Fair Lending In The Mortgage Industry How You will do Business in 2014?

|

|

|

- Augusta Watson

- 5 years ago

- Views:

Transcription

1 Fair Lending In The Mortgage Industry How You will do Business in 2014? Presenter: Tammy Butler, Master CMB and Director of Fair lending and Compliance, Optimal Blue

2

3 Time to Prepare for January Was the year of change Will be the year of implementation and reconfiguration of what we once thought was our business model.

4 CFPB

5 CFPB Mission The CFPB is consumer based. They care little about: How your recruiting is affected. How your originator s income is affected. Or, your profit margins. What they do care about is the consumer and the consumer experience. Anything that harms the consumer (in their opinion) will harm you. Think of them as the consumer s Momma! You do not mess with Momma s children!

6 Regulators Are Combining Their Efforts! 6

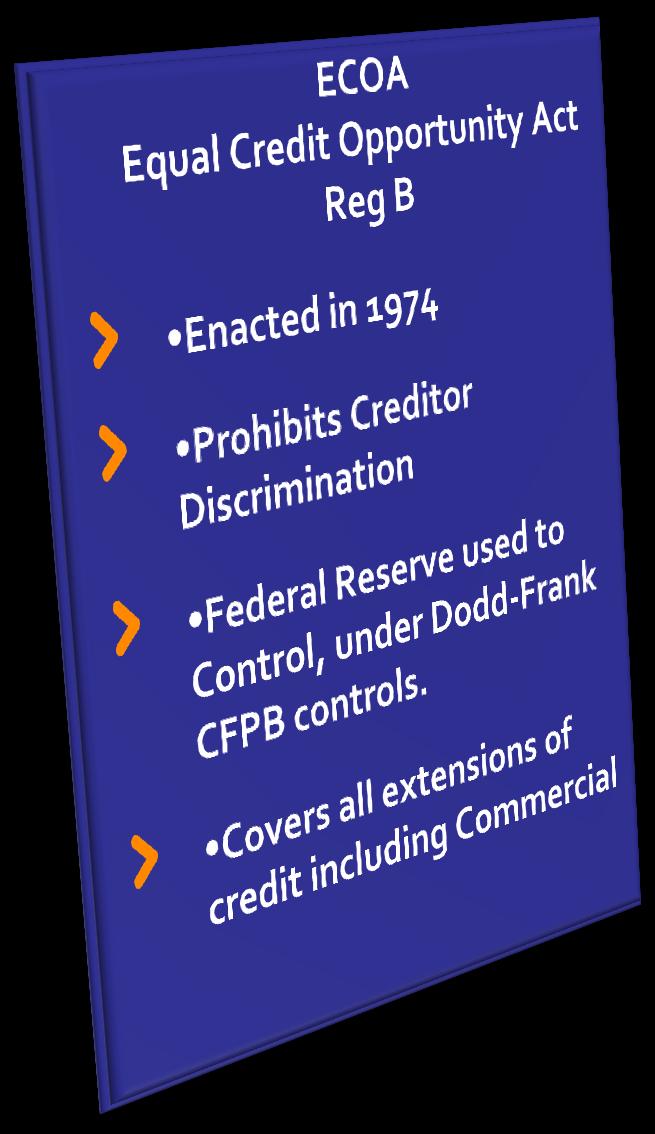

7 The Laws Prohibited Basis ECOA (Equal Credit Opportunity Act) Regulation B Fair Housing Act Race Color Religion National Origin Sex Gender Identity Handicap Familial Status Marital Status Age Receipt of Public Assistance Exercise of Rights Under The Consumer Credit Protection Act Under Authority Of CFPB HUD Purpose All Credit Types Housing & Residential Finance 7

8 Mortgage lenders are severely under-equipped to handle these changes An ideology shift A Business Model Shift Slimmer Profit Margins which will equate to Higher Efficiency if you are to survive and thrive. Monitoring & Controls

9 To Do This: You will need to add professional compliance managers, counsel and auditing (in house or outsourced) Put systems in place to monitor everything you do and provide statistical results. Train your staff more than ever before. Self-Audit Truly make the Customer King and Prove that you have. (complaint analysis, remediation) Develop new recruiting techniques and new ways to pay people. Employ Fair Lending Techniques that you never considered before. (MSA Diversity) Monitor Pricing Exceptions Improve Data Flow and Integrity Create policies, procedures and workflow diagrams that describe and monitor your work from start to finish (no more boiler plates)

10

11 Where Does Fair Lending Start? First Contact With Prospective Client! Marketing Outreach Your Material -Audience Appropriate? Represented Neutrally? Unintentionally or Intentionally Excluding on Prohibited Basis? Phone Call Not Returning Phone Calls Screening Calls Based on Voice Mail Not Returning Visit Stereotyping or Generalizing Not Offering All Program Options 11

12 Case U.S. v. Countrywide Financial Corporation (2012) U.S. v. Wells Fargo Bank, N.A. (2012) WHY? $335 million U.S. v. SunTrust Mortgage, Inc. (2012) U.S. v. GFI Mortgage Bankers Inc. (2012) U.S. v. PrimeLending (2011) FTC v. Gateway Funding (2009) FTC v. Golden Empire Mortgage (2010) U.S. v. Texas Champion Bank (2013) $700,000 U.S. v. C&F Mortgage Corp. (2011) $140,000 U.S. v. Nixon State Bank (2011) $100,000 Settlement Amount $175 million for wholesale, plus potential liability for retail $21 million $3.555 million $2 million $2 million (deferred) $1.5 million 12

Limits on activities or functions, including suspension & termination Civil money penalties Up to $5,000/day (any")

13 If the CFPB Finds Problems, Very Broad Remedies: Rescission or reformation of contracts Refund of moneys Return of real property Restitution Disgorgement of profits Compensation for unjust enrichment Damages Public notification of violations (with costs to be borne by the violator) Limits on activities or functions, including suspension & termination Civil money penalties Up to $5,000/day (any violation) Up to $25,000/day (reckless) Up to $1 million/day (knowing) 13

14 Where HMDA & Fair Lending Software Fail HMDA Data and Fair Lending Software Misses: Pricing/Rate Trace (Memorialize each step for each loan) Pricing/Rate Start to LO Pricing Adjustments (Each loan level price adjustment defined) Pricing/Rate Final Results to consumer Re-Lock Audit Trail and Notation Trace as to Reason for Re-lock. Credits (Memorialize fees and credits and show the net affect) Seller Credits Lender Fees Grant/Subsidy credits Pricing Concession/Exception (Resolve with notation as to why) APR More definition on Property type (i.e. Condo, Coop, etc.) Income Type (Certain types of income require specialty investors or guidelines) 14

15 Developing Policy Is policy well thought-out and workflow diagrammed? Is policy applied consistently? How do you monitor policy? What happens when an employee doesn t follow company policy? No program should roll without compliance overview as well. Look at the CFPB exam manual! Follow it to the T. 3 Rules for Every Process! Policy & Procedure Policy Training needs to be thorough and very tight Monitoring with red flags for deviation! 15

16 Fair Lending Trigger Points! 1. Pricing Disparity: Similar borrowers receive different rates/closing costs. 2. Pricing Exceptions: Given to some but not others. 3. Underwriting Disparity: Conditions or denials not consistent. 4. Underwriting Exceptions: Given to some but not others similarly situated. 5. Marketing Disparity & UDAAP Violations 6. Redlining 7. Steering 8. Disparate Impact 9. Data Integrity 10. Client Interaction & Client Parity 16

