Financial Management Guidelines and Procedures

|

|

|

- Corey Johns

- 6 years ago

- Views:

Transcription

1 The financial position and future of the Colorado School of Mines is dependent on several variables including enrollment, research growth, changes in industry demand, and competing institutions at the national and international levels. In order to capitalize on these variables and respond to the challenges they may present, the school must maintain a strong financial position, flexible resources, and accountable financial management. These financial management guidelines were designed to provide the ability to track, forecast, and project current and future resource needs in order to respond to the changing financial environment and the continuously strengthen the university s financial position. Financial Management is performed on all sources and uses of funds; unrestricted, designated, and restricted. Unrestricted operating budgets (education and general, and undesignated auxiliaries) are approved by the line item category as described below; designated budgets are subject to the purpose of the fund sources; and restricted budgets are subject to the policies and instructions of the sponsor or donor. Budget Stages Prior to approval by the Board of Trustees, there are several steps in developing the budget, all of which are interrelated. While developing the budget, it is critical to review the cumulative impact of current year activity and decisions on long-term projections. These stages are outlined below: Annual Budget Development - a detailed Board approved budget incorporating projections, departmental requests and institutional strategic investments. Budget Management - Allocation of the annual budget to colleges and individual departments and the ongoing monitoring of how and when those budgets are utilized. Forecast Development - quarterly changes to the annual budget must be approved by the Board of Trustees and are derived from unanticipated changes to projections, subsequent departmental requests, and unanticipated expenditures or savings. Projections - a ten year impact projection model, using various assumption scenarios, providing a long term outlook based on current year decisions. Budget Components Budgets are allocated in three major categories: Labor, Operating, and Capital as defined below. The development and usage of each category is detailed in separate sections of these guidelines. Mid-year realignments of budget from one category to another must be approved through the forecast process. Labor - includes salary and benefits for: academic and research faculty, administrative faculty, classified staff, hourly staff, adjuncts, graduate support, personal service contracts and student employees. o FTE for budgeting purposes includes all academic faculty, administrative faculty, transitional faculty, and classified staff. It does not include research faculty, adjuncts, graduate TA's and RA's, temporary, or students. 1

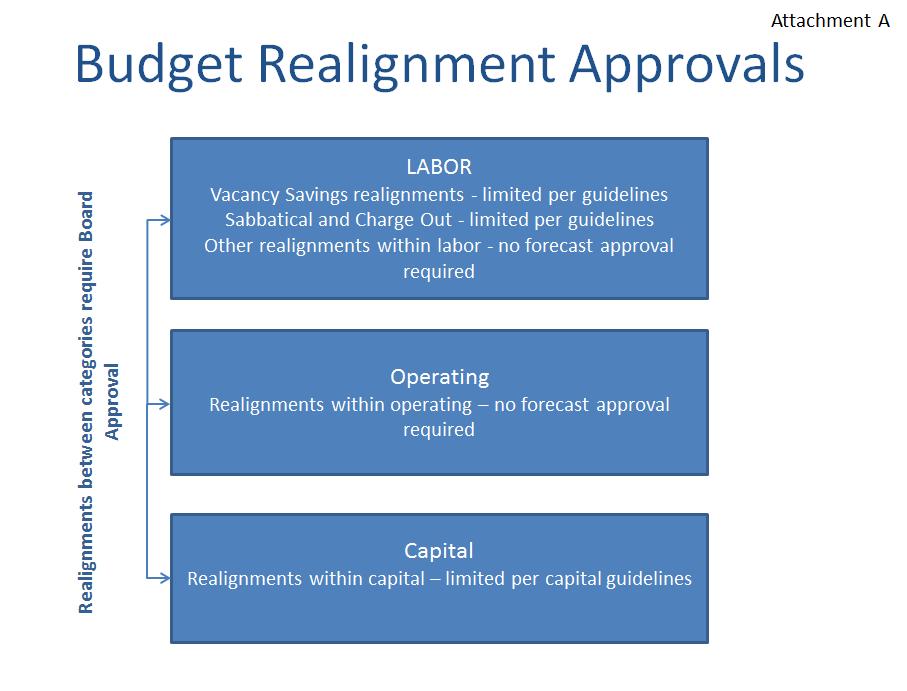

2 Operating - expenditures and transfers that are not labor and are used to provide goods and services to support a specific program. It also includes single item equipment expenditures or capital projects below $25,000. Capital - capital projects and/or equipment where total costs are greater or equal to $25,000 and/or are funded from the capital budget (see Capital Budget Guidelines). Forecast Adjustments Three forecasts are developed during the year that provide for an avenue to address unplanned changes from what was approved in the annual budget process. The President has committed that he will present to the Board of Trustees, for their approval, any requested changes to the budget as reflected in each of the three forecasts. Adjustments prior to Board approval are allowed in two situations: 1) when there is unanticipated enrollment increases that have a direct impact on the classroom and new faculty, adjunct, TA s or classroom material are required to mitigate that impact; and 2) in emergency situations where expenditures are required to prevent business interruptions. Such forecast adjustments will be reported to the Finance and Audit Committee during their next regularly scheduled meeting. Each month, the Budget Office will review budget to actual activity. Major variances must be explained by respective areas. Then, three times during the year, a full funds forecast will be requested from each major area as determined by the Budget Office. These forecast periods provide an opportunity to request approval for a modification (increase or decrease) to a current year budget allocation. Forecast requests shall be approved by each Vice President for their respective area or Dean in the case of Colleges. To ensure adequate budget exists for the university as a whole, the Executive Vice President for Finance and Administration (EVPFA) will approve the forecast in its entirety before submitting to the President for approval and then the Finance and Audit Committee and Board of Trustees for consideration of approval. The following forecast adjustments must be approved prior to allocation: Revenue modifications FTE increases with or without a budget impact Operating and Labor budget increases or decreases Vacancy savings (see Vacancy Savings below) Realignments of budget between categories: Labor, Operating or Capital (See Attachment A) Once approved, these adjustments will be allocated in Banner. Realignments of budget within the same category do not require approval prior to making the adjustments (e.g. moving operating budget from one department to another, or moving an FTE budget from one college to another). Also, the Academic Departments have the flexibility to realign between TA, adjunct, student hourly and operating budgets at their discretion. 2

3 Unused Budget Colleges and Academic Departments may carry forward year end unused budget into a subsequent year that is derived from operating, TA, adjunct or student hourly budgets, excluding any new budget allocated and/or forecast adjustments. These funds may accumulate up to the annual amount of the respective operating budget only and can be used at the discretion of the Dean or Department head. In no circumstances will any other excess funds whether derived from excess revenue or savings in expenses will be carried forward into subsequent years to pre-fund future year projects, expenses or any other purpose. Collaboration Below is an example of the areas that will be required to provide information to the Budget Office for monthly variance analysis as well as the forecast process. Note that the list below may not be all inclusive and at times more or less frequent meetings may be required. Financial Management When Area Monthly Forecast Colleges/Academic Departments Positions Operating CCIT All other Academic Affairs Facilities Management Positions Operating All other Finance and Administration Student Life Positions Operating Athletics Financial Aid Operating All other Student Life VPRTT SPACE All other VPSE President's Office All other President's Office Labor Budget and Vacancy Savings Position budgeting is in place for all academic faculty, administrative faculty, transitional faculty, and classified staff. We do not use position budgets for research faculty, adjuncts, graduate TA's and RA's, temporary, or students. Position budgets are allocated in the Banner system by labor type account code. These codes are detailed in Attachment B. Labor budgets are aligned with existing positions to properly track available FTE. If a vacant FTE does not have budget, then it is not available to fill unless the respective area requests a permanent reduction in operating funds to create a labor budget via an approved forecast adjustment. Therefore, a position 3

