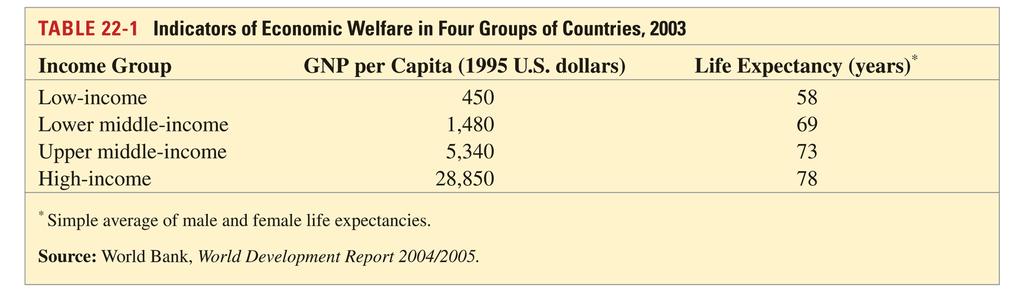

Rich and Poor. Indicators of Economic Welfare for 4 groups of countries, 2003 GNP per capita (1995 US$)

|

|

|

- Gladys Robertson

- 5 years ago

- Views:

Transcription

1 Rich and Poor Indicators of Economic Welfare for 4 groups of countries, 2003 GNP per capita (1995 US$) Life expectancy Low income Lower-middle income Upper-middle income High income Source: World Bank, World Development Report 2004/2005 Low income: most sub-saharan Africa, India, Pakistan Lower-middle income: China, former Soviet Union, Caribbean Upper-middle income: Brazil, Mexico, Saudi Arabia, Malaysia, South Africa, Czech Republic High income: US, France, Japan, Singapore, Kuwait 1

2 Rich and Poor (cont.) While some previously middle and low income countries economies have grown faster than high income countries, and thus have caught up with high income countries, others have languished. The income levels of high income countries and some middle income and low income countries have converged. But the some of the poorest countries have had the lowest growth rates. 2

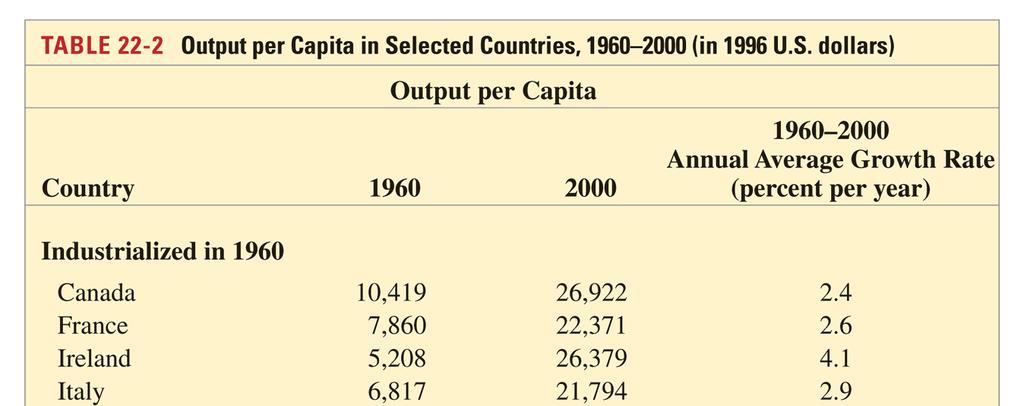

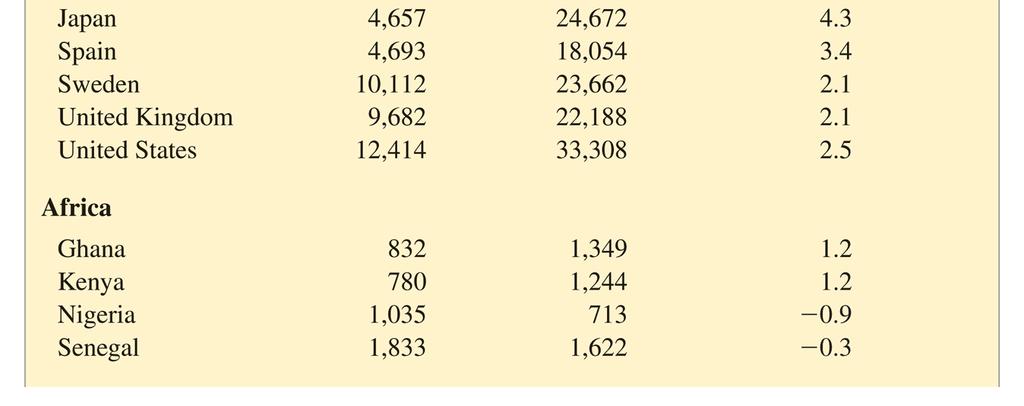

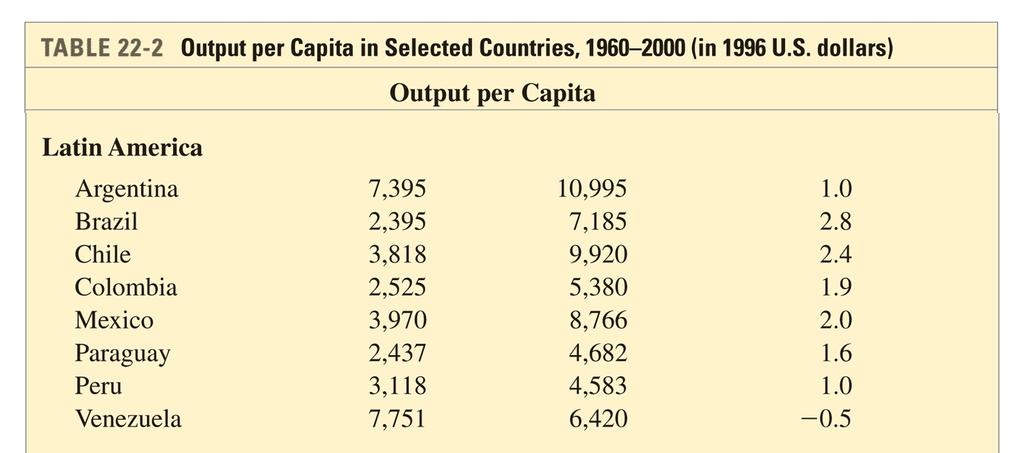

3 Rich and Poor (cont.) GDP per capita (1996 US $) annual growth rate Country average United States Canada Hong Kong Ireland Singapore Japan Sweden France United Kingdom Italy Spain Taiwan South Korea Argentina

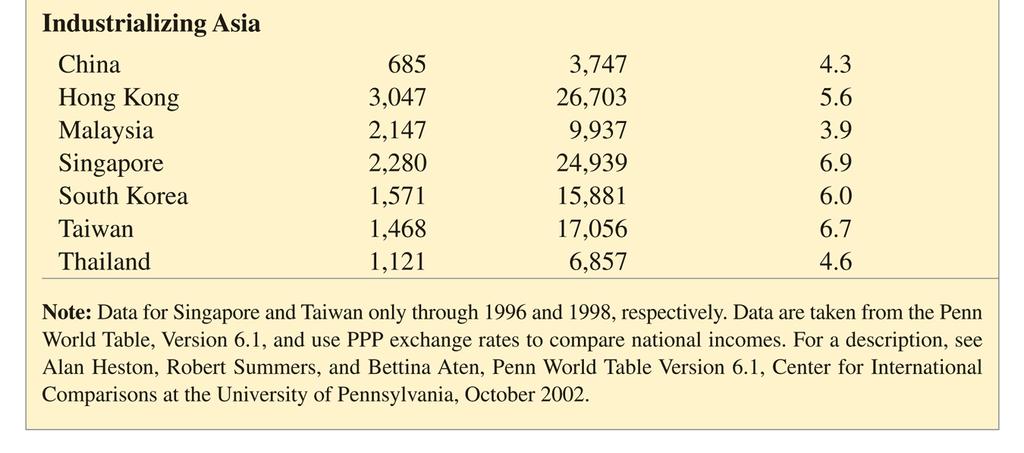

4 Rich and Poor (cont.) GDP per capita (1996 US $) annual growth rate Country average Malaysia Chile Mexico Brazil Thailand Venezuela Colombia Paraguay Peru China Senegal Ghana Kenya Nigeria Source: Alan Heston, Robert Summers and Bettina Aten, Penn World Table Version 6.1 4

5 Rich and Poor (cont.) Poor countries have not grown faster: growth rates relative to per capita GDP in

6 Characteristics of Poor Countries What causes poverty? A difficult question, but low income countries have at least some of following characteristics, which could contribute to poverty: 1. Government control of the economy Restrictions on trade Direct control of production in industries and a high level of government purchases relative to GNP Direct control of financial transactions Reduced competition reduces innovation; lack of market prices prevents efficient allocation of resources. 6

7 Characteristics of Poor Countries (cont.) 2. Unsustainable macroeconomic polices which cause high inflation and unstable output and employment If governments can not pay for debts through taxes, they can print money to finance debts. Seignoirage is paying for real goods and services by printing money. Seignoirage generally leads to high inflation. High inflation reduces the real value of debt that the government has to repay and acts as a tax on lenders. High and variable inflation is costly to society; unstable output and employment is also costly. 7

8 Characteristics of Poor Countries (cont.) 3. Lack of financial markets that allow transfer of funds from savers to borrowers 4. Weak enforcement of economic laws and regulations Weak enforcement of property rights makes investors less willing to engage in investment activities and makes savers less willing to lend to investors/borrowers. Weak enforcement of bankruptcy laws and loan contracts makes savers less willing to lend to borrowers/investors. Weak enforcement of tax laws makes collection of tax revenues more difficult, making seignoirage necessary (see 2) and makes tax evasion a problem (see 5). 8

