Regulatory Environments

|

|

|

- Jean Terry

- 6 years ago

- Views:

Transcription

1 Analytics in Fair Lending and Regulatory Environments Deanna Neal First Vice-President Corporate Compliance SunTrust Bank Jeff Morrison First Vice-President Corporate Compliance SunTrust Bank #AnalyticsX C o p y r ig ht 201 6, SAS In sti tute In c. Al l r ig hts r ese rve d.

2 NEW OPPORTUNITIES IN STATISTICS: NAVIGATING THE REGULATORY ENVIRONMENT IN FAIR BANKING Traditional Statistics SAS programming Regression Analysis Clustering Text Mining The views expressed in this presentation are those of the authors, and do not represent the opinion of SunTrust Banks, Inc. or its subsidiaries SunTr ust Banks, Inc. SunTr ust is a federally r egistered trademark of SunTr ust Banks, Inc.

3 NAVIGATING THE REGULATORY ENVIRONMENT IN FAIR BANKING Fair and Responsible Banking The Fair Housing Act (FHA) was enacted in It prohibits discrimination by anyone during certain residential real estate transactions, including the following activities: Marketing Originating Pricing Underwriting Purchasing Selling Brokering Appraising 2

4 Fair and Responsible Banking NAVIGATING THE REGULATORY ENVIRONMENT IN FAIR BANKING The Fair Housing Act and U.S. Department of Housing and Urban Development regulations prohibit discrimination based on the following customer characteristics: Race MASTER Color TITLE STYLE National Origin Religion Sex Familial Status Handicap or Disability, including parental or family leave Sexual orientation or gender identity not explicitly covered, but housing discrimination against LGBTQ persons may be covered if it is based on non-conformity to gender stereotypes (discrimination on the basis of sex); fear of HIV/AIDS (discrimination on the basis of disability); or assumptions about marital or familial status. 3

5 Fair and Responsible Banking NAVIGATING THE REGULATORY ENVIRONMENT IN FAIR BANKING The Equal Credit Opportunity Act (ECOA) was enacted in 1974 to prohibit creditors from discriminating in any credit transaction, such as: Mortgages MASTER Small business TITLE loans Overdraft credit, including courtesy STYLE overdrafts Consumer loans (automobile, home equity lines/loans, credit cards) Loan modifications ECOA prohibits discrimination on the basis of: Race Color National Origin Religion Sex, including maternity or family leave Marital Status Age (provided the applicant can legally contract) Receipt of income from public assistance Exercise of rights under the Consumer Credit Protection Act 4

6 NAVIGATING THE REGULATORY ENVIRONMENT IN FAIR BANKING Fair and Responsible Banking Dodd-Frank Consumer Protection and Wall St. Reform Act of 2010 prudential regulators and FTC enforces UDAP. Among other effects, the Dodd-Frank Consumer Protection and Wall St. Reform Act of 2010 (Dodd-Frank Act) expanded the definition of unfair and deceptive acts. The CFPB enforces UDAAP, while the Unfair, deceptive, or abusive acts and practices (UDAAPs) can cause significant financial injury to consumers, erode consumer confidence, and undermine the financial marketplace. Under the Dodd-Frank Act, it is unlawful for any provider of consumer financial products or services or a service provider to engage in any unfair, deceptive, or abusive acts or practices. Consumer complaints play an important role in regulatory reviews and detection of unfair, deceptive, or abusive practices, as do high volumes of charge-backs or refunds for products or services. 5

7 PROXY FOR RACE / ETHNICITY FOR NON-MORTGAGE PRODUCTS Bayesian Improved Surname Geocoding (BISG) by CFPB CLICK Official TO CFPB Document: EDIT methodology.pdf This methodology mathematically combines (weights) last name frequencies and census tract and block demographic information into probabilities of an individual being a member of one of six racial or ethnic categories Census tables provided by CFPB in the public domain as well as implementation code. Requires the data to be geocoded using standard address formats along with the last name of the primary borrower and co-borrower 6

8 EXAMPLE OF GEOCODING / BISG IMPUTATION PROCESS Data needed: Name and Address Information for Geocoding and BISG Imputation Data returned: BISG Imputation and Gender Note: Information is fictitious and for illustrative purposes only 7

9 FAIR LENDING STATISTICAL REVIEW OF UNDERWRITING, PRICING Purpose Methodology underwriting or pricing decisions Check for potential disparate impact on minorities due to Logistic Regression, Linear Regression Means Test For underwriting, dependent variable =Probability of Decline For pricing, dependent variable = APR or discretionary component of pricing Implement BISG (Bayesian Improved Surname Geocoding) Statistical Results Difference in Average Decline Rate or Average Price between Whites and Minority or Protected Class Results from Regression Analysis Outlier Review, Random Sample, or Matched Pairs 8

10 FAIR LENDING STATISTICAL REVIEW OF UNDERWRITING POLICIES Create a Decline Event by assigning each applicant a value of 1 if Initial Credit Decision= Decline Methodology if Approve or Incomplete, assign a value of 0; else remove from sample Calculate BISG Probabilities for Whites, Blacks, Hispanics, Asians, American Indians, and Multi-race using Geocoding, Surname Lists, and the CFPB computer program. (pr_black, pr_hispanic, etc. 1 6 = 1) Assign Gender by using from name list or geocoding software (WIZ, Social Security or Census name lists, etc.) Apply Statistical Methods against Decline Event using control variables (custom score, FICO, etc.) for underwriting along with BISG data. Control variables should include credit policy quantitative mapping (FICO minimums, etc.) 9

11 FAIR LENDING STATISTICAL REVIEW OF UNDERWRITING, PRICING Declines=~20k MASTER TITLE Approvals=~50k STYLE Findings / Results Illustrative Example Decline Event for Underwriting Decision Simple Means Test Significant Differences? Use BISG to assign membership in demographic group Decline Means for Blacks (0.9) Whites (0.6) Decline Means for Hispanics (0.8) Whites (0.6) Decline Means for Asians (0.7) Whites (0.6) Regression Results Potential Issues Without Controls (BISG only) With Controls (Custom Score, FICO minimums, Joint Status, Gender, Overrides, DTI, etc.) 10

12 EXAMPLE OF POTENTIAL DISPARITY BISG ONLY (OMIT BISG FOR WHITES) Standard Estimate Error Parameter Logistic Regression: BISG Only Wald Chi- Square Pr > Chi Sq Intercept <.0001 pr_black <.0001 pr_hispanic <.0001 pr_api <.0001 pr_aian <.0001 pr_mult_other <.0001 Note: Above results are fictitious and for illustrative purposes only 11

13 EXAMPLE OF POTENTIAL DISPARITY ADD CONTROL VARIABLES - MASTER TITLE -- STYLE Parameter Logistic Regression: BISG + Control (Credit) Variables Estimate Standard Error Wald Chi- Square Pr > Chi Sq Intercept pr_black <.0001 pr_hispanic <.0001 pr_api pr_aian pr_mult_other Gender_Female Gender_Missing Gender_Joint <.0001 Average Credit Score <.0001 Minimum FICO <.0001 Debt to Income <.0001 Channel Dummy Override Year_dum Self Employment Dummy QTR QTR QTR Note: Above results are fictitious and for illustrative purposes only 12

14 True Positives True Positives CLASSIFICATION ACCURACY PREDICTED DECLINE EVENT No Control Variables With Underwriting Controls Poor information content Excellent information content False Positives Legend: Area Under Curve 90-1 = excellent (A) = good (B) = fair (C) = poor (D) = fail (F) False Positives 13

15 CASE STUDY REQUESTED LOAN (PRICING: APR) No Control Variables Variable Coefficient Significance FIT reduced. Black < Hispanic < Asian < Female... Results from Regression Analysis show disparities above the acceptable threshold for all protected classes using no controls other than BISG probabilities. By using pricing control variables, such as credit quality and collateral information, the disparities are significantly With Pricing Control Variables Coefficient Comparison Variable Coefficient Significance FIT Black Hispanic Asian Female < Note: Above results are fictitious and for illustrative purposes only 14