4 may not exist without a budget. If budget is realigned from a position, that position must be abolished or a plan for backfilling that budget must be submitted to the Budget Office and approved by the EVPFA within the same fiscal year that the position budget was removed. New FTE or reductions in FTE must be requested/reported with the budget or forecast development process except for those situations where new adjunct or faculty positions are needed due to unexpected enrollment increases that have a direct impact on the classroom. Realignments of salary from one position to another do not require additional approvals. Vacancy savings from positions with budgets are created from a variety of situations and should be budgeted in anticipation of vacant positions. Vacancy savings incurred during the year will first be used to fulfill the budget for current year operations before any other forecast adjustments will be considered. Each type of savings must be tracked via position control feature in Banner to determine the appropriate budget adjustment. Any positions that become vacant during the year must be reported to the Budget Office within the first month of the vacancy. The following list outlines the general treatment for each type of vacancy savings after the budget commitment has been fulfilled: New approved FTE, not filled - the position will be held in a Budget Office central account and the budget will be reduced by the estimated savings (based on hire date) in the first quarter forecast adjustment. New faculty positions in the search process will be held in a separate Budget Office account in order to track those positions already committed to a department. Existing FTE vacancies for classified, academic faculty and administrative staff - typically due to normal turnover. All vacancy savings (except for those generated from sabbaticals, charge out and custodial staff) above the budged amount will be held in central budged accounts designated for each Vice President. The Vice Presidents may use these savings in two ways: 1) to backfill the vacated position that generated the savings with temporary staff or adjunct and 2) for one-time expenditures to be expended within the current fiscal year pursuant to the annual cumulative thresholds below: Provost - $50,000 Deans - $50,000 each (total of $150,000) Executive Vice President of Finance and Administration - $40,000 Vice President for Student Life - $40,000 Vice President for Research and Technology Transfer - $10,000 Senior Vice President for Strategic Enterprises - $10,000 If there are not enough savings to fund the budget commitment, the above thresholds will be reduced proportionately until the vacancy savings budget is fulfilled. Any use beyond the above thresholds will require a forecast adjustment approved through the forecast process prior to use of the savings for one-time capital and operating items. All other savings will be included in the forecast to reduce the overall labor budget. Custodial FTE - due to the high turnover in this position class, all vacant positions are kept within the Facilities Management department. An annual estimate of total savings is calculated and a "lump sum" labor budget reduction is included in the first quarter forecast adjustment and reviewed monthly to determine if additional modifications are required. 4

5 Sabbatical Savings - Academic Affairs retains these savings to backfill the position and to realign the savings for other purposes. The allocation of Sabbatical Savings is provided below: 93% of salary will be allocated to the College 7% of salary will be allocated to the Provost 100% of the fringe will be allocated to the provost Research Charge Out - some faculty may "buy out" of teaching a course to pursue a research project. In those situations the department retains the salary savings to backfill that position and to realign the savings for other departmental purposes. Charge out must relieve the general fund of the salary and benefit expense. The current distribution of these savings is as follows: 90% of salary will remain with the departments with $6,800 (plus fringe) to fund adjuncts 10% of salary will be allocated to the Dean 50% of the fringe will be allocated to the Dean 50% of the fringe will be allocated to the Provost Other adjunct, workstudy, undergraduate research match and graduate support and other miscellaneous labor will be reviewed and updated during the departmental review. Estimated savings will result in a budget reduction for the quarterly forecast. Permanent savings may also exist when a position is filled at a lower salary than budgeted. In these situations, each Vice President is allowed to retain that savings to reallocate to other positions as necessary. These savings are tracked in unique position codes for each Vice President. These codes are also outlined in Attachment B. Vacancy savings may not be used for permanent budget adjustments and may not be rolled to a future fiscal year. Operating Budgets Approved operating budgets are allocated to each department once the budget is approved. In general, operating budgets are allocated to a budget pool and not by account type unless specifically requested by a department. There are some transfer budget codes that are used for tracking specific activity. All operating budget codes are detailed in Attachment C. Operating budget may only be used for the general operations of the program in the year in which it is allocated. Transfers that are not budgeted are not allowed unless approved by the Budget Office. Operating budgets may not be used for capital projects, renovations or equipment where the cost exceeds $25,000. Such projects must be submitted and approved through the capital request process. Realignment of operating budget to labor must be included in a forecast adjustment request and approved by the President and the Board of Trustees. Realignment of operating budgets between programs (operating budget moved between two academic departments) does not require additional approvals. 5

6 Budget Development and Projections The projections and annual budget development are a year-long process and requires input from several departmental representatives throughout campus. In addition, this process is vetted with the institution's Budget Committee during monthly meetings typically from September through April. A high level schedule is provided below and a more detailed calendar may be found in Attachment D. Budget Development Calendar (dates are approximate) August-December - Budget Office updates the projection models and develops budget for mandated costs and strategic investments January 1 - Budget Office Calls for Requests March 1 - Vice Presidents submit prioritized requests for their respective areas to the Budget Office March Vice Presidents prioritize all budget requests with strategic investments March Board of Trustees Meeting - Executive Vice President for Finance and Administration (EVPFA) updates the Board of Trustees regarding tuition, student fees and charges, and the expenditure budget April 1 - Executive Committee review prioritized requests April 15 - Budget Committee votes to submit formal recommendation for the following: o Salary and Benefit Actions o Tuition Increases o New Fees and Charges o Current Fees and Charges o Prioritization of budget requests (includes new FTE) April 20 - Executive Committee and President reviews Budget Committee Recommendation May 1 - Budget recommendation from the President submitted to the Finance and Audit Committee for review and recommendation to the Board of Trustees May 20 - Budget recommendation submitted to the Board or Trustees for review and approval Budget Committee The Budget Committee is defined in the Faculty Handbook, section 12.3 which states: The Budget Committee shall be responsible for gathering and analyzing appropriate data regarding the budgetary requirements of CSM, preparing proposed annual budgets for CSM, preparing proposed budgetary revisions from time to time, and advising the President and the CSM administration on budgetary matters and long-range fiscal planning. The appointed membership of the Budget Committee shall consist of two academic department heads, three full-time academic faculty members, and one full-time administrative faculty member. One of the academic faculty members must be a Faculty Senator and shall serve as a representative of the Faculty Senate. Additionally, the Provost, the Senior Vice President for Finance and Administration, the Vice President for Student Life and Dean of Students, the Vice President for Research and Technology 6

7 Transfer, and the Senior Vice President for Strategic Enterprises shall serve as voting, ex officio committee members. The Executive Director of the CSM Foundation shall serve as a non-voting, ex officio committee member. University-wide Projections Some increases impact the entire institution and are projected by administrative groups across campus. Examples included mandated salary increases for classified staff, fringe benefit increases, utilities etc. Below is a list (not all inclusive) of information that is required of several groups across campus: Institutional Research and Admissions - Undergraduate Enrollment projections Graduate Office - Graduate Enrollment Projections Financial Aid - Institutional financial aid expenditure projections Registrar's Office - Graduation projections Academic Affairs - Undergraduate summer enrollment projections; faculty startup Student Life - Auxiliary revenue and expense projections ORA and VPRTT - Research activity and Indirect Cost Return Projections Human Resources - Salary increases for classified staff and benefit increases applicable to all faculty and staff. Facilities Maintenance - Utility adjustments Center for Computing and Informational Technologies Campus wide licensing increases Deadlines for submitting projections are different for each area and a detailed schedule in provided in Attachment E. In addition to projections, each area is required to submit current year updates to the Budget Office each quarter to provide changes to the Forecast (the 15th day of September, December and March). Departmental Requests Each Vice President (and other direct reports of the President) are responsible for prioritizing departmental requests for their respective areas and submitting their prioritized requests to the Budget Office. Once the Budget Office has compiled one list for the entire university, led by the EVPFA, the Vice Presidents will coordinate and prioritize the requests along with university-wide increases and strategic investments. These requests may include labor, capital or operating increases or realignments. Each request must indicate how it aligns with the institution's strategic plan or meets a critical need in order to be considered. Budget Office and Executive Committee The Budget Office will coordinate and develop the projection models, the university-wide increases and departmental requests. As projections and various scenario models are developed they will be provided to the Executive Committee and Budget Committee for review. Based on this and other external information, the Executive Committee will develop recommendations for policy increases, including (but not limited to): 7

8 Tuition Student Fees Financial Aid Allocations The Budget Office will present the annual budget model to the Budget Committee for final review and approval of their recommendation. Once approved by the Budget Committee, their recommendation will be submitted to the President who, upon approval, will submit to the Board of Trustees Finance and Audit Committee for their consideration before submitting to the Board of Trustees for final approval at the May Board of Trustees Meeting. 8

