FY 17 Year-End Fact Sheet

|

|

|

- Erick O’Neal’

- 5 years ago

- Views:

Transcription

1 FY 17 Year-End Fact Sheet University Accounting & Financial Reporting Copyright University of Illinois Office of Business and Financial Services. All rights reserved. No part of this publication may be reproduced or used in any form or by any means graphic, electronic or mechanical, including photocopying, recording, taping or in information storage and retrieval systems without written permission of University of Illinois OBFS. OFFICE OF BUSINESS AND FINANCIAL SERVICES UNIVERSITY ACCOUNTING & FINANCIAL REPORTING 6/20/2017 1

2 Presenters Roger Fredenhagen, CPA Business & Financial Coordinator Jason Bane Senior Business & Financial Coordinator 2

3 Sound Check If you hear audio, please raise your hand. If you are not able to hear us, type your name in the Questions area and click the Send button. Michelle Flack 3

4 Agenda 1. Objectives 2. Fact Sheet Overview 3. Application Tour 4. Fact Sheet Template 5. Case Study 6. Resources 4

5 OBJECTIVES 5

6 Objectives Review the Fact Sheet process Identify components of the Fact Sheet application Explain the information required for the Fact Sheet template Locate resources and contacts 6

7 FACT SHEET OVERVIEW 7

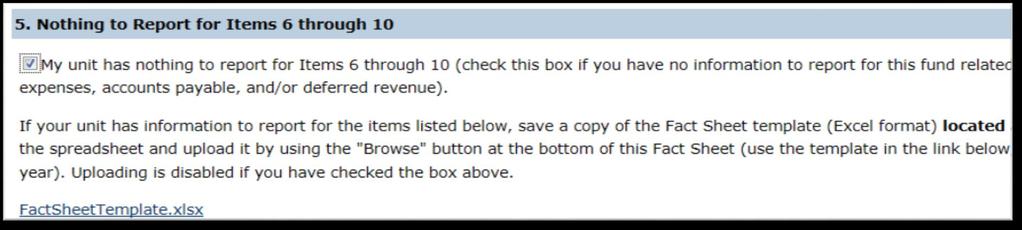

8 What are Fact Sheets? Reflect fund s financial condition As of June 30, 2017 All Self-Supporting Funds Separate Fact Sheet for each fund All DSP/NSP/OHSP practice plan No minimum dollar threshold 8

9 Receive notification Financial Manager Submit Fact Sheet and template Gather financial data 9

10 July 5:00 p.m

11 11

12 12

13 13

14 Review UAFR Accrual entries P14 Accept or return 14

15 APPLICATION TOUR 15

16 16

17 17

18 18

19 19

20 20

21 21

22 QUESTION & ANSWER 22

23 FACT SHEET TEMPLATE 23

24 24

25 25

26 26

27 27

28 28

29 29

30 30

31 31

32 32

33 33

34 QUESTION & ANSWER 34

35 CASE STUDY: Completing The Year-End Fact Sheet 35

36 The Facts Fund performs testing services. On December 31, 2016, fund signs a contract to perform testing services for the Chicago Department of Labor for 1/1/2017 through 12/31/2017. The total compensation for the contract is $100,000. A check is received on January 15, 2017, for $100,000. On May 1, 2017, testing services were performed for Boeing. On June 1, 2017, Boeing was sent an invoice for $25,000. On June 15, 2017, fund received a $10,000 payment from Boeing. On June 1, 2017, three laptop computers totaling $5,000 were ordered. As of June 30, 2017, the computers had not been received nor had any payments been made. The computers were shipped from the merchant on June 15, The testing services performed require a $25 supply kit. A charge of $27.50 per test is built into the service rate. On June 30, 2017, 500 supply kits are on hand. Publishes its quarterly magazine Lab Safety for $5.00 each. Remaining inventory from past issues: January copies, $3.25; April copies $3.25; April copies $

37 QUIZ QUESTIONS 37

38 Quiz Question #1 What dollar amount should be reported for unearned revenue? 38

39 The Facts Fund performs testing services for external customers. On December 31, 2016, fund signed a contract to perform testing services for the Chicago Department of Labor for 1/1/2017 through 12/31/2017. The total compensation for the contract is $100,000. A check is received on January 15, 2017, for $100,

40 Quiz Question #1 What dollar amount should be reported for unearned revenue? Unearned revenue is revenue collected in the current fiscal year for goods/services to be provided in a future fiscal year 40

41 Quiz Question #1 What dollar amount should be reported for unearned revenue? $100,000 is received for services performed for the time period 1/1/17 to 12/31/17. On June 30, 2017, half of the total services revenue is earned. Remaining $50,000 recorded as unearned revenue. 41

42 42

43 Quiz Question #2 What dollar amount should be reported for accounts receivable? 43

44 The Facts Fund performs testing services for external customers. On May 1, 2017, testing services were performed for Boeing. On June 1, 2017, Boeing was sent an invoice for $25,000. On June 15, 2017, fund received a $10,000 payment from Boeing. 44

45 Quiz Question #2 What dollar amount should be reported for accounts receivable? A receivable should be recorded once services have been substantially completed or goods have been delivered, and you have reasonable expectation to receive payment for that service or good. 45

46 Quiz Question #2 What dollar amount should be reported for accounts receivable? On June 1, 2017, a receivable should be recorded for $25,000. On June 15, 2017, a payment was received for $10,000. This would reduce the receivable to $15,000. $15,000 of receivables should be recorded on the template. 46

47 47

48 Quiz Question #3 What dollar amount should be reported for accounts payable? 48

49 The Facts Fund performs testing services for external customers. On June 1, 2017, three laptop computers totaling $5,000 were ordered. As of June 30, 2017, the computers had not been received nor had any payments been made. The computers were shipped from the merchant on June 15,

50 Quiz Question #3 What dollar amount should be reported for accounts payable? A payable should be recorded once legal ownership has transferred from the merchant to the customer. 50

51 Quiz Question #3 It is important to check shipping terms when purchasing tangible goods. FOB shipping point or FOB origin means that the buyer pays shipping cost and takes responsibility for the goods when they leave the seller's premises. FOB destination means that the seller pays shipping costs and remains responsible for the goods until the buyer takes possession. 51

52 52

53 Quiz Question #3 What dollar amount should be reported for accounts payable? If the shipping terms were FOB shipping point or FOB origin, a payable for $5,000 would be required as of June 30, 2017 legal ownership transfers once the computers are shipped. If the shipping terms were FOB destination, a payable wouldn t be recorded until the computers are received. 53

54 NOTE: This example assumes the shipping terms are FOB shipping point" or "FOB origin. 54

55 Quiz Question #4 What dollar amount should be reported for inventory for resale? 55

56 The Facts Fund performs testing services for external customers. The testing services performed require a $25 supply kit. A charge of $27.50 per test is built into the service rate. On June 30, 2017, 500 supply kits are on hand. 56

57 Quiz Question #4 What dollar amount should be reported for inventory for resale? The tangible items in stock and sold as part of your self-supporting activity. Physical count and value as of June 30 th. 57

