Bank Secrecy Act & Anti-Money Laundering for Directors. Mike Lee Director of Regulatory Advocacy

|

|

|

- Nickolas Floyd

- 6 years ago

- Views:

Transcription

1 Bank Secrecy Act & Anti-Money Laundering for Directors Mike Lee Director of Regulatory Advocacy

2 Legal Disclaimer: Information provided in this presentation, including all materials, should not be construed as legal services, legal advice, or in any way establishing an attorney-client relationship. Credit unions should contact their own legal counsel for advice. Information may have changed since this presentation was prepared. This information is intended to only be a summary and is not all inclusive.

3 Goals By the end of this Presentation we will: 1. Identify regulators expectations for CU directors under BSA. 2. Identify the required components of your BSA Compliance Program. 3. Introduce the requirements of the Beneficial Ownership Rule. 4. Review Case Studies of Credit Unions that Failed BSA Compliance.

4 Why are you here? Required annual training Clarified in 05-CU-09. Advisory FIN-2014-A007: The guidance was provided due to shortcomings in compliance due to a lack of involvement from institutions senior management. It pointed to the poor culture of compliance which existed in part due to a lack of leadership to improve and strengthen organizational compliance with Bank Secrecy Act (BSA) obligations.

5 What is a Culture of Compliance? Characteristics defined by FinCEN (FIN-2014-A007): Leadership Should Be Engaged. Compliance Should Not Be Compromised By Revenue Interests. Information Should Be Shared Throughout the Organization. Leadership Should Provide Adequate Human and Technological Resources. The Program Should Be Effective and Tested By an Independent and Competent Party. Leadership and Staff Should Understand How Their BSA Reports are Used.

6 What the BSA Exam Manual says: The board of directors and senior management should be informed of changes and new developments in the BSA...they need to understand the importance of BSA/AML regulatory requirements, the ramifications of noncompliance, and the risks posed to the bank. Without a general understanding of the BSA, the board of directors cannot adequately provide BSA/AML oversight; approve BSA/AML policies, procedures, and processes; or provide sufficient BSA/AML resources.

7 BSA Framework The Law The Bank Secrecy Act and a medley of other statutes (PATRIOT Act). FinCEN Promulgates/enforces the BSA regulations. NCUA Enforces compliance via examination.(12 CFR Part 748) Federal Law Enforcement utilizes data for investigations. Statute Regulation FinCEN Credit Union Compliance Experience Analysis Prosecution Law Enforcement

8 Prevent Money Laundering

9 Then

10 And Now

11 BSA Procedures for monitoring Bank Secrecy Act (BSA) compliance. a) Purpose. This section is issued to ensure that all federally insured credit unions establish and maintain procedures reasonably designed to assure and monitor compliance b) Establishment of a BSA compliance program 1. Program requirement. Each federally insured credit union shall develop and provide for the continued administration of a program reasonably designed to assure and monitor compliance with the recordkeeping and recording requirements The compliance program must be written, approved by the credit union's board of directors, and reflected in the credit union's minutes. 2. Customer identification Program. Each federally insured credit union is subject to the requirements which require a customer identification program to be implemented as part of the BSA compliance program required under this section.

12 Pillars of BSA Compliance 1. Implement proper internal controls to ensure that your BSA program is functioning as intended; 2. Provide training for appropriate personnel, at least annually; 3. Provide adequate annual independent audit procedures; 4. Require the participation of a qualified and knowledgeable BSA officer; 5. Implement Risk Based procedures for Customer Due Diligence / Beneficial Ownership Rule

13 Pillar 1: Internal Controls Biggest Challenge? The board of directors, acting through senior management, is ultimately responsible for ensuring that the bank maintains an effective BSA/AML internal control structure, including suspicious activity monitoring and reporting. The board of directors and management should create a culture of compliance to ensure staff adherence to the bank s BSA/AML policies, procedures, and processes. Internal controls are the bank s policies, procedures, and processes designed to limit and control risks and to achieve compliance with the BSA. The level of sophistication of the internal controls should be commensurate with the size, structure, risks, and complexity of the bank.

14 Pillar 1: Internal Controls Risk Assessment An examiner will review whether the BSA/AML compliance program is adequate and provides the controls necessary to mitigate risks. Step 1: ID Risk Categories - Risks may vary according to: Products and Services Prepaid Cards, remittances Customers MSBs, attorneys, non-resident aliens Geography High Intensity Drug Trafficking Areas (HIDTA): Jefferson, Mobile, Polk, Miami-Dade, Nassau High Intensity Financial Crime Areas (HIFCA) South Florida Step 2: Analyzing the Risk Categories Using CU s data: Purpose of the account. Actual or anticipated activity in the account. Nature of the customer s business/occupation. Customer s location. Types of products and services used by the customer.

15 Pillar 1: Internal Controls SAR Suspicious Activity Report filing required for: Criminal violations involving insider abuse in any amount. Criminal violations aggregating $5,000 or more when a suspect can be identified. Criminal violations aggregating $25,000 or more regardless of a potential suspect. Transactions conducted or attempted by, at or through a credit union aggregating $5,000 or more, of the credit union knows, suspects or has reason to suspect that the transaction: May involve potential money laundering or other illegal activity. Is designed to evade the BSA or its implementing regulations. Has no business or apparent lawful purpose, or is not the type of transaction that the particular member would normally be expected to engage in, and the credit union knows of no reasonable explanation for the transaction.

16 Pillar 1: SAR Systems and Safe Harbor Credit Unions must have policies and procedures in place to monitor systems for suspicious activity, specifically regarding high risk factors and refer those activities to those who investigate and decide whether to file a SAR. The decision to file a SAR is an inherently subjective judgment. CU should not be criticized for the failure to file a SAR unless the failure is significant or accompanied by evidence of bad faith. Federal law (31 USC 5318(g)(3)) provides protection from civil liability for all reports of suspicious transactions made to appropriate authorities.

17 Pillar 1: SAR Filing SARs must be filed: Electronically; No later than 30 days from the detection of facts constituting the basis for filing. If no suspect is identified, the filing is extended to 60 days. 5 year record retention. Board should be kept aware of SAR filings. SARs are confidential, disclosure of the existence or nonexistence of a SAR is prohibited, especially to suspect Member (and associates). Can be shared with Federal law enforcement and NCUA. Must not comply with subpoenas unless requested to do so by LE. Seek Counsel.

18 Pillar 1: Internal Controls CTR File Currency Transaction Report (CTR) for each transaction in currency (deposit, withdrawal, exchange, or other payment or transfer) of more than $10,000. Multiple currency transactions totaling more than $10,000 during any one business day are treated as a single transaction if the credit union has knowledge that they are by or on behalf of the same person. Must be filed within 15 days after the date of the transaction. Bank Secrecy Act Currency Transaction Report (BCTR)/electronic. 5 year record retention.

19 CTRs Use in Investigation (NBC News) Mandalay Bay shooter Stephen Paddock gambled with at least $160,000 in the past several weeks at Las Vegas casinos, according to senior law enforcement officials. There were 16 Currency Transaction Reports, or CTRs, filed for Paddock in recent weeks. The Treasury Department and the IRS mandate that casinos file the reports for "each transaction in currency involving cash-in and cash-out of more than $10,000 in a gaming day." The reports don't show whether Paddock won or lost or both on the days in question. They do show that on same days there were multiple transactions. A source familiar with the investigation told NBC News that Paddock was a frequent player "with the highest status" at Caesars Entertainment properties in Las Vegas.

20 Pillar 2 - Training At a minimum: the credit union s training program must include employees whose duties involve BSA. training should be tailored to the person s specific responsibilities. In addition, an overview of the BSA/AML requirements typically should be given to new staff during employee orientation. The BSA compliance officer should receive periodic training that is relevant and appropriate given changes to regulatory requirements as well as the activities and overall BSA/AML risk profile of the bank. Credit unions should document their training programs.

21 Pillar 3 - Audit months Independent testing should, at a minimum, include: An evaluation of the overall adequacy and effectiveness of the BSA/AML compliance program, including policies, procedures, and processes. A review of the bank s risk assessment Appropriate risk-based transaction testing An evaluation of management s efforts to resolve violations and deficiencies A review of staff training for adequacy, accuracy, and completeness. A review of the effectiveness of the suspicious activity monitoring systems (manual, automated, or a combination) used for BSA/AML compliance.

22 Pillar 4 - Staff : BSA Officer The board of directors is responsible for ensuring that the BSA compliance officer has sufficient authority and resources (monetary, physical, and personnel) to administer an effective BSA/AML compliance program based on the bank s risk profile. The BSA compliance officer should be fully knowledgeable of: the BSA and all related regulations; and the bank s products, services, customers, etc. The BSA compliance officer should regularly apprise the board of directors and senior management of ongoing BSA compliance.

23 CIP: Collect Member Information Purpose: To enable the CU to form a reasonable belief that it knows the identity of each member. 1. Identifying Info: 1. Name 2. DOB for individuals. 3. Address 4. ID= Tax ID = SSN 2. Verifying Info: Documentary - Unexpired government issued identification, such as: A driver s license; Passport; or Military ID. Non-Documentary Information obtained from a credit bureau, or against fraud and bad check databases References from other financial institutions Confirm information such as telephone number and address by contacting member Tax return or a financial statement

24 CIP: Verifying Member Information Procedures explaining verification and non-verification. (Flowchart) Identifying info must be kept for five years after the account is closed. Included in this is documents used to verify the ID, with a full description of such document. Methods used and results of verification. Results of discrepancies in ID. Must include cross reference of ID with federal terrorist list. Must provide notice to applicant that CU is requesting info to identify their ID.

