DEMOGRAPHICS OF PAYDAY LENDING IN OKLAHOMA

|

|

|

- Hillary Reynolds

- 5 years ago

- Views:

Transcription

1 October 2014 DEMOGRAPHICS OF PAYDAY LENDING IN OKLAHOMA Report Prepared for the Oklahoma Assets Network by Haydar Kurban Adji Fatou Diagne 0

2 This report was prepared for the Oklahoma Assets Network by researchers at the Howard University Center on Race and Wealth, with generous support from the Ford Foundation Financial Assets Unit. The contents of this publication are solely the responsibility of the authors and do not reflect the views of the Howard University Center on Race and Wealth, Oklahoma Assets Network, or the Ford Foundation. October 2014 Howard University Center on Race and Wealth th Street, NW, Room 316 Washington, DC

3 TABLE OF CONTENTS 1. Executive Summary 2 2. Introduction 3 3. Methodology and Data 5 4. Findings and Analysis 7 5. Summary and Conclusion 28 References 29 1

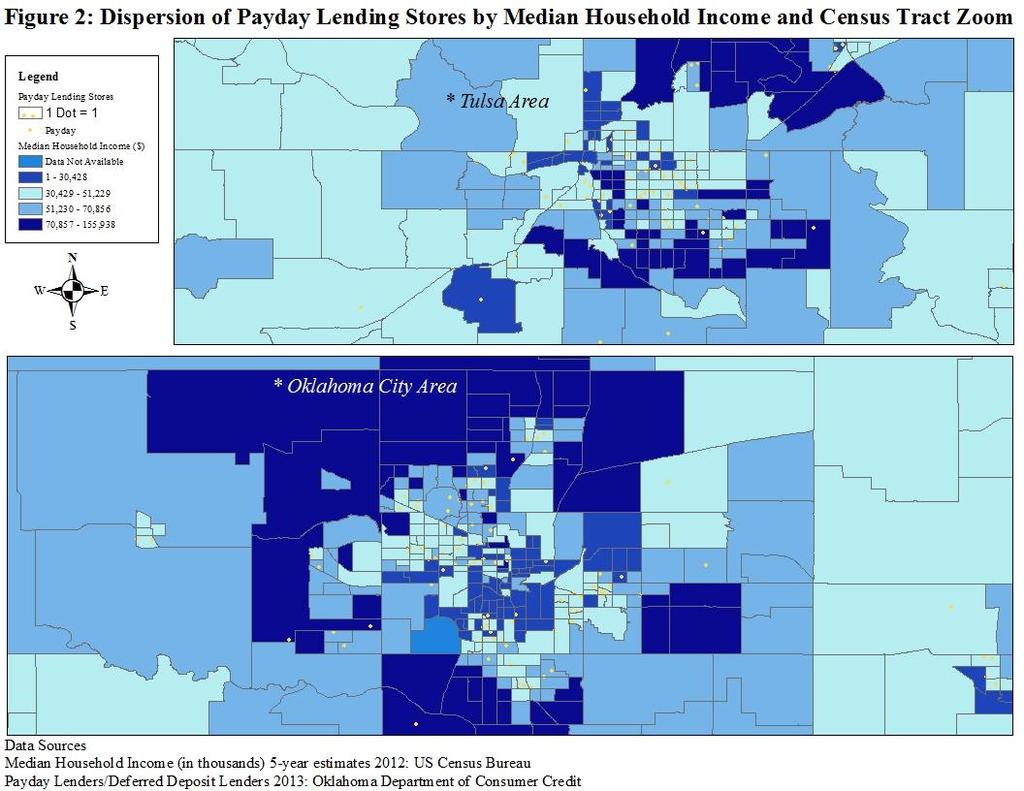

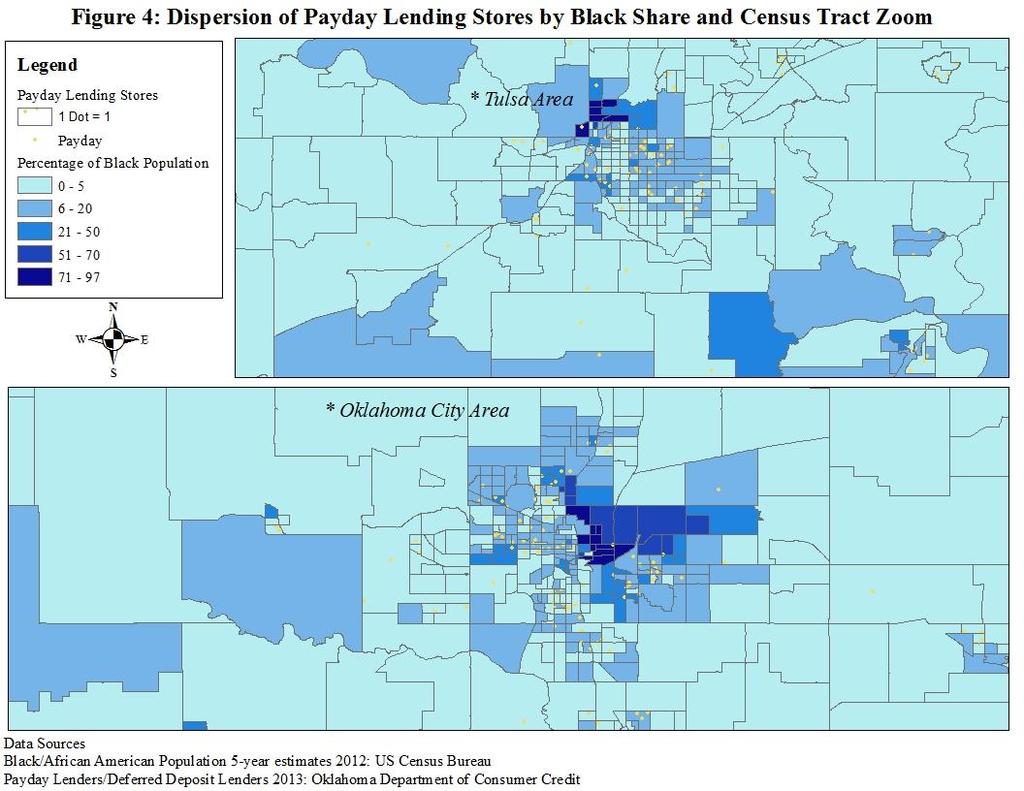

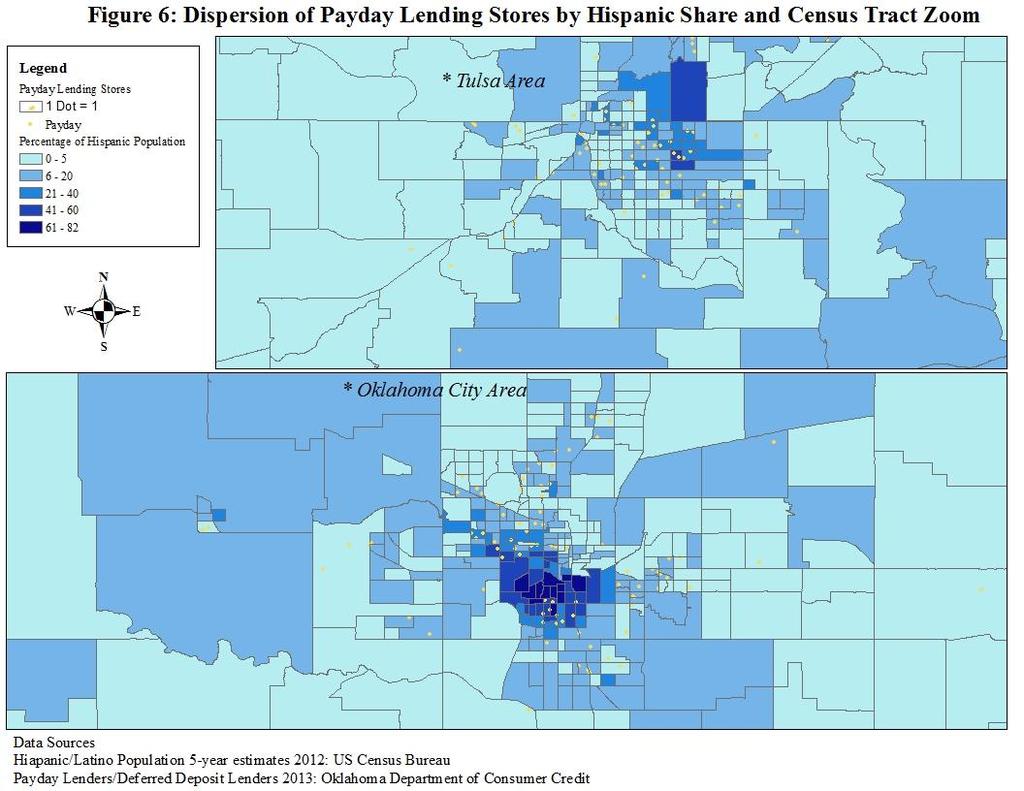

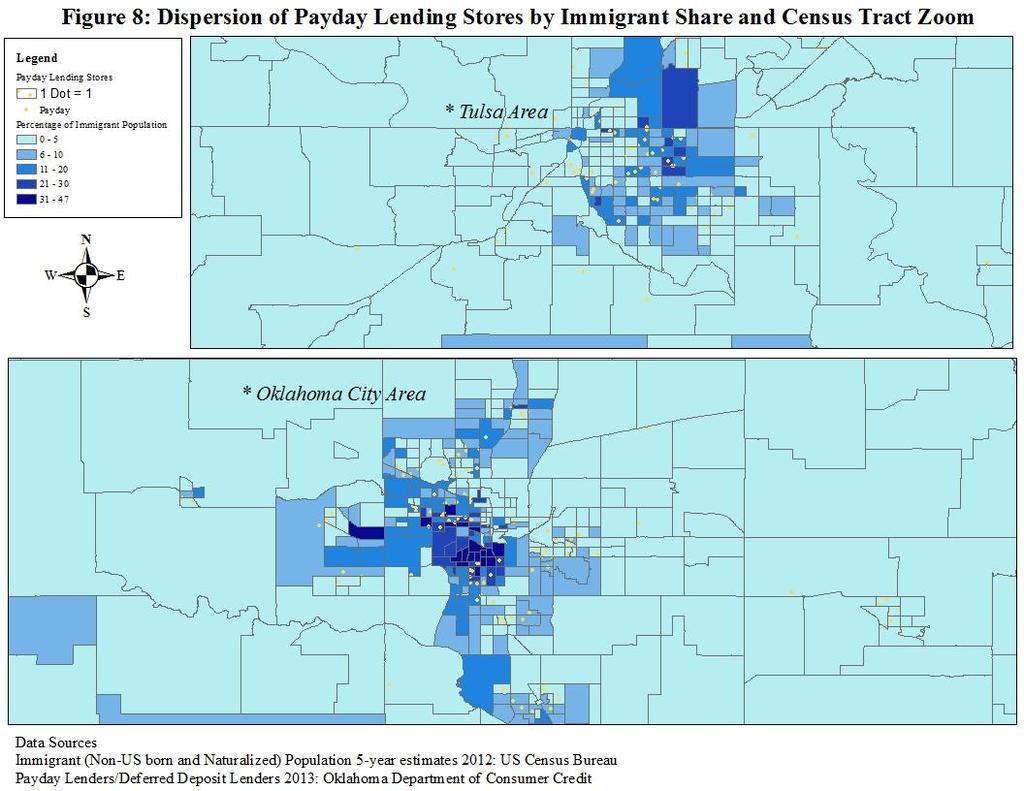

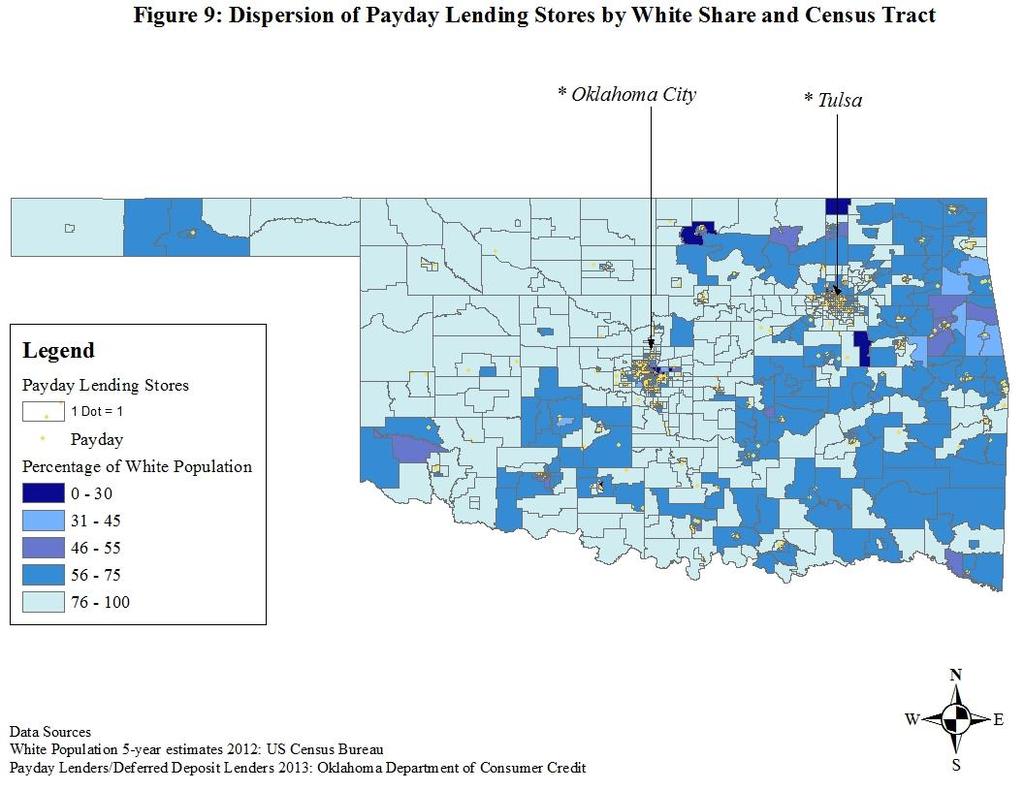

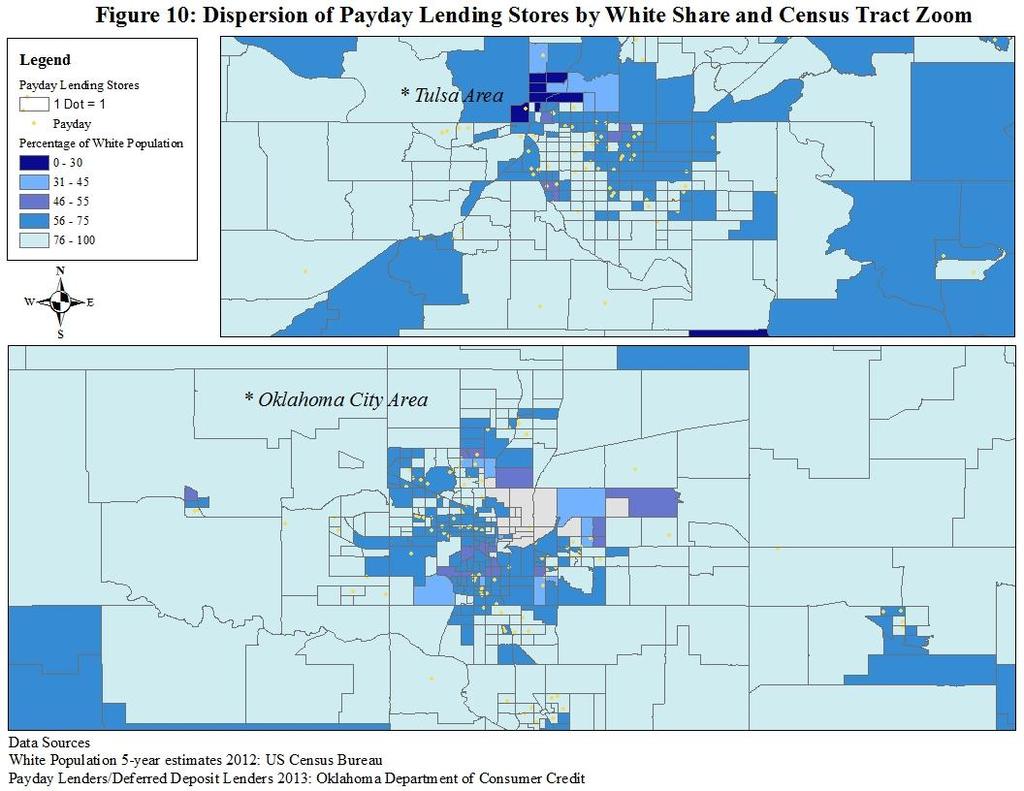

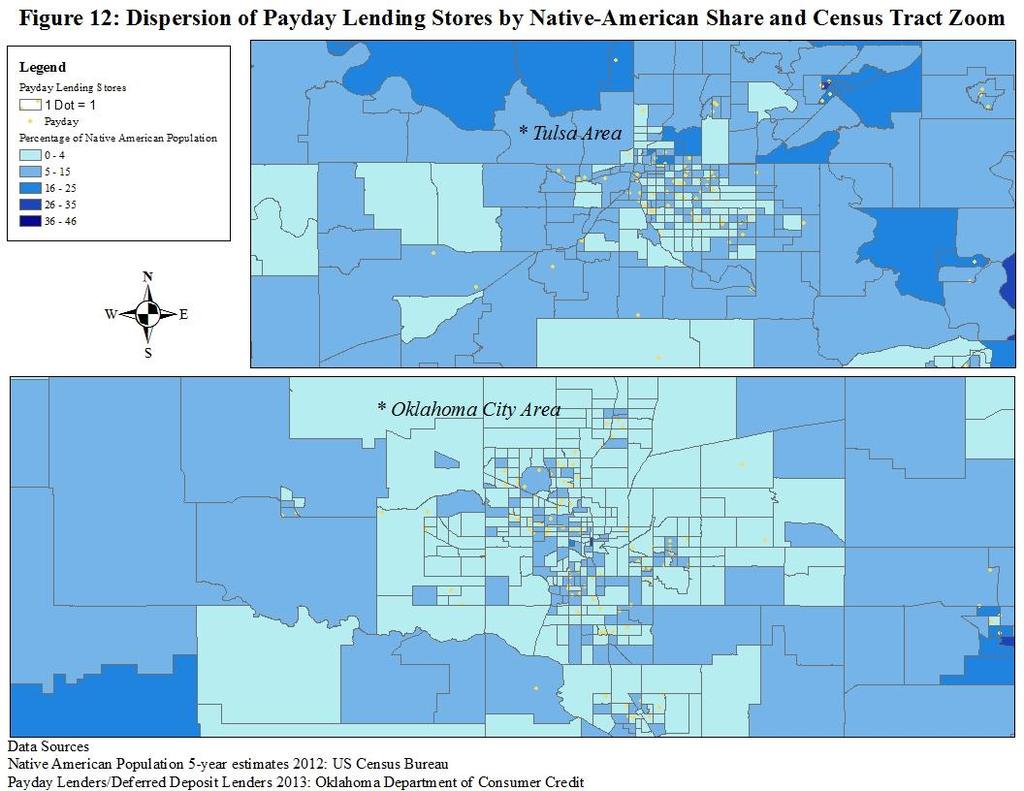

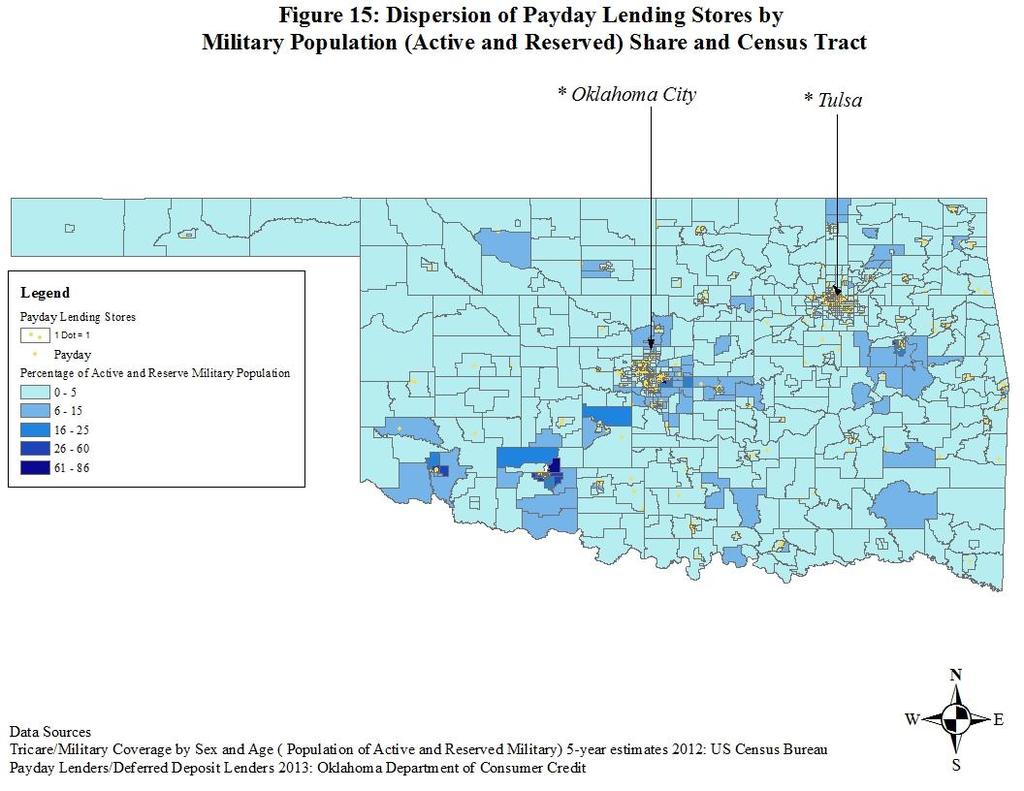

4 1. EXECUTIVE SUMMARY A recent report on the performance of Oklahoma s payday lending industry indicates that payday lenders charge consumers about 350 percent APR on a two-week loan in the state (Veritec, 2011). In 2011, the average payday loan was $ with an average fee of $ Given the 350 percent APR, payday loans in Oklahoma are more expensive than most traditional loans, including regular bank loans and mortgage loans. Because of its higher APR and other abusive practices, payday lending is characterized as a form of predatory lending (Graves and Peterson, 2005). Many studies have shown that payday lenders mostly target younger, lower income, and immigrant/minority populations (Gallmeyer and Roberts, 2009; Melzer, 2011; and Prager, 2009). The industry has also found a profitable customer base among military personnel (Graves and Peterson, 2005). Through high loan fees and other abusive tactics, the payday lending industry extracts a sizeable portion of disposable income and wealth from economically vulnerable communities. In this report, we identify the demographic and economic characteristics that attract payday lenders to communities. In addition, by using spatial research tools such as ArcGIS we were able to demonstrate that most of the payday lenders (199 out of 324) in Oklahoma are located within a 10-mile radius of military installations and bases. To determine the level of concentration of payday lenders around military installations, we spatially joined the national military installations and bases shape file and the census tract shape file of the state of Oklahoma. We then employed the means test and logistic regression methods to identify the demographic and economic factors that attract payday lenders to a neighborhood. Our results are summarized and presented in Tables 1-4 and Figures Tables 1-4 show that payday lenders target economically distressed communities in Oklahoma, specifically census tracts in which the population is largely elderly, young adults, immigrants and lower income. The means test, t-test and F-test employed in Tables 2 and 4 confirm that payday lenders target economically vulnerable communities in Oklahoma, and that the intensity of market penetration is even stronger in the census tracts around military installations and bases. The results in Tables 2-4 provide strong statistical evidence for the visual patterns in Figures These maps not only show that payday lenders are clustered in the census tracts populated mostly by economically vulnerable populations, but also that payday lending stores are more clustered around Oklahoma City and Tulsa. 2

