California State University, Los Angeles University Resource Allocation Process for Change CURRENT ALLOCATION MODEL OVERVIEW

|

|

|

- Samson Paul

- 5 years ago

- Views:

Transcription

1

2

3

4 Overview

5 California State University, Los Angeles University Resource Allocation Process for Change CURRENT ALLOCATION MODEL OVERVIEW The University Resource Allocation, as defined by Administrative Procedure 212, establishes the policy and procedures for allocating the fiscal resources of the University. Campus budget allocations are based upon predefined Chancellor s Office allocations (formula-based) and the campus strategic initiatives (non-formula). Around January of each year, the President provides the preliminary budget guidelines that outline the campus priorities for the following year. The preliminary budget guidelines initiate the university s Resource Allocation Plan and these are provided to campus stakeholders for input, consultation, discussion and information. Following the Governor s January Budget, the Chancellor s Office provides preliminary funding allocation information for the next fiscal year. Administration identifies the funding changes and prepares a resource allocation handout for the Resource Allocation Advisory Committee (RAAC). The RAAC s role is to advise the President on budget policy, planning, and resource allocation matters. As outlined in Administrative Procedure 212 Section 5.10, RAAC members include faculty, administration and student representation. The Chancellor s Office issued the final budget allocation, B , on July 24, The University s General Fund base budget is $221,839,675 consisting of General Fund Appropriation, Tuition Fee Revenue, Non-Resident Tuition Revenue, and Other Fee Revenue and Reimbursements. General Fund Appropriation $ 103,544,039 Tuition Fee Revenue 112,223,870 Non-Resident Tuition Revenue 4,621,000 Other Fee Revenue & Reimbursements 1,450,766 Total Estimated Gross Budget $ 221,839,675 The University has operated under a traditional incremental (or decremental) budget model in which, generally speaking, annual increases (or decreases) are adjusted by a uniform percentage. The University provides annual base-funding to the Executive areas in support of their on-going operations. The budget allocations were as follows: Academic Affairs 65.90%, Student Affairs 7.59%, Administration and Finance 13.37%, Information Technology Services 7.98%, Office of the President 3.58%, and Institutional Advancement 1.57% 2. Benefits pool, compensation pool and University-wide programs are centrally managed. Included in the Executive allocations are restricted funds dedicated for specific programs or purposes (i.e., Financial Aid programs, utilities, University Reserve, etc.). The restricted funds cannot be used towards operational needs or to fund division deficits. SUMMARY BY EXECUTIVE OFFICE RAP BASE BUDGET RAP RESTRICTED BUDGET RAP ADJ. BASE BUDGET RAP % BASE BUDGET President's Area 6,760,859 (2,821,114) 3,939,745 a 3.58% Academic Affairs 72,918,904 (328,500) 72,590,404 b 65.90% Information Tech. Services 8,791, ,791, % Student Affairs 53,540,657 (45,174,869) 8,365,788 c 7.59% Admin. & Finance 22,595,735 (7,863,787) 14,731,948 d 13.37% Institutional Advancement 1,767,081 (35,880) 1,731,201 e 1.57% TOTALS 166,374,651 (56,224,150) 110,150,501 f % 1

6 Notes: a Excludes University Reserves b Excludes MSN graduate nursing c Excludes Federal and State Financial Aid Programs d Excludes Utilities, IRA, Child Care Center and Student Financial System upgrades. e Excludes Catalog f Excludes University-wide (i.e., Comp and Benefits Pool, Risk Pool premium) accounts which is about $11.5 M Strengths of Current Model: Incremental budgeting provides budgetary stability and allows operating units/colleges to plan multiple years into the future due to the predictability of funding. Base budget funding is systematic and provides operational continuity. Incremental budgeting is simple to understand (transparency) and easy to implement (efficiency). It simplifies the allocation process (formula-based) and facilitates accounting. Shortcomings of Current Model: Since only the incremental portion of the budgets is analyzed, this model may perpetuate inequities in funding that existed and does not encourage redirection of funds. Incremental allocation model is limited in its vision. The divisions are accountable for what they spend in the most basic sense. The model does not measure or link performance-based outcomes, relevance, quality and productivity with funding levels. The divisions have sense of base budget ownership (property rights). Based budget does not account for cost increases due to inflation or other economic uncertainties. NEW RESOURCE ALLOCATION MODEL TIMELINE TARGET DATES 1. Preliminary planning, research, and evaluation of requirements for Sep Dec development of new resource allocation model. This includes an assessment of current funding model. 2. Establish Budget Allocation Model Task Force to develop campus allocation principles and priorities and explore allocation model options. Jan Recommended committee composition: Resource Allocation Advisory Committee (RAAC); VP for Engagement and Economic Development and Chief of Staff; and one staff appointed by the President. 3. Assessment of base expenditure need: After the mid-year assessment, conduct campus wide zero-based Feb Apr assessment to establish fiscal year base expenditure need. 4. Design framework of the new allocation model(s) based on items 1 and 3. May 2014 Feb Vetting and feedback from campus constituents on allocation models. Mar June Selection and communication of the new allocation model. Jul Sep Implementation of new allocation model. Fiscal Year Post implementation evaluation and refinement of adopted model. Jul June

