United States v. First United Security Bank (2009)

|

|

|

- Garey Doyle

- 6 years ago

- Views:

Transcription

")

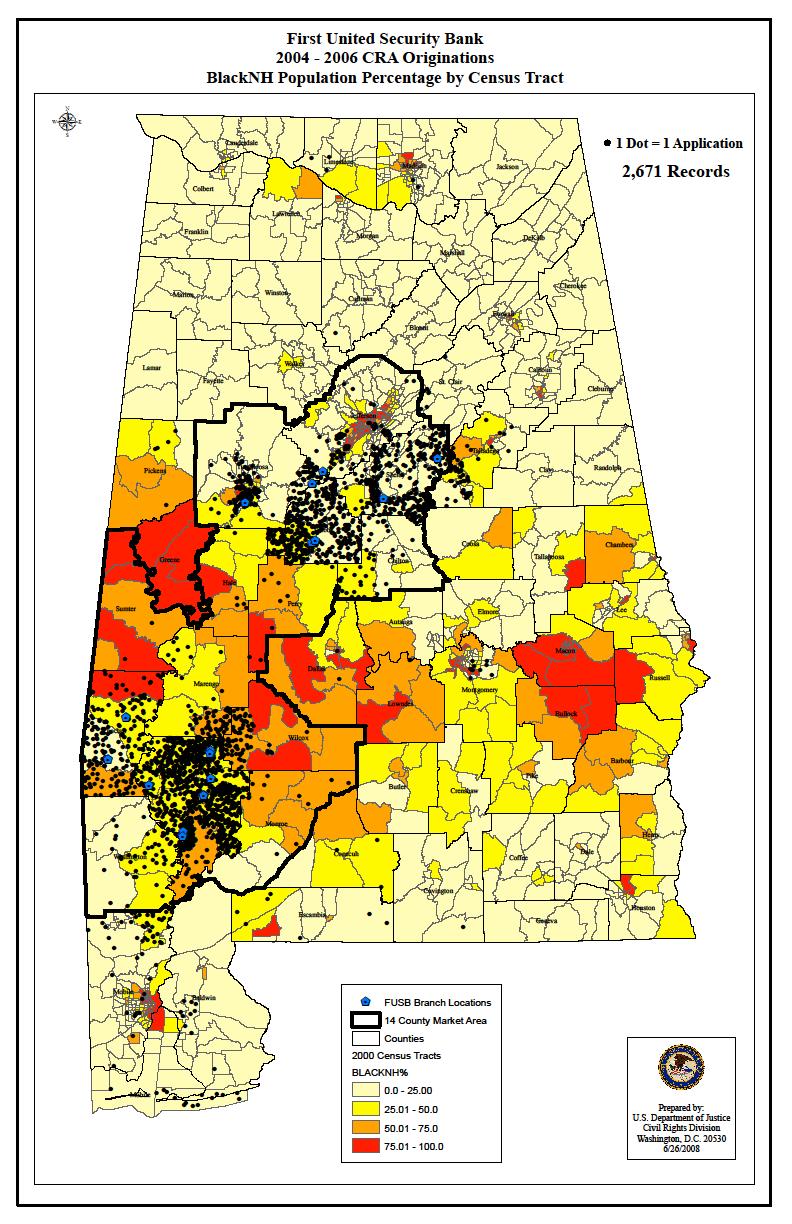

1 DOJ Redlining Cases Failure to provide lending services to minority areas Few or no branches Little or no marketing CRA ( Community Reinvestment Act ) assessment area excluding minority areas Extremely low proportion of loans

Redlining evidence included long term pattern in majority African-American counties and census tracts of: no")

2 United States v. First United Security Bank (2009) Redlining evidence included long term pattern in majority African-American counties and census tracts of: no branches little or no marketing exclusion from the bank s three separate CRA assessment areas extremely low proportion of loans

3

")

4 United States v. First United Security Bank (2009) Redlining claim: Evidence of low proportion of loans in majority African-American counties and census tracts Used market area designated in SEC 10K reports because African-American areas were excluded from bank s CRA assessment areas & bank operated outside of MSAs

Complaint alleged")

in majority-minority census")

This")

5 United States v. First United Security Bank (2009) Complaint alleged that from : Bank made only 218 of its 1563 mortgage loans (14%) in majority-minority census tracts Comparable lenders made 31% of such loans in majority minority census tracts (twice as many) This difference is statistically significant

6

in majorityminority census tracts All lenders made 21% of such loans in majority minority census tracts (almost twice as many) This difference is")

7 United States v. First United Security Bank (2009) Complaint alleged that from : Bank made only 245 of its 2134 CRA small business loans (11.5%) in majorityminority census tracts All lenders made 21% of such loans in majority minority census tracts (almost twice as many) This difference is statistically significant

8

9 United States v. First United Security Bank (2009) Consent order filed with complaint includes: non-discrimination injunction one new branch in a majority A-A area training requirements affirmative outreach and marketing revised CRA assessment areas

Monetary relief: $500K in loan discount fund $110K for")

10 United States v. First United Security Bank (2009) Monetary relief: $500K in loan discount fund $110K for outreach $55K damages for African-American customers charged higher interest rates

11 Recent ECOA/FHA Redlining Actions U.S. v. Midwest BankCentre (2011) mortgage redlining Federal Reserve Board ( FRB ) referral U.S. v. Citizens Republic Bancorp and Citizens Bank (2011) mortgage redlining FRB referral

12 Allegations include: Midwest and Citizens branches exclusively or almost exclusively in white census tracts CRA assessment area formed horseshoe around minority communities fewer applications and/or originations from African-American census tracts than peers

13 Midwest and Citizens Relief includes: Opening full-service branches in African-American neighborhoods Required investment of > $1 million in African-American neighborhoods, including special financing program, consumer education and credit repair, and outreach. Partnership with City to provide > $1 million in matching grants of up to $5,000 to existing homeowners for exterior improvements.

14 U.S. v. Community State Bank (2013) Redlining allegations include: CRA assessment area drawn to exclude minority neighborhoods Written policies discouraging loans outside assessment area 1 application from African-American census tracts between 2006 and 2009

15 U.S. v. Community State Bank (2013) Relief includes: Opening loan production office in one of the redlined neighborhoods $75,000 loan subsidy fund $75,000 partnership program with groups promoting revitalization of redlined neighborhoods $15,000 outreach program Expansion of lending area to redlined neighborhoods

16 U.S. v. Luther Burbank Savings (2012) Challenge to $400,000 minimum loan amount policy for wholesale mortgage lending that had an unjustified disparate impact on African American and Latino borrowers; resolved by consent order requiring $2 million investment in impacted majority-minority California neighborhoods. only 5.8 percent of Luther s single-family residential mortgage loans were made to African-American and Hispanic borrowers, compared to 31.8 percent of such loans made to African-American and Hispanic borrowers by comparable prime lenders. Similarly, only 5.2 percent of Luther s single-family residential loans in the greater Los Angeles area were made in majority-minority census tracts (areas with a non-white population greater than 50 percent), compared to 41.7 percent of such loans made in these tracts by comparable prime lenders.

17 DOJ Redlining Settlements All recent redlining settlements include: Nondiscrimination provisions New branches in previously redlined areas Outreach & consumer education Training and changes to bank procedures Monetary relief ranging from $3 to $10 million in loan subsidies for previously redlined areas

18 Reverse Redlining Targeting underserved communities for abusive lending practices Redlining by prime lenders leaves minority areas vulnerable Investigations may focus on: Large percentage of loans made to minorities Specific marketing to minorities Predatory nature of loans

19 Reverse Redlining Redlining creates the market conditions in which reverse redlining thrives. Where entire communities are abandoned by mainstream financial institutions, they become attractive prey to unscrupulous lenders. See also Clark v. Universal Builders, Inc., 501 F.2d 324, 328, (7 th Cir. 1973), cert. denied ("[t]hrough the medium of exorbitant prices and severe, long-term land contract terms blacks are tied to housing in the ghetto and segregated inner-city neighborhoods.").

20 Reverse Redlining Must demonstrate that a defendant s lending practices were: unfair or predatory and either intentionally targeted on the basis of a protected category or that there is a disparate impact on the basis of protected category

Barkley v. Olympia Mortg. Corp., 2007 WL 2437810 (E.D.N.Y.")