9 Characteristics of Poor Countries (cont.) Weak of enforcement of banking and financial regulations (e.g., lack of examinations, asset restrictions, capital requirements) causes banks and firms to engage in risky or even fraudulent activities and makes savers less willing to lend to these institutions. A lack of monitoring causes a lack of transparency (a lack of information). Moral hazard: a hazard that a borrower (e.g., bank or firm) will engage in activities that are undesirable (e.g., risky investment, fraudulent activities) from the less informed lender s point of view. 9

10 Characteristics of Poor Countries (cont.) 5. A large underground economy relative to official GDP and a large amount of corruption Because of government control of the economy (see 1) and weak enforcement of economic laws and regulations (see 4), underground economies and corruption flourish. 6. Low measures of literacy, numeracy, and other measures of education and training: low levels of human capital Human capital makes workers more productive. 10

11 Characteristics of Poor Countries (cont.) 11

12 Borrowing and Debt in Developing Economies Another common characteristic for many middle income and low income countries is that they have borrowed extensively from foreign countries. Financial capital flows from foreign countries are able to finance investment projects, eventually leading to higher production and consumption. But some investment projects fail and other borrowed funds are used primarily for consumption purposes. Some countries have defaulted on their foreign debts when the domestic economy stagnated or during financial crises. 12

13 Borrowing and Debt in Developing Economies (cont.) national saving investment = the current account where the current account is approximately equal to the value of exports minus the value of imports Countries with national saving less than domestic investment will have a financial capital inflows and negative current account (a trade deficit). 13

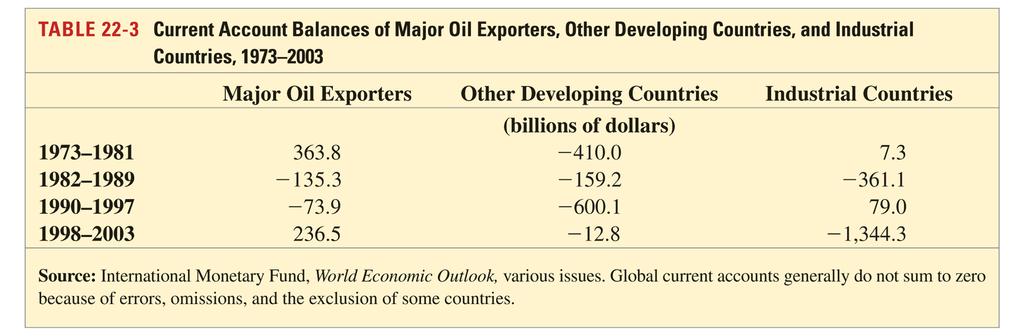

14 Borrowing and Debt in Developing Economies (cont.) Current account balances of major oil exporters, other developing countries and high income countries, in billions of US$ Major oil exporters Other developing countries High income countries Source: IMF, World Economic Outlook, various issues 14

15 Borrowing and Debt in Developing Economies (cont.) A financial crisis may involve 1. a debt crisis: an inability to repay government debt or private sector debt. 2. a balance of payments crisis under a fixed exchange rate system. 3. a banking crisis: bankruptcy and other problems for private sector banks. 15

16 Borrowing and Debt in Developing Economies (cont.) A debt crisis in which governments default on their debt can be a self-fulfilling mechanism. Fear of default reduces financial capital inflows and increases financial capital outflows (capital flight), decreasing investment and increasing interest rates, leading to low aggregate demand, output and income. Financial capital outflows must be matched with an increase in net exports or a decrease in official international reserves in order to pay people who desire foreign funds. 16

17 Borrowing and Debt in Developing Economies (cont.) Otherwise, the country can not afford to pay people who want to remove their funds from the domestic economy. The domestic government may have no choice but to default on its sovereign debt when it comes due and investors are unwilling to re-invest. 17

18 Borrowing and Debt in Developing Economies (cont.) In general, a debt crisis causes low income and high interest rates, which makes sovereign (government) and private sector debt even harder to repay. High interest rates cause high interest payments for both the government and the private sector. Low income causes low tax revenue for the government. Low income makes private loans harder to repay: the default rate for private banks increases, which may lead to increased bankruptcy. 18

19 Borrowing and Debt in Developing Economies (cont.) If the central bank tries to fix the exchange rate, a balance of payment crisis may result with a debt crisis. Official international reserves may quickly be depleted, forcing the central bank to abandon the fixed exchange rate. A banking crisis may result with a debt crisis. High default rates may increase bankruptcy. If depositors fear bankruptcy due to possible devaluation of the currency or default on government debt (assets for banks), then they will quickly withdraw funds (and possibly purchase foreign assets), leading to bankruptcy. 19

20 Borrowing and Debt in Developing Economies (cont.) A debt crisis, a balance of payments crisis and a banking crisis can occur together, and each can make the other worse. Each can cause aggregate demand, output and employment to fall (further). If people expect a default on sovereign debt, a currency devaluation, or bankruptcy of private banks, each can occur, and each can lead to another. 20

21 The Problem of Original Sin When developing economies borrow in international financial capital markets, the debt is almost always denominated in US$, yen, euros: original sin. The debt of the US, Japan and European countries is also mostly denominated in their respective currencies. When a depreciation of domestic currencies occurs in the US, Japan or European countries, liabilities (debt) which are denominated in domestic currencies do not increase, but the value of foreign assets does increase. A devaluation of the domestic currency causes an increase in net foreign wealth. 21

22 The Problem of Original Sin (cont.) When a depreciation/devaluation of domestic currencies occurs in developing economies, the value of their liabilities (debt) rises because their liabilities are denominated in foreign currencies. A fall in demand for domestic products causes a depreciation/devaluation of the domestic currency and causes a decrease in net foreign wealth if assets are denominated in domestic currencies. A situation of negative insurance against a fall in aggregate demand. 22

23 Types of Financial Capital 1. Bond finance: government or commercial bonds are sold to private foreign citizens. 2. Bank finance: commercial banks lend to foreign governments or foreign businesses. 3. Official lending: the World Bank or Inter-American Development Bank or other official agencies lend to governments. Sometimes these loans are made on a concessional or favorable basis, in which the interest rate is low. 23

24 Types of Financial Capital (cont.) 4. Foreign direct investment: a foreign firm directly acquires or expands operations in a subsidiary firm. A purchase by Ford of a subsidiary firm in Mexico is classified as foreign direct investment. 5. Portfolio equity investment: a foreign investor purchases equity (stock) for his portfolio. Privatization of government owned firms has occurred in many countries, and private investors have bought stock in such firms. 24

25 Types of Financial Capital (cont.) Debt finance includes bond finance, bank finance and official lending. Equity finance includes direct investment and portfolio equity investment. While debt finance requires fixed payments regardless of the state of the economy, the value of equity finance fluctuates depending on aggregate demand and output. 25

26 Latin American Financial Crises In the 1980s, high interest rates and an appreciation of the US dollar, caused the burden of dollar denominated debts in Argentina, Mexico, Brazil and Chile to increase drastically. A worldwide recession and a fall in many commodity prices also hurt export sectors in these countries. In August 1982, Mexico announced that it could not repay its debts, mostly to private banks. 26

27 Latin American Financial Crises (cont.) The US government insisted that the private banks reschedule the debts, and in 1989 Mexico was able to achieve: a reduction in the interest rate, an extension of the repayment period a reduction in the principal by 12% Brazil, Argentina and other countries were also allowed to reschedule their debts with private banks after they defaulted. 27

28 Latin American Financial Crises (cont.) The Mexican government implemented several reforms due to the crisis. Starting in 1987, It reduced government deficits. It reduced production in the public sector (including banking) by privatizing industries. It reduced barriers to trade. It maintained an adjustable fixed exchange rate ( crawling peg ) until 1994 to help curb inflation. 28

29 Latin American Financial Crises (cont.) It extended credit to newly privatized banks with loan losses. Losses were a problem due to weak enforcement or lack of accounting standards like asset restrictions and capital requirements. Political instability and the banks loan defaults contributed to another crisis in 1994, after which the Mexican government allowed the value of the peso to fluctuate. 29

30 Latin American Financial Crises (cont.) Staring in 1991, Argentina carried out similar reforms: It reduced government deficits. It reduced production in the public sector by privatizing industries. It reduced barriers to trade. It enacted tax reforms to increase tax revenues. It enacted the Convertibility Law, which required that each peso be backed with 1 US dollar, and it fixed the exchange rate to 1 peso per US dollar. 30

31 Latin American Financial Crises (cont.) Because the central was not allowed to print more pesos without have more dollar reserves, inflation slowed dramatically. Yet inflation was about 5% per annum, faster than US inflation, so that the price/value of Argentinean goods appreciated relative to US and other foreign goods. Due to the relatively rapid peso price increases, markets began to speculate about a peso devaluation. A global recession in 2001 further reduced the demand for Argentinean goods and currency. 31

32 Latin American Financial Crises (cont.) Maintaining the fixed exchange rate was costly because high interest rates were needed to attract investors, further reducing investment and consumption demand, output and employment. As incomes fell, tax revenues fell and government spending rose, contributing to further peso inflation. 32

33 Latin American Financial Crises (cont.) Argentina tried to uphold the fixed exchange rate, but the government devalued the peso in 2001 and shortly thereafter allowed its value to fluctuate. It also defaulted on its debt in December 2001 because of the unwillingness of investors to reinvest when the debt was due. 33