16 Matched Pair # CASE STUDY REQUESTED LOAN Pricing Matched Pair Review MASTER Protected TITLE Loan to STYLE Class FICO Term APR Value 11 White % Black % White % Hispanic % White % Asian % White % Black % White % Hispanic % Key variables used to determine similarly situated protected class FICO Term Loan to Value Conduct Manual File Review Manually review applications of the matched pairs to determine if there are factors not captured in the data file which could explain the variance in markup. Note: Above results are fictitious and for illustrative purposes only 15

17 NAVIGATING THE REGULATORY ENVIRONMENT IN FAIR BANKING Fair Lending vs. Traditional Models / Tools or Controls Traditional official business need Fair Lending regulatory screening tool MASTER Traditional TITLE forward looking STYLE Fair Lending forensic in nature Traditional weight of evidence, binning Fair Lending quantifying policy variables Traditional outlier analysis Fair Lending outlier analysis (DFBETAs, Cook s D) Traditional model validation (hold-out), stress testing Fair Lending forensic file reviews 16

18 TEXT MINING AND COMPLAINT ANALYSIS (PROOF OF CONCEPT APPROACH)

19 COMPLAINT ANALYSIS USING TEXT MINING Purpose Determine Feasibility of Predicting Complaint Resolutions Potentially Facilitate Work Priority Sampling for Review Methodology Closed Complaint Data Clean & Organize Complaint Narratives Determine Additional Predictors K Nearest Neighbor Classification (KNN) Preliminary Results Suggest Prediction Variables Word Clouds of Complaint Narratives KNN Classification Accuracy Supporting Paper, Implementation 18

20 COMPLAINT PATTERN NARRATIVES (EXAMPLES ARE FICTITIOUS) Example where NO ACTION REQUIRED was found Customer wants to submit a complaint because she is waiting for her closing of her refi since 04/15 and it is taking too long for the mortgage to close. The loan officer is XXX. Example where POTENTIAL EXCEPTION was found The customer complained that a branch employee refused to cash a check. Customer is a long-term client, and noticed that checks were cashed for white clients while she was being refused service. Customer is upset and complains that teller was rude and disrespectful. 19

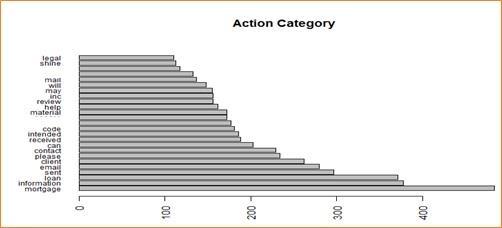

21 WORD CLOUDS BY CLASSIFICATION Classification = No Action Classification = Action 20

22 WORD FREQUENCY BY CLASSIFICATION 21

23 CREATION / IDENTIFICATION OF ADDITIONAL PREDICTORS Classification Outcome: No Action Required vs. Action Required Some Information Content (AUC=.68)

24 KNN NEAREST NEIGHBOR CLASSIFICATION Data is mathematically mapped to Euclidian distances Class assignment made by proximity to nearest neighboring data points Here, point c is closer to the o points rather than the a points, so it is classified as an o Here, 2 out of 3 votes are cast for group O 23

model 1/3 rd of data used to test")

25 MODELING DATA WAS SPLIT INTO 2 PARTITIONS 2/3 rds of data used to train (calibrate) model 1/3 rd of data used to test (i.e. validate) model MODEL CORRECTLY CLASSIFIES ALMOST ALL OF THE TEST NO ACTION GROUP AND ABOUT HALF OF THE TEST ACTION GROUP 24

26 CORRECTLY CLASSIFYING ACTION COMPLAINTS AS ACTION Model apparently picks up on complaint narratives that are more complex and wordy, classifying them as Action events, all other things remaining equal. Complaints that contain High Risk Terms, Tier 2, , and CRT 25

ranked by their probability.")

27 USING PROBABILITY OF ACTION NEEDED TO RANK ORDER COMPLAINTS Similar to a credit score, we can compute the probabilities of each classification and rank order them from high to low to select samples for review and auditing. Below we found about 75% of the action needed complaints in the first two deciles (20%) ranked by their probability. 26

28 #AnalyticsX C o p y r ig ht 201 6, SAS In sti tute In c. Al l r ig hts r ese rve d.

Fair Lending Examination Procedures Summary and Risk Factors Table

Federal Reserve Bank of Dallas Fair Lending Examination Procedures Summary and Risk Factors Table This publication is intended as a summary of the Fair Lending Examination Procedures. Also included is

Federal Reserve Bank of Dallas Fair Lending Examination Procedures Summary and Risk Factors Table This publication is intended as a summary of the Fair Lending Examination Procedures. Also included is

Non-Mortgage Products

Non-Mortgage Products Hot Issues in Non-Mortgage Lending Melanie Brody Partner Mayer Brown mbrody@mayerbrown.com Brian Clark Senior Manager Ernst & Young Brian.Clark@ey.com Speakers Melanie Brody Partner

Non-Mortgage Products Hot Issues in Non-Mortgage Lending Melanie Brody Partner Mayer Brown mbrody@mayerbrown.com Brian Clark Senior Manager Ernst & Young Brian.Clark@ey.com Speakers Melanie Brody Partner

To learn about navigation and other features of this e-learning course, click Help. Click Next to continue to the next page.

Welcome to Fair Lending Practices Extending credit is a cornerstone of banking. Because of the need society has for lending and credit, Congress has passed a number of acts ensuring that banks distribute

Welcome to Fair Lending Practices Extending credit is a cornerstone of banking. Because of the need society has for lending and credit, Congress has passed a number of acts ensuring that banks distribute

Notice. Conducting a Fair Lending Self Assessment Britt Faircloth, CRCM 4/2/2018. April 2018 Florida Bankers Association

Conducting a Fair Lending Self Assessment Britt Faircloth, CRCM April 2018 Florida Bankers Association Notice The information presented in this seminar summarizes general guidance and is intended only

Conducting a Fair Lending Self Assessment Britt Faircloth, CRCM April 2018 Florida Bankers Association Notice The information presented in this seminar summarizes general guidance and is intended only

HMDA Workshop Part IV: Fair Lending & HMDA

HMDA Workshop Part IV: Fair Lending & HMDA Sunday, Sept. 18, 2016, 4:45 pm Moderator: Richard H. Harvey, Jr., Chief Compliance Officer, Colonial Savings, F.A. Panelists: Melanie Brody, Partner, Mayer Brown

HMDA Workshop Part IV: Fair Lending & HMDA Sunday, Sept. 18, 2016, 4:45 pm Moderator: Richard H. Harvey, Jr., Chief Compliance Officer, Colonial Savings, F.A. Panelists: Melanie Brody, Partner, Mayer Brown

Keeping Fintech Fair: Thinking about Fair Lending and UDAP Risks

Keeping Fintech Fair: Thinking about Fair Lending and UDAP Risks Outlook Live Webinar July 16, 2018 Carol A. Evans Associate Director Div. of Consumer & Community Affairs Federal Reserve Board Katrina

Keeping Fintech Fair: Thinking about Fair Lending and UDAP Risks Outlook Live Webinar July 16, 2018 Carol A. Evans Associate Director Div. of Consumer & Community Affairs Federal Reserve Board Katrina

Keeping Fintech Fair: Thinking about Fair Lending and UDAP Risks

Keeping Fintech Fair: Thinking about Fair Lending and UDAP Risks Outlook Live Webinar July 16, 2018 Carol A. Evans Associate Director Div. of Consumer & Community Affairs Federal Reserve Board Katrina

Keeping Fintech Fair: Thinking about Fair Lending and UDAP Risks Outlook Live Webinar July 16, 2018 Carol A. Evans Associate Director Div. of Consumer & Community Affairs Federal Reserve Board Katrina

