Regulatory Compliance Update

|

|

|

- Hugo Stephens

- 5 years ago

- Views:

Transcription

1 Regulatory Compliance Update ACUIA Region 6 Conference Presented By: Kristie Kenney Hoover, NCCO Internal Audit Manager, Doeren Mayhew Florida Michigan North Carolina Texas Insight. Oversight. Foresight.

2 Discussion Areas Workshop objectives The recent focus on regulatory compliance The many areas of compliance and recent changes affecting credit unions Open forum

3 Workshop Objectives Gain an understanding of: BSA/AML and Final CDD Rule Unfair, Deceptive, Abusive Acts and Practices ACH Same-Day Processing Rules New Mortgage Servicing Rule Truth in Lending Act/Real Estate Settlement Procedures Act Integrated Disclosure Rule (reminders) HMDA Final Rule Military Lending Act How compliance with these requirements is also an important part of managing risk within the credit union Open participation

4 Recent Focus on Regulatory Compliance

5 Focus on Regulatory Compliance Why do the regulators have their eyes on this area? What is the public perception of the many regulations? What are the risks of non-compliance? What does regulatory compliance cost?

6 The Many Areas of Compliance

7 BSA/AML Compliance Bank Secrecy Act (BSA) was enacted in 1970 and helps to safeguard financial institutions from the abuses of financial crimes including money laundering, terrorist financing and other illegal transactions. The Patriot Act of 2001 strengthened Anti-Money Laundering (AML) laws, criminalizing terrorist financing and increasing the civil and criminal penalties for money laundering. The Act also augmented the BSA framework by requiring stronger member identification and due diligence procedures.

8 BSA/AML Compliance A written BSA/AML compliance program must be approved by the Board and should be developed using the BSA/AML risk assessment completed by management. The written program must include internal controls, provide for independent testing, designate a BSA officer and address training. The credit union s BSA/AML compliance program must also implement a Customer Identification Program (CIP). The CIP should enable the credit union to form a reasonable belief that it knows the true identity of each member.

9 BSA/AML Compliance FinCEN finalized Customer Due Diligence (CDD) Rule on May 11, 2016 and implementation is required May 11, Credit unions already required to conduct CDD as part of internal controls; however, rule clarifies existing CDD expectations.

10 BSA/AML Compliance Final CDD Rule is made up of four explicit requirements including: 1. Identifying and verifying the identity of members. 2. Identifying and verifying the identity of beneficial owners and legal entity members. 3. Understanding the nature and purpose of member relationships. 4. Conducting ongoing monitoring to maintain and update member information and to identify and report suspicious transactions.

11 BSA/AML Compliance Final CDD Rule (continued): Beneficial Ownership Form (Appendix A to ) must be completed by the person opening a new account (not limited to share level accounts) on behalf of a legal entity. Institutions can use their own forms. Credit unions should obtain beneficial ownership information for existing members when, in the course of normal monitoring, the financial institution detects information relevant to assessing or reevaluating the risk associated with that member.

12 BSA/AML Compliance BSA/AML Software Validation Recommended to be performed to verify that software is working effectively/efficiently and transaction data from the core system is being accurately mapped/uploaded to the AML software. Limited guidance on required frequency in FFIEC BSA/AML Manual. NCUA has been including lack of performance/completion in recent Exams.

13 Unfair, Deceptive, Abusive Acts and Practices UDAAP - In accordance with 12 U.S. Code Section 5536(a), it shall be unlawful for: (1) any covered person or service provider: (A) to offer or provide to a consumer any financial product or service not in conformity with Federal consumer financial law, or otherwise commit any act or omission in violation of a Federal consumer financial law; or (B) to engage in any unfair, deceptive, or abusive act or practice.

14 Unfair, Deceptive, Abusive Acts and Practices UDAAP implementation: No CFPB regulations to date specifically under UDAAP. CFPB s enforcement of UDAAP has been through enforcement actions. A specific number of consumers does not need to be affected or sustain any specific amount of damages to require CFPB enforcement.

15 Unfair, Deceptive, Abusive Acts and Practices Areas for UDAAP concern: Payday loans. Student loans. Overdraft protection (i.e. Courtesy Pay). Mortgage loan servicing. Ancillary loan products (debit and ID theft protection, service contracts). Vehicle loans (i.e. dealer rate mark ups)

16 ACH Same-Day Rules ACH transactions are governed by the National Automated Clearing House Association (NACHA) Operating Rules, which provide the legal foundation for the exchange of ACH payments. To be a participant in the ACH network, an annual audit of compliance with the NACHA Operating Rules must be completed annually by Dec. 31st. A three-phased implementation effort to provide for a faster ACH processing environment began in Sept It is known as same day processing.

17 ACH Same-Day Rules ACH Same-Day Rules Transactions above $25,000 and international ACH transactions are not eligible. Phase 1 (effective Sept. 23, 2016): Same day credit entries must be made available by the end of the credit union s processing day.

18 ACH Same-Day Rules ACH Same-Day Rules (continued) Phase 2 (effective Sept. 23, 2017): Same day debit entries must also be made available by the same deadline effective for same day credit entries. Phase 3 (effective Mar. 16, 2018): For the second processing window, same day credit and debit entries must be made available by 5 p.m. Same Day Fees: Fee of approximately 5.2 cents for each same day entry accepted, which is paid to the RDFI from the ODFI.

19 Lending Compliance 2016 Mortgage Servicing Rule Truth in Lending Act (TILA)/Real Estate Settlement Procedures Act (RESPA) Integrated Disclosure Rule Home Mortgage Disclosure Act (HMDA) Military Lending Act

20 Lending Compliance In August 2016, CFPB published a final rule that amended certain mortgage servicing rules. It is known as the 2016 Mortgage Servicing Rule. Most provisions are effective October 19, Provisions related to successors in interest and bankruptcy periodic statements are effective April 19, In accordance with the 2016 Mortgage Servicing Rule, credit unions must consider compliance with the following changes: Excludes certain seller-financed transactions and mortgage loans serviced for a non-affiliate from being counted toward the 5,000 loan limit for small servicer exemption.

21 Lending Compliance In accordance with the 2016 Mortgage Servicing Rule, credit unions must consider compliance with the following changes (continued): Adds definitions of successor in interest to RESPA and TILA and includes provisions to confirm a successor s interest and identity. Clarifies certain periodic statement disclosure requirements for mortgage loans, requires certain borrowers in bankruptcy to be provided with modified periodic statement, and exempts servicers from periodic statement requirement for charged-off mortgage loans in certain circumstances.

22 Lending Compliance In accordance with the 2016 Mortgage Servicing Rule, credit unions must consider compliance with the following changes (continued): Amends the force-placed insurance disclosures and model forms to account for when the borrower has insufficient coverage on the property. Clarifies the obligations for servicers to establish or make good faith efforts to establish live contact with delinquent borrowers and revises the exemption from early intervention for borrowers in bankruptcy or invoked a case under the FDCPA.

23 Lending Compliance In accordance with the 2016 Mortgage Servicing Rule, credit unions must consider compliance with the following changes (continued): Adopts a general definition of delinquency that applies to all servicing provisions under RESPA and periodic statements for mortgage loans under TILA. Amends and modifies several sections of the Loss Mitigation Rule.

24 Lending Compliance TRID Rule - Reminders TRID prohibits the collection of fees (other than fee to obtain credit report) prior to providing the Loan Estimate to the consumer. TRID includes rules for providing Revised Loan Estimates and Corrected Closing Disclosures. TRID also requires two post-consummation notices including the Escrow Closing Notice and partial payment policy addition to the existing mortgage transfer servicing notice.