17

18 Is This Your Current Marketing/SM Compliance Plan? The Problem With That Plan is That CFPB Sees It All BEFORE They Even Contact You! 18

19 Marketing & UDAAP-The Unknown! Websites Facebook, Twitter, LinkedIn, et al Print Advertising and Marketing Lead Acquisition What is Your Compliance Management System? What is Your Policy? How is it Monitored? FTC Guidelines: 19

20 Pump The Brakes! Old Way Production Staff Compliance New Way Compliance Staff Production Embrace Change! 20

21 Policy & Best Practices Prevent This! Proper Prior Planning Prevents Poor Performance! 21

22 Free Resource Center

23 Thank You! Tammy Butler, Master CMB Director of Fair Lending & Compliance Join in the Discussion on Linked Group Optimal Blue Fair Lending & Compliance or

Fair Lending Risk Management

Presented by: Martin (Marty) Mitchell, CRCM Managing Director, ProBank Austin Robert J. (Bob) Mullenbach, CRCM Managing Director, Compliance Division Deputy, ProBank Austin Fair Lending Laws ECOA Prohibits

Presented by: Martin (Marty) Mitchell, CRCM Managing Director, ProBank Austin Robert J. (Bob) Mullenbach, CRCM Managing Director, Compliance Division Deputy, ProBank Austin Fair Lending Laws ECOA Prohibits

National Association of Federal Credit Unions. Fair Lending Training (Part I) March 19, Lori J. Sommerfield Counsel BuckleySandler LLP

March 19, Lori J. Sommerfield Counsel BuckleySandler LLP") National Association of Federal Credit Unions Fair Lending Training (Part I) March 19, 2014 Lori J. Sommerfield Counsel BuckleySandler LLP Order of Presentation Overview of Fair Lending Laws & Regulations

National Association of Federal Credit Unions Fair Lending Training (Part I) March 19, 2014 Lori J. Sommerfield Counsel BuckleySandler LLP Order of Presentation Overview of Fair Lending Laws & Regulations

Fair Lending Hot Topics

Fair Lending Hot Topics Outlook Live Webinar October 17, 2012 Non-Discrimination Working Group of the Financial Fraud Enforcement Task Force Visit us at www.consumercomplianceoutlook.org informational

Fair Lending Hot Topics Outlook Live Webinar October 17, 2012 Non-Discrimination Working Group of the Financial Fraud Enforcement Task Force Visit us at www.consumercomplianceoutlook.org informational

To learn about navigation and other features of this e-learning course, click Help. Click Next to continue to the next page.

Welcome to Fair Lending Practices Extending credit is a cornerstone of banking. Because of the need society has for lending and credit, Congress has passed a number of acts ensuring that banks distribute

Welcome to Fair Lending Practices Extending credit is a cornerstone of banking. Because of the need society has for lending and credit, Congress has passed a number of acts ensuring that banks distribute

MBBA-NH & MAMP. Compliance Conference. April 19, 2017

MBBA-NH & MAMP Compliance Conference April 19, 2017 Agenda HMDA Overview Readiness Steps HMDA Expansion Fields 2 New HMDA Rule Summary Changes to Home Mortgage Disclosure: Regulation C Types of institutions

MBBA-NH & MAMP Compliance Conference April 19, 2017 Agenda HMDA Overview Readiness Steps HMDA Expansion Fields 2 New HMDA Rule Summary Changes to Home Mortgage Disclosure: Regulation C Types of institutions

July 31, :30PM to 2:30PM CDT. Fair Lending: Can You Make Exceptions?

July 31, 2018 1:30PM to 2:30PM CDT Fair Lending: Can You Make Exceptions? Options to Join Webinar and audio Click on the link: Fair Lending Webcast Connect to audio Call Using Computer (preferred method):

July 31, 2018 1:30PM to 2:30PM CDT Fair Lending: Can You Make Exceptions? Options to Join Webinar and audio Click on the link: Fair Lending Webcast Connect to audio Call Using Computer (preferred method):

Fair Lending Risk Management: Lessons from Recent Settlements

November 2012 Fair Lending Risk Management: Lessons from Recent Settlements Introduction Fair lending continues to be a major enforcement priority of federal agencies, and the financial implications have

November 2012 Fair Lending Risk Management: Lessons from Recent Settlements Introduction Fair lending continues to be a major enforcement priority of federal agencies, and the financial implications have

Fair Lending Internal Audits

Fair Lending Internal Audits ACUIA Region 6 Conference Presented By: Kristie Kenney Hoover, NCCO Internal Audit Manager, Doeren Mayhew Florida Michigan North Carolina Texas Insight. Oversight. Foresight.

Fair Lending Internal Audits ACUIA Region 6 Conference Presented By: Kristie Kenney Hoover, NCCO Internal Audit Manager, Doeren Mayhew Florida Michigan North Carolina Texas Insight. Oversight. Foresight.

Fair Lending Examination Procedures Summary and Risk Factors Table

Federal Reserve Bank of Dallas Fair Lending Examination Procedures Summary and Risk Factors Table This publication is intended as a summary of the Fair Lending Examination Procedures. Also included is

Federal Reserve Bank of Dallas Fair Lending Examination Procedures Summary and Risk Factors Table This publication is intended as a summary of the Fair Lending Examination Procedures. Also included is

Loan Growth and Compliance Pitfalls

Loan Growth and Compliance Pitfalls presented by LOANLINER Compliance Information provided in this presentation, including all materials, should not be construed as legal services, legal advice, or in

Loan Growth and Compliance Pitfalls presented by LOANLINER Compliance Information provided in this presentation, including all materials, should not be construed as legal services, legal advice, or in

FAIR LENDING PLAN. NMLS #1820 Fair Lending Plan Policy. (Fair Housing Act/Equal Credit Opportunity Act/Home Mortgage Disclosure Act) March 2013

March 2013") FAIR LENDING PLAN (Fair Housing Act/Equal Credit Opportunity Act/Home Mortgage Disclosure Act) March 2013 CMG Mortgage, Inc. is committed to making high quality mortgage services available to diverse communities

FAIR LENDING PLAN (Fair Housing Act/Equal Credit Opportunity Act/Home Mortgage Disclosure Act) March 2013 CMG Mortgage, Inc. is committed to making high quality mortgage services available to diverse communities

FAIR SERVICING: REGULATORS WATCH FOR DISCRIMINATION BY SERVICERS

FAIR SERVICING: REGULATORS WATCH FOR DISCRIMINATION BY SERVICERS BY BENJAMIN P. SAUL AND DANIEL ZYTNICK Fair lending requirements apply throughout the life of the loan! 1 Federal regulators delivered that

FAIR SERVICING: REGULATORS WATCH FOR DISCRIMINATION BY SERVICERS BY BENJAMIN P. SAUL AND DANIEL ZYTNICK Fair lending requirements apply throughout the life of the loan! 1 Federal regulators delivered that

What You Need to Know About the CFPB s Short-Term, Small- Dollar Lending Examination Procedures

What You Need to Know About the CFPB s Short-Term, Small- Dollar Lending Examination Procedures Richard P. Eckman Timothy R. McTaggart Pepper Hamilton LLP John C. Soffronoff, Jr. ICS Risk Advisors September

What You Need to Know About the CFPB s Short-Term, Small- Dollar Lending Examination Procedures Richard P. Eckman Timothy R. McTaggart Pepper Hamilton LLP John C. Soffronoff, Jr. ICS Risk Advisors September

Fair Lending Compliance Basics: Class is in Session!

