A Future for Community Credit Unions

|

|

|

- Gerald Washington

- 6 years ago

- Views:

Transcription

1 A Future for Community Credit Unions Martin D. Eakes September 24, 2015 National Federation of CDCUs, Phoenix, Arizona Ownership and Economic Opportunity for All

2 Goals of this presentation Brief overview of Self-Help Credit Union and its key affiliate organizations Credit union consolidation over next 20 years (or less) Key goals/numbers for credit union sustainability Passion for the mission: economic equality and justice 2

3 Self-Help Overview 3

4 About Self-Help and CRL Self-Help Credit Union is a $670 million NC chartered credit union, 58,000 members, NC focused (1984). Self-Help Ventures Fund is a $1 billion community development loan fund: home loans and new markets (1984). Self-Help Federal Credit Union is a $600 million federal credit union, 61,000 members, CA and Chicago (2008). Center for Responsible Lending is an affiliated nonprofit, nonpartisan research and policy organization dedicated to protecting homeownership and family wealth by working to eliminate abusive financial practices (2002). 4

Lending Methodology SH Internal Capacity Mission & Impact (Front")

5 Self-Help s Business Model Long-Term Sustainability Capital Grants Mission & Impact Wealth-Building, Civil Rights, Social Justice Movements Financial Sustainability (Back Wheel) Lending Methodology SH Internal Capacity Mission & Impact (Front Wheel) 5

6 Self-Help s Mission Our Mission Creating and protecting ownership and economic opportunity for all, especially people of color, women, rural residents and low-wealth families and communities. 6

7 Our Story Humble Beginning Founded in 1980 in Durham, NC Originally created to encourage and support worker-owned cooperative businesses First capital in Self-Help Credit Union was $77 donation from a bake sale in late

8 Self-Help Now $1.8 billion in total assets $942 million in total deposits $508 million in net worth Serving 117,000 borrowers, depositors, and members $6.8 billion invested in more than 102,000 families, individuals, businesses and nonprofits since staff working in NC, DC, CA, and Chicago ~73% of our staff are women; ~52% are people of color. More than 60% of staff directly serve credit union members 8

9 SHFCU Growth (California & Chicago) Second Federal Savings 11/2012 2/2013 $150MM; 3 branches 9

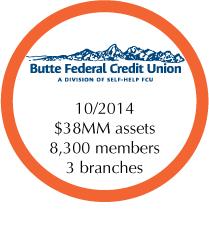

10 SHCU Growth (North Carolina) 10/2013 $61 MM assets 10,600 members 7 branches 1/2010 $46 MM assets 9,700 members 1 branch 9/2006 $2 MM assets 650 members 1 branch 4/2014 $20 MM assets 8,600 members 4 branches 3/2004 $9 MM assets 4,100 members 1 branch 11/2009 $44 MM assets 7,000 members 3 branches 9/2006 $7 MM assets 3,000 members 1 branch 12/2006 $13 MM assets 3,000 members 1 branch 5/2010 $11 MM assets 1,700 members 1 branches 10

11 American Tobacco Campus $40 million dollar loan One million sq. ft. redevelopment of mixed use space 11

12 Revitalizing Downtowns 12

13 Affordable Homeownership Originated over 6,300 home loans totaling $527 million Provided $4.5 billion in financing to support more than 50,000 homebuyers through Self-Help Home Loan Secondary Market Program 13

14 Revolution Mill 14

15 Greening Food Deserts Renaissance, a 40,000 SF neighborhood shopping center in Greensboro, NC, sat vacant of a grocery store for 15+ years Self-Help plans to complete a $5 million renovation project and recruit tenants such as a Co-op grocery store, independent pharmacy, and other neighborhood retail 15

16 Solar Lending Self-Help has financed over $100 million of Solar Loan Development in NC alone. Self-Help has supported the development and expansion of 37 Solar Loan projects, across 20 of NC s counties. 16

17 Self-Help Structure and Principles Charitable civil rights nonprofit joined at the hip with federally insured depository credit union Equity shares and secondary capital Advocacy voice for the underserved: families of color, women, immigrants, rural communities Always do what s right for members, families, and communities Two tithing principles Tithe to the future Tithe to the movement Equal balance between social justice mission and financial sustainability 17

18 Some unlikely successes Home loans to un-bankable African American and Latino families Secondary capital - $50 million to grow SHFCU $5 billion home loan secondary market from 30 national lenders Helped design the CDFI Fund and legislation passed in 1994 Commercial loans $200+ million of NMTC business and facility loans $100 million of loans to child care centers and charter schools $100+ million of solar energy loans to power 60,000 homes $150+ million of direct real estate development projects Outreach and lending to dreamers and deferred action immigrants Purchase of $140 million and 3 branch failed bank in Chicago 40 CRL advocates and researchers helped design CFPB and model legislation against payday lending and abusive mortgages 18

19 Credit Union Consolidation 19

20 1994 to 2014: Half as many credit unions 50% more credit union members 1994 Count Members Assets % of total ($) Federal 7,498 40,837, ,528,894,599 62% State 4,494 24,294, ,000,969,044 36% Priv Insur 209 1,106,372 5,314,944,535 2% 12,201 66,238, ,844,808, % 2014 Count Members Assets % of total ($) Federal 3,927 53,396, ,140,433,294 52% State 2,346 45,888, ,042,131,739 46% Priv Insur 129 1,229,660 13,939,921,196 1% 6, ,514,100 1,136,122,486, % 20

21 1994 to 2014: Larger credit unions had massive growth in % of members and assets 1994 Count Members Assets <$500 mm* 12,088 53,272, ,421,641,213 >$500 mm* ,966,427 81,423,166,965 % 0.9% 19.6% 27.6% *$500 mm is equivalent to $340 mm in 1994 dollars 2014 Count Members Assets <$500 mm 5,942 38,909, ,777,580,287 >$500 mm ,604, ,344,905,942 % 7.2% 61.3% 69.4% Growth in share 8x 3x 2.5x 21

22 2014 to 2034: Larger credit unions will dominate % of members and assets 2014 Count Members Assets Av Assets/ CU Totals 6, ,514,100 1,136,122,486, ,463,681 <$500 mm 5,942 38,909, ,777,580,287 58,528,708 >$500 mm ,604, ,344,905,942 1,713,793,274 % for large 7.2% 61.3% 69.4% 2034 Count Members Assets Av Assets/ CU 20 yr change -40% +50% +225% (50% cpi) Totals 3, ,771,150 2,556,275,594, ,488,804 <$500 mm* 3,265 15,077, ,627,559,402 87,507,723 >$500 mm* ,694,035 2,300,648,034,614 2,500,704,385 % for large 24% 90%+ 90%+ Growth in share 3x.33x 30% *$500 mm will be equivalent to $750 mm - $900 mm in 2034 dollars 22

23 Possible implications for the movement The voice of the small credit unions that survive will be marginalized. CUNA/NAFCU and Leagues will be dominated by large credit unions. Just a fact. Trade groups will focus on federal and state policy advocacy, and to lesser degree, face-to-face peer networking among large credit unions If trades do not adapt soon, new credit union associations will emerge Smaller credit unions must Come Together, Right Now CUSOs for core processing, mobile, info security, mortgage, and ALM (The alternative Beatles song is: Let It Be ) 23

24 Sustainability of Community Credit Unions 24

25 Sustainability keys for community credit unions Expand assets per member!! Home loans for 50% of loan portfolio! Cannot survive with car loans only 90% of credit unions >$75 mm already offer home mortgage loans (15% at CUs of $5 to $10 million) Mobile phone technology is essential 25

26 Typical view of larger CU expense advantage <$5 mm $5-$20 mm $20-$100 mm $100 mm+ 26

27 Small credit unions serve more members / FTE Number of Members Served/ FTE 2014 year end call report data (credit union size in millions) ,000 1,000-2,000 2,000-5,000 5,000-10,000 27

28 Spread operating costs over more assets!! Operating Expense Comparisons (based on 12/31/14 call reports) $$/ Avg Loans/ Mem/ Assets Mems RoA OpEx Mem Loan Assets FTE Fees NW% NW SECU $29 B 1,900, % 1.7% 15,083 21,574 57% % 7.97% $1.9 B Self-Help (includes affiliates) $1.8 B 120, % 2.5% 11,570 21,367 59% % 13.16% $508 M CU #1 (pre-merger 2008) $43 mm 7, % 4.4% 5,457 7,533 72% % 6.20% $3 M CU #2 (pre-merger 2012) $60 mm 11, % 5.1% 5,151 7,636 66% % 13.80% $7.9 M CU #3 CDCU $36 mm 9, % 6.8% 4,021 7,687 75% % 15.30% $5.6 M 28

