WHAT YOU NEED TO KNOW ABOUT THE DBZ LOAN APPLICATION PROCESS

|

|

|

- Estella Morton

- 6 years ago

- Views:

Transcription

1 WHAT YOU NEED TO KNOW ABOUT THE DBZ LOAN APPLICATION PROCESS i) Which Zambian Sectors Does DBZ Finance? DBZ finances projects in all sectors of the Zambian economy which include, inter alia: Agriculture, Agro Processing, Manufacturing, Construction, Mining, Services, Real Estate, Medical, Education, Transport and Energy sectors. ii) Who Is Eligible To Apply For These Funds? The applicant should be a Zambian Registered Limited Company with a shareholding structure of at least 50% Zambian owned. iii) Which Business Categories Does DBZ Finance & What Is The Cost Of Funds? The Bank finances businesses which fall in the Small, Medium and Large scale categories. The table below shows these categories: Organization Size Employee Assets Turnover KWACHA KWACHA Small ,000,000-6,000,000-18,600,000 18,600,000 Medium ,600,001-93,000,000 18,600,001-93,000,000 Large >300 >93,000,000 >93,000,000 - Small and Medium Enterprises - Which according to the DBZ classification are Registered Limited Companies with an annual turnover between K6 million to K93 million and employing up to 300 people. Depending on the availability and cost of funds, SMEs are given incentivized low interest rates. For instance, the US$20 million euro bond proceed received by the Bank from government was lent out at interest rates based on inflation rate plus a margin of 2%, i.e 9% to SMEs. - Large Enterprises These are registered companies which have an annual turnover of above K93 million and employing more than 300 people. Large

2 enterprises are normally funded from the DBZ funds which are pegged at BoZ Policy rate plus a margin of 9%. iv) Do I Need To Pledge Security To Access These Funds? Security is required and the Bank usually prefers landed property of good value with a minimum Loan: Security Ratio of (1:1.5 or more). v) What Is The Minimum Loan Amount That One Can Apply For? Minimum Loan Amount is K1 million vi) What Tenure Is Applied On DBZ Loans? DBZ loan tenures are classified as short term, medium term or long term as follows: Short term: 12 months Medium term: 1 to 5 years Long term: above 5 years vii) What Information Does DBZ Need To Process My Application The Bank requires that the applicant submits a Business Plan/Business Proposal with all supporting documentation. Examples of supporting documentation includes inter alia; - Zema clearance certificate for certain agricultural, mining & construction projects - ZRA tax clearance certificate - Audited financials & management accounts for established businesses For a complete list of supporting documentation, refer to the application guideline. viii) Are There Any Fees or Service Charges Payable By The Applicant?

3 There are two types of fees payable by an applicant at application and after approval and these are: - Appraisal Fee this is a Non-Refundable Fee of 1% of the loan amount which is payable upfront for assessment of the viability and profitability of the project before approval. - Facility Fee This is 2% of the loan amount which is payable upon the client accepting the loan offer by virtue of signing the facility letter. Simply put, a facility fee is a service charge which the Bank will use to service and manage the loan over its life span. ix) Where And How Do I Submit My Application? The application or business plan should be submitted in hard copy and addressed to the Managing Director as follows: THE MANAGING DIRECTOR DEVELOPMENT BANK OF ZAMBIA DEVELOPMENT HOUSE P.O. BOX 33955, KATONDO STREET, LUSAKA Alternatively, an application can be submitted to our regional office in Ndola and should be addressed to the Managing Director as shown above. This application will immediately be channeled to the Regional Office in Ndola.

4 KEY DEVELOPMENT STATISTICS & DATA The development Bank of Zambia continues to lead the way in providing affordable development finance to all sectors of the Zambian economy. It is the Banks desire to provide equitable growth opportunities to both men and women, aid government in its process of fostering financial inclusion across the country and provide the most affordable project finance to the Zambian economy. Below are some key development statistics which reinforce the Banks commitment to meeting its mandate as stipulated above: JOB CREATION DBZ has continued to stimulate growth in the Zambian economy by providing affordable development finance across all sectors of the economy which is a catalyst for job creation. The Bank estimates that from January 2012 to October 2014, its interventions in the Zambian economy through project finance has catalyzed the creation of approximately 6,698 (direct & indirect) jobs. It is also estimated that 2,493 and 4,205 of these jobs were estimated to be females and males, respectively. It was discovered that the skewedness of jobs towards men has been mainly due to the construction, financial and agricultural sectors which employees mostly males over females. The table below summarizes these statistics: S/N JOBS CREATED GENDER Sector Direct Jobs Indirect Jobs Female Male 1 Education Agriculture Manufacturing Construction 290 1, ,947 5 Financial 93 1, ,033 6 Tourism/Hospitality Service Health Energy Real Estate (Direct) Real Estate(Apex Lending) Telcoms Subtotal ,670 2,493 4,205 Grand Total 6,698 6,698

5 FINANCIAL INCLUSION & GENDER SENSITIVITY The Bank has continued to lend to all the specified sectors crucial to the country s economic development, with an approach of inclusion ensuring that women entrepreneurs also have access to the credit facilities the bank is offering. The Chart below gives a percentage distribution of the direct lending portfolio by province. Although the Bank is currently funding projects in all 10 provinces, there is still need to ensure that more projects are funded in all other provinces other than Lusaka which currently enjoys 65% of the total portfolio. Furthermore, the Bank acknowledges the importance of gender balance and the inclusion of women entrepreneurs in national development. It is for this reason that the Bank has deliberately decided to increase the number of women ownership within these projects by, for instance, advocating for deliberate inclusion of women partners within business shareholding structures (jointly run businesses) and giving priority to female entrepreneurs who approach the Bank for funding. Despite these measures the Bank acknowledges that there is still need for more women to become enterprising and narrow the playing field with their male counterparts. The Chart below gives a summary of the gender distribution under the direct lending portfolio:

and the Rural Finance Programme (RFP).")

6 CONSOLIDATED DBZ PORTFOLIO & DIRECT LENDING EXPOSURE BY SECTOR The consolidated DBZ portfolio consists mainly of 3 sub-portfolios namely: Direct Lending, Wholesale lending (Enterprise Development Program) and the Rural Finance Programme (RFP). The direct lending portfolio is the largest portfolio with 91% of the total banks exposure, followed by wholesale lending and RFP with 6% and 3%, respectively. The chart below gives a graphical representation of the banks current consolidated exposure.

sectors.")