5 2. INTRODUCTION A recent report on the performance of Oklahoma s payday lending industry indicates that payday lenders charge consumers about 350 percent APR on a two- week loan in the state (Veritec, 2011). In 2011, the average payday loan was $394.22, with an average fee of $ With a 350 percent APR, payday loans have become the most expensive loans on the market, much more expensive than traditional bank loans or mortgage loans. Because of its higher APR and other abusive practices, payday lending is characterized as a form of predatory lending (Graves and Peterson, 2005). As documented in the literature, payday lenders mostly target younger, lower income, and immigrant/minority populations (Gallmeyer and Roberts, 2009; Melzer, 2011; and Prager, 2009). The industry has also found a profitable customer base among military personnel (Graves and Peterson, 2005). The most recent report by the Oklahoma Department of Consumer Credit (OKDOCC) indicates that there were 324 in-state deferred deposit/payday lenders in Oklahoma in 2014 (see An earlier report (Veritec, 2011) showed that, in October 2011, there were 358 active and registered payday stores in Oklahoma. There is no reliable information on the total number of active payday lenders because a significant portion of payday lenders are unregistered and states do not regularly gather information even on the registered ones (Graves and Peterson, 2005). The emergence of online payday lenders has further complicated the issue. Our report is based on the data made available by the OKDOCC. Of the 324 payday lending stores in Oklahoma, 59 were located in Tulsa and 69 were located in Oklahoma City. Together these two large population centers accounted for nearly 40 percent (128 of 324) of the payday lending stores in the state. The literature has provided ample evidence that payday lenders target military personnel by opening shops around military installations (Graves and Peterson, 2005). By using the national military installations and bases shape file available from the U.S. Census Bureau, we have identified six military installations and bases in Oklahoma. Table 1 presents the number of payday lending stores within the 5-mile and 10-mile buffer zones around the six military installations and bases in Oklahoma. Of the 324 payday lending stores, 199 (61.4%) are located within the 10-mile buffer zone around the military installations and bases. Tinker AFB and Fort Sill have the highest number of payday lending stores within the 10-mile radius. 3

6 Table 1: Number of Payday Loan Stores 5-mile Buffer 10-mile Buffer Altus AFB 3 5 Camp Gruber 2 Ft Chaffee Maneuver Training Center 1 Ft Sill McAlester Army Ammunition Plant 6 Tinker AFB Vance AFB 4 7 Total Though the data show a concentration of payday lending stores around military installations, some military installations and bases, such as Tinker AFB, are also in the vicinity of large population centers. To control for the effect of population size, we use census tract population as an independent variable in our regression analysis. Payday lenders target certain population groups who are vulnerable because they either do not have access to regular banking services or they are misinformed about the terms and conditions of payday loans (Graves and Peterson, 2005). We employ a means test to determine whether census tracts with payday lenders differ from those without payday lenders based on income and other demographic factors. The remainder of the paper is organized as follows: Section 3 provides a description of the basic research methods and data used in the analyses. Section 4 presents the main findings of this report. Section 5 summarizes the findings and presents recommendations for future research. 4

7 3. METHODOLOGY AND DATA To study the demographic composition of census tracts with and without payday/deferred deposit lenders, we combined census tract level demographic and economic data from the U.S. Census Bureau with census tract level data on the location of payday lenders in Oklahoma. Specifically, we used year estimates of demographic and economic data from the American Community Survey. We obtained data on active payday lending stores from the Oklahoma Department of Consumer Credit (OKDOCC). The OKDOCC posted the addresses of the 324 in-state deferred deposit lenders on its website (see documents/ DDL-OK.pdf). Of the 1,046 census tracts in Oklahoma, only 226 had payday lenders. The number of payday lenders per census tract varied between 0 and 4. The data set on the number of payday lenders is incomplete because the number of active payday lenders is greater than the figure displayed by official statistics. The existence of unregistered payday lenders is well documented in the literature (Graves and Peterson, 2005). Since our data is limited to the registered payday lenders, our analysis is based on an incomplete list of payday lenders in Oklahoma. Payday lenders do not randomly select a place to operate. They target certain population groups who are vulnerable because they either do not have access to regular banking services or they are misinformed about the terms and conditions of payday loans (Graves and Peterson, 2005). The literature has provided ample evidence that payday lenders also target military personnel by opening shops around military installations (Graves and Peterson, 2005). We have created a new data set to investigate whether the census tracts around the military installations and bases have a higher concentration of payday lending stores. We retrieved the national military bases and installations shape file from the U.S. Census Bureau and created buffer zones of 5 miles and 10 miles around each base and installation in the state. Then we spatially joined this map with the census tract shape file map of Oklahoma. Our 5-mile and 10- mile buffers show the number of payday lending stores in each census tract within the buffer zone. We then were able to statistically test whether the census tracts within the buffer zones have a statistically different concentration of payday lenders than those that are away from military bases and installations. We used the means test to test whether the census tracts with payday lending stores differed from those without a payday lending store based on demographic and economic variables. We also employed the means test to investigate whether the census tracts closer to military installations and bases in Oklahoma have a higher concentration of payday lenders than those that are farther away. We then used the logistic regression method to investigate the relationship between various demographic and economic factors and the likelihood of attracting a pay day lender to a neighborhood. Since our 5

8 dependent variable takes a value of 0 and 1, the logistic regression method is more appropriate than an ordinary least squares (OLS) method. In addition to conducting statistical analysis, we created maps to spatially summarize and present our results (Figures 1-16). 6

9 4. FINDINGS AND ANALYSIS Table 2 presents the summary of our main variables for the 1,046 Oklahoma census tracts in On average, about 73 percent of the population was white, 6.7 percent was Native American, 9.19 percent was Hispanic, and 8.3 percent was black. On average, percent of households were female-headed, 4.09 percent of the population over 18 years old was covered by TRICARE or military health coverage, and percent of the total population was covered by TRICARE or military health coverage. About 6.9 percent (73) of the census tracts were within the 5-mile buffer zone of the military installations and bases and about 6.9 percent (199) were within the 10-mile buffer zone. About 21.6 percent (226) of the census tracts had at least one payday loan store. The average number of payday lending stores per population of 100,000 was about This latter variable measures the concentration of payday lending stores in a neighborhood. Table 2. Description of Main Variables Variable N Mean Standard Deviation Minimum Maximum Population # Payday White Share Black Share Native Am. Share Asian Share Hispanic Share Immigrant Share Payday Dummy Share Age Share Female HH TRICARE/Mil.Health Cov.Share, Within 5-mile Buffer TRICARE/Mil.Health Cov.Share, All Within 10-mile Buffer # Payday Store/100,000 pop

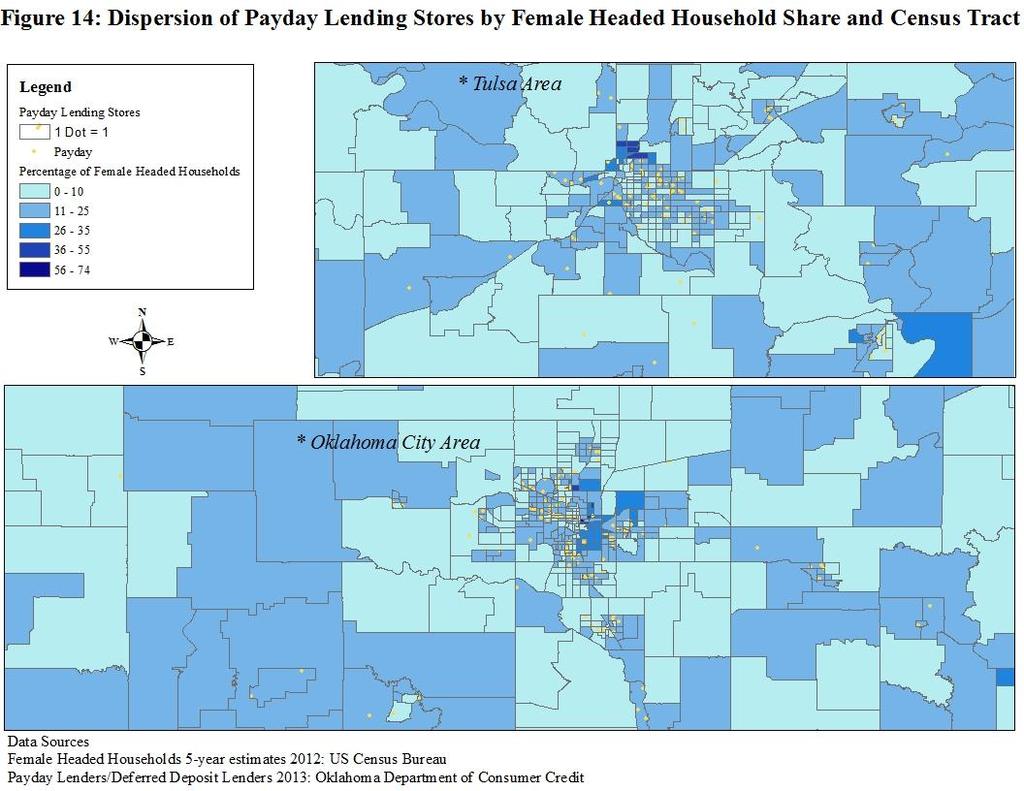

10 The means test statistics presented in Table 3 indicate that the census tracts with payday lending stores differ from those without payday lending stores based on income, immigrant population share, share of younger adults as household heads, and share of female-headed households. We also tested for whether the census tracts with payday lenders have different means than those without payday lenders along dimensions such as black population share, Hispanic population share, Native American population share and population share ages 60 or older, but we found statistically insignificant t-values which suggest that these variables do not play a role independent of other demographic variables such as immigrant share and femaleheaded household share in determining the location of payday stores. Our preliminary conclusion, based on the means test, is that the census tracts with at least one payday loan store differ from those without a payday loan store in terms of median income, immigrant population share, share of younger adults as household heads, and share of female-headed households. TABLE 3: MEANS TEST FOR CENSUS TRACTS WITH/WITHOUT PAYDAY LENDING STORE Census Tract (N) Median Income (Mean) Immigrant Share Household Head Age (20-29) Share Female Headed Household Share PAYDAY LENDER (NO =0) 818 $ 47, % 14.01% 12.10% PAYDAY LENDER (YES = 1) 226 $42, % 16.05% 13.87% diff = mean(0) - mean(1), diff = mean(0) - mean(1) diff = mean(0) - mean(1) diff = mean(0) - mean(1) t =3.56 t = t = t = P (means are not equal) = P (means are not equal) = P (means are not equal) = P (means are not equal) = As shown in Table 1, most of the payday loan stores are located within a 10-mile radius of military installations and bases in Oklahoma. We created an indicator of payday lending concentration by dividing the number of payday loan stores by census tract level population. 8