Fair Lending Compliance Basics: Class is in Session! How to Control Fair Lending Risk and Identify Redlining Risk Meet Your Teacher Kimberly Boatwright, CRCM, CAMS Director of Compliance TRUPOINT Partners

Fair Lending Compliance Basics: Class is in Session! How to Control Fair Lending Risk and Identify Redlining Risk Meet Your Teacher Kimberly Boatwright, CRCM, CAMS Director of Compliance TRUPOINT Partners

Fair & Responsible Lending in the Regulatory Crosshairs

Fair & Responsible Lending in the Regulatory Crosshairs Legal Counsel to the Financial Services Industry Minnesota Banking Law Institute April 5, 2013 Andrea K. Mitchell Partner Lori J. Sommerfield Counsel

Fair & Responsible Lending in the Regulatory Crosshairs Legal Counsel to the Financial Services Industry Minnesota Banking Law Institute April 5, 2013 Andrea K. Mitchell Partner Lori J. Sommerfield Counsel

Regulatory Update OLA Fall Meeting. Suzanne Garwood

Regulatory Update OLA Fall Meeting Suzanne Garwood sgarwood@venable.com 202-344-8046 1 Regulated Issues Advertising Credit Denial Electronic Payments Customer Data Security 2 3 ADVERTISING Advertising

Regulatory Update OLA Fall Meeting Suzanne Garwood sgarwood@venable.com 202-344-8046 1 Regulated Issues Advertising Credit Denial Electronic Payments Customer Data Security 2 3 ADVERTISING Advertising

Fair Winds and Following Seas The sea, its perils and fair lending management? Timothy R. Burniston Executive Vice President, WKFS Consulting

Fair Winds and Following Seas The sea, its perils and fair lending management? Timothy R. Burniston Executive Vice President, WKFS Consulting SEA CAPTAIN: Responsible for operating ships in lakes, rivers,

Fair Winds and Following Seas The sea, its perils and fair lending management? Timothy R. Burniston Executive Vice President, WKFS Consulting SEA CAPTAIN: Responsible for operating ships in lakes, rivers,

FAIR LENDING POLICY I. INTRODUCTION A. OVERVIEW

FAIR LENDING POLICY I. INTRODUCTION A. OVERVIEW The purpose of this Fair Lending Policy ( Policy ) is to implement consumer protection mechanisms that ensure compliance with all applicable federal and

FAIR LENDING POLICY I. INTRODUCTION A. OVERVIEW The purpose of this Fair Lending Policy ( Policy ) is to implement consumer protection mechanisms that ensure compliance with all applicable federal and

Action Taken. Boot Camp 360 Series Presented by Kimberly Lundquist

Action Taken Boot Camp 360 Series Presented by Kimberly Lundquist Action Taken During the Pre-Application Process, most of the laws pertaining to real estate lending will come into play. We must be careful

Action Taken Boot Camp 360 Series Presented by Kimberly Lundquist Action Taken During the Pre-Application Process, most of the laws pertaining to real estate lending will come into play. We must be careful

Fair Lending Issues and Hot Topics

Fair Lending Issues and Hot Topics Outlook Live Webinar November 2, 2011 Non-Discrimination Working Group of the Financial Fraud Enforcement Task Force Visit us at www.consumercomplianceoutlook.org informational

Fair Lending Issues and Hot Topics Outlook Live Webinar November 2, 2011 Non-Discrimination Working Group of the Financial Fraud Enforcement Task Force Visit us at www.consumercomplianceoutlook.org informational

United States v. First United Security Bank (2009)

") DOJ Redlining Cases Failure to provide lending services to minority areas Few or no branches Little or no marketing CRA ( Community Reinvestment Act ) assessment area excluding minority areas Extremely

DOJ Redlining Cases Failure to provide lending services to minority areas Few or no branches Little or no marketing CRA ( Community Reinvestment Act ) assessment area excluding minority areas Extremely

The Commercial Real Estate Lending Decision Process Series (RMA)

") Business Banking & Commercial Lending Analyzing Business Financial Statements and Tax Returns Analyzing Financial Statements Analyzing Personal Financial Statements and Tax Returns Certificate in Business

Business Banking & Commercial Lending Analyzing Business Financial Statements and Tax Returns Analyzing Financial Statements Analyzing Personal Financial Statements and Tax Returns Certificate in Business

New and Re-emerging Fair Lending Risks. Article by Austin Brown & Loretta Kirkwood October 2014

New and Re-emerging Fair Lending Risks Article by Austin Brown & Loretta Kirkwood BY AUSTIN BROWN & LORETTA KIRKWOOD Austin Brown Loretta Kirkwood Regulators have been focused recently on several new and

New and Re-emerging Fair Lending Risks Article by Austin Brown & Loretta Kirkwood BY AUSTIN BROWN & LORETTA KIRKWOOD Austin Brown Loretta Kirkwood Regulators have been focused recently on several new and

LENDING: KEY EXAMINER TRENDS

LENDING: KEY EXAMINER TRENDS 2015 Temenos USA, Inc. All rights reserved. Leah M. Hamilton Chief Compliance Officer, TriComply Services WHAT YOU WILL LEARN TRID Compliance Reprieve Common issues Regulation

LENDING: KEY EXAMINER TRENDS 2015 Temenos USA, Inc. All rights reserved. Leah M. Hamilton Chief Compliance Officer, TriComply Services WHAT YOU WILL LEARN TRID Compliance Reprieve Common issues Regulation

Wholesale Price Monitoring in the Age of Tough Enforcement

Wholesale Price Monitoring in the Age of Tough Enforcement Melanie H. Brody, Partner, K&L Gates LLP Ric Pace, Principal, PricewaterhouseCoopers LLP Copyright 2010 by K&L Gates LLP. All rights reserved

Wholesale Price Monitoring in the Age of Tough Enforcement Melanie H. Brody, Partner, K&L Gates LLP Ric Pace, Principal, PricewaterhouseCoopers LLP Copyright 2010 by K&L Gates LLP. All rights reserved

National Mortgage Loan Originator Review Crammer (ml) Federal Mortgage-Related Laws

Federal Mortgage-Related Laws") Course: Lesson: National Mortgage Loan Originator Review Crammer (ml) Federal Mortgage-Related Laws 1. According to HMDA, what must be forwarded to the regulator by March 1 of each year? A. Adverse Action

Course: Lesson: National Mortgage Loan Originator Review Crammer (ml) Federal Mortgage-Related Laws 1. According to HMDA, what must be forwarded to the regulator by March 1 of each year? A. Adverse Action

Compliance Risk Assessments Chicago Region Banker Workshop Series

Compliance Risk Assessments 2016 Chicago Region Banker Workshop Series Statement During the onsite portion of a compliance examination, examiners review adherence to all consumer protection-related regulations.

Compliance Risk Assessments 2016 Chicago Region Banker Workshop Series Statement During the onsite portion of a compliance examination, examiners review adherence to all consumer protection-related regulations.

