CFPB Home Mortgage Disclosure Act (HMDA) Final Rule. Webinar August 4, 2016

|

|

|

- Cleopatra Matthews

- 6 years ago

- Views:

Transcription

Final Rule Webinar August 4,")

1 CFPB Home Mortgage Disclosure Act (HMDA) Final Rule Webinar August 4, 2016

2 Topics Regulation C, the Bureau s HMDA rule 1. Overview of the final rule 2. Institutional coverage 3. Transactional coverage 4. Data disclosure and submission process 5. Key dates 2

3 General Disclaimer This presentation is current as of August 4 th This presentation does not represent legal interpretation, guidance, or advice of the Bureau. While efforts have been made to ensure accuracy, only the rule and its Official Interpretations can provide complete and definitive information regarding requirements. 3

4 v Overview of the final rule Background

5 Background Information

6 Background Information

7 HMDA s Purposes

8 HMDA s Purposes

9 HMDA s Purposes

10 Who Uses the Data? Public officials

11 Who Uses the Data? Public officials Communities

12 Who Uses the Data? Public officials Communities Mortgage industry

13 Expansion of HMDA and Regulation C Changing needs of homeowners Evolution of Mortgage market

14 Expansion of HMDA and Regulation C 2010 July 24, 2014 October 15, 2015 Dodd Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act) Amended HMDA Transferred rulemaking authority from Federal Reserve Board to the Bureau Added new reporting requirements

15 Amending Regulation C 2010 July 24, 2014 October 15, 2015 Proposed amendments to Regulation C to implement Dodd-Frank changes Received, reviewed and considered approximately 400 comments

16 Amending Regulation C 2010 July 24, 2014 October 15, 2015 Issued final rule that changes: Institutions subject to Regulation C Transactions subject to Regulation C Data collection and reporting requirements Process for reporting and disclosing data

17 Amending Regulation C What institutions and transactions are subject to Regulation C under the final rule? Submissions Disclosures Key Dates

18 v Institutional coverage Home Mortgage Disclosure Act (HMDA) Regulation C - Final Rule 18

19 What is a financial institution? HMDA

20 What is a financial institution? Phase 1 Definition Regulation C Phase 2

21 Regulation C Phase

22 Regulation C Phase 1 tests Phase 1

23 Regulation C Phase 1 tests Bank Savings association Credit Union

24 Regulation C Phase 1 tests Asset-Size Location Loan Activity Federally Related Loan Volume

25 Regulation C The change for Home Purchases

26 Regulation C The change for Home Purchases

27

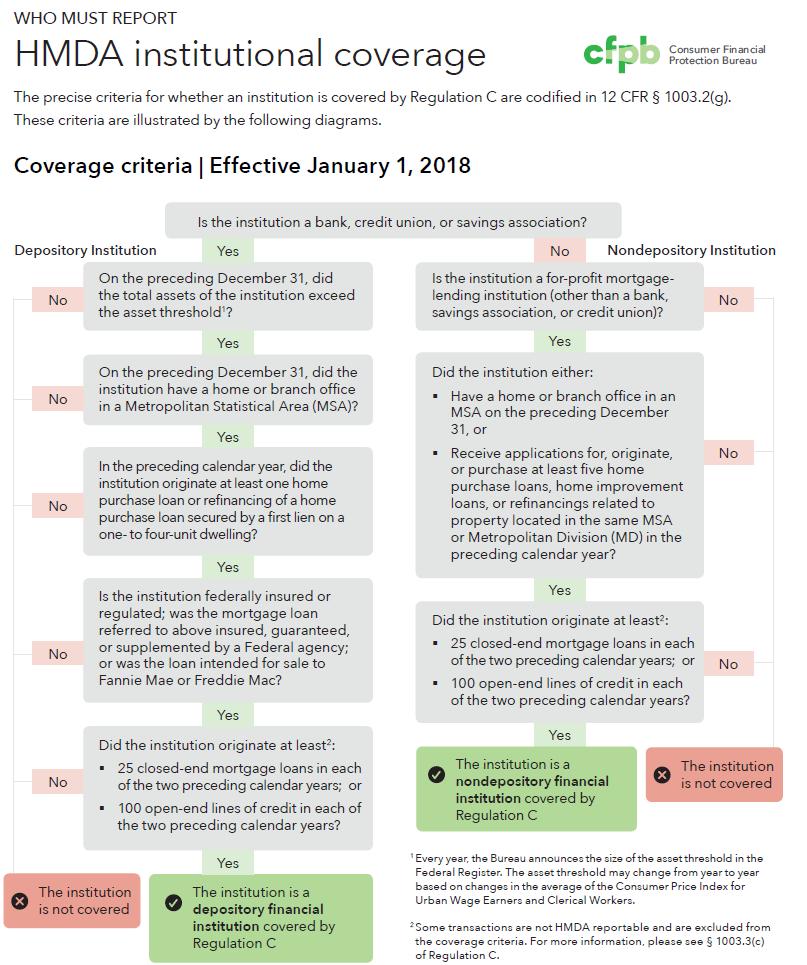

28 HMDA Institutional Coverage Coverage criteria Effective January 1 December 31, 2017 Is the institution a bank, credit union, or savings association? Yes Depository Institution No Other Mortgage Lending Institution Is the institution a for-profit mortgagelending institution (other than a bank, savings association, or credit union)?

29 HMDA Institutional Coverage Is the institution a bank, credit union, or savings association? Yes No Is the institution a for-profit mortgagelending institution (other than a bank, savings association, or credit union)? Yes Other Mortgage Lending Institution No Did the institution either: Have a home or branch office in an MSA on the preceding December 31, or Receive applications for, originate, or purchase at least five home purchase loans, home improvement loans, or refinancings related to property located in the same MSA or Metropolitan Division (MD) in the preceding calendar year? No Yes Did the institution originate at least 2 : 25 closed-end mortgage loans in each of the two preceding calendar years; or 100 open-end lines of credit in each of the two preceding calendar years? No

30 Is the institution a bank, credit union, or savings association? Yes No Other Mortgage Lending Institution Is the institution a for-profit mortgagelending institution (other than a bank, savings association, or credit union)? No Yes Did the institution either: Have a home or branch office in an MSA on the preceding December 31, or Receive applications for, originate, or purchase at least five home purchase loans, home improvement loans, or refinancings related to property located in the same MSA or Metropolitan Division (MD) in the preceding calendar year? No Yes Did the institution originate at least 2 : 25 closed-end mortgage loans in each of the two preceding calendar years; or 100 open-end lines of credit in each of the two preceding calendar years? No Yes The institution is a nondepository financial institution covered by Regulation C The institution is not covered 30

31 HMDA Institutional Coverage The precise criteria for whether an institution is covered by Regulation C are codified in 12 CFR (g). These criteria are illustrated by the following diagrams. Coverage criteria Effective January 1 December 31, 2017 Is the institution a bank, credit union, or savings association? Depository Institution No Yes On the preceding December 31, did the total assets of the institution exceed the asset threshold 1? No Asset-Size Test Yes 1 Every year, the Bureau announces the size of the asset threshold in the Federal Register. The asset threshold may change from year to year based on changes in the average of the Consumer Price Index for Urban Wage Earners and Clerical Workers.

32 HMDA Institutional Coverage The precise criteria for whether an institution is covered by Regulation C are codified in 12 CFR (g). These criteria are illustrated by the following diagrams. Coverage criteria Effective January 1 December 31, 2017 Is the institution a bank, credit union, or savings association? Depository Institution No Yes On the preceding December 31, did the total assets of the institution exceed the asset threshold 1? No Asset-Size Test No Yes On the preceding December 31, did the institution have a home or branch office in a Metropolitan Statistical Area (MSA)? Yes Location Test 1 Every year, the Bureau announces the size of the asset threshold in the Federal Register. The asset threshold may change from year to year based on changes in the average of the Consumer Price Index for Urban Wage Earners and Clerical Workers.

33 HMDA Institutional Coverage Depository Institution No Is the institution a bank, credit union, or savings association? Yes On the preceding December 31, did the total assets of the institution exceed the asset threshold 1? Yes No Asset-Size Test No No On the preceding December 31, did the institution have a home or branch office in a Metropolitan Statistical Area (MSA)? Yes In the preceding calendar year, did the institution originate at least one home purchase loan or refinancing of a home purchase loan secured by a first lien on a one- to four-family dwelling? Location Test Loan Activity Test 1 Every year, the Bureau announces the size of the asset threshold in the Federal Register. The asset threshold may change from year to year based on changes in the average of the Consumer Price Index for Urban Wage Earners and Clerical Workers.

34 HMDA Institutional Coverage Depository Institution No Is the institution a bank, credit union, or savings association? Yes On the preceding December 31, did the total assets of the institution exceed the asset threshold 1? Yes No Asset-Size Test No No No On the preceding December 31, did the institution have a home or branch office in a Metropolitan Statistical Area (MSA)? Yes In the preceding calendar year, did the institution originate at least one home purchase loan or refinancing of a home purchase loan secured by a first lien on a one- to four-family dwelling? Yes Is the institution federally insured or regulated; was the mortgage loan referred to above insured, guaranteed, or supplemented by a Federal agency; or was the loan intended for sale to Fannie Mae or Freddie Mac? Location Test Loan Activity Test Federally Related Test 1 Every year, the Bureau announces the size of the asset threshold in the Federal Register. The asset threshold may change from year to year based on changes in the average of the Consumer Price Index for Urban Wage Earners and Clerical Workers.