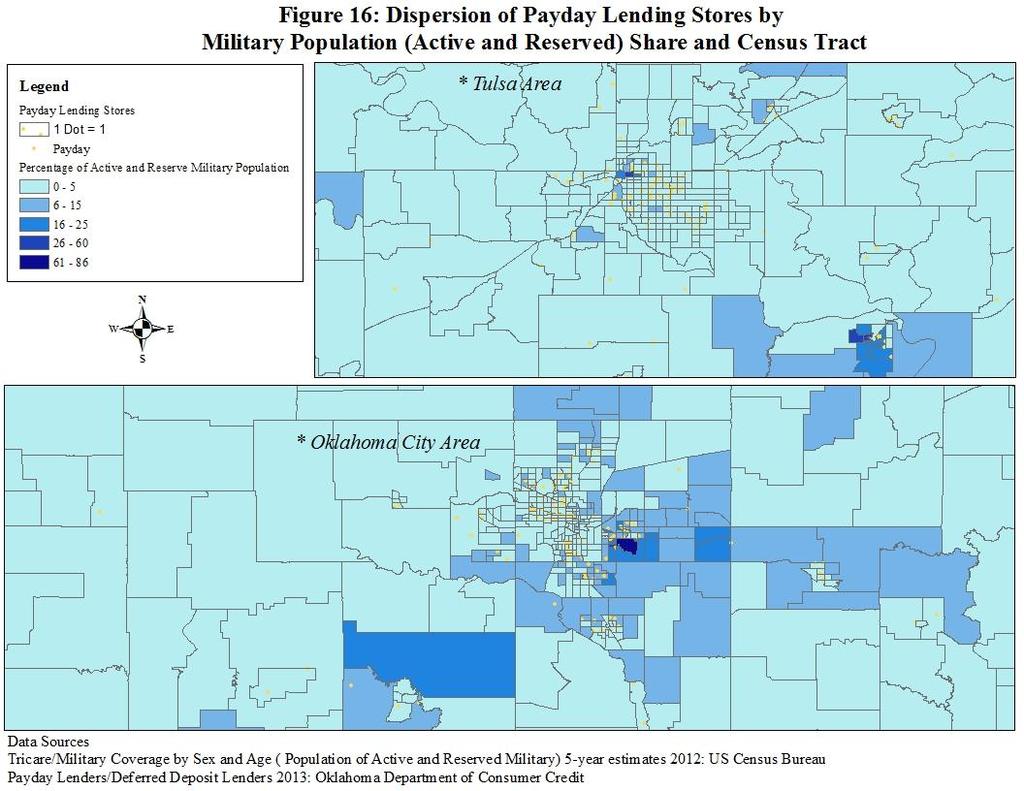

11 We then multiplied this by 100,000 to find the number of payday loan stores per population of 100,000. (This variable has been used in the literature to measure the variation in concentration or penetration of the payday lending industry across neighborhoods.) We then employed the means test to investigate whether the census tracts within a 10-mile radius of military installations and bases differ in terms of the number of payday loan stores per 100,000. We found that there was an average of payday loan stores per 100,000 in the census tracts within the 10-mile buffer zones and 8.41 in the census tracts that were away from the 10- mile buffer zones. The t-value that tests for the differences in the two mean values was -2.04, and significant at the 5 percent level. Therefore, we can conclude that the census tracts within a 10-mile radius zone had a higher concentration of payday loan stores than those that were farther away. Figures 1-16 illustrate the number of payday loan stores against census tract level demographic and economic variables. The concentration of payday loan stores in lower income and immigrant neighborhoods is more visually clear in Tulsa and Oklahoma City. Figures 1-16 also show the higher concentration of payday loan stores in Oklahoma City and Tulsa. To determine the factors that increase or decrease the likelihood of attracting a payday lender to a census tract, we employ regression analysis. Since our dependent variable (payday lender) takes a value of 0 or 1, the Ordinary Least Squares (OLS) method is not appropriate. Instead, we use the logistic regression method in which the estimated regression coefficients measure whether the independent variables are positively or negatively related to the likelihood of attracting a payday lender. Additionally, we can control for correlations among the independent variables. For example, some military bases are located in higher population areas. To control for the population effect, we include census tract level population as a control variable in our regressions. Similarly, the median household income and the population share of female-headed households are correlated. The estimated correlation coefficient is When we include both of these variables in the regression, the estimated coefficient of the logarithm of median household income became insignificant. The census tracts with a high share of female-headed households also tend to be lower income neighborhoods. Table 4 presents the results of our logistic regressions. The logistic regression results presented in Table 4 help us to identify the factors that attract payday lenders to a census tract. The results show that the likelihood of attracting a payday lending store to a community is positively related to the share of younger and older households. The logarithm of census tract population has a positive and significant coefficient which means that as the census tract population grows, it attracts more payday lenders. This variable also plays a control variable role for the within 5-mile or 10-mile buffer zone variables. The coefficient of the within 5-mile variable has 4 percent significance level. When we included 9

12 the within 10-mile buffer zone variable, we observed that this variable was also positively related to the dependent variable and it was significant at the 5 percent level. The positive and significant coefficients of the within 5-mile or 10-mile buffer zone variables indicate that payday lenders are attracted to the census tracts around the military installations not merely because some of them happen to be located in large population centers. Since we already include the logarithm of population as an independent variable, we can conclude that the industry targets these areas because it finds them more profitable. Graves and Peterson (2005) have also provided empirical support for this hypothesis. Table 4: Factors that Increase the Likelihood of Attracting Payday Lenders in Oklahoma (Logistic Regression Output) Logistic regression Number of observation= 1045 LR chi2(5) = Prob > chi2 = Log likelihood = Pseudo R2 = Probability Odds Standard z P> z (PaydayStore) Ratio Error. [95% Confidence Interval] Log pop age20-29 share andover share Immigrant share sharefemhh sharemillall Within 5-mile buffer Table 4 also shows that a rise in the share of older households (60 years and over) and younger households (ages years) increases the likelihood of the location of a payday lender. Similarly, an increase in the share of female headed households (sharefemhh) and the share of immigrant population increase the likelihood of a payday lending store locating in the area. We also added the share of population that receives TRICARE or military health benefit (sharemillall) as a proxy for the share of reserve, active and retired military personnel. The coefficient of this variable has a negative sign and the coefficient of within 5-mile or 10-mile buffer zone variable has positive sign. It appears that not all military related personnel are equally targeted by payday lenders. The positive and significant coefficients of within 5-mile 10

13 and 10-mile suggest that the industry targets civilian and military personnel around the bases. However, finding a better measure of the share of active military personnel is a challenge. By creating 5-mile or 10-mile buffers around military installations and bases we were able to document that payday lenders are disproportionately concentrated in the census tracts closer to military installations and bases in Oklahoma. We also included dummy variables for Tulsa and Oklahoma City in the logistic regressions. However, we did not obtain statistically significant coefficients for these variables. The higher concentration of payday lenders in Oklahoma City and Tulsa is attributable to the higher share of immigrant population, femaleheaded households, and younger and older households. Tables 1-4 show that payday lenders target economically distressed communities in Oklahoma. The census tracts with economically vulnerable populations (elderly, young adults, immigrants and lower income) are more likely to be targeted by payday lending stores. Figures 1-16 show that payday lenders are more clustered around Oklahoma City and Tulsa. We show that the relationship between the likelihood of attracting payday lenders and the share of economically vulnerable populations is statistically significant. Note that t-statistics for all independent variables have a significance level of 96 percent or higher. Table 4 further provides evidence that payday lenders more intensively target the neighborhoods with a higher percentage of economically vulnerable populations. The means test, t-test and F-test employed in Tables 2 and 4 confirm that payday lenders target economically vulnerable communities in Oklahoma and the intensity of market penetration is even stronger in the census tracts around military installations and bases. The results in Tables 2-4 provide statistical evidence for the visual patterns in Figures These maps also show that payday lenders are clustered in the census tracts populated mostly by economically vulnerable populations. 11

14 12

15 13

16 14

17 15

18 16

19 17

20 18

21 19

22 20

23 21

24 22

25 23

26 24

27 25

28 26

29 27

30 5. SUMMARY AND CONCLUSION Because of its higher APR and other abusive practices, payday lending has been characterized as a form of predatory lending (Graves and Peterson, 2005). Payday lenders mostly target younger, lower income, and immigrant/minority populations (Gallmeyer and Roberts, 2009; Melzer, 2011; and Prager, 2009). The industry also has found a profitable customer base among military personnel (Graves and Peterson, 2005). By using spatial research tools such as ArcGIS we were able to demonstrate that most of the payday lenders (199 of 324) in Oklahoma are located within a 10-mile radius of military installations and bases. We then employed the means test and logistic regression methods to identify the demographic and economic factors that attract payday lenders to a neighborhood. Our results show the census tracts with a higher concentration of economically vulnerable populations (elderly, young adults, immigrants and lower income) are more likely to be targeted by payday lending stores. Figures 1-16 show that payday lenders are more clustered around Oklahoma City and Tulsa. The means test, t-test and F-test employed in Tables 2 and 4 confirm that payday lenders target economically vulnerable communities in Oklahoma and the intensity of market penetration is even stronger in the census tracts around military installations and bases. In a way, the statistical tests employed in Tables 2-4 provide statistical evidence for the visual patterns in Figures To improve our results we need to find a better measure of the share of active military personnel at the census tract level. Our current proxy variable, obtained from the American Community Survey, measures the share of active, reserve and retired population that receives TRICARE and health benefits. As documented in the literature, payday lenders do not target active, reserve and retired military personnel with equal intensity. The demand for short term credit in economically disadvantaged communities attracts payday lenders. This demand can be met with loans that are more affordable for these communities. Credit unions and traditional banks should be encouraged to provide small dollar loans with affordable rates, and state and federal regulators must develop policies to prevent the abusive practices of the payday loan industry. 28

31 REFERENCES Applied Research and Consulting LLC Financial Capability in the United States: Initial Report of Research Findings from the 2009 National Survey. New York: Applied Research and Consulting LLC. Gallmeyer, Alice and Wade T. Roberts (2009). Payday lenders and economically distressed communities: A spatial analysis of financial predation. The Social Science Journal 46, Graves, Steven M. and Christopher L. Peterson (2005). Predatory Lending and the Military: The Law and Geography of Payday Loans in Military Towns. Ohio State Law Journal 66 (4), Meltzer, Brian T. (2011). The Real Costs of Credit Access: Evidence from the Payday Lending Market. The Quarterly Journal of Economics, 126, Prager, R. A Determinants of the Locations of Payday Lenders, Pawnshops, and Check-Cashing Outlets. Washington, DC: Federal Reserve Board. Veritec Oklahoma Trends in Deferred Deposit Lending Oklahoma Deferred Deposit Program March

32 ABOUT THE HOWARD UNIVERSITY CENTER ON RACE AND WEALTH The Howard University Center on Race and Wealth seeks to enrich the dialogue and research on asset building, wealth accumulation, and racial wealth disparities. As a resource grantee of the Ford Foundation Building Economic Security over a Lifetime initiative, the Center s goal is to provide ongoing technical assistance and research support to the Initiative s state and regional asset building coalition grantees in developing and promoting policies to reduce the wealth gap and build assets among low-income persons and in communities of color. ABOUT THE AUTHORS Haydar Kurban is a Research Associate of the Howard University Center on Race and Wealth and an associate professor in the Howard University Department of Economics. He joined Howard in August Dr. Kurban has worked on research projects in the areas of urban sprawl, gentrification, vulnerability of underinsured households in natural disasters, redistribution of education property taxes, and economic impacts of urban renewal programs. His research projects have been funded by NSF, HUD and DHS through awards and subcontracts, and his research papers have been published in academic journals and as book chapters, reports and discussion papers. Dr. Kurban received his Ph.D. in economics from the University of Illinois at Chicago. Adji Fatou Diagne is a doctoral student in the Howard University Department of Economics, and a Research Assistant at the Center on Race and Wealth. She has conducted research on housing issues, public transit, and poverty among women. She earned a M.A. in economics with a concentration in Urban Economics from Howard University in

THE ECONOMIC IMPACT OF PAYDAY LENDING IN ECONOMICALLY VULNERABLE COMMUNITIES

THE ECONOMIC IMPACT OF PAYDAY LENDING IN ECONOMICALLY VULNERABLE COMMUNITIES ALABAMA, FLORIDA, LOUISIANA, AND MISSISSIPPI HAYDAR KURBAN ADJI FATOU DIAGNE CHARLOTTE OTABOR DECEMBER 2014 This report was

THE ECONOMIC IMPACT OF PAYDAY LENDING IN ECONOMICALLY VULNERABLE COMMUNITIES ALABAMA, FLORIDA, LOUISIANA, AND MISSISSIPPI HAYDAR KURBAN ADJI FATOU DIAGNE CHARLOTTE OTABOR DECEMBER 2014 This report was

Mile High Money: Payday Stores Target Colorado Communities of Color

Mile High Money: Payday Stores Target Colorado Communities of Color Delvin Davis, Senior Researcher August 2017 (amended February 2018) Summary Findings: Majority minority areas in Colorado (over 50% African

Mile High Money: Payday Stores Target Colorado Communities of Color Delvin Davis, Senior Researcher August 2017 (amended February 2018) Summary Findings: Majority minority areas in Colorado (over 50% African

THE ECONOMIC IMPACTS OF PAYDAY LOANS IN AL, FL, LA & MS

THE ECONOMIC IMPACTS OF PAYDAY LOANS IN AL, FL, LA & MS Presented by Haydar Kurban, Ph.D. Southern Regional Asset Building Coalition Conference New Orleans, LA September 25, 2014 RECENT STUDIES DOCUMENT

THE ECONOMIC IMPACTS OF PAYDAY LOANS IN AL, FL, LA & MS Presented by Haydar Kurban, Ph.D. Southern Regional Asset Building Coalition Conference New Orleans, LA September 25, 2014 RECENT STUDIES DOCUMENT

