis life-cycle theory of consumption

Intermediate Macroeconomics Lecture 10 - Consumption 2 Zsófia L. Bárány Sciences Po 2014 April Last week Keynesian consumption function Kuznets puzzle permanent income hypothesis life-cycle theory of consumption

Markus K. Brunnermeier

Markus K. Brunnermeier 1 Overview Two world views 1. No financial frictions sticky price 2. Financial sector + bubbles Role of the financial sector Leverage Maturity mismatch maturity rat race linkage

Markus K. Brunnermeier 1 Overview Two world views 1. No financial frictions sticky price 2. Financial sector + bubbles Role of the financial sector Leverage Maturity mismatch maturity rat race linkage

Liquidity and Leverage

Tobias Adrian Federal Reserve Bank of New York Hyun Song Shin Princeton University European Central Bank, November 29, 2007 The views expressed in this presentation are those of the authors and do not

Tobias Adrian Federal Reserve Bank of New York Hyun Song Shin Princeton University European Central Bank, November 29, 2007 The views expressed in this presentation are those of the authors and do not

Shadow Banking and Financial Stability

Shadow Banking and Financial Stability Professor Dr. Claudia M. Buch Magdeburg University Institute for Economic Research Halle (IWH) German Council of Economic Experts Symposium Financial Stability and

Shadow Banking and Financial Stability Professor Dr. Claudia M. Buch Magdeburg University Institute for Economic Research Halle (IWH) German Council of Economic Experts Symposium Financial Stability and

General Examination in Macroeconomic Theory SPRING 2016

HARVARD UNIVERSITY DEPARTMENT OF ECONOMICS General Examination in Macroeconomic Theory SPRING 2016 You have FOUR hours. Answer all questions Part A (Prof. Laibson): 60 minutes Part B (Prof. Barro): 60

HARVARD UNIVERSITY DEPARTMENT OF ECONOMICS General Examination in Macroeconomic Theory SPRING 2016 You have FOUR hours. Answer all questions Part A (Prof. Laibson): 60 minutes Part B (Prof. Barro): 60

Optimal Credit Market Policy. CEF 2018, Milan

Optimal Credit Market Policy Matteo Iacoviello 1 Ricardo Nunes 2 Andrea Prestipino 1 1 Federal Reserve Board 2 University of Surrey CEF 218, Milan June 2, 218 Disclaimer: The views expressed are solely

Optimal Credit Market Policy Matteo Iacoviello 1 Ricardo Nunes 2 Andrea Prestipino 1 1 Federal Reserve Board 2 University of Surrey CEF 218, Milan June 2, 218 Disclaimer: The views expressed are solely

How do we cope with uncertainty?

Topic 3: Choice under uncertainty (K&R Ch. 6) In 1965, a Frenchman named Raffray thought that he had found a great deal: He would pay a 90-year-old woman $500 a month until she died, then move into her

Topic 3: Choice under uncertainty (K&R Ch. 6) In 1965, a Frenchman named Raffray thought that he had found a great deal: He would pay a 90-year-old woman $500 a month until she died, then move into her

Structural credit risk models and systemic capital

Structural credit risk models and systemic capital Somnath Chatterjee CCBS, Bank of England November 7, 2013 Structural credit risk model Structural credit risk models are based on the notion that both

Structural credit risk models and systemic capital Somnath Chatterjee CCBS, Bank of England November 7, 2013 Structural credit risk model Structural credit risk models are based on the notion that both

The I Theory of Money

The I Theory of Money Markus Brunnermeier and Yuliy Sannikov Presented by Felipe Bastos G Silva 09/12/2017 Overview Motivation: A theory of money needs a place for financial intermediaries (inside money

The I Theory of Money Markus Brunnermeier and Yuliy Sannikov Presented by Felipe Bastos G Silva 09/12/2017 Overview Motivation: A theory of money needs a place for financial intermediaries (inside money

Financial Intermediation, Loanable Funds and The Real Sector

Financial Intermediation, Loanable Funds and The Real Sector Bengt Holmstrom and Jean Tirole April 3, 2017 Holmstrom and Tirole Financial Intermediation, Loanable Funds and The Real Sector April 3, 2017