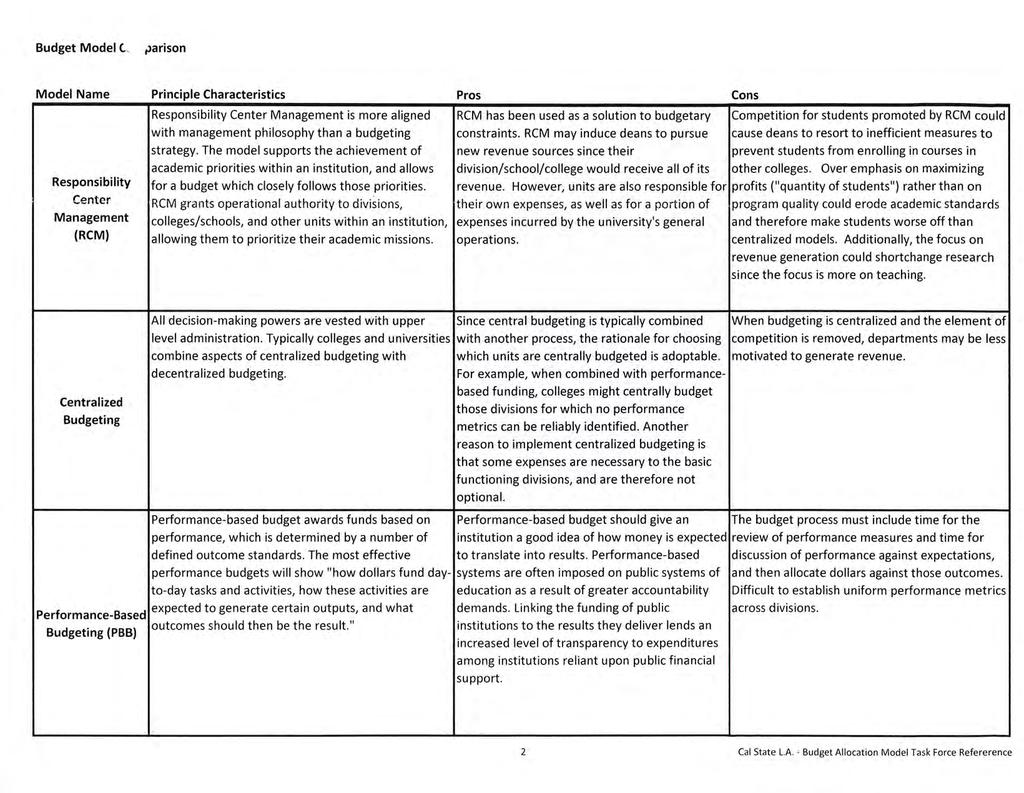

7 BUDGET MODELS IN HIGHER EDUCATION There are six budget models or budget-related practices used in higher education. The following overview of the budget models was derived from Hanoverresearch s published study 3 : Incremental Budgeting Definition: Traditional budget model where budget proposals and allocations are based upon the prior year s funding and only new revenue is allocated. Budget reductions are made as a percentage of the institution s historical budget, and are typically across-the-board. Benefit: Incremental budgeting has been popular in higher education since it is easy to implement, provides funding stability, and allows units and institutions to plan multiple years, due to the predictability of the model. Drawback: Difficult to determine where costs have been incurred and how these costs contribute to revenue and value creation. Institutions are accountable for what they spend. Zero-Based Budget Definition: The previous year s funding level is not considered in developing the following year s budget. Every part of the institution must re-request funding levels, and all spending must be re-justified. Benefit: Zero-based budgeting is an effective way of controlling for unnecessary costs. Since departments and divisions do not automatically receive a certain sum each year, all money allocated to a unit has a purpose, keeping waste and discretionary spending to a minimum. Drawback: Zero-based budgets take longer to prepare; hence, implementation is difficult. Activity-Based Budgeting Definition: Activity-based budgeting allocates funding to institutional activities with the highest return (in the form of increased revenues) for the institution. This may include developing and designing: Activity groupings for budgeting, in coordination with campus leaders and constituents; Fund resource grouping; Budget processes whereby allocation plans are used to align resources to institutional strategic objectives; and Implementing an activity-based campus budget allocation process. Drawback: Requires substantial time and resource commitment, which may not be feasible for some institutions. Responsibility Center Management (RCM) Definition: Responsibility Center Management is more aligned with management philosophy than a budgeting strategy. The model supports the achievement of academic priorities within an institution, and allows for a budget which closely follows those priorities. RCM grants operational authority to divisions, colleges/schools, and other units within an institution, allowing them to prioritize their academic missions. Each unit receives all of its own revenues and incomes, including the tuition for its enrolled students. Each unit is also assigned a portion of government support (where applicable). However, units are also responsible for their own expenses, as well as for a portion of expenses incurred by the university s general operations. Benefits: RCM has been used as a solution to budgetary constraints. RCM may induce deans to pursue new revenue sources since their division/school/college would receive all of its revenue. 3

8 Drawbacks: Competition for students promoted by RCM could cause deans to resort to inefficient measures to prevent students from enrolling in courses in other colleges. Centralized Budgeting Definition: All decision-making powers are vested with upper level administration. Typically colleges and universities combine aspects of centralized budgeting with decentralized budgeting. Benefits: Since central budgeting is typically combined with another process, the rationale for choosing which units are centrally budgeted is adoptable. For example, when combined with performance-based funding, colleges might centrally budget those divisions for which no performance metrics can be reliably identified. Another reason to implement centralized budgeting is that some expenses are necessary to the basic functioning divisions, and are therefore not optional. Drawback: When budgeting is centralized and the element of competition is removed, departments may be less motivated to generate revenue. Performance-Based Budgeting (PBB) Definition: Performance-based budget awards funds based on performance, which is determined by a number of defined outcome standards. The most effective performance budgets will show how dollars fund day-to-day tasks and activities, how these activities are expected to generate certain outputs, and what outcomes should then be the result. Benefit: Performance-based budget should give an institution a good idea of how money is expected to translate into results. Performance-based systems are often imposed on public systems of education as a result of greater accountability demands. Linking the funding of public institutions to the results they deliver lends an increased level of transparency to expenditures among institutions reliant upon public financial support. Drawback: The budget process must include time for the review of performance measures and time for discussion of performance against expectations, and then allocate dollars against those outcomes. University Resource Allocation Guiding Principles The following principles will guide the University s resource allocation process: Aligns budget and resources with the University s strategic plan, mission, vision and goals. Recognizes the differences and varying needs across divisions and programs. Provides for differential growth and differential needs within the University. Provides certainty of allocation (within the realities of public funding) for long-term efficiency and stability Assures transparency in decision making Be fair and equitable, based on the chosen plan and policies of the University. Promotes collaboration among divisions The following are the desired characteristics of a funding formula or guideline, according to published study of the Nevada System of Higher Education 4 : Equitable The funding formula should provide both horizontal equity (equal treatment of equals) and vertical equity (unequal treatment of equals) based on size, mission and growth characteristics of the institutions. 4

9 Adequacy-Driven The funding formula should determine the funding level needed by each institution to fulfill its approved mission. Goal-Based The funding formula should incorporate and reinforce the broad goals of the state for its system of colleges and universities as expressed through approved missions, quality expectations and performance standards. Mission-Sensitive The funding formula should be based on the recognition that different institutional missions (including differences in degree levels, program offerings, student readiness for college success and geographic location) require different rates of funding. Size-Sensitive The funding formula should reflect the impact that relative levels of student enrollment have on funding requirements, including economies of scale. Responsive The funding formula should reflect changes in institutional workloads and missions as well as changing external conditions in measuring the need for resources. Adaptable to Economic Conditions The funding formula should have the capacity to apply under a variety of economic situations, such as when the state appropriations for higher education are increasing, stable, or decreasing. Concerned with Stability The funding formula should not permit shifts in funding levels to occur more quickly than institutional managers can reasonably be expected to respond. Simple to Understand The funding formula should effectively communicate to key participants in the state budget process how changes in institutional characteristics and performance and modifications in budget policies will affect funding levels. Adaptable to Special Situations The funding formula should include provisions for supplemental state funding for unique activities that represent significant financial commitments and that are not common across the institutions. References: 1 CSU 2013/14 Enacted Budget Allocations University Resource Allocation Plan (RAP) Alternative Budget Models for Colleges and Universities, April 2, 2012, Hanoverresearch.com 4 Nevada System of Higher Education Evaluation of the NSHE Funding Formula, May 2011, MGT of America, Inc. 5

10

11

12

13

14

15

16 Timeline and Milestones

17

18 CSU Budget Allocation Model Survey

19

20

21 Budget Guiding Principles in Higher Education Nevada System of Higher Education Temple University Portland State University University of Wisconsin Milwaukee

22 Nevada System of Higher Education

23

24 Temple University

25

26 Portland State University

27

28

29

30

31 University of Wisconsin Milwaukee

32

33 Budget Allocation Models in Higher Education Allocating Resources State Systems of Public Higher Education Resource Allocation in Higher Education Budget Guiding Principles: Budget Model Matrix

34 Allocating Resources State Systems of Public Higher Education

35

36

37

38

39

40

41

42

43 Resource Allocation in Higher Education

44

45

46

47

48

49

50 Budget Guiding Principles Budget Model Matrix

51

52

53 Task Force Follow-Up Items

54

55

56

Resource Allocation, Management, and Planning Presentation for Board of Regents

Resource Allocation, Management, and Planning Presentation for Board of Regents April 27, 2018 1 Industry Overview 2 Recent Trends in Budgeting A significant number of institutions have recently decided

Resource Allocation, Management, and Planning Presentation for Board of Regents April 27, 2018 1 Industry Overview 2 Recent Trends in Budgeting A significant number of institutions have recently decided

New Campus Budget Model

New Campus Budget Model Moving to an All Funds Model May 25, 2016 Presented By: Nancy Warter-Perez Chair of the Academic Senate Peter McAllister Dean, College of Arts and Letters Lisa Chavez Vice President

New Campus Budget Model Moving to an All Funds Model May 25, 2016 Presented By: Nancy Warter-Perez Chair of the Academic Senate Peter McAllister Dean, College of Arts and Letters Lisa Chavez Vice President

Budget Model Assessment

Budget Model Assessment An Update on the Activities of the Joint Task Force on Resource Allocation Co-chairs: Elizabeth Chilton and Tim Anderson January 30 th, 2014 JTFRA Charge The Joint Task Force on