25 Information Sharing - Section 314(a) of the USA PATRIOT Act (31 CFR ) Law Enforcement via FinCEN requests information on suspects. Credit Union must review their current account or those active previous 12 months, or transactions with suspect for six months. Credit Union has 14 days to report matches. Credit Unions must develop policies and procedures to process requests. Credit Union should document its: receipt, review and response. Voluntary Information Sharing Section 314(b) of the USA PATRIOT Act (31 CFR )

List against membership.")

26 OFAC - Office of Foreign Assets Control Enforces sanctions on people, nations, entities. Credit Unions must regularly review the Specially Designated Nationals (SDN) List against membership. Credit Unions must block or reject people or entities on the list and report those transactions to OFAC. Must perform risk assessment: International funds transfers. Nonresident alien accounts. Foreign customer accounts. Etc OFAC compliance pillars are essentially the same as for BSA.

27 Beneficial Owners : Due Diligence Rule May 2018 Must have written procedures designed to Id and verify legal entity members. At minimum the procedures to verify the identity must contain elements of CIP program already in place. develop risk profile regarding member relationships, monitor activities for suspicious transactions. ID beneficial owners when new account is opened by: Using Beneficial Owner Certification Form in Appendix A; or (no safe harbor) Collecting the info asked for on the form. Beneficial Owners Those who own 25% or more of equity interest in a legal entity; & Those who control a legal entity. (CEO, CFO, President, Treasurer) For trusts that own 25% of entity, the beneficial owner is the trustee.

28 Beneficial Owners : Legal Entity Defined Legal Entity means: corp., LLC, or other entity created by filing a public document with Sec. of State. Definition does not include: Financial institutions regulated by Fed. or state. The Fed. or state gov t. Publicly traded companies or their subsidiaries. Issuers of registered securities, investment companies or advisors. Public Accounting firms. Insurance companies regulated by the state. Non-US gov t entity that doesn t engage in commercial activities.

29 Beneficial Owners : Record keeping Credit union must establish procedures for making and maintaining a record of all info obtained under the rule. The record must include at least: For identification: any identifying info in certification. For verification: description of documents relied upon or nondocumentary methods. Records must be retained for 5 years after the account is closed for identification or 5 years after it is made for verification. Compliance date: May 11, 2018

included: $54.8 million in cash orders, $1.")

30 Case Study 1: North Dade Community Development Federal Credit Union FOM: Community charter North Miami-Dade County, FL Employees: 5 Assets: $4.1 million Serviced MSBs outside FOM, performing High Risk activities in High Risk jurisdictions. 2013: MSBs transactions (90% of revenue) included: $54.8 million in cash orders, $1.01 billion in outgoing wires, $5.3 million in returned checks, $984.4 million in remote deposit capture. NCUA ordered C&D in 2013.

31 North Dade s compliance with BSA: 1. Internal Controls Failed to assess money laundering and terrorist financing risks. Risk assessment wasn t performed from 2009 until Nov Inadequate controls to monitor suspicious activity and 3 rd party vendors. 56 MSB accounts were serviced rather than the 1 vendor, without additional assessments or monitoring. From , one person accounted for 60% of business banking, they filed over 2000 CTRs, but didn t monitor the account as high risk. Failed to follow policy on MSBs without licenses, continued to service MSBs. 2. BSA Officer- failed to designate. 3. Training- No record of Board or employee BSA training. 4. Audit: Had no evidence of BSA audit prior to C & D.

32 North Dade s compliance with BSA: 3. Member Identification Program Failed to ID MSBs. By not knowing its members, North Dade was not capable of understanding their expected transactional behavior and thus was unable to appropriately monitor for suspicious activities. 4. SAR Reporting: - Filed only 15 SARs in a 3 year period. Failed to file SAR after Law Enforcement seized $1.5 million from MSB owner/member. 5. Review 314(a) lists: Failed to review lists for 2 years. FinCen Fine: $300,000 Result: Liquidiation

. Did not update internal controls.")

33 Case Study 2: FOM: low-moderate income in Bronx, NY Employees: 22 Maintained internal controls to its membership since In 2011, began servicing MSBs, including those in high risk jurisdictions with high risk activities (wires to Middle East). Did not update internal controls. Relied on vendor for Due Diligence and monitoring of MSBs.

34 Bethex s compliance with BSA: 1. Internal Controls In 2010, Bethex processed $657 million domestic transactions. In 2012, Bethex processed over $4 billion in domestic and international transactions, an increase of more than 300% with modifying its controls. Generated high fee income. Failed to conduct risk assessment while transacting in 30 countries, some high risk. Failed to perform Due Diligence four MSBs owned by one person at one address, serviced one Mexican MSB wasn t monitored. Failed to monitor suspicious activities, had insufficient staff. 2. BSA Officer Failed to have BSA officer with sufficient experience, authority, and resources to ensure compliance. Willfully undermined controls by sending multiple wires under policy threshold.

35 Bethex s compliance with BSA: 3. Audit: Ignored auditor findings. 4. Training- Inadequate Suspicious Activity Reporting: Failed to file SARs for wires with high dollar amounts to Middle East. SARs were filed late and were inadequate. FinCen Fine: $500,000 Result: Liquidiation

36 Takeaway from FinCEN Enforcement Actions. 1. Internal Controls: Don t rely on 3 rd party vendors for compliance. Don t wire money abroad. Don t service MSBs. Do - Update controls annually, specifically when introducing new products and services. 2. BSA Officer- Hire sufficient and competent staff 3. Training- Annual training for Board and relevant employees. 4. Audit: Independent. Listen to them.

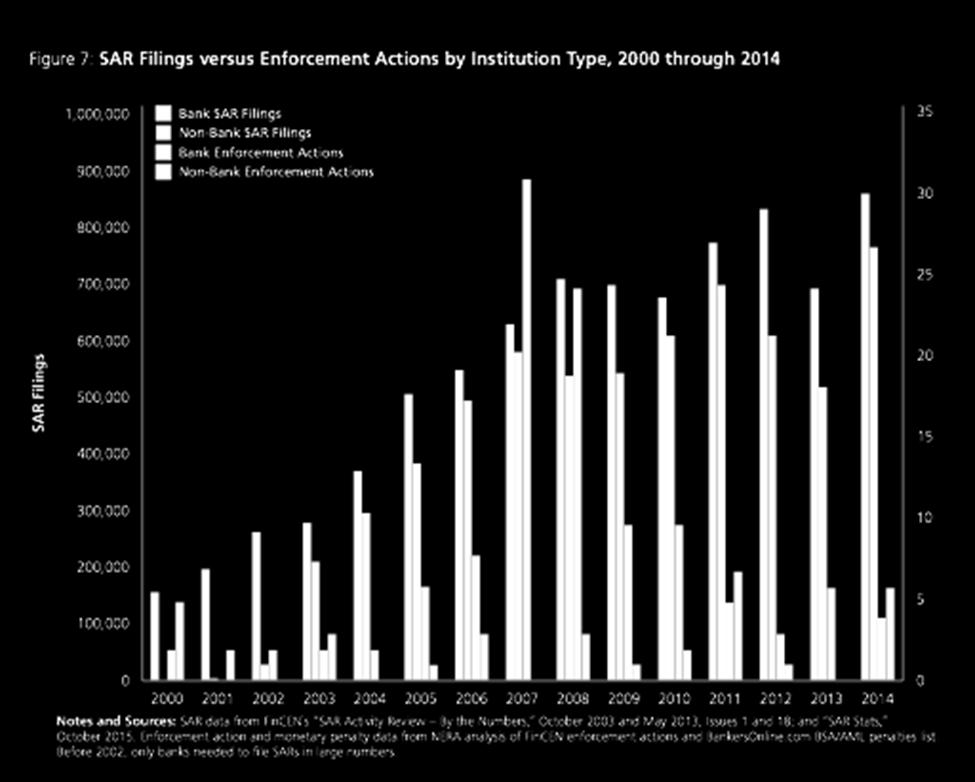

37 SAR Filing Data Month January - 12,232 65,898 66,101 70,460 February - 21,088 61,637 65,984 73,927 March 24 45,719 64,462 73,420 83,964 April ,278 73,302 74,049 81,282 May 1,210 72,255 75,301 68,216 80,822 June 1,713 63,579 71,773 77,162 91,400 July 2,505 70,857 75,559 77,508 83,284 August 3,115 74,312 70,856 75,503 84,726 September 2,947 68,751 70,703 75,863 78,014 October 5,561 79,201 77,735 78,096 76,943 November 7,954 69,631 63,761 71,500 75,599 December 10,098 69,027 68,327 76,505 78,116 Subtotal 35, , , , ,537 Total Filings 3,427,424

