Understanding the World Economy Master in Economics and Business. Financial crisis. Nicolas Coeurdacier

|

|

|

- Andra Chase

- 5 years ago

- Views:

Transcription

1 Understanding the World Economy Master in Economics and Business Financial crisis Lecture 12 Nicolas Coeurdacier

2 Lecture 12 : Financial crisis 1. Currency crisis: first generation 2. Self fulfilling currency crisis 3. Sovereign debt crisis

3 Currency crisis Often just seen as a large devaluation Speculative attack with sudden loss of confidence in the central bank promise to keep the exchange rate fixed: run on the central bank foreign reserves : to defend the fixed exchange rate the central bank sells its reserves But not all attacks succeed distinguish between currency crash (large devaluation) and crisis, when authorities defend exchange rate peg - with sharp spike in interest rates - sharp fall in foreign exchange reserves

4 The dangers of managed exchange rates

5 And 11 years later Iceland ISK/EUR

Reserves in")

6 And 11 years later Pakistan Current account Reserves and exchange rate (up is depreciation) Reserves in billions of dollars Billions of dollars % of GDP Rupee/dollar IMF

7 Currency crises are common Most fixed exchange rate regimes eventually come under severe strain (and flexible rates can also suffer sudden depreciation) Currency crises have been frequent in the past and also since the 1990s 1992/1993 : European Monetary system and the attack on Pound 1994 : Mexico 1997/1999 : Thailand, South Korea, Indonesia, Brazil, Russia 2000/2001 : Turkey, Argentina 2008 : Iceland, Pakistan, Hungary, Baltic states

8 Zimbabwe Venezuala Uruguay Turkey Thailand Some countries experience repeated crises Number of Currency Crises ( ) Taiwan Sri Lanka South Africa Singapore Phillipines Peru Paraguay Pakistan Nigeria New Zealand Mexico Malaysia Korea Jamaica Israel Ireland Indonesia India Iceland Egypt Ecuador Costa Rica Colombia China Bangladesh

9 Currency crises are costly

10 Models of currency crisis 1) «Fundamental» balance of payments crisis (Krugman, 1979) 2) Crisis with self-fulfilling expectations and multiple equilibria (Obstfeld, 1994, Krugman, 1999) We start with 1).

11 Fundamentals based crises (Krugman, 1979) The fixed exchange rate is «fundamentally» inconsistent with macro policy (fiscal and monetary) : monetary policy too expansionary (CB buys domestic assets) E.g., CB finances budget deficit; buys T-Bills For ER to remain fixed, r = r*, money supply M S remains fixed: CB must sell reserves at the same rate as it buys T-Bills : Central bank balance sheet: M S = Reserves + Domestic assets Does the fixed ER collapse when CB has no more reserves? Rational speculators understand that at some point reserves will be exhausted and fixed ER will be abandoned. Crisis will come before (speculative attack): run on CB reserves (all speculators want to sell domestic currency and buy reserves of the CB). Looks like panic but the result of rational speculators who understand the fundamental inconsistency of the fixed ER.

12 Exchange rate, E E S T Shadow floating exchange rate: E s t Shadow floating E that would prevail if no foreign reserves and the CB lets the exchange rate float E F E S T T T T time Falling reserves Central bank fixes exchange rate at E F ; domestic assets increase over time (CB buys TBs); shadow exchange rate depreciates over time Foreign reserves of the CB: F

13 The logic and timing of the crisis - Are reserves depleted at T? If so, ER jumps from E F to E S T (currency depreciates from fixed exchange rate to shadow ER consistent with level of money supply): not possible as all speculators know this (rational); they could make money by buying all reserves (before they hit zero) at price E F and sell at E S T - Are reserves depleted at an earlier time T? No because if so, ER jumps (currency appreciates) from E F to E S T : speculators will not buy reserves at that price as they would loose money. They would sell home currency at low price or buy foreign currency at a high price.

14 The logic and timing of the crisis - The run on reserves comes exactly at T when E F = E S T - At T: all speculators go to the central bank sell domestic currency and buy foreign reserves - Looks like panic (all speculators rush to sell domestic currency) but this is a fundamental based speculative attack with rational agents.

15 Lecture 12 : Financial crisis 1. Currency crisis: first generation 2. Self fulfilling currency crisis 3. Sovereign debt crisis

16 Strategic foundations of financial crises: speculative attacks with self-fulfilling expectations So-called second & third generation crises: Models with self-fulfilling expectations bank run: speculation against a fixed ER regime generates the objective conditions that make the crisis possible Multiple equilibria: the determination of the realized equilibrium (crisis with devaluation or no crisis and no devaluation) does not depend only on fundamentals but also on speculators expectations

17 Balance sheet effects: the international channel Third generation crises (Krugman, 1999): To explain Asian crises of Russia ( ) Argentina (2001) More recently: Iceland (2008) Danger of debts (private and public) in foreign currency Currency mismatch: economic agents (banks, firms, households) borrow in foreign currency but their assets and incomes are in domestic currency.

18 Reasons for the currency mismatch Original Sin : to borrow abroad, firms, banks, governments in developing countries cannot borrow in their own currency (long memory of markets of very large depreciations of their currency). Lack of reputation of Central Bank. Might be desirable sometimes to make exchange rate regime more credible. Original sin has weakened since the crisis

19 Original sin: Share of foreign debt in foreign currency (OSIN1) is falling but still very high ; source Hausmann and Panizza (2010)

20 A simple model with balance sheet effect (Krugman 1999) AA curve Investment I Demand for domestic currency Appreciation E appreciates as I CC curve Credit constraints: firms borrow to invest, but borrowing is constrained by the expected value of the firm V e = collateral in case of default Balance sheet effect: I = λ. V e = λ (π e d D E e. d F ) Profit debt payment in domestic currency debt payment in foreign currency Key mechanism Expected depreciation (E e ) value of foreign denominated debt E e. d F value of firm (collateral in case of default) : banks their lending investment; CC curve: I decreases as E e If E e > E crash : Firms value <0 (default) ; I = 0

21 E and E e The case of a unique equilibrium The case of share of private debt in foreign currency is small : CC is almost vertical CC: investment does not depend much on E e AA : E appreciates with investment I or credit

22 E and E e Multiple equilibria The case of large share of debt in foreign currency E crash Crash: I =0, big depreciation, firms default, stock market crash, sudden stop 3 equilibria, 2 only are stable : crash and boom Multiple equilibria driven by expectations! Boom: I high, ER is appreciated CC : investment decreases as expected depreciation E e AA : E appreciates with investment I or credit

23 Circular mechanism: the crisis equilibrium Expected crisis and depreciation Credit and investment crisis (sudden stop), demand Balance sheet effect: value of foreign debt in domessc currency Value of collateral of households, firms and banks

24 Similar mechanism with banks (Iceland) Banks lend massively to firms (I) and households (real estate) : assets of three main banks = 10 x Iceland GDP Banks in Iceland borrow massively in foreign currency ( ): collateral of the banks is based on the value of their net assets : decreasing Icelandic Krona depreciates. Expected depreciation (E e ) collateral of banks banks cannot borrow on international markets Economic, financial, real estate, credit and currency crisis. Again, circular mechanism

Increasein leverage and")

25 Icelandic Banking Sector Assets and liabilities of the three main banks compared to GDP (m. ISK.) Increasein leverage and size of the Icelandic banking sector Source: Buiter and Sibert (2008)

26 Icelandic Banking Sector 800% Foreign currency liabilities of banks and CB forex reserves september % 600% 750% GDP 500% 400% 300% 200% CB forex reserves: 21% GDP CB swaps and credit lines: 14% GDP 100% 0% Foreign currency liabilities of the banks CB forex liquidity and highly vulnerable to a currency crash

27 Icelandic Crash ISK/EUR Currency Crash

28 : : : : : : : : : : : : : : : 3 Icelandic Crash Share price indices U.S. U.K. Spain Ireland Iceland 3 0 / 0 9 / / 0 3 / / 0 9 / / 0 3 / / 0 9 / / 0 3 / / 0 9 / / 0 3 / / 0 9 / / 0 3 / / 0 9 / / 0 3 / / 0 9 / / 0 3 / / 0 9 / / 0 3 / / 0 9 / / 0 3 / / 0 9 / / 0 3 / / 0 9 / / 0 3 / (2000Q1=100) House price indices Source: Benediktsdottir et al. (2010)

29 Balance sheet effects in the recent crisis: the domestic channel (households) See Lecture 7. Households borrow using their house as collateral: if negative shock on house prices borrowing falls house purchases fall house prices fall Collateral value fall further house prices fall further Again, circular mechanism

30 Balance sheet effects in the recent crisis: the domestic channel (banks) See Lecture 7. Banks lend long-term (think mortgages) and borrow shortterm (extensively before the crisis): maturity mismatch Vulnerable to balance-sheet effects: as asset/house prices fall, fall in the value of bank assets Cannot borrow short-term (decrease in the value of their assets and collateral/increase in uncertainty/fear of bankruptcy ). Need to sell assets (deleveraging) Banking assets prices fall further Vicious circle!