35 Depository Institution No Is the institution a bank, credit union, or savings association? Yes No On the preceding December 31, did the total assets of the institution exceed the asset threshold 1? Yes Asset-Size Test No No No On the preceding December 31, did the institution have a home or branch office in a Metropolitan Statistical Area (MSA)? Yes In the preceding calendar year, did the institution originate at least one home purchase loan or refinancing of a home purchase loan secured by a first lien on a one- to four-family dwelling? Yes Is the institution federally insured or regulated; was the mortgage loan referred to above insured, guaranteed, or supplemented by a Federal agency; or was the loan intended for sale to Fannie Mae or Freddie Mac? Location Test Loan Activity Test Federally Related Test No Yes Did the institution originate at least25 closed-end mortgage loans in each of the two preceding calendar years? 2 Loan Volume Test 1 Every year, the Bureau announces the size of the asset threshold in the Federal Register. The asset threshold may change from year to year based on changes in the average of the Consumer Price Index for Urban Wage Earners and Clerical Workers. 2 Some transactions are not HMDA reportable and are excluded from the coverage criteria. For more information, please see (d) of Regulation C. 35

36 Regulation C Phase 1 Phase 2

37 Regulation C Phase

38 Regulation C Phase 2 tests Phase 2

39 Regulation C Phase 2 tests The change beginning in closed-end mortgage loans 100 open-end lines of credit 2 year look back

40

41 HMDA Institutional Coverage The precise criteria for whether an institution is covered by Regulation C are codified in 12 CFR (g). These criteria are illustrated by the following diagrams. Coverage criteria Effective January 1, 2018 Is the institution a bank, credit union, or savings association? Yes No Nondepository institution Is the institution a for-profit mortgagelending institution (other than a bank, savings association, or credit union)? No Yes

42 HMDA Institutional Coverage Is the institution a bank, credit union, or savings association? Yes No Is the institution a for-profit mortgagelending institution (other than a bank, savings association, or credit union)? Yes Nondepository Institution No Location Test Did the institution either: Have a home or branch office in an MSA on the preceding December 31, or Receive applications for, originate, or purchase at least five home purchase loans, home improvement loans, or refinancings related to property located in the same MSA or Metropolitan Division (MD) in the preceding calendar year? Yes No Loan Volume Test Did the institution originate at least 2 : 25 closed-end mortgage loans in each of the two preceding calendar years; or 100 open-end lines of credit in each of the two preceding calendar years? No

43 Is the institution a bank, credit union, or savings association? Yes No Is the institution a for-profit mortgagelending institution (other than a bank, savings association, or credit union)? Yes Nondepository institution No Location Test Did the institution either: Have a home or branch office in an MSA on the preceding December 31, or Receive applications for, originate, or purchase at least five home purchase loans, home improvement loans, or refinancings related to property located in the same MSA or Metropolitan Division (MD) in the preceding calendar year? Yes No Loan Volume Test Did the institution originate at least 2 : 25 closed-end mortgage loans in each of the two preceding calendar years; or 100 open-end lines of credit in each of the two preceding calendar years? Yes No The institution is a nondepository financial institution covered by Regulation C The institution is not covered 43

44 2018 Data Collection 25 closed-end mortgage loans 100 open-end lines of credit 2 year look back 2016 and 2017

45 2018 Data Collection Collect Data Submit Data January 1 st, December 31 st, 2018 March 1 st, 2019

46 2018 Data Collection Location test Loan volume test

47 2018 Data Collection Collect Data March 1 st, 2019 Submit Data

48 Depository Institutions Current Coverage Test Asset-Size Test Location Test Loan Activity Test Federally Related Test

49 Depository Institution Coverage Current Coverage Test New for 2018 Asset-Size Test Location Test 25 Closed End Mortgage Loans Loan Activity Test Federally Related Test or 100 Open End Lines of Credit

50 v HMDA Transactional Coverage Home Mortgage Disclosure Act (HMDA) Regulation C - Final Rule

51 Transactional Coverage Final Rule: Modifies the types of transactions covered From a purpose based test To a dwelling secured test for consumer purpose transactions Dwelling secured test + Purpose-based test for commercial purpose transactions

52 Transactional Coverage Covered Loans Closed-end mortgage loan Open-end line of credit Must be secured by a dwelling

53 Transactional Coverage Covered Loans Closed-end mortgage loan A closed-end mortgage loan is an extension of credit secured by a lien on a dwelling and that is not an open-end line of credit.

54 Transactional Coverage Covered Transaction An open-end line of credit is an extension of credit that is secured by a lien on a dwelling and is an open-end credit plan defined under Regulation Z (a)(20) without regard to whether the credit is consumer credit, extended by a creditor, or extended to a consumer. Open-end line of credit

55 Extension of Credit Extension of Credit New Debt Obligation

56 Extension of Credit If the transaction Modifies Renews Extends Amends Existing debt obligation, but does not satisfy and replace it NOT an extension of credit

57 Extension of Credit Extension of Credit Regulation B Extension of Credit Regulation C to include the granting of credit in any form. to the granting of credit pursuant to a new debt obligation.

58 Extension of Credit Extension of Credit New debt obligation 2 Exceptions Assumptions NY Consolidation, Extensions, Modifications

59 Extension of Credit - Assumptions Assumptions Comment 2(d)(2)-2.i A transaction in which the financial institution enters into a written agreement accepting a new borrower as the obligor on an existing debt obligation No new debt obligation is created The new borrower assumes an existing debt obligation

60 Extension of Credit - Assumptions Assumptions Successor-in-interest transactions Comment 2(d)(2)-2.i Individual succeeds the prior owner as the property owner Takes on the existing debt secured by the property.

61 Extension of Credit New York New York Consolidation, Extensions, Modifications Comment 2(d)(2)-2.ii Transactions pursuant to a New York State consolidation, extension, and modification agreement. CEMAS Supplemental Mortgage New York Tax Law Section 255 Reduced or no mortgage recording taxes

62 Extension of Credit New York New York Consolidation, Extensions, Modifications Comment 2(d)(2)-2.ii New York CEMAs Loans Secured by Dwellings Located in New York State Replace traditional refinancings

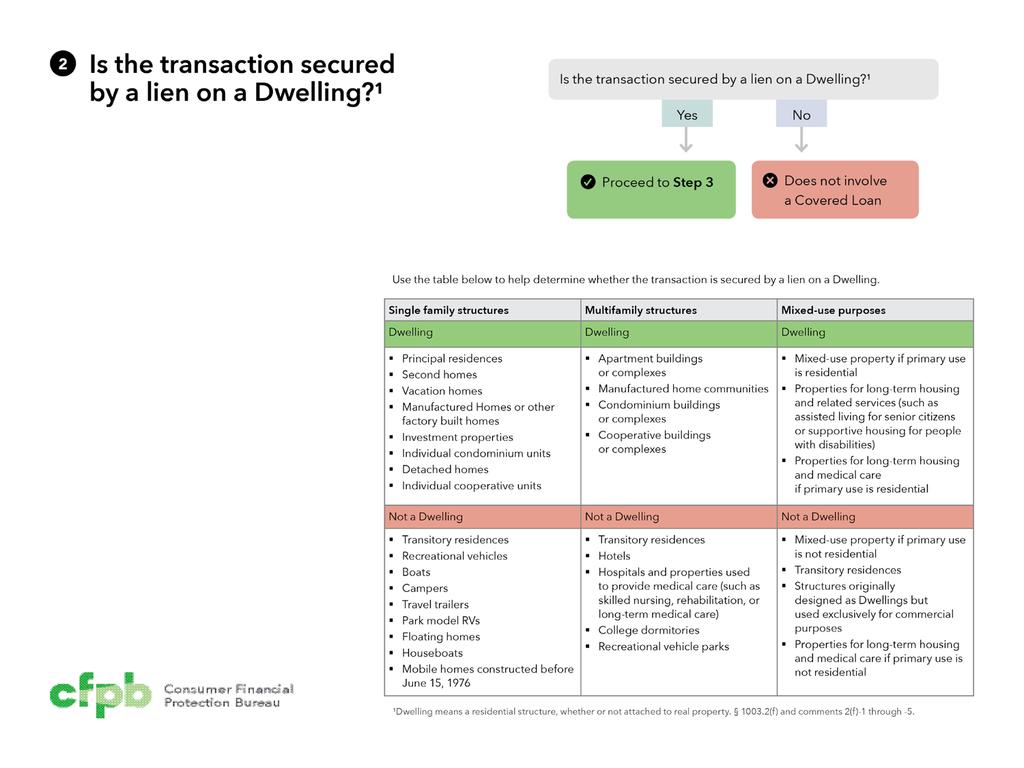

63 Secured by Lien on a Dwelling Dwelling (f) Second Test Closed-end mortgage loan Open-end line of credit Is the transaction secured by a lien on a dwelling?

Residential Structure Whether or not it is attached to real property Not limited to principal")

64 What is a Dwelling? Dwelling (f) Residential Structure Whether or not it is attached to real property Not limited to principal residence Nor is it limited to a structure that has 4 or less units

65 Dwelling Examples Second homes and vacations homes Investment properties Manufactured homes or other factory-built homes Multifamily residential structures or communities Apartments Condominiums Cooperative buildings or complexes Manufactured homes

66 What is NOT a Dwelling? NOT a Dwelling Comment 2(f)-3 Recreational vehicles Boats, Campers, Trailers, Park Model Houseboats, floating homes, and mobile homes constructed before June 15, 1976 Transitory residences such as hotels, hospitals, and college dorms Structures originally designed as a dwelling but converted to exclusive commercial use

67 Mixed Use Properties Mixed Use Official Interpretations 2(f)-4 Commercial Residential Apartment units and retail space

-4 Primary Use of the property Square footage Income")

68 Mixed Use Properties Mixed Use Official Interpretations 2(f)-4 Primary Use of the property Square footage Income generated

69 Mixed Use Properties Mixed Use Official Interpretations 2(f)-4 Commercial Residential IF primary use is residential Considered a dwelling

70 Summary of Closed-End Mortgage Loan Closed-end mortgage Extension of Credit Secured by a lien on a dwelling Not an open line of credit

71 What is an Open-End Line of Credit? Open-end Line of Credit (o) Extension of credit secured by a dwelling Open-end credit plan under Regulation Z Without regard to whether the credit is Consumer credit Extended by a creditor Extended to a consumer

72 What is an Open-End Line of Credit? Open-end Line of Credit (o) Creditor contemplates repeated transactions May impose a finance charge on an outstanding unpaid balance Amount of credit that may be extended to the borrower during the term of the plan is generally made available to the extent any outstanding balance is repaid

73 What is an Open-End Line of Credit? Open-end Line of Credit (o) Amount of credit extended to the borrower during the term of the plan up to limit established by the creditor

74 Excluded Transactions Excluded transactions (c) Closed-end mortgage loan Open-end line of credit Secured by a lien on unimproved land But note 2 year rule, unless temporary financing

75 Excluded Transactions Excluded transactions (c) Closed-end mortgage loan Open-end line of credit Temporary Financing NOT determined by duration of loan Is designed to be replaced by permanent financing at a later time

76 Example transaction: Temporary financing Excluded transactions (c) Temporary Financing Construction Loan where proceeds will finance Construction phase of dwelling New extension of credit will be obtained Excluded as a temporary financing

77 Example transaction: Not temporary financing NOT Temporary Financing Construction-to-permanent Loan where proceeds Finance the construction of dwelling Converted to permanent financing Without separate closing once complete

78 Excluded Transactions - Agriculture Excluded transactions (c) Closed-end mortgage loan Open-end line of credit Proceeds for Agriculture Dwelling on real property used primarily for agriculture Determine primary use of property Select Reasonable Standard

79 What is Agricultural Purpose? See Regulation Z, 12 CFR Part 1026, Supplement I Comment 3(a)-8

80 Excluded Transactions Business and Commercial Excluded transactions (c) Closed-end mortgage loan Open-end line of credit Proceeds for business use Proceeds for commercial use

81 Business and Commercial Excluded transactions (c) Closed-end mortgage loan Open-end line of credit And meets Regulation C definition of Used for Commercial or Business Home improvement loan Home purchase loan Refinancing Not excluded

82 Covered Transaction Business or Commercial Transaction Closed-end mortgage loan Open-end line of credit Purchase multifamily dwelling, secured by the dwelling

83 Covered Transaction Business or Commercial Transaction Closed-end mortgage loan Open-end line of credit Home improvement loan to improve an office located in a dwelling