38

39 Civil Monetary Penalties After 1/15/17 12 U.S.C. 1829b(j) Relating to Recordkeeping Violations For Funds Transfers $20, U.S.C Willful or Grossly Negligent Recordkeeping Violations 20, U.S.C. 5318(k)(3)(C) Failure to Terminate Correspondent Relationship with Foreign Bank 31 U.S.C. 5321(a)(1) General Civil Penalty Provision for Willful Violations of Bank Secrecy Act Requirements 31 U.S.C. Foreign Financial Agency Transaction Non-Willful Violation 5321(a)(5)(B)(i) of Transaction 31 U.S.C. 5321(a)(5)(C) Foreign Financial Agency Transaction Willful Violation of Transaction 31 U.S.C. 5321(a)(6)(A) Negligent Violation by Financial Institution or Non-Financial Trade or Business 31 U.S.C. 5321(a)(6)(B) Pattern of Negligent Activity by Financial Institution or Non- Financial Trade or Business 31 U.S.C. 5321(a)(7) Violation of Certain Due Diligence Requirements, Prohibition on Correspondent Accounts for Shell Banks, and Special Measures 31 U.S.C. 5330(e) Civil Penalty for Failure to Register as Money Transmitting Business 13,603 54,789 $219,156 12, ,626 1,096 85,236 1,360,317 8,084

40

41 Advocate for Changing BSA Regime Recommendations for Changes by FAITH LLEVA ANDERSON of American Airlines FCU at House Financial Services Committee hearing titled, Examining the BSA/AML Regulatory Compliance Regime. 1. SAR and CTR Forms Should Be Combined 2. Reporting Thresholds and Deadline to File Should Be Increased to Reflect Today s Environment. ($20k $50k) 3. Beneficial Owner and Beneficiaries Requirements 4. Monetary Instrument Purchases Remove Separate Documentation.

42 Upcoming Events: BSA Seminar by Federal Law Enforcement Jan. 30 Birmingham, AL Jan. 31 Huntsville, AL Note: The last element of the culture of compliance. Nov. 7 Compliance Meeting Avadian CU, Birmingham.

BSA/AML & OFAC Volunteer Compliance Training. Agenda

Ideas + Solutions = Success BSA/AML & OFAC Volunteer Compliance Training Ideas + Solutions = Success Presented by Dorie Fitchett HCUL Regulatory Officer May 17, 2018 Agenda 1. Bank Secrecy Act 2. Office

Ideas + Solutions = Success BSA/AML & OFAC Volunteer Compliance Training Ideas + Solutions = Success Presented by Dorie Fitchett HCUL Regulatory Officer May 17, 2018 Agenda 1. Bank Secrecy Act 2. Office

for Boards 2015 Spring Leadership Development Conference

for Boards 2015 Spring Leadership Development Conference With Barb Boyd, CUCE Compliance Content Manager MCUL CU Solutions Group 1 AGENDA Purpose Compliance Culture Compliance Program Reporting Information

for Boards 2015 Spring Leadership Development Conference With Barb Boyd, CUCE Compliance Content Manager MCUL CU Solutions Group 1 AGENDA Purpose Compliance Culture Compliance Program Reporting Information

Bank Secrecy Act for Directors

Bank Secrecy Act for Directors Agenda What is the Bank Secrecy Act? How to have a successful BSA Compliance Program? OFAC responsibilities. Penalties for non-compliance. 2 What is the Bank Secrecy Act?

Bank Secrecy Act for Directors Agenda What is the Bank Secrecy Act? How to have a successful BSA Compliance Program? OFAC responsibilities. Penalties for non-compliance. 2 What is the Bank Secrecy Act?

2015 Bank Secrecy Act

2015 Erin O Hern, Director of League Compliance Services The services of PolicyWorks and this presentation, including all materials, should not be construed as legal services, legal advice, or in any way

2015 Erin O Hern, Director of League Compliance Services The services of PolicyWorks and this presentation, including all materials, should not be construed as legal services, legal advice, or in any way

Bank Secrecy Act and OFAC Compliance Board of Directors Training

Bank Secrecy Act and OFAC Compliance Board of Directors Training Introduction Today s presenters: Karen M. Janota Assurance Manager Disclaimer: The contents of this presentation are intended to provide

Bank Secrecy Act and OFAC Compliance Board of Directors Training Introduction Today s presenters: Karen M. Janota Assurance Manager Disclaimer: The contents of this presentation are intended to provide

Bank Secrecy Act for Volunteers Southeast Leadership Development Conference Destin, Florida November 5, 2015

Bank Secrecy Act for Volunteers Southeast Leadership Development Conference Destin, Florida November 5, 2015 April N. Ales, BSACS, CCUFC, CUDE Overview of Presentation What Laws Govern Money Laundering

Bank Secrecy Act for Volunteers Southeast Leadership Development Conference Destin, Florida November 5, 2015 April N. Ales, BSACS, CCUFC, CUDE Overview of Presentation What Laws Govern Money Laundering

Trans-Fast Remittance LLC. AML Compliance Training for Agents

Trans-Fast Remittance LLC AML Compliance Training for Agents 2016 Trans-Fast expects all of its agents to adhere to the following: terms of agent agreement; establish AML Program as per Section 352 of

Trans-Fast Remittance LLC AML Compliance Training for Agents 2016 Trans-Fast expects all of its agents to adhere to the following: terms of agent agreement; establish AML Program as per Section 352 of

How to Ace Your BSA Exam & Risk Assessment

How to Ace Your BSA Exam & Risk Assessment LeVar Anderson, CAMS, AAP Auditor, Carolinas Credit Union League Agenda NCUA Examiners review compliance with BSA as part of every exam cycle using examination

How to Ace Your BSA Exam & Risk Assessment LeVar Anderson, CAMS, AAP Auditor, Carolinas Credit Union League Agenda NCUA Examiners review compliance with BSA as part of every exam cycle using examination

CUSTOMER DUE DILIGENC

CUSTOMER DUE DILIGENC of the Bank Secrecy Act Coverage: Federally insured credit unions Agency/Citation: FinCEN 31 CFR Parts 1010, 1020, 1023, 1024 and 1026 Effective Date: May 11, 2018 EXECUTIVE SUMMARY

CUSTOMER DUE DILIGENC of the Bank Secrecy Act Coverage: Federally insured credit unions Agency/Citation: FinCEN 31 CFR Parts 1010, 1020, 1023, 1024 and 1026 Effective Date: May 11, 2018 EXECUTIVE SUMMARY

UNITED STATES OF AMERICA DEPARTMENT OF THE TREASURY FINANCIAL CRIMES ENFORCEMENT NETWORK ASSESSMENT OF CIVIL MONEY PENALTY

UNITED STATES OF AMERICA DEPARTMENT OF THE TREASURY FINANCIAL CRIMES ENFORCEMENT NETWORK IN THE MATTER OF: ) ) ) ) Number 2017-02 Merchants Bank of California, N.A. ) Carson, California ) ASSESSMENT OF

UNITED STATES OF AMERICA DEPARTMENT OF THE TREASURY FINANCIAL CRIMES ENFORCEMENT NETWORK IN THE MATTER OF: ) ) ) ) Number 2017-02 Merchants Bank of California, N.A. ) Carson, California ) ASSESSMENT OF

Anti-Money Laundering and Terrorist Financing Prevention Compliance Program Creation Guide

Anti-Money Laundering and Terrorist Financing Prevention Compliance Program Creation Guide Compliance Program Creation Guide January 2015 1 Compliance Program Creation Guide January 2015 2 Insert Business

Anti-Money Laundering and Terrorist Financing Prevention Compliance Program Creation Guide Compliance Program Creation Guide January 2015 1 Compliance Program Creation Guide January 2015 2 Insert Business

Federal Bank Secrecy Act / Anti-Money Laundering (BSA/AML) Oversight

Oversight") Federal Bank Secrecy Act / Anti-Money Laundering (BSA/AML) Oversight Brief Overview of BSA/AML Requirements and Regulatory Expectations Enforcement Authority Recent Consent Orders / Deferred Prosecution

Federal Bank Secrecy Act / Anti-Money Laundering (BSA/AML) Oversight Brief Overview of BSA/AML Requirements and Regulatory Expectations Enforcement Authority Recent Consent Orders / Deferred Prosecution

Protecting Native American casinos from money-laundering risks

Protecting Native American casinos from money-laundering risks For the vast majority of patrons, Native American casinos are ideal destinations for entertainment and leisure. Casinos are cash-intensive

Protecting Native American casinos from money-laundering risks For the vast majority of patrons, Native American casinos are ideal destinations for entertainment and leisure. Casinos are cash-intensive

Bank Secrecy Act. CUNA Must Know Mondays. November 17, 2014

Bank Secrecy Act CUNA Must Know Mondays November 17, 2014 1 David A. Reed Attorney at Law Reed & Jolly, PLLC Fairfax, Virginia david@reedandjolly.com (703) 675-9578 2 2 The contents of this presentation

Bank Secrecy Act CUNA Must Know Mondays November 17, 2014 1 David A. Reed Attorney at Law Reed & Jolly, PLLC Fairfax, Virginia david@reedandjolly.com (703) 675-9578 2 2 The contents of this presentation

Practical Suggestions for an Effective AML/OFAC Compliance Function

Practical Suggestions for an Effective AML/OFAC Compliance Function Institute of International Bankers 2013 Annual Anti-Money Laundering Seminar Paul S. Pilecki May 7, 2013 2013 Kilpatrick Townsend Recent

Practical Suggestions for an Effective AML/OFAC Compliance Function Institute of International Bankers 2013 Annual Anti-Money Laundering Seminar Paul S. Pilecki May 7, 2013 2013 Kilpatrick Townsend Recent

