Homeownership. Cycling Demand

|

|

|

- Walter Perry

- 5 years ago

- Views:

Transcription

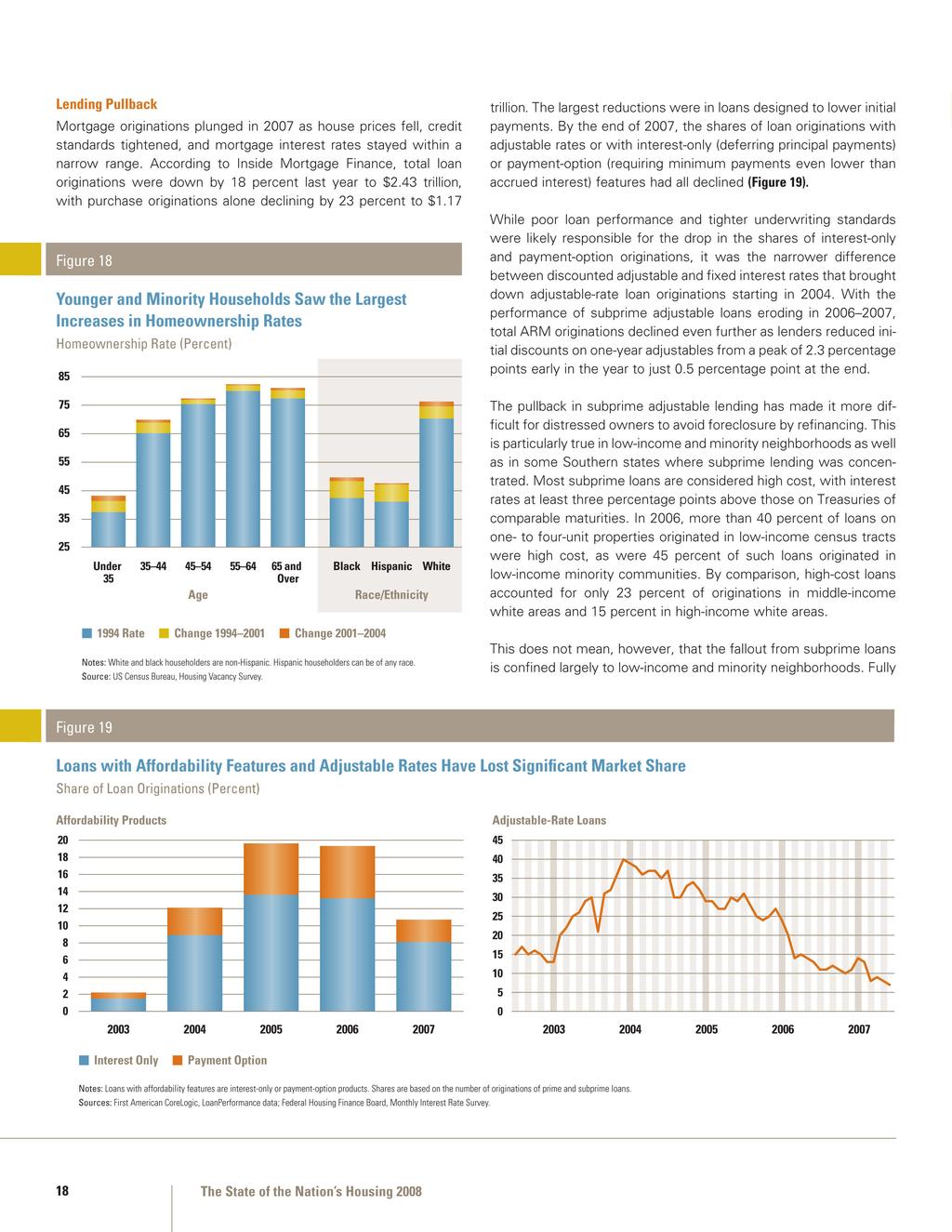

1 4 Homeownership Falling home prices, stringent credit standards, and stubbornly high inventories of vacant homes roiled homeownership markets throughout 7 and into 8. Homeowners whose mortgage interest rates have reset or who have lost their jobs are especially hard hit. With home prices down, many of these owners cannot sell or refinance to get out of unmanageable loans. But even those able to pay their mortgages and under no pressure to sell are feeling the spillover effects from the foreclosure crisis on home prices and credit markets. The only silver lining is that lower prices and slightly lower mortgage interest rates are easing affordability for first-time buyers still able to qualify for loans. Cycling Demand Despite all the attention that subprime and so-called affordability loans have gotten for fueling the housing boom, the national homeownership rate had already peaked by the time these products took off in 4. Indeed, the homeownership rate began to retreat in 5 and 6 and then dropped more sharply in 7, to 67.8 percent in the fourth quarter. Thus, it appears that these mortgage innovations did less to lift homeownership than to enable homebuyers to chase prices higher, investors to borrow money to speculate, and owners to borrow against home equity. What sparked the decade-long homeownership boom was instead the improved affordability brought by lower interest rates and flat home prices in the wake of the recession. That downturn was quickly followed by the longest economic expansion since World War II and unusually strong, broad-based income growth. During this period, Congress and regulators also leaned on financial institutions to step up lending in low-income and minority neighborhoods. Equally important, widespread adoption of automated underwriting tools in the latter part of the 199s allowed many more borrowers to qualify for prime loans while adding little to credit risk. From 1994 to 1, the national homeownership rate surged by 3.8 percentage points, and rose even more among minorities and younger households (Figure 18). Innovations in prime mortgage lending contributed to larger homeownership rate advances among blacks (up 5.9 points), Hispanics (up 6.1 points), and households under 35 years old (up 3.9 points). After the 1 recession but before house prices and lending practices went wild, the national homeownership rate climbed another 1.2 percentage points to a peak of 69. percent. In the three years since, homeownership rates have fallen back for most groups, including a nearly 2.-point drop among black households and a 1.4-point drop among young households (Table A-5). Once the current turmoil passes, the full benefits of automated underwriting tools in the prime mortgage market will once again provide a favorable climate for homeownership growth. With more prudent underwriting and less risky products, subprime lending may well reassert itself as a viable business although one unlikely to serve as many borrowers as it did at its peak when more reckless practices were tolerated. Joint Center for Housing Studies of Harvard University 17

