Building a Financial Conditions Index for the Euro Area and Selected Euro Area Countries: What does it tell us about the crisis?

|

|

|

- Muriel Little

- 5 years ago

- Views:

Transcription

1 Building a Financial Conditions Index for the Euro Area and Selected Euro Area Countries: What does it tell us about the crisis? Eleni Angelopoulou, Hiona Balfoussia and Heather Gibson Special Studies Division, Bank of Greece

2 A Brief History of Financial Conditions Indices Research on FCIs dates back to the early 2000s, motivated by: a. A growing realisation of the key role played by financial variables in monetary policy transmission b. The dot com bubble: Should central banks account for financial variables (e.g. asset prices) in their policy stance?

3 A Brief History of Financial Conditions Indices a. A growing realisation of the key role played by financial variables in monetary policy transmission The bank lending channel literature highlights the role of financial market imperfections in propagating the effects of monetary policy on the economy, by leading to excessive responses of liquidity constrained banks and firms (e.g. Bernanke and Gertler, 1995) The consumption literature also indicates that liquidity constraints lead to larger fluctuations in consumption (e.g. Zeldes 1989)

4 A Brief History of Financial Conditions Indices b. The dot com bubble: Should central banks account for financial variables (e.g. asset prices) in their policy stance? Financial asset prices should be used to improve on central banks inflation forecasts (Bernanke and Gertler, 1999, 2001) They should form part of a broader price index targeted by central banks (Goodhart and Hofmann, 2000, 2001 and 2003) Monetary policy should actively pursue a stabilization of asset prices around fundamentals (Cecchetti et al., 2000)

5 A Brief History of Financial Conditions Indices First FCIs included: asset prices (stocks and housing) money market rates and spreads (shape of the yield curve) Recently (for the US): Credit terms and conditions (Swiston, 2008) Survey data (Hatzius et al. 2010) FCIs constructed: for a number of countries with different aims (most commonly as forecasting tools or leading indicators)

6 What we do We construct: FCIs for the euroarea, with and without monetary policy variables ( ) Analogous FCIs for Germany and countries of the periphery in crisis (Greece, Ireland, Portugal and Spain) We examine: The evolution of each of these FCIs over time, against the timeline of the crisis How financial conditions differed between euroarea countries at different points in time The contribution of monetary policy to financial conditions

7 Methodology Principal Components Analysis (PCA) is a way of: identifying patterns in the data obtaining factors which explain most of the variance compressing datasets with minimal (controlled) loss of info Disadvantage: no structure, atheoretical Advantage: no structure, the results do not reflect a priori beliefs, they merely reflect the data However, our approach is not atheoretical. Theory is used in: Identifying variables which capture all aspects of financial conditions (thus the inclusion of up to 24 variables) Including them in the direction indicated by economic theory

8 Data selection: the economic underpinnings of the FCI Prices: Healthier balance sheets which facilitate borrowing Quantities: In the presence of incomplete markets and/or extreme financial conditions, quantities also contain valuable information Interest Rate Spreads: Credit, Interbank, Sovereign Volatilities: A sign of heightened tension in financial markets ECB Bank Lending Surveys: Credit terms / availability Monetary policy variables impact on financial conditions

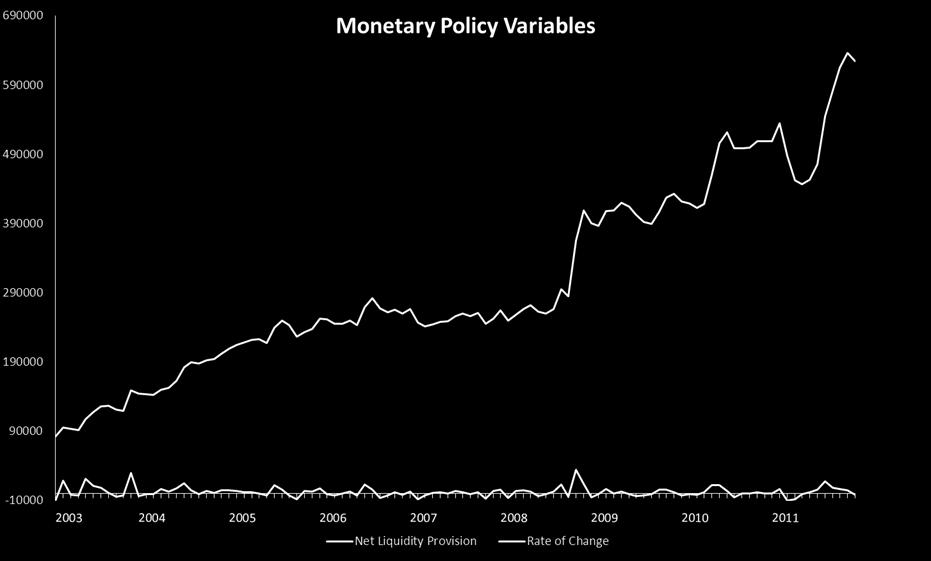

9 Data selection: the economic underpinnings of the FCI 1. Loans to non financial corporations (NFCs, flows) 2. Loans to households (Hhlds, flows) 3. Spread: loans and deposits to NFCs 4. Spread: overdrafts and deposits to NFCs 5. Spread: consumer loans and deposits to Hhlds 6. Spread: mortgage loans and deposits to Hhlds 7. Net liquidity provision by Eurosystem 8. Growth rate of net liquidity provision by Eurosystem 9. Debt securities issued by NFCs 10. Debt securities issued by monetary financial institutions

10 Data selection: the economic underpinnings of the FCI 11. Rate of change of residential property prices 12. Rate of change of Harmonised Index of Consumer Prices 13. Spread: 3 month overnight 14. Spread: 2 year 3 month EURIBOR 15. Spread: 10 year 3 month EURIBOR 16. Average spreads of long term government debt vs Germany 17. Rate of change of stock prices 18. Volatility of stock prices 19. Volatility of bond prices

11 Data selection: the economic underpinnings of the FCI 20. Bank lending survey banks access to market financing 21. Bank lending survey banks liquidity position 22. Bank lending survey housing market prospects 23. Bank lending survey consumer creditworthiness 24. ECB refinancing rate

12 What we find Our FCIs: intuitively track financial and credit related developments, for the euroarea as well as for individual countries can be used to gauge and assess the impact of monetary policy on financial conditions at different points in time strongly indicate that financial conditions across the euroarea have varied greatly between the core and the periphery, especially during the recent crisis suggest that monetary policy in the euroarea has not been equally effective over the sample period, nor equally suitable for different countries

13 Results: Euro area principal components Cut off threshold: 70% of the dataset s overall variability For the euro area dataset this is explained by: 1 st principal component: the Bank Lending Survey, residential property prices, interbank spread 2 nd principal component: bank credit variables (prices and quantities), securities 3 rd principal component : Loan to deposit spreads To construct the FCI, the selected principal components are weighted by the share of variance they explain and their sum is divided by the total share of variance explained, to ensure comparability between FCIs

