REPORT AND RECOMMENDATION OF THE EXECUTIVE COMMITTEE OF THE DISTRICT BUDGET COMMITTEE

|

|

|

- Marjory Osborne

- 5 years ago

- Views:

Transcription

1 REPORT AND RECOMMENDATION OF THE EXECUTIVE COMMITTEE OF THE DISTRICT BUDGET COMMITTEE January 2012

2 LOS ANGELES COMMUNITY COLLEGE DISTRICT Executive Committee of the District Budget Committee January 2012 Chancellor Dr. Daniel J. LaVista Jeanette L. Gordon, Chair Academic Senate/Faculty/Union David E. Beaulieu Dr. Allison Moore John McDowell (alternate) Carl Friedlander, DBC Co-chair Velma Butler College Presidents Dr. Kathleen Burke-Kelly Dr. Jack E. Daniels, III, DBC Co-chair Vice Presidents Dr. Ann Tomlinson Renee Martinez Deputy Chancellor Dr. Adriana Barrera

3 After several months of meetings discussing and reviewing allocation models of the other multi-campus districts, and discussing various alternate scenarios for allocating the District s revenues in a manner that would provide enough funding to cover college basic operations, the Committee recommends to the District Budget Committee for review to increase the colleges basic allocation to include minimum administrative staffing costs and maintenance and operations (M&O) costs. Details of the recommendation are provided on page 3. Recognizing that the changes will result in allocation reductions to some colleges and increases to other colleges, the Committee further recommends providing transition funding adjustments to those colleges that receive allocation reductions. This recommendation was not supported by the entire committee. Two members voted against it. Below is the rationale for the recommendation: RATIONALE TO SUPPORT CHANGES All colleges should have the minimum basic funding to support operations and should be allowed to offer a full menu of programs and services to serve their communities. The current District budget allocation is modeled on the State SB 361 funding model. It is a revenue model based on enrollment (FTES generation) and decentralized budgeting in which colleges receive their allocations and set their own budget priorities to meet their program and service needs. It does not address in a meaningful way the differences in expenditures among the colleges that result from a variety of factors (e.g. scale, program mix, square footage, acreage, utilities costs, FT/PT ratio, etc.). The State funding model has provided a clear and simpler distribution of funds received from the State to college districts. However, this model has, over time, disproportionately impacted college operations in the following key ways: 1. The model has contributed to the extreme variations in the fiscal conditions of the individual colleges, with ELAC carrying massive balances, several colleges chronically in debt, and other colleges in between. These huge differences make District decision-making more difficult. 2. The current annual basic allocation for each college is based on the State s SB 361 model for large, medium, and small colleges 1

4 plus $500,000 supplemental allocation for four small colleges and Trade-Technical College. This basic allocation does not cover the minimum administrative staff and M&O costs. At the state level, small colleges have been exempted from the apportionment cuts associated with workload reductions in recognition of the fact that the state s foundation grants are insufficient. 3. The formula does not make provision for the subsequent year costs of collective bargaining and other mandated decisions (FON- Faculty Obligation Number). 4. Under the current mechanism, the growth cap for all colleges is the same. There is no mechanism for assigning different growth caps to different colleges based on service area density, participation rates, need to grow to achieve greater economy of scale or other factors. (the ECDBC believes that the issue of differential growth rates should be taken up in the next phase of the DBC s work on the LACCD allocation mechanism). The recommended change to the minimum college base funding allocation is premised on the concept that each college will receive a minimum operational funding level to open the doors to students. 2

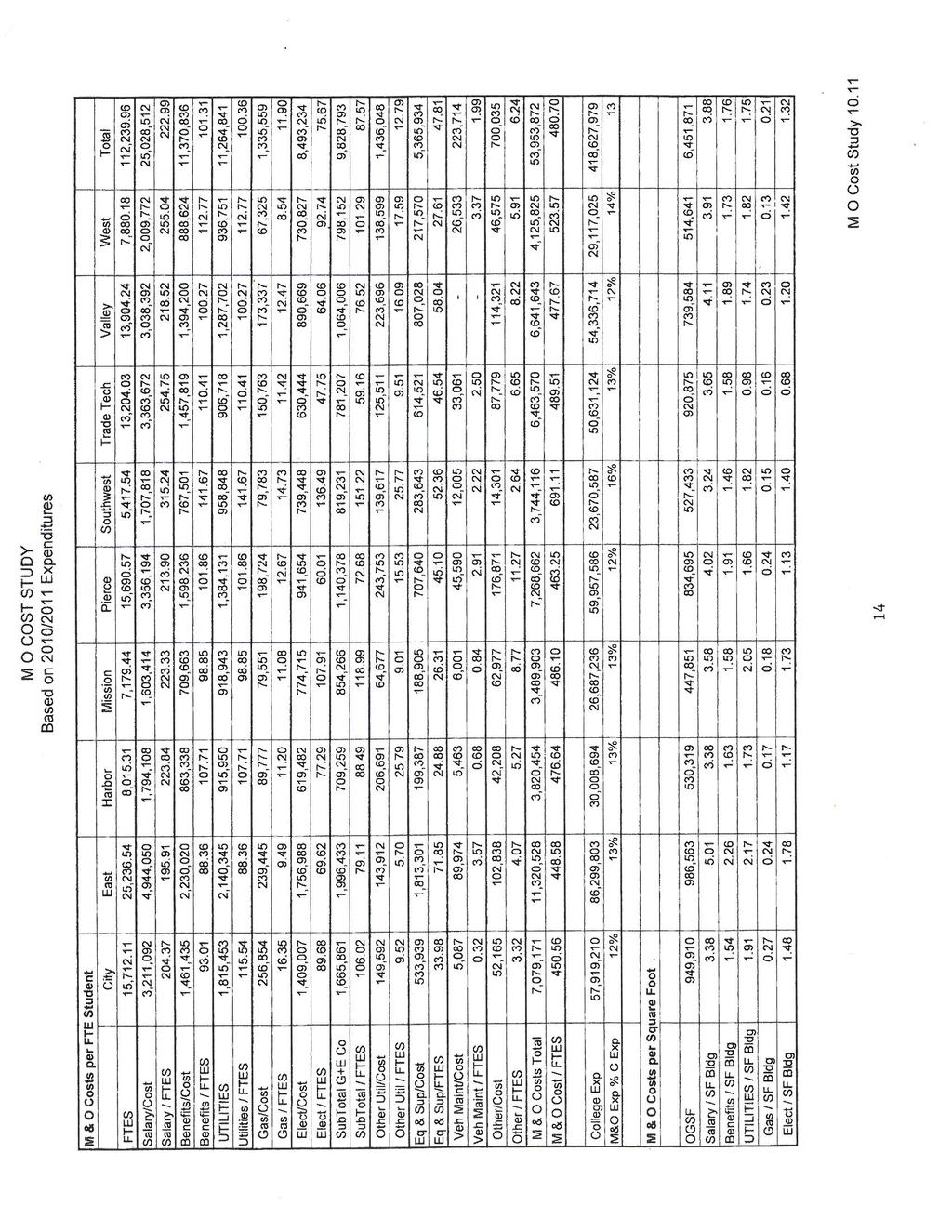

5 RECOMMENDATION: A. Increase the colleges basic allocation to include minimum administrative staffing costs and maintenance and operations (M&O) costs. Each college shall receive an annual base allocation to fully fund the following: 1. Minimum Administrative Staffing: a. (1) President, b. (3) Vice Presidents, (Academic Affairs, Student Services, Administrative Services) c. (1) Institutional Research Dean, d. (1) Facilities Manager, e. Deans i. (4) Deans => small colleges (FTES<10,000), ii. (8) Deans => medium colleges (FTES >= 10,000 and < 20,000), iii. (12) Deans => large colleges (FTES>= 20,000); 2. Maintenance and Operations costs based on average cost per gross square foot After allocating the minimum base allocation in items 1 and 2 above, all remaining revenue (except non-resident tuition, dedicated revenue, and apprenticeship revenue) shall be distributed to colleges based on their proportionate share (according to funded FTES) of the revenue being allocated to the colleges. B. Transition Funding Adjustment: The colleges that experience financial disadvantage (allocation reduction) as a result of the implementation of this change shall only be assessed 50% of the allocation reduction amount during the first three years of this implementation. Complete Allocation Simulation is provided in Attachment I (pages 12-15), Proposed Minimum Base Funding and M&O Costs Study; and Attachment II (pages 16-22), Proposed Budget Allocation. These attachments provide the calculation used to formulate the proposed minimum base funding and a comparison with the current allocation model. 3