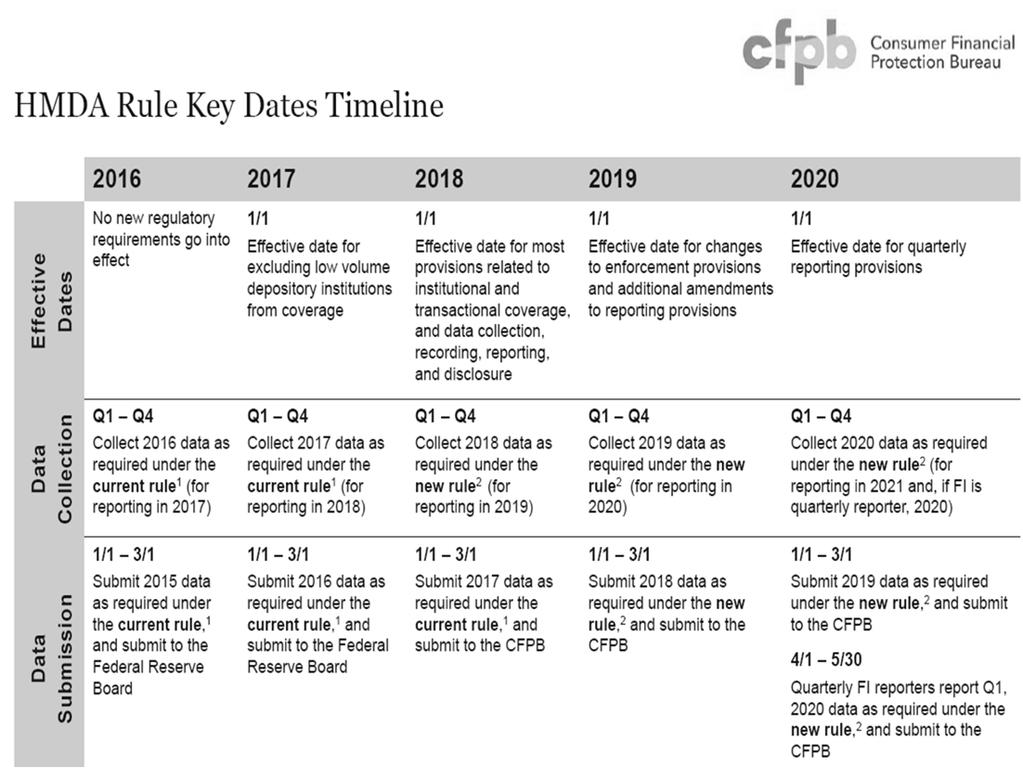

25 Lending Compliance HMDA (Regulation C) provides the public and government with information to help determine whether the credit union is serving the credit needs of its community and helps discourage redlining, which is the practice of denying or limiting credit based on neighborhood characteristics (race, national origin, income). HMDA requires the credit union to report data for home purchase loans, home improvement loans and refinances.

26 Lending Compliance HMDA (continued) The Consumer Financial Protection Bureau recently issued a Final Rule amending HMDA. The Final Rule, effective in phases starting in 2017, changes the following: Types of institutions subject to the regulation. Types of transactions subject to the regulation (now includes home equity lines of credit). Specific information to be collected, recorded and reported. Processes for reporting and disclosing data.

27 Lending Compliance

28 Lending Compliance HMDA (continued) Expanded data fields apply to covered transactions that have final action taken on or after January 1, This is going to effect the credit unions pipeline of loans as any applications taken in November/December 2017 with a final action date in January 2018 will be subject to collection of the expanded data fields.

29 Lending Compliance Military Lending Act (MLA) was recently expanded by the DoD to apply to more than only payday loans, vehicle title loans, and tax refund anticipation loans. The final rule went into effect October 3, 2016 (2017 for credit cards) and applies to more consumer credit products granted to covered borrowers subjecting the products to the 36 percent interest rate ceiling using the all in Military Annual Percentage Rate (MAPR), as well as disclosure requirements, prohibitions on prepayment penalties, and limitations on mandatory arbitration.

30 Lending Compliance MLA (continued) Consumer credit is credit which is offered or extended to a covered borrower primarily for personal, family, or household purposes and subject to a finance charge or payable in more than four installments. Exceptions include residential mortgages, transactions to finance the purchase of a motor vehicle, and loans that are exempt for the purposes of Regulation Z (1026.3, ). Applies to members (or their dependents) of the armed forces serving on active duty or active guard and reserve duty at the time the consumer becomes obligated on a consumer credit transaction or establishes an account for consumer credit The MAPR includes finance charges under Regulation Z (1026.4) and specific fees otherwise excluded by Regulation Z such as credit insurance premiums, fees for debt cancellation contract, and fees for credit related ancillary products sold in connection with the loan.

31 What Makes for an Effective Compliance Program

32 An Effective Compliance Program Identification Analyze the products and services offered by the credit union to determine the applicable regulatory requirements. Risk Assessment Assign risk ratings for each applicable regulation based on the likelihood of a violation and the severity of the penalties. Policies and Procedures Act as tools to ensure that compliance-related issues are handled consistently.

33 An Effective Compliance Program Key Members of the Compliance Team Compliance officer, Board, executive management, legal counsel, internal audit personnel, loan officers/processors, tellers, member services and marketing personnel. Education Ongoing training is a necessity. Independent Testing Audits must be performed at an appropriate frequency and the depth of the review is dependent on the credit union s size and complexity.

34 Open Forum

35 Thank You! Kristie Kenney Hoover, NCCO Internal Audit Manager

Bank Secrecy Act Errors & Exceptions: How Does Your Credit Union Compare?

2018 Conference & Expo Louisville, Kentucky June 14, 2018 Bank Secrecy Act Errors & Exceptions: How Does Your Credit Union Compare? Presented By: Joseph A. Zito, CPA, MBA Shareholder, Doeren Mayhew 1 Michigan

2018 Conference & Expo Louisville, Kentucky June 14, 2018 Bank Secrecy Act Errors & Exceptions: How Does Your Credit Union Compare? Presented By: Joseph A. Zito, CPA, MBA Shareholder, Doeren Mayhew 1 Michigan

Fair Lending Internal Audits

Fair Lending Internal Audits ACUIA Region 6 Conference Presented By: Kristie Kenney Hoover, NCCO Internal Audit Manager, Doeren Mayhew Florida Michigan North Carolina Texas Insight. Oversight. Foresight.

Fair Lending Internal Audits ACUIA Region 6 Conference Presented By: Kristie Kenney Hoover, NCCO Internal Audit Manager, Doeren Mayhew Florida Michigan North Carolina Texas Insight. Oversight. Foresight.

LENDING (LEND) Division

Division") AFSA University Course List As of 4/1/2017 Lesson Name Lesson ID Module Duration Test Duration (Total mins. LENDING (LEND) Division General Vendor Management AFSA1001 30 10 40 Anti-Predatory Lending (with

AFSA University Course List As of 4/1/2017 Lesson Name Lesson ID Module Duration Test Duration (Total mins. LENDING (LEND) Division General Vendor Management AFSA1001 30 10 40 Anti-Predatory Lending (with

Important Compliance Dates December 2017

Ongoing NIST Framework for Improving Critical Infrastructure Cybersecurity June 9, 2017 DoL 29 CFR Part 541 The National Institute of Standards and Technology released a voluntary framework for use to

Ongoing NIST Framework for Improving Critical Infrastructure Cybersecurity June 9, 2017 DoL 29 CFR Part 541 The National Institute of Standards and Technology released a voluntary framework for use to

Important Compliance Dates as of April 2018

The issued a final rule making several substantive revisions to Regulation C s reporting requirements under the Home Mortgage Disclosure Act (HMDA). With the changes, the class of covered transactions

The issued a final rule making several substantive revisions to Regulation C s reporting requirements under the Home Mortgage Disclosure Act (HMDA). With the changes, the class of covered transactions

The Compliance Challenges of Credit Union Collections. Collections and Compliance?