9 9

10 Labor Budget Account Codes Position Budget Account Codes Description Account Academic Faculty 5210 Acad Faculty Fringe Benefits 5130 Administrative Faculty 5212 Admin Faculty Fringe Benefits 5137 Classified Full Time 5201 Classified Permanent Part Time 5202 Classified Temporary Full Time 5203 Classified Temporary Part Time 5204 Classified Fringe Benefits 5100 Classified Temp Fringe Benefits 5139 Research Faculty 5211 Research Faculty Fringe Benefits 5138 Other Labor Account Codes Description Account Adjunct Faculty 5220 Temporary Faculty Fringe Benefits (Adjunct) 5135 Classified Overtime 5206 Grad Salary Budget Pool 5215P/5213/5214 Grad Tuition Budget Pool 5118P/5119 Hourly Student Help 5218 Research Faculty Wages Budget Pool 5211P Research Fac Benefits Budget Pool 5112P Tuition Waiver-Classified 5141 Tuition Waiver-Faculty/Admin 5142 Academic Fac-Sabbatical Savings 5210S Academic Faculty-Chargeout Savings 5210C AF Benefits Budget Pool-Chargeout 5130C AF Benefits Budget Pool-Sabbatical 5130S Contracted Professional Services 5129 Independent Contractors 5125 Part Time Research Support 5231 Personal Service Contracts 5124 Temporary Admin Fac, PT 5225 Permanent Vacancy Savings Pooled Position Number Description Employee Type Academic Affairs SVADAA Savings-Admin Fac-Acad Affairs Administrative Faculty SVAFFA Savings-Acad Fac-Fin & Admin Academic Faculty SVCLAA Savings-Classified-Acad Affair Classified Staff Finance & Administration SVADFA Savings-Admin Fac-Fin & Admin Administrative Faculty SVAFFA Savings-Acad Fac-Fin & Admin AF SVCLFA Savings-Classified-Fin & Admin Classified Staff President SVADPR Savings-Admin Fac-President Administrative Faculty SVAFPR Savings-Acad Fac-President Academic Faculty SVCLPR Savings-Classified-President Classified Staff Research and Tech Transfer SVADRT Savings-Admin Fac-Res&Tech Administrative Faculty SVAFRT Savings-Acad Fac-Res&Tech Academic Faculty SVCLRT Savings-Classified-Res&Tech Classified Staff Student Life SVADSL Savings-Admin Fac-Stdnt Life Administrative Faculty SVAFSL Savings-Acad Fac-Stdnt Life Academic Faculty SVCLSL Savings-Classified-Stdnt Life Classified Staff Institution SVNWAF Savings-New Academic Faculty Academic Faculty Attachment B 10

11 Attachment C Operating Budget Account Codes Description Account Operating Budget Pool 5300P Capital Outlay Budget Pool 5905P Non-Mandatory Transfer In 8870 Transfer Budget Pool 8970P Debt Transfer Budget Pool 8971P 11

12 Final Presidential Review VPs work with President and Executive Committee to review and provide feedback on all budget requests VPs prioritize all requests VPs work with respective areas Financial Management Guidelines and Procedures Budget Development Calendar (dates are approximate) Attachment D Important dates for the State Major Colorado School of Mines due dates January 1 January 26 February 10 Budget Office Calls for Requests CSM census day Revenue estimates due to JBC/Legislative Council February 15* March 1 Budget Committee meeting - Budget Office presents projections with mandated costs Prioritized departmental requests due to the Budget Office from the Vice Presidents March 5 March 20 March 15* March 31 Joint Budget Committee figure setting March state revenue forecast Budget committee meeting-discuss tuition rates, mandated costs and salary actions Vice Presidents' prioritized budget requests with strategic investments due to the Budget Office March/April Board of Trustees meeting- tuition update, budget update, review of student fees and charges April 1 April 5 Prioritized budget requests discussed by Executive Committee Budget committee meeting to begin review of prioritized budget requests and review of FY15 budget scenarios. Discuss tuition rates, mandated costs and salary actions. April 15* April 20 May Budget Committee meeting to submit formal recommendation of budget: - Salary and benefit actions - Tuition increases - New fees and charges - Current fees and charges - Prioritization of budget requests (includes Executive new Committee FTE) meeting to review Budget Committee recommendations Long bill signed May 1 May 20 President submits budget recommendation to the Finance and Audit Committee Board of Trustees meeting - approve budget and tuition rates 12 *Budget Committee meets the third Thursday of each month. Additional meetings may be scheduled in March and April to finalize the budget recommendation.

13 Attachment E University Wide Projection Time Line Responsible Department Required Estimates Dates Institutional Research and Admissions Graduate Office Financial Aid Undergraduate Enrollment projections Graduate Enrollment Projections Institutional financial aid expenditure projections March for projected admissions in following year; Spring and Fall Census forecast update March for projected admissions in following year; Spring and Fall Census forecast update March for projected expenditure in following year; Spring and Fall Census for forecast update Registrar's Office Graduation projections September and March Academic Affairs Student Life ORA and VPRTT Human Resources Facilities Maintenance Undergraduate summer enrollment projections; faculty startup Auxiliary revenue and expense projections Research activity and Indirect Cost Return Projections Salary and Benefit Increases Utility adjustments March October for budget; Spring and Fall Census for forecast update October for budget; September, December and March for forecast update November for benefit budget; April for salary budget October for budget; September, December and March for forecast update Center for Computing and Informational Technologies Campus wide licensing increases January for Budget 13

Joseph Trubacz Senior Vice President for Finance and Administration

TO: FROM: Board of Trustees Joseph Trubacz Senior Vice President for Finance and Administration DATE: May 21, 2011 SUBJECT: FY 2013 Budget I. BACKGROUND INFORMATION Fiscal Year 2013 Operating Budget Summary

TO: FROM: Board of Trustees Joseph Trubacz Senior Vice President for Finance and Administration DATE: May 21, 2011 SUBJECT: FY 2013 Budget I. BACKGROUND INFORMATION Fiscal Year 2013 Operating Budget Summary

Colorado School of Mines Board of Trustees Meeting June 18, Operating Budget for the Fiscal Year

Colorado School of Mines Board of Trustees Meeting June 18, 2004 Operating Budget for the 2004-05 Fiscal Year The campus Budget Committee met on June 10, 2004 to review and discuss the proposed budget.

Colorado School of Mines Board of Trustees Meeting June 18, 2004 Operating Budget for the 2004-05 Fiscal Year The campus Budget Committee met on June 10, 2004 to review and discuss the proposed budget.

FY 2019 UNIVERSITY BUDGET CALENDAR

FY 2019 UNIVERSITY BUDGET CALENDAR FY2019 UNIVERSITY BUDGET CALENDAR PLANNING: July, 2017 Office of Budget Management distributes the following to all Vice Presidents, Provost Office, and Business Representatives

FY 2019 UNIVERSITY BUDGET CALENDAR FY2019 UNIVERSITY BUDGET CALENDAR PLANNING: July, 2017 Office of Budget Management distributes the following to all Vice Presidents, Provost Office, and Business Representatives

I. Background. Budget Advisory Council

Office of the Vice President for Finance & Business Operations 330.941.1331 Fax 330.941.1380 University Budget Process Updated 1/17/18 I. Background Youngstown State University s annual operating budget

Office of the Vice President for Finance & Business Operations 330.941.1331 Fax 330.941.1380 University Budget Process Updated 1/17/18 I. Background Youngstown State University s annual operating budget

SECTION B: Budgeting. Introduction. I. Legislative Budget Request

SECTION B: Budgeting Introduction Budget development and monitoring at the College is a collaborative process comprised of several different components, beginning with the biennial legislative budget request.

SECTION B: Budgeting Introduction Budget development and monitoring at the College is a collaborative process comprised of several different components, beginning with the biennial legislative budget request.

Technical Budget Process. Overview FY18

Technical Budget Process Overview FY18 TABLE OF CONTENTS Introduction... 3 Conceptual Overview... 3 Basic steps in preparation process... 5 Budget development review report... 6 Classification of budget

Technical Budget Process Overview FY18 TABLE OF CONTENTS Introduction... 3 Conceptual Overview... 3 Basic steps in preparation process... 5 Budget development review report... 6 Classification of budget

FY15 Six Month Budget Update

FY15 Six Month Budget Update February 2015 Overview of the Operating and Research Funds For the Six Months Ended December 31, 2014 Summary On June 25, 2014, the Board of Trustees approved a Spending Plan

FY15 Six Month Budget Update February 2015 Overview of the Operating and Research Funds For the Six Months Ended December 31, 2014 Summary On June 25, 2014, the Board of Trustees approved a Spending Plan

Hostos Community College Budget Process

Hostos Community College Budget Process Note: The following is largely excerpted from the 2017 MSCHE Periodic Review Report The Budget Components and Financial Planning Process The primary source of annual

Hostos Community College Budget Process Note: The following is largely excerpted from the 2017 MSCHE Periodic Review Report The Budget Components and Financial Planning Process The primary source of annual

New Jersey Institute of Technology

New Jersey Institute of Technology Budget Presentation to the Faculty Senate FY17 Budget Highlights FY17 Budget Status Status of Business Process Improvements Budget Development Calendar November 10, 2016

New Jersey Institute of Technology Budget Presentation to the Faculty Senate FY17 Budget Highlights FY17 Budget Status Status of Business Process Improvements Budget Development Calendar November 10, 2016

Budget Reform Update. Paul Ellinger, Associate Chancellor & Vice Provost Budget and Resource Planning

Budget Reform Update Paul Ellinger, Associate Chancellor & Vice Provost Budget and Resource Planning February 2018 Outline Brief budget model overview Communication plan Principles Major components Timeline

Budget Reform Update Paul Ellinger, Associate Chancellor & Vice Provost Budget and Resource Planning February 2018 Outline Brief budget model overview Communication plan Principles Major components Timeline

BUDGETING FOR A FUNDS. Education and General Unrestricted Operating Funds

BUDGETING FOR A FUNDS Education and General Unrestricted Operating Funds What is a budget? Why have a budget? Planning Controlling spending Identifying funding sources Good budgeting does not set priorities