14

15

16 FRFA: Fixed Rate tender Full Allotment ECB interest rate on main refinancing operations

17

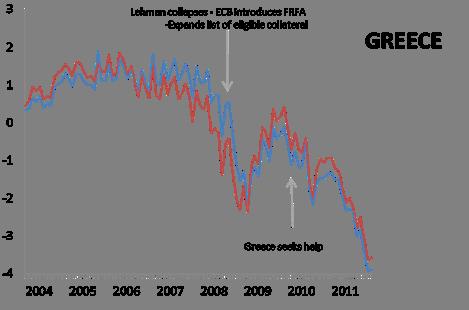

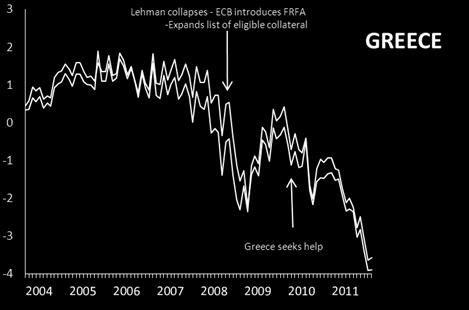

18 GREECE Greece Monetary Policy Contribution ECB interest rate on main refinancing operations

19 IRELAND Ireland Monetary Policy Contribution ECB interest rate on main refinancing operations

20 PORTUGAL Portugal Monetary Policy Contribution ECB interest rate on main refinancing operations

21 SPAIN Spain Monetary Policy Contribution ECB interest rate on main refinancing operations

22 Periphery

23 GERMANY Germany Monetary Policy Contribution ECB interest rate on main refinancing operations

24 Weighted loadings of monetary policy variables in FCIs Euro area Germany Greece Ireland Portugal S pain Net liquidity provis ion by the Eurosystem Growth of net liquidity provis ion ECB refinancing rate

25 Cross correlations between FCIs Without monetary policy Euro area Greece Ireland Portugal S pain Germany Euro area 1 Greece Ireland Portugal S pain Germany With monetary policy Euro area Greece Ireland Portugal S pain Germany Euro area 1 Greece Ireland Portugal S pain Germany

26 Main findings Financial conditions fluctuate substantially over time Strong evidence of heterogeneous financial conditions within EMU both before and during the global financial crisis, in spite of the single monetary policy Asymmetric responses to financial shocks: Lehman fall has different impact on different countries Divergent experiences of the crisis: Periphery: financial conditions did not loosen as much up to 2008, then tightened earlier on than in Germany Germany: No evidence of the deterioration seen in euro area financial conditions in the second half of 2011

27 Main findings Monetary policy appears to have leaned against the wind in the run up to the crisis, containing the credit easing. The same appears to have been the case in the periphery, in the aftermath of Lehman Brothers, setting a break on the unprecedented tightening of credit conditions. However, during the sovereign debt crisis and once the interest rate tool became available, monetary policy seems to have led to tighter financial conditions across the EMU. Overall, the single monetary policy does seem to help convergence in conditions across the euro area.

28 In conclusion 1. Our FCIs appear to be potentially valuable tools, both for monitoring financial conditions and for assessing the impact and appropriateness of monetary policy with regards to financial conditions. 2. Making monetary policy which will adequately account for the heterogeneity and asymmetries detected in financial conditions across the euro area represents a considerable challenge.

BUILDING A FINANCIAL CONDITIONS INDEX FOR THE EURO AREA AND SELECTED EURO AREA COUNTRIES: WHAT DOES IT TELL US ABOUT THE CRISIS?

BANK OF GREECE Economic Research Department Special Studies Division 21, Ε. Venizelos Avenue GR-102 50 Athens Τel: +30210-320 3610 Fax: +30210-320 2432 www.bankofgreece.gr Printed in Athens, Greece at

BANK OF GREECE Economic Research Department Special Studies Division 21, Ε. Venizelos Avenue GR-102 50 Athens Τel: +30210-320 3610 Fax: +30210-320 2432 www.bankofgreece.gr Printed in Athens, Greece at

WP/15/220. A Financial Conditions Index for Greece. By Jonathan Manning and Maral Shamloo

WP/15/22 A Financial Conditions Index for Greece By Jonathan Manning and Maral Shamloo IMF Working Papers describe research in progress by the author(s) and are published to elicit comments and to encourage

WP/15/22 A Financial Conditions Index for Greece By Jonathan Manning and Maral Shamloo IMF Working Papers describe research in progress by the author(s) and are published to elicit comments and to encourage

The crisis response in the euro area. Peter Praet Pioneer Investment s Colloquia Series Beijing, 17 April 2013

The crisis response in the euro area Peter Praet Pioneer Investment s Colloquia Series Beijing, 17 April 213 Outline A. How the crisis developed B. Monetary policy response C. Structural adjustment underway

The crisis response in the euro area Peter Praet Pioneer Investment s Colloquia Series Beijing, 17 April 213 Outline A. How the crisis developed B. Monetary policy response C. Structural adjustment underway

Nonstandard Monetary Policy Measures and Central Bank Balance Sheet Risks. Franziska Schobert

Nonstandard Monetary Policy Measures and Central Bank Balance Sheet Risks Franziska Schobert Agenda 1. Overview on crisis-related developments in the euro area 2. Impact of crisis-related measures on central

Nonstandard Monetary Policy Measures and Central Bank Balance Sheet Risks Franziska Schobert Agenda 1. Overview on crisis-related developments in the euro area 2. Impact of crisis-related measures on central

Effectiveness and Transmission of the ECB s Balance Sheet Policies

Effectiveness and Transmission of the ECB s Balance Sheet Policies Jef Boeckx NBB Maarten Dossche NBB Gert Peersman UGent Motivation There is a large literature that has used SVAR models to examine the

Effectiveness and Transmission of the ECB s Balance Sheet Policies Jef Boeckx NBB Maarten Dossche NBB Gert Peersman UGent Motivation There is a large literature that has used SVAR models to examine the

The ECB and the crisis

The ECB and the crisis Stefan Gerlach Chief Economist and Senior Vice President Hong Kong Institute for Monetary Research 29 February 2016 Outline 1. Introduction and background 2. The crisis 3. ECB s

The ECB and the crisis Stefan Gerlach Chief Economist and Senior Vice President Hong Kong Institute for Monetary Research 29 February 2016 Outline 1. Introduction and background 2. The crisis 3. ECB s

In response to the financial crisis, the Eurosystem has introduced

Understanding Central Bank Balance Sheets B Y J O A C H I M N A G E L The new monetary tool. THE MAGAZINE OF INTERNATIONAL ECONOMIC POLICY 220 I Street, N.E., Suite 200 Washington, D.C. 20002 Phone: 202-861-0791

Understanding Central Bank Balance Sheets B Y J O A C H I M N A G E L The new monetary tool. THE MAGAZINE OF INTERNATIONAL ECONOMIC POLICY 220 I Street, N.E., Suite 200 Washington, D.C. 20002 Phone: 202-861-0791

Challenges to the single monetary policy and the ECB s response. Benoît Cœuré Member of the Executive Board European Central Bank

Challenges to the single monetary policy and the ECB s response Benoît Cœuré Member of the Executive Board European Central Bank Institut d études politiques, Paris 2 September 212 1 Prime conduit of monetary

Challenges to the single monetary policy and the ECB s response Benoît Cœuré Member of the Executive Board European Central Bank Institut d études politiques, Paris 2 September 212 1 Prime conduit of monetary

Benoît Cœuré: SME financing a euro area perspective

Benoît Cœuré: SME financing a euro area perspective Speech by Mr Benoît Cœuré, Member of the Executive Board of the European Central Bank, at the Conference on Small Business Financing, jointly organised

Benoît Cœuré: SME financing a euro area perspective Speech by Mr Benoît Cœuré, Member of the Executive Board of the European Central Bank, at the Conference on Small Business Financing, jointly organised

ECB LTRO Dec Greece program

International Monetary Fund June 9, 212 Euro Area Crisis: Still in the Danger Zone */ Emil Stavrev Research Department ( */ Views expressed in this presentation are those of the author and do not necessarily