58 Quiz Question #4 What dollar amount should be reported for inventory for resale? On June30, 2017, 500 supply kits were on hand. The cost of each supply kit was $25. $12,500 of inventory for resale should be recorded on the template (500 kits x $25 = $12,500). 58

59 59

60 Quiz Question #5 What dollar amount should be reported for publications inventory for resale? 60

61 The Facts Fund publishes its quarterly magazine Lab Safety for $5.00 each. Remaining inventory from past issues: January copies, $3.25 April copies, $3.25 April copies, $

62 Quiz Question #5 What dollar amount should be reported for publications inventory for resale? The tangible issues of printed materials for resale. Original publication date and cost Ongoing demand Physical count and value as of June 30 th 62

63 The Facts Fund Lab Safety quarterly magazine for internal and external customers. New issue is released the first of every quarter. Publication cost 2016 $ $3.55 Inventory quantity on June 30 th January issues April issues April issues 63

64 64

65 QUESTION & ANSWER 65

66 RESOURCES 66

67 Year-End Fact Sheet Open Labs Chicago July 18: 9:00am-12:00pm at 723 MAB Springfield July 18: 9:00am-12:00pm at BSB 108 Urbana July 17: 9:00am-12:00pm at Lab #11, 111 E. Green 67

68 68

69 69

70 FZMFUND See the Updating the Financial Manager job aid for steps on how to review and update the financial manager for a Fund. 70

71 71

72 Contacts Self-Supporting Funds Jason Bane Michelle Flack Roger Fredenhagen Anne Larimore Nikki Melander Bridget To UAFR UAFR Who to Ask 72

73 QUESTION & ANSWER 73

74 University Accounting and Financial Reporting THANK YOU! 74

Successfully Managing Self-Supporting Funds

2012 Administrative Leadership Conference Successfully Managing Self-Supporting Funds October 24, 2012 9:30 to 10:45am 1:30 to 2:45pm Leadership Lived by Taking Care of Business through Professional Excellence

2012 Administrative Leadership Conference Successfully Managing Self-Supporting Funds October 24, 2012 9:30 to 10:45am 1:30 to 2:45pm Leadership Lived by Taking Care of Business through Professional Excellence

Understanding Key Accounting Issues. University Accounting & Financial Reporting

Understanding Key Accounting Issues University Accounting & Financial Reporting Workshop Presenters Timisha Luster Resource & Policy Analyst Roger Wade, CPA Business & Financial Coordinator Jason Bane

Understanding Key Accounting Issues University Accounting & Financial Reporting Workshop Presenters Timisha Luster Resource & Policy Analyst Roger Wade, CPA Business & Financial Coordinator Jason Bane

A Fact Sheet must be submitted for each self-supporting or dental/nursing/occupational health service plan fund by 5 p.m. on July 20, 2018.

Fact Sheet Overview A Fact Sheet must be submitted for each self-supporting or dental/nursing/occupational health service plan fund by 5 p.m. on July 20, 2018. All supporting documentation should be kept

Fact Sheet Overview A Fact Sheet must be submitted for each self-supporting or dental/nursing/occupational health service plan fund by 5 p.m. on July 20, 2018. All supporting documentation should be kept

Rent Revenue, Interest Revenue, Investment Income, Gains. Interest Expense, Losses

Chapter 5 Assigned Questions: 1, 4, 5, 7, 9, 11, 16, 17, 19, 20 1. The components of revenues and expenses differ as follows: Merchandising Revenue Sales Service Service Revenue, Fees Earned, Rent Revenue,

Chapter 5 Assigned Questions: 1, 4, 5, 7, 9, 11, 16, 17, 19, 20 1. The components of revenues and expenses differ as follows: Merchandising Revenue Sales Service Service Revenue, Fees Earned, Rent Revenue,

MERCHANDISING OPERATIONS

MERCHANDISING OPERATIONS Key Topics to Know Merchandising Businesses The revenue account is Sales, not Fees Earned New expense account, Cost of Goods Sold (COGS), records the cost of merchandise inventory

MERCHANDISING OPERATIONS Key Topics to Know Merchandising Businesses The revenue account is Sales, not Fees Earned New expense account, Cost of Goods Sold (COGS), records the cost of merchandise inventory

Ch.7 Accounting for a Merchandising Business: Purchases and Cash Payments

Ch.7 Accounting for a Merchandising Business: Purchases and Cash Payments 1 Procedures and forms used in purchasing merchandise Record credit purchases in a general journal and a purchases journal, and

Ch.7 Accounting for a Merchandising Business: Purchases and Cash Payments 1 Procedures and forms used in purchasing merchandise Record credit purchases in a general journal and a purchases journal, and

AGRIMASTER HELP NOTE. Create a New Budget from Last Year s Actuals

AGRIMASTER HELP NOTE Create a New Budget from Last Year s Actuals A budget can be created from the cashbook actuals by importing the previous year s data. This will give you a guide or template to make

AGRIMASTER HELP NOTE Create a New Budget from Last Year s Actuals A budget can be created from the cashbook actuals by importing the previous year s data. This will give you a guide or template to make

June 30, 2015 Closing Procedures And July 1, 2015 Opening Procedures

University of Illinois Office of Business and Financial Services June 30, 2015 Closing Procedures And July 1, 2015 Opening Procedures (Subject to revision if required by legislative action) Table of Contents

University of Illinois Office of Business and Financial Services June 30, 2015 Closing Procedures And July 1, 2015 Opening Procedures (Subject to revision if required by legislative action) Table of Contents

Travel and Expense Management (TEM): Good Habits and Helpful Hints

: Good Habits and Helpful Hints") 2017 UIC Procurement Symposium Travel and Expense Management (TEM): Good Habits and Helpful Hints Copyright 2017 University of Illinois Office of Business and Financial Services. All rights reserved. No

2017 UIC Procurement Symposium Travel and Expense Management (TEM): Good Habits and Helpful Hints Copyright 2017 University of Illinois Office of Business and Financial Services. All rights reserved. No

What s in Your Wallet?

What s in Your Wallet? University Purchasing Card (P-Card) University Corporate Travel Card (T-Card) By Cheryl Harris and Kandra Miller OBFS UPAY Card Services Copyright 2016 University of Illinois Office

What s in Your Wallet? University Purchasing Card (P-Card) University Corporate Travel Card (T-Card) By Cheryl Harris and Kandra Miller OBFS UPAY Card Services Copyright 2016 University of Illinois Office

ETF PORFOLIO DATA SERVICE A DTCC DATA SERVICES OFFERING

ETF PORFOLIO DATA SERVICE A DTCC DATA SERVICES OFFERING ONBOARDING STEPS APRIL 17, 2018 Copyright 2018 DTCC. All rights reserved. This work (including, without limitation, all text, images, logos, compilation

ETF PORFOLIO DATA SERVICE A DTCC DATA SERVICES OFFERING ONBOARDING STEPS APRIL 17, 2018 Copyright 2018 DTCC. All rights reserved. This work (including, without limitation, all text, images, logos, compilation

Accounting for Merchandising Businesses

C H A P T E R 5 Accounting for Merchandising Businesses Corporate Financial Accounting 13e Warren Reeve Duchac human/istock/360/getty Images Operating Cycle The operating cycle is the process by which

C H A P T E R 5 Accounting for Merchandising Businesses Corporate Financial Accounting 13e Warren Reeve Duchac human/istock/360/getty Images Operating Cycle The operating cycle is the process by which

H&R Block Canada, Inc All Rights Reserved. Copyright is not claimed for any material secured from official government sources.