Financial Intermediation, Loanable Funds and The Real Sector Bengt Holmstrom and Jean Tirole April 3, 2017 Holmstrom and Tirole Financial Intermediation, Loanable Funds and The Real Sector April 3, 2017

Regulation, Competition, and Stability in the Banking Industry

Regulation, Competition, and Stability in the Banking Industry Dean Corbae University of Wisconsin - Madison and NBER October 2017 How does policy affect competition and vice versa? Most macro (DSGE) models

Regulation, Competition, and Stability in the Banking Industry Dean Corbae University of Wisconsin - Madison and NBER October 2017 How does policy affect competition and vice versa? Most macro (DSGE) models

Leverage Restrictions in a Business Cycle Model. March 13-14, 2015, Macro Financial Modeling, NYU Stern.

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda Northwestern University Bank of Japan March 13-14, 2015, Macro Financial Modeling, NYU Stern. Background Wish to address

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda Northwestern University Bank of Japan March 13-14, 2015, Macro Financial Modeling, NYU Stern. Background Wish to address

Introduction. New Basel III liquidity standards. are designed to mitigate banks liquidity risk. Liquidity requirements may also limit solvency

B LIQUIDITY REGULATION AS A PRUDENTIAL TOOL: A RESEARCH PERSPECTIVE In response to the flaws in banks liquidity risk management revealed by the global financial crisis, the Basel Committee on Banking Supervision

B LIQUIDITY REGULATION AS A PRUDENTIAL TOOL: A RESEARCH PERSPECTIVE In response to the flaws in banks liquidity risk management revealed by the global financial crisis, the Basel Committee on Banking Supervision

Optimal Monetary and Macroprudential Policy: Gains and Pitfalls in a Model of Financial Intermediation. March 28, 2014

Optimal Monetary and Macroprudential Policy: Gains and Pitfalls in a Model of Financial Intermediation Michael T. Kiley Jae W. Sim March 28, 2014 THEORETICAL FRAMEWORK Financial intermediation sector in

Optimal Monetary and Macroprudential Policy: Gains and Pitfalls in a Model of Financial Intermediation Michael T. Kiley Jae W. Sim March 28, 2014 THEORETICAL FRAMEWORK Financial intermediation sector in

Monetary Easing and Financial Instability

Monetary Easing and Financial Instability Viral Acharya NYU Stern, CEPR and NBER Guillaume Plantin Sciences Po April 22, 2016 Acharya & Plantin Monetary Easing and Financial Instability April 22, 2016

Monetary Easing and Financial Instability Viral Acharya NYU Stern, CEPR and NBER Guillaume Plantin Sciences Po April 22, 2016 Acharya & Plantin Monetary Easing and Financial Instability April 22, 2016

The usual disclaimer applies. The opinions are those of the discussant only and in no way involve the responsibility of the Bank of Italy.

Business Models in Banking: Is There a Best Practice? Conference Centre for Applied Research in Finance Università Bocconi September 21, 2009, Milan Tests of Ex Ante versus Ex Post Theories of Collateral

Business Models in Banking: Is There a Best Practice? Conference Centre for Applied Research in Finance Università Bocconi September 21, 2009, Milan Tests of Ex Ante versus Ex Post Theories of Collateral

Agency Costs, Net Worth and Business Fluctuations. Bernanke and Gertler (1989, AER)

") Agency Costs, Net Worth and Business Fluctuations Bernanke and Gertler (1989, AER) 1 Introduction Many studies on the business cycles have suggested that financial factors, or more specifically the condition

Agency Costs, Net Worth and Business Fluctuations Bernanke and Gertler (1989, AER) 1 Introduction Many studies on the business cycles have suggested that financial factors, or more specifically the condition

Assessing the Spillover Effects of Changes in Bank Capital Regulation Using BoC-GEM-Fin: A Non-Technical Description

Assessing the Spillover Effects of Changes in Bank Capital Regulation Using BoC-GEM-Fin: A Non-Technical Description Carlos de Resende, Ali Dib, and Nikita Perevalov International Economic Analysis Department

Assessing the Spillover Effects of Changes in Bank Capital Regulation Using BoC-GEM-Fin: A Non-Technical Description Carlos de Resende, Ali Dib, and Nikita Perevalov International Economic Analysis Department

Expectations vs. Fundamentals-based Bank Runs: When should bailouts be permitted?