Anti-Money Laundering and Terrorist Financing Prevention Compliance Program Creation Guide

Anti-Money Laundering and Terrorist Financing Prevention Compliance Program Creation Guide Insert Business Name Here Date of Adoption of this Anti-Money Laundering Program ANTI-MONEY LAUNDERING AND TERRORIST

Anti-Money Laundering and Terrorist Financing Prevention Compliance Program Creation Guide Insert Business Name Here Date of Adoption of this Anti-Money Laundering Program ANTI-MONEY LAUNDERING AND TERRORIST

Jamie L. Howell, CUCE

Bank Secrecy Act Jamie L. Howell, CUCE 20 years in credit unions; has worked with dozens of CUs worldwide Specializing in training & education Credit Union Compliance Expert (CUCE) since 2006 Spent 2+

Bank Secrecy Act Jamie L. Howell, CUCE 20 years in credit unions; has worked with dozens of CUs worldwide Specializing in training & education Credit Union Compliance Expert (CUCE) since 2006 Spent 2+

Anti-Money Laundering. How to set up a strong Compliance Program

Anti-Money Laundering How to set up a strong Compliance Program Importance of AML Protection Financial institutions face a growing number of threats from criminals that seek to misuse the U.S. financial

Anti-Money Laundering How to set up a strong Compliance Program Importance of AML Protection Financial institutions face a growing number of threats from criminals that seek to misuse the U.S. financial

Bank Secrecy Act (BSA)/Anti-Money Laundering (AML) Employee & Agent Training

/Anti-Money Laundering (AML) Employee & Agent Training") Bank Secrecy Act (BSA)/Anti-Money Laundering (AML) Employee & Agent Training OVERVIEW The Bank Secrecy Act, or BSA, was passed by congress in 1970. The BSA required banks to maintain records of certain

Bank Secrecy Act (BSA)/Anti-Money Laundering (AML) Employee & Agent Training OVERVIEW The Bank Secrecy Act, or BSA, was passed by congress in 1970. The BSA required banks to maintain records of certain

TokenLot, LLC BSA Officer TokenLot, LLC Board of Directors

Bank Secrecy Act (BSA)/Anti-Money Laundering (AML) Program APPROVED BY TokenLot, LLC BSA Officer TokenLot, LLC Board of Directors TokenLot, LLC BSA/AML Program 2017 1 TABLE OF CONTENTS 1. Bank Secrecy

Bank Secrecy Act (BSA)/Anti-Money Laundering (AML) Program APPROVED BY TokenLot, LLC BSA Officer TokenLot, LLC Board of Directors TokenLot, LLC BSA/AML Program 2017 1 TABLE OF CONTENTS 1. Bank Secrecy

Bank Secrecy Act- USA Patriot Act Compliance

Bank Secrecy Act- USA Patriot Act Compliance Federal Laws Regulating Money Service Businesses Bank Secrecy Act (1970) Establishes recording of high dollar transactions & the reporting of suspicious activity

Bank Secrecy Act- USA Patriot Act Compliance Federal Laws Regulating Money Service Businesses Bank Secrecy Act (1970) Establishes recording of high dollar transactions & the reporting of suspicious activity

Identify and Monitor High- Risk and Money Service Businesses Accounts. Presented by Lynn English Lafayette Federal Credit Union

Identify and Monitor High- Risk and Money Service Businesses Accounts Presented by Lynn English Lafayette Federal Credit Union Key Takeaways After this webinar, participants should have an understanding

Identify and Monitor High- Risk and Money Service Businesses Accounts Presented by Lynn English Lafayette Federal Credit Union Key Takeaways After this webinar, participants should have an understanding

Bank Secrecy Act OFAC FinCEN

Bank Secrecy Act OFAC FinCEN 2017 CREDIT UNION VOLUNTEER TRAINING Financial Crimes Identify Track Report Common BSA Acronyms CIP CDD CTR SAR FinCEN OFAC Customer Identification Program Customer Due Diligence

Bank Secrecy Act OFAC FinCEN 2017 CREDIT UNION VOLUNTEER TRAINING Financial Crimes Identify Track Report Common BSA Acronyms CIP CDD CTR SAR FinCEN OFAC Customer Identification Program Customer Due Diligence

UNITED STATES OF AMERICA DEPARTMENT OF THE TREASURY FINANCIAL CRIMES ENFORCEMENT NETWORK

UNITED STATES OF AMERICA DEPARTMENT OF THE TREASURY FINANCIAL CRIMES ENFORCEMENT NETWORK ZIONS FIRST NATIONAL BANK SAL T LAKE CITY, UTAH Under the authority of the Bank Secrecy Act ("BSA") and regulations

UNITED STATES OF AMERICA DEPARTMENT OF THE TREASURY FINANCIAL CRIMES ENFORCEMENT NETWORK ZIONS FIRST NATIONAL BANK SAL T LAKE CITY, UTAH Under the authority of the Bank Secrecy Act ("BSA") and regulations

Introduction. Background on Money Laundering. Background on Terrorist financing. Bank Secrecy Act (Regulations)

") XM - US Compliance Introduction Background on Money Laundering Background on Terrorist financing Bank Secrecy Act (Regulations) How MSB (Money Service Business) can help to prevent Money Laundering & Terrorist

XM - US Compliance Introduction Background on Money Laundering Background on Terrorist financing Bank Secrecy Act (Regulations) How MSB (Money Service Business) can help to prevent Money Laundering & Terrorist

Bank Secrecy Act Examination Procedures. Sections 313, 314, and 319(b) of the USA PATRIOT Act (31 CFR , , , 103.

of the USA PATRIOT Act (31 CFR , , , 103.") Bank Secrecy Act Examination Procedures Sections 313, 314, and 319(b) of the USA PATRIOT Act (31 CFR 103.100, 103.110, 103.177, 103.185) Table of Contents Correspondent Accounts for Foreign Shell Banks

Bank Secrecy Act Examination Procedures Sections 313, 314, and 319(b) of the USA PATRIOT Act (31 CFR 103.100, 103.110, 103.177, 103.185) Table of Contents Correspondent Accounts for Foreign Shell Banks

Developments in Anti-Money Laundering Regulation for Investment Advisers and Funding Portals. May 2016

Developments in Anti-Money Laundering Regulation for Investment Advisers and Funding Portals May 2016 John L. Sullivan Washington, D.C. jlsullivan@wsgr.com Michael Chiswick-Patterson Washington, D.C. mchiswickpatterson@wsgr.com

Developments in Anti-Money Laundering Regulation for Investment Advisers and Funding Portals May 2016 John L. Sullivan Washington, D.C. jlsullivan@wsgr.com Michael Chiswick-Patterson Washington, D.C. mchiswickpatterson@wsgr.com

AGENT ANTI-MONEY LAUNDERING COMPLIANCE PROGRAM FOR MONEY ORDER SALES

AGENT ANTI-MONEY LAUNDERING COMPLIANCE PROGRAM FOR MONEY ORDER SALES Revision as of January 17, 2018 Explanation/Training Video Link: www.northamericanmoneyorder.com/aml This Program should be reviewed

AGENT ANTI-MONEY LAUNDERING COMPLIANCE PROGRAM FOR MONEY ORDER SALES Revision as of January 17, 2018 Explanation/Training Video Link: www.northamericanmoneyorder.com/aml This Program should be reviewed

10 ESSENTIAL TERMS FOR BITCOIN REGULATION

In March 2013, the U.S. Financial Crimes Enforcement Network (FinCEN) classified Bitcoin and Virtual Currency exchanges as Money Services Businesses (MSB s) in the U.S., which are financial businesses

In March 2013, the U.S. Financial Crimes Enforcement Network (FinCEN) classified Bitcoin and Virtual Currency exchanges as Money Services Businesses (MSB s) in the U.S., which are financial businesses

BSA/AML/OFAC for Bankers Jennifer Morrison Education Chair, COAFP for Buckeye Financial Forum, April 24, 2017

BSA/AML/OFAC for Bankers Jennifer Morrison Education Chair, COAFP for Buckeye Financial Forum, April 24, 2017 Disclaimer The following represents the opinions of the presenter, not those of my employer,

BSA/AML/OFAC for Bankers Jennifer Morrison Education Chair, COAFP for Buckeye Financial Forum, April 24, 2017 Disclaimer The following represents the opinions of the presenter, not those of my employer,

ANTI-MONEY LAUNDERING IN

ANTI-MONEY LAUNDERING IN THE ACQUIRING INDUSTRY Presented by Laura H. Goldzung, CAMS, CCFE, CFCF, CCRP AML Audit Services, LLC March 8, 2016 AGENDA AML Regulatory Overview OFAC Regulatory Overview AML

ANTI-MONEY LAUNDERING IN THE ACQUIRING INDUSTRY Presented by Laura H. Goldzung, CAMS, CCFE, CFCF, CCRP AML Audit Services, LLC March 8, 2016 AGENDA AML Regulatory Overview OFAC Regulatory Overview AML

UNITED STATES OF AMERICA DEPARTMENT OF THE TREASURY FINANCIAL CRIMES ENFORCEMENT NETWORK

UNITED STATES OF AMERICA DEPARTMENT OF THE TREASURY FINANCIAL CRIMES ENFORCEMENT NETWORK IN THE MATTER OF: ) ) ) ) Number 2017-04 Lone Star National Bank ) Pharr, Texas ) ASSESSMENT OF CIVIL MONEY PENALTY