29 How to expand assets to $10k per member Target small % of older or Robin Hood members w larger savings 2% of members at $250k increases avg by $5k 5% of members at $100k increases avg by $5k Loans, deposits, net worth, and expertise must be balanced Loans come first -- without sufficient member loan demand, more deposits are harmful (See section on home loans) Must have expertise to increase loans responsibly Must have net worth to support doubling of deposits Can grow assets at same rate as ROE w/o decreasing net worth Figure out how to raise rates on your 1 year CD Regulators often get this dead wrong and push for lower CD rates If operating expense is too high and assets/member too low, the solution is to spread expenses across a larger asset base 29

30 Challenges to home lending by credit unions Cannot break even putting Fannie/Freddie-eligible home loans in portfolio Small lenders cannot break even with home loan servicing business, but important for member relationship Niches are credit-blemished borrowers, jumbo loans, and ARM borrowers loans not covered by GSEs ALM and interest rate swaps needed to serve low and moderate income borrowers, who prefer fixed rate loans Regulations for HMDA, RESPA, HOEPA, ECOA, Fair Housing, Dodd-Frank, SAFE Act for mortgage originators are COMPLEX 30

31 How to make home loans 50% of total loans CU portfolio target is only 2.5% 3% of its members! This is true even for $30+ billion NC SECU If $10k av assets/ member, it takes 20 members to support one home loan of $200k Thus, only possible to fund 5% of members even if 100% of credit union assets used for portfolio home loans, which is NOT prudent At goal of 50% of assets, home loan target is 2.5% of total members Must come together with other credit unions and CUSOs to handle originations, ALM, legal compliance, mortgage loan servicing And yet CDCU and Community CUs cannot survive without portfolio home lending program! $200k home loan vs $20k car loan: 10x difference 8 yr av life for home loan vs 2 yr av life for car loan: 4x difference 40 times greater impact on balance sheet for home vs car loan If doubling assets/ member, home loans are how to deploy 31

32 Mobile phone banking is essential Mobile access is great cost equalizer for small cu s Natural outcome of two technology trends Cost of MIPS (CPU speed) trending toward $0 Cost of bandwidth trending toward $0 Hence, EVERYONE will have a smart phone Adopted faster than ANY other banking innovation Faster than ATMs, checking, credit, debit cards B of A, Chase report 25% reduction in branch transactions in just two years. 32

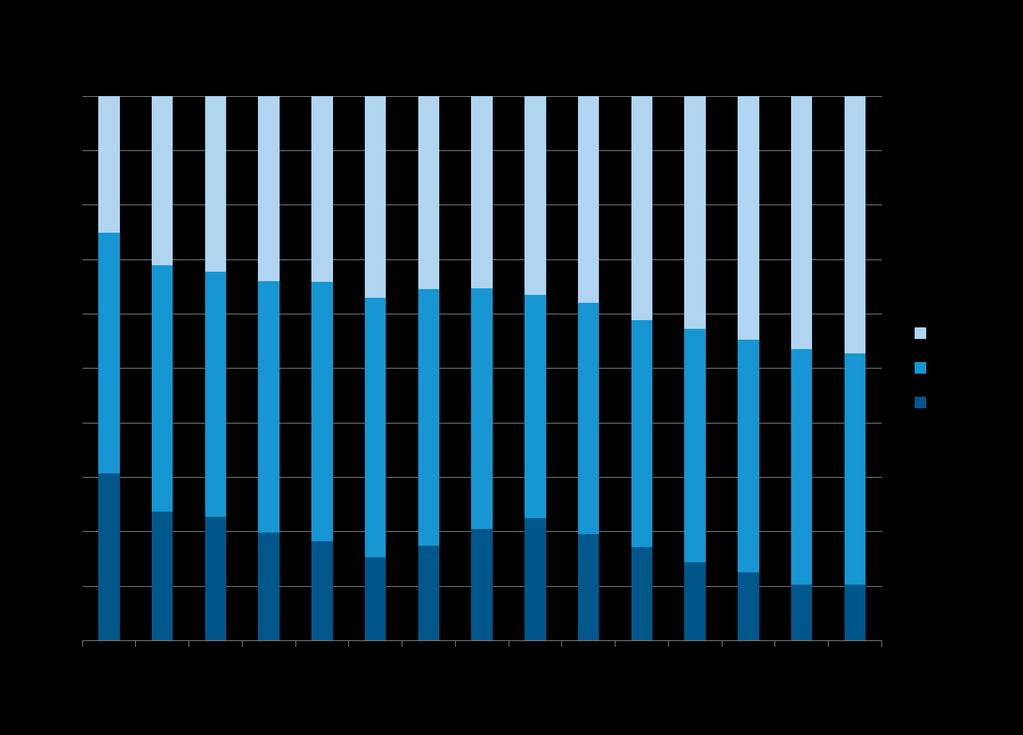

33 Mission the front wheel 33

34 Mission Overview Homeownership by race Self-Help Home Loan Secondary Market (appendix) Abusive subprime lending Economic inequality 34

35 Percent Homeownership Rates by Race & Ethnicity 80 Average Homeownership Rates by Race and Ethnicity U.S. Average Non-Hispanic White Black All Other Races Hispanic (of any race) Source: U.S. Census Bureau 35

36 36 36

37 Minority Household Growth Joint Center for Housing Studies & US Census Bureau 37

38 SH Home Loan Purchases Median Net Worth (2005 vs 2012) Net Worth 2005 Net Worth 2012 Source: Center for Community Capital, Low and Moderate income Homeownership and Wealth Creation

39 Higher cost 1 st lien total loans, 2005 HMDA # Higher cost % of total African American 388,471 52% Latino 375,889 40% White 1,214,003 19% 39

40 40 40

41 U.S. Single Family Market Cycles (1976 Q Q2) Note: Percentage values in boxes represent real cumulative changes during shaded area Source: Consumer Price Index (CPI) & Case-Schiller as of June 30,

42 Jan-1976 Jan-1977 Jan-1978 Jan-1979 Jan-1980 Jan-1981 Jan-1982 Jan-1983 Jan-1984 Jan-1985 Jan-1986 Jan-1987 Jan-1988 Jan-1989 Jan-1990 Jan-1991 Jan-1992 Jan-1993 Jan-1994 Jan-1995 Jan-1996 Jan-1997 Jan-1998 Jan-1999 Jan-2000 Jan-2001 Jan-2002 Jan-2003 Jan-2004 Jan-2005 Jan-2006 Jan-2007 Jan-2008 Jan-2009 Jan-2010 Jan-2011 Jan-2012 Jan-2013 Jan-2014 U.S. Single Family Market Cycles (1976 Q Q2) 16% 12-month Rolling Growth Rate in Case-Schiller U.S. National Home Price Index 12% 8% Real Nominal 4% 0% +19% +20% +58% +13% -13% -39% -4% -15% -8% -12% Real Growth Rate Nominal Growth Rate -16% Note: Percentage values in boxes represent real cumulative changes during shaded area Source: Consumer Price Index (CPI) & Case-Schiller Index as of June 30,

43 National Income Inequality 43

44 Thomas Piketty, Top 10% Share of U.S. National Income

45

46 Addendum Slides 46

47 National Income Inequality 47

48 Thomas Piketty, Top 1% Wealth Holdings since 1810

49 Self-Help Affiliated Organizations Self-Help Credit Union SHCU is a member-owned, federally-insured, NC-chartered (1983) CU, originally launched to raise deposits from members to make commercial, consumer, and home loans. To expand our impact and provision of services, in 2006, SHCU began merging in NC credit unions. SHCU has merged in nine credit unions that have served NC since as early as 1954, and now has over 20 branches, $650 million in assets, and serves 60,000 North Carolinians. SHCU is a Treasury Department certified Community Development Financial Institution (CDFI), and a low income designated CU. Self-Help Federal Credit Union SHFCU is a member-owned, federally-insured, federally chartered CU. SHFCU was chartered in 2008, to build a network of CU branches to operate on a scale uncommon in the community development industry. Through a series of over 10 mergers, acquisitions, and new branch launches, in both CA and IL, we are building a CDCU that provides highimpact financial services to working-class communities. SHFCU now has over 20 branches, $600 million in assets, and serves over 80,000 people. SHFCU family includes credit unions that have served CA since as early as 1936 and IL as early as SHFCU is a Treasury-certified CDFI, a low-income designated CU, and a Minority Depository Institution (MDI). Self-Help Ventures Fund Nonprofit 501(c)(3) loan fund capitalized with loans and grants from foundations, religious organizations, corporations and government sources. SHVF manages Self-Help's higher-risk business loans, real estate development and home loan secondary market programs. Center for Responsible Lending CRL is a national nonprofit, nonpartisan research and policy organization. CRL is dedicated to protecting homeownership and family wealth by working to eliminate abusive financial practices. Center for Community Self-Help Charitable nonprofit 501(c)(3) organization that develops and coordinates Self-Help's programs, raises resources, and advocates for economic opportunity. 58