Keeping Fintech Fair: Thinking about Fair Lending and UDAP Risks

Keeping Fintech Fair: Thinking about Fair Lending and UDAP Risks Outlook Live Webinar July 16, 2018 Carol A. Evans Associate Director Div. of Consumer & Community Affairs Federal Reserve Board Katrina

Keeping Fintech Fair: Thinking about Fair Lending and UDAP Risks Outlook Live Webinar July 16, 2018 Carol A. Evans Associate Director Div. of Consumer & Community Affairs Federal Reserve Board Katrina

Keeping Fintech Fair: Thinking about Fair Lending and UDAP Risks

Keeping Fintech Fair: Thinking about Fair Lending and UDAP Risks Outlook Live Webinar July 16, 2018 Carol A. Evans Associate Director Div. of Consumer & Community Affairs Federal Reserve Board Katrina

Keeping Fintech Fair: Thinking about Fair Lending and UDAP Risks Outlook Live Webinar July 16, 2018 Carol A. Evans Associate Director Div. of Consumer & Community Affairs Federal Reserve Board Katrina

2/4/2014. Consumer Financial Protection Bureau Update A New Era of Regulation Begins. A Quick Overview of the CFPB. CFPB Overview (cont.

Consumer Financial Protection Bureau Update A New Era of Regulation Begins A Quick Overview of the CFPB The CFPB was created by Title X of the Dodd-Frank Act and became operational on July 21, 2011 Independent

Consumer Financial Protection Bureau Update A New Era of Regulation Begins A Quick Overview of the CFPB The CFPB was created by Title X of the Dodd-Frank Act and became operational on July 21, 2011 Independent

Action Taken. PRE-APPLICATION Do you Prequalify? Do you have Preapprovals? Which road do you take? Be Consistent!

1 Action Taken 2 PRE-APPLICATION Do you Prequalify? Do you have Preapprovals? Which road do you take? Be Consistent! 3 1 Discrimination & Fair Lending During the Pre-Application Process - use caution gathering

1 Action Taken 2 PRE-APPLICATION Do you Prequalify? Do you have Preapprovals? Which road do you take? Be Consistent! 3 1 Discrimination & Fair Lending During the Pre-Application Process - use caution gathering

Fair Housing Conference

Fair Housing Conference U.S. Attorney s Office for the District of Idaho April 2012 Laws Enforced by DOJ Fair Housing Act (FHA) Equal Credit Opportunity Act (ECOA) Titles II and III, Civil Rights Act of

Fair Housing Conference U.S. Attorney s Office for the District of Idaho April 2012 Laws Enforced by DOJ Fair Housing Act (FHA) Equal Credit Opportunity Act (ECOA) Titles II and III, Civil Rights Act of

Facing Today s Real Estate Regulations

Proudly Sponsored by Facing Today s Real Estate Regulations Presented by Don Braspenninckx Day, June 11, 2016 1:30 p.m. 1 Introduction Numerous regulatory changes in the real estate industry within last

Proudly Sponsored by Facing Today s Real Estate Regulations Presented by Don Braspenninckx Day, June 11, 2016 1:30 p.m. 1 Introduction Numerous regulatory changes in the real estate industry within last

Flanagan State Banks Guide to FHA Disclosures

This reference guide outlines the packet that is provided for Initial Disclosures when using FSB Mortgagebot for disclosing. The documents are listed in the order the system prints the forms. Form Name

This reference guide outlines the packet that is provided for Initial Disclosures when using FSB Mortgagebot for disclosing. The documents are listed in the order the system prints the forms. Form Name

NCUA s Fair Lending Compliance Program

Office of Consumer Protection NCUA s Fair Lending Compliance Program Virginia Credit Union League Fall Compliance Conference Williamsburg, VA October 16, 2013 OCP Organization 2 Division of Consumer Affairs

Office of Consumer Protection NCUA s Fair Lending Compliance Program Virginia Credit Union League Fall Compliance Conference Williamsburg, VA October 16, 2013 OCP Organization 2 Division of Consumer Affairs

Mortgage Regulation Update

Presented by: Mortgage Regulation Update Wisconsin Credit Union League Convention 1 Objectives At the end of this session, you will: Recognize recent updates to existing mortgage rules TILA/RESPA Integrated

Presented by: Mortgage Regulation Update Wisconsin Credit Union League Convention 1 Objectives At the end of this session, you will: Recognize recent updates to existing mortgage rules TILA/RESPA Integrated

National Association of Federal Credit Unions Fair Lending Training (Part II)

") National Association of Federal Credit Unions Fair Lending Training (Part II) April 23, 2014 Jeremiah S. Buckley, Partner Lori J. Sommerfield, Counsel Order of Presentation Key Players in Fair Lending

National Association of Federal Credit Unions Fair Lending Training (Part II) April 23, 2014 Jeremiah S. Buckley, Partner Lori J. Sommerfield, Counsel Order of Presentation Key Players in Fair Lending

ACTS & REGULATIONS. ECOA REG B Equal Credit Opportunity Act

ACTS & REGULATIONS ACT ECOA REG B Equal Credit Opportunity Act Issued by the Board of Governors of the Federal Reserve System HMDA REG C Home Mortgage Disclosure Act Implemented by the Federal Reserve

ACTS & REGULATIONS ACT ECOA REG B Equal Credit Opportunity Act Issued by the Board of Governors of the Federal Reserve System HMDA REG C Home Mortgage Disclosure Act Implemented by the Federal Reserve

REQUIRED ATTACHMENTS Please provide the following documents with this completed Annual Recertification

ANNUAL RECERTIFICATION For renewals through March, 2020 Company Legal Name: DBA(s): Street Address (Main Office): City, State, Zip: Affiliated Companies: REQUIRED INFORMATION Please provide company information

ANNUAL RECERTIFICATION For renewals through March, 2020 Company Legal Name: DBA(s): Street Address (Main Office): City, State, Zip: Affiliated Companies: REQUIRED INFORMATION Please provide company information

By electronic delivery to regulations.gov

Nessa Feddis Senior Vice President & Deputy Chief Counsel for Consumer Protection and Payments Center for Regulatory Compliance Government Relations Regulatory & Trust Affairs 202 663 5433 nfeddis@aba.com

Nessa Feddis Senior Vice President & Deputy Chief Counsel for Consumer Protection and Payments Center for Regulatory Compliance Government Relations Regulatory & Trust Affairs 202 663 5433 nfeddis@aba.com

Understanding the Regulatory Compliance Framework for Commercial and Business-Purpose Mortgage Loans

ONE VOICE. ONE VISION. ONE RESOURCE. MBA s COMMERCIAL / MULTIFAMILY FINANCE Understanding the Regulatory Compliance Framework for Commercial and Business-Purpose Mortgage Loans IN COOPERATION WITH 18292

ONE VOICE. ONE VISION. ONE RESOURCE. MBA s COMMERCIAL / MULTIFAMILY FINANCE Understanding the Regulatory Compliance Framework for Commercial and Business-Purpose Mortgage Loans IN COOPERATION WITH 18292

Sonia Lee Director of Affiliate Financial Services HFH International

Sonia Lee Director of Affiliate Financial Services HFH International Topics for Today Anti-Discrimination Laws Other Laws Outreach and Marketing Application Intake Selection Criteria Procedural Issues