UNITED STATES OF AMERICA DEPARTMENT OF THE TREASURY FINANCIAL CRIMES ENFORCEMENT NETWORK IN THE MATTER OF: ) ) ) ) Number 2017-04 Lone Star National Bank ) Pharr, Texas ) ASSESSMENT OF CIVIL MONEY PENALTY

Federal Reserve Bank of Dallas

ll K Federal Reserve Bank of Dallas 2200 N. PEARL ST. DALLAS, TX 75201-2272 October 31, 2003 Notice 03-63 TO: The Chief Executive Officer of each financial institution and others concerned in the Eleventh

ll K Federal Reserve Bank of Dallas 2200 N. PEARL ST. DALLAS, TX 75201-2272 October 31, 2003 Notice 03-63 TO: The Chief Executive Officer of each financial institution and others concerned in the Eleventh

CITIZENS, INC. BANK SECRECY ACT/ ANTI-MONEY LAUNDERING POLICY AND PROGRAM

I. Introduction CITIZENS, INC. BANK SECRECY ACT/ ANTI-MONEY LAUNDERING POLICY AND PROGRAM The Bank Secrecy Act/Anti-Money Laundering Responsibilities of Insurance Companies U.S. insurance companies have

I. Introduction CITIZENS, INC. BANK SECRECY ACT/ ANTI-MONEY LAUNDERING POLICY AND PROGRAM The Bank Secrecy Act/Anti-Money Laundering Responsibilities of Insurance Companies U.S. insurance companies have

Beneficial Ownership Rules. Iowa Bankers Association

Beneficial Ownership Rules Iowa Bankers Association November 2017 TABLE OF CONTENTS Program Description and Purpose... 1 FinCEN s Regulation X Beneficial Ownership... 2 Definitions... 3 BSA/AML Program

Beneficial Ownership Rules Iowa Bankers Association November 2017 TABLE OF CONTENTS Program Description and Purpose... 1 FinCEN s Regulation X Beneficial Ownership... 2 Definitions... 3 BSA/AML Program

Bank Secrecy Act 101 Fall Colleen Kelly & Valerie Moss CUNA Compliance

Bank Secrecy Act 101 Fall 2016 Colleen Kelly & Valerie Moss CUNA Compliance BSA: COMBAT ILLICIT FINANCIAL TRANSACTIONS BSA Reporting Homeland Security: The only way to stop ISIS is to cut off their money

Bank Secrecy Act 101 Fall 2016 Colleen Kelly & Valerie Moss CUNA Compliance BSA: COMBAT ILLICIT FINANCIAL TRANSACTIONS BSA Reporting Homeland Security: The only way to stop ISIS is to cut off their money

New Coordinates. Boards of Directors Face Growing AML Accountability By Saverio Mirarchi

From New Coordinates Boards of Directors Face Growing AML Accountability By Saverio Mirarchi Bank Boards of Directors are coming under mounting pressure to ensure effective Anti-Money Laundering (AML)

From New Coordinates Boards of Directors Face Growing AML Accountability By Saverio Mirarchi Bank Boards of Directors are coming under mounting pressure to ensure effective Anti-Money Laundering (AML)

Bank Secrecy Act for Operations Staff

Bank Secrecy Act for Operations Staff Presented by Jan Vogel, Center for Professional Development WilliamsTown Communications, Contributing Writer #TR1118 l Introduction Welcome to CUNA s Bank Secrecy

Bank Secrecy Act for Operations Staff Presented by Jan Vogel, Center for Professional Development WilliamsTown Communications, Contributing Writer #TR1118 l Introduction Welcome to CUNA s Bank Secrecy

was either an actual or potential victim of a criminal violation, or series of criminal violations, or that the

Title 12 NCUA 12 CFR 707.9 Enforcement and record retention. (a) Administrative enforcement. Section 270 of TISA (12 U.S.C. 4309) contains the provisions relating to administrative sanctions for failure

Title 12 NCUA 12 CFR 707.9 Enforcement and record retention. (a) Administrative enforcement. Section 270 of TISA (12 U.S.C. 4309) contains the provisions relating to administrative sanctions for failure

ANTI-MONEY LAUNDERING COMPLIANCE GUIDE

ANTI-MONEY LAUNDERING COMPLIANCE GUIDE Revision as of January 17, 2018 This revision supersedes and replaces all other Anti-Money Laundering Compliance Guides issued by North American Money Order Company,

ANTI-MONEY LAUNDERING COMPLIANCE GUIDE Revision as of January 17, 2018 This revision supersedes and replaces all other Anti-Money Laundering Compliance Guides issued by North American Money Order Company,

POLICY: USA Patriot Act and Customer Identification Program (CIP) Policy. Purpose. Policy Goal. General Provisions. Reviewed by and Date:

Policy. Purpose. Policy Goal. General Provisions. Reviewed by and Date:") Purpose The Board of Directors of NorthPark Community Credit Union (hereafter NPCCU) adopted this Customer Identification Program (CIP) policy, as required by Section 326 of the USA Patriot Act. This CIP

Purpose The Board of Directors of NorthPark Community Credit Union (hereafter NPCCU) adopted this Customer Identification Program (CIP) policy, as required by Section 326 of the USA Patriot Act. This CIP

BSA/AML Literacy Test 1

BSA/AML Literacy Test 1 Please Note: The Basic Training consists of three videos approximately 15 minutes each, and should be viewed first. A lot of the following material is also to be found in the Basic

BSA/AML Literacy Test 1 Please Note: The Basic Training consists of three videos approximately 15 minutes each, and should be viewed first. A lot of the following material is also to be found in the Basic

Implementing New CDD Rules for BSA Part I Legal Entities 2016

Implementing New CDD Rules for BSA Part I Legal Entities 2016 The material used in this text has been drawn from sources believed to be reliable. Every effort has been made to assure the accuracy of the

Implementing New CDD Rules for BSA Part I Legal Entities 2016 The material used in this text has been drawn from sources believed to be reliable. Every effort has been made to assure the accuracy of the

ACFE and ACAMS South Florida Chapter 2015 AML/Fraud Conference

ACFE and ACAMS South Florida Chapter 2015 AML/Fraud Conference Marc Benson Director, Global Investigations & Compliance Navigant Consulting Inc. Salvatore LaScala Managing Director, Global Investigations

ACFE and ACAMS South Florida Chapter 2015 AML/Fraud Conference Marc Benson Director, Global Investigations & Compliance Navigant Consulting Inc. Salvatore LaScala Managing Director, Global Investigations

OFAC Compliance Officer Responsibilities. OFAC Regulations. Transactions Subject to OFAC. Reviewed by and Date:

OFAC Compliance Officer Responsibilities NorthPark has designated as the BSA/CIP/OFAC Compliance Officer. The BSA Officer will maintain and update the policies. At least annually the policy will be reviewed

OFAC Compliance Officer Responsibilities NorthPark has designated as the BSA/CIP/OFAC Compliance Officer. The BSA Officer will maintain and update the policies. At least annually the policy will be reviewed

BENEFICIAL OWNERSHIP REFERENCE GUIDE

Sterling COMPLIANCE BENEFICIAL OWNERSHIP REFERENCE GUIDE FACILITATE THOUGHT ENGAGE DIALOGUE ENCOURAGE SMART RISK CULTIVATE A NETWORK BUILD KNOWLEDGE IN THIS GUIDE The documents within this package were

Sterling COMPLIANCE BENEFICIAL OWNERSHIP REFERENCE GUIDE FACILITATE THOUGHT ENGAGE DIALOGUE ENCOURAGE SMART RISK CULTIVATE A NETWORK BUILD KNOWLEDGE IN THIS GUIDE The documents within this package were

BSA/AML ENFORCEMENT. See 12 U.S.C (2000).

.") MONEY LAUNDERING AND CRIMINAL PROSECUTIONS OF BANKS: A FOCUS OF BANK ENFORCEMENT ACTIVITY IN RECENT YEARS By Thomas P. Vartanian and Dominic A. Labitzky * Bank Secrecy Act and Anti-Money Laundering (BSA/AML)

MONEY LAUNDERING AND CRIMINAL PROSECUTIONS OF BANKS: A FOCUS OF BANK ENFORCEMENT ACTIVITY IN RECENT YEARS By Thomas P. Vartanian and Dominic A. Labitzky * Bank Secrecy Act and Anti-Money Laundering (BSA/AML)

AUTO-OWNERS ASSOCIATES CREDIT UNION POLICY AND PROCEDURES MANUAL

Reviewed/Approved by Board of Directors: September 20, 2011 Page 1 of 16 BSA/AML Compliance Auto-Owners Associates Credit Union s (AOACU) Bank Secrecy Act (BSA) Program will include internal policies,

Reviewed/Approved by Board of Directors: September 20, 2011 Page 1 of 16 BSA/AML Compliance Auto-Owners Associates Credit Union s (AOACU) Bank Secrecy Act (BSA) Program will include internal policies,

NOTICE: THIS IS ONLY A SAMPLE. DO NOT USE THIS DOCUMENT WITHOUT FIRST CONSULTING WITH LEGAL COUNSEL.