34 Latin American Financial Crises (cont.) Brazil carried out similar reforms in the 1980s and 1990s: It reduced production in the public sector by privatizing industries. It reduced barriers to trade. It enacted tax reforms to increase tax revenues. It created fixed the exchange rate to 1 real per US dollar. But government deficits remained high. 34

35 Latin American Financial Crises (cont.) High government deficits lead to inflation and speculation about a devaluation of the real. The government did devalue the real in 1999, but a widespread banking crisis was avoided because Brazilian banks and firms did not borrow extensively in dollar denominated assets. 35

36 Latin American Financial Crises (cont.) Chile suffered a recession and financial crisis in the 1980s, but thereafter enacted stringent financial regulations for banks. removed the guarantee from the central bank that private banks would be bailed out if their loans failed. imposed financial capital controls on short term debt, so that funds could not be quickly withdrawn during a financial panic. granted the central bank independence from fiscal authorities, allowing slower money supply growth. Chile avoided a financial crisis in the 1990s. 36

37 East Asian Financial Crises Before the 1990s, Indonesia, Korea, Malaysia, Philippines, and Thailand relied mostly on domestic saving to finance investment. But afterwards, foreign financial capital financed much of investment, and current account balances turned negative. 37

38 East Asian Financial Crises (cont.) 38

39 East Asian Financial Crises (cont.) Despite the rapid economic growth in East Asia between , growth was predicted to slow as economies caught up with Western countries. Most of the East Asian growth during this period is attributed to an increase in physical capital and an increase in education. Returns to physical capital and education are diminishing, as more physical capital was built and as more people acquired more education and training, each increase became less productive. The economic growth was predicted to slow after the rapid increases in early generations. 39

40 East Asian Financial Crises (cont.) More directly related to the East Asian crises are issues related to economic laws and regulations: 1. Weak of enforcement of financial regulations and a lack of monitoring caused firms, banks and borrowers to engage in risky or even fraudulent activities: moral hazard. Ties between businesses and banks on one hand and government regulators on the other hand lead to some risky investments. 40

41 East Asian Financial Crises (cont.) 2. Non-existent or weakly enforced bankruptcy laws and loan contracts caused problems after the crisis started. Financially troubled firms stopped paying their debts, and they could not operate because no one would lend more until previous debts were paid. But creditors lacked the legal means to confiscate assets or restructure firms to make them productive again. 41

42 East Asian Financial Crises (cont.) The East Asian crisis started in Thailand in 1997, but quickly spread to other countries. A fall in real estate prices, and then stock prices weakened aggregate demand and output in Thailand. A fall in aggregate demand in Japan, a major export market, also contributed to the economic slowdown. Speculation about a devaluation in the value of the baht occurred, and in July 1997 the government devalued the baht slightly, but this only invited further speculation. Malaysia, Indonesia, Korea, and the Philippines soon faced speculations about the value of their currencies. 42

43 East Asian Financial Crises (cont.) Most debts of banks and firms were denominated in US dollars, so that devaluations of domestic currencies would make the burden of the debts in domestic currency increase. Bankruptcy and a banking crisis would have resulted. To maintain fixed exchange rates would have required high interest rates and a reduction in government deficits, leading to a reduction in aggregate demand, output and employment. This would have also lead to widespread default on debts and a banking crisis. 43

44 East Asian Financial Crises (cont.) All of the effected economies except Malaysia turned to the IMF for loans to address the balance of payments crises and to maintain the value of the domestic currencies. The loans were conditional on increased interest rates (reduced money supply growth), reduced budget deficits, and reforms in banking regulation and bankruptcy laws. Malaysia instead imposed financial capital controls so that it could increase its money supply (and lower interest rates), increase government purchases, and still try to maintain the value of the ringgit. 44

Due to decreased consumption and investment that occurred with decreased output, income and")

45 East Asian Financial Crises (cont.) Due to decreased consumption and investment that occurred with decreased output, income and employment, imports fell and the current account increased after

46 Russia s Financial Crisis After liberalization in 1991, Russia s economic laws were weakly enforced or non-existent. There was weak enforcement of banking regulations, tax laws, property rights, loan contracts and bankruptcy laws. Financial markets were not well established. Corruption and crime became growing problems. Because of a lack of tax revenue, the government financed spending by seignoirage. Due to unsustainable seignoirage, interest rates rose on government debt to reflect high inflation and the risk of default. 46

47 Russia s Financial Crisis (cont.) The IMF offered loans of foreign reserves to try to support the fixed exchange rate conditional on reforms. But in 1998, Russia devalued the ruble and defaulted on its debt and froze financial capital flows. Without international financial capital for investment, output fell in 1998 but recovered thereafter, partially helped by rising oil prices. Inflation rose in 1998 and 1999 but fell thereafter. 47

48 Russia s Financial Crisis (cont.) Real output growth Inflation rate Russia s real output growth and inflation, % -14.5% -8.7% -12.7% -4.1% -3.4% 1.4% -5.3% 6.3% 6.8% 92.7% % 878.8% 307.5% 198.0% 47.7% 14.8% 27.7% 85.7% 18.0% Source: IMF, World Economic Outlook 48

49 Currency Boards and Dollarization A currency board is a monetary policy where the money supply is entirely backed by foreign currency, and where the central bank is prevented from holding domestic assets. The central bank may not increase the domestic money supply (by buying government bonds). This policy restrains inflation and government deficits. The central bank also can not run out of foreign reserves to support a fixed exchange rate. Argentina enacted a currency board under the 1991 Convertibility Law. 49

50 Currency Boards and Dollarization (cont.) But a currency board can be restrictive (more than a regular fixed exchange rate system). Since the central bank may not acquire domestic assets, it can not lend currency to domestic banks during financial crisis: no lender of last resort policy or seignoirage. Dollarization is a monetary policy that replaces the domestic currency in circulation with US dollars. In effect, control of domestic money supply, interest rates and inflation is given the Federal Reserve. A lender of last resort policy and the possibility of seignoirage for domestic policy makers are eliminated. 50

51 Currency Boards and Dollarization (cont.) Argentina ultimately abandoned its currency board because the cost was too high: high interest rates and a reduction in prices were needed to sustain it. The government was unwilling to reduce its deficit to reduce aggregate demand, output, employment and prices. Labor unions kept wages (and output prices) from falling. Weak enforcement of financial regulations lead to risky loans, leading to troubled banks when output, income and employment fell. Under the currency board, the central bank was not allowed to increase the money supply or loan to troubled banks. 51

52 Lessons of Crises 1. Fixing the exchange rate has risks: governments desire to fix exchange rates to provide stability in the export and import sectors, but the price to pay may be high interest rates or high unemployment. High inflation (caused by government deficits or increases in the money supply) or a drop in demand for domestic exports leads to an over-valued currency and pressure for devaluation. Given pressure for devaluation, commitment to a fixed exchange rate usually means high interest rates (a reduction in the money supply) and a reduction in domestic prices. 52

53 Lessons of Crises (cont.) Prices are reduced through a reduction in government deficits, leading to a reduction in aggregate demand, output and employment. A fixed currency may encourage banks and firms to borrow in foreign currencies, but a devaluation will cause an increase in the burden of this debt and may lead to a banking crisis and bankruptcy. Commitment a fixed exchange rate can cause a financial crisis to worsen: high interest rates make loans for banks and firms harder to repay, and the central bank can not freely print money to give to troubled banks (can not act as a lender of last resort). 53

54 Lessons of Crises (cont.) 2. Weak enforcement of financial regulations can lead to risky investments and a banking crisis when a currency crisis erupts or when a fall in output, income and employment occurs. 3. Liberalizing financial capital flows without implementing sound financial regulations can lead to financial capital flight when risky loans or other risky assets lose value during a recession. 54

55 Lessons of Crises (cont.) 4. The importance of expectations: even healthy economies are vulnerable to crises when expectations change. Expectations about an economy often change when other economies suffer from adverse events. International crises may result from contagion: an adverse event in one country leads to a similar event in other countries. 55

56 Potential Reforms: Policy Trade-offs Countries face trade-offs when trying to achieve the following goals: exchange rate stability financial capital mobility autonomous monetary policy devoted to domestic goals Generally, countries can attain only 2 of the 3 goals, and as financial capital has become more mobile, maintaining a fixed exchange with an autonomous monetary policy has been difficult. 56

57 Potential Reforms: Policy Tradeoffs (cont.) 57

58 Potential Reforms Preventative measures: 1. Better monitoring and more transparency: more information for the public allows investors to make sound financial decisions in good and bad times 2. Stronger enforcement of financial regulations: reduces moral hazard 3. Deposit insurance and reserve requirements 4. Increased equity finance relative to debt finance 5. Increased credit for troubled banks through the central bank or the IMF? 58

59 Potential Reforms (cont.) Reforms for after a crisis occurs: 1. Bankruptcy procedures for default on sovereign debt and improved bankruptcy law for private sector debt. 2. A bigger or smaller role for the IMF as a lender of last resort? (See 5 above.) Moral hazard versus benefit of insurance before and after a crisis occurs. 59

60 Geography, Human Capital What causes poverty? and Institutions A difficult question, but economists argue if geography or human capital is more important in influencing economic and political institutions, and ultimately poverty. 60

61 Geography, Human Capital and Institutions (cont.) Geography matters: 1. International trade is important for growth, and ocean harbors and a lack of geographical barriers foster trade with foreign markets. Landlocked and mountainous regions are predicted to be poor. 2. Also, geography determined institutions, which may play a role in development. Geography determined whether Westerners established property rights and long-term investment in colonies, which in turn influenced economic growth. 61

