Regulatory Change Management

|

|

|

- Milton Cooper

- 6 years ago

- Views:

Transcription

1 Regulatory Change Management Adapting to Evolving Laws and Regulations Allison Wirth, Director Center of Regulatory Intelligence Kevin Cochran, Assistant Director Center of Regulatory Intelligence May 2017

2 Agenda 1 CHANGING REGULATORY AND ENFORCEMENT CLIMATE 2 BEYOND EFFECTIVE REGULATORY CHANGE MANAGEMENT 3 THE BASICS: ADVANCED REGULATORY CHANGE MANAGEMENT 4 IMPLEMENTATION STRATEGIES AND CONSIDERATIONS HMDA Amendments FinCEN Beneficial Ownership Rule Incentive Compensation 5 KEY TAKEAWAYS 2

3 3

4 The Changing Regulatory and Enforcement Climate 4

5 President Trump Financial Services Positions Dodd-Frank Act Dodd-Frank has made it impossible for bankers to function. It makes it very hard for bankers to loan money for people to create jobs, for people with businesses to create jobs. And that has to stop. Priorities - President Trump (Reuters) We re going to be doing a big number on Dodd-Frank. Immigration Tax Reform Healthcare Financial Reform - President Trump (White House) 5

6 President Trump Financial Services Positions Dodd-Frank Act (continued) Dodd-Frank has made it impossible for bankers to function. It makes it very hard for bankers to loan money for people to create jobs, for people with businesses to create jobs. And that has to stop. We re going to be doing a big number on Dodd-Frank. - President Trump (White House) Priorities - President Trump (Reuters) Immigration Tax Reform Healthcare Financial Reform 6

7 Procedural Vehicles for Regulatory Change Options available to the Trump Administration to address federal rulemaking under the Dodd-Frank Act Amendments Guidance Clarifications Moratoria Compliance Materials Policy Statements Enforcement Actions Reports Extension or postponement of effective dates Rulemaking Executive Orders Speeches Presidential Memoranda Technical Assistance Frequently Asked Questions Testimonies 7

8 Executive Order: Core Principles for Regulating the U.S. Financial System Empower Americans to make independent financial decisions and informed choices in the market place, save for retirement, and build individual wealth Prevent taxpayer-funded bailouts Core Principles Foster economic growth and vibrant financial markets through more rigorous regulatory impact analysis that addresses systemic risk and market failures, such as moral hazard and information asymmetry Enable American companies to be competitive with foreign firms in domestic and foreign markets Advance American interests in financial regulatory negotiations and meetings Make regulation efficient, effective, and appropriately tailored Restore public accountability within Federal financial regulatory agencies and rationalize the Federal regulatory frameworks 8

9 Executive Action Presidential Memorandum Presidential Memorandum on DOL Fiduciary Rule Directs the Department of Labor (DOL) to examine the fiduciary rule to determine whether if adversely affects the ability of Americans to gain access to retirement information and financial advice Prepare economic and legal analysis considering whether the fiduciary rule: will harm or is likely to harm investors due to a cutback to products and services will result in dislocations or disruptions within the retirement services industry will likely cause an increase in litigation in the prices that investors and retirees must pay to gain access to retirement services If an affirmative determination is made for any of the three considerations above, or for any other reason after appropriate review, the DOL should publish for notice and comment a proposed rule rescinding or revising the rule DOL has announced 60-day delay following the memorandum to June 9 9

10 Financial CHOICE Act Overview CHOICE Act Eliminate the CAMELS requirement from the capital election 02 Reduce the CCAR stress-test cycle to every two-years and eliminate the companyrun stress test 03 Restructure the Consumer Financial Protection Bureau (CFPB), UDAAP authority repealed, and change what functions the agency is authorized to perform 04 Raise the Sarbanes- Oxley 404(b) threshold from $250 million to $500 million 10

11 Change management processes are posing a challenge as banks allocate resources to implement processes and controls for multiple new or amended regulations ~ Office of the Comptroller of the Currency, Semiannual Risk Perspective, Fall

Know Before You Owe (KBYO) Fair Lending Fair Servicing")

12 Key Exam Topics Risk Enterprise Risk Third Party (Vendor) Risk Management Incentive Compensation Loans to Insiders/ Regulation O Business Continuity Planning Information Security Cybersecurity/ Information Security GLBA/Privacy of Consumer Financial Information AML/BSA/OFAC Anti-Bribery Compliance Compliance Management System (CMS) Know Before You Owe (KBYO) Fair Lending Fair Servicing Unfair, Deceptive or Abusive Acts or Practices (UDAAP) Complaint Management 12

13 Soaring Legislative Complexity Financial Insights Too Small to Succeed? Community Banks in a New Regulatory Environment From , 10 major banking acts became law, totaling 1,858 pages 13

14 Regulatory Road Map 14

15 Enforcement Trends Source: FIS Center of Regulatory Intelligence 15

16 Effective Regulatory Change Management 16

17 Challenges Information overload Insufficient planning and timetables Regulatory monitoring gaps Lack of follow up and testing Unclear roles and authority Inadequate stakeholder involvement Lack of evidence of tracking and/or analyses of laws and regulation Reactive vs. proactive regulatory change management modes Lack of clear change management policy and processes Disjointed data 17

18 Formula for Success Plan Identify Track & Monitor Analyze Impact Implement Report 18

19 Effective Regulatory Change Management Overview 01 Plan 02 Identify 03 Monitor and Track 04 Analyze 05 Prioritize and 06 Allocate 07 Report 08 Execute Repeat 19

20 Effective Regulatory Change Management Plan Identify Monitor and Track Analyze Prioritize and Allocate Execute Report Repeat PLAN Governance structure Policies and procedures Lines of reporting and points of contact Sign off and escalation Document management Board approval, if needed Involve all stakeholders Internal Third parties Vendors Ample timeline for implementation and testing Develop lines of communication and reporting 20

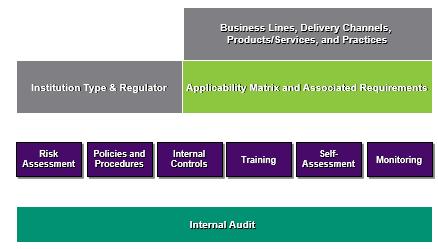

21 Effective Regulatory Change Management Plan Identify Monitor and Track Analyze Prioritize and Allocate Execute Report Repeat IDENTIFY Regulatory Applicability Matrix Policies and procedures Products, services, customers, and business lines Geographic locations Enforcement actions, fines, and penalties High-risk areas, operating environments, and risk tolerances Applicable laws and regulations Governing bodies Regulating authorities Legislators Law enforcement Self regulatory organization(s) 21

22 Effective Regulatory Change Management Plan Identify Monitor and Track Analyze Prioritize and Allocate Execute Report Repeat MONITOR AND TRACK Monitoring Cockpit Official and unofficial sources Analyst monitoring Subject matter expert reviewing and testing Recordkeeping Assign frequency for each source Controls Tracking Control documents Data feed(s) Manual tracking 22

23 Effective Regulatory Change Management Plan Identify Monitor and Track Analyze Prioritize and Allocate Execute Report Repeat ANALYZE Analyses Subject matter experts General Counsel Outside Counsel Consultants Associations Government(s) and Regulator(s) Impact statements Vendor, SME, Counsel Regulator summary or rule-to-rule Timelines Deliverables Deadlines 23

24 Effective Regulatory Change Management Plan Identify Monitor and Track Analyze Prioritize and Allocate Execute Report Repeat PRIORITIZE AND ALLOCATE Priority level Effective dates Implementation timelines Extent of impact Risks Resource allocation Financial Staff Third parties 24

25 Effective Regulatory Change Management Plan Identify Monitor and Track Analyze Prioritize and Allocate Execute EXECUTE Execution Tone at the top Board-to-basement Communication key Follow project plan Adequate accountability and oversight Adapt and document Test, test, and retest Education Training and testing Document Report Repeat 25

26 Effective Regulatory Change Management Plan Identify Monitor and Track Analyze Prioritize and Allocate Execute Report Repeat REPORT Reporting Milestones Setbacks Lessons learned Regular intervals Regulatory reporting library Archive 26

