A Practical Guide to Fair Lending Success. Utah Bankers Association Tuesday, October 25 9:00 am

|

|

|

- Melvyn Magnus Gibson

- 5 years ago

- Views:

Transcription

1 A Practical Guide to Fair Lending Success Utah Bankers Association Tuesday, October 25 9:00 am

2 Thank You! TRUPOINT Partners is honored to be here with you today

3 Show of Hands (Experience with Fair Lending?)

4 First Couple Thoughts Doctor

5 First Couple Thoughts Cheerleader

6 First Couple Thoughts Realtor

7 First Couple Thoughts Football Player

8 First Couple Thoughts Compliance Officer

9 First Couple Thoughts Car Salesman

10 First Couple Thoughts Regulator

11 First Couple Thoughts Farmer

12 First Couple Thoughts Ephraim Sanpete County?

13 First Couple Thoughts San Juan County?

14 Americans Generous Optimistic Hardworking Materialistic Ignorant of all countries and cultures beyond their own Gun-loving Environmental Unconsciousness Arrogance Quick to Use Force

15

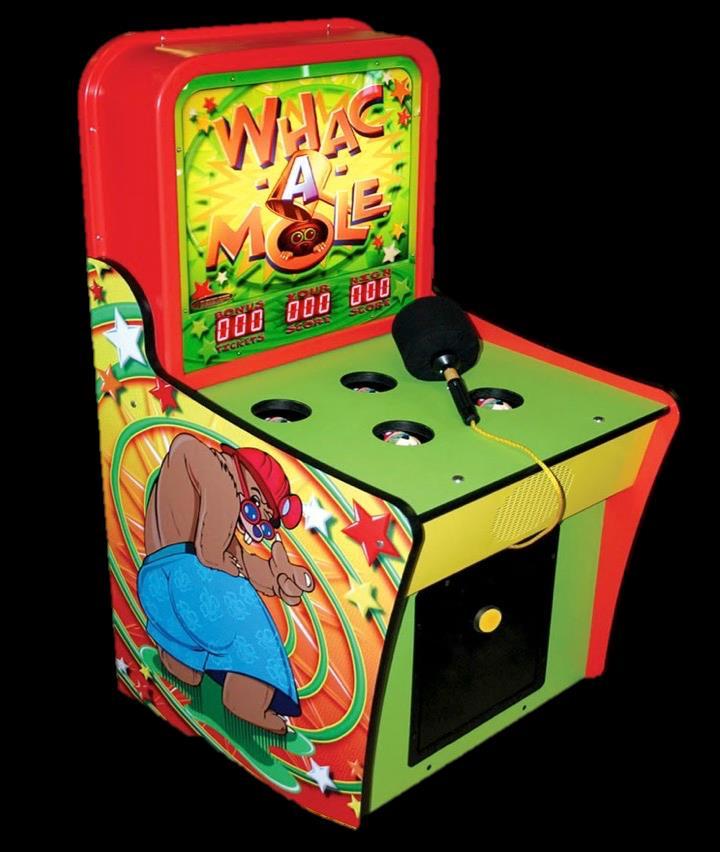

16 Stereotypes Defined as an over-generalized belief about a particular group. Simplify: We use stereotypes to simplify our world. They reduce the amount of thinking we have to do when we meet or interact with new people. Disadvantage: The use of stereotypes and generalizations can makes us ignore differences between individuals. Can be both positive or negative

17 Bottom Line If you re willing to accept that stereotypes exist, you re willing to accept that your institution may have fair lending risk

18 Conclusion #0 Stereotypes are everywhere. We employ stereotypes to consume our complex world. They may also bring fair lending risk to your organization

19 What We ll Cover Today Establish that Fair Lending Risks Exist Today Today s Regulatory Landscape Stopping the Insanity Fair Lending Overview Utah: Unique Fair Lending Issues! 8 Key Fair Lending Risks Qualitative and Quantitative Risks Common Fair Lending Tripwires Team Work for Fair Lending

20 Today s Regulatory Compliance Environment TODAY S REGULATORY COMPLIANCE LANDSCAPE

21 Today s Compliance Realities Time is Limited. Resources are Constrained. Teamwork is Essential. Compliance is Complex & Evolving. Risks are Real. Consequences are Serious. In today s compliance environment, it s more important than ever to understand your compliance risks and prioritize your focal points. Neglecting compliance can be costly in time, reputation and resources. Tip: Try thinking about compliance less like boxes to be checked, and more like resource protection

22 Regulatory Compliance

23 Can Feel Like Whack-A-Mole! Effective Complaint Management Increased Cyber Threats BSA/AML CFPB Impact and Rules Changes TRID Anyone? HMDA Plus? Servicing HMDA Data Integrity Third-Party Vendor Management UDAAP Fair Lending (Mortgage and Non-Mortgage)

24 State of Overwhelm in Risk Management & Compliance

25 STOP THE INSANITY

26 There is a Road Map to Sanity Manage Overwhelm Sheer volume of compliance work. Develop Priorities Priorities: Allow you to focus, with confidence. Risk Assessment Build awareness. Clear view of variables. Identify and focus on areas with highest risk. Alignment Agree on the controls needed to ensure efficient, effective operations

27 Conclusion #1 There is too much going on in the world of compliance. YOU MUST PRIORITIZE in a way that is ALIGNED WITH EXECUTIVE MANAGEMENT. Risk Assessments should help identify your biggest areas of risk!

28 A Quick Intro to Fair Lending Compliance FAIR LENDING OVERVIEW

29 Fair Lending is one of the Hottest Topics

30 What is Fair Lending Here are two of the most simplistic definitions of Fair Lending: Dodd-Frank Act: Fair, equitable and nondiscriminatory access to credit for consumers. ECOA: A creditor shall not discriminate against any applicant on a prohibited basis regarding any aspect of a credit transaction

31 Fair Lending Risk at Every Stage of Credit Transaction Marketing Risk Pricing Risk Current Steering Risk Delinquent Approvals Servicing & Loss Mitigation Risk Denials Redlining Risk Underwriting Risk

Equal Credit Opportunity Act (ECOA) Home Mortgage Disclosure Act (HMDA) Community Reinvestment Act (CRA)")

32 Fair Lending Umbrella Fair Lending Principle laws that govern Fair Lending Principle laws that monitor Fair Lending Fair Housing Act (FHA) Equal Credit Opportunity Act (ECOA) Home Mortgage Disclosure Act (HMDA) Community Reinvestment Act (CRA)

33 Prohibited Basis Characteristics Equal Credit Opportunity Act ECOA & Fair Housing Act Fair Housing Act Marital Status Age Receipt of Income from public assistance programs Exercise of rights under the CCPA (Consumer Credit Protection Act) Race or Color Religion National Origin Gender or Sex Handicap Familial Status

34 3 Types of Illegal Discrimination Overt Evidence of Disparate Treatment When a lender openly discriminates on a prohibited basis or expresses a discriminatory preference. There is overt evidence of discrimination even when a lender expresses, but does not act on, a discriminatory preference. Example: Statements that indicate a discriminatory preference event if it is not acted upon. We don t like to lend to Methodists. Comparative Evidence of Disparate Treatment When a lender treats similarly situated credit applicant differently based on one of the prohibited bases (during underwriting, pricing, and/or assistance). Does not require any showing the treatment was motivated by prejudice or a conscious intention to discriminate beyond the difference in treatment itself. Example: Assisting non-minority couple with adverse information on their credit report while denying a minority with a similar issue without offering the same level of assistance. Example: Offer a credit card limit of $1,000 to applicants age 21 and less. Offer credit card limit of $2,000 for applicants above age 21. Disparate Impact (Upheld by the Supreme Court 6/25/15) When a lender applies a racially (or otherwise) neutral policy or practice equally to all credit applicants but the policy or practice disproportionately excludes or burdens certain persons on a prohibited basis. Also known as the Effects Test. When an Agency finds that a lender s policy or practice has a disparate impact, the next step is to seek to determine whether the policy or practice is justified by business necessity. Example: No residential loans for less than $400,000. This policy might exclude a high number of applicants from who have lower income levels or lower home values. The uneven effect of the policy is called disparate impact

35 Examples of Prohibited Practices A Lender May Not Because of a Prohibited Basis Characteristic: Fail to provide or provide different information or services regarding any aspect of the lending process; Either discourage or selectively encourage individuals who inquire or apply for credit; or Refuse to extend credit or use different standards in determining whether to extend credit. Adjust or vary the terms of credit offered; Use different standards to evaluate collateral; Treat a borrower differently in servicing a loan or invoking default remedies

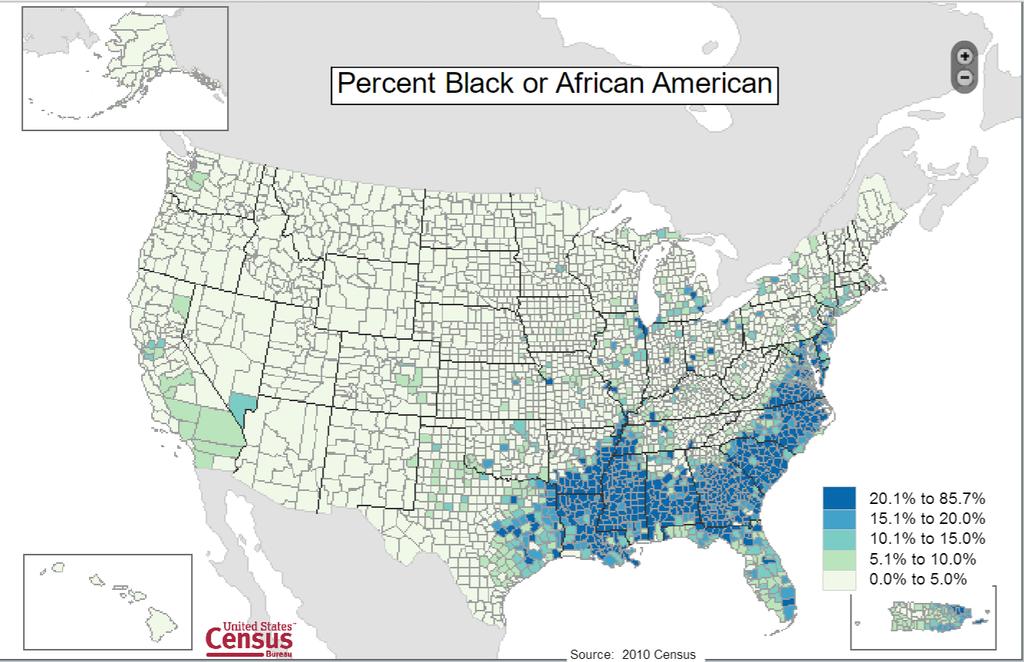

36 Disparate Impact Theory Upheld In June 2015, SCOTUS upheld the concept of disparate impact. This holds financial institutions accountable for understanding where and why disparities exist. However, there are limits on how the regulators can review. The regulators shouldn t pursue or make accusations against a bank based only on data. With disparate impact upheld, fair lending is back squarely in the regulators cross-hairs