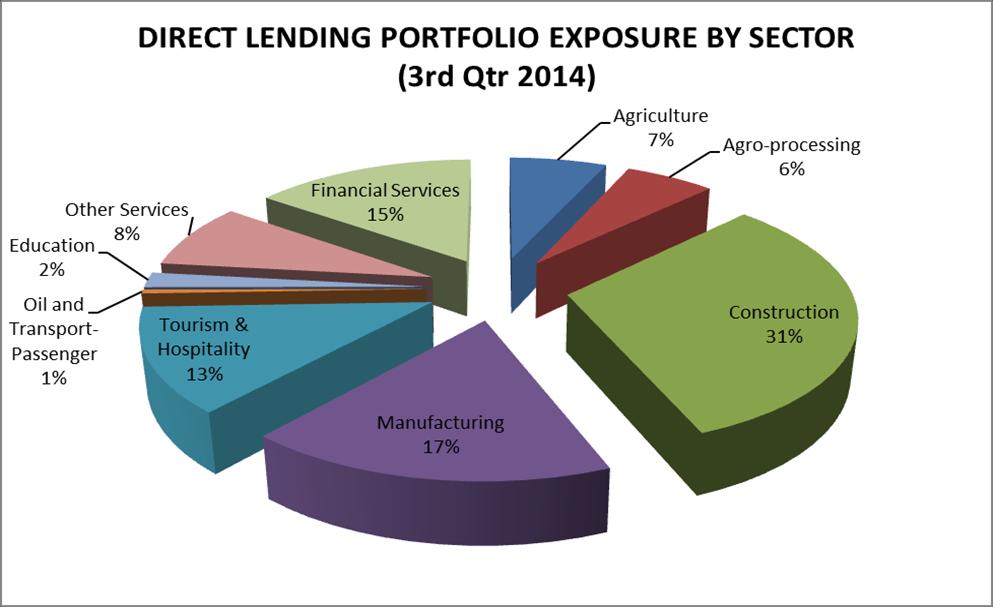

7 An in-depth analysis of the sectorial distribution of the Direct Lending portfolio reveals that the Bank top 3 exposures are in the Construction (31%), Manufacturing (17%) and Financial Services (15%) sectors. It is not surprising to note that the Bank is highly exposed to the construction sector given the priority the sector has received from government in recent past, which has seen several established companies and SME s approach the bank for funding to purchase machinery and equipment. The Agriculture and Agro-Processing Sectors have also been vibrant sectors particularly for SME s who engage in deferent forms of Agriculture production and Agro-Processing such as egg production, aqua culture, commercial maize farming and pig farming among other things. The chart below summarizes all of the above:

8

9 FINANCIAL DEVELOPMENT INDICATORS The Development Bank of Zambia continues to lead the way in providing affordable finance in the required quantities to the Zambian businesses and entrepreneurs. With interest rates from as low as 9% for SME s (depending on the availability of funds) the Bank continues to fulfill its mandate of been Zambia s premier development finance partner by providing low cost and flexible credit. The Bank s loan portfolio is skewed towards low quantity borrowers who are mostly SME s with 40.7% of the entire portfolio borrowing below K2 million across all sectors. The chart below summaries this distribution: The Banks exposure in foreign currency which is predominantly the US Dollar is minimum with 85% of the entire portfolio been Kwacha dominated. This is simply because most of money is used locally for purchase of machinery and equipment, construction and working capital purposes hence it is kwacha dominated. Firms which require dollar disbursements use that money for importation of specialized equipment and machinery which cannot be acquired locally. The chart below gives a summary of this distribution:

10

Contributing family workers and poverty. Shebo Nalishebo

Contributing family workers and poverty Shebo Nalishebo January 2013 Zambia Institute for Policy Analysis & Research 2013 Zambia Institute for Policy Analysis & Research (ZIPAR) CSO Annex Building Cnr

Contributing family workers and poverty Shebo Nalishebo January 2013 Zambia Institute for Policy Analysis & Research 2013 Zambia Institute for Policy Analysis & Research (ZIPAR) CSO Annex Building Cnr

National budget brief Review of 2016 social sector budget allocations

ZAMBIA National budget brief Review of 2016 social sector budget allocations UNICEF Zambia The aim of this budget brief is to improve awareness and understanding of allocations to social sectors health,

ZAMBIA National budget brief Review of 2016 social sector budget allocations UNICEF Zambia The aim of this budget brief is to improve awareness and understanding of allocations to social sectors health,

Central Bank of Sudan Microfinance Unit

Central Bank of Sudan Microfinance Unit Role & Mission April 2007 Mutwakil Bakri Why Microfinance Matters? Poverty Map in Sudan: 76% Under Poverty Line,70% in Rural Deprived Areas Demand Gap:only 1-3%

Central Bank of Sudan Microfinance Unit Role & Mission April 2007 Mutwakil Bakri Why Microfinance Matters? Poverty Map in Sudan: 76% Under Poverty Line,70% in Rural Deprived Areas Demand Gap:only 1-3%

Financial and Other Statistics 2017

Financial and Other Statistics 2017 i Financial and Other Statistics MISSION STATEMENT To achieve and maintain price and financial system stability to foster sustainable economic development Contents Financial

Financial and Other Statistics 2017 i Financial and Other Statistics MISSION STATEMENT To achieve and maintain price and financial system stability to foster sustainable economic development Contents Financial

AFIN208: PRINCIPLES OF TAXATION

SCHOOL OF BUSINESS, ECONOMICS AND MANAGEMENT AFIN208: PRINCIPLES OF TAXATION Page 1 of 6 UNIVERSITY OF LUSAKA BACHELOR OF ACCOUNTANCY PROGRAMME AFIN208 TAXATION COURSE OBJECTIVES The objectives of this

SCHOOL OF BUSINESS, ECONOMICS AND MANAGEMENT AFIN208: PRINCIPLES OF TAXATION Page 1 of 6 UNIVERSITY OF LUSAKA BACHELOR OF ACCOUNTANCY PROGRAMME AFIN208 TAXATION COURSE OBJECTIVES The objectives of this

MicroBank. Facilitating the access to microfinance

MicroBank The Social Bank of la Caixa Facilitating the access to microfinance Conference on Microfinance in Europe Brussels - November 10, 2010 2 la Caixa Savings Bank MicroBank was created in 2007 as