27 Effective Regulatory Change Management Plan Identify Monitor and Track Analyze Prioritize and Allocate Execute Report Repeat REPEAT Best in class Evolutionary and dynamic Reevaluate as needed, but no less than annually Learn from past successes and mistakes 27

28 Beyond the Basics: Advanced Regulatory Change Management 28

29 Advanced Regulatory Change Management 29

30 Advanced Regulatory Change Management U.S. Congress Congressional Sources Committee Members and State/Congressional District Committee Jurisdiction Authorization and Appropriations Political Action Committee (PAC) Legislation Analyses from Introduction-to-Law Committee Action Hearings, Statements, Congressional Record, Votes Floor Debate Statements, Votes, and Congressional Record Legislation Legislation, Reports, and Appropriations Private and Public Sector Sources Trade, Business, and Consumer Associations Statements, Lobbying, and Campaigns News and Industry Publications Banks and Financial Institutions Lobbying Registrations and Reports 30

; National Security Council (NSC) Office of")

31 Advanced Regulatory Change Management U.S. Government Federal Government Sources Public and Private Sector Sources Primary Regulator U.S. Federal Reserve; CFPB; FDIC; OCC Secondary Department and Agencies U.S. Department of Defense; U.S. Department of Agriculture U.S. Congress Members of Congress and Committees Councils National Economic Council (NEC); National Security Council (NSC) Office of Management and Budget (OMB) Trade, Business, and Consumers Associations Lobbying Firms Private Sector and Public Sector Law Firms Consultants Vendors U.S. Courts 31

32 Advanced Regulatory Change Management CFPB s Consumer Complaint Database and Consumer Response Annual Report Source: CFPB Consumer Response Annual Report, December

33 Implementation Strategies and Considerations: - HMDA Amendments - FinCEN Beneficial Ownership Rule - Incentive Compensation 33

34 HMDA Amendments Timeline 34

35 HMDA Amendments Data Fields NOT Changing 35

36 HMDA Amendments Modified Data Fields Legal Entity Identifier (LEI) Universal Loan Identifier (ULI) Loan purpose Preapproval request Construction method Occupancy type Loan amount Ethnicity, race and sex Income Type of purchaser Rate spread Loan status Denial reason Property address Age Credit score Total loan costs or total points and fees Origination charges Discount points Lender credits Interest rates 36

37 HMDA Amendments New Data Fields Prepayment penalty term Debt to Income Ratio (DTI) Combined Loan to Value Ratio (CLTV) Loan terms Introductory rate period Non-amortizing features Property value Manufactured home secured property type Manufactured home land interest property Total units Multifamily affordable units Mortgage Loan Originator NMLSR Identifier 37

38 New Data Fields Total loan costs or total points and fees Property address Age Credit score Origination charges Discount points Lender credits Interest rates Financial Application institutions channel MUST submit the HMDA LAR electronically. Automated underwriting system Reverse mortgages Open-end line of credit All HMDA reportable institutions will use a new internet-based submission tool in Business or commercial purpose 38

39 FinCEN Beneficial Ownership Rule Customer Due Diligence Requirements EFFECTIVE DATE COMPLIANCE DEADLINE COVERED INSTITUTIONS KEY DEFINITIONS July 11, 2016 May 11, 2018 Covered Institutions are required to identify the beneficial owners of new legal entity customers Covered Institution Legal Entity Customer Beneficial Owner 39

40 FinCEN Beneficial Ownership Rule Fifth Pillar to AML Program Requirements Covered institutions required to gain an understanding of the nature and purpose of relationships in order to: Develop a customer risk profile Conduct ongoing monitoring for reporting suspicious transactions, and Maintain and update customer information using a risk-based approach 40

41 FinCEN Beneficial Ownership Rule Requirements to Identify Beneficial Ownership Maintain written procedures as part of AML compliance program to identify a natural person owner for each legal entity customer opening new accounts who meet the following criteria: Reliance Covered institutions may relay on other financial institutions to perform the requirements to identify beneficial ownership provided that the covered institution has no knowledge of facts that would reasonably call into question the reliability of the information. Maintenance Information must be updated on an event-driven basis not an ongoing basis 41

42 FinCEN Beneficial Ownership Rule Key Requirements 42

43 Incentive Compensation Key Requirements Dodd-Frank Act Section 956 FDIC Guidance on Sound Incentive Compensation Policies Federal Reserve Incentive Compensation Practices Study CFPB Compliance Bulletin Dodd-Frank Act Section 953(b) Dodd-Frank Act Section 951 Enforcement 43

44 Key Takeaways 44

45 Touchpoints 45

46 Formula for Success INFORMATION Cover final state and federal laws and news as secondary sources BUSINESS STRATEGY Include Compliance in strategy and product and service development EXPERTISE Ensure appropriate knowledge and proficiency for internal and external staffing and vendors EXISTING RESOURCES Integrate government affairs, general counsel, and communications COMMUNICATIONS Articulate clear expectations and behavioral guidelines for internal and external stakeholders, customers, and governments VISION Compliance adds vision enterprise-wide and improves overall business strategy and revenue ENFORCEMENT ACTIONS Review to identify trends and emerging risks 46

47 Visit us in the expo hall to learn more Questions? Sign up for free, monthly Regulatory Intelligence Briefings:

Regulatory Change Management

Regulatory Change Management Adapting to Evolving Laws and Regulations Peter Dugas, Managing Director Allison Wirth, Director April 11, 2017 Agenda 12345 CHANGING REGULATORY AND ENFORCEMENT CLIMATE EFFECTIVE

Regulatory Change Management Adapting to Evolving Laws and Regulations Peter Dugas, Managing Director Allison Wirth, Director April 11, 2017 Agenda 12345 CHANGING REGULATORY AND ENFORCEMENT CLIMATE EFFECTIVE

Home Mortgage Disclosure Act 2017, 2018, and Beyond. Presented by Marissa Blundell Bankers Advisory A CliftonLarsonAllen LLP Division

Home Mortgage Disclosure Act 2017, 2018, and Beyond Presented by Marissa Blundell Bankers Advisory A CliftonLarsonAllen LLP Division Home Mortgage Disclosure Act (HMDA) Consumer Financial Protection Bureau

Home Mortgage Disclosure Act 2017, 2018, and Beyond Presented by Marissa Blundell Bankers Advisory A CliftonLarsonAllen LLP Division Home Mortgage Disclosure Act (HMDA) Consumer Financial Protection Bureau

HMDA 2018 IMPLEMENTATION PLANNING. HMDA Process Inventory

Affected Products Application Methods (Face to face (online, paper), Mail, Online, Telephone, Fax HMDA Process Inventory Demographic Data Gathering Methods LAR Software Used or Manual LAR Preparation Responsible

Affected Products Application Methods (Face to face (online, paper), Mail, Online, Telephone, Fax HMDA Process Inventory Demographic Data Gathering Methods LAR Software Used or Manual LAR Preparation Responsible

Consumer Financial Protection Bureau. March 15, Draft, Sensitive and Pre-Decisional Not for External Distribution

Consumer Financial Protection Bureau March 15, 2016 Draft, Sensitive and Pre-Decisional Not for External Distribution Outline Home Mortgage Disclosure Act 1) Background 2) Rule Making 3) Changes Coming

Consumer Financial Protection Bureau March 15, 2016 Draft, Sensitive and Pre-Decisional Not for External Distribution Outline Home Mortgage Disclosure Act 1) Background 2) Rule Making 3) Changes Coming

HMDA / Regulation C Amendments New 1003 Application

HMDA / Regulation C Amendments New 1003 Application January 2017 1Nations Direct Mortgage, LLC Mission Statement - To lead the third party residential mortgage industry by providing products and services

HMDA / Regulation C Amendments New 1003 Application January 2017 1Nations Direct Mortgage, LLC Mission Statement - To lead the third party residential mortgage industry by providing products and services

Please stand by, the presentation will begin shortly. Your phones have been muted. If you re using the speakers on your PC you don t need to call in.