2

3 Figure Skyrocketing Subprime Delinquencies 6+ Day Delinquency Rates (Percent) :1 4:1 5:1 6:1 7:1 Fixed Loans Adjustable Loans Interest-Only and Payment-Option Loans Caused the Collapse of Subprime Credit Originations Subprime Mortgage Originations (Billions of 7 dollars) 4:4 5:4 6:4 7:4 Notes: Subprime loans are defined by lenders and are primarily 2/28 ARMs. Interest-only and payment-option delinquency rates are averages of monthly data. Delinquency rates are the share of loans serviced that are at least 6 days past due or in foreclosure. Sources: First American CoreLogic, LoanPerformance data; Mortgage Bankers Association, National Delinquency Survey; Inside Mortgage Finance, 8 Mortgage Market Statistical Annual adjusted for inflation by the CPI-U for All Items. 57 percent of high-cost loans in 6 were originated outside such areas. While more diffuse, some of these markets are also seeing pockets of distressed properties. The markets most exposed to the cutback in loans with interestonly and payment-option features are the country s most expensive. Indeed, a simple measure of affordability the ratio of median home price to median income alone accounts for almost 7 percent of the variation in the metro share of these products at the 6 peak. Furthermore, the areas with the highest shares of these affordability products in 6 saw the largest declines in 7. For example, loans with affordability features accounted for more than half of all loans originated in San Diego, San Jose, and Santa Cruz in 6 but less than a third in 7. States with high 6 shares and large 7 declines include Nevada (from 41 percent to 25 percent), Arizona (29 percent to 18 percent), Florida (25 percent to 13 percent), and Washington, DC (26 percent to 15 percent). As they continued their exit from markets in 7, housing investors also contributed to the drop in mortgage lending. First American CoreLogic s LoanPerformance data indicate that the investor share of all non-prime loan originations (including subprime, Alt-A, and non-conforming loans) peaked at 12.2 percent in the first quarter of 6, before falling back to 8.7 percent in the third quarter of 7 (Table W-8). The dollar volume of all non-prime investor loans plunged by two-thirds over this period, and of just subprime investor loans by a whopping seven-eighths. According to the Mortgage Bankers Association, loans to absentee owners also accounted for almost one in five loans entering foreclosure in that quarter. Shares in states with distressed economies (such as Ohio and Michigan) or with widespread speculation (such as Nevada and Colorado) were even higher. Subprime Turmoil While mortgage performance in general has been slipping since mid-6, delinquencies in the subprime market are particularly high especially among riskier adjustable-rate, interest-only, and payment-option mortgages (Figure ). While each lender has its own rules of thumb to define subprime, these loans are made primarily to borrowers with past credit problems. Because of their abysmal performance, subprime loans fell from percent of originations in 5 6 to just 3.1 percent in the fourth quarter of 7 (Table A-6). The real dollar volume plummeted from $139 billion in the fourth quarter of 6 to $14 billion at the end of last year. So far in 8, the volume of subprime lending has likely dropped further. The roots of the crisis lie in the unusually tight housing markets, historically low interest rates, and investor demand for high returns in the first half of this decade. This was also a period of unprecedented global economic growth, and capital was pouring into the United States. American homebuyers took advantage of the low interest rates these conditions produced to snap up properties. But with markets tight and multiple bidding situations common, home prices started to climb much faster than incomes. Even subprime loans, which predictably perform worse than prime loans, were seen as safe enough investments because home values were appreciating so quickly. In their search for ever-higher returns, investors borrowed shortterm money from banks to purchase securities backed by subprime mortgages. By leveraging their investments, they hoped to boost their profits but exposed themselves to refinance risk each time they had to roll over their debt. Meanwhile, the cash flows associated with mortgage payments were sliced up and in some cases pooled with nonresidential loans, obscuring how deterioration in loan performance would affect many bond issues. Joint Center for Housing Studies of Harvard University 19

4 At the same time, lenders enabled buyers to chase prices higher by offering products that lowered initial mortgage payments but exposed borrowers to the risk of payment shocks when their interest rates reset. Lenders also took on additional risk by requiring small downpayments, even though modest home price declines could wipe out an owner s equity. On top of this, lenders were all too willing to relax income-reporting requirements to draw selfemployed and other hard-to-qualify borrowers into the market. These borrowers were willing to pay slightly higher interest rates or fees in return for not having to verify their incomes. With paymentoption, low-downpayment, and no-income-verification loans readily available, housing investors had access to low-cost, highly leveraged capital as never before. Lenders layered risks on top of risks without considering the potential consequences for performance, while mortgage investors continued to buy up staggering volumes of these loans. But by 5, higher borrowing costs and skyrocketing home prices were slowing homebuyer demand in some markets. With the underlying indexes on adjustable-rate loans increasing by three percentage points, mortgage rates rose just as many subprime loans began to hit their reset dates. At that point, borrowers with these loans started to see their monthly mortgage costs go up. In 6 and 7, the inventory of vacant homes for sale ballooned and prices fell, eliminating the protection afforded by strong appreciation and boosting the share of distressed borrowers. Making Figure 21 Delinquency Rates on Recent Adjustable Subprime Loans Soared Even Before Resets 6+ Day Delinquency Rates (Percent) Months 12 Months 18 Months Time Since Origination Year of Origination: Notes: Subprime loans are defined by lenders and are primarily 2/28 ARMs. Delinquency rates are the share of loans serviced that are at least 6 days past due or in foreclosure. Source: First American CoreLogic, LoanPerformance data. matters worse, several metropolitan areas in the Midwest were in recession and tighter credit standards prevented borrowers from refinancing out of their troubles. Charges of unfair and deceptive practices were also leveled against many lenders. Defaults on subprime loans within six to eighteen months of origination even before most resets hit increased with each successive vintage from 3 to 7 (Figure 21). The speed and severity of the erosion in subprime loan performance had disastrous impacts on credit availability and liquidity. Stung by losses and uncertain about how much worse performance would become, mortgage investors stopped buying new originations and tried to sell their positions in existing loans in a market with little demand. Once sought-after mortgage securities suddenly dropped sharply in value. Lenders lost confidence in some investment funds and mortgage companies, and demanded repayment of their shortterm borrowings. With no other lenders stepping up, many investment funds collapsed and mortgage companies went under. These troubles not only shuttered the subprime market but also badly crippled the prime and near-prime (Alt-A) markets. In particular, the interest-rate differential between prime mortgages that can and cannot be sold to Fannie Mae and Freddie Mac widened dramatically. In addition, loans requiring no documentation and very low downpayments all but disappeared by late 7. The Foreclosure Crisis With borrowers defaulting in record numbers and lenders unable to restructure the loans, the number and share of homes entering foreclosure skyrocketed to their highest levels since recordkeeping began in According to Mortgage Bankers Association counts covering about 8 percent of loans, the number of loans in foreclosure more than doubled from an average of 455, annually in 2 6 to nearly 94, in the fourth quarter of 7. Meanwhile, the share of loans in foreclosure jumped from less than 1. percent in the fourth quarter of 5 to more than 2. percent by the end of last year, and the share entering foreclosure rose from.4 percent to.9 percent. Subprime loans are largely the culprit. The foreclosure rate on subprime loans soared from 4.5 percent in the fourth quarter of 6 to 8.7 percent a year later. Over the same period, the foreclosure rate for adjustable-rate subprime loans more than doubled from 5.6 percent to 13.4 percent, while that for fixed-rate subprime loans nudged up from 3.2 percent to 3.8 percent. Although the rate for prime loans also increased, it remained under 1. percent. As troubling as the foreclosure crisis is on the national stage, conditions in the economically depressed Midwest are even worse. In the fourth quarter of 7, Ohio had the country s highest foreclosure rate of 3.9 percent equivalent to 1 in 25 loans followed closely by Michigan and Indiana (Table W-9). In other states with high foreclosure rates, the main driver was not a faltering economy but rather high subprime loan shares or sharp price declines following heavy speculation. The State of the Nation s Housing 8