Budget Model Assessment An Update on the Activities of the Joint Task Force on Resource Allocation Co-chairs: Elizabeth Chilton and Tim Anderson January 30 th, 2014 JTFRA Charge The Joint Task Force on

Budget Planning and Development Workshop

Budget Planning and Development Workshop Presented By: Administration and Finance Student Life Information Technology Services Workshop Agenda Resource Allocation Overview All Funds Budget Model Budget

Budget Planning and Development Workshop Presented By: Administration and Finance Student Life Information Technology Services Workshop Agenda Resource Allocation Overview All Funds Budget Model Budget

Strategic Budgeting Initiative

Strategic Budgeting Initiative Senate Presentation November 5, 2013 Financial Challenges Sharply reduced state support Increased risk from tuition dependency At Auburn, dependency rose from 44% to 63%

Strategic Budgeting Initiative Senate Presentation November 5, 2013 Financial Challenges Sharply reduced state support Increased risk from tuition dependency At Auburn, dependency rose from 44% to 63%

General Fund Summary. Faculty Senate Presentation August 30, 2006

General Fund Summary Faculty Senate Presentation August 30, 2006 1 General Fund Summary Agenda State Budget Process CSU and Sac State General Fund Process Higher Education Compact Student Fees FTES Comparison

General Fund Summary Faculty Senate Presentation August 30, 2006 1 General Fund Summary Agenda State Budget Process CSU and Sac State General Fund Process Higher Education Compact Student Fees FTES Comparison

Resource Allocation, Management, and Planning Steering Committee #7

Resource Allocation, Management, and Planning Steering #7 August 28, 2018 1 Agenda Huron is pleased to partner with WKU on this resource allocation, management, and planning ( RAMP ) initiative. Our goals

Resource Allocation, Management, and Planning Steering #7 August 28, 2018 1 Agenda Huron is pleased to partner with WKU on this resource allocation, management, and planning ( RAMP ) initiative. Our goals

Sacramento City College

Sacramento City College Strategic ning System Title: Type: OPR: Collaborative Groups: References: Unit Procedures Unit (Departments, Divisions and/or Direct Reporting ) Academic Senate Budget Campus Development

Sacramento City College Strategic ning System Title: Type: OPR: Collaborative Groups: References: Unit Procedures Unit (Departments, Divisions and/or Direct Reporting ) Academic Senate Budget Campus Development

A New Academic Business Model for UMass Dartmouth

Resourcing the Mission A New Academic Business Model for UMass Dartmouth Budgetary Planning Council 2016 Public Higher Ed in the 21 st C The situation The social compact has been compromised Resulting

Resourcing the Mission A New Academic Business Model for UMass Dartmouth Budgetary Planning Council 2016 Public Higher Ed in the 21 st C The situation The social compact has been compromised Resulting

ANNUAL STRATEGIC PLANNING RETREAT AUGUST 21, 2012

ANNUAL STRATEGIC PLANNING RETREAT AUGUST 21, 2012 The mission of Los Angeles Southwest College is to facilitate student success, encourage life-long learning, and enrich the lives of its diverse community

ANNUAL STRATEGIC PLANNING RETREAT AUGUST 21, 2012 The mission of Los Angeles Southwest College is to facilitate student success, encourage life-long learning, and enrich the lives of its diverse community

Finance and Budget Modeling Town Hall. March 27 & 28, 2018

Finance and Budget Modeling Town Hall March 27 & 28, 2018 FINANCE AND BUDGET MODELING TASK FORCE Charge The Finance and Budget Modeling Task Force will create a new budget model that is transparent, data-driven,

Finance and Budget Modeling Town Hall March 27 & 28, 2018 FINANCE AND BUDGET MODELING TASK FORCE Charge The Finance and Budget Modeling Task Force will create a new budget model that is transparent, data-driven,

An Overview: Responsibility Center Management (RCM) Treasurer s Town Hall January 15, 2015

Treasurer s Town Hall January 15, 2015") An Overview: Responsibility Center Management (RCM) Treasurer s Town Hall January 15, 2015 Common University Budget Models EVERY TUB ON ITS OWN BOTTOM INCREMENTAL FORMULA-BASED RESPONSIBILITY CENTER MANAGEMENT

An Overview: Responsibility Center Management (RCM) Treasurer s Town Hall January 15, 2015 Common University Budget Models EVERY TUB ON ITS OWN BOTTOM INCREMENTAL FORMULA-BASED RESPONSIBILITY CENTER MANAGEMENT

EASTERN WASHINGTON UNIVERSITY BUDGET PRIMER

EASTERN WASHINGTON UNIVERSITY BUDGET PRIMER STATE BIENNIAL BUDGET CYCLE OFM issues budget instructions EVEN YEARS JUN EWU BIENNIAL BUDGET CYCLE ONGOING Agency Strategic Planning Agencies submit budget

EASTERN WASHINGTON UNIVERSITY BUDGET PRIMER STATE BIENNIAL BUDGET CYCLE OFM issues budget instructions EVEN YEARS JUN EWU BIENNIAL BUDGET CYCLE ONGOING Agency Strategic Planning Agencies submit budget

Introduction to the UND s New Budget Model

Introduction to the UND s New Budget Model Existing Budget Model? UND s budget approach has been historical and incremental Meaning: The next year s budget for a unit would be what units got this year

Introduction to the UND s New Budget Model Existing Budget Model? UND s budget approach has been historical and incremental Meaning: The next year s budget for a unit would be what units got this year

UTSA FY 2018 Budget 101 Presentation Foundational

UTSA FY 2018 Budget 101 Presentation Foundational Kathryn Funk-Baxter, Vice President for www.utsa.edu/businessaffairs UTSA Budget Process Current budgeting process overview Overview of Revenue (sources)

UTSA FY 2018 Budget 101 Presentation Foundational Kathryn Funk-Baxter, Vice President for www.utsa.edu/businessaffairs UTSA Budget Process Current budgeting process overview Overview of Revenue (sources)

Atlanta Public Schools Board of Education Budget Commission. September 20, 2018

Atlanta Public Schools Board of Education Budget Commission September 20, 2018 1 Agenda FY2020 Budget Timeline Anticipated Challenges for FY2020 FY2020 Resource and Expenditure Parameters 2 Goals To align

Atlanta Public Schools Board of Education Budget Commission September 20, 2018 1 Agenda FY2020 Budget Timeline Anticipated Challenges for FY2020 FY2020 Resource and Expenditure Parameters 2 Goals To align

What is Responsibility Centered Management?

Jim Florian Associate Vice President, Institutional Analysis Office of the Provost What is Responsibility Centered Management? Budget model that links budgets to activity Allocates revenues based on activity

Jim Florian Associate Vice President, Institutional Analysis Office of the Provost What is Responsibility Centered Management? Budget model that links budgets to activity Allocates revenues based on activity

UW-Platteville Pioneer Budget Model

UW-Platteville Pioneer Budget Model This document is intended to provide a comprehensive overview of the UW-Platteville s budget model. Specifically, this document will cover the following topics: Model

UW-Platteville Pioneer Budget Model This document is intended to provide a comprehensive overview of the UW-Platteville s budget model. Specifically, this document will cover the following topics: Model

Office of the Provost University of Illinois at Urbana-Champaign. 3 February 2016

Office of the Provost University of Illinois at Urbana-Champaign BUDGET REPORT GUIDANCE FOR FY17: CTE, DRES, I 3, KAM, KCPA, SPURLOCK, UNIVERSITY LIBRARY, LAW LIBRARY 3 February 2016 The campus finds itself

Office of the Provost University of Illinois at Urbana-Champaign BUDGET REPORT GUIDANCE FOR FY17: CTE, DRES, I 3, KAM, KCPA, SPURLOCK, UNIVERSITY LIBRARY, LAW LIBRARY 3 February 2016 The campus finds itself