Expectations vs. Fundamentals-based Bank Runs: When should bailouts be permitted? Todd Keister Rutgers University Vijay Narasiman Harvard University October 2014 The question Is it desirable to restrict

Expectations vs. Fundamentals-based Bank Runs: When should bailouts be permitted? Todd Keister Rutgers University Vijay Narasiman Harvard University October 2014 The question Is it desirable to restrict

Corporate Financial Management. Lecture 3: Other explanations of capital structure

Corporate Financial Management Lecture 3: Other explanations of capital structure As we discussed in previous lectures, two extreme results, namely the irrelevance of capital structure and 100 percent

Corporate Financial Management Lecture 3: Other explanations of capital structure As we discussed in previous lectures, two extreme results, namely the irrelevance of capital structure and 100 percent

Why are Banks Highly Interconnected?

Why are Banks Highly Interconnected? Alexander David Alfred Lehar University of Calgary Fields Institute - 2013 David and Lehar () Why are Banks Highly Interconnected? Fields Institute - 2013 1 / 35 Positive

Why are Banks Highly Interconnected? Alexander David Alfred Lehar University of Calgary Fields Institute - 2013 David and Lehar () Why are Banks Highly Interconnected? Fields Institute - 2013 1 / 35 Positive

Development Economics Part II Lecture 7

Development Economics Part II Lecture 7 Risk and Insurance Theory: How do households cope with large income shocks? What are testable implications of different models? Empirics: Can households insure themselves

Development Economics Part II Lecture 7 Risk and Insurance Theory: How do households cope with large income shocks? What are testable implications of different models? Empirics: Can households insure themselves

Optimal margins and equilibrium prices

Optimal margins and equilibrium prices Bruno Biais Florian Heider Marie Hoerova Toulouse School of Economics ECB ECB Bocconi Consob Conference Securities Markets: Trends, Risks and Policies February 26,

Optimal margins and equilibrium prices Bruno Biais Florian Heider Marie Hoerova Toulouse School of Economics ECB ECB Bocconi Consob Conference Securities Markets: Trends, Risks and Policies February 26,

Liquidity. Why do people choose to hold fiat money despite its lower rate of return?

Liquidity Why do people choose to hold fiat money despite its lower rate of return? Maybe because fiat money is less risky than most of the other assets. Maybe because fiat money is more liquid than alternative

Liquidity Why do people choose to hold fiat money despite its lower rate of return? Maybe because fiat money is less risky than most of the other assets. Maybe because fiat money is more liquid than alternative

Convertible Bonds and Bank Risk-taking

Natalya Martynova 1 Enrico Perotti 2 Bailouts, bail-in, and financial stability Paris, November 28 2014 1 De Nederlandsche Bank 2 University of Amsterdam, CEPR Motivation In the credit boom, high leverage

Natalya Martynova 1 Enrico Perotti 2 Bailouts, bail-in, and financial stability Paris, November 28 2014 1 De Nederlandsche Bank 2 University of Amsterdam, CEPR Motivation In the credit boom, high leverage

Should Unconventional Monetary Policies Become Conventional?

Should Unconventional Monetary Policies Become Conventional? Dominic Quint and Pau Rabanal Discussant: Annette Vissing-Jorgensen, University of California Berkeley and NBER Question: Should LSAPs be used

Should Unconventional Monetary Policies Become Conventional? Dominic Quint and Pau Rabanal Discussant: Annette Vissing-Jorgensen, University of California Berkeley and NBER Question: Should LSAPs be used

Banking Crises and the Lender of Last Resort: How crucial is the role of information?