5 Figure 22 Slightly Lower Mortgage Costs Did Little to Ease the Run-Up in Affordability Problems in Many Areas in 7 Change in Monthly Mortgage Costs (7 dollars) 1,4 1, 1, Boston Chicago Miami Los Angeles Notes: Costs are based on a median-priced home purchased with a 1% downpayment and a 3-year fixed-rate mortgage. Prices are adjusted for inflation by the CPI-U for All Items. Sources: National Association of Realtors, Median Sales Price of Existing Single-Family Homes; Federal Housing Finance Board, Fixed Rate Contract Interest Rate for All Homes. For households, the consequences of foreclosures go beyond wiping out equity and even losing the roof over their heads. The implications for their credit scores and long-term financial well-being can be disastrous. For lenders, foreclosures also mean significant losses. In 2, TowerGroup estimated that the foreclosure process for a single property cost $59, and took an average of 18 months. These costs are no doubt higher today in markets where lenders cannot sell the properties for enough to recoup their losses. Moreover, foreclosures impose economic and social costs on the neighborhood and larger community, depriving municipalities of tax revenue and driving down prices of nearby homes. States were among the first to react to the mounting foreclosure crisis. Ohio introduced one of the more sweeping prevention strategies that included partnering with loan servicers to reach out to borrowers at risk, providing counseling, conducting loan workouts, and offering education on how to avoid such situations in the future. Massachusetts, Pennsylvania, and North Carolina have enacted similar programs, while other states have stepped up regulation of lenders and strengthened anti-predatory lending rules. On the federal side, the Treasury Department and the Federal Reserve led efforts to persuade lenders to restructure loans and write down mortgage balances, to eliminate some credit market uncertainty by providing guidance on underwriting standards and enforcement of lending practices, and to recommend regulatory changes that will help prevent a recurrence of today s conditions. The Federal Housing Administration, Fannie Mae, and Freddie Mac have also been tapped to help refinance mortgages. Congress is now looking at legislation to target predatory lending. Finally, community, lender, and government groups have created a handful of programs to help borrowers facing default and interest-rate resets. Modest Affordability Relief Even with widespread price declines, affordability for would-be homeowners has not improved significantly (Figure 22). Assuming a 1-percent downpayment and a 3-year fixed-rate loan, the real monthly mortgage costs for principal and interest on a medianpriced single-family home bought in 7 was only $76 lower, and the downpayment $1, lower, than on a home bought in 6. In 45 of 138 NAR covered metros, real mortgage costs were marginally lower for a house bought in 7 than for one bought in 5. In just 17 metros (primarily in the Midwest), costs were lower last year than in 3 when interest rates were at their bottom. At current interest rates, the national median price would have to fall another 12 percent from the end of 7 to bring the monthly payments on a newly purchased median-priced home to 3 levels. In 4 metros, prices would have to drop by more than 25 percent. Even if interest rates were to come down by a full percentage point, the national median home price would still have to decline by 2 percent and by more than 25 percent in 18 metro areas to reduce mortgage costs to 3 levels. Of course, only first-time buyers still able to qualify for a loan can take full advantage of the improved affordability brought on by lower house prices. Most repeat buyers must sell their homes at discounts similar to those on the homes that they buy. The Outlook With subprime mortgage troubles hanging over the market, the near-term outlook for homeownership is grim. Late in 7, First American CoreLogic estimated that interest rates on $314 billion of subprime debt would reset this year. Fortunately, fully indexed rates on one-year adjustable loans have fallen by 3. percentage points since early 7, which may spare some borrowers with resets from default. In addition, the federal government is working on a range of initiatives to blunt the impact of subprime interestrate resets. The wave of foreclosures will take months to process and the number of homes entering foreclosure could continue to rise even if the volume of loans with resets drops from last year s level. Job losses and falling home prices are now adding to foreclosure risks. Meanwhile, mortgage credit will remain tight and larger risk premiums will offset much of the decline in short-term rates. While changes in the age and family composition of US households favor homeownership over the next five to ten years, market conditions will overwhelm any positive lift from these demographic drivers at least in the short term. How long homebuying will take to recover from the bust remains uncertain. Joint Center for Housing Studies of Harvard University 21

Homeownership. The State of the Nation s Housing 2009

Homeownership Entering 9, foreclosures were at a record high, price declines were keeping many would-be buyers on the sidelines, and tighter underwriting standards were preventing many of those ready to

Homeownership Entering 9, foreclosures were at a record high, price declines were keeping many would-be buyers on the sidelines, and tighter underwriting standards were preventing many of those ready to

The state of the nation s Housing 2013

The state of the nation s Housing 2013 Fact Sheet PURPOSE The State of the Nation s Housing report has been released annually by Harvard University s Joint Center for Housing Studies since 1988. Now in

The state of the nation s Housing 2013 Fact Sheet PURPOSE The State of the Nation s Housing report has been released annually by Harvard University s Joint Center for Housing Studies since 1988. Now in

HOMEOWNERSHIP. Low interest rates, stronger job growth, and. rapid house price appreciation all helped to. sustain the homeownership boom through its

HOMEOWNERSHIP Low interest rates, stronger job growth, and rapid house price appreciation all helped to sustain the homeownership boom through its 12th year. With well over one million owners added in

HOMEOWNERSHIP Low interest rates, stronger job growth, and rapid house price appreciation all helped to sustain the homeownership boom through its 12th year. With well over one million owners added in

Executive Summary. Joint Center for Housing Studies of Harvard University 1

1 Executive Summary Despite unprecedented federal efforts to jumpstart the economy and help homeowners keep up with their mortgage payments, home prices continued to fall and foreclosures continued to

1 Executive Summary Despite unprecedented federal efforts to jumpstart the economy and help homeowners keep up with their mortgage payments, home prices continued to fall and foreclosures continued to

(Table A-2). Again, this is the first time in recorded history. Plumbing the Depths. Promising Signs. The State of the Nation s Housing 2010

. Again, this is the first time in recorded history. Plumbing the Depths. Promising Signs. The State of the Nation s Housing 2010") 2 Housing Markets Housing markets showed some signs of recovery in 29. The question now is whether the large overhang of vacant units combined with high unemployment and record foreclosures will allow

2 Housing Markets Housing markets showed some signs of recovery in 29. The question now is whether the large overhang of vacant units combined with high unemployment and record foreclosures will allow

Weakness in the U.S. Housing Market Likely to Persist in 2008

Weakness in the U.S. Housing Market Likely to Persist in 2008 Commentary by Sondra Albert, Chief Economist AFL-CIO Housing Investment Trust January 29, 2008 The national housing market entered 2008 mired

Weakness in the U.S. Housing Market Likely to Persist in 2008 Commentary by Sondra Albert, Chief Economist AFL-CIO Housing Investment Trust January 29, 2008 The national housing market entered 2008 mired

Demographic Drivers. Joint Center for Housing Studies of Harvard University 11

3 Demographic Drivers Household formations were already on the decline when the recession started to hit in December 27. Annual net additions fell from 1.37 million in the first half of the decade to only

3 Demographic Drivers Household formations were already on the decline when the recession started to hit in December 27. Annual net additions fell from 1.37 million in the first half of the decade to only

SINGLE-FAMILY SLOWDOWN

1 Executive Summary With promising increases in home construction, sales, and prices, the housing market gained steam in early 13. But when interest rates notched up at mid-year, momentum slowed. This

1 Executive Summary With promising increases in home construction, sales, and prices, the housing market gained steam in early 13. But when interest rates notched up at mid-year, momentum slowed. This

GRIM CONSTRUCTION AND SALES REPORTS

2 Housing Markets Despite the most favorable mortgage rates in decades and two rounds of homebuyer tax credits, major housing market indicators stood at or near record lows in 2010. Construction was particularly

2 Housing Markets Despite the most favorable mortgage rates in decades and two rounds of homebuyer tax credits, major housing market indicators stood at or near record lows in 2010. Construction was particularly

Don t Raise the Federal Debt Ceiling, Torpedo the U.S. Housing Market

Don t Raise the Federal Debt Ceiling, Torpedo the U.S. Housing Market Failure to Act Would Have Serious Consequences for Housing Just as the Market Is Showing Signs of Recovery Christian E. Weller May

Don t Raise the Federal Debt Ceiling, Torpedo the U.S. Housing Market Failure to Act Would Have Serious Consequences for Housing Just as the Market Is Showing Signs of Recovery Christian E. Weller May