After participating LEARNING OUTCOME MOVING TO A RESPONSIBILITY- CENTERED BUDGET MODEL

#AIwebcast MOVING TO A RESPONSIBILITY- CENTERED BUDGET MODEL PRINCIPLES OF RESPONSIBILITY-CENTER MANAGEMENT Larry Goldstein Campus Strategies, LLC Larry.Goldstein@Campus-Strategies.com 1 LEARNING OUTCOME

#AIwebcast MOVING TO A RESPONSIBILITY- CENTERED BUDGET MODEL PRINCIPLES OF RESPONSIBILITY-CENTER MANAGEMENT Larry Goldstein Campus Strategies, LLC Larry.Goldstein@Campus-Strategies.com 1 LEARNING OUTCOME

University Budget Advisory Committee Composition

University Budget Advisory Composition The University Budget (UBAC) is established by the President to provide input and recommendations to the President regarding the University s General Operating Fund

University Budget Advisory Composition The University Budget (UBAC) is established by the President to provide input and recommendations to the President regarding the University s General Operating Fund

North Orange County Community College District Integrated. Planning Manual March 2014 Update

2013 Integrated Planning Manual March 2014 Update 2013 Integrated Planning Manual NOCCCD Mission Statement The mission of the is to serve and enrich our diverse communities by providing a comprehensive

2013 Integrated Planning Manual March 2014 Update 2013 Integrated Planning Manual NOCCCD Mission Statement The mission of the is to serve and enrich our diverse communities by providing a comprehensive

Planning and Budgeting Integration (PBI) Model

Model") Peralta Community College District Planning and Budgeting Integration (PBI) Model OVERVIEW Introduction This document describes the central principles and features of Peralta s Planning and Budgeting Integration

Peralta Community College District Planning and Budgeting Integration (PBI) Model OVERVIEW Introduction This document describes the central principles and features of Peralta s Planning and Budgeting Integration

California Community Colleges/Districts Funding Model Proposal Submitted to Chancellor Oakley December 20, 2017

NOTE as of January 29, 2018: The CCC Funding Model Proposal recommendations by the Advisory Workgroup on Fiscal Affairs was provided to Chancellor Oakley prior to the release of the Governor s 2018-19

NOTE as of January 29, 2018: The CCC Funding Model Proposal recommendations by the Advisory Workgroup on Fiscal Affairs was provided to Chancellor Oakley prior to the release of the Governor s 2018-19

Budget Allocation Subcommittee: Report and Recommendations

RESOURCES PLANNING TASK FORCE Budget Allocation Subcommittee: Report and Recommendations I. Preamble The Committee was asked to determine how KPU should move forward in a budget environment that needs

RESOURCES PLANNING TASK FORCE Budget Allocation Subcommittee: Report and Recommendations I. Preamble The Committee was asked to determine how KPU should move forward in a budget environment that needs

Integrated Resource Planning Process University of Wisconsin-Parkside June 21, 2012

Integrated Resource Planning Process University of Wisconsin-Parkside June 21, 2012 Members: Terry Brown, Provost Kim Kelley, Assistant Vice Chancellor OIE Michele Gee, Faculty Budget Committee Facilitator:

Integrated Resource Planning Process University of Wisconsin-Parkside June 21, 2012 Members: Terry Brown, Provost Kim Kelley, Assistant Vice Chancellor OIE Michele Gee, Faculty Budget Committee Facilitator:

Sequoias Community College District RESOURCE

RESOURCE A L L O C AT I O N Sequoias Community College District College of the Sequoias 2013 Resource Allocation Manual College of the Sequoias Community College District Visalia Campus 915 S. Mooney Blvd.

RESOURCE A L L O C AT I O N Sequoias Community College District College of the Sequoias 2013 Resource Allocation Manual College of the Sequoias Community College District Visalia Campus 915 S. Mooney Blvd.

Planning Driven Budget Development Process

Planning Driven Budget Development Process BUDGET DEVELOPMENT COMMITTEE Adopted by the Budget Committee on May 19, 2016 MT. SAN JACINTO COLLEGE INTRODUCTION The Mt. San Jacinto College District resource

Planning Driven Budget Development Process BUDGET DEVELOPMENT COMMITTEE Adopted by the Budget Committee on May 19, 2016 MT. SAN JACINTO COLLEGE INTRODUCTION The Mt. San Jacinto College District resource

UNTHSC. Annual Budget Development Process Fiscal Year 2019 Guidelines & Instructions - Spring 2018

UNTHSC Annual Budget Development Process Fiscal Year 2019 Guidelines & Instructions - Spring 2018 INTRODUCTION: The budgeting process at the University of North Texas Health Science Center (UNTHSC) assigns

UNTHSC Annual Budget Development Process Fiscal Year 2019 Guidelines & Instructions - Spring 2018 INTRODUCTION: The budgeting process at the University of North Texas Health Science Center (UNTHSC) assigns

Resource Allocation Charter Document

Resource Allocation Charter Document v8 Updated: September 12, 2012 Team Name Resource Allocation Executive Sponsors Business Process Owner(s) Governance Objectives - Chancellor - Provost - Vice Chancellor

Resource Allocation Charter Document v8 Updated: September 12, 2012 Team Name Resource Allocation Executive Sponsors Business Process Owner(s) Governance Objectives - Chancellor - Provost - Vice Chancellor

Campuswide Benefit Decentralization Implementation Process

DRAFT--ISSUE REPORT January 18, 2012 Campuswide Benefit Decentralization 2012-13 Implementation Process TERMINOLOGY Unless otherwise stated, the term unit is intended to refer to the primary campus organizational

DRAFT--ISSUE REPORT January 18, 2012 Campuswide Benefit Decentralization 2012-13 Implementation Process TERMINOLOGY Unless otherwise stated, the term unit is intended to refer to the primary campus organizational

DRAFT August 2, Overview of OSU New Education and General (or Shared Responsibility) Budget Model Academic Colleges Focus

Budget Model Academic Colleges Focus") Overview of OSU New Education and General (or Shared Responsibility) Budget Model Academic Colleges Focus OSU-Corvallis is implementing a new budget model with the FY18 E&G budget. The model was used to

Overview of OSU New Education and General (or Shared Responsibility) Budget Model Academic Colleges Focus OSU-Corvallis is implementing a new budget model with the FY18 E&G budget. The model was used to

University of Houston Student Leadership Forum Budget and Legislative Processes

University of Houston Student Leadership Forum Budget and Legislative Processes June 13, 2012 Overview of the Planning and Budget Process 2 Multiple Cycles January 2012 February 2012 March 2012 April 2012

University of Houston Student Leadership Forum Budget and Legislative Processes June 13, 2012 Overview of the Planning and Budget Process 2 Multiple Cycles January 2012 February 2012 March 2012 April 2012

On behalf of the Resource Allocation Task Force (RATF), I am pleased to forward you our final report. Your charge to the RATF was:

, I am pleased to forward you our final report. Your charge to the RATF was:") To: Dr. Rodolfo Arévalo, President From: Rex Fuller, Dean and Task Force Chair Date: May 21, 2008 Re: Resource Allocation Task Force On behalf of the Resource Allocation Task Force (RATF), I am pleased

To: Dr. Rodolfo Arévalo, President From: Rex Fuller, Dean and Task Force Chair Date: May 21, 2008 Re: Resource Allocation Task Force On behalf of the Resource Allocation Task Force (RATF), I am pleased

Budget Reform Update. Paul Ellinger, Associate Chancellor & Vice Provost Budget and Resource Planning

Budget Reform Update Paul Ellinger, Associate Chancellor & Vice Provost Budget and Resource Planning February 2018 Outline Brief budget model overview Communication plan Principles Major components Timeline

Budget Reform Update Paul Ellinger, Associate Chancellor & Vice Provost Budget and Resource Planning February 2018 Outline Brief budget model overview Communication plan Principles Major components Timeline