Please stand by, the presentation will begin shortly. Your phones have been muted. If you re using the speakers on your PC you don t need to call in. While you are waiting, you may download the presentation

Please stand by, the presentation will begin shortly. Your phones have been muted. If you re using the speakers on your PC you don t need to call in. While you are waiting, you may download the presentation

ICBA Summary of the Home Mortgage Disclosure Act (HMDA) Revisions to Regulation C

Revisions to Regulation C") ICBA Summary of the Home Mortgage Disclosure Act (HMDA) Revisions to Regulation C June 2017 INSERT YEAR HERE Contact Information: Rhonda Thomas-Whitley Assistant Vice President & Regulatory Counsel Rhonda.Thomas-Whitley@icba.org

ICBA Summary of the Home Mortgage Disclosure Act (HMDA) Revisions to Regulation C June 2017 INSERT YEAR HERE Contact Information: Rhonda Thomas-Whitley Assistant Vice President & Regulatory Counsel Rhonda.Thomas-Whitley@icba.org

Summary of Reportable HMDA Data Regulatory Reference Chart a

Summary of Reportable HMDA Data Regulatory Reference Chart a This chart is intended to be used as a reference tool for data points required to be collected, recorded, and reported under Regulation C, as

Summary of Reportable HMDA Data Regulatory Reference Chart a This chart is intended to be used as a reference tool for data points required to be collected, recorded, and reported under Regulation C, as

Revised HMDA Reporting Overview, Implementation and Planning March 2017

Revised HMDA Reporting Overview, Implementation and Planning March 2017 Kathy Keller, Managing Director, Regulatory Compliance, Newbold Advisors, LLC NewboldAdvisors.com Agenda Overview of the New HMDA

Revised HMDA Reporting Overview, Implementation and Planning March 2017 Kathy Keller, Managing Director, Regulatory Compliance, Newbold Advisors, LLC NewboldAdvisors.com Agenda Overview of the New HMDA

S.2155 Implementation The Latest HMDA Changes

S.2155 Implementation The Latest HMDA Changes The webinar will begin at the top of the hour. You may download the presentation at: www.questsoft.com/hmdachanges S.2155 Implementation The Latest HMDA Changes

S.2155 Implementation The Latest HMDA Changes The webinar will begin at the top of the hour. You may download the presentation at: www.questsoft.com/hmdachanges S.2155 Implementation The Latest HMDA Changes

Executive Summary of the 2018 HMDA Interpretive and Procedural Rule

Bureau of Consumer Financial Protection 1700 G Street NW Washington, D.C. 20552 August 31, 2018 Executive Summary of the 2018 HMDA Interpretive and Procedural Rule On August 31, 2018, the Bureau of Consumer

Bureau of Consumer Financial Protection 1700 G Street NW Washington, D.C. 20552 August 31, 2018 Executive Summary of the 2018 HMDA Interpretive and Procedural Rule On August 31, 2018, the Bureau of Consumer

What do HMDA Rule Changes Mean for Covered Institutions?

What do HMDA Rule Changes Mean for Covered Institutions? Tips to prepare for regulatory and institutional change Paula Witt, Director, Consumer Finance & Fair Banking Elizabeth Rozsa, Manager, Consumer

What do HMDA Rule Changes Mean for Covered Institutions? Tips to prepare for regulatory and institutional change Paula Witt, Director, Consumer Finance & Fair Banking Elizabeth Rozsa, Manager, Consumer

Facing Today s Real Estate Regulations

Proudly Sponsored by Facing Today s Real Estate Regulations Presented by Don Braspenninckx Day, June 11, 2016 1:30 p.m. 1 Introduction Numerous regulatory changes in the real estate industry within last

Proudly Sponsored by Facing Today s Real Estate Regulations Presented by Don Braspenninckx Day, June 11, 2016 1:30 p.m. 1 Introduction Numerous regulatory changes in the real estate industry within last

The Added Value of IBS Compliant Solutions

The Added Value of IBS Compliant Solutions Carl Bahneman, IBS Product Line Manager Karla Booe, Deputy Chief Compliance Officer Peter Dugas, Managing Director, Center of Regulatory Intelligence April 11,

The Added Value of IBS Compliant Solutions Carl Bahneman, IBS Product Line Manager Karla Booe, Deputy Chief Compliance Officer Peter Dugas, Managing Director, Center of Regulatory Intelligence April 11,

Home Mortgage Disclosure (Regulation C)

") October 2017 OMB Control No. 3170-0008 Home Mortgage Disclosure (Regulation C) Small Entity Compliance Guide Version Log The Bureau updates this guide on a periodic basis. Below is a version log noting

October 2017 OMB Control No. 3170-0008 Home Mortgage Disclosure (Regulation C) Small Entity Compliance Guide Version Log The Bureau updates this guide on a periodic basis. Below is a version log noting

Loan Growth and Compliance Pitfalls

Loan Growth and Compliance Pitfalls presented by LOANLINER Compliance Information provided in this presentation, including all materials, should not be construed as legal services, legal advice, or in

Loan Growth and Compliance Pitfalls presented by LOANLINER Compliance Information provided in this presentation, including all materials, should not be construed as legal services, legal advice, or in

Compliance Policy 2003-ALL

Overview The following policy describes how CMG Mortgage, Inc., dba CMG Financial, NMLS #1820, ( CMG ) complies with the Home Mortgage Disclosure Act (HMDA) and its implementing regulation, Regulation

Overview The following policy describes how CMG Mortgage, Inc., dba CMG Financial, NMLS #1820, ( CMG ) complies with the Home Mortgage Disclosure Act (HMDA) and its implementing regulation, Regulation

What s New in Mortgage Lending Compliance?

What s New in Mortgage Lending Compliance? Michael R. Christians Senior Federal Compliance Counsel Credit Union National Association Copyright 2016 by Credit Union National Association. All rights reserved.

What s New in Mortgage Lending Compliance? Michael R. Christians Senior Federal Compliance Counsel Credit Union National Association Copyright 2016 by Credit Union National Association. All rights reserved.

Covered loans or applications if the property is

Application Date 1003.4(a)(1)(ii) Property Address State County Census Tract Covered loans or applications if the property address of the property securing the covered loan is not known (e.g., the property

Application Date 1003.4(a)(1)(ii) Property Address State County Census Tract Covered loans or applications if the property address of the property securing the covered loan is not known (e.g., the property

1) The credit union's assets total more than $44 million as of December 31, 2017,

The credit union's assets total more than $44 million as of December 31, 2017,") Exemption: This regulation only applies if the following criteria are met: 1) The credit union's assets total more than $44 million as of December 31, 2017, 2) The credit union has a home or branch office

Exemption: This regulation only applies if the following criteria are met: 1) The credit union's assets total more than $44 million as of December 31, 2017, 2) The credit union has a home or branch office

CONSUMER COMPLIANCE UPDATE. David Wright, Field Supervisor

CONSUMER COMPLIANCE UPDATE David Wright, Field Supervisor AGENDA Introduction Consumer Harm Making compliance examinations more effective and efficient Compliance Emerging Issues Updated FFIEC Compliance

CONSUMER COMPLIANCE UPDATE David Wright, Field Supervisor AGENDA Introduction Consumer Harm Making compliance examinations more effective and efficient Compliance Emerging Issues Updated FFIEC Compliance

HMDA: Haven or Havoc. Michigan Bankers Association. Compliance Services 2016 Temenos USA. All rights reserved.