FREQUENTLY ASKED QUESTIONS ABOUT THE NEW HMDA DATA. General Background

Federal Reserve Bank of New York Statistics Function March 31, 2005 FREQUENTLY ASKED QUESTIONS ABOUT THE NEW HMDA DATA General Background 1. What is the Home Mortgage Disclosure Act (HMDA)? HMDA, enacted

Federal Reserve Bank of New York Statistics Function March 31, 2005 FREQUENTLY ASKED QUESTIONS ABOUT THE NEW HMDA DATA General Background 1. What is the Home Mortgage Disclosure Act (HMDA)? HMDA, enacted

Fair Lending Risk Management

Presented by: Martin (Marty) Mitchell, CRCM Managing Director, ProBank Austin Robert J. (Bob) Mullenbach, CRCM Managing Director, Compliance Division Deputy, ProBank Austin Fair Lending Laws ECOA Prohibits

Presented by: Martin (Marty) Mitchell, CRCM Managing Director, ProBank Austin Robert J. (Bob) Mullenbach, CRCM Managing Director, Compliance Division Deputy, ProBank Austin Fair Lending Laws ECOA Prohibits

Fair Lending Compliance Management: Developing Strategies for Emerging Challenges

Fair Lending Compliance Management: Developing Strategies for Emerging Challenges August 20, 2014 2014 Crowe Horwath LLP 1 Agenda: The principal concepts of fair lending Current trends in fair lending

Fair Lending Compliance Management: Developing Strategies for Emerging Challenges August 20, 2014 2014 Crowe Horwath LLP 1 Agenda: The principal concepts of fair lending Current trends in fair lending

CLIENT UPDATE CFPB PROPOSES AUTO FINANCE LARGER PARTICIPANT RULE, RELEASES FAIR LENDING SUPERVISORY REPORT AND PROXY METHODOLOGY

CLIENT UPDATE CFPB PROPOSES AUTO FINANCE LARGER PARTICIPANT RULE, RELEASES FAIR LENDING SUPERVISORY REPORT AND PROXY METHODOLOGY NEW YORK Helen V. Cantwell hvcantwell@debevoise.com Courtney M. Dankworth

CLIENT UPDATE CFPB PROPOSES AUTO FINANCE LARGER PARTICIPANT RULE, RELEASES FAIR LENDING SUPERVISORY REPORT AND PROXY METHODOLOGY NEW YORK Helen V. Cantwell hvcantwell@debevoise.com Courtney M. Dankworth

Sue Quilty, Quilty & Associates (781)

") Sue Quilty, Quilty & Associates susan.quilty@verizon.net (781)706-9235 Agenda HMDA Today: Review HMDA in the Future: Proposed Changes Surviving HMDA Reporting 2 HMDA Review HMDA Overview Why is HMDA Important

Sue Quilty, Quilty & Associates susan.quilty@verizon.net (781)706-9235 Agenda HMDA Today: Review HMDA in the Future: Proposed Changes Surviving HMDA Reporting 2 HMDA Review HMDA Overview Why is HMDA Important

2017 Interagency Fair Lending Hot Topics

2017 Interagency Fair Lending Hot Topics Outlook Live Webinar November 16, 2017 Visit us at www.consumercomplianceoutlook.org Visit us at www.consumercomplianceoutlook.org 1 Welcome to Outlook Live Logistics

2017 Interagency Fair Lending Hot Topics Outlook Live Webinar November 16, 2017 Visit us at www.consumercomplianceoutlook.org Visit us at www.consumercomplianceoutlook.org 1 Welcome to Outlook Live Logistics

Regulatory Practice Letter December 2014 RPL 14-22

Regulatory Practice Letter December 2014 RPL 14-22 Automobile Supervision and Enforcement Regulatory Actions and CFPB Proposed Rule Executive Summary The automobile finance industry is under heightened

Regulatory Practice Letter December 2014 RPL 14-22 Automobile Supervision and Enforcement Regulatory Actions and CFPB Proposed Rule Executive Summary The automobile finance industry is under heightened

Road Map To CFPB Compliance For The Auto Finance Industry

Road Map To CFPB Compliance For The Auto Finance Industry Michael A. Thurman, Partner Consumer Protection Defense Department LOEB & LOEB Adds Value 2012 LOEB & LOEB LLP The Usual Disclaimers This presentation

Road Map To CFPB Compliance For The Auto Finance Industry Michael A. Thurman, Partner Consumer Protection Defense Department LOEB & LOEB Adds Value 2012 LOEB & LOEB LLP The Usual Disclaimers This presentation

Indirect Auto Lending Fair Lending Considerations

Indirect Auto Lending Fair Lending Considerations Outlook Live Webinar August 6, 2013 Consumer Financial Protection Bureau Federal Reserve Board U.S. Department of Justice Visit us at www.consumercomplianceoutlook.org

Indirect Auto Lending Fair Lending Considerations Outlook Live Webinar August 6, 2013 Consumer Financial Protection Bureau Federal Reserve Board U.S. Department of Justice Visit us at www.consumercomplianceoutlook.org

Spearfish Economic Development Corporation Community Capital Revolving Loan Fund. Application Information

Spearfish Economic Development Corporation Community Capital Revolving Loan Fund Application Information SEDC Revolving Loan Fund Application Information Spearfish Economic Development is a private non-profit

Spearfish Economic Development Corporation Community Capital Revolving Loan Fund Application Information SEDC Revolving Loan Fund Application Information Spearfish Economic Development is a private non-profit

Implications and Risks of New HMDA Data Disclosure

Implications and Risks of New HMDA Data Disclosure By David Skanderson, Ph.D. January 2018 A version of this paper appeared in ABA Bank Compliance, January/February 2018 The conclusions set forth herein

Implications and Risks of New HMDA Data Disclosure By David Skanderson, Ph.D. January 2018 A version of this paper appeared in ABA Bank Compliance, January/February 2018 The conclusions set forth herein

Fair & Responsible Lending in the Regulatory Crosshairs

Fair & Responsible Lending in the Regulatory Crosshairs Legal Counsel to the Financial Services Industry Minnesota Banking Law Institute April 5, 2013 Andrea K. Mitchell Partner Lori J. Sommerfield Counsel

Fair & Responsible Lending in the Regulatory Crosshairs Legal Counsel to the Financial Services Industry Minnesota Banking Law Institute April 5, 2013 Andrea K. Mitchell Partner Lori J. Sommerfield Counsel

Loan Growth and Compliance Pitfalls

Loan Growth and Compliance Pitfalls presented by LOANLINER Compliance Information provided in this presentation, including all materials, should not be construed as legal services, legal advice, or in

Loan Growth and Compliance Pitfalls presented by LOANLINER Compliance Information provided in this presentation, including all materials, should not be construed as legal services, legal advice, or in

ONLINE APPENDIX. The Vulnerability of Minority Homeowners in the Housing Boom and Bust. Patrick Bayer Fernando Ferreira Stephen L Ross

ONLINE APPENDIX The Vulnerability of Minority Homeowners in the Housing Boom and Bust Patrick Bayer Fernando Ferreira Stephen L Ross Appendix A: Supplementary Tables for The Vulnerability of Minority Homeowners

ONLINE APPENDIX The Vulnerability of Minority Homeowners in the Housing Boom and Bust Patrick Bayer Fernando Ferreira Stephen L Ross Appendix A: Supplementary Tables for The Vulnerability of Minority Homeowners

FAIR SERVICING: REGULATORS WATCH FOR DISCRIMINATION BY SERVICERS

FAIR SERVICING: REGULATORS WATCH FOR DISCRIMINATION BY SERVICERS BY BENJAMIN P. SAUL AND DANIEL ZYTNICK Fair lending requirements apply throughout the life of the loan! 1 Federal regulators delivered that