PLAN FOR ASSESSMENT OF INSTITUTIONAL EFFECTIVENESS AND STUDENT LEARNING

Community College of Allegheny County PLAN FOR ASSESSMENT OF INSTITUTIONAL EFFECTIVENESS AND STUDENT LEARNING Prepared by: Office of Planning & Institutional Research Office of Learning Outcomes & Achieving

Community College of Allegheny County PLAN FOR ASSESSMENT OF INSTITUTIONAL EFFECTIVENESS AND STUDENT LEARNING Prepared by: Office of Planning & Institutional Research Office of Learning Outcomes & Achieving

Budget Model Redesign Initiative

Budget Model Redesign Initiative University Initiative Update October 17, 2016 Bannatyne Campus October 18, 2016 Fort Garry Campus Context and Initiative Background Increasing financial constraints Costs

Budget Model Redesign Initiative University Initiative Update October 17, 2016 Bannatyne Campus October 18, 2016 Fort Garry Campus Context and Initiative Background Increasing financial constraints Costs

Strategic Budgeting. Meredith Michaels October 26, 2006

Strategic Budgeting Meredith Michaels October 26, 2006 1 Principles Institutional perspective Invest strategically and differentially Be realistic about our goals Now At the margin The base is the base

Strategic Budgeting Meredith Michaels October 26, 2006 1 Principles Institutional perspective Invest strategically and differentially Be realistic about our goals Now At the margin The base is the base

Dean s RCM Workshops January 2015

Dean s RCM Workshops January 2015 Agenda General overview of RCM Overview of the model and college budget composition Education s view of RCM Engineering s view of RCM Group Activity: Scenarios 2 General

Dean s RCM Workshops January 2015 Agenda General overview of RCM Overview of the model and college budget composition Education s view of RCM Engineering s view of RCM Group Activity: Scenarios 2 General

I. INTRODUCTION II. ROLES & RESPONSIBILITIES

Page 1 I. INTRODUCTION The District implements a broad-based comprehensive and integrated planning system that is a foundation for strategic directions and resource allocation decisions. The Superintendent/President

Page 1 I. INTRODUCTION The District implements a broad-based comprehensive and integrated planning system that is a foundation for strategic directions and resource allocation decisions. The Superintendent/President

Presented to the Board of Trustees

Presented to the Board of Trustees 0 July 5, 2016 CSPP Budget Decision-Making Principles & Process The budget planning and development will be guided by the following Board of Trustees approved resource

Presented to the Board of Trustees 0 July 5, 2016 CSPP Budget Decision-Making Principles & Process The budget planning and development will be guided by the following Board of Trustees approved resource

San Francisco State University. We Make Great Things Happen. University Budget Committee July 2017

San Francisco State University We Make Great Things Happen University Budget Committee July 2017 Agenda 1. Call to Order 2. Welcome and Announcements (Ann Sherman) a. Approval of April 21 st, 2017 Meeting

San Francisco State University We Make Great Things Happen University Budget Committee July 2017 Agenda 1. Call to Order 2. Welcome and Announcements (Ann Sherman) a. Approval of April 21 st, 2017 Meeting

Los Angeles Community College District Budget Allocation Model

Los Angeles Community College District Budget Allocation Model 1 FUNDS ALLOCATION MECHANISM State Funds Revenue + Balances K-14 Share Community College Share Base Revenue COLA Growth Decline on Enrollment/Adjust.

Los Angeles Community College District Budget Allocation Model 1 FUNDS ALLOCATION MECHANISM State Funds Revenue + Balances K-14 Share Community College Share Base Revenue COLA Growth Decline on Enrollment/Adjust.

California State University Long Beach: Budget Outlook February, 2012

California State University Long Beach: Budget Outlook 2012-13 February, 2012 Gov s Proposed 2012-13 Budget 05 Jan 2012, Gov Brown proposed 2012-13 budget Addresses $9.2b budget deficit Depends on successful

California State University Long Beach: Budget Outlook 2012-13 February, 2012 Gov s Proposed 2012-13 Budget 05 Jan 2012, Gov Brown proposed 2012-13 budget Addresses $9.2b budget deficit Depends on successful

KAPI'OLANI CC OPERATIONAL POLICY

KAPI'OLANI CC OPERATIONAL POLICY KOP #1.111 Created March 14, 2014 Revised January 31, 2017 SUBJECT: Planning and Assessment Integration with Resource Allocation (PAIR) 1. Purpose: a. The primary purpose

KAPI'OLANI CC OPERATIONAL POLICY KOP #1.111 Created March 14, 2014 Revised January 31, 2017 SUBJECT: Planning and Assessment Integration with Resource Allocation (PAIR) 1. Purpose: a. The primary purpose

UTAH VALLEY UNIVERSITY. May 2, 2013 BUDGETING

UTAH VALLEY UNIVERSITY May 2, 2013 BUDGETING BUDGET PHILOSOPHY A budget is a map guiding an institution on its journey in pursuit of its mission. Source: College & University Budgeting, NACUBO Plan Drives

UTAH VALLEY UNIVERSITY May 2, 2013 BUDGETING BUDGET PHILOSOPHY A budget is a map guiding an institution on its journey in pursuit of its mission. Source: College & University Budgeting, NACUBO Plan Drives

q. PLANNING, RESOURCE, AND BUDGET COMMITTEE CURRENT

q. PLANNING, RESOURCE, AND BUDGET COMMITTEE CURRENT 1) Composition. Vice President for Academic Affairs, Vice President for Administration and Finance, Vice President for Human Resources, Equity and Inclusiveness,

q. PLANNING, RESOURCE, AND BUDGET COMMITTEE CURRENT 1) Composition. Vice President for Academic Affairs, Vice President for Administration and Finance, Vice President for Human Resources, Equity and Inclusiveness,

New Mexico Highlands University Annual Operating Budget Process. approved Fall 2016

New Mexico Highlands University Annual Operating Budget Process approved Fall 2016 Appendix I added Spring 2017 2 Table of Contents Introduction... 3 NMHU Budget Values and the NMHU Strategic Plan... 4

New Mexico Highlands University Annual Operating Budget Process approved Fall 2016 Appendix I added Spring 2017 2 Table of Contents Introduction... 3 NMHU Budget Values and the NMHU Strategic Plan... 4

University of California, Berkeley

University of California, Berkeley 2 nd Annual Finance Leadership Summit Pauley Ballroom November 29, 2012 Agenda 1 2 3 Campus Financial Vision for the Future UC Berkeley s Evolving Financial Philosophy

University of California, Berkeley 2 nd Annual Finance Leadership Summit Pauley Ballroom November 29, 2012 Agenda 1 2 3 Campus Financial Vision for the Future UC Berkeley s Evolving Financial Philosophy

Frequently Asked Questions (FAQs) about NKU s New Budget Model

about NKU s New Budget Model") Frequently Asked Questions (FAQs) about NKU s New Budget Model Philosophy and guiding principles Why did NKU need a new budget model? Internal and external factors pointed to the need for a more flexible,

Frequently Asked Questions (FAQs) about NKU s New Budget Model Philosophy and guiding principles Why did NKU need a new budget model? Internal and external factors pointed to the need for a more flexible,

Oral and written testimony of M. Angelo before the BOR on 2/11/16 regarding the UHM budget model

2/11/2016 University of Hawaii Mail Oral and written testimony of M. Angelo before the BOR on 2/11/16 regarding the UHM budget model Board of Regents Oral and written testimony of M. Angelo

2/11/2016 University of Hawaii Mail Oral and written testimony of M. Angelo before the BOR on 2/11/16 regarding the UHM budget model Board of Regents Oral and written testimony of M. Angelo

Accreditation Action Plan for Removal of Probation presented to the LACCD Board of Trustees. Aug. 22, 2012 Los Angeles Harbor College

Accreditation Action for Removal of Probation presented to the LACCD Board of Trustees Aug. 22, 2012 Los Angeles Harbor College Rolled up our sleeves and got to work Focused on our students success Affirmed

Accreditation Action for Removal of Probation presented to the LACCD Board of Trustees Aug. 22, 2012 Los Angeles Harbor College Rolled up our sleeves and got to work Focused on our students success Affirmed

Competency Profile: A breakdown of the general areas of competencies into specific competency statements.