SLUGGISH HOUSEHOLD GROWTH

3 Demographic Drivers Household growth has yet to rebound fully as the weak economic recovery continues to prevent many young adults from living independently. As the economy strengthens, though, millions

3 Demographic Drivers Household growth has yet to rebound fully as the weak economic recovery continues to prevent many young adults from living independently. As the economy strengthens, though, millions

INTRODUCTION AND SUMMARY

1 INTRODUCTION AND SUMMARY Rising house prices and incomes, an aging housing stock, and a pickup in household growth are all contributing to today s strong home improvement market. Demand is robust in

1 INTRODUCTION AND SUMMARY Rising house prices and incomes, an aging housing stock, and a pickup in household growth are all contributing to today s strong home improvement market. Demand is robust in

National Housing Market Summary

1st 2017 June 2017 HUD PD&R National Housing Market Summary The Housing Market Recovery Showed Progress in the First The housing market improved in the first quarter of 2017. Construction starts rose for

1st 2017 June 2017 HUD PD&R National Housing Market Summary The Housing Market Recovery Showed Progress in the First The housing market improved in the first quarter of 2017. Construction starts rose for

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners November 2012 U.S. Department U.S Department of Housing of Housing and Urban and Urban Development Development

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners November 2012 U.S. Department U.S Department of Housing of Housing and Urban and Urban Development Development

From a National Housing Boom to Bust

After a period of sharply declining house prices and a very slow pace of new construction at the end of the past decade, U.S. housing activity has begun to recover. Americans, who endured an unprecedented

After a period of sharply declining house prices and a very slow pace of new construction at the end of the past decade, U.S. housing activity has begun to recover. Americans, who endured an unprecedented

The Office of Economic Policy HOUSING DASHBOARD. March 16, 2016

The Office of Economic Policy HOUSING DASHBOARD March 16, 216 Recent housing market indicators suggest that housing activity continues to strengthen. Solid residential investment in 215Q4 contributed.3

The Office of Economic Policy HOUSING DASHBOARD March 16, 216 Recent housing market indicators suggest that housing activity continues to strengthen. Solid residential investment in 215Q4 contributed.3

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners February 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners February 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research

THE HOUSING MARKET REVIVAL

1 Executive Summary The long-awaited housing recovery finally took hold in 2012, heralded by rising home prices and further rental market tightening. While still at historically low levels, housing construction

1 Executive Summary The long-awaited housing recovery finally took hold in 2012, heralded by rising home prices and further rental market tightening. While still at historically low levels, housing construction

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners April 2012 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners April 2012 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

Special Report. March 10, ,600 1,400 1,200

March 1, 1 HIGHLIGHTS After nearly three years of decline, the U.S housing market showed considerable signs of improvement in 9. In particular, a rise in home sales helped to pull down housing inventories

March 1, 1 HIGHLIGHTS After nearly three years of decline, the U.S housing market showed considerable signs of improvement in 9. In particular, a rise in home sales helped to pull down housing inventories

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners May 2011 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners May 2011 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

Hearing on The Housing Decline: The Extent of the Problem and Potential Remedies December 13, 2007

Statement of Michael Decker Senior Managing Director, Research and Public Policy Before the Committee on Finance United States Senate Hearing on The Housing Decline: The Extent of the Problem and Potential

Statement of Michael Decker Senior Managing Director, Research and Public Policy Before the Committee on Finance United States Senate Hearing on The Housing Decline: The Extent of the Problem and Potential

NAR Research on the Impact of Jumbo Mortgage Credit Crunch

NAR Research on the Impact of Jumbo Mortgage Credit Crunch Introduction Mortgage rates are at 50 year lows, thereby raising housing affordability conditions to all-time high levels. However, the historically

NAR Research on the Impact of Jumbo Mortgage Credit Crunch Introduction Mortgage rates are at 50 year lows, thereby raising housing affordability conditions to all-time high levels. However, the historically

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners August 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research U.S

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners August 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research U.S

A Divided Real Estate Nation

Real Estate Reality Check Explanation of "What Happened" from the 26 Leadership Conference Boom ended August 2 Mortgage rates rose almost one point Affordability conditions deteriorated Speculative investors

Real Estate Reality Check Explanation of "What Happened" from the 26 Leadership Conference Boom ended August 2 Mortgage rates rose almost one point Affordability conditions deteriorated Speculative investors

Federal National Mortgage Association

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 10-Q QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 n For the quarterly period ended

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 10-Q QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 n For the quarterly period ended

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2010

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2010 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2010 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

Ben S Bernanke: Reducing preventable mortgage foreclosures

Ben S Bernanke: Reducing preventable mortgage foreclosures Speech of Mr Ben S Bernanke, Chairman of the Board of Governors of the US Federal Reserve System, at the Independent Community Bankers of America

Ben S Bernanke: Reducing preventable mortgage foreclosures Speech of Mr Ben S Bernanke, Chairman of the Board of Governors of the US Federal Reserve System, at the Independent Community Bankers of America

TRENDS IN DELINQUENCIES AND FORECLOSURES IN SOUTHERN CALIFORNIA

TRENDS IN DELINQUENCIES AND FORECLOSURES IN SOUTHERN CALIFORNIA April 2009 Melody Nava, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising

TRENDS IN DELINQUENCIES AND FORECLOSURES IN SOUTHERN CALIFORNIA April 2009 Melody Nava, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising

Housing Recovery is Underway, But Not for Everyone

Housing Recovery is Underway, But Not for Everyone Eric Belsky August 2013 Dallas, TX Housing Markets Have Corrected In Significant Ways Both price and quantity reductions have occurred Even after price

Housing Recovery is Underway, But Not for Everyone Eric Belsky August 2013 Dallas, TX Housing Markets Have Corrected In Significant Ways Both price and quantity reductions have occurred Even after price

S&P/Case Shiller index

S&P/Case Shiller index Home price index Index Jan. 2000=100, 3 month ending 240 220 200 180 160 10-metro composite 140 20-metro composite 120 100 80 2000 2001 2002 2003 2004 Sources: Standard & Poor's

S&P/Case Shiller index Home price index Index Jan. 2000=100, 3 month ending 240 220 200 180 160 10-metro composite 140 20-metro composite 120 100 80 2000 2001 2002 2003 2004 Sources: Standard & Poor's

Florida: An Economic Overview

Florida: An Economic Overview August 21, 2013 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Global

Florida: An Economic Overview August 21, 2013 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Global

Update on Homeownership Wealth Trajectories Through the Housing Boom and Bust

The Harvard Joint Center for Housing Studies advances understanding of housing issues and informs policy through research, education, and public outreach. Working Paper, February 2016 Update on Homeownership

The Harvard Joint Center for Housing Studies advances understanding of housing issues and informs policy through research, education, and public outreach. Working Paper, February 2016 Update on Homeownership

Chicago-Naperville-Joliet Area Local Market Report, Third Quarter Median Price (Red Line) and One-year Price Growth. Chicago

and One-year Price Growth. Chicago") -Naperville-Joliet Area Local Market Report, Third Quarter 2010 Today's Market Median Price (Red Line) and One-year Price Growth $350,000 $300,000 $250,000 $200,000 $150,000 $100,000 $50,000 $0 7-year

-Naperville-Joliet Area Local Market Report, Third Quarter 2010 Today's Market Median Price (Red Line) and One-year Price Growth $350,000 $300,000 $250,000 $200,000 $150,000 $100,000 $50,000 $0 7-year

The Mortgage and Housing Market Outlook

The Mortgage and Housing Market Outlook National Economists Club Washington, DC March 27, 2008 Frank E. Nothaft Chief Economist Recession Risk, Housing Contraction Worsen 1-in-2 chance of recession in

The Mortgage and Housing Market Outlook National Economists Club Washington, DC March 27, 2008 Frank E. Nothaft Chief Economist Recession Risk, Housing Contraction Worsen 1-in-2 chance of recession in

Florida: An Economic Overview

Florida: An Economic Overview June 19, 2013 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Global

Florida: An Economic Overview June 19, 2013 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Global

Managing Your Money: "Housing and Public Policy the Bubble, Present, and Future

Managing Your Money: "Housing and Public Policy the Bubble, Present, and Future PLATO (Participatory Learning and Teaching Organization) J. Michael Collins UW Madison Center for Financial Security Overview

Managing Your Money: "Housing and Public Policy the Bubble, Present, and Future PLATO (Participatory Learning and Teaching Organization) J. Michael Collins UW Madison Center for Financial Security Overview

Why is the Country Facing a Financial Crisis?