MicroBank The Social Bank of la Caixa Facilitating the access to microfinance Conference on Microfinance in Europe Brussels - November 10, 2010 2 la Caixa Savings Bank MicroBank was created in 2007 as

Quick Facts. n n. Total population of Zambia million Total adult population 8.1 million. o o

FinScope Zambia 2015 Quick Facts n n Total population of Zambia 1 15.5 million Total adult population 8.1 million o o 54.8% of adults live in rural areas; 45.2% in urban areas 49.0% of adults are male;

FinScope Zambia 2015 Quick Facts n n Total population of Zambia 1 15.5 million Total adult population 8.1 million o o 54.8% of adults live in rural areas; 45.2% in urban areas 49.0% of adults are male;

AMFI SECTOR REPORT DECEMBER 2017

AMFI SECTOR REPORT DECEMBER 2017 1.1.0: INTRODUCTION 1.1.1: BACKGROUND INFORMATION The Association for Microfinance Institutions (AMFI) is a member-based organization that was established and registered

AMFI SECTOR REPORT DECEMBER 2017 1.1.0: INTRODUCTION 1.1.1: BACKGROUND INFORMATION The Association for Microfinance Institutions (AMFI) is a member-based organization that was established and registered

Development Bank of Zambia ZMK 150 Billion Medium Term Note ( MTN ) Programme Brings Multiple Firsts to the Market

Programme Brings Multiple Firsts to the Market") For immediate release Development Bank of Zambia ZMK 150 Billion Medium Term Note ( MTN ) Programme Brings Multiple Firsts to the Market Issue and listing of ZMK 68.620 Billion Senior Unsecured Notes under

For immediate release Development Bank of Zambia ZMK 150 Billion Medium Term Note ( MTN ) Programme Brings Multiple Firsts to the Market Issue and listing of ZMK 68.620 Billion Senior Unsecured Notes under

Caleb M Fundanga: Fourth quarter 2010 media briefing

Caleb M Fundanga: Fourth quarter 2010 media briefing Presented by Dr Caleb M Fundanga, Governor of the Bank of Zambia, Lusaka, 18 February 2011. * * * Executive summary 1. This brief examines monetary

Caleb M Fundanga: Fourth quarter 2010 media briefing Presented by Dr Caleb M Fundanga, Governor of the Bank of Zambia, Lusaka, 18 February 2011. * * * Executive summary 1. This brief examines monetary

Loans for rural development , Estonia. Case Study. - EAFRD - EUR 36 million - Rural enterprise support - Estonia

- EAFRD - EUR 36 million - Rural enterprise support - Estonia Loans for rural development 2014-2020, Estonia... supporting rural growth and investment through financial instruments... DISCLAIMER This document

- EAFRD - EUR 36 million - Rural enterprise support - Estonia Loans for rural development 2014-2020, Estonia... supporting rural growth and investment through financial instruments... DISCLAIMER This document

Business Partners Limited SME Confidence Index

Business Partners Limited SME Confidence Index Fourth Quarter of 2017: October December Issued February 2018 1 RATIONALE FOR THE BUSINESS PARTNERS LIMITED SME CONFIDENCE INDEX SMEs are often punted as

Business Partners Limited SME Confidence Index Fourth Quarter of 2017: October December Issued February 2018 1 RATIONALE FOR THE BUSINESS PARTNERS LIMITED SME CONFIDENCE INDEX SMEs are often punted as

fiji Regional Forum Gender-responsive Budgeting in Asia and the Pacific

fiji Regional Forum Gender-responsive Budgeting in Asia and the Pacific Held at the United Nations Conference Centre in Bangkok, Thailand on the 18 th July, 2017 Context International Treaties: Convention

fiji Regional Forum Gender-responsive Budgeting in Asia and the Pacific Held at the United Nations Conference Centre in Bangkok, Thailand on the 18 th July, 2017 Context International Treaties: Convention

REQUEST FOR PROPOSALS

BANK Of ZAMBIA REQUEST FOR PROPOSALS GRAPHIC DESIGN FOR THE ZAMBIA INTERNATIONAL TRADE FAIR (ZITF) AND ZAMBIA AGRICULTURE AND COMMERCIAL SHOW (ZACS) STANDS BANK OF ZAMBIA RFP NO. IFB NO. BOZ/PMS/ONB/09/2017

BANK Of ZAMBIA REQUEST FOR PROPOSALS GRAPHIC DESIGN FOR THE ZAMBIA INTERNATIONAL TRADE FAIR (ZITF) AND ZAMBIA AGRICULTURE AND COMMERCIAL SHOW (ZACS) STANDS BANK OF ZAMBIA RFP NO. IFB NO. BOZ/PMS/ONB/09/2017

OFFICIAL -1 L(-L DOCUMENTS. Between. and

Public Disclosure Authorized OFFICIAL -1 L(-L DOCUMENTS ADDENDUM No 2 TO ADMINISTRATION AGREEMENT Between Public Disclosure Authorized Public Disclosure Authorized the EUROPEAN UNION (represented by the

Public Disclosure Authorized OFFICIAL -1 L(-L DOCUMENTS ADDENDUM No 2 TO ADMINISTRATION AGREEMENT Between Public Disclosure Authorized Public Disclosure Authorized the EUROPEAN UNION (represented by the

Technical Assistance Consultant s Report

Technical Assistance Consultant s Report Project Number: 49273 January 2017 Sri Lanka: Small and Medium-Sized Enterprises Line of Credit Project (Financed by the Japan Fund for Poverty Reduction) Prepared

Technical Assistance Consultant s Report Project Number: 49273 January 2017 Sri Lanka: Small and Medium-Sized Enterprises Line of Credit Project (Financed by the Japan Fund for Poverty Reduction) Prepared

Financing Agriculture Forum 2013: Profitable Agricultural Banking Colombo, Sri Lanka. Florence Kariuki August 2013

Financing Agriculture Forum 2013: Profitable Agricultural Banking Colombo, Sri Lanka Florence Kariuki August 2013 Introduction Equity Bank was founded as Equity Building Society (EBS) in October 1984 and

Financing Agriculture Forum 2013: Profitable Agricultural Banking Colombo, Sri Lanka Florence Kariuki August 2013 Introduction Equity Bank was founded as Equity Building Society (EBS) in October 1984 and