84 Non Covered Transaction Business or Commercial Transaction Closed-end mortgage loan Open-end line of credit Proceeds to expand a business Proceeds will be used to purchase business equipment

85 Non Covered Transaction Business or Commercial Transaction Proceeds to expand a business Extended to a corporation where proceeds are used to purchase business equipment Home Improvement Does NOT meet Home Purchase Loan Refinancing

86 Excluded Transactions Originated Fewer than 25 closed-end mortgage loans or 100 open-end lines of credit In either of the last two preceding calendar years

87 Excluded Transactions If fewer than 25 Closed-end mortgage loans in either of the two last calendar years NOT required to: Collect Record Report Closed-end mortgage loans

88 Excluded Transactions If fewer than 100 Open-end lines of credit in either of the last two calendar years NOT required to: Collect Record Report Open-end lines of credit

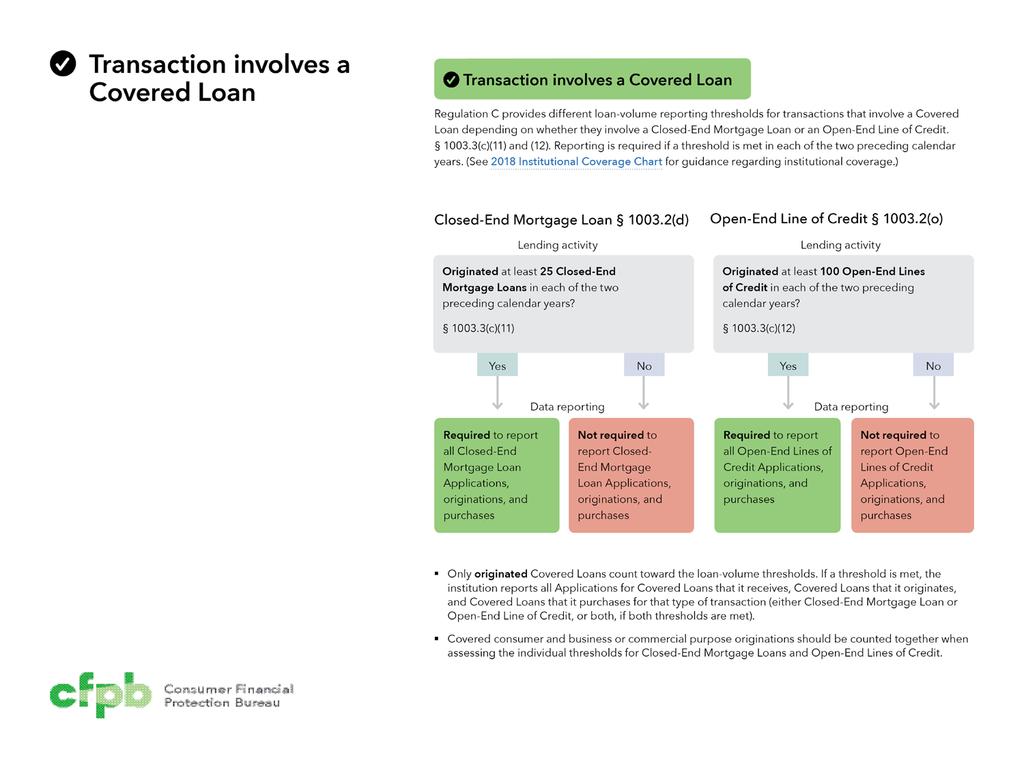

89 Excluded Transactions Closed-end mortgage loan Open-end line of credit At least 25 in each of the preceding two calendar years Fewer than 100 in either of the preceding two calendar years Report Report

90 Excluded Transactions Closed-end mortgage loan Open-end line of credit Fewer than 25 in either of the preceding two calendar years At least 100 in each of the preceding two calendar years Report Report

91 v Loan-Volume thresholds Examples

92 Examples Loan volume thresholds Loan type Originations during calendar year Must collect in 2018 and report in 2019 A Closed end mortgage loans Open end lines of credit 30 1, ,200 Only open-end lines of credit B Closed end mortgage loans Open end lines of credit Only closed-end mortgage loans C Closed end mortgage loans 55 Open end lines of credit Both closed-end mortgage loans and open-end lines of credit D Closed end mortgage loans Open end lines of credit Neither

93 v HMDA Transactional Coverage chart Home Mortgage Disclosure Act (HMDA) Regulation C - Final Rule

94 94

95 95

96 96

97 97

98 98

99 99

100 v When to report a covered transaction

101 When to Report a Covered Transaction Transaction is Covered Determine whether institution engaged in activity that obligates it to report Reports actions taken Applications Originations Purchases

102 When to Report a Covered Transaction Application did not result in originated covered loan Collect Report Application if financial institution took action Application was withdrawn while under review

103 When to Report a Covered Transaction Application results in originated covered loan Report Origination of the covered loan Do not report application and origination separately

104 What is an Application? Application Written or oral request for a covered loan Accordance with procedures the financial institution uses Type of credit requested

105 What is a Request for Preapproval? Preapproval Request Considered an application under Regulation C Home purchase loan NOT secured by a multifamily dwelling NOT for an open-end line of credit or Not for reverse mortgage Reviewed under a preapproval program

106 What is a Preapproval Program? Home Purchase Preapproval Program Institution conducts comprehensive analysis of creditworthiness Issues a written commitment Subject only to permitted conditions

107 What are Permitted Conditions? Preapproval Program Identification of a suitable property Require no material change occur regarding the applicant s financial condition prior to closing Limited conditions that not are related to the applicant s financial condition or creditworthiness and ordinarily attached to a traditional home mortgage application Ordinarily attaches to a traditional home mortgage application

108 Example - Permitted Conditions Acceptable Title Insurance Binder or Certificate OR Indicates clear termite inspection certification Required to report data on preapproval request only if denied or results in: Home purchase loan or was approved but not accepted

109 Who Reports Multiple Entities? Who reports the origination? Comment 4(a)-2 Only one entity reports the covered loan as an origination The institution that made the credit decision approving the application before closing or account opening Regardless of whether loan closed in the institution s name

110 Multiple Applications Who reports an application? Comment 4(a)-2 Multiple applications Institution that approved the loan before closing and purchased the loan after closing reports the loan as an origination Any institutions that received the application before closing reports the action it took on the application

111 Multiple Application Approvals Who Reports? Report action taken on applications received Comment 4(a)-2 Does not matter Method Received (Applicant, broker, another financial institution) Application does not result in an origination

112 Credit Decisions through Agents Who Reports? Decisions made through actions of agents Comment 4(a)-4 Ficus Bank (agent for Elm Bank) Elm Bank

113 Credit Decisions through Agents Who Reports? Comment 4(a)-4 Applicant does not accept loan Ficus Bank Elm Bank Who reports the transaction? Report as approved but not accepted Acting Agent to Elm Bank State law determines agent party

114 Broker Rule Examples can be found in Comments 4(a)-2 through -4

115 v Data submission process Home Mortgage Disclosure Act (HMDA) Regulation C - Final Rule

116 How do we file HMDA data? Data Collected in 2017 Bureau By March 1 st, 2018

117 How to submit HMDA data? consumerfinance.gov/hmda

118 How do we file HMDA data? Data Collected in 2018 Bureau By March 1 st, 2019

119 How to submit HMDA data? Appendix A Appendix A January 1, 2018 January 1, 2019

120 Quarterly Reporting January 1st, ,000 Covered loans and applications

121 Quarterly Reporting Quarterly Reporting Does not apply to 4 th Quarter Data Reports 4 th Quarter Data with Annual First 3 quarters Corrections 4 th Quarter Data

122 Example Bank Name Reported Loans and Applications in 2019 HMDA Data HMDA Reporting in 2020 Quarterly Reporting Ficus Bank 60,000 1 st quarter data due by May 30, nd quarter data due by August 30, 2020 Yes 3 rd quarter data due by November 30, th quarter data along with previously submitted 1 st, 2 nd, and 3 rd quarter data, including corrections due by March 1, 2021

123 Example Bank Name Reported Loans and Applications in 2019 HMDA Data HMDA Reporting in 2020 Quarterly Reporting Pine Bank 59,999 Due by March 1 st, 2021 No

124 v Disclosure of data Home Mortgage Disclosure Act (HMDA) Regulation C - Final Rule

125 How are HMDA data disclosed? FFIEC

126 How are HMDA data disclosed? Public consumerfinance.gov/hmda

127 Sample Notice Home Mortgage Disclosure Act Notice The HMDA data about our residential mortgage lending are available online for review. The data show geographic distribution of loans and applications; ethnicity, race, sex, age and income of applicants and borrowers; and information about loan approvals and denials. These data are available online at the Consumer Financial Protection Bureau s Web site ( HMDA data for many other financial institutions are also available at this Web site.

128 Disclosure Data Requester

129 Obligation to Disclose Beginning in 2018 Provide written notice regarding availability

130 Obligation to Disclose consumerfinance.gov/hmda

131 Sample Notice Home Mortgage Disclosure Act Notice The HMDA data about our residential mortgage lending are available online for review. The data show geographic distribution of loans and applications; ethnicity, race, sex, age and income of applicants and borrowers; and information about loan approvals and denials. These data are available online at the Consumer Financial Protection Bureau s Web site ( HMDA data for many other financial institutions are also available online. For more information, visit the Consumer Financial Protection Bureau s Web site (

132 Modified LAR Requester

133 v Overview of effective dates Home Mortgage Disclosure Act (HMDA) Regulation C - Final Rule

134 HMDA Rule Key Dates Timeline Data Data Effective Submission Collection Dates No new regulatory requirements go into effect Q1 Q4 Collect 2016 data as required under the current rule 1 (for reporting in 2017) 1/1 Effective date for excluding low volume depository institutions from coverage Q1 Q4 Collect 2017 data as required under the current rule 1 (for reporting in 2018) 1/1 Effective date for most provisions related to institutional and transactional coverage, and data collection, recording, reporting, and disclosure Q1 Q4 Collect 2018 data as required under the new rule 2 (for reporting in 2019) 1/1 Effective date for changes to enforcement provisions and additional amendments to reporting provisions Q1 Q4 Collect 2019 data as required under the new rule 2 (for reporting in 2020) 1/1 Effective date for quarterly reporting provisions 1/1 3/1 1/1 3/1 1/1 3/1 1/1 3/1 1/1 3/1 Q1 Q4 Collect 2020 data as required under the new rule 2 (for reporting in 2021 and, if FI is quarterly reporter, 2020) Submit 2015 data Submit 2016 data as Submit 2017 data as Submit 2018 data as Submit 2019 data as required as required under required under the required under the required under the new under the new rule, 2 and submit the current rule, 1 current rule, 1 and current rule, 1 and rule, 2 and submit to the to the CFPB and submit to submit to the submit to the CFPB CFPB 4/1 5/30 the Federal Reserve Federal Reserve Board Board Quarterly FI reporters report Q1, 2020 data as required under the new rule, 2 and submit to the CFPB