31 Circular mechanism: the domestic channel (Expected) drop in (long-term) asset values Deleveraging (credit crunch propagates to the real economy) Balance sheet effect: cost of borrowing Value of collateral of households and banks

32 Lecture 12 : Financial crisis 1. Currency crisis: first and second generation 2. Currency crisis: balance-sheets effects 3. Sovereign debt crisis

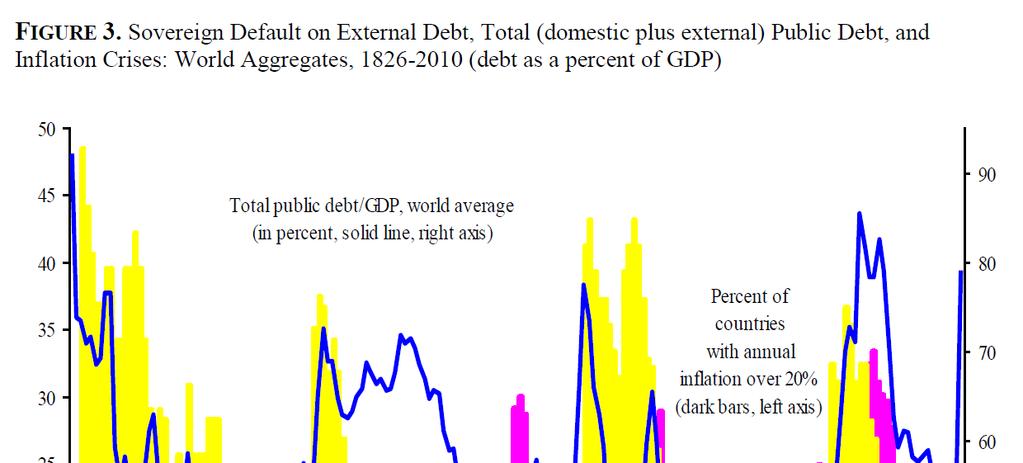

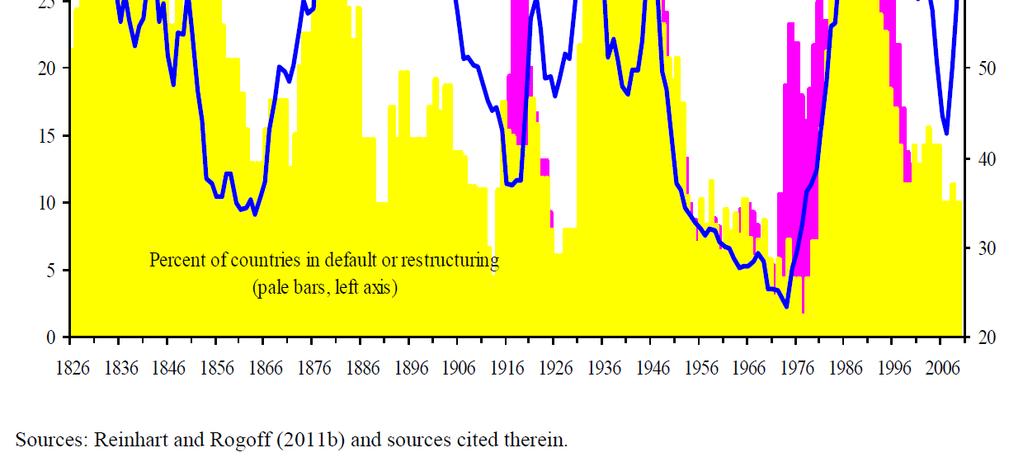

33 Sovereign debt crisis Sovereign - no international enforcement of debt contracts (difficult for creditors to seize assets, no collateral, no bankruptcy court) What is default? Missing any contractual payment: - outright complete default (rare) - repudiation or moratorium - restructuring: renegotiation (with terms less favorable to the lender: haircut) Serial default (long history): a widespread phenomenon

34

35 What is the cost of sovereign default? Gain (wealth transfer) against reputation costs Greece default (1826): no access to international capital markets for 53 years More recently: Uruguay (2003) restructured its debt (stretching maturity dates 5 years). Returned to capital markets a month later. The haircut, or loss to bondholders, was small (13.3%, in net present value) orderly sovereign workouts are possible (not the case of Argentina)

36 Broader macroeconomic costs Triggers or worsen banking crisis Triggers currency crisis Both together generate large output losses Trade disruption (Rose, 2005): countries in default face very high risk premia to finance simple trade activities; disruption of trade credit

37 Understanding defaults: some basic theory

38 Understanding defaults: some basic theory

39 Understanding defaults: some basic theory

40 From financial crisis to sovereign default Typical stages of financial crises (Reinhart and Rogoff, 2009) 1) private debt surges (domestic banking credit growth + external borrowing) 2) banking crises often precede sovereign debt crises (bail outs + collapsing revenues: government debts rise by about 86% in the 3 years after financial crisis): See Ireland (bail out of banks: public debt increased by 20 % point of GDP) 3) public borrowing accelerates ahead of a sovereign debt crisis ; government often has hidden debts (Greece) 4) On eve of banking and debt crises composition of debt shifts toward short-term maturities

")

41 (Source Reinhart and Rogoff)

42 Cumulative increase in public debt after the financial crisis (selected countries) Source Reinhart and Rogoff

43 Sustainable debt - reminder To keep debt levels constant fiscal policy needs to generate primary surplus/gdp = If > government has to run a primary surplus in order to control the Debt/GDP ratio. If < then government can run a deficit (of a certain size) without seeing Debt/GDP ratio increase. Shifts in interest rates and growth rates have big impact on government debt dynamics. If r increases with Debt/GDP and higher r leads to lower g then countries can rapidly find their public finances deteriorating

44 Sovereign debt crisis in Argentina ( ) Context: The Convertibility Plan , President Carlos Menem takes office. Monthly inflation > 200%. Output plummeting April 1991, Finance Minister Domingo Cavallo implements the Convertibility Plan, including the policy of a Currency Board: Fixed Exchange Rate of 1 Peso / $1 People free to buy and sell Dollars. Implication: Central Bank no longer controls monetary policy. gradual loss of competitiveness as no longer possible to depreciate the currency and inflation still high

45 (Hyper)Inflation in Argentina Inflation Rate % change per year Stabilization Policy in Argentina in early nineties breaks down hyperinflation.

46 In 2000 Argentina does not stand out as hopeless

47 Indicators of Fiscal Sustainability Argentina s crisis caused not by high debt (around 50% GDP) but high r and falling g! (source: Perry & Serven, WB03)

48 Sustainable Debt - Argentina To stabilize the debt to GDP ratio, one needs: (r-g)d/y=pdf/y. D(dec 2001) = 140 bn. Pesos Y(2001) = 269 bn Pesos g( ) = -2.9 % (2001: -4.4%; 2000: -0.8, 1999: -3.5) r = 8.7 % (high but including risk premium) Required primary surplus = (140/269)*(11.6) = 6%! (actual primary surplus in 2000 = 0.3%) If negative growth is seen as persistent, this is unsustainable. Unless fiscal policy is adjusted, debt will rise continuously.