BUDGETING FOR A FUNDS Education and General Unrestricted Operating Funds What is a budget? Why have a budget? Planning Controlling spending Identifying funding sources Good budgeting does not set priorities

Campuswide Benefit Decentralization Implementation Process

DRAFT--ISSUE REPORT January 18, 2012 Campuswide Benefit Decentralization 2012-13 Implementation Process TERMINOLOGY Unless otherwise stated, the term unit is intended to refer to the primary campus organizational

DRAFT--ISSUE REPORT January 18, 2012 Campuswide Benefit Decentralization 2012-13 Implementation Process TERMINOLOGY Unless otherwise stated, the term unit is intended to refer to the primary campus organizational

UW-Platteville Pioneer Budget Model

UW-Platteville Pioneer Budget Model This document is intended to provide a comprehensive overview of the UW-Platteville s budget model. Specifically, this document will cover the following topics: Model

UW-Platteville Pioneer Budget Model This document is intended to provide a comprehensive overview of the UW-Platteville s budget model. Specifically, this document will cover the following topics: Model

Budget Submission Calendar

How to Submit the 2006-07 Budget University of Virginia Submissions, with prior vice presidential approval, must be received by the close of business on the dates listed. Each vice president, dean and

How to Submit the 2006-07 Budget University of Virginia Submissions, with prior vice presidential approval, must be received by the close of business on the dates listed. Each vice president, dean and

UNTHSC. Annual Budget Development Process Fiscal Year 2019 Guidelines & Instructions - Spring 2018

UNTHSC Annual Budget Development Process Fiscal Year 2019 Guidelines & Instructions - Spring 2018 INTRODUCTION: The budgeting process at the University of North Texas Health Science Center (UNTHSC) assigns

UNTHSC Annual Budget Development Process Fiscal Year 2019 Guidelines & Instructions - Spring 2018 INTRODUCTION: The budgeting process at the University of North Texas Health Science Center (UNTHSC) assigns

Click to Add Title. What HR Professionals Need to Know About Budgets at UIC. HR Academy November 7, 2014

What HR Professionals Need to Know About Budgets at UIC Click to Add Title HR Academy November 7, 2014 Janet Parker Associate Chancellor & Vice Provost Budget & Resource Planning Agenda Fund Accounting

What HR Professionals Need to Know About Budgets at UIC Click to Add Title HR Academy November 7, 2014 Janet Parker Associate Chancellor & Vice Provost Budget & Resource Planning Agenda Fund Accounting

GENERAL FUND. For the Three Months Ended September 30, 2018

GENERAL FUND For the Three Months Ended September 30, 2018 FY19 Annual Budget with results for the three months ended September 30, 2018 Approved Budget Actual $ Budget Variance % of Budget Tuition & General

GENERAL FUND For the Three Months Ended September 30, 2018 FY19 Annual Budget with results for the three months ended September 30, 2018 Approved Budget Actual $ Budget Variance % of Budget Tuition & General

Sequoias Community College District RESOURCE

RESOURCE A L L O C AT I O N Sequoias Community College District College of the Sequoias 2013 Resource Allocation Manual College of the Sequoias Community College District Visalia Campus 915 S. Mooney Blvd.

RESOURCE A L L O C AT I O N Sequoias Community College District College of the Sequoias 2013 Resource Allocation Manual College of the Sequoias Community College District Visalia Campus 915 S. Mooney Blvd.

STANDARD OPERATING PROCEDURE

Page 1 of 8 STANDARD OPERATING PROCEDURE DEPARTMENT: Business and Admin. Services TITLE: College Budget Planning PURPOSE: The College President, in consultation with the President s Executive Council (EC),

Page 1 of 8 STANDARD OPERATING PROCEDURE DEPARTMENT: Business and Admin. Services TITLE: College Budget Planning PURPOSE: The College President, in consultation with the President s Executive Council (EC),

Fiscal Year Budget Planning & Outlook

Fiscal Year 2016-2017 Budget Planning & Outlook David Bea Executive Vice Chancellor for Finance and Administration Spring 2016 Major Factors Impacting Budget No State Appropriations Continued Enrollment

Fiscal Year 2016-2017 Budget Planning & Outlook David Bea Executive Vice Chancellor for Finance and Administration Spring 2016 Major Factors Impacting Budget No State Appropriations Continued Enrollment

ANTHONY P. JIGA Vice President Budget and Planning

ANTHONY P. JIGA Vice President Budget and Planning 70 Washington Square South, Room 1202 New York, NY 10012 P: 212 998 2278 anthony.jiga@nyu.edu To: School, Administrative and Auxiliary Fiscal Officers

ANTHONY P. JIGA Vice President Budget and Planning 70 Washington Square South, Room 1202 New York, NY 10012 P: 212 998 2278 anthony.jiga@nyu.edu To: School, Administrative and Auxiliary Fiscal Officers

ANTHONY P. JIGA Vice President Budget and Planning

ANTHONY P. JIGA Vice President Budget and Planning 70 Washington Square South, Room 1202 New York, NY 10012 P: 212 998 2278 anthony.jiga@nyu.edu To: School, Administrative and Auxiliary Fiscal Officers

ANTHONY P. JIGA Vice President Budget and Planning 70 Washington Square South, Room 1202 New York, NY 10012 P: 212 998 2278 anthony.jiga@nyu.edu To: School, Administrative and Auxiliary Fiscal Officers

FY 2011 BUDGET (MAY 5, 2010)

") Approved by Chancellor Spakes May 11, 2010 FY 2011 BUDGET (MAY 5, 2010) INTRODUCTION Taking into account a constrained resource environment, the FY 2011 budget recommendation supports the mission of the

Approved by Chancellor Spakes May 11, 2010 FY 2011 BUDGET (MAY 5, 2010) INTRODUCTION Taking into account a constrained resource environment, the FY 2011 budget recommendation supports the mission of the

FY 15 & 16 Operating and Capital Budget Calendar Page 1 of 6

Page 1 of 6 August 1, 2014 Run faculty salary report in data warehouse to validate base salary correct notify Provost Office of discrepancies (this is different than the Payroll report) September 2014

Page 1 of 6 August 1, 2014 Run faculty salary report in data warehouse to validate base salary correct notify Provost Office of discrepancies (this is different than the Payroll report) September 2014

September 1, 2016 Revised May 12, 2017

New York University Title: Position Management Operating Policy and Procedures Effective Date: Issuing Authority: Executive VP, Finance and Information Technology Responsible Officers: Vice President,

New York University Title: Position Management Operating Policy and Procedures Effective Date: Issuing Authority: Executive VP, Finance and Information Technology Responsible Officers: Vice President,

Gov s Proposed Budget

May 10, 2012 Gov s Proposed 2012-13 Budget Jan 05, 2012 Addressed $9.2b budget deficit Depends on successful November 2012 initiative on temporary tax increases No change to CSU budget if initiative passes

May 10, 2012 Gov s Proposed 2012-13 Budget Jan 05, 2012 Addressed $9.2b budget deficit Depends on successful November 2012 initiative on temporary tax increases No change to CSU budget if initiative passes

FY10 and FY11 Bu get Up ate Office of Institute Budget Budget Planning and A dministration Administration November 15, 2010

FY10 and FY11 Budget Update Office of Institute Budget Planning and Administration Office of Institute Budget Planning and Administration November 15, 2010 Current & Previous Budget Challenges Faculty

FY10 and FY11 Budget Update Office of Institute Budget Planning and Administration Office of Institute Budget Planning and Administration November 15, 2010 Current & Previous Budget Challenges Faculty

SOUTHWEST TENNESSEE COMMUNITY COLLEGE

SOUTHWEST TENNESSEE COMMUNITY COLLEGE Policy No. 4:00:00:00/2 Page 1 of 12 SUBJECT: Budget Policies and Procedures EFFECTIVE DATE: July 1, 2000; Revised: May 31, 2013. I Index I Index 1 II Introduction

SOUTHWEST TENNESSEE COMMUNITY COLLEGE Policy No. 4:00:00:00/2 Page 1 of 12 SUBJECT: Budget Policies and Procedures EFFECTIVE DATE: July 1, 2000; Revised: May 31, 2013. I Index I Index 1 II Introduction

Georgia Institute of Technology Institute Budget Planning & Administration Policies and Procedures

Georgia Institute of Technology Institute Budget Planning & Administration Policies and Procedures Table of Contents Table of Contents... 1 General Information... 2 Definitions... 4 Resource Allocation

Georgia Institute of Technology Institute Budget Planning & Administration Policies and Procedures Table of Contents Table of Contents... 1 General Information... 2 Definitions... 4 Resource Allocation

University of California, Merced Final and Preliminary All-Funds Base Budget

University of California, Merced 201516 Final and 201617 Preliminary AllFunds Base Budget FINAL Division of Planning and Budget Finance Group 1 WE WELCOME YOUR COMMENTS Division of Planning and Budget