The Compliance Challenges of Credit Union Collections Presented by Maria Peyton NSWC Federal Credit Union Collections and Compliance? Yes! It is about more than just collecting a debt Collectors must be

The Compliance Challenges of Credit Union Collections Presented by Maria Peyton NSWC Federal Credit Union Collections and Compliance? Yes! It is about more than just collecting a debt Collectors must be

Bank Secrecy Act and OFAC Compliance Board of Directors Training

Bank Secrecy Act and OFAC Compliance Board of Directors Training Introduction Today s presenters: Karen M. Janota Assurance Manager Disclaimer: The contents of this presentation are intended to provide

Bank Secrecy Act and OFAC Compliance Board of Directors Training Introduction Today s presenters: Karen M. Janota Assurance Manager Disclaimer: The contents of this presentation are intended to provide

ABA Frontline Compliance Course Descriptions

ABA Frontline Compliance Course Descriptions Active Aggressor for Employees (35 minutes) New May 2017 Provides indicators of potential active shooters to prevent incidents. Explores the run, hide, or fight

ABA Frontline Compliance Course Descriptions Active Aggressor for Employees (35 minutes) New May 2017 Provides indicators of potential active shooters to prevent incidents. Explores the run, hide, or fight

6/21/2013. Section I. Purpose of Course. History and Overview of Mortgage Law, Regulation and Requirements

20 Hour Mortgage Loan Originator Certification Course Purpose of Course Gain historical perspective of mortgage lending Understand contemporary mortgage loan origination process Examine federal rules,

20 Hour Mortgage Loan Originator Certification Course Purpose of Course Gain historical perspective of mortgage lending Understand contemporary mortgage loan origination process Examine federal rules,

Regulatory Compliance Update. Hoi Luk, Senior Manager, Financial Services Consulting

Regulatory Compliance Update Hoi Luk, Senior Manager, Financial Services Consulting What are WE Seeing and Hearing? Supervisory Committee Workshop 3 Supervisory Letter SL 17-01 March 29, 2017 Evaluating

Regulatory Compliance Update Hoi Luk, Senior Manager, Financial Services Consulting What are WE Seeing and Hearing? Supervisory Committee Workshop 3 Supervisory Letter SL 17-01 March 29, 2017 Evaluating

Definitions AML/BSA Risks Assess Your Risks Identify the Risks Mitigate the Risks Scenario Questions?

Definitions AML/BSA Risks Assess Your Risks Identify the Risks Mitigate the Risks Scenario Questions? 2 BSA Bank Secrecy Act Currency and Foreign Transactions Reporting Act, is legislation passed by the

Definitions AML/BSA Risks Assess Your Risks Identify the Risks Mitigate the Risks Scenario Questions? 2 BSA Bank Secrecy Act Currency and Foreign Transactions Reporting Act, is legislation passed by the

Bank Secrecy Act. CUNA Must Know Mondays. November 17, 2014

Bank Secrecy Act CUNA Must Know Mondays November 17, 2014 1 David A. Reed Attorney at Law Reed & Jolly, PLLC Fairfax, Virginia david@reedandjolly.com (703) 675-9578 2 2 The contents of this presentation

Bank Secrecy Act CUNA Must Know Mondays November 17, 2014 1 David A. Reed Attorney at Law Reed & Jolly, PLLC Fairfax, Virginia david@reedandjolly.com (703) 675-9578 2 2 The contents of this presentation

by: Stephen King, JD, AMLP

Community Bank Audit Group Compliance Management Structure / Compliance Risk Assessment June 2, 2014 by: Stephen King, JD, AMLP MEMBER OF PKF NORTH AMERICA, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS

Community Bank Audit Group Compliance Management Structure / Compliance Risk Assessment June 2, 2014 by: Stephen King, JD, AMLP MEMBER OF PKF NORTH AMERICA, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS

Register. Regulatory Compliance. Regulatory Compliance. Lending Compliance

Regulatory Compliance Regulatory Compliance Register Lending Compliance In today s rapidly evolving economy, lenders must have expert knowledge of the latest federal regulation changes that determine banks,

Regulatory Compliance Regulatory Compliance Register Lending Compliance In today s rapidly evolving economy, lenders must have expert knowledge of the latest federal regulation changes that determine banks,

Military Lending Act Amendments Effective: 10/03/ Loans and Open-end lines

Military Lending Act Amendments Effective: 10/03/2016 - Loans and Open-end lines Presented by: Pam Perdue EVP Regulatory Insight, Continuity 10/03/2017 - Credit cards Presented September 2016 Presenting

Military Lending Act Amendments Effective: 10/03/2016 - Loans and Open-end lines Presented by: Pam Perdue EVP Regulatory Insight, Continuity 10/03/2017 - Credit cards Presented September 2016 Presenting

Short-Term, Small-Dollar Lending

Commonly Known as Payday Lending Exam Date: Prepared By: Reviewer: Docket #: Entity Name: [Click&type] [Click&type] [Click&type] [Click&type] [Click&type] These examination procedures apply to the short-term,

Commonly Known as Payday Lending Exam Date: Prepared By: Reviewer: Docket #: Entity Name: [Click&type] [Click&type] [Click&type] [Click&type] [Click&type] These examination procedures apply to the short-term,

2017 WEBINAR SCHEDULE Affordable training, when and where you choose

2017 WEBINAR SCHEDULE Affordable training, when and where you choose With engaging, hot-topic webinars from your Association, you get all of the benefits of a classroom, without the time and hassle of

2017 WEBINAR SCHEDULE Affordable training, when and where you choose With engaging, hot-topic webinars from your Association, you get all of the benefits of a classroom, without the time and hassle of

Sanctions Risk Management Symposium

What U.S. Federal Bank Examiners Look For in Their OFAC Compliance Examinations Tuesday, September 19, 2017, 10:30 11:15 AM Michaela Arndt Head, Sanctions Compliance, Americas and Group Head, US Sanctions

What U.S. Federal Bank Examiners Look For in Their OFAC Compliance Examinations Tuesday, September 19, 2017, 10:30 11:15 AM Michaela Arndt Head, Sanctions Compliance, Americas and Group Head, US Sanctions

EMERGING CONSUMER RISKS FOR COMMUNITY BANKS

November 14, 2016 1 EMERGING CONSUMER RISKS FOR COMMUNITY BANKS 2016 ANNUAL RISK MANAGEMENT CONFERENCE NOVEMBER 14, 2016 November 14, 2016 2 Paul J. Stark, SVP & Chief Credit Officer Civista Bank, Sandusky

November 14, 2016 1 EMERGING CONSUMER RISKS FOR COMMUNITY BANKS 2016 ANNUAL RISK MANAGEMENT CONFERENCE NOVEMBER 14, 2016 November 14, 2016 2 Paul J. Stark, SVP & Chief Credit Officer Civista Bank, Sandusky

ABA Compliance School Foundational

ABA Compliance School Foundational Deposit/Operations Module March 10 13, 2018 Grand Hyatt Denver Denver, Colorado COURSE CATALOG aba.com 1-800-BANKERS October 2014 Session Emory Conference Center and

ABA Compliance School Foundational Deposit/Operations Module March 10 13, 2018 Grand Hyatt Denver Denver, Colorado COURSE CATALOG aba.com 1-800-BANKERS October 2014 Session Emory Conference Center and

Regulatory Update NAFCU Webcast

Regulatory Update NAFCU Webcast Thursday, November 14 2:00 3:30 p.m. Presented by: Steve Van Beek, Esq. (248)723-0521 svb@h2law.com Overview CFPB s Agenda Supervisory Highlights CFPB s Radar AKA, What

Regulatory Update NAFCU Webcast Thursday, November 14 2:00 3:30 p.m. Presented by: Steve Van Beek, Esq. (248)723-0521 svb@h2law.com Overview CFPB s Agenda Supervisory Highlights CFPB s Radar AKA, What

BSA/AML & OFAC Volunteer Compliance Training. Agenda

Ideas + Solutions = Success BSA/AML & OFAC Volunteer Compliance Training Ideas + Solutions = Success Presented by Dorie Fitchett HCUL Regulatory Officer May 17, 2018 Agenda 1. Bank Secrecy Act 2. Office

Ideas + Solutions = Success BSA/AML & OFAC Volunteer Compliance Training Ideas + Solutions = Success Presented by Dorie Fitchett HCUL Regulatory Officer May 17, 2018 Agenda 1. Bank Secrecy Act 2. Office

CU PolicyPro POLICY UPDATE HISTORY

CU PolicyPro POLICY UPDATE HISTORY This document lists all policies updated since 2012, and includes a short description of each update from 2015 through March 2018. Policy 1150 Field of Membership 2017

CU PolicyPro POLICY UPDATE HISTORY This document lists all policies updated since 2012, and includes a short description of each update from 2015 through March 2018. Policy 1150 Field of Membership 2017