FAIR SERVICING: REGULATORS WATCH FOR DISCRIMINATION BY SERVICERS BY BENJAMIN P. SAUL AND DANIEL ZYTNICK Fair lending requirements apply throughout the life of the loan! 1 Federal regulators delivered that

Testing Methodologies for Credit Score Models to Identify Statistical Bias toward Protected Classes

White Paper Series May 2014 Testing Methodologies for Credit Score Models to Identify Statistical Bias toward Protected Classes Introduction The Equal Credit Opportunity Act (ECOA), implemented by Federal

White Paper Series May 2014 Testing Methodologies for Credit Score Models to Identify Statistical Bias toward Protected Classes Introduction The Equal Credit Opportunity Act (ECOA), implemented by Federal

Decorah Small Business Revolving Loan Fund Application

Decorah Small Business Revolving Loan Fund Application Name of Applicant: Street Address: State: Legal Entity Zip: Email: Sole Proprietorship Partnership Corporation Federal Employer ID#: Date Business

Decorah Small Business Revolving Loan Fund Application Name of Applicant: Street Address: State: Legal Entity Zip: Email: Sole Proprietorship Partnership Corporation Federal Employer ID#: Date Business

FAIR LENDING PLAN. NMLS #1820 Fair Lending Plan Policy. (Fair Housing Act/Equal Credit Opportunity Act/Home Mortgage Disclosure Act) March 2013

March 2013") FAIR LENDING PLAN (Fair Housing Act/Equal Credit Opportunity Act/Home Mortgage Disclosure Act) March 2013 CMG Mortgage, Inc. is committed to making high quality mortgage services available to diverse communities

FAIR LENDING PLAN (Fair Housing Act/Equal Credit Opportunity Act/Home Mortgage Disclosure Act) March 2013 CMG Mortgage, Inc. is committed to making high quality mortgage services available to diverse communities

West River Revolving Loan Fund. Application Information

West River Revolving Loan Fund Application Information Revised 2/17/2011 West River Revolving Loan Fund Application Information The West River Foundation, Inc., a private non-profit corporation, governs

West River Revolving Loan Fund Application Information Revised 2/17/2011 West River Revolving Loan Fund Application Information The West River Foundation, Inc., a private non-profit corporation, governs

6/21/2013. Section I. Purpose of Course. History and Overview of Mortgage Law, Regulation and Requirements

20 Hour Mortgage Loan Originator Certification Course Purpose of Course Gain historical perspective of mortgage lending Understand contemporary mortgage loan origination process Examine federal rules,

20 Hour Mortgage Loan Originator Certification Course Purpose of Course Gain historical perspective of mortgage lending Understand contemporary mortgage loan origination process Examine federal rules,

REQUIRED ATTACHMENTS Please provide the following documents with this completed Annual Recertification

ANNUAL RECERTIFICATION For renewals through March, 2020 Company Legal Name: DBA(s): Street Address (Main Office): City, State, Zip: Affiliated Companies: REQUIRED INFORMATION Please provide company information

ANNUAL RECERTIFICATION For renewals through March, 2020 Company Legal Name: DBA(s): Street Address (Main Office): City, State, Zip: Affiliated Companies: REQUIRED INFORMATION Please provide company information

Equal Credit Opportunity Act - Regulation B

Equal Credit Opportunity Act - Regulation B General Policy Statement: The purpose of the Equal Credit Opportunity Act (the Act) is to promote the availability of credit to all creditworthy applicants without

Equal Credit Opportunity Act - Regulation B General Policy Statement: The purpose of the Equal Credit Opportunity Act (the Act) is to promote the availability of credit to all creditworthy applicants without

BUSINESS LOAN APPLICATION

BUSINESS LOAN APPLICATION 1. Applicant Name: Name of Business: Sole Proprietorship: S Corporation: Partnership: C Corporation: LLC/LLP: Mailing Address: Street Address: Business Telephone: Home Telephone:

BUSINESS LOAN APPLICATION 1. Applicant Name: Name of Business: Sole Proprietorship: S Corporation: Partnership: C Corporation: LLC/LLP: Mailing Address: Street Address: Business Telephone: Home Telephone:

BUSINESS LOAN APPLICATION

BUSINESS LOAN APPLICATION SECTION I: APPLICANT INFORMATION First Name: Last Name: Mailing Address: Physical Address: City: State & Zip Code: Primary Phone: Cell Phone: E-Mail Address: Is the applicant

BUSINESS LOAN APPLICATION SECTION I: APPLICANT INFORMATION First Name: Last Name: Mailing Address: Physical Address: City: State & Zip Code: Primary Phone: Cell Phone: E-Mail Address: Is the applicant

CONSUMER CREDIT APPLICATION

CONSUMER CREDIT APPLICATION CREDIT REQUEST Which product are you applying for? Personal Loan Term Requested: Overdraft Protection for Account #: Personal Line of Credit Amount Requested: Loan Purpose (check

CONSUMER CREDIT APPLICATION CREDIT REQUEST Which product are you applying for? Personal Loan Term Requested: Overdraft Protection for Account #: Personal Line of Credit Amount Requested: Loan Purpose (check

APPLICATION FOR SMALL BUSINESS LOAN

APPLICATION FOR SMALL BUSINESS LOAN Please return this form with the applicable credit report fees. We cannot consider any loan request that is not accompanied by a completed application. COMPANY INFORMATION

APPLICATION FOR SMALL BUSINESS LOAN Please return this form with the applicable credit report fees. We cannot consider any loan request that is not accompanied by a completed application. COMPANY INFORMATION

FAIR LENDING POLICY I. INTRODUCTION A. OVERVIEW

FAIR LENDING POLICY I. INTRODUCTION A. OVERVIEW The purpose of this Fair Lending Policy ( Policy ) is to implement consumer protection mechanisms that ensure compliance with all applicable federal and

FAIR LENDING POLICY I. INTRODUCTION A. OVERVIEW The purpose of this Fair Lending Policy ( Policy ) is to implement consumer protection mechanisms that ensure compliance with all applicable federal and

Fair Lending Issues and Hot Topics

Fair Lending Issues and Hot Topics Outlook Live Webinar November 2, 2011 Non-Discrimination Working Group of the Financial Fraud Enforcement Task Force Visit us at www.consumercomplianceoutlook.org informational

Fair Lending Issues and Hot Topics Outlook Live Webinar November 2, 2011 Non-Discrimination Working Group of the Financial Fraud Enforcement Task Force Visit us at www.consumercomplianceoutlook.org informational

National Association of Federal Credit Unions. Fair Lending Training (Part I) March 19, Lori J. Sommerfield Counsel BuckleySandler LLP

March 19, Lori J. Sommerfield Counsel BuckleySandler LLP") National Association of Federal Credit Unions Fair Lending Training (Part I) March 19, 2014 Lori J. Sommerfield Counsel BuckleySandler LLP Order of Presentation Overview of Fair Lending Laws & Regulations

National Association of Federal Credit Unions Fair Lending Training (Part I) March 19, 2014 Lori J. Sommerfield Counsel BuckleySandler LLP Order of Presentation Overview of Fair Lending Laws & Regulations

Fair Housing Conference

Fair Housing Conference U.S. Attorney s Office for the District of Idaho April 2012 Laws Enforced by DOJ Fair Housing Act (FHA) Equal Credit Opportunity Act (ECOA) Titles II and III, Civil Rights Act of

Fair Housing Conference U.S. Attorney s Office for the District of Idaho April 2012 Laws Enforced by DOJ Fair Housing Act (FHA) Equal Credit Opportunity Act (ECOA) Titles II and III, Civil Rights Act of

Consumer Data Industry Association Fair Lending Teleseminar

Consumer Data Industry Association Fair Lending Teleseminar May 10, 2016 D. Jean Veta, Covington & Burling LLP Michael Nonaka, Covington & Burling LLP Marsha J. Courchane, Charles River Associates Agenda

Consumer Data Industry Association Fair Lending Teleseminar May 10, 2016 D. Jean Veta, Covington & Burling LLP Michael Nonaka, Covington & Burling LLP Marsha J. Courchane, Charles River Associates Agenda