21 Reverse Redlining When there is direct evidence that the defendant deliberately targeted a protected class with unfair terms in a realestate related transaction, comparative evidence of the defendant s treatment of other nonprotected classes need not be established. Matthews v. New Century Mortg. Corp., 185 F.Supp.2d 874 (S.D. Ohio 2002) Barkley v. Olympia Mortg. Corp., 2007 WL (E.D.N.Y. 2007)

22 Reverse Redlining Through Use of Discretionary Pricing A number of class action lawsuits have alleged that lenders discretionary and subjective pricing practices had a disparate impact on the cost of loans extended to minority borrowers Ramirez v. Greenpoint Mortg. Funding, Inc., 633 F. Supp. 2d (N.D. Cal. 2008) Miller v. Countrywide Bank, N.A., 571 F. Supp. 2d 251 (D. Mass. 2008) Taylor v. Accredited Home Lenders, Inc., 580 F.Supp.2d 1062 (S.D. Cal. 2008)

23 Disparate Impact Allegations Plaintiffs relied on statistical data about the prevalence of subjective risk-based pricing on minorities more likely to receive: subprime loans higher yield spread premiums higher fees steered into less advantageous loan products

Defendants operate Buy Here Pay Here auto")

24 United States v. AutoFare (2014) Defendants operate Buy Here Pay Here auto dealerships, providing direct financing for used cars Customers are only required to make down payment and prove residency and income Complaint filed January 2014

25 United States v. AutoFare (2014) Complaint alleges that defendants targeted African-American borrowers for predatory auto loans Predatory loan features: Excessive sales price Very high down payment Disproportionately high APR

26 United States v. AutoFare (2014) Complaint alleges owner used racial slurs and epithets and made derogatory statements about African-American customers Many of defendants customers defaulted and/or had vehicles repossessed

27 US v. GFI Mortgage (2012) Challenge to pattern or practice of charging African American and Latino borrowers discriminatory mortgage prices; resolved by $3.55 million settlement. Settlement also required GFI to pay the maximum $55,000 civil penalty allowed by the Fair Housing Act and to document its loan pricing decisions

28 US v. SunTrust Mortgage (2012) Nationwide challenge to pattern or practice of charging African American and Latino borrowers discriminatory mortgage prices; resolved by $21 million settlement. SunTrust also required to maintain policy of document and review of any variation in loan interest rates and fees and restrict compensating loan officers and mortgage brokers based on the terms or conditions of a particular loan.

MBBA-NH & MAMP. Compliance Conference. April 19, 2017

MBBA-NH & MAMP Compliance Conference April 19, 2017 Agenda HMDA Overview Readiness Steps HMDA Expansion Fields 2 New HMDA Rule Summary Changes to Home Mortgage Disclosure: Regulation C Types of institutions

MBBA-NH & MAMP Compliance Conference April 19, 2017 Agenda HMDA Overview Readiness Steps HMDA Expansion Fields 2 New HMDA Rule Summary Changes to Home Mortgage Disclosure: Regulation C Types of institutions

Fair Lending Risk Management: Lessons from Recent Settlements

November 2012 Fair Lending Risk Management: Lessons from Recent Settlements Introduction Fair lending continues to be a major enforcement priority of federal agencies, and the financial implications have

November 2012 Fair Lending Risk Management: Lessons from Recent Settlements Introduction Fair lending continues to be a major enforcement priority of federal agencies, and the financial implications have

Fair Lending Hot Topics

Fair Lending Hot Topics Outlook Live Webinar October 17, 2012 Non-Discrimination Working Group of the Financial Fraud Enforcement Task Force Visit us at www.consumercomplianceoutlook.org informational

Fair Lending Hot Topics Outlook Live Webinar October 17, 2012 Non-Discrimination Working Group of the Financial Fraud Enforcement Task Force Visit us at www.consumercomplianceoutlook.org informational

US Department of Justice Fair Lending Enforcement

US Department of Justice Fair Lending Enforcement Daniel P. Mosteller Acting Special Litigation Counsel for Fair Lending Housing and Civil Enforcement Section, Civil Rights Division US Department of Justice

US Department of Justice Fair Lending Enforcement Daniel P. Mosteller Acting Special Litigation Counsel for Fair Lending Housing and Civil Enforcement Section, Civil Rights Division US Department of Justice

Fair Housing Conference

Fair Housing Conference U.S. Attorney s Office for the District of Idaho April 2012 Laws Enforced by DOJ Fair Housing Act (FHA) Equal Credit Opportunity Act (ECOA) Titles II and III, Civil Rights Act of

Fair Housing Conference U.S. Attorney s Office for the District of Idaho April 2012 Laws Enforced by DOJ Fair Housing Act (FHA) Equal Credit Opportunity Act (ECOA) Titles II and III, Civil Rights Act of

SELECTED LAW ENFORCEMENT AGENCY AND BANK REGULATORY MATTERS

SELECTED LAW ENFORCEMENT AGENCY AND BANK REGULATORY MATTERS OVERVIEW BuckleySandler s attorneys have represented many of the nation's leading banks, insurance companies, securities firms and other financial

SELECTED LAW ENFORCEMENT AGENCY AND BANK REGULATORY MATTERS OVERVIEW BuckleySandler s attorneys have represented many of the nation's leading banks, insurance companies, securities firms and other financial

Fair Lending Issues and Hot Topics

Fair Lending Issues and Hot Topics Outlook Live Webinar November 2, 2011 Non-Discrimination Working Group of the Financial Fraud Enforcement Task Force Visit us at www.consumercomplianceoutlook.org informational

Fair Lending Issues and Hot Topics Outlook Live Webinar November 2, 2011 Non-Discrimination Working Group of the Financial Fraud Enforcement Task Force Visit us at www.consumercomplianceoutlook.org informational

HOUSING DISCRIMINATION COMPLAINT

HOUSING DISCRIMINATION COMPLAINT CASE NUMBER: 1. Complainants California Reinvestment Coalition (CRC) 474 Valencia St, Ste 230 San Francisco, CA 94103 Representing CRC: Kevin Stein, Deputy Director California

HOUSING DISCRIMINATION COMPLAINT CASE NUMBER: 1. Complainants California Reinvestment Coalition (CRC) 474 Valencia St, Ste 230 San Francisco, CA 94103 Representing CRC: Kevin Stein, Deputy Director California

IN THE UNITED STATES DISTRICT COURT FOR THE DISTRICT OF MINNESOTA

CASE 0:17-cv-00136-PAM-FLN Document 1 Filed 01/13/17 Page 1 of 14 IN THE UNITED STATES DISTRICT COURT FOR THE DISTRICT OF MINNESOTA UNITED STATES OF AMERICA, ) ) Plaintiff, ) CIVIL ACTION NO 17-cv-136

CASE 0:17-cv-00136-PAM-FLN Document 1 Filed 01/13/17 Page 1 of 14 IN THE UNITED STATES DISTRICT COURT FOR THE DISTRICT OF MINNESOTA UNITED STATES OF AMERICA, ) ) Plaintiff, ) CIVIL ACTION NO 17-cv-136

New and Re-emerging Fair Lending Risks. Article by Austin Brown & Loretta Kirkwood October 2014

New and Re-emerging Fair Lending Risks Article by Austin Brown & Loretta Kirkwood BY AUSTIN BROWN & LORETTA KIRKWOOD Austin Brown Loretta Kirkwood Regulators have been focused recently on several new and

New and Re-emerging Fair Lending Risks Article by Austin Brown & Loretta Kirkwood BY AUSTIN BROWN & LORETTA KIRKWOOD Austin Brown Loretta Kirkwood Regulators have been focused recently on several new and

UNITED STATES DISTRICT COURT FOR THE WESTERN DISTRICT OF TENNESSEE WESTERN DIVISION

Case 2:09-cv-02857-dkv Document 1 Filed 12/30/09 Page 1 of 56 UNITED STATES DISTRICT COURT FOR THE WESTERN DISTRICT OF TENNESSEE WESTERN DIVISION ) CITY OF MEMPHIS ) 125 N. Main Street, Room 336 ) Memphis,

Case 2:09-cv-02857-dkv Document 1 Filed 12/30/09 Page 1 of 56 UNITED STATES DISTRICT COURT FOR THE WESTERN DISTRICT OF TENNESSEE WESTERN DIVISION ) CITY OF MEMPHIS ) 125 N. Main Street, Room 336 ) Memphis,