62 Geography, Human Capital and Institutions (cont.) Geography determined whether Westerners died from malaria and other diseases. With high mortality rates, they established practices and institutions based on quick plunder of colonies resources, rather than institutions favoring long-term economic growth. Plunder lead to property confiscation and corruption, even after political independence from Westerners. Geography also determined whether local economies were better for plantation agriculture, which resulted in income inequalities and political inequalities. Under this system, equal property rights were not established, hindering long-term economic growth. 62

63 Geography, Human Capital and Institutions (cont.) Human capital matters: 1. As a population becomes more literate, numerate and educated, economic and political institutions evolve to foster long-term economic growth. Rather than geography, Western colonization and plantation agriculture; the amount of education and other forms of human capital determine the existence or lack of property rights, financial markets, international trade and other institutions that encourage economic growth. 63

64 Summary 1. Some countries have grown rapidly since 1960, but others have stagnated and remained poor. 2. Many poor countries have extensive government control of the economy, unsustainable fiscal and monetary policies, lack of financial markets, weak enforcement of economic laws, a large amount of corruption and low levels of education. 64

65 Summary (cont.) 3. Many developing economies have borrowed heavily from international capital markets, and some have suffered from periodic sovereign debt, balance of payments and banking crises. 4. Sovereign debt, balance of payments and banking crises can be self-fulfilling, and each crisis can lead to another within a country or in another country. 5. Original sin refers to the fact that developing economies can not borrow in their domestic currencies. 65

66 Summary (cont.) 6. A currency board fixes exchange rates by backing up each unit of domestic currency with foreign reserves. 7. Dollarization is the replacement of domestic currency in circulation with US dollars. 8. Fixing exchange rates may lead to financial crises if the country is unwilling restrict monetary and fiscal policies. 66

67 Summary (cont.) 9. Weak enforcement of financial regulations causes a moral hazard and may lead to a banking crisis, especially with free movement of financial capital. 10. Geography and human capital may influence economic and political institutions, which in turn may affect long-term economic growth. 67

68 68

69 69

70 70

71 71

72 72

73 73

Chapter 22 (11) Developing Countries: Growth, Crisis, and Reform

Developing Countries: Growth, Crisis, and Reform") Chapter 22 (11) Developing Countries: Growth, Crisis, and Reform Preview Snapshots of rich and poor countries Characteristics of poor countries Borrowing and debt in poor and middle-income economies The

Chapter 22 (11) Developing Countries: Growth, Crisis, and Reform Preview Snapshots of rich and poor countries Characteristics of poor countries Borrowing and debt in poor and middle-income economies The

Developing Countries Chapter 22

Developing Countries Chapter 22 1. Growth 2. Borrowing and Debt 3. Money-financed deficits and crises 4. Other crises 5. Currency board 6. International financial architecture for the future 1 Growth 1.1

Developing Countries Chapter 22 1. Growth 2. Borrowing and Debt 3. Money-financed deficits and crises 4. Other crises 5. Currency board 6. International financial architecture for the future 1 Growth 1.1

Prepared by Iordanis Petsas To Accompany. by Paul R. Krugman and Maurice Obstfeld

Chapter 22 Developing Countries: Growth, Crisis, and Reform Prepared by Iordanis Petsas To Accompany International Economics: Theory and Policy, Sixth Edition by Paul R. Krugman and Maurice Obstfeld Chapter

Chapter 22 Developing Countries: Growth, Crisis, and Reform Prepared by Iordanis Petsas To Accompany International Economics: Theory and Policy, Sixth Edition by Paul R. Krugman and Maurice Obstfeld Chapter

East Asia Crisis of Econ October 8, Team 5 Bryan Darch Svend Egholm Paramdeep Singh Sarah Zullo

East Asia Crisis of 1997 Econ 7920 October 8, 2008 Team 5 Bryan Darch Svend Egholm Paramdeep Singh Sarah Zullo The East Asian currency crisis of 1997 caused severe distress for the countries of East Asia

East Asia Crisis of 1997 Econ 7920 October 8, 2008 Team 5 Bryan Darch Svend Egholm Paramdeep Singh Sarah Zullo The East Asian currency crisis of 1997 caused severe distress for the countries of East Asia

Asian Financial Crisis. Jianing Li/Wei Ye/Jingyan Zhang 2018/11/29

Asian Financial Crisis Jianing Li/Wei Ye/Jingyan Zhang 2018/11/29 Causes--Current account deficit 1. Liberalization of capital markets. 2. Large capital inflow due to the interest rates fall in developed

Asian Financial Crisis Jianing Li/Wei Ye/Jingyan Zhang 2018/11/29 Causes--Current account deficit 1. Liberalization of capital markets. 2. Large capital inflow due to the interest rates fall in developed

Chapter 10. Preview. Introduction. Trade Policy in Developing Countries

Chapter 10 Trade Policy in Developing Countries Slides prepared by Thomas Bishop Copyright 2009 Pearson Addison-Wesley. All rights reserved. Preview Import substituting industrialization Trade liberalization

Chapter 10 Trade Policy in Developing Countries Slides prepared by Thomas Bishop Copyright 2009 Pearson Addison-Wesley. All rights reserved. Preview Import substituting industrialization Trade liberalization

Preview. Chapter 10. Introduction. Introduction

Chapter 10 Trade Policy in Developing Countries Preview Import substituting industrialization Trade liberalization since 1985 Export oriented industrialization Slides prepared by Thomas Bishop Copyright

Chapter 10 Trade Policy in Developing Countries Preview Import substituting industrialization Trade liberalization since 1985 Export oriented industrialization Slides prepared by Thomas Bishop Copyright

What is Wrong with Market-Oriented Policies?

June 2003 In 1999, SigmaBleyzer initiated the International Private Capital Task Force (IPCTF) in Ukraine. Its objective was to benchmark transition economies to identify best practices in government policies

June 2003 In 1999, SigmaBleyzer initiated the International Private Capital Task Force (IPCTF) in Ukraine. Its objective was to benchmark transition economies to identify best practices in government policies

POLI 12D: International Relations Sections 1, 6

POLI 12D: International Relations Sections 1, 6 Spring 2017 TA: Clara Suong Chapter 9 International Monetary Relations 9 INTERNATIONAL MONETARY RELATIONS Core of the Analysis National Monetary Order Fixed

POLI 12D: International Relations Sections 1, 6 Spring 2017 TA: Clara Suong Chapter 9 International Monetary Relations 9 INTERNATIONAL MONETARY RELATIONS Core of the Analysis National Monetary Order Fixed

Currency Crises: Theory and Evidence

Currency Crises: Theory and Evidence Lecture 3 IME LIUC 2008 1 The most dramatic form of exchange rate volatility is a currency crisis when an exchange rate depreciates substantially in a short period.

Currency Crises: Theory and Evidence Lecture 3 IME LIUC 2008 1 The most dramatic form of exchange rate volatility is a currency crisis when an exchange rate depreciates substantially in a short period.

Government Intervention during the Asian Crisis

Government Intervention during the Asian Crisis From 990 to 997, Asian countries achieved higher economic growth than any other countries. They were viewed as models for advances in technology and economic

Government Intervention during the Asian Crisis From 990 to 997, Asian countries achieved higher economic growth than any other countries. They were viewed as models for advances in technology and economic

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 18 The International Financial System

Chapter 18 The International Financial System") Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 18 The International Financial System 18.1 Intervention in the Foreign Exchange Market 1) A central bank of domestic currency and corresponding

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 18 The International Financial System 18.1 Intervention in the Foreign Exchange Market 1) A central bank of domestic currency and corresponding

The Asian Financial Crisis

The Asian Financial Crisis The Asian crisis 1996 Miraculous growth in EA But some signs of worsening current accounts in Korea and Thailand Signs of worsening financial institutions in Thailand 1997 January

The Asian Financial Crisis The Asian crisis 1996 Miraculous growth in EA But some signs of worsening current accounts in Korea and Thailand Signs of worsening financial institutions in Thailand 1997 January

Global Construction 2030 Expo EDIFICA 2017 Santiago Chile. 4-6 October 2017

Global Construction 2030 Expo EDIFICA 2017 Santiago Chile 4-6 October 2017 Graham Robinson Global Construction Perspectives Global Construction 2030 is the fourth in a series of global studies of the construction

Global Construction 2030 Expo EDIFICA 2017 Santiago Chile 4-6 October 2017 Graham Robinson Global Construction Perspectives Global Construction 2030 is the fourth in a series of global studies of the construction

Fiscal Policy and the Global Crisis

Fiscal Policy and the Global Crisis Presentation at Koҫ University, Istanbul Carlo Cottarelli Director IMF Fiscal Affairs Department June 9, 2009 1 Two fiscal questions What is the appropriate fiscal policy

Fiscal Policy and the Global Crisis Presentation at Koҫ University, Istanbul Carlo Cottarelli Director IMF Fiscal Affairs Department June 9, 2009 1 Two fiscal questions What is the appropriate fiscal policy

No October 2013

DEVELOPING AND TRANSITION ECONOMIES ABSORBED MORE THAN 60 PER CENT OF GLOBAL FDI INFLOWS A RECORD SHARE IN THE FIRST HALF OF 2013 EMBARGO The content of this Monitor must not be quoted or summarized in

DEVELOPING AND TRANSITION ECONOMIES ABSORBED MORE THAN 60 PER CENT OF GLOBAL FDI INFLOWS A RECORD SHARE IN THE FIRST HALF OF 2013 EMBARGO The content of this Monitor must not be quoted or summarized in