HMDA: Haven or Havoc Michigan Bankers Association 1 2016 Temenos USA. All rights reserved. About the Speaker Rachelle Dekker CRCM Rachelle Dekker is a Senior Compliance Advisor with the Temenos Compliance

HMDA: Haven or Havoc Michigan Bankers Association 1 2016 Temenos USA. All rights reserved. About the Speaker Rachelle Dekker CRCM Rachelle Dekker is a Senior Compliance Advisor with the Temenos Compliance

HMDA FACT SHEET YOUR MAP TO REGULATORY CHANGE

FACILITATE THOUGHT ENGAGE DIALOGUE ENCOURAGE SMART RISK CULTIVATE A NETWORK BUILD KNOWLEDGE HMDA FACT SHEET YOUR MAP TO REGULATORY CHANGE Regulation C implements the Home Mortgage Disclosure Act (HMDA),

FACILITATE THOUGHT ENGAGE DIALOGUE ENCOURAGE SMART RISK CULTIVATE A NETWORK BUILD KNOWLEDGE HMDA FACT SHEET YOUR MAP TO REGULATORY CHANGE Regulation C implements the Home Mortgage Disclosure Act (HMDA),

HMDA Regulations and New 1003 Application - Part 2

HMDA Regulations and New 1003 Application - Part 2 Broker / Correspondent Training May 10 & 12, 2017 1Nations Direct Mortgage Agenda Overview of New Regulations New and Modified HMDA Data Fields Detail

HMDA Regulations and New 1003 Application - Part 2 Broker / Correspondent Training May 10 & 12, 2017 1Nations Direct Mortgage Agenda Overview of New Regulations New and Modified HMDA Data Fields Detail

Sue Quilty, Quilty & Associates (781)

") Sue Quilty, Quilty & Associates susan.quilty@verizon.net (781)706-9235 Agenda HMDA Today: Review HMDA in the Future: Proposed Changes Surviving HMDA Reporting 2 HMDA Review HMDA Overview Why is HMDA Important

Sue Quilty, Quilty & Associates susan.quilty@verizon.net (781)706-9235 Agenda HMDA Today: Review HMDA in the Future: Proposed Changes Surviving HMDA Reporting 2 HMDA Review HMDA Overview Why is HMDA Important

Implications and Risks of New HMDA Data Disclosure

Implications and Risks of New HMDA Data Disclosure By David Skanderson, Ph.D. January 2018 A version of this paper appeared in ABA Bank Compliance, January/February 2018 The conclusions set forth herein

Implications and Risks of New HMDA Data Disclosure By David Skanderson, Ph.D. January 2018 A version of this paper appeared in ABA Bank Compliance, January/February 2018 The conclusions set forth herein

2018 HMDA Implementation. Presented By: Karen Ruckle, Director of Compliance Bank of the Ozarks

2018 HMDA Implementation Presented By: Karen Ruckle, Director of Compliance Bank of the Ozarks 2018 HMDA Loan Volume Test # Loans #Loans #Loans Home Purchase Or Refi (Dwelling Secured) in prior calendar

2018 HMDA Implementation Presented By: Karen Ruckle, Director of Compliance Bank of the Ozarks 2018 HMDA Loan Volume Test # Loans #Loans #Loans Home Purchase Or Refi (Dwelling Secured) in prior calendar

Partial Exemptions from the Requirements of the Home Mortgage Disclosure Act under

BILLING CODE: 4810-AM-P BUREAU OF CONSUMER FINANCIAL PROTECTION 12 CFR Part 1003 RIN 3170-AA81 Partial Exemptions from the Requirements of the Home Mortgage Disclosure Act under the Economic Growth, Regulatory

BILLING CODE: 4810-AM-P BUREAU OF CONSUMER FINANCIAL PROTECTION 12 CFR Part 1003 RIN 3170-AA81 Partial Exemptions from the Requirements of the Home Mortgage Disclosure Act under the Economic Growth, Regulatory

HMDA Insights : Capitalizing on New Perspectives HMDA Adoption Costs: Did You Say $2 Billion?

Summary: Two adjustments to ensure consistency and comparability with estimated annual HMDA compliance costs increase the CFPB s estimated one-time HMDA adoption costs from $1.34 Billion to $2.12 Billion,

Summary: Two adjustments to ensure consistency and comparability with estimated annual HMDA compliance costs increase the CFPB s estimated one-time HMDA adoption costs from $1.34 Billion to $2.12 Billion,

2016 Interagency Fair Lending Hot Topics

2016 Interagency Fair Lending Hot Topics Outlook Live Webinar October 4, 2016 Visit us at www.consumercomplianceoutlook.org Welcome to Outlook Live Logistics Call-in number: 1-888-625-5230 Conference code:

2016 Interagency Fair Lending Hot Topics Outlook Live Webinar October 4, 2016 Visit us at www.consumercomplianceoutlook.org Welcome to Outlook Live Logistics Call-in number: 1-888-625-5230 Conference code:

HMDA Update Nov. 13, Nov. 13, 2018 HMDA Update 1. Our Agenda Today

HMDA Update Panel Discussion: Ongoing Challenges & Solutions Nov. 13, 2018 HMDA Update 1 Our Agenda Today HMDA Partial Exemption Common Data Collection Exceptions Panel Discussion The future of HMDA Nov.

HMDA Update Panel Discussion: Ongoing Challenges & Solutions Nov. 13, 2018 HMDA Update 1 Our Agenda Today HMDA Partial Exemption Common Data Collection Exceptions Panel Discussion The future of HMDA Nov.

Major Changes Looming for HMDA Reporting

Major Changes Looming for HMDA Reporting CLIENT ALERT September 25, 2017 Scott D. Samlin samlins@pepperlaw.com Mark T. Dabertin dabertinm@pepperlaw.com In this article, we review the requirements of the

Major Changes Looming for HMDA Reporting CLIENT ALERT September 25, 2017 Scott D. Samlin samlins@pepperlaw.com Mark T. Dabertin dabertinm@pepperlaw.com In this article, we review the requirements of the

Managing Fair and Responsible Lending Challenges and Risks

Managing Fair and Responsible Lending Challenges and Risks NYBA Technology, Compliance and Risk Management Forum White Plains, NY May 13, 2015 Legal Counsel to the Financial Services Industry Presented

Managing Fair and Responsible Lending Challenges and Risks NYBA Technology, Compliance and Risk Management Forum White Plains, NY May 13, 2015 Legal Counsel to the Financial Services Industry Presented

2018 Interagency Fair Lending Hot Topics

2018 Interagency Fair Lending Hot Topics Outlook Live Webinar December 3, 2018 Visit us at www.consumercomplianceoutlook.org Visit us at www.consumercomplianceoutlook.org Welcome to Outlook Live Logistics

2018 Interagency Fair Lending Hot Topics Outlook Live Webinar December 3, 2018 Visit us at www.consumercomplianceoutlook.org Visit us at www.consumercomplianceoutlook.org Welcome to Outlook Live Logistics

MBBA-NH & MAMP. Compliance Conference. April 19, 2017

MBBA-NH & MAMP Compliance Conference April 19, 2017 Agenda HMDA Overview Readiness Steps HMDA Expansion Fields 2 New HMDA Rule Summary Changes to Home Mortgage Disclosure: Regulation C Types of institutions

MBBA-NH & MAMP Compliance Conference April 19, 2017 Agenda HMDA Overview Readiness Steps HMDA Expansion Fields 2 New HMDA Rule Summary Changes to Home Mortgage Disclosure: Regulation C Types of institutions

FINANCIAL INSTITUTION GOVERNANCE AND REGULATION SERVICES EXPERTS WITH IMPACT

FINANCIAL INSTITUTION GOVERNANCE AND REGULATION SERVICES EXPERTS WITH IMPACT In today s highly competitive and heavily regulated environment, financial institutions are challenged to remain profitable

FINANCIAL INSTITUTION GOVERNANCE AND REGULATION SERVICES EXPERTS WITH IMPACT In today s highly competitive and heavily regulated environment, financial institutions are challenged to remain profitable

S & HMDA: Complying with New Partial Exemptions. Brought to you by: ABA & BCFP

S. 2155 & HMDA: Complying with New Partial Exemptions Brought to you by: ABA & BCFP Welcome Rob Rowe Vice President Center for Regulatory Compliance American Bankers Association Our Agenda for Today Background

S. 2155 & HMDA: Complying with New Partial Exemptions Brought to you by: ABA & BCFP Welcome Rob Rowe Vice President Center for Regulatory Compliance American Bankers Association Our Agenda for Today Background

National Association of Federal Credit Unions Fair Lending Training (Part II)

") National Association of Federal Credit Unions Fair Lending Training (Part II) April 23, 2014 Jeremiah S. Buckley, Partner Lori J. Sommerfield, Counsel Order of Presentation Key Players in Fair Lending

National Association of Federal Credit Unions Fair Lending Training (Part II) April 23, 2014 Jeremiah S. Buckley, Partner Lori J. Sommerfield, Counsel Order of Presentation Key Players in Fair Lending