37 Conclusion #2 Fair Lending is not going to fade in the background. It is a political hot potato. You must proactively address Fair Lending

38 Focal Points UTAH UNIQUE FAIR LENDING ISSUES

39

40

41

42

43

44 16.7% - Weber County 17.1% - Salt Lake County 12.8% - Millard County 13.5% - Wasatch County

45

46 Conclusion #3 Utah is unique (growth of Hispanics). Individual markets within Utah are unique. Need to Know: How is your market unique? Does marketing understand their responsibility? Does management have a clear picture?

47 8 8 A Quick Overview of the Core Fair Lending Risks 8 KEY FAIR LENDING RISKS & QUESTIONS

48 Fair Lending Risk at Every Stage of Credit Transaction Marketing Risk Pricing Risk Current Steering Risk Delinquent Approvals Servicing & Loss Mitigation Risk Denials Redlining Risk Underwriting Risk

49 Example of Risks in Fair Lending Inherent Risk Market Population Demographics Sales & Marketing Product Lines Socioeconomics Channel Complexity Regulatory Environment Compliance Controls Policies Procedures Monitoring Audits Training Residual Risk Risk

50 8 Primary Fair Lending Risk Areas 1. Compliance Management Risk 2. Marketing Risk 3. Steering Risk 4. Underwriting Risk 5. Pricing Risk 6. Redlining Risk 7. Servicing Risk 8. Modeling Risk

51 2 Parts of Risk 1 Qualitative View 2 Quantitative View

52 Qualitative Assessment Evaluate Your Practices Industry Best Practices Qualitative View Quantitative View

53 Quantitative Assessment Internal Comparison External Comparisons Quantitative View Qualitative View Quantitative View

54 Compliance Program Risk Critical Question: When is the last time you conducted a fair lending risk assessment? Qualitative Review Review Compliance Organization, Staffing, Management Involvement, Training, Record Keeping, Auditing, Policies & Procedures of the Institution s Fair Lending Compliance Systems Quantitative Review General Monitoring Systems: Exception Reports, Audit Results, HMDA Data, Complaints, and Lending Disparities

55 Marketing Risk Critical Question: When is the last time you compared census data to your lending data (applications and originations)? Qualitative Review Advertising: Are there any marketing or advertising that would lead a reasonable person to believe that prohibited basis customers are less desirable? Collateral images exclude minority groups? Advertising in media only serving non-minority areas of the market? Using mediums that are focused on nonminorities? Marketing: Using marketing programs or procedures that exclude one or more regions or geographies that have higher percentages of minority groups? Using mail or distribution lists or other marketing techniques for pre-screened or other offerings that exclude groups of prospective borrowers on a prohibited basis? Exclude geographies that have significantly higher percentages of minority group residents. Quantitative Review: Compare the prohibited basis applicants to representation in total population of the market area. When applicable, compare prohibited basis applicants to applicable HMDA benchmark data. Analysis: Financial Institution Applications vs. Census Demographics Vs. Market Benchmarks

56 Steering Risk Critical Question: When is the last time you compared product take rates been demographic groups? Qualitative Review: Standards for sales process? Standards for referring applicants to subsidiaries, affiliates, channels, and alternative products? Financial incentives to place potential borrowers? Quantitative Review: Compare product take rates (applications and loan originations) between prohibited basis groups and control group(s)? Pay attention to products and features that have potentially negative consequences for borrowers. Compare differences in the percentage of prohibited basis groups and control group(s) between lending channels

57 Underwriting Risk Critical Question: When is the last time you evaluated your exception management program? Qualitative Review: Presence of discretion in the underwriting process? Vague or subjective underwriting criteria? Clear guidance on exceptions (process for approval, reporting, guardrails, compensating factors, documentation) Quantitative Review: Exception Frequency and Reason Codes Disparities (prohibited basis groups vs. control group) Processing Times (Application Date vs. Action Taken) Withdrawn/Incomplete Applications Approval Rates/Denial Rates/Indexed (Denial Disparity Index)

58 Pricing Risk Critical Question: When is the last time you analyzed the disparities between control group and prohibited basis group? Qualitative Review: Presence of broad discretion in loan pricing (rate sheets and fee schedules) Compensation systems for loan officers, brokers and management to charge higher prices? Risk based pricing adjustments not based on objective criteria (or applied consistently) Clear guidance on exceptions (process for approval, reporting, guardrails, compensating factors, documentation) Quantitative Review: Disparities (prohibited basis groups vs. control group) Incidence of rate spread (higher priced) loans Disparities in pricing charged

59 Redlining Risk Critical Question: When is the last time you compared your lending in LMI Census Tracts and Majority-Minority Census Tracts? Qualitative Review: Review lending patterns during the most recent CRA exam (concentration patterns) Does CRA or Market assessment area exclude areas with high concentrations of minorities? Branches in predominantly non-minority neighborhoods? Is there a demarcation of loan products are made available? Redlining and Reverse Redlining. Differences in services available or hours of operation (exclude geographic areas with high concentrations of minorities)? Employee statements that reflect an aversion to doing business in areas with high concentrations of minority residents? Quantitative Review: Disparities (high minority group tracts compared to tracts with low concentrations of minorities) Application, Origination, Denial Rates By Tract Number of rate spread originations By Tract When subprime or alternative products are made available: Explore Reverse Redlining (targeting certain borrowers or areas with less advantageous products or services) Look for excluding certain areas AND targeting certain areas (predatory lending with products with less favorable loan terms sometimes called reverse redlining)

60 Servicing Risk 7 7 Critical Question: When is the last time you reviewed your fee waiver policies, procedures and operating results? Qualitative Review: Controls (policies, audits, monitoring) to ensure ongoing fair lending compliance (consistent treatment of similarly situated individuals) Clear guidance on file documentation for policy exceptions or fee waivers (collections, late fees, etc.) Discretion in determining loan servicing and loss mitigation actions Compensation based on workout, loss mitigation or foreclosure strategy adopted. Consumer complaints (true on all risks especially here) Quantitative Review: Disparities (prohibited basis groups vs. control group) Disparities in loss mitigation servicing options. Disparities in decision processing times. Disparities in collections processes

61 Modeling Risk 8 8 Critical Question: When was the last time you audited the underwriting or pricing model to ensure consistency between policy/procedure and the model? Qualitative Review: Does the financial institution use models to accept or refer applications, or assist in product selection? Does the firm use models to make credit decisions? Does the firm use automated pricing models? How often are the models subject to periodic review? What type of testing exits for the models? Do any of the models treat individuals differently on a prohibited basis? Is age used? Are any third party models used? Quantitative Review: Most Common Disparities (prohibited basis groups vs. control group): Pricing Underwriting

62 Conclusion #4 Risk Assessments don t have to be overly complicated. You simply need to know the right questions to explore in order to gauge risk

63 Fair Lending Compliance Tips COMMON FAIR LENDING TRIPWIRES

64 Common Tripwires for Fair Lending Complaints Consider All Sources Best Practice Tip: Actively Embrace and Compete for Complaints Discretion in Process Marketing, Sales Process, Pricing, Servicing, Loss Mitigation Best Practice Tip: Where discretion exists, monitor! Disparities in Loan Data Control Group vs. Prohibited Basis Group Best Practice Tip: Analyze your data. Know your numbers

65 Common Tripwires for Fair Lending Compensation Systems Individuals rewarded based on loan terms? Best Practice Tip: Have written compensation plans that outline variable compensation. HMDA Data Quality Accuracy of LAR and Source Document (e.g., application) Best Practice Tip: Conduct Independent Review of HMDA Integrity. Exam and Enforcement History Prior Supervisory Issues Identified Best Practice Tip: Formally Track, Address and Be Prepared to Report on All Findings

66 Common Tripwires for Fair Lending Regulation B Violations Technical Violations of Reg B which implements ECOA Best Practice Tip: Beware of Common Violations proactively monitor: Failure to Collect Information Improperly Collecting Information Poor Execution of Adverse Action Notices Reasons for Adverse Action Timely Adverse Action Notices Improperly Requiring Spousal Signature

67 Common Tripwires for Fair Lending Quality of Compliance Management System Based on Size, Complexity and Risk Profile Best Practice Tip: You Should Have Fair Lending Policy Regular Training Regular Review of Lending Policies Ongoing Monitoring Regular Analysis of Loan Data Regular Risk Assessment of Products Active Management Oversight

68 Common Tripwires for Fair Lending Redlining Need to consider both intrabank comparisons and interbank comparisons Best Practice TipReview both internal and external performance context data

69 The Two Ds of Fair Lending Combined.these set of alarms in regards to fair lending risk: 1. Disparities 2. Discretion

70 CFPB: Posted Billboards Beyond ECOA and Fair Housing Act Exam Manuals Bulletins Presentations Reports Semi-Annual Reports Annual FL Reports Settlements Guidance