International Monetary Fund June 9, 212 Euro Area Crisis: Still in the Danger Zone */ Emil Stavrev Research Department ( */ Views expressed in this presentation are those of the author and do not necessarily

Negative interest rates: Lessons from the euro area

Jens Eisenschmidt and Frank Smets European Central Bank Negative interest rates: Lessons from the euro area The views expressed are our own and should not be attributed to those of the European Central

Jens Eisenschmidt and Frank Smets European Central Bank Negative interest rates: Lessons from the euro area The views expressed are our own and should not be attributed to those of the European Central

Economic state of the union, EuroMemo Engelbert Stockhammer Kingston University

Economic state of the union, EuroMemo 2013 Engelbert Stockhammer Kingston University structure Economic developments Background: export-led growth and debt-led growth Growth, trade imbalances, ages and

Economic state of the union, EuroMemo 2013 Engelbert Stockhammer Kingston University structure Economic developments Background: export-led growth and debt-led growth Growth, trade imbalances, ages and

EUROZONE BANKS AND CAPITAL FLOW REVERSAL

EUROZONE BANKS AND CAPITAL FLOW REVERSAL Ashoka Mody Research Department International Monetary Fund European Crisis: Historical Parallels and Economic Lessons Julis-Rabinowitz Center for Public Policy

EUROZONE BANKS AND CAPITAL FLOW REVERSAL Ashoka Mody Research Department International Monetary Fund European Crisis: Historical Parallels and Economic Lessons Julis-Rabinowitz Center for Public Policy

Bank Contagion in Europe

Bank Contagion in Europe Reint Gropp and Jukka Vesala Workshop on Banking, Financial Stability and the Business Cycle, Sveriges Riksbank, 26-28 August 2004 The views expressed in this paper are those of

Bank Contagion in Europe Reint Gropp and Jukka Vesala Workshop on Banking, Financial Stability and the Business Cycle, Sveriges Riksbank, 26-28 August 2004 The views expressed in this paper are those of

Income and Wealth of Euro Area Households in Times of Ultra- Loose Monetary Policy

Income and Wealth of Euro Area Households in Times of Ultra- Loose Monetary Policy Stylised Facts from National and Financial Accounts Data Banca d Italia Conference: How Financial Systems Work: Evidence

Income and Wealth of Euro Area Households in Times of Ultra- Loose Monetary Policy Stylised Facts from National and Financial Accounts Data Banca d Italia Conference: How Financial Systems Work: Evidence

BANK LENDING SURVEY Results for Portugal January 2017

BANK LENDING SURVEY Results for Portugal January 2017 I. Overall assessment According to the results of the January survey conducted on the five banking groups included in the Portuguese sample, credit

BANK LENDING SURVEY Results for Portugal January 2017 I. Overall assessment According to the results of the January survey conducted on the five banking groups included in the Portuguese sample, credit

Survey on Access to Finance

Survey on Access to Finance Article published in the Annual Report 2014, pp. 33-39 BOX 1: SURVEY ON ACCESS TO FINANCE (SAFE) 1 Small and medium-sized enterprises (SME) form the backbone of the European

Survey on Access to Finance Article published in the Annual Report 2014, pp. 33-39 BOX 1: SURVEY ON ACCESS TO FINANCE (SAFE) 1 Small and medium-sized enterprises (SME) form the backbone of the European

Monetary Policy in Euroland

Monetary Policy in Euroland Asymmetric shocks Perfect asymmetry : positive shock in one country is offset by a negative shock in the other country. The ECB, which is concerned with price stability and

Monetary Policy in Euroland Asymmetric shocks Perfect asymmetry : positive shock in one country is offset by a negative shock in the other country. The ECB, which is concerned with price stability and

Jürgen Stark, Markus K. Brunnermeier, Paul Tucker, Jaime Caruana, Vítor Constâncio (Chair) (from left to right)

(from left to right)") Jürgen Stark, Markus K. Brunnermeier, Paul Tucker, Jaime Caruana, Vítor Constâncio (Chair) (from left to right) 14 SESSION 1 OPTIMIZING THE CURRENCY AREA BY MARKUS K. BRUNNERMEIER, PRINCETON UNIVERSITY

Jürgen Stark, Markus K. Brunnermeier, Paul Tucker, Jaime Caruana, Vítor Constâncio (Chair) (from left to right) 14 SESSION 1 OPTIMIZING THE CURRENCY AREA BY MARKUS K. BRUNNERMEIER, PRINCETON UNIVERSITY

ECB MONETARY POLICY DURING THE FINANCIAL CRISIS AND ASSET PRICE DEVELOPMENTS

Box 7 MONETARY POLICY DURING THE FINANCIAL CRISIS AND ASSET PRICE The has responded swiftly and decisively to the crisis and the subsequent deterioration in economic, monetary and conditions with the aim

Box 7 MONETARY POLICY DURING THE FINANCIAL CRISIS AND ASSET PRICE The has responded swiftly and decisively to the crisis and the subsequent deterioration in economic, monetary and conditions with the aim

3 Lower interest rates and sectoral changes in interest income

Chart A 3 Lower interest rates and sectoral changes in interest income Euro area balance sheet and euro area property income This box describes the impact of the decline in interest rates on interest income

Chart A 3 Lower interest rates and sectoral changes in interest income Euro area balance sheet and euro area property income This box describes the impact of the decline in interest rates on interest income

Rescuing the Interest Rate Pass Through: Role of Unconventional Policies & Banks Financing Choices

Rescuing the Interest Rate Pass Through: Role of Unconventional Policies & Banks Financing Choices Francesco Paolo Mongelli (ECB & Goethe Univ.) ASSOCIATION FOR COMPARATIVE ECONOMIC STUDIES Poster Session,

Rescuing the Interest Rate Pass Through: Role of Unconventional Policies & Banks Financing Choices Francesco Paolo Mongelli (ECB & Goethe Univ.) ASSOCIATION FOR COMPARATIVE ECONOMIC STUDIES Poster Session,

Corporate leverage and investment in the aftermath of the financial crisis

ECB-UNRESTRICTED FINAL Corporate leverage and investment in the aftermath of the financial crisis Philip Vermeulen European Central Bank Directorate General Research Copyright rests with the author. All

ECB-UNRESTRICTED FINAL Corporate leverage and investment in the aftermath of the financial crisis Philip Vermeulen European Central Bank Directorate General Research Copyright rests with the author. All

The ECB s Strategy in Good and Bad Times Massimo Rostagno European Central Bank

The ECB s Strategy in Good and Bad Times Massimo Rostagno European Central Bank The views expressed herein are those of the presenter only and do not necessarily reflect those of the ECB or the European

The ECB s Strategy in Good and Bad Times Massimo Rostagno European Central Bank The views expressed herein are those of the presenter only and do not necessarily reflect those of the ECB or the European

Towards a Stronger EMU: Recent Developments in Monetary Policy and EMU Governance Reform

Towards a Stronger EMU: Recent Developments in Monetary Policy and EMU Governance Reform Gilles Noblet Deputy Director General DG International and European Relations European Central Bank Presentation

Towards a Stronger EMU: Recent Developments in Monetary Policy and EMU Governance Reform Gilles Noblet Deputy Director General DG International and European Relations European Central Bank Presentation

Understanding Global Liquidity

Understanding Global Liquidity Boris Hofmann Bank for International Settlements Seminar presentation at the National Bank of Poland 13 May 214 The opinions are those of the author only and do not necessarily