Wholesale Price Monitoring in the Age of Tough Enforcement

Wholesale Price Monitoring in the Age of Tough Enforcement Melanie H. Brody, Partner, K&L Gates LLP Ric Pace, Principal, PricewaterhouseCoopers LLP Copyright 2010 by K&L Gates LLP. All rights reserved

Wholesale Price Monitoring in the Age of Tough Enforcement Melanie H. Brody, Partner, K&L Gates LLP Ric Pace, Principal, PricewaterhouseCoopers LLP Copyright 2010 by K&L Gates LLP. All rights reserved

Compliance Policy 2003-ALL

Overview The following policy describes how CMG Mortgage, Inc., dba CMG Financial, NMLS #1820, ( CMG ) complies with the Home Mortgage Disclosure Act (HMDA) and its implementing regulation, Regulation

Overview The following policy describes how CMG Mortgage, Inc., dba CMG Financial, NMLS #1820, ( CMG ) complies with the Home Mortgage Disclosure Act (HMDA) and its implementing regulation, Regulation

Consumer Financial Protection Bureau. March 15, Draft, Sensitive and Pre-Decisional Not for External Distribution

Consumer Financial Protection Bureau March 15, 2016 Draft, Sensitive and Pre-Decisional Not for External Distribution Outline Home Mortgage Disclosure Act 1) Background 2) Rule Making 3) Changes Coming

Consumer Financial Protection Bureau March 15, 2016 Draft, Sensitive and Pre-Decisional Not for External Distribution Outline Home Mortgage Disclosure Act 1) Background 2) Rule Making 3) Changes Coming

HMDA INPUT AND REQUIREMENTS. Updated: 3/16/2017, S. Noble

HMDA INPUT AND REQUIREMENTS Updated: 3/16/2017, S. Noble 1 What is HMDA?? The Home Mortgage Disclosure Act (HMDA) was enacted by Congress in 1975 and was implemented by the Federal Reserve Board s Regulation

HMDA INPUT AND REQUIREMENTS Updated: 3/16/2017, S. Noble 1 What is HMDA?? The Home Mortgage Disclosure Act (HMDA) was enacted by Congress in 1975 and was implemented by the Federal Reserve Board s Regulation

Presentation Topics. Changing Data Requirements Will Effect. Census data update and implications for CRA, HMDA and Fair Lending

Changing Data Requirements Will Effect the CRA and Fair Lending Environment Prepared for the 2012 National Community Reinvestment Conference by Glenn Canner March 28, 2012 The views expressed are those

Changing Data Requirements Will Effect the CRA and Fair Lending Environment Prepared for the 2012 National Community Reinvestment Conference by Glenn Canner March 28, 2012 The views expressed are those

Confusion in scorecard construction - the wrong scores for the right reasons

Confusion in scorecard construction - the wrong scores for the right reasons David J. Hand Imperial College, London and Winton Capital Management September 2012 Confusion in scorecard construction - Hand

Confusion in scorecard construction - the wrong scores for the right reasons David J. Hand Imperial College, London and Winton Capital Management September 2012 Confusion in scorecard construction - Hand

Major Changes Looming for HMDA Reporting

Major Changes Looming for HMDA Reporting CLIENT ALERT September 25, 2017 Scott D. Samlin samlins@pepperlaw.com Mark T. Dabertin dabertinm@pepperlaw.com In this article, we review the requirements of the

Major Changes Looming for HMDA Reporting CLIENT ALERT September 25, 2017 Scott D. Samlin samlins@pepperlaw.com Mark T. Dabertin dabertinm@pepperlaw.com In this article, we review the requirements of the

MORTGAGE REFORM UNDER THE DODD FRANK WALL STREET REFORM AND CONSUMER PROTECTION ACT

MORTGAGE REFORM UNDER THE DODD FRANK WALL STREET REFORM AND CONSUMER PROTECTION ACT KENNETH BENTON SENIOR CONSUMER REGULATIONS SPECIALIST FEDERAL RESERVE BANK OF PHILADELPHIA MAY 10, 2012 Disclaimer: the

MORTGAGE REFORM UNDER THE DODD FRANK WALL STREET REFORM AND CONSUMER PROTECTION ACT KENNETH BENTON SENIOR CONSUMER REGULATIONS SPECIALIST FEDERAL RESERVE BANK OF PHILADELPHIA MAY 10, 2012 Disclaimer: the

Fair Winds and Following Seas The sea, its perils and fair lending management? Timothy R. Burniston Executive Vice President, WKFS Consulting

Fair Winds and Following Seas The sea, its perils and fair lending management? Timothy R. Burniston Executive Vice President, WKFS Consulting SEA CAPTAIN: Responsible for operating ships in lakes, rivers,

Fair Winds and Following Seas The sea, its perils and fair lending management? Timothy R. Burniston Executive Vice President, WKFS Consulting SEA CAPTAIN: Responsible for operating ships in lakes, rivers,

Managing Fair and Responsible Lending Challenges and Risks

Managing Fair and Responsible Lending Challenges and Risks NYBA Technology, Compliance and Risk Management Forum White Plains, NY May 13, 2015 Legal Counsel to the Financial Services Industry Presented

Managing Fair and Responsible Lending Challenges and Risks NYBA Technology, Compliance and Risk Management Forum White Plains, NY May 13, 2015 Legal Counsel to the Financial Services Industry Presented

Fair Lending In The Mortgage Industry How You will do Business in 2014?

Fair Lending In The Mortgage Industry How You will do Business in 2014? Presenter: Tammy Butler, Master CMB and Director of Fair lending and Compliance, Optimal Blue Time to Prepare for January 2014 2013

Fair Lending In The Mortgage Industry How You will do Business in 2014? Presenter: Tammy Butler, Master CMB and Director of Fair lending and Compliance, Optimal Blue Time to Prepare for January 2014 2013

Division of Depositor and Consumer Protection Dallas Region Quarterly Newsletter 3rd Quarter 2017

Volume 5, Issue 3 Division of Depositor and Consumer Protection Dallas Region Quarterly Newsletter 3rd Quarter 2017 Revised Pre-Examination Planning Process I nside this i s s u e : Revised Pre- Examination

Volume 5, Issue 3 Division of Depositor and Consumer Protection Dallas Region Quarterly Newsletter 3rd Quarter 2017 Revised Pre-Examination Planning Process I nside this i s s u e : Revised Pre- Examination

Closing Costs & Information

Closing Costs & Information Congratulations! You have decided to buy a new home. This will help you take this big financial step by describing the home buying, home financing, and settlement process. Lenders

Closing Costs & Information Congratulations! You have decided to buy a new home. This will help you take this big financial step by describing the home buying, home financing, and settlement process. Lenders

LOAN APPLICATION P.O. BOX 1138, HUNTSVILLE, AR OFFICE: FAX:

LOAN APPLICATION P.O. BOX 1138, HUNTSVILLE, AR 72740 OFFICE: 479.738.1585 FAX: 479.738.6288 FORGE@forgefund.org Please take your time filling out this application. If you need help, please contact FORGE

LOAN APPLICATION P.O. BOX 1138, HUNTSVILLE, AR 72740 OFFICE: 479.738.1585 FAX: 479.738.6288 FORGE@forgefund.org Please take your time filling out this application. If you need help, please contact FORGE

The High Cost of Segregation: Exploring the Relationship Between Racial Segregation and Subprime Lending

F u r m a n C e n t e r f o r r e a l e s t a t e & u r b a n p o l i c y N e w Y o r k U n i v e r s i t y s c h o o l o f l aw wa g n e r s c h o o l o f p u b l i c s e r v i c e n o v e m b e r 2 0

F u r m a n C e n t e r f o r r e a l e s t a t e & u r b a n p o l i c y N e w Y o r k U n i v e r s i t y s c h o o l o f l aw wa g n e r s c h o o l o f p u b l i c s e r v i c e n o v e m b e r 2 0