The effects of the financial crisis on developing countries mapping out the issues. By Julian Jessop

The effects of the financial crisis on developing countries mapping out the issues By Julian Jessop 1. Plan of My Talk The outlook for advanced economies. Impact on developing countries. Some losers and

The effects of the financial crisis on developing countries mapping out the issues By Julian Jessop 1. Plan of My Talk The outlook for advanced economies. Impact on developing countries. Some losers and

Governments and Exchange Rates

Governments and Exchange Rates Exchange Rate Behavior Existing spot exchange rate covered interest arbitrage locational arbitrage triangular arbitrage Existing spot exchange rates at other locations Existing

Governments and Exchange Rates Exchange Rate Behavior Existing spot exchange rate covered interest arbitrage locational arbitrage triangular arbitrage Existing spot exchange rates at other locations Existing

Emerging Markets: Broader opportunities and declining systematic risk

June 2013 Emerging Markets: Broader opportunities and declining systematic risk Favorable outlook for emerging markets equity and debt Alexander Muromcew, Portfolio Manager, Emerging Markets Equity Strategy

June 2013 Emerging Markets: Broader opportunities and declining systematic risk Favorable outlook for emerging markets equity and debt Alexander Muromcew, Portfolio Manager, Emerging Markets Equity Strategy

THE IMPACT OF FINANCIAL TURMOIL ON THE WORLD COTTON AND TEXTILE MARKET

THE IMPACT OF FINANCIAL TURMOIL ON THE WORLD COTTON AND TEXTILE MARKET Presented by Paul Morris Chairman of the Standing Committee INTERNATIONAL COTTON ADVISORY COMMITTEE 1999 China International Cotton

THE IMPACT OF FINANCIAL TURMOIL ON THE WORLD COTTON AND TEXTILE MARKET Presented by Paul Morris Chairman of the Standing Committee INTERNATIONAL COTTON ADVISORY COMMITTEE 1999 China International Cotton

GLOBAL FDI OUTFLOWS CONTINUED TO RISE IN 2011 DESPITE ECONOMIC UNCERTAINTIES; HOWEVER PROSPECTS REMAIN GUARDED HIGHLIGHTS

GLOBAL FDI OUTFLOWS CONTINUED TO RISE IN 211 DESPITE ECONOMIC UNCERTAINTIES; HOWEVER PROSPECTS REMAIN GUARDED No. 9 12 April 212 ADVANCE UNEDITED COPY HIGHLIGHTS Global foreign direct investment (FDI)

GLOBAL FDI OUTFLOWS CONTINUED TO RISE IN 211 DESPITE ECONOMIC UNCERTAINTIES; HOWEVER PROSPECTS REMAIN GUARDED No. 9 12 April 212 ADVANCE UNEDITED COPY HIGHLIGHTS Global foreign direct investment (FDI)

Developing Housing Finance Systems

Developing Housing Finance Systems Veronica Cacdac Warnock IIMB-IMF Conference on Housing Markets, Financial Stability and Growth December 11, 2014 Based on Warnock V and Warnock F (2012). Developing Housing

Developing Housing Finance Systems Veronica Cacdac Warnock IIMB-IMF Conference on Housing Markets, Financial Stability and Growth December 11, 2014 Based on Warnock V and Warnock F (2012). Developing Housing

Chapter 18. The International Financial System Intervention in the Foreign Exchange Market

Chapter 18 The International Financial System 18.1 Intervention in the Foreign Exchange Market 1) A central bank of domestic currency and corresponding of foreign assets in the foreign exchange market

Chapter 18 The International Financial System 18.1 Intervention in the Foreign Exchange Market 1) A central bank of domestic currency and corresponding of foreign assets in the foreign exchange market

Suggested Solutions to Problem Set 6

Department of Economics University of California, Berkeley Spring 2006 Economics 182 Suggested Solutions to Problem Set 6 Problem 1: International diversification Because raspberries are nontradable, asset

Department of Economics University of California, Berkeley Spring 2006 Economics 182 Suggested Solutions to Problem Set 6 Problem 1: International diversification Because raspberries are nontradable, asset

Global growth fragile: The global economy is projected to grow at 3.5% in 2019 and 3.6% in 2020, 0.2% and 0.1% below October 2018 projections.

Monday January 21st 19 1:05pm International Prepared by: Ravi Kurjah, Senior Economic Analyst (Research & Analytics) ravi.kurjah@firstcitizenstt.com World Economic Outlook: A Weakening Global Expansion

Monday January 21st 19 1:05pm International Prepared by: Ravi Kurjah, Senior Economic Analyst (Research & Analytics) ravi.kurjah@firstcitizenstt.com World Economic Outlook: A Weakening Global Expansion

Chapter Eleven. The International Monetary System

Chapter Eleven The International Monetary System Introduction 11-3 The international monetary system refers to the institutional arrangements that govern exchange rates. Floating exchange rates occur when

Chapter Eleven The International Monetary System Introduction 11-3 The international monetary system refers to the institutional arrangements that govern exchange rates. Floating exchange rates occur when

3/9/2010. Topics PP542. Macroeconomic Goals (cont.) Macroeconomic Goals. Gold Standard. Macroeconomic Goals (cont.) International Monetary History

Macroeconomic Goals. Gold Standard. Macroeconomic Goals (cont.) International Monetary History") Topics PP542 International Monetary History Goals of macroeconomic policies Gold standard International monetary system during 98-939 Bretton Woods system: 944-973 Collapse of the Bretton Woods system

Topics PP542 International Monetary History Goals of macroeconomic policies Gold standard International monetary system during 98-939 Bretton Woods system: 944-973 Collapse of the Bretton Woods system

: Monetary Economics and the European Union. Lecture 8. Instructor: Prof Robert Hill. The Costs and Benefits of Monetary Union II

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

Study Questions (with Answers) Lecture 20 International Policies for Economic Development: Financial

Lecture 20 International Policies for Economic Development: Financial") Study Questions (with Answers) Page 1 of 5 Study Questions (with Answers) Lecture 20 International Policies for Economic Development: Financial Part 1: Multiple Choice Select the best answer of those given.

Study Questions (with Answers) Page 1 of 5 Study Questions (with Answers) Lecture 20 International Policies for Economic Development: Financial Part 1: Multiple Choice Select the best answer of those given.

Slides for International Finance Financial Globalization (KOM 21)

") Financial Globalization (KOM 21) American University 2011-10-05 Preview International Capital Markets Gains from Trade International Capital Markets Policy constraints and international financial markets

Financial Globalization (KOM 21) American University 2011-10-05 Preview International Capital Markets Gains from Trade International Capital Markets Policy constraints and international financial markets

Argus Butadiene Annual 2017

Argus Butadiene Annual 2017 Market Reporting Petrochemicals Consulting Events Argus Butadiene Annual 2017 Summary Three major developments have shaped the global butadiene (BD) markets over the past decade.

Argus Butadiene Annual 2017 Market Reporting Petrochemicals Consulting Events Argus Butadiene Annual 2017 Summary Three major developments have shaped the global butadiene (BD) markets over the past decade.

Why Invest In Emerging Markets? Why Now?

Why Invest In Emerging Markets? Why Now? 2017 Over the long term, Emerging Markets (EM) have been a winning alternative compared to traditional Developed Markets (DM)... 350 300 250 200 150 100 50 1997

Why Invest In Emerging Markets? Why Now? 2017 Over the long term, Emerging Markets (EM) have been a winning alternative compared to traditional Developed Markets (DM)... 350 300 250 200 150 100 50 1997

Why Invest In Emerging Markets? Why Now?

Why Invest In Emerging Markets? Why Now? 2018 Over the long term, Emerging Markets (EM) have been a winning alternative compared to traditional Developed Markets (DM)... 350 300 250 200 150 100 50 1998

Why Invest In Emerging Markets? Why Now? 2018 Over the long term, Emerging Markets (EM) have been a winning alternative compared to traditional Developed Markets (DM)... 350 300 250 200 150 100 50 1998

Chapter 18 (7) Fixed Exchange Rates and Foreign Exchange Intervention

Fixed Exchange Rates and Foreign Exchange Intervention") Chapter 18 (7) Fixed Exchange Rates and Foreign Exchange Intervention Preview Balance sheets of central banks Intervention in the foreign exchange markets and the money supply How the central bank fixes

Chapter 18 (7) Fixed Exchange Rates and Foreign Exchange Intervention Preview Balance sheets of central banks Intervention in the foreign exchange markets and the money supply How the central bank fixes

Monetary Policy Stance amid the Risk of Uneven Global Growth and External Imbalance

Monetary Policy Stance amid the Risk of Uneven Global Growth and External Imbalance Agus D.W. Martowardojo Governor Bank Indonesia Prepared for Mandiri Investment Forum, January 27, 2015 2 1 Global Economic

Monetary Policy Stance amid the Risk of Uneven Global Growth and External Imbalance Agus D.W. Martowardojo Governor Bank Indonesia Prepared for Mandiri Investment Forum, January 27, 2015 2 1 Global Economic

Chapter 18. The International Financial System

Chapter 18 The International Financial System Unsterilized Foreign Exchange Intervention Federal Reserve System Assets Liabilities Federal Reserve System Assets Liabilities Foreign Assets -$1B Currency

Chapter 18 The International Financial System Unsterilized Foreign Exchange Intervention Federal Reserve System Assets Liabilities Federal Reserve System Assets Liabilities Foreign Assets -$1B Currency

Financial Crisis What do we know?