SAMPLE. 1 Bank Secrecy Act / Anti-Money Laundering. 2 E-Sign Act / Electronic Funds Transfer Act

1 Bank Secrecy Act / Anti-Money Laundering Summary 1 1 Purpose and History of the BSA 1 1 General Requirements of the BSA/AML Compliance Program 1 3 Money Laundering Defined 1 4 BSA / AML Violations 1

1 Bank Secrecy Act / Anti-Money Laundering Summary 1 1 Purpose and History of the BSA 1 1 General Requirements of the BSA/AML Compliance Program 1 3 Money Laundering Defined 1 4 BSA / AML Violations 1

Consumer Compliance Hot Topics

Consumer Compliance Hot Topics Agenda Regulatory Timeline: Issued in 2014 On the Horizon for 2015 Areas of Supervisory Focus: Fair Lending Unfair or Deceptive Acts or Practices (UDAP) Flood Vendor Management

Consumer Compliance Hot Topics Agenda Regulatory Timeline: Issued in 2014 On the Horizon for 2015 Areas of Supervisory Focus: Fair Lending Unfair or Deceptive Acts or Practices (UDAP) Flood Vendor Management

Leveling the Playing Field CFPB Regulations and Guidance Targeted for Review by Treasury Under President Trump s February 3 Executive Order

Leveling the Playing Field CFPB Regulations and Guidance Targeted for Review by Treasury Under President Trump s February 3 Executive Order March 6, 2017 Moderator Richard J. Andreano, Jr. Practice Leader

Leveling the Playing Field CFPB Regulations and Guidance Targeted for Review by Treasury Under President Trump s February 3 Executive Order March 6, 2017 Moderator Richard J. Andreano, Jr. Practice Leader

A Brief Overview of Actions Taken by the Consumer Financial Protection Bureau (CFPB) in Its First Year

in Its First Year") A Brief Overview of Actions Taken by the Consumer Financial Protection Bureau (CFPB) in Its First Year Sean M. Hoskins Analyst in Financial Economics August 29, 2012 CRS Report for Congress Prepared for

A Brief Overview of Actions Taken by the Consumer Financial Protection Bureau (CFPB) in Its First Year Sean M. Hoskins Analyst in Financial Economics August 29, 2012 CRS Report for Congress Prepared for

EMERGING CONSUMER RISKS FOR COMMUNITY BANKS

November 14, 2016 1 EMERGING CONSUMER RISKS FOR COMMUNITY BANKS 2016 ANNUAL RISK MANAGEMENT CONFERENCE NOVEMBER 14, 2016 November 14, 2016 2 Paul J. Stark, SVP & Chief Credit Officer Civista Bank, Sandusky

November 14, 2016 1 EMERGING CONSUMER RISKS FOR COMMUNITY BANKS 2016 ANNUAL RISK MANAGEMENT CONFERENCE NOVEMBER 14, 2016 November 14, 2016 2 Paul J. Stark, SVP & Chief Credit Officer Civista Bank, Sandusky

Regulatory and Enforcement Trends

NY2 717563 Regulatory and Enforcement Trends April 11, 2013 2013 Morrison & Foerster LLP All Rights Reserved mofo.com Agenda We will provide an overview of the regulatory and enforcement trends that may

NY2 717563 Regulatory and Enforcement Trends April 11, 2013 2013 Morrison & Foerster LLP All Rights Reserved mofo.com Agenda We will provide an overview of the regulatory and enforcement trends that may

2017 Interagency Fair Lending Hot Topics

2017 Interagency Fair Lending Hot Topics Outlook Live Webinar November 16, 2017 Visit us at www.consumercomplianceoutlook.org Visit us at www.consumercomplianceoutlook.org 1 Welcome to Outlook Live Logistics

2017 Interagency Fair Lending Hot Topics Outlook Live Webinar November 16, 2017 Visit us at www.consumercomplianceoutlook.org Visit us at www.consumercomplianceoutlook.org 1 Welcome to Outlook Live Logistics

Consumer Financial Protection Bureau Update

Consumer Financial Protection Bureau Update Patricia Scherschel February 2016 Student Lending Program Manager Installment Lending and Collections Markets Division of Research, Markets, and Regulations

Consumer Financial Protection Bureau Update Patricia Scherschel February 2016 Student Lending Program Manager Installment Lending and Collections Markets Division of Research, Markets, and Regulations

Fair Lending Risks and HMDA

Fair Lending Risks and HMDA Kathleen O. Blanchard Key Compliance Services, LLC October 8, 2018 1 Topics HMDA History Partial Exemptions Privacy of HMDA Data Fair Lending Concerns 2 HMDA History 3 HMDA

Fair Lending Risks and HMDA Kathleen O. Blanchard Key Compliance Services, LLC October 8, 2018 1 Topics HMDA History Partial Exemptions Privacy of HMDA Data Fair Lending Concerns 2 HMDA History 3 HMDA

SUMMARY: The Bureau of Consumer Financial Protection (CFPB or Bureau) is publishing this agenda

is publishing this agenda") This document is scheduled to be published in the Federal Register on 06/09/2016 and available online at http://federalregister.gov/a/2016-12931, and on FDsys.gov BUREAU OF CONSUMER FINANCIAL PROTECTION

This document is scheduled to be published in the Federal Register on 06/09/2016 and available online at http://federalregister.gov/a/2016-12931, and on FDsys.gov BUREAU OF CONSUMER FINANCIAL PROTECTION

U.S. Treasury Report Proposes Changes to the Financial Regulatory System

June 22, 2017 U.S. Treasury Report Proposes Changes to the Financial Regulatory System The U.S. Department of the Treasury has issued its first in a series of reports required by Executive Order 13772

June 22, 2017 U.S. Treasury Report Proposes Changes to the Financial Regulatory System The U.S. Department of the Treasury has issued its first in a series of reports required by Executive Order 13772

Regulatory Practice Letter December 2014 RPL 14-22

Regulatory Practice Letter December 2014 RPL 14-22 Automobile Supervision and Enforcement Regulatory Actions and CFPB Proposed Rule Executive Summary The automobile finance industry is under heightened

Regulatory Practice Letter December 2014 RPL 14-22 Automobile Supervision and Enforcement Regulatory Actions and CFPB Proposed Rule Executive Summary The automobile finance industry is under heightened

CFPB Home Mortgage Disclosure Act (HMDA) Final Rule. Webinar August 4, 2016

Final Rule. Webinar August 4, 2016") CFPB Home Mortgage Disclosure Act (HMDA) Final Rule Webinar August 4, 2016 Topics Regulation C, the Bureau s HMDA rule 1. Overview of the final rule 2. Institutional coverage 3. Transactional coverage

CFPB Home Mortgage Disclosure Act (HMDA) Final Rule Webinar August 4, 2016 Topics Regulation C, the Bureau s HMDA rule 1. Overview of the final rule 2. Institutional coverage 3. Transactional coverage

Regulatory Influences to the Motor Vehicle Service Contract and Ancillary Product Industry

Regulatory Influences to the Motor Vehicle Service Contract and Ancillary Product Industry Aaron E. Lunt, JD, CPCU, ARe Assistant General Counsel, Head of Regulatory Affairs The Warranty Group August 29,

Regulatory Influences to the Motor Vehicle Service Contract and Ancillary Product Industry Aaron E. Lunt, JD, CPCU, ARe Assistant General Counsel, Head of Regulatory Affairs The Warranty Group August 29,

CFPB Compliance Bulletin Date: July 31, 2017

1700 G Street NW, Washington, DC 20552 CFPB Compliance Bulletin 2017-01 Date: July 31, 2017 Subject: Phone Pay Fees The Consumer Financial Protection Bureau (CFPB or Bureau) issues this Compliance Bulletin

1700 G Street NW, Washington, DC 20552 CFPB Compliance Bulletin 2017-01 Date: July 31, 2017 Subject: Phone Pay Fees The Consumer Financial Protection Bureau (CFPB or Bureau) issues this Compliance Bulletin

Presentation Topics. Changing Data Requirements Will Effect. Census data update and implications for CRA, HMDA and Fair Lending