(low) Mission Impact (high)")

50 Mission / Finances Chart (high) Benefit to Net Worth (low) (low) Mission Impact (high) 59

51

52

New members of the Self-Help family bring long histories of service

Creating and protecting ownership and economic opportunity for all. Self-Help is a credit union and community development organization helping families and neighborhoods grow and thrive. Together with

Creating and protecting ownership and economic opportunity for all. Self-Help is a credit union and community development organization helping families and neighborhoods grow and thrive. Together with

Annual Report. Self-Help Credit Union. Self-Help Federal Credit Union. Self-Help Ventures Fund. Center for Responsible Lending

Annual Report 2014 Self-Help Credit Union Self-Help Federal Credit Union Self-Help Ventures Fund Center for Responsible Lending Dear friends and supporters, As we grow and welcome new members, some may

Annual Report 2014 Self-Help Credit Union Self-Help Federal Credit Union Self-Help Ventures Fund Center for Responsible Lending Dear friends and supporters, As we grow and welcome new members, some may

Self Help Federal Credit Union California

April 28, 2011 Self Help Federal Credit Union California Strong Capital Ratio Rapid Growth Merger Strategy Community Development Strategies New England Market Research, Inc. Mission: Creating and protecting

April 28, 2011 Self Help Federal Credit Union California Strong Capital Ratio Rapid Growth Merger Strategy Community Development Strategies New England Market Research, Inc. Mission: Creating and protecting

Annual Report Self-Help Credit Union Self-Help Federal Credit Union Self-Help Ventures Fund Center for Responsible Lending

Annual Report 2013 Self-Help Credit Union Self-Help Federal Credit Union Self-Help Ventures Fund Center for Responsible Lending Dear friends and supporters, As our nation continues its slow recovery, new

Annual Report 2013 Self-Help Credit Union Self-Help Federal Credit Union Self-Help Ventures Fund Center for Responsible Lending Dear friends and supporters, As our nation continues its slow recovery, new

Credit Union Access to Capital

Credit Union Access to Capital & How the Federation Can Help! 2012 AACUC Annual Conference Charleston, SC Terri J. Fowlkes Director, Community Development Investments National Federation of Community Development

Credit Union Access to Capital & How the Federation Can Help! 2012 AACUC Annual Conference Charleston, SC Terri J. Fowlkes Director, Community Development Investments National Federation of Community Development

BUILDING STRONGER COMMUNITIES TOGETHER: IMMIGRANTS AND ASSET BUILDING FLORIDA PHILANTHROPY NETWORK SUMMIT FEBRUARY 2017

BUILDING STRONGER COMMUNITIES TOGETHER: IMMIGRANTS AND ASSET BUILDING 1 FLORIDA PHILANTHROPY NETWORK SUMMIT FEBRUARY 2017 GCIR PROVIDES A FORUM FOR FUNDERS TO: Learn about current issues through in-depth

BUILDING STRONGER COMMUNITIES TOGETHER: IMMIGRANTS AND ASSET BUILDING 1 FLORIDA PHILANTHROPY NETWORK SUMMIT FEBRUARY 2017 GCIR PROVIDES A FORUM FOR FUNDERS TO: Learn about current issues through in-depth

OUR WORK AND IMPACT ( )

") OUR WORK AND IMPACT (1980-2018) Creating and protecting ownership and economic opportunity for all. Self-Help is a community development organization helping families and neighborhoods grow and thrive.

OUR WORK AND IMPACT (1980-2018) Creating and protecting ownership and economic opportunity for all. Self-Help is a community development organization helping families and neighborhoods grow and thrive.

Expanding Homeownership Responsibly with Freddie Mac Home Possible. Nadja Vital MBA Central FL, Nov.8, 2017

Expanding Homeownership Responsibly with Freddie Mac Home Possible Nadja Vital MBA Central FL, Nov.8, 2017 A Better Freddie Mac and a better housing finance system For families...innovating to improve

Expanding Homeownership Responsibly with Freddie Mac Home Possible Nadja Vital MBA Central FL, Nov.8, 2017 A Better Freddie Mac and a better housing finance system For families...innovating to improve

THE CFPB WHAT IT DOES, AND WHY YOU SHOULD CARE

THE CFPB WHAT IT DOES, AND WHY YOU SHOULD CARE Center for Responsible Lending CRL is a nonprofit, non-partisan organization that works to protect homeownership and family wealth by fighting predatory lending

THE CFPB WHAT IT DOES, AND WHY YOU SHOULD CARE Center for Responsible Lending CRL is a nonprofit, non-partisan organization that works to protect homeownership and family wealth by fighting predatory lending

Why is Non-Bank Lending Highest in Communities of Color?

Why is Non-Bank Lending Highest in Communities of Color? An ANHD White Paper October 2017 New York is a city of renters, but nearly a third of New Yorkers own their own homes. The stock of 2-4 family homes

Why is Non-Bank Lending Highest in Communities of Color? An ANHD White Paper October 2017 New York is a city of renters, but nearly a third of New Yorkers own their own homes. The stock of 2-4 family homes

State of the Housing Market

State of the Housing Market 2 Freddie Mac s Mission Freddie Mac makes homeownership and rental housing more accessible and affordable by providing liquidity, stability, and affordability to the U.S. housing

State of the Housing Market 2 Freddie Mac s Mission Freddie Mac makes homeownership and rental housing more accessible and affordable by providing liquidity, stability, and affordability to the U.S. housing

PUBLIC DISCLOSURE COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION

PUBLIC DISCLOSURE June 12, 2017 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION The First National Bank of Granbury 101 E. Bridge Street Granbury, TX 76048 Office of the Comptroller of the Currency Fort

PUBLIC DISCLOSURE June 12, 2017 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION The First National Bank of Granbury 101 E. Bridge Street Granbury, TX 76048 Office of the Comptroller of the Currency Fort

Who is Lending and Who is Getting Loans?

Trends in 1-4 Family Lending in New York City An ANHD White Paper February 2016 As much as New York City is a city of renters, nearly a third of New Yorkers own their own homes. Responsible, affordable

Trends in 1-4 Family Lending in New York City An ANHD White Paper February 2016 As much as New York City is a city of renters, nearly a third of New Yorkers own their own homes. Responsible, affordable

Strengthening Your Capacity to Serve the Underserved

Strengthening Your Capacity to Serve the Underserved Blake Myers Consultant, National Federation of Community Development Credit Unions Teri Robinson CEO, Pacific NW Ironworkers FCU Agenda 1. The Opportunity:

Strengthening Your Capacity to Serve the Underserved Blake Myers Consultant, National Federation of Community Development Credit Unions Teri Robinson CEO, Pacific NW Ironworkers FCU Agenda 1. The Opportunity:

Fundamentals of the Opportunity Finance Industry Certificate in Community Development Finance

Fundamentals of the Opportunity Finance Industry Certificate in Community Development Finance Day 1 Presentation Fundamentals of the Opportunity Finance Industry Certificate in Community Development Finance

Fundamentals of the Opportunity Finance Industry Certificate in Community Development Finance Day 1 Presentation Fundamentals of the Opportunity Finance Industry Certificate in Community Development Finance

Credit Research Center Seminar

Credit Research Center Seminar Ensuring Fair Lending: What Do We Know about Pricing in Mortgage Markets and What Will the New HMDA Data Fields Tell US? www.msb.edu/prog/crc March 14, 2005 Introduction