49 Sustainable Debt - Argentina Simple calculations but firm implications: (a) Although debt was not extraordinarily high, the low growth (and high interest rates) quickly makes the debt burden unsustainable (b) If growth prospects turn around, no major problems, but that requires reforms (c) Default is only a temporary relief, unless growth picks up and fiscal policy changes

50 Currency Mismatch and Balance Sheets Effects

51 The Unravelling recession exacerbated government s fiscal position investor fears that currency board would be abandoned fear of devaluation pushed up yield spreads dramatically increasing fiscal burden from interest payments, banking system increasingly based around dollars peso devaluation even more expensive with election focused on economic policy, capital inflows dried up. In December 2000, IMF offered $40bn subject to fiscal conditions Very costly debt exchange in mid-2001, then Argentina convinced US to get IMF to offer a further $8bn But by December 2001, the conditions had not been met, IMF pulled the plug, and government introduced outright default on public debt and exchange controls, abandoned peg, let currency float. Forced pesification of dollar bank deposits at 1.40 Peso to $, dollar loans converted at 1-1, banks foreign exchange reserves confiscated huge balance sheet blow to the banks

52 Run on Banks and Capital Outflows $US billion $US billion IVQ 2000 IQ 2001 IIQ 2001 IIIQ 2001 IVQ IVQ 2000 IQ 2001 IIQ 2001 IIIQ 2001 IVQ 2001 Bank Deposits Balance of Payments-Non Financial Private Sector Capital Account Source: Argentine Central Bank and Ministry of Economy

53 2002:1 2003:1 2004:1 2001: Exchange Rate: Peso / $ (inverted scale) 1995:1 1996:1 1997:1 1998:1 1999:1 2000:1 1994:1 1993:1 1992:1 1991:1

54 The Hair Cut March 4, 2005 NY Times It took more than three years of stop-and-go negotiations, threats, political maneuvers and court battles, but the largest government debt default in history ended here Thursday, as the Argentine government announced that 76 percent of its creditors had accepted a proposal that will pay them at most 30 cents. This was the biggest haircut or loss on principal, for investors of any sovereign bond restructuring in modern times.

55 The euro sovereign debt crisis Investor fear of sovereign debt and default. Confidence/liquidity crisis = Similar mechanism of self-fulfilling expectations Demand higher interest rates to cover risk of default. High interest rate more difficult to pay if the debt-gdp ratio is high. Even more so if growth is low. Default could be caused by the belief that a country can t repay debt --- validating expectations ex-ante. Fear of break-up of the euro ECB role = attempt to manage the confidence/liquidity crisis

56 The euro sovereign debt crisis Confidence/liquidity crisis Circular causality with self-fulfilling expectations. remedy --- break the expectations = ECB intervention and creation of financial safety nets Solvency crisis: some countries will not be able to repay (whatever markets reactions) remedy --- restructure sovereign debt. When? How much?

57 Summary Currency crisis are a common phenomenon in countries with pegged exchange rates. They can be due to misaligned policies but also to self-fulfilling expectations combined with weak fundamentals. Borrowing in foreign currency and lending in domestic currency makes countries vulnerable to self-fulfilling crashes due to balance sheet effects. Similar balance-sheet effects might arise when borrowing short-term and lending longterm. This makes highly leveraged banks very vulnerable to liquidity shocks. Sovereign risk can lead to sovereign debt crisis when public debt becomes unsustainable. Changes in interest rates and growth rates have large impact on debt sustainability.

International financial crises

International Macroeconomics Master in International Economic Policy International financial crises Lectures 11-12 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lectures 11 and 12 International

International Macroeconomics Master in International Economic Policy International financial crises Lectures 11-12 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lectures 11 and 12 International

Fixed Exchange Rates and Currency Unions

Trade and International Finance SciencesPo Second Year Fall 2018 Fixed Exchange Rates and Currency Unions Lecture 8 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Fixed exchange rates and currency

Trade and International Finance SciencesPo Second Year Fall 2018 Fixed Exchange Rates and Currency Unions Lecture 8 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Fixed exchange rates and currency

Fixed versus floating exchange rates and the role of central bank interventions

Fixed versus floating exchange rates and the role of central bank interventions Lecture 8-9 Nicolas Coeurdacier nicolas.coeurdacier@sciences-po.fr Fixed versus floating exchange rates and the role of central

Fixed versus floating exchange rates and the role of central bank interventions Lecture 8-9 Nicolas Coeurdacier nicolas.coeurdacier@sciences-po.fr Fixed versus floating exchange rates and the role of central

Currency Crises: Theory and Evidence

Currency Crises: Theory and Evidence Lecture 3 IME LIUC 2008 1 The most dramatic form of exchange rate volatility is a currency crisis when an exchange rate depreciates substantially in a short period.

Currency Crises: Theory and Evidence Lecture 3 IME LIUC 2008 1 The most dramatic form of exchange rate volatility is a currency crisis when an exchange rate depreciates substantially in a short period.

L-3: BALANCE OF PAYMENT CRISES IRINA BUNDA MACROECONOMIC POLICIES IN TIMES OF HIGH CAPITAL MOBILITY VIENNA, MARCH 21 25, 2016

L-3: BALANCE OF PAYMENT CRISES IRINA BUNDA MACROECONOMIC POLICIES IN TIMES OF HIGH CAPITAL MOBILITY VIENNA, MARCH 21 25, 2016 THIS TRAINING MATERIAL IS THE PROPERTY OF THE JOINT VIENNA INSTITUTE (JVI)

L-3: BALANCE OF PAYMENT CRISES IRINA BUNDA MACROECONOMIC POLICIES IN TIMES OF HIGH CAPITAL MOBILITY VIENNA, MARCH 21 25, 2016 THIS TRAINING MATERIAL IS THE PROPERTY OF THE JOINT VIENNA INSTITUTE (JVI)

Other similar crisis: Euro, Emerging Markets

Session 15. Understanding Macroeconomic Crises. Mexican Crisis 1994-95 Other similar crisis: Euro, Emerging Markets Global Scenarios 2017-2021 The Mexican Peso Crisis in 1994: Background An economy that

Session 15. Understanding Macroeconomic Crises. Mexican Crisis 1994-95 Other similar crisis: Euro, Emerging Markets Global Scenarios 2017-2021 The Mexican Peso Crisis in 1994: Background An economy that

Developing Countries Chapter 22

Developing Countries Chapter 22 1. Growth 2. Borrowing and Debt 3. Money-financed deficits and crises 4. Other crises 5. Currency board 6. International financial architecture for the future 1 Growth 1.1

Developing Countries Chapter 22 1. Growth 2. Borrowing and Debt 3. Money-financed deficits and crises 4. Other crises 5. Currency board 6. International financial architecture for the future 1 Growth 1.1

Prepared by Iordanis Petsas To Accompany. by Paul R. Krugman and Maurice Obstfeld

Chapter 22 Developing Countries: Growth, Crisis, and Reform Prepared by Iordanis Petsas To Accompany International Economics: Theory and Policy, Sixth Edition by Paul R. Krugman and Maurice Obstfeld Chapter

Chapter 22 Developing Countries: Growth, Crisis, and Reform Prepared by Iordanis Petsas To Accompany International Economics: Theory and Policy, Sixth Edition by Paul R. Krugman and Maurice Obstfeld Chapter

Lecture 6: Intermediate macroeconomics, autumn Lars Calmfors

Lecture 6: Intermediate macroeconomics, autumn 2009 Lars Calmfors 1 Topics Systems of fixed exchange rates Interest rate parity under a fixed exchange rate Stabilisation policy under a fixed exchange rate

Lecture 6: Intermediate macroeconomics, autumn 2009 Lars Calmfors 1 Topics Systems of fixed exchange rates Interest rate parity under a fixed exchange rate Stabilisation policy under a fixed exchange rate

Open Economy AS/AD: Applications

Open Economy AS/AD: Applications Econ 309 Martin Ellison UBC Agenda and References Trilemma Jones, chapter 20, section 7 Euro crisis Jones, chapter 20, section 8 Global imbalances Jones, chapter 29, section

Open Economy AS/AD: Applications Econ 309 Martin Ellison UBC Agenda and References Trilemma Jones, chapter 20, section 7 Euro crisis Jones, chapter 20, section 8 Global imbalances Jones, chapter 29, section

ARGENTINA: WHAT WENT WRONG? Guillermo Perry and Luis Servén World Bank May 2003

ARGENTINA: WHAT WENT WRONG? Guillermo Perry and Luis Servén World Bank May 2003 Performance in the nineties: Better than most up to 1998, worse than most afterwards Real GDP Growth Rate (Percentages) 1981-90