Improving Lending Through Modeling Defaults. BUDT 733: Data Mining for Business May 10, 2010 Team 1 Lindsey Cohen Ross Dodd Wells Person Amy Rzepka

Improving Lending Through Modeling Defaults BUDT 733: Data Mining for Business May 10, 2010 Team 1 Lindsey Cohen Ross Dodd Wells Person Amy Rzepka EXECUTIVE SUMMARY Background Prosper.com is an online

Improving Lending Through Modeling Defaults BUDT 733: Data Mining for Business May 10, 2010 Team 1 Lindsey Cohen Ross Dodd Wells Person Amy Rzepka EXECUTIVE SUMMARY Background Prosper.com is an online

HMDA / Regulation C Amendments New 1003 Application

HMDA / Regulation C Amendments New 1003 Application January 2017 1Nations Direct Mortgage, LLC Mission Statement - To lead the third party residential mortgage industry by providing products and services

HMDA / Regulation C Amendments New 1003 Application January 2017 1Nations Direct Mortgage, LLC Mission Statement - To lead the third party residential mortgage industry by providing products and services

Gan-Aden of Colchester 385 South Main Street, Colchester

Paradise Agency, LLC Property Development & Management 151 Broadway P.O. Box 175 Colchester, Connecticut 06415 Phone: (860) 537-7044 Fax: (860) 537-1142 TDD/TT: 1-800-842-9710 Visit us at www.paradiseagency.com

Paradise Agency, LLC Property Development & Management 151 Broadway P.O. Box 175 Colchester, Connecticut 06415 Phone: (860) 537-7044 Fax: (860) 537-1142 TDD/TT: 1-800-842-9710 Visit us at www.paradiseagency.com

DISPARATE IMPACT S EFFECTS ON PRICING AND COMPENSATION

DISPARATE IMPACT S EFFECTS ON PRICING AND COMPENSATION Ari Karen Principal, Offit Kurman akaren@offitkurman.com 301-575-0340 Daniella Casseres Associate, Offit Kurman dcasseres@offitkurman.com 703-745-1811

DISPARATE IMPACT S EFFECTS ON PRICING AND COMPENSATION Ari Karen Principal, Offit Kurman akaren@offitkurman.com 301-575-0340 Daniella Casseres Associate, Offit Kurman dcasseres@offitkurman.com 703-745-1811

Welcome to Pine Grove Apartments. Thank you for your interest in our community.

PINE GROVE APARTMENTS 600 Carlton Rd., #111 Palmetto, Georgia 30268 Tel 770-463-2107 Fax 770-463-5952 TDD # 800-255-0135 Visit our website: apartmentspalmetto.com TO ALL PROSPECTIVE RESIDENTS: Welcome

PINE GROVE APARTMENTS 600 Carlton Rd., #111 Palmetto, Georgia 30268 Tel 770-463-2107 Fax 770-463-5952 TDD # 800-255-0135 Visit our website: apartmentspalmetto.com TO ALL PROSPECTIVE RESIDENTS: Welcome

MBBA-NH & MAMP. Compliance Conference. April 19, 2017

MBBA-NH & MAMP Compliance Conference April 19, 2017 Agenda HMDA Overview Readiness Steps HMDA Expansion Fields 2 New HMDA Rule Summary Changes to Home Mortgage Disclosure: Regulation C Types of institutions

MBBA-NH & MAMP Compliance Conference April 19, 2017 Agenda HMDA Overview Readiness Steps HMDA Expansion Fields 2 New HMDA Rule Summary Changes to Home Mortgage Disclosure: Regulation C Types of institutions

Federal Reserve System Primary Market Secondary Market

Chapter 14: Real Estate Financing: Practices Introduction to the Real Estate Financing Market Federal Reserve System Primary Market Secondary Market Federal Reserve System Role Maintain sound credit conditions

Chapter 14: Real Estate Financing: Practices Introduction to the Real Estate Financing Market Federal Reserve System Primary Market Secondary Market Federal Reserve System Role Maintain sound credit conditions

HMDA: Haven or Havoc. Cindy Prince, Presenter December 5, 6 & 7, 2017 Assisted by Rachelle Dekker and Matt Goble

HMDA: Haven or Havoc Cindy Prince, Presenter December 5, 6 & 7, 2017 Assisted by Rachelle Dekker and Matt Goble Recap Day One 2 1. Annual expectations 2. Two proposals and a new final rule 3. Key definitions

HMDA: Haven or Havoc Cindy Prince, Presenter December 5, 6 & 7, 2017 Assisted by Rachelle Dekker and Matt Goble Recap Day One 2 1. Annual expectations 2. Two proposals and a new final rule 3. Key definitions

CFPB Compliance Bulletin Date: July 31, 2017

1700 G Street NW, Washington, DC 20552 CFPB Compliance Bulletin 2017-01 Date: July 31, 2017 Subject: Phone Pay Fees The Consumer Financial Protection Bureau (CFPB or Bureau) issues this Compliance Bulletin

1700 G Street NW, Washington, DC 20552 CFPB Compliance Bulletin 2017-01 Date: July 31, 2017 Subject: Phone Pay Fees The Consumer Financial Protection Bureau (CFPB or Bureau) issues this Compliance Bulletin

Loan Originator Compensation and Steering Prohibitions. Branch Originations March 2011

Loan Originator Compensation and Steering Prohibitions Branch Originations March 2011 Regulation Z - Loan Originator Compensation Truth in Lending Act, Regulation Z amendments on loan originator compensation

Loan Originator Compensation and Steering Prohibitions Branch Originations March 2011 Regulation Z - Loan Originator Compensation Truth in Lending Act, Regulation Z amendments on loan originator compensation

Status of New Uniform Residential Loan Application and Collection of Expanded Home

BILLING CODE: 4810-AM-P BUREAU OF CONSUMER FINANCIAL PROTECTION Status of New Uniform Residential Loan Application and Collection of Expanded Home Mortgage Disclosure Act Information about Ethnicity and

BILLING CODE: 4810-AM-P BUREAU OF CONSUMER FINANCIAL PROTECTION Status of New Uniform Residential Loan Application and Collection of Expanded Home Mortgage Disclosure Act Information about Ethnicity and

Summary. October 2009

white paper FICO Successfully Defends Insurance Industry s Use of Credit The correlation between credit risk management patterns and insurance loss is statistically proven and helps insurers make faster,

white paper FICO Successfully Defends Insurance Industry s Use of Credit The correlation between credit risk management patterns and insurance loss is statistically proven and helps insurers make faster,

Fair Lending Risk Management: Lessons from Recent Settlements

November 2012 Fair Lending Risk Management: Lessons from Recent Settlements Introduction Fair lending continues to be a major enforcement priority of federal agencies, and the financial implications have

November 2012 Fair Lending Risk Management: Lessons from Recent Settlements Introduction Fair lending continues to be a major enforcement priority of federal agencies, and the financial implications have

Fair Lending Compliance Basics: Class is in Session!

Fair Lending Compliance Basics: Class is in Session! How to Control Fair Lending Risk and Identify Redlining Risk Meet Your Teacher Kimberly Boatwright, CRCM, CAMS Director of Compliance TRUPOINT Partners

Fair Lending Compliance Basics: Class is in Session! How to Control Fair Lending Risk and Identify Redlining Risk Meet Your Teacher Kimberly Boatwright, CRCM, CAMS Director of Compliance TRUPOINT Partners

Teresa Garcia, Mission Economic Development Agency

facilitate enforcement of fair lending laws and enable communities, governmental entities, and creditors to identify business and community development needs and opportunities of women owned, minority-owned,

facilitate enforcement of fair lending laws and enable communities, governmental entities, and creditors to identify business and community development needs and opportunities of women owned, minority-owned,

July 31, :30PM to 2:30PM CDT. Fair Lending: Can You Make Exceptions?