Credit Research Center Seminar Ensuring Fair Lending: What Do We Know about Pricing in Mortgage Markets and What Will the New HMDA Data Fields Tell US? www.msb.edu/prog/crc March 14, 2005 Introduction

Community. An Overview of the CDFI Industry. by Brandy Curtis

Community Developments Emerging Issues in Community Development and Consumer Affairs Federal Reserve Bank of Boston 006 Issue An Overview of the CDFI Industry Inside Updates 1 There are an estimated 1,000

Community Developments Emerging Issues in Community Development and Consumer Affairs Federal Reserve Bank of Boston 006 Issue An Overview of the CDFI Industry Inside Updates 1 There are an estimated 1,000

The Community Development Financial

Community Development Financial Institutions Fund By Shannon Ross, Director, Government Relations, Housing Partnership Network Administering agency: U.S. Department of the Treasury (Treasury) Year program

Community Development Financial Institutions Fund By Shannon Ross, Director, Government Relations, Housing Partnership Network Administering agency: U.S. Department of the Treasury (Treasury) Year program

PACIFIC WESTERN BANK S CRA COMMUNITY BENEFIT 3-YEAR PLAN

PACIFIC WESTERN BANK S CRA COMMUNITY BENEFIT 3-YEAR PLAN 2017-2019 Motivating Sustainable Communities I. Introduction and Overview Pacific Western Bank's (the "Bank") Community Reinvestment Act ("CRA")

PACIFIC WESTERN BANK S CRA COMMUNITY BENEFIT 3-YEAR PLAN 2017-2019 Motivating Sustainable Communities I. Introduction and Overview Pacific Western Bank's (the "Bank") Community Reinvestment Act ("CRA")

CDFI Certification. A Pathway to Growth and Impact

CDFI Certification A Pathway to Growth and Impact CDFI Fund Basics Established by Congress 1994 Federation and CDCUs instrumental in founding CDFIs include regulated and unregulated institutions that meet

CDFI Certification A Pathway to Growth and Impact CDFI Fund Basics Established by Congress 1994 Federation and CDCUs instrumental in founding CDFIs include regulated and unregulated institutions that meet

Upon completion of this session you should: Become more familiar with the history/purpose of CRA;

CRA Basics Objectives Upon completion of this session you should: Become more familiar with the history/purpose of CRA; Become more familiar with terms and definitions under the CRA regulation; Introduce

CRA Basics Objectives Upon completion of this session you should: Become more familiar with the history/purpose of CRA; Become more familiar with terms and definitions under the CRA regulation; Introduce

COMMUNITY DEVELOPMENT PLAN

COMMUNITY DEVELOPMENT PLAN OF CIBC BANK USA CIBC Bank USA 1 (the Bank ) has a long history of serving the credit, banking and financial literacy needs of our communities and strives to be a leader in community

COMMUNITY DEVELOPMENT PLAN OF CIBC BANK USA CIBC Bank USA 1 (the Bank ) has a long history of serving the credit, banking and financial literacy needs of our communities and strives to be a leader in community

Mortgage Assistance Program (MAP)

") Mortgage Assistance Program (MAP) A Briefing to the Housing Committee Housing Department September 16, 2008 KEY FOCUS AREA: ECONOMIC VIBRANCY Purpose To provide an update of the Mortgage Assistance Program

Mortgage Assistance Program (MAP) A Briefing to the Housing Committee Housing Department September 16, 2008 KEY FOCUS AREA: ECONOMIC VIBRANCY Purpose To provide an update of the Mortgage Assistance Program

A Nation of Renters? Promoting Homeownership Post-Crisis. Roberto G. Quercia Kevin A. Park

A Nation of Renters? Promoting Homeownership Post-Crisis Roberto G. Quercia Kevin A. Park 2 Outline of Presentation Why homeownership? The scale of the foreclosure crisis today (20112Q) Mississippi and

A Nation of Renters? Promoting Homeownership Post-Crisis Roberto G. Quercia Kevin A. Park 2 Outline of Presentation Why homeownership? The scale of the foreclosure crisis today (20112Q) Mississippi and

Advocacy In The Federal Policy Arena:

Advocacy In The Federal Policy Arena: Small Business Resources June 13, 2017 Federal Spending in 2016 Net Interest 6% Discretionary 31% $1.5 trillion Defense Non-Defense Non-Defense 16% Defense 15% Total

Advocacy In The Federal Policy Arena: Small Business Resources June 13, 2017 Federal Spending in 2016 Net Interest 6% Discretionary 31% $1.5 trillion Defense Non-Defense Non-Defense 16% Defense 15% Total

Commonly Collected OUTPUT and OUTCOME Indicators

Commonly Collected OUTPUT and OUTCOME Indicators Business Line Indicator Name Type Potential Uses Cross-Cutting Housing (single and multi-family) # Loans originated Output HMDA, CRA, CDFI Fund, NCIF, GIIN

Commonly Collected OUTPUT and OUTCOME Indicators Business Line Indicator Name Type Potential Uses Cross-Cutting Housing (single and multi-family) # Loans originated Output HMDA, CRA, CDFI Fund, NCIF, GIIN

SUMMARY: The Bureau of Consumer Financial Protection (CFPB or Bureau) is publishing this agenda

is publishing this agenda") This document is scheduled to be published in the Federal Register on 06/09/2016 and available online at http://federalregister.gov/a/2016-12931, and on FDsys.gov BUREAU OF CONSUMER FINANCIAL PROTECTION

This document is scheduled to be published in the Federal Register on 06/09/2016 and available online at http://federalregister.gov/a/2016-12931, and on FDsys.gov BUREAU OF CONSUMER FINANCIAL PROTECTION

Craft3 & Self-Help Single-Family Residential Energy Efficiency Loan Sale. June 2015

Craft3 & Self-Help Single-Family Residential Energy Efficiency Loan Sale June 2015 Craft3 A Community Development Financial Institution (CDFI) A nonprofit and charitable corporation Not a bank or credit

Craft3 & Self-Help Single-Family Residential Energy Efficiency Loan Sale June 2015 Craft3 A Community Development Financial Institution (CDFI) A nonprofit and charitable corporation Not a bank or credit

National Case Statement

Discussion Topics Session Description Learn about the advantages your Credit Union Members can receive by obtaining low-income designation and CDFI Certification and how this translates to Member value.

Discussion Topics Session Description Learn about the advantages your Credit Union Members can receive by obtaining low-income designation and CDFI Certification and how this translates to Member value.

ASSOCIATED BANK, N.A. COMMUNITY COMMITMENT PLAN FOR

ASSOCIATED BANK, N.A. COMMUNITY COMMITMENT PLAN FOR 2018-2020 Our Purpose Associated Bank, N.A. (Associated) recognizes our success is dependent upon strong relationships with the communities where we

ASSOCIATED BANK, N.A. COMMUNITY COMMITMENT PLAN FOR 2018-2020 Our Purpose Associated Bank, N.A. (Associated) recognizes our success is dependent upon strong relationships with the communities where we

27% 42% 51% 16% 51% 19% PROFILE. Assets & opportunity ProfILe: PortLANd. key highlights. ABoUt the ProfILe ASSETS & OPPORTUNITY

Assets & opportunity ProfILe: PortLANd ASSETS & OPPORTUNITY PROFILE key highlights 27% of Portland households live in asset poverty Cities have long been thought of as places of opportunity for low-income

Assets & opportunity ProfILe: PortLANd ASSETS & OPPORTUNITY PROFILE key highlights 27% of Portland households live in asset poverty Cities have long been thought of as places of opportunity for low-income

Testimony of Michael D. Calhoun President, Center for Responsible Lending. Before the House Committee on Financial Services

Testimony of Michael D. Calhoun President, Center for Responsible Lending Before the House Committee on Financial Services Hearing: A Legislative Proposal to Protect American Taxpayers and Homeowners by

Testimony of Michael D. Calhoun President, Center for Responsible Lending Before the House Committee on Financial Services Hearing: A Legislative Proposal to Protect American Taxpayers and Homeowners by

Consumer Financial Services Webinar Series. Webinar #6:

Consumer Financial Services Webinar Series Webinar #6: The Power and Potential of CDFI Credit Union and Loan Fund Partnerships June 22, 2016 1:00 2:00 PM ET Presenters Lauren Stebbins Senior Associate,