Understanding Global Liquidity Boris Hofmann Bank for International Settlements Seminar presentation at the National Bank of Poland 13 May 214 The opinions are those of the author only and do not necessarily

The ECB and The Fed. How Did They React to the Crisis? Executive Director Monetary and Statistics Department. 11 July 2012, Prague

The ECB and The Fed How Did They React to the Crisis? Tomáš Holub Executive Director Monetary and Statistics Department 11 July 2012, Prague Outline Interest rate response to the crisis Unconventional

The ECB and The Fed How Did They React to the Crisis? Tomáš Holub Executive Director Monetary and Statistics Department 11 July 2012, Prague Outline Interest rate response to the crisis Unconventional

SURVEY ON ACCESS TO FINANCE (SAFE) IN 2015

IN 2015") SURVEY ON ACCESS TO FINANCE (SAFE) IN 2015 Article published in the Quarterly Review 2016:1, pp. 80-88 BOX 6: SURVEY ON ACCESS TO FINANCE (SAFE) IN 2015 1 In Malta the reliance of the non-financial business

SURVEY ON ACCESS TO FINANCE (SAFE) IN 2015 Article published in the Quarterly Review 2016:1, pp. 80-88 BOX 6: SURVEY ON ACCESS TO FINANCE (SAFE) IN 2015 1 In Malta the reliance of the non-financial business

Monetary policy of the ECB, its concepts and tools

Monetary policy of the ECB, its concepts and tools Frankfurt am Main, 20 September 2011 Markus A. Schmidt Directorate Monetary Policy 1 Disclaimer The views expressed are those of the presenter and should

Monetary policy of the ECB, its concepts and tools Frankfurt am Main, 20 September 2011 Markus A. Schmidt Directorate Monetary Policy 1 Disclaimer The views expressed are those of the presenter and should

The crisis of the Sovereign Debt markets and its impact on the Banking System: the Italian case

The crisis of the Sovereign Debt markets and its impact on the Banking System: the Italian case January, 19 2012 Maria Cannata Director General - Public Debt Management Introduction In the case of Italy,

The crisis of the Sovereign Debt markets and its impact on the Banking System: the Italian case January, 19 2012 Maria Cannata Director General - Public Debt Management Introduction In the case of Italy,

Recent developments and challenges for the Portuguese economy

Recent developments and challenges for the Portuguese economy Carlos Name da Job Silva Costa Governor 13 January 214 Seminar National Seminar Bank name of Poland 19 June 215 Outline 1. Growing imbalances

Recent developments and challenges for the Portuguese economy Carlos Name da Job Silva Costa Governor 13 January 214 Seminar National Seminar Bank name of Poland 19 June 215 Outline 1. Growing imbalances

FINANCIAL MARKETS IN EARLY AUGUST 2011 AND THE ECB S MONETARY POLICY MEASURES

Chart 28 Implied forward overnight interest rates (percentages per annum; daily data) 5. 4.5 4. 3.5 3. 2.5 2. 1.5 1..5 7 September 211 31 May 211.. 211 213 215 217 219 221 Sources:, EuroMTS (underlying

Chart 28 Implied forward overnight interest rates (percentages per annum; daily data) 5. 4.5 4. 3.5 3. 2.5 2. 1.5 1..5 7 September 211 31 May 211.. 211 213 215 217 219 221 Sources:, EuroMTS (underlying

Macroeconomic Implications of Financial Frictions in the Euro Zone: Lessons from Canada

THE TWENTIETH DUBROVNIK ECONOMIC CONFERENCE Organized by the Croatian National Bank Pierre L. Siklos Macroeconomic Implications of Financial Frictions in the Euro Zone: Lessons from Canada Hotel "Grand

THE TWENTIETH DUBROVNIK ECONOMIC CONFERENCE Organized by the Croatian National Bank Pierre L. Siklos Macroeconomic Implications of Financial Frictions in the Euro Zone: Lessons from Canada Hotel "Grand

MA Advanced Macroeconomics: 12. Default Risk, Collateral and Credit Rationing

MA Advanced Macroeconomics: 12. Default Risk, Collateral and Credit Rationing Karl Whelan School of Economics, UCD Spring 2016 Karl Whelan (UCD) Default Risk and Credit Rationing Spring 2016 1 / 39 Moving

MA Advanced Macroeconomics: 12. Default Risk, Collateral and Credit Rationing Karl Whelan School of Economics, UCD Spring 2016 Karl Whelan (UCD) Default Risk and Credit Rationing Spring 2016 1 / 39 Moving

Non-standard monetary policy in the euro area Economics Roundtable discussion (8 September 2017)

") Non-standard monetary policy in the euro area Economics Roundtable discussion (8 September 2017) Gillian Phelan Outline Monetary policy action Interest rate policy Non-standard measures Monetary policy

Non-standard monetary policy in the euro area Economics Roundtable discussion (8 September 2017) Gillian Phelan Outline Monetary policy action Interest rate policy Non-standard measures Monetary policy

ARTICLES THE ECB S MONETARY POLICY STANCE DURING THE FINANCIAL CRISIS

ARTICLES THE S MONETARY POLICY STANCE DURING THE FINANCIAL CRISIS The s assessment of its monetary policy stance is essential for the preparation of its monetary policy decisions. That assessment aims

ARTICLES THE S MONETARY POLICY STANCE DURING THE FINANCIAL CRISIS The s assessment of its monetary policy stance is essential for the preparation of its monetary policy decisions. That assessment aims

Information in Financial Market Indicators: An Overview

Information in Financial Market Indicators: An Overview By Gerard O Reilly 1 ABSTRACT Asset prices can provide central banks with valuable information regarding market expectations of macroeconomic variables.

Information in Financial Market Indicators: An Overview By Gerard O Reilly 1 ABSTRACT Asset prices can provide central banks with valuable information regarding market expectations of macroeconomic variables.

Economic consequences of high public debt and lessons learned from past episodes

ECB-RESTRICTED Economic consequences of high public debt and lessons learned from past episodes Presented by Cristina Checherita-Westphal Pascal Jacquinot Based on joint work with ESCB WGPF Team ECFIN

ECB-RESTRICTED Economic consequences of high public debt and lessons learned from past episodes Presented by Cristina Checherita-Westphal Pascal Jacquinot Based on joint work with ESCB WGPF Team ECFIN

The Financial System: Opportunities and Dangers

CHAPTER 20 : Opportunities and Dangers Modified for ECON 2204 by Bob Murphy 2016 Worth Publishers, all rights reserved IN THIS CHAPTER, YOU WILL LEARN: the functions a healthy financial system performs

CHAPTER 20 : Opportunities and Dangers Modified for ECON 2204 by Bob Murphy 2016 Worth Publishers, all rights reserved IN THIS CHAPTER, YOU WILL LEARN: the functions a healthy financial system performs

PORTUGUESE BANKING SECTOR OVERVIEW

PORTUGUESE BANKING SECTOR OVERVIEW AGENDA I. Importance of the banking sector for the economy II. III. Credit activity Funding IV. Solvency V. State guarantee and recapitalisation schemes for credit institutions

PORTUGUESE BANKING SECTOR OVERVIEW AGENDA I. Importance of the banking sector for the economy II. III. Credit activity Funding IV. Solvency V. State guarantee and recapitalisation schemes for credit institutions

HOUSEHOLDS INDEBTEDNESS: A MICROECONOMIC ANALYSIS BASED ON THE RESULTS OF THE HOUSEHOLDS FINANCIAL AND CONSUMPTION SURVEY*