Changing Data Requirements Will Effect the CRA and Fair Lending Environment Prepared for the 2012 National Community Reinvestment Conference by Glenn Canner March 28, 2012 The views expressed are those

Changing Data Requirements Will Effect the CRA and Fair Lending Environment Prepared for the 2012 National Community Reinvestment Conference by Glenn Canner March 28, 2012 The views expressed are those

Important Compliance Dates December 2017

Ongoing NIST Framework for Improving Critical Infrastructure Cybersecurity June 9, 2017 DoL 29 CFR Part 541 The National Institute of Standards and Technology released a voluntary framework for use to

Ongoing NIST Framework for Improving Critical Infrastructure Cybersecurity June 9, 2017 DoL 29 CFR Part 541 The National Institute of Standards and Technology released a voluntary framework for use to

Regulatory Compliance Update. Hoi Luk, Senior Manager, Financial Services Consulting

Regulatory Compliance Update Hoi Luk, Senior Manager, Financial Services Consulting What are WE Seeing and Hearing? Supervisory Committee Workshop 3 Supervisory Letter SL 17-01 March 29, 2017 Evaluating

Regulatory Compliance Update Hoi Luk, Senior Manager, Financial Services Consulting What are WE Seeing and Hearing? Supervisory Committee Workshop 3 Supervisory Letter SL 17-01 March 29, 2017 Evaluating

Filing instructions guide for HMDA data collected in 2018

September 2018 Filing instructions guide for HMDA data collected in 2018 OMB Control #3170-0008 Version log The following is a version log that tracks the history of this document and its updates: Date

September 2018 Filing instructions guide for HMDA data collected in 2018 OMB Control #3170-0008 Version log The following is a version log that tracks the history of this document and its updates: Date

U.S. Consumer Financial Services Regulation: What to Expect in 2016

U.S. Consumer Financial Services Regulation: What to Expect in 2016 Digital Payments Intensive April 13, 2016 Andrew J. Lorentz No. 1 RULEMAKING BY ENFORCEMENT 2 Rulemaking by enforcement New Consumer

U.S. Consumer Financial Services Regulation: What to Expect in 2016 Digital Payments Intensive April 13, 2016 Andrew J. Lorentz No. 1 RULEMAKING BY ENFORCEMENT 2 Rulemaking by enforcement New Consumer

Comment Call (14-15) CFPB Home Mortgage Disclosure Act (HMDA)

CFPB Home Mortgage Disclosure Act (HMDA)") Comment Call (14-15) CFPB Home Mortgage Disclosure Act (HMDA) Impact: Federal and State Chartered Credit Unions Relevant Department: CEO / Lending Priority Level: High Background / Credit Union Summary

Comment Call (14-15) CFPB Home Mortgage Disclosure Act (HMDA) Impact: Federal and State Chartered Credit Unions Relevant Department: CEO / Lending Priority Level: High Background / Credit Union Summary

Managing the Managers: International Coordination of Financial Supervision

Managing the Managers: International Coordination of Financial Supervision Barbara Novick, Vice Chairman May 2017 The opinions expressed are as of May 2017 and may change as subsequent conditions vary.

Managing the Managers: International Coordination of Financial Supervision Barbara Novick, Vice Chairman May 2017 The opinions expressed are as of May 2017 and may change as subsequent conditions vary.

New Products and Business Initiatives. 27th National Risk Management Training Conference

New Products and Business Initiatives 27th National Risk Management Training Conference Gregory J. Lyons May 1, 2013 Agenda Succeeding in a difficult regulatory environment Why offer, when, and who should

New Products and Business Initiatives 27th National Risk Management Training Conference Gregory J. Lyons May 1, 2013 Agenda Succeeding in a difficult regulatory environment Why offer, when, and who should

Home Mortgage Disclosure Act HMDA Part 1. Presented by: Aaron Kouhoupt, Esq.

Home Mortgage Disclosure Act HMDA Part 1 Presented by: Aaron Kouhoupt, Esq. Timeline January 1, 2018 Coverage and collection of expanded data required under new rule (Be careful!) March 1, 2019 Report

Home Mortgage Disclosure Act HMDA Part 1 Presented by: Aaron Kouhoupt, Esq. Timeline January 1, 2018 Coverage and collection of expanded data required under new rule (Be careful!) March 1, 2019 Report

Regulatory Compliance Update

Regulatory Compliance Update ACUIA Region 6 Conference Presented By: Kristie Kenney Hoover, NCCO Internal Audit Manager, Doeren Mayhew Florida Michigan North Carolina Texas Insight. Oversight. Foresight.

Regulatory Compliance Update ACUIA Region 6 Conference Presented By: Kristie Kenney Hoover, NCCO Internal Audit Manager, Doeren Mayhew Florida Michigan North Carolina Texas Insight. Oversight. Foresight.

FREQUENTLY ASKED QUESTIONS ABOUT THE NEW HMDA DATA. General Background

Federal Reserve Bank of New York Statistics Function March 31, 2005 FREQUENTLY ASKED QUESTIONS ABOUT THE NEW HMDA DATA General Background 1. What is the Home Mortgage Disclosure Act (HMDA)? HMDA, enacted

Federal Reserve Bank of New York Statistics Function March 31, 2005 FREQUENTLY ASKED QUESTIONS ABOUT THE NEW HMDA DATA General Background 1. What is the Home Mortgage Disclosure Act (HMDA)? HMDA, enacted

by: Stephen King, JD, AMLP

Community Bank Audit Group Compliance Management Structure / Compliance Risk Assessment June 2, 2014 by: Stephen King, JD, AMLP MEMBER OF PKF NORTH AMERICA, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS

Community Bank Audit Group Compliance Management Structure / Compliance Risk Assessment June 2, 2014 by: Stephen King, JD, AMLP MEMBER OF PKF NORTH AMERICA, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS

Regulatory Update NAFCU Webcast

Regulatory Update NAFCU Webcast Thursday, November 14 2:00 3:30 p.m. Presented by: Steve Van Beek, Esq. (248)723-0521 svb@h2law.com Overview CFPB s Agenda Supervisory Highlights CFPB s Radar AKA, What

Regulatory Update NAFCU Webcast Thursday, November 14 2:00 3:30 p.m. Presented by: Steve Van Beek, Esq. (248)723-0521 svb@h2law.com Overview CFPB s Agenda Supervisory Highlights CFPB s Radar AKA, What

CFPB Consumer Laws and Regulations

Consumer Laws and Regulations Home Mortgage Disclosure Act 1 The Home Mortgage Disclosure Act () was enacted by the Congress in 1975 and is implemented by Regulation C (12 CFR Part 1003). 2 The period

Consumer Laws and Regulations Home Mortgage Disclosure Act 1 The Home Mortgage Disclosure Act () was enacted by the Congress in 1975 and is implemented by Regulation C (12 CFR Part 1003). 2 The period

The New CFPB HMDA Rules

The New CFPB HMDA Rules What You Need to Know Thank you for attending. The webinar has started. Today s Panelists Kathleen Ryan Counsel BuckleySandler LLP Leonard Ryan President QuestSoft Corporation Moderator

The New CFPB HMDA Rules What You Need to Know Thank you for attending. The webinar has started. Today s Panelists Kathleen Ryan Counsel BuckleySandler LLP Leonard Ryan President QuestSoft Corporation Moderator

UDAAP. Understanding What It Is and Where It Applies. Presented by: Thomas Fox, Partner Schwartz & Ballen LLP

June 21, 2016 UDAAP Understanding What It Is and Where It Applies Presented by: Thomas Fox, Partner Schwartz & Ballen LLP Copyright 2016 by the Electronic Check Clearing House Organization Disclaimer This

June 21, 2016 UDAAP Understanding What It Is and Where It Applies Presented by: Thomas Fox, Partner Schwartz & Ballen LLP Copyright 2016 by the Electronic Check Clearing House Organization Disclaimer This

Final Rules and Effective Dates

Final Rules and Effective Dates Agency Final Rule Federal Register Publication Date and Page Number Effective Date Bureau of Consumer Financial Protection (CFPB) CORRECTION: Regulation X and Regulation