Consumer Financial Services Webinar Series Webinar #6: The Power and Potential of CDFI Credit Union and Loan Fund Partnerships June 22, 2016 1:00 2:00 PM ET Presenters Lauren Stebbins Senior Associate,

Community Development Investment Program (CDIP) for CDCUs SECONDARY CAPITAL I APPLICATION

for CDCUs SECONDARY CAPITAL I APPLICATION") Community Development Investment Program (CDIP) for CDCUs SECONDARY CAPITAL I APPLICATION Date: Credit Union: Charter Number: Contact Person: Title : Telephone: ( ) Fax: ( ) E-mail Mailing Address: Secondary

Community Development Investment Program (CDIP) for CDCUs SECONDARY CAPITAL I APPLICATION Date: Credit Union: Charter Number: Contact Person: Title : Telephone: ( ) Fax: ( ) E-mail Mailing Address: Secondary

Paying More for the American Dream III

Paying More for the American Dream III Promoting Responsible Lending to Lower-Income Communities and Communities of Color April 2009 A Joint Report By: California Reinvestment Coalition Community Reinvestment

Paying More for the American Dream III Promoting Responsible Lending to Lower-Income Communities and Communities of Color April 2009 A Joint Report By: California Reinvestment Coalition Community Reinvestment

Community Development Financial Institutions (CDFIs)

") Community Development Financial Institutions (CDFIs) o Private financial institutions focused on serving low income communities o Combine financial & development services o Raise capital with interest

Community Development Financial Institutions (CDFIs) o Private financial institutions focused on serving low income communities o Combine financial & development services o Raise capital with interest

Executive Summary of the 2018 HMDA Interpretive and Procedural Rule

Bureau of Consumer Financial Protection 1700 G Street NW Washington, D.C. 20552 August 31, 2018 Executive Summary of the 2018 HMDA Interpretive and Procedural Rule On August 31, 2018, the Bureau of Consumer

Bureau of Consumer Financial Protection 1700 G Street NW Washington, D.C. 20552 August 31, 2018 Executive Summary of the 2018 HMDA Interpretive and Procedural Rule On August 31, 2018, the Bureau of Consumer

Expanding Homeownership Responsibly with Freddie Mac Home Possible

Expanding Homeownership Responsibly with Freddie Mac Home Possible March 23, 2017 A Better Freddie Mac and a better housing finance system For families...innovating to improve the liquidity, stability

Expanding Homeownership Responsibly with Freddie Mac Home Possible March 23, 2017 A Better Freddie Mac and a better housing finance system For families...innovating to improve the liquidity, stability

CITY OF GAINESVILLE. CHIP 1 st TIME HOMEBUYER DOWN PAYMENT ASSISTANCE UNDERWRITING GUIDELINES

CITY OF GAINESVILLE CHIP 1 st TIME HOMEBUYER DOWN PAYMENT ASSISTANCE UNDERWRITING GUIDELINES Mission Statement The City of Gainesville Housing and Community Development Division is dedicated to improving

CITY OF GAINESVILLE CHIP 1 st TIME HOMEBUYER DOWN PAYMENT ASSISTANCE UNDERWRITING GUIDELINES Mission Statement The City of Gainesville Housing and Community Development Division is dedicated to improving

May 17, Housing Sector Overview

May 17, 2017 Housing Sector Overview Housing Finance Policy Center May 17, 2017 AFFORDABLE HOUSING: In general, housing for which the occupant(s) is/are paying no more than 30 percent of his or her income

May 17, 2017 Housing Sector Overview Housing Finance Policy Center May 17, 2017 AFFORDABLE HOUSING: In general, housing for which the occupant(s) is/are paying no more than 30 percent of his or her income

CDFI Credit Unions A Business Case for Community Development Finance. CDFI Institute February 28, 2017

CDFI Credit Unions A Business Case for Community Development Finance CDFI Institute February 28, 2017 What it means to be a CDFI? Community Development Key Products & Services Inclusive transaction services

CDFI Credit Unions A Business Case for Community Development Finance CDFI Institute February 28, 2017 What it means to be a CDFI? Community Development Key Products & Services Inclusive transaction services

RE: Comments on Financial Access Activities, 76 FR 56499

November 14, 2011 Louisa Quittman Office of Financial Education and Financial Access U.S. Department of the Treasury 1500 Pennsylvania Ave., N.W. Washington, D.C. 20220 ofe@treasury.gov RE: Comments on

November 14, 2011 Louisa Quittman Office of Financial Education and Financial Access U.S. Department of the Treasury 1500 Pennsylvania Ave., N.W. Washington, D.C. 20220 ofe@treasury.gov RE: Comments on

Lending to ITIN and Immigrant Markets. Alejandra Seluja CU Breakthrough

Lending to ITIN and Immigrant Markets Alejandra Seluja CU Breakthrough Overview Why reach out to Latino and immigrant borrowers? What is an ITIN? What does an ITIN lending program look like? Auto and consumer

Lending to ITIN and Immigrant Markets Alejandra Seluja CU Breakthrough Overview Why reach out to Latino and immigrant borrowers? What is an ITIN? What does an ITIN lending program look like? Auto and consumer

Congressional District Report For the 115th Congress

Congressional District Report For the 115th Congress Arizona District 6 Honorable David Schweikert (R) May 2017 Report National Association of REALTORS Congressional District Report For the 115th Congress

Congressional District Report For the 115th Congress Arizona District 6 Honorable David Schweikert (R) May 2017 Report National Association of REALTORS Congressional District Report For the 115th Congress

Despite Growing Market, African Americans and Latinos Remain Underserved

Despite Growing Market, African Americans and Latinos Remain Underserved Issue Brief September 2017 Introduction Enacted by Congress in 1975, the Home Mortgage Disclosure Act (HMDA) requires an annual

Despite Growing Market, African Americans and Latinos Remain Underserved Issue Brief September 2017 Introduction Enacted by Congress in 1975, the Home Mortgage Disclosure Act (HMDA) requires an annual

In Baltimore City today, 20% of households live in poverty, but more than half of the

Building Economic Opportunity in Baltimore: A Data Profile Baltimore Highlights In Baltimore City today, 20% of households live in poverty, but more than half of the city s population 55% is financially

Building Economic Opportunity in Baltimore: A Data Profile Baltimore Highlights In Baltimore City today, 20% of households live in poverty, but more than half of the city s population 55% is financially

Financial Inclusion for Immigrant Consumers Roundtable

Financial Inclusion for Immigrant Consumers Roundtable Assessing your Readiness 1/16/15 Miriam De Dios, CEO Coopera Pablo DeFilippi, VP Membership & Business Development, Federation Coopera Our Mission:

Financial Inclusion for Immigrant Consumers Roundtable Assessing your Readiness 1/16/15 Miriam De Dios, CEO Coopera Pablo DeFilippi, VP Membership & Business Development, Federation Coopera Our Mission:

36% 50% 11% 59% 35% PROFILE ASSETS & OPPORTUNITY PROFILE: CHARLOTTE KEY HIGHLIGHTS ABOUT THE PROFILE ASSETS & OPPORTUNITY

ASSETS & OPPORTUNITY PROFILE: CHARLOTTE ASSETS & OPPORTUNITY PROFILE KEY HIGHLIGHTS 36% of Charlotte households live in asset poverty Cities have long been thought of as places of opportunity for low-income

ASSETS & OPPORTUNITY PROFILE: CHARLOTTE ASSETS & OPPORTUNITY PROFILE KEY HIGHLIGHTS 36% of Charlotte households live in asset poverty Cities have long been thought of as places of opportunity for low-income

Regional Initiative Council Meetings Financing the Vision Lunch Discussion August 27, Carolinas. Durham Bulls Athletic Park.