The current study builds on previous research to estimate the regional gap in

Summary 1 The current study builds on previous research to estimate the regional gap in state funding assistance between municipalities in South NJ compared to similar municipalities in Central and North

Summary 1 The current study builds on previous research to estimate the regional gap in state funding assistance between municipalities in South NJ compared to similar municipalities in Central and North

The High Cost of Segregation: Exploring the Relationship Between Racial Segregation and Subprime Lending

F u r m a n C e n t e r f o r r e a l e s t a t e & u r b a n p o l i c y N e w Y o r k U n i v e r s i t y s c h o o l o f l aw wa g n e r s c h o o l o f p u b l i c s e r v i c e n o v e m b e r 2 0

F u r m a n C e n t e r f o r r e a l e s t a t e & u r b a n p o l i c y N e w Y o r k U n i v e r s i t y s c h o o l o f l aw wa g n e r s c h o o l o f p u b l i c s e r v i c e n o v e m b e r 2 0

during the Financial Crisis

Minority borrowers, Subprime lending and Foreclosures during the Financial Crisis Stephen L Ross University of Connecticut The work presented is joint with Patrick Bayer, Fernando Ferreira and/or Yuan

Minority borrowers, Subprime lending and Foreclosures during the Financial Crisis Stephen L Ross University of Connecticut The work presented is joint with Patrick Bayer, Fernando Ferreira and/or Yuan

JSU Public Policy Student Symposium April 23,2014 Alan Branson Ph.D. Student Public Policy and Public Administration Program

DETERMINANTS OF PAYDAY LENDING LOCATIONS IN MISSISSIPPI JSU Public Policy Student Symposium April 23,2014 Alan Branson Ph.D. Student Public Policy and Public Administration Program Background on Payday

DETERMINANTS OF PAYDAY LENDING LOCATIONS IN MISSISSIPPI JSU Public Policy Student Symposium April 23,2014 Alan Branson Ph.D. Student Public Policy and Public Administration Program Background on Payday

COMMUNITY ADVANTAGE PANEL SURVEY: DATA COLLECTION UPDATE AND ANALYSIS OF PANEL ATTRITION

COMMUNITY ADVANTAGE PANEL SURVEY: DATA COLLECTION UPDATE AND ANALYSIS OF PANEL ATTRITION Technical Report: February 2012 By Sarah Riley HongYu Ru Mark Lindblad Roberto Quercia Center for Community Capital

COMMUNITY ADVANTAGE PANEL SURVEY: DATA COLLECTION UPDATE AND ANALYSIS OF PANEL ATTRITION Technical Report: February 2012 By Sarah Riley HongYu Ru Mark Lindblad Roberto Quercia Center for Community Capital

COMMUNITY ADVANTAGE PANEL SURVEY: DATA COLLECTION UPDATE AND ANALYSIS OF PANEL ATTRITION

COMMUNITY ADVANTAGE PANEL SURVEY: DATA COLLECTION UPDATE AND ANALYSIS OF PANEL ATTRITION Technical Report: February 2013 By Sarah Riley Qing Feng Mark Lindblad Roberto Quercia Center for Community Capital

COMMUNITY ADVANTAGE PANEL SURVEY: DATA COLLECTION UPDATE AND ANALYSIS OF PANEL ATTRITION Technical Report: February 2013 By Sarah Riley Qing Feng Mark Lindblad Roberto Quercia Center for Community Capital

Individual and Neighborhood Effects on FHA Mortgage Activity: Evidence from HMDA Data

JOURNAL OF HOUSING ECONOMICS 7, 343 376 (1998) ARTICLE NO. HE980238 Individual and Neighborhood Effects on FHA Mortgage Activity: Evidence from HMDA Data Zeynep Önder* Faculty of Business Administration,

JOURNAL OF HOUSING ECONOMICS 7, 343 376 (1998) ARTICLE NO. HE980238 Individual and Neighborhood Effects on FHA Mortgage Activity: Evidence from HMDA Data Zeynep Önder* Faculty of Business Administration,

COMMUNITY ADVANTAGE PANEL SURVEY: DATA COLLECTION UPDATE AND ANALYSIS OF PANEL ATTRITION

COMMUNITY ADVANTAGE PANEL SURVEY: DATA COLLECTION UPDATE AND ANALYSIS OF PANEL ATTRITION Technical Report: March 2011 By Sarah Riley HongYu Ru Mark Lindblad Roberto Quercia Center for Community Capital

COMMUNITY ADVANTAGE PANEL SURVEY: DATA COLLECTION UPDATE AND ANALYSIS OF PANEL ATTRITION Technical Report: March 2011 By Sarah Riley HongYu Ru Mark Lindblad Roberto Quercia Center for Community Capital

Health Insurance Coverage in Oklahoma: 2008

Health Insurance Coverage in Oklahoma: 2008 Results from the Oklahoma Health Care Insurance and Access Survey July 2009 The Oklahoma Health Care Authority (OHCA) contracted with the State Health Access

Health Insurance Coverage in Oklahoma: 2008 Results from the Oklahoma Health Care Insurance and Access Survey July 2009 The Oklahoma Health Care Authority (OHCA) contracted with the State Health Access

SB 17 Testimony: Committee on Commerce, Labor, and Energy

SB 17 Testimony: Committee on Commerce, Labor, and Energy Dr. Justin S Gardner, PhD Innovative Research and Analysis LLC Applied Research and Policy Institute Hello Senate Members of the Committee on Commerce,

SB 17 Testimony: Committee on Commerce, Labor, and Energy Dr. Justin S Gardner, PhD Innovative Research and Analysis LLC Applied Research and Policy Institute Hello Senate Members of the Committee on Commerce,

Efforts to Improve Homeownership Opportunities for Hispanics

Efforts to Improve Homeownership Opportunities for Hispanics Case Studies of Three Market Areas U.S. Department of Housing and Urban Development Office of Policy Development and Research Efforts to Improve

Efforts to Improve Homeownership Opportunities for Hispanics Case Studies of Three Market Areas U.S. Department of Housing and Urban Development Office of Policy Development and Research Efforts to Improve

Issue Brief. Sources of Health Insurance and Characteristics of the Uninsured: Analysis of the March 2007 Current Population Survey. No.

Issue Brief Sources of Health Insurance and Characteristics of the Uninsured: Analysis of the March 2007 Current Population Survey By Paul Fronstin, EBRI No. 310 October 2007 This Issue Brief provides

Issue Brief Sources of Health Insurance and Characteristics of the Uninsured: Analysis of the March 2007 Current Population Survey By Paul Fronstin, EBRI No. 310 October 2007 This Issue Brief provides

Does a Weak Social Fabric Fuel the Predatory Lending Industry? The Link Between Payday Lending Activity and Community Trust

Illinois State University ISU ReD: Research and edata Master's Theses - Economics Economics 9-2013 Does a Weak Social Fabric Fuel the Predatory Lending Industry? The Link Between Payday Lending Activity

Illinois State University ISU ReD: Research and edata Master's Theses - Economics Economics 9-2013 Does a Weak Social Fabric Fuel the Predatory Lending Industry? The Link Between Payday Lending Activity

SALARY EQUITY ANALYSIS AT ARL INSTITUTIONS

SALARY EQUITY ANALYSIS AT ARL INSTITUTIONS Quinn Galbraith, MSS & MLS - Sociology and Family Life Librarian, ARL Visiting Program Officer Michael Groesbeck, BS - Statistician Brigham R. Frandsen, PhD -

SALARY EQUITY ANALYSIS AT ARL INSTITUTIONS Quinn Galbraith, MSS & MLS - Sociology and Family Life Librarian, ARL Visiting Program Officer Michael Groesbeck, BS - Statistician Brigham R. Frandsen, PhD -

NORTH MINNEAPOLIS: INTRODUCTION

NORTH MINNEAPOLIS: INTRODUCTION This report is part of a larger collaborative between the Local Initiatives Support Corporation (LISC) and the Center for Urban and al Affairs (CURA) that addresses regional

NORTH MINNEAPOLIS: INTRODUCTION This report is part of a larger collaborative between the Local Initiatives Support Corporation (LISC) and the Center for Urban and al Affairs (CURA) that addresses regional

In Baltimore City today, 20% of households live in poverty, but more than half of the

Building Economic Opportunity in Baltimore: A Data Profile Baltimore Highlights In Baltimore City today, 20% of households live in poverty, but more than half of the city s population 55% is financially

Building Economic Opportunity in Baltimore: A Data Profile Baltimore Highlights In Baltimore City today, 20% of households live in poverty, but more than half of the city s population 55% is financially

Population & Demographic Analysis

Population & Demographic Analysis The United States Census Bureau conducts a nationwide census every ten years. This census compiles information relating to the socio-economic characteristics of the entire

Population & Demographic Analysis The United States Census Bureau conducts a nationwide census every ten years. This census compiles information relating to the socio-economic characteristics of the entire

One Industry s Risk is Another Community s Loss: The Impact of Clustered Mortgage Foreclosures on Neighborhood Property Values in Philadelphia

One Industry s Risk is Another Community s Loss: The Impact of Clustered Mortgage Foreclosures on Neighborhood Property Values in Philadelphia Presentation before the Federal Reserve Bank of Philadelphia

One Industry s Risk is Another Community s Loss: The Impact of Clustered Mortgage Foreclosures on Neighborhood Property Values in Philadelphia Presentation before the Federal Reserve Bank of Philadelphia

Profile of Virginia s Uninsured, 2014

Profile of Virginia s Uninsured, 2014 Michael Huntress Genevieve Kenney Nathaniel Anderson 2100 M Street NW Washington, D.C., 20037 Prepared for The Virginia Health Care Foundation 707 East Main Street,

Profile of Virginia s Uninsured, 2014 Michael Huntress Genevieve Kenney Nathaniel Anderson 2100 M Street NW Washington, D.C., 20037 Prepared for The Virginia Health Care Foundation 707 East Main Street,

How House Price Dynamics and Credit Constraints affect the Equity Extraction of Senior Homeowners

How House Price Dynamics and Credit Constraints affect the Equity Extraction of Senior Homeowners Stephanie Moulton, John Glenn College of Public Affairs, The Ohio State University Donald Haurin, Department

How House Price Dynamics and Credit Constraints affect the Equity Extraction of Senior Homeowners Stephanie Moulton, John Glenn College of Public Affairs, The Ohio State University Donald Haurin, Department

The Demographics of Wealth

Demographics and the Future of American Families The Demographics of Wealth May 13, 2015 William R. Emmons Bryan J. Noeth Center for Household Financial Stability Federal Reserve Bank of St. Louis William.R.Emmons@stls.frb.org

Demographics and the Future of American Families The Demographics of Wealth May 13, 2015 William R. Emmons Bryan J. Noeth Center for Household Financial Stability Federal Reserve Bank of St. Louis William.R.Emmons@stls.frb.org

Payday Lenders and the Military: A Study of Hampton Roads, Virginia

Payday Lenders and the Military: A Study of Hampton Roads, Virginia Karen J. Hastings Advisor: Gregory Thomas Pennsylvania State University Introduction Payday Lenders have long been identified as targeting

Payday Lenders and the Military: A Study of Hampton Roads, Virginia Karen J. Hastings Advisor: Gregory Thomas Pennsylvania State University Introduction Payday Lenders have long been identified as targeting

Table 1 Annual Median Income of Households by Age, Selected Years 1995 to Median Income in 2008 Dollars 1

Fact Sheet Income, Poverty, and Health Insurance Coverage of Older Americans, 2008 AARP Public Policy Institute Median household income and median family income in the United States declined significantly

Fact Sheet Income, Poverty, and Health Insurance Coverage of Older Americans, 2008 AARP Public Policy Institute Median household income and median family income in the United States declined significantly

The Demand for Risky Assets in Retirement Portfolios. Yoonkyung Yuh and Sherman D. Hanna

The Demand for Risky Assets in Retirement Portfolios Yoonkyung Yuh and Sherman D. Hanna 1. Introduction Asset allocation decisions in for retirement savings have become more important for individuals with

The Demand for Risky Assets in Retirement Portfolios Yoonkyung Yuh and Sherman D. Hanna 1. Introduction Asset allocation decisions in for retirement savings have become more important for individuals with

Poverty in the United Way Service Area

Poverty in the United Way Service Area Year 4 Update - 2014 The Institute for Urban Policy Research At The University of Texas at Dallas Poverty in the United Way Service Area Year 4 Update - 2014 Introduction

Poverty in the United Way Service Area Year 4 Update - 2014 The Institute for Urban Policy Research At The University of Texas at Dallas Poverty in the United Way Service Area Year 4 Update - 2014 Introduction

Kim Manturuk American Sociological Association Social Psychological Approaches to the Study of Mental Health

Linking Social Disorganization, Urban Homeownership, and Mental Health Kim Manturuk American Sociological Association Social Psychological Approaches to the Study of Mental Health 1 Preview of Findings

Linking Social Disorganization, Urban Homeownership, and Mental Health Kim Manturuk American Sociological Association Social Psychological Approaches to the Study of Mental Health 1 Preview of Findings

Health Insurance Coverage in 2013: Gains in Public Coverage Continue to Offset Loss of Private Insurance

Health Insurance Coverage in 2013: Gains in Public Coverage Continue to Offset Loss of Private Insurance Laura Skopec, John Holahan, and Megan McGrath Since the Great Recession peaked in 2010, the economic

Health Insurance Coverage in 2013: Gains in Public Coverage Continue to Offset Loss of Private Insurance Laura Skopec, John Holahan, and Megan McGrath Since the Great Recession peaked in 2010, the economic

Subprime Originations and Foreclosures in New York State: A Case Study of Nassau, Suffolk, and Westchester Counties.