Final Rules and Effective Dates Agency Final Rule Federal Register Publication Date and Page Number Effective Date Bureau of Consumer Financial Protection (CFPB) CORRECTION: Regulation X and Regulation

Kevin L. Petrasic. Washington, D.C. Practice Areas. Admissions. Education. Partner, Corporate Department

Kevin L. Petrasic Partner, Corporate Department kevinpetrasic@paulhastings.com Kevin L. Petrasic is a partner in the Global Banking and Payments Systems practice of Paul Hastings and is based in the firm

Kevin L. Petrasic Partner, Corporate Department kevinpetrasic@paulhastings.com Kevin L. Petrasic is a partner in the Global Banking and Payments Systems practice of Paul Hastings and is based in the firm

Client Update CHOICE 2.0 and New Presidential Memoranda

1 Client Update CHOICE 2.0 and New Presidential Memoranda NEW YORK Courtney M. Dankworth cmdankworth@debevoise.com Gregory J. Lyons gjlyons@debevoise.com David L. Portilla dlportilla@debevoise.com Alexandra

1 Client Update CHOICE 2.0 and New Presidential Memoranda NEW YORK Courtney M. Dankworth cmdankworth@debevoise.com Gregory J. Lyons gjlyons@debevoise.com David L. Portilla dlportilla@debevoise.com Alexandra

Consumer Regulatory Changes

Consumer Regulatory Changes Federal Reserve Board Division of Consumer and Community Affairs August 19, 2010 Visit us at www.consumercomplianceoutlook.org The The opinions expressed in in this this presentation

Consumer Regulatory Changes Federal Reserve Board Division of Consumer and Community Affairs August 19, 2010 Visit us at www.consumercomplianceoutlook.org The The opinions expressed in in this this presentation

ANTI-MONEY LAUNDERING IN

ANTI-MONEY LAUNDERING IN THE ACQUIRING INDUSTRY Presented by Laura H. Goldzung, CAMS, CCFE, CFCF, CCRP AML Audit Services, LLC March 8, 2016 AGENDA AML Regulatory Overview OFAC Regulatory Overview AML

ANTI-MONEY LAUNDERING IN THE ACQUIRING INDUSTRY Presented by Laura H. Goldzung, CAMS, CCFE, CFCF, CCRP AML Audit Services, LLC March 8, 2016 AGENDA AML Regulatory Overview OFAC Regulatory Overview AML

Best Practices in Vendor Management Mortgage Servicer and Subservicer Oversight. Scott D. Samlin, Partner

Best Practices in Vendor Management Mortgage Servicer and Subservicer Oversight Scott D. Samlin, Partner November 29, 2017 Presenter Scott Samlin is a partner in the Financial Services Practice Group and

Best Practices in Vendor Management Mortgage Servicer and Subservicer Oversight Scott D. Samlin, Partner November 29, 2017 Presenter Scott Samlin is a partner in the Financial Services Practice Group and

Final Rules & Studies (by DFA Section) April 30, 2012

April 30, 2012") Final Rules & Studies (by DFA Section) April 30, 2012 Publication Date Effective Date Action Type Description Topics DFA Reference 7/26/2011 N/A FSOC Report FSOC 2011 Annual Report. 4/11/2012 5/11/2012

Final Rules & Studies (by DFA Section) April 30, 2012 Publication Date Effective Date Action Type Description Topics DFA Reference 7/26/2011 N/A FSOC Report FSOC 2011 Annual Report. 4/11/2012 5/11/2012

Department of the Treasury Issues Report Recommending U.S. Capital Markets Regulatory Reforms

WHITE PAPER November 2017 Department of the Treasury Issues Report Recommending U.S. Capital Markets Regulatory Reforms The U.S. Department of the Treasury has issued a report to the President recommending

WHITE PAPER November 2017 Department of the Treasury Issues Report Recommending U.S. Capital Markets Regulatory Reforms The U.S. Department of the Treasury has issued a report to the President recommending

CFPB & UDAAP. Recent Developments & Hot Topics. Michael Stockham. Nicole Williams. June 23,

CFPB & UDAAP Recent Developments & Hot Topics Michael Stockham Michael.Stockham@tklaw.com 214.969.2515 Nicole Williams Nicole.Williams@tklaw.com 214.969.1149 June 23, 2015 Agenda Background Trends Hot

CFPB & UDAAP Recent Developments & Hot Topics Michael Stockham Michael.Stockham@tklaw.com 214.969.2515 Nicole Williams Nicole.Williams@tklaw.com 214.969.1149 June 23, 2015 Agenda Background Trends Hot

Dodd-Frank Reconsidered: The Financial CHOICE Act 2.0

Memorandum Dodd-Frank Reconsidered: The Financial CHOICE Act 2.0 April 26, 2017 On April 26, 2017, the House Financial Services Committee held hearings on the Financial CHOICE Act, a proposal that aims

Memorandum Dodd-Frank Reconsidered: The Financial CHOICE Act 2.0 April 26, 2017 On April 26, 2017, the House Financial Services Committee held hearings on the Financial CHOICE Act, a proposal that aims

Chapter 2: Government Policies and Regulation Test Bank Solutions Principles of Bank Management 8th Edition by Koch Multiple Choice

Chapter 2: Government Policies and Regulation Test Bank Solutions Principles of Bank Management 8th Edition by Koch Multiple Choice 1. Historically, a commercial bank was defined as a firm that: a. accepted

Chapter 2: Government Policies and Regulation Test Bank Solutions Principles of Bank Management 8th Edition by Koch Multiple Choice 1. Historically, a commercial bank was defined as a firm that: a. accepted

Overdraft Protection:

Overdraft Protection: Does Your System Match Disclosures? Karla Alexander-White, CRCM, Compliance Manager-Corporate Compliance Jason Spelliscy, CRCM, Regional Director, RISC Solutions Thursday, April 13,

Overdraft Protection: Does Your System Match Disclosures? Karla Alexander-White, CRCM, Compliance Manager-Corporate Compliance Jason Spelliscy, CRCM, Regional Director, RISC Solutions Thursday, April 13,

Filing instructions guide for HMDA data collected in 2018

August 2017 Filing instructions guide for HMDA data collected in 2018 OMB Control #3170-0008 Version log The following is a version log that tracks the history of this document and its updates: Date Version

August 2017 Filing instructions guide for HMDA data collected in 2018 OMB Control #3170-0008 Version log The following is a version log that tracks the history of this document and its updates: Date Version

The Commercial Real Estate Lending Decision Process Series (RMA)

") Business Banking & Commercial Lending Analyzing Business Financial Statements and Tax Returns Analyzing Financial Statements Analyzing Personal Financial Statements and Tax Returns Certificate in Business

Business Banking & Commercial Lending Analyzing Business Financial Statements and Tax Returns Analyzing Financial Statements Analyzing Personal Financial Statements and Tax Returns Certificate in Business

Non-Mortgage Products

Non-Mortgage Products Hot Issues in Non-Mortgage Lending Melanie Brody Partner Mayer Brown mbrody@mayerbrown.com Brian Clark Senior Manager Ernst & Young Brian.Clark@ey.com Speakers Melanie Brody Partner

Non-Mortgage Products Hot Issues in Non-Mortgage Lending Melanie Brody Partner Mayer Brown mbrody@mayerbrown.com Brian Clark Senior Manager Ernst & Young Brian.Clark@ey.com Speakers Melanie Brody Partner

Kevin Patterson Partner

100 Quentin Roosevelt Boulevard Garden City, NY 11530-4850 ph: 516.296.9196 fx: 516.357.3792 kpatterson@cullenanddykman.com AREAS OF PRACTICE Banking Compliance Bank Operations Bank Regulatory and Compliance

100 Quentin Roosevelt Boulevard Garden City, NY 11530-4850 ph: 516.296.9196 fx: 516.357.3792 kpatterson@cullenanddykman.com AREAS OF PRACTICE Banking Compliance Bank Operations Bank Regulatory and Compliance

Hosted By Mike Gallagher October 2017

Risk Management, Compliance and CRA Hosted By Mike Gallagher October 2017 Today s Agenda Risk Management Risk governance Enterprise Risk Management Operational Risk Management Categories of Risk Compliance