71 CFPB Fair Lending Annual Report Released April, 2016 Areas of Focus Mortgage Indirect Auto Credit Cards Small Business New HMDA FL Tripwires Adverse Action Notices HMDA Integrity Use of all types of income FL Tripwires (Continued) Complaints Tips (Advocacy Groups, Whistleblowers, and Government Agencies) Supervisory and Enforcement History Quality of CMS Data Analysis Market Insights

72 Conclusion #5 We all learn from others. We can learn from their mistakes and successes. The common tripwires are built from regulator publications (supervisory reports, consent orders, presentations, etc.) and TRUPOINT s consulting work. Pay specific attention to these common tripwires

73 Hot Spots Worth Proactively Monitoring 2 HOT TOPICS ON FAIR LENDING

74 Hot Topic: Redlining Redlining is the practice of denying services, either directly or through selectively raising prices, to residents of certain areas based on the racial or ethnic makeups of those areas. CRA + Fair Lending

75 Hot Topic: Redlining

76 Redlining Trip Wires Redlining Compliance Management System: Do you have a robust redlining Compliance Management Program for Redlining? Explore: Your policies, procedures, training, monitoring, risk assessments, disparity analysis within data, and management reporting/oversight. Marketing Risk (Demand Side of Redlining Risk): Do you have geographic areas with elevated minority populations that are being ignored or excluded? Explore: Applications in minority census tracts, distribution of applications inside market areas, and application market share within the unique market areas. Review quantitative (stats) and qualitative (mapping) perspectives. Be sure to review how your bank compares to peer and/or benchmark data. Origination or Underwriting Risk (Supply Side of Redlining Risk): Do you have geographic areas with elevated minority populations that are being ignored or excluded? Explore: Originations in minority census tracts, distribution of originations inside market areas, and origination market share within the unique market areas. Review quantitative (stats) and qualitative (mapping) perspectives. Be sure to review how your bank compares to peer and/or benchmark data. Reverse Redlining Risk (Targeting): Do you have higher-priced products that are concentrated in high-minority or LMI tracts? Explore: Applications and originations in majority-minority census tracts and compare market share within the unique market areas. Again, review quantitative (stats) and qualitative (mapping) perspectives. Be sure to review how your bank compares to peer and/or benchmark data. Assessment Area Risk (CRA): Do your designated assessment areas intentionally exclude adjacent minority census tracts? Where are your points of distribution (e.g., branches and brokers)? Explore: Annually review your assessment areas in comparison to the underlying Low- and Moderate-Income Census Tracts and Majority-Minority Census Tracts. Be sure to layer-in your geocoded branches, ATMs, broker locations and your lending patterns

77 Hot Topic: New HMDA Here Comes HMDA Plus 2015 New HMDA Extensive Changes Covered Institutions Exempt Low Volume (25/100) Covered Transactions Dwelling Secured Standard (change from purpose based criteria) Disclosure Loan Level Data Types of Loans Dwelling Secured Test: Home Purchases, Home Improvement, Refinance Loans Pricing Pricing (interest rate, points and fees, rate spreads for all loans, riskier features) Loan Information Channel, Property Value, DTI, CLTV, AUS Results Denial Reasons Borrower s Age, Credit Score

78 Hot Topic: HMDA Plus 2017 Dates: 1/1/2017 is effective date for excluding lowvolume depository institutions from coverage Add Temporary Low Volume Threshold - 25 Home Purchase Loans (including refinancings) in each of the two proceeding years Data Collection: Collect 2017 data as required under current rule for reporting in 2018 Data Submission: Submit 2016 data by 3/1/ Dates: 1/1/2018 is effective date for MOST provisions related to coverage, data collection, recording, reporting and disclosing Data Collection: Collect 2018 data as required under the NEW rule for reporting in 2019 Data Submission: Submit 2017 data by 3/1/2017 to the CFPB 2019 Dates: 1/1/2019 is effective date for changes to enforcement provisions and additional amendments to reporting provisions 2010 Dates: 1/1/2020 is effective date for quarterly reporting provisions (60,000 applications per year roughly 20 institutions)

79 Hot Topic: HMDA Plus Should be thinking about Project Plan Project Owner Software Workflow Analysis to Determine Impacted Software Policies Detailed Procedures Detailed Data Dictionary Training Detailed Analytics Know Your Story

80 Transactional Coverage

81

82 The Many Emotions of HMDA 82

83 HMDA Analysis Lets kick this data analysis up a notch. 83

84 Analyzing Your HMDA Data Analytics Pendulum is Swinging Evolution Simple Comparisons Complex Statistical Analysis Simple Comparisons On Limited Data Simple HMDA Analysis Comple x Complex Statistical Analysis on Multiple Dimensions + Speed of Analysis + Consistency 84

85 Fair Lending Compliance Tips SUMMARY & BEST PRACTICE TIPS

86 8 Fair Lending Best Practices 1. Conduct a Regular Risk Assessment Focus on alignment and evaluating high-risk areas Double D: Discretion and Disparities 2. Ensure top-down leadership and a culture of compliance Fair Lending is the Ultimate Team Sport 3. Develop or improve written policies and procedures that comply with the spirit and technicalities of the regulations (Reg B and HMDA) Include core components, like a fair lending policy statement and a training plan. Don t create policies and procedures you don t have the capacity manage! 4. Conduct Both General and Role-Specific Training Include training for new hires, methods to test retention and reinforce learnings Don t forget the Board of Directors 5. Monitor your Lending Data, Exceptions, and Service Activity (like fee waivers, collections deferrals, and loss mitigation to determine where discrimination may exist) 6. Audit to Confirm Execution HMDA Scrubs, Regulation B (e.g., adverse action notices), Exception Files, Models (e.g., Pricing) 7. Aggregate activities and reporting for a more complete fair lending perspective Make it easy on Senior Management to have Optics into Fair Lending Risk 8. Continuously review the regulatory environment Look to settlements, regulatory guidance, press releases, presentations, supervisory updates, and peer bank conversations for insights

87 Conclusion #6 Adopt the best practices. Lower your bank s fair lending risk!

88 Don t Underestimate The Importance of a Strong Compliance Culture FAIR LENDING IS A TEAM SPORT

89 You Must Understand Different Points of View At the bank, everyone has different points of view Compliance Officer

90 Points of View Matter in Fair Lending Compliance Officer Mortgage Loan Officer

91 Points of View Compliance vs. Lenders? Exceptions are bad. They are risky! Exceptions are necessary. They are required!

92 Conclusion #7 Fair Lending is the ultimate team sport in Banking. It takes everyone! To be successful: acknowledge the different points of view. Find a common ground and common goals

93 The Wrap Up! CONCLUSIONS CONCLUDED

94 Conclusions Concluded 0. Stereotypes are everywhere. How do they impact your financial institution? 1. Risk Assessments can bring sanity back to your world How do you prioritize your biggest areas of risk? 2. Fair Lending risk remains a popular focus of regulators and outside groups. How are you helping your organization embrace it? 3. Utah is different. It impacts approach to Fair Lending. How is your market area unique? Does management understand? 4. Risk Assessments don t have to be overly complex. Do you know the right questions to ask? 5. Learn from the common tripwires. How does your organization effectively deal with the issues? 6. Consider the Best Practices How do you currently compare? 7. Fair Lending is a Ultimate Team Sport. It is not compliance s role! - How do you inspire collaboration and team work?

95 About Us TRUPOINT PARTNERS

96 Me Free Risk Assessment Questions? Succinct Fair Lending Risk Assessment Template Andy Barksdale:

97 About TRUPOINT Partners TRUPOINT Partners is committed to financial institution success through efficient insight. TRUPOINT provides compliance solutions to more than 500 financial institutions through an innovative blend of data analytics, business intelligence, and compliance expertise. Specialties include Fair Lending, HMDA, CRA, and UDAAP compliance, including analysis, regression, consulting and more. Headquartered in Charlotte, NC

98 Andy Barksdale, CRCM Andy Barksdale is a Managing Director at TRUPOINT Partners. Since starting his banking career more than 20 years ago, Mr. Barksdale has held positions that demonstrate his commitment to, and knowledge of, community banking. He has consulted with over a hundred financial institutions by analyzing their lending data; identifying the areas of risk; advising on the focal points for ongoing fair lending analysis; conducting CRA self-assessments and providing assessment-area reviews; implementing risk assessments and best-practice reviews for fair lending; delivering training; and providing confidence in preparing for upcoming examinations. Andy s career stated with SunTrust Banks in Atlanta after earning a bachelor s degree in finance from the University of Georgia. At SunTrust, he spent time as a commercial lender, internal loan review, and coordinated the affiliate bank relations. He also worked with Georgia National Bank in Athens, Georgia serving various roles including internal audit, compliance and loan review. Before joining TRUPOINT Partners, Andy held a variety of roles serving community banks including ten years with UVEST Financial Services in Charlotte, N.C. where he supported financial institutions by providing consulting and broker-dealer services. Today, Mr. Barksdale leads and manages TRUPOINT Partners Professional Services Organization where the team delivers valued regulatory compliance consulting and analytic services. TRUPOINT Partners specializes in providing Fair Lending, CRA, HMDA and related compliance services to more than 500 financial institutions across the country. Other 1989 BBA University of Georgia 1993 MBA University of Georgia Certified Regulatory Compliance Manager (CRCM) Die Hard Georgia Bulldog Fan Bourbon Tasting Expert

99 We Can Help! TRUPOINT Partners Andy Barksdale Cell: General HMDA Data Analysis HMDA Data Interpretation Redlining Analysis Fair Lending Risk Mitigation HMDA Scrubs Consumer Lending Analysis Risk Assessments CRA Geocoding and Analysis AML/BSA Compliance

Fair Lending Compliance Basics: Class is in Session!