Sonia Lee Director of Affiliate Financial Services HFH International Topics for Today Anti-Discrimination Laws Other Laws Outreach and Marketing Application Intake Selection Criteria Procedural Issues

2017 Interagency Fair Lending Hot Topics

2017 Interagency Fair Lending Hot Topics Outlook Live Webinar November 16, 2017 Visit us at www.consumercomplianceoutlook.org Visit us at www.consumercomplianceoutlook.org 1 Welcome to Outlook Live Logistics

2017 Interagency Fair Lending Hot Topics Outlook Live Webinar November 16, 2017 Visit us at www.consumercomplianceoutlook.org Visit us at www.consumercomplianceoutlook.org 1 Welcome to Outlook Live Logistics

Housing Discrimination in your Community. October 27, 2017 Bloomington, IL Sponsored by:

Housing Discrimination in your Community October 27, 2017 Bloomington, IL Sponsored by: Agenda Fair Housing Laws Fair Lending Laws Community Reinvestment Act How laws are implemented/enforced Local and

Housing Discrimination in your Community October 27, 2017 Bloomington, IL Sponsored by: Agenda Fair Housing Laws Fair Lending Laws Community Reinvestment Act How laws are implemented/enforced Local and

Closing Costs & Information

Closing Costs & Information Congratulations! You have decided to buy a new home. This will help you take this big financial step by describing the home buying, home financing, and settlement process. Lenders

Closing Costs & Information Congratulations! You have decided to buy a new home. This will help you take this big financial step by describing the home buying, home financing, and settlement process. Lenders

Federal Reserve Bank ATTN: Karen Smith Petition To Downgrade CRA Rating Complaint August 10, 2018 The Renaissance Indexes Group (RIG, Claimant) files

files") Federal Reserve Bank ATTN: Karen Smith Petition To Downgrade CRA Rating Complaint August 10, 2018 The Renaissance Indexes Group (RIG, Claimant) files the Petition To Downgrade Complaint against Comerica

Federal Reserve Bank ATTN: Karen Smith Petition To Downgrade CRA Rating Complaint August 10, 2018 The Renaissance Indexes Group (RIG, Claimant) files the Petition To Downgrade Complaint against Comerica

Is Your Mortgage Technology Really TRID-Ready?

Prepared by ComplianceEase September 2015 When the Consumer Financial Protection Bureau (CFPB) moved the effective date of the new TILA-RESPA Integrated Disclosure (TRID) rule from August 1 to October

Prepared by ComplianceEase September 2015 When the Consumer Financial Protection Bureau (CFPB) moved the effective date of the new TILA-RESPA Integrated Disclosure (TRID) rule from August 1 to October

CFPB Supervision and Examination Manual ECOA Components

APPENDIX D5 CFPB Supervision and Examination Manual ECOA Components [Editor s Note: This appendix reprints the Equal Credit Opportunity Act components of the Consumer Financial Protection Bureau s Supervision

APPENDIX D5 CFPB Supervision and Examination Manual ECOA Components [Editor s Note: This appendix reprints the Equal Credit Opportunity Act components of the Consumer Financial Protection Bureau s Supervision

Managing Fair and Responsible Lending Challenges and Risks

Managing Fair and Responsible Lending Challenges and Risks NYBA Technology, Compliance and Risk Management Forum White Plains, NY May 13, 2015 Legal Counsel to the Financial Services Industry Presented

Managing Fair and Responsible Lending Challenges and Risks NYBA Technology, Compliance and Risk Management Forum White Plains, NY May 13, 2015 Legal Counsel to the Financial Services Industry Presented

Fair Lending 2012 Significant Risk Management Agenda Items

June 4, 2012 Fair Lending 2012 Significant Risk Management Agenda Items by Joseph T. Lynyak III In the first few months of 2012, lenders were cautiously optimistic that a recent Supreme Court case and

June 4, 2012 Fair Lending 2012 Significant Risk Management Agenda Items by Joseph T. Lynyak III In the first few months of 2012, lenders were cautiously optimistic that a recent Supreme Court case and

JANUARY THROUGH APRIL 2013

www.coloradobankers.org / 303-825-1575 The delivery of training courses via the Internet provides students with the greatest flexibility and convenience. Whether for more traditional, instructor-led titles

www.coloradobankers.org / 303-825-1575 The delivery of training courses via the Internet provides students with the greatest flexibility and convenience. Whether for more traditional, instructor-led titles

CFPB Consumer Laws and Regulations

Consumer Laws and Regulations ECOA Equal Credit Opportunity Act (ECOA) The Equal Credit Opportunity Act (ECOA), which is implemented by Regulation B, applies to all creditors. When originally enacted,

Consumer Laws and Regulations ECOA Equal Credit Opportunity Act (ECOA) The Equal Credit Opportunity Act (ECOA), which is implemented by Regulation B, applies to all creditors. When originally enacted,

Intention of Presentation

Intention of Presentation This is intended to be a high level presentation and not to get into the detail of each individual area. More of an overview. If there are questions or you would like to go over

Intention of Presentation This is intended to be a high level presentation and not to get into the detail of each individual area. More of an overview. If there are questions or you would like to go over

CFPB Integrated Mortgage Disclosure Final Rule

CFPB Integrated Mortgage Disclosure Final Rule Current Status of the New Rule Mary Schuster Chief Product Officer - RamQuest The Regulatory Reform Ecosystem Meet the CFPB Mission Statement o To make markets

CFPB Integrated Mortgage Disclosure Final Rule Current Status of the New Rule Mary Schuster Chief Product Officer - RamQuest The Regulatory Reform Ecosystem Meet the CFPB Mission Statement o To make markets

Chapter 15 Real Estate Financing: Practice

Chapter 15 Real Estate Financing: Practice LECTURE OUTLINE: I. Introduction to the Real Estate Financing Market A. Federal Reserve System 1. Created to help maintain sound credit conditions 2. Helps counteract

Chapter 15 Real Estate Financing: Practice LECTURE OUTLINE: I. Introduction to the Real Estate Financing Market A. Federal Reserve System 1. Created to help maintain sound credit conditions 2. Helps counteract

How to Use This Service

BANKER S GUIDE TO COMPLIANCE How to Use This Service The Banker s Guide to Compliance is written in bankers language and intended for use by bankers. You need not be a lawyer or compliance expert to use

BANKER S GUIDE TO COMPLIANCE How to Use This Service The Banker s Guide to Compliance is written in bankers language and intended for use by bankers. You need not be a lawyer or compliance expert to use

Loan Originator Compensation Rules for Reverse Mortgages NRMLA Western Regional May 11, Jim Milano

Loan Originator Compensation Rules for Reverse Mortgages NRMLA Western Regional May 11, 2016 Jim Milano milano@thewbkfirm.com 1 Today s Agenda Loan Originator Compensation Rule (LO Comp) UDAAP RESPA FHA

Loan Originator Compensation Rules for Reverse Mortgages NRMLA Western Regional May 11, 2016 Jim Milano milano@thewbkfirm.com 1 Today s Agenda Loan Originator Compensation Rule (LO Comp) UDAAP RESPA FHA

WELCOME! Are You Ready for TRID?