6 BACKGROUND Since 2007, the District has allocated funds to colleges using the current District Budget Allocation model which was based on the State SB361 funding model. It is a revenue model based on enrollment and decentralized funding in which colleges receive their allocations and set their own budget priorities to meet their program and service needs. It has served the District well by providing the colleges with the revenue generated from enrollment growth over the years. State general revenue earned by colleges is distributed to colleges less assessments to pay for centralized expenditures, district office functions and services, and set-aside funds for contingency reserve. Changes have been made in the past to provide additional funding to increase college basic allocations for small colleges (H, M, SW, and W). There was also an increase to the basic allocation of Los Angeles Trade-Technical College in recognition of the college s high proportion of high-cost CTE programs. I. RESOURCE ALLOCATION AND FUNDING ISSUES Over the last five years that the District has used this funding mechanism, several colleges have consistently ended the year with expenditures in excess of revenue. Colleges' Open Orders and Balances From through City 1,915, ,648 (2,316,097) 1,927,063 2,909,368 East 16,982,624 21,290,288 19,068,973 25,898,669 31,268,204 Harbor (873,408) (3,048,065) (2,441,782) (1,708,181) 435,931 Mission (522,672) 330, , ,270 1,413,901 Pierce 7,564,192 8,697,811 8,454,681 9,603,360 9,785,035 Southwest (838,218) (1,611,551) (1,364,784) (1,466,650) (1,757,597) Trade-Tech 150,951 (2,079,123) 107,679 1,484,552 2,078,957 Valley (81,280) (1,735,776) (460,779) (531,310) (315,686) West 1,091, ,909 (596,118) 228,484 1,733,917 ITV 116,139 31, , , ,984 4

7 In August 2010, the Chancellor reconvened the Fiscal Policy and Review Committee (FPRC), to address the state budget reduction impact on the District for fiscal years and , and tasked the Committee with reviewing the budget allocation model. II. WHAT HAS BEEN STUDIED AND DISCUSSED? Since March 2011, the Executive Committee of the District Budget Committee (formerly FPRC) has been reviewing the budget allocation model. The Committee has reviewed the following analysis and information: A. Current resource allocation and funding issues. The following funding issues were identified for the Committee to review: 1. College base allocation that may not be sufficient for college to operate, 2. Growth allocation formula, 3. District-wide assessments for centralized functions and services, district offices, contingency reserve, and college supplemental allocation to the college base, 4. District reserve and balance policy, and 5. College deficits and debt repayment policy. The current funding drivers (basic allocation and funding per credit, noncredit, and enhanced noncredit rates) under the current budget allocation model (SB361), and assessments (cost per funded FTES) were reviewed Expenditures and Preliminary Allocation were analyzed to further understanding of how the current budget mechanism distributed the available revenue to colleges. Assessments were reviewed for District Office, Information Technology, Centralized Services, Faculty Overbase, Base Supplemental Allocation, and Contingency Reserve. Various funding issues such as equity, insufficiency, economy of scale (small colleges), and dedicated revenue (other) generated by colleges were also studied. A comparison of cost per FTES and net funding per FTES among colleges showed that several colleges received less funding than the projected expenditures and other colleges have a large balance to keep. Possible solutions are to allow colleges to grow at different rates to allow them to generate sufficient enrollment to cover expenses and to restrict the keeping of balance to a certain percentage of the college budget to control the size of college balances. 5

8 B. Analysis of Small Colleges and Resource Allocation Mechanism (Mr. Larry Serot Report, Consultant, November 2009, former Executive Vice President for the Glendale CCD) The Committee reviewed Mr. Serot s report on the analysis of the current resource allocation mechanism used by the District and his recommendations. The current budget allocation funding has consistently resulted in four colleges - Harbor, Mission, Southwest, and West - ending the fiscal year with expenditures in excess of revenues. An analysis of operating costs at the four colleges was made in comparison with five single-college districts and ten colleges within multi-college districts, as well as a comparison of costs for each college with the average of the other eight LACCD colleges. A review of the workings of the allocation mechanism was also performed. Following are the excerpts of findings and recommendations from Mr. Larry Serot s report: Findings 1. The total operating costs per FTES for three of the four colleges are not significantly out of line with the costs of the 15 comparison colleges. 2. The instructional efficiency and productivity of the four colleges is low in comparison to other L.A. colleges and is a result of a failure to adequately budget for part-time faculty and to use the part-time faculty budget as a control for instructional efficiency. 3. The four colleges consistently use the 1300 Object series, Teacher, Hourly, as a means to balance their operating budget against their budget allocation. This in turn leads to regular and significant over expenditures in this Object series, which often results in over expending the entire budget. 4. Staffing Costs per FTES are higher than the averages of the L.A. colleges and only Mission College shows a reduction in classified staff during fiscal years in which over expenditures have occurred. 5. The four colleges should work to improve instructional productivity, thereby reducing costs and they should develop a comprehensive staffing plan that considers efficiency and recognizes their limited funding. 6. The current resource allocation mechanism, based on the State s SB 361 model, does not adequately fund the smaller colleges. The current mechanism has a number of flaws: 6

9 It caps growth at all colleges at the same percentage cap as that received by the District. Large Colleges such as East and Pierce receive more dollars than the smaller colleges. By allocating funding on the basis of FTES that is capped, smaller colleges do not have the ability to grow into efficiency. Colleges such as Harbor and Southwest, which seem to have difficulty growing, are at a constant disadvantage. Treating over expenditures as loans to be paid back over three years has merit but the smaller colleges, which appear to be under funded by the formula, are placed into a deeper hole by such a mechanism making it even more difficult for them to stay within their budget. With no efficiency or productivity component, colleges are driven to grow at whatever cost which creates budget overdrafts and a worsening efficiency. The formula has produced a situation where several colleges receive funding in excess of their operating costs while others consistently over expend their budgets. The formula does not make provisions for the subsequent year costs of collective bargaining decisions which can have a negative effect on colleges that are not growing. 7. Colleges are allowed to establish budgets that have no internal integrity. This is most obvious in the consistent use of the 1300 Object accounts as the mechanism for balancing the budget even though historical expenditures clearly indicate that the budget is inadequate. Colleges are then allowed to over expend these accounts with apparent impunity. There appears to be no disincentive to management for playing this game year in and year out. Budgets lose their value as control mechanisms. Recommendations 1. The District should re-evaluate its existing resource allocation mechanism. Two options are suggested: The first is to modify the existing model to make it more responsive to the operating costs of smaller colleges. Three modifications are suggested: 1) Increase the Base Allocation, and use the same base for each college. 7

10 2) The funding assessment for the District Office, Districtwide Centralized Services, and the Contingency Reserve should be based on a percent of budget with larger colleges paying a larger percentage. 3) Allocate growth funds in the year following the year earned. Distribute growth funds to smaller colleges at their actual growth rate rather than the capped growth rate if the smaller college increases FTES through improved efficiency and productivity. The second is to re-evaluate the use of a revenue based model and consider one that looks at costs, productivity and efficiency. Several suggestions are offered: 1) A base allocation for each college should be constructed based on the determination of Full-Time Equivalent Faculty computed using a predetermined level of WSCH/FTEF, a staffing plan for all non classroom staff based upon an agreed upon level of efficiency, and a standard cost for utilities. 2) An allocation of funds based on FTES should be used to distribute the remaining available funds. 3) Allocate growth funds in the year following the year earned. Distribute growth funds to smaller colleges at their actual growth rate rather than the capped growth rate if the smaller college increases FTES through improved efficiency and productivity. 4) Operating deficits may be treated as alone in the first year, but deficits should not be accumulated. Continuous deficits should be seen as a failure of management and corrective personnel action should be taken. 2. The operating costs of the smaller colleges should be reduced by improving instructional efficiency and productivity and by managing noninstructional staffing through a well thought out and conservative staffing plan. 3. Realistic operating budgets should be developed that can be used as a means to control expenditures and eliminate over spending. C. Review of Ventura CCD Budget Model The Committee reviewed the Ventura CCD budget model. Ventura CCD has three colleges and distributes its Unrestricted General Fund to various operating units based on the following methodology: 8

11 1. Fund district-wide support, such as insurance, legal, audit costs, etc., based on the proposed expenses (similar to funding for LACCD s Centralized Services) 2. Fund utilities as district-wide costs 3. Fund District Administrative Center (District Office) at 6.4% of available Unrestricted General Fund Revenue 4. Transition funding and college initiatives set-aside funds 5. Remainder of available revenue distributed to colleges as follows: - Base allocation 15% of the revenue available for distribution and divided equally among colleges - Class schedule delivery allocation productivity factor and fulltime faculty staffing - FTES adjustment and cost allocations need to verify what this is? - FTES Allocation remaining revenue distributed to colleges proportionate to the college s percent of total FTES 6. Application of carryover allowed to carry over up to 1% of their prior year Unrestricted General Fund Budget A simulation of LACCD budget distribution based on the Ventura CCD budget model was presented and reviewed by the committee. D. Review of San Diego CCD Budget Model The Committee reviewed the San Diego CCD budget model. San Diego CCD has three colleges and distributes its Unrestricted General Fund to various operating units based on the cost allocation model, as follows: 1. Fund set-asides and reserve estimates. Set-aside amounts are approved expenditure/budget items that will have future impact, either in the current year or future years, and are known at the point of budget preparation. 2. Fund District Office Department Budgets. The District Office budgets are by department. Within each department, there are budgets for office operations and custodial, district-wide budgets. Projections are made based on current position and expense information. 3. Fund Campus Budgets based on the following data: FTEF Allocations and Campus FTEF Budget Plans Department Chair ESU s, Reassign Time FTEF, and 11-Month Contracts Current Year Salary & Benefit Amounts (Contract Positions) 9