NCCO Exam Study Guide

NCCO Exam Study Guide The questions on the NCCO exams are drawn from material contained in NAFCU s Credit Union Compliance GPS. Purchase of the Compliance GPS is not required in order to take the NCCO

NCCO Exam Study Guide The questions on the NCCO exams are drawn from material contained in NAFCU s Credit Union Compliance GPS. Purchase of the Compliance GPS is not required in order to take the NCCO

ABA Compliance School - Intermediate

ABA Compliance School - Intermediate March 14 16, 2018 Grand Hyatt Denver Denver, Colorado COURSE CATALOG aba.com 1-800-BANKERS October 2014 Session Emory Conference Center and Hotel Atlanta, GA aba.com

ABA Compliance School - Intermediate March 14 16, 2018 Grand Hyatt Denver Denver, Colorado COURSE CATALOG aba.com 1-800-BANKERS October 2014 Session Emory Conference Center and Hotel Atlanta, GA aba.com

SAMPLE. 1 Bank Secrecy Act / Anti-Money Laundering. 2 E-Sign Act / Electronic Funds Transfer Act

1 Bank Secrecy Act / Anti-Money Laundering Summary 1 1 Purpose and History of the BSA 1 1 General Requirements of the BSA/AML Compliance Program 1 3 Money Laundering Defined 1 4 BSA / AML Violations 1

1 Bank Secrecy Act / Anti-Money Laundering Summary 1 1 Purpose and History of the BSA 1 1 General Requirements of the BSA/AML Compliance Program 1 3 Money Laundering Defined 1 4 BSA / AML Violations 1

BSA/AML Hot Topics and UIGEA Daniel Hastings Financial Institution Examiner - FDIC

BSA/AML Hot Topics and UIGEA Daniel Hastings Financial Institution Examiner - FDIC Common BSA Deficiencies Revised FFIEC BSA/AML Examination Manual Proposed CDD Requirements for Financial Institutions

BSA/AML Hot Topics and UIGEA Daniel Hastings Financial Institution Examiner - FDIC Common BSA Deficiencies Revised FFIEC BSA/AML Examination Manual Proposed CDD Requirements for Financial Institutions

ANTI-MONEY LAUNDERING IN

ANTI-MONEY LAUNDERING IN THE ACQUIRING INDUSTRY Presented by Laura H. Goldzung, CAMS, CCFE, CFCF, CCRP AML Audit Services, LLC March 8, 2016 AGENDA AML Regulatory Overview OFAC Regulatory Overview AML

ANTI-MONEY LAUNDERING IN THE ACQUIRING INDUSTRY Presented by Laura H. Goldzung, CAMS, CCFE, CFCF, CCRP AML Audit Services, LLC March 8, 2016 AGENDA AML Regulatory Overview OFAC Regulatory Overview AML

COMPLIANCE MANAGEMENT: THE ART OF BOARD REPORTING

COMPLIANCE MANAGEMENT: THE ART OF BOARD REPORTING 2015 Temenos USA, Inc. All rights reserved. Leah M. Hamilton Chief Compliance Officer, TriComply Services WHAT YOU WILL LEARN: 2 How to write a Board Report

COMPLIANCE MANAGEMENT: THE ART OF BOARD REPORTING 2015 Temenos USA, Inc. All rights reserved. Leah M. Hamilton Chief Compliance Officer, TriComply Services WHAT YOU WILL LEARN: 2 How to write a Board Report

Trendspotting the CFPB: What s Coming and How Institutions Can Prepare

Trendspotting the CFPB: What s Coming and How Institutions Can Prepare Courtney H. Gilmer Baker Donelson Center Suite 800 211 Commerce Street Nashville, TN 37201 615.726.5747 cgilmer@bakerdonelson.com

Trendspotting the CFPB: What s Coming and How Institutions Can Prepare Courtney H. Gilmer Baker Donelson Center Suite 800 211 Commerce Street Nashville, TN 37201 615.726.5747 cgilmer@bakerdonelson.com

CUSTOMER DUE DILIGENC

CUSTOMER DUE DILIGENC of the Bank Secrecy Act Coverage: Federally insured credit unions Agency/Citation: FinCEN 31 CFR Parts 1010, 1020, 1023, 1024 and 1026 Effective Date: May 11, 2018 EXECUTIVE SUMMARY

CUSTOMER DUE DILIGENC of the Bank Secrecy Act Coverage: Federally insured credit unions Agency/Citation: FinCEN 31 CFR Parts 1010, 1020, 1023, 1024 and 1026 Effective Date: May 11, 2018 EXECUTIVE SUMMARY

Mortgage Regulation Update

Presented by: Mortgage Regulation Update Wisconsin Credit Union League Convention 1 Objectives At the end of this session, you will: Recognize recent updates to existing mortgage rules TILA/RESPA Integrated

Presented by: Mortgage Regulation Update Wisconsin Credit Union League Convention 1 Objectives At the end of this session, you will: Recognize recent updates to existing mortgage rules TILA/RESPA Integrated

REQUIRED ATTACHMENTS Please provide the following documents with this completed Annual Recertification

ANNUAL RECERTIFICATION For renewals through March, 2020 Company Legal Name: DBA(s): Street Address (Main Office): City, State, Zip: Affiliated Companies: REQUIRED INFORMATION Please provide company information

ANNUAL RECERTIFICATION For renewals through March, 2020 Company Legal Name: DBA(s): Street Address (Main Office): City, State, Zip: Affiliated Companies: REQUIRED INFORMATION Please provide company information

Sonia Lee Director of Affiliate Financial Services HFH International

Sonia Lee Director of Affiliate Financial Services HFH International Topics for Today Anti-Discrimination Laws Other Laws Outreach and Marketing Application Intake Selection Criteria Procedural Issues

Sonia Lee Director of Affiliate Financial Services HFH International Topics for Today Anti-Discrimination Laws Other Laws Outreach and Marketing Application Intake Selection Criteria Procedural Issues

Preparing for Your BSA Compliance Exams. Ted Dreyer, Senior Attorney Wolters Kluwer

Preparing for Your BSA Compliance Exams Ted Dreyer, Senior Attorney Wolters Kluwer Scoping And Planning of Exam BSA/AML Examination Manual Overview Examination procedures First thing on list Previous Criticism

Preparing for Your BSA Compliance Exams Ted Dreyer, Senior Attorney Wolters Kluwer Scoping And Planning of Exam BSA/AML Examination Manual Overview Examination procedures First thing on list Previous Criticism

BSA Regulatory Discussion on Emerging Issues. Salt Lake City ACAMS Chapter Meeting June 21, 2018

BSA Regulatory Discussion on Emerging Issues Salt Lake City ACAMS Chapter Meeting June 21, 2018 Today s Discussion FinCEN s Customer Due Diligence Rule AML Monitoring Systems Providing Services to Marijuana

BSA Regulatory Discussion on Emerging Issues Salt Lake City ACAMS Chapter Meeting June 21, 2018 Today s Discussion FinCEN s Customer Due Diligence Rule AML Monitoring Systems Providing Services to Marijuana

Operational Impacts of the Economic Growth, Regulatory Relief, & Consumer Protection Act (S.2155)

") Operational Impacts of the Economic Growth, Regulatory Relief, & Consumer Protection Act (S.2155) NAFCU s Regulatory Compliance Seminar Presented by Brandy Bruyere, VP of Regulatory Compliance, NAFCU 1

Operational Impacts of the Economic Growth, Regulatory Relief, & Consumer Protection Act (S.2155) NAFCU s Regulatory Compliance Seminar Presented by Brandy Bruyere, VP of Regulatory Compliance, NAFCU 1

MORTGAGE REFORM UNDER THE DODD FRANK WALL STREET REFORM AND CONSUMER PROTECTION ACT

MORTGAGE REFORM UNDER THE DODD FRANK WALL STREET REFORM AND CONSUMER PROTECTION ACT KENNETH BENTON SENIOR CONSUMER REGULATIONS SPECIALIST FEDERAL RESERVE BANK OF PHILADELPHIA MAY 10, 2012 Disclaimer: the