ARGENTINA: WHAT WENT WRONG? Guillermo Perry and Luis Servén World Bank May 2003 Performance in the nineties: Better than most up to 1998, worse than most afterwards Real GDP Growth Rate (Percentages) 1981-90

Rich and Poor. Indicators of Economic Welfare for 4 groups of countries, 2003 GNP per capita (1995 US$)

") Rich and Poor Indicators of Economic Welfare for 4 groups of countries, 2003 GNP per capita (1995 US$) Life expectancy Low income 450 58 Lower-middle income 1480 69 Upper-middle income 5340 73 High income

Rich and Poor Indicators of Economic Welfare for 4 groups of countries, 2003 GNP per capita (1995 US$) Life expectancy Low income 450 58 Lower-middle income 1480 69 Upper-middle income 5340 73 High income

ABSTRACT. This paper shows that the Russian 1998 crisis had a big impact on capital flows to Emerging Market

Sudden Stop, Financial Factors and Economic Collapse in Latin America: Learning from Argentina and Chile Guillermo A. Calvo and Ernesto Talvi NBER Working Paper No. 11153 February 2005 JEL No. F31, F32,

Sudden Stop, Financial Factors and Economic Collapse in Latin America: Learning from Argentina and Chile Guillermo A. Calvo and Ernesto Talvi NBER Working Paper No. 11153 February 2005 JEL No. F31, F32,

Chapter 22 (11) Developing Countries: Growth, Crisis, and Reform

Developing Countries: Growth, Crisis, and Reform") Chapter 22 (11) Developing Countries: Growth, Crisis, and Reform Preview Snapshots of rich and poor countries Characteristics of poor countries Borrowing and debt in poor and middle-income economies The

Chapter 22 (11) Developing Countries: Growth, Crisis, and Reform Preview Snapshots of rich and poor countries Characteristics of poor countries Borrowing and debt in poor and middle-income economies The

East Asia Crisis of Econ October 8, Team 5 Bryan Darch Svend Egholm Paramdeep Singh Sarah Zullo

East Asia Crisis of 1997 Econ 7920 October 8, 2008 Team 5 Bryan Darch Svend Egholm Paramdeep Singh Sarah Zullo The East Asian currency crisis of 1997 caused severe distress for the countries of East Asia

East Asia Crisis of 1997 Econ 7920 October 8, 2008 Team 5 Bryan Darch Svend Egholm Paramdeep Singh Sarah Zullo The East Asian currency crisis of 1997 caused severe distress for the countries of East Asia

Global Business Economics. Mark Crosby SEMBA International Economics

Global Business Economics Mark Crosby SEMBA International Economics The balance of payments and exchange rates Understand the structure of a country s balance of payments. Understand the difference between

Global Business Economics Mark Crosby SEMBA International Economics The balance of payments and exchange rates Understand the structure of a country s balance of payments. Understand the difference between

LEARNING OBJECTIVES 4. Debt and

LEARNING OBJECTIVES 4. Debt and Default Describe how sovereign debt is a contingent claim in context of financial mar rket penalties and broader macroeconomic costs. Determine the probability of default

LEARNING OBJECTIVES 4. Debt and Default Describe how sovereign debt is a contingent claim in context of financial mar rket penalties and broader macroeconomic costs. Determine the probability of default

Fiscal Policy and the Global Crisis

Fiscal Policy and the Global Crisis Presentation at Koҫ University, Istanbul Carlo Cottarelli Director IMF Fiscal Affairs Department June 9, 2009 1 Two fiscal questions What is the appropriate fiscal policy

Fiscal Policy and the Global Crisis Presentation at Koҫ University, Istanbul Carlo Cottarelli Director IMF Fiscal Affairs Department June 9, 2009 1 Two fiscal questions What is the appropriate fiscal policy

Chapter Eleven. The International Monetary System

Chapter Eleven The International Monetary System Introduction 11-3 The international monetary system refers to the institutional arrangements that govern exchange rates. Floating exchange rates occur when

Chapter Eleven The International Monetary System Introduction 11-3 The international monetary system refers to the institutional arrangements that govern exchange rates. Floating exchange rates occur when

THE GLOBAL ECONOMY: SECULAR STAGNATION OR RECOVERY AT LAST? Adair Turner Chairman Institute for New Economic Thinking

THE GLOBAL ECONOMY: SECULAR STAGNATION OR RECOVERY AT LAST? Adair Turner Chairman Institute for New Economic Thinking Institutional Money Kongress Frankfurt, 21 February 2017 300 Park Avenue South - 5

THE GLOBAL ECONOMY: SECULAR STAGNATION OR RECOVERY AT LAST? Adair Turner Chairman Institute for New Economic Thinking Institutional Money Kongress Frankfurt, 21 February 2017 300 Park Avenue South - 5

Export Group Meeting on the Contribution and Effective Use of External Resources for Development, in Particular for Productive Capacity Building

Export Group Meeting on the Contribution and Effective Use of External Resources for Development, in Particular for Productive Capacity Building 22-24 February 21 Debt Sustainability and the Implications

Export Group Meeting on the Contribution and Effective Use of External Resources for Development, in Particular for Productive Capacity Building 22-24 February 21 Debt Sustainability and the Implications

Threats to Financial Stability in Emerging Markets: The New (Very Active) Role of Central Banks. LILIANA ROJAS-SUAREZ Chicago, November 2011

Role of Central Banks. LILIANA ROJAS-SUAREZ Chicago, November 2011") Threats to Financial Stability in Emerging Markets: The New (Very Active) Role of Central Banks LILIANA ROJAS-SUAREZ Chicago, November 2011 Currently, the Major Threats to Financial Stability in Emerging

Threats to Financial Stability in Emerging Markets: The New (Very Active) Role of Central Banks LILIANA ROJAS-SUAREZ Chicago, November 2011 Currently, the Major Threats to Financial Stability in Emerging

Asian Financial Crisis. Jianing Li/Wei Ye/Jingyan Zhang 2018/11/29

Asian Financial Crisis Jianing Li/Wei Ye/Jingyan Zhang 2018/11/29 Causes--Current account deficit 1. Liberalization of capital markets. 2. Large capital inflow due to the interest rates fall in developed

Asian Financial Crisis Jianing Li/Wei Ye/Jingyan Zhang 2018/11/29 Causes--Current account deficit 1. Liberalization of capital markets. 2. Large capital inflow due to the interest rates fall in developed

The International Financial System

The International Financial System Notes on Mishkin, Chapter 21 Leigh Tesfatsion Economics Department Iowa State University, Ames IA Last Revised: 27 April 2011 Key In-Class Discussion Questions Mishkin,

The International Financial System Notes on Mishkin, Chapter 21 Leigh Tesfatsion Economics Department Iowa State University, Ames IA Last Revised: 27 April 2011 Key In-Class Discussion Questions Mishkin,

Final exam Non-detailed correction 3 hours. This are indicative directions on how structure the essay questions and what was expected.