135 Effective dates Loan-Volume Threshold for Depository Institutions Effective Date: January 1 st, 2017 As of December 31 st, 2016 As of December 31 st, 2016 Calendar year 2016 Calendar year 2016 Calendar year 2015 Calendar year 2016 Asset Size Test Location test Loan activity test Federally related test Temporary loan volume test Temporary loan volume test 135

136 Effective Dates January 1, 2018 Institutional coverage Transactional coverage Data Collection Data Reporting Disclosure

137 Effective Dates for Transactional Coverage January 1 st, 2018 Collects Records Reports Data points

138 Action Taken and Date to Report - Comment 4(a)(8)(i) Action taken Reportable date Loan originated Loan purchased Application approved but not accepted Application denied Application withdrawn* File closed for incompleteness* Preapproval request approved but not accepted Preapproval request denied Generally, loan closing or account opening date Date of purchase Any reasonable date, such as approval date, deadline for accepting offer, or date file was closed Date application is denied or date notice sent to applicant Date the express withdrawal was received or date shown on the notification form (if written withdrawal) Date file was closed or date notice sent to applicant Any reasonable date, such as approval date, deadline for accepting offer, or date file was closed Date preapproval request was denied or date notice sent to applicant

139 Determining collection and reporting year Date of Application or Purchase Final Action Taken Final Action Taken Date Collect HMDA data Report HMDA data by Application received 10/1/2017 Loan Originated 12/1/2017 as required under the old (prior to 2018) rule 3/1/2018 Loan purchased 10/1/2017 Loan Purchased 10/1/2017 as required under the old (prior to 2018) rule 3/1/2018 Application received 10/1/2017 Loan Originated 1/5/2018 as required under the new (effective 2018) rule* 3/1/2019 Application received 2/15/2018 Application Denied 3/15/2018 as required under the new (effective 2018) rule* 3/1/2019 Loan purchased 1/5/2018 Loan Purchased 1/5/2018 as required under the new (effective 2018) rule 3/1/2019 *See comment 4(a)(10)(i)

140 Reminder Data points Application channel Points and fees Underwriting information Debt-to-income Ratio Unique loan identifier Property value

141 Determining collection and reporting year Date of Application or Purchase Final Action Taken Final Action Taken Date Collect HMDA data Report HMDA data by Application received 10/1/2017 Loan Originated 12/15/2017 as required under the old (prior to 2018) rule 3/1/2018 Loan purchased 10/1/2017 Loan Purchased 10/1/2017 as required under the old (prior to 2018) rule 3/1/2018 Application received 10/1/2017 Loan Originated 1/5/2018 as required under the new (effective 2018) rule* 3/1/2019 Application received 2/15/2018 Application Denied 3/15/2018 as required under the new (effective 2018) rule* 3/1/2019 Loan purchased 1/5/2018 Loan Purchased 1/5/2018 as required under the new (effective 2018) rule 3/1/2019 *Collect race, ethnicity, and sex according to the Appendix B instructions in effect for 2017 data collection. See comment 4(a)(10)(i)

142 Determining collection and reporting year Date of Application or Purchase Final Action Taken Final Action Taken Date Collect HMDA data Report HMDA data by Application received 10/1/2017 Loan Originated 12/15/2017 as required under the old (prior to 2018) rule 3/1/2018 Loan purchased 10/1/2017 Loan Purchased 10/1/2017 as required under the old (prior to 2018) rule 3/1/2018 Application received 10/1/2017 Loan Originated 1/5/2018 as required under the new (effective 2018) rule* 3/1/2019 Application received 2/15/2018 Application Denied 3/15/2018 as required under the new (effective 2018) rule* 3/1/2019 Loan purchased 1/5/2018 Loan Purchased 1/5/2018 as required under the new (effective 2018) rule 3/1/2019 * Collect race, ethnicity, and sex according to the Appendix B instructions under the final rule. See comment 4(a)(10)(i)

143 Effective Dates Submit Data Electronically Effective on January 1 st, 2018 Report by March 1 st, 2018

144 Effective Dates Beginning in 2018 Provide written notice regarding LAR availability consumerfinance.gov/hmda

145 Effective Dates January 1 st, 2019 Reports Timely Reports Fully Corrects Data Reports Accurately

146 Effective Dates Beginning in 2020 Large Volume Financial Institutions Report HMDA Data Quarterly 2019 Data 2019 Data 59,999 Covered Loans and applications 60,000 Covered Loans and applications Do Not Submit Quarterly Submit Quarterly in 2020

147 v Closing Home Mortgage Disclosure Act (HMDA)

148 For more information

149 Submit specific regulatory questions Technical questions:

150 Thank you

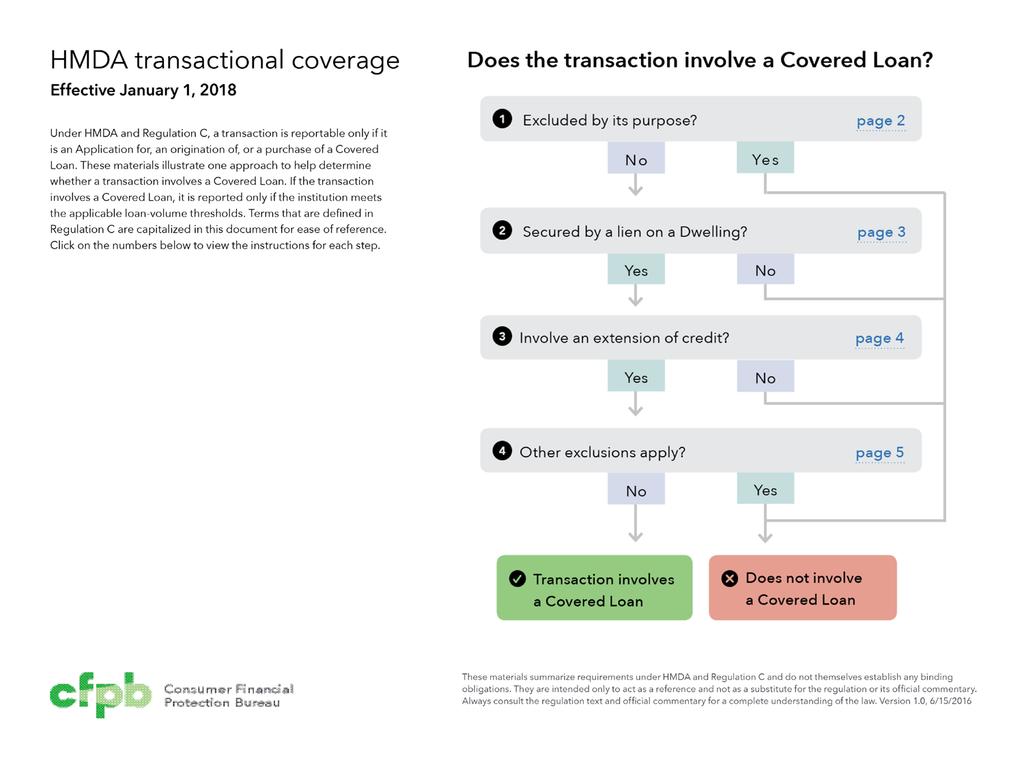

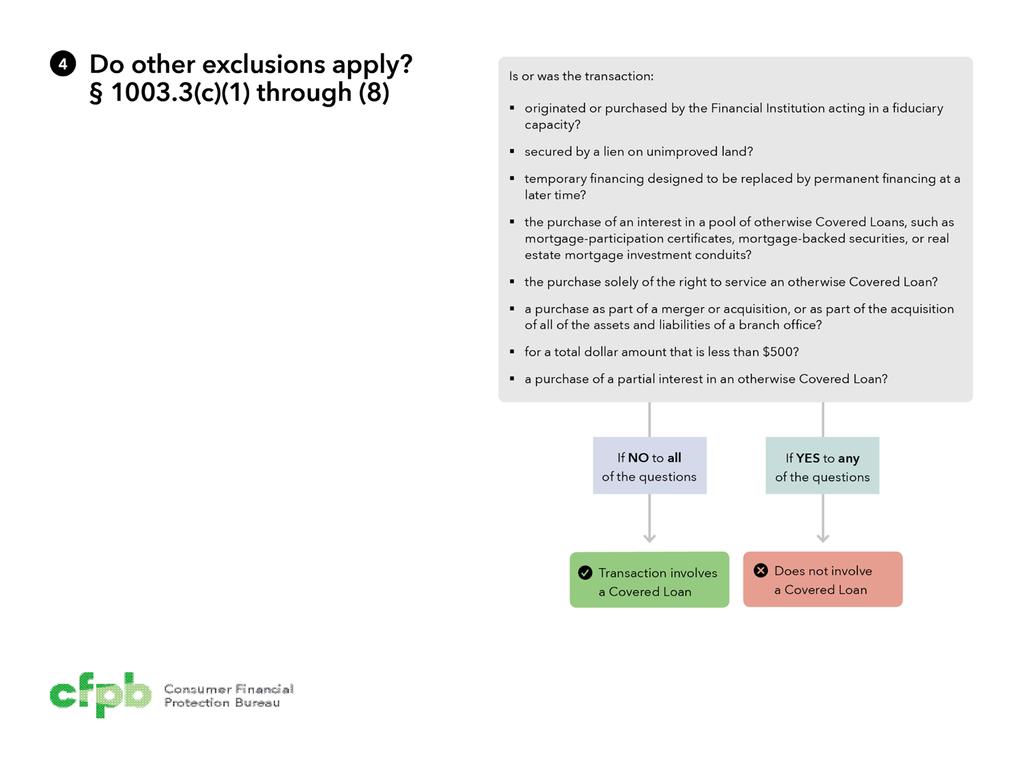

HMDA transactional coverage

HMDA transactional coverage Protection Bureau Effective January 1, 2018 Under HMDA and Regulation C, a transaction is reportable only if it is an Application for, an origination of, or a purchase of. These

HMDA transactional coverage Protection Bureau Effective January 1, 2018 Under HMDA and Regulation C, a transaction is reportable only if it is an Application for, an origination of, or a purchase of. These

1) The credit union's assets total more than $44 million as of December 31, 2017,

The credit union's assets total more than $44 million as of December 31, 2017,") Exemption: This regulation only applies if the following criteria are met: 1) The credit union's assets total more than $44 million as of December 31, 2017, 2) The credit union has a home or branch office

Exemption: This regulation only applies if the following criteria are met: 1) The credit union's assets total more than $44 million as of December 31, 2017, 2) The credit union has a home or branch office

HMDA FACT SHEET YOUR MAP TO REGULATORY CHANGE

FACILITATE THOUGHT ENGAGE DIALOGUE ENCOURAGE SMART RISK CULTIVATE A NETWORK BUILD KNOWLEDGE HMDA FACT SHEET YOUR MAP TO REGULATORY CHANGE Regulation C implements the Home Mortgage Disclosure Act (HMDA),