1 WELCOME! www.grantsimon.com Are You Ready for TRID? 2 Dodd Frank the CFPB & You Featuring TRID TRID TILA-RESPA INTEGRATED DISCLOSURE 3 Ready For It New Jargon Lender Borrower Closing GFE & TIL HUD 1

1 WELCOME! www.grantsimon.com Are You Ready for TRID? 2 Dodd Frank the CFPB & You Featuring TRID TRID TILA-RESPA INTEGRATED DISCLOSURE 3 Ready For It New Jargon Lender Borrower Closing GFE & TIL HUD 1

A Brief Overview of the CFPB

A Brief Overview of the CFPB May 2011 Tara Sugiyama Potashnik tspotashnik@venable.com 2008 Venable LLP 1 Overview How we ended up with the CFPB Who is covered by the CFPB How the CFPB is structured CFPB

A Brief Overview of the CFPB May 2011 Tara Sugiyama Potashnik tspotashnik@venable.com 2008 Venable LLP 1 Overview How we ended up with the CFPB Who is covered by the CFPB How the CFPB is structured CFPB

CFPB Supervision and Examination Process

Background Title X of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (the Act) 1 established the Consumer Financial Protection Bureau (CFPB) and authorizes it to supervise certain

Background Title X of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (the Act) 1 established the Consumer Financial Protection Bureau (CFPB) and authorizes it to supervise certain

WELCOME!

WELCOME! www.grantsimon.com Are You Ready for TRID? Dodd Frank the CFPB & You Featuring TRID TRID TILA-RESPA INTEGRATED DISCLOSURE Ready For It New Jargon Lender Borrower Closing GFE & TIL HUD 1 & TIL

WELCOME! www.grantsimon.com Are You Ready for TRID? Dodd Frank the CFPB & You Featuring TRID TRID TILA-RESPA INTEGRATED DISCLOSURE Ready For It New Jargon Lender Borrower Closing GFE & TIL HUD 1 & TIL

Distance Learning 2018

Distance Learning 2018 Unmatched Financial Training for over 110 Years Independent Study Courses Credits Length Accounting II 3 4 months $595 Advertising 3 4 months $595 Agricultural Lending 3 4 months

Distance Learning 2018 Unmatched Financial Training for over 110 Years Independent Study Courses Credits Length Accounting II 3 4 months $595 Advertising 3 4 months $595 Agricultural Lending 3 4 months

Case 3:12-cv HZ Document 23-1 Filed 11/25/13 Page 1 of 15 Page ID#: 87

Case 3:12-cv-02006-HZ Document 23-1 Filed 11/25/13 Page 1 of 15 Page ID#: 87 STUART F. DELERY Assistant Attorney General MAAME EWUSI-MENSAH FRIMPONG Deputy Assistant Attorney General MICHAEL S. BLUME Director,

Case 3:12-cv-02006-HZ Document 23-1 Filed 11/25/13 Page 1 of 15 Page ID#: 87 STUART F. DELERY Assistant Attorney General MAAME EWUSI-MENSAH FRIMPONG Deputy Assistant Attorney General MICHAEL S. BLUME Director,

Presented by: David Luna, CMP

Presented by: David Luna, CMP Industry Veteran over 30 years Past Regional Manager for a California Bank Past Vice-President for a Federal Credit Union Past Regulator American Association of Residential

Presented by: David Luna, CMP Industry Veteran over 30 years Past Regional Manager for a California Bank Past Vice-President for a Federal Credit Union Past Regulator American Association of Residential

Road Map To CFPB Compliance For The Auto Finance Industry

Road Map To CFPB Compliance For The Auto Finance Industry Michael A. Thurman, Partner Consumer Protection Defense Department LOEB & LOEB Adds Value 2012 LOEB & LOEB LLP The Usual Disclaimers This presentation

Road Map To CFPB Compliance For The Auto Finance Industry Michael A. Thurman, Partner Consumer Protection Defense Department LOEB & LOEB Adds Value 2012 LOEB & LOEB LLP The Usual Disclaimers This presentation

Fair Lending THIS PUBLICATION IS. counsel for advice on specific fact situations. Copyrighted by Compliance Resource, LLC, April 2017

Fair Lending THIS PUBLICATION IS Not offered as legal advice SO Readers should consult with legal counsel for advice on specific fact situations. Copyrighted by Compliance Resource, LLC, April 2017 No

Fair Lending THIS PUBLICATION IS Not offered as legal advice SO Readers should consult with legal counsel for advice on specific fact situations. Copyrighted by Compliance Resource, LLC, April 2017 No

The New Loan Estimate & a. Closing Disclosure Explained. Know before you close.

Know before you close. The New Loan Estimate & a Closing Disclosure Explained A look at the different sections of each new form and explanations of each page. http://cfpb.fntic.com/ Barry S. Wolfinsohn

Know before you close. The New Loan Estimate & a Closing Disclosure Explained A look at the different sections of each new form and explanations of each page. http://cfpb.fntic.com/ Barry S. Wolfinsohn

Short-Term, Small-Dollar Lending

Commonly Known as Payday Lending Exam Date: Prepared By: Reviewer: Docket #: Entity Name: [Click&type] [Click&type] [Click&type] [Click&type] [Click&type] These examination procedures apply to the short-term,

Commonly Known as Payday Lending Exam Date: Prepared By: Reviewer: Docket #: Entity Name: [Click&type] [Click&type] [Click&type] [Click&type] [Click&type] These examination procedures apply to the short-term,

Section 1.35 Compliance Overview

Section 1.35 Compliance Overview In This Section This section contains the following topics: Overview... 2 General... 2 Overview... 2 Related Bulletins... 2 General... 2 Nationwide Mortgage Licensing System

Section 1.35 Compliance Overview In This Section This section contains the following topics: Overview... 2 General... 2 Overview... 2 Related Bulletins... 2 General... 2 Nationwide Mortgage Licensing System

Sue Quilty, Quilty & Associates (781)

") Sue Quilty, Quilty & Associates susan.quilty@verizon.net (781)706-9235 Agenda HMDA Today: Review HMDA in the Future: Proposed Changes Surviving HMDA Reporting 2 HMDA Review HMDA Overview Why is HMDA Important

Sue Quilty, Quilty & Associates susan.quilty@verizon.net (781)706-9235 Agenda HMDA Today: Review HMDA in the Future: Proposed Changes Surviving HMDA Reporting 2 HMDA Review HMDA Overview Why is HMDA Important

UDAP Analysis, Examinations, Case Studies, and Emerging Risks

UDAP Analysis, Examinations, Case Studies, and Emerging Risks Outlook Live Webinar March 5, 2013 Maureen Yap, Special Counsel Art Zaino, Senior Compliance Manager Tracy Anderson, Manager Visit us at www.consumercomplianceoutlook.org

UDAP Analysis, Examinations, Case Studies, and Emerging Risks Outlook Live Webinar March 5, 2013 Maureen Yap, Special Counsel Art Zaino, Senior Compliance Manager Tracy Anderson, Manager Visit us at www.consumercomplianceoutlook.org

6/21/2013. Section I. Purpose of Course. History and Overview of Mortgage Law, Regulation and Requirements

20 Hour Mortgage Loan Originator Certification Course Purpose of Course Gain historical perspective of mortgage lending Understand contemporary mortgage loan origination process Examine federal rules,

20 Hour Mortgage Loan Originator Certification Course Purpose of Course Gain historical perspective of mortgage lending Understand contemporary mortgage loan origination process Examine federal rules,