12 Annual Rates for Adjunct, Overload, Substitutes, and ESU s Computing Pro-Rata Allocations Determining Other Adjusting Contractual Items Computing Discretionary Funding Funding for Sabbatical Leaves Funding for Vacant Positions Funding for Faculty Promotion E. Review of Los Rios CCD Budget Model The Committee reviewed the Los Rios CCD budget model. Los Rios CCD utilizes an allocation formula that distributes funds into two categories: (1) Compensation Fund Bucket and (2) Program Development Fund. The Compensation Fund Bucket is computed for salaries and benefits and grouped by bargaining unit. The Program Development Funds are to cover operational costs, including utilities and district administrative costs. Base Revenues for these two categories are from the existing resources available in the previous year and are driven by the formula. New Revenue will be distributed as 80% to the Compensation Bucket to cover salaries and benefits; and 20% to the Program Development Fund to cover operating costs. The allocation model is rather complicated and requires working in cooperation with the bargaining units to determine the 80/20 split for funding between the two categories. III. Remaining Allocation Areas Identified for Review and Change After several months of reviewing the District s current budget allocation formula and other multi-campus districts budget allocation formulas, the Executive Committee of the DBC (ECDBC) spent a significant amount of time determining the appropriate funding level for the college funding allocation. The Committee has tentatively agreed to maintain the framework of the current SB361 funding allocation mechanism, and has identified the following possible changes to the existing model to provide adequate funding for colleges to sustain operations: 1. Increase the basic allocation to cover minimum administrative costs and M&O costs. 2. Set a limited percentage of future college balances allowed to be carried forward. 10

13 3. The funding assessment for the District Office, District-wide Centralized Services, and the Contingency Reserve should be based on a percent of budget with larger colleges paying a larger percentage. 4. Fund colleges using a differential growth rate based on an agreed-upon instructional growth target and productivity level rather than on the State capped growth rate. 5. The operating costs of colleges should reflect efficiency and improvement in productivity by management of non-instructional staffing through a well thought-out and conservative staffing plan. 6. Operating deficits may be treated as a loan in the first year, but deficits should not be accumulated. On November 28, 2011, the ECDBC felt that it would be too much to implement all the suggested changes at once. Instead, Recommendation #1 should be implemented first, to increase the basic allocation to cover minimum administrative costs and M&O costs, and other recommended changes should be deferred for future discussion. On January 5, 2012, the Committee voted 7 to 2 votes to recommend to the DBC the increase of the basic allocation to cover minimum administrative costs and M&O costs as delineated in the Recommendation (page 3). 11

14

15

16

17

18

19

20

21

22

23

24

25

26

Los Angeles Community College District Budget Allocation Model

Los Angeles Community College District Budget Allocation Model 1 FUNDS ALLOCATION MECHANISM State Funds Revenue + Balances K-14 Share Community College Share Base Revenue COLA Growth Decline on Enrollment/Adjust.

Los Angeles Community College District Budget Allocation Model 1 FUNDS ALLOCATION MECHANISM State Funds Revenue + Balances K-14 Share Community College Share Base Revenue COLA Growth Decline on Enrollment/Adjust.

Los Angeles Community College District

Los Angeles Community College District District Budget Committee Meeting Minutes April 24, 2013 1:30-3:30 p.m., Board Room, District Office Roll Call Committee members present as indicated (X). Academic

Los Angeles Community College District District Budget Committee Meeting Minutes April 24, 2013 1:30-3:30 p.m., Board Room, District Office Roll Call Committee members present as indicated (X). Academic

Los Angeles Community College District

Los Angeles Community College District District Budget Committee Meeting Minutes May 22, 2013 1:30-3:30 p.m., Board Room, District Office Roll Call Committee members present as indicated (X). Academic

Los Angeles Community College District District Budget Committee Meeting Minutes May 22, 2013 1:30-3:30 p.m., Board Room, District Office Roll Call Committee members present as indicated (X). Academic

VENTURA COUNTY COMMUNITY COLLEGE DISTRICT DISTRICTWIDE RESOURCE BUDGET ALLOCATION MODEL GENERAL FUND UNRESTRICTED BUDGET. Fiscal Year

VENTURA COUNTY COMMUNITY COLLEGE DISTRICT DISTRICTWIDE RESOURCE BUDGET ALLOCATION MODEL GENERAL FUND UNRESTRICTED BUDGET Fiscal Year 2017-18 I. Introduction The Districtwide Resource Budget Allocation

VENTURA COUNTY COMMUNITY COLLEGE DISTRICT DISTRICTWIDE RESOURCE BUDGET ALLOCATION MODEL GENERAL FUND UNRESTRICTED BUDGET Fiscal Year 2017-18 I. Introduction The Districtwide Resource Budget Allocation

VENTURA COUNTY COMMUNITY COLLEGE DISTRICT DISTRICTWIDE RESOURCE BUDGET ALLOCATION MODEL GENERAL FUND UNRESTRICTED BUDGET. Fiscal Year

VENTURA COUNTY COMMUNITY COLLEGE DISTRICT DISTRICTWIDE RESOURCE BUDGET ALLOCATION MODEL GENERAL FUND UNRESTRICTED BUDGET Fiscal Year 2011-12 Background Effective in fiscal year 2003-04, the District set

VENTURA COUNTY COMMUNITY COLLEGE DISTRICT DISTRICTWIDE RESOURCE BUDGET ALLOCATION MODEL GENERAL FUND UNRESTRICTED BUDGET Fiscal Year 2011-12 Background Effective in fiscal year 2003-04, the District set

STATE CENTER COMMUNITY COLLEGE DISTRICT

STATE CENTER COMMUNITY COLLEGE DISTRICT Districtwide Resource Allocation Model General Fund Unrestricted Budget Fresno Reedley Madera Oakhurst Willow International Table of Contents Background... 3 Elements

STATE CENTER COMMUNITY COLLEGE DISTRICT Districtwide Resource Allocation Model General Fund Unrestricted Budget Fresno Reedley Madera Oakhurst Willow International Table of Contents Background... 3 Elements

BUDGET ALLOCATION MODEL. August 2017 Office of Budget and Management Analysis

BUDGET ALLOCATION MODEL August 2017 Office of Budget and Management Analysis General Fund FY 2015-16 2 3 SB361 CCC Funding Formula Effective October 1, 2006; State funding formula includes : Basic Allocation

BUDGET ALLOCATION MODEL August 2017 Office of Budget and Management Analysis General Fund FY 2015-16 2 3 SB361 CCC Funding Formula Effective October 1, 2006; State funding formula includes : Basic Allocation

Budget Allocation Model

Budget Allocation Model Peralta Community College District Berkeley City College College of Alameda Laney College Merritt College Adopted by the Planning and Budgeting Council May 20, 2011 Revised February

Budget Allocation Model Peralta Community College District Berkeley City College College of Alameda Laney College Merritt College Adopted by the Planning and Budgeting Council May 20, 2011 Revised February

Contra Costa Community College District SB 361 Allocation Model FREQUENTLY ASKED QUESTIONS. April 9, 2010

Contra Costa Community College District SB 361 Allocation Model FREQUENTLY ASKED QUESTIONS April 9, 2010 General Inquiries 1. When will the new allocation model be approved by the Governing Board? Will

Contra Costa Community College District SB 361 Allocation Model FREQUENTLY ASKED QUESTIONS April 9, 2010 General Inquiries 1. When will the new allocation model be approved by the Governing Board? Will

Contra Costa Community College District SB 361/College First Allocation Model Proposal November 25, 2009

Introduction Contra Costa Community College District SB 361/College First Allocation Model Proposal November 25, 2009 Why develop a new allocation model? For many years, the District has used a funding

Introduction Contra Costa Community College District SB 361/College First Allocation Model Proposal November 25, 2009 Why develop a new allocation model? For many years, the District has used a funding

Rancho Santiago Community College District Budget Allocation Model Based on SB 361

Updated November 16, 2016 Rancho Santiago Community College District Budget Allocation Model Based on SB 361 The Rancho Santiago Community College District Budget Allocation Model Based on SB361, February

Updated November 16, 2016 Rancho Santiago Community College District Budget Allocation Model Based on SB 361 The Rancho Santiago Community College District Budget Allocation Model Based on SB361, February

Peralta Community College Budget Allocation Model. BAM November 17, 2014

Peralta Community College Budget Allocation Model BAM November 17, 2014 Modeled after SB 361 Used for funding apportionment for all California Community Colleges 3 fundamental revenue drivers Base allocation

Peralta Community College Budget Allocation Model BAM November 17, 2014 Modeled after SB 361 Used for funding apportionment for all California Community Colleges 3 fundamental revenue drivers Base allocation

SOUND FISCAL MANAGEMENT Self-Assessment Checklist

SOUND FISCAL MANAGEMENT Self-Assessment Checklist for Fiscal Year Ended June 30, 2015 (Completed January 2016) 1. Deficit Spending: Is this area acceptable? Yes Is the district spending within their revenue