Banking Crises and the Lender of Last Resort: How crucial is the role of information? Hassan Naqvi NUS Business School, National University of Singapore February 27, 2006 Abstract This article develops

Banking Crises and the Lender of Last Resort: How crucial is the role of information? Hassan Naqvi NUS Business School, National University of Singapore February 27, 2006 Abstract This article develops

Discussion Liquidity requirements, liquidity choice and financial stability by Doug Diamond

Discussion Liquidity requirements, liquidity choice and financial stability by Doug Diamond Guillaume Plantin Sciences Po Plantin Liquidity requirements 1 / 23 The Diamond-Dybvig model Summary of the paper

Discussion Liquidity requirements, liquidity choice and financial stability by Doug Diamond Guillaume Plantin Sciences Po Plantin Liquidity requirements 1 / 23 The Diamond-Dybvig model Summary of the paper

Liquidity, Asset Price, and Welfare

Liquidity, Asset Price, and Welfare Jiang Wang MIT October 20, 2006 Microstructure of Foreign Exchange and Equity Markets Workshop Norges Bank and Bank of Canada Introduction Determinants of liquidity?

Liquidity, Asset Price, and Welfare Jiang Wang MIT October 20, 2006 Microstructure of Foreign Exchange and Equity Markets Workshop Norges Bank and Bank of Canada Introduction Determinants of liquidity?

Should Norway Change the 60% Equity portion of the GPFG fund?

Should Norway Change the 60% Equity portion of the GPFG fund? Pierre Collin-Dufresne EPFL & SFI, and CEPR April 2016 Outline Endowment Consumption Commitments Return Predictability and Trading Costs General

Should Norway Change the 60% Equity portion of the GPFG fund? Pierre Collin-Dufresne EPFL & SFI, and CEPR April 2016 Outline Endowment Consumption Commitments Return Predictability and Trading Costs General

Bank Leverage and Monetary Policy s Risk-Taking Channel: Evidence from the United States

Bank Leverage and Monetary Policy s Risk-Taking Channel: Evidence from the United States by Giovanni Dell Ariccia (IMF and CEPR) Luc Laeven (IMF and CEPR) Gustavo Suarez (Federal Reserve Board) CSEF Unicredit

Bank Leverage and Monetary Policy s Risk-Taking Channel: Evidence from the United States by Giovanni Dell Ariccia (IMF and CEPR) Luc Laeven (IMF and CEPR) Gustavo Suarez (Federal Reserve Board) CSEF Unicredit

Banking Crises and the Lender of Last Resort: How crucial is the role of information?

Banking Crises and the Lender of Last Resort: How crucial is the role of information? Hassan Naqvi NUS Business School, National University of Singapore & Financial Markets Group, London School of Economics

Banking Crises and the Lender of Last Resort: How crucial is the role of information? Hassan Naqvi NUS Business School, National University of Singapore & Financial Markets Group, London School of Economics

Monetary Economics July 2014

ECON40013 ECON90011 Monetary Economics July 2014 Chris Edmond Office hours: by appointment Office: Business & Economics 423 Phone: 8344 9733 Email: cedmond@unimelb.edu.au Course description This year I

ECON40013 ECON90011 Monetary Economics July 2014 Chris Edmond Office hours: by appointment Office: Business & Economics 423 Phone: 8344 9733 Email: cedmond@unimelb.edu.au Course description This year I

Lecture 25 Unemployment Financial Crisis. Noah Williams

Lecture 25 Unemployment Financial Crisis Noah Williams University of Wisconsin - Madison Economics 702 Changes in the Unemployment Rate What raises the unemployment rate? Anything raising reservation wage:

Lecture 25 Unemployment Financial Crisis Noah Williams University of Wisconsin - Madison Economics 702 Changes in the Unemployment Rate What raises the unemployment rate? Anything raising reservation wage:

Expectations versus Fundamentals: Does the Cause of Banking Panics Matter for Prudential Policy?