Risk Management, Compliance and CRA Hosted By Mike Gallagher October 2017 Today s Agenda Risk Management Risk governance Enterprise Risk Management Operational Risk Management Categories of Risk Compliance

Mortgage Regulation Update

Presented by: Mortgage Regulation Update Wisconsin Credit Union League Convention 1 Objectives At the end of this session, you will: Recognize recent updates to existing mortgage rules TILA/RESPA Integrated

Presented by: Mortgage Regulation Update Wisconsin Credit Union League Convention 1 Objectives At the end of this session, you will: Recognize recent updates to existing mortgage rules TILA/RESPA Integrated

Special Alert: CFPB Issues Rule Regarding Payday, Title, Deposit Advance, and Certain Other Installment Loans

Special Alert: CFPB Issues Rule Regarding Payday, Title, Deposit Advance, and Certain Other Installment Loans On October 5, 2017, the CFPB published its final rule (the Rule ) addressing payday loans,

Special Alert: CFPB Issues Rule Regarding Payday, Title, Deposit Advance, and Certain Other Installment Loans On October 5, 2017, the CFPB published its final rule (the Rule ) addressing payday loans,

SUMMARY: The Bureau is reissuing its guidance on service providers, formerly titled CFPB

Billing Code: 4810-AM-P BUREAU OF CONSUMER FINANCIAL PROTECTION Compliance Bulletin and Policy Guidance; 2016-02, Service Providers AGENCY: Bureau of Consumer Financial Protection. ACTION: Compliance Bulletin

Billing Code: 4810-AM-P BUREAU OF CONSUMER FINANCIAL PROTECTION Compliance Bulletin and Policy Guidance; 2016-02, Service Providers AGENCY: Bureau of Consumer Financial Protection. ACTION: Compliance Bulletin

Expert Analysis Understanding the Evolving Legal And Regulatory Landscape for Consumer Marketplace Lending

Westlaw Journal bank & Lender Liability Litigation News and Analysis Legislation Regulation Expert Commentary VOLUME 21, issue 19 / february 8, 2016 Expert Analysis Understanding the Evolving Legal And

Westlaw Journal bank & Lender Liability Litigation News and Analysis Legislation Regulation Expert Commentary VOLUME 21, issue 19 / february 8, 2016 Expert Analysis Understanding the Evolving Legal And

S (a) Impact Data. Unchanged Value 01 Record Identifier x 01 Legal Entity Identifier (LEI) 02 Legal Entity Identifier (LEI) x

Impact Data. Unchanged Value 01 Record Identifier x 01 Legal Entity Identifier (LEI) 02 Legal Entity Identifier (LEI) x") Eempt 01 Record Identifier 01 Legal Entity Identifier (LEI) 02 Legal Entity Identifier (LEI) 02 Universal Loan Identifier (ULI) / Non Universal Loan Identifier (NULI) 03 Universal Loan Identifier (ULI)

Eempt 01 Record Identifier 01 Legal Entity Identifier (LEI) 02 Legal Entity Identifier (LEI) 02 Universal Loan Identifier (ULI) / Non Universal Loan Identifier (NULI) 03 Universal Loan Identifier (ULI)

UDAAP: The CFPB s Emerging and Evolving Doctrine

UDAAP: The CFPB s Emerging and Evolving Doctrine October 5, 2016 Moderator: Allyson Baker, Esq., Partner, Venable LLP Panelists: Jennifer McCabe, Vice President, Cornerstone Research Meredith Boylan, Esq.,

UDAAP: The CFPB s Emerging and Evolving Doctrine October 5, 2016 Moderator: Allyson Baker, Esq., Partner, Venable LLP Panelists: Jennifer McCabe, Vice President, Cornerstone Research Meredith Boylan, Esq.,

Please Support Community Bank Priorities

Please Support Community Bank Priorities October 2018 On behalf of the 320 community banks represented by the Community Bankers Association of Illinois (CBAI) we urge your support for our positions on

Please Support Community Bank Priorities October 2018 On behalf of the 320 community banks represented by the Community Bankers Association of Illinois (CBAI) we urge your support for our positions on

UDAP Analysis, Examinations, Case Studies, and Emerging Risks

UDAP Analysis, Examinations, Case Studies, and Emerging Risks Outlook Live Webinar March 5, 2013 Maureen Yap, Special Counsel Art Zaino, Senior Compliance Manager Tracy Anderson, Manager Visit us at www.consumercomplianceoutlook.org

UDAP Analysis, Examinations, Case Studies, and Emerging Risks Outlook Live Webinar March 5, 2013 Maureen Yap, Special Counsel Art Zaino, Senior Compliance Manager Tracy Anderson, Manager Visit us at www.consumercomplianceoutlook.org

The New CFPB HMDA Rules What You Need to Know

The presentation will begin shortly. Your phones have been muted. If you re using the speakers on your PC, you don t need to call in. While you are waiting, you may download the presentation online at:

The presentation will begin shortly. Your phones have been muted. If you re using the speakers on your PC, you don t need to call in. While you are waiting, you may download the presentation online at:

Table of Contents CLICK ANY TITLE TO GO DIRECTLY TO THAT SECTION. SUBTITLE A: Bureau of Consumer Financial Protection

Venable CFPB monitor Please contact our attorneys in our CFPB Task Force if you have any questions regarding this information. Table of Contents CLICK ANY TITLE TO GO DIRECTLY TO THAT SECTION Last updated

Venable CFPB monitor Please contact our attorneys in our CFPB Task Force if you have any questions regarding this information. Table of Contents CLICK ANY TITLE TO GO DIRECTLY TO THAT SECTION Last updated

Navigating the New Federal and State Debt Collection Enforcement Landscape Presented by Venable LLP Speakers:

Navigating the New Federal and State Debt Collection Enforcement Landscape Presented by Venable LLP Speakers: Jonathan L. Pompan, Esq. Kevin L. Turner, Esq. Alexandra Megaris, Esq. Andrew E. Bigart, Esq.

Navigating the New Federal and State Debt Collection Enforcement Landscape Presented by Venable LLP Speakers: Jonathan L. Pompan, Esq. Kevin L. Turner, Esq. Alexandra Megaris, Esq. Andrew E. Bigart, Esq.

October 10, Paul Watkins, Director, Office of Innovation Bureau of Consumer Financial Protection 1700 G Street NW Washington, DC 20552

Paul Watkins, Director, Office of Innovation Bureau of Consumer Financial Protection 1700 G Street NW Washington, DC 20552 RE: Policy to Encourage Trial Disclosure Programs (Docket No. CFPB-2018-0023)

Paul Watkins, Director, Office of Innovation Bureau of Consumer Financial Protection 1700 G Street NW Washington, DC 20552 RE: Policy to Encourage Trial Disclosure Programs (Docket No. CFPB-2018-0023)

CFPB Complaints, Compliance, and Enforcement: Trends and Tips

CFPB Complaints, Compliance, and Enforcement: Trends and Tips Wednesday, February 17, 2016 David Morgan Jonathan L. Pompan PerformLine Venable LLP Chief Revenue Officer Partner and Co-Chair of CFPB Task

CFPB Complaints, Compliance, and Enforcement: Trends and Tips Wednesday, February 17, 2016 David Morgan Jonathan L. Pompan PerformLine Venable LLP Chief Revenue Officer Partner and Co-Chair of CFPB Task

7 Steps to Reduce UDAAP Risks. Steve Van Beek, Esq., NCCO Howard & Howard Attorneys PLLC

7 Steps to Reduce UDAAP Risks Steve Van Beek, Esq., NCCO Howard & Howard Attorneys PLLC svb@h2law.com 248.723.0521 Overview What is UDAAP? UDAP versus UDAAP 7 Steps to Reduce UDAAP Risk Conducting UDAAP

7 Steps to Reduce UDAAP Risks Steve Van Beek, Esq., NCCO Howard & Howard Attorneys PLLC svb@h2law.com 248.723.0521 Overview What is UDAAP? UDAP versus UDAAP 7 Steps to Reduce UDAAP Risk Conducting UDAAP