KENTUCKY: CHOICE OF INSURANCE NOTICE

Borrower: KENTUCKY: CHOICE OF INSURANCE NOTICE KY REVISED STATUTES CHAPTER 304.12-150 If you are required to provide any form of insurance coverage as part of your obligation on the above-referenced loan,

Borrower: KENTUCKY: CHOICE OF INSURANCE NOTICE KY REVISED STATUTES CHAPTER 304.12-150 If you are required to provide any form of insurance coverage as part of your obligation on the above-referenced loan,

HMDA Workshop Part IV: Fair Lending & HMDA

HMDA Workshop Part IV: Fair Lending & HMDA Sunday, Sept. 18, 2016, 4:45 pm Moderator: Richard H. Harvey, Jr., Chief Compliance Officer, Colonial Savings, F.A. Panelists: Melanie Brody, Partner, Mayer Brown

HMDA Workshop Part IV: Fair Lending & HMDA Sunday, Sept. 18, 2016, 4:45 pm Moderator: Richard H. Harvey, Jr., Chief Compliance Officer, Colonial Savings, F.A. Panelists: Melanie Brody, Partner, Mayer Brown

FREQUENTLY ASKED QUESTIONS ABOUT THE NEW HMDA DATA. General Background

Federal Reserve Bank of New York Statistics Function March 31, 2005 FREQUENTLY ASKED QUESTIONS ABOUT THE NEW HMDA DATA General Background 1. What is the Home Mortgage Disclosure Act (HMDA)? HMDA, enacted

Federal Reserve Bank of New York Statistics Function March 31, 2005 FREQUENTLY ASKED QUESTIONS ABOUT THE NEW HMDA DATA General Background 1. What is the Home Mortgage Disclosure Act (HMDA)? HMDA, enacted

CFPB & UDAAP. Recent Developments & Hot Topics. Michael Stockham. Nicole Williams. June 23,

CFPB & UDAAP Recent Developments & Hot Topics Michael Stockham Michael.Stockham@tklaw.com 214.969.2515 Nicole Williams Nicole.Williams@tklaw.com 214.969.1149 June 23, 2015 Agenda Background Trends Hot

CFPB & UDAAP Recent Developments & Hot Topics Michael Stockham Michael.Stockham@tklaw.com 214.969.2515 Nicole Williams Nicole.Williams@tklaw.com 214.969.1149 June 23, 2015 Agenda Background Trends Hot

Fair lending report of the Consumer Financial Protection Bureau

Fair lending report of the Consumer Financial Protection Bureau April 2014 Message from Richard Cordray Director of the CFPB From the moment we first opened our doors, the Consumer Financial Protection

Fair lending report of the Consumer Financial Protection Bureau April 2014 Message from Richard Cordray Director of the CFPB From the moment we first opened our doors, the Consumer Financial Protection

HMDA FACT SHEET YOUR MAP TO REGULATORY CHANGE

FACILITATE THOUGHT ENGAGE DIALOGUE ENCOURAGE SMART RISK CULTIVATE A NETWORK BUILD KNOWLEDGE HMDA FACT SHEET YOUR MAP TO REGULATORY CHANGE Regulation C implements the Home Mortgage Disclosure Act (HMDA),

FACILITATE THOUGHT ENGAGE DIALOGUE ENCOURAGE SMART RISK CULTIVATE A NETWORK BUILD KNOWLEDGE HMDA FACT SHEET YOUR MAP TO REGULATORY CHANGE Regulation C implements the Home Mortgage Disclosure Act (HMDA),

Copyright 2013 Carey Green - 1

Copyright 2013 Carey Green - 1 Mortgage Law Study Charts These charts are intended for use as a study-aid, not as compliance documents or official policies of any kind. Copyright 2013 Carey Green www.passthesafeexam.com

Copyright 2013 Carey Green - 1 Mortgage Law Study Charts These charts are intended for use as a study-aid, not as compliance documents or official policies of any kind. Copyright 2013 Carey Green www.passthesafeexam.com

Advertising Compliance

Advertising Compliance John Zasada Principal 218 790 1086 1 1 Credit Union Compliance Practice Review websites and social media for compliance before CU release Ongoing Regulatory Compliance Assistance

Advertising Compliance John Zasada Principal 218 790 1086 1 1 Credit Union Compliance Practice Review websites and social media for compliance before CU release Ongoing Regulatory Compliance Assistance

Regulatory Practice Letter December 2014 RPL 14-22

Regulatory Practice Letter December 2014 RPL 14-22 Automobile Supervision and Enforcement Regulatory Actions and CFPB Proposed Rule Executive Summary The automobile finance industry is under heightened

Regulatory Practice Letter December 2014 RPL 14-22 Automobile Supervision and Enforcement Regulatory Actions and CFPB Proposed Rule Executive Summary The automobile finance industry is under heightened

November 11, Early Resolution is Inconsistent with the CFPB s Loss Mitigation Requirements

November 11, 2014 William R. Breetz, Chairman Uniform Law Commission Home Foreclosure Procedures Act Committee University of Connecticut School of Law Knight Hall Room 202 35 Elizabeth Street Hartford,

November 11, 2014 William R. Breetz, Chairman Uniform Law Commission Home Foreclosure Procedures Act Committee University of Connecticut School of Law Knight Hall Room 202 35 Elizabeth Street Hartford,

Regulatory Environments

Analytics in Fair Lending and Regulatory Environments Deanna Neal First Vice-President Corporate Compliance SunTrust Bank Jeff Morrison First Vice-President Corporate Compliance SunTrust Bank #AnalyticsX

Analytics in Fair Lending and Regulatory Environments Deanna Neal First Vice-President Corporate Compliance SunTrust Bank Jeff Morrison First Vice-President Corporate Compliance SunTrust Bank #AnalyticsX

Section 1.35 Compliance Overview

Section 1.35 Compliance Overview In This Section This section contains the following topics: Overview... 2 Related Bulletins... 2 Nationwide Mortgage Licensing System Registry (S.A.F.E. Act)... 3 Nationwide

Section 1.35 Compliance Overview In This Section This section contains the following topics: Overview... 2 Related Bulletins... 2 Nationwide Mortgage Licensing System Registry (S.A.F.E. Act)... 3 Nationwide

Update on CFPB Enforcement Actions; UDAAP and Third-Party Lending

Update on CFPB Enforcement Actions; UDAAP and Third-Party Lending Presented to Pennsylvania Association of Community Bankers Quarterly Compliance Seminar Series 2016 October 19, 2016 2012 Kilpatrick Townsend

Update on CFPB Enforcement Actions; UDAAP and Third-Party Lending Presented to Pennsylvania Association of Community Bankers Quarterly Compliance Seminar Series 2016 October 19, 2016 2012 Kilpatrick Townsend

CFPB Compliance Bulletin Date: July 31, 2017

1700 G Street NW, Washington, DC 20552 CFPB Compliance Bulletin 2017-01 Date: July 31, 2017 Subject: Phone Pay Fees The Consumer Financial Protection Bureau (CFPB or Bureau) issues this Compliance Bulletin

1700 G Street NW, Washington, DC 20552 CFPB Compliance Bulletin 2017-01 Date: July 31, 2017 Subject: Phone Pay Fees The Consumer Financial Protection Bureau (CFPB or Bureau) issues this Compliance Bulletin