POLICY CATEGORY Academic POLICY NUMBER D35 POLICY NAME Program Curriculum Committee CROSS REFERENCE D20 - Graduation D21 Course Development and Revision D22 Program Review D27 Granting of Credit D34 New

POLICY CATEGORY Academic POLICY NUMBER D35 POLICY NAME Program Curriculum Committee CROSS REFERENCE D20 - Graduation D21 Course Development and Revision D22 Program Review D27 Granting of Credit D34 New

BP 2220 Committees of the Board

Coast Community College District BOARD POLICY Chapter 2 Board of Trustees BP 2220 Committees of the Board Reference: Government Code Section 54952 The Board may by action establish committees that it determines

Coast Community College District BOARD POLICY Chapter 2 Board of Trustees BP 2220 Committees of the Board Reference: Government Code Section 54952 The Board may by action establish committees that it determines

New Budget Process Overview

New Budget Process Overview 1 Millions $0 $20 $40 $60 $80 $100 $120 State Budget Reductions : FY 08/09 to 16/17 08/09 09/10 10/11 11/12 12/13 13/14 14/15 15/16 16/17 $16.6 $16.6 $20.7 $37.3 $24.8 $62.2

New Budget Process Overview 1 Millions $0 $20 $40 $60 $80 $100 $120 State Budget Reductions : FY 08/09 to 16/17 08/09 09/10 10/11 11/12 12/13 13/14 14/15 15/16 16/17 $16.6 $16.6 $20.7 $37.3 $24.8 $62.2

UW-STOUT Annual Operating Budget Process

UW-STOUT Annual Operating Budget Process An institution s budget process is shaped by institutional character; institutional size; administrative sophistication; faculty governance structures and processes;

UW-STOUT Annual Operating Budget Process An institution s budget process is shaped by institutional character; institutional size; administrative sophistication; faculty governance structures and processes;

DEANS, VICE CHANCELLORS, UNIVERSITY LIBRARIAN, ATHLETIC DIRECTOR AND CHIEF INFORMATION OFFICER

DEANS, VICE CHANCELLORS, UNIVERSITY LIBRARIAN, ATHLETIC DIRECTOR AND CHIEF INFORMATION OFFICER Re: Dear Colleagues, The budget planning process for 2019-20 marks a point of inflection for our financial

DEANS, VICE CHANCELLORS, UNIVERSITY LIBRARIAN, ATHLETIC DIRECTOR AND CHIEF INFORMATION OFFICER Re: Dear Colleagues, The budget planning process for 2019-20 marks a point of inflection for our financial

California State University. Fullerton. Budget Report Fiscal Year

California State University Fullerton Budget Report Fiscal Year 2016-17 Table of Contents I. Foreword II. University Resources a. Fiscal Year Budget 1 b. Highlights: 2016-17 Operating Budget 2 c. Operating

California State University Fullerton Budget Report Fiscal Year 2016-17 Table of Contents I. Foreword II. University Resources a. Fiscal Year Budget 1 b. Highlights: 2016-17 Operating Budget 2 c. Operating

Sacramento City College Strategic Planning System

Sacramento City College Strategic Planning System Title: Plan Type: OPR: Collaborative Groups: Resource Management and Capital Outlay Master Plan 2018 Institutional VPA Resource Allocation Groups: Budget

Sacramento City College Strategic Planning System Title: Plan Type: OPR: Collaborative Groups: Resource Management and Capital Outlay Master Plan 2018 Institutional VPA Resource Allocation Groups: Budget

Hers Institute Budgeting. This Session Will Include a Discussion of:

Hers Institute 2016 Budgeting This Session Will Include a Discussion of: The Purpose of the Budgeting Process Budget Types Approaches to Budgeting The Budget Process Why do we participate in the budget

Hers Institute 2016 Budgeting This Session Will Include a Discussion of: The Purpose of the Budgeting Process Budget Types Approaches to Budgeting The Budget Process Why do we participate in the budget

Breakfast for Progress. Ensuring a Sustainable Financial Future at Ohio University

1 Breakfast for Progress Ensuring a Sustainable Financial Future at Ohio University 1-31-18 2 Decision-making Structure What is the role of shared governance in OHIO s budget process? Board of Trustees

1 Breakfast for Progress Ensuring a Sustainable Financial Future at Ohio University 1-31-18 2 Decision-making Structure What is the role of shared governance in OHIO s budget process? Board of Trustees

BUDGET REPORT GUIDANCE FOR FY19: ACTIVITY-BASED UNITS

Office of the Provost University of Illinois at Urbana-Champaign BUDGET REPORT GUIDANCE FOR FY19: ACTIVITY-BASED UNITS 3 November 2017 The State of Illinois recent budget impasse ended in July 2017. Allocations

Office of the Provost University of Illinois at Urbana-Champaign BUDGET REPORT GUIDANCE FOR FY19: ACTIVITY-BASED UNITS 3 November 2017 The State of Illinois recent budget impasse ended in July 2017. Allocations

The School District of Clayton s Budget Planning Guide. Zero-Based Budgeting An Overview. Helpful Definitions

The s Zero-Based Budgeting An Overview Transition to Zero-Based Budgeting (ZBB) is a major outcome within the Resource Management theme of the District s strategic plan. It is not a budget reduction process.

The s Zero-Based Budgeting An Overview Transition to Zero-Based Budgeting (ZBB) is a major outcome within the Resource Management theme of the District s strategic plan. It is not a budget reduction process.

Peralta Planning and Budgeting Integration (PBI) Model. OVERVIEW (August 6, 2009)

Model. OVERVIEW (August 6, 2009)") Peralta Planning and Budgeting Integration (PBI) Model OVERVIEW (August 6, 2009) On August 3, 2009, Chancellor Harris issued Administrative Procedure 2.20 to implement the Planning and Budgeting Integration

Peralta Planning and Budgeting Integration (PBI) Model OVERVIEW (August 6, 2009) On August 3, 2009, Chancellor Harris issued Administrative Procedure 2.20 to implement the Planning and Budgeting Integration

Financial Management Guidelines and Procedures

The financial position and future of the Colorado School of Mines is dependent on several variables including enrollment, research growth, changes in industry demand, and competing institutions at the

The financial position and future of the Colorado School of Mines is dependent on several variables including enrollment, research growth, changes in industry demand, and competing institutions at the

POLICY RECOMMENDATION THE PLANNING AND BUDGET PROCESS AT SJSU

A campus of The California State University Office of the Academic Senate One Washington Square San Jose, California 95192-0024 408-924-2440 Fax: 408-924-2451 S05-10 At its meeting of May 9, 2005, the

A campus of The California State University Office of the Academic Senate One Washington Square San Jose, California 95192-0024 408-924-2440 Fax: 408-924-2451 S05-10 At its meeting of May 9, 2005, the

University Cabinet Outline of Budget Reduction Decisions February 22, 2018

Priorities in Budget Planning Student success Equity and diversity Fiscal stability and good stewardship of resources Shared responsibility and accountability Values (These are summarized from the Values

Priorities in Budget Planning Student success Equity and diversity Fiscal stability and good stewardship of resources Shared responsibility and accountability Values (These are summarized from the Values

STATE CENTER COMMUNITY COLLEGE DISTRICT

STATE CENTER COMMUNITY COLLEGE DISTRICT Districtwide Resource Allocation Model General Fund Unrestricted Budget Fresno Reedley Madera Oakhurst Willow International Table of Contents Background... 3 Elements