Fiji Agricultural Partnership Project (FAPP) Negotiated financing agreement

Negotiated financing agreement") Document: EB 2015/LOT/P.6/Sup.1 Date: 10 April 2015 Distribution: Public Original: English E Republic of Fiji Fiji Agricultural Partnership Project (FAPP) Negotiated financing agreement For: Information

Document: EB 2015/LOT/P.6/Sup.1 Date: 10 April 2015 Distribution: Public Original: English E Republic of Fiji Fiji Agricultural Partnership Project (FAPP) Negotiated financing agreement For: Information

Bank of Zambia Monetary Policy Statement

Bank Of Zambia Bank of Zambia Monetary Policy Statement JULY DECEMBER 004 Bank of Zambia MISSION STATEMENT The principal purpose of the Bank of Zambia is to formulate and implement monetary and supervisory

Bank Of Zambia Bank of Zambia Monetary Policy Statement JULY DECEMBER 004 Bank of Zambia MISSION STATEMENT The principal purpose of the Bank of Zambia is to formulate and implement monetary and supervisory

Democratic Socialist Republic of Sri Lanka. Smallholder Agribusiness Partnerships (SAP) Programme. Negotiated financing agreement

Programme. Negotiated financing agreement") Document: EB 2017/120/R.13/Sup.1 Agenda: 9(b)(iii) Date: 8 April 2017 Distribution: Public Original: English E Democratic Socialist Republic of Sri Lanka Smallholder Agribusiness Partnerships (SAP) Programme

Document: EB 2017/120/R.13/Sup.1 Agenda: 9(b)(iii) Date: 8 April 2017 Distribution: Public Original: English E Democratic Socialist Republic of Sri Lanka Smallholder Agribusiness Partnerships (SAP) Programme

BANK of ZAMBIA REQUIREMENTS FOR SETTING UP A BANK IN ZAMBIA

BANK of ZAMBIA REQUIREMENTS FOR SETTING UP A BANK IN ZAMBIA 1 PROCEDURES AND REQUIREMENTS FOR SETTING UP A BANKING INSTITUTION UNDER THE BFSA IN ZAMBIA INTRODUCTION The Banking and Financial Services Act

BANK of ZAMBIA REQUIREMENTS FOR SETTING UP A BANK IN ZAMBIA 1 PROCEDURES AND REQUIREMENTS FOR SETTING UP A BANKING INSTITUTION UNDER THE BFSA IN ZAMBIA INTRODUCTION The Banking and Financial Services Act

Brief description, overall objective and project objectives with indicators

Sri Lanka: NDB IV (Promotion of the private sector) Ex post evaluation OECD sector BMZ project ID 1999 65 062 Project executing agency Consultant 24030 - Financial institutions of the formal financial

Sri Lanka: NDB IV (Promotion of the private sector) Ex post evaluation OECD sector BMZ project ID 1999 65 062 Project executing agency Consultant 24030 - Financial institutions of the formal financial

Correlation of Personal Factors on Unemployment, Severity of Poverty and Migration in the Northeastern Region of Thailand

Correlation of Personal Factors on Unemployment, Severity of Poverty and Migration in the Northeastern Region of Thailand Thitiwan Sricharoen Abstract This study examines characteristics of unemployment

Correlation of Personal Factors on Unemployment, Severity of Poverty and Migration in the Northeastern Region of Thailand Thitiwan Sricharoen Abstract This study examines characteristics of unemployment

REPUBLIC OF ZAMBIA CENTRAL STATISTICAL OFFICE PRELIMINARY RESULTS OF THE 2012 LABOUR FORCE SURVEY

REPUBLIC OF ZAMBIA CENTRAL STATISTICAL OFFICE PRELIMINARY RESULTS OF THE 2012 LABOUR FORCE SURVEY This report presents preliminary results of the 2012 Labour Force Survey. The results presented herein

REPUBLIC OF ZAMBIA CENTRAL STATISTICAL OFFICE PRELIMINARY RESULTS OF THE 2012 LABOUR FORCE SURVEY This report presents preliminary results of the 2012 Labour Force Survey. The results presented herein

Our Expertise. IFC blends investment with advice and resource mobilization to help the private sector advance development.

Our Expertise IFC blends investment with advice and resource mobilization to help the private sector advance development. 76 IFC ANNUAL REPORT 2016 Where We Work As the largest global development institution

Our Expertise IFC blends investment with advice and resource mobilization to help the private sector advance development. 76 IFC ANNUAL REPORT 2016 Where We Work As the largest global development institution

OFFICIAL DOCUMENTS. The World Bank. Public Disclosure Authorized. Public Disclosure Authorized

Public Disclosure Authorized OFFICIAL DOCUMENTS The World Bank 1818 H Street N.W. (202) 473-1000 INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT Washington, D.C. 20433 Cable Address: INTBAFRAD INTERNATIONAL

Public Disclosure Authorized OFFICIAL DOCUMENTS The World Bank 1818 H Street N.W. (202) 473-1000 INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT Washington, D.C. 20433 Cable Address: INTBAFRAD INTERNATIONAL

Ghana : Financial services for women entrepreneurs in the informal sector

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized No. 136 June 1999 Findings occasionally reports on development initiatives not assisted

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized No. 136 June 1999 Findings occasionally reports on development initiatives not assisted

CHAPTER 425 THE SMALL ENTERPRISES DEVELOPMENT ACT PART I PRELIMINARY. Section 1. Short title and commencement 2. Interpretation PART II

CHAPTER 425 THE SMALL ENTERPRISES DEVELOPMENT ACT ARRANGEMENT OF SECTIONS PART I PRELIMINARY Section 1. Short title and commencement 2. Interpretation PART II THE SMALL ENTERPRISE DEVELOPMENT BOARD 3.

CHAPTER 425 THE SMALL ENTERPRISES DEVELOPMENT ACT ARRANGEMENT OF SECTIONS PART I PRELIMINARY Section 1. Short title and commencement 2. Interpretation PART II THE SMALL ENTERPRISE DEVELOPMENT BOARD 3.