Regional Initiative Council Meetings Financing the Vision Lunch Discussion August 27, 2015 Carolinas PNC Triangle Club Durham Bulls Athletic Park Panel Members TUCKER BARTLETT Executive Vice President,

Regional Initiative Council Meetings Financing the Vision Lunch Discussion August 27, 2015 Carolinas PNC Triangle Club Durham Bulls Athletic Park Panel Members TUCKER BARTLETT Executive Vice President,

BROWARD HOUSING COUNCIL CRA PERFORMANCE BY BROWARD BANKS IN MEETING HOUSING CREDIT NEEDS

BROWARD HOUSING COUNCIL CRA PERFORMANCE BY BROWARD BANKS IN MEETING HOUSING CREDIT NEEDS CRA IMPLEMENTATION WORKSHOP January 23, 2015 2 South Florida Context Areas of Opportunity Overview of HMDA Data

BROWARD HOUSING COUNCIL CRA PERFORMANCE BY BROWARD BANKS IN MEETING HOUSING CREDIT NEEDS CRA IMPLEMENTATION WORKSHOP January 23, 2015 2 South Florida Context Areas of Opportunity Overview of HMDA Data

Funding Sources for FQHC Capital Projects: Updates on New Markets Tax Credits and HRSA's Loan Guarantee Program

Funding Sources for FQHC Capital Projects: Updates on New Markets Tax Credits and HRSA's Loan Guarantee Program Duncan McGillivray Project Consultant November 29, 2018 1 Capital Link Launched in 1995,

Funding Sources for FQHC Capital Projects: Updates on New Markets Tax Credits and HRSA's Loan Guarantee Program Duncan McGillivray Project Consultant November 29, 2018 1 Capital Link Launched in 1995,

Overview of the CDFI Industry

Overview of the CDFI Industry Lauren Stebbins, Opportunity Finance Network April 1, 2016 CDFIs are Private, mission-driven financial institution benefitting lowincome, low-wealth, and other disadvantaged

Overview of the CDFI Industry Lauren Stebbins, Opportunity Finance Network April 1, 2016 CDFIs are Private, mission-driven financial institution benefitting lowincome, low-wealth, and other disadvantaged

An introduction to the Community Reinvestment Act. John Meeks Atlanta Region FDIC Community Affairs

An introduction to the Community Reinvestment Act John Meeks Atlanta Region FDIC Community Affairs What is the CRA? CRA stands for: The Community Reinvestment Act of 1977 The regulations implementing the

An introduction to the Community Reinvestment Act John Meeks Atlanta Region FDIC Community Affairs What is the CRA? CRA stands for: The Community Reinvestment Act of 1977 The regulations implementing the

Notice Regarding Updated Regulations and Summary of Recent CFPB Mortgage Rules

April 23, 2012 Notice Regarding Updated Regulations and Summary of Recent CFPB Mortgage Rules The Consumer Financial Protection Bureau ( CFPB or Bureau ) recently issued final rules related to mortgage

April 23, 2012 Notice Regarding Updated Regulations and Summary of Recent CFPB Mortgage Rules The Consumer Financial Protection Bureau ( CFPB or Bureau ) recently issued final rules related to mortgage

February 14, Dear Ms. Naulty:

February 14, 2014 Ms. Peggy Naulty Division of Consumer and Community Affairs Board of Governors of the Federal Reserve System 20 th Street and Constitution Avenue N.W. Washington, DC 20551 Dear Ms. Naulty:

February 14, 2014 Ms. Peggy Naulty Division of Consumer and Community Affairs Board of Governors of the Federal Reserve System 20 th Street and Constitution Avenue N.W. Washington, DC 20551 Dear Ms. Naulty:

Homeownership Policies to Improve the Financial Security of Households of Color and Low-Income Families. September 25, 2017

Homeownership Policies to Improve the Financial Security of Households of Color and Low-Income Families September 25, 2017 Welcome Carmen Shorter Senior Manager for Learning, Field Engagement Prosperity

Homeownership Policies to Improve the Financial Security of Households of Color and Low-Income Families September 25, 2017 Welcome Carmen Shorter Senior Manager for Learning, Field Engagement Prosperity

New Products in Consumer Financial Services. The Underserved Population

New Products in Consumer Financial Services Joshua Sledge, Center for Financial Services Innovation October 17th, 2013 Approximately 34 million U.S. households 68 million people are financially underserved

New Products in Consumer Financial Services Joshua Sledge, Center for Financial Services Innovation October 17th, 2013 Approximately 34 million U.S. households 68 million people are financially underserved

Consumer Financial Protection Bureau. March 15, Draft, Sensitive and Pre-Decisional Not for External Distribution

Consumer Financial Protection Bureau March 15, 2016 Draft, Sensitive and Pre-Decisional Not for External Distribution Outline Home Mortgage Disclosure Act 1) Background 2) Rule Making 3) Changes Coming

Consumer Financial Protection Bureau March 15, 2016 Draft, Sensitive and Pre-Decisional Not for External Distribution Outline Home Mortgage Disclosure Act 1) Background 2) Rule Making 3) Changes Coming

CRA a Brief History Lynette C. Briggs, VP - Regional CRA Officer

CRA a Brief History Lynette C. Briggs, VP - Regional CRA Officer August 2016 Community Reinvestment Act (CRA) a Brief History 2 Community Reinvestment Act (CRA) The Community Reinvestment Act (CRA) Brief

CRA a Brief History Lynette C. Briggs, VP - Regional CRA Officer August 2016 Community Reinvestment Act (CRA) a Brief History 2 Community Reinvestment Act (CRA) The Community Reinvestment Act (CRA) Brief

31% 41% 11% 50% 18% PROFILE ASSETS & OPPORTUNITY PROFILE: SAN FRANCISCO KEY HIGHLIGHTS ABOUT THE PROFILE ASSETS & OPPORTUNITY

ASSETS & OPPORTUNITY PROFILE: SAN FRANCISCO ASSETS & OPPORTUNITY PROFILE KEY HIGHLIGHTS 31% of San Francisco residents live in asset poverty Cities have long been thought of as places of opportunity for

ASSETS & OPPORTUNITY PROFILE: SAN FRANCISCO ASSETS & OPPORTUNITY PROFILE KEY HIGHLIGHTS 31% of San Francisco residents live in asset poverty Cities have long been thought of as places of opportunity for

A Look at Tennessee Mortgage Activity: A one-state analysis of the Home Mortgage Disclosure Act (HMDA) Data

Data") September, 2015 A Look at Tennessee Mortgage Activity: A one-state analysis of the Home Mortgage Disclosure Act (HMDA) Data 2004-2013 Hulya Arik, Ph.D. Tennessee Housing Development Agency TABLE OF CONTENTS

September, 2015 A Look at Tennessee Mortgage Activity: A one-state analysis of the Home Mortgage Disclosure Act (HMDA) Data 2004-2013 Hulya Arik, Ph.D. Tennessee Housing Development Agency TABLE OF CONTENTS

Facing Today s Real Estate Regulations

Proudly Sponsored by Facing Today s Real Estate Regulations Presented by Don Braspenninckx Day, June 11, 2016 1:30 p.m. 1 Introduction Numerous regulatory changes in the real estate industry within last

Proudly Sponsored by Facing Today s Real Estate Regulations Presented by Don Braspenninckx Day, June 11, 2016 1:30 p.m. 1 Introduction Numerous regulatory changes in the real estate industry within last

CRA COMMUNITY BENEFIT 3-YEAR PLAN

CRA COMMUNITY BENEFIT 3-YEAR PLAN 2018-2020 Motivating Sustainable Communities March 2018 I. Introduction and Executive Summary Annually, Pacific Western Bank ( PWB or the Bank ) establishes a Community

CRA COMMUNITY BENEFIT 3-YEAR PLAN 2018-2020 Motivating Sustainable Communities March 2018 I. Introduction and Executive Summary Annually, Pacific Western Bank ( PWB or the Bank ) establishes a Community

35% 26% 57% 51% PROFILE. CIty of durham: Assets & opportunity ProfILe. key highlights. ABoUt the ProfILe ASSETS & OPPORTUNITY

CIty of durham: Assets & opportunity ProfILe ASSETS & OPPORTUNITY PROFILE key highlights 35% of Durham County households live in asset poverty Cities have long been thought of as places of opportunity

CIty of durham: Assets & opportunity ProfILe ASSETS & OPPORTUNITY PROFILE key highlights 35% of Durham County households live in asset poverty Cities have long been thought of as places of opportunity

The distribution of wealth in the United States and implications for a net worth tax

The distribution of wealth in the United States and implications for a net worth tax March 2019 By Greg Leiserson, Will McGrew, and Raksha Kopparam Wealth inequality in the United States is high and has

The distribution of wealth in the United States and implications for a net worth tax March 2019 By Greg Leiserson, Will McGrew, and Raksha Kopparam Wealth inequality in the United States is high and has

Review of Regulations

Comments of National Consumer Law Center (on behalf of its low income clients) Center for Responsible Lending Consumer Action Consumer Federation of America Consumers Union National Association of Consumer