STATE CENTER COMMUNITY COLLEGE DISTRICT Districtwide Resource Allocation Model General Fund Unrestricted Budget Fresno Reedley Madera Oakhurst Willow International Table of Contents Background... 3 Elements

Sacramento City College

Sacramento City College Strategic Planning System Title: Plan Type: OPR: Collaborative Group: References: Facility Management Resource Allocation Operations Division Campus Development Committee ADA Transition

Sacramento City College Strategic Planning System Title: Plan Type: OPR: Collaborative Group: References: Facility Management Resource Allocation Operations Division Campus Development Committee ADA Transition

SANTA BARBARA CITY COLLEGE ASSUMPTIONS USED TO DEVELOP THE ADOPTED BUDGET Board of Trustees Study Session June 14, 2012

SANTA BARBARA CITY COLLEGE ASSUMPTIONS USED TO DEVELOP THE 2012-13 ADOPTED BUDGET Board of Trustees Study Session June 14, 2012 The budget revenue assumptions are from the Annual Statewide Budget Workshop

SANTA BARBARA CITY COLLEGE ASSUMPTIONS USED TO DEVELOP THE 2012-13 ADOPTED BUDGET Board of Trustees Study Session June 14, 2012 The budget revenue assumptions are from the Annual Statewide Budget Workshop

Finance Reform. Speaker Series March

Finance Reform A new metrics-informed financial model designed to improve transparency, align incentives with campus goals, and simplify our planning and management environment http://budget.berkeley.edu/financereform

Finance Reform A new metrics-informed financial model designed to improve transparency, align incentives with campus goals, and simplify our planning and management environment http://budget.berkeley.edu/financereform

RESOURCE. Sequoias Community College District. College of the Sequoias

RESOURCE A L L O C AT I O N Sequoias Community College District College of the Sequoias College of the Sequoias 2014 Resource Allocation Manual College of the Sequoias Community College District Visalia

RESOURCE A L L O C AT I O N Sequoias Community College District College of the Sequoias College of the Sequoias 2014 Resource Allocation Manual College of the Sequoias Community College District Visalia

LEHIGH University. Financial Planning Report With Budget

LEHIGH University Financial Planning Report With 2012-2013 Budget L E H I G H U N I V E R S I T Y 2 0 1 2-1 3 B U D G E T ------------------------- T A B L E O F C O N T E N T S PAGE I. COMMENTARY 1-9

LEHIGH University Financial Planning Report With 2012-2013 Budget L E H I G H U N I V E R S I T Y 2 0 1 2-1 3 B U D G E T ------------------------- T A B L E O F C O N T E N T S PAGE I. COMMENTARY 1-9

Adopting a Different Approach to University Budgeting February 10, 2016

Adopting a Different Approach to University Budgeting February 10, 2016 1. Purpose. This document captures the analytical process and decision to change the Northwestern State University budgeting model

Adopting a Different Approach to University Budgeting February 10, 2016 1. Purpose. This document captures the analytical process and decision to change the Northwestern State University budgeting model

Budgets in the CSU. CSU 101 Budget February 2012 Pismo Beach. Debbie Brothwell Deputy Vice President, Finance CSU East Bay

Budgets in the CSU CSU 101 Budget February 2012 Pismo Beach Debbie Brothwell Deputy Vice President, Finance CSU East Bay Overview How is the CSU Funded? Overview of the CSU Budget Process State of California

Budgets in the CSU CSU 101 Budget February 2012 Pismo Beach Debbie Brothwell Deputy Vice President, Finance CSU East Bay Overview How is the CSU Funded? Overview of the CSU Budget Process State of California

FAQs Finance and Budget Modeling Initiative

FAQs Finance and Budget Modeling Initiative Why do we need to create a new budget model? o To improve transparency, to ensure that data drives decision making, and to make strategic decisions based on

FAQs Finance and Budget Modeling Initiative Why do we need to create a new budget model? o To improve transparency, to ensure that data drives decision making, and to make strategic decisions based on

BUDGET MESSAGE FISCAL YEAR Presented May 13, 2015

BUDGET MESSAGE FISCAL YEAR 2015-16 Presented May 13, 2015 The fiscal year 2015-16 budget reflects a year-long process of analysis, review, and application of our budget development principles, criteria

BUDGET MESSAGE FISCAL YEAR 2015-16 Presented May 13, 2015 The fiscal year 2015-16 budget reflects a year-long process of analysis, review, and application of our budget development principles, criteria

Office of the Academic Senate One Washington Square San Jose, California Fax:

A campus of The California State University Office of the Academic Senate One Washington Square San Jose, California 95192-0024 408-924-2440 Fax: 408-924-2451 At its meeting of February 25, 2002, the Academic

A campus of The California State University Office of the Academic Senate One Washington Square San Jose, California 95192-0024 408-924-2440 Fax: 408-924-2451 At its meeting of February 25, 2002, the Academic

2019 Budget and Grid Management Charge Initial Stakeholder Meeting

2019 Budget and Grid Management Charge Initial Stakeholder Meeting July 24, 2018 Agenda Topic: Welcome and Introductions Presenter: Kristina Osborne 2019 Budget Process & GMC Rate Outlook April Gordon

2019 Budget and Grid Management Charge Initial Stakeholder Meeting July 24, 2018 Agenda Topic: Welcome and Introductions Presenter: Kristina Osborne 2019 Budget Process & GMC Rate Outlook April Gordon

In fiscal year (FY) , the general fund base budgets by department were as follows:

, the general fund base budgets by department were as follows:") 1.6 Fiscal Resources. The school shall have financial resources adequate to fulfill its stated mission and goals, and its instructional, research and service objectives. a. Description of the budgetary

1.6 Fiscal Resources. The school shall have financial resources adequate to fulfill its stated mission and goals, and its instructional, research and service objectives. a. Description of the budgetary

Campus Budget Open Forum. October 5, 2017

Campus Budget Open Forum October 5, 2017 2 Agenda WSCUC Accreditation Area of Inquiry URPC membership and role Budget update Public facing budget dashboards Achieved budget savings (Spring 2017 - Phase

Campus Budget Open Forum October 5, 2017 2 Agenda WSCUC Accreditation Area of Inquiry URPC membership and role Budget update Public facing budget dashboards Achieved budget savings (Spring 2017 - Phase

ASL Budget Forum. May 8, 2017

ASL Budget Forum May 8, 2017 Today s Agenda Final model (changes) Governance Philosophy Current Governance Structure New Governance Structure Model Changes Changes since Winter Forums Revenue estimates

ASL Budget Forum May 8, 2017 Today s Agenda Final model (changes) Governance Philosophy Current Governance Structure New Governance Structure Model Changes Changes since Winter Forums Revenue estimates

USF SYSTEM ANNUAL STRATEGIC BUDGET PLANNING PROCESS OVERVIEW

USF SYSTEM ANNUAL STRATEGIC BUDGET PLANNING PROCESS OVERVIEW Ralph C. Wilcox, Ph.D. Provost & Senior Vice President for Academic Affairs January 21, 2009 Purpose Prepare balanced budget and legislative

USF SYSTEM ANNUAL STRATEGIC BUDGET PLANNING PROCESS OVERVIEW Ralph C. Wilcox, Ph.D. Provost & Senior Vice President for Academic Affairs January 21, 2009 Purpose Prepare balanced budget and legislative

INSTITUTIONAL EFFECTIVENESS Procedures Manual. Developed by the Office of Institutional Effectiveness

INSTITUTIONAL EFFECTIVENESS Procedures Manual Developed by the Office of Institutional Effectiveness 2014-2018 INSTITUTIONAL EFFECTIVENESS PROCEDURES MANUAL Purpose < To support a comprehensive institutional

INSTITUTIONAL EFFECTIVENESS Procedures Manual Developed by the Office of Institutional Effectiveness 2014-2018 INSTITUTIONAL EFFECTIVENESS PROCEDURES MANUAL Purpose < To support a comprehensive institutional