HOUSEHOLDS INDEBTEDNESS: A MICROECONOMIC ANALYSIS BASED ON THE RESULTS OF THE HOUSEHOLDS FINANCIAL AND CONSUMPTION SURVEY* Sónia Costa** Luísa Farinha** 133 Abstract The analysis of the Portuguese households

HOUSEHOLDS INDEBTEDNESS: A MICROECONOMIC ANALYSIS BASED ON THE RESULTS OF THE HOUSEHOLDS FINANCIAL AND CONSUMPTION SURVEY* Sónia Costa** Luísa Farinha** 133 Abstract The analysis of the Portuguese households

Sovereign Stress, Non-conventional Monetary Policy, and SME Access to Finance

Sovereign Stress, Non-conventional Monetary Policy, and SME Access to Finance Annalisa Ferrando, Alexander Popov and Gregory F. Udell Presented at RIETI-MoFiR-Hitotsubashi-JFC International Workshop on

Sovereign Stress, Non-conventional Monetary Policy, and SME Access to Finance Annalisa Ferrando, Alexander Popov and Gregory F. Udell Presented at RIETI-MoFiR-Hitotsubashi-JFC International Workshop on

Peter Praet: Preserving monetary accommodation in times of normalisation

Peter Praet: Preserving monetary accommodation in times of normalisation Speech by Mr Peter Praet, Member of the Executive Board of the European Central Bank, at the UBS Conference, London, 13 November

Peter Praet: Preserving monetary accommodation in times of normalisation Speech by Mr Peter Praet, Member of the Executive Board of the European Central Bank, at the UBS Conference, London, 13 November

António Afonso, Jorge Silva Debt crisis and 10-year sovereign yields in Ireland and in Portugal

Department of Economics António Afonso, Jorge Silva Debt crisis and 1-year sovereign yields in Ireland and in Portugal WP6/17/DE/UECE WORKING PAPERS ISSN 183-181 Debt crisis and 1-year sovereign yields

Department of Economics António Afonso, Jorge Silva Debt crisis and 1-year sovereign yields in Ireland and in Portugal WP6/17/DE/UECE WORKING PAPERS ISSN 183-181 Debt crisis and 1-year sovereign yields

Insights on the Greek economy from the 3D macro model

Insights on the Greek economy from the 3D macro model Hiona Balfoussia * and Dimitris Papageorgiou ** This version: April 26 Word count (excluding first page, tables and figures): 274 Abstract The DSGE

Insights on the Greek economy from the 3D macro model Hiona Balfoussia * and Dimitris Papageorgiou ** This version: April 26 Word count (excluding first page, tables and figures): 274 Abstract The DSGE

Current Situation, Outlook, and Challenges

's Economy: Current Situation, Outlook, and Challenges November 8, Masaaki Shirakawa Governor of the Bank of Chart The Bank of 's Economic and Price Forecasts A. Real GDP B. CPI (all items less fresh food)..

's Economy: Current Situation, Outlook, and Challenges November 8, Masaaki Shirakawa Governor of the Bank of Chart The Bank of 's Economic and Price Forecasts A. Real GDP B. CPI (all items less fresh food)..

Scenario for the European Insurance and Occupational Pensions Authority s EU-wide insurance stress test in 2016

17 March 2016 ECB-PUBLIC Scenario for the European Insurance and Occupational Pensions Authority s EU-wide insurance stress test in 2016 Introduction In accordance with its mandate, the European Insurance

17 March 2016 ECB-PUBLIC Scenario for the European Insurance and Occupational Pensions Authority s EU-wide insurance stress test in 2016 Introduction In accordance with its mandate, the European Insurance

Recent liquidity injections by the European Central Bank have brought relief to the banking system and sovereign bond markets.

OBSERVATION TD Economics February 29, 2 DELEVERAGING BEGETS WEAK ECONOMIES ACROSS EURO ZONE PERIPHERY Highlights Recent liquidity injections by the European Central Bank have brought relief to the banking

OBSERVATION TD Economics February 29, 2 DELEVERAGING BEGETS WEAK ECONOMIES ACROSS EURO ZONE PERIPHERY Highlights Recent liquidity injections by the European Central Bank have brought relief to the banking

The European Economic Crisis

The European Economic Crisis Patrick Leblond Teaching about the EU in the Classroom Centre for European Studies Carleton University, 25 November 2013 Outline Before the crisis European economic integration

The European Economic Crisis Patrick Leblond Teaching about the EU in the Classroom Centre for European Studies Carleton University, 25 November 2013 Outline Before the crisis European economic integration

Incorporating Macro-Financial Linkages into Forecasts Using Financial Conditions Indices: The Case of France

WP/17/269 Incorporating Macro-Financial Linkages into Forecasts Using Financial Conditions Indices: The Case of France by Piyabha Kongsamut, Christian Mumssen, Anne-Charlotte Paret, Thierry Tressel IMF

WP/17/269 Incorporating Macro-Financial Linkages into Forecasts Using Financial Conditions Indices: The Case of France by Piyabha Kongsamut, Christian Mumssen, Anne-Charlotte Paret, Thierry Tressel IMF

Irish Retail Interest Rates: Why do they differ from the rest of Europe?

Irish Retail Interest Rates: Why do they differ from the rest of Europe? By Rory McElligott * ABSTRACT In this paper, we compare Irish retail interest rates with similar rates in the euro area, and examine

Irish Retail Interest Rates: Why do they differ from the rest of Europe? By Rory McElligott * ABSTRACT In this paper, we compare Irish retail interest rates with similar rates in the euro area, and examine

Housing Market Heterogeneity in a Monetary Union

Housing Market Heterogeneity in a Monetary Union Margarita Rubio Bank of Spain SAE Zaragoza, 28 Introduction Costs and bene ts of monetary unions is a big question Di erence national characteristics and

Housing Market Heterogeneity in a Monetary Union Margarita Rubio Bank of Spain SAE Zaragoza, 28 Introduction Costs and bene ts of monetary unions is a big question Di erence national characteristics and

HOUSEHOLDS LENDING MARKET IN THE ENLARGED EUROPE. Debora Revoltella and Fabio Mucci copyright with the author New Europe Research

HOUSEHOLDS LENDING MARKET IN THE ENLARGED EUROPE Debora Revoltella and Fabio Mucci copyright with the author New Europe Research ECFin Workshop on Housing and mortgage markets and the EU economy, Brussels,

HOUSEHOLDS LENDING MARKET IN THE ENLARGED EUROPE Debora Revoltella and Fabio Mucci copyright with the author New Europe Research ECFin Workshop on Housing and mortgage markets and the EU economy, Brussels,

Fiscal Policies in High Debt

Antonella Cavallo Pietro Dallari Antonio Ribba Fiscal Policies in High Debt Euro-Area Countries * ) Springer Contents 1 Introduction 1 1.1 The Controversial Macroeconomic Outcomes of Fiscal Policy... 1

Antonella Cavallo Pietro Dallari Antonio Ribba Fiscal Policies in High Debt Euro-Area Countries * ) Springer Contents 1 Introduction 1 1.1 The Controversial Macroeconomic Outcomes of Fiscal Policy... 1

Is the Euro Crisis Over?