SOUND FISCAL MANAGEMENT Self-Assessment Checklist for Fiscal Year Ended June 30, 2015 (Completed January 2016) 1. Deficit Spending: Is this area acceptable? Yes Is the district spending within their revenue

Coast Community College District ADMINISTRATIVE PROCEDURE Chapter 6 Business and Fiscal Affairs BUDGET PREPARATION

Coast Community College District ADMINISTRATIVE PROCEDURE Chapter 6 Business and Fiscal Affairs AP 6200 BUDGET PREPARATION New Proposed AP Draft 11/06/13 04/11/14 Legal References: Education Code Section

Coast Community College District ADMINISTRATIVE PROCEDURE Chapter 6 Business and Fiscal Affairs AP 6200 BUDGET PREPARATION New Proposed AP Draft 11/06/13 04/11/14 Legal References: Education Code Section

SOUND FISCAL MANAGEMENT Self-Assessment Checklist

SOUND FISCAL MANAGEMENT Self-Assessment Checklist for Fiscal Year Ended June 30, 2014 (Completed January 2015) 1. Deficit Spending: Is this area acceptable? Yes Is the district spending within their revenue

SOUND FISCAL MANAGEMENT Self-Assessment Checklist for Fiscal Year Ended June 30, 2014 (Completed January 2015) 1. Deficit Spending: Is this area acceptable? Yes Is the district spending within their revenue

Los Angeles City College Budget Forum. June 5, FY15 Preliminary College Budget

Los Angeles City College Budget Forum June 5, 2014 FY15 Preliminary College Budget Renee D. Martinez, President John al-amin, Vice President, Administrative Services GOVERNOR S BUDGET MAY REVISE HIGHLIGHTS

Los Angeles City College Budget Forum June 5, 2014 FY15 Preliminary College Budget Renee D. Martinez, President John al-amin, Vice President, Administrative Services GOVERNOR S BUDGET MAY REVISE HIGHLIGHTS

$97.6 million for a 1.56% cost of living adjustment (COLA) to the unrestricted general state apportionment

to the unrestricted general state apportionment") 2017-18 State Budget - Impact to Community Colleges The state budget will include the following items: $97.6 million for a 1.56% cost of living adjustment (COLA) to the unrestricted general state apportionment

2017-18 State Budget - Impact to Community Colleges The state budget will include the following items: $97.6 million for a 1.56% cost of living adjustment (COLA) to the unrestricted general state apportionment

Budget Update March 7, Kevin McElroy, Vice Chancellor, Business Services Bernata Slater, Budget Director

Budget Update March 7, 2012 Kevin McElroy, Vice Chancellor, Business Services Bernata Slater, Budget Director Current State Outlook for 2012/13 The state economy is improving, but there is still a structural

Budget Update March 7, 2012 Kevin McElroy, Vice Chancellor, Business Services Bernata Slater, Budget Director Current State Outlook for 2012/13 The state economy is improving, but there is still a structural

December 9, 2009 CONTRA COSTA COMMUNITY COLLEGE DISTRICT RESOURCE ALLOCATION

December 9, 2009 CONTRA COSTA COMMUNITY COLLEGE DISTRICT RESOURCE ALLOCATION WHY DEVELOP A NEW MODEL? Allocation formulas not aligned to revenues FTE for faculty, management historical FTE Classified formula

December 9, 2009 CONTRA COSTA COMMUNITY COLLEGE DISTRICT RESOURCE ALLOCATION WHY DEVELOP A NEW MODEL? Allocation formulas not aligned to revenues FTE for faculty, management historical FTE Classified formula

District Budget Forums

District Budget Forums (Traveling Road Show) 2006-07 Budget Development May 1-10, 2006 Presented by: Helen Benjamin, Chancellor Doug Roberts, Acting Vice Chancellor, Finance & Administration PURPOSE To

District Budget Forums (Traveling Road Show) 2006-07 Budget Development May 1-10, 2006 Presented by: Helen Benjamin, Chancellor Doug Roberts, Acting Vice Chancellor, Finance & Administration PURPOSE To

FINAL BUDGET

FINAL BUDGET 2017-2018 Office of the Chancellor September 2017 Los Angeles Community College District BOARD OF TRUSTEES Sydney K. Kamlager, President Mike Fong, Vice President Gabriel Buelna, Ph.D. Andra

FINAL BUDGET 2017-2018 Office of the Chancellor September 2017 Los Angeles Community College District BOARD OF TRUSTEES Sydney K. Kamlager, President Mike Fong, Vice President Gabriel Buelna, Ph.D. Andra

BOARD OF TRUSTEES MEETING August 22, 2016

BOARD OF TRUSTEES MEETING August 22, 2016 Board Budget Development Guidelines Guiding Principles: The following guiding principles are provided to the District Resources Allocation Council (DRAC) and the

BOARD OF TRUSTEES MEETING August 22, 2016 Board Budget Development Guidelines Guiding Principles: The following guiding principles are provided to the District Resources Allocation Council (DRAC) and the

Linking Strategic Planning to Budget

1 District Mission Linking Strategic Planning to Budget GCCCD 2016-2022 Mission, Vision, Goals Provide outstanding diverse learning opportunities that prepare students to meet community needs, promotes

1 District Mission Linking Strategic Planning to Budget GCCCD 2016-2022 Mission, Vision, Goals Provide outstanding diverse learning opportunities that prepare students to meet community needs, promotes

SOUTHWEST TENNESSEE COMMUNITY COLLEGE

SOUTHWEST TENNESSEE COMMUNITY COLLEGE Policy No. 4:00:00:00/2 Page 1 of 12 SUBJECT: Budget Policies and Procedures EFFECTIVE DATE: July 1, 2000; Revised: May 31, 2013. I Index I Index 1 II Introduction

SOUTHWEST TENNESSEE COMMUNITY COLLEGE Policy No. 4:00:00:00/2 Page 1 of 12 SUBJECT: Budget Policies and Procedures EFFECTIVE DATE: July 1, 2000; Revised: May 31, 2013. I Index I Index 1 II Introduction

Planning & Budget Meeting

Planning & Budget Meeting April 15, 2014 THE PLANNING AND BUDGET COMMITTEE is the participatory governance committee responsible for recommending budget priorities, procedures, and processes to the College

Planning & Budget Meeting April 15, 2014 THE PLANNING AND BUDGET COMMITTEE is the participatory governance committee responsible for recommending budget priorities, procedures, and processes to the College

Ventura County Community College District

Background The District currently distributes nearly all its unrestricted resources through a single funding allocation model. Those resources include state apportionment (enrollment fees, property taxes

Background The District currently distributes nearly all its unrestricted resources through a single funding allocation model. Those resources include state apportionment (enrollment fees, property taxes

SANTA BARBARA CITY COLLEGE COLLEGE PLANNING COUNCIL February 4, :00-4:30 PM Room A218C

SANTA BARBARA CITY COLLEGE COLLEGE PLANNING COUNCIL February 4, 2003 3:00-4:30 PM Room A218C MINUTES PRESENT: GUESTS: J. Friedlander, B. Fahnestock, S. Ehrlich, L. Fairly, B. Hamre, K. Mclellan, A. Serban,

SANTA BARBARA CITY COLLEGE COLLEGE PLANNING COUNCIL February 4, 2003 3:00-4:30 PM Room A218C MINUTES PRESENT: GUESTS: J. Friedlander, B. Fahnestock, S. Ehrlich, L. Fairly, B. Hamre, K. Mclellan, A. Serban,

Planning Driven Budget Development Process

Planning Driven Budget Development Process BUDGET DEVELOPMENT COMMITTEE Adopted by the Budget Committee on May 19, 2016 MT. SAN JACINTO COLLEGE INTRODUCTION The Mt. San Jacinto College District resource

Planning Driven Budget Development Process BUDGET DEVELOPMENT COMMITTEE Adopted by the Budget Committee on May 19, 2016 MT. SAN JACINTO COLLEGE INTRODUCTION The Mt. San Jacinto College District resource

ACCCA s Administration 101 July 25, 2016

ACCCA s Administration 101 July 25, 2016 Dr. Bonnie Ann Dowd Executive Vice Chancellor, Business and Technology Services San Diego Community College District Peter Hardash Vice Chancellor Business Operations/Fiscal

ACCCA s Administration 101 July 25, 2016 Dr. Bonnie Ann Dowd Executive Vice Chancellor, Business and Technology Services San Diego Community College District Peter Hardash Vice Chancellor Business Operations/Fiscal

Sequoias Community College District RESOURCE

RESOURCE A L L O C AT I O N Sequoias Community College District College of the Sequoias 2013 Resource Allocation Manual College of the Sequoias Community College District Visalia Campus 915 S. Mooney Blvd.

RESOURCE A L L O C AT I O N Sequoias Community College District College of the Sequoias 2013 Resource Allocation Manual College of the Sequoias Community College District Visalia Campus 915 S. Mooney Blvd.