2017 Provincial Supplement Saskatchewan H&R Block Canada, Inc. 2017 All Rights Reserved Copyright is not claimed for any material secured from official government sources. No part of this book may be reproduced

2017 Provincial Supplement Saskatchewan H&R Block Canada, Inc. 2017 All Rights Reserved Copyright is not claimed for any material secured from official government sources. No part of this book may be reproduced

Fiscal Year End Quick Guide. Financial Services

Fiscal Year End Quick Guide http://finance.wfu.edu Table of Contents Importance of Fiscal Year End & Accrual Accounting Process.. 1 Payroll, SFS, and Accounting & Treasury. 5 Procurement Services. 7 Accounts

Fiscal Year End Quick Guide http://finance.wfu.edu Table of Contents Importance of Fiscal Year End & Accrual Accounting Process.. 1 Payroll, SFS, and Accounting & Treasury. 5 Procurement Services. 7 Accounts

Reporting Toolbox: So Many Tools, Which One Should I Use?

2018 BRINGING ADMINISTRATORS TOGETHER CONFERENCE Reporting Toolbox: So Many Tools, Which One Should I Use? April 5, 2018 10:15 to 11:15 Conference Sponsors: The Office of the Chancellor, Budget & Financial

2018 BRINGING ADMINISTRATORS TOGETHER CONFERENCE Reporting Toolbox: So Many Tools, Which One Should I Use? April 5, 2018 10:15 to 11:15 Conference Sponsors: The Office of the Chancellor, Budget & Financial

Accounting Definitions. Definitions

Accounting Definitions Definitions What s Here Introduction Definitions Introduction This training contains definitions of common accounting terms. If you come across accounting or financial terms with

Accounting Definitions Definitions What s Here Introduction Definitions Introduction This training contains definitions of common accounting terms. If you come across accounting or financial terms with

1031 Exchanges. Seminar Topic: This material provides an in-depth examination. The Basics and Pitfalls

1031 Exchanges The Basics and Pitfalls Seminar Topic: This material provides an in-depth examination of the process and procedure in a 1031 Exchange including structuring the transaction as an exchange

1031 Exchanges The Basics and Pitfalls Seminar Topic: This material provides an in-depth examination of the process and procedure in a 1031 Exchange including structuring the transaction as an exchange

Module 4. Instructions:

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

Oracle. SCM Cloud Using Fiscal Document Capture. Release 13 (update 17B)

") Oracle SCM Cloud Release 13 (update 17B) Release 13 (update 17B) Part Number E84337-03 Copyright 2011-2017, Oracle and/or its affiliates. All rights reserved. Author: Sathyan Nagarajan This software and

Oracle SCM Cloud Release 13 (update 17B) Release 13 (update 17B) Part Number E84337-03 Copyright 2011-2017, Oracle and/or its affiliates. All rights reserved. Author: Sathyan Nagarajan This software and

Chapter 7 2 Cash Discounts, Credit Terms and Partial Payments. net price equivalent rate

Chapter 7 2 Cash Discounts, Credit Terms and Partial Payments Review list price chain discount net price equivalent rate single equivalent rate traded discount net price $599 3/1 $199 8/4/3 $269 7/3/1

Chapter 7 2 Cash Discounts, Credit Terms and Partial Payments Review list price chain discount net price equivalent rate single equivalent rate traded discount net price $599 3/1 $199 8/4/3 $269 7/3/1

THE UNITED REPUBLIC OF TANZANIA NATIONAL EXAMINATIONS COUNCIL CERTIFICATE OF SECONDARY EDUCATION EXAMINATION. Instructions

THE UNITED REPUBLIC OF TANZANIA NATIONAL EXAMINATIONS COUNCIL CERTIFICATE OF SECONDARY EDUCATION EXAMINATION 062 BOOK KEEPING (For Both School and Private Candidates) Time: 3 Hours Friday, 12 th October

THE UNITED REPUBLIC OF TANZANIA NATIONAL EXAMINATIONS COUNCIL CERTIFICATE OF SECONDARY EDUCATION EXAMINATION 062 BOOK KEEPING (For Both School and Private Candidates) Time: 3 Hours Friday, 12 th October

3 End user cancellation policy regarding distance sales contracts

I. MAGIX Software GmbH General Terms and Conditions As of october 2016 1 Scope of application 1. All deliveries, services and offers of MAGIX Software GmbH (hereinafter referred to as MAGIX ) are made

I. MAGIX Software GmbH General Terms and Conditions As of october 2016 1 Scope of application 1. All deliveries, services and offers of MAGIX Software GmbH (hereinafter referred to as MAGIX ) are made

Use Tax for Businesses 146

www.revenue.state.mn.us Use Tax for Businesses 146 Sales Tax Fact Sheet 146 What s new in 2017 We updated the layout to make this fact sheet easier to use. Minnesota Use Tax applies when you buy, lease,

www.revenue.state.mn.us Use Tax for Businesses 146 Sales Tax Fact Sheet 146 What s new in 2017 We updated the layout to make this fact sheet easier to use. Minnesota Use Tax applies when you buy, lease,

Grade 12 Accounting Review & Practice Questions

Grade 12 Accounting Review & Practice Questions Chapter 1 Review Questions Chapter 1 Theory: Do m/c Page 30 31 #1 10 Chapter 1 Practice: o BE1 1 o BE1 5 o BE1 6 o BE1 11 o BE1 15 Exercises o E1 4 o E1

Grade 12 Accounting Review & Practice Questions Chapter 1 Review Questions Chapter 1 Theory: Do m/c Page 30 31 #1 10 Chapter 1 Practice: o BE1 1 o BE1 5 o BE1 6 o BE1 11 o BE1 15 Exercises o E1 4 o E1

Current Quarter. State University Retirement Annuitants not eligible for Social Security Withholding at the University of Illinois

UNIVERSITY PAYROLL NEWSLETTER Volume 3, Issue 3 November 2007 Highlights and Hot Topics Payloan Policy Revision By Laura Barnett University Payroll policy and guidelines for the approval of payloans have

UNIVERSITY PAYROLL NEWSLETTER Volume 3, Issue 3 November 2007 Highlights and Hot Topics Payloan Policy Revision By Laura Barnett University Payroll policy and guidelines for the approval of payloans have

REFUND OVERVIEW. Here s an overview on how refunds should be handled:

1 REFUND OVERVIEW Here s an overview on how refunds should be handled: 1. Agree with the customer on how the product(s) will be returned Verify with the customer that you have their correct email address.