International Finance Master PEI Fall 2011 Nicolas Coeurdacier Final exam Non-detailed correction 3 hours This are indicative directions on how structure the essay questions and what was expected. 1. Multiple

International Finance Master PEI Fall 2011 Nicolas Coeurdacier Final exam Non-detailed correction 3 hours This are indicative directions on how structure the essay questions and what was expected. 1. Multiple

19.2 Exchange Rates in the Long Run Introduction 1/24/2013. Exchange Rates and International Finance. The Nominal Exchange Rate

Chapter 19 Exchange Rates and International Finance By Charles I. Jones International trade of goods and services exceeds 20 percent of GDP in most countries. Media Slides Created By Dave Brown Penn State

Chapter 19 Exchange Rates and International Finance By Charles I. Jones International trade of goods and services exceeds 20 percent of GDP in most countries. Media Slides Created By Dave Brown Penn State

LECTURE 26: Speculative Attack Models

LECTURE 26: Speculative Attack Models Generation I Generation II Generation III Breaching the central bank s defenses. Speculative Attacks Breaching the central bank s defenses. Traditional pattern: Reserves

LECTURE 26: Speculative Attack Models Generation I Generation II Generation III Breaching the central bank s defenses. Speculative Attacks Breaching the central bank s defenses. Traditional pattern: Reserves

Global Financial Systems Chapter 19 Sovereign Debt Crises

Global Financial Systems Chapter 19 Sovereign Debt Crises Jon Danielsson London School of Economics 2018 To accompany Global Financial Systems: Stability and Risk http://www.globalfinancialsystems.org/

Global Financial Systems Chapter 19 Sovereign Debt Crises Jon Danielsson London School of Economics 2018 To accompany Global Financial Systems: Stability and Risk http://www.globalfinancialsystems.org/

The Evolution of the International Monetary System. Professor Keith Pilbeam City University, London

The Evolution of the International Monetary System Professor Keith Pilbeam City University, London The Postwar International Monetary System some highlights Bretton Woods 1949-72 sets up IMF, fixes dollar

The Evolution of the International Monetary System Professor Keith Pilbeam City University, London The Postwar International Monetary System some highlights Bretton Woods 1949-72 sets up IMF, fixes dollar

REAL ESTATE BOOMS, RECESSIONS AND FINANCIAL CRISES

REAL ESTATE BOOMS, RECESSIONS AND FINANCIAL CRISES Christophe André OECD Economics Department Joint work with Thomas Chalaux OECD Economics Department Recent trends in the real estate market and its analysis,

REAL ESTATE BOOMS, RECESSIONS AND FINANCIAL CRISES Christophe André OECD Economics Department Joint work with Thomas Chalaux OECD Economics Department Recent trends in the real estate market and its analysis,

Monetary and Exchange Rate Policy Responses to the Global Financial Crisis: The Case of Colombia

Monetary and Exchange Rate Policy Responses to the Global Financial Crisis: The Case of Colombia Hernando Vargas Banco de la República Colombia March, 2009 Contents I. The state of the Colombian economy

Monetary and Exchange Rate Policy Responses to the Global Financial Crisis: The Case of Colombia Hernando Vargas Banco de la República Colombia March, 2009 Contents I. The state of the Colombian economy

Chapter 17 Appendix B

Speculative Attacks and Foreign Exchange Crises Chapter 17 Appendix B In the following two applications, we use our model of exchange rate determination to understand how speculative attacks in both advanced

Speculative Attacks and Foreign Exchange Crises Chapter 17 Appendix B In the following two applications, we use our model of exchange rate determination to understand how speculative attacks in both advanced

International Finance and Macroeconomics (Econ 422)

") Professor Eric van Wincoop Econ 422 Department of Economics Spring 2015 231 Monroe Hall TR 9:30-10:45 Office Hours: Monday 2-3, Tuesday 11-12 Monroe 116 E-mail: vanwincoop@virginia.edu Phone: 924-3997

Professor Eric van Wincoop Econ 422 Department of Economics Spring 2015 231 Monroe Hall TR 9:30-10:45 Office Hours: Monday 2-3, Tuesday 11-12 Monroe 116 E-mail: vanwincoop@virginia.edu Phone: 924-3997

Monetary Policy in a Global Economy: Past and Future Research Challenges

Monetary Policy in a Global Economy: Past and Future Research Challenges Presentation at the Conference Globalization and the Macroeconomy 24 July 2007 John B. Taylor Stanford University Past Challenges

Monetary Policy in a Global Economy: Past and Future Research Challenges Presentation at the Conference Globalization and the Macroeconomy 24 July 2007 John B. Taylor Stanford University Past Challenges

The International Financial Crises of the 1990s: Analytics

1 The International Financial Crises of the 1990s: Analytics J. Bradford DeLong http://www.j-bradford-delong.net/ November 2001 The decade of the 1990s was marked by the sudden emergence of capital-account

1 The International Financial Crises of the 1990s: Analytics J. Bradford DeLong http://www.j-bradford-delong.net/ November 2001 The decade of the 1990s was marked by the sudden emergence of capital-account

The Financial Crisis, Global Imbalances, and the

The Financial Crisis, Global Imbalances, and the International Monetary System David Vines Oxford University, Australian National University, and CEPR ICRIER-CEPII-BRUEGEL Conference on International Cooperation

The Financial Crisis, Global Imbalances, and the International Monetary System David Vines Oxford University, Australian National University, and CEPR ICRIER-CEPII-BRUEGEL Conference on International Cooperation

Financial Crisis What do we know?

Financial Crisis What do we know? Pedro Videla IESE Global Propagation of the Financial Crisis United Kingdom Ireland Iceland United States Spain January 2008 March 2008 June 2008 September 2008 January

Financial Crisis What do we know? Pedro Videla IESE Global Propagation of the Financial Crisis United Kingdom Ireland Iceland United States Spain January 2008 March 2008 June 2008 September 2008 January

Greece should restructure its debt but stay in the Euro

Greece should restructure its debt but stay in the Euro By Domingo Cavallo Sep 23, 2011 Greece should restructure its debt and reorganize its economy, but stay in the Euro and accept its monetary discipline.

Greece should restructure its debt but stay in the Euro By Domingo Cavallo Sep 23, 2011 Greece should restructure its debt and reorganize its economy, but stay in the Euro and accept its monetary discipline.

MANAGING CAPITAL FLOWS

MANAGING CAPITAL FLOWS Yılmaz Akyüz South Centre, Geneva Capital Account Regulations and Global Economic Governance Workshop Organized by UNCTAD and GEGI, Geneva, Palais des Nations, 3-4 October 2013 www.southcentre.int

MANAGING CAPITAL FLOWS Yılmaz Akyüz South Centre, Geneva Capital Account Regulations and Global Economic Governance Workshop Organized by UNCTAD and GEGI, Geneva, Palais des Nations, 3-4 October 2013 www.southcentre.int

Final exam Non-detailed correction 3 hours

International Finance Master PEI Spring 2013 Nicolas Coeurdacier Final exam Non-detailed correction 3 hours Documents not allowed. Basic calculator allowed. For the Multiple Choice Questions, use the answer

International Finance Master PEI Spring 2013 Nicolas Coeurdacier Final exam Non-detailed correction 3 hours Documents not allowed. Basic calculator allowed. For the Multiple Choice Questions, use the answer

1. Generation One. 2. Generation Two. 3. Sudden Stops. 4. Banking Crises. 5. Fiscal Solvency

Currency Crises 1. Generation One 2. Generation Two 3. Sudden Stops 4. Banking Crises 5. Fiscal Solvency 1 Generation One 1.1 Monetary and Fiscal Policy Initial position long-run equilibrium purchasing

Currency Crises 1. Generation One 2. Generation Two 3. Sudden Stops 4. Banking Crises 5. Fiscal Solvency 1 Generation One 1.1 Monetary and Fiscal Policy Initial position long-run equilibrium purchasing

FUND MANAGEMENT DIARY Meeting held on 31 st July 2018

FUND MANAGEMENT DIARY Meeting held on 31 st July 2018 Why are EMs less vulnerable to external shocks? Previous financial crises in emerging markets have typically been caused by a build-up of external

FUND MANAGEMENT DIARY Meeting held on 31 st July 2018 Why are EMs less vulnerable to external shocks? Previous financial crises in emerging markets have typically been caused by a build-up of external

Financial System Stabilized, but Exit, Reform, and Fiscal Challenges Lie Ahead

January 21 Financial System Stabilized, but Exit, Reform, and Fiscal Challenges Lie Ahead Systemic risks have continued to subside as economic fundamentals have improved and substantial public support

January 21 Financial System Stabilized, but Exit, Reform, and Fiscal Challenges Lie Ahead Systemic risks have continued to subside as economic fundamentals have improved and substantial public support

ROUNDTABLE COMMENTS ON MONETARY AND REGULATORY POLICY IN AN ERA OF GLOBAL MARKETS

ROUNDTABLE COMMENTS ON MONETARY AND REGULATORY POLICY IN AN ERA OF GLOBAL MARKETS Liliana Rojas-Suarez Institute for International Economics D uring the conference we have heard a lot of stress placed

ROUNDTABLE COMMENTS ON MONETARY AND REGULATORY POLICY IN AN ERA OF GLOBAL MARKETS Liliana Rojas-Suarez Institute for International Economics D uring the conference we have heard a lot of stress placed

Lessons of the Financial Crisis for the Design of the New International Financial Architecture