Cabrillo College Governing Board Monday, February 14, 2011 Cabrillo College Sesnon House 6500 Soquel Drive Aptos, California 95003

Cabrillo College Governing Board Monday, Cabrillo College Sesnon House 6500 Soquel Drive Aptos, California 95003 1 OPEN SESSION PAGE TIME 1. Call to Order and Roll Call 4:00 2. Adoption of Agenda 3. Public

Cabrillo College Governing Board Monday, Cabrillo College Sesnon House 6500 Soquel Drive Aptos, California 95003 1 OPEN SESSION PAGE TIME 1. Call to Order and Roll Call 4:00 2. Adoption of Agenda 3. Public

9 th Annual Budget Forum April 2014

9 th Annual Budget Forum April 2014 Presenters: Helen Benjamin Chancellor Gene Huff Executive Vice Chancellor Jonah Nicholas Associate Vice Chancellor GOALS Information Arzu Smith Director of District

9 th Annual Budget Forum April 2014 Presenters: Helen Benjamin Chancellor Gene Huff Executive Vice Chancellor Jonah Nicholas Associate Vice Chancellor GOALS Information Arzu Smith Director of District

PIERCE COLLEGE Budget Crisis: Impact on Pierce College

2012-2013 Budget Crisis: Impact on Pierce College District Budget Process State Identifies Allocation to LACCD LACCD allocates funds to all Colleges PIERCE prepares Preliminary Budget and submits to District

2012-2013 Budget Crisis: Impact on Pierce College District Budget Process State Identifies Allocation to LACCD LACCD allocates funds to all Colleges PIERCE prepares Preliminary Budget and submits to District

California Community Colleges/Districts Funding Model Proposal Submitted to Chancellor Oakley December 20, 2017

NOTE as of January 29, 2018: The CCC Funding Model Proposal recommendations by the Advisory Workgroup on Fiscal Affairs was provided to Chancellor Oakley prior to the release of the Governor s 2018-19

NOTE as of January 29, 2018: The CCC Funding Model Proposal recommendations by the Advisory Workgroup on Fiscal Affairs was provided to Chancellor Oakley prior to the release of the Governor s 2018-19

GENERAL CAMPUS COMPENSATION PLAN TRIAL (GCCP) FAQ Last updated 03/16/18

FAQ Last updated 03/16/18") GENERAL CAMPUS COMPENSATION PLAN TRIAL (GCCP) FAQ Last updated 03/16/18 Eligibility and Approvals 1. Q: Who is eligible to participate? A: Ladder rank and In-Residence professors in participating general

GENERAL CAMPUS COMPENSATION PLAN TRIAL (GCCP) FAQ Last updated 03/16/18 Eligibility and Approvals 1. Q: Who is eligible to participate? A: Ladder rank and In-Residence professors in participating general

Los Rios Community College District Tentative Budget Presented to the Board of Trustees June 8, 2016

Los Rios Community College District 2016 17 Tentative Budget Presented to the Board of Trustees June 8, 2016 Los Rios Community College District 2016 17 Tentative Budget Proposed State Budget Projections

Los Rios Community College District 2016 17 Tentative Budget Presented to the Board of Trustees June 8, 2016 Los Rios Community College District 2016 17 Tentative Budget Proposed State Budget Projections

Presentation to the District Budget Advisory Committee March 14, 2013

Presentation to the District Budget Advisory Committee March 14, 2013 Presented by Andy Dunn, Vice Chancellor Finance and Administrative Services Inspiration. Innovation. Graduation. Discussion Budget

Presentation to the District Budget Advisory Committee March 14, 2013 Presented by Andy Dunn, Vice Chancellor Finance and Administrative Services Inspiration. Innovation. Graduation. Discussion Budget

STANDARD OPERATING PROCEDURE

Page 1 of 8 STANDARD OPERATING PROCEDURE DEPARTMENT: Business and Admin. Services TITLE: College Budget Planning PURPOSE: The College President, in consultation with the President s Executive Council (EC),

Page 1 of 8 STANDARD OPERATING PROCEDURE DEPARTMENT: Business and Admin. Services TITLE: College Budget Planning PURPOSE: The College President, in consultation with the President s Executive Council (EC),

SUMMARY OF KEY BUDGET MODEL ISSUES WITH RECOMMENDATIONS

SUMMARY OF KEY BUDGET MODEL ISSUES WITH RECOMMENDATIONS The current budget model used by UM-Flint was developed over several years by the Vice Chancellor for Administration and Director of Financial Services

SUMMARY OF KEY BUDGET MODEL ISSUES WITH RECOMMENDATIONS The current budget model used by UM-Flint was developed over several years by the Vice Chancellor for Administration and Director of Financial Services

SANTA BARBARA CITY COLLEGE ASSUMPTIONS USED TO DEVELOP THE ADOPTED BUDGET Board of Trustees Study Session June 14, 2012

SANTA BARBARA CITY COLLEGE ASSUMPTIONS USED TO DEVELOP THE 2012-13 ADOPTED BUDGET Board of Trustees Study Session June 14, 2012 The budget revenue assumptions are from the Annual Statewide Budget Workshop

SANTA BARBARA CITY COLLEGE ASSUMPTIONS USED TO DEVELOP THE 2012-13 ADOPTED BUDGET Board of Trustees Study Session June 14, 2012 The budget revenue assumptions are from the Annual Statewide Budget Workshop

Terms Related to Budgeting. Dr. Richard L. Brown

Terms Related to Budgeting Dr. Richard L. Brown TYPES OF BUDGETS Generally there are two types of budgets: OPERATING (MAINTENANCE) a plan, including unrestricted and restricted revenues and expenditures,

Terms Related to Budgeting Dr. Richard L. Brown TYPES OF BUDGETS Generally there are two types of budgets: OPERATING (MAINTENANCE) a plan, including unrestricted and restricted revenues and expenditures,

Standard III. D FINANCIAL RESOURCES

Standard III. D FINANCIAL RESOURCES III.D.1 Financial resources are sufficient to support and sustain student learning programs and services and improve institutional effectiveness. The distribution of

Standard III. D FINANCIAL RESOURCES III.D.1 Financial resources are sufficient to support and sustain student learning programs and services and improve institutional effectiveness. The distribution of

Transcript Budget Principles. Slide 1: Budget Principles. Slide 2: Student Learning Outcomes

Slide 1: Budget Principles How is this for a bold look? Hopefully this bold and bright red design will help to keep you awake and focused on some of the most important big picture budgeting principles.

Slide 1: Budget Principles How is this for a bold look? Hopefully this bold and bright red design will help to keep you awake and focused on some of the most important big picture budgeting principles.

California State University, Los Angeles University Resource Allocation Process for Change CURRENT ALLOCATION MODEL OVERVIEW

Overview California State University, Los Angeles University Resource Allocation Process for Change CURRENT ALLOCATION MODEL OVERVIEW The University Resource Allocation, as defined by Administrative Procedure

Overview California State University, Los Angeles University Resource Allocation Process for Change CURRENT ALLOCATION MODEL OVERVIEW The University Resource Allocation, as defined by Administrative Procedure

Campus Budget Submissions Due: August 19, 2008

System Budget Office 401 Golden Shore, 5 th Floor Long Beach, CA 90802-4210 562-951-4560 Fax 562-951-4971 www.calstate.edu/budget FINAL-Budget Act of 2008 was chaptered on 9/23/08, AB 1781, Chapter 268

System Budget Office 401 Golden Shore, 5 th Floor Long Beach, CA 90802-4210 562-951-4560 Fax 562-951-4971 www.calstate.edu/budget FINAL-Budget Act of 2008 was chaptered on 9/23/08, AB 1781, Chapter 268

Los Angeles Community College District

Los Angeles Community College District Basic Financial Statements and Supplemental Information June 30, 2016 and 2015 (With Independent Auditors Report Thereon) June 30, 2016 and 2015 Los Angeles County,

Los Angeles Community College District Basic Financial Statements and Supplemental Information June 30, 2016 and 2015 (With Independent Auditors Report Thereon) June 30, 2016 and 2015 Los Angeles County,

UNIVERSITY OF ILLINOIS AT URBANA-CHAMPAIGN FY 2017 BUDGET GUIDELINES

UNIVERSITY OF ILLINOIS AT URBANA-CHAMPAIGN FY 2017 BUDGET GUIDELINES SALARY RATE INCREASES At the time of issuing these guidelines, there is no general salary program except where union settlements dictate

UNIVERSITY OF ILLINOIS AT URBANA-CHAMPAIGN FY 2017 BUDGET GUIDELINES SALARY RATE INCREASES At the time of issuing these guidelines, there is no general salary program except where union settlements dictate

LOTTERY FUNDS SONOMA STATE UNIVERSITY. Audit Report May 7, 2014

LOTTERY FUNDS SONOMA STATE UNIVERSITY Audit Report 14-24 May 7, 2014 Lupe C. Garcia, Chair Adam Day, Vice Chair Rebecca D. Eisen Steven M. Glazer Hugo Morales Members, Committee on Audit Vice Chancellor

LOTTERY FUNDS SONOMA STATE UNIVERSITY Audit Report 14-24 May 7, 2014 Lupe C. Garcia, Chair Adam Day, Vice Chair Rebecca D. Eisen Steven M. Glazer Hugo Morales Members, Committee on Audit Vice Chancellor