Fair Lending Compliance Basics: Class is in Session! How to Control Fair Lending Risk and Identify Redlining Risk Meet Your Teacher Kimberly Boatwright, CRCM, CAMS Director of Compliance TRUPOINT Partners

Fair Lending Compliance Basics: Class is in Session! How to Control Fair Lending Risk and Identify Redlining Risk Meet Your Teacher Kimberly Boatwright, CRCM, CAMS Director of Compliance TRUPOINT Partners

Fair Lending Risk Management

Presented by: Martin (Marty) Mitchell, CRCM Managing Director, ProBank Austin Robert J. (Bob) Mullenbach, CRCM Managing Director, Compliance Division Deputy, ProBank Austin Fair Lending Laws ECOA Prohibits

Presented by: Martin (Marty) Mitchell, CRCM Managing Director, ProBank Austin Robert J. (Bob) Mullenbach, CRCM Managing Director, Compliance Division Deputy, ProBank Austin Fair Lending Laws ECOA Prohibits

Fair Lending Examination Procedures Summary and Risk Factors Table

Federal Reserve Bank of Dallas Fair Lending Examination Procedures Summary and Risk Factors Table This publication is intended as a summary of the Fair Lending Examination Procedures. Also included is

Federal Reserve Bank of Dallas Fair Lending Examination Procedures Summary and Risk Factors Table This publication is intended as a summary of the Fair Lending Examination Procedures. Also included is

Fair Winds and Following Seas The sea, its perils and fair lending management? Timothy R. Burniston Executive Vice President, WKFS Consulting

Fair Winds and Following Seas The sea, its perils and fair lending management? Timothy R. Burniston Executive Vice President, WKFS Consulting SEA CAPTAIN: Responsible for operating ships in lakes, rivers,

Fair Winds and Following Seas The sea, its perils and fair lending management? Timothy R. Burniston Executive Vice President, WKFS Consulting SEA CAPTAIN: Responsible for operating ships in lakes, rivers,

To learn about navigation and other features of this e-learning course, click Help. Click Next to continue to the next page.

Welcome to Fair Lending Practices Extending credit is a cornerstone of banking. Because of the need society has for lending and credit, Congress has passed a number of acts ensuring that banks distribute

Welcome to Fair Lending Practices Extending credit is a cornerstone of banking. Because of the need society has for lending and credit, Congress has passed a number of acts ensuring that banks distribute

Managing Fair and Responsible Lending Challenges and Risks

Managing Fair and Responsible Lending Challenges and Risks NYBA Technology, Compliance and Risk Management Forum White Plains, NY May 13, 2015 Legal Counsel to the Financial Services Industry Presented

Managing Fair and Responsible Lending Challenges and Risks NYBA Technology, Compliance and Risk Management Forum White Plains, NY May 13, 2015 Legal Counsel to the Financial Services Industry Presented

Notice. Conducting a Fair Lending Self Assessment Britt Faircloth, CRCM 4/2/2018. April 2018 Florida Bankers Association

Conducting a Fair Lending Self Assessment Britt Faircloth, CRCM April 2018 Florida Bankers Association Notice The information presented in this seminar summarizes general guidance and is intended only

Conducting a Fair Lending Self Assessment Britt Faircloth, CRCM April 2018 Florida Bankers Association Notice The information presented in this seminar summarizes general guidance and is intended only

MBBA-NH & MAMP. Compliance Conference. April 19, 2017

MBBA-NH & MAMP Compliance Conference April 19, 2017 Agenda HMDA Overview Readiness Steps HMDA Expansion Fields 2 New HMDA Rule Summary Changes to Home Mortgage Disclosure: Regulation C Types of institutions

MBBA-NH & MAMP Compliance Conference April 19, 2017 Agenda HMDA Overview Readiness Steps HMDA Expansion Fields 2 New HMDA Rule Summary Changes to Home Mortgage Disclosure: Regulation C Types of institutions

HMDA Workshop Part IV: Fair Lending & HMDA

HMDA Workshop Part IV: Fair Lending & HMDA Sunday, Sept. 18, 2016, 4:45 pm Moderator: Richard H. Harvey, Jr., Chief Compliance Officer, Colonial Savings, F.A. Panelists: Melanie Brody, Partner, Mayer Brown

HMDA Workshop Part IV: Fair Lending & HMDA Sunday, Sept. 18, 2016, 4:45 pm Moderator: Richard H. Harvey, Jr., Chief Compliance Officer, Colonial Savings, F.A. Panelists: Melanie Brody, Partner, Mayer Brown

Identifying, Assessing and Mitigating Potential Redlining Risk

Identifying, Assessing and Mitigating Potential Redlining Risk Objectives Understanding Potential Redlining Risk Understanding the Reasonable Expected Market Area (REMA) vs CRA Assessment Area Understanding

Identifying, Assessing and Mitigating Potential Redlining Risk Objectives Understanding Potential Redlining Risk Understanding the Reasonable Expected Market Area (REMA) vs CRA Assessment Area Understanding

Fair Lending Risk Management: Lessons from Recent Settlements

November 2012 Fair Lending Risk Management: Lessons from Recent Settlements Introduction Fair lending continues to be a major enforcement priority of federal agencies, and the financial implications have

November 2012 Fair Lending Risk Management: Lessons from Recent Settlements Introduction Fair lending continues to be a major enforcement priority of federal agencies, and the financial implications have

Facing Today s Real Estate Regulations

Proudly Sponsored by Facing Today s Real Estate Regulations Presented by Don Braspenninckx Day, June 11, 2016 1:30 p.m. 1 Introduction Numerous regulatory changes in the real estate industry within last

Proudly Sponsored by Facing Today s Real Estate Regulations Presented by Don Braspenninckx Day, June 11, 2016 1:30 p.m. 1 Introduction Numerous regulatory changes in the real estate industry within last

2016 Interagency Fair Lending Hot Topics

2016 Interagency Fair Lending Hot Topics Outlook Live Webinar October 4, 2016 Visit us at www.consumercomplianceoutlook.org Welcome to Outlook Live Logistics Call-in number: 1-888-625-5230 Conference code:

2016 Interagency Fair Lending Hot Topics Outlook Live Webinar October 4, 2016 Visit us at www.consumercomplianceoutlook.org Welcome to Outlook Live Logistics Call-in number: 1-888-625-5230 Conference code:

Fair & Responsible Lending in the Regulatory Crosshairs

Fair & Responsible Lending in the Regulatory Crosshairs Legal Counsel to the Financial Services Industry Minnesota Banking Law Institute April 5, 2013 Andrea K. Mitchell Partner Lori J. Sommerfield Counsel

Fair & Responsible Lending in the Regulatory Crosshairs Legal Counsel to the Financial Services Industry Minnesota Banking Law Institute April 5, 2013 Andrea K. Mitchell Partner Lori J. Sommerfield Counsel

Fair Housing Conference

Fair Housing Conference U.S. Attorney s Office for the District of Idaho April 2012 Laws Enforced by DOJ Fair Housing Act (FHA) Equal Credit Opportunity Act (ECOA) Titles II and III, Civil Rights Act of

Fair Housing Conference U.S. Attorney s Office for the District of Idaho April 2012 Laws Enforced by DOJ Fair Housing Act (FHA) Equal Credit Opportunity Act (ECOA) Titles II and III, Civil Rights Act of

2017 Interagency Fair Lending Hot Topics

2017 Interagency Fair Lending Hot Topics Outlook Live Webinar November 16, 2017 Visit us at www.consumercomplianceoutlook.org Visit us at www.consumercomplianceoutlook.org 1 Welcome to Outlook Live Logistics

2017 Interagency Fair Lending Hot Topics Outlook Live Webinar November 16, 2017 Visit us at www.consumercomplianceoutlook.org Visit us at www.consumercomplianceoutlook.org 1 Welcome to Outlook Live Logistics

National Association of Federal Credit Unions. Fair Lending Training (Part I) March 19, Lori J. Sommerfield Counsel BuckleySandler LLP

March 19, Lori J. Sommerfield Counsel BuckleySandler LLP") National Association of Federal Credit Unions Fair Lending Training (Part I) March 19, 2014 Lori J. Sommerfield Counsel BuckleySandler LLP Order of Presentation Overview of Fair Lending Laws & Regulations

National Association of Federal Credit Unions Fair Lending Training (Part I) March 19, 2014 Lori J. Sommerfield Counsel BuckleySandler LLP Order of Presentation Overview of Fair Lending Laws & Regulations

New Jersey Bankers Association 2017 Compliance University Fair Lending Redlining Risks

New Jersey Bankers Association 2017 Compliance University Fair Lending Redlining Risks June 14, 2017 Presented by Rose N. Egbuiwe, Fair Lending Examination Specialist 1 Objectives Provide Insight on Fair

New Jersey Bankers Association 2017 Compliance University Fair Lending Redlining Risks June 14, 2017 Presented by Rose N. Egbuiwe, Fair Lending Examination Specialist 1 Objectives Provide Insight on Fair

Fair Lending Internal Audits

Fair Lending Internal Audits ACUIA Region 6 Conference Presented By: Kristie Kenney Hoover, NCCO Internal Audit Manager, Doeren Mayhew Florida Michigan North Carolina Texas Insight. Oversight. Foresight.

Fair Lending Internal Audits ACUIA Region 6 Conference Presented By: Kristie Kenney Hoover, NCCO Internal Audit Manager, Doeren Mayhew Florida Michigan North Carolina Texas Insight. Oversight. Foresight.