Why is the Country Facing a Financial Crisis? Prepared by: Julie L. Stackhouse Senior Vice President Federal Reserve Bank of St. Louis November 3, 2008 The views expressed in this presentation are the

Why is the Country Facing a Financial Crisis? Prepared by: Julie L. Stackhouse Senior Vice President Federal Reserve Bank of St. Louis November 3, 2008 The views expressed in this presentation are the

Mortgage Delinquencies and Foreclosures: Hawaii

Mortgage Delinquencies and Foreclosures: Hawaii Presentation prepared by Carolina Reid, Ph.D. Community Development Department Federal Reserve Bank of San Francisco July 21, 2008 Analysis of First American

Mortgage Delinquencies and Foreclosures: Hawaii Presentation prepared by Carolina Reid, Ph.D. Community Development Department Federal Reserve Bank of San Francisco July 21, 2008 Analysis of First American

WHAT THE REALLY HAPPENED...

WHAT THE F#@K REALLY HAPPENED... THE ECONOMIC CRISIS OF 08 EDMOND GRADY A BANKER IS A FELLOW WHO LENDS YOU HIS UMBRELLA WHEN THE SUN IS SHINING, BUT WANTS IT BACK THE MINUTE IT BEGINS TO RAIN. MARK TWAIN

WHAT THE F#@K REALLY HAPPENED... THE ECONOMIC CRISIS OF 08 EDMOND GRADY A BANKER IS A FELLOW WHO LENDS YOU HIS UMBRELLA WHEN THE SUN IS SHINING, BUT WANTS IT BACK THE MINUTE IT BEGINS TO RAIN. MARK TWAIN

Randall S Kroszner: Loan modifications and foreclosure prevention

Randall S Kroszner: Loan modifications and foreclosure prevention Testimony by Mr Randall S Kroszner, Member of the Board of Governors of the US Federal Reserve System, before the Committee on Financial

Randall S Kroszner: Loan modifications and foreclosure prevention Testimony by Mr Randall S Kroszner, Member of the Board of Governors of the US Federal Reserve System, before the Committee on Financial

Testimony of SIFMA before the House Judiciary Subcommittee on Commercial and Administrative Law

Testimony of SIFMA before the House Judiciary Subcommittee on Commercial and Administrative Law Hearing on Straightening Out the Mortgage Mess: How Can we Protect Home Ownership and Provide Relief to Consumers

Testimony of SIFMA before the House Judiciary Subcommittee on Commercial and Administrative Law Hearing on Straightening Out the Mortgage Mess: How Can we Protect Home Ownership and Provide Relief to Consumers

TRENDS IN DELINQUENCIES AND FORECLOSURES IN IDAHO

TRENDS IN DELINQUENCIES AND FORECLOSURES IN IDAHO February 2009 Craig Nolte, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising foreclosures

TRENDS IN DELINQUENCIES AND FORECLOSURES IN IDAHO February 2009 Craig Nolte, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising foreclosures

Remarks on the Housing Market and Subprime Lending. Remarks. Ben S. Bernanke. Chairman. (via satellite) to the International Monetary Conference

to the International Monetary Conference") For release on delivery 8:15 a.m. EDT (2:15 p.m. local time) June 5, 2007 Remarks on the Housing Market and Subprime Lending Remarks By Ben S. Bernanke Chairman Board of Governors ofthe Federal Reserve

For release on delivery 8:15 a.m. EDT (2:15 p.m. local time) June 5, 2007 Remarks on the Housing Market and Subprime Lending Remarks By Ben S. Bernanke Chairman Board of Governors ofthe Federal Reserve

Grand Rapids Area Local Market Report, Fourth Quarter Median Price (Red Line) and One-year Price Growth 20% $140,000 $120,000 $100,000

and One-year Price Growth 20% $140,000 $120,000 $100,000") Area Local Market Report, Fourth Quarter Today's Market $160,000 Median Price (Red Line) and One-year Price Growth 20 $140,000 $120,000 $100,000 10 0 $80,000-10 $60,000 $40,000 $20,000-20 -30 $0 2000 2002

Area Local Market Report, Fourth Quarter Today's Market $160,000 Median Price (Red Line) and One-year Price Growth 20 $140,000 $120,000 $100,000 10 0 $80,000-10 $60,000 $40,000 $20,000-20 -30 $0 2000 2002

TRENDS IN DELINQUENCIES AND FORECLOSURES IN CALIFORNIA

TRENDS IN DELINQUENCIES AND FORECLOSURES IN CALIFORNIA April 2009 Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising foreclosures House

TRENDS IN DELINQUENCIES AND FORECLOSURES IN CALIFORNIA April 2009 Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising foreclosures House

Housing & Mortgage Market Outlook

Housing & Mortgage Market Outlook 2005 Economic Outlook Symposium Federal Reserve Bank of Chicago December 2005 David W. Berson Vice President & Chief Economist What You Want to Know: We expect economic

Housing & Mortgage Market Outlook 2005 Economic Outlook Symposium Federal Reserve Bank of Chicago December 2005 David W. Berson Vice President & Chief Economist What You Want to Know: We expect economic

Credit Crisis: The Sky is not Falling

Credit Crisis: The Sky is not Falling U.S. stock markets are gyrating on news of an apparent credit crunch generated by defaults among subprime home mortgage loans. Such frenzy has spurred Wall Street

Credit Crisis: The Sky is not Falling U.S. stock markets are gyrating on news of an apparent credit crunch generated by defaults among subprime home mortgage loans. Such frenzy has spurred Wall Street

Citi U.S. Consumer Mortgage Lending Data and Servicing Foreclosure Prevention Efforts

Citi U.S. Consumer Mortgage Lending Data and Servicing Foreclosure Prevention Efforts Third Quarter 29 EXECUTIVE SUMMARY In February 28, we published our initial data report on Citi s U.S. mortgage lending

Citi U.S. Consumer Mortgage Lending Data and Servicing Foreclosure Prevention Efforts Third Quarter 29 EXECUTIVE SUMMARY In February 28, we published our initial data report on Citi s U.S. mortgage lending

The US Housing Market Crisis and Its Aftermath

The US Housing Market Crisis and Its Aftermath Asian Development Bank November 16, 2009 Table of Contents Section I II III IV V US Economy and the Housing Market Freddie Mac Overview Business Activities

The US Housing Market Crisis and Its Aftermath Asian Development Bank November 16, 2009 Table of Contents Section I II III IV V US Economy and the Housing Market Freddie Mac Overview Business Activities