MORTGAGE REFORM UNDER THE DODD FRANK WALL STREET REFORM AND CONSUMER PROTECTION ACT KENNETH BENTON SENIOR CONSUMER REGULATIONS SPECIALIST FEDERAL RESERVE BANK OF PHILADELPHIA MAY 10, 2012 Disclaimer: the

RKL Regulatory Compliance Report for Financial Institutions

RKL for Financial Institutions September 2018 RKL s quarterly compliance report identifies proposed and finalized, federally issued consumer compliance/regulatory items. JULY FINAL ISSUANCES Date July

RKL for Financial Institutions September 2018 RKL s quarterly compliance report identifies proposed and finalized, federally issued consumer compliance/regulatory items. JULY FINAL ISSUANCES Date July

CU PolicyPro Policy Guidance. March 2018

CU PolicyPro March 2018 KEY MO CM CMO R O = Mandatory Policy credit union must have a policy covering the subject matter contained in the CU PolicyPro Policy. = Mandatory if service/product offered if

CU PolicyPro March 2018 KEY MO CM CMO R O = Mandatory Policy credit union must have a policy covering the subject matter contained in the CU PolicyPro Policy. = Mandatory if service/product offered if

The Commercial Real Estate Lending Decision Process Series (RMA)

") Business Banking & Commercial Lending Analyzing Business Financial Statements and Tax Returns Analyzing Financial Statements Analyzing Personal Financial Statements and Tax Returns Certificate in Business

Business Banking & Commercial Lending Analyzing Business Financial Statements and Tax Returns Analyzing Financial Statements Analyzing Personal Financial Statements and Tax Returns Certificate in Business

CFPB National Servicing Standards, Are Servicers Ready?

CFPB National Servicing Standards, Are Servicers Ready? On January 13 th of this year the US Consumer Financial Protection Bureau (CFPB) published comprehensive rules establishing national servicing standards

CFPB National Servicing Standards, Are Servicers Ready? On January 13 th of this year the US Consumer Financial Protection Bureau (CFPB) published comprehensive rules establishing national servicing standards

CFPB Laws and Regulations

Military Lending Act () Interagency Examination Procedures 2015 Amendments Background The Military Lending Act 1 (), enacted in 2006 and implemented by the Department of Defense (DoD), protects active

Military Lending Act () Interagency Examination Procedures 2015 Amendments Background The Military Lending Act 1 (), enacted in 2006 and implemented by the Department of Defense (DoD), protects active

Military Lending Act: How LOANLINER Document Solutions Can Help

Presented by: Military Lending Act: How LOANLINER Document Solutions Can Help Casey Hunt Portfolio & Compliance Manager CUNA Mutual Group Proprietary Reproduction, Adaptation or Distribution Prohibited

Presented by: Military Lending Act: How LOANLINER Document Solutions Can Help Casey Hunt Portfolio & Compliance Manager CUNA Mutual Group Proprietary Reproduction, Adaptation or Distribution Prohibited

Military Lending Act. Presented by Kris McIsaac

Presented by Kris McIsaac 04.28.2017 Why is compliance with the MLA so important?? **Credit Agreements in violation of the MLA are VOID FROM INCEPTION!! Who is covered? Covered Borrower A consumer who,

Presented by Kris McIsaac 04.28.2017 Why is compliance with the MLA so important?? **Credit Agreements in violation of the MLA are VOID FROM INCEPTION!! Who is covered? Covered Borrower A consumer who,

LENDING: KEY EXAMINER TRENDS

LENDING: KEY EXAMINER TRENDS 2015 Temenos USA, Inc. All rights reserved. Leah M. Hamilton Chief Compliance Officer, TriComply Services WHAT YOU WILL LEARN TRID Compliance Reprieve Common issues Regulation

LENDING: KEY EXAMINER TRENDS 2015 Temenos USA, Inc. All rights reserved. Leah M. Hamilton Chief Compliance Officer, TriComply Services WHAT YOU WILL LEARN TRID Compliance Reprieve Common issues Regulation

Name: Brian Short, Kim Miller, Mike Simmons, Jim Tew Qualifications: Past TNAMP Instructors, all with over 20 years in the industry

8 Hour SAFE Comprehensive: Compliance in Action 2018 Course Description and Purpose This course satisfies the requirements set forth by the SAFE Act for a comprehensive 8-hour continuing education course

8 Hour SAFE Comprehensive: Compliance in Action 2018 Course Description and Purpose This course satisfies the requirements set forth by the SAFE Act for a comprehensive 8-hour continuing education course

Welcome to the Military Lending Act Roundtable

Welcome to the Military Lending Act Roundtable Are you in the new Councils Community? Join your Lending Council peers and members of all six Councils in 13 Discussion Communities today! Visit the Community

Welcome to the Military Lending Act Roundtable Are you in the new Councils Community? Join your Lending Council peers and members of all six Councils in 13 Discussion Communities today! Visit the Community

CU PolicyPro Alphabetical Policy Listing

A 3160 2235 7332 2222 2215 3000 6120 8110 2210 3105 2216 2214 2212 2210 2213 11003 2610 2612 2611 1000 11005 9430 11016 5100 5110 7615 9500 Abandoned Property (Unclaimed Property) Abusive Member (Member

A 3160 2235 7332 2222 2215 3000 6120 8110 2210 3105 2216 2214 2212 2210 2213 11003 2610 2612 2611 1000 11005 9430 11016 5100 5110 7615 9500 Abandoned Property (Unclaimed Property) Abusive Member (Member

An Overview of FinCEN s Customer Due Diligence Rule

An Overview of FinCEN s Customer Due Diligence Rule Tina Bottaro, Risk Specialist Supervision Regulation & Credit FEDERAL RESERVE BANK OF PHILADELPHIA Disclaimer The information presented are the views

An Overview of FinCEN s Customer Due Diligence Rule Tina Bottaro, Risk Specialist Supervision Regulation & Credit FEDERAL RESERVE BANK OF PHILADELPHIA Disclaimer The information presented are the views

With so much change, be sure to stay up to date!

With so much change, be sure to stay up to date! Glory LeDu Glory.LeDu@mcul.org Sarah Stevenson Sarah.Stevenson@mcul.org Barb Boyd Barb.Boyd@cusolutionsgroup.com Your Crazy Compliance Peeps Agenda What

With so much change, be sure to stay up to date! Glory LeDu Glory.LeDu@mcul.org Sarah Stevenson Sarah.Stevenson@mcul.org Barb Boyd Barb.Boyd@cusolutionsgroup.com Your Crazy Compliance Peeps Agenda What

ANTI-MONEY LAUNDERING FOR LENDERS

ANTI-MONEY LAUNDERING FOR LENDERS A webinar for MBA members Ari Karen Offit Kurman akaren@offitkurman.com 240.507.1740 Bill Heyman Offit Kurman wheyman@offitkurman.com 301.575.0393 AGENDA Today we will

ANTI-MONEY LAUNDERING FOR LENDERS A webinar for MBA members Ari Karen Offit Kurman akaren@offitkurman.com 240.507.1740 Bill Heyman Offit Kurman wheyman@offitkurman.com 301.575.0393 AGENDA Today we will

CITIZENS, INC. BANK SECRECY ACT/ ANTI-MONEY LAUNDERING POLICY AND PROGRAM

I. Introduction CITIZENS, INC. BANK SECRECY ACT/ ANTI-MONEY LAUNDERING POLICY AND PROGRAM The Bank Secrecy Act/Anti-Money Laundering Responsibilities of Insurance Companies U.S. insurance companies have

I. Introduction CITIZENS, INC. BANK SECRECY ACT/ ANTI-MONEY LAUNDERING POLICY AND PROGRAM The Bank Secrecy Act/Anti-Money Laundering Responsibilities of Insurance Companies U.S. insurance companies have

Examination Procedures

After completing the risk assessment and examination scoping, examiners should use these procedures, in conjunction with the compliance management system Exam Date: Exam ID No. Prepared By: Reviewer: Docket

After completing the risk assessment and examination scoping, examiners should use these procedures, in conjunction with the compliance management system Exam Date: Exam ID No. Prepared By: Reviewer: Docket