Subprime Originations and Foreclosures in New York State: A Case Study of Nassau, Suffolk, and Westchester Counties Cambridge, MA Lexington, MA Hadley, MA Bethesda, MD Washington, DC Chicago, IL Cairo,

Subprime Originations and Foreclosures in New York State: A Case Study of Nassau, Suffolk, and Westchester Counties Cambridge, MA Lexington, MA Hadley, MA Bethesda, MD Washington, DC Chicago, IL Cairo,

Increasing homeownership among

Subprime Lending and Foreclosure in Hennepin and Ramsey Counties: An Empirical Analysis by Jeff Crump Increasing homeownership among low-income and minority communities is a major goal of housing policy

Subprime Lending and Foreclosure in Hennepin and Ramsey Counties: An Empirical Analysis by Jeff Crump Increasing homeownership among low-income and minority communities is a major goal of housing policy

Evaluating the BLS Labor Force projections to 2000

Evaluating the BLS Labor Force projections to 2000 Howard N Fullerton Jr. Bureau of Labor Statistics, Office of Occupational Statistics and Employment Projections Washington, DC 20212-0001 KEY WORDS: Population

Evaluating the BLS Labor Force projections to 2000 Howard N Fullerton Jr. Bureau of Labor Statistics, Office of Occupational Statistics and Employment Projections Washington, DC 20212-0001 KEY WORDS: Population

Overdraft Frequency and Payday Borrowing An analysis of characteristics associated with overdrafters

A brief from Feb 2015 Overdraft Frequency and Payday Borrowing An analysis of characteristics associated with overdrafters Overview According to an analysis of banks account data published by the Consumer

A brief from Feb 2015 Overdraft Frequency and Payday Borrowing An analysis of characteristics associated with overdrafters Overview According to an analysis of banks account data published by the Consumer

The Neighborhood Distribution of Subprime Mortgage Lending

The Neighborhood Distribution of Subprime Mortgage Lending Paul S. Calem Division of Research and Statistics Board of Governors of the Federal Reserve System Kevin Gillen The Wharton School University

The Neighborhood Distribution of Subprime Mortgage Lending Paul S. Calem Division of Research and Statistics Board of Governors of the Federal Reserve System Kevin Gillen The Wharton School University

Health Status, Health Insurance, and Health Services Utilization: 2001

Health Status, Health Insurance, and Health Services Utilization: 2001 Household Economic Studies Issued February 2006 P70-106 This report presents health service utilization rates by economic and demographic

Health Status, Health Insurance, and Health Services Utilization: 2001 Household Economic Studies Issued February 2006 P70-106 This report presents health service utilization rates by economic and demographic

Issue Brief No Sources of Health Insurance and Characteristics of the Uninsured: Analysis of the March 2005 Current Population Survey

Issue Brief No. 287 Sources of Health Insurance and Characteristics of the Uninsured: Analysis of the March 2005 Current Population Survey by Paul Fronstin, EBRI November 2005 This Issue Brief provides

Issue Brief No. 287 Sources of Health Insurance and Characteristics of the Uninsured: Analysis of the March 2005 Current Population Survey by Paul Fronstin, EBRI November 2005 This Issue Brief provides

Credit Research Center Seminar

Credit Research Center Seminar Ensuring Fair Lending: What Do We Know about Pricing in Mortgage Markets and What Will the New HMDA Data Fields Tell US? www.msb.edu/prog/crc March 14, 2005 Introduction

Credit Research Center Seminar Ensuring Fair Lending: What Do We Know about Pricing in Mortgage Markets and What Will the New HMDA Data Fields Tell US? www.msb.edu/prog/crc March 14, 2005 Introduction

Although several factors determine whether and how women use health

CHAPTER 3: WOMEN AND HEALTH INSURANCE COVERAGE Although several factors determine whether and how women use health care services, the importance of health coverage as a critical resource in promoting access

CHAPTER 3: WOMEN AND HEALTH INSURANCE COVERAGE Although several factors determine whether and how women use health care services, the importance of health coverage as a critical resource in promoting access

Financial Literacy and Financial Behavior among Young Adults: Evidence and Implications

Numeracy Advancing Education in Quantitative Literacy Volume 6 Issue 2 Article 5 7-1-2013 Financial Literacy and Financial Behavior among Young Adults: Evidence and Implications Carlo de Bassa Scheresberg

Numeracy Advancing Education in Quantitative Literacy Volume 6 Issue 2 Article 5 7-1-2013 Financial Literacy and Financial Behavior among Young Adults: Evidence and Implications Carlo de Bassa Scheresberg

Cumberland Comprehensive Plan - Demographics Element Town Council adopted August 2003, State adopted June 2004 II. DEMOGRAPHIC ANALYSIS

II. DEMOGRAPHIC ANALYSIS A. INTRODUCTION This demographic analysis establishes past trends and projects future population characteristics for the Town of Cumberland. It then explores the relationship of

II. DEMOGRAPHIC ANALYSIS A. INTRODUCTION This demographic analysis establishes past trends and projects future population characteristics for the Town of Cumberland. It then explores the relationship of

ONLINE APPENDIX. The Vulnerability of Minority Homeowners in the Housing Boom and Bust. Patrick Bayer Fernando Ferreira Stephen L Ross

ONLINE APPENDIX The Vulnerability of Minority Homeowners in the Housing Boom and Bust Patrick Bayer Fernando Ferreira Stephen L Ross Appendix A: Supplementary Tables for The Vulnerability of Minority Homeowners

ONLINE APPENDIX The Vulnerability of Minority Homeowners in the Housing Boom and Bust Patrick Bayer Fernando Ferreira Stephen L Ross Appendix A: Supplementary Tables for The Vulnerability of Minority Homeowners

Proportion of income 1 Hispanics may be of any race.

POLICY PAPER This report addresses how individuals from various racial and ethnic groups fare under the current Social Security system. It examines the relative importance of Social Security for these

POLICY PAPER This report addresses how individuals from various racial and ethnic groups fare under the current Social Security system. It examines the relative importance of Social Security for these

How Do Predatory Lending Laws Influence Mortgage Lending in Urban Areas? A Tale of Two Cities

How Do Predatory Lending Laws Influence Mortgage Lending in Urban Areas? A Tale of Two Cities Authors Keith D. Harvey and Peter J. Nigro Abstract This paper examines the effects of predatory lending laws

How Do Predatory Lending Laws Influence Mortgage Lending in Urban Areas? A Tale of Two Cities Authors Keith D. Harvey and Peter J. Nigro Abstract This paper examines the effects of predatory lending laws

The U.S. Gender Earnings Gap: A State- Level Analysis

The U.S. Gender Earnings Gap: A State- Level Analysis Christine L. Storrie November 2013 Abstract. Although the size of the earnings gap has decreased since women began entering the workforce in large

The U.S. Gender Earnings Gap: A State- Level Analysis Christine L. Storrie November 2013 Abstract. Although the size of the earnings gap has decreased since women began entering the workforce in large

TECHNICAL REPORT NO. 11 (5 TH EDITION) THE POPULATION OF SOUTHEASTERN WISCONSIN PRELIMINARY DRAFT SOUTHEASTERN WISCONSIN REGIONAL PLANNING COMMISSION

THE POPULATION OF SOUTHEASTERN WISCONSIN PRELIMINARY DRAFT SOUTHEASTERN WISCONSIN REGIONAL PLANNING COMMISSION") TECHNICAL REPORT NO. 11 (5 TH EDITION) THE POPULATION OF SOUTHEASTERN WISCONSIN PRELIMINARY DRAFT 208903 SOUTHEASTERN WISCONSIN REGIONAL PLANNING COMMISSION KRY/WJS/lgh 12/17/12 203905 SEWRPC Technical

TECHNICAL REPORT NO. 11 (5 TH EDITION) THE POPULATION OF SOUTHEASTERN WISCONSIN PRELIMINARY DRAFT 208903 SOUTHEASTERN WISCONSIN REGIONAL PLANNING COMMISSION KRY/WJS/lgh 12/17/12 203905 SEWRPC Technical

2016 Labor Market Profile

2016 Labor Market Profile Prepared by The Tyler Economic Development Council Tyler Area Sponsor June 2016 The ability to demonstrate a regions availability of talented workers has become a vital tool

2016 Labor Market Profile Prepared by The Tyler Economic Development Council Tyler Area Sponsor June 2016 The ability to demonstrate a regions availability of talented workers has become a vital tool

The Economic Downturn and Changes in Health Insurance Coverage, John Holahan & Arunabh Ghosh The Urban Institute September 2004

The Economic Downturn and Changes in Health Insurance Coverage, 2000-2003 John Holahan & Arunabh Ghosh The Urban Institute September 2004 Introduction On August 26, 2004 the Census released data on changes

The Economic Downturn and Changes in Health Insurance Coverage, 2000-2003 John Holahan & Arunabh Ghosh The Urban Institute September 2004 Introduction On August 26, 2004 the Census released data on changes

401(k) PLANS AND RACE

PLANS AND RACE") November 2009, Number 9-24 401(k) PLANS AND RACE By Alicia H. Munnell and Christopher Sullivan* Introduction Many data sources show a disparity among racial and ethnic groups regarding participation in

November 2009, Number 9-24 401(k) PLANS AND RACE By Alicia H. Munnell and Christopher Sullivan* Introduction Many data sources show a disparity among racial and ethnic groups regarding participation in

Percentage of foreclosures in the area is the ratio between the monthly foreclosures and the number of outstanding home-related loans in the Zip code

Data Appendix A. Survey design In this paper we use 8 waves of the FTIS - the Chicago Booth Kellogg School Financial Trust Index survey (see http://financialtrustindex.org). The FTIS is 1,000 interviews,

Data Appendix A. Survey design In this paper we use 8 waves of the FTIS - the Chicago Booth Kellogg School Financial Trust Index survey (see http://financialtrustindex.org). The FTIS is 1,000 interviews,

Urban Action Agenda Community Profiles COVER TO GO HERE. City of Beacon

Urban Action Agenda Community Profiles COVER TO GO HERE City of Beacon COMMUNITY OVERVIEW MAP POPULATION & DEMOGRAPHICS Population Basics 2,212 Population (2015) Population Change 2. since 2000 0.5 Square

Urban Action Agenda Community Profiles COVER TO GO HERE City of Beacon COMMUNITY OVERVIEW MAP POPULATION & DEMOGRAPHICS Population Basics 2,212 Population (2015) Population Change 2. since 2000 0.5 Square

Population in the U.S. Floodplains

D ATA B R I E F D E C E M B E R 2 0 1 7 Population in the U.S. Floodplains Population in the U.S. Floodplains As sea levels rise due to climate change, planners and policymakers in flood-prone areas must

D ATA B R I E F D E C E M B E R 2 0 1 7 Population in the U.S. Floodplains Population in the U.S. Floodplains As sea levels rise due to climate change, planners and policymakers in flood-prone areas must

The Determinants of Planned Retirement Age

The Determinants of Planned Retirement Age Lishu Zhang, Ph.D. student, Consumer Sciences Department, Ohio State University, 1787 Neil Ave., Columbus, OH 43210. e-mail: lishu.zhang@yahoo.com Sherman D.