July 31, 2018 1:30PM to 2:30PM CDT Fair Lending: Can You Make Exceptions? Options to Join Webinar and audio Click on the link: Fair Lending Webcast Connect to audio Call Using Computer (preferred method):

July 31, 2018 1:30PM to 2:30PM CDT Fair Lending: Can You Make Exceptions? Options to Join Webinar and audio Click on the link: Fair Lending Webcast Connect to audio Call Using Computer (preferred method):

DEMOGRAPHICS OF PAYDAY LENDING IN OKLAHOMA

October 2014 DEMOGRAPHICS OF PAYDAY LENDING IN OKLAHOMA Report Prepared for the Oklahoma Assets Network by Haydar Kurban Adji Fatou Diagne 0 This report was prepared for the Oklahoma Assets Network by

October 2014 DEMOGRAPHICS OF PAYDAY LENDING IN OKLAHOMA Report Prepared for the Oklahoma Assets Network by Haydar Kurban Adji Fatou Diagne 0 This report was prepared for the Oklahoma Assets Network by

Chapter 15 Real Estate Financing: Practice

Chapter 15 Real Estate Financing: Practice LECTURE OUTLINE: I. Introduction to the Real Estate Financing Market A. Federal Reserve System 1. Created to help maintain sound credit conditions 2. Helps counteract

Chapter 15 Real Estate Financing: Practice LECTURE OUTLINE: I. Introduction to the Real Estate Financing Market A. Federal Reserve System 1. Created to help maintain sound credit conditions 2. Helps counteract

Is There Such a Thing as Legal Credit Repair?

Is There Such a Thing as Legal Credit Repair? Not only does the legal credit repair process work for errors but can also help remove "unverifiable" negative, yet accurate, information. Credit Laws Fair

Is There Such a Thing as Legal Credit Repair? Not only does the legal credit repair process work for errors but can also help remove "unverifiable" negative, yet accurate, information. Credit Laws Fair

Proposed Rules and Comment Due Dates

Proposed Rules and Comment Due Dates Agency Proposed Rule Federal Register Publication Date and Page Number Comment Due Date Bureau of Consumer Financial Protection (CFPB) Prototypes of New Overdraft Opt-

Proposed Rules and Comment Due Dates Agency Proposed Rule Federal Register Publication Date and Page Number Comment Due Date Bureau of Consumer Financial Protection (CFPB) Prototypes of New Overdraft Opt-

Credit Card Default Predictive Modeling

Credit Card Default Predictive Modeling Background: Predicting credit card payment default is critical for the successful business model of a credit card company. An accurate predictive model can help

Credit Card Default Predictive Modeling Background: Predicting credit card payment default is critical for the successful business model of a credit card company. An accurate predictive model can help

SALARY EQUITY ANALYSIS AT ARL INSTITUTIONS

SALARY EQUITY ANALYSIS AT ARL INSTITUTIONS Quinn Galbraith, MSS & MLS - Sociology and Family Life Librarian, ARL Visiting Program Officer Michael Groesbeck, BS - Statistician Brigham R. Frandsen, PhD -

SALARY EQUITY ANALYSIS AT ARL INSTITUTIONS Quinn Galbraith, MSS & MLS - Sociology and Family Life Librarian, ARL Visiting Program Officer Michael Groesbeck, BS - Statistician Brigham R. Frandsen, PhD -

Trendspotting the CFPB: What s Coming and How Institutions Can Prepare

Trendspotting the CFPB: What s Coming and How Institutions Can Prepare Courtney H. Gilmer Baker Donelson Center Suite 800 211 Commerce Street Nashville, TN 37201 615.726.5747 cgilmer@bakerdonelson.com

Trendspotting the CFPB: What s Coming and How Institutions Can Prepare Courtney H. Gilmer Baker Donelson Center Suite 800 211 Commerce Street Nashville, TN 37201 615.726.5747 cgilmer@bakerdonelson.com

Please stand by, the presentation will begin shortly. Your phones have been muted. If you re using the speakers on your PC you don t need to call in.

Please stand by, the presentation will begin shortly. Your phones have been muted. If you re using the speakers on your PC you don t need to call in. While you are waiting, you may download the presentation

Please stand by, the presentation will begin shortly. Your phones have been muted. If you re using the speakers on your PC you don t need to call in. While you are waiting, you may download the presentation

How Cities Can Pursue Responsible Banking: Model Local Responsible Banking Ordinance Creates Community Reinvestment Requirements for Financial

How Cities Can Pursue Responsible Banking: Model Local Responsible Banking Ordinance Creates Community Reinvestment Requirements for Financial Institutions JULY 2012 How Cities Can Pursue Responsible Banking:

How Cities Can Pursue Responsible Banking: Model Local Responsible Banking Ordinance Creates Community Reinvestment Requirements for Financial Institutions JULY 2012 How Cities Can Pursue Responsible Banking:

Lending Audit. Chapter 8. Introduction. Laws and Regulations Covered by the Audit

Chapter 8 Introduction Auditing the lending functions of the bank for compliance with federal regulations can be an intimidating job. In general, the laws and regulations that deal with the lending function

Chapter 8 Introduction Auditing the lending functions of the bank for compliance with federal regulations can be an intimidating job. In general, the laws and regulations that deal with the lending function

Fair Lending THIS PUBLICATION IS. counsel for advice on specific fact situations. Copyrighted by Compliance Resource, LLC, April 2017

Fair Lending THIS PUBLICATION IS Not offered as legal advice SO Readers should consult with legal counsel for advice on specific fact situations. Copyrighted by Compliance Resource, LLC, April 2017 No

Fair Lending THIS PUBLICATION IS Not offered as legal advice SO Readers should consult with legal counsel for advice on specific fact situations. Copyrighted by Compliance Resource, LLC, April 2017 No

Home Mortgage Disclosure Act 2017, 2018, and Beyond. Presented by Marissa Blundell Bankers Advisory A CliftonLarsonAllen LLP Division

Home Mortgage Disclosure Act 2017, 2018, and Beyond Presented by Marissa Blundell Bankers Advisory A CliftonLarsonAllen LLP Division Home Mortgage Disclosure Act (HMDA) Consumer Financial Protection Bureau

Home Mortgage Disclosure Act 2017, 2018, and Beyond Presented by Marissa Blundell Bankers Advisory A CliftonLarsonAllen LLP Division Home Mortgage Disclosure Act (HMDA) Consumer Financial Protection Bureau

The Illinois Illinois Department Department of Human Human Rights

The Illinois Department of Human Rights presents To secure for all individuals id within the State t of Illinois, i freedom from unlawful discrimination or sexual harassment in employment and in education.

The Illinois Department of Human Rights presents To secure for all individuals id within the State t of Illinois, i freedom from unlawful discrimination or sexual harassment in employment and in education.