University of California, Merced 201516 Final and 201617 Preliminary AllFunds Base Budget FINAL Division of Planning and Budget Finance Group 1 WE WELCOME YOUR COMMENTS Division of Planning and Budget

NORTHWESTERN STATE UNIVERSITY Budget Development. Budget Model

VII-2 Budget Development NORTHWESTERN STATE UNIVERSITY Budget Development Budget Model The Planning, Programming, and Budget Execution (PPBE) model best fits the University s Budget Development. This model

VII-2 Budget Development NORTHWESTERN STATE UNIVERSITY Budget Development Budget Model The Planning, Programming, and Budget Execution (PPBE) model best fits the University s Budget Development. This model

University of Houston-Clear Lake Appendix A - Allocation of New FY 2014 Resources

Appendix A - Allocation of New FY 2014 Resources Revenue Changes A Reallocations/Reductions B Appropriations Bill 1 Reallocations $ (920,892) 1 General Revenue $ 1,310,875 2 Reductions (985,000) 2 State

Appendix A - Allocation of New FY 2014 Resources Revenue Changes A Reallocations/Reductions B Appropriations Bill 1 Reallocations $ (920,892) 1 General Revenue $ 1,310,875 2 Reductions (985,000) 2 State

RESOURCE. Sequoias Community College District. College of the Sequoias

RESOURCE A L L O C AT I O N Sequoias Community College District College of the Sequoias College of the Sequoias 2014 Resource Allocation Manual College of the Sequoias Community College District Visalia

RESOURCE A L L O C AT I O N Sequoias Community College District College of the Sequoias College of the Sequoias 2014 Resource Allocation Manual College of the Sequoias Community College District Visalia

Leadership Steering Committee Report

Leadership Steering Committee Report Response to Administrative Review of Texas A&M University conducted by PwC The starting point The PwC report recognizes that Texas A&M University is already highly

Leadership Steering Committee Report Response to Administrative Review of Texas A&M University conducted by PwC The starting point The PwC report recognizes that Texas A&M University is already highly

EXECUTIVE SUMMARY. Performance Fund* 4,414,100 Total $74,448,900

EXECUTIVE SUMMARY House Bill 200, the Executive Branch Budget, was passed by the 2018 Regular Session of the Kentucky General Assembly and provides a state expenditure plan for the 2018-20 biennium. The

EXECUTIVE SUMMARY House Bill 200, the Executive Branch Budget, was passed by the 2018 Regular Session of the Kentucky General Assembly and provides a state expenditure plan for the 2018-20 biennium. The

TABLE OF CONTENTS. Graphs 1-3. Statement of Net Assets 4-6. Statement of Revenues, Expenses and Changes in Net Assets 7. Statement of Cash Flows 8

Financial Statements October 30, 2011 TABLE OF CONTENTS Title Page Graphs 1-3 Statement of Net Assets 4-6 Statement of Revenues, Expenses and Changes in Net Assets 7 Statement of Cash Flows 8 Total Expenditures

Financial Statements October 30, 2011 TABLE OF CONTENTS Title Page Graphs 1-3 Statement of Net Assets 4-6 Statement of Revenues, Expenses and Changes in Net Assets 7 Statement of Cash Flows 8 Total Expenditures

Budget Preparation Manual FY

Budget Preparation Manual FY 2018-19 Table of Contents Introduction...1 Purpose...1 Strategic Plan...1 Challenges...1 The Process...2 Initial E&G Budget Submission (BUDRPT19) and Updated Scenarios...2

Budget Preparation Manual FY 2018-19 Table of Contents Introduction...1 Purpose...1 Strategic Plan...1 Challenges...1 The Process...2 Initial E&G Budget Submission (BUDRPT19) and Updated Scenarios...2

New Jersey Institute of Technology

New Jersey Institute of Technology FY18 Budget Status Report and FY19 Budget Development Status Presented to the Joint Session of the Strategic Planning Steering Committee and Committee on Academic Strategic

New Jersey Institute of Technology FY18 Budget Status Report and FY19 Budget Development Status Presented to the Joint Session of the Strategic Planning Steering Committee and Committee on Academic Strategic

Finances, Budget and Facilities

III.1 IChapter II Finances, Budget and Facilities A Financial Reporting 1. Fund Accounting Principles & Objectives................. III.3 2. Types of Funds................................. III.4 3. Funding

III.1 IChapter II Finances, Budget and Facilities A Financial Reporting 1. Fund Accounting Principles & Objectives................. III.3 2. Types of Funds................................. III.4 3. Funding

Lewis-Clark State College Policy: Page: 1 of 6 Policy and Procedures Date: 6/2018 Rev: New

Lewis-Clark State College Policy: 4.125 Page: 1 of 6 Subject: Budget Policy Background: This policy describes responsibility for budgetary control and specific actions required in the event of deficits.

Lewis-Clark State College Policy: 4.125 Page: 1 of 6 Subject: Budget Policy Background: This policy describes responsibility for budgetary control and specific actions required in the event of deficits.

Fiscal Year (FY13) Operating Budget and Capital Budget Overview

Operating Budget and Capital Budget Overview") Approved by President Rush Fiscal Year 2012-2013 (FY13) Operating Budget and Capital Budget Overview Background A university budget represents the complex interchange between revenue streams that support

Approved by President Rush Fiscal Year 2012-2013 (FY13) Operating Budget and Capital Budget Overview Background A university budget represents the complex interchange between revenue streams that support

FY2016 FY2018 Projection Estimate

FY2016 FY2018 Projection Estimate November 16, 2016 11.16.16 11.16.16 Estimate Projection FY2016 Actual Fund I & IX FY2017 FY2018 10.8% CR decrease 4% CR decrease 0% CR decrease REVENUE $350K increase

FY2016 FY2018 Projection Estimate November 16, 2016 11.16.16 11.16.16 Estimate Projection FY2016 Actual Fund I & IX FY2017 FY2018 10.8% CR decrease 4% CR decrease 0% CR decrease REVENUE $350K increase

Budget Flint Campus

2016-2017 Budget Flint Campus This page left blank intentionally. Table of Contents The University of Michigan - Flint Section One - Summary of Budgeted Revenues and Expenditures Schedule A: Summary by

2016-2017 Budget Flint Campus This page left blank intentionally. Table of Contents The University of Michigan - Flint Section One - Summary of Budgeted Revenues and Expenditures Schedule A: Summary by

TABLE OF CONTENTS. Graphs 1-3. Statement of Net Assets 4-6. Statement of Revenues, Expenses and Changes in Net Assets 7. Statement of Cash Flows 8

Financial Statements November 30, 2011 TABLE OF CONTENTS Title Page Graphs 1-3 Statement of Net Assets 4-6 Statement of Revenues, Expenses and Changes in Net Assets 7 Statement of Cash Flows 8 Total Expenditures

Financial Statements November 30, 2011 TABLE OF CONTENTS Title Page Graphs 1-3 Statement of Net Assets 4-6 Statement of Revenues, Expenses and Changes in Net Assets 7 Statement of Cash Flows 8 Total Expenditures

Budget Model Initiative (Phase 1)

") Budget Model Initiative (Phase 1) March 2017 Higher Purpose. Greater Good. 1 The Budget Model initiative is divided into two phases Phase 1: Transparency (Fall 2016 / Winter 2017) Phase 2: Redesign (Q2

Budget Model Initiative (Phase 1) March 2017 Higher Purpose. Greater Good. 1 The Budget Model initiative is divided into two phases Phase 1: Transparency (Fall 2016 / Winter 2017) Phase 2: Redesign (Q2

Annual Summary

2011-2012 Annual Summary Dept Name: STUDENT FINANCIAL AID Grants and Contracts Sponsored Program Support by Fiscal Year Departmental Proposals Departmental Awards # Amount 5 $1,093,330 data as of: Monday,

2011-2012 Annual Summary Dept Name: STUDENT FINANCIAL AID Grants and Contracts Sponsored Program Support by Fiscal Year Departmental Proposals Departmental Awards # Amount 5 $1,093,330 data as of: Monday,

University of Maryland FY 2019 Working Budget Instructions

MEMORANDUM TO: FROM: Divisional and College Business Officers Colleen Dove Auburger Executive Director, Financial Operations, Division of Administration and Finance DATE: April 24, 2018 SUBJECT: FY 2019

MEMORANDUM TO: FROM: Divisional and College Business Officers Colleen Dove Auburger Executive Director, Financial Operations, Division of Administration and Finance DATE: April 24, 2018 SUBJECT: FY 2019

The Florida International University Budget Town Hall Discussion. March 9, 2009

The Florida International University Budget Town Hall Discussion March 9, 2009 1 FLORIDA INTERNATIONAL UNIVERSITY AGENDA Direction What is the University s strategic direction? What are the state revenue