Lessons of the Financial Crisis for the Design of the New International Financial Architecture John B. Taylor Hoover Institution and Stanford University Written Version of Keynote Address Conference on

Lessons of the Financial Crisis for the Design of the New International Financial Architecture John B. Taylor Hoover Institution and Stanford University Written Version of Keynote Address Conference on

Suggested Solutions to Problem Set 6

Department of Economics University of California, Berkeley Spring 2006 Economics 182 Suggested Solutions to Problem Set 6 Problem 1: International diversification Because raspberries are nontradable, asset

Department of Economics University of California, Berkeley Spring 2006 Economics 182 Suggested Solutions to Problem Set 6 Problem 1: International diversification Because raspberries are nontradable, asset

Developing Housing Finance Systems

Developing Housing Finance Systems Veronica Cacdac Warnock IIMB-IMF Conference on Housing Markets, Financial Stability and Growth December 11, 2014 Based on Warnock V and Warnock F (2012). Developing Housing

Developing Housing Finance Systems Veronica Cacdac Warnock IIMB-IMF Conference on Housing Markets, Financial Stability and Growth December 11, 2014 Based on Warnock V and Warnock F (2012). Developing Housing

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 9 Financial Crises. 9.1 What is a Financial Crisis?

Chapter 9 Financial Crises. 9.1 What is a Financial Crisis?") Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 9 Financial Crises 9.1 What is a Financial Crisis? 1) A major disruption in financial markets characterized by sharp declines in asset

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 9 Financial Crises 9.1 What is a Financial Crisis? 1) A major disruption in financial markets characterized by sharp declines in asset

Presentation at the 2011 Philadelphia Fed Policy Forum December 2, University of Maryland & NBER

Presentation at the 2011 Philadelphia Fed Policy Forum December 2, 2011 Enrique G. Mendoza Enrique G. Mendoza University of Maryland & NBER 1. Short: May/Dec. 2010 Greece, Ireland plans 2. Tall: July 2011

Presentation at the 2011 Philadelphia Fed Policy Forum December 2, 2011 Enrique G. Mendoza Enrique G. Mendoza University of Maryland & NBER 1. Short: May/Dec. 2010 Greece, Ireland plans 2. Tall: July 2011

Foreign Currency Debt, Financial Crises and Economic Growth : A Long-Run Exploration

Foreign Currency Debt, Financial Crises and Economic Growth : A Long-Run Exploration Michael D. Bordo Rutgers University and NBER Christopher M. Meissner UC Davis and NBER GEMLOC Conference, World Bank,

Foreign Currency Debt, Financial Crises and Economic Growth : A Long-Run Exploration Michael D. Bordo Rutgers University and NBER Christopher M. Meissner UC Davis and NBER GEMLOC Conference, World Bank,

A Stable International Monetary System Emerges: Inflation Targeting as Bretton Woods, Reversed

A Stable International Monetary System Emerges: Inflation Targeting as Bretton Woods, Reversed Andrew K. Rose UC Berkeley, CEPR and NBER September, 2007 Motivation Many Currency Crises through end of 20

A Stable International Monetary System Emerges: Inflation Targeting as Bretton Woods, Reversed Andrew K. Rose UC Berkeley, CEPR and NBER September, 2007 Motivation Many Currency Crises through end of 20

Global Economic Prospects

Global Economic Prospects Back from the Brink? Andrew Burns World Bank Prospects Group April 12, 212 1 Amid some signs of improvement, global recovery remains fragile First quarter of 212 has been generally

Global Economic Prospects Back from the Brink? Andrew Burns World Bank Prospects Group April 12, 212 1 Amid some signs of improvement, global recovery remains fragile First quarter of 212 has been generally

cepr Briefing Paper Paying the Bills in Brazil: Does the IMF s Math Add Up? CENTER FOR ECONOMIC AND POLICY RESEARCH By Mark Weisbrot and Dean Baker 1

cepr CENTER FOR ECONOMIC AND POLICY RESEARCH Briefing Paper Paying the Bills in Brazil: Does the IMF s Math Add Up? By Mark Weisbrot and Dean Baker 1 September 25, 2002 CENTER FOR ECONOMIC AND POLICY RESEARCH

cepr CENTER FOR ECONOMIC AND POLICY RESEARCH Briefing Paper Paying the Bills in Brazil: Does the IMF s Math Add Up? By Mark Weisbrot and Dean Baker 1 September 25, 2002 CENTER FOR ECONOMIC AND POLICY RESEARCH

Governments and Exchange Rates

Governments and Exchange Rates Exchange Rate Behavior Existing spot exchange rate covered interest arbitrage locational arbitrage triangular arbitrage Existing spot exchange rates at other locations Existing

Governments and Exchange Rates Exchange Rate Behavior Existing spot exchange rate covered interest arbitrage locational arbitrage triangular arbitrage Existing spot exchange rates at other locations Existing

Emerging Markets Debt: Outlook for the Asset Class

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

Greece, November 2011, in light of Argentinean Experience exactly ten years ago.

1 Greece, November 2011, in light of Argentinean Experience exactly ten years ago. Keynote speech by Domingo Cavallo at the CEO Summit, Doing More on Less, Athens, November 22, 2011 Let me be very sincere

1 Greece, November 2011, in light of Argentinean Experience exactly ten years ago. Keynote speech by Domingo Cavallo at the CEO Summit, Doing More on Less, Athens, November 22, 2011 Let me be very sincere

Review of. Financial Crises, Liquidity, and the International Monetary System by Jean Tirole. Published by Princeton University Press in 2002

Review of Financial Crises, Liquidity, and the International Monetary System by Jean Tirole Published by Princeton University Press in 2002 Reviewer: Franklin Allen, Finance Department, Wharton School,

Review of Financial Crises, Liquidity, and the International Monetary System by Jean Tirole Published by Princeton University Press in 2002 Reviewer: Franklin Allen, Finance Department, Wharton School,

Suggested Solutions to Problem Set 4

Department of Economics University of California, Berkeley Spring 2006 Economics 182 Suggested Solutions to Problem Set 4 Problem 1 : True, False, Uncertain (a) False or Uncertain. In first generation

Department of Economics University of California, Berkeley Spring 2006 Economics 182 Suggested Solutions to Problem Set 4 Problem 1 : True, False, Uncertain (a) False or Uncertain. In first generation

Rutgers University Spring Econ 336 International Balance of Payments Professor Roberto Chang. Problem Set 5. Deadline: April 30th

Rutgers University Spring 2012 Name: Econ 336 International Balance of Payments Professor Roberto Chang Problem Set 5. Deadline: April 30th 1. If the marginal propensity to consume for a nation is 0.8,

Rutgers University Spring 2012 Name: Econ 336 International Balance of Payments Professor Roberto Chang Problem Set 5. Deadline: April 30th 1. If the marginal propensity to consume for a nation is 0.8,

Discussion of Bacchetta & Benhima paper The Demand for Liquid Assets and International Capital Flows

Discussion of Bacchetta & Benhima paper The Demand for Liquid Assets and International Capital Flows Marcel Fratzscher European Central Bank Conference Financial Globalization: Shifting Balances Banco

Discussion of Bacchetta & Benhima paper The Demand for Liquid Assets and International Capital Flows Marcel Fratzscher European Central Bank Conference Financial Globalization: Shifting Balances Banco

Chapter 18. The International Financial System Intervention in the Foreign Exchange Market

Chapter 18 The International Financial System 18.1 Intervention in the Foreign Exchange Market 1) A central bank of domestic currency and corresponding of foreign assets in the foreign exchange market

Chapter 18 The International Financial System 18.1 Intervention in the Foreign Exchange Market 1) A central bank of domestic currency and corresponding of foreign assets in the foreign exchange market

Why Currency Mismatches Matter

2 Why Currency Mismatches Matter Earlier financial crises provide ample evidence of the role currency mismatches have played in them. Consider the Asian financial crisis of 1997 98. As shown in table 2.1,

2 Why Currency Mismatches Matter Earlier financial crises provide ample evidence of the role currency mismatches have played in them. Consider the Asian financial crisis of 1997 98. As shown in table 2.1,

Understanding the World Economy Final Exam Indicative answers

Nicolas Coeurdacier Master Economics & Business Spring 2017 Understanding the World Economy Final Exam Indicative answers I. Multiple choice [50 points = 2 per question] It is a multiple choice questionnaire.