UNITED STATES DISTRICT COURT FOR THE DISTRICT OF MARYLAND BALTIMORE DIVISION

Case 1:08-cv-00062-JFM Document 153 Filed 04/07/10 Page 1 of 107 UNITED STATES DISTRICT COURT FOR THE DISTRICT OF MARYLAND BALTIMORE DIVISION ) MAYOR AND CITY COUNCIL ) OF BALTIMORE, ) City Hall ) 100

Case 1:08-cv-00062-JFM Document 153 Filed 04/07/10 Page 1 of 107 UNITED STATES DISTRICT COURT FOR THE DISTRICT OF MARYLAND BALTIMORE DIVISION ) MAYOR AND CITY COUNCIL ) OF BALTIMORE, ) City Hall ) 100

Identifying, Assessing and Mitigating Potential Redlining Risk

Identifying, Assessing and Mitigating Potential Redlining Risk Objectives Understanding Potential Redlining Risk Understanding the Reasonable Expected Market Area (REMA) vs CRA Assessment Area Understanding

Identifying, Assessing and Mitigating Potential Redlining Risk Objectives Understanding Potential Redlining Risk Understanding the Reasonable Expected Market Area (REMA) vs CRA Assessment Area Understanding

Credit Research Center Seminar

Credit Research Center Seminar Ensuring Fair Lending: What Do We Know about Pricing in Mortgage Markets and What Will the New HMDA Data Fields Tell US? www.msb.edu/prog/crc March 14, 2005 Introduction

Credit Research Center Seminar Ensuring Fair Lending: What Do We Know about Pricing in Mortgage Markets and What Will the New HMDA Data Fields Tell US? www.msb.edu/prog/crc March 14, 2005 Introduction

New Jersey Bankers Association 2017 Compliance University Fair Lending Redlining Risks

New Jersey Bankers Association 2017 Compliance University Fair Lending Redlining Risks June 14, 2017 Presented by Rose N. Egbuiwe, Fair Lending Examination Specialist 1 Objectives Provide Insight on Fair

New Jersey Bankers Association 2017 Compliance University Fair Lending Redlining Risks June 14, 2017 Presented by Rose N. Egbuiwe, Fair Lending Examination Specialist 1 Objectives Provide Insight on Fair

National Association of Federal Credit Unions. Fair Lending Training (Part I) March 19, Lori J. Sommerfield Counsel BuckleySandler LLP

March 19, Lori J. Sommerfield Counsel BuckleySandler LLP") National Association of Federal Credit Unions Fair Lending Training (Part I) March 19, 2014 Lori J. Sommerfield Counsel BuckleySandler LLP Order of Presentation Overview of Fair Lending Laws & Regulations

National Association of Federal Credit Unions Fair Lending Training (Part I) March 19, 2014 Lori J. Sommerfield Counsel BuckleySandler LLP Order of Presentation Overview of Fair Lending Laws & Regulations

Fair & Responsible Lending in the Regulatory Crosshairs

Fair & Responsible Lending in the Regulatory Crosshairs Legal Counsel to the Financial Services Industry Minnesota Banking Law Institute April 5, 2013 Andrea K. Mitchell Partner Lori J. Sommerfield Counsel

Fair & Responsible Lending in the Regulatory Crosshairs Legal Counsel to the Financial Services Industry Minnesota Banking Law Institute April 5, 2013 Andrea K. Mitchell Partner Lori J. Sommerfield Counsel

UNITED STATES DISTRICT COURT FOR THE WESTERN DISTRICT OF TENNESSEE WESTERN DIVISION

Case 2:09-cv-02857-STA-dkv Document 29 Filed 04/07/10 Page 1 of 83 UNITED STATES DISTRICT COURT FOR THE WESTERN DISTRICT OF TENNESSEE WESTERN DIVISION ) CITY OF MEMPHIS ) 125 N. Main Street, Room 336 )

Case 2:09-cv-02857-STA-dkv Document 29 Filed 04/07/10 Page 1 of 83 UNITED STATES DISTRICT COURT FOR THE WESTERN DISTRICT OF TENNESSEE WESTERN DIVISION ) CITY OF MEMPHIS ) 125 N. Main Street, Room 336 )

) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) )

) ) ) ) ) ) ) ) ) ) ) ) ) ) ) )") 0 0 CHAVEZ & GERTLER, L.L.P. Mark A. Chavez (CA SBN 0 Nance F. Becker (CA SBN Dan Gildor (CA SBN 0 Miller Avenue Mill Valley, California Tel: ( - Fax: ( - E-mail: mark@chavezgertler.com nance@chavezgertler.com

0 0 CHAVEZ & GERTLER, L.L.P. Mark A. Chavez (CA SBN 0 Nance F. Becker (CA SBN Dan Gildor (CA SBN 0 Miller Avenue Mill Valley, California Tel: ( - Fax: ( - E-mail: mark@chavezgertler.com nance@chavezgertler.com

Indirect Auto Lending Fair Lending Considerations

Indirect Auto Lending Fair Lending Considerations Outlook Live Webinar August 6, 2013 Consumer Financial Protection Bureau Federal Reserve Board U.S. Department of Justice Visit us at www.consumercomplianceoutlook.org

Indirect Auto Lending Fair Lending Considerations Outlook Live Webinar August 6, 2013 Consumer Financial Protection Bureau Federal Reserve Board U.S. Department of Justice Visit us at www.consumercomplianceoutlook.org

HMDA Workshop Part IV: Fair Lending & HMDA

HMDA Workshop Part IV: Fair Lending & HMDA Sunday, Sept. 18, 2016, 4:45 pm Moderator: Richard H. Harvey, Jr., Chief Compliance Officer, Colonial Savings, F.A. Panelists: Melanie Brody, Partner, Mayer Brown

HMDA Workshop Part IV: Fair Lending & HMDA Sunday, Sept. 18, 2016, 4:45 pm Moderator: Richard H. Harvey, Jr., Chief Compliance Officer, Colonial Savings, F.A. Panelists: Melanie Brody, Partner, Mayer Brown

2016 Interagency Fair Lending Hot Topics

2016 Interagency Fair Lending Hot Topics Outlook Live Webinar October 4, 2016 Visit us at www.consumercomplianceoutlook.org Welcome to Outlook Live Logistics Call-in number: 1-888-625-5230 Conference code:

2016 Interagency Fair Lending Hot Topics Outlook Live Webinar October 4, 2016 Visit us at www.consumercomplianceoutlook.org Welcome to Outlook Live Logistics Call-in number: 1-888-625-5230 Conference code:

Cuyahoga County Mortgage Lending Patterns

Cuyahoga County Mortgage Lending Patterns July 2018 Michael Lepley & Lenore Mangiarelli About the Authors MICHAEL LEPLEY is Fair Housing Center for Rights & Research s Senior Research Associate. He received

Cuyahoga County Mortgage Lending Patterns July 2018 Michael Lepley & Lenore Mangiarelli About the Authors MICHAEL LEPLEY is Fair Housing Center for Rights & Research s Senior Research Associate. He received

Fair Lending THIS PUBLICATION IS. counsel for advice on specific fact situations. Copyrighted by Compliance Resource, LLC, April 2017

Fair Lending THIS PUBLICATION IS Not offered as legal advice SO Readers should consult with legal counsel for advice on specific fact situations. Copyrighted by Compliance Resource, LLC, April 2017 No

Fair Lending THIS PUBLICATION IS Not offered as legal advice SO Readers should consult with legal counsel for advice on specific fact situations. Copyrighted by Compliance Resource, LLC, April 2017 No

The High Cost of Segregation: Exploring the Relationship Between Racial Segregation and Subprime Lending

F u r m a n C e n t e r f o r r e a l e s t a t e & u r b a n p o l i c y N e w Y o r k U n i v e r s i t y s c h o o l o f l aw wa g n e r s c h o o l o f p u b l i c s e r v i c e n o v e m b e r 2 0

F u r m a n C e n t e r f o r r e a l e s t a t e & u r b a n p o l i c y N e w Y o r k U n i v e r s i t y s c h o o l o f l aw wa g n e r s c h o o l o f p u b l i c s e r v i c e n o v e m b e r 2 0

CIT Group Accused of Redlining and Violating Fair Housing Act

November 17, 2016 Contact: Kevin Stein (415) 864-3980 Caroline Peattie: (415) 457-5025 (Ext. 106) CIT Group Accused of Redlining and Violating Fair Housing Act CALIFORNIA REINVESTMENT COALITION AND FAIR