Is the Euro Crisis Over? Klaus Regling, Managing Director, ESM International Center for Monetary and Banking Studies, Geneva 25 March 2014 Eight reasons for the sovereign debt crisis 1. Member States did

Is the Euro Crisis Over? Klaus Regling, Managing Director, ESM International Center for Monetary and Banking Studies, Geneva 25 March 2014 Eight reasons for the sovereign debt crisis 1. Member States did

Bank lending survey for the euro area

Bank lending survey for the euro area Glossary To assist respondent banks in filling out the questionnaire, this glossary defines the most important terminology used in the bank lending survey. This glossary

Bank lending survey for the euro area Glossary To assist respondent banks in filling out the questionnaire, this glossary defines the most important terminology used in the bank lending survey. This glossary

Economic and monetary. developments. The results of the euro area bank lending survey for the second quarter of 2014

Economic and monetary Monetary and financial Box 2 The results of the euro area bank lending survey for the second quarter of 214 This box summarises the main results of the euro area bank lending survey

Economic and monetary Monetary and financial Box 2 The results of the euro area bank lending survey for the second quarter of 214 This box summarises the main results of the euro area bank lending survey

Negative Interest Rate Policies: Sources and Implications

Negative Interest Rate Policies: Sources and Implications November 4, 216 Marc Stocker Based on a recently published CEPR / World Bank Working Paper Disclaimer! The views presented here are those of the

Negative Interest Rate Policies: Sources and Implications November 4, 216 Marc Stocker Based on a recently published CEPR / World Bank Working Paper Disclaimer! The views presented here are those of the

BANK LENDING SURVEY. October de Results for Portugal

BANK LENDING SURVEY October de 13 Results for Portugal I. Overall assessment In general, both credit standards and conditions and terms applied in to companies and households remained broadly unchanged,

BANK LENDING SURVEY October de 13 Results for Portugal I. Overall assessment In general, both credit standards and conditions and terms applied in to companies and households remained broadly unchanged,

Can the euro still be saved? Morning session: the threats

Can the euro still be saved? Morning session: the threats Anton Brender and Florence Pisani Berlin, June 17 1 Fiscal and monetary policies: some problems have not yet been fully fixed! Budget balance Budget

Can the euro still be saved? Morning session: the threats Anton Brender and Florence Pisani Berlin, June 17 1 Fiscal and monetary policies: some problems have not yet been fully fixed! Budget balance Budget

Portfolio Rebalancing and the Transmission of Large-Scale Asset Programs: Evidence from the Euro Area

Rubric Ugo Albertazzi Banca d Italia Bo Becker University of Stockholm Miguel Boucinha European Central Bank Portfolio Rebalancing and the Transmission of Large-Scale Asset Programs: Evidence from the

Rubric Ugo Albertazzi Banca d Italia Bo Becker University of Stockholm Miguel Boucinha European Central Bank Portfolio Rebalancing and the Transmission of Large-Scale Asset Programs: Evidence from the

Vítor Constâncio ECB Vice-President. Fragmentation and Rebalancing in the euro area

Vítor Constâncio ECB Vice-President Fragmentation and Rebalancing in the euro area Joint EC-ECB Conference on Financial Integration Brussels, 25 April 2013 Introduction Rubric In the first half of 2012,

Vítor Constâncio ECB Vice-President Fragmentation and Rebalancing in the euro area Joint EC-ECB Conference on Financial Integration Brussels, 25 April 2013 Introduction Rubric In the first half of 2012,

MONETARY POLICY IN THE EURO AREA: THE EXPERIENCE OF SPAIN

MONETARY POLICY IN THE EURO AREA: THE EXPERIENCE OF SPAIN Óscar Arce Associate Director General Economics and Research 14 July 2017 XXVI International Financial Congress St. Petersburg ADG ECONOMICS AND

MONETARY POLICY IN THE EURO AREA: THE EXPERIENCE OF SPAIN Óscar Arce Associate Director General Economics and Research 14 July 2017 XXVI International Financial Congress St. Petersburg ADG ECONOMICS AND

COUNCIL OF THE EUROPEAN UNION. Brussels, 9 June /09 ADD 1 ECOFIN 429 UEM 158 EF 89 RC 9

COUNCIL OF THE EUROPEAN UNION Brussels, 9 June 2009 10772/09 ADD 1 ECOFIN 429 UEM 158 EF 89 RC 9 NOTE from: to: Subject: Council (Ecofin) European Council Annex to the Council (Ecofin) Report to the 18-19

COUNCIL OF THE EUROPEAN UNION Brussels, 9 June 2009 10772/09 ADD 1 ECOFIN 429 UEM 158 EF 89 RC 9 NOTE from: to: Subject: Council (Ecofin) European Council Annex to the Council (Ecofin) Report to the 18-19

The Transmission Mechanism of Credit Support Policies in the Euro Area

The Transmission Mechanism of Credit Support Policies in the Euro Area ECB workshop on Monetary policy in non-standard times Frankfurt, 12 September 2016 INTERN J. Boeckx (NBB) M. De Sola Perea (NBB) G.

The Transmission Mechanism of Credit Support Policies in the Euro Area ECB workshop on Monetary policy in non-standard times Frankfurt, 12 September 2016 INTERN J. Boeckx (NBB) M. De Sola Perea (NBB) G.

The impact of negative rates on bank balance sheets: Evidence from the euro area

The impact of negative rates on bank balance sheets: Evidence from the euro area discussion by Angela Maddaloni (ECB) and José-Luis Peydró (ICREA-UPF, CREI, Barcelona GSE, CEPR) European Central Bank Workshop

The impact of negative rates on bank balance sheets: Evidence from the euro area discussion by Angela Maddaloni (ECB) and José-Luis Peydró (ICREA-UPF, CREI, Barcelona GSE, CEPR) European Central Bank Workshop

Will the Troika Adjustment Program of Internal Devaluation Work? Dr. Aidan Regan Blog: Euro-Irish Public Policy

The Origins and Impact of the Eurozone Crisis Will the Troika Adjustment Program of Internal Devaluation Work? Dr. Aidan Regan Blog: Euro-Irish Public Policy Outline Introduction The Origins of the Eurozone

The Origins and Impact of the Eurozone Crisis Will the Troika Adjustment Program of Internal Devaluation Work? Dr. Aidan Regan Blog: Euro-Irish Public Policy Outline Introduction The Origins of the Eurozone

Cross-country risk-sharing in the EMU:

Cross-country risk-sharing in the EMU: Current mechanism and new proposals Cinzia Alcidi FIRSTRUN CONFERENCE Fiscal Rules, Stabilization and Risk-Sharing in the EMU Helsinki, 3 October, 2017 CEPS_thinktank

Cross-country risk-sharing in the EMU: Current mechanism and new proposals Cinzia Alcidi FIRSTRUN CONFERENCE Fiscal Rules, Stabilization and Risk-Sharing in the EMU Helsinki, 3 October, 2017 CEPS_thinktank

Fragmentation of the European financial market and the cost of bank financing

Fragmentation of the European financial market and the cost of bank financing Joaquín Maudos 1 European market fragmentation following the crisis has resulted in a widening of borrowing costs across Euro

Fragmentation of the European financial market and the cost of bank financing Joaquín Maudos 1 European market fragmentation following the crisis has resulted in a widening of borrowing costs across Euro

Rakan Mosely Head of Financial Markets Phone: (0)

") Rakan Mosely Head of Financial Markets Phone: (0)20 7803 1400 rmosely@oxfordeconomics.com The ECB s TLTROs: bazooka or peashooter? Ben May Senior Eurozone Economist bmay@oxfordeconomics.com June 2014 Outline

Rakan Mosely Head of Financial Markets Phone: (0)20 7803 1400 rmosely@oxfordeconomics.com The ECB s TLTROs: bazooka or peashooter? Ben May Senior Eurozone Economist bmay@oxfordeconomics.com June 2014 Outline

What is the economic outlook for OECD countries? An interim assessment

What is the economic outlook for OECD countries? An interim assessment Paris, 3 rd September 2009 11h00 Paris time Jorgen Elmeskov Acting Head of Economics Department www.oecd.org/oecdeconomicoutlook 1.