Campus Budget Reform September 2018 O F F I C E O F T H E P R O V O S T

Campus Budget Reform September 2018 O F F I C E O F T H E P R O V O S T Outline Fall: Update on Campus Budget Reform Campus budget overview Budget reform Spring: Planning your Department s Budget Budget

Campus Budget Reform September 2018 O F F I C E O F T H E P R O V O S T Outline Fall: Update on Campus Budget Reform Campus budget overview Budget reform Spring: Planning your Department s Budget Budget

San Francisco State University. We Make Great Things Happen. University Budget Committee September 12, 2017

San Francisco State University We Make Great Things Happen University Budget Committee September 12, 2017 Welcome to the new Academic 2017-2018 Year! Today s Agenda Welcome and Announcements (President

San Francisco State University We Make Great Things Happen University Budget Committee September 12, 2017 Welcome to the new Academic 2017-2018 Year! Today s Agenda Welcome and Announcements (President

USF System Annual Strategic Budget Planning Process

USF System Annual Strategic Budget Planning Process University budget strategy, planning and development should be led by the Provost to assure that the budget reflects USF s strategic priorities The President

USF System Annual Strategic Budget Planning Process University budget strategy, planning and development should be led by the Provost to assure that the budget reflects USF s strategic priorities The President

Mequon-Thiensville School District Releases Administrative Action Plan

Please direct inquiries to: Dr. Demond Means, Superintendent (262) 238-8502 dmeans@mtsd.k12.wi.us FOR IMMEDIATE RELEASE: October 29, 2012 Mequon-Thiensville School District Releases Administrative MEQUON,

Please direct inquiries to: Dr. Demond Means, Superintendent (262) 238-8502 dmeans@mtsd.k12.wi.us FOR IMMEDIATE RELEASE: October 29, 2012 Mequon-Thiensville School District Releases Administrative MEQUON,

RESPONSIBILITY CENTRED MANAGEMENT

Page 1 of 7 RESPONSIBILITY CENTRED MANAGEMENT In 2014/15, Trent University will introduce a new approach to budget planning called Responsibility Centred Management (RCM). It aims to improve financial

Page 1 of 7 RESPONSIBILITY CENTRED MANAGEMENT In 2014/15, Trent University will introduce a new approach to budget planning called Responsibility Centred Management (RCM). It aims to improve financial

New Jersey Institute of Technology

New Jersey Institute of Technology University Senate Committee on Finances November 1, 2017 FY2018 Approved Operating Budget Executive Summary The approved FY2018 Operating Budget: Totals $518.8M, a 6.8%

New Jersey Institute of Technology University Senate Committee on Finances November 1, 2017 FY2018 Approved Operating Budget Executive Summary The approved FY2018 Operating Budget: Totals $518.8M, a 6.8%

BUDGET ALLOCATION PROCESS University Administrators Forum February 6, 2013

DIVISION OF BUSINESS AND FINANCE BUDGET ALLOCATION PROCESS University Administrators Forum February 6, 2013 North Carolina Agricultural and Technical State University Presentation Outline Budget Overview

DIVISION OF BUSINESS AND FINANCE BUDGET ALLOCATION PROCESS University Administrators Forum February 6, 2013 North Carolina Agricultural and Technical State University Presentation Outline Budget Overview

CATEGORY 8 PLANNING CONTINUOUS IMPROVEMENT

INTRODUCTION The College s processes related to Planning Continuous Improvement are very mature. JC s key planning processes are aligned. Clear processes are in place for strategic planning and the College

INTRODUCTION The College s processes related to Planning Continuous Improvement are very mature. JC s key planning processes are aligned. Clear processes are in place for strategic planning and the College

INTEGRATING ASSESSMENT, PLANNING & BUDGETING. Presentation to URPC August 26, 2016 Lisa Castellino, PhD Office of Institutional Effectiveness

INTEGRATING ASSESSMENT, PLANNING & BUDGETING Presentation to URPC August 26, 2016 Lisa Castellino, PhD Office of Institutional Effectiveness 1 Campus Context Why integrate these activities? ON TOP Strategic

INTEGRATING ASSESSMENT, PLANNING & BUDGETING Presentation to URPC August 26, 2016 Lisa Castellino, PhD Office of Institutional Effectiveness 1 Campus Context Why integrate these activities? ON TOP Strategic

Food Services Advisory Committee. UH Planning and Budgeting

Food Services Advisory Committee UH Planning and Budgeting November 12, 2010 Food Services Advisory Committee UH Planning and Budgeting Budgeting Process 2 Overview of the Planning and Budget Process Internal

Food Services Advisory Committee UH Planning and Budgeting November 12, 2010 Food Services Advisory Committee UH Planning and Budgeting Budgeting Process 2 Overview of the Planning and Budget Process Internal

Planning and Budgeting Forum Mission Achievement Planning

Planning and Budgeting Forum Mission Achievement Planning September 22, 2014 Denver, Colorado Gordon Jensen Introduction Metropolitan Community College (MCC): One of six community colleges in Nebraska

Planning and Budgeting Forum Mission Achievement Planning September 22, 2014 Denver, Colorado Gordon Jensen Introduction Metropolitan Community College (MCC): One of six community colleges in Nebraska

2014 Planning & Budgeting Forum

2014 Planning & Budgeting Forum The Accounting of RCM September 23, 2014 Denver, CO Conference Session Speakers Name Title Contact Details Andrew L. Laws Managing Director (session facilitator) Huron Consulting

2014 Planning & Budgeting Forum The Accounting of RCM September 23, 2014 Denver, CO Conference Session Speakers Name Title Contact Details Andrew L. Laws Managing Director (session facilitator) Huron Consulting

GFOA AWARD FOR BEST PRACTICES IN SCHOOL BUDGETING. Applicant and Judge's Guide

GFOA AWARD FOR BEST PRACTICES IN SCHOOL BUDGETING Applicant and Judge's Guide GFOA Award for Best Practices in School Budgeting Applicant and Judges Guide Introduction... 2 Definitions... 2 About the Award...

GFOA AWARD FOR BEST PRACTICES IN SCHOOL BUDGETING Applicant and Judge's Guide GFOA Award for Best Practices in School Budgeting Applicant and Judges Guide Introduction... 2 Definitions... 2 About the Award...

UWM Budget Model Development: Proposal for a New Incentive Based Resource Allocation Model Prepared by the Budget Model Working Group

UWM Budget Model Development: Proposal for a New Incentive Based Resource Allocation Model Prepared by the Budget Model Working Group Chancellor Mone, Provost Britz and Vice Chancellor Van Harpen, This

UWM Budget Model Development: Proposal for a New Incentive Based Resource Allocation Model Prepared by the Budget Model Working Group Chancellor Mone, Provost Britz and Vice Chancellor Van Harpen, This

Multi-year Budget Planning Strategies and Implementation Under the Budget Reform Initiative

Multi-year Budget Planning Strategies and Implementation Under the Budget Reform Initiative OFFICE OF THE PROVOST Outline Motivation for multi-year planning Operational Excellence @ Illinois Budget reform

Multi-year Budget Planning Strategies and Implementation Under the Budget Reform Initiative OFFICE OF THE PROVOST Outline Motivation for multi-year planning Operational Excellence @ Illinois Budget reform

BUDGET REVIEW WORK GROUP FINAL REPORT

BUDGET REVIEW WORK GROUP FINAL REPORT April 26, 2012 TABLE OF CONTENTS I. Executive Summary... 2 II. Introduction and Report Organization..... 4 III. Campus Budget Planning Process... 5 IV. Core Funds

BUDGET REVIEW WORK GROUP FINAL REPORT April 26, 2012 TABLE OF CONTENTS I. Executive Summary... 2 II. Introduction and Report Organization..... 4 III. Campus Budget Planning Process... 5 IV. Core Funds