FACILITATE THOUGHT ENGAGE DIALOGUE ENCOURAGE SMART RISK CULTIVATE A NETWORK BUILD KNOWLEDGE HMDA FACT SHEET YOUR MAP TO REGULATORY CHANGE Regulation C implements the Home Mortgage Disclosure Act (HMDA),

Home Mortgage Disclosure (Regulation C)

") October 2017 OMB Control No. 3170-0008 Home Mortgage Disclosure (Regulation C) Small Entity Compliance Guide Version Log The Bureau updates this guide on a periodic basis. Below is a version log noting

October 2017 OMB Control No. 3170-0008 Home Mortgage Disclosure (Regulation C) Small Entity Compliance Guide Version Log The Bureau updates this guide on a periodic basis. Below is a version log noting

Compliance Policy 2003-ALL

Overview The following policy describes how CMG Mortgage, Inc., dba CMG Financial, NMLS #1820, ( CMG ) complies with the Home Mortgage Disclosure Act (HMDA) and its implementing regulation, Regulation

Overview The following policy describes how CMG Mortgage, Inc., dba CMG Financial, NMLS #1820, ( CMG ) complies with the Home Mortgage Disclosure Act (HMDA) and its implementing regulation, Regulation

ICBA Summary of the Home Mortgage Disclosure Act (HMDA) Revisions to Regulation C

Revisions to Regulation C") ICBA Summary of the Home Mortgage Disclosure Act (HMDA) Revisions to Regulation C June 2017 INSERT YEAR HERE Contact Information: Rhonda Thomas-Whitley Assistant Vice President & Regulatory Counsel Rhonda.Thomas-Whitley@icba.org

ICBA Summary of the Home Mortgage Disclosure Act (HMDA) Revisions to Regulation C June 2017 INSERT YEAR HERE Contact Information: Rhonda Thomas-Whitley Assistant Vice President & Regulatory Counsel Rhonda.Thomas-Whitley@icba.org

What do HMDA Rule Changes Mean for Covered Institutions?

What do HMDA Rule Changes Mean for Covered Institutions? Tips to prepare for regulatory and institutional change Paula Witt, Director, Consumer Finance & Fair Banking Elizabeth Rozsa, Manager, Consumer

What do HMDA Rule Changes Mean for Covered Institutions? Tips to prepare for regulatory and institutional change Paula Witt, Director, Consumer Finance & Fair Banking Elizabeth Rozsa, Manager, Consumer

Comment Call (14-15) CFPB Home Mortgage Disclosure Act (HMDA)

CFPB Home Mortgage Disclosure Act (HMDA)") Comment Call (14-15) CFPB Home Mortgage Disclosure Act (HMDA) Impact: Federal and State Chartered Credit Unions Relevant Department: CEO / Lending Priority Level: High Background / Credit Union Summary

Comment Call (14-15) CFPB Home Mortgage Disclosure Act (HMDA) Impact: Federal and State Chartered Credit Unions Relevant Department: CEO / Lending Priority Level: High Background / Credit Union Summary

CFPB Consumer Laws and Regulations

Consumer Laws and Regulations Home Mortgage Disclosure Act 1 The Home Mortgage Disclosure Act () was enacted by the Congress in 1975 and is implemented by Regulation C (12 CFR Part 1003). 2 The period

Consumer Laws and Regulations Home Mortgage Disclosure Act 1 The Home Mortgage Disclosure Act () was enacted by the Congress in 1975 and is implemented by Regulation C (12 CFR Part 1003). 2 The period

HMDA LET S GET IT RIGHT!

HMDA LET S GET IT RIGHT! Home Mortgage Disclosure Act December 19, 2017 Joan Crenshaw, CRCM, CAFP Director jcrenshaw@bkd.com 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they

HMDA LET S GET IT RIGHT! Home Mortgage Disclosure Act December 19, 2017 Joan Crenshaw, CRCM, CAFP Director jcrenshaw@bkd.com 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they

New HMDA Requirements

New HMDA Requirements August 18, 2016 INSTITUTE OF CERTIFIED BANKERS Certification of Attendance at an Activity This form is to be used by the individual attendee for his/her records only. ICB will send

New HMDA Requirements August 18, 2016 INSTITUTE OF CERTIFIED BANKERS Certification of Attendance at an Activity This form is to be used by the individual attendee for his/her records only. ICB will send

Home Mortgage Disclosure Act 2017, 2018, and Beyond. Presented by Marissa Blundell Bankers Advisory A CliftonLarsonAllen LLP Division

Home Mortgage Disclosure Act 2017, 2018, and Beyond Presented by Marissa Blundell Bankers Advisory A CliftonLarsonAllen LLP Division Home Mortgage Disclosure Act (HMDA) Consumer Financial Protection Bureau

Home Mortgage Disclosure Act 2017, 2018, and Beyond Presented by Marissa Blundell Bankers Advisory A CliftonLarsonAllen LLP Division Home Mortgage Disclosure Act (HMDA) Consumer Financial Protection Bureau

HMDA: Haven or Havoc. Cindy Prince, Presenter December 5, 6 & 7, 2017 Assisted by Rachelle Dekker and Matt Goble

HMDA: Haven or Havoc Cindy Prince, Presenter December 5, 6 & 7, 2017 Assisted by Rachelle Dekker and Matt Goble Agenda Day One 1. Effective dates 2. Overview of reporting requirements Annual expectations

HMDA: Haven or Havoc Cindy Prince, Presenter December 5, 6 & 7, 2017 Assisted by Rachelle Dekker and Matt Goble Agenda Day One 1. Effective dates 2. Overview of reporting requirements Annual expectations

Covered loans or applications if the property is

Application Date 1003.4(a)(1)(ii) Property Address State County Census Tract Covered loans or applications if the property address of the property securing the covered loan is not known (e.g., the property

Application Date 1003.4(a)(1)(ii) Property Address State County Census Tract Covered loans or applications if the property address of the property securing the covered loan is not known (e.g., the property

What s New in Mortgage Lending Compliance?

What s New in Mortgage Lending Compliance? Michael R. Christians Senior Federal Compliance Counsel Credit Union National Association Copyright 2016 by Credit Union National Association. All rights reserved.

What s New in Mortgage Lending Compliance? Michael R. Christians Senior Federal Compliance Counsel Credit Union National Association Copyright 2016 by Credit Union National Association. All rights reserved.

2018 HMDA Implementation. Presented By: Karen Ruckle, Director of Compliance Bank of the Ozarks

2018 HMDA Implementation Presented By: Karen Ruckle, Director of Compliance Bank of the Ozarks 2018 HMDA Loan Volume Test # Loans #Loans #Loans Home Purchase Or Refi (Dwelling Secured) in prior calendar

2018 HMDA Implementation Presented By: Karen Ruckle, Director of Compliance Bank of the Ozarks 2018 HMDA Loan Volume Test # Loans #Loans #Loans Home Purchase Or Refi (Dwelling Secured) in prior calendar

Home Mortgage Disclosure Act (HMDA) 2014 FIS and/or its subsidiaries. All Rights Reserved.

2014 FIS and/or its subsidiaries. All Rights Reserved.") Home Mortgage Disclosure Act (HMDA) 2014 FIS and/or its subsidiaries. All Rights Reserved. 1 Home Mortgage Disclosure Act (HMDA) 12 CFR 1003 Purpose: Detect illegal discrimination Detect predatory lending

Home Mortgage Disclosure Act (HMDA) 2014 FIS and/or its subsidiaries. All Rights Reserved. 1 Home Mortgage Disclosure Act (HMDA) 12 CFR 1003 Purpose: Detect illegal discrimination Detect predatory lending

Home Mortgage Disclosure Act HMDA Part 1. Presented by: Aaron Kouhoupt, Esq.

Home Mortgage Disclosure Act HMDA Part 1 Presented by: Aaron Kouhoupt, Esq. Timeline January 1, 2018 Coverage and collection of expanded data required under new rule (Be careful!) March 1, 2019 Report

Home Mortgage Disclosure Act HMDA Part 1 Presented by: Aaron Kouhoupt, Esq. Timeline January 1, 2018 Coverage and collection of expanded data required under new rule (Be careful!) March 1, 2019 Report

Home Mortgage Disclosure Act. with Anne Lolley. / X4

TOTAL TRAINING SOLUTIONS SPECIAL CREDIT UNION WEBINAR HMDA Home Mortgage Disclosure Act with Anne Lolley DECEMBER 2014 alolley@cox.net / 877-778-5192 X4 Copyright Total Training Solutions and Anne Lolley

TOTAL TRAINING SOLUTIONS SPECIAL CREDIT UNION WEBINAR HMDA Home Mortgage Disclosure Act with Anne Lolley DECEMBER 2014 alolley@cox.net / 877-778-5192 X4 Copyright Total Training Solutions and Anne Lolley

HMDA: Haven or Havoc. Michigan Bankers Association. Compliance Services 2016 Temenos USA. All rights reserved.

HMDA: Haven or Havoc Michigan Bankers Association 1 2016 Temenos USA. All rights reserved. About the Speaker Rachelle Dekker CRCM Rachelle Dekker is a Senior Compliance Advisor with the Temenos Compliance

HMDA: Haven or Havoc Michigan Bankers Association 1 2016 Temenos USA. All rights reserved. About the Speaker Rachelle Dekker CRCM Rachelle Dekker is a Senior Compliance Advisor with the Temenos Compliance

V. Lending HMDA. Home Mortgage Disclosure Act 1 V-9.1. Introduction. Applicability

Home Mortgage Disclosure Act 1 Introduction The Home Mortgage Disclosure Act (HMDA) was enacted by the Congress in 1975 and is implemented by the Federal Reserve Board s (FRB s) Regulation C, Home Mortgage

Home Mortgage Disclosure Act 1 Introduction The Home Mortgage Disclosure Act (HMDA) was enacted by the Congress in 1975 and is implemented by the Federal Reserve Board s (FRB s) Regulation C, Home Mortgage

Consumer Financial Protection Bureau. March 15, Draft, Sensitive and Pre-Decisional Not for External Distribution

Consumer Financial Protection Bureau March 15, 2016 Draft, Sensitive and Pre-Decisional Not for External Distribution Outline Home Mortgage Disclosure Act 1) Background 2) Rule Making 3) Changes Coming

Consumer Financial Protection Bureau March 15, 2016 Draft, Sensitive and Pre-Decisional Not for External Distribution Outline Home Mortgage Disclosure Act 1) Background 2) Rule Making 3) Changes Coming

HMDA / Regulation C Amendments New 1003 Application

HMDA / Regulation C Amendments New 1003 Application January 2017 1Nations Direct Mortgage, LLC Mission Statement - To lead the third party residential mortgage industry by providing products and services

HMDA / Regulation C Amendments New 1003 Application January 2017 1Nations Direct Mortgage, LLC Mission Statement - To lead the third party residential mortgage industry by providing products and services

Summary of Reportable HMDA Data Regulatory Reference Chart a

Summary of Reportable HMDA Data Regulatory Reference Chart a This chart is intended to be used as a reference tool for data points required to be collected, recorded, and reported under Regulation C, as