Nicolas Coeurdacier Master Economics & Business Spring 2017 Understanding the World Economy Final Exam Indicative answers I. Multiple choice [50 points = 2 per question] It is a multiple choice questionnaire.

The Financial System. Sherif Khalifa. Sherif Khalifa () The Financial System 1 / 52

The Financial System 1 / 52") The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 52 Financial System Definition The financial system consists of those institutions in the economy that matches saving with

The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 52 Financial System Definition The financial system consists of those institutions in the economy that matches saving with

From boom to bust and back again

From boom to bust and back again The financial crisis and the recent recovery in Iceland The Finnish Academy in Stockholm 25 August 2017 Thórarinn G. Pétursson Chief Economist Central Bank of Iceland The

From boom to bust and back again The financial crisis and the recent recovery in Iceland The Finnish Academy in Stockholm 25 August 2017 Thórarinn G. Pétursson Chief Economist Central Bank of Iceland The

Financial Crises and Debt Overhangs: Some Reflections

Financial Crises and Debt Overhangs: Some Reflections Carmen M. Reinhart Peterson Institute for International Economics NBER and CEPR InterAmerican Development Bank April 18, 2012, Washington DC Reinhart

Financial Crises and Debt Overhangs: Some Reflections Carmen M. Reinhart Peterson Institute for International Economics NBER and CEPR InterAmerican Development Bank April 18, 2012, Washington DC Reinhart

Are BRIC countries currencies to play. a dominant role in the system? A Brazilian perception

Are BRIC countries currencies to play The Policy of International Reserves a dominant role in the system? Accumulation: Lessons from the A Brazilian perception Crisis (Brazil s Perspective) Carlos Hamilton

Are BRIC countries currencies to play The Policy of International Reserves a dominant role in the system? Accumulation: Lessons from the A Brazilian perception Crisis (Brazil s Perspective) Carlos Hamilton

The Financial System. Sherif Khalifa. Sherif Khalifa () The Financial System 1 / 55

The Financial System 1 / 55") The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 55 The financial system consists of those institutions in the economy that matches saving with investment. The financial system

The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 55 The financial system consists of those institutions in the economy that matches saving with investment. The financial system

Federal Reserve System/IMF/World Bank. Seminar for Senior Bank Supervisors October 19 30, David S. Hoelscher

Federal Reserve System/IMF/World Bank Seminar for Senior Bank Supervisors October 19 30, 2009 David S. Hoelscher Money and Capital Markets Department International Monetary Fund Typology of Crises Type

Federal Reserve System/IMF/World Bank Seminar for Senior Bank Supervisors October 19 30, 2009 David S. Hoelscher Money and Capital Markets Department International Monetary Fund Typology of Crises Type

Government Intervention during the Asian Crisis

Government Intervention during the Asian Crisis From 990 to 997, Asian countries achieved higher economic growth than any other countries. They were viewed as models for advances in technology and economic

Government Intervention during the Asian Crisis From 990 to 997, Asian countries achieved higher economic growth than any other countries. They were viewed as models for advances in technology and economic

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 18 The International Financial System

Chapter 18 The International Financial System") Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 18 The International Financial System 18.1 Intervention in the Foreign Exchange Market 1) A central bank of domestic currency and corresponding

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 18 The International Financial System 18.1 Intervention in the Foreign Exchange Market 1) A central bank of domestic currency and corresponding

Xtrackers MSCI All World ex US High Dividend Yield Equity ETF

Summary Prospectus September 28, 2018 Ticker: HDAW Stock Exchange: NYSE Arca, Inc. Before you invest, you may wish to review the Fund s prospectus, which contains more information about the Fund and its

Summary Prospectus September 28, 2018 Ticker: HDAW Stock Exchange: NYSE Arca, Inc. Before you invest, you may wish to review the Fund s prospectus, which contains more information about the Fund and its

Comments of Exchange Rate Management and Crisis Susceptibility: A Reassessment

14TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 7 8, 2013 Comments of Exchange Rate Management and Crisis Susceptibility: A Reassessment Jeffrey Frankel Harvard University Paper presented at the

14TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 7 8, 2013 Comments of Exchange Rate Management and Crisis Susceptibility: A Reassessment Jeffrey Frankel Harvard University Paper presented at the

The Open Economy Revisited: the Exchange-Rate Regime

C H A P T E R 12 : the Mundell-Fleming Model and the Exchange-Rate Regime MACROECONOMICS SIXTH EDITION N. GREGORY MANKIW PowerPoint Slides by Ron Cronovich 2008 Worth Publishers, all rights reserved In

C H A P T E R 12 : the Mundell-Fleming Model and the Exchange-Rate Regime MACROECONOMICS SIXTH EDITION N. GREGORY MANKIW PowerPoint Slides by Ron Cronovich 2008 Worth Publishers, all rights reserved In

Acadian Emerging Markets Debt Fund

Click here to view the fund s statutory prospectus or statement of additional information The Advisors Inner Circle Fund Acadian Emerging Markets Debt Fund Summary Prospectus March 1, 2015 Ticker: Institutional

Click here to view the fund s statutory prospectus or statement of additional information The Advisors Inner Circle Fund Acadian Emerging Markets Debt Fund Summary Prospectus March 1, 2015 Ticker: Institutional

Argentina s Challenges and Opportunities: Reasons for (Sober and Realistic) Optimism

Optimism") Argentina s Challenges and Opportunities: Reasons for (Sober and Realistic) Optimism Eugenio Diaz Bonilla Executive Director for Argentina and Haiti Inter American Development Bank Recent History Argentina:

Argentina s Challenges and Opportunities: Reasons for (Sober and Realistic) Optimism Eugenio Diaz Bonilla Executive Director for Argentina and Haiti Inter American Development Bank Recent History Argentina:

The fiscal adjustment after the crisis in Argentina

65 The fiscal adjustment after the 2001-02 crisis in Argentina 1 Mario Damill, Roberto Frenkel, and Martín Rapetti After the crisis of the convertibility regime, Argentina experienced a significant adjustment

65 The fiscal adjustment after the 2001-02 crisis in Argentina 1 Mario Damill, Roberto Frenkel, and Martín Rapetti After the crisis of the convertibility regime, Argentina experienced a significant adjustment

The International Monetary System

INTERNATIONAL FINANCIAL MANAGEMENT Fourth Edition EUN / RESNICK The International Monetary System 2 Chapter Two INTERNATIONAL Chapter Objective: FINANCIAL MANAGEMENT This chapter serves to introduce the

INTERNATIONAL FINANCIAL MANAGEMENT Fourth Edition EUN / RESNICK The International Monetary System 2 Chapter Two INTERNATIONAL Chapter Objective: FINANCIAL MANAGEMENT This chapter serves to introduce the

Overview: Financial Stability and Systemic Risk

Overview: Financial Stability and Systemic Risk Bank Indonesia International Workshop and Seminar Central Bank Policy Mix: Issues, Challenges, and Policies Jakarta, 9-13 April 2018 Rajan Govil The views

Overview: Financial Stability and Systemic Risk Bank Indonesia International Workshop and Seminar Central Bank Policy Mix: Issues, Challenges, and Policies Jakarta, 9-13 April 2018 Rajan Govil The views

European Sovereign Crisis, what s the Outcome? Gonzalo Rengifo June 2012 Mexico

European Sovereign Crisis, what s the Outcome? Gonzalo Rengifo June 2012 Mexico 1 Current situation Eurozone (im)balances: a Small World Rising imbalances since the creation of the euro Eurozone current

European Sovereign Crisis, what s the Outcome? Gonzalo Rengifo June 2012 Mexico 1 Current situation Eurozone (im)balances: a Small World Rising imbalances since the creation of the euro Eurozone current

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics Eurozone s design failures: in a nutshell 1. Endogenous dynamics of booms and busts endemic in capitalism continued

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics Eurozone s design failures: in a nutshell 1. Endogenous dynamics of booms and busts endemic in capitalism continued

Chapter 13 The Open Economy Revisited: the Mundell-Fleming Model and the Exchange-Rate Regime