Fair Lending Issues and Hot Topics

Fair Lending Issues and Hot Topics Outlook Live Webinar November 2, 2011 Non-Discrimination Working Group of the Financial Fraud Enforcement Task Force Visit us at www.consumercomplianceoutlook.org informational

Fair Lending Issues and Hot Topics Outlook Live Webinar November 2, 2011 Non-Discrimination Working Group of the Financial Fraud Enforcement Task Force Visit us at www.consumercomplianceoutlook.org informational

FAIR LENDING POLICY I. INTRODUCTION A. OVERVIEW

FAIR LENDING POLICY I. INTRODUCTION A. OVERVIEW The purpose of this Fair Lending Policy ( Policy ) is to implement consumer protection mechanisms that ensure compliance with all applicable federal and

FAIR LENDING POLICY I. INTRODUCTION A. OVERVIEW The purpose of this Fair Lending Policy ( Policy ) is to implement consumer protection mechanisms that ensure compliance with all applicable federal and

Fair Lending Risks and HMDA

Fair Lending Risks and HMDA Kathleen O. Blanchard Key Compliance Services, LLC October 8, 2018 1 Topics HMDA History Partial Exemptions Privacy of HMDA Data Fair Lending Concerns 2 HMDA History 3 HMDA

Fair Lending Risks and HMDA Kathleen O. Blanchard Key Compliance Services, LLC October 8, 2018 1 Topics HMDA History Partial Exemptions Privacy of HMDA Data Fair Lending Concerns 2 HMDA History 3 HMDA

New and Re-emerging Fair Lending Risks. Article by Austin Brown & Loretta Kirkwood October 2014

New and Re-emerging Fair Lending Risks Article by Austin Brown & Loretta Kirkwood BY AUSTIN BROWN & LORETTA KIRKWOOD Austin Brown Loretta Kirkwood Regulators have been focused recently on several new and

New and Re-emerging Fair Lending Risks Article by Austin Brown & Loretta Kirkwood BY AUSTIN BROWN & LORETTA KIRKWOOD Austin Brown Loretta Kirkwood Regulators have been focused recently on several new and

Keeping Fintech Fair: Thinking about Fair Lending and UDAP Risks

Keeping Fintech Fair: Thinking about Fair Lending and UDAP Risks Outlook Live Webinar July 16, 2018 Carol A. Evans Associate Director Div. of Consumer & Community Affairs Federal Reserve Board Katrina

Keeping Fintech Fair: Thinking about Fair Lending and UDAP Risks Outlook Live Webinar July 16, 2018 Carol A. Evans Associate Director Div. of Consumer & Community Affairs Federal Reserve Board Katrina

Keeping Fintech Fair: Thinking about Fair Lending and UDAP Risks

Keeping Fintech Fair: Thinking about Fair Lending and UDAP Risks Outlook Live Webinar July 16, 2018 Carol A. Evans Associate Director Div. of Consumer & Community Affairs Federal Reserve Board Katrina

Keeping Fintech Fair: Thinking about Fair Lending and UDAP Risks Outlook Live Webinar July 16, 2018 Carol A. Evans Associate Director Div. of Consumer & Community Affairs Federal Reserve Board Katrina

FAIR SERVICING: REGULATORS WATCH FOR DISCRIMINATION BY SERVICERS

FAIR SERVICING: REGULATORS WATCH FOR DISCRIMINATION BY SERVICERS BY BENJAMIN P. SAUL AND DANIEL ZYTNICK Fair lending requirements apply throughout the life of the loan! 1 Federal regulators delivered that

FAIR SERVICING: REGULATORS WATCH FOR DISCRIMINATION BY SERVICERS BY BENJAMIN P. SAUL AND DANIEL ZYTNICK Fair lending requirements apply throughout the life of the loan! 1 Federal regulators delivered that

Loan Growth and Compliance Pitfalls

Loan Growth and Compliance Pitfalls presented by LOANLINER Compliance Information provided in this presentation, including all materials, should not be construed as legal services, legal advice, or in

Loan Growth and Compliance Pitfalls presented by LOANLINER Compliance Information provided in this presentation, including all materials, should not be construed as legal services, legal advice, or in

Implications and Risks of New HMDA Data Disclosure

Implications and Risks of New HMDA Data Disclosure By David Skanderson, Ph.D. January 2018 A version of this paper appeared in ABA Bank Compliance, January/February 2018 The conclusions set forth herein

Implications and Risks of New HMDA Data Disclosure By David Skanderson, Ph.D. January 2018 A version of this paper appeared in ABA Bank Compliance, January/February 2018 The conclusions set forth herein

Compliance Risk Assessments Chicago Region Banker Workshop Series

Compliance Risk Assessments 2016 Chicago Region Banker Workshop Series Statement During the onsite portion of a compliance examination, examiners review adherence to all consumer protection-related regulations.

Compliance Risk Assessments 2016 Chicago Region Banker Workshop Series Statement During the onsite portion of a compliance examination, examiners review adherence to all consumer protection-related regulations.

FREQUENTLY ASKED QUESTIONS ABOUT THE NEW HMDA DATA. General Background

Federal Reserve Bank of New York Statistics Function March 31, 2005 FREQUENTLY ASKED QUESTIONS ABOUT THE NEW HMDA DATA General Background 1. What is the Home Mortgage Disclosure Act (HMDA)? HMDA, enacted

Federal Reserve Bank of New York Statistics Function March 31, 2005 FREQUENTLY ASKED QUESTIONS ABOUT THE NEW HMDA DATA General Background 1. What is the Home Mortgage Disclosure Act (HMDA)? HMDA, enacted

July 31, :30PM to 2:30PM CDT. Fair Lending: Can You Make Exceptions?

July 31, 2018 1:30PM to 2:30PM CDT Fair Lending: Can You Make Exceptions? Options to Join Webinar and audio Click on the link: Fair Lending Webcast Connect to audio Call Using Computer (preferred method):

July 31, 2018 1:30PM to 2:30PM CDT Fair Lending: Can You Make Exceptions? Options to Join Webinar and audio Click on the link: Fair Lending Webcast Connect to audio Call Using Computer (preferred method):

Fair Lending THIS PUBLICATION IS. counsel for advice on specific fact situations. Copyrighted by Compliance Resource, LLC, April 2017

Fair Lending THIS PUBLICATION IS Not offered as legal advice SO Readers should consult with legal counsel for advice on specific fact situations. Copyrighted by Compliance Resource, LLC, April 2017 No

Fair Lending THIS PUBLICATION IS Not offered as legal advice SO Readers should consult with legal counsel for advice on specific fact situations. Copyrighted by Compliance Resource, LLC, April 2017 No

Fair Lending Hot Topics

Fair Lending Hot Topics Outlook Live Webinar October 17, 2012 Non-Discrimination Working Group of the Financial Fraud Enforcement Task Force Visit us at www.consumercomplianceoutlook.org informational

Fair Lending Hot Topics Outlook Live Webinar October 17, 2012 Non-Discrimination Working Group of the Financial Fraud Enforcement Task Force Visit us at www.consumercomplianceoutlook.org informational

DISPARATE IMPACT S EFFECTS ON PRICING AND COMPENSATION

DISPARATE IMPACT S EFFECTS ON PRICING AND COMPENSATION Ari Karen Principal, Offit Kurman akaren@offitkurman.com 301-575-0340 Daniella Casseres Associate, Offit Kurman dcasseres@offitkurman.com 703-745-1811

DISPARATE IMPACT S EFFECTS ON PRICING AND COMPENSATION Ari Karen Principal, Offit Kurman akaren@offitkurman.com 301-575-0340 Daniella Casseres Associate, Offit Kurman dcasseres@offitkurman.com 703-745-1811

Redlining. Evaluating Risk and Defending Claims. Melanie Brody Partner Mayer Brown

Redlining Evaluating Risk and Defending Claims Melanie Brody Partner Mayer Brown mbrody@mayerbrown.com Brian Clark Senior Manager Ernst & Young Brian.Clark@ey.com Speakers Melanie Brody Partner Mayer Brown

Redlining Evaluating Risk and Defending Claims Melanie Brody Partner Mayer Brown mbrody@mayerbrown.com Brian Clark Senior Manager Ernst & Young Brian.Clark@ey.com Speakers Melanie Brody Partner Mayer Brown

Non-Mortgage Products

Non-Mortgage Products Hot Issues in Non-Mortgage Lending Melanie Brody Partner Mayer Brown mbrody@mayerbrown.com Brian Clark Senior Manager Ernst & Young Brian.Clark@ey.com Speakers Melanie Brody Partner

Non-Mortgage Products Hot Issues in Non-Mortgage Lending Melanie Brody Partner Mayer Brown mbrody@mayerbrown.com Brian Clark Senior Manager Ernst & Young Brian.Clark@ey.com Speakers Melanie Brody Partner

Fair Lending Compliance Management: Developing Strategies for Emerging Challenges

Fair Lending Compliance Management: Developing Strategies for Emerging Challenges August 20, 2014 2014 Crowe Horwath LLP 1 Agenda: The principal concepts of fair lending Current trends in fair lending

Fair Lending Compliance Management: Developing Strategies for Emerging Challenges August 20, 2014 2014 Crowe Horwath LLP 1 Agenda: The principal concepts of fair lending Current trends in fair lending

Fair lending report of the Consumer Financial Protection Bureau

Fair lending report of the Consumer Financial Protection Bureau April 2014 Message from Richard Cordray Director of the CFPB From the moment we first opened our doors, the Consumer Financial Protection

Fair lending report of the Consumer Financial Protection Bureau April 2014 Message from Richard Cordray Director of the CFPB From the moment we first opened our doors, the Consumer Financial Protection

GAO. LARGE BANK MERGERS Fair Lending Review Could be Enhanced With Better Coordination

GAO United States General Accounting Office Report to the Honorable Maxine Waters and the Honorable Bernard Sanders House of Representatives November 1999 LARGE BANK MERGERS Fair Lending Review Could be

GAO United States General Accounting Office Report to the Honorable Maxine Waters and the Honorable Bernard Sanders House of Representatives November 1999 LARGE BANK MERGERS Fair Lending Review Could be

Fair Lending In The Mortgage Industry How You will do Business in 2014?