LOS ANGELES COMMUNITY COLLEGE DISTRICT. Basic Financial Statements. June 30, (With Independent Auditors Report Thereon)

") Basic Financial Statements (With Independent Auditors Report Thereon) Los Angeles County, California: East Los Angeles College Los Angeles City College Los Angeles Harbor College Los Angeles Mission College

Basic Financial Statements (With Independent Auditors Report Thereon) Los Angeles County, California: East Los Angeles College Los Angeles City College Los Angeles Harbor College Los Angeles Mission College

Financial Management Guidelines and Procedures

The financial position and future of the Colorado School of Mines is dependent on several variables including enrollment, research growth, changes in industry demand, and competing institutions at the

The financial position and future of the Colorado School of Mines is dependent on several variables including enrollment, research growth, changes in industry demand, and competing institutions at the

LOS ANGELES COMMUNITY COLLEGE DISTRICT. June 30, 2003

Los Angeles Community College District Report on Audited Basic Financial Statements June 30, 2003 June 30, 2003 Los Angeles County, California: East Los Angeles College Los Angeles City College Los Angeles

Los Angeles Community College District Report on Audited Basic Financial Statements June 30, 2003 June 30, 2003 Los Angeles County, California: East Los Angeles College Los Angeles City College Los Angeles

Colorado School of Mines Board of Trustees Meeting June 18, Operating Budget for the Fiscal Year

Colorado School of Mines Board of Trustees Meeting June 18, 2004 Operating Budget for the 2004-05 Fiscal Year The campus Budget Committee met on June 10, 2004 to review and discuss the proposed budget.

Colorado School of Mines Board of Trustees Meeting June 18, 2004 Operating Budget for the 2004-05 Fiscal Year The campus Budget Committee met on June 10, 2004 to review and discuss the proposed budget.

Presentation to the District Budget Advisory Committee December 8, Presented by: Andy Dunn Vice Chancellor Finance & Administrative Services

Presentation to the District Budget Advisory Committee December 8, 2011 Presented by: Andy Dunn Vice Chancellor Finance & Administrative Services Areas of Discussion What Informs Coast s Institutional

Presentation to the District Budget Advisory Committee December 8, 2011 Presented by: Andy Dunn Vice Chancellor Finance & Administrative Services Areas of Discussion What Informs Coast s Institutional

District Budget Process

1. District Budget Development Process This is Jim Austin. In this lesson we are going to review the general process and timelines for the development and approval of California community college budgets.

1. District Budget Development Process This is Jim Austin. In this lesson we are going to review the general process and timelines for the development and approval of California community college budgets.

Planning & Budget Manual 13/14

Planning & Budget Manual 13/14 The mission of Santa Ana College is to be a leader and partner in meeting the intellectual, cultural, technological, workforce and economic development needs of our diverse

Planning & Budget Manual 13/14 The mission of Santa Ana College is to be a leader and partner in meeting the intellectual, cultural, technological, workforce and economic development needs of our diverse

March 2015 Board Budget Update

Please find below a Summary Report and Monthly Expenditure Chart for the Unrestricted General Fund summarizing the College s financial activity for fiscal year 2014-15 as of February 28, 2015. These summaries

Please find below a Summary Report and Monthly Expenditure Chart for the Unrestricted General Fund summarizing the College s financial activity for fiscal year 2014-15 as of February 28, 2015. These summaries

Office of the Provost University of Illinois at Urbana-Champaign. 3 February 2016

Office of the Provost University of Illinois at Urbana-Champaign BUDGET REPORT GUIDANCE FOR FY17: CTE, DRES, I 3, KAM, KCPA, SPURLOCK, UNIVERSITY LIBRARY, LAW LIBRARY 3 February 2016 The campus finds itself

Office of the Provost University of Illinois at Urbana-Champaign BUDGET REPORT GUIDANCE FOR FY17: CTE, DRES, I 3, KAM, KCPA, SPURLOCK, UNIVERSITY LIBRARY, LAW LIBRARY 3 February 2016 The campus finds itself

Fiscal Year Budget Planning & Outlook

Fiscal Year 2016-2017 Budget Planning & Outlook David Bea Executive Vice Chancellor for Finance and Administration Spring 2016 Major Factors Impacting Budget No State Appropriations Continued Enrollment

Fiscal Year 2016-2017 Budget Planning & Outlook David Bea Executive Vice Chancellor for Finance and Administration Spring 2016 Major Factors Impacting Budget No State Appropriations Continued Enrollment

The Who, What, Where and When of FON in California Community Colleges

The Who, What, Where and When of FON in California Community Colleges Presented by: Andy Suleski, Vice President, Administrative Services, Butte-Glenn CCD Kuldeep Kaur, Chief Business Officer, Yuba CCD

The Who, What, Where and When of FON in California Community Colleges Presented by: Andy Suleski, Vice President, Administrative Services, Butte-Glenn CCD Kuldeep Kaur, Chief Business Officer, Yuba CCD

MIRACOSTA COMMUNITY COLLEGE DISTRICT ANNUAL FINANCIAL REPORT JUNE 30, 2018

MIRACOSTA COMMUNITY COLLEGE DISTRICT ANNUAL FINANCIAL REPORT TABLE OF CONTENTS FINANCIAL SECTION Independent Auditor's Report 2 Management's Discussion and Analysis 5 Basic Financial Statements - Primary

MIRACOSTA COMMUNITY COLLEGE DISTRICT ANNUAL FINANCIAL REPORT TABLE OF CONTENTS FINANCIAL SECTION Independent Auditor's Report 2 Management's Discussion and Analysis 5 Basic Financial Statements - Primary

Santa Rosa Junior College Adopted Budget

Santa Rosa Junior College 2015-16 Adopted Budget SRJC Funds The District receives funds from a number of sources. However, much of that money is restricted and can only be spent for restricted purposes.

Santa Rosa Junior College 2015-16 Adopted Budget SRJC Funds The District receives funds from a number of sources. However, much of that money is restricted and can only be spent for restricted purposes.

Standard Operating Procedure. Summer Salary and Supplemental Pay for 9-Month Faculty. February 15, 2017 (First Issued May 1, 2012)

") Standard Operating Procedure Summer Salary and Supplemental Pay for 9-Month Faculty February 15, 2017 (First Issued May 1, 2012) I. Applicability Regulation 05.58.01 categorizes summer salary and supplemental

Standard Operating Procedure Summer Salary and Supplemental Pay for 9-Month Faculty February 15, 2017 (First Issued May 1, 2012) I. Applicability Regulation 05.58.01 categorizes summer salary and supplemental

Presentation on New Student Centered Funding Formula Proposal and FY Riverside Community College District Budget Planning

e-board Agenda Item Agenda Item Agenda Item (IV D 4) Meeting Agenda Item Subject College/District 5/1/2018 Committee Committee Resources (IV D 4) Presentation on New Student Centered Funding Formula Proposal

e-board Agenda Item Agenda Item Agenda Item (IV D 4) Meeting Agenda Item Subject College/District 5/1/2018 Committee Committee Resources (IV D 4) Presentation on New Student Centered Funding Formula Proposal

Budget Forum April 2013

Budget Forum April 2013 Presenters: Helen Benjamin Chancellor Gene Huff Vice Chancellor, Human Resources Jonah Nicholas Director of District Finance Services Why we re here Our Goal Your Opportunity The

Budget Forum April 2013 Presenters: Helen Benjamin Chancellor Gene Huff Vice Chancellor, Human Resources Jonah Nicholas Director of District Finance Services Why we re here Our Goal Your Opportunity The

IMPERIAL COMMUNITY COLLEGE DISTRICT

IMPERIAL COMMUNITY COLLEGE DISTRICT COUNTY OF IMPERIAL AUDIT REPORT FOR THE FISCAL YEAR ENDED JUNE 30, 2016 AUDIT REPORT For the Fiscal Year Ended June 30, 2016 Table of Contents FINANCIAL SECTION Independent

IMPERIAL COMMUNITY COLLEGE DISTRICT COUNTY OF IMPERIAL AUDIT REPORT FOR THE FISCAL YEAR ENDED JUNE 30, 2016 AUDIT REPORT For the Fiscal Year Ended June 30, 2016 Table of Contents FINANCIAL SECTION Independent

ANNUAL STRATEGIC PLANNING RETREAT AUGUST 21, 2012

ANNUAL STRATEGIC PLANNING RETREAT AUGUST 21, 2012 The mission of Los Angeles Southwest College is to facilitate student success, encourage life-long learning, and enrich the lives of its diverse community

ANNUAL STRATEGIC PLANNING RETREAT AUGUST 21, 2012 The mission of Los Angeles Southwest College is to facilitate student success, encourage life-long learning, and enrich the lives of its diverse community

Meeting of the District Budget Advisory Committee March 22, Presented by: Andy Dunn Vice Chancellor Finance & Administrative Services

Meeting of the District Budget Advisory Committee March 22, 2012 Presented by: Andy Dunn Vice Chancellor Finance & Administrative Services Areas of Discussion Review 2012-13 Budget Development Strategy