November 17, 2016 Contact: Kevin Stein (415) 864-3980 Caroline Peattie: (415) 457-5025 (Ext. 106) CIT Group Accused of Redlining and Violating Fair Housing Act CALIFORNIA REINVESTMENT COALITION AND FAIR

Managing Fair and Responsible Lending Challenges and Risks

Managing Fair and Responsible Lending Challenges and Risks NYBA Technology, Compliance and Risk Management Forum White Plains, NY May 13, 2015 Legal Counsel to the Financial Services Industry Presented

Managing Fair and Responsible Lending Challenges and Risks NYBA Technology, Compliance and Risk Management Forum White Plains, NY May 13, 2015 Legal Counsel to the Financial Services Industry Presented

Fair Lending Developments: Standing to Sue Takes the Floor

Fair Lending Developments: Standing to Sue Takes the Floor By John L. Ropiequet, Christopher S. Naveja, and L. Jean Noonan* INTRODUCTION The past year once again saw the U.S. Supreme Court grant certiorari

Fair Lending Developments: Standing to Sue Takes the Floor By John L. Ropiequet, Christopher S. Naveja, and L. Jean Noonan* INTRODUCTION The past year once again saw the U.S. Supreme Court grant certiorari

IN THE UNITED STATES DISTRICT COURT FOR THE NORTHERN DISTRICT OF GEORGIA ATLANTA DIVISION COMPLAINT

1 of 5 7/31/2007 4:02 PM IN THE UNITED STATES DISTRICT COURT FOR THE NORTHERN DISTRICT OF GEORGIA ATLANTA DIVISION UNITED STATES OF AMERICA, Plaintiff, v. DECATUR FEDERAL SAVINGS AND LOAN ASSOCIATION,

1 of 5 7/31/2007 4:02 PM IN THE UNITED STATES DISTRICT COURT FOR THE NORTHERN DISTRICT OF GEORGIA ATLANTA DIVISION UNITED STATES OF AMERICA, Plaintiff, v. DECATUR FEDERAL SAVINGS AND LOAN ASSOCIATION,

SETTLEMENT AGREEMENT BETWEEN THE UNITED STATES OF AMERICA AND KLEINBANK I. INTRODUCTION

SETTLEMENT AGREEMENT BETWEEN THE UNITED STATES OF AMERICA AND KLEINBANK I. INTRODUCTION 1. This Settlement Agreement ( Agreement ) is made and entered into by and between the United States of America (

SETTLEMENT AGREEMENT BETWEEN THE UNITED STATES OF AMERICA AND KLEINBANK I. INTRODUCTION 1. This Settlement Agreement ( Agreement ) is made and entered into by and between the United States of America (

Redlining. Evaluating Risk and Defending Claims. Melanie Brody Partner Mayer Brown

Redlining Evaluating Risk and Defending Claims Melanie Brody Partner Mayer Brown mbrody@mayerbrown.com Brian Clark Senior Manager Ernst & Young Brian.Clark@ey.com Speakers Melanie Brody Partner Mayer Brown

Redlining Evaluating Risk and Defending Claims Melanie Brody Partner Mayer Brown mbrody@mayerbrown.com Brian Clark Senior Manager Ernst & Young Brian.Clark@ey.com Speakers Melanie Brody Partner Mayer Brown

UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF FLORIDA CASE NO:

Case 1:13-cv-24506-XXXX Document 1 Entered on FLSD Docket 12/13/2013 Page 1 of 60 CITY OF MIAMI, a Florida municipal Corporation, UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF FLORIDA CASE NO: v. Plaintiff,

Case 1:13-cv-24506-XXXX Document 1 Entered on FLSD Docket 12/13/2013 Page 1 of 60 CITY OF MIAMI, a Florida municipal Corporation, UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF FLORIDA CASE NO: v. Plaintiff,

Housing Discrimination in your Community. October 27, 2017 Bloomington, IL Sponsored by:

Housing Discrimination in your Community October 27, 2017 Bloomington, IL Sponsored by: Agenda Fair Housing Laws Fair Lending Laws Community Reinvestment Act How laws are implemented/enforced Local and

Housing Discrimination in your Community October 27, 2017 Bloomington, IL Sponsored by: Agenda Fair Housing Laws Fair Lending Laws Community Reinvestment Act How laws are implemented/enforced Local and

UNITED STATES DISTRICT COURT WESTERN DISTRICT OF NEW YORK

!aaassseee 111:::111444- - -cccvvv- - -000000777222666 DDDooocccuuummmeeennnttt 111 FFFiiillleeeddd 000999///000222///111444 PPPaaagggeee 111 ooofff 333111 UNITED STATES DISTRICT COURT WESTERN DISTRICT

!aaassseee 111:::111444- - -cccvvv- - -000000777222666 DDDooocccuuummmeeennnttt 111 FFFiiillleeeddd 000999///000222///111444 PPPaaagggeee 111 ooofff 333111 UNITED STATES DISTRICT COURT WESTERN DISTRICT

Fair Lending Compliance Basics: Class is in Session!

Fair Lending Compliance Basics: Class is in Session! How to Control Fair Lending Risk and Identify Redlining Risk Meet Your Teacher Kimberly Boatwright, CRCM, CAMS Director of Compliance TRUPOINT Partners

Fair Lending Compliance Basics: Class is in Session! How to Control Fair Lending Risk and Identify Redlining Risk Meet Your Teacher Kimberly Boatwright, CRCM, CAMS Director of Compliance TRUPOINT Partners

FREQUENTLY ASKED QUESTIONS ABOUT THE NEW HMDA DATA. General Background

Federal Reserve Bank of New York Statistics Function March 31, 2005 FREQUENTLY ASKED QUESTIONS ABOUT THE NEW HMDA DATA General Background 1. What is the Home Mortgage Disclosure Act (HMDA)? HMDA, enacted

Federal Reserve Bank of New York Statistics Function March 31, 2005 FREQUENTLY ASKED QUESTIONS ABOUT THE NEW HMDA DATA General Background 1. What is the Home Mortgage Disclosure Act (HMDA)? HMDA, enacted

Anand S. Raman Bank Counsel Conference. November 13, Skadden

Fair Lending Update Anand S. Raman Louisiana Bankers Association 2008 Bank Counsel Conference November 13, 2008 Loan Modification Becomes Central Focus FDIC IndyMac plan Massachusetts AG action against

Fair Lending Update Anand S. Raman Louisiana Bankers Association 2008 Bank Counsel Conference November 13, 2008 Loan Modification Becomes Central Focus FDIC IndyMac plan Massachusetts AG action against

Fair Lending Examination Procedures Summary and Risk Factors Table

Federal Reserve Bank of Dallas Fair Lending Examination Procedures Summary and Risk Factors Table This publication is intended as a summary of the Fair Lending Examination Procedures. Also included is

Federal Reserve Bank of Dallas Fair Lending Examination Procedures Summary and Risk Factors Table This publication is intended as a summary of the Fair Lending Examination Procedures. Also included is

GAO. LARGE BANK MERGERS Fair Lending Review Could be Enhanced With Better Coordination

GAO United States General Accounting Office Report to the Honorable Maxine Waters and the Honorable Bernard Sanders House of Representatives November 1999 LARGE BANK MERGERS Fair Lending Review Could be

GAO United States General Accounting Office Report to the Honorable Maxine Waters and the Honorable Bernard Sanders House of Representatives November 1999 LARGE BANK MERGERS Fair Lending Review Could be

Courthouse News Service

IN THE CIRCUIT COURT OF JEFFERSON COUNTY, ALABAMA ELECTRONICALLY FILED 11/12/2008 2:03 PM CV-2008-903691.00 CIRCUIT COURT OF JEFFERSON COUNTY, ALABAMA ANNE-MARIE ADAMS, CLERK CITY OF BIRMINGHAM, a municipal

IN THE CIRCUIT COURT OF JEFFERSON COUNTY, ALABAMA ELECTRONICALLY FILED 11/12/2008 2:03 PM CV-2008-903691.00 CIRCUIT COURT OF JEFFERSON COUNTY, ALABAMA ANNE-MARIE ADAMS, CLERK CITY OF BIRMINGHAM, a municipal

Case 1:07-cv GAO Document 1 Filed 09/06/07 Page 1 of 18 IN THE UNITED STATES DISTRICT COURT FOR THE DISTRICT OF MASSACHUSETTS