Fair Lending In The Mortgage Industry How You will do Business in 2014? Presenter: Tammy Butler, Master CMB and Director of Fair lending and Compliance, Optimal Blue Time to Prepare for January 2014 2013

Fair Lending In The Mortgage Industry How You will do Business in 2014? Presenter: Tammy Butler, Master CMB and Director of Fair lending and Compliance, Optimal Blue Time to Prepare for January 2014 2013

Sue Quilty, Quilty & Associates (781)

") Sue Quilty, Quilty & Associates susan.quilty@verizon.net (781)706-9235 Agenda HMDA Today: Review HMDA in the Future: Proposed Changes Surviving HMDA Reporting 2 HMDA Review HMDA Overview Why is HMDA Important

Sue Quilty, Quilty & Associates susan.quilty@verizon.net (781)706-9235 Agenda HMDA Today: Review HMDA in the Future: Proposed Changes Surviving HMDA Reporting 2 HMDA Review HMDA Overview Why is HMDA Important

Econ 321 Group Project EVIDENCE OF DISCRIMINATION IN MORTGAGE LENDING B Y H E L E N F. L A D D

Econ 321 Group Project EVIDENCE OF DISCRIMINATION IN MORTGAGE LENDING B Y H E L E N F. L A D D Goals of Paper Show that discrimination models can prove that there is discrimination in mortgage lending

Econ 321 Group Project EVIDENCE OF DISCRIMINATION IN MORTGAGE LENDING B Y H E L E N F. L A D D Goals of Paper Show that discrimination models can prove that there is discrimination in mortgage lending

April Fair Lending Report of the Consumer Financial Protection Bureau

April 2017 Fair Lending Report of the Consumer Financial Protection Bureau Message from Richard Cordray Director of the CFPB For over five years, the Consumer Financial Protection Bureau has pursued its

April 2017 Fair Lending Report of the Consumer Financial Protection Bureau Message from Richard Cordray Director of the CFPB For over five years, the Consumer Financial Protection Bureau has pursued its

Presentation Topics. Changing Data Requirements Will Effect. Census data update and implications for CRA, HMDA and Fair Lending

Changing Data Requirements Will Effect the CRA and Fair Lending Environment Prepared for the 2012 National Community Reinvestment Conference by Glenn Canner March 28, 2012 The views expressed are those

Changing Data Requirements Will Effect the CRA and Fair Lending Environment Prepared for the 2012 National Community Reinvestment Conference by Glenn Canner March 28, 2012 The views expressed are those

2018 Interagency Fair Lending Hot Topics

2018 Interagency Fair Lending Hot Topics Outlook Live Webinar December 3, 2018 Visit us at www.consumercomplianceoutlook.org Visit us at www.consumercomplianceoutlook.org Welcome to Outlook Live Logistics

2018 Interagency Fair Lending Hot Topics Outlook Live Webinar December 3, 2018 Visit us at www.consumercomplianceoutlook.org Visit us at www.consumercomplianceoutlook.org Welcome to Outlook Live Logistics

Table of Contents. Sample

TABLE OF CONTENTS... 1 CHAPTER 1 INTRODUCTION... 3 1.1 GOALS AND OBJECTIVES... 3 1.2 REQUIRED REVIEW... 3 1.3 APPLICABILITY... 3 CHAPTER 2 ACCOUNTABILITY AND MONITORING... 4 2.1 INTERNAL CONTROLS... 4

TABLE OF CONTENTS... 1 CHAPTER 1 INTRODUCTION... 3 1.1 GOALS AND OBJECTIVES... 3 1.2 REQUIRED REVIEW... 3 1.3 APPLICABILITY... 3 CHAPTER 2 ACCOUNTABILITY AND MONITORING... 4 2.1 INTERNAL CONTROLS... 4

Please stand by, the presentation will begin shortly. Your phones have been muted. If you re using the speakers on your PC you don t need to call in.

Please stand by, the presentation will begin shortly. Your phones have been muted. If you re using the speakers on your PC you don t need to call in. While you are waiting, you may download the presentation

Please stand by, the presentation will begin shortly. Your phones have been muted. If you re using the speakers on your PC you don t need to call in. While you are waiting, you may download the presentation

FAIR LENDING PLAN. NMLS #1820 Fair Lending Plan Policy. (Fair Housing Act/Equal Credit Opportunity Act/Home Mortgage Disclosure Act) March 2013

March 2013") FAIR LENDING PLAN (Fair Housing Act/Equal Credit Opportunity Act/Home Mortgage Disclosure Act) March 2013 CMG Mortgage, Inc. is committed to making high quality mortgage services available to diverse communities

FAIR LENDING PLAN (Fair Housing Act/Equal Credit Opportunity Act/Home Mortgage Disclosure Act) March 2013 CMG Mortgage, Inc. is committed to making high quality mortgage services available to diverse communities

Regulatory Practice Letter December 2014 RPL 14-22

Regulatory Practice Letter December 2014 RPL 14-22 Automobile Supervision and Enforcement Regulatory Actions and CFPB Proposed Rule Executive Summary The automobile finance industry is under heightened

Regulatory Practice Letter December 2014 RPL 14-22 Automobile Supervision and Enforcement Regulatory Actions and CFPB Proposed Rule Executive Summary The automobile finance industry is under heightened

Consumer Financial Protection Bureau. March 15, Draft, Sensitive and Pre-Decisional Not for External Distribution

Consumer Financial Protection Bureau March 15, 2016 Draft, Sensitive and Pre-Decisional Not for External Distribution Outline Home Mortgage Disclosure Act 1) Background 2) Rule Making 3) Changes Coming

Consumer Financial Protection Bureau March 15, 2016 Draft, Sensitive and Pre-Decisional Not for External Distribution Outline Home Mortgage Disclosure Act 1) Background 2) Rule Making 3) Changes Coming

Action Taken. Boot Camp 360 Series Presented by Kimberly Lundquist

Action Taken Boot Camp 360 Series Presented by Kimberly Lundquist Action Taken During the Pre-Application Process, most of the laws pertaining to real estate lending will come into play. We must be careful

Action Taken Boot Camp 360 Series Presented by Kimberly Lundquist Action Taken During the Pre-Application Process, most of the laws pertaining to real estate lending will come into play. We must be careful

Hosted By Mike Gallagher October 2017

Risk Management, Compliance and CRA Hosted By Mike Gallagher October 2017 Today s Agenda Risk Management Risk governance Enterprise Risk Management Operational Risk Management Categories of Risk Compliance

Risk Management, Compliance and CRA Hosted By Mike Gallagher October 2017 Today s Agenda Risk Management Risk governance Enterprise Risk Management Operational Risk Management Categories of Risk Compliance

The New CFPB HMDA Rules

The New CFPB HMDA Rules What You Need to Know Thank you for attending. The webinar has started. Today s Panelists Kathleen Ryan Counsel BuckleySandler LLP Leonard Ryan President QuestSoft Corporation Moderator

The New CFPB HMDA Rules What You Need to Know Thank you for attending. The webinar has started. Today s Panelists Kathleen Ryan Counsel BuckleySandler LLP Leonard Ryan President QuestSoft Corporation Moderator

Racial Discrimination in Mortgage Lending Is There a Problem Here?

Racial Discrimination in Mortgage Lending Is There a Problem Here? Is there racial discrimination in the mortgage lending market of America, and if so, is the problem eroding as time heals old prejudices

Racial Discrimination in Mortgage Lending Is There a Problem Here? Is there racial discrimination in the mortgage lending market of America, and if so, is the problem eroding as time heals old prejudices

Revised HMDA Reporting Overview, Implementation and Planning March 2017

Revised HMDA Reporting Overview, Implementation and Planning March 2017 Kathy Keller, Managing Director, Regulatory Compliance, Newbold Advisors, LLC NewboldAdvisors.com Agenda Overview of the New HMDA

Revised HMDA Reporting Overview, Implementation and Planning March 2017 Kathy Keller, Managing Director, Regulatory Compliance, Newbold Advisors, LLC NewboldAdvisors.com Agenda Overview of the New HMDA

Housing Discrimination in your Community. October 27, 2017 Bloomington, IL Sponsored by:

Housing Discrimination in your Community October 27, 2017 Bloomington, IL Sponsored by: Agenda Fair Housing Laws Fair Lending Laws Community Reinvestment Act How laws are implemented/enforced Local and

Housing Discrimination in your Community October 27, 2017 Bloomington, IL Sponsored by: Agenda Fair Housing Laws Fair Lending Laws Community Reinvestment Act How laws are implemented/enforced Local and

Fair Lending 2012 Significant Risk Management Agenda Items

June 4, 2012 Fair Lending 2012 Significant Risk Management Agenda Items by Joseph T. Lynyak III In the first few months of 2012, lenders were cautiously optimistic that a recent Supreme Court case and

June 4, 2012 Fair Lending 2012 Significant Risk Management Agenda Items by Joseph T. Lynyak III In the first few months of 2012, lenders were cautiously optimistic that a recent Supreme Court case and

HMDA: Haven or Havoc. Michigan Bankers Association. Compliance Services 2016 Temenos USA. All rights reserved.