Meeting of the District Budget Advisory Committee March 22, 2012 Presented by: Andy Dunn Vice Chancellor Finance & Administrative Services Areas of Discussion Review 2012-13 Budget Development Strategy

Part I: The State-approved COLA applied to all of the elements of the Council salary schedule, plus

2014-2017 TENTATIVE AGREEMENT BETWEEN LOS ANGELES COMMUNITY COLLEGE DISTRICT AND LOS ANGELES/ORANGE COUNTIES BUILDING AND CONSTRUCTION TRADES COUNCIL (rev 11-17-14) ARTICLE CHANGES Cover Change term as

2014-2017 TENTATIVE AGREEMENT BETWEEN LOS ANGELES COMMUNITY COLLEGE DISTRICT AND LOS ANGELES/ORANGE COUNTIES BUILDING AND CONSTRUCTION TRADES COUNCIL (rev 11-17-14) ARTICLE CHANGES Cover Change term as

Linking Strategic Planning to Budget

1 Student Access o Students first Linking Strategic Planning to Budget Values Students, Employees, & Community Learning and Student Success o Protecting the learning core Value and Support of Employees

1 Student Access o Students first Linking Strategic Planning to Budget Values Students, Employees, & Community Learning and Student Success o Protecting the learning core Value and Support of Employees

Santa Barbara City College Adopted Budget Presented to: Study Session September 12, 2013

Santa Barbara City College Adopted Budget 2013 14 Presented to: Study Session CONTENTS General Fund Total (Unrestricted & Restricted combined) General Fund Unrestricted Revenues Expenditures General Fund

Santa Barbara City College Adopted Budget 2013 14 Presented to: Study Session CONTENTS General Fund Total (Unrestricted & Restricted combined) General Fund Unrestricted Revenues Expenditures General Fund

Campuswide Benefit Decentralization Implementation Process

DRAFT--ISSUE REPORT January 18, 2012 Campuswide Benefit Decentralization 2012-13 Implementation Process TERMINOLOGY Unless otherwise stated, the term unit is intended to refer to the primary campus organizational

DRAFT--ISSUE REPORT January 18, 2012 Campuswide Benefit Decentralization 2012-13 Implementation Process TERMINOLOGY Unless otherwise stated, the term unit is intended to refer to the primary campus organizational

LOS ANGELES COMMUNITY COLLEGE DISTRICT BOARD OF TRUSTEES BUDGET & FINANCE COMMITTEE

LOS ANGELES COMMUNITY COLLEGE DISTRICT BOARD OF TRUSTEES BUDGET & FINANCE COMMITTEE Educational Services Center Board Room First Floor 770 Wilshire Boulevard Los Angeles, CA 90017 Wednesday, May 24, 2017

LOS ANGELES COMMUNITY COLLEGE DISTRICT BOARD OF TRUSTEES BUDGET & FINANCE COMMITTEE Educational Services Center Board Room First Floor 770 Wilshire Boulevard Los Angeles, CA 90017 Wednesday, May 24, 2017

BUDGET MESSAGE FISCAL YEAR Presented May 13, 2015

BUDGET MESSAGE FISCAL YEAR 2015-16 Presented May 13, 2015 The fiscal year 2015-16 budget reflects a year-long process of analysis, review, and application of our budget development principles, criteria

BUDGET MESSAGE FISCAL YEAR 2015-16 Presented May 13, 2015 The fiscal year 2015-16 budget reflects a year-long process of analysis, review, and application of our budget development principles, criteria

BUDGET COMMITTEE MEETING August 17, 2016 Fireside Room 2:00-3:30 p.m. MINUTES

1 BUDGET COMMITTEE MEETING August 17, 2016 Fireside Room 2:00-3:30 p.m. MINUTES CALL TO ORDER: The meeting was called to order at 2:00 p.m. by Committee Chair, Morris Rodrigue. ROLL CALL: x Jill Ault x

1 BUDGET COMMITTEE MEETING August 17, 2016 Fireside Room 2:00-3:30 p.m. MINUTES CALL TO ORDER: The meeting was called to order at 2:00 p.m. by Committee Chair, Morris Rodrigue. ROLL CALL: x Jill Ault x

2018/19 Proposed Adopted Budget Board of Trustees Meeting

2018/19 Proposed Adopted Budget Board of Trustees Meeting September 10, 2018 Outline of Presentation New Student Centered Funding Formula (SCFF) Updated Adopted Budget Assumptions and Impact on Adopted

2018/19 Proposed Adopted Budget Board of Trustees Meeting September 10, 2018 Outline of Presentation New Student Centered Funding Formula (SCFF) Updated Adopted Budget Assumptions and Impact on Adopted

TENTATIVE BUDGET

201213 TENTATIVE BUDGET June 13, 2012 GOVERNING BOARD Mr. Kendall Pierson, President Mr. Scott Swendiman, Vice President Mr. Duane Miller, Clerk Mr. Harold Lucas, Trustee Mrs. Judi Beck, Trustee Mrs. Rayola

201213 TENTATIVE BUDGET June 13, 2012 GOVERNING BOARD Mr. Kendall Pierson, President Mr. Scott Swendiman, Vice President Mr. Duane Miller, Clerk Mr. Harold Lucas, Trustee Mrs. Judi Beck, Trustee Mrs. Rayola

California Community Colleges Advisory Workgroup on Fiscal Affairs September 5, Meeting Notes

California Community Colleges Advisory Workgroup on Fiscal Affairs September 5, Meeting Notes Actions Taken Members voted to accept the August 15 meeting notes with some minor changes. The revised notes

California Community Colleges Advisory Workgroup on Fiscal Affairs September 5, Meeting Notes Actions Taken Members voted to accept the August 15 meeting notes with some minor changes. The revised notes

Notice of Tentative Budget. Finance & Audit Committee June 12, 2013

2013-14 Notice of Tentative Budget Finance & Audit Committee June 12, 2013 1 Total Tentative Budget All Funds 6 2 2013-14 Proposed Tentative Budget All Funds =$3,181,503,141 APPROPRIATIONS 2011-12 2012-13

2013-14 Notice of Tentative Budget Finance & Audit Committee June 12, 2013 1 Total Tentative Budget All Funds 6 2 2013-14 Proposed Tentative Budget All Funds =$3,181,503,141 APPROPRIATIONS 2011-12 2012-13

LOS ANGELES COMMUNITY COLLEGE DISTRICT. June 30, 2011

June 30, 2011 Los Angeles County, California: East Los Angeles College Los Angeles City College Los Angeles Harbor College Los Angeles Mission College Pierce College Los Angeles Southwest College Los Angeles

June 30, 2011 Los Angeles County, California: East Los Angeles College Los Angeles City College Los Angeles Harbor College Los Angeles Mission College Pierce College Los Angeles Southwest College Los Angeles

CHAFFEY COMMUNITY COLLEGE DISTRICT TENTATIVE BUDGET

2017 2018 TENTATIVE BUDGET Developed and Prepared by: Lisa Bailey, Associate Superintendent Business Services and Economic Development Anita D. Undercoffer, Executive Director, Budgeting and Fiscal Services

2017 2018 TENTATIVE BUDGET Developed and Prepared by: Lisa Bailey, Associate Superintendent Business Services and Economic Development Anita D. Undercoffer, Executive Director, Budgeting and Fiscal Services

University Resources & Planning Committee

University Resources & Planning Committee Date: June 15, 2016 TO: FROM: RE: President Rossbacher, Humboldt State University University Resources & Planning Committee (URPC) URPC Recommendation to the President

University Resources & Planning Committee Date: June 15, 2016 TO: FROM: RE: President Rossbacher, Humboldt State University University Resources & Planning Committee (URPC) URPC Recommendation to the President

UW-Platteville Pioneer Budget Model

UW-Platteville Pioneer Budget Model This document is intended to provide a comprehensive overview of the UW-Platteville s budget model. Specifically, this document will cover the following topics: Model

UW-Platteville Pioneer Budget Model This document is intended to provide a comprehensive overview of the UW-Platteville s budget model. Specifically, this document will cover the following topics: Model

RESOURCE. Sequoias Community College District. College of the Sequoias

RESOURCE A L L O C AT I O N Sequoias Community College District College of the Sequoias College of the Sequoias 2014 Resource Allocation Manual College of the Sequoias Community College District Visalia

RESOURCE A L L O C AT I O N Sequoias Community College District College of the Sequoias College of the Sequoias 2014 Resource Allocation Manual College of the Sequoias Community College District Visalia

STUDY SESSION ON THE DISTRICT BUDGET APRIL 24, Contra Costa Community College District 500 Court Street Martinez, California 94553

STUDY SESSION ON THE 2013-14 DISTRICT BUDGET APRIL 24, 2013 Contra Costa Community College District 500 Court Street Martinez, California 94553 STUDY SESSION ON THE 2013-14 DISTRICT BUDGET Table of Contents

STUDY SESSION ON THE 2013-14 DISTRICT BUDGET APRIL 24, 2013 Contra Costa Community College District 500 Court Street Martinez, California 94553 STUDY SESSION ON THE 2013-14 DISTRICT BUDGET Table of Contents