Notice. Conducting a Fair Lending Self Assessment Britt Faircloth, CRCM 4/2/2018. April 2018 Florida Bankers Association

Conducting a Fair Lending Self Assessment Britt Faircloth, CRCM April 2018 Florida Bankers Association Notice The information presented in this seminar summarizes general guidance and is intended only

Conducting a Fair Lending Self Assessment Britt Faircloth, CRCM April 2018 Florida Bankers Association Notice The information presented in this seminar summarizes general guidance and is intended only

Regulation by Enforcement CFPB s Use of UDAAP

Regulation by Enforcement CFPB s Use of UDAAP December 5, 2016 David Piper Cheryl Chang Dodd-Frank Act Dodd-Frank Act Consumer Financial Protection Bureau (CFPB) CFPB has independent rulemaking and enforcement

Regulation by Enforcement CFPB s Use of UDAAP December 5, 2016 David Piper Cheryl Chang Dodd-Frank Act Dodd-Frank Act Consumer Financial Protection Bureau (CFPB) CFPB has independent rulemaking and enforcement

Welcome to the California Mortgage Bankers Association s Mortgage Quality and Compliance Committee (MQAC)

") Welcome to the California Mortgage Bankers Association s Mortgage Quality and Compliance Committee (MQAC) April 25, 2013 You have entered the call on mute. If you have a question for Susan or CMBA, please

Welcome to the California Mortgage Bankers Association s Mortgage Quality and Compliance Committee (MQAC) April 25, 2013 You have entered the call on mute. If you have a question for Susan or CMBA, please

EMERGING CONSUMER RISKS FOR COMMUNITY BANKS

November 14, 2016 1 EMERGING CONSUMER RISKS FOR COMMUNITY BANKS 2016 ANNUAL RISK MANAGEMENT CONFERENCE NOVEMBER 14, 2016 November 14, 2016 2 Paul J. Stark, SVP & Chief Credit Officer Civista Bank, Sandusky

November 14, 2016 1 EMERGING CONSUMER RISKS FOR COMMUNITY BANKS 2016 ANNUAL RISK MANAGEMENT CONFERENCE NOVEMBER 14, 2016 November 14, 2016 2 Paul J. Stark, SVP & Chief Credit Officer Civista Bank, Sandusky

PUBLIC ENTITY PAK EMPLOYMENT PRACTICES LIABILITY COVERAGE

THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY. PUBLIC ENTITY PAK EMPLOYMENT PRACTICES LIABILITY COVERAGE This endorsement modifies insurance provided under the following: COMMERCIAL GENERAL

THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY. PUBLIC ENTITY PAK EMPLOYMENT PRACTICES LIABILITY COVERAGE This endorsement modifies insurance provided under the following: COMMERCIAL GENERAL

Fair Credit Compliance POLICY & PROGRAM

Fair Credit Compliance POLICY & PROGRAM Table of Contents Overview of Fair Credit Policy & Compliance Program Templates 1 Instructions for Completing Fair Credit Policy and Compliance Program Templates

Fair Credit Compliance POLICY & PROGRAM Table of Contents Overview of Fair Credit Policy & Compliance Program Templates 1 Instructions for Completing Fair Credit Policy and Compliance Program Templates

2016 Interagency Fair Lending Hot Topics

2016 Interagency Fair Lending Hot Topics Outlook Live Webinar October 4, 2016 Visit us at www.consumercomplianceoutlook.org Welcome to Outlook Live Logistics Call-in number: 1-888-625-5230 Conference code:

2016 Interagency Fair Lending Hot Topics Outlook Live Webinar October 4, 2016 Visit us at www.consumercomplianceoutlook.org Welcome to Outlook Live Logistics Call-in number: 1-888-625-5230 Conference code:

REAL ESTATE SETTLEMENT PROCEDURES ACT ( RESPA ) POLICY

POLICY") I. INTRODUCTION A. Background and Overview REAL ESTATE SETTLEMENT PROCEDURES ACT ( RESPA ) POLICY The Real Estate Settlement Procedures Act of 1974 ( RESPA ), 12 U.S.C. 2601 et seq., is a consumer disclosure

I. INTRODUCTION A. Background and Overview REAL ESTATE SETTLEMENT PROCEDURES ACT ( RESPA ) POLICY The Real Estate Settlement Procedures Act of 1974 ( RESPA ), 12 U.S.C. 2601 et seq., is a consumer disclosure

Status of New Uniform Residential Loan Application and Collection of Expanded Home

BILLING CODE: 4810-AM-P BUREAU OF CONSUMER FINANCIAL PROTECTION Status of New Uniform Residential Loan Application and Collection of Expanded Home Mortgage Disclosure Act Information about Ethnicity and

BILLING CODE: 4810-AM-P BUREAU OF CONSUMER FINANCIAL PROTECTION Status of New Uniform Residential Loan Application and Collection of Expanded Home Mortgage Disclosure Act Information about Ethnicity and

Regulatory Compliance Update

Regulatory Compliance Update ACUIA Region 6 Conference Presented By: Kristie Kenney Hoover, NCCO Internal Audit Manager, Doeren Mayhew Florida Michigan North Carolina Texas Insight. Oversight. Foresight.

Regulatory Compliance Update ACUIA Region 6 Conference Presented By: Kristie Kenney Hoover, NCCO Internal Audit Manager, Doeren Mayhew Florida Michigan North Carolina Texas Insight. Oversight. Foresight.

Fair Lending Compliance Management: Developing Strategies for Emerging Challenges

Fair Lending Compliance Management: Developing Strategies for Emerging Challenges August 20, 2014 2014 Crowe Horwath LLP 1 Agenda: The principal concepts of fair lending Current trends in fair lending

Fair Lending Compliance Management: Developing Strategies for Emerging Challenges August 20, 2014 2014 Crowe Horwath LLP 1 Agenda: The principal concepts of fair lending Current trends in fair lending

Distance Learning 2018

Distance Learning 2018 Unmatched Financial Training for over 110 Years Independent Study Courses Credits Length Accounting II 3 4 months $595 Advertising 3 4 months $595 Agricultural Lending 3 4 months

Distance Learning 2018 Unmatched Financial Training for over 110 Years Independent Study Courses Credits Length Accounting II 3 4 months $595 Advertising 3 4 months $595 Agricultural Lending 3 4 months

Real Estate Finance: 10/17/2017. Why use a mortgage?

Real Estate Finance: McGraw-Hill/Irwin Laws and Contracts Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Fixed rate (Monthly charge is 1/12 of stated annual rate) Adjustable rate

Real Estate Finance: McGraw-Hill/Irwin Laws and Contracts Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Fixed rate (Monthly charge is 1/12 of stated annual rate) Adjustable rate

Open-End Loan Advertising Compliance. John Zasada Principal CliftonLarsonAllen

Open-End Loan Advertising Compliance John Zasada Principal CliftonLarsonAllen 218 790 1086 Agenda Advertising compliance importance Regulation Z open end loan requirements APR Trigger terms HELOCs Credit

Open-End Loan Advertising Compliance John Zasada Principal CliftonLarsonAllen 218 790 1086 Agenda Advertising compliance importance Regulation Z open end loan requirements APR Trigger terms HELOCs Credit