NOTICE: THIS IS ONLY A SAMPLE. DO NOT USE THIS DOCUMENT WITHOUT FIRST CONSULTING WITH LEGAL COUNSEL. THIS DOCUMENT IS A SAMPLE FOR REFERENCE PURPOSES ONLY. PLEASE CONSULT WITH LEGAL COUNSEL BEFORE IMPLEMENTING

NOTICE: THIS IS ONLY A SAMPLE. DO NOT USE THIS DOCUMENT WITHOUT FIRST CONSULTING WITH LEGAL COUNSEL. THIS DOCUMENT IS A SAMPLE FOR REFERENCE PURPOSES ONLY. PLEASE CONSULT WITH LEGAL COUNSEL BEFORE IMPLEMENTING

ANTI-MONEY LAUNDERING FOR LENDERS

ANTI-MONEY LAUNDERING FOR LENDERS A webinar for MBA members Ari Karen Offit Kurman akaren@offitkurman.com 240.507.1740 Bill Heyman Offit Kurman wheyman@offitkurman.com 301.575.0393 AGENDA Today we will

ANTI-MONEY LAUNDERING FOR LENDERS A webinar for MBA members Ari Karen Offit Kurman akaren@offitkurman.com 240.507.1740 Bill Heyman Offit Kurman wheyman@offitkurman.com 301.575.0393 AGENDA Today we will

Sanctions Risk Management Symposium

What U.S. Federal Bank Examiners Look For in Their OFAC Compliance Examinations Tuesday, September 19, 2017, 10:30 11:15 AM Michaela Arndt Head, Sanctions Compliance, Americas and Group Head, US Sanctions

What U.S. Federal Bank Examiners Look For in Their OFAC Compliance Examinations Tuesday, September 19, 2017, 10:30 11:15 AM Michaela Arndt Head, Sanctions Compliance, Americas and Group Head, US Sanctions

Government Personnel Mutual Life Insurance Company. Anti-Money Laundering (AML) Program; Including Suspicious Activity Reports

Program; Including Suspicious Activity Reports") Government Personnel Mutual Life Insurance Company Anti-Money Laundering (AML) Program; Including Suspicious Activity Reports Policies, Procedures, Internal Controls For Compliance With the Patriot Act

Government Personnel Mutual Life Insurance Company Anti-Money Laundering (AML) Program; Including Suspicious Activity Reports Policies, Procedures, Internal Controls For Compliance With the Patriot Act

Anti-Money Laundering and U.S. Compliance

U.S. Regulatory/Compliance Orientation for International Bankers Anti-Money Laundering and U.S. Compliance Conference of State Bank Supervisors & Institute of International Bankers New York City, New York

U.S. Regulatory/Compliance Orientation for International Bankers Anti-Money Laundering and U.S. Compliance Conference of State Bank Supervisors & Institute of International Bankers New York City, New York

UNITED STATES OF AMERICA DEPARTMENT OF THE TREASURY FINANCIAL CRIMES ENFORCEMENT NETWORK

UNITED STATES OF AMERICA DEPARTMENT OF THE TREASURY FINANCIAL CRIMES ENFORCEMENT NETWORK IN THE MATTER OF: ) ) ) Number 2018-03 UBS Financial Services Inc. ) Weehawken, NJ ) ASSESSMENT OF CIVIL MONEY PENALTY

UNITED STATES OF AMERICA DEPARTMENT OF THE TREASURY FINANCIAL CRIMES ENFORCEMENT NETWORK IN THE MATTER OF: ) ) ) Number 2018-03 UBS Financial Services Inc. ) Weehawken, NJ ) ASSESSMENT OF CIVIL MONEY PENALTY

Bank Secrecy Act. The board establishes adequate policies and procedures in accordance with anti-money laundering laws and regulations.

Bank Secrecy Act Standards Examiners should evaluate the above-captioned function against the following control and performance standards. The Standards represent control and performance objectives that

Bank Secrecy Act Standards Examiners should evaluate the above-captioned function against the following control and performance standards. The Standards represent control and performance objectives that

Bank Secrecy Act. Presented by: Martin (Marty) Mitchell, CRCM Managing Director, ProBank Austin

Mitchell, CRCM Managing Director, ProBank Austin") Presented by: Martin (Marty) Mitchell, CRCM Managing Director, ProBank Austin Robert J. (Bob) Mullenbach, CRCM Managing Director, Compliance Division Deputy, ProBank Austin Key Points 1. BSA Compliance

Presented by: Martin (Marty) Mitchell, CRCM Managing Director, ProBank Austin Robert J. (Bob) Mullenbach, CRCM Managing Director, Compliance Division Deputy, ProBank Austin Key Points 1. BSA Compliance

Bank Secrecy Act Credit Union Training for Board Members and other Volunteers. Overview. Overview. Overview of Money Laundering and Financial Crime

Bank Secrecy Act Credit Union Training for Board Members and other Volunteers Overview Overview of Money Laundering and Financial Crime The Bank Secrecy Act The Role of the Board and Supervisory Committee

Bank Secrecy Act Credit Union Training for Board Members and other Volunteers Overview Overview of Money Laundering and Financial Crime The Bank Secrecy Act The Role of the Board and Supervisory Committee

Bank Secrecy Act (BSA) BSA-AML-OFAC-CIP Overview

BSA-AML-OFAC-CIP Overview") Bank Secrecy Act (BSA) BSA-AML-OFAC-CIP Overview What is the BSA? The Bank Secrecy Act (BSA) requires all financial institutions, casinos, and certain other businesses to: Monitor customer behavior File

Bank Secrecy Act (BSA) BSA-AML-OFAC-CIP Overview What is the BSA? The Bank Secrecy Act (BSA) requires all financial institutions, casinos, and certain other businesses to: Monitor customer behavior File

Bank Secrecy Act Errors & Exceptions: How Does Your Credit Union Compare?

2018 Conference & Expo Louisville, Kentucky June 14, 2018 Bank Secrecy Act Errors & Exceptions: How Does Your Credit Union Compare? Presented By: Joseph A. Zito, CPA, MBA Shareholder, Doeren Mayhew 1 Michigan

2018 Conference & Expo Louisville, Kentucky June 14, 2018 Bank Secrecy Act Errors & Exceptions: How Does Your Credit Union Compare? Presented By: Joseph A. Zito, CPA, MBA Shareholder, Doeren Mayhew 1 Michigan

8300/OFAC COMPLIANCE. Aka: What you don t know can hurt you. Presented by: Robert Frimet, CAMS

8300/OFAC COMPLIANCE Aka: What you don t know can hurt you Presented by: Robert Frimet, CAMS 1 Presentation Objectives Discuss the 8300 requirement for pawn brokers TO INCLUDE: When to fill out an 8300

8300/OFAC COMPLIANCE Aka: What you don t know can hurt you Presented by: Robert Frimet, CAMS 1 Presentation Objectives Discuss the 8300 requirement for pawn brokers TO INCLUDE: When to fill out an 8300

BSA/AML Hot Topics and UIGEA Daniel Hastings Financial Institution Examiner - FDIC

BSA/AML Hot Topics and UIGEA Daniel Hastings Financial Institution Examiner - FDIC Common BSA Deficiencies Revised FFIEC BSA/AML Examination Manual Proposed CDD Requirements for Financial Institutions

BSA/AML Hot Topics and UIGEA Daniel Hastings Financial Institution Examiner - FDIC Common BSA Deficiencies Revised FFIEC BSA/AML Examination Manual Proposed CDD Requirements for Financial Institutions

Bank Secrecy Act OFAC FinCEN

Bank Secrecy Act OFAC FinCEN SOUTHEAST DIRECTORS AND SUPERVISORY COMMITTEE CONFERENCE SEPTEMBER 18, 2017 Financial Crimes Identify Track Report Common BSA Acronyms CIP CDD CTR SAR FinCEN OFAC Customer

Bank Secrecy Act OFAC FinCEN SOUTHEAST DIRECTORS AND SUPERVISORY COMMITTEE CONFERENCE SEPTEMBER 18, 2017 Financial Crimes Identify Track Report Common BSA Acronyms CIP CDD CTR SAR FinCEN OFAC Customer

BSA/AML Excellence and the Role of Governance NEW JERSEY BANKERS ASSOCIATION ANNUAL CONFERENCE MAY 2017

BSA/AML Excellence and the Role of Governance NEW JERSEY BANKERS ASSOCIATION ANNUAL CONFERENCE MAY 2017 Your Presenters Asaad Faquir, MBA, MBS Director, RSK Compliance Solutions, LLC Salvatore Zerilli,

BSA/AML Excellence and the Role of Governance NEW JERSEY BANKERS ASSOCIATION ANNUAL CONFERENCE MAY 2017 Your Presenters Asaad Faquir, MBA, MBS Director, RSK Compliance Solutions, LLC Salvatore Zerilli,

Bank Secrecy Act for Consumer Lending Staff

Bank Secrecy Act for Consumer Lending Staff Hello, and welcome to CUNA s Bank Secrecy Act for Consumer Lending Staff Training on Demand course! Compliance with the Bank Secrecy Act, otherwise known as

Bank Secrecy Act for Consumer Lending Staff Hello, and welcome to CUNA s Bank Secrecy Act for Consumer Lending Staff Training on Demand course! Compliance with the Bank Secrecy Act, otherwise known as

UNITED STATES OF AMERICA DEPARTMENT OF THE TREASURY FINANCIAL CRIMES ENFORCEMENT NETWORK

UNITED STATES OF AMERICA DEPARTMENT OF THE TREASURY FINANCIAL CRIMES ENFORCEMENT NETWORK IN THE MATTER OF: ) ) ) ) Number 2017-03 BTC-E a/k/a Canton Business Corporation ) and Alexander Vinnik ) ) I. INTRODUCTION