HMDA 2018 IMPLEMENTATION PLANNING. HMDA Process Inventory

Affected Products Application Methods (Face to face (online, paper), Mail, Online, Telephone, Fax HMDA Process Inventory Demographic Data Gathering Methods LAR Software Used or Manual LAR Preparation Responsible

Affected Products Application Methods (Face to face (online, paper), Mail, Online, Telephone, Fax HMDA Process Inventory Demographic Data Gathering Methods LAR Software Used or Manual LAR Preparation Responsible

Fair lending report of the Consumer Financial Protection Bureau

Fair lending report of the Consumer Financial Protection Bureau April 2014 Message from Richard Cordray Director of the CFPB From the moment we first opened our doors, the Consumer Financial Protection

Fair lending report of the Consumer Financial Protection Bureau April 2014 Message from Richard Cordray Director of the CFPB From the moment we first opened our doors, the Consumer Financial Protection

New Jersey Bankers Association 2017 Compliance University Fair Lending Redlining Risks

New Jersey Bankers Association 2017 Compliance University Fair Lending Redlining Risks June 14, 2017 Presented by Rose N. Egbuiwe, Fair Lending Examination Specialist 1 Objectives Provide Insight on Fair

New Jersey Bankers Association 2017 Compliance University Fair Lending Redlining Risks June 14, 2017 Presented by Rose N. Egbuiwe, Fair Lending Examination Specialist 1 Objectives Provide Insight on Fair

CIT Group Accused of Redlining and Violating Fair Housing Act

November 17, 2016 Contact: Kevin Stein (415) 864-3980 Caroline Peattie: (415) 457-5025 (Ext. 106) CIT Group Accused of Redlining and Violating Fair Housing Act CALIFORNIA REINVESTMENT COALITION AND FAIR

November 17, 2016 Contact: Kevin Stein (415) 864-3980 Caroline Peattie: (415) 457-5025 (Ext. 106) CIT Group Accused of Redlining and Violating Fair Housing Act CALIFORNIA REINVESTMENT COALITION AND FAIR

Sonia Lee Director of Affiliate Financial Services HFH International

Sonia Lee Director of Affiliate Financial Services HFH International Topics for Today Anti-Discrimination Laws Other Laws Outreach and Marketing Application Intake Selection Criteria Procedural Issues

Sonia Lee Director of Affiliate Financial Services HFH International Topics for Today Anti-Discrimination Laws Other Laws Outreach and Marketing Application Intake Selection Criteria Procedural Issues

Regulatory Update OLA Fall Meeting. Suzanne Garwood

Regulatory Update OLA Fall Meeting Suzanne Garwood sgarwood@venable.com 202-344-8046 1 Regulated Issues Advertising Credit Denial Electronic Payments Customer Data Security 2 3 ADVERTISING Advertising

Regulatory Update OLA Fall Meeting Suzanne Garwood sgarwood@venable.com 202-344-8046 1 Regulated Issues Advertising Credit Denial Electronic Payments Customer Data Security 2 3 ADVERTISING Advertising

Advertising Compliance

Advertising Compliance John Zasada Principal 218 790 1086 1 1 Credit Union Compliance Practice Review websites and social media for compliance before CU release Ongoing Regulatory Compliance Assistance

Advertising Compliance John Zasada Principal 218 790 1086 1 1 Credit Union Compliance Practice Review websites and social media for compliance before CU release Ongoing Regulatory Compliance Assistance

Anand S. Raman Bank Counsel Conference. November 13, Skadden

Fair Lending Update Anand S. Raman Louisiana Bankers Association 2008 Bank Counsel Conference November 13, 2008 Loan Modification Becomes Central Focus FDIC IndyMac plan Massachusetts AG action against

Fair Lending Update Anand S. Raman Louisiana Bankers Association 2008 Bank Counsel Conference November 13, 2008 Loan Modification Becomes Central Focus FDIC IndyMac plan Massachusetts AG action against

A Nation of Renters? Promoting Homeownership Post-Crisis. Roberto G. Quercia Kevin A. Park

A Nation of Renters? Promoting Homeownership Post-Crisis Roberto G. Quercia Kevin A. Park 2 Outline of Presentation Why homeownership? The scale of the foreclosure crisis today (20112Q) Mississippi and

A Nation of Renters? Promoting Homeownership Post-Crisis Roberto G. Quercia Kevin A. Park 2 Outline of Presentation Why homeownership? The scale of the foreclosure crisis today (20112Q) Mississippi and

2018 HMDA Implementation. Presented By: Karen Ruckle, Director of Compliance Bank of the Ozarks

2018 HMDA Implementation Presented By: Karen Ruckle, Director of Compliance Bank of the Ozarks 2018 HMDA Loan Volume Test # Loans #Loans #Loans Home Purchase Or Refi (Dwelling Secured) in prior calendar

2018 HMDA Implementation Presented By: Karen Ruckle, Director of Compliance Bank of the Ozarks 2018 HMDA Loan Volume Test # Loans #Loans #Loans Home Purchase Or Refi (Dwelling Secured) in prior calendar

New and Re-emerging Fair Lending Risks. Article by Austin Brown & Loretta Kirkwood October 2014

New and Re-emerging Fair Lending Risks Article by Austin Brown & Loretta Kirkwood BY AUSTIN BROWN & LORETTA KIRKWOOD Austin Brown Loretta Kirkwood Regulators have been focused recently on several new and

New and Re-emerging Fair Lending Risks Article by Austin Brown & Loretta Kirkwood BY AUSTIN BROWN & LORETTA KIRKWOOD Austin Brown Loretta Kirkwood Regulators have been focused recently on several new and

We are excited that you have chosen Habitat for Humanity Saint Louis as your partner in your journey towards owning your own home!

We are excited that you have chosen Habitat for Humanity Saint Louis as your partner in your journey towards owning your own home! The first step in the application process is to complete a pre-screen

We are excited that you have chosen Habitat for Humanity Saint Louis as your partner in your journey towards owning your own home! The first step in the application process is to complete a pre-screen

HMDA Regulations and New 1003 Application - Part 2

HMDA Regulations and New 1003 Application - Part 2 Broker / Correspondent Training May 10 & 12, 2017 1Nations Direct Mortgage Agenda Overview of New Regulations New and Modified HMDA Data Fields Detail

HMDA Regulations and New 1003 Application - Part 2 Broker / Correspondent Training May 10 & 12, 2017 1Nations Direct Mortgage Agenda Overview of New Regulations New and Modified HMDA Data Fields Detail

SAMPLE. 1 Bank Secrecy Act / Anti-Money Laundering. 2 E-Sign Act / Electronic Funds Transfer Act

1 Bank Secrecy Act / Anti-Money Laundering Summary 1 1 Purpose and History of the BSA 1 1 General Requirements of the BSA/AML Compliance Program 1 3 Money Laundering Defined 1 4 BSA / AML Violations 1

1 Bank Secrecy Act / Anti-Money Laundering Summary 1 1 Purpose and History of the BSA 1 1 General Requirements of the BSA/AML Compliance Program 1 3 Money Laundering Defined 1 4 BSA / AML Violations 1

CFPB Consumer Laws and Regulations

Consumer Laws and Regulations Home Mortgage Disclosure Act 1 The Home Mortgage Disclosure Act () was enacted by the Congress in 1975 and is implemented by Regulation C (12 CFR Part 1003). 2 The period

Consumer Laws and Regulations Home Mortgage Disclosure Act 1 The Home Mortgage Disclosure Act () was enacted by the Congress in 1975 and is implemented by Regulation C (12 CFR Part 1003). 2 The period

Redlining. Evaluating Risk and Defending Claims. Melanie Brody Partner Mayer Brown

Redlining Evaluating Risk and Defending Claims Melanie Brody Partner Mayer Brown mbrody@mayerbrown.com Brian Clark Senior Manager Ernst & Young Brian.Clark@ey.com Speakers Melanie Brody Partner Mayer Brown

Redlining Evaluating Risk and Defending Claims Melanie Brody Partner Mayer Brown mbrody@mayerbrown.com Brian Clark Senior Manager Ernst & Young Brian.Clark@ey.com Speakers Melanie Brody Partner Mayer Brown

Action Taken. Boot Camp 360 Series Presented by Kimberly Lundquist

Action Taken Boot Camp 360 Series Presented by Kimberly Lundquist Action Taken During the Pre-Application Process, most of the laws pertaining to real estate lending will come into play. We must be careful

Action Taken Boot Camp 360 Series Presented by Kimberly Lundquist Action Taken During the Pre-Application Process, most of the laws pertaining to real estate lending will come into play. We must be careful

Home Mortgage Disclosure (Regulation C)

") October 2017 OMB Control No. 3170-0008 Home Mortgage Disclosure (Regulation C) Small Entity Compliance Guide Version Log The Bureau updates this guide on a periodic basis. Below is a version log noting

October 2017 OMB Control No. 3170-0008 Home Mortgage Disclosure (Regulation C) Small Entity Compliance Guide Version Log The Bureau updates this guide on a periodic basis. Below is a version log noting