Housing & Mortgage Outlook. Frank Nothaft Chief Economist May 22, 2018

Housing & Mortgage Outlook Frank Nothaft Chief Economist May 22, 2018 Economic & Housing Outlook Effect of higher mortgage rates Inventory-for-sale remains low Less refinance, more purchase & home-improvement

Housing & Mortgage Outlook Frank Nothaft Chief Economist May 22, 2018 Economic & Housing Outlook Effect of higher mortgage rates Inventory-for-sale remains low Less refinance, more purchase & home-improvement

Florida: An Economic Overview

Florida: An Economic Overview May 1, 2012 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Mixed Economy Turned

Florida: An Economic Overview May 1, 2012 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Mixed Economy Turned

Joint Center for Housing Studies of Harvard University NATION S

Joint Center for Housing Studies of Harvard University THE STA TE OF THE NATION S HOUSING 28 Joint Center for Housing Studies of Harvard University Graduate School of Design Harvard Kennedy School Principal

Joint Center for Housing Studies of Harvard University THE STA TE OF THE NATION S HOUSING 28 Joint Center for Housing Studies of Harvard University Graduate School of Design Harvard Kennedy School Principal

The Mortgage Industry

Financing Residential Real Estate Lesson 4: The Mortgage Industry Introduction In this lesson, we will cover: steps in the residential mortgage process; participants in the process, including loan originators

Financing Residential Real Estate Lesson 4: The Mortgage Industry Introduction In this lesson, we will cover: steps in the residential mortgage process; participants in the process, including loan originators

DEMOGRAPHIC DRIVERS. Household growth is picking up pace. With more. than a million young foreign-born adults arriving

DEMOGRAPHIC DRIVERS Household growth is picking up pace. With more than a million young foreign-born adults arriving each year, household formations in the next decade will outnumber those in the last

DEMOGRAPHIC DRIVERS Household growth is picking up pace. With more than a million young foreign-born adults arriving each year, household formations in the next decade will outnumber those in the last

Housing, Exports, and North Carolina s Economy

Economics Bulletin number 1 august 2008 Housing, Exports, and North Carolina s Economy Karl W. Smith Introduction From 2000 to 2006, the average value of a home in the United States rose by 89 percent.

Economics Bulletin number 1 august 2008 Housing, Exports, and North Carolina s Economy Karl W. Smith Introduction From 2000 to 2006, the average value of a home in the United States rose by 89 percent.

A Look Behind the Numbers: Subprime Loan Report for Youngstown

Page1 A Look Behind the Numbers is a publication of the Federal Reserve Bank of Cleveland s Community Development group. Through data analysis, these reports examine issues relating to access to credit

Page1 A Look Behind the Numbers is a publication of the Federal Reserve Bank of Cleveland s Community Development group. Through data analysis, these reports examine issues relating to access to credit

After housing s best year in a decade, what s next?

DECEMBER 2016 After housing s best year in a decade, what s next? The year is drawing to a close and it is time to take stock of where housing and mortgage markets have been and where they likely are headed.

DECEMBER 2016 After housing s best year in a decade, what s next? The year is drawing to a close and it is time to take stock of where housing and mortgage markets have been and where they likely are headed.

Randall S Kroszner: Legislative proposals on reforming mortgage practices

Randall S Kroszner: Legislative proposals on reforming mortgage practices Testimony by Mr Randall S Kroszner, Member of the Board of Governors of the US Federal Reserve System, before the Committee on

Randall S Kroszner: Legislative proposals on reforming mortgage practices Testimony by Mr Randall S Kroszner, Member of the Board of Governors of the US Federal Reserve System, before the Committee on

The State of the Nation s Housing Report 2017

The State of the Nation s Housing Report 217 Tennessee Governor s Housing Conference Nashville, Tennessee September 2, 217 The Report s Major Themes National home prices have regained their previous peak,

The State of the Nation s Housing Report 217 Tennessee Governor s Housing Conference Nashville, Tennessee September 2, 217 The Report s Major Themes National home prices have regained their previous peak,

Real gross domestic product

Real gross domestic product United States Compound annual growth rate 10 5 0-5 -10 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 Sources: Bureau of Economic Analysis, IHS Global Insight. Employment by sector

Real gross domestic product United States Compound annual growth rate 10 5 0-5 -10 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 Sources: Bureau of Economic Analysis, IHS Global Insight. Employment by sector

2017 MORTGAGE MARKET OUTLOOK: EXECUTIVE ECONOMIC REPORT JANUARY 2017

2017 MORTGAGE MARKET OUTLOOK: EXECUTIVE ECONOMIC REPORT JANUARY 2017 1 2017 FORECAST OVERVIEW For the 2017 housing market, the outlook is generally positive. The long recovery from the elevated delinquency

2017 MORTGAGE MARKET OUTLOOK: EXECUTIVE ECONOMIC REPORT JANUARY 2017 1 2017 FORECAST OVERVIEW For the 2017 housing market, the outlook is generally positive. The long recovery from the elevated delinquency

How Affordability Affects Housing s Spring Season

MARCH 2017 How Affordability Affects Housing s Spring Season Recent indications of stronger growth convinced the Federal Reserve to raise the Federal funds rate this month and to signal further increases

MARCH 2017 How Affordability Affects Housing s Spring Season Recent indications of stronger growth convinced the Federal Reserve to raise the Federal funds rate this month and to signal further increases

Homeowner Affordability and Stability Plan Fact Sheet

Homeowner Affordability and Stability Plan Fact Sheet The deep contraction in the economy and in the housing market has created devastating consequences for homeowners and communities throughout the country.

Homeowner Affordability and Stability Plan Fact Sheet The deep contraction in the economy and in the housing market has created devastating consequences for homeowners and communities throughout the country.

FILED: NEW YORK COUNTY CLERK 12/21/2013 INDEX NO /2013 NYSCEF DOC. NO. 30 RECEIVED NYSCEF: 12/21/2013. Exhibit 22

FILED: NEW YORK COUNTY CLERK 12/21/2013 INDEX NO. 653335/2013 NYSCEF DOC. NO. 30 RECEIVED NYSCEF: 12/21/2013 Exhibit 22 Page1 1of1DOCUMENT Copyright 2006 Factiva, from Dow Jones All Rights Reserved (Copyright(c)

FILED: NEW YORK COUNTY CLERK 12/21/2013 INDEX NO. 653335/2013 NYSCEF DOC. NO. 30 RECEIVED NYSCEF: 12/21/2013 Exhibit 22 Page1 1of1DOCUMENT Copyright 2006 Factiva, from Dow Jones All Rights Reserved (Copyright(c)

Out of the Shadows: Projected Levels for Future REO Inventory

ECONOMIC COMMENTARY Number 2010-14 October 19, 2010 Out of the Shadows: Projected Levels for Future REO Inventory Guhan Venkatu Nearly one homeowner in ten is more than 90 days delinquent on his mortgage

ECONOMIC COMMENTARY Number 2010-14 October 19, 2010 Out of the Shadows: Projected Levels for Future REO Inventory Guhan Venkatu Nearly one homeowner in ten is more than 90 days delinquent on his mortgage

Group 14 Dallas Hall, Chuck Dobson, Guy Tahye, Tunde Olabiyi

In order to understand how we have gotten to the point where government intervention is needed to save our financial markets, it is necessary to look back and examine the many causes that lead to this

In order to understand how we have gotten to the point where government intervention is needed to save our financial markets, it is necessary to look back and examine the many causes that lead to this

Ben S Bernanke: The subprime mortgage market

Ben S Bernanke: The subprime mortgage market Remarks by Mr Ben S Bernanke, Chairman of the Board of Governors of the US Federal Reserve System, at the Federal Reserve Bank of Chicago s 43rd Annual Conference

Ben S Bernanke: The subprime mortgage market Remarks by Mr Ben S Bernanke, Chairman of the Board of Governors of the US Federal Reserve System, at the Federal Reserve Bank of Chicago s 43rd Annual Conference

b. Financial innovation and/or financial liberalization (the elimination of restrictions on financial markets) can cause financial firms to go on a

can cause financial firms to go on a") Financial Crises This lecture begins by examining the features of a financial crisis. It then describes the causes and consequences of the 2008 financial crisis and the resulting changes in financial regulations.