Summary of Reportable HMDA Data Regulatory Reference Chart a This chart is intended to be used as a reference tool for data points required to be collected, recorded, and reported under Regulation C, as

HMDA Regulations and New 1003 Application - Part 2

HMDA Regulations and New 1003 Application - Part 2 Broker / Correspondent Training May 10 & 12, 2017 1Nations Direct Mortgage Agenda Overview of New Regulations New and Modified HMDA Data Fields Detail

HMDA Regulations and New 1003 Application - Part 2 Broker / Correspondent Training May 10 & 12, 2017 1Nations Direct Mortgage Agenda Overview of New Regulations New and Modified HMDA Data Fields Detail

Home Mortgage Disclosure Act. I. Existing Rule a. Purpose b. Requirements II. New Rule a. When b. What

Home Mortgage Disclosure Act I. Existing Rule a. Purpose b. Requirements II. New Rule a. When b. What EDITION EFFECTIVE JANUARY 1, 2013 (For HMDA Submissions due March 1, 2014) A GUIDE TO HMDA Reporting

Home Mortgage Disclosure Act I. Existing Rule a. Purpose b. Requirements II. New Rule a. When b. What EDITION EFFECTIVE JANUARY 1, 2013 (For HMDA Submissions due March 1, 2014) A GUIDE TO HMDA Reporting

Major Changes Looming for HMDA Reporting

Major Changes Looming for HMDA Reporting CLIENT ALERT September 25, 2017 Scott D. Samlin samlins@pepperlaw.com Mark T. Dabertin dabertinm@pepperlaw.com In this article, we review the requirements of the

Major Changes Looming for HMDA Reporting CLIENT ALERT September 25, 2017 Scott D. Samlin samlins@pepperlaw.com Mark T. Dabertin dabertinm@pepperlaw.com In this article, we review the requirements of the

Action Taken. PRE-APPLICATION Do you Prequalify? Do you have Preapprovals? Which road do you take? Be Consistent!

1 Action Taken 2 PRE-APPLICATION Do you Prequalify? Do you have Preapprovals? Which road do you take? Be Consistent! 3 1 Discrimination & Fair Lending During the Pre-Application Process - use caution gathering

1 Action Taken 2 PRE-APPLICATION Do you Prequalify? Do you have Preapprovals? Which road do you take? Be Consistent! 3 1 Discrimination & Fair Lending During the Pre-Application Process - use caution gathering

Executive Summary of the 2018 HMDA Interpretive and Procedural Rule

Bureau of Consumer Financial Protection 1700 G Street NW Washington, D.C. 20552 August 31, 2018 Executive Summary of the 2018 HMDA Interpretive and Procedural Rule On August 31, 2018, the Bureau of Consumer

Bureau of Consumer Financial Protection 1700 G Street NW Washington, D.C. 20552 August 31, 2018 Executive Summary of the 2018 HMDA Interpretive and Procedural Rule On August 31, 2018, the Bureau of Consumer

Banks, Banking, Credit unions, Mortgages, National banks, Savings associations,

List of Subjects in 12 CFR Part 1003 Banks, Banking, Credit unions, Mortgages, National banks, Savings associations, Reporting and recordkeeping requirements. Authority and Issuance For the reasons set

List of Subjects in 12 CFR Part 1003 Banks, Banking, Credit unions, Mortgages, National banks, Savings associations, Reporting and recordkeeping requirements. Authority and Issuance For the reasons set

Sue Quilty, Quilty & Associates (781)

") Sue Quilty, Quilty & Associates susan.quilty@verizon.net (781)706-9235 Agenda HMDA Today: Review HMDA in the Future: Proposed Changes Surviving HMDA Reporting 2 HMDA Review HMDA Overview Why is HMDA Important

Sue Quilty, Quilty & Associates susan.quilty@verizon.net (781)706-9235 Agenda HMDA Today: Review HMDA in the Future: Proposed Changes Surviving HMDA Reporting 2 HMDA Review HMDA Overview Why is HMDA Important

Home Mortgage Disclosure Act; Regulation C; Official Staff Interpretations; HMDA FAQs

Home Mortgage Disclosure Act UNITED STATES CODE TITLE 12. BANKS AND BANKING CHAPTER 29--HOME MORTGAGE DISCLOSURE 1/2/2011 7:35:47 PM WKFS CompliSource January 2011 Page: 1 1/2/2011 7:35:47 PM HMDA 12 USC

Home Mortgage Disclosure Act UNITED STATES CODE TITLE 12. BANKS AND BANKING CHAPTER 29--HOME MORTGAGE DISCLOSURE 1/2/2011 7:35:47 PM WKFS CompliSource January 2011 Page: 1 1/2/2011 7:35:47 PM HMDA 12 USC

SAMPLE. 1 Bank Secrecy Act / Anti-Money Laundering. 2 E-Sign Act / Electronic Funds Transfer Act

1 Bank Secrecy Act / Anti-Money Laundering Summary 1 1 Purpose and History of the BSA 1 1 General Requirements of the BSA/AML Compliance Program 1 3 Money Laundering Defined 1 4 BSA / AML Violations 1

1 Bank Secrecy Act / Anti-Money Laundering Summary 1 1 Purpose and History of the BSA 1 1 General Requirements of the BSA/AML Compliance Program 1 3 Money Laundering Defined 1 4 BSA / AML Violations 1

Partial Exemptions from the Requirements of the Home Mortgage Disclosure Act under

BILLING CODE: 4810-AM-P BUREAU OF CONSUMER FINANCIAL PROTECTION 12 CFR Part 1003 RIN 3170-AA81 Partial Exemptions from the Requirements of the Home Mortgage Disclosure Act under the Economic Growth, Regulatory

BILLING CODE: 4810-AM-P BUREAU OF CONSUMER FINANCIAL PROTECTION 12 CFR Part 1003 RIN 3170-AA81 Partial Exemptions from the Requirements of the Home Mortgage Disclosure Act under the Economic Growth, Regulatory

Quarterly Report Mid-South Regulatory Compliance Group

Quarterly Report Mid-South Regulatory Compliance Group February 2016 Vol. 13 No. 1 HEADS UP ON FINAL HMDA RULE As we reported in November, the CFPB issued a final rule on October 15, 2015 amending Regulation

Quarterly Report Mid-South Regulatory Compliance Group February 2016 Vol. 13 No. 1 HEADS UP ON FINAL HMDA RULE As we reported in November, the CFPB issued a final rule on October 15, 2015 amending Regulation

A Look at Tennessee Mortgage Activity: A one-state analysis of the Home Mortgage Disclosure Act (HMDA) Data

Data") September, 2015 A Look at Tennessee Mortgage Activity: A one-state analysis of the Home Mortgage Disclosure Act (HMDA) Data 2004-2013 Hulya Arik, Ph.D. Tennessee Housing Development Agency TABLE OF CONTENTS

September, 2015 A Look at Tennessee Mortgage Activity: A one-state analysis of the Home Mortgage Disclosure Act (HMDA) Data 2004-2013 Hulya Arik, Ph.D. Tennessee Housing Development Agency TABLE OF CONTENTS

HMDA Update Nov. 13, Nov. 13, 2018 HMDA Update 1. Our Agenda Today

HMDA Update Panel Discussion: Ongoing Challenges & Solutions Nov. 13, 2018 HMDA Update 1 Our Agenda Today HMDA Partial Exemption Common Data Collection Exceptions Panel Discussion The future of HMDA Nov.

HMDA Update Panel Discussion: Ongoing Challenges & Solutions Nov. 13, 2018 HMDA Update 1 Our Agenda Today HMDA Partial Exemption Common Data Collection Exceptions Panel Discussion The future of HMDA Nov.

Home Mortgage Disclosure Act Report ( ) Submitted by Jonathan M. Cabral, AICP

Submitted by Jonathan M. Cabral, AICP") Home Mortgage Disclosure Act Report (2008-2015) Submitted by Jonathan M. Cabral, AICP Introduction This report provides a review of the single family (1-to-4 units) mortgage lending activity in Connecticut

Home Mortgage Disclosure Act Report (2008-2015) Submitted by Jonathan M. Cabral, AICP Introduction This report provides a review of the single family (1-to-4 units) mortgage lending activity in Connecticut

FEDERAL RESERVE SYSTEM. 12 CFR Part 203. [Regulation C; Docket No. R-1186] HOME MORTGAGE DISCLOSURE

![FEDERAL RESERVE SYSTEM. 12 CFR Part 203. [Regulation C; Docket No. R-1186] HOME MORTGAGE DISCLOSURE](/thumbs/89/97922501.jpg "FEDERAL RESERVE SYSTEM. 12 CFR Part 203. [Regulation C; Docket No. R-1186] HOME MORTGAGE DISCLOSURE") FEDERAL RESERVE SYSTEM 12 CFR Part 203 [Regulation C; Docket No. R-1186] HOME MORTGAGE DISCLOSURE AGENCY: Board of Governors of the Federal Reserve System. ACTION: Request for comment on revised formats

FEDERAL RESERVE SYSTEM 12 CFR Part 203 [Regulation C; Docket No. R-1186] HOME MORTGAGE DISCLOSURE AGENCY: Board of Governors of the Federal Reserve System. ACTION: Request for comment on revised formats

Revised HMDA Reporting Overview, Implementation and Planning March 2017

Revised HMDA Reporting Overview, Implementation and Planning March 2017 Kathy Keller, Managing Director, Regulatory Compliance, Newbold Advisors, LLC NewboldAdvisors.com Agenda Overview of the New HMDA

Revised HMDA Reporting Overview, Implementation and Planning March 2017 Kathy Keller, Managing Director, Regulatory Compliance, Newbold Advisors, LLC NewboldAdvisors.com Agenda Overview of the New HMDA

Please stand by, the presentation will begin shortly. Your phones have been muted. If you re using the speakers on your PC you don t need to call in.