HMDA: Haven or Havoc Michigan Bankers Association 1 2016 Temenos USA. All rights reserved. About the Speaker Rachelle Dekker CRCM Rachelle Dekker is a Senior Compliance Advisor with the Temenos Compliance

HMDA: Haven or Havoc Michigan Bankers Association 1 2016 Temenos USA. All rights reserved. About the Speaker Rachelle Dekker CRCM Rachelle Dekker is a Senior Compliance Advisor with the Temenos Compliance

IN THE UNITED STATES DISTRICT COURT FOR THE DISTRICT OF MINNESOTA

CASE 0:17-cv-00136-PAM-FLN Document 1 Filed 01/13/17 Page 1 of 14 IN THE UNITED STATES DISTRICT COURT FOR THE DISTRICT OF MINNESOTA UNITED STATES OF AMERICA, ) ) Plaintiff, ) CIVIL ACTION NO 17-cv-136

CASE 0:17-cv-00136-PAM-FLN Document 1 Filed 01/13/17 Page 1 of 14 IN THE UNITED STATES DISTRICT COURT FOR THE DISTRICT OF MINNESOTA UNITED STATES OF AMERICA, ) ) Plaintiff, ) CIVIL ACTION NO 17-cv-136

Memorandum of Understanding between The Consumer Financial Protection Bureau and The United States Department of Justice

Memorandum of Understanding between The Consumer Financial Protection Bureau and The United States Department of Justice I. Background and Purpose. Section 1054(d)(2)(B) of the Dodd-Frank Wall Street Reform

Memorandum of Understanding between The Consumer Financial Protection Bureau and The United States Department of Justice I. Background and Purpose. Section 1054(d)(2)(B) of the Dodd-Frank Wall Street Reform

Major Changes Looming for HMDA Reporting

Major Changes Looming for HMDA Reporting CLIENT ALERT September 25, 2017 Scott D. Samlin samlins@pepperlaw.com Mark T. Dabertin dabertinm@pepperlaw.com In this article, we review the requirements of the

Major Changes Looming for HMDA Reporting CLIENT ALERT September 25, 2017 Scott D. Samlin samlins@pepperlaw.com Mark T. Dabertin dabertinm@pepperlaw.com In this article, we review the requirements of the

Consumer Compliance Hot Topics

Consumer Compliance Hot Topics Agenda Regulatory Timeline: Issued in 2014 On the Horizon for 2015 Areas of Supervisory Focus: Fair Lending Unfair or Deceptive Acts or Practices (UDAP) Flood Vendor Management

Consumer Compliance Hot Topics Agenda Regulatory Timeline: Issued in 2014 On the Horizon for 2015 Areas of Supervisory Focus: Fair Lending Unfair or Deceptive Acts or Practices (UDAP) Flood Vendor Management

National Association of Federal Credit Unions Fair Lending Training (Part II)

") National Association of Federal Credit Unions Fair Lending Training (Part II) April 23, 2014 Jeremiah S. Buckley, Partner Lori J. Sommerfield, Counsel Order of Presentation Key Players in Fair Lending

National Association of Federal Credit Unions Fair Lending Training (Part II) April 23, 2014 Jeremiah S. Buckley, Partner Lori J. Sommerfield, Counsel Order of Presentation Key Players in Fair Lending

EMERGING CONSUMER RISKS FOR COMMUNITY BANKS

November 14, 2016 1 EMERGING CONSUMER RISKS FOR COMMUNITY BANKS 2016 ANNUAL RISK MANAGEMENT CONFERENCE NOVEMBER 14, 2016 November 14, 2016 2 Paul J. Stark, SVP & Chief Credit Officer Civista Bank, Sandusky

November 14, 2016 1 EMERGING CONSUMER RISKS FOR COMMUNITY BANKS 2016 ANNUAL RISK MANAGEMENT CONFERENCE NOVEMBER 14, 2016 November 14, 2016 2 Paul J. Stark, SVP & Chief Credit Officer Civista Bank, Sandusky

CFPB Consumer Laws and Regulations

Consumer Laws and Regulations ECOA Equal Credit Opportunity Act (ECOA) The Equal Credit Opportunity Act (ECOA), which is implemented by Regulation B, applies to all creditors. When originally enacted,

Consumer Laws and Regulations ECOA Equal Credit Opportunity Act (ECOA) The Equal Credit Opportunity Act (ECOA), which is implemented by Regulation B, applies to all creditors. When originally enacted,

Regulatory Environments

Analytics in Fair Lending and Regulatory Environments Deanna Neal First Vice-President Corporate Compliance SunTrust Bank Jeff Morrison First Vice-President Corporate Compliance SunTrust Bank #AnalyticsX

Analytics in Fair Lending and Regulatory Environments Deanna Neal First Vice-President Corporate Compliance SunTrust Bank Jeff Morrison First Vice-President Corporate Compliance SunTrust Bank #AnalyticsX

LENDING: KEY EXAMINER TRENDS

LENDING: KEY EXAMINER TRENDS 2015 Temenos USA, Inc. All rights reserved. Leah M. Hamilton Chief Compliance Officer, TriComply Services WHAT YOU WILL LEARN TRID Compliance Reprieve Common issues Regulation

LENDING: KEY EXAMINER TRENDS 2015 Temenos USA, Inc. All rights reserved. Leah M. Hamilton Chief Compliance Officer, TriComply Services WHAT YOU WILL LEARN TRID Compliance Reprieve Common issues Regulation

CONSUMER COMPLIANCE UPDATE. David Wright, Field Supervisor

CONSUMER COMPLIANCE UPDATE David Wright, Field Supervisor AGENDA Introduction Consumer Harm Making compliance examinations more effective and efficient Compliance Emerging Issues Updated FFIEC Compliance

CONSUMER COMPLIANCE UPDATE David Wright, Field Supervisor AGENDA Introduction Consumer Harm Making compliance examinations more effective and efficient Compliance Emerging Issues Updated FFIEC Compliance

Why CRA Data and Analysis is More Important Than Ever

Why CRA Data and Analysis is More Important Than Ever The webinar will begin at the top of the hour. You may download the presentation at: www.questsoft.com/cradata Why CRA Data and Analysis is More Important

Why CRA Data and Analysis is More Important Than Ever The webinar will begin at the top of the hour. You may download the presentation at: www.questsoft.com/cradata Why CRA Data and Analysis is More Important

2018 HMDA Implementation. Presented By: Karen Ruckle, Director of Compliance Bank of the Ozarks

2018 HMDA Implementation Presented By: Karen Ruckle, Director of Compliance Bank of the Ozarks 2018 HMDA Loan Volume Test # Loans #Loans #Loans Home Purchase Or Refi (Dwelling Secured) in prior calendar

2018 HMDA Implementation Presented By: Karen Ruckle, Director of Compliance Bank of the Ozarks 2018 HMDA Loan Volume Test # Loans #Loans #Loans Home Purchase Or Refi (Dwelling Secured) in prior calendar

CFPB Consumer Laws and Regulations

Consumer Laws and Regulations Home Mortgage Disclosure Act 1 The Home Mortgage Disclosure Act () was enacted by the Congress in 1975 and is implemented by Regulation C (12 CFR Part 1003). 2 The period

Consumer Laws and Regulations Home Mortgage Disclosure Act 1 The Home Mortgage Disclosure Act () was enacted by the Congress in 1975 and is implemented by Regulation C (12 CFR Part 1003). 2 The period

Why CRA Data and Analysis is More Important Than Ever

Why CRA Data and Analysis is More Important Than Ever The webinar will begin at the top of the hour. You may download the presentation at: www.questsoft.com/cradata Why CRA Data and Analysis is More Important

Why CRA Data and Analysis is More Important Than Ever The webinar will begin at the top of the hour. You may download the presentation at: www.questsoft.com/cradata Why CRA Data and Analysis is More Important

PUBLIC DISCLOSURE. June 4, 2012 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION. Utah Independent Bank RSSD #

PUBLIC DISCLOSURE June 4, 2012 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION Utah Independent RSSD # 256179 55 South State Street Salina, Utah 84654 Federal Reserve of San Francisco 101 Market Street

PUBLIC DISCLOSURE June 4, 2012 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION Utah Independent RSSD # 256179 55 South State Street Salina, Utah 84654 Federal Reserve of San Francisco 101 Market Street

CFPB Supervision and Examination Manual ECOA Components

APPENDIX D5 CFPB Supervision and Examination Manual ECOA Components [Editor s Note: This appendix reprints the Equal Credit Opportunity Act components of the Consumer Financial Protection Bureau s Supervision

APPENDIX D5 CFPB Supervision and Examination Manual ECOA Components [Editor s Note: This appendix reprints the Equal Credit Opportunity Act components of the Consumer Financial Protection Bureau s Supervision

To Ensure Fair and Equal Treatment

Self-Testing To Ensure Fair and Equal Treatment Self-testing is a voluntary undertaking designed to ensure compliance and manage legal and business risk. Self-testing offers the compliance manager a window

Self-Testing To Ensure Fair and Equal Treatment Self-testing is a voluntary undertaking designed to ensure compliance and manage legal and business risk. Self-testing offers the compliance manager a window

HMDA / Regulation C Amendments New 1003 Application

HMDA / Regulation C Amendments New 1003 Application January 2017 1Nations Direct Mortgage, LLC Mission Statement - To lead the third party residential mortgage industry by providing products and services

HMDA / Regulation C Amendments New 1003 Application January 2017 1Nations Direct Mortgage, LLC Mission Statement - To lead the third party residential mortgage industry by providing products and services

CFPB Supervision and Examination Process

Background Title X of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (the Act) 1 established the Consumer Financial Protection Bureau (CFPB) and authorizes it to supervise certain

Background Title X of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (the Act) 1 established the Consumer Financial Protection Bureau (CFPB) and authorizes it to supervise certain

MORTGAGE BANKERS ASSOCIATION OF ALABAMA

MORTGAGE BANKERS ASSOCIATION OF ALABAMA What s on the horizon for 2017? January 17, 2017 Presented by: J. David Dresher Jason R. Bushby Bradley Arant Boult Cummings LLP Attorney-Client Privilege. Agenda

MORTGAGE BANKERS ASSOCIATION OF ALABAMA What s on the horizon for 2017? January 17, 2017 Presented by: J. David Dresher Jason R. Bushby Bradley Arant Boult Cummings LLP Attorney-Client Privilege. Agenda

Who is Lending and Who is Getting Loans?

Trends in 1-4 Family Lending in New York City An ANHD White Paper February 2016 As much as New York City is a city of renters, nearly a third of New Yorkers own their own homes. Responsible, affordable

Trends in 1-4 Family Lending in New York City An ANHD White Paper February 2016 As much as New York City is a city of renters, nearly a third of New Yorkers own their own homes. Responsible, affordable

What s New in Mortgage Lending Compliance?

What s New in Mortgage Lending Compliance? Michael R. Christians Senior Federal Compliance Counsel Credit Union National Association Copyright 2016 by Credit Union National Association. All rights reserved.

What s New in Mortgage Lending Compliance? Michael R. Christians Senior Federal Compliance Counsel Credit Union National Association Copyright 2016 by Credit Union National Association. All rights reserved.