Financial Crises This lecture begins by examining the features of a financial crisis. It then describes the causes and consequences of the 2008 financial crisis and the resulting changes in financial regulations.

A Look Behind the Numbers: FHA Lending in Ohio

Page1 Recent news articles have carried the worrisome suggestion that Federal Housing Administration (FHA)-insured loans may be the next subprime. Given the high correlation between subprime lending and

Page1 Recent news articles have carried the worrisome suggestion that Federal Housing Administration (FHA)-insured loans may be the next subprime. Given the high correlation between subprime lending and

Florida: An Economic Overview

Florida: An Economic Overview May 14, 2014 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Economy

Florida: An Economic Overview May 14, 2014 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Economy

How We're Doing: What s Blocking the Recovery

How We're Doing: What s Blocking the Recovery Karen Dynan, Vice President and Co-Director, Economic Studies Ted Gayer, Co-Director, Economic Studies Alan Berube, Senior Fellow and Research Director, Metropolitan

How We're Doing: What s Blocking the Recovery Karen Dynan, Vice President and Co-Director, Economic Studies Ted Gayer, Co-Director, Economic Studies Alan Berube, Senior Fellow and Research Director, Metropolitan

The Joint center for Housing Studies of Harvard University THE STATE OF THE

The Joint center for Housing Studies of Harvard University THE STATE OF THE Nation s Housing 21 Joint Center for Housing Studies of Harvard University Graduate School of Design Harvard Kennedy School Principal

The Joint center for Housing Studies of Harvard University THE STATE OF THE Nation s Housing 21 Joint Center for Housing Studies of Harvard University Graduate School of Design Harvard Kennedy School Principal

Joseph S Tracy: A strategy for the 2011 economic recovery

Joseph S Tracy: A strategy for the 2011 economic recovery Remarks by Mr Joseph S Tracy, Executive Vice President of the Federal Reserve Bank of New York, at Dominican College, Orangeburg, New York, 28

Joseph S Tracy: A strategy for the 2011 economic recovery Remarks by Mr Joseph S Tracy, Executive Vice President of the Federal Reserve Bank of New York, at Dominican College, Orangeburg, New York, 28

TRENDS IN DELINQUENCIES AND FORECLOSURES IN

TRENDS IN DELINQUENCIES AND FORECLOSURES IN ARIZONA April 2009 Jan Bontrager, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising foreclosures

TRENDS IN DELINQUENCIES AND FORECLOSURES IN ARIZONA April 2009 Jan Bontrager, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising foreclosures

SPECIAL REPORT. TD Economics CONDITIONS ARE RIPE FOR AMERICAN CONSUMERS TO LEAD ECONOMIC GROWTH

SPECIAL REPORT TD Economics CONDITIONS ARE RIPE FOR AMERICAN CONSUMERS TO LEAD ECONOMIC GROWTH Highlights American consumers have has had a rough go of things over the past several years. After plummeting

SPECIAL REPORT TD Economics CONDITIONS ARE RIPE FOR AMERICAN CONSUMERS TO LEAD ECONOMIC GROWTH Highlights American consumers have has had a rough go of things over the past several years. After plummeting

TRENDS IN DELINQUENCIES AND FORECLOSURES IN

TRENDS IN DELINQUENCIES AND FORECLOSURES IN IDAHO April 2009 Craig Nolte, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising foreclosures

TRENDS IN DELINQUENCIES AND FORECLOSURES IN IDAHO April 2009 Craig Nolte, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising foreclosures

Florida: An Economic Overview

Florida: An Economic Overview March 24, 2013 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Global

Florida: An Economic Overview March 24, 2013 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Global

MORTGAGE MARKETS AND THE ENTERPRISES IN July 2008

MORTGAGE MARKETS AND THE ENTERPRISES IN 2007 July 2008 Preface This Office of Federal Housing Enterprise Oversight (OFHEO) research paper reviews developments in the housing sector and the primary and

MORTGAGE MARKETS AND THE ENTERPRISES IN 2007 July 2008 Preface This Office of Federal Housing Enterprise Oversight (OFHEO) research paper reviews developments in the housing sector and the primary and

e-brief Not Here? Housing Market Policy and the Risk of a Housing Bust

e-brief August 31, 2010 FINANCIAL SERVICES Not Here? Housing Market Policy and the Risk of a Housing Bust By Jim MacGee Can a US-style housing bust happen in Canada? Recent swings in Canadian house prices

e-brief August 31, 2010 FINANCIAL SERVICES Not Here? Housing Market Policy and the Risk of a Housing Bust By Jim MacGee Can a US-style housing bust happen in Canada? Recent swings in Canadian house prices

Conventional Financing

Financing Residential Real Estate Lesson 10: Conventional Financing Introduction In this lesson we will cover: conforming and nonconforming loans, characteristics of conventional loans, qualifying standards

Financing Residential Real Estate Lesson 10: Conventional Financing Introduction In this lesson we will cover: conforming and nonconforming loans, characteristics of conventional loans, qualifying standards

AUGUST MORTGAGE INSURANCE DATA AT A GLANCE

AUGUST MORTGAGE INSURANCE DATA AT A GLANCE CONTENTS 4 OVERVIEW 32 PRITE-LABEL SECURITIES Mortgage Insurance Market Composition 6 AGENCY MORTGAGE MARKET Defaults : 90+ Days Delinquent Loss Severity GSE

AUGUST MORTGAGE INSURANCE DATA AT A GLANCE CONTENTS 4 OVERVIEW 32 PRITE-LABEL SECURITIES Mortgage Insurance Market Composition 6 AGENCY MORTGAGE MARKET Defaults : 90+ Days Delinquent Loss Severity GSE

Testimony of Dr. Michael J. Lea Director The Corky McMillin Center for Real Estate San Diego State University

Testimony of Dr. Michael J. Lea Director The Corky McMillin Center for Real Estate San Diego State University To the Senate Banking, Housing and Urban Affairs Subcommittee on Security and International

Testimony of Dr. Michael J. Lea Director The Corky McMillin Center for Real Estate San Diego State University To the Senate Banking, Housing and Urban Affairs Subcommittee on Security and International

JOINT CENTER FOR HOUSING STUDIES OF HARVARD UNIVERSITY THE STATE OF THE NATION S HOUSING

JOINT CENTER FOR HOUSING STUDIES OF HARVARD UNIVERSITY THE STATE OF THE NATION S HOUSING 2011 JOINT CENTER FOR HOUSING STUDIES OF HARVARD UNIVERSITY GRADUATE SCHOOL OF DESIGN JOHN F. KENNEDY SCHOOL OF

JOINT CENTER FOR HOUSING STUDIES OF HARVARD UNIVERSITY THE STATE OF THE NATION S HOUSING 2011 JOINT CENTER FOR HOUSING STUDIES OF HARVARD UNIVERSITY GRADUATE SCHOOL OF DESIGN JOHN F. KENNEDY SCHOOL OF

Future Housing Secondary Market Entities, Their Affordable Housing Responsibility, and the State HFA Opportunity

Future Housing Secondary Market Entities, Their Affordable Housing Responsibility, and the State HFA Opportunity The National Council of State Housing Agencies (NCSHA) and the state Housing Finance Agencies

Future Housing Secondary Market Entities, Their Affordable Housing Responsibility, and the State HFA Opportunity The National Council of State Housing Agencies (NCSHA) and the state Housing Finance Agencies

Florida: An Economic Overview

Florida: An Economic Overview March 31, 2014 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Economy

Florida: An Economic Overview March 31, 2014 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Economy

Ivan Gjaja (212) Natalia Nekipelova (212)

Natalia Nekipelova (212)") Ivan Gjaja (212) 816-8320 ivan.m.gjaja@ssmb.com Natalia Nekipelova (212) 816-8075 natalia.nekipelova@ssmb.com In a departure from seasonal patterns, January speeds were 1% CPR higher than December speeds.