1 REFUND OVERVIEW Here s an overview on how refunds should be handled: 1. Agree with the customer on how the product(s) will be returned Verify with the customer that you have their correct email address.

Chapter 16 Completing the Tests in the Sales and Collection Cycle:

Chapter 16 Completing the Tests in the Sales and Collection Cycle: Accounts Receivable Describe the methodology for designing tests of details of balances using the audit risk model. Design and perform

Chapter 16 Completing the Tests in the Sales and Collection Cycle: Accounts Receivable Describe the methodology for designing tests of details of balances using the audit risk model. Design and perform

CHAPTER 11. Financial Reporting Concepts ANSWERS TO QUESTIONS

CHAPTER 11 Financial Reporting Concepts ANSWERS TO QUESTIONS 2. (a) The main objective of financial reporting is to provide information that is useful for decision-making. More specifically, the conceptual

CHAPTER 11 Financial Reporting Concepts ANSWERS TO QUESTIONS 2. (a) The main objective of financial reporting is to provide information that is useful for decision-making. More specifically, the conceptual

IFA Paper 2. Accounting. Mark scheme. November ICSA 2016 Page 1 of 11

IFA Paper 2 Accounting scheme November 2016 ICSA 2016 Page 1 of 11 Section A 1 A The goods are sent to the customer 1 2 Changes in cost of sales Changes in selling prices Reward other valid responses 2

IFA Paper 2 Accounting scheme November 2016 ICSA 2016 Page 1 of 11 Section A 1 A The goods are sent to the customer 1 2 Changes in cost of sales Changes in selling prices Reward other valid responses 2

Church Accounting Icon Systems Inc.

IconCMO Church Software by Icon Systems Inc. All rights reserved. No parts of this work may be reproduced in any form or by any means - graphic, electronic, or mechanical, including photocopying, recording,

IconCMO Church Software by Icon Systems Inc. All rights reserved. No parts of this work may be reproduced in any form or by any means - graphic, electronic, or mechanical, including photocopying, recording,

PURCHASE ORDER QUALITY CLAUSES

Operational Document: SQD-741-01 Rev: H Page 1 Right of Access Steelville Manufacturing Co. (SMC), the SMC Customer(s), and Government and Regulatory agencies purchasing the end product shall be allowed

Operational Document: SQD-741-01 Rev: H Page 1 Right of Access Steelville Manufacturing Co. (SMC), the SMC Customer(s), and Government and Regulatory agencies purchasing the end product shall be allowed

REFUND POLICY Retail and Preferred Customer Return Policy Guidelines PrimeMyBody PrimeMyBody Affiliate s Responsibilities for Customer Refund Policy

REFUND POLICY Retail and Preferred Customer Return Policy Guidelines PrimeMyBody offers a thirty-day (30-day) refund policy (less shipping and handling) to all retail and preferred customers. The refund

REFUND POLICY Retail and Preferred Customer Return Policy Guidelines PrimeMyBody offers a thirty-day (30-day) refund policy (less shipping and handling) to all retail and preferred customers. The refund

ORIGINAL PRONOUNCEMENTS

Financial Accounting Standards Board ORIGINAL PRONOUNCEMENTS AS AMENDED FASB Technical Bulletin No. 90-1 Accounting for Separately Priced Extended Copyright 2008 by Financial Accounting Standards Board.

Financial Accounting Standards Board ORIGINAL PRONOUNCEMENTS AS AMENDED FASB Technical Bulletin No. 90-1 Accounting for Separately Priced Extended Copyright 2008 by Financial Accounting Standards Board.

Section 22 Self-Supporting/Revenue Generating - Service and Storeroom Activities

Section 22 Self-Supporting/Revenue Generating - Service and Storeroom Activities Welcome to the Office of Business and Financial Services Open Comment Blog! The University of Illinois System, Office of

Section 22 Self-Supporting/Revenue Generating - Service and Storeroom Activities Welcome to the Office of Business and Financial Services Open Comment Blog! The University of Illinois System, Office of

Statement of Financial Accounting Standards No. 49

Statement of Financial Accounting Standards No. 49 FAS49 Status Page FAS49 Summary Accounting for Product Financing Arrangements June 1981 Financial Accounting Standards Board of the Financial Accounting

Statement of Financial Accounting Standards No. 49 FAS49 Status Page FAS49 Summary Accounting for Product Financing Arrangements June 1981 Financial Accounting Standards Board of the Financial Accounting

Profit or loss recorded to Retained Earnings

Cash basis Recognizes transactions when cash or equivalents DIAGRAM OF T-ACCOUNTS METHODS & ORGS Balance Sheet as of 12/31/2100 Accrual basis Follows the matching principle and recognizes Assets = Liabilities

Cash basis Recognizes transactions when cash or equivalents DIAGRAM OF T-ACCOUNTS METHODS & ORGS Balance Sheet as of 12/31/2100 Accrual basis Follows the matching principle and recognizes Assets = Liabilities

Accounting)Exam)Notes!

Exam)Notes!") Accounting)Exam)Notes! Week 1 The role of accounting in business Adjusting processes can be created Accounting period - a measurement period. 12 months. Listed companies can be 6 months - even quarterly.

Accounting)Exam)Notes! Week 1 The role of accounting in business Adjusting processes can be created Accounting period - a measurement period. 12 months. Listed companies can be 6 months - even quarterly.

ASU Revenue from Contracts with Customers

ASU 2014-09 Revenue from Contracts with Customers Prepared by the PICPA Greater Philadelphia A&A Committee May 2015 Introduction The Greater Philadelphia Chapter s Accounting and Attest Committee has developed

ASU 2014-09 Revenue from Contracts with Customers Prepared by the PICPA Greater Philadelphia A&A Committee May 2015 Introduction The Greater Philadelphia Chapter s Accounting and Attest Committee has developed

Transfer an Employee s Time Off Balance

Absence & Leave Transfer an Employee s Time Off Balance Use this job aid to: Transfer an employee s Time Off Plan balance from their current plan to their future plan View the transfer with a Time Off

Absence & Leave Transfer an Employee s Time Off Balance Use this job aid to: Transfer an employee s Time Off Plan balance from their current plan to their future plan View the transfer with a Time Off

SURPLUS BID ATTACHMENT

SACRAMENTO MUNICIPAL UTILITY SMUD INSTRUCTIONS TO BIDDERS SURPLUS BID ATTACHMENT 1. INSPECTION: This material should be carefully inspected before bidding and any questions regarding quantities or specifications

SACRAMENTO MUNICIPAL UTILITY SMUD INSTRUCTIONS TO BIDDERS SURPLUS BID ATTACHMENT 1. INSPECTION: This material should be carefully inspected before bidding and any questions regarding quantities or specifications

Financial Services Procurement Card Policies and Procedures. Table of Contents

Table of Contents 1.0 Purpose... 2 2.0 Applicability... 2 3.0 Definitions... 2 4.0 Card Issuing Bank... 3 5.0 Program Benefits... 3 6.0 Compliance with University Procurement Policies... 3 7.0 Procedures...