Comments of National Consumer Law Center (on behalf of its low income clients) Center for Responsible Lending Consumer Action Consumer Federation of America Consumers Union National Association of Consumer

Community Reinvestment Act for Community-Based Organizations. March 24, 2015 Providence, RI

Community Reinvestment Act for Community-Based Organizations March 24, 2015 Providence, RI Objectives Understand the purpose of the CRA and key definitions Understand how banks are evaluated under CRA

Community Reinvestment Act for Community-Based Organizations March 24, 2015 Providence, RI Objectives Understand the purpose of the CRA and key definitions Understand how banks are evaluated under CRA

Creating a Sustainable Foundation for Financial Inclusion

Creating a Sustainable Foundation for Financial Inclusion Scott Butterfield, Your Credit Union Partner Sarah Marshall, North Side Community Credit Union Jamey Gill, Mendo Lake Credit Union Purpose of this

Creating a Sustainable Foundation for Financial Inclusion Scott Butterfield, Your Credit Union Partner Sarah Marshall, North Side Community Credit Union Jamey Gill, Mendo Lake Credit Union Purpose of this

The Community Reinvestment Act and Mortgage Lending. Terri Hasson Director Community Reinvestment WSFS Bank

The Community Reinvestment Act and Mortgage Lending Terri Hasson Director Community Reinvestment WSFS Bank thasson@wsfsbank.com 302-571-7015 Landscape of Home Purchase Lending in Delaware County PA Setting

The Community Reinvestment Act and Mortgage Lending Terri Hasson Director Community Reinvestment WSFS Bank thasson@wsfsbank.com 302-571-7015 Landscape of Home Purchase Lending in Delaware County PA Setting

The Untold Costs of Subprime Lending: Communities of Color in California. Carolina Reid. Federal Reserve Bank of San Francisco.

The Untold Costs of Subprime Lending: The Impacts of Foreclosure on Communities of Color in California Carolina Reid Federal Reserve Bank of San Francisco April 10, 2009 The views expressed herein are

The Untold Costs of Subprime Lending: The Impacts of Foreclosure on Communities of Color in California Carolina Reid Federal Reserve Bank of San Francisco April 10, 2009 The views expressed herein are

With so much change, be sure to stay up to date!

With so much change, be sure to stay up to date! Glory LeDu Glory.LeDu@mcul.org Sarah Stevenson Sarah.Stevenson@mcul.org Barb Boyd Barb.Boyd@cusolutionsgroup.com Your Crazy Compliance Peeps Agenda What

With so much change, be sure to stay up to date! Glory LeDu Glory.LeDu@mcul.org Sarah Stevenson Sarah.Stevenson@mcul.org Barb Boyd Barb.Boyd@cusolutionsgroup.com Your Crazy Compliance Peeps Agenda What

Congressional District Report For the 115th Congress

Congressional District Report For the 115th Congress Washington District 5 Honorable Cathy McMorris Rodgers (R) February 2017 Report National Association of REALTORS Congressional District Report For the

Congressional District Report For the 115th Congress Washington District 5 Honorable Cathy McMorris Rodgers (R) February 2017 Report National Association of REALTORS Congressional District Report For the

BANKING, the original and most important form of crowdfunding, was broken until

BANKING, the original and most important form of crowdfunding, was broken until THEORY OF CHANGE A new model to change the banking system for good Social enterprise bank founded in 2007 with a triple bottom

BANKING, the original and most important form of crowdfunding, was broken until THEORY OF CHANGE A new model to change the banking system for good Social enterprise bank founded in 2007 with a triple bottom

Credit Access and Consumer Protection: Searching for the Right Balance

Credit Access and Consumer Protection: Searching for the Right Balance North Carolina Banking Institute March 26, 2013 Charlotte, NC Michael D. Calhoun Impact On Consumer Finances Already New Rapidly Appreciating

Credit Access and Consumer Protection: Searching for the Right Balance North Carolina Banking Institute March 26, 2013 Charlotte, NC Michael D. Calhoun Impact On Consumer Finances Already New Rapidly Appreciating

How Cities Can Pursue Responsible Banking: Model Local Responsible Banking Ordinance Creates Community Reinvestment Requirements for Financial

How Cities Can Pursue Responsible Banking: Model Local Responsible Banking Ordinance Creates Community Reinvestment Requirements for Financial Institutions JULY 2012 How Cities Can Pursue Responsible Banking:

How Cities Can Pursue Responsible Banking: Model Local Responsible Banking Ordinance Creates Community Reinvestment Requirements for Financial Institutions JULY 2012 How Cities Can Pursue Responsible Banking:

Telesca Center for Justice One West Main Street, Suite 200 Rochester, NY Phone Fax

Telesca Center for Justice One West Main Street, Suite 200 Rochester, NY 14614 Phone 585.454.4060 Fax 585.454.2518 www.empirejustice.org October 7, 2016 Ivan J. Hurwitz Vice President Federal Reserve Bank

Telesca Center for Justice One West Main Street, Suite 200 Rochester, NY 14614 Phone 585.454.4060 Fax 585.454.2518 www.empirejustice.org October 7, 2016 Ivan J. Hurwitz Vice President Federal Reserve Bank

Re: Response to Request for Comment on Capital Magnet Fund

May 5, 2009 Mr. Matt Josephs Deputy Director of Policy and Programs CDFI Fund U.S. Department of the Treasury 601 13 th Street, NW Suite 200 South Washington, DC 20005 Re: Response to Request for Comment

May 5, 2009 Mr. Matt Josephs Deputy Director of Policy and Programs CDFI Fund U.S. Department of the Treasury 601 13 th Street, NW Suite 200 South Washington, DC 20005 Re: Response to Request for Comment

Self-Help s Rural Impact & Partnership with USDA

September, 2017 Self-Help s Rural Impact & Partnership with USDA Self-Help 1, a lending national community development financial institution (CDFI) headquartered in Durham, has always had service to rural

September, 2017 Self-Help s Rural Impact & Partnership with USDA Self-Help 1, a lending national community development financial institution (CDFI) headquartered in Durham, has always had service to rural

Michael I. Sanders and Megan Christensen. September 20, 2013 ABA Tax Section Exempt Organizations Meeting San Francisco, CA

Use of the New Markets Tax Credit by Tax-Exempt Entities Michael I. Sanders and Megan Christensen Blank Rome LLP September 20, 2013 ABA Tax Section Exempt Organizations Meeting San Francisco, CA NMTC Overview:

Use of the New Markets Tax Credit by Tax-Exempt Entities Michael I. Sanders and Megan Christensen Blank Rome LLP September 20, 2013 ABA Tax Section Exempt Organizations Meeting San Francisco, CA NMTC Overview:

A Long Road Back to Work. The Realities of Unemployment since the Great Recession

1101 Connecticut Ave NW, Suite 810 Washington, DC 20036 http://www.nul.org A Long Road Back to Work The Realities of Unemployment since the Great Recession June 2011 Valerie Rawlston Wilson, PhD National

1101 Connecticut Ave NW, Suite 810 Washington, DC 20036 http://www.nul.org A Long Road Back to Work The Realities of Unemployment since the Great Recession June 2011 Valerie Rawlston Wilson, PhD National

CRA History. The Community Reinvestment Act passage did two things:

CRA History The Community Reinvestment Act passage did two things: The discussion of CRA brought light to the illegal practice of redlining. Required regulated financial institutions to help meet the credit

CRA History The Community Reinvestment Act passage did two things: The discussion of CRA brought light to the illegal practice of redlining. Required regulated financial institutions to help meet the credit

THE WEALTH BUILDING HOME LOAN. AEI s Housing Center

THE WEALTH BUILDING HOME LOAN Presented by Stephen Oliner and Edward Pinto stephen.oliner@aei.org, pintoedward1@gmail.com American Enterprise Institute Center on Housing Markets and Finance http://www.aei.org/housing/

THE WEALTH BUILDING HOME LOAN Presented by Stephen Oliner and Edward Pinto stephen.oliner@aei.org, pintoedward1@gmail.com American Enterprise Institute Center on Housing Markets and Finance http://www.aei.org/housing/

Bank of America to Massachusetts Homebuyers:

Bank of America to Massachusetts Homebuyers: Life s Expensive When We re Connected A report on Bank of America s Massachusetts mortgage lending from 2004-2014 by the Homeownership Action Network June 4,