Case 1:07-cv-11669-GAO Document 1 Filed 09/06/07 Page 1 of 18 IN THE UNITED STATES DISTRICT COURT FOR THE DISTRICT OF MASSACHUSETTS SUYAPA ALLEN on behalf of herself and all others similarly situated,

Case 1:07-cv-11669-GAO Document 1 Filed 09/06/07 Page 1 of 18 IN THE UNITED STATES DISTRICT COURT FOR THE DISTRICT OF MASSACHUSETTS SUYAPA ALLEN on behalf of herself and all others similarly situated,

BROWARD HOUSING COUNCIL CRA PERFORMANCE BY BROWARD BANKS IN MEETING HOUSING CREDIT NEEDS

BROWARD HOUSING COUNCIL CRA PERFORMANCE BY BROWARD BANKS IN MEETING HOUSING CREDIT NEEDS CRA IMPLEMENTATION WORKSHOP January 23, 2015 2 South Florida Context Areas of Opportunity Overview of HMDA Data

BROWARD HOUSING COUNCIL CRA PERFORMANCE BY BROWARD BANKS IN MEETING HOUSING CREDIT NEEDS CRA IMPLEMENTATION WORKSHOP January 23, 2015 2 South Florida Context Areas of Opportunity Overview of HMDA Data

A PHILANTHROPIC PARTNERSHIP FOR BLACK COMMUNITIES. Wealth and Asset Building BLACK FACTS

A PHILANTHROPIC PARTNERSHIP FOR BLACK COMMUNITIES Wealth and Asset Building BLACK FACTS Barriers to Wealth and Asset Creation: Homeownershiip DURING THE HOUSING CRISIS, BLACK HOMEOWNERS WERE TWICE AS LIKELY

A PHILANTHROPIC PARTNERSHIP FOR BLACK COMMUNITIES Wealth and Asset Building BLACK FACTS Barriers to Wealth and Asset Creation: Homeownershiip DURING THE HOUSING CRISIS, BLACK HOMEOWNERS WERE TWICE AS LIKELY

Is the site rent scheduled to increase over the next four years? If so, please explain.

APPLICANT CREDIT INFORMATION: If this is an INDIVIDUAL application, complete section A. If this is a JOINT application, complete section A&B. NOTE: If married, the spouse is not required to be the joint

APPLICANT CREDIT INFORMATION: If this is an INDIVIDUAL application, complete section A. If this is a JOINT application, complete section A&B. NOTE: If married, the spouse is not required to be the joint

FAIR LENDING and MORTGAGE SERVICING

FAIR LENDING and MORTGAGE SERVICING. What Is Housing Discrimination? Different treatment of a person by a housing provider or supplier of housing-related services because of that person s personal characteristics

FAIR LENDING and MORTGAGE SERVICING. What Is Housing Discrimination? Different treatment of a person by a housing provider or supplier of housing-related services because of that person s personal characteristics

in North Carolina House Select Committee on Rising Home Foreclosures January 23, 2008

Rising Foreclosures in North Carolina House Select Committee on Rising Home Foreclosures January 23, 2008 Mark E. Pearce, Deputy Commissioner NC Office of the Commissioner of Banks NCCOB s regulation of

Rising Foreclosures in North Carolina House Select Committee on Rising Home Foreclosures January 23, 2008 Mark E. Pearce, Deputy Commissioner NC Office of the Commissioner of Banks NCCOB s regulation of

Continued Racial and Ethnic Disparities in Ohio Mortgage Lending

Continued Racial and Ethnic Disparities in Ohio Mortgage Lending JEFFREY D. DILLMAN CARRIE PLEASANTS MERAN E. CHANG February 8 HOUSING RESEARCH & ADVOCACY CENTER 3631 PERKINS AVENUE, #3A-2 CLEVELAND, OHIO

Continued Racial and Ethnic Disparities in Ohio Mortgage Lending JEFFREY D. DILLMAN CARRIE PLEASANTS MERAN E. CHANG February 8 HOUSING RESEARCH & ADVOCACY CENTER 3631 PERKINS AVENUE, #3A-2 CLEVELAND, OHIO

Fair Lending 2012 Significant Risk Management Agenda Items

June 4, 2012 Fair Lending 2012 Significant Risk Management Agenda Items by Joseph T. Lynyak III In the first few months of 2012, lenders were cautiously optimistic that a recent Supreme Court case and

June 4, 2012 Fair Lending 2012 Significant Risk Management Agenda Items by Joseph T. Lynyak III In the first few months of 2012, lenders were cautiously optimistic that a recent Supreme Court case and

MEMORANDUM QUESTIONS PRESENTED. 1. Does the Equal Credit Opportunity Act ( ECOA ) and the Fair Housing Act

and the Fair Housing Act") MEMORANDUM To: Judge Howell Jackson and Judge Peter Tufano From: Alexis Chernak and Sheila Lopez Re: On a Motion to Dismiss, Jackson v. Ames Date: April 19, 2010 QUESTIONS PRESENTED 1. Does the Equal Credit

MEMORANDUM To: Judge Howell Jackson and Judge Peter Tufano From: Alexis Chernak and Sheila Lopez Re: On a Motion to Dismiss, Jackson v. Ames Date: April 19, 2010 QUESTIONS PRESENTED 1. Does the Equal Credit

IN THE CIRCUIT COURT OF COOK COUNTY, ILLINOIS COUNTY DEPARTMENT, CHANCERY DIVISION COMPLAINT FOR INJUNCTIVE AND OTHER RELIEF

... IN THE CIRCUIT COURT OF COOK COUNTY, ILLINOIS COUNTY DEPARTMENT, CHANCERY DIVISION Attorney No. 99000 ( THE PEOPLE OF THE STATE OF ( ILLINOIS, ( ( U9CH2648.t Plaintiff, ( ( v. ( ( No. WELLS FARGO AND

... IN THE CIRCUIT COURT OF COOK COUNTY, ILLINOIS COUNTY DEPARTMENT, CHANCERY DIVISION Attorney No. 99000 ( THE PEOPLE OF THE STATE OF ( ILLINOIS, ( ( U9CH2648.t Plaintiff, ( ( v. ( ( No. WELLS FARGO AND

The Untold Costs of Subprime Lending: Communities of Color in California. Carolina Reid. Federal Reserve Bank of San Francisco.

The Untold Costs of Subprime Lending: The Impacts of Foreclosure on Communities of Color in California Carolina Reid Federal Reserve Bank of San Francisco April 10, 2009 The views expressed herein are

The Untold Costs of Subprime Lending: The Impacts of Foreclosure on Communities of Color in California Carolina Reid Federal Reserve Bank of San Francisco April 10, 2009 The views expressed herein are

Fair Lending In The Mortgage Industry How You will do Business in 2014?

Fair Lending In The Mortgage Industry How You will do Business in 2014? Presenter: Tammy Butler, Master CMB and Director of Fair lending and Compliance, Optimal Blue Time to Prepare for January 2014 2013

Fair Lending In The Mortgage Industry How You will do Business in 2014? Presenter: Tammy Butler, Master CMB and Director of Fair lending and Compliance, Optimal Blue Time to Prepare for January 2014 2013

Racial and Ethnic Disparities in Ohio Mortgage Lending

Racial and Ethnic Disparities in Ohio Mortgage Lending JEFFREY D. DILLMAN CARRIE BENDER PLEASANTS DAVID M. BROWN November 2006 HOUSING RESEARCH & ADVOCACY CENTER 3631 PERKINS AVENUE, #3A-2 CLEVELAND, OHIO

Racial and Ethnic Disparities in Ohio Mortgage Lending JEFFREY D. DILLMAN CARRIE BENDER PLEASANTS DAVID M. BROWN November 2006 HOUSING RESEARCH & ADVOCACY CENTER 3631 PERKINS AVENUE, #3A-2 CLEVELAND, OHIO

CRA a Brief History Lynette C. Briggs, VP - Regional CRA Officer

CRA a Brief History Lynette C. Briggs, VP - Regional CRA Officer August 2016 Community Reinvestment Act (CRA) a Brief History 2 Community Reinvestment Act (CRA) The Community Reinvestment Act (CRA) Brief

CRA a Brief History Lynette C. Briggs, VP - Regional CRA Officer August 2016 Community Reinvestment Act (CRA) a Brief History 2 Community Reinvestment Act (CRA) The Community Reinvestment Act (CRA) Brief

Who is Lending and Who is Getting Loans?