UNITED STATES OF AMERICA DEPARTMENT OF THE TREASURY FINANCIAL CRIMES ENFORCEMENT NETWORK IN THE MATTER OF: ) ) ) ) Number 2017-03 BTC-E a/k/a Canton Business Corporation ) and Alexander Vinnik ) ) I. INTRODUCTION

This Webcast Will Begin Shortly

This Webcast Will Begin Shortly If you have any technical problems with the Webcast or the streaming audio, please contact us via email at: webcast@acc.com Thank You! 1 The ABC s of AML: An Introduction

This Webcast Will Begin Shortly If you have any technical problems with the Webcast or the streaming audio, please contact us via email at: webcast@acc.com Thank You! 1 The ABC s of AML: An Introduction

Member Identification Program

Member Identification Program Presented by Sarah White, Contributing Writer Tracy Blaske, Director, Compliance Education, CUNA #TR1139 Introduction Hello, and welcome to CUNA s Member Identification Program

Member Identification Program Presented by Sarah White, Contributing Writer Tracy Blaske, Director, Compliance Education, CUNA #TR1139 Introduction Hello, and welcome to CUNA s Member Identification Program

FINCEN GUIDANCE. Under 31 CFR , an MSB s AML program must, at a minimum:

FIN-2016-G001 Issued: March 11, 2016 Subject: Guidance on Existing AML Program Rule Compliance Obligations for MSB Principals with Respect to Agent Monitoring This guidance reiterates the anti-money laundering

FIN-2016-G001 Issued: March 11, 2016 Subject: Guidance on Existing AML Program Rule Compliance Obligations for MSB Principals with Respect to Agent Monitoring This guidance reiterates the anti-money laundering

New Bank Secrecy Act Beneficial Owners Rule May 2017

Veronica Madsen, Attorney vm@h2law.com (248) 723-0536 New Bank Secrecy Act Beneficial Owners Rule May 2017 Disclaimer: This presentation does not constitute legal advice or a legal opinion on any matter

Veronica Madsen, Attorney vm@h2law.com (248) 723-0536 New Bank Secrecy Act Beneficial Owners Rule May 2017 Disclaimer: This presentation does not constitute legal advice or a legal opinion on any matter

Anti-Money Laundering

INFORMATIONAL Anti-Money Laundering NASD Provides Guidance To Member Firms Concerning Anti-Money Laundering Compliance Programs Required By Federal Law SUGGESTED ROUTING The Suggested Routing function

INFORMATIONAL Anti-Money Laundering NASD Provides Guidance To Member Firms Concerning Anti-Money Laundering Compliance Programs Required By Federal Law SUGGESTED ROUTING The Suggested Routing function

ANTI-MONEY LAUNDERING PROGRAM Applicable to:

ANTI-MONEY LAUNDERING PROGRAM Applicable to: Athene USA (the Company) 1 Purpose a) This Program is designed to comply specifically with the requirements of the Bank Secrecy Act (as amended by the USA PATRIOT

ANTI-MONEY LAUNDERING PROGRAM Applicable to: Athene USA (the Company) 1 Purpose a) This Program is designed to comply specifically with the requirements of the Bank Secrecy Act (as amended by the USA PATRIOT

BSA Excellence: Officer Training

Welcome to BSA Excellence: Officer Training 1 Compliance Outsourcing Partnership Solutions The Karen I. Martino Group COPS A Partner Only Firm Specializing in: BSA Independent Third Party Audits Compliance

Welcome to BSA Excellence: Officer Training 1 Compliance Outsourcing Partnership Solutions The Karen I. Martino Group COPS A Partner Only Firm Specializing in: BSA Independent Third Party Audits Compliance

Agent Compliance Manual. For Caribbean Airmail, Inc. Bank Secrecy Act Anti Money Laundering OFAC USA PATRIOT ACT CFPB July 2014

Agent Compliance Manual For Caribbean Airmail, Inc. Bank Secrecy Act Anti Money Laundering OFAC USA PATRIOT ACT CFPB July 2014 May Not Be Used Or Disclosed Outside Caribbean Airmail Inc Without Management

Agent Compliance Manual For Caribbean Airmail, Inc. Bank Secrecy Act Anti Money Laundering OFAC USA PATRIOT ACT CFPB July 2014 May Not Be Used Or Disclosed Outside Caribbean Airmail Inc Without Management

Oklahoma Agent Compliance Training Guide

Anti-Money Laundering Compliance Guide USA PATRIOT Act Prevention of Terrorism Financing Oklahoma Agent Compliance Training Guide Reporting Requirements Recordkeeping FinCEN Resources Employee Training

Anti-Money Laundering Compliance Guide USA PATRIOT Act Prevention of Terrorism Financing Oklahoma Agent Compliance Training Guide Reporting Requirements Recordkeeping FinCEN Resources Employee Training

Bank Secrecy Act (BSA) and Anti-Money Laundering (AML) Policy and Program for BancStar, Inc. Affiliated Banks

and Anti-Money Laundering (AML) Policy and Program for BancStar, Inc. Affiliated Banks") Bank Secrecy Act (BSA) and Anti-Money Laundering (AML) Policy and Program for BancStar, Inc. Affiliated Banks Reviewed and Approved by Board of Directors on: Bank Star One 09/18/14 Bank Star 09/26/14 Bank

Bank Secrecy Act (BSA) and Anti-Money Laundering (AML) Policy and Program for BancStar, Inc. Affiliated Banks Reviewed and Approved by Board of Directors on: Bank Star One 09/18/14 Bank Star 09/26/14 Bank

Preparing for Your BSA Compliance Exams. Ted Dreyer, Senior Attorney Wolters Kluwer

Preparing for Your BSA Compliance Exams Ted Dreyer, Senior Attorney Wolters Kluwer Scoping And Planning of Exam BSA/AML Examination Manual Overview Examination procedures First thing on list Previous Criticism

Preparing for Your BSA Compliance Exams Ted Dreyer, Senior Attorney Wolters Kluwer Scoping And Planning of Exam BSA/AML Examination Manual Overview Examination procedures First thing on list Previous Criticism

United States Agent Compliance Training Guide

Anti-Money Laundering Compliance Guide USA PATRIOT Act Prevention of Terrorist Financing United States Agent Compliance Training Guide Reporting Requirements Recordkeeping FinCEN Resources Employee Training

Anti-Money Laundering Compliance Guide USA PATRIOT Act Prevention of Terrorist Financing United States Agent Compliance Training Guide Reporting Requirements Recordkeeping FinCEN Resources Employee Training

Understanding the Bank Secrecy Act

Understanding the Bank Secrecy Act What has FinCen been up to? 4/4/2015 Lone Star National Bank CMP - $1,000,000 Customer due diligence and enhanced due diligence of high risk accounts unsatisfactory Deficiencies

Understanding the Bank Secrecy Act What has FinCen been up to? 4/4/2015 Lone Star National Bank CMP - $1,000,000 Customer due diligence and enhanced due diligence of high risk accounts unsatisfactory Deficiencies

Bank Secrecy Act Hot Topics!

Bank Secrecy Act Hot Topics! Barb Boyd, Glory LeDu, Sarah Stevenson, Mary Jo White Bank Secrecy Act Hot Topics What Changed in 2014? Guidance on Virtual Currency (1/31/14) Virtual Currency Rulings (10/28/14)

Bank Secrecy Act Hot Topics! Barb Boyd, Glory LeDu, Sarah Stevenson, Mary Jo White Bank Secrecy Act Hot Topics What Changed in 2014? Guidance on Virtual Currency (1/31/14) Virtual Currency Rulings (10/28/14)

LEGAL ENTITY PROFILE

LEGAL ENTITY PROFILE (Check one) o New Customer o Existing Customer o Exempt (Check one) o In Person o Other PART 1 Information of legal entity: Physical address: Mailing address: Phone number: Email address:

LEGAL ENTITY PROFILE (Check one) o New Customer o Existing Customer o Exempt (Check one) o In Person o Other PART 1 Information of legal entity: Physical address: Mailing address: Phone number: Email address:

Anti-Money Laundering and Counter Terrorism

1 Anti-Money Laundering and Counter Terrorism 1. INTRODUCTION SimpleFX Ltd. ( The Company ) aims to prevent, detect and not knowingly facilitate money laundering and terrorism financing activities. The

1 Anti-Money Laundering and Counter Terrorism 1. INTRODUCTION SimpleFX Ltd. ( The Company ) aims to prevent, detect and not knowingly facilitate money laundering and terrorism financing activities. The

FinCEN's Customer Due Diligence Final Rule What You Need To Know

FinCEN's Customer Due Diligence Final Rule What You Need To Know June 2, 2016 Moderator Alan S. Kaplinsky Practice Leader Consumer Financial Services 215.864.8544 kaplinsky@ballardspahr.com Panelists Peter

FinCEN's Customer Due Diligence Final Rule What You Need To Know June 2, 2016 Moderator Alan S. Kaplinsky Practice Leader Consumer Financial Services 215.864.8544 kaplinsky@ballardspahr.com Panelists Peter