Please stand by, the presentation will begin shortly. Your phones have been muted. If you re using the speakers on your PC you don t need to call in. While you are waiting, you may download the presentation

Please stand by, the presentation will begin shortly. Your phones have been muted. If you re using the speakers on your PC you don t need to call in. While you are waiting, you may download the presentation

Action Taken. Boot Camp 360 Series Presented by Kimberly Lundquist

Action Taken Boot Camp 360 Series Presented by Kimberly Lundquist Action Taken During the Pre-Application Process, most of the laws pertaining to real estate lending will come into play. We must be careful

Action Taken Boot Camp 360 Series Presented by Kimberly Lundquist Action Taken During the Pre-Application Process, most of the laws pertaining to real estate lending will come into play. We must be careful

HMDA 2018 (Correspondent)

") HMDA 2018 (Correspondent) Legal Disclaimer The materials and information provided during this presentation is limited to the discussion of PRMG s policies with respect to the amended Home Mortgage Disclosure

HMDA 2018 (Correspondent) Legal Disclaimer The materials and information provided during this presentation is limited to the discussion of PRMG s policies with respect to the amended Home Mortgage Disclosure

Loan Growth and Compliance Pitfalls

Loan Growth and Compliance Pitfalls presented by LOANLINER Compliance Information provided in this presentation, including all materials, should not be construed as legal services, legal advice, or in

Loan Growth and Compliance Pitfalls presented by LOANLINER Compliance Information provided in this presentation, including all materials, should not be construed as legal services, legal advice, or in

FREQUENTLY ASKED QUESTIONS ABOUT THE NEW HMDA DATA. General Background

Federal Reserve Bank of New York Statistics Function March 31, 2005 FREQUENTLY ASKED QUESTIONS ABOUT THE NEW HMDA DATA General Background 1. What is the Home Mortgage Disclosure Act (HMDA)? HMDA, enacted

Federal Reserve Bank of New York Statistics Function March 31, 2005 FREQUENTLY ASKED QUESTIONS ABOUT THE NEW HMDA DATA General Background 1. What is the Home Mortgage Disclosure Act (HMDA)? HMDA, enacted

Filing instructions guide for HMDA data collected in 2017

August 07 Filing instructions guide for HMDA data collected in 07 OMB Control #70-0008 Version log The following is a version log that tracks the history of this document and its updates: Date Version

August 07 Filing instructions guide for HMDA data collected in 07 OMB Control #70-0008 Version log The following is a version log that tracks the history of this document and its updates: Date Version

SUMMARY: The Bureau of Consumer Financial Protection (Bureau) is amending Regulation

is amending Regulation") BILLING CODE: 4810-AM-P BUREAU OF CONSUMER FINANCIAL PROTECTION 12 CFR Part 1003 [Docket Nos. CFPB 2017 0010; CFPB 2017 0021] RIN 3170 AA64; 3170 AA76 Home Mortgage Disclosure (Regulation C), Final Rule

BILLING CODE: 4810-AM-P BUREAU OF CONSUMER FINANCIAL PROTECTION 12 CFR Part 1003 [Docket Nos. CFPB 2017 0010; CFPB 2017 0021] RIN 3170 AA64; 3170 AA76 Home Mortgage Disclosure (Regulation C), Final Rule

Q: Any discussion regarding tolerance violations with all the new additional fields?

Q & A The following are questions posed by attendees at the August 19, 2014 QuestSoft webinar that addressed the new HMDA proposal from the CFPB, and the answers from Leonard Ryan of QuestSoft. DISCLAIMER:

Q & A The following are questions posed by attendees at the August 19, 2014 QuestSoft webinar that addressed the new HMDA proposal from the CFPB, and the answers from Leonard Ryan of QuestSoft. DISCLAIMER:

CFPB Consumer Laws and Regulation

Secure and Fair Enforcement for Mortgage Licensing Act 1 The Secure and Fair Enforcement for Mortgage Licensing Act of 2008 2 () was enacted on July 30, 2008, and mandates a nationwide licensing and registration

Secure and Fair Enforcement for Mortgage Licensing Act 1 The Secure and Fair Enforcement for Mortgage Licensing Act of 2008 2 () was enacted on July 30, 2008, and mandates a nationwide licensing and registration

Executive Summary of the Home Mortgage Disclosure Act (Regulation C), Final Rule

, Final Rule") 1700 G Street NW, Washington, DC 20552 August 24, 2017 Executive Summary of the Home Mortgage Disclosure Act (Regulation C), Final Rule The Consumer Financial Protection Bureau (Bureau) has issued a final

1700 G Street NW, Washington, DC 20552 August 24, 2017 Executive Summary of the Home Mortgage Disclosure Act (Regulation C), Final Rule The Consumer Financial Protection Bureau (Bureau) has issued a final

Mortgage Lending Compliance Issues Session 1. Higher Priced and High-Cost Mortgages

Mortgage Lending Compliance Issues Session 1 Higher Priced and High-Cost Mortgages Today s Topics Learn the definitions of Higher Priced and High Cost Mortgages and how to test to determine if you are

Mortgage Lending Compliance Issues Session 1 Higher Priced and High-Cost Mortgages Today s Topics Learn the definitions of Higher Priced and High Cost Mortgages and how to test to determine if you are

Filing instructions guide for HMDA data collected in 2018

September 2018 Filing instructions guide for HMDA data collected in 2018 OMB Control #3170-0008 Version log The following is a version log that tracks the history of this document and its updates: Date

September 2018 Filing instructions guide for HMDA data collected in 2018 OMB Control #3170-0008 Version log The following is a version log that tracks the history of this document and its updates: Date

Facing Today s Real Estate Regulations

Proudly Sponsored by Facing Today s Real Estate Regulations Presented by Don Braspenninckx Day, June 11, 2016 1:30 p.m. 1 Introduction Numerous regulatory changes in the real estate industry within last

Proudly Sponsored by Facing Today s Real Estate Regulations Presented by Don Braspenninckx Day, June 11, 2016 1:30 p.m. 1 Introduction Numerous regulatory changes in the real estate industry within last

Procedures for Denying Loans at the Branch Level (Updated )

") Procedures for Denying Loans at the Branch Level (Updated 2-22-2018) Applies to Loans in the Active Pipeline as well as Loans in the Pre-Approval Pipeline -----------------------------------------------------------------------------------------------

Procedures for Denying Loans at the Branch Level (Updated 2-22-2018) Applies to Loans in the Active Pipeline as well as Loans in the Pre-Approval Pipeline -----------------------------------------------------------------------------------------------

Expanded NMLS Mortgage Call Report Field Definitions & Instructions Effective for Q Reporting

Expanded NMLS Mortgage Call Report Field Definitions & Instructions Effective for Q1 2016 Reporting This document provides field definitions, instructions and data formatting requirements for completing

Expanded NMLS Mortgage Call Report Field Definitions & Instructions Effective for Q1 2016 Reporting This document provides field definitions, instructions and data formatting requirements for completing

NCUA s Fair Lending Compliance Program

Office of Consumer Protection NCUA s Fair Lending Compliance Program Virginia Credit Union League Fall Compliance Conference Williamsburg, VA October 16, 2013 OCP Organization 2 Division of Consumer Affairs

Office of Consumer Protection NCUA s Fair Lending Compliance Program Virginia Credit Union League Fall Compliance Conference Williamsburg, VA October 16, 2013 OCP Organization 2 Division of Consumer Affairs

Presentation Topics. Changing Data Requirements Will Effect. Census data update and implications for CRA, HMDA and Fair Lending

Changing Data Requirements Will Effect the CRA and Fair Lending Environment Prepared for the 2012 National Community Reinvestment Conference by Glenn Canner March 28, 2012 The views expressed are those

Changing Data Requirements Will Effect the CRA and Fair Lending Environment Prepared for the 2012 National Community Reinvestment Conference by Glenn Canner March 28, 2012 The views expressed are those

With so much change, be sure to stay up to date!

With so much change, be sure to stay up to date! Glory LeDu Glory.LeDu@mcul.org Sarah Stevenson Sarah.Stevenson@mcul.org Barb Boyd Barb.Boyd@cusolutionsgroup.com Your Crazy Compliance Peeps Agenda What

With so much change, be sure to stay up to date! Glory LeDu Glory.LeDu@mcul.org Sarah Stevenson Sarah.Stevenson@mcul.org Barb Boyd Barb.Boyd@cusolutionsgroup.com Your Crazy Compliance Peeps Agenda What

9/30/2014. TILA-RESPA Integrated Disclosures. Outlook Live Webinar- October 1, Presented by the Consumer Financial Protection Bureau

Outlook Live Webinar- October 1, 2014 TILA-RESPA Integrated Disclosures Presented by the Consumer Financial Protection Bureau Visit us at www.consumercomplianceoutlook.org Disclaimer The Bureau issued

Outlook Live Webinar- October 1, 2014 TILA-RESPA Integrated Disclosures Presented by the Consumer Financial Protection Bureau Visit us at www.consumercomplianceoutlook.org Disclaimer The Bureau issued

Filing instructions guide for HMDA data collected in 2018

August 2017 Filing instructions guide for HMDA data collected in 2018 OMB Control #3170-0008 Version log The following is a version log that tracks the history of this document and its updates: Date Version

August 2017 Filing instructions guide for HMDA data collected in 2018 OMB Control #3170-0008 Version log The following is a version log that tracks the history of this document and its updates: Date Version

CFPB s Final Mortgage Regulations: Ability-to-Repay and Qualified Mortgage Rules March 6, E. Andrew Keeney, Esq. Kaufman & Canoles, P.C.

CFPB s Final Mortgage Regulations: Ability-to-Repay and Qualified Mortgage Rules March 6, 2013 E. Andrew Keeney, Esq. Kaufman & Canoles, P.C. Ability-to-Repay and Qualified Mortgage Rules E. Andrew Keeney,

CFPB s Final Mortgage Regulations: Ability-to-Repay and Qualified Mortgage Rules March 6, 2013 E. Andrew Keeney, Esq. Kaufman & Canoles, P.C. Ability-to-Repay and Qualified Mortgage Rules E. Andrew Keeney,

CFPB Consumer Laws and Regulations

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage

S.2155 Implementation The Latest HMDA Changes

S.2155 Implementation The Latest HMDA Changes The webinar will begin at the top of the hour. You may download the presentation at: www.questsoft.com/hmdachanges S.2155 Implementation The Latest HMDA Changes

S.2155 Implementation The Latest HMDA Changes The webinar will begin at the top of the hour. You may download the presentation at: www.questsoft.com/hmdachanges S.2155 Implementation The Latest HMDA Changes

S DODD-FRANK ACT REVISIONS REGULATORY RELIEF

July 27, 2018 Vol. XXXV, No. 16 S. 2155 DODD-FRANK ACT REVISIONS REGULATORY RELIEF I. INTRODUCTION President Trump recently signed Senate Bill 2155, the Economic Growth, Regulatory Relief and Consumer

July 27, 2018 Vol. XXXV, No. 16 S. 2155 DODD-FRANK ACT REVISIONS REGULATORY RELIEF I. INTRODUCTION President Trump recently signed Senate Bill 2155, the Economic Growth, Regulatory Relief and Consumer

HMDA LAR Fields Effective 1/1/2018 Comparison with Current HMDA Fields - Updated 7/17/2016 Current Field New/Revised Field

Current New/Revised Record Identifier Record Identifier 2 2 software may enter this value or bank will enter on every line of LAR this entry is on every line No change Respondent ID Value depends upon

Current New/Revised Record Identifier Record Identifier 2 2 software may enter this value or bank will enter on every line of LAR this entry is on every line No change Respondent ID Value depends upon

TIPS BULLETIN #13-17

TIPS BULLETIN #13-17 To: Subject: All Credit Unions Ability to Repay & Qualified Mortgage Standards under the Truth in Lending Act (Regulation Z) The material in this publication is provided for educational

TIPS BULLETIN #13-17 To: Subject: All Credit Unions Ability to Repay & Qualified Mortgage Standards under the Truth in Lending Act (Regulation Z) The material in this publication is provided for educational