FINANCIAL INSTITUTION GOVERNANCE AND REGULATION SERVICES EXPERTS WITH IMPACT

FINANCIAL INSTITUTION GOVERNANCE AND REGULATION SERVICES EXPERTS WITH IMPACT In today s highly competitive and heavily regulated environment, financial institutions are challenged to remain profitable

FINANCIAL INSTITUTION GOVERNANCE AND REGULATION SERVICES EXPERTS WITH IMPACT In today s highly competitive and heavily regulated environment, financial institutions are challenged to remain profitable

CRA for Community-Based Organizations. An Introduction to the Community Reinvestment Act

CRA for Community-Based Organizations An Introduction to the Community Reinvestment Act 1 CRA: History and Context CRA: What It Is A U.S. law that encourages regulated, insured depository institutions

CRA for Community-Based Organizations An Introduction to the Community Reinvestment Act 1 CRA: History and Context CRA: What It Is A U.S. law that encourages regulated, insured depository institutions

Why is Non-Bank Lending Highest in Communities of Color?

Why is Non-Bank Lending Highest in Communities of Color? An ANHD White Paper October 2017 New York is a city of renters, but nearly a third of New Yorkers own their own homes. The stock of 2-4 family homes

Why is Non-Bank Lending Highest in Communities of Color? An ANHD White Paper October 2017 New York is a city of renters, but nearly a third of New Yorkers own their own homes. The stock of 2-4 family homes

Compliance Challenges in a Changing Economic Environment

Compliance Challenges in a Changing Economic Environment Call the Fed Audio Conference December 10, 2008 The following presentation contains the views and opinions of the speakers and his or her interpretation

Compliance Challenges in a Changing Economic Environment Call the Fed Audio Conference December 10, 2008 The following presentation contains the views and opinions of the speakers and his or her interpretation

Indirect Auto Lending Fair Lending Considerations

Indirect Auto Lending Fair Lending Considerations Outlook Live Webinar August 6, 2013 Consumer Financial Protection Bureau Federal Reserve Board U.S. Department of Justice Visit us at www.consumercomplianceoutlook.org

Indirect Auto Lending Fair Lending Considerations Outlook Live Webinar August 6, 2013 Consumer Financial Protection Bureau Federal Reserve Board U.S. Department of Justice Visit us at www.consumercomplianceoutlook.org

PUBLIC DISCLOSURE. January 17, 2006 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION. 500 Linden Avenue South San Francisco, California 94080

PUBLIC DISCLOSURE January 17, 2006 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION Liberty Bank RSSD - 478766 500 Linden Avenue South San Francisco, California 94080 Federal Reserve Bank of San Francisco

PUBLIC DISCLOSURE January 17, 2006 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION Liberty Bank RSSD - 478766 500 Linden Avenue South San Francisco, California 94080 Federal Reserve Bank of San Francisco

Home Mortgage Disclosure Act; Regulation C; Official Staff Interpretations; HMDA FAQs

Home Mortgage Disclosure Act UNITED STATES CODE TITLE 12. BANKS AND BANKING CHAPTER 29--HOME MORTGAGE DISCLOSURE 1/2/2011 7:35:47 PM WKFS CompliSource January 2011 Page: 1 1/2/2011 7:35:47 PM HMDA 12 USC

Home Mortgage Disclosure Act UNITED STATES CODE TITLE 12. BANKS AND BANKING CHAPTER 29--HOME MORTGAGE DISCLOSURE 1/2/2011 7:35:47 PM WKFS CompliSource January 2011 Page: 1 1/2/2011 7:35:47 PM HMDA 12 USC

IN THE UNITED STATES DISTRICT COURT FOR THE NORTHERN DISTRICT OF GEORGIA ATLANTA DIVISION COMPLAINT

1 of 5 7/31/2007 4:02 PM IN THE UNITED STATES DISTRICT COURT FOR THE NORTHERN DISTRICT OF GEORGIA ATLANTA DIVISION UNITED STATES OF AMERICA, Plaintiff, v. DECATUR FEDERAL SAVINGS AND LOAN ASSOCIATION,

1 of 5 7/31/2007 4:02 PM IN THE UNITED STATES DISTRICT COURT FOR THE NORTHERN DISTRICT OF GEORGIA ATLANTA DIVISION UNITED STATES OF AMERICA, Plaintiff, v. DECATUR FEDERAL SAVINGS AND LOAN ASSOCIATION,

6/21/2013. Section I. Purpose of Course. History and Overview of Mortgage Law, Regulation and Requirements

20 Hour Mortgage Loan Originator Certification Course Purpose of Course Gain historical perspective of mortgage lending Understand contemporary mortgage loan origination process Examine federal rules,

20 Hour Mortgage Loan Originator Certification Course Purpose of Course Gain historical perspective of mortgage lending Understand contemporary mortgage loan origination process Examine federal rules,

HMDA Regulations and New 1003 Application - Part 2

HMDA Regulations and New 1003 Application - Part 2 Broker / Correspondent Training May 10 & 12, 2017 1Nations Direct Mortgage Agenda Overview of New Regulations New and Modified HMDA Data Fields Detail

HMDA Regulations and New 1003 Application - Part 2 Broker / Correspondent Training May 10 & 12, 2017 1Nations Direct Mortgage Agenda Overview of New Regulations New and Modified HMDA Data Fields Detail

COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION

PUBLIC DISCLOSURE December 6, 2010 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION Alden State Bank RSSD No. 414102 13216 Broadway Alden, New York 14004 FEDERAL RESERVE BANK OF NEW YORK 33 LIBERTY STREET

PUBLIC DISCLOSURE December 6, 2010 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION Alden State Bank RSSD No. 414102 13216 Broadway Alden, New York 14004 FEDERAL RESERVE BANK OF NEW YORK 33 LIBERTY STREET

Regulatory Change Management

Regulatory Change Management Adapting to Evolving Laws and Regulations Allison Wirth, Director Center of Regulatory Intelligence Kevin Cochran, Assistant Director Center of Regulatory Intelligence May

Regulatory Change Management Adapting to Evolving Laws and Regulations Allison Wirth, Director Center of Regulatory Intelligence Kevin Cochran, Assistant Director Center of Regulatory Intelligence May

The Compliance Management Program and Understanding the Examination Process

The Compliance Management Program and Understanding the Examination Process Bank Operations Institute October 17, 2013 Annette Schindler FDIC Lauri Angle- FDIC Molly McKnight - OCC Diane van Gelder Federal

The Compliance Management Program and Understanding the Examination Process Bank Operations Institute October 17, 2013 Annette Schindler FDIC Lauri Angle- FDIC Molly McKnight - OCC Diane van Gelder Federal

The Untold Costs of Subprime Lending: Communities of Color in California. Carolina Reid. Federal Reserve Bank of San Francisco.

The Untold Costs of Subprime Lending: The Impacts of Foreclosure on Communities of Color in California Carolina Reid Federal Reserve Bank of San Francisco April 10, 2009 The views expressed herein are

The Untold Costs of Subprime Lending: The Impacts of Foreclosure on Communities of Color in California Carolina Reid Federal Reserve Bank of San Francisco April 10, 2009 The views expressed herein are

PUBLIC DISCLOSURE AUGUST 16, 2010 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION AMERICAN HERITAGE BANK RSSD#

PUBLIC DISCLOSURE AUGUST 16, 2010 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION AMERICAN HERITAGE BANK RSSD# 311050 2 SOUTH MAIN SAPULPA, OKLAHOMA 74066 Federal Reserve Bank of Kansas City 1 Memorial

PUBLIC DISCLOSURE AUGUST 16, 2010 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION AMERICAN HERITAGE BANK RSSD# 311050 2 SOUTH MAIN SAPULPA, OKLAHOMA 74066 Federal Reserve Bank of Kansas City 1 Memorial

Credit Research Center Seminar

Credit Research Center Seminar Ensuring Fair Lending: What Do We Know about Pricing in Mortgage Markets and What Will the New HMDA Data Fields Tell US? www.msb.edu/prog/crc March 14, 2005 Introduction

Credit Research Center Seminar Ensuring Fair Lending: What Do We Know about Pricing in Mortgage Markets and What Will the New HMDA Data Fields Tell US? www.msb.edu/prog/crc March 14, 2005 Introduction

The New CFPB HMDA Rules What You Need to Know

The presentation will begin shortly. Your phones have been muted. If you re using the speakers on your PC, you don t need to call in. While you are waiting, you may download the presentation online at:

The presentation will begin shortly. Your phones have been muted. If you re using the speakers on your PC, you don t need to call in. While you are waiting, you may download the presentation online at:

Road Map To CFPB Compliance For The Auto Finance Industry

Road Map To CFPB Compliance For The Auto Finance Industry Michael A. Thurman, Partner Consumer Protection Defense Department LOEB & LOEB Adds Value 2012 LOEB & LOEB LLP The Usual Disclaimers This presentation

Road Map To CFPB Compliance For The Auto Finance Industry Michael A. Thurman, Partner Consumer Protection Defense Department LOEB & LOEB Adds Value 2012 LOEB & LOEB LLP The Usual Disclaimers This presentation

The High Cost of Segregation: Exploring the Relationship Between Racial Segregation and Subprime Lending

F u r m a n C e n t e r f o r r e a l e s t a t e & u r b a n p o l i c y N e w Y o r k U n i v e r s i t y s c h o o l o f l aw wa g n e r s c h o o l o f p u b l i c s e r v i c e n o v e m b e r 2 0

F u r m a n C e n t e r f o r r e a l e s t a t e & u r b a n p o l i c y N e w Y o r k U n i v e r s i t y s c h o o l o f l aw wa g n e r s c h o o l o f p u b l i c s e r v i c e n o v e m b e r 2 0

Pricing Discretion. Managing the Risk of

PRICING Managing the Risk of Pricing Discretion b y DAV I D S K A N D E R S O N, M I K E M c AU L E Y A N D J O E G A R R E T T As advisers to mortgage lenders on operations, risk management and compliance,

PRICING Managing the Risk of Pricing Discretion b y DAV I D S K A N D E R S O N, M I K E M c AU L E Y A N D J O E G A R R E T T As advisers to mortgage lenders on operations, risk management and compliance,