IAM SURE MOST OF YOU HAVE BEEN ON A ROLLER COASTER at

The Compliance Regulatory Roller Coaster Just A LOOK AHEA IAM SURE MOST OF YOU HAVE BEEN ON A ROLLER COASTER at some point in your lives. The ride provides thrills, drops, hills, sharp turns, high speeds,

The Compliance Regulatory Roller Coaster Just A LOOK AHEA IAM SURE MOST OF YOU HAVE BEEN ON A ROLLER COASTER at some point in your lives. The ride provides thrills, drops, hills, sharp turns, high speeds,

Notice on Defense Department s New Rules for Consumer Loans to Service Members

Notice on Defense Department s New Rules for Consumer Loans to Service Members The Department of Defense has finalized a regulation for consumer payday loans, vehicle title loans, and tax refund anticipation

Notice on Defense Department s New Rules for Consumer Loans to Service Members The Department of Defense has finalized a regulation for consumer payday loans, vehicle title loans, and tax refund anticipation

Kevin Patterson Partner

100 Quentin Roosevelt Boulevard Garden City, NY 11530-4850 ph: 516.296.9196 fx: 516.357.3792 kpatterson@cullenanddykman.com AREAS OF PRACTICE Banking Compliance Bank Operations Bank Regulatory and Compliance

100 Quentin Roosevelt Boulevard Garden City, NY 11530-4850 ph: 516.296.9196 fx: 516.357.3792 kpatterson@cullenanddykman.com AREAS OF PRACTICE Banking Compliance Bank Operations Bank Regulatory and Compliance

Regulatory and Enforcement Trends

NY2 717563 Regulatory and Enforcement Trends April 11, 2013 2013 Morrison & Foerster LLP All Rights Reserved mofo.com Agenda We will provide an overview of the regulatory and enforcement trends that may

NY2 717563 Regulatory and Enforcement Trends April 11, 2013 2013 Morrison & Foerster LLP All Rights Reserved mofo.com Agenda We will provide an overview of the regulatory and enforcement trends that may

Bank Secrecy Act (BSA)/Anti-Money Laundering (AML) Employee & Agent Training

/Anti-Money Laundering (AML) Employee & Agent Training") Bank Secrecy Act (BSA)/Anti-Money Laundering (AML) Employee & Agent Training OVERVIEW The Bank Secrecy Act, or BSA, was passed by congress in 1970. The BSA required banks to maintain records of certain

Bank Secrecy Act (BSA)/Anti-Money Laundering (AML) Employee & Agent Training OVERVIEW The Bank Secrecy Act, or BSA, was passed by congress in 1970. The BSA required banks to maintain records of certain

Bank Secrecy Act & Anti-Money Laundering for Directors. Mike Lee Director of Regulatory Advocacy

Bank Secrecy Act & Anti-Money Laundering for Directors Mike Lee Director of Regulatory Advocacy michael.lee@lscu.coop Legal Disclaimer: Information provided in this presentation, including all materials,

Bank Secrecy Act & Anti-Money Laundering for Directors Mike Lee Director of Regulatory Advocacy michael.lee@lscu.coop Legal Disclaimer: Information provided in this presentation, including all materials,

2019 Regulatory Compliance School Louisville ~ March 4-8, 2019

2019 Regulatory Compliance School Louisville ~ March 4-8, 2019 Monday, March 4, 2019 Deposit Hot Topics Although deposit regulations have been quiet, examiners have been taking a deep dive into existing

2019 Regulatory Compliance School Louisville ~ March 4-8, 2019 Monday, March 4, 2019 Deposit Hot Topics Although deposit regulations have been quiet, examiners have been taking a deep dive into existing

Hosted By Mike Gallagher October 2017

Risk Management, Compliance and CRA Hosted By Mike Gallagher October 2017 Today s Agenda Risk Management Risk governance Enterprise Risk Management Operational Risk Management Categories of Risk Compliance

Risk Management, Compliance and CRA Hosted By Mike Gallagher October 2017 Today s Agenda Risk Management Risk governance Enterprise Risk Management Operational Risk Management Categories of Risk Compliance

How to Ace Your BSA Exam & Risk Assessment

How to Ace Your BSA Exam & Risk Assessment LeVar Anderson, CAMS, AAP Auditor, Carolinas Credit Union League Agenda NCUA Examiners review compliance with BSA as part of every exam cycle using examination

How to Ace Your BSA Exam & Risk Assessment LeVar Anderson, CAMS, AAP Auditor, Carolinas Credit Union League Agenda NCUA Examiners review compliance with BSA as part of every exam cycle using examination

PowerPoint Presentation INCLUDING COMPLIANCE IN THE BANK S RISK PROGRAM

PowerPoint Presentation INCLUDING COMPLIANCE IN THE BANK S RISK PROGRAM Chuck Lewis Vice President, Compliance Services Missouri Bankers Association Jefferson City, Missouri clewis@mobankers.com 573-301-1884

PowerPoint Presentation INCLUDING COMPLIANCE IN THE BANK S RISK PROGRAM Chuck Lewis Vice President, Compliance Services Missouri Bankers Association Jefferson City, Missouri clewis@mobankers.com 573-301-1884

How to Use This Service

BANKER S GUIDE TO COMPLIANCE How to Use This Service The Banker s Guide to Compliance is written in bankers language and intended for use by bankers. You need not be a lawyer or compliance expert to use

BANKER S GUIDE TO COMPLIANCE How to Use This Service The Banker s Guide to Compliance is written in bankers language and intended for use by bankers. You need not be a lawyer or compliance expert to use

Policy or Policies. Commercial, Lending policy. Consumer, Business Loans Originations & Servicing. Loan origination. Lending policy.

Bank: as of date TABLE OF LAWS AND REGULATIONS CONSUMER PROTECTION LAW...AND MORE (Does not include BSA/AML/OFAC/CIP) REG NAME/Recent Update - Blue generally not included in Consumer Compliance, purple

Bank: as of date TABLE OF LAWS AND REGULATIONS CONSUMER PROTECTION LAW...AND MORE (Does not include BSA/AML/OFAC/CIP) REG NAME/Recent Update - Blue generally not included in Consumer Compliance, purple

Identify and Monitor High- Risk and Money Service Businesses Accounts. Presented by Lynn English Lafayette Federal Credit Union

Identify and Monitor High- Risk and Money Service Businesses Accounts Presented by Lynn English Lafayette Federal Credit Union Key Takeaways After this webinar, participants should have an understanding

Identify and Monitor High- Risk and Money Service Businesses Accounts Presented by Lynn English Lafayette Federal Credit Union Key Takeaways After this webinar, participants should have an understanding

FEDERAL DEPOSIT INSURANCE CORPORATION WASHINGTON, D.C. ) ) ) ) ) ) ) ) ) )

) ) ) ) ) ) ) ) )") FEDERAL DEPOSIT INSURANCE CORPORATION WASHINGTON, D.C. IN THE MATTER OF SHINHAN BANK AMERICA NEW YORK, NEW YORK (INSURED STATE NONMEMBER BANK CONSENT ORDER FDIC-16-0237b The Federal Deposit Insurance Corporation

FEDERAL DEPOSIT INSURANCE CORPORATION WASHINGTON, D.C. IN THE MATTER OF SHINHAN BANK AMERICA NEW YORK, NEW YORK (INSURED STATE NONMEMBER BANK CONSENT ORDER FDIC-16-0237b The Federal Deposit Insurance Corporation

RE: Customer Due Diligence Requirements for Financial Institutions, Docket No. FINCEN

October 3, 2014 Policy Division Financial Crimes Enforcement Network P.O. Box 39 Vienna, VA 22183 RE: Customer Due Diligence Requirements for Financial Institutions, Docket No. FINCEN-2014-0001 VIA ELECTRONIC

October 3, 2014 Policy Division Financial Crimes Enforcement Network P.O. Box 39 Vienna, VA 22183 RE: Customer Due Diligence Requirements for Financial Institutions, Docket No. FINCEN-2014-0001 VIA ELECTRONIC