Fewer Applications, Falling Denial Rates

August 2016 Fewer Applications, Falling Denial Rates Identifying Home Loan Trends in Tennessee from Home Mortgage Disclosure Act (HMDA) Data Hulya Arik, Ph.D. Tennessee Housing Development Agency TABLE

August 2016 Fewer Applications, Falling Denial Rates Identifying Home Loan Trends in Tennessee from Home Mortgage Disclosure Act (HMDA) Data Hulya Arik, Ph.D. Tennessee Housing Development Agency TABLE

TO: Freddie Mac Sellers and Servicers November 15,

TO: Freddie Mac Sellers and Servicers November 15, 2013 2013-23 SUBJECTS This Single-Family Seller/Servicer Guide ( Guide ) Bulletin updates and revises our selling and Servicing requirements, including:

TO: Freddie Mac Sellers and Servicers November 15, 2013 2013-23 SUBJECTS This Single-Family Seller/Servicer Guide ( Guide ) Bulletin updates and revises our selling and Servicing requirements, including:

CFPB Consumer Laws and Regulations

Homeowners Protection Act (PMI Cancellation Act) 1 The Homeowners Protection Act of 1998 ( or PMI Cancellation Act, or Act) was signed into law on July 29, 1998, became effective on July 29, 1999, and

Homeowners Protection Act (PMI Cancellation Act) 1 The Homeowners Protection Act of 1998 ( or PMI Cancellation Act, or Act) was signed into law on July 29, 1998, became effective on July 29, 1999, and

Consumer Financial Protection & Owner Financing

Consumer Financial Protection & Owner Financing The Dodd-Frank Wall Street Reform and Consumer Protection Act ( Dodd-Frank ) introduced a host of new regulations designed to protect consumers and avoid

Consumer Financial Protection & Owner Financing The Dodd-Frank Wall Street Reform and Consumer Protection Act ( Dodd-Frank ) introduced a host of new regulations designed to protect consumers and avoid

Washington Bankers Association S.2155: Regulatory Reform Leah M. Hamilton, JD -1-

Washington Bankers Association S.2155: Regulatory Reform 2018 Leah M. Hamilton, JD 2- What You Will Learn Summary of key impacts of S.2155 Title I Improving Consumer Access to Mortgage Credit Title II

Washington Bankers Association S.2155: Regulatory Reform 2018 Leah M. Hamilton, JD 2- What You Will Learn Summary of key impacts of S.2155 Title I Improving Consumer Access to Mortgage Credit Title II

CUNA Short Summary of the Dodd-Frank Wall Street Reform and Consumer Protection Act (H.R. 4173; Public Law Number ) August 2, 2010

August 2, 2010") CUNA Short Summary of the Dodd-Frank Wall Street Reform and Consumer Protection Act (H.R. 4173; Public Law Number 111-203) August 2, 2010 Here is a short summary highlighting the provisions of the Dodd-Frank

CUNA Short Summary of the Dodd-Frank Wall Street Reform and Consumer Protection Act (H.R. 4173; Public Law Number 111-203) August 2, 2010 Here is a short summary highlighting the provisions of the Dodd-Frank

Assistance Program: City of Tuscaloosa Home Purchase Assistance Program Code: DALTUSHPP

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

AMENDMENTS TO THE CFPB MORTGAGE SERVICING REGULATIONS EFFECTIVE OCTOBER 19, 2017 NATIONAL FAIR HOUSING ALLIANCE WEBINAR PRESENTATION OCTOBER 18, 2017

AMENDMENTS TO THE CFPB MORTGAGE SERVICING REGULATIONS EFFECTIVE OCTOBER 19, 2017 NATIONAL FAIR HOUSING ALLIANCE WEBINAR PRESENTATION OCTOBER 18, 2017 1 Diane Cipollone, Esq. Consultant to National Fair

AMENDMENTS TO THE CFPB MORTGAGE SERVICING REGULATIONS EFFECTIVE OCTOBER 19, 2017 NATIONAL FAIR HOUSING ALLIANCE WEBINAR PRESENTATION OCTOBER 18, 2017 1 Diane Cipollone, Esq. Consultant to National Fair

CFPB: The New Closing Process

CFPB: The New Closing Process Course Objective: Relate the new CFPB Rules to what the real estate transaction process could look like after August 1, 2015 (CFPB revised date: October 3, 2015) INTRODUCTION

CFPB: The New Closing Process Course Objective: Relate the new CFPB Rules to what the real estate transaction process could look like after August 1, 2015 (CFPB revised date: October 3, 2015) INTRODUCTION

Regulation X Real Estate Settlement Procedures Act

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 (RESPA) (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders,

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 (RESPA) (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders,

HMDA INPUT AND REQUIREMENTS. Updated: 3/16/2017, S. Noble

HMDA INPUT AND REQUIREMENTS Updated: 3/16/2017, S. Noble 1 What is HMDA?? The Home Mortgage Disclosure Act (HMDA) was enacted by Congress in 1975 and was implemented by the Federal Reserve Board s Regulation

HMDA INPUT AND REQUIREMENTS Updated: 3/16/2017, S. Noble 1 What is HMDA?? The Home Mortgage Disclosure Act (HMDA) was enacted by Congress in 1975 and was implemented by the Federal Reserve Board s Regulation

HMDA: Haven or Havoc. Cindy Prince, Presenter December 5, 6 & 7, 2017 Assisted by Rachelle Dekker and Matt Goble

HMDA: Haven or Havoc Cindy Prince, Presenter December 5, 6 & 7, 2017 Assisted by Rachelle Dekker and Matt Goble Recap Day One 2 1. Annual expectations 2. Two proposals and a new final rule 3. Key definitions

HMDA: Haven or Havoc Cindy Prince, Presenter December 5, 6 & 7, 2017 Assisted by Rachelle Dekker and Matt Goble Recap Day One 2 1. Annual expectations 2. Two proposals and a new final rule 3. Key definitions

WORRIED. about Foreclosure? HAFA MAY BE ABLE TO HELP HOME AFFORDABLE FORECLOSURE ALTERNATIVES PROGRAM (HAFA)

") WORRIED about Foreclosure? HAFA MAY BE ABLE TO HELP HOME AFFORDABLE FORECLOSURE ALTERNATIVES PROGRAM (HAFA) About HAFA Keeping families in their homes is a top priority for REALTORS. While there are loan

WORRIED about Foreclosure? HAFA MAY BE ABLE TO HELP HOME AFFORDABLE FORECLOSURE ALTERNATIVES PROGRAM (HAFA) About HAFA Keeping families in their homes is a top priority for REALTORS. While there are loan

Amendments to Equal Credit Opportunity Act (Regulation B) Ethnicity and Race

Ethnicity and Race") BILLING CODE: 4810-AM-P BUREAU OF CONSUMER FINANCIAL PROTECTION 12 CFR Part 1002 [Docket No. CFPB-2017-0009] RIN 3170-AA65 Amendments to Equal Credit Opportunity Act (Regulation B) Ethnicity and Race Information

BILLING CODE: 4810-AM-P BUREAU OF CONSUMER FINANCIAL PROTECTION 12 CFR Part 1002 [Docket No. CFPB-2017-0009] RIN 3170-AA65 Amendments to Equal Credit Opportunity Act (Regulation B) Ethnicity and Race Information

Section Ability to Repay (ATR) (c)(1) and Qualified Mortgage (QM) (e), (f)

(c)(1) and Qualified Mortgage (QM) (e), (f)") Section 1026.43 Ability to Repay (ATR) 1026.43(c)(1) and Qualified Mortgage (QM) 1026.43(e), (f) This section applies to any consumer credit transaction that is secured by a dwelling, as defined in 1026.2(a)(19),

Section 1026.43 Ability to Repay (ATR) 1026.43(c)(1) and Qualified Mortgage (QM) 1026.43(e), (f) This section applies to any consumer credit transaction that is secured by a dwelling, as defined in 1026.2(a)(19),

Interagency Consumer Laws and Regulations

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage

MHA Reason Codes and Descriptions

s and s MHA Reason Code 1 Ineligible Mortgage Loan is not eligible for modification under the MHA program because it does not meet one or more of the following basic program eligibility criteria: Mortgage

s and s MHA Reason Code 1 Ineligible Mortgage Loan is not eligible for modification under the MHA program because it does not meet one or more of the following basic program eligibility criteria: Mortgage

MBBA-NH & MAMP. Compliance Conference. April 19, 2017

MBBA-NH & MAMP Compliance Conference April 19, 2017 Agenda HMDA Overview Readiness Steps HMDA Expansion Fields 2 New HMDA Rule Summary Changes to Home Mortgage Disclosure: Regulation C Types of institutions

MBBA-NH & MAMP Compliance Conference April 19, 2017 Agenda HMDA Overview Readiness Steps HMDA Expansion Fields 2 New HMDA Rule Summary Changes to Home Mortgage Disclosure: Regulation C Types of institutions

Delivered in partnership with your local title agency

Delivered in partnership with your local title agency titlesinsured 1.877.439.4910 About this Manual In an effort to provide a thorough condensed training reference, this manual was created based on the

Delivered in partnership with your local title agency titlesinsured 1.877.439.4910 About this Manual In an effort to provide a thorough condensed training reference, this manual was created based on the

BUSINESS LOAN APPLICATION COMPANY INFORMATION

BUSINESS LOAN APPLICATION Thank you for considering your Credit Union for your business borrowing needs. Your Credit Union will be utilizing the services of Cooperative Business Services, LLC ("CBS") to

BUSINESS LOAN APPLICATION Thank you for considering your Credit Union for your business borrowing needs. Your Credit Union will be utilizing the services of Cooperative Business Services, LLC ("CBS") to

Assistance Program: City of Austin Shared Equity Down Payment Assistance Code: DTXSHARED

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

Fully Amortizing Payment A periodic payment of principal and interest that will fully repay the loan amount over the loan term.

Section 12.7: : Regulation Z Ability to Repay and Qualified Mortgages Summary On January 10, 2013, Regulation Z was amended to require creditors to make a reasonable, good faith determination of a consumer

Section 12.7: : Regulation Z Ability to Repay and Qualified Mortgages Summary On January 10, 2013, Regulation Z was amended to require creditors to make a reasonable, good faith determination of a consumer

Supplemental Directive October 18, 2013

Supplemental Directive 13-09 October 18, 2013 Making Home Affordable Program CFPB Mortgage Servicing Regulations In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Supplemental Directive 13-09 October 18, 2013 Making Home Affordable Program CFPB Mortgage Servicing Regulations In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

THE TRID RULE: IMPACT AND CONSEQUENCES ON THE RESIDENTIAL MORTGAGE LENDING MARKET. Christopher W. Smart

THE TRID RULE: IMPACT AND CONSEQUENCES ON THE RESIDENTIAL MORTGAGE LENDING MARKET Christopher W. Smart Introduction and Background Residential mortgage lenders have long been required to disclose to their