Table of Contents 1.0 Purpose... 2 2.0 Applicability... 2 3.0 Definitions... 2 4.0 Card Issuing Bank... 3 5.0 Program Benefits... 3 6.0 Compliance with University Procurement Policies... 3 7.0 Procedures...

Avalara Tax Connect version 2017

version 2017 Disclaimer This document is for informational purposes only and is subject to change without notice. This document and its contents, including the viewpoints, dates and functional content

version 2017 Disclaimer This document is for informational purposes only and is subject to change without notice. This document and its contents, including the viewpoints, dates and functional content

Part I Handset Protection Programs Overview of Insurance and Service Contract Regulation

Part I Handset Protection Programs Overview of Insurance and Service Contract Regulation Gerald Gary Mize Chair, Handset Protection and Insurance Practice Gerald.Mize@alston.com Direct: (404) 881-7579

Part I Handset Protection Programs Overview of Insurance and Service Contract Regulation Gerald Gary Mize Chair, Handset Protection and Insurance Practice Gerald.Mize@alston.com Direct: (404) 881-7579

FASB Technical Bulletin No. 81-1

FASB Technical Bulletin No. 81-1 Note: This Technical Bulletin has been completely superseded FTB 81-1 Status Page Disclosure of Interest Rate Futures Contracts and Forward and Standby Contracts February

FASB Technical Bulletin No. 81-1 Note: This Technical Bulletin has been completely superseded FTB 81-1 Status Page Disclosure of Interest Rate Futures Contracts and Forward and Standby Contracts February

SUPPLIER - TERMS AND CONDITIONS Materials and Goods

SUPPLIER - TERMS AND CONDITIONS Materials and Goods 1. BINDING EFFECT; ACCEPTANCE. This purchase order and all subsequent purchase orders delivered by Buyer to Seller (each, an "order"), shall be governed

SUPPLIER - TERMS AND CONDITIONS Materials and Goods 1. BINDING EFFECT; ACCEPTANCE. This purchase order and all subsequent purchase orders delivered by Buyer to Seller (each, an "order"), shall be governed

eres VAT Increase Guide

Guide This product is owned by H.T.I Pty (Ltd) and is protected by copyright laws. However, you are authorised to make copies of the application solely for backup/ training purposes. Copyright 2018 1.

Guide This product is owned by H.T.I Pty (Ltd) and is protected by copyright laws. However, you are authorised to make copies of the application solely for backup/ training purposes. Copyright 2018 1.

The Growing Influence of the Streamlined Sales Tax Initiative

The Growing Influence of the Streamlined Sales Tax Initiative Wednesday, March 12, 2008 Copyright 2008. All rights reserved. This content may not be reproduced or repurposed without written permission

The Growing Influence of the Streamlined Sales Tax Initiative Wednesday, March 12, 2008 Copyright 2008. All rights reserved. This content may not be reproduced or repurposed without written permission

Government and Health Care

Chapter 9 Government and Health Care Copyright 2002 by Thomson Learning, Inc. Copyright 2002 Thomson Learning, Inc. Thomson Learning is a trademark used herein under license. ALL RIGHTS RESERVED. Instructors

Chapter 9 Government and Health Care Copyright 2002 by Thomson Learning, Inc. Copyright 2002 Thomson Learning, Inc. Thomson Learning is a trademark used herein under license. ALL RIGHTS RESERVED. Instructors

Click to Add Title. What HR Professionals Need to Know About Budgets at UIC. HR Academy November 7, 2014

What HR Professionals Need to Know About Budgets at UIC Click to Add Title HR Academy November 7, 2014 Janet Parker Associate Chancellor & Vice Provost Budget & Resource Planning Agenda Fund Accounting

What HR Professionals Need to Know About Budgets at UIC Click to Add Title HR Academy November 7, 2014 Janet Parker Associate Chancellor & Vice Provost Budget & Resource Planning Agenda Fund Accounting

General Terms & Conditions of Purchase H&R Singapore Pte. Ltd.

General Terms & Conditions of Purchase H&R Singapore Pte. Ltd. Scope Asia H&R Singapore Pte.Ltd. 8, Boon Lay Way, #11-11 TradeHub21, Singapore 609964 Tel.: +65 96490148 Fax: +65 83426899 http://www.hur.com

General Terms & Conditions of Purchase H&R Singapore Pte. Ltd. Scope Asia H&R Singapore Pte.Ltd. 8, Boon Lay Way, #11-11 TradeHub21, Singapore 609964 Tel.: +65 96490148 Fax: +65 83426899 http://www.hur.com

Module 9. Table of Contents

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

Chapter 1. Individuals and Government

Chapter 1 Individuals and Government Copyright 2002 by Thomson Learning, Inc. Copyright 2002 Thomson Learning, Inc. Thomson Learning is a trademark used herein under license. ALL RIGHTS RESERVED. Instructors

Chapter 1 Individuals and Government Copyright 2002 by Thomson Learning, Inc. Copyright 2002 Thomson Learning, Inc. Thomson Learning is a trademark used herein under license. ALL RIGHTS RESERVED. Instructors

Institute of Certified Management Accountants of Sri Lanka Operational Level November 2015 Examination

Copyright Reserved Serial No Institute of Certified Management Accountants of Sri Lanka Operational Level November 2015 Examination Examination Date : 14 th November 2015 Number of Pages : 10 Examination

Copyright Reserved Serial No Institute of Certified Management Accountants of Sri Lanka Operational Level November 2015 Examination Examination Date : 14 th November 2015 Number of Pages : 10 Examination

ValuAdder. Business Valuation Handbook. Eighth Edition

ValuAdder Business Valuation Handbook Eighth Edition ValuAdder Business Valuation Handbook Eighth Edition Copyright 2004-2017 Haleo Corporation All rights reserved. No part of this book may be reproduced

ValuAdder Business Valuation Handbook Eighth Edition ValuAdder Business Valuation Handbook Eighth Edition Copyright 2004-2017 Haleo Corporation All rights reserved. No part of this book may be reproduced

ANZ ONLINE TRADE TRADE LOANS

ANZ ONLINE TRADE TRADE LOANS USER GUIDE ADDENDUM October 2017 ANZ Online Trade Trade Loans User Guide NEW TRADE LOANS 1 ANZ Online Trade Trade Loans User Guide October 2017 NEW TRADE LOANS... 3 Buttons...

ANZ ONLINE TRADE TRADE LOANS USER GUIDE ADDENDUM October 2017 ANZ Online Trade Trade Loans User Guide NEW TRADE LOANS 1 ANZ Online Trade Trade Loans User Guide October 2017 NEW TRADE LOANS... 3 Buttons...