Trends in 1-4 Family Lending in New York City An ANHD White Paper February 2016 As much as New York City is a city of renters, nearly a third of New Yorkers own their own homes. Responsible, affordable

Trends in 1-4 Family Lending in New York City An ANHD White Paper February 2016 As much as New York City is a city of renters, nearly a third of New Yorkers own their own homes. Responsible, affordable

HOUSING & PREDATORY LENDING WORKING GROUP ON CLOSING THE RACIAL WEALTH GAP

Page 1 of 5 HOUSING & PREDATORY LENDING WORKING GROUP ON CLOSING THE RACIAL WEALTH GAP JOHN POWELL, JASON REECE, CRAIG RATCHFORD AND CHRISTY ROGERS KIRWAN INSTITUTE AUGUST 27 PREPARED FOR THE INSIGHT CENTER

Page 1 of 5 HOUSING & PREDATORY LENDING WORKING GROUP ON CLOSING THE RACIAL WEALTH GAP JOHN POWELL, JASON REECE, CRAIG RATCHFORD AND CHRISTY ROGERS KIRWAN INSTITUTE AUGUST 27 PREPARED FOR THE INSIGHT CENTER

MORTGAGE BANKERS ASSOCIATION OF ALABAMA

MORTGAGE BANKERS ASSOCIATION OF ALABAMA What s on the horizon for 2017? January 17, 2017 Presented by: J. David Dresher Jason R. Bushby Bradley Arant Boult Cummings LLP Attorney-Client Privilege. Agenda

MORTGAGE BANKERS ASSOCIATION OF ALABAMA What s on the horizon for 2017? January 17, 2017 Presented by: J. David Dresher Jason R. Bushby Bradley Arant Boult Cummings LLP Attorney-Client Privilege. Agenda

Fair Winds and Following Seas The sea, its perils and fair lending management? Timothy R. Burniston Executive Vice President, WKFS Consulting

Fair Winds and Following Seas The sea, its perils and fair lending management? Timothy R. Burniston Executive Vice President, WKFS Consulting SEA CAPTAIN: Responsible for operating ships in lakes, rivers,

Fair Winds and Following Seas The sea, its perils and fair lending management? Timothy R. Burniston Executive Vice President, WKFS Consulting SEA CAPTAIN: Responsible for operating ships in lakes, rivers,

Subprime Originations and Foreclosures in New York State: A Case Study of Nassau, Suffolk, and Westchester Counties.

Subprime Originations and Foreclosures in New York State: A Case Study of Nassau, Suffolk, and Westchester Counties Cambridge, MA Lexington, MA Hadley, MA Bethesda, MD Washington, DC Chicago, IL Cairo,

Subprime Originations and Foreclosures in New York State: A Case Study of Nassau, Suffolk, and Westchester Counties Cambridge, MA Lexington, MA Hadley, MA Bethesda, MD Washington, DC Chicago, IL Cairo,

Lake County Community Lending Factbook

Lake County Community Lending Factbook SAMANTHA HOOVER CARRIE PLEASANTS July 2009 HOUSING RESEARCH & ADVOCACY CENTER 3631 PERKINS AVENUE, #3A-2 CLEVELAND, OHIO 44114 (216) 361-9240 (PHONE) (216) 426-1290

Lake County Community Lending Factbook SAMANTHA HOOVER CARRIE PLEASANTS July 2009 HOUSING RESEARCH & ADVOCACY CENTER 3631 PERKINS AVENUE, #3A-2 CLEVELAND, OHIO 44114 (216) 361-9240 (PHONE) (216) 426-1290

FEDERAL RESERVE SYSTEM. Goldman Sachs Bank USA New York, New York. Order Approving the Acquisition of Assets and Assumption of Liabilities

FRB Order No. 2016-03 March 21, 2016 FEDERAL RESERVE SYSTEM Goldman Sachs Bank USA New York, New York Order Approving the Acquisition of Assets and Assumption of Liabilities Goldman Sachs Bank USA ( GS

FRB Order No. 2016-03 March 21, 2016 FEDERAL RESERVE SYSTEM Goldman Sachs Bank USA New York, New York Order Approving the Acquisition of Assets and Assumption of Liabilities Goldman Sachs Bank USA ( GS

Case 1:08-cv RWZ Document 57 Filed 07/09/09 Page 1 of 41 UNITED STATES DISTRICT COURT DISTRICT OF MASSACHUSETTS

Case 1:08-cv-10157-RWZ Document 57 Filed 07/09/09 Page 1 of 41 UNITED STATES DISTRICT COURT DISTRICT OF MASSACHUSETTS CECIL BARRETT, JR., CYNTHIA BARRETT, JEAN BLANCO GUERRIER, ANGELIQUE M. BASTIEN, JACQUELINE

Case 1:08-cv-10157-RWZ Document 57 Filed 07/09/09 Page 1 of 41 UNITED STATES DISTRICT COURT DISTRICT OF MASSACHUSETTS CECIL BARRETT, JR., CYNTHIA BARRETT, JEAN BLANCO GUERRIER, ANGELIQUE M. BASTIEN, JACQUELINE

LENDING: KEY EXAMINER TRENDS

LENDING: KEY EXAMINER TRENDS 2015 Temenos USA, Inc. All rights reserved. Leah M. Hamilton Chief Compliance Officer, TriComply Services WHAT YOU WILL LEARN TRID Compliance Reprieve Common issues Regulation

LENDING: KEY EXAMINER TRENDS 2015 Temenos USA, Inc. All rights reserved. Leah M. Hamilton Chief Compliance Officer, TriComply Services WHAT YOU WILL LEARN TRID Compliance Reprieve Common issues Regulation

Implications and Risks of New HMDA Data Disclosure

Implications and Risks of New HMDA Data Disclosure By David Skanderson, Ph.D. January 2018 A version of this paper appeared in ABA Bank Compliance, January/February 2018 The conclusions set forth herein

Implications and Risks of New HMDA Data Disclosure By David Skanderson, Ph.D. January 2018 A version of this paper appeared in ABA Bank Compliance, January/February 2018 The conclusions set forth herein

Fair Lending Compliance Management: Developing Strategies for Emerging Challenges

Fair Lending Compliance Management: Developing Strategies for Emerging Challenges August 20, 2014 2014 Crowe Horwath LLP 1 Agenda: The principal concepts of fair lending Current trends in fair lending

Fair Lending Compliance Management: Developing Strategies for Emerging Challenges August 20, 2014 2014 Crowe Horwath LLP 1 Agenda: The principal concepts of fair lending Current trends in fair lending

Federal Reserve Bank ATTN: Karen Smith Petition To Downgrade CRA Rating Complaint August 10, 2018 The Renaissance Indexes Group (RIG, Claimant) files

files") Federal Reserve Bank ATTN: Karen Smith Petition To Downgrade CRA Rating Complaint August 10, 2018 The Renaissance Indexes Group (RIG, Claimant) files the Petition To Downgrade Complaint against Comerica

Federal Reserve Bank ATTN: Karen Smith Petition To Downgrade CRA Rating Complaint August 10, 2018 The Renaissance Indexes Group (RIG, Claimant) files the Petition To Downgrade Complaint against Comerica

Increasing homeownership among

Subprime Lending and Foreclosure in Hennepin and Ramsey Counties: An Empirical Analysis by Jeff Crump Increasing homeownership among low-income and minority communities is a major goal of housing policy

Subprime Lending and Foreclosure in Hennepin and Ramsey Counties: An Empirical Analysis by Jeff Crump Increasing homeownership among low-income and minority communities is a major goal of housing policy

An introduction to the Community Reinvestment Act. John Meeks Atlanta Region FDIC Community Affairs

An introduction to the Community Reinvestment Act John Meeks Atlanta Region FDIC Community Affairs What is the CRA? CRA stands for: The Community Reinvestment Act of 1977 The regulations implementing the

An introduction to the Community Reinvestment Act John Meeks Atlanta Region FDIC Community Affairs What is the CRA? CRA stands for: The Community Reinvestment Act of 1977 The regulations implementing the

Widening the Gap: How the Housing Crisis Deepened Racial Disparities in St. Paul and How to Fix It

Widening the Gap: How the Housing Crisis Deepened Racial Disparities in St. Paul and How to Fix It 2720 East 22nd Street Minneapolis, MN 55406-1315 (612) 333-1260 www.isaiah-mn.org Widening the Gap: How