PROJECT INFORMATION DOCUMENT (PID) CONCEPT STAGE Report No.: AB5715 Project Name. Cambodia Agribusiness SME Access to Finance Project Region

CONCEPT STAGE Report No.: AB5715 Project Name. Cambodia Agribusiness SME Access to Finance Project Region") Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized PROJECT INFORMATION DOCUMENT (PID) CONCEPT STAGE Report No.: AB5715 Project Name Cambodia

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized PROJECT INFORMATION DOCUMENT (PID) CONCEPT STAGE Report No.: AB5715 Project Name Cambodia

Financing Profiles SMALL BUSINESS. Women Entrepreneurs. SME Financing Data Initiative October 2010

SMALL BUSINESS Financing Profiles SME Financing Data Initiative October Women Entrepreneurs Owen Jung Small Business and Tourism Branch, Industry Canada highlights $ $ female-owned small and medium-sized

SMALL BUSINESS Financing Profiles SME Financing Data Initiative October Women Entrepreneurs Owen Jung Small Business and Tourism Branch, Industry Canada highlights $ $ female-owned small and medium-sized

Non Bank Financial Institutions Supervision Department. BANK of ZAMBIA REQUIREMENTS FOR SETTING UP A NON BANK FINANCIAL INSTITUTION IN ZAMBIA

BANK of ZAMBIA REQUIREMENTS FOR SETTING UP A NON BANK FINANCIAL INSTITUTION IN ZAMBIA 1 REQUIREMENTS FOR SETTING UP A NON-BANK FINANCIAL INSTITUTION IN ZAMBIA INTRODUCTION The Banking and Financial Services

BANK of ZAMBIA REQUIREMENTS FOR SETTING UP A NON BANK FINANCIAL INSTITUTION IN ZAMBIA 1 REQUIREMENTS FOR SETTING UP A NON-BANK FINANCIAL INSTITUTION IN ZAMBIA INTRODUCTION The Banking and Financial Services

ANNEX 2 to the Call for Expression of Interest No JER-00. Part I: Description of the Financial F

Investícia do Vašej budúcnosti ANNEX 2 to the Call for Expression of Interest No JER-00 First Loss Portfolio Guarantee Financial Instrument: Description and Selection Criteria Part I: Description of the

Investícia do Vašej budúcnosti ANNEX 2 to the Call for Expression of Interest No JER-00 First Loss Portfolio Guarantee Financial Instrument: Description and Selection Criteria Part I: Description of the

A.ANITHA Assistant Professor in BBA, Sree Saraswathi Thyagaraja College, Pollachi

THE ROLE OF PARALLEL MICRO FINANCE INSTITUTIONS IN POVERTY ALLEVIATION IN RURAL TAMILNADU A STUDY WITH SPECIAL REFERENCE TO UDUMALPET TALUK, TIRUPUR DISTRICT A.ANITHA Assistant Professor in BBA, Sree Saraswathi

THE ROLE OF PARALLEL MICRO FINANCE INSTITUTIONS IN POVERTY ALLEVIATION IN RURAL TAMILNADU A STUDY WITH SPECIAL REFERENCE TO UDUMALPET TALUK, TIRUPUR DISTRICT A.ANITHA Assistant Professor in BBA, Sree Saraswathi

Retirement Savings Account (RSA) Membership Distribution

Membership Distribution") Retirement Savings Account (RSA) Membership Distribution (Q1 2017) Report Date: April 2017 Data Source: National Bureau of Statistics / National Pension Commission Contents Executive Summary Retirement

Retirement Savings Account (RSA) Membership Distribution (Q1 2017) Report Date: April 2017 Data Source: National Bureau of Statistics / National Pension Commission Contents Executive Summary Retirement

Retirement Plan Coverage of Baby Boomers: Analysis of 1998 SIPP Data. Satyendra K. Verma

A Data and Chart Book by Satyendra K. Verma August 2005 Retirement Plan Coverage of Baby Boomers: Analysis of 1998 SIPP Data by Satyendra K. Verma August 2005 Components Retirement Plan Coverage in 1998:

A Data and Chart Book by Satyendra K. Verma August 2005 Retirement Plan Coverage of Baby Boomers: Analysis of 1998 SIPP Data by Satyendra K. Verma August 2005 Components Retirement Plan Coverage in 1998:

Agricultural and Rural Finance

Chapter8 Annual Agricultural Credit Programme 8.1 In Bangladesh about 70 percent of the poor people live in rural areas and are concentrated in the agriculture sector. The performance of the agriculture

Chapter8 Annual Agricultural Credit Programme 8.1 In Bangladesh about 70 percent of the poor people live in rural areas and are concentrated in the agriculture sector. The performance of the agriculture

Agenda item 12: Consideration of accreditation proposals

Page 5 (h) (j) (k) (l) (m) (n) Also requests the Appointment Committee to provide additional recommendations on the salary levels for consideration by the Board at its eleventh meeting; Decides that the

Page 5 (h) (j) (k) (l) (m) (n) Also requests the Appointment Committee to provide additional recommendations on the salary levels for consideration by the Board at its eleventh meeting; Decides that the

The Aboriginal Economic Benchmarking Report. Core Indicator 1: Employment. The National Aboriginal Economic Development Board June, 2013

The Economic Benchmarking Report Core Indicator 1: Employment The National Economic Development Board June, 2013 The National Economic Development Board 10 Wellington St., 9th floor Gatineau, (Quebec)

The Economic Benchmarking Report Core Indicator 1: Employment The National Economic Development Board June, 2013 The National Economic Development Board 10 Wellington St., 9th floor Gatineau, (Quebec)

ALBERTA LABOUR FORCE PROFILES Aboriginal People in the Labour Force Alberta Labour Force Profiles

ALBERTA LABOUR FORCE PROFILES Aboriginal People in the Labour Force 2009 Alberta Labour Force Profiles Aboriginal People 2011 Highlights 1. Population of More than 60.0% of the working age population (WAP)

ALBERTA LABOUR FORCE PROFILES Aboriginal People in the Labour Force 2009 Alberta Labour Force Profiles Aboriginal People 2011 Highlights 1. Population of More than 60.0% of the working age population (WAP)

Technical Assistance Consultant s Report

Technical Assistance Consultant s Report Project Number: 49273 May 2017 Sri Lanka: Small and Medium-Sized Enterprises Line of Credit Project (Financed by the Japan Fund for Poverty Reduction) Prepared

Technical Assistance Consultant s Report Project Number: 49273 May 2017 Sri Lanka: Small and Medium-Sized Enterprises Line of Credit Project (Financed by the Japan Fund for Poverty Reduction) Prepared

FISCAL STRATEGY PAPER

REPUBLIC OF KENYA MACHAKOS COUNTY GOVERNMENT THE COUNTY TREASURY MEDIUM TERM FISCAL STRATEGY PAPER ACHIEVING EQUITABLE SOCIAL AND ECONOMIC DEVELOPMENT IN MACHAKOS COUNTY FEBRUARY2014 Foreword This Fiscal