Proposed 2019 Changes to Experience Rating

W o r k e r s C o m p e n s a t i o n I n s u r a n c e R a t i n g B u r e a u o f C a l i f o r n i a WCIRB Mod Talks Proposed 2019 Changes to Experience Rating The webinar will begin shortly. Notice

W o r k e r s C o m p e n s a t i o n I n s u r a n c e R a t i n g B u r e a u o f C a l i f o r n i a WCIRB Mod Talks Proposed 2019 Changes to Experience Rating The webinar will begin shortly. Notice

Making an Online Payment

Making an Online Payment August 2015 This document is intended for restricted use only. Infinite Campus asserts that this document contains proprietary information that would give our competitors undue

Making an Online Payment August 2015 This document is intended for restricted use only. Infinite Campus asserts that this document contains proprietary information that would give our competitors undue

830 CMR 64H.1.3 Computer Industry Services and Products

830 CMR 64H.1.3 Computer Industry Services and Products 830 CMR: DEPARTMENT OF REVENUE 830 CMR 64H:00: SALES AND USE TAX 830 CMR 64H.1.3 is repealed and replaced with the following (1) Statement of Purpose;

830 CMR 64H.1.3 Computer Industry Services and Products 830 CMR: DEPARTMENT OF REVENUE 830 CMR 64H:00: SALES AND USE TAX 830 CMR 64H.1.3 is repealed and replaced with the following (1) Statement of Purpose;

FASB Technical Bulletin No. 81-4

FASB Technical Bulletin No. 81-4 Note: This Technical Bulletin has been completely superseded FTB 81-4 Status Page Classification as Monetary or Nonmonetary Items February 1981 Financial Accounting Standards

FASB Technical Bulletin No. 81-4 Note: This Technical Bulletin has been completely superseded FTB 81-4 Status Page Classification as Monetary or Nonmonetary Items February 1981 Financial Accounting Standards

State & Local Tax Alert

State & Local Tax Alert Breaking state and local tax developments from Grant Thornton LLP Colorado Enforcement of Remote Seller Notice and Reporting Requirements Commences On July 1, 2017, the Colorado

State & Local Tax Alert Breaking state and local tax developments from Grant Thornton LLP Colorado Enforcement of Remote Seller Notice and Reporting Requirements Commences On July 1, 2017, the Colorado

CONTRACT RELEASE: T-752(5) WEB SITE: CONTRACT VENDOR CONTRACT NO.

WEB SITE: CONTRACT VENDOR CONTRACT NO.") Admin Minnesota Materials Management Division Room 112 Administration Bldg., 50 Sherburne Ave., St. Paul, MN 55155; Phone: 651.296.2600, Fax: 651.297.3996 Persons with a hearing or speech disability can

Admin Minnesota Materials Management Division Room 112 Administration Bldg., 50 Sherburne Ave., St. Paul, MN 55155; Phone: 651.296.2600, Fax: 651.297.3996 Persons with a hearing or speech disability can

UW ProCard Cardholder Training Class

UW ProCard Cardholder Training Class Agenda: Procard Overview ProCard Basics Maintenance Purchasing Rules Management JPMC PaymentNet website Transaction reviews Running reports ProCard Cardholder Training

UW ProCard Cardholder Training Class Agenda: Procard Overview ProCard Basics Maintenance Purchasing Rules Management JPMC PaymentNet website Transaction reviews Running reports ProCard Cardholder Training

Fixed Assets Inventory

Fixed Assets Inventory Preliminary User Manual User Manual Edition: 2/3/2006 For Program version: 2/3/2006 Your inside track for making your job easier! Tenmast Software 132 Venture Court, Suite 1 Lexington,

Fixed Assets Inventory Preliminary User Manual User Manual Edition: 2/3/2006 For Program version: 2/3/2006 Your inside track for making your job easier! Tenmast Software 132 Venture Court, Suite 1 Lexington,

FIXTURE TERMS & CONDITIONS Materials & Goods

FIXTURE TERMS & CONDITIONS Materials & Goods 1. BINDING EFFECT; ACCEPTANCE. This purchase order and all subsequent purchase orders delivered by Supplier to The Pep Boys Manny, Moe & Jack, and its affiliates,

FIXTURE TERMS & CONDITIONS Materials & Goods 1. BINDING EFFECT; ACCEPTANCE. This purchase order and all subsequent purchase orders delivered by Supplier to The Pep Boys Manny, Moe & Jack, and its affiliates,

HUMANITIX TICKET PURCHASING AGREEMENT

HUMANITIX TICKET PURCHASING AGREEMENT 1 Agreement 1.1 You should read these Terms and Conditions carefully. In these Terms and Conditions the words, Humanitix, Company, we, our and us refer to Humanitix

HUMANITIX TICKET PURCHASING AGREEMENT 1 Agreement 1.1 You should read these Terms and Conditions carefully. In these Terms and Conditions the words, Humanitix, Company, we, our and us refer to Humanitix

General Provision for Purchase Orders (GP-PO)

") As used herein, "Seller" includes Seller, its subsidiaries and affiliates; "Insitu" includes The Insitu, Inc. and its subsidiaries and affiliates. Seller and Insitu hereby agree as follows: 1. Goods and

As used herein, "Seller" includes Seller, its subsidiaries and affiliates; "Insitu" includes The Insitu, Inc. and its subsidiaries and affiliates. Seller and Insitu hereby agree as follows: 1. Goods and

Thank you for your interest in becoming a supplier to Neenah Inc.

Thank you for your interest in becoming a supplier to Neenah Inc. Neenah is a leader in premium image and performance-based products, including filtration, specialized substrates used for tapes, labels

Thank you for your interest in becoming a supplier to Neenah Inc. Neenah is a leader in premium image and performance-based products, including filtration, specialized substrates used for tapes, labels

- Tax Reporting Ledger in 11i.10. Alex Fiteni CMA Fiteni International LLC Managing Risk, Leading Change

Oracle E-Business E Suite - Tax Reporting Ledger in 11i.10 Alex Fiteni CMA Fiteni International LLC Managing Risk, Leading Change Fiteni International LLC Fiteni International LLC is a professional services

Oracle E-Business E Suite - Tax Reporting Ledger in 11i.10 Alex Fiteni CMA Fiteni International LLC Managing Risk, Leading Change Fiteni International LLC Fiteni International LLC is a professional services

Microsoft Dynamics NAV Prepayments. Prepayments Supportability White Paper

Microsoft Dynamics NAV 2013 - Prepayments Prepayments Supportability White Paper Released: January 17, 2013 Conditions and Terms of Use Microsoft Confidential This training package content is proprietary

Microsoft Dynamics NAV 2013 - Prepayments Prepayments Supportability White Paper Released: January 17, 2013 Conditions and Terms of Use Microsoft Confidential This training package content is proprietary

HI6026 Audit, Assurance and Compliance TRIMESTER 2, 2017 INDIVIDUAL ASSIGNMENT 1

HI6026 Audit, Assurance and Compliance TRIMESTER 2, 2017 INDIVIDUAL ASSIGNMENT 1 Assessment Value: 20% Instructions: This assignment is to be submitted in accordance with assessment policy stated in the

HI6026 Audit, Assurance and Compliance TRIMESTER 2, 2017 INDIVIDUAL ASSIGNMENT 1 Assessment Value: 20% Instructions: This assignment is to be submitted in accordance with assessment policy stated in the