What is the economic outlook for OECD countries? An interim assessment Paris, 3 rd September 2009 11h00 Paris time Jorgen Elmeskov Acting Head of Economics Department www.oecd.org/oecdeconomicoutlook 1.

For the second quarter of 2019, banks do not anticipate major changes in credit standards applied on loans.

Bank Lending Survey Results for Portugal April 219 The Portuguese banks that participate in the survey indicated that the lending policy set for the first quarter of 219 remained broadly unchanged compared

Bank Lending Survey Results for Portugal April 219 The Portuguese banks that participate in the survey indicated that the lending policy set for the first quarter of 219 remained broadly unchanged compared

Inflation Stabilization and Default Risk in a Currency Union. OKANO, Eiji Nagoya City University at Otaru University of Commerce on Aug.

Inflation Stabilization and Default Risk in a Currency Union OKANO, Eiji Nagoya City University at Otaru University of Commerce on Aug. 10, 2014 1 Introduction How do we conduct monetary policy in a currency

Inflation Stabilization and Default Risk in a Currency Union OKANO, Eiji Nagoya City University at Otaru University of Commerce on Aug. 10, 2014 1 Introduction How do we conduct monetary policy in a currency

Cyclical Convergence and Divergence in the Euro Area

Cyclical Convergence and Divergence in the Euro Area Presentation by Val Koromzay, Director for Country Studies, OECD to the Brussels Forum, April 2004 1 1 I. Introduction: Why is the issue important?

Cyclical Convergence and Divergence in the Euro Area Presentation by Val Koromzay, Director for Country Studies, OECD to the Brussels Forum, April 2004 1 1 I. Introduction: Why is the issue important?

Fiscal union and the need for accurate macroeconomic statistics. Guntram Wolff, Bruegel Luxembourg 26 Jan 2016

Fiscal union and the need for accurate macroeconomic statistics Guntram Wolff, Bruegel Luxembourg 26 Jan 2016 Outline The euro area crisis The new institutional setup Importance of macroeconomic statistics

Fiscal union and the need for accurate macroeconomic statistics Guntram Wolff, Bruegel Luxembourg 26 Jan 2016 Outline The euro area crisis The new institutional setup Importance of macroeconomic statistics

Euro area economic developments from monetary policy maker s perspective

Euro area economic developments from monetary policy maker s perspective Member of Executive Board Structure of the presentation: 1. Where do we come from? ECB s monetary policy set up and main reactions

Euro area economic developments from monetary policy maker s perspective Member of Executive Board Structure of the presentation: 1. Where do we come from? ECB s monetary policy set up and main reactions

Portuguese Banking System: latest developments. 2 nd quarter 2018

Portuguese Banking System: latest developments 2 nd quarter 218 Lisbon, 218 www.bportugal.pt Prepared with data available up to 26 th September of 218. Macroeconomic indicators and banking system data

Portuguese Banking System: latest developments 2 nd quarter 218 Lisbon, 218 www.bportugal.pt Prepared with data available up to 26 th September of 218. Macroeconomic indicators and banking system data

International Money and Banking: 13. Default Risk and Collateral

International Money and Banking: 13. Default Risk and Collateral Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) Default Risk and Collateral Spring 2018 1 / 13 Moving Beyond Risk-Free

International Money and Banking: 13. Default Risk and Collateral Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) Default Risk and Collateral Spring 2018 1 / 13 Moving Beyond Risk-Free

TIGER: Tracking Indexes for the Global Economic Recovery By Eswar Prasad and Karim Foda

TIGER: Tracking Indexes for the Global Economic Recovery By Eswar Prasad and Karim Foda Technical Appendix Methodology In our analysis, we employ a statistical procedure called Principal Component Analysis

TIGER: Tracking Indexes for the Global Economic Recovery By Eswar Prasad and Karim Foda Technical Appendix Methodology In our analysis, we employ a statistical procedure called Principal Component Analysis

Introduction. Stijn Ferrari Glenn Schepens

Loans to non-financial corporations : what can we learn from credit condition surveys? Stijn Ferrari Glenn Schepens Patrick Van Roy Introduction Bank lending is an important determinant of economic growth

Loans to non-financial corporations : what can we learn from credit condition surveys? Stijn Ferrari Glenn Schepens Patrick Van Roy Introduction Bank lending is an important determinant of economic growth

Europe s Response to the Sovereign Debt Crisis. Christophe Frankel, CFO of EFSF ICMA Conference, Milan 24 May 2012

Europe s Response to the Sovereign Debt Crisis Christophe Frankel, CFO of EFSF ICMA Conference, Milan 24 May 2012 The reasons for sovereign debt crisis 1 Member States did not fully accept the political

Europe s Response to the Sovereign Debt Crisis Christophe Frankel, CFO of EFSF ICMA Conference, Milan 24 May 2012 The reasons for sovereign debt crisis 1 Member States did not fully accept the political

Impact of US real estate crisis and financial market turbulence on the economy

Allianz Dresdner Economic Research Working Paper No.: 91, 18. September 2007 Authors: Thomas Hofmann, Dr. Rolf Schneider Impact of US real estate crisis and financial market turbulence on the economy What

Allianz Dresdner Economic Research Working Paper No.: 91, 18. September 2007 Authors: Thomas Hofmann, Dr. Rolf Schneider Impact of US real estate crisis and financial market turbulence on the economy What

JPMorgan Europe High Yield Bond Fund

AVAILABLE FOR PUBLIC CIRCULATION NEW JPMorgan Europe High Yield Bond Fund Asset Management Company of the Year, Asia + Important information 1. The Fund invests at least 7 in European and non-european

AVAILABLE FOR PUBLIC CIRCULATION NEW JPMorgan Europe High Yield Bond Fund Asset Management Company of the Year, Asia + Important information 1. The Fund invests at least 7 in European and non-european

Channels of Monetary Policy Transmission. Konstantinos Drakos, MacroFinance, Monetary Policy Transmission 1

Channels of Monetary Policy Transmission Konstantinos Drakos, MacroFinance, Monetary Policy Transmission 1 Discusses the transmission mechanism of monetary policy, i.e. how changes in the central bank

Channels of Monetary Policy Transmission Konstantinos Drakos, MacroFinance, Monetary Policy Transmission 1 Discusses the transmission mechanism of monetary policy, i.e. how changes in the central bank

Discussion of Confidence Cycles and Liquidity Hoarding by Volha Audzei (2016)

") Discussion of Confidence Cycles and Liquidity Hoarding by Volha Audzei (2016) Niki Papadopoulou 1 Central Bank of Cyprus CNB Research Open Day, 15 May 2017 1 The views expressed are solely my own and do

Discussion of Confidence Cycles and Liquidity Hoarding by Volha Audzei (2016) Niki Papadopoulou 1 Central Bank of Cyprus CNB Research Open Day, 15 May 2017 1 The views expressed are solely my own and do

Impact of the Great Recession and the Role of Assistance Programmes in EMU Countries

UNIVERSIDADE DE TRÁS-OS-MONTES E ALTO DOURO Impact of the Great Recession and the Role of Assistance Programmes in EMU Countries Leonida Correia and Patrícia Martins Centre for Transdisciplinary Development

UNIVERSIDADE DE TRÁS-OS-MONTES E ALTO DOURO Impact of the Great Recession and the Role of Assistance Programmes in EMU Countries Leonida Correia and Patrícia Martins Centre for Transdisciplinary Development