The Determinants of Planned Retirement Age Lishu Zhang, Ph.D. student, Consumer Sciences Department, Ohio State University, 1787 Neil Ave., Columbus, OH 43210. e-mail: lishu.zhang@yahoo.com Sherman D.

Import Competition and Household Debt

Import Competition and Household Debt Barrot (MIT) Plosser (NY Fed) Loualiche (MIT) Sauvagnat (Bocconi) USC Spring 2017 The views expressed in this paper are those of the authors and do not necessarily

Import Competition and Household Debt Barrot (MIT) Plosser (NY Fed) Loualiche (MIT) Sauvagnat (Bocconi) USC Spring 2017 The views expressed in this paper are those of the authors and do not necessarily

Payday Lenders and the Military: A Study of Hampton Roads, Virginia Karen J. Hastings

Payday Lenders and the Military: A Study of Hampton Roads, Virginia Karen J. Hastings Executive Summary Payday lenders have long been identified as targeting military populations. In the last ten years,

Payday Lenders and the Military: A Study of Hampton Roads, Virginia Karen J. Hastings Executive Summary Payday lenders have long been identified as targeting military populations. In the last ten years,

Older Households : Projections and Implications for Housing A Growing Population

Older Households 215-235: Projections and Implications for Housing A Growing Population Jennifer Molinsky February 15, 217 Setting the Stage: HOUSEHOLD GROWTH AMONG OLDER ADULTS 2 The Older Adult Population

Older Households 215-235: Projections and Implications for Housing A Growing Population Jennifer Molinsky February 15, 217 Setting the Stage: HOUSEHOLD GROWTH AMONG OLDER ADULTS 2 The Older Adult Population

Wealth Inequality Reading Summary by Danqing Yin, Oct 8, 2018

Summary of Keister & Moller 2000 This review summarized wealth inequality in the form of net worth. Authors examined empirical evidence of wealth accumulation and distribution, presented estimates of trends

Summary of Keister & Moller 2000 This review summarized wealth inequality in the form of net worth. Authors examined empirical evidence of wealth accumulation and distribution, presented estimates of trends

2000s, a trend. rates and with. workforce participation as. followed. 2015, 50 th

Labor Force Participat tion Trends in Michigan and the United States Executive Summary Labor force participation rates in the United States have been on the gradual decline since peaking in the early 2000s,

Labor Force Participat tion Trends in Michigan and the United States Executive Summary Labor force participation rates in the United States have been on the gradual decline since peaking in the early 2000s,

A Look Behind the Numbers: Foreclosures in Allegheny County, PA

Page1 Introduction This is the second report in a series that looks at the geographic distribution of foreclosures in counties located within the Federal Reserve s Fourth District. In this report we focus

Page1 Introduction This is the second report in a series that looks at the geographic distribution of foreclosures in counties located within the Federal Reserve s Fourth District. In this report we focus

WISDOM FUND CREDIT ACCESS FOR WOMEN OWNED SMALL BUSINESSES RESEARCH BRIEF

WISDOM FUND CREDIT ACCESS FOR WOMEN OWNED SMALL BUSINESSES RESEARCH BRIEF MARCH 2019 FUND COMMUNITY INSTITUTE 1165 N. CLARK ST, SUITE 300 CHICAGO, IL 60610 P. 773.281.8845 1 TABLE OF CONTENTS Introduction

WISDOM FUND CREDIT ACCESS FOR WOMEN OWNED SMALL BUSINESSES RESEARCH BRIEF MARCH 2019 FUND COMMUNITY INSTITUTE 1165 N. CLARK ST, SUITE 300 CHICAGO, IL 60610 P. 773.281.8845 1 TABLE OF CONTENTS Introduction

The Well-Being of Women in Utah

1 The Well-Being of Women in Utah YWCA Utah s vision is that all Utah women are thriving and leading the lives they choose, with their strength benefiting their families, communities, and the state as

1 The Well-Being of Women in Utah YWCA Utah s vision is that all Utah women are thriving and leading the lives they choose, with their strength benefiting their families, communities, and the state as

LISC Building Sustainable Communities Initiative Neighborhood Quality Monitoring Report

LISC Building Sustainable Communities Initiative Neighborhood Quality Monitoring Report Neighborhood:, Kansas City, MO The LISC Building Sustainable Communities (BSC) Initiative supports community efforts

LISC Building Sustainable Communities Initiative Neighborhood Quality Monitoring Report Neighborhood:, Kansas City, MO The LISC Building Sustainable Communities (BSC) Initiative supports community efforts

HEALTH INSURANCE COVERAGE AMONG WORKERS AND THEIR DEPENDENTS IN NEW YORK,

HEALTH INSURANCE COVERAGE AMONG WORKERS AND THEIR DEPENDENTS IN NEW YORK, 2001 2002 UNITED HOSPITAL FUND Danielle Holahan Elise Hubert URBAN INSTITUTE John Holahan Linda Blumberg HEALTH INSURANCE COVERAGE

HEALTH INSURANCE COVERAGE AMONG WORKERS AND THEIR DEPENDENTS IN NEW YORK, 2001 2002 UNITED HOSPITAL FUND Danielle Holahan Elise Hubert URBAN INSTITUTE John Holahan Linda Blumberg HEALTH INSURANCE COVERAGE

Rifle city Demographic and Economic Profile

Rifle city Demographic and Economic Profile Community Quick Facts Population (2014) 9,289 Population Change 2010 to 2014 156 Place Median HH Income (ACS 10-14) $52,539 State Median HH Income (ACS 10-14)

Rifle city Demographic and Economic Profile Community Quick Facts Population (2014) 9,289 Population Change 2010 to 2014 156 Place Median HH Income (ACS 10-14) $52,539 State Median HH Income (ACS 10-14)

Recreational marijuana and collision claim frequencies

Highway Loss Data Institute Bulletin Vol. 34, No. 14 : April 2017 Recreational marijuana and collision claim frequencies Summary Colorado was the first state to legalize recreational marijuana for adults

Highway Loss Data Institute Bulletin Vol. 34, No. 14 : April 2017 Recreational marijuana and collision claim frequencies Summary Colorado was the first state to legalize recreational marijuana for adults

The Impact of the Massachusetts Health Care Reform on Health Care Use Among Children

The Impact of the Massachusetts Health Care Reform on Health Care Use Among Children Sarah Miller December 19, 2011 In 2006 Massachusetts enacted a major health care reform aimed at achieving nearuniversal

The Impact of the Massachusetts Health Care Reform on Health Care Use Among Children Sarah Miller December 19, 2011 In 2006 Massachusetts enacted a major health care reform aimed at achieving nearuniversal

Lapkoff & Gobalet Demographic Research, Inc.

Lapkoff & Gobalet Demographic Research, Inc. 22361 Rolling Hills Road, Saratoga, CA 95070-6560 (408) 725-8164 Fax (408) 725-1479 2120 6 th Street #9, Berkeley, CA 94710-2204 (510) 540-6424 Fax (510) 540-6425

Lapkoff & Gobalet Demographic Research, Inc. 22361 Rolling Hills Road, Saratoga, CA 95070-6560 (408) 725-8164 Fax (408) 725-1479 2120 6 th Street #9, Berkeley, CA 94710-2204 (510) 540-6424 Fax (510) 540-6425

Minnesota's Uninsured in 2017: Rates and Characteristics

HEALTH ECONOMICS PROGRAM Minnesota's Uninsured in 2017: Rates and Characteristics FEBRUARY 2018 As noted in the companion issue brief to this analysis, Minnesota s uninsurance rate climbed significantly

HEALTH ECONOMICS PROGRAM Minnesota's Uninsured in 2017: Rates and Characteristics FEBRUARY 2018 As noted in the companion issue brief to this analysis, Minnesota s uninsurance rate climbed significantly

THE POPULARITY OF PAYDAY LENDING: POLITICS, RELIGION, RACE OR POVERTY? James P. Dow Jr.* Associate Professor

THE POPULARITY OF PAYDAY LENDING: POLITICS, RELIGION, RACE OR POVERTY? James P. Dow Jr.* Associate Professor Department of Finance, Real Estate and Insurance California State University, Northridge September

THE POPULARITY OF PAYDAY LENDING: POLITICS, RELIGION, RACE OR POVERTY? James P. Dow Jr.* Associate Professor Department of Finance, Real Estate and Insurance California State University, Northridge September

PUBLIC DISCLOSURE. October 10, 2006 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION. BPD BANK RSSD No

PUBLIC DISCLOSURE October 10, 2006 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION BPD BANK RSSD No. 66015 90 BROAD STREET NEW YORK, NEW YORK 10004 Federal Reserve Bank of New York 33 Liberty Street

PUBLIC DISCLOSURE October 10, 2006 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION BPD BANK RSSD No. 66015 90 BROAD STREET NEW YORK, NEW YORK 10004 Federal Reserve Bank of New York 33 Liberty Street

Are Old Age Workers Out of Luck? An Empirical Study of the U.S. Labor Market. Keith Brian Kline II Sreenath Majumder, PhD March 16, 2015

Are Old Age Workers Out of Luck? An Empirical Study of the U.S. Labor Market Keith Brian Kline II Sreenath Majumder, PhD March 16, 2015 Are Old Age Workers Out of Luck? An Empirical Study of the U.S. Labor

Are Old Age Workers Out of Luck? An Empirical Study of the U.S. Labor Market Keith Brian Kline II Sreenath Majumder, PhD March 16, 2015 Are Old Age Workers Out of Luck? An Empirical Study of the U.S. Labor

PUBLIC DISCLOSURE COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION

PUBLIC DISCLOSURE September 17, 2007 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION Belgrade State Bank RSSD #761244 410 Main Street Belgrade, Missouri 63622 Federal Reserve Bank of St. Louis P.O. Box

PUBLIC DISCLOSURE September 17, 2007 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION Belgrade State Bank RSSD #761244 410 Main Street Belgrade, Missouri 63622 Federal Reserve Bank of St. Louis P.O. Box

OHIO MEDICAID ASSESSMENT SURVEY 2012

OHIO MEDICAID ASSESSMENT SURVEY 2012 Taking the pulse of health in Ohio Policy Brief A HEALTH PROFILE OF OHIO WOMEN AND CHILDREN Kelly Balistreri, PhD and Kara Joyner, PhD Department of Sociology and the

OHIO MEDICAID ASSESSMENT SURVEY 2012 Taking the pulse of health in Ohio Policy Brief A HEALTH PROFILE OF OHIO WOMEN AND CHILDREN Kelly Balistreri, PhD and Kara Joyner, PhD Department of Sociology and the

Health Insurance Coverage in the District of Columbia

Health Insurance Coverage in the District of Columbia Estimates from the 2009 DC Health Insurance Survey The Urban Institute April 2010 Julie Hudman, PhD Director Department of Health Care Finance Linda

Health Insurance Coverage in the District of Columbia Estimates from the 2009 DC Health Insurance Survey The Urban Institute April 2010 Julie Hudman, PhD Director Department of Health Care Finance Linda

Loan Product Steering in Mortgage Markets

Loan Product Steering in Mortgage Markets CFPB Research Conference Washington, DC December 16, 2016 Sumit Agarwal, Georgetown University Gene Amromin, Federal Reserve Bank of Chicago Itzhak Ben David,

Loan Product Steering in Mortgage Markets CFPB Research Conference Washington, DC December 16, 2016 Sumit Agarwal, Georgetown University Gene Amromin, Federal Reserve Bank of Chicago Itzhak Ben David,

THE POPULARITY OF PAYDAY LENDING: POLITICS, RELIGION, RACE OR POVERTY? James P. Dow Jr.*

THE POPULARITY OF PAYDAY LENDING: POLITICS, RELIGION, RACE OR POVERTY? James P. Dow Jr.* Associate Professor Department of Finance, Real Estate and Insurance California State University, Northridge September

THE POPULARITY OF PAYDAY LENDING: POLITICS, RELIGION, RACE OR POVERTY? James P. Dow Jr.* Associate Professor Department of Finance, Real Estate and Insurance California State University, Northridge September

FIGURE I.1 / Per Capita Gross Domestic Product and Unemployment Rates. Year

FIGURE I.1 / Per Capita Gross Domestic Product and Unemployment Rates 40,000 12 Real GDP per Capita (Chained 2000 Dollars) 35,000 30,000 25,000 20,000 15,000 10,000 5,000 Real GDP per Capita Unemployment

FIGURE I.1 / Per Capita Gross Domestic Product and Unemployment Rates 40,000 12 Real GDP per Capita (Chained 2000 Dollars) 35,000 30,000 25,000 20,000 15,000 10,000 5,000 Real GDP per Capita Unemployment

First-time Homebuyers in Rural and Urban Pennsylvania

First-time Homebuyers in Rural and Urban Pennsylvania September 2015 This fact sheet presents an analysis of first-time homebuyers in Pennsylvania. According to 2013 data from the Federal Housing Finance

First-time Homebuyers in Rural and Urban Pennsylvania September 2015 This fact sheet presents an analysis of first-time homebuyers in Pennsylvania. According to 2013 data from the Federal Housing Finance

Small Area Health Insurance Estimates from the Census Bureau: 2008 and 2009

October 2011 Small Area Health Insurance Estimates from the Census Bureau: 2008 and 2009 Introduction The U.S. Census Bureau s Small Area Health Insurance Estimates (SAHIE) program produces model based

October 2011 Small Area Health Insurance Estimates from the Census Bureau: 2008 and 2009 Introduction The U.S. Census Bureau s Small Area Health Insurance Estimates (SAHIE) program produces model based

Did States Maximize Their Opportunity Zone Selections?