ANTI-MONEY LAUNDERING AND COUNTER TERRORISM FINANCING PROCEDURE MANUAL. Fcorp Services Ltd

ANTI-MONEY LAUNDERING AND COUNTER TERRORISM FINANCING PROCEDURE MANUAL Fcorp Services Ltd The manual is property of Fcorp LTD The reproduction in whole or in part in any way including the reproduction

ANTI-MONEY LAUNDERING AND COUNTER TERRORISM FINANCING PROCEDURE MANUAL Fcorp Services Ltd The manual is property of Fcorp LTD The reproduction in whole or in part in any way including the reproduction

Bank Secrecy Act/ Anti-Money Laundering Examination Manual

Bank Secrecy Act/ Anti-Money Laundering Examination Manual Federal Financial Institutions Examination Council Board of Governors of the Federal Reserve System, Federal Deposit Insurance Corporation, National

Bank Secrecy Act/ Anti-Money Laundering Examination Manual Federal Financial Institutions Examination Council Board of Governors of the Federal Reserve System, Federal Deposit Insurance Corporation, National

THE USA PATRIOT ACT New Responsibilities for Institutions in the Financial Industry

P THE USA PATRIOT ACT New Responsibilities for Institutions in the Financial Industry By Michael P. Malloy 2002. Reproduced by permission. resident Bush signed into law the Uniting and Strengthening America

P THE USA PATRIOT ACT New Responsibilities for Institutions in the Financial Industry By Michael P. Malloy 2002. Reproduced by permission. resident Bush signed into law the Uniting and Strengthening America

Money Laundering: Suspicious Activity Reports

strategies from numbers Money Laundering: Suspicious Activity Reports What you Need to Know & Florida Institute of Certified Public Accountants Presentation José I. Marrero, EA Luis O. Rivera, CPA, CFF,

strategies from numbers Money Laundering: Suspicious Activity Reports What you Need to Know & Florida Institute of Certified Public Accountants Presentation José I. Marrero, EA Luis O. Rivera, CPA, CFF,

FinCEN s New Customer Due Diligence Requirements and Their Impact on Community Banks

October 2016 FinCEN s New Customer Due Diligence Requirements and Their Impact on Community Banks On May 10, 2016, the Financial Crimes Enforcement Network ( FinCEN ) issued a final rule regarding customer

October 2016 FinCEN s New Customer Due Diligence Requirements and Their Impact on Community Banks On May 10, 2016, the Financial Crimes Enforcement Network ( FinCEN ) issued a final rule regarding customer

Prepare for Customer Due Diligence Final Rule

Prepare for Customer Due Diligence Final Rule Presented by: Carrie Mansbridge Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC-registered investment advisor.

Prepare for Customer Due Diligence Final Rule Presented by: Carrie Mansbridge Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC-registered investment advisor.

PRESIDENTIAL LIFE INSURANCE COMPANY

PRESIDENTIAL LIFE INSURANCE COMPANY 69 LYDECKER STREET NYACK, NEW YORK 10960 (845) 358-2300 FAX (845) 353-0273 MEMORANDUM TO: FROM: Presidential Life General and Writing Agents (Representatives) Agency

PRESIDENTIAL LIFE INSURANCE COMPANY 69 LYDECKER STREET NYACK, NEW YORK 10960 (845) 358-2300 FAX (845) 353-0273 MEMORANDUM TO: FROM: Presidential Life General and Writing Agents (Representatives) Agency

Regulatory Compliance Update

Regulatory Compliance Update ACUIA Region 6 Conference Presented By: Kristie Kenney Hoover, NCCO Internal Audit Manager, Doeren Mayhew Florida Michigan North Carolina Texas Insight. Oversight. Foresight.

Regulatory Compliance Update ACUIA Region 6 Conference Presented By: Kristie Kenney Hoover, NCCO Internal Audit Manager, Doeren Mayhew Florida Michigan North Carolina Texas Insight. Oversight. Foresight.

Foreign Financial Institutions Anti-Money Laundering Questionnaire

SECTION I - GENERAL ADMINISTRATIVE INFORMATION 1. Legal Name of Financial Institution D/B/A (if applicable) 2. Registered Address (attach proof) Physical presence at this address? o Yes o No 3. Head Office

SECTION I - GENERAL ADMINISTRATIVE INFORMATION 1. Legal Name of Financial Institution D/B/A (if applicable) 2. Registered Address (attach proof) Physical presence at this address? o Yes o No 3. Head Office

Customer Identification Programs, Anti-Money Laundering Programs, and. Beneficial Ownership Requirements for Banks Lacking a Federal Functional

This document is scheduled to be published in the Federal Register on 08/25/2016 and available online at http://federalregister.gov/a/2016-20219, and on FDsys.gov BILLING CODE 4810-02 DEPARTMENT OF THE

This document is scheduled to be published in the Federal Register on 08/25/2016 and available online at http://federalregister.gov/a/2016-20219, and on FDsys.gov BILLING CODE 4810-02 DEPARTMENT OF THE

BANK SECRECY ACT COMPLIANCE VOLUNTEER LEADERSHIP CONFERENCE. November 17-19, 2017

BANK SECRECY ACT COMPLIANCE VOLUNTEER LEADERSHIP CONFERENCE November 17-19, 2017 THE BANK SECRECY ACT The Bank Secrecy Act (BSA), also known as the Financial Record-keeping and Reporting of Currency and

BANK SECRECY ACT COMPLIANCE VOLUNTEER LEADERSHIP CONFERENCE November 17-19, 2017 THE BANK SECRECY ACT The Bank Secrecy Act (BSA), also known as the Financial Record-keeping and Reporting of Currency and

Anti-Money Laundering Primer for Health Insurers

Anti-Money Laundering Primer for Health Insurers Health Care Compliance Association April 26, 2004 Stephen W. Koslow and Rhys W. Jones PwC Agenda The Crime of Money Laundering The Risk of Money Laundering

Anti-Money Laundering Primer for Health Insurers Health Care Compliance Association April 26, 2004 Stephen W. Koslow and Rhys W. Jones PwC Agenda The Crime of Money Laundering The Risk of Money Laundering

Article 1. Article 2. Article 3 A FCM shall comply with the following provisions in undertaking CDD measures:

Chinese National Futures Association Guidelines for Anti-Money Laundering and Countering Terrorism Financing for Futures Commission Merchants (Template) Article 1 Passed in the 11th Joint Session of 3th-term

Chinese National Futures Association Guidelines for Anti-Money Laundering and Countering Terrorism Financing for Futures Commission Merchants (Template) Article 1 Passed in the 11th Joint Session of 3th-term

Bank Secrecy Act (BSA) BSA-AML-CIP-OFAC For New Accounts

BSA-AML-CIP-OFAC For New Accounts") Bank Secrecy Act (BSA) BSA-AML-CIP-OFAC For New Accounts What is the BSA? The Bank Secrecy Act (BSA) requires all financial institutions, casinos, and certain other businesses to: Monitor customer behavior

Bank Secrecy Act (BSA) BSA-AML-CIP-OFAC For New Accounts What is the BSA? The Bank Secrecy Act (BSA) requires all financial institutions, casinos, and certain other businesses to: Monitor customer behavior

FinCEN Form 102a Suspicious Activity Report Instructions 1

FinCEN Form 102a Suspicious Activity Report Instructions 1 Safe Harbor Federal law (31 U.S.C. 5318(g)(3)) provides complete protection from civil liability for all reports of suspicious transactions made

FinCEN Form 102a Suspicious Activity Report Instructions 1 Safe Harbor Federal law (31 U.S.C. 5318(g)(3)) provides complete protection from civil liability for all reports of suspicious transactions made

FXPRIMUS ANTI-MONEY LAUNDERING ("AML") POLICY

POLICY") FXPRIMUS ANTI-MONEY LAUNDERING ("AML") POLICY POLICY STATEMENT AND PRINCIPLES In compliance with The Financial Intelligence and Anti-Money Laundering Act 2002 (FIAMLA 2002), the Prevention of Corruption

FXPRIMUS ANTI-MONEY LAUNDERING ("AML") POLICY POLICY STATEMENT AND PRINCIPLES In compliance with The Financial Intelligence and Anti-Money Laundering Act 2002 (FIAMLA 2002), the Prevention of Corruption

New BSA Officer Training Community Bankers Webinar Network June 2017

Community Bankers Webinar Network June 2017 Copyright 2017 Young & Associates, Inc. All rights reserved bille@younginc.com Table of Contents Section 1: Introduction... 1 Section 2: Risk Assessment... 2

Community Bankers Webinar Network June 2017 Copyright 2017 Young & Associates, Inc. All rights reserved bille@younginc.com Table of Contents Section 1: Introduction... 1 Section 2: Risk Assessment... 2

AML Best Practices for Investment Advisers and Broker/ Dealers. July 7, :00 p.m. to 3:00 p.m. (ET) 2016 National Regulatory Services

2016 National Regulatory Services") AML Best Practices for Investment Advisers and Broker/ Dealers July 7, 2016 2:00 p.m. to 3:00 p.m. (ET) 2016 National Regulatory Services Instructor Jennifer Sullivan Jennifer Sullivan Consultant NRS Lakeville,

AML Best Practices for Investment Advisers and Broker/ Dealers July 7, 2016 2:00 p.m. to 3:00 p.m. (ET) 2016 National Regulatory Services Instructor Jennifer Sullivan Jennifer Sullivan Consultant NRS Lakeville,