Chapter 13 The Open Economy Revisited: the Mundell-Fleming Model and the Exchange-Rate Regime Modified by Yun Wang Eco 3203 Intermediate Macroeconomics Florida International University Summer 2017 2016

Chapter 13 The Open Economy Revisited: the Mundell-Fleming Model and the Exchange-Rate Regime Modified by Yun Wang Eco 3203 Intermediate Macroeconomics Florida International University Summer 2017 2016

Development Policy Macro Management and Development Macro Stability and Growth: Case Study of Vietnam

Development Policy Macro Management and Development Macro Stability and Growth: Case Study of Vietnam James Riedel Outline: 1. How macro stability/instability is measured? 2. Inflation rate in Vietnam

Development Policy Macro Management and Development Macro Stability and Growth: Case Study of Vietnam James Riedel Outline: 1. How macro stability/instability is measured? 2. Inflation rate in Vietnam

Study Questions. Lecture 15 International Macroeconomics

Study Questions Page 1 of 5 Study Questions Lecture 15 International Macroeconomics Part 1: Multiple Choice Select the best answer of those given. 1. If the aggregate supply and demand curves in the figure

Study Questions Page 1 of 5 Study Questions Lecture 15 International Macroeconomics Part 1: Multiple Choice Select the best answer of those given. 1. If the aggregate supply and demand curves in the figure

MACROECONOMICS. The Open Economy Revisited: the Mundell-Fleming Model and the Exchange-Rate Regime MANKIW N. GREGORY

C H A P T E R 12 The Open Economy Revisited: the Mundell-Fleming Model and the Exchange-Rate Regime MACROECONOMICS N. GREGORY MANKIW 2007 Worth Publishers, all rights reserved SIXTH EDITION PowerPoint

C H A P T E R 12 The Open Economy Revisited: the Mundell-Fleming Model and the Exchange-Rate Regime MACROECONOMICS N. GREGORY MANKIW 2007 Worth Publishers, all rights reserved SIXTH EDITION PowerPoint

Money and Exchange rates

Macroeconomic policy Class Notes Money and Exchange rates Revised: December 13, 2011 Latest version available at www.fperri.net/teaching/macropolicyf11.htm So far we have learned that monetary policy can

Macroeconomic policy Class Notes Money and Exchange rates Revised: December 13, 2011 Latest version available at www.fperri.net/teaching/macropolicyf11.htm So far we have learned that monetary policy can

Global Financial Crisis. Econ 690 Spring 2019

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

Details of the changes to the Investment Policies and Revision of the Investment Restrictions on the underlying funds of:

Details of the changes to the Investment Policies and Revision of the Investment Restrictions on the underlying funds of: 1. J60 Templeton Emerging Markets 2. L05 Templeton Global Bond (EUR) 3. L06 Templeton

Details of the changes to the Investment Policies and Revision of the Investment Restrictions on the underlying funds of: 1. J60 Templeton Emerging Markets 2. L05 Templeton Global Bond (EUR) 3. L06 Templeton

POLICY PRESCRIPTIONS FOR EAST ASIA

POLICY PRESCRIPTIONS FOR EAST ASIA Masaru Yoshitomi* At the Asian Development Bank Institute in Tokyo, we recently produced policy recommendations about how to avoid another financial crisis and, if we

POLICY PRESCRIPTIONS FOR EAST ASIA Masaru Yoshitomi* At the Asian Development Bank Institute in Tokyo, we recently produced policy recommendations about how to avoid another financial crisis and, if we

Study Questions (with Answers) Lecture 15 International Macroeconomics

Lecture 15 International Macroeconomics") Study Questions (with Answers) Page 1 of 5 Study Questions (with Answers) Lecture 15 International Macroeconomics Part 1: Multiple Choice Select the best answer of those given. 1. If the aggregate supply

Study Questions (with Answers) Page 1 of 5 Study Questions (with Answers) Lecture 15 International Macroeconomics Part 1: Multiple Choice Select the best answer of those given. 1. If the aggregate supply

Chapter 24 CRISES IN EMERGING MARKETS

Chapter 24 CRISES IN EMERGING MARKETS The previous chapter extended the IS-LM-BP model to accommodate high capital mobility. Chapter 24 applies that model to the crises that beset some middle-income countries

Chapter 24 CRISES IN EMERGING MARKETS The previous chapter extended the IS-LM-BP model to accommodate high capital mobility. Chapter 24 applies that model to the crises that beset some middle-income countries

Business cycle fluctuations Part II

Understanding the World Economy Master in Economics and Business Business cycle fluctuations Part II Lecture 7 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 7: Business cycle fluctuations

Understanding the World Economy Master in Economics and Business Business cycle fluctuations Part II Lecture 7 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 7: Business cycle fluctuations

: Monetary Economics and the European Union. Lecture 8. Instructor: Prof Robert Hill. The Costs and Benefits of Monetary Union II

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

External Factors, Macro Policies and Growth in LAC: Is Performance that Good?

External Factors, Macro Policies and Growth in LAC: Is Performance that Good? Alejandro Izquierdo IADB Emerging Powers in Global Governance Conference Paris, July 6, 2007 (based on work with Ernesto Talvi)

External Factors, Macro Policies and Growth in LAC: Is Performance that Good? Alejandro Izquierdo IADB Emerging Powers in Global Governance Conference Paris, July 6, 2007 (based on work with Ernesto Talvi)

Econ 340. Recall Macro from Econ 102. Recall Macro from Econ 102. Recall Macro from Econ 102. Recall Macro from Econ 102

Econ 34 Lecture 5 International Macroeconomics Outline: International Macroeconomics Recall Macro from Econ 2 Aggregate Supply and Demand Policies Effects ON the Exchange Expansion Interest Rate Depreciation

Econ 34 Lecture 5 International Macroeconomics Outline: International Macroeconomics Recall Macro from Econ 2 Aggregate Supply and Demand Policies Effects ON the Exchange Expansion Interest Rate Depreciation

What could debt restructuring imply for the Eurozone? Adrian Cooper

What could debt restructuring imply for the Eurozone? Adrian Cooper acooper@oxfordeconomics.com June 2011 What could debt restructuring imply for the Eurozone? New stage in Eurozone debt crisis: first

What could debt restructuring imply for the Eurozone? Adrian Cooper acooper@oxfordeconomics.com June 2011 What could debt restructuring imply for the Eurozone? New stage in Eurozone debt crisis: first

Chapter 6. Government Influence on Exchange Rates. Lecture Outline

Chapter 6 Government Influence on Exchange Rates Lecture Outline Exchange Rate Systems Fixed Exchange Rate System Freely Floating Exchange Rate System Managed Float Exchange Rate System Pegged Exchange

Chapter 6 Government Influence on Exchange Rates Lecture Outline Exchange Rate Systems Fixed Exchange Rate System Freely Floating Exchange Rate System Managed Float Exchange Rate System Pegged Exchange

FINANCIAL SECTOR REFORM

FINANCIAL SECTOR REFORM BANGKOK, THAILAND NOVEMBER 24 DECEMBER 3, 2014 Bangkok December 01, 2014 Rajan Govil, Consultant This activity is supported by a grant from Japan. Outline Financial repression Financial

FINANCIAL SECTOR REFORM BANGKOK, THAILAND NOVEMBER 24 DECEMBER 3, 2014 Bangkok December 01, 2014 Rajan Govil, Consultant This activity is supported by a grant from Japan. Outline Financial repression Financial

The Trilemma: Insights and Limitations

The Trilemma: Insights and Limitations Menzie D. Chinn University of Wisconsin, Madison and NBER Universität Leipzig/Universität Duisburg Essen Conference on Exchange Rates, Monetary Policy and Financial

The Trilemma: Insights and Limitations Menzie D. Chinn University of Wisconsin, Madison and NBER Universität Leipzig/Universität Duisburg Essen Conference on Exchange Rates, Monetary Policy and Financial

Sovereign Risks and Financial Spillovers

Sovereign Risks and Financial Spillovers International Monetary Fund October 21 Roadmap What is the Outlook for Global Financial Stability? Sovereign Risks and Financial Fragilities Sovereign and Banking

Sovereign Risks and Financial Spillovers International Monetary Fund October 21 Roadmap What is the Outlook for Global Financial Stability? Sovereign Risks and Financial Fragilities Sovereign and Banking