Widening the Gap: How the Housing Crisis Deepened Racial Disparities in St. Paul and How to Fix It 2720 East 22nd Street Minneapolis, MN 55406-1315 (612) 333-1260 www.isaiah-mn.org Widening the Gap: How

FORECLOSURES, INTEGRATION, AND THE FUTURE OF THE FAIR HOUSING ACT

FORECLOSURES, INTEGRATION, AND THE FUTURE OF THE FAIR HOUSING ACT JOHN P. RELMAN * INTRODUCTION In their seminal work, American Apartheid, Douglas Massey and Nancy Denton compellingly chronicle the way

FORECLOSURES, INTEGRATION, AND THE FUTURE OF THE FAIR HOUSING ACT JOHN P. RELMAN * INTRODUCTION In their seminal work, American Apartheid, Douglas Massey and Nancy Denton compellingly chronicle the way

Regulatory Practice Letter December 2014 RPL 14-22

Regulatory Practice Letter December 2014 RPL 14-22 Automobile Supervision and Enforcement Regulatory Actions and CFPB Proposed Rule Executive Summary The automobile finance industry is under heightened

Regulatory Practice Letter December 2014 RPL 14-22 Automobile Supervision and Enforcement Regulatory Actions and CFPB Proposed Rule Executive Summary The automobile finance industry is under heightened

October 22, Joseph A. Smith Office of Mortgage Settlement Oversight 301 Fayetteville St., Suite 1801 Raleigh, NC Via electronic mail

October 22, 2012 Joseph A. Smith Office of Mortgage Settlement Oversight 301 Fayetteville St., Suite 1801 Raleigh, NC 27601 Via electronic mail Dear Mr. Smith: Thank you again for speaking with members

October 22, 2012 Joseph A. Smith Office of Mortgage Settlement Oversight 301 Fayetteville St., Suite 1801 Raleigh, NC 27601 Via electronic mail Dear Mr. Smith: Thank you again for speaking with members

27% 42% 51% 16% 51% 19% PROFILE. Assets & opportunity ProfILe: PortLANd. key highlights. ABoUt the ProfILe ASSETS & OPPORTUNITY

Assets & opportunity ProfILe: PortLANd ASSETS & OPPORTUNITY PROFILE key highlights 27% of Portland households live in asset poverty Cities have long been thought of as places of opportunity for low-income

Assets & opportunity ProfILe: PortLANd ASSETS & OPPORTUNITY PROFILE key highlights 27% of Portland households live in asset poverty Cities have long been thought of as places of opportunity for low-income

FEDERAL RESERVE BANK OF DALLAS KAREN R. SMITH DIRECTOR-APPLICATIONS 2200 NORTH PEARL STREET DALI.AS. TX 75201 August 10, 2017 Ms. Catherine Jaure Compliance Officer Frost Bank 3838 Rogers Road San Antonio,

FEDERAL RESERVE BANK OF DALLAS KAREN R. SMITH DIRECTOR-APPLICATIONS 2200 NORTH PEARL STREET DALI.AS. TX 75201 August 10, 2017 Ms. Catherine Jaure Compliance Officer Frost Bank 3838 Rogers Road San Antonio,

REINVESTMENT ALERT. Woodstock Institute November, 1997 Number 11

REINVESTMENT ALERT Woodstock Institute November, 1997 Number 11 New Small Business Data Show Loans Going To Higher-Income Neighborhoods in Chicago Area In October, federal banking regulators released new

REINVESTMENT ALERT Woodstock Institute November, 1997 Number 11 New Small Business Data Show Loans Going To Higher-Income Neighborhoods in Chicago Area In October, federal banking regulators released new

NJBA Community Reinvestment Act and Fair Lending Conference February 23, 2016 Kevin McMahon, Senior Compliance Examiner

NJBA Community Reinvestment Act and Fair Lending Conference February 23, 2016 Kevin McMahon, Senior Compliance Examiner Overview CRA - Community Development Definition - Best Practices Fair Lending - Analysis

NJBA Community Reinvestment Act and Fair Lending Conference February 23, 2016 Kevin McMahon, Senior Compliance Examiner Overview CRA - Community Development Definition - Best Practices Fair Lending - Analysis

DRAFT December 10, 2015 Real Estate Finance Spring 2016

UNIVERSITY OF BALTIMORE SCHOOL OF LAW SPRING SEMESTER 2016 Course: Instructor: Class hours: LAW 753, Real Estate Finance, 3 credits Nina F. Simon, Esq. Phone: (202) 827-9770 Email: nsimon@ubalt.edu Office

UNIVERSITY OF BALTIMORE SCHOOL OF LAW SPRING SEMESTER 2016 Course: Instructor: Class hours: LAW 753, Real Estate Finance, 3 credits Nina F. Simon, Esq. Phone: (202) 827-9770 Email: nsimon@ubalt.edu Office

Fair Lending Risk Management

Presented by: Martin (Marty) Mitchell, CRCM Managing Director, ProBank Austin Robert J. (Bob) Mullenbach, CRCM Managing Director, Compliance Division Deputy, ProBank Austin Fair Lending Laws ECOA Prohibits

Presented by: Martin (Marty) Mitchell, CRCM Managing Director, ProBank Austin Robert J. (Bob) Mullenbach, CRCM Managing Director, Compliance Division Deputy, ProBank Austin Fair Lending Laws ECOA Prohibits

SECTION FIVE: FORECLOSURE AND LENDING CHARACTERISTICS

SECTION FIVE: FORECLOSURE AND LENDING CHARACTERISTICS Legend Regulated Affiliate of Regulated Unregulated 0 Miles 10 Foreclosures by Type of Lending Institution This map shows the type of lending institutions

SECTION FIVE: FORECLOSURE AND LENDING CHARACTERISTICS Legend Regulated Affiliate of Regulated Unregulated 0 Miles 10 Foreclosures by Type of Lending Institution This map shows the type of lending institutions

Teresa Garcia, Mission Economic Development Agency

facilitate enforcement of fair lending laws and enable communities, governmental entities, and creditors to identify business and community development needs and opportunities of women owned, minority-owned,

facilitate enforcement of fair lending laws and enable communities, governmental entities, and creditors to identify business and community development needs and opportunities of women owned, minority-owned,

Compliance Challenges in a Changing Economic Environment

Compliance Challenges in a Changing Economic Environment Call the Fed Audio Conference December 10, 2008 The following presentation contains the views and opinions of the speakers and his or her interpretation

Compliance Challenges in a Changing Economic Environment Call the Fed Audio Conference December 10, 2008 The following presentation contains the views and opinions of the speakers and his or her interpretation

Re: Docket No.: CFPB ; Proposed Rule on Class Action Waivers in Forced Arbitration Agreements

CENTER FOR JUSTICE & DEMOCRACY 185 WEST BROADWAY NEW YORK, NY 10013 TEL: 212.431.2882 centerjd@centerjd.org http://centerjd.org August 1, 2016 The Honorable Richard Cordray Director Consumer Financial

CENTER FOR JUSTICE & DEMOCRACY 185 WEST BROADWAY NEW YORK, NY 10013 TEL: 212.431.2882 centerjd@centerjd.org http://centerjd.org August 1, 2016 The Honorable Richard Cordray Director Consumer Financial

Keeping Fintech Fair: Thinking about Fair Lending and UDAP Risks

Keeping Fintech Fair: Thinking about Fair Lending and UDAP Risks Outlook Live Webinar July 16, 2018 Carol A. Evans Associate Director Div. of Consumer & Community Affairs Federal Reserve Board Katrina

Keeping Fintech Fair: Thinking about Fair Lending and UDAP Risks Outlook Live Webinar July 16, 2018 Carol A. Evans Associate Director Div. of Consumer & Community Affairs Federal Reserve Board Katrina

Keeping Fintech Fair: Thinking about Fair Lending and UDAP Risks

Keeping Fintech Fair: Thinking about Fair Lending and UDAP Risks Outlook Live Webinar July 16, 2018 Carol A. Evans Associate Director Div. of Consumer & Community Affairs Federal Reserve Board Katrina

Keeping Fintech Fair: Thinking about Fair Lending and UDAP Risks Outlook Live Webinar July 16, 2018 Carol A. Evans Associate Director Div. of Consumer & Community Affairs Federal Reserve Board Katrina

How Cities Can Pursue Responsible Banking: Model Local Responsible Banking Ordinance Creates Community Reinvestment Requirements for Financial