REPUBLIC OF KENYA MACHAKOS COUNTY GOVERNMENT THE COUNTY TREASURY MEDIUM TERM FISCAL STRATEGY PAPER ACHIEVING EQUITABLE SOCIAL AND ECONOMIC DEVELOPMENT IN MACHAKOS COUNTY FEBRUARY2014 Foreword This Fiscal

Ex post evaluation Georgia

Ex post evaluation Georgia Sector: Formal sector financial intermediaries (24030) Programme/Project: Agricultural financing programme (fiduciary holding) (BMZ No. 2011 66 552)* Implementing agency: three

Ex post evaluation Georgia Sector: Formal sector financial intermediaries (24030) Programme/Project: Agricultural financing programme (fiduciary holding) (BMZ No. 2011 66 552)* Implementing agency: three

MADAGASCAR PORTFOLIO REVIEW REPORT

AFRICAN DEVELOPMENT BANK AFRICAN DEVELOPMENT FUND MADAGASCAR PORTFOLIO REVIEW REPORT SOUTH REGION DEPARTMENT OCTOBER 2007 SCCD :N.A. i CURRENCY EQUIVALENTS (October 2007) UA1 = US$ 1.55665 UA1 = EURO 1.9786

AFRICAN DEVELOPMENT BANK AFRICAN DEVELOPMENT FUND MADAGASCAR PORTFOLIO REVIEW REPORT SOUTH REGION DEPARTMENT OCTOBER 2007 SCCD :N.A. i CURRENCY EQUIVALENTS (October 2007) UA1 = US$ 1.55665 UA1 = EURO 1.9786

THE INTERNATIONAL JOURNAL OF BUSINESS & MANAGEMENT

THE INTERNATIONAL JOURNAL OF BUSINESS & MANAGEMENT Lending to Micro Small and Medium Enterprises: An Analysis of Bank Approaches and Risk Perceptions Harsha S. Talaulikar Research Scholar, Department of

THE INTERNATIONAL JOURNAL OF BUSINESS & MANAGEMENT Lending to Micro Small and Medium Enterprises: An Analysis of Bank Approaches and Risk Perceptions Harsha S. Talaulikar Research Scholar, Department of

ALBERTA PROFILE: YOUTH

ALBERTA PROFILE: YOUTH IN THE LABOUR FORCE Prepared By:, Data Development and Evaluation Released: June 2003 Highlights Statistics Canada defines youth as those people between the ages of 15-24 years.

ALBERTA PROFILE: YOUTH IN THE LABOUR FORCE Prepared By:, Data Development and Evaluation Released: June 2003 Highlights Statistics Canada defines youth as those people between the ages of 15-24 years.

Financial Products to Promote Climate Change Resilience in Bolivia

Financial Products to Promote Climate Change Resilience in Bolivia Country / Region: Bolivia Project Id: PPCRBO602A Fund Name: PPCR Comment Type Commenter Name Commenter Profile Comment Date Comment 1

Financial Products to Promote Climate Change Resilience in Bolivia Country / Region: Bolivia Project Id: PPCRBO602A Fund Name: PPCR Comment Type Commenter Name Commenter Profile Comment Date Comment 1

ZAMBIA REVENUE AUTHORITY DIRECT TAXES DIVISION INCOME TAX (AMENDMENT) ACT 2006

ACT 2006") ZAMBIA REVENUE AUTHORITY DIRECT TAXES DIVISION INCOME TAX (AMENDMENT) ACT 2006 PRACTICE NOTE NO. 1/2006 CONTENTS 1. GENERAL 3 PAGE 2. SUMMARY OF THE PRINCIPAL CHANGES 4 3. COMMENTARY ON THE INCOME TAX

ZAMBIA REVENUE AUTHORITY DIRECT TAXES DIVISION INCOME TAX (AMENDMENT) ACT 2006 PRACTICE NOTE NO. 1/2006 CONTENTS 1. GENERAL 3 PAGE 2. SUMMARY OF THE PRINCIPAL CHANGES 4 3. COMMENTARY ON THE INCOME TAX

POLICY BRIEF Gender Analysis of the Ministry of Gender, Children, Disability and Social Welfare Budgets,

POLICY BRIEF Gender Analysis of the Ministry of Gender, Children, Disability and Social Welfare Budgets, 2009-2015 A call for equal and meaningful distribution of the National Cake October 2015 The Ministry

POLICY BRIEF Gender Analysis of the Ministry of Gender, Children, Disability and Social Welfare Budgets, 2009-2015 A call for equal and meaningful distribution of the National Cake October 2015 The Ministry

PMRC POLICY ANALYSIS: STATUTORY INSTRUMENT No. 55 OF 2013 GOVERNMENT TO MONITOR BALANCE OF PAYMENTS POLICY MONITORING AND RESEARCH CENTRE

POLICY MONITORING AND RESEARCH CENTRE PMRC POLICY ANALYSIS: STATUTORY INSTRUMENT No. 55 OF 2013 GOVERNMENT TO MONITOR BALANCE OF PAYMENTS Unlocking Zambia's Potential www.pmrczambia.org www.scribd.com/pmrczambia

POLICY MONITORING AND RESEARCH CENTRE PMRC POLICY ANALYSIS: STATUTORY INSTRUMENT No. 55 OF 2013 GOVERNMENT TO MONITOR BALANCE OF PAYMENTS Unlocking Zambia's Potential www.pmrczambia.org www.scribd.com/pmrczambia

TD/505. United Nations Conference on Trade and Development. Declaration of the Least Developed Countries. United Nations

United Nations United Nations Conference on Trade and Development Distr.: General 18 July 2016 Original: English TD/505 Fourteenth session Nairobi 17 22 July 2016 Declaration of the Least Developed Countries

United Nations United Nations Conference on Trade and Development Distr.: General 18 July 2016 Original: English TD/505 Fourteenth session Nairobi 17 22 July 2016 Declaration of the Least Developed Countries

SubC Imaging. Business Investment Corporation

SubC Imaging Business Investment Corporation p. 2 annual report 2013-14 p. 3 message from the chair As Chair of the Board of Directors of the Business Investment Corporation (BIC), I am pleased to present

SubC Imaging Business Investment Corporation p. 2 annual report 2013-14 p. 3 message from the chair As Chair of the Board of Directors of the Business Investment Corporation (BIC), I am pleased to present

SECTION- III RESULTS. Married Widowed Divorced Total

SECTION- III RESULTS The results of this survey are based on the data of 18890 sample households enumerated during four quarters of the year from July, 2001 to June, 2002. In order to facilitate computation

SECTION- III RESULTS The results of this survey are based on the data of 18890 sample households enumerated during four quarters of the year from July, 2001 to June, 2002. In order to facilitate computation

INDIA. GDP, and the 3 rd largest by purchasing power parity.