ST. LOUIS COMMUNITY COLLEGE E-BID FORM

ST. LOUIS COMMUNITY COLLEGE E-BID FORM General Requirements St. Louis Community College (the College ) requires that all bids be received in the College s Purchasing Department by emailing to cgreen2@stlcc.edu

ST. LOUIS COMMUNITY COLLEGE E-BID FORM General Requirements St. Louis Community College (the College ) requires that all bids be received in the College s Purchasing Department by emailing to cgreen2@stlcc.edu

Washburn University Memorandum

Washburn University Memorandum To: All Faculty and Staff From: Chris Leach, Director of Finance Copy: Date: May 28, 2013 Subject: Year-End Financial Closing Procedures Fiscal Year Ending June 30, 2013

Washburn University Memorandum To: All Faculty and Staff From: Chris Leach, Director of Finance Copy: Date: May 28, 2013 Subject: Year-End Financial Closing Procedures Fiscal Year Ending June 30, 2013

Financial Accounting (Corporation)

") Financial Accounting (Corporation) This course covers the topics shown below. Students navigate learning paths based on their level of readiness. Institutional users may customize the scope and sequence

Financial Accounting (Corporation) This course covers the topics shown below. Students navigate learning paths based on their level of readiness. Institutional users may customize the scope and sequence

UCC Article 9 Blanket Asset Lien Exclusions and Purchase Money Security Interests

Presenting a live 90-minute webinar with interactive Q&A UCC Article 9 Blanket Asset Lien Exclusions and Purchase Money Security Interests Navigating Statutory, Contractual and Other Exclusions to All

Presenting a live 90-minute webinar with interactive Q&A UCC Article 9 Blanket Asset Lien Exclusions and Purchase Money Security Interests Navigating Statutory, Contractual and Other Exclusions to All

Interest Calculation Add-on Supernova Add-on for SAP Business One

User Manual Supernova Add-on for SAP Business One Date: October 2013 Copyright 2013 Supernova Consulting Ltd. All rights reserved. This content may not be reproduced or transmitted in any form or by any

User Manual Supernova Add-on for SAP Business One Date: October 2013 Copyright 2013 Supernova Consulting Ltd. All rights reserved. This content may not be reproduced or transmitted in any form or by any

Experience Rating Eligibility and the Impact of Unaudited Payroll

W o r k e r s C o m p e n s a t i o n I n s u r a n c e R a t i n g B u r e a u o f C a l i f o r n i a WCIRB Talks Experience Rating Eligibility and the Impact of Unaudited Payroll The webinar will begin

W o r k e r s C o m p e n s a t i o n I n s u r a n c e R a t i n g B u r e a u o f C a l i f o r n i a WCIRB Talks Experience Rating Eligibility and the Impact of Unaudited Payroll The webinar will begin

Managing Payment Information

Managing Payment Information April 2013 This document is intended for restricted use only. Infinite Campus asserts that this document contains proprietary information that would give our competitors undue

Managing Payment Information April 2013 This document is intended for restricted use only. Infinite Campus asserts that this document contains proprietary information that would give our competitors undue

Accounting Cheat Sheet

DIAGRAM OF TACCOUNTS Assets = Balance Sheet as of 12/31/20 Liabilit ies + = + Equity METHODS & ORGS Accrual basis Follows the matching principle and recognizes transactions as they occur (GAAP Method)

DIAGRAM OF TACCOUNTS Assets = Balance Sheet as of 12/31/20 Liabilit ies + = + Equity METHODS & ORGS Accrual basis Follows the matching principle and recognizes transactions as they occur (GAAP Method)

A Study of the Alignment of the NWEA RIT Scale with the Maryland Assessment System. Deborah Adkins

A Study of the Alignment of the NWEA RIT Scale with the Maryland Assessment System Deborah Adkins March, 2007 Copyright 2007 Northwest Evaluation Association All rights reserved. No part of this document

A Study of the Alignment of the NWEA RIT Scale with the Maryland Assessment System Deborah Adkins March, 2007 Copyright 2007 Northwest Evaluation Association All rights reserved. No part of this document

Features for Singapore

Features for Singapore Microsoft Corporation Published: November 2006 Microsoft Dynamics is a line of integrated, adaptable business management solutions that enables you and your people to make business

Features for Singapore Microsoft Corporation Published: November 2006 Microsoft Dynamics is a line of integrated, adaptable business management solutions that enables you and your people to make business

Senior Fitness Test Terms and Conditions Thank you for visiting SFT.HumanKinetics.com, which is operated by Human Kinetics, Inc. (HK).

.") Terms and Conditions Senior Fitness Test Terms and Conditions Thank you for visiting SFT.HumanKinetics.com, which is operated by Human Kinetics, Inc. (HK). This Terms and Conditions document outlines the

Terms and Conditions Senior Fitness Test Terms and Conditions Thank you for visiting SFT.HumanKinetics.com, which is operated by Human Kinetics, Inc. (HK). This Terms and Conditions document outlines the

MAGENTO 2 AUCTION. (Version 1.0) USER GUIDE

USER GUIDE") MAGENTO 2 AUCTION (Version 1.0) USER GUIDE 0 Confidential Information Notice Copyright2016. All Rights Reserved. Any unauthorized reproduction of this document is prohibited. This document and the information

MAGENTO 2 AUCTION (Version 1.0) USER GUIDE 0 Confidential Information Notice Copyright2016. All Rights Reserved. Any unauthorized reproduction of this document is prohibited. This document and the information

Definitions I. GENERAL PROVISIONS

GENERAL TERMS OF PURCHASE of the private limited liability company SIF Group B.V. with registered office and place of business at 6041 TA ROERMOND, the Netherlands, in the Mijnheerkensweg nr. 33. Filed

GENERAL TERMS OF PURCHASE of the private limited liability company SIF Group B.V. with registered office and place of business at 6041 TA ROERMOND, the Netherlands, in the Mijnheerkensweg nr. 33. Filed

Your Collateral is in the Mail PART 1: IN-TRANSIT INVENTORY

Your Collateral is in the Mail Importing goods has a significant impact on the U.S. economy and is of particular relevance to asset-based lenders as it can lead to an important source of collateral for

Your Collateral is in the Mail Importing goods has a significant impact on the U.S. economy and is of particular relevance to asset-based lenders as it can lead to an important source of collateral for

Chapter 7. Trade Discounts Cash Discounts (and Freight Charges)

") Chapter 7 Trade Discounts Cash Discounts (and Freight Charges) 7-1 McGraw-Hill/Irwin Copyright 2006 by The McGraw-Hill Companies, Inc. All rights reserved. Distribution Chain Manufacturer (General Mills)

Chapter 7 Trade Discounts Cash Discounts (and Freight Charges) 7-1 McGraw-Hill/Irwin Copyright 2006 by The McGraw-Hill Companies, Inc. All rights reserved. Distribution Chain Manufacturer (General Mills)

Drop Shipments and Sales Tax Navigating Varying State Policies on Registrations and Exemptions

Presenting a live 110 minute teleconference with interactive Q&A Drop Shipments and Sales Tax Navigating Varying State Policies on Registrations and Exemptions THURSDAY, JUNE 9, 2011 1pm Eastern 12pm Central