M E T R O P O L I T A N H O U S I N G A N D C O M M U N I T I E S P O L I C Y C E N T E R Did States Maximize Their Opportunity Zone Selections? Analysis of the Opportunity Zone Designations Brett Theodos,

M E T R O P O L I T A N H O U S I N G A N D C O M M U N I T I E S P O L I C Y C E N T E R Did States Maximize Their Opportunity Zone Selections? Analysis of the Opportunity Zone Designations Brett Theodos,

Demographic and Economic Characteristics of Children in Families Receiving Social Security

Each month, over 3 million children receive benefits from Social Security, accounting for one of every seven Social Security beneficiaries. This article examines the demographic characteristics and economic

Each month, over 3 million children receive benefits from Social Security, accounting for one of every seven Social Security beneficiaries. This article examines the demographic characteristics and economic

Cuyahoga County Mortgage Lending Patterns

Cuyahoga County Mortgage Lending Patterns July 2018 Michael Lepley & Lenore Mangiarelli About the Authors MICHAEL LEPLEY is Fair Housing Center for Rights & Research s Senior Research Associate. He received

Cuyahoga County Mortgage Lending Patterns July 2018 Michael Lepley & Lenore Mangiarelli About the Authors MICHAEL LEPLEY is Fair Housing Center for Rights & Research s Senior Research Associate. He received

Legacy City Revitalization: The Role of Federal Historic Tax Credit Projects

Legacy City Revitalization: The Role of Federal Historic Tax Credit Projects Kelly L. Kinahan, AICP Doctoral Candidate Levin College Research Conference August 20, 2015 Research Questions (1) What is the

Legacy City Revitalization: The Role of Federal Historic Tax Credit Projects Kelly L. Kinahan, AICP Doctoral Candidate Levin College Research Conference August 20, 2015 Research Questions (1) What is the

TitleMax INVESTMENT OFFERING. Todd Bunke South Western Avenue Blue Island, IL 60406

INVESTMENT OFFERING TitleMax 12434 South Western Avenue Blue Island, IL 60406 Todd Bunke 404.964.9048 tbunke@atlantaregroup.com Confidentiality Agreement This is a confidential Memorandum intended solely

INVESTMENT OFFERING TitleMax 12434 South Western Avenue Blue Island, IL 60406 Todd Bunke 404.964.9048 tbunke@atlantaregroup.com Confidentiality Agreement This is a confidential Memorandum intended solely

Program on Retirement Policy Number 1, February 2011

URBAN INSTITUTE Retirement Security Data Brief Program on Retirement Policy Number 1, February 2011 Poverty among Older Americans, 2009 Philip Issa and Sheila R. Zedlewski About one in three Americans

URBAN INSTITUTE Retirement Security Data Brief Program on Retirement Policy Number 1, February 2011 Poverty among Older Americans, 2009 Philip Issa and Sheila R. Zedlewski About one in three Americans

COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION

PUBLIC DISCLOSURE June 2, 2008 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION Legacy Bank & Trust Company RSSD # 397755 10603 Highway 32 P.O. Box D Plato, Missouri 65552 Federal Reserve Bank of St.

PUBLIC DISCLOSURE June 2, 2008 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION Legacy Bank & Trust Company RSSD # 397755 10603 Highway 32 P.O. Box D Plato, Missouri 65552 Federal Reserve Bank of St.

Financing Floods in Chicago. Sephra Thomas. GIS for Water Resources C E 394K. Dr. David Maidment

Financing Floods in Chicago Sephra Thomas GIS for Water Resources C E 394K Dr. David Maidment Fall 2018 Abstract The objective of this term paper is to study the hydrology and social vulnerability of Chicago,

Financing Floods in Chicago Sephra Thomas GIS for Water Resources C E 394K Dr. David Maidment Fall 2018 Abstract The objective of this term paper is to study the hydrology and social vulnerability of Chicago,

IMPACT OF THE SOCIAL SECURITY RETIREMENT EARNINGS TEST ON YEAR-OLDS

#2003-15 December 2003 IMPACT OF THE SOCIAL SECURITY RETIREMENT EARNINGS TEST ON 62-64-YEAR-OLDS Caroline Ratcliffe Jillian Berk Kevin Perese Eric Toder Alison M. Shelton Project Manager The Public Policy

#2003-15 December 2003 IMPACT OF THE SOCIAL SECURITY RETIREMENT EARNINGS TEST ON 62-64-YEAR-OLDS Caroline Ratcliffe Jillian Berk Kevin Perese Eric Toder Alison M. Shelton Project Manager The Public Policy

Determinants of Federal and State Community Development Spending:

Determinants of Federal and State Community Development Spending: 1981 2004 by David Cashin, Julie Gerenrot, and Anna Paulson Introduction Federal and state community development spending is an important

Determinants of Federal and State Community Development Spending: 1981 2004 by David Cashin, Julie Gerenrot, and Anna Paulson Introduction Federal and state community development spending is an important

THE POPULARITY OF PAYDAY LENDING: POLITICS, RELIGION, RACE OR POVERTY?

The Popularity of Payday Lending: Politics, Religion, Race or Poverty? THE POPULARITY OF PAYDAY LENDING: POLITICS, RELIGION, RACE OR POVERTY? James P. Dow Jr, California State University, Northridge ABSTRACT

The Popularity of Payday Lending: Politics, Religion, Race or Poverty? THE POPULARITY OF PAYDAY LENDING: POLITICS, RELIGION, RACE OR POVERTY? James P. Dow Jr, California State University, Northridge ABSTRACT

Sources. of the. Survey. No September 2011 N. nonelderly. health. population. in population in 2010, and. of Health Insurance.

September 2011 N No. 362 Sources of Health Insurance and Characteristics of the Uninsured: Analysis of the March 2011 Current Population Survey By Paul Fronstin, Employee Benefit Research Institute LATEST

September 2011 N No. 362 Sources of Health Insurance and Characteristics of the Uninsured: Analysis of the March 2011 Current Population Survey By Paul Fronstin, Employee Benefit Research Institute LATEST

DYNAMICS OF URBAN INFORMAL

DYNAMICS OF URBAN INFORMAL EMPLOYMENT IN BANGLADESH Selim Raihan Professor of Economics, University of Dhaka and Executive Director, SANEM ICRIER Conference on Creating Jobs in South Asia 3-4 December

DYNAMICS OF URBAN INFORMAL EMPLOYMENT IN BANGLADESH Selim Raihan Professor of Economics, University of Dhaka and Executive Director, SANEM ICRIER Conference on Creating Jobs in South Asia 3-4 December

CRS Report for Congress Received through the CRS Web

Order Code RL33387 CRS Report for Congress Received through the CRS Web Topics in Aging: Income of Americans Age 65 and Older, 1969 to 2004 April 21, 2006 Patrick Purcell Specialist in Social Legislation

Order Code RL33387 CRS Report for Congress Received through the CRS Web Topics in Aging: Income of Americans Age 65 and Older, 1969 to 2004 April 21, 2006 Patrick Purcell Specialist in Social Legislation

Public-private sector pay differential in UK: A recent update

Public-private sector pay differential in UK: A recent update by D H Blackaby P D Murphy N C O Leary A V Staneva No. 2013-01 Department of Economics Discussion Paper Series Public-private sector pay differential

Public-private sector pay differential in UK: A recent update by D H Blackaby P D Murphy N C O Leary A V Staneva No. 2013-01 Department of Economics Discussion Paper Series Public-private sector pay differential

Toshiko Kaneda, PhD Population Reference Bureau (PRB) James Kirby, PhD Agency for Healthcare Research and Quality (AHRQ)

James Kirby, PhD Agency for Healthcare Research and Quality (AHRQ)") Disparities in Health Care Spending among Older Adults: Trends in Total and Out-of-Pocket Health Expenditures by Sex, Race/Ethnicity, and Income between 1996 and 21 Toshiko Kaneda, PhD Population Reference

Disparities in Health Care Spending among Older Adults: Trends in Total and Out-of-Pocket Health Expenditures by Sex, Race/Ethnicity, and Income between 1996 and 21 Toshiko Kaneda, PhD Population Reference

Output and Unemployment

o k u n s l a w 4 The Regional Economist October 2013 Output and Unemployment How Do They Relate Today? By Michael T. Owyang, Tatevik Sekhposyan and E. Katarina Vermann Potential output measures the productive

o k u n s l a w 4 The Regional Economist October 2013 Output and Unemployment How Do They Relate Today? By Michael T. Owyang, Tatevik Sekhposyan and E. Katarina Vermann Potential output measures the productive

PUBLIC DISCLOSURE. September 4, 2001 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION CITIZENS BANK OF EDMOND RSSD#

PUBLIC DISCLOSURE COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION CITIZENS BANK OF EDMOND RSSD# 172457 ONE EAST 1 st STREET, P.O. BOX 30 EDMOND, OKLAHOMA 73034 Federal Reserve Bank of Kansas City 925

PUBLIC DISCLOSURE COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION CITIZENS BANK OF EDMOND RSSD# 172457 ONE EAST 1 st STREET, P.O. BOX 30 EDMOND, OKLAHOMA 73034 Federal Reserve Bank of Kansas City 925

kaiser medicaid commission on and the uninsured How Will Health Reform Impact Young Adults? By Karyn Schwartz and Tanya Schwartz Executive Summary

I S S U E P A P E R kaiser commission on medicaid and the uninsured How Will Health Reform Impact Young Adults? By Karyn Schwartz and Tanya Schwartz Executive Summary May 2010 The health reform law that

I S S U E P A P E R kaiser commission on medicaid and the uninsured How Will Health Reform Impact Young Adults? By Karyn Schwartz and Tanya Schwartz Executive Summary May 2010 The health reform law that

Income and Poverty Among Older Americans in 2008

Income and Poverty Among Older Americans in 2008 Patrick Purcell Specialist in Income Security October 2, 2009 Congressional Research Service CRS Report for Congress Prepared for Members and Committees

Income and Poverty Among Older Americans in 2008 Patrick Purcell Specialist in Income Security October 2, 2009 Congressional Research Service CRS Report for Congress Prepared for Members and Committees

Older Immigrants and Health Insurance: Differences by Region of Origin in Patterns and Sources of Coverage

Older Immigrants and Health Insurance: Differences by Region of Origin in Patterns and Sources of Coverage Adriana M. Reyes and Melissa A. Hardy Pennsylvania State Univeristy Much attention has been paid

Older Immigrants and Health Insurance: Differences by Region of Origin in Patterns and Sources of Coverage Adriana M. Reyes and Melissa A. Hardy Pennsylvania State Univeristy Much attention has been paid