Financial Crisis What do we know? Pedro Videla IESE Global Propagation of the Financial Crisis United Kingdom Ireland Iceland United States Spain January 2008 March 2008 June 2008 September 2008 January

Financial Crisis What do we know? Pedro Videla IESE Global Propagation of the Financial Crisis United Kingdom Ireland Iceland United States Spain January 2008 March 2008 June 2008 September 2008 January

Hamid Rashid, Ph.D. Chief Global Economic Monitoring Unit Development Policy Analysis Division UNDESA, New York

Hamid Rashid, Ph.D. Chief Global Economic Monitoring Unit Development Policy Analysis Division UNDESA, New York 1 Global macroeconomic trends Major headwinds Risks and uncertainties Policy questions and

Hamid Rashid, Ph.D. Chief Global Economic Monitoring Unit Development Policy Analysis Division UNDESA, New York 1 Global macroeconomic trends Major headwinds Risks and uncertainties Policy questions and

Chapter 17 Appendix B

Speculative Attacks and Foreign Exchange Crises Chapter 17 Appendix B In the following two applications, we use our model of exchange rate determination to understand how speculative attacks in both advanced

Speculative Attacks and Foreign Exchange Crises Chapter 17 Appendix B In the following two applications, we use our model of exchange rate determination to understand how speculative attacks in both advanced

Self-Protection for Emerging Market Economies. Martin Feldstein *

Self-Protection for Emerging Market Economies Martin Feldstein * International economic crises will continue to occur in the future as they have for centuries past. The rapid spread of the 1997 crisis

Self-Protection for Emerging Market Economies Martin Feldstein * International economic crises will continue to occur in the future as they have for centuries past. The rapid spread of the 1997 crisis

Session 16. Review Session

Session 16. Review Session The long run [Fundamentals] Output, saving, and investment Money and inflation Economic growth Labor markets The short run [Business cycles] What are the causes business cycles?

Session 16. Review Session The long run [Fundamentals] Output, saving, and investment Money and inflation Economic growth Labor markets The short run [Business cycles] What are the causes business cycles?

Ten Years After The Asian Financial Crisis * Heh-Song Wang **

Ten Years After The Asian Financial Crisis * I. Introduction Heh-Song Wang ** It is indeed a great honor and pleasure for me to be here to talk about the topic Ten years after the Asian financial crisis.

Ten Years After The Asian Financial Crisis * I. Introduction Heh-Song Wang ** It is indeed a great honor and pleasure for me to be here to talk about the topic Ten years after the Asian financial crisis.

Economic Update. Port Finance Seminar. Paul Bingham. Global Insight, Inc. Copyright 2006 Global Insight, Inc.

Economic Update Copyright 26 Global Insight, Inc. Port Finance Seminar Paul Bingham Global Insight, Inc. Baltimore, MD May 16, 26 The World Economy: Is the Risk of a Boom-Bust Rising? As the U.S. Economy

Economic Update Copyright 26 Global Insight, Inc. Port Finance Seminar Paul Bingham Global Insight, Inc. Baltimore, MD May 16, 26 The World Economy: Is the Risk of a Boom-Bust Rising? As the U.S. Economy

Global Economic Prospects and the Developing Countries William Shaw December 1999

Global Economic Prospects and the Developing Countries 2000 William Shaw December 1999 Prospects for Growth and Poverty Reduction in Developing Countries Recovery from financial crisis uneven International

Global Economic Prospects and the Developing Countries 2000 William Shaw December 1999 Prospects for Growth and Poverty Reduction in Developing Countries Recovery from financial crisis uneven International

The Chilean economy: Institutional buildup and perspectives

The Chilean economy: Institutional buildup and perspectives Vittorio Corbo Governor 1 Outline 1. Introduction 2. Chile s economic reforms and institutional buildup 3. Performance of the Chilean economy

The Chilean economy: Institutional buildup and perspectives Vittorio Corbo Governor 1 Outline 1. Introduction 2. Chile s economic reforms and institutional buildup 3. Performance of the Chilean economy

Financial wealth of private households worldwide

Economic Research Financial wealth of private households worldwide Munich, October 217 Recovery in turbulent times Assets and liabilities of private households worldwide in EUR trillion and annualrate

Economic Research Financial wealth of private households worldwide Munich, October 217 Recovery in turbulent times Assets and liabilities of private households worldwide in EUR trillion and annualrate

Two tales of development

Two tales of development BRAZIL-INDIA 17 Liliana Lavoratti, Rio de Janeiro India is still almost unknown to Brazilians in general. Given the distance not only geographically as well as quite different

Two tales of development BRAZIL-INDIA 17 Liliana Lavoratti, Rio de Janeiro India is still almost unknown to Brazilians in general. Given the distance not only geographically as well as quite different

The International Financial System

The International Financial System Notes on Mishkin, Chapter 21 Leigh Tesfatsion Economics Department Iowa State University, Ames IA Last Revised: 27 April 2011 Key In-Class Discussion Questions Mishkin,

The International Financial System Notes on Mishkin, Chapter 21 Leigh Tesfatsion Economics Department Iowa State University, Ames IA Last Revised: 27 April 2011 Key In-Class Discussion Questions Mishkin,

Japanese Capital Market

Japanese Capital Market The objectives of the chapter are to provide an understanding of: o o o o o o Financial system reforms. The banking sector. Japanese government bonds. Corporate debt markets. Stock

Japanese Capital Market The objectives of the chapter are to provide an understanding of: o o o o o o Financial system reforms. The banking sector. Japanese government bonds. Corporate debt markets. Stock

Federal Reserve System/IMF/World Bank. Seminar for Senior Bank Supervisors October 19 30, David S. Hoelscher

Federal Reserve System/IMF/World Bank Seminar for Senior Bank Supervisors October 19 30, 2009 David S. Hoelscher Money and Capital Markets Department International Monetary Fund Typology of Crises Type

Federal Reserve System/IMF/World Bank Seminar for Senior Bank Supervisors October 19 30, 2009 David S. Hoelscher Money and Capital Markets Department International Monetary Fund Typology of Crises Type

PRODUCT KEY FACTS. Principal Global Investors Funds Global Equity Fund April 2018

Global Equity Fund This statement provides you with key information about - Global Equity Fund ( Sub-Fund ). This statement is a part of the offering document. You should not invest in the Sub-Fund based

Global Equity Fund This statement provides you with key information about - Global Equity Fund ( Sub-Fund ). This statement is a part of the offering document. You should not invest in the Sub-Fund based

Planning Global Compensation Budgets for 2018 November 2017 Update

Planning Global Compensation Budgets for 2018 November 2017 Update Planning Global Compensation Budgets for 2018 The year is rapidly coming to a close, and we are now in the midst of 2018 global compensation

Planning Global Compensation Budgets for 2018 November 2017 Update Planning Global Compensation Budgets for 2018 The year is rapidly coming to a close, and we are now in the midst of 2018 global compensation

Chapter 18 (7) Fixed Exchange Rates and Foreign Exchange Intervention

Fixed Exchange Rates and Foreign Exchange Intervention") Chapter 18 (7) Fixed Exchange Rates and Foreign Exchange Intervention Preview Balance sheets of central banks Intervention in the foreign exchange markets and the money supply How the central bank fixes

Chapter 18 (7) Fixed Exchange Rates and Foreign Exchange Intervention Preview Balance sheets of central banks Intervention in the foreign exchange markets and the money supply How the central bank fixes

PRODUCT KEY FACTS. Principal Global Investors Funds Global Equity Fund April 2017

Global Equity Fund This statement provides you with key information about - Global Equity Fund ( Sub-Fund ). This statement is a part of the offering document. You should not invest in the Sub-Fund based

Global Equity Fund This statement provides you with key information about - Global Equity Fund ( Sub-Fund ). This statement is a part of the offering document. You should not invest in the Sub-Fund based

Ten Lessons Learned from the Korean Crisis Center for International Development, 11/19/99. Jeffrey A. Frankel, Harpel Professor, Harvard University

Ten Lessons Learned from the Korean Crisis Center for International Development, 11/19/99 Jeffrey A. Frankel, Harpel Professor, Harvard University The crisis has now passed in Korea. The excessive optimism

Ten Lessons Learned from the Korean Crisis Center for International Development, 11/19/99 Jeffrey A. Frankel, Harpel Professor, Harvard University The crisis has now passed in Korea. The excessive optimism

Global growth weakening as some risks materialise

OECD INTERIM ECONOMIC OUTLOOK Global growth weakening as some risks materialise 6 March 2019 Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE blog: oecdecoscope.wordpress.com

OECD INTERIM ECONOMIC OUTLOOK Global growth weakening as some risks materialise 6 March 2019 Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE blog: oecdecoscope.wordpress.com

A short history of debt

A short history of debt In the words of the late Charles Kindleberger, debt/financial crises are a hardy perennial we have been here many times before. Over the past decade and a half the ratio of global

A short history of debt In the words of the late Charles Kindleberger, debt/financial crises are a hardy perennial we have been here many times before. Over the past decade and a half the ratio of global

OVERVIEW of INTERNATIONAL CAPITAL FLOWS

OVERVIEW of INTERNATIONAL CAPITAL FLOWS By Mack Ott, CEE, 2008 [Mack Ott is an international economic consultant whose major assignments have been in theformer Soviet Union countries, the Balkans, and

OVERVIEW of INTERNATIONAL CAPITAL FLOWS By Mack Ott, CEE, 2008 [Mack Ott is an international economic consultant whose major assignments have been in theformer Soviet Union countries, the Balkans, and