INDIA India s GDP has more than quadrupled since 1990; GDP per capita increased from $309 in 1991 to $14,77 in 2010. The annual median per capita income in India stood at $616 in 2013, the 99 th position

INDIA India s GDP has more than quadrupled since 1990; GDP per capita increased from $309 in 1991 to $14,77 in 2010. The annual median per capita income in India stood at $616 in 2013, the 99 th position

Microinsurance Technical Advisory Group. MICROINSURANCE LANDSCAPE - ZAMBIA MICROINSURANCE FOCUS NOTE No. 9 JUNE Funded by

Microinsurance Technical Advisory Group FOCUS NOTE No. 9 JUNE 2018 Funded by ABOUT THIS FOCUS NOTE Since 2009, the Technical Advisory Group for Microinsurance (TAG) has been spearheading the development

Microinsurance Technical Advisory Group FOCUS NOTE No. 9 JUNE 2018 Funded by ABOUT THIS FOCUS NOTE Since 2009, the Technical Advisory Group for Microinsurance (TAG) has been spearheading the development

NACD Public Company Governance Survey SELECTED MATERIALS

2018 2019 NACD Public Company Governance Survey SELECTED MATERIALS About Our Survey The 2018 2019 NACD Public Company Governance Survey presents findings from our annual questionnaire. This report details

2018 2019 NACD Public Company Governance Survey SELECTED MATERIALS About Our Survey The 2018 2019 NACD Public Company Governance Survey presents findings from our annual questionnaire. This report details

Research Brief 09/47

Research Brief 09/47 24.09.2009 WOMEN HAVE LONGER UNEMPLOYMENT SPELLS Seyfettin Gürsel, Burak Darbaz, Duygu Güner Executive Summary Turkish labor market exhibits substantial gender differences in labor-market

Research Brief 09/47 24.09.2009 WOMEN HAVE LONGER UNEMPLOYMENT SPELLS Seyfettin Gürsel, Burak Darbaz, Duygu Güner Executive Summary Turkish labor market exhibits substantial gender differences in labor-market

Summary report. Technical workshop on principles guiding new investments in agriculture: Screening of prospective investors and investment proposals

Summary report Technical workshop on principles guiding new investments in agriculture: Screening of prospective investors and investment proposals Lilongwe, Malawi, 26-27 September 2017 1 1. Introduction

Summary report Technical workshop on principles guiding new investments in agriculture: Screening of prospective investors and investment proposals Lilongwe, Malawi, 26-27 September 2017 1 1. Introduction

TAXATION PROGRAMME EXAMINATIONS CERTIFICATE LEVEL C5: INDIRECT TAXES THURSDAY 16 JUNE 2016 TOTAL MARKS 100: TIME ALLOWED: THREE (3) HOURS

HOURS") TAXATION PROGRAMME EXAMINATIONS CERTIFICATE LEVEL C5: INDIRECT TAXES THURSDAY 16 JUNE 2016 TOTAL MARKS 100: TIME ALLOWED: THREE (3) HOURS INSTRUCTIONS TO CANDIDATES 1. You have fifteen (15) minutes reading

TAXATION PROGRAMME EXAMINATIONS CERTIFICATE LEVEL C5: INDIRECT TAXES THURSDAY 16 JUNE 2016 TOTAL MARKS 100: TIME ALLOWED: THREE (3) HOURS INSTRUCTIONS TO CANDIDATES 1. You have fifteen (15) minutes reading

Follow-up by the European Commission to the EU-ACP JPA on the resolution on private sector development strategy, including innovation, for sustainable

Follow-up by the European Commission to the EU-ACP JPA on the resolution on private sector development strategy, including innovation, for sustainable Development. The European External Action Service

Follow-up by the European Commission to the EU-ACP JPA on the resolution on private sector development strategy, including innovation, for sustainable Development. The European External Action Service

EU financial instruments under the multiannual financial framework (MFF) 2021 to 2027:

2021 to 2027:") EU financial instruments under the multiannual financial framework (MFF) 2021 to 2027: Comments of UEAPME and AECM on the proposal of the European Commission for a regulation establishing the InvestEU

EU financial instruments under the multiannual financial framework (MFF) 2021 to 2027: Comments of UEAPME and AECM on the proposal of the European Commission for a regulation establishing the InvestEU

KCB GROUP PLC INVESTOR PRESENTATION. FY17 FINANCIAL RESULTS

KCB GROUP PLC INVESTOR PRESENTATION. FY17 FINANCIAL RESULTS JOSHUA OIGARA GROUP CEO & MD LAWRENCE KIMATHI GROUP CFO KCB Group at a glance 6,483 staff 15.7M Customers 153,431 shareholders Market Capitalization

KCB GROUP PLC INVESTOR PRESENTATION. FY17 FINANCIAL RESULTS JOSHUA OIGARA GROUP CEO & MD LAWRENCE KIMATHI GROUP CFO KCB Group at a glance 6,483 staff 15.7M Customers 153,431 shareholders Market Capitalization

Thirty-eighth Regular Meeting of the Executive Committee Program Budget. IICA/CE/Doc. 679 (18) - Original: Spanish

- Original: Spanish") Thirty-eighth Regular Meeting of the Executive Committee 2019 Program Budget IICA/CE/Doc. 679 (18) - Original: Spanish San Jose, Costa Rica 17-18 July 2018 Program Budget 2019 Inter-American Institute

Thirty-eighth Regular Meeting of the Executive Committee 2019 Program Budget IICA/CE/Doc. 679 (18) - Original: Spanish San Jose, Costa Rica 17-18 July 2018 Program Budget 2019 Inter-American Institute

Implications of the New Cooperative Act on the Financial Sector in Nepal

Implications of the New Cooperative Act on the Financial Sector in Nepal Definition A cooperative (also known as co-operative, co-op, or coop) is "an autonomous association of persons united voluntarily