Grossmont-Cuyamaca Community College District Presented by:

Grossmont-Cuyamaca Community College District Presented by: Cindy Miles, Sunita Cooke, Mark Zacovic, Sue Rearic, Christopher Tarman, Tim Flood, Arleen Satele, Sahar Abushaban GCCCD Mission & Areas of Focus

Grossmont-Cuyamaca Community College District Presented by: Cindy Miles, Sunita Cooke, Mark Zacovic, Sue Rearic, Christopher Tarman, Tim Flood, Arleen Satele, Sahar Abushaban GCCCD Mission & Areas of Focus

Los Angeles Community College District. Subject: ADOPT THE REVISED SPENDING PLAN OF THE EDUCATSON

t :?*i 8B v. s vs g 'I*. Los Angeles Community College District A Corn. No. BF3 Division: BUSINESS AND FINANCE Date: July 9, 2014 Subject: ADOPT THE 2013-14 REVISED SPENDING PLAN OF THE EDUCATSON PROTECTION

t :?*i 8B v. s vs g 'I*. Los Angeles Community College District A Corn. No. BF3 Division: BUSINESS AND FINANCE Date: July 9, 2014 Subject: ADOPT THE 2013-14 REVISED SPENDING PLAN OF THE EDUCATSON PROTECTION

$(48,525,600) $(5,574,700) $(54,100,300)

$(5,574,700) $(54,100,300)") Budget reductions, cost increases Permanent One-Time Total Campus share of $571.1M $(44,076,600) $(44,076,600) Campus share of $77.5M $ (5,574,700) (5,574,700) Mandatory costs increases (2,101,700) (2,101,700)

Budget reductions, cost increases Permanent One-Time Total Campus share of $571.1M $(44,076,600) $(44,076,600) Campus share of $77.5M $ (5,574,700) (5,574,700) Mandatory costs increases (2,101,700) (2,101,700)

LOS ANGELES COMMUNITY COLLEGE DISTRICT. June 30, 2012 and Los Angeles County, California:

June 30, 2012 and 2011 Los Angeles County, California: East Los Angeles College Los Angeles City College Los Angeles Harbor College Los Angeles Mission College Pierce College Los Angeles Southwest College

June 30, 2012 and 2011 Los Angeles County, California: East Los Angeles College Los Angeles City College Los Angeles Harbor College Los Angeles Mission College Pierce College Los Angeles Southwest College

1/25/2014 PRESENTED BY: Heather DeBlanc 153 TOWNSEND STREET, SUITE 520 SAN FRANCISCO, CALIFORNIA T: (415) F: (415)

F: (415)") 6033 WEST CENTURY BOULEVARD, 5 TH FLOOR LOS ANGELES, CALIFORNIA 90045 T: (310) 981-2000 F: (310) 337-0837 153 TOWNSEND STREET, SUITE 520 SAN FRANCISCO, CALIFORNIA 94107 T: (415) 512-3000 F: (415) 856-0306

6033 WEST CENTURY BOULEVARD, 5 TH FLOOR LOS ANGELES, CALIFORNIA 90045 T: (310) 981-2000 F: (310) 337-0837 153 TOWNSEND STREET, SUITE 520 SAN FRANCISCO, CALIFORNIA 94107 T: (415) 512-3000 F: (415) 856-0306

Chancellor s Budget Forum

SAN DIEGO COMMUNITY COLLEGE DISTRICT Chancellor s Budget Forum May June, 2012 Dr. Constance M. Carroll Chancellor Dr. Bonnie Dowd Executive Vice Chancellor, Business Services 1 California Community Colleges

SAN DIEGO COMMUNITY COLLEGE DISTRICT Chancellor s Budget Forum May June, 2012 Dr. Constance M. Carroll Chancellor Dr. Bonnie Dowd Executive Vice Chancellor, Business Services 1 California Community Colleges

SIERRA JOINT COMMUNITY COLLEGE DISTRICT Rocklin, California. FINANCIAL STATEMENTS June 30, 2014

Rocklin, California FINANCIAL STATEMENTS June 30, 2014 ORGANIZATION June 30, 2014 Sierra Joint Community College District (the "District") is comprised of areas in Placer, Nevada, El Dorado and Sacramento

Rocklin, California FINANCIAL STATEMENTS June 30, 2014 ORGANIZATION June 30, 2014 Sierra Joint Community College District (the "District") is comprised of areas in Placer, Nevada, El Dorado and Sacramento

North Orange County Community College District Integrated. Planning Manual March 2014 Update

2013 Integrated Planning Manual March 2014 Update 2013 Integrated Planning Manual NOCCCD Mission Statement The mission of the is to serve and enrich our diverse communities by providing a comprehensive

2013 Integrated Planning Manual March 2014 Update 2013 Integrated Planning Manual NOCCCD Mission Statement The mission of the is to serve and enrich our diverse communities by providing a comprehensive

PROPOSED BUDGET San Jacinto Community College District Budget Hearing August 4, 2014

PROPOSED BUDGET 2014-2015 San Jacinto Community College District Budget Hearing August 4, 2014 1 Highlights of the Proposed 2014 2015 Budget State Revenue Major Revenue Assumptions No change in rate FY15,

PROPOSED BUDGET 2014-2015 San Jacinto Community College District Budget Hearing August 4, 2014 1 Highlights of the Proposed 2014 2015 Budget State Revenue Major Revenue Assumptions No change in rate FY15,

SPECIAL MEETING MINUTES

BOARD OF TRUSTEES SANTA MONICA COMMUNITY COLLEGE DISTRICT SPECIAL MEETING April 30, 2007 SPECIAL MEETING MINUTES A special meeting of the Santa Monica Community College District Board of Trustees was held

BOARD OF TRUSTEES SANTA MONICA COMMUNITY COLLEGE DISTRICT SPECIAL MEETING April 30, 2007 SPECIAL MEETING MINUTES A special meeting of the Santa Monica Community College District Board of Trustees was held

FIRST QUARTER REPORT

2018-19 FIRST QUARTER REPORT This page intentionally left blank. FOOTHILL-DE ANZA COMMUNITY COLLEGE DISTRICT Board of Trustees Bruce Swenson, President Pearl Cheng, Vice President Laura Casas Peter Landsberger

2018-19 FIRST QUARTER REPORT This page intentionally left blank. FOOTHILL-DE ANZA COMMUNITY COLLEGE DISTRICT Board of Trustees Bruce Swenson, President Pearl Cheng, Vice President Laura Casas Peter Landsberger

MIRACOSTA COMMUNITY COLLEGE DISTRICT ANNUAL FINANCIAL REPORT JUNE 30, 2016

MIRACOSTA COMMUNITY COLLEGE DISTRICT ANNUAL FINANCIAL REPORT TABLE OF CONTENTS FINANCIAL SECTION Independent Auditor's Report 2 Management's Discussion and Analysis 5 Basic Financial Statements - Primary

MIRACOSTA COMMUNITY COLLEGE DISTRICT ANNUAL FINANCIAL REPORT TABLE OF CONTENTS FINANCIAL SECTION Independent Auditor's Report 2 Management's Discussion and Analysis 5 Basic Financial Statements - Primary

Santa Ana College Santiago Canyon College TENTATIVE BUDGET

Santa Ana College Santiago Canyon College TENTATIVE BUDGET 2011-2012 TENTATIVE BUDGET Submitted on June 20, 2011 by Dr. Raúl Rodriguez, Chancellor to the BOARD OF TRUSTEES Brian E. Conley, M.A., President

Santa Ana College Santiago Canyon College TENTATIVE BUDGET 2011-2012 TENTATIVE BUDGET Submitted on June 20, 2011 by Dr. Raúl Rodriguez, Chancellor to the BOARD OF TRUSTEES Brian E. Conley, M.A., President

Glossary of Accounting Terminology San Jose/Evergreen CCD February 26, 2002

Glossary of Accounting Terminology San Jose/Evergreen CCD February 26, 2002 50 Percent Law Section 84362 of the Education Code, commonly known as the Fifty Percent Law, requires that a minimum of 50% of

Glossary of Accounting Terminology San Jose/Evergreen CCD February 26, 2002 50 Percent Law Section 84362 of the Education Code, commonly known as the Fifty Percent Law, requires that a minimum of 50% of

6870 Board of Governors of the California Community Colleges

EDUCATION EDU 1 6870 Board of Governors of the California Community Colleges The Board of Governors of the California Community Colleges was established in 1967 to provide statewide leadership to California's

EDUCATION EDU 1 6870 Board of Governors of the California Community Colleges The Board of Governors of the California Community Colleges was established in 1967 to provide statewide leadership to California's

Administrative Procedure 6200 Budget Preparation and Resource Allocation

Administrative Procedure 6200 Budget Preparation and Resource Allocation Reference: Accreditation Standard III.D; Education Code Section 70902(b)(5); Title 5, Sections 58300 et seq. The communities within

Administrative Procedure 6200 Budget Preparation and Resource Allocation Reference: Accreditation Standard III.D; Education Code Section 70902(b)(5); Title 5, Sections 58300 et seq. The communities within