The Florida International University Budget Town Hall Discussion March 9, 2009 1 FLORIDA INTERNATIONAL UNIVERSITY AGENDA Direction What is the University s strategic direction? What are the state revenue

New Jersey Institute of Technology

New Jersey Institute of Technology FY2018 Budget Development Presented to the Board of Trustees June 1, 2017 1 FY2018 Developing Operating Budget The developing FY2018 operating budget is the result of

New Jersey Institute of Technology FY2018 Budget Development Presented to the Board of Trustees June 1, 2017 1 FY2018 Developing Operating Budget The developing FY2018 operating budget is the result of

FY 19 & 20 Operating and Capital Budget Calendar Page 1 of 5

Page 1 of 5 August 1, 2018 Run faculty salary report in data warehouse to validate base salary correct notify Provost of discrepancies (this is different than the Payroll report) September 2018 FY 2019

Page 1 of 5 August 1, 2018 Run faculty salary report in data warehouse to validate base salary correct notify Provost of discrepancies (this is different than the Payroll report) September 2018 FY 2019

TABLE OF CONTENTS. Graphs 1-3. Statement of Net Assets 4-6. Statement of Revenues, Expenses and Changes in Net Assets 7. Statement of Cash Flows 8

Financial Statements December 31, 2011 TABLE OF CONTENTS Title Page Graphs 1-3 Statement of Net Assets 4-6 Statement of Revenues, Expenses and Changes in Net Assets 7 Statement of Cash Flows 8 Total Expenditures

Financial Statements December 31, 2011 TABLE OF CONTENTS Title Page Graphs 1-3 Statement of Net Assets 4-6 Statement of Revenues, Expenses and Changes in Net Assets 7 Statement of Cash Flows 8 Total Expenditures

PROPOSED FY 2018 EDUCATIONAL & GENERAL BUDGETS

PROPOSED FY 2018 EDUCATIONAL & GENERAL BUDGETS Proposed to Board of Trustees Prepared by the Office of Finance and Administration June 2017 TABLE OF CONTENTS Page No. Bowling Green Campus Income & Expenditure

PROPOSED FY 2018 EDUCATIONAL & GENERAL BUDGETS Proposed to Board of Trustees Prepared by the Office of Finance and Administration June 2017 TABLE OF CONTENTS Page No. Bowling Green Campus Income & Expenditure

Budget Reduction and Efficiency Actions Updated February 3, 2009

Budget Reduction and Efficiency Actions Updated Arizona State University has taken a number of management actions that result in lower cost structures and improved efficiency. These measures have been

Budget Reduction and Efficiency Actions Updated Arizona State University has taken a number of management actions that result in lower cost structures and improved efficiency. These measures have been

Highlights financial report. June 30 June (in thousands)

") Highlights FINANCIAL (in thousands) June 30 June 30 2000 1999 Total revenues $1,680,943 $1,367,175 Total cash gifts and equipment gifts $220,642 $211,215 Capital expenditures $118,799 $94,896 Total assets

Highlights FINANCIAL (in thousands) June 30 June 30 2000 1999 Total revenues $1,680,943 $1,367,175 Total cash gifts and equipment gifts $220,642 $211,215 Capital expenditures $118,799 $94,896 Total assets

Introduction to the UND s New Budget Model

Introduction to the UND s New Budget Model Existing Budget Model? UND s budget approach has been historical and incremental Meaning: The next year s budget for a unit would be what units got this year

Introduction to the UND s New Budget Model Existing Budget Model? UND s budget approach has been historical and incremental Meaning: The next year s budget for a unit would be what units got this year

FY 2019 Budget Development Subcommittee Consensus Budget Balancing Items

FY 2019 Budget Development Subcommittee Consensus Budget Balancing Items Planning Projection, March 8, 2018 ($ 5,904,500) UPDATES, ADDITIONS & CORRECTIONS Tuition HEPI Update/Correction $ 430,000 The 2017

FY 2019 Budget Development Subcommittee Consensus Budget Balancing Items Planning Projection, March 8, 2018 ($ 5,904,500) UPDATES, ADDITIONS & CORRECTIONS Tuition HEPI Update/Correction $ 430,000 The 2017

UNIVERSITY OF ILLINOIS AT URBANA-CHAMPAIGN FY 2017 BUDGET GUIDELINES

UNIVERSITY OF ILLINOIS AT URBANA-CHAMPAIGN FY 2017 BUDGET GUIDELINES SALARY RATE INCREASES At the time of issuing these guidelines, there is no general salary program except where union settlements dictate

UNIVERSITY OF ILLINOIS AT URBANA-CHAMPAIGN FY 2017 BUDGET GUIDELINES SALARY RATE INCREASES At the time of issuing these guidelines, there is no general salary program except where union settlements dictate

Presented to the Board of Trustees

Presented to the Board of Trustees 0 July 5, 2016 CSPP Budget Decision-Making Principles & Process The budget planning and development will be guided by the following Board of Trustees approved resource

Presented to the Board of Trustees 0 July 5, 2016 CSPP Budget Decision-Making Principles & Process The budget planning and development will be guided by the following Board of Trustees approved resource

UH-Clear Lake Budget

FY2016 Total Budget $ Millions Operating Budget $ 131.5 Capital Facilities 23.1 Total $ 154.6 Operating Budget Source of Funds Other Operating, $2.0M 2% Tuition & Fees $71.1M 54% Contracts & Grants *,

FY2016 Total Budget $ Millions Operating Budget $ 131.5 Capital Facilities 23.1 Total $ 154.6 Operating Budget Source of Funds Other Operating, $2.0M 2% Tuition & Fees $71.1M 54% Contracts & Grants *,

Office of Finance & Administration. June BGS SU FY Pr ropo osed Budgets. Educational & General Budgets (Bowling Green & Firelands Campus)

") Office of Finance & Administration June 2012 BGS SU FY 20 13 Pr ropo osed Budgets BGSU FY 2013 Proposed Budgets Educational & General Budgets (Bowling Green & Firelands Campus) General Fee & Related Auxiliary

Office of Finance & Administration June 2012 BGS SU FY 20 13 Pr ropo osed Budgets BGSU FY 2013 Proposed Budgets Educational & General Budgets (Bowling Green & Firelands Campus) General Fee & Related Auxiliary

M E M O R A N D U M. Noel Sloan, Vice President for Administration and Finance and Chief Financial Officer

TEXAS TECH UNIVERSITY Office of the Vice President for Administration and Finance Box 42006 Lubbock, Texas 79409-2006 (806) 742-4250 (806) 742-6600 (FAX) M E M O R A N D U M TO: FROM: Financial Managers

TEXAS TECH UNIVERSITY Office of the Vice President for Administration and Finance Box 42006 Lubbock, Texas 79409-2006 (806) 742-4250 (806) 742-6600 (FAX) M E M O R A N D U M TO: FROM: Financial Managers

Financial Statements September 31, 2010

Financial Statements September 31, 2010 TABLE OF CONTENTS Title Page Graphs 1-3 Statement of Net Assets 4-6 Statement of Revenues, Expenses and Changes in Net Assets 7 Statement of Cash Flows 8 Total Expenditures

Financial Statements September 31, 2010 TABLE OF CONTENTS Title Page Graphs 1-3 Statement of Net Assets 4-6 Statement of Revenues, Expenses and Changes in Net Assets 7 Statement of Cash Flows 8 Total Expenditures

General Budget Terminology

Presentation FY 2018-19 Operating Title Budget Subtitle June 22, 2018 2 General Budget Terminology Current Funds Budget The current funds budget includes those economic resources of the institution which

Presentation FY 2018-19 Operating Title Budget Subtitle June 22, 2018 2 General Budget Terminology Current Funds Budget The current funds budget includes those economic resources of the institution which

FISCAL PROFILE

FISCAL PROFILE 2007-2011 The University of North Carolina at Greensboro FISCAL PROFILE 2007-2011 INTRODUCTION This document is an overview of financial, budgetary, and student data for The University of

FISCAL PROFILE 2007-2011 The University of North Carolina at Greensboro FISCAL PROFILE 2007-2011 INTRODUCTION This document is an overview of financial, budgetary, and student data for The University of

Budgeting and Planning Process as of FY17

Budgeting and Planning Process as of FY17 Summary The budget is an important annual planning document for the university and reflects choices, priorities and tactics set forth as the result of intensive

Budgeting and Planning Process as of FY17 Summary The budget is an important annual planning document for the university and reflects choices, priorities and tactics set forth as the result of intensive

CARROLL COMMUNITY COLLEGE FINANCIAL STATEMENTS YEARS ENDED JUNE 30, 2017 AND 2016

FINANCIAL STATEMENTS YEARS ENDED TABLE OF CONTENTS YEARS ENDED INDEPENDENT AUDITORS REPORT 1 MANAGEMENT S DISCUSSION AND ANALYSIS 3 FINANCIAL STATEMENTS STATEMENTS OF NET POSITION (DEFICIT) 13 STATEMENTS