Economic and Monetary Policy Perspectives for Europe and the Euro Area

Economic and Monetary Policy Perspectives for Europe and the Euro Area Peter Mooslechner Executive Director and Member of the Governing Board Oesterreichische Nationalbank Roundtable Discussion, Austrian

Economic and Monetary Policy Perspectives for Europe and the Euro Area Peter Mooslechner Executive Director and Member of the Governing Board Oesterreichische Nationalbank Roundtable Discussion, Austrian

Macro-Financial Stability and the Euro. Philip R. Lane, Euro At 20 Conference

Macro-Financial Stability and the Euro Philip R. Lane, Euro At 20 Conference Two Lessons from Twenty Years of the Euro Avoid accumulation of excessive imbalances: pre-emptive use of fiscal and macroprudential

Macro-Financial Stability and the Euro Philip R. Lane, Euro At 20 Conference Two Lessons from Twenty Years of the Euro Avoid accumulation of excessive imbalances: pre-emptive use of fiscal and macroprudential

STRUCTURAL SHIFTS AND CHALLENGES IN THE GLOBAL ECONOMY M I C H A E L S P E N C E N E W D E L H I J A N U A R Y

STRUCTURAL SHIFTS AND CHALLENGES IN THE GLOBAL ECONOMY M I C H A E L S P E N C E N E W D E L H I J A N U A R Y 2 0 1 2 2 3 What is the Next Convergence? Before the Industrial Revolution 200 years of divergence

STRUCTURAL SHIFTS AND CHALLENGES IN THE GLOBAL ECONOMY M I C H A E L S P E N C E N E W D E L H I J A N U A R Y 2 0 1 2 2 3 What is the Next Convergence? Before the Industrial Revolution 200 years of divergence

Open Economy AS/AD: Applications

Open Economy AS/AD: Applications Econ 309 Martin Ellison UBC Agenda and References Trilemma Jones, chapter 20, section 7 Euro crisis Jones, chapter 20, section 8 Global imbalances Jones, chapter 29, section

Open Economy AS/AD: Applications Econ 309 Martin Ellison UBC Agenda and References Trilemma Jones, chapter 20, section 7 Euro crisis Jones, chapter 20, section 8 Global imbalances Jones, chapter 29, section

June 2012 Monetary policy in the United States and in the euro area during the crisis 39

Monetary policy in the United States and in the euro area during the crisis N. Cordemans S. Ide Introduction On both sides of the Atlantic, the initial shocks of the financial crisis were experienced in

Monetary policy in the United States and in the euro area during the crisis N. Cordemans S. Ide Introduction On both sides of the Atlantic, the initial shocks of the financial crisis were experienced in

Monetary Policy Operations

Monetary Policy Operations Denis Blenck DG Market Operations Generation uro Students Award Teachers session 24 September 2012 Outline MONETARY POLICY IMPLEMENTATION IN NORMAL TIMES MONETARY POLICY IMPLEMENTATION

Monetary Policy Operations Denis Blenck DG Market Operations Generation uro Students Award Teachers session 24 September 2012 Outline MONETARY POLICY IMPLEMENTATION IN NORMAL TIMES MONETARY POLICY IMPLEMENTATION

The repo market, the public debt management and the implementation of the ECB monetary policy

The repo market, the public debt management and the implementation of the ECB monetary policy Denis Blenck Head of Operations Analysis Division 13th OECD Global Forum 27 November 2003 0 Contents I II Eurosystem

The repo market, the public debt management and the implementation of the ECB monetary policy Denis Blenck Head of Operations Analysis Division 13th OECD Global Forum 27 November 2003 0 Contents I II Eurosystem

Communications Breakdown: The Transmission of Dierent types of ECB Policy Announcements

Communications Breakdown: The Transmission of Dierent types of ECB Policy Announcements Andrew Kane, John H. Rogers and Bo Sun April 27, 218 1 / 27 Background I Large literature using high-frequency changes

Communications Breakdown: The Transmission of Dierent types of ECB Policy Announcements Andrew Kane, John H. Rogers and Bo Sun April 27, 218 1 / 27 Background I Large literature using high-frequency changes

THE CONTAGION EFFECT AND THE RESPONSE OF THE EUROZONE TO THE SOVEREIGN DEBT PROBLEM

THE CONTAGION EFFECT AND THE RESPONSE OF THE EUROZONE TO THE SOVEREIGN DEBT PROBLEM Claudiu Peptine * Claudiu Gabriel Tiganas Dumitru Filipeanu Abstract: This paper addresses a number of phenomena that

THE CONTAGION EFFECT AND THE RESPONSE OF THE EUROZONE TO THE SOVEREIGN DEBT PROBLEM Claudiu Peptine * Claudiu Gabriel Tiganas Dumitru Filipeanu Abstract: This paper addresses a number of phenomena that

Macroeconomic Effects of Unconventional Monetary Policy in the Euro Area

FACULTEIT ECONOMIE EN BEDRIJFSKUNDE TWEEKERKENSTRAAT 2 B-9000 GENT Tel. : 32 - (0)9 264.34.61 Fax. : 32 - (0)9 264.35.92 WORKING PAPER Macroeconomic Effects of Unconventional Monetary Policy in the Euro

FACULTEIT ECONOMIE EN BEDRIJFSKUNDE TWEEKERKENSTRAAT 2 B-9000 GENT Tel. : 32 - (0)9 264.34.61 Fax. : 32 - (0)9 264.35.92 WORKING PAPER Macroeconomic Effects of Unconventional Monetary Policy in the Euro

What does Western Economic Crisis Mean for South Africa?

What does Western Economic Crisis Mean for South Africa? Seeraj Mohamed Corporate Strategy and Industrial Development Research Programme University of the Witwatersrand Context for Europe s Crisis Global

What does Western Economic Crisis Mean for South Africa? Seeraj Mohamed Corporate Strategy and Industrial Development Research Programme University of the Witwatersrand Context for Europe s Crisis Global

The Eurosystem Household Finance and Consumption Survey

ECB-PUBLIC DRAFT The Eurosystem Household Finance and Consumption Survey Carlos Sánchez Muñoz Frankfurt Fudan Financial Research Forum 25 September 2015 ECB-PUBLIC DRAFT ECB-PUBLIC DRAFT Outline 1. Background

ECB-PUBLIC DRAFT The Eurosystem Household Finance and Consumption Survey Carlos Sánchez Muñoz Frankfurt Fudan Financial Research Forum 25 September 2015 ECB-PUBLIC DRAFT ECB-PUBLIC DRAFT Outline 1. Background

BANK LENDING SURVEY Results for Portugal April 2018

BANK LENDING SURVEY Results for Portugal April 2018 I. Overall assessment According to the results of the April 2018 survey of the five banks included in the Portuguese sample, credit standards applied

BANK LENDING SURVEY Results for Portugal April 2018 I. Overall assessment According to the results of the April 2018 survey of the five banks included in the Portuguese sample, credit standards applied

IV SPECIAL FEATURES LIQUIDITY HOARDING AND INTERBANK MARKET SPREADS

B LIQUIDITY HOARDING AND INTERBANK MARKET SPREADS Chart B.1 Three phases in the euro area interbank market Interbank markets play a key role in banks liquidity management and the transmission of monetary

B LIQUIDITY HOARDING AND INTERBANK MARKET SPREADS Chart B.1 Three phases in the euro area interbank market Interbank markets play a key role in banks liquidity management and the transmission of monetary