POST-CRISIS GLOBAL REBALANCING CONFERENCE ON GLOBALIZATION AND THE LAW OF THE SEA WASHINGTON DC, DEC 1-3, Barry Bosworth

POST-CRISIS GLOBAL REBALANCING CONFERENCE ON GLOBALIZATION AND THE LAW OF THE SEA WASHINGTON DC, DEC 1-3, 2010 Barry Bosworth I. Economic Rise of Asia Emerging economies of Asia have performed extremely

POST-CRISIS GLOBAL REBALANCING CONFERENCE ON GLOBALIZATION AND THE LAW OF THE SEA WASHINGTON DC, DEC 1-3, 2010 Barry Bosworth I. Economic Rise of Asia Emerging economies of Asia have performed extremely

Xtrackers MSCI All World ex US High Dividend Yield Equity ETF

Summary Prospectus September 28, 2018 Ticker: HDAW Stock Exchange: NYSE Arca, Inc. Before you invest, you may wish to review the Fund s prospectus, which contains more information about the Fund and its

Summary Prospectus September 28, 2018 Ticker: HDAW Stock Exchange: NYSE Arca, Inc. Before you invest, you may wish to review the Fund s prospectus, which contains more information about the Fund and its

Financial Crises. Benjamin Graham. Videos in this lecture are from Kahn Academy

Financial Crises Videos in this lecture are from Kahn Academy Today s Plan An updated syllabus is posted Today s topics: Kahn Academy Videos on foreign currency reserves and speculative attacks The Asian

Financial Crises Videos in this lecture are from Kahn Academy Today s Plan An updated syllabus is posted Today s topics: Kahn Academy Videos on foreign currency reserves and speculative attacks The Asian

UP OR DOWN? 2015 Q3 NIELSEN GLOBAL SURVEY OF CONSUMER CONFIDENCE AND SPENDING INTENTIONS

UP OR DOWN? 2015 Q3 NIELSEN GLOBAL SURVEY OF CONSUMER CONFIDENCE AND SPENDING INTENTIONS Among the world s largest economies, U.S. consumer confidence jumped 18 index points in the third quarter to a score

UP OR DOWN? 2015 Q3 NIELSEN GLOBAL SURVEY OF CONSUMER CONFIDENCE AND SPENDING INTENTIONS Among the world s largest economies, U.S. consumer confidence jumped 18 index points in the third quarter to a score

The International Monetary System

INTERNATIONAL FINANCIAL MANAGEMENT Fourth Edition EUN / RESNICK The International Monetary System 2 Chapter Two INTERNATIONAL Chapter Objective: FINANCIAL MANAGEMENT This chapter serves to introduce the

INTERNATIONAL FINANCIAL MANAGEMENT Fourth Edition EUN / RESNICK The International Monetary System 2 Chapter Two INTERNATIONAL Chapter Objective: FINANCIAL MANAGEMENT This chapter serves to introduce the

Overview of Demographic Dividend. Andrew Mason Demographic Dividend Working Group Barcelona, Spain June 5 8, 2013

Overview of Demographic Dividend Andrew Mason Demographic Dividend Working Group Barcelona, Spain June 5 8, 2013 First Demographic Dividend At an early stage of [demographic] transition, fertility rates

Overview of Demographic Dividend Andrew Mason Demographic Dividend Working Group Barcelona, Spain June 5 8, 2013 First Demographic Dividend At an early stage of [demographic] transition, fertility rates

Economics Higher level Paper 2

Economics Higher level Paper 2 Tuesday 5 May 2015 (morning) 1 hour 30 minutes Instructions to candidates Do not open this examination paper until instructed to do so. You are not permitted access to any

Economics Higher level Paper 2 Tuesday 5 May 2015 (morning) 1 hour 30 minutes Instructions to candidates Do not open this examination paper until instructed to do so. You are not permitted access to any

483 Subject Index. Global Depositiory Receipts, 250 Grassman s law, 148, 160

Subject Index Adjustabonos, 401-3 Agency for International Development, 100 American depository receipts (ADRs): considered as foreign securities, 250; traded on over-the-counter market, 245 Arbitrage:

Subject Index Adjustabonos, 401-3 Agency for International Development, 100 American depository receipts (ADRs): considered as foreign securities, 250; traded on over-the-counter market, 245 Arbitrage:

Econ 340. Lecture 20 International Policies for Economic Development: Financial

Econ 340 Lecture 20 International Policies for Economic Development: Financial Exam 2 Curve 2 News: Nov 19-26 US considers quotas on steel and aluminum from Canada and Mexico -- NYT: 11/21 Canvas As of

Econ 340 Lecture 20 International Policies for Economic Development: Financial Exam 2 Curve 2 News: Nov 19-26 US considers quotas on steel and aluminum from Canada and Mexico -- NYT: 11/21 Canvas As of

Growth, investment and jobs: The international financial dimension. Working Party on the Social Dimension of Globalization November 14th, 2005

Growth, investment and jobs: The international financial dimension Working Party on the Social Dimension of Globalization November 14th, 2005 Growth, investment and jobs At times of global economic integration,

Growth, investment and jobs: The international financial dimension Working Party on the Social Dimension of Globalization November 14th, 2005 Growth, investment and jobs At times of global economic integration,

Other similar crisis: Euro, Emerging Markets

Session 15. Understanding Macroeconomic Crises. Mexican Crisis 1994-95 Other similar crisis: Euro, Emerging Markets Global Scenarios 2017-2021 The Mexican Peso Crisis in 1994: Background An economy that

Session 15. Understanding Macroeconomic Crises. Mexican Crisis 1994-95 Other similar crisis: Euro, Emerging Markets Global Scenarios 2017-2021 The Mexican Peso Crisis in 1994: Background An economy that

Capital Account Controls and Liberalization: Lessons for India and China

UBS Investment Research Capital Account Controls and Liberalization: Lessons for India and China Jonathan Anderson November 2003 ANALYST CERTIFICATION AND REQUIRED DISCLOSURES BEGIN ON PAGE 50 UBS does

UBS Investment Research Capital Account Controls and Liberalization: Lessons for India and China Jonathan Anderson November 2003 ANALYST CERTIFICATION AND REQUIRED DISCLOSURES BEGIN ON PAGE 50 UBS does

Macroeconomic Measurement 3: The Accumulation of Value

International Economics and Business Dynamics Class Notes Macroeconomic Measurement 3: The Accumulation of Value Revised: October 30, 2012 Latest version available at http://www.fperri.net/teaching/20205.htm

International Economics and Business Dynamics Class Notes Macroeconomic Measurement 3: The Accumulation of Value Revised: October 30, 2012 Latest version available at http://www.fperri.net/teaching/20205.htm

Lecture 6: Intermediate macroeconomics, autumn Lars Calmfors

Lecture 6: Intermediate macroeconomics, autumn 2009 Lars Calmfors 1 Topics Systems of fixed exchange rates Interest rate parity under a fixed exchange rate Stabilisation policy under a fixed exchange rate

Lecture 6: Intermediate macroeconomics, autumn 2009 Lars Calmfors 1 Topics Systems of fixed exchange rates Interest rate parity under a fixed exchange rate Stabilisation policy under a fixed exchange rate

Chapter 19 (8) International Monetary Systems: An Historical Overview

International Monetary Systems: An Historical Overview") Chapter 19 (8) International Monetary Systems: An Historical Overview Preview Goals of macroeconomic policies internal and external balance Gold standard era 1870 1914 International monetary system during

Chapter 19 (8) International Monetary Systems: An Historical Overview Preview Goals of macroeconomic policies internal and external balance Gold standard era 1870 1914 International monetary system during

The Asian Crisis: Causes and Cures IMF Staff

June 1998, Volume 35, Number 2 The Asian Crisis: Causes and Cures IMF Staff The financial crisis that struck many Asian countries in late 1997 did so with an unexpected severity. What went wrong? How can

June 1998, Volume 35, Number 2 The Asian Crisis: Causes and Cures IMF Staff The financial crisis that struck many Asian countries in late 1997 did so with an unexpected severity. What went wrong? How can

Asia s Debt Risks The risk of financial crises is limited, but attention should be paid to slowing domestic demand.

Mizuho Economic Outlook & Analysis November 15, 218 Asia s Debt Risks The risk of financial crises is limited, but attention should be paid to slowing domestic demand. < Summary > Expanding private debt

Mizuho Economic Outlook & Analysis November 15, 218 Asia s Debt Risks The risk of financial crises is limited, but attention should be paid to slowing domestic demand. < Summary > Expanding private debt

PMITM. The world s leading economic indicator

PMITM The world s leading economic indicator The Purchasing Managers IndexTM (PMITM) is based on monthly surveys of carefully selected companies representing major and developing economies worldwide. KEY

PMITM The world s leading economic indicator The Purchasing Managers IndexTM (PMITM) is based on monthly surveys of carefully selected companies representing major and developing economies worldwide. KEY

Chapter 20 (9) Financial Globalization: Opportunity and Crisis

Financial Globalization: Opportunity and Crisis") Chapter 20 (9) Financial Globalization: Opportunity and Crisis Preview Gains from trade Portfolio diversification Players in the international capital markets Attainable policies with international capital

Chapter 20 (9) Financial Globalization: Opportunity and Crisis Preview Gains from trade Portfolio diversification Players in the international capital markets Attainable policies with international capital

Chapter 6. Government Influence on Exchange Rates. Lecture Outline

Chapter 6 Government Influence on Exchange Rates Lecture Outline Exchange Rate Systems Fixed Exchange Rate System Freely Floating Exchange Rate System Managed Float Exchange Rate System Pegged Exchange