Bank of America to Massachusetts Homebuyers: Life s Expensive When We re Connected A report on Bank of America s Massachusetts mortgage lending from 2004-2014 by the Homeownership Action Network June 4,

REINVESTMENT ALERT. Woodstock Institute November, 1997 Number 11

REINVESTMENT ALERT Woodstock Institute November, 1997 Number 11 New Small Business Data Show Loans Going To Higher-Income Neighborhoods in Chicago Area In October, federal banking regulators released new

REINVESTMENT ALERT Woodstock Institute November, 1997 Number 11 New Small Business Data Show Loans Going To Higher-Income Neighborhoods in Chicago Area In October, federal banking regulators released new

Overview of the CDFI Industry, OFN, and the OFN Conference

Overview of the CDFI Industry, OFN, and the OFN Conference Seth Julyan, Opportunity Finance Network Agenda Conference information Opportunity Finance Network overview CDFI overview 1 Questions Why are

Overview of the CDFI Industry, OFN, and the OFN Conference Seth Julyan, Opportunity Finance Network Agenda Conference information Opportunity Finance Network overview CDFI overview 1 Questions Why are

September 8, The Honorable Mel Watt Director, Federal Housing Finance Agency th Street SW, Ninth Floor Washington, DC 20024

September 8, 2014 The Honorable Mel Watt Director, Federal Housing Finance Agency 4000 7 th Street SW, Ninth Floor Washington, DC 20024 Re: Private Mortgage Insurer Eligibility Requirements-Request for

September 8, 2014 The Honorable Mel Watt Director, Federal Housing Finance Agency 4000 7 th Street SW, Ninth Floor Washington, DC 20024 Re: Private Mortgage Insurer Eligibility Requirements-Request for

December 19, Director Kathleen Kraninger Consumer Financial Protection Bureau 1700 G Street NW Washington, DC 20552

December 19, 2018 Director Kathleen Kraninger Consumer Financial Protection Bureau 1700 G Street NW Washington, DC 20552 Re: Ongoing Rulemaking on Debt Collection Dear Director Kraninger, As we approach

December 19, 2018 Director Kathleen Kraninger Consumer Financial Protection Bureau 1700 G Street NW Washington, DC 20552 Re: Ongoing Rulemaking on Debt Collection Dear Director Kraninger, As we approach

Role of HFAs and FHA in supporting homeownership

Role of HFAs and FHA in supporting homeownership Ed Golding Housing Finance Policy Center Urban Institute HFA Institute Washington, DC January 12, 2018 Introduction Homeownership has been supported by

Role of HFAs and FHA in supporting homeownership Ed Golding Housing Finance Policy Center Urban Institute HFA Institute Washington, DC January 12, 2018 Introduction Homeownership has been supported by

Federal Budget Overview

Federal Budget Overview FY 2018 spending bill passed in March; FY 2019 spending bills are still being considered by Congress FY 2018 includes: Increased funding for defense as well as domestic discretionary

Federal Budget Overview FY 2018 spending bill passed in March; FY 2019 spending bills are still being considered by Congress FY 2018 includes: Increased funding for defense as well as domestic discretionary

In Support of Affordable Housing Initiatives. NCSHA - October 2018

In Support of Affordable Housing Initiatives NCSHA - October 2018 For Today Central to our mission is the support of affordable housing by providing liquidity to the market. We are focused on innovating

In Support of Affordable Housing Initiatives NCSHA - October 2018 For Today Central to our mission is the support of affordable housing by providing liquidity to the market. We are focused on innovating

Community Development with a Purpose. CDFI Certification: A Building Block of Community Finance

Community Development with a Purpose CDFI Certification: A Building Block of Community Finance CDFI Fund CDFI Fund established by Congress in 1994 through the efforts of Federation and others in community

Community Development with a Purpose CDFI Certification: A Building Block of Community Finance CDFI Fund CDFI Fund established by Congress in 1994 through the efforts of Federation and others in community

Challenges and Opportunities for Low Downpayment Lending

Challenges and Opportunities for Low Downpayment Lending Roberto G. Quercia UNC Center for Community Capital University of North Carolina at Chapel Hill Chapel Hill NC, May 17, 2013 Research Funded by

Challenges and Opportunities for Low Downpayment Lending Roberto G. Quercia UNC Center for Community Capital University of North Carolina at Chapel Hill Chapel Hill NC, May 17, 2013 Research Funded by

39% 22% 56% 49% 35% 60% PROFILE. Assets & opportunity ProfILe: winston-salem ANd forsyth CoUNtY. KeY HIgHLIgHts. AboUt the ProfILe

Assets & opportunity ProfILe: winston-salem ANd forsyth CoUNtY ASSETS & OPPORTUNITY PROFILE KeY HIgHLIgHts 39% of Winston-Salem households live in asset poverty Cities have long been thought of as places

Assets & opportunity ProfILe: winston-salem ANd forsyth CoUNtY ASSETS & OPPORTUNITY PROFILE KeY HIgHLIgHts 39% of Winston-Salem households live in asset poverty Cities have long been thought of as places

Mortgage Lending Compliance Issues Session 1. Higher Priced and High-Cost Mortgages

Mortgage Lending Compliance Issues Session 1 Higher Priced and High-Cost Mortgages Today s Topics Learn the definitions of Higher Priced and High Cost Mortgages and how to test to determine if you are

Mortgage Lending Compliance Issues Session 1 Higher Priced and High-Cost Mortgages Today s Topics Learn the definitions of Higher Priced and High Cost Mortgages and how to test to determine if you are

RE: Comments/RIN AA65, the Proposed Rule on the Enterprises Housing Goals

October 28, 2014 Mr. Alfred M. Pollard General Counsel Federal Housing Finance Agency 400 Seventh St., S.W. Washington, DC 20024 RE: Comments/RIN 25690-AA65, the Proposed Rule on the Enterprises Housing

October 28, 2014 Mr. Alfred M. Pollard General Counsel Federal Housing Finance Agency 400 Seventh St., S.W. Washington, DC 20024 RE: Comments/RIN 25690-AA65, the Proposed Rule on the Enterprises Housing

1. Sustained increases in population and job growth. According to US Census information, the

Financial Crisis Inquiry Commission Phil Angelides, Chairman Sacramento Field Hearing September 23, 2010 Thomas C. Putnam, President Putnam Housing Finance Consulting Mr. Chairman and Commissioners Thank

Financial Crisis Inquiry Commission Phil Angelides, Chairman Sacramento Field Hearing September 23, 2010 Thomas C. Putnam, President Putnam Housing Finance Consulting Mr. Chairman and Commissioners Thank

Quo Vadis? Where To for Affordable Mortgage Finance?

Quo Vadis? Where To for Affordable Mortgage Finance? Remarks by Roberto G. Quercia to Fannie Mae s Affordable Housing Advisory Council Washington, D.C. April 17, 2012 It has been a long time since I gave

Quo Vadis? Where To for Affordable Mortgage Finance? Remarks by Roberto G. Quercia to Fannie Mae s Affordable Housing Advisory Council Washington, D.C. April 17, 2012 It has been a long time since I gave

HMDA / Regulation C Amendments New 1003 Application

HMDA / Regulation C Amendments New 1003 Application January 2017 1Nations Direct Mortgage, LLC Mission Statement - To lead the third party residential mortgage industry by providing products and services

HMDA / Regulation C Amendments New 1003 Application January 2017 1Nations Direct Mortgage, LLC Mission Statement - To lead the third party residential mortgage industry by providing products and services

Fundamentals of the Opportunity Finance Industry Certificate in Community Development Finance

Fundamentals of the Opportunity Finance Industry Certificate in Community Development Finance Day 2 Presentation Fundamentals of the Opportunity Finance Industry Certificate in Community Development Finance

Fundamentals of the Opportunity Finance Industry Certificate in Community Development Finance Day 2 Presentation Fundamentals of the Opportunity Finance Industry Certificate in Community Development Finance

Update On Mortgage Originations, Delinquency and Foreclosures In Maryland

Update On Mortgage Originations, Delinquency and Foreclosures In Maryland The Reinvestment Fund builds wealth and opportunity for low-wealth people and places through the promotion of socially and environmentally

Update On Mortgage Originations, Delinquency and Foreclosures In Maryland The Reinvestment Fund builds wealth and opportunity for low-wealth people and places through the promotion of socially and environmentally