Ivan Gjaja (212) 816-8320 ivan.m.gjaja@ssmb.com Natalia Nekipelova (212) 816-8075 natalia.nekipelova@ssmb.com In a departure from seasonal patterns, January speeds were 1% CPR higher than December speeds.

Perspectives on the U.S. Economy

Perspectives on the U.S. Economy Presentation for Irish Institute Seminar, April 14, 2008 Bob Murphy Department of Economics Boston College Three Perspectives 1. Historical Overview of U.S. Economic Performance

Perspectives on the U.S. Economy Presentation for Irish Institute Seminar, April 14, 2008 Bob Murphy Department of Economics Boston College Three Perspectives 1. Historical Overview of U.S. Economic Performance

Comments on Forecasts

Comments on Forecasts Kenneth T. Rosen The Sky s The Limit Conference and Expo November 3, 2017 Risks to Economic Outlook Tax cuts in a full employment economy and a global synchronized expansion leads

Comments on Forecasts Kenneth T. Rosen The Sky s The Limit Conference and Expo November 3, 2017 Risks to Economic Outlook Tax cuts in a full employment economy and a global synchronized expansion leads

Testimony of Angelo Mozilo. Before the Committee on Oversight and Government Reform. March 7, 2008

Testimony of Angelo Mozilo Before the Committee on Oversight and Government Reform March 7, 2008 Good morning Chairman Waxman, Ranking Member Davis, and Members of the Committee. My name is Angelo Mozilo,

Testimony of Angelo Mozilo Before the Committee on Oversight and Government Reform March 7, 2008 Good morning Chairman Waxman, Ranking Member Davis, and Members of the Committee. My name is Angelo Mozilo,

Discussion: The Mortgage Meltdown Implications for Credit Availability. Eric S. Rosengren, President and CEO, Federal Reserve Bank of Boston

Discussion: The Mortgage Meltdown Implications for Credit Availability Eric S. Rosengren, President and CEO, Federal Reserve Bank of Boston U.S. Monetary Policy Forum, February 29, 2008 I am very pleased

Discussion: The Mortgage Meltdown Implications for Credit Availability Eric S. Rosengren, President and CEO, Federal Reserve Bank of Boston U.S. Monetary Policy Forum, February 29, 2008 I am very pleased

Mortgage REITs. March 20, Calvin Schnure Senior Vice President, Research & Economic Analysis

Mortgage REITs March 20, 2018 Calvin Schnure Senior Vice President, Research & Economic Analysis cschnure@nareit.com, 202-739-9434 Executive Summary Mortgage REITs (mreits) are companies that finance residential

Mortgage REITs March 20, 2018 Calvin Schnure Senior Vice President, Research & Economic Analysis cschnure@nareit.com, 202-739-9434 Executive Summary Mortgage REITs (mreits) are companies that finance residential

The Equifax Economic and Credit Markets Outlook

The Equifax Economic and Credit Markets Outlook A CUNA Roundtable Amy Crews Cutts SVP- Chief Economist, Equifax May 15, 2014 Comments on the Economic Outlook General forecast is that economic growth accelerates

The Equifax Economic and Credit Markets Outlook A CUNA Roundtable Amy Crews Cutts SVP- Chief Economist, Equifax May 15, 2014 Comments on the Economic Outlook General forecast is that economic growth accelerates

National Community Land Trust Network 2008 Foreclosure Survey Report October 26, 2009

National Community Land Trust Network 2008 Foreclosure Survey Report October 26, 2009 By Marge Misak, Cuyahoga Community Land Trust, Cleveland and National CLT Academy Board Member, with support from Roger

National Community Land Trust Network 2008 Foreclosure Survey Report October 26, 2009 By Marge Misak, Cuyahoga Community Land Trust, Cleveland and National CLT Academy Board Member, with support from Roger

THE STATE OF THE NATION S HOUSING. Joint Center for Housing Studies of Harvard University

THE STATE OF THE NATION S HOUSING 26 Joint Center for Housing Studies of Harvard University Joint Center for Housing Studies of Harvard University Graduate School of Design John F. Kennedy School of Government

THE STATE OF THE NATION S HOUSING 26 Joint Center for Housing Studies of Harvard University Joint Center for Housing Studies of Harvard University Graduate School of Design John F. Kennedy School of Government

Massachusetts Tax Revenue Forecasts for FY 2009 and FY 2010

Massachusetts Tax Revenue Forecasts for FY 2009 and FY 2010 Beacon Hill Institute at Suffolk University 8 Ashburton Place, Boston, MA 02108 www.beaconhill.org 617 573 8750 bhi@beaconhill.org December 15,

Massachusetts Tax Revenue Forecasts for FY 2009 and FY 2010 Beacon Hill Institute at Suffolk University 8 Ashburton Place, Boston, MA 02108 www.beaconhill.org 617 573 8750 bhi@beaconhill.org December 15,

Home Financing in Kansas City and Its Contribution to Low- and Moderate-Income Neighborhood Development

FEBRUARY 2007 Home Financing in Kansas City and Its Contribution to Low- and Moderate-Income Neighborhood Development JAMES HARVEY AND KENNETH SPONG James Harvey is a policy economist and Kenneth Spong

FEBRUARY 2007 Home Financing in Kansas City and Its Contribution to Low- and Moderate-Income Neighborhood Development JAMES HARVEY AND KENNETH SPONG James Harvey is a policy economist and Kenneth Spong

JOINT CENTER FOR HOUSING STUDIES OF HARVARD UNIVERSITY

1 Executive Summary After several false starts, there is reason to believe that 212 will mark the beginning of a true housing market recovery. Sustained employment growth remains key, providing the stimulus

1 Executive Summary After several false starts, there is reason to believe that 212 will mark the beginning of a true housing market recovery. Sustained employment growth remains key, providing the stimulus

The Future of the Mortgage Market: Where Do We Go From Here?

The Future of the Mortgage Market: Where Do We Go From Here? Stuart Gabriel, Director of the Ziman Center for Real Estate, Arden Realty Chair and Professor of Finance, Anderson School of Management, University

The Future of the Mortgage Market: Where Do We Go From Here? Stuart Gabriel, Director of the Ziman Center for Real Estate, Arden Realty Chair and Professor of Finance, Anderson School of Management, University

BEYOND THE CREDIT SCORE: The Secondary Mortgage Market

BEYOND THE CREDIT SCORE: The Secondary Mortgage Market Housing Action IL Housing Action Illinois is a statewide coalition formed to protect and expand the availability of quality, affordable housing throughout

BEYOND THE CREDIT SCORE: The Secondary Mortgage Market Housing Action IL Housing Action Illinois is a statewide coalition formed to protect and expand the availability of quality, affordable housing throughout