FINANCIAL STATEMENTS YEARS ENDED TABLE OF CONTENTS YEARS ENDED INDEPENDENT AUDITORS REPORT 1 MANAGEMENT S DISCUSSION AND ANALYSIS 3 FINANCIAL STATEMENTS STATEMENTS OF NET POSITION (DEFICIT) 13 STATEMENTS

Overview of the University s Operating Budget. University of Mary Washington University Budget Advisory Committee September 11, 2013

Overview of the University s Operating Budget University of Mary Washington University Budget Advisory Committee September 11, 2013 Discussion Points 2014-15 Budget Development Timeline Overview of the

Overview of the University s Operating Budget University of Mary Washington University Budget Advisory Committee September 11, 2013 Discussion Points 2014-15 Budget Development Timeline Overview of the

LEHIGH University. Financial Planning Report With Budget

LEHIGH University Financial Planning Report With 2012-2013 Budget L E H I G H U N I V E R S I T Y 2 0 1 2-1 3 B U D G E T ------------------------- T A B L E O F C O N T E N T S PAGE I. COMMENTARY 1-9

LEHIGH University Financial Planning Report With 2012-2013 Budget L E H I G H U N I V E R S I T Y 2 0 1 2-1 3 B U D G E T ------------------------- T A B L E O F C O N T E N T S PAGE I. COMMENTARY 1-9

ASL Budget Forum. May 8, 2017

ASL Budget Forum May 8, 2017 Today s Agenda Final model (changes) Governance Philosophy Current Governance Structure New Governance Structure Model Changes Changes since Winter Forums Revenue estimates

ASL Budget Forum May 8, 2017 Today s Agenda Final model (changes) Governance Philosophy Current Governance Structure New Governance Structure Model Changes Changes since Winter Forums Revenue estimates

Budget Preparation Manual FY

Budget Preparation Manual FY 2017-18 Table of Contents Introduction...1 Purpose...1 Strategic Plan: Impact 2015 Extended to 2017...1 Challenges...1 The Process...2 Initial E&G Budget Submission (BUDRPT18)

Budget Preparation Manual FY 2017-18 Table of Contents Introduction...1 Purpose...1 Strategic Plan: Impact 2015 Extended to 2017...1 Challenges...1 The Process...2 Initial E&G Budget Submission (BUDRPT18)

FY Operating Budget

FY 2014-15 Operating Budget Board of Regents Meeting June 26-27, 2014 FY 2014-15 Colorado Tuition Rate Increases Resident Undergraduate Tuition & Fee Rate Increases Institution FY14 to FY15 Percent Increase

FY 2014-15 Operating Budget Board of Regents Meeting June 26-27, 2014 FY 2014-15 Colorado Tuition Rate Increases Resident Undergraduate Tuition & Fee Rate Increases Institution FY14 to FY15 Percent Increase

THE UNIVERSITY OF IOWA Comprehensive Fiscal Report FY 2014

THE UNIVERSITY OF IOWA Comprehensive Fiscal Report FY 2014 Each year, the University of Iowa is required to submit to the Board of Regents, a comprehensive fiscal report which compares actual revenues

THE UNIVERSITY OF IOWA Comprehensive Fiscal Report FY 2014 Each year, the University of Iowa is required to submit to the Board of Regents, a comprehensive fiscal report which compares actual revenues

1 Campus Budget. 1.1 Revenues

UCR Budget Primer prepared for Senate Committee on Planning & Budget as of September 2016 as understood by Christian Shelton with thanks to VC Maria Anguiano & former committee chair Ken Barish Abstract

UCR Budget Primer prepared for Senate Committee on Planning & Budget as of September 2016 as understood by Christian Shelton with thanks to VC Maria Anguiano & former committee chair Ken Barish Abstract

Operating Budget Salary Increase Guidelines INTRODUCTION

University of Louisville 2011-12 Operating Budget SALARY INCREASE GUIDELINES INTRODUCTION President Ramsey and the senior leadership team are committed to providing equitable compensation to all University

University of Louisville 2011-12 Operating Budget SALARY INCREASE GUIDELINES INTRODUCTION President Ramsey and the senior leadership team are committed to providing equitable compensation to all University

Overview of Responsibility Centered Management (RCM) Budget Model Aug 2017

Budget Model Aug 2017") Overview of Responsibility Centered Management (RCM) Budget Model Aug 2017 The Responsibility Centered Management Budget Model was designed with the input of the University community to 1) encourage revenue

Overview of Responsibility Centered Management (RCM) Budget Model Aug 2017 The Responsibility Centered Management Budget Model was designed with the input of the University community to 1) encourage revenue

Table of Contents. Executive Summary... Overview...

Table of Contents Executive Summary... Overview... iii 1 Delegation of Authority to the Administration... Summary Revenue and Expense by Program... Summary Revenue and Expense by Account... Operating Resources

Table of Contents Executive Summary... Overview... iii 1 Delegation of Authority to the Administration... Summary Revenue and Expense by Program... Summary Revenue and Expense by Account... Operating Resources

Operating Budget FY 2009 Budget (in $M)

") Operating Budget REVENUES Tuition and Fees 671.8 Financial Aid (230.4) Grants and Contracts - (Direct and Indirect) 387.4 Endowment Distribution 272.5 Other Investment Income 48.1 Gifts and Restricted

Operating Budget REVENUES Tuition and Fees 671.8 Financial Aid (230.4) Grants and Contracts - (Direct and Indirect) 387.4 Endowment Distribution 272.5 Other Investment Income 48.1 Gifts and Restricted

STRATEGIES ASSESSMENT

DRAFT MONTANA STATE UNIVERSITY - BOZEMAN Annual Planning & Budgeting Cycle STRATEGIES PLANNING MISSION and VISION BUDGETING ASSESSMENT c:pba plan 02.20.01 Planning & Budgeting Committee Organization President

DRAFT MONTANA STATE UNIVERSITY - BOZEMAN Annual Planning & Budgeting Cycle STRATEGIES PLANNING MISSION and VISION BUDGETING ASSESSMENT c:pba plan 02.20.01 Planning & Budgeting Committee Organization President

SECTION B: Budgeting. I. Legislative Budget Request

SECTION B: Budgeting I. Legislative Budget Request The College prepares a legislative budget request (currently on a biennial basis) as a plan of operation for the legislative funding period. This biennial

SECTION B: Budgeting I. Legislative Budget Request The College prepares a legislative budget request (currently on a biennial basis) as a plan of operation for the legislative funding period. This biennial

FY2017 Budget Discussion Administrative Council Presentation April

FY2017 Budget Discussion Administrative Council Presentation April 6 2016 2015 Boise State University 1 2016-17 General State Appropriations College and University Allocation BSU ISU UI LCSC Systemwide

FY2017 Budget Discussion Administrative Council Presentation April 6 2016 2015 Boise State University 1 2016-17 General State Appropriations College and University Allocation BSU ISU UI LCSC Systemwide

$97.6 million for a 1.56% cost of living adjustment (COLA) to the unrestricted general state apportionment

to the unrestricted general state apportionment") 2017-18 State Budget - Impact to Community Colleges The state budget will include the following items: $97.6 million for a 1.56% cost of living adjustment (COLA) to the unrestricted general state apportionment

2017-18 State Budget - Impact to Community Colleges The state budget will include the following items: $97.6 million for a 1.56% cost of living adjustment (COLA) to the unrestricted general state apportionment

F I N A N C I A L R E P O R T

3 M A N A G E M E N T S D I S C U S S I O N A N D A N A L Y S I S Beginning in fiscal year 2002 the university will implement the new financial reporting requirements contained in Statement Numbers 34

3 M A N A G E M E N T S D I S C U S S I O N A N D A N A L Y S I S Beginning in fiscal year 2002 the university will implement the new financial reporting requirements contained in Statement Numbers 34

Five-Year Financial Plan (FY2019 FY 2023) 02/23/18

02/23/18") Five-Year Financial Plan (FY2019 FY 2023) 02/23/18 Renewing Our Vow to the Commonwealth Six years ago, we committed to a bold vision for UK- rebuild our campus, grow funds, support faculty and staff, and

Five-Year Financial Plan (FY2019 FY 2023) 02/23/18 Renewing Our Vow to the Commonwealth Six years ago, we committed to a bold vision for UK- rebuild our campus, grow funds, support faculty and staff, and

UNIVERSITY OF NORTH DAKOTA BUDGET OFFICE MEMORANDUM

UNIVERSITY OF NORTH DAKOTA BUDGET OFFICE MEMORANDUM DATE: April 20, 2018 TO: FROM: RE: Deans, Department Heads and Administrators Cindy Fetsch and Jennifer Moe, Budget Office 2018-2019 Personnel, Operating

UNIVERSITY OF NORTH DAKOTA BUDGET OFFICE MEMORANDUM DATE: April 20, 2018 TO: FROM: RE: Deans, Department Heads and Administrators Cindy Fetsch and Jennifer Moe, Budget Office 2018-2019 Personnel, Operating

Oregon State University 4 th Quarter Operating Management Report

Oregon State University 4 th Quarter Operating Management Report Oregon State University s 4 th Quarter FY 2014 Operating Management Report presents the final fiscal year operating results for the three

Oregon State University 4 th Quarter Operating Management Report Oregon State University s 4 th Quarter FY 2014 Operating Management Report presents the final fiscal year operating results for the three

FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORTS YEAR ENDED JUNE 30, 2017 TABLE OF CONTENTS

FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORTS YEAR ENDED JUNE 30, 2017 TABLE OF CONTENTS Page MANAGEMENT S LETTER... 1 INDEPENDENT AUDITOR S REPORT... 2-4 MANAGEMENT S DISCUSSION AND ANALYSIS...

FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORTS YEAR ENDED JUNE 30, 2017 TABLE OF CONTENTS Page MANAGEMENT S LETTER... 1 INDEPENDENT AUDITOR S REPORT... 2-4 MANAGEMENT S DISCUSSION AND ANALYSIS...

3/21/2017 WASHINGTON STATE UNIVERSITY. March 21, Recording date of this workshop is

Understanding the University Budget Kelley Westhoff Operating Budget Director March 21, 2017 Recording date of this workshop is March 21, 2017 Some of the rules and procedures discussed in this workshop

Understanding the University Budget Kelley Westhoff Operating Budget Director March 21, 2017 Recording date of this workshop is March 21, 2017 Some of the rules and procedures discussed in this workshop

BGSU FY P ropose ed Bu dgets

Office of Finance & Administration June 2013 BGSU FY 20 014 P ropose ed Bu dgets BGSU FY 2014 Proposed Budgets Educational & General Budgets (Bowling Green & Firelands Campus) General Fee & Related Auxiliary

Office of Finance & Administration June 2013 BGSU FY 20 014 P ropose ed Bu dgets BGSU FY 2014 Proposed Budgets Educational & General Budgets (Bowling Green & Firelands Campus) General Fee & Related Auxiliary

FISCAL 2018 BUDGET UPDATE

FISCAL 2018 BUDGET UPDATE BASED ON APPROVED BUDGET INSTITUTE BUDGET PLANNING AND ADMINISTRATION JULY 1, 2017 Outline 1. Capital Budget funding sources & current projects 2. Fiscal 2018 Operating Budget

FISCAL 2018 BUDGET UPDATE BASED ON APPROVED BUDGET INSTITUTE BUDGET PLANNING AND ADMINISTRATION JULY 1, 2017 Outline 1. Capital Budget funding sources & current projects 2. Fiscal 2018 Operating Budget

EXECUTIVE SUMMARY. The enacted budget, House Bill 303, and Senate Bill 153 include the following WKU state funding for FY 2018:

EXECUTIVE SUMMARY The enacted 2016-18 Budget of the Commonwealth (HB 303) directed the Council on Postsecondary Education (CPE) to establish a working group comprised of the President of the Council, the

EXECUTIVE SUMMARY The enacted 2016-18 Budget of the Commonwealth (HB 303) directed the Council on Postsecondary Education (CPE) to establish a working group comprised of the President of the Council, the

California State University Long Beach: Budget Outlook February, 2012

California State University Long Beach: Budget Outlook 2012-13 February, 2012 Gov s Proposed 2012-13 Budget 05 Jan 2012, Gov Brown proposed 2012-13 budget Addresses $9.2b budget deficit Depends on successful

California State University Long Beach: Budget Outlook 2012-13 February, 2012 Gov s Proposed 2012-13 Budget 05 Jan 2012, Gov Brown proposed 2012-13 budget Addresses $9.2b budget deficit Depends on successful

OPERATING BUDGETS FOR FISCAL YEAR

OPERATING BUDGETS FOR FISCAL YEAR 2018 FY 2018 BUDGET DOCUMENTS A. The FY 2018 Education and General Budget Page 1. Executive Summary 1 2. General Budget Priorities 1 3. Revenue Assumptions 1 4. Planned

OPERATING BUDGETS FOR FISCAL YEAR 2018 FY 2018 BUDGET DOCUMENTS A. The FY 2018 Education and General Budget Page 1. Executive Summary 1 2. General Budget Priorities 1 3. Revenue Assumptions 1 4. Planned

Financial Statements January 31, 2015

Financial Statements January 31, 2015 TABLE OF CONTENTS Title Page Graphs 1-3 Statement of Net Position 4-8 Statement of Revenues, Expenses and Changes in Net Position 9 Statement of Cash Flows 10 Total

Financial Statements January 31, 2015 TABLE OF CONTENTS Title Page Graphs 1-3 Statement of Net Position 4-8 Statement of Revenues, Expenses and Changes in Net Position 9 Statement of Cash Flows 10 Total

RCM Review. Responsibility Centered Management Review September Budget Planning & Resource Analysis

RCM Review Responsibility Centered Management Review September 2011 Budget Planning & Resource Analysis What is RCM and RCB? RCM is Responsibility Centered Management RCB is Responsibility Centered Budgeting

RCM Review Responsibility Centered Management Review September 2011 Budget Planning & Resource Analysis What is RCM and RCB? RCM is Responsibility Centered Management RCB is Responsibility Centered Budgeting

CARROLL COMMUNITY COLLEGE FINANCIAL STATEMENTS JUNE 30, 2016 AND 2015

FINANCIAL STATEMENTS TABLE OF CONTENTS YEARS ENDED INDEPENDENT AUDITORS REPORT 1 MANAGEMENT S DISCUSSION AND ANALYSIS 3 FINANCIAL STATEMENTS STATEMENTS OF NET POSITION (DEFICIT) 12 STATEMENTS OF REVENUES,

FINANCIAL STATEMENTS TABLE OF CONTENTS YEARS ENDED INDEPENDENT AUDITORS REPORT 1 MANAGEMENT S DISCUSSION AND ANALYSIS 3 FINANCIAL STATEMENTS STATEMENTS OF NET POSITION (DEFICIT) 12 STATEMENTS OF REVENUES,

Financial Statements February 28, 2015

Financial Statements February 28, 2015 TABLE OF CONTENTS Title Page Graphs 1-3 Statement of Net Position 4-8 Statement of Revenues, Expenses and Changes in Net Position 9 Statement of Cash Flows 10 Total

Financial Statements February 28, 2015 TABLE OF CONTENTS Title Page Graphs 1-3 Statement of Net Position 4-8 Statement of Revenues, Expenses and Changes in Net Position 9 Statement of Cash Flows 10 Total

Transition Review Team Report to President Stearns August 2017

Transition Review Team Report to President Stearns August 2017 In December 2016, the Commissioner of Higher Education sent a memorandum to the campus and the Board of Regents discussing a transition plan

Transition Review Team Report to President Stearns August 2017 In December 2016, the Commissioner of Higher Education sent a memorandum to the campus and the Board of Regents discussing a transition plan

GEORGIA INSTITUTE OF TECHNOLOGY BUDGET SUBMISSION INSTRUCTIONS FOR FISCAL YEAR 2015

GEORGIA INSTITUTE OF TECHNOLOGY BUDGET SUBMISSION INSTRUCTIONS FOR FISCAL YEAR 2015 Purpose: The principal purpose of the budget planning process is to provide Georgia Tech s senior leadership the essential

GEORGIA INSTITUTE OF TECHNOLOGY BUDGET SUBMISSION INSTRUCTIONS FOR FISCAL YEAR 2015 Purpose: The principal purpose of the budget planning process is to provide Georgia Tech s senior leadership the essential

Biennium Open Budget Forum April 2009

2009-11 Biennium Open Budget Forum April 2009 Table of Contents Eastern Washington University Open Budget Forum April 2009 Comparison of Governor, House, & Senate Proposals.. A-1 A-4 Biennial Budget Proposals

2009-11 Biennium Open Budget Forum April 2009 Table of Contents Eastern Washington University Open Budget Forum April 2009 Comparison of Governor, House, & Senate Proposals.. A-1 A-4 Biennial Budget Proposals

Comparison of Unaudited Actual to Adopted Budget

Comparison of 2010-11 Unaudited Actual to 2011-12 Adopted Budget REVENUE EXPENSE - BUDGET EXPENSE - ACTUAL EXPENSE - ACTUAL One-time Decrease $1,000,000 Deficit Factor, $25 million in fee revenue shortfall

Comparison of 2010-11 Unaudited Actual to 2011-12 Adopted Budget REVENUE EXPENSE - BUDGET EXPENSE - ACTUAL EXPENSE - ACTUAL One-time Decrease $1,000,000 Deficit Factor, $25 million in fee revenue shortfall