Chapter 6 Government Influence on Exchange Rates Lecture Outline Exchange Rate Systems Fixed Exchange Rate System Freely Floating Exchange Rate System Managed Float Exchange Rate System Pegged Exchange

Global Economic Outlook John Hawksworth Chief Economist, PwC September 2012

www.pwc.co.uk/economics Global Economic Outlook John Hawksworth Chief Economist, September 2012 Agenda Global overview Short term prospects for Europe, US and BRICs Long term trends: demographics, growth

www.pwc.co.uk/economics Global Economic Outlook John Hawksworth Chief Economist, September 2012 Agenda Global overview Short term prospects for Europe, US and BRICs Long term trends: demographics, growth

Econ 340. The Issues. The Washington Consensus. Outline: International Policies for Economic Development: Trade

Econ 340 Lecture 19 International Policies for 2 3 The Issues The Two Main Issues: Should developing countries be open to international trade? Should developing countries be open to international capital

Econ 340 Lecture 19 International Policies for 2 3 The Issues The Two Main Issues: Should developing countries be open to international trade? Should developing countries be open to international capital

Actuarial Supply & Demand. By i.e. muhanna. i.e. muhanna Page 1 of

By i.e. muhanna i.e. muhanna Page 1 of 8 040506 Additional Perspectives Measuring actuarial supply and demand in terms of GDP is indeed a valid basis for setting the actuarial density of a country and

By i.e. muhanna i.e. muhanna Page 1 of 8 040506 Additional Perspectives Measuring actuarial supply and demand in terms of GDP is indeed a valid basis for setting the actuarial density of a country and

EQUITY REPORTING & WITHHOLDING. Updated May 2016

EQUITY REPORTING & WITHHOLDING Updated May 2016 When you exercise stock options or have RSUs lapse, there may be tax implications in any country in which you worked for P&G during the period from the

EQUITY REPORTING & WITHHOLDING Updated May 2016 When you exercise stock options or have RSUs lapse, there may be tax implications in any country in which you worked for P&G during the period from the

Global Consumer Confidence

Global Consumer Confidence The Conference Board Global Consumer Confidence Survey is conducted in collaboration with Nielsen 4TH QUARTER 2017 RESULTS CONTENTS Global Highlights Asia-Pacific Africa and

Global Consumer Confidence The Conference Board Global Consumer Confidence Survey is conducted in collaboration with Nielsen 4TH QUARTER 2017 RESULTS CONTENTS Global Highlights Asia-Pacific Africa and

Belgium s foreign trade 2011

Belgium s Belgium s BELGIAN FOREIGN TRADE IN Analysis of the figures for (Source: nbb community concept*) The following results demonstrate that Belgian did not suffer the negative effects of the crisis

Belgium s Belgium s BELGIAN FOREIGN TRADE IN Analysis of the figures for (Source: nbb community concept*) The following results demonstrate that Belgian did not suffer the negative effects of the crisis

China's Current Account and International Financial Integration

China's Current Account China's Current Account and International Financial Integration Kaiji Chen University of Oslo March 20, 2007 1 China's Current Account Why should we care about China's net foreign

China's Current Account China's Current Account and International Financial Integration Kaiji Chen University of Oslo March 20, 2007 1 China's Current Account Why should we care about China's net foreign

Global Business Barometer April 2008

Global Business Barometer April 2008 The Global Business Barometer is a quarterly business-confidence index, conducted for The Economist by the Economist Intelligence Unit What are your expectations of

Global Business Barometer April 2008 The Global Business Barometer is a quarterly business-confidence index, conducted for The Economist by the Economist Intelligence Unit What are your expectations of

Asia Business Council Annual Survey 2011

Asia Business Council Annual Survey 2011 Executive Summary September 2011 Survey Overview Survey was conducted in July-August 2011 Response rate of 76% (49 of 64 members) Members were asked about their

Asia Business Council Annual Survey 2011 Executive Summary September 2011 Survey Overview Survey was conducted in July-August 2011 Response rate of 76% (49 of 64 members) Members were asked about their

EMBA Chapters 7&8 FDI Global Trading Blocks Competitiveness

EMBA 716 2008 Chapters 7&8 FDI Global Trading Blocks Competitiveness Outline What is FDI? Government policy and FDI FDI inflow and outflow Capital inflow to US Regional economic integration (Global Trading

EMBA 716 2008 Chapters 7&8 FDI Global Trading Blocks Competitiveness Outline What is FDI? Government policy and FDI FDI inflow and outflow Capital inflow to US Regional economic integration (Global Trading

Latin American Finance

MMost countries in Latin America have made serious strides toward reforming their economies in the last 15 years, opening their markets to trade and foreign investment, reducing government budget deficits,

MMost countries in Latin America have made serious strides toward reforming their economies in the last 15 years, opening their markets to trade and foreign investment, reducing government budget deficits,

Balance of Payments, Debt, Financial Crises, and Stabilization Policies

Chapter 9 Balance of Payments, Debt, Financial Crises, and Stabilization Policies Problems and Policies: international and macro 1 International Finance and Investment: Key Issues How major debt crises

Chapter 9 Balance of Payments, Debt, Financial Crises, and Stabilization Policies Problems and Policies: international and macro 1 International Finance and Investment: Key Issues How major debt crises

Charting Mexico s Economy

Charting Mexico s Economy Designed to help executives catch up with the economy and incorporate macro impacts into company s planning. Annual subscription includes 2 semiannual issues published in June

Charting Mexico s Economy Designed to help executives catch up with the economy and incorporate macro impacts into company s planning. Annual subscription includes 2 semiannual issues published in June

SPP 542 International Financial Policy South Korea s Next Step

SPP 542 International Financial Policy South Korea s Next Step Date: April 16, 2003 Written by: Tsutomu Hayafuji Mitsuru Ikeda Hironori Yamada 1. South Korean Economy Outlook From the mid-1960s to the

SPP 542 International Financial Policy South Korea s Next Step Date: April 16, 2003 Written by: Tsutomu Hayafuji Mitsuru Ikeda Hironori Yamada 1. South Korean Economy Outlook From the mid-1960s to the

2012 Canazei Winter Workshop on Inequality

2012 Canazei Winter Workshop on Inequality Measuring the Global Distribution of Wealth Jim Davies 11 January 2012 Collaborators Susanna Sandström, Tony Shorrocks, Ed Wolff The world distribution of household

2012 Canazei Winter Workshop on Inequality Measuring the Global Distribution of Wealth Jim Davies 11 January 2012 Collaborators Susanna Sandström, Tony Shorrocks, Ed Wolff The world distribution of household

International Monetary Fund. World Economic Outlook. Jörg Decressin Senior Advisor Research Department, IMF

International Monetary Fund World Economic Outlook Jörg Decressin Senior Advisor Research Department, IMF IMF Presentation April 3, The recovery is solidifying but it will take some time before it significantly

International Monetary Fund World Economic Outlook Jörg Decressin Senior Advisor Research Department, IMF IMF Presentation April 3, The recovery is solidifying but it will take some time before it significantly

OECD ECONOMIC OUTLOOK

OECD ECONOMIC OUTLOOK (A EUROPEAN AND GLOBAL PERSPECTIVE) GIC Conference, London, 3 June, 2016 Christian Kastrop Director, Economics Department Key messages 1 The global economy is stuck in a low growth

OECD ECONOMIC OUTLOOK (A EUROPEAN AND GLOBAL PERSPECTIVE) GIC Conference, London, 3 June, 2016 Christian Kastrop Director, Economics Department Key messages 1 The global economy is stuck in a low growth

The Evolution of the International Monetary System. Professor Keith Pilbeam City University, London

The Evolution of the International Monetary System Professor Keith Pilbeam City University, London The Postwar International Monetary System some highlights Bretton Woods 1949-72 sets up IMF, fixes dollar

The Evolution of the International Monetary System Professor Keith Pilbeam City University, London The Postwar International Monetary System some highlights Bretton Woods 1949-72 sets up IMF, fixes dollar

Chapter 18: Output and the Exchange Rate in the Short Run

Chapter 18: Output and the Exchange Rate in the Short Run Krugman, P.R., Obstfeld, M.: International Economics: Theory and Policy, 8th Edition, Pearson Addison-Wesley, 460-500 1 Preview Balance sheets

Chapter 18: Output and the Exchange Rate in the Short Run Krugman, P.R., Obstfeld, M.: International Economics: Theory and Policy, 8th Edition, Pearson Addison-Wesley, 460-500 1 Preview Balance sheets

International Monetary Fund

International Monetary Fund World Economic Outlook Jörg Decressin Deputy Director Research Department, IMF April 212 Towards Lasting Stability Global Economy Pulled Back from the Brink Policies Stepped

International Monetary Fund World Economic Outlook Jörg Decressin Deputy Director Research Department, IMF April 212 Towards Lasting Stability Global Economy Pulled Back from the Brink Policies Stepped

International financial crises

International Macroeconomics Master in International Economic Policy International financial crises Lectures 11-12 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lectures 11 and 12 International

International Macroeconomics Master in International Economic Policy International financial crises Lectures 11-12 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lectures 11 and 12 International

Global Edge: to Manage the Risks of Cross-Border Business. Joel Kurtzman Chairman, Kurtzman Group

Global Edge: Using the Opacity Index to Manage the Risks of Cross-Border Business Joel Kurtzman Chairman, Kurtzman Group Senior Fellow, Milken Institute Approach Today s hypercompetition changes the old

Global Edge: Using the Opacity Index to Manage the Risks of Cross-Border Business Joel Kurtzman Chairman, Kurtzman Group Senior Fellow, Milken Institute Approach Today s hypercompetition changes the old