REAL ESTATE SETTLEMENT PROCEDURES ACT ( RESPA ) POLICY

POLICY") I. INTRODUCTION A. Background and Overview REAL ESTATE SETTLEMENT PROCEDURES ACT ( RESPA ) POLICY The Real Estate Settlement Procedures Act of 1974 ( RESPA ), 12 U.S.C. 2601 et seq., is a consumer disclosure

I. INTRODUCTION A. Background and Overview REAL ESTATE SETTLEMENT PROCEDURES ACT ( RESPA ) POLICY The Real Estate Settlement Procedures Act of 1974 ( RESPA ), 12 U.S.C. 2601 et seq., is a consumer disclosure

FinCEN Proposes to Expand Financial Institution Customer Due Diligence Requirements

August 5, 2014 FinCEN Proposes to Expand Financial Institution Customer Due Diligence Requirements The proposal would require financial institutions to identify beneficial owners of legal entities and

August 5, 2014 FinCEN Proposes to Expand Financial Institution Customer Due Diligence Requirements The proposal would require financial institutions to identify beneficial owners of legal entities and

The Current Regulatory Environment and the Regulatory Compliance Module Update. Cynthia Boehmer, JD January 13, 2016

The Current Regulatory Environment and the Regulatory Compliance Module Update Cynthia Boehmer, JD January 13, 2016 MEMBER OF PKF NORTH AMERICA, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS 2012 Wolf &

The Current Regulatory Environment and the Regulatory Compliance Module Update Cynthia Boehmer, JD January 13, 2016 MEMBER OF PKF NORTH AMERICA, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS 2012 Wolf &

Regulatory Notice 17-40

Regulatory Notice 17-40 FinCEN s Customer Due Diligence Requirements for Financial Institutions and FINRA Rule 3310 FINRA Provides Guidance to Firms Regarding Anti- Money Laundering Program Requirements

Regulatory Notice 17-40 FinCEN s Customer Due Diligence Requirements for Financial Institutions and FINRA Rule 3310 FINRA Provides Guidance to Firms Regarding Anti- Money Laundering Program Requirements

Mortgage Loan Originator SAFE TN Comprehensive Course Mortgage Loan Originator Prelicensing / National Topics 20-Hour Course Syllabus

Mortgage Loan Originator SAFE TN Comprehensive Course Mortgage Loan Originator Prelicensing / National 20-Hour Course Syllabus Course Provider School Name: Tennessee Association of Mortgage Professionals

Mortgage Loan Originator SAFE TN Comprehensive Course Mortgage Loan Originator Prelicensing / National 20-Hour Course Syllabus Course Provider School Name: Tennessee Association of Mortgage Professionals

Temenos USA, Inc All rights reserved.

Temenos USA, Inc. 2017. All rights reserved. TRID: THE REALLY IMPORTANT DETAILS Temenos USA, Inc. 2017. All rights reserved. WHAT YOU WILL LEARN 3 1. Brief Overview a) Coverage b) Key Definitions c) Timing

Temenos USA, Inc. 2017. All rights reserved. TRID: THE REALLY IMPORTANT DETAILS Temenos USA, Inc. 2017. All rights reserved. WHAT YOU WILL LEARN 3 1. Brief Overview a) Coverage b) Key Definitions c) Timing

Payday Lending Provision 2007 Defense Authorization Bill

Payday Lending Provision 2007 Defense Authorization Bill Overview H.R. 5122, the John Warner National Defense Authorization Act for Fiscal Year 2007, includes a provision (Subtitle F, Section 670) originally

Payday Lending Provision 2007 Defense Authorization Bill Overview H.R. 5122, the John Warner National Defense Authorization Act for Fiscal Year 2007, includes a provision (Subtitle F, Section 670) originally

SUMMARY: The Bureau of Consumer Financial Protection (Bureau) is issuing its seventeenth

is issuing its seventeenth") This document is scheduled to be published in the Federal Register on 10/18/2018 and available online at https://federalregister.gov/d/2018-22726, and on govinfo.gov BILLING CODE: 4810-AM-P BUREAU OF CONSUMER

This document is scheduled to be published in the Federal Register on 10/18/2018 and available online at https://federalregister.gov/d/2018-22726, and on govinfo.gov BILLING CODE: 4810-AM-P BUREAU OF CONSUMER

for Boards 2015 Spring Leadership Development Conference

for Boards 2015 Spring Leadership Development Conference With Barb Boyd, CUCE Compliance Content Manager MCUL CU Solutions Group 1 AGENDA Purpose Compliance Culture Compliance Program Reporting Information

for Boards 2015 Spring Leadership Development Conference With Barb Boyd, CUCE Compliance Content Manager MCUL CU Solutions Group 1 AGENDA Purpose Compliance Culture Compliance Program Reporting Information

S Analysis of Regulatory Relief for Credit Union

S. 2155 Analysis of Regulatory Relief for Credit Union June 2018 SECTION Minimum Standards for Residential Mortgage Loans (Section 101) Adds a new safe harbor category of Qualified Mortgages (QMs) to Section

S. 2155 Analysis of Regulatory Relief for Credit Union June 2018 SECTION Minimum Standards for Residential Mortgage Loans (Section 101) Adds a new safe harbor category of Qualified Mortgages (QMs) to Section

Anti-Money Laundering. How to set up a strong Compliance Program

Anti-Money Laundering How to set up a strong Compliance Program Importance of AML Protection Financial institutions face a growing number of threats from criminals that seek to misuse the U.S. financial

Anti-Money Laundering How to set up a strong Compliance Program Importance of AML Protection Financial institutions face a growing number of threats from criminals that seek to misuse the U.S. financial

Introduction. Background on Money Laundering. Background on Terrorist financing. Bank Secrecy Act (Regulations)

") XM - US Compliance Introduction Background on Money Laundering Background on Terrorist financing Bank Secrecy Act (Regulations) How MSB (Money Service Business) can help to prevent Money Laundering & Terrorist

XM - US Compliance Introduction Background on Money Laundering Background on Terrorist financing Bank Secrecy Act (Regulations) How MSB (Money Service Business) can help to prevent Money Laundering & Terrorist

CFPB Supervision and Examination Process

Background Title X of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (the Act) 1 established the Consumer Financial Protection Bureau (CFPB) and authorizes it to supervise certain

Background Title X of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (the Act) 1 established the Consumer Financial Protection Bureau (CFPB) and authorizes it to supervise certain

Trans-Fast Remittance LLC. AML Compliance Training for Agents

Trans-Fast Remittance LLC AML Compliance Training for Agents 2016 Trans-Fast expects all of its agents to adhere to the following: terms of agent agreement; establish AML Program as per Section 352 of

Trans-Fast Remittance LLC AML Compliance Training for Agents 2016 Trans-Fast expects all of its agents to adhere to the following: terms of agent agreement; establish AML Program as per Section 352 of

2/4/2014. Consumer Financial Protection Bureau Update A New Era of Regulation Begins. A Quick Overview of the CFPB. CFPB Overview (cont.

Consumer Financial Protection Bureau Update A New Era of Regulation Begins A Quick Overview of the CFPB The CFPB was created by Title X of the Dodd-Frank Act and became operational on July 21, 2011 Independent

Consumer Financial Protection Bureau Update A New Era of Regulation Begins A Quick Overview of the CFPB The CFPB was created by Title X of the Dodd-Frank Act and became operational on July 21, 2011 Independent

Loan Growth and Compliance Pitfalls

Loan Growth and Compliance Pitfalls presented by LOANLINER Compliance Information provided in this presentation, including all materials, should not be construed as legal services, legal advice, or in

Loan Growth and Compliance Pitfalls presented by LOANLINER Compliance Information provided in this presentation, including all materials, should not be construed as legal services, legal advice, or in

Federal Bank Secrecy Act / Anti-Money Laundering (BSA/AML) Oversight

Oversight") Federal Bank Secrecy Act / Anti-Money Laundering (BSA/AML) Oversight Brief Overview of BSA/AML Requirements and Regulatory Expectations Enforcement Authority Recent Consent Orders / Deferred Prosecution

Federal Bank Secrecy Act / Anti-Money Laundering (BSA/AML) Oversight Brief Overview of BSA/AML Requirements and Regulatory Expectations Enforcement Authority Recent Consent Orders / Deferred Prosecution