How Cities Can Pursue Responsible Banking: Model Local Responsible Banking Ordinance Creates Community Reinvestment Requirements for Financial Institutions JULY 2012 How Cities Can Pursue Responsible Banking:

How Cities Can Pursue Responsible Banking: Model Local Responsible Banking Ordinance Creates Community Reinvestment Requirements for Financial Institutions JULY 2012 How Cities Can Pursue Responsible Banking:

City of Cleveland Community Lending Factbook

City of Cleveland Community Lending Factbook KRISSIE WELLS CARRIE PLEASANTS September 2010 HOUSING RESEARCH & ADVOCACY CENTER 3631 PERKINS AVENUE, #3A-2 CLEVELAND, OHIO 44114 (216) 361-9240 (PHONE) (216)

City of Cleveland Community Lending Factbook KRISSIE WELLS CARRIE PLEASANTS September 2010 HOUSING RESEARCH & ADVOCACY CENTER 3631 PERKINS AVENUE, #3A-2 CLEVELAND, OHIO 44114 (216) 361-9240 (PHONE) (216)

**PRESS RELEASE** FEUER SUES JP MORGAN CHASE, ALLEGING DISCRIMINATORY MORTGAGE LENDING

FOR IMMEDIATE RELEASE Rob Wilcox 1-- Suite 00, City Hall East Los Angeles, CA 001 From the Office of the City Attorney Mike Feuer Phone: 1--0 Fax: 1--0 http://www.atty.lacity.org May 0, 01 **PRESS RELEASE**

FOR IMMEDIATE RELEASE Rob Wilcox 1-- Suite 00, City Hall East Los Angeles, CA 001 From the Office of the City Attorney Mike Feuer Phone: 1--0 Fax: 1--0 http://www.atty.lacity.org May 0, 01 **PRESS RELEASE**

Fair Lending: Learn the Facts

Fair Lending: Learn the Facts Now, I say to you today my friends, even though we face the difficulties of today and tomorrow, I still have a dream. It is a dream deeply rooted in the American dream. I

Fair Lending: Learn the Facts Now, I say to you today my friends, even though we face the difficulties of today and tomorrow, I still have a dream. It is a dream deeply rooted in the American dream. I

In the first three months of 2007, there

Subprime Lending and Foreclosure in Hennepin and Ramsey Counties by Jeff Crump In the first three months of 2007, there were 678 foreclosure sales in the city of Minneapolis, an increase of more than 100%

Subprime Lending and Foreclosure in Hennepin and Ramsey Counties by Jeff Crump In the first three months of 2007, there were 678 foreclosure sales in the city of Minneapolis, an increase of more than 100%

Foreclosures on Non-Owner-Occupied Properties in Ohio s Cuyahoga County: Evidence from Mortgages Originated in

FEDERAL RESERVE BANK OF MINNEAPOLIS COMMUNITY AFFAIRS REPORT Report No. 2010-2 Foreclosures on Non-Owner-Occupied Properties in Ohio s Cuyahoga County: Evidence from Mortgages Originated in 2005 2006 Richard

FEDERAL RESERVE BANK OF MINNEAPOLIS COMMUNITY AFFAIRS REPORT Report No. 2010-2 Foreclosures on Non-Owner-Occupied Properties in Ohio s Cuyahoga County: Evidence from Mortgages Originated in 2005 2006 Richard

Mile High Money: Payday Stores Target Colorado Communities of Color

Mile High Money: Payday Stores Target Colorado Communities of Color Delvin Davis, Senior Researcher August 2017 (amended February 2018) Summary Findings: Majority minority areas in Colorado (over 50% African

Mile High Money: Payday Stores Target Colorado Communities of Color Delvin Davis, Senior Researcher August 2017 (amended February 2018) Summary Findings: Majority minority areas in Colorado (over 50% African

Paying More for the American Dream III

Paying More for the American Dream III Promoting Responsible Lending to Lower-Income Communities and Communities of Color April 2009 A Joint Report By: California Reinvestment Coalition Community Reinvestment

Paying More for the American Dream III Promoting Responsible Lending to Lower-Income Communities and Communities of Color April 2009 A Joint Report By: California Reinvestment Coalition Community Reinvestment

ASSOCIATED BANK, N.A. COMMUNITY COMMITMENT PLAN FOR

ASSOCIATED BANK, N.A. COMMUNITY COMMITMENT PLAN FOR 2018-2020 Our Purpose Associated Bank, N.A. (Associated) recognizes our success is dependent upon strong relationships with the communities where we

ASSOCIATED BANK, N.A. COMMUNITY COMMITMENT PLAN FOR 2018-2020 Our Purpose Associated Bank, N.A. (Associated) recognizes our success is dependent upon strong relationships with the communities where we

The Effect of GSEs, CRA, and Institutional. Characteristics on Home Mortgage Lending to. Underserved Markets

The Effect of GSEs, CRA, and Institutional Characteristics on Home Mortgage Lending to Underserved Markets HUD Final Report Richard Williams, University of Notre Dame December 1999 Direct all inquiries

The Effect of GSEs, CRA, and Institutional Characteristics on Home Mortgage Lending to Underserved Markets HUD Final Report Richard Williams, University of Notre Dame December 1999 Direct all inquiries

Compensation. November 16, 2016

Compensation November 16, 2016 Moderator: Robert Northway, Partner & Head of Consumer Banking and Global RE Practice, McLagan Speaker: Richard Andreano, Jr., Practice Group Leader, Ballard Spahr LLP Compensation

Compensation November 16, 2016 Moderator: Robert Northway, Partner & Head of Consumer Banking and Global RE Practice, McLagan Speaker: Richard Andreano, Jr., Practice Group Leader, Ballard Spahr LLP Compensation

April Fair Lending Report of the Consumer Financial Protection Bureau

April 2017 Fair Lending Report of the Consumer Financial Protection Bureau Message from Richard Cordray Director of the CFPB For over five years, the Consumer Financial Protection Bureau has pursued its

April 2017 Fair Lending Report of the Consumer Financial Protection Bureau Message from Richard Cordray Director of the CFPB For over five years, the Consumer Financial Protection Bureau has pursued its

PUBLIC DISCLOSURE. December 6, 2004 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION BANK OF EUFAULA RSSD#

PUBLIC DISCLOSURE COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION BANK OF EUFAULA RSSD# 343051 P.O. BOX 607 EUFAULA, OKLAHOMA 74432-0607 Federal Reserve Bank of Kansas City 925 Grand Boulevard Kansas

PUBLIC DISCLOSURE COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION BANK OF EUFAULA RSSD# 343051 P.O. BOX 607 EUFAULA, OKLAHOMA 74432-0607 Federal Reserve Bank of Kansas City 925 Grand Boulevard Kansas

Notice. Conducting a Fair Lending Self Assessment Britt Faircloth, CRCM 4/2/2018. April 2018 Florida Bankers Association

Conducting a Fair Lending Self Assessment Britt Faircloth, CRCM April 2018 Florida Bankers Association Notice The information presented in this seminar summarizes general guidance and is intended only

Conducting a Fair Lending Self Assessment Britt Faircloth, CRCM April 2018 Florida Bankers Association Notice The information presented in this seminar summarizes general guidance and is intended only

Case 2:16-cv Document 1 Filed 09/22/16 Page 1 of 16 Page ID #:1

Case :-cv-0 Document Filed 0// Page of Page ID #: 0 R. GABRIEL D. O MALLEY, MA BAR # (Email: gabriel.o malley@cfpb.gov) (Phone: 0--) SARAH PREIS, DC BAR # (Email: sarah.preis@cfpb.gov) (Phone: 0--) PATRICK

Case :-cv-0 Document Filed 0// Page of Page ID #: 0 R. GABRIEL D. O MALLEY, MA BAR # (Email: gabriel.o malley@cfpb.gov) (Phone: 0--) SARAH PREIS, DC BAR # (Email: sarah.preis@cfpb.gov) (Phone: 0--) PATRICK

Predatory & Subprime Lending

OHIO RANKS FIFTH IN THE NATION FOR THE NUMBER OF SUBPRIME REFINANCING LOANS The Miami Valley Fair Housing Center In The News, July 6, 2000 Predatory & Subprime Lending City of Ashtabula Fair Housing Office

OHIO RANKS FIFTH IN THE NATION FOR THE NUMBER OF SUBPRIME REFINANCING LOANS The Miami Valley Fair Housing Center In The News, July 6, 2000 Predatory & Subprime Lending City of Ashtabula Fair Housing Office