Presenting a live 110 minute teleconference with interactive Q&A Drop Shipments and Sales Tax Navigating Varying State Policies on Registrations and Exemptions THURSDAY, JUNE 9, 2011 1pm Eastern 12pm Central

Fund Accounting 101. March 11, :00 10:15 1:45 3:00

Fund Accounting 101 March 11, 2013 9:00 10:15 1:45 3:00 Workshop Presenters Jason Bane Senior Business & Financial Coordinator jabane@uillinois.edu (217) 206-7848 Tim Parrish Financial Accounting & Reporting

Fund Accounting 101 March 11, 2013 9:00 10:15 1:45 3:00 Workshop Presenters Jason Bane Senior Business & Financial Coordinator jabane@uillinois.edu (217) 206-7848 Tim Parrish Financial Accounting & Reporting

REQUEST FOR QUOTATION INVITATION

REQUEST FOR QUOTATION INVITATION DATE: August 3, 2010 DPS: REQUIREMENT: SUBJECT: Carolyn Sammons DPS Contract Administrator Email: Carolyn.Sammons@cityofchicago.org Telephone: 312-744-7284 Sharpening of

REQUEST FOR QUOTATION INVITATION DATE: August 3, 2010 DPS: REQUIREMENT: SUBJECT: Carolyn Sammons DPS Contract Administrator Email: Carolyn.Sammons@cityofchicago.org Telephone: 312-744-7284 Sharpening of

AICE NEW YORK SALES TAX & INSURANCE MEETING

AICE NEW YORK SALES TAX & INSURANCE MEETING Experts: Scott Taylor, President, Taylor & Taylor Associates, Inc. taylor@taylorinsurance.com Roger Blane, from Hutton & Solomon: Tax Law Attorneys rblane@hstax.com

AICE NEW YORK SALES TAX & INSURANCE MEETING Experts: Scott Taylor, President, Taylor & Taylor Associates, Inc. taylor@taylorinsurance.com Roger Blane, from Hutton & Solomon: Tax Law Attorneys rblane@hstax.com

The Regulatory Filing Process

W o r k e r s C o m p e n s a t i o n I n s u r a n c e R a t i n g B u r e a u o f C a l i f o r n i a WCIRB Talks The Regulatory Filing Process The webinar will begin shortly. Notice The information

W o r k e r s C o m p e n s a t i o n I n s u r a n c e R a t i n g B u r e a u o f C a l i f o r n i a WCIRB Talks The Regulatory Filing Process The webinar will begin shortly. Notice The information

Seminar on Bookkeeping Basics

Seminar on Bookkeeping Basics (Handout) Our materials are copyright AccountingCoach, LLC and are for personal use by the original purchaser only. We do not allow our materials to be reproduced or distributed

Seminar on Bookkeeping Basics (Handout) Our materials are copyright AccountingCoach, LLC and are for personal use by the original purchaser only. We do not allow our materials to be reproduced or distributed

Accounting for Merchandising Businesses

Accounting for Merchandising Businesses LearningObjective1 Distinguish between the activities and financial statements of service and merchandising businesses. Nature of Merchandising Businesses Service

Accounting for Merchandising Businesses LearningObjective1 Distinguish between the activities and financial statements of service and merchandising businesses. Nature of Merchandising Businesses Service

How to make payments using the Payment Wizard

How to make payments using the Payment Wizard Overall Business Processes BANKING Related Business Process FINANCIAL ACCOUNTING Responsible Department ACCOUNTING Involved Departments ACCOUNTING Last Updated

How to make payments using the Payment Wizard Overall Business Processes BANKING Related Business Process FINANCIAL ACCOUNTING Responsible Department ACCOUNTING Involved Departments ACCOUNTING Last Updated

UCSD AGREEMENT # 015/SD/1210 SIGMA ALDRICH INC, CHEMICALS AND REAGENTS

UCSD AGREEMENT # 015/SD/1210 SIGMA ALDRICH INC, CHEMICALS AND REAGENTS THIS UCSD AGREEMENT ( Agreement ) is made and entered into this 1 st day of January, 2010 by and between The Regents of the University

UCSD AGREEMENT # 015/SD/1210 SIGMA ALDRICH INC, CHEMICALS AND REAGENTS THIS UCSD AGREEMENT ( Agreement ) is made and entered into this 1 st day of January, 2010 by and between The Regents of the University

Module 4. Table of Contents

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

SALES & USE TAX FOR PUBLIC PROCUREMENT THE BASICS OF SALES TAX

SALES & USE TAX FOR PUBLIC PROCUREMENT SC ASSOCIATION OF GOVERNMENTAL PURCHASING OFFICIALS SEPTEMBER 14, 2017 1 THE BASICS OF SALES TAX South Carolina imposes a sales tax equal to 6%, plus applicable local

SALES & USE TAX FOR PUBLIC PROCUREMENT SC ASSOCIATION OF GOVERNMENTAL PURCHASING OFFICIALS SEPTEMBER 14, 2017 1 THE BASICS OF SALES TAX South Carolina imposes a sales tax equal to 6%, plus applicable local

Gift & Endowment Income Funds FAQs & Answers

Gift & Endowment Income Funds FAQs & Answers Gift Funds - Basic Information Q. I need to set up a new gift or endowment income fund. What steps do I need to take? A. A University of Illinois Foundation

Gift & Endowment Income Funds FAQs & Answers Gift Funds - Basic Information Q. I need to set up a new gift or endowment income fund. What steps do I need to take? A. A University of Illinois Foundation

Chargeback and Dispute Guide. December 2, 2016

Chargeback and Dispute Guide December 2, 2016 Table of Contents Definitions... 3 Introduction... 4 Responsibilities... 5 GoInterpay Responsibilities... 5 Seller Responsibilities... 5 Fraud-Dispute Procedures...

Chargeback and Dispute Guide December 2, 2016 Table of Contents Definitions... 3 Introduction... 4 Responsibilities... 5 GoInterpay Responsibilities... 5 Seller Responsibilities... 5 Fraud-Dispute Procedures...

26/07/2017 COURSE OUTLINE. The Key Elements of US GAAP session 2. Introduction to gaap, underpinning principles and high-level considerations

The Key Elements of US GAAP session 2 Wayne Bartlett, CPA COURSE OUTLINE SESSION 1: Intro Core principles Overarching standards SESSION 2: Statement of Financial Position Property, Plant and Equipment

The Key Elements of US GAAP session 2 Wayne Bartlett, CPA COURSE OUTLINE SESSION 1: Intro Core principles Overarching standards SESSION 2: Statement of Financial Position Property, Plant and Equipment

Commercial Coverage For

Customarq Series Commercial Coverage For Participating members of the Prospectors and Developers Association (See Form 80-02-1408) Producer: Partners Indemnity - PDAC Affinity Group 10 Adelaide Street

Customarq Series Commercial Coverage For Participating members of the Prospectors and Developers Association (See Form 80-02-1408) Producer: Partners Indemnity - PDAC Affinity Group 10 Adelaide Street