Audit Planning PRESENTED BY: MICHAEL L. FORTMAN, CPA SENIOR MANAGER BROK A. LAHRMAN, CPA SENIOR MANAGER

Audit Planning PRESENTED BY: MICHAEL L. FORTMAN, CPA SENIOR MANAGER BROK A. LAHRMAN, CPA SENIOR MANAGER INTRODUCTIONS Michael L. Fortman, CPA Senior Manager Indianapolis, Indiana Brok A. Lahrman, CPA Senior

Audit Planning PRESENTED BY: MICHAEL L. FORTMAN, CPA SENIOR MANAGER BROK A. LAHRMAN, CPA SENIOR MANAGER INTRODUCTIONS Michael L. Fortman, CPA Senior Manager Indianapolis, Indiana Brok A. Lahrman, CPA Senior

Lending to Military Members: The Servicemembers Civil Relief Act and Military Lending Act Final Rule

Lending to Military Members: The Servicemembers Civil Relief Act and Military Lending Act Final Rule Louisiana Bankers Association 2015 Bank Counsel Conference December 11, 2015 Presented by: Laura Brown,

Lending to Military Members: The Servicemembers Civil Relief Act and Military Lending Act Final Rule Louisiana Bankers Association 2015 Bank Counsel Conference December 11, 2015 Presented by: Laura Brown,

Compliance Town Hall Getting Ready for Release

Compliance Town Hall Getting Ready for Release 2017.00 Eleanor Hopkins, NCCO Product Manager, Compliance June 27, 2017 Enhancement dates contained in this document are provided as estimates only and can

Compliance Town Hall Getting Ready for Release 2017.00 Eleanor Hopkins, NCCO Product Manager, Compliance June 27, 2017 Enhancement dates contained in this document are provided as estimates only and can

FINCEN GUIDANCE. Under 31 CFR , an MSB s AML program must, at a minimum:

FIN-2016-G001 Issued: March 11, 2016 Subject: Guidance on Existing AML Program Rule Compliance Obligations for MSB Principals with Respect to Agent Monitoring This guidance reiterates the anti-money laundering

FIN-2016-G001 Issued: March 11, 2016 Subject: Guidance on Existing AML Program Rule Compliance Obligations for MSB Principals with Respect to Agent Monitoring This guidance reiterates the anti-money laundering

Point of view. Analyzing Strategic Regulatory Policy Shifts. Americas FS Regulatory Center of Excellence

Point of view Analyzing Strategic Regulatory Policy Shifts Americas FS Regulatory Center of Excellence Amendments to 2013 Mortgage Servicing Rules under the Real Estate Settlement Procedures Act (Regulation

Point of view Analyzing Strategic Regulatory Policy Shifts Americas FS Regulatory Center of Excellence Amendments to 2013 Mortgage Servicing Rules under the Real Estate Settlement Procedures Act (Regulation

NOTICE: THIS IS ONLY A SAMPLE. DO NOT USE THIS DOCUMENT WITHOUT FIRST CONSULTING WITH LEGAL COUNSEL.

NOTICE: THIS IS ONLY A SAMPLE. DO NOT USE THIS DOCUMENT WITHOUT FIRST CONSULTING WITH LEGAL COUNSEL. THIS DOCUMENT IS A SAMPLE FOR REFERENCE PURPOSES ONLY. PLEASE CONSULT WITH LEGAL COUNSEL BEFORE IMPLEMENTING

NOTICE: THIS IS ONLY A SAMPLE. DO NOT USE THIS DOCUMENT WITHOUT FIRST CONSULTING WITH LEGAL COUNSEL. THIS DOCUMENT IS A SAMPLE FOR REFERENCE PURPOSES ONLY. PLEASE CONSULT WITH LEGAL COUNSEL BEFORE IMPLEMENTING

Compliance Perspectives

Compliance Perspectives Carl Pry November 19, 2015 CFPB Supervisory Highlights Covers exam findings from May 2015 to August 2015 Non-public CFPB supervisory actions resulted in $107 million in restitution

Compliance Perspectives Carl Pry November 19, 2015 CFPB Supervisory Highlights Covers exam findings from May 2015 to August 2015 Non-public CFPB supervisory actions resulted in $107 million in restitution

June 6, Introduction

June 6, 2016 Commission s Secretary Office of the Secretary Federal Communications Commission 445 12th St., SW Room TW-A325 Washington, DC 20554 Submitted via Regulations.gov Subject: Comments of the Consumer

June 6, 2016 Commission s Secretary Office of the Secretary Federal Communications Commission 445 12th St., SW Room TW-A325 Washington, DC 20554 Submitted via Regulations.gov Subject: Comments of the Consumer

Consumer Regulatory Changes

Consumer Regulatory Changes Federal Reserve Board Division of Consumer and Community Affairs August 19, 2010 Visit us at www.consumercomplianceoutlook.org The The opinions expressed in in this this presentation

Consumer Regulatory Changes Federal Reserve Board Division of Consumer and Community Affairs August 19, 2010 Visit us at www.consumercomplianceoutlook.org The The opinions expressed in in this this presentation

S DODD-FRANK ACT REVISIONS REGULATORY RELIEF

July 27, 2018 Vol. XXXV, No. 16 S. 2155 DODD-FRANK ACT REVISIONS REGULATORY RELIEF I. INTRODUCTION President Trump recently signed Senate Bill 2155, the Economic Growth, Regulatory Relief and Consumer

July 27, 2018 Vol. XXXV, No. 16 S. 2155 DODD-FRANK ACT REVISIONS REGULATORY RELIEF I. INTRODUCTION President Trump recently signed Senate Bill 2155, the Economic Growth, Regulatory Relief and Consumer

Consumer Compliance Hot Topics

Consumer Compliance Hot Topics Agenda Regulatory Timeline: Issued in 2014 On the Horizon for 2015 Areas of Supervisory Focus: Fair Lending Unfair or Deceptive Acts or Practices (UDAP) Flood Vendor Management

Consumer Compliance Hot Topics Agenda Regulatory Timeline: Issued in 2014 On the Horizon for 2015 Areas of Supervisory Focus: Fair Lending Unfair or Deceptive Acts or Practices (UDAP) Flood Vendor Management

TRID RULE UPDATES AND THE BLACK HOLE CONUNDRUM JONATHAN FOXX *

TRID RULE UPDATES AND THE BLACK HOLE CONUNDRUM JONATHAN FOXX * On August 11, 2017, the Consumer Financial Protection Bureau ( Bureau ) issued a Final Rule (2017 TILA-RESPA Rule or 2017 Rule, hereinafter

TRID RULE UPDATES AND THE BLACK HOLE CONUNDRUM JONATHAN FOXX * On August 11, 2017, the Consumer Financial Protection Bureau ( Bureau ) issued a Final Rule (2017 TILA-RESPA Rule or 2017 Rule, hereinafter

Mortgage Procedures and Regulations (MPAR) Mortgage Origination Equal Credit Opportunity Act (ECOA) Phase

Mortgage Origination Equal Credit Opportunity Act (ECOA) Phase") Mortgage Procedures and Regulations (MPAR) Mortgage Origination Equal Credit Opportunity Act (ECOA) Phase Sonia Lee Director, Affiliate Financial Service Agenda Today s goal: Equip participants with working

Mortgage Procedures and Regulations (MPAR) Mortgage Origination Equal Credit Opportunity Act (ECOA) Phase Sonia Lee Director, Affiliate Financial Service Agenda Today s goal: Equip participants with working

MORTGAGE BANKERS ASSOCIATION OF ALABAMA

MORTGAGE BANKERS ASSOCIATION OF ALABAMA What s on the horizon for 2017? January 17, 2017 Presented by: J. David Dresher Jason R. Bushby Bradley Arant Boult Cummings LLP Attorney-Client Privilege. Agenda

MORTGAGE BANKERS ASSOCIATION OF ALABAMA What s on the horizon for 2017? January 17, 2017 Presented by: J. David Dresher Jason R. Bushby Bradley Arant Boult Cummings LLP Attorney-Client Privilege. Agenda