Federal Reserve Bank of New York Staff Reports Expectations versus Fundamentals: Does the Cause of Banking Panics Matter for Prudential Policy? Todd Keister Vijay Narasiman Staff Report no. 519 October

Federal Reserve Bank of New York Staff Reports Expectations versus Fundamentals: Does the Cause of Banking Panics Matter for Prudential Policy? Todd Keister Vijay Narasiman Staff Report no. 519 October

Credit Booms, Financial Crises and Macroprudential Policy

Credit Booms, Financial Crises and Macroprudential Policy Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 219 1 The views expressed in this paper are those

Credit Booms, Financial Crises and Macroprudential Policy Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 219 1 The views expressed in this paper are those

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko The views presented here are the authors and are not representative of the views of the Federal Reserve Bank of New

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko The views presented here are the authors and are not representative of the views of the Federal Reserve Bank of New

COLLECTIVE MORAL HAZARD, MATURITY MISMATCH AND SYSTEMIC BAILOUTS. November 12th, Emmanuel Farhi (Harvard) and Jean Tirole (TSE)

and Jean Tirole (TSE)") COLLECTIVE MORAL HAZARD, MATURITY MISMATCH AND SYSTEMIC BAILOUTS November 12th, 2009 Emmanuel Farhi (Harvard) and Jean Tirole (TSE) INTRODUCTION Two facts: 1 Overall macroeconomic fragility (sensitivity

COLLECTIVE MORAL HAZARD, MATURITY MISMATCH AND SYSTEMIC BAILOUTS November 12th, 2009 Emmanuel Farhi (Harvard) and Jean Tirole (TSE) INTRODUCTION Two facts: 1 Overall macroeconomic fragility (sensitivity

PART II-FINANCIAL INSTITUTIONS (INTERMEDIARIES)

") Boğaziçi University Department of Economics Money, Banking and Financial Institutions L.Yıldıran PART II-FINANCIAL INSTITUTIONS (INTERMEDIARIES) What do banks and other intermediaries do? Why do they exist?

Boğaziçi University Department of Economics Money, Banking and Financial Institutions L.Yıldıran PART II-FINANCIAL INSTITUTIONS (INTERMEDIARIES) What do banks and other intermediaries do? Why do they exist?

Lecture 26 Exchange Rates The Financial Crisis. Noah Williams

Lecture 26 Exchange Rates The Financial Crisis Noah Williams University of Wisconsin - Madison Economics 312/702 Money and Exchange Rates in a Small Open Economy Now look at relative prices of currencies:

Lecture 26 Exchange Rates The Financial Crisis Noah Williams University of Wisconsin - Madison Economics 312/702 Money and Exchange Rates in a Small Open Economy Now look at relative prices of currencies:

The science of monetary policy

Macroeconomic dynamics PhD School of Economics, Lectures 2018/19 The science of monetary policy Giovanni Di Bartolomeo giovanni.dibartolomeo@uniroma1.it Doctoral School of Economics Sapienza University

Macroeconomic dynamics PhD School of Economics, Lectures 2018/19 The science of monetary policy Giovanni Di Bartolomeo giovanni.dibartolomeo@uniroma1.it Doctoral School of Economics Sapienza University

Convertible Bonds and Bank Risk-taking

Natalya Martynova 1 Enrico Perotti 2 European Central Bank Workshop June 26, 2013 1 University of Amsterdam, Tinbergen Institute 2 University of Amsterdam, CEPR and ECB In the credit boom, high leverage

Natalya Martynova 1 Enrico Perotti 2 European Central Bank Workshop June 26, 2013 1 University of Amsterdam, Tinbergen Institute 2 University of Amsterdam, CEPR and ECB In the credit boom, high leverage

Peer Monitoring via Loss Mutualization

Peer Monitoring via Loss Mutualization Francesco Palazzo Bank of Italy November 19, 2015 Systemic Risk Center, LSE Motivation Extensive bailout plans in response to the financial crisis... US Treasury

Peer Monitoring via Loss Mutualization Francesco Palazzo Bank of Italy November 19, 2015 Systemic Risk Center, LSE Motivation Extensive bailout plans in response to the financial crisis... US Treasury