Implications of the New Cooperative Act on the Financial Sector in Nepal Definition A cooperative (also known as co-operative, co-op, or coop) is "an autonomous association of persons united voluntarily

5 th ZAMBIA ALTERNATIVE MINING INDABA DECLARATION. 21 ST to 23 rd JUNE 2016 CRESTA GOLFVIEW HOTEL, LUSAKA, ZAMBIA. Preamble

5 th ZAMBIA ALTERNATIVE MINING INDABA Our Natural Resources, our Future! Extraction for Sustainable Development 21 ST to 23 rd JUNE 2016 CRESTA GOLFVIEW HOTEL, LUSAKA, ZAMBIA OBJECTIVES OF THE INDABA DECLARATION

5 th ZAMBIA ALTERNATIVE MINING INDABA Our Natural Resources, our Future! Extraction for Sustainable Development 21 ST to 23 rd JUNE 2016 CRESTA GOLFVIEW HOTEL, LUSAKA, ZAMBIA OBJECTIVES OF THE INDABA DECLARATION

Ex post evaluation Pakistan

Ex post evaluation Pakistan Sector: Informal/semi-formal financial intermediaries (CRS 24040) Project: A. Microfinancing programme (THB) (BMZ No. 2008 66 541)* B. Microfinancing programme (THB subordinated

Ex post evaluation Pakistan Sector: Informal/semi-formal financial intermediaries (CRS 24040) Project: A. Microfinancing programme (THB) (BMZ No. 2008 66 541)* B. Microfinancing programme (THB subordinated

AFME Response to European Commission Consultation on the EU2020 Industrial Policy Flagship Initiative

AFME Response to European Commission Consultation on the EU2020 Industrial Policy Flagship Initiative 7 th August 2012 Q2.2.1 Access to finance and risk capital: please explain the importance of the issue,

AFME Response to European Commission Consultation on the EU2020 Industrial Policy Flagship Initiative 7 th August 2012 Q2.2.1 Access to finance and risk capital: please explain the importance of the issue,

Experience with World Bank Conditionality. Stefan Koeberle and Thaddeus Malesa

Experience with World Bank Conditionality Stefan Koeberle and Thaddeus Malesa 1. Summary. This note summarizes key trends in the application of conditionality in World Bank policy-based lending since fiscal

Experience with World Bank Conditionality Stefan Koeberle and Thaddeus Malesa 1. Summary. This note summarizes key trends in the application of conditionality in World Bank policy-based lending since fiscal

Romero Catholic Academy Gender Pay Reporting Findings

Romero Catholic Academy Gender Pay Reporting Findings March 2018 Introduction In light of the recent Government Regulations regarding Mandatory Gender Pay Gap Reporting, Total Reward Group have been tasked

Romero Catholic Academy Gender Pay Reporting Findings March 2018 Introduction In light of the recent Government Regulations regarding Mandatory Gender Pay Gap Reporting, Total Reward Group have been tasked

THINK DEVELOPMENT THINK WIDER

THINK DEVELOPMENT THINK WIDER WIDER Development Conference 13-15 September 2018, Helsinki, Finland FINANCING THE ZAMBIA SOCIAL CASH TRANSFER SCALE UP A TAX BENEFIT MICRO SIMULATION ANALYSIS BASED ON MICROZAMOD

THINK DEVELOPMENT THINK WIDER WIDER Development Conference 13-15 September 2018, Helsinki, Finland FINANCING THE ZAMBIA SOCIAL CASH TRANSFER SCALE UP A TAX BENEFIT MICRO SIMULATION ANALYSIS BASED ON MICROZAMOD

**The chart below shows the amount of leisure time enjoyed by men and women of different employment status.

Bar Graph **The chart below shows the amount of leisure time enjoyed by men and women of different employment status. Write a report for a university lecturer describing the information shown below. Leisure

Bar Graph **The chart below shows the amount of leisure time enjoyed by men and women of different employment status. Write a report for a university lecturer describing the information shown below. Leisure

Comments to be submitted by March 15, Consultative Paper on the Review of the Microfinance Legislations

Consultative Paper on the Review of the Microfinance Legislations FEBRUARY 23 2018 CONSULTATIVE PAPER ON THE REVIEW OF THE MICROFINANCE LEGISLATIONS 1.0. Introduction The Central Bank of Kenya (CBK) is

Consultative Paper on the Review of the Microfinance Legislations FEBRUARY 23 2018 CONSULTATIVE PAPER ON THE REVIEW OF THE MICROFINANCE LEGISLATIONS 1.0. Introduction The Central Bank of Kenya (CBK) is

Decision 3/CP.17. Launching the Green Climate Fund

Decision 3/CP.17 Launching the Green Climate Fund The Conference of the Parties, Recalling decision 1/CP.16, 1. Welcomes the report of the Transitional Committee (FCCC/CP/2011/6 and Add.1), taking note

Decision 3/CP.17 Launching the Green Climate Fund The Conference of the Parties, Recalling decision 1/CP.16, 1. Welcomes the report of the Transitional Committee (FCCC/CP/2011/6 and Add.1), taking note

Blended finance in Myanmar. TCX s role in realizing financial inclusion through innovative partnerships in Myanmar

Blended finance in Myanmar TCX s role in realizing financial inclusion through innovative partnerships in Myanmar Table of Contents FOREWORD 4 TCX AT WORK 5 How local currency finance benefits Myanmar

Blended finance in Myanmar TCX s role in realizing financial inclusion through innovative partnerships in Myanmar Table of Contents FOREWORD 4 TCX AT WORK 5 How local currency finance benefits Myanmar

Alberta Self-Employment Profile

Alberta Self-Employment Profile 2016 Overview Self-employment represents the entrepreneurial spirit of Alberta. This spirit is at the heart of Alberta s vibrant economy. By creating employment, producing

Alberta Self-Employment Profile 2016 Overview Self-employment represents the entrepreneurial spirit of Alberta. This spirit is at the heart of Alberta s vibrant economy. By creating employment, producing

Research notes Basic Information on Recent Elderly Employment Trends in Japan

Research notes Basic Information on Recent Elderly Employment Trends in Japan Yutaka Asao The aim of this paper is to provide basic information on the employment of older people in Japan over the last

Research notes Basic Information on Recent Elderly Employment Trends in Japan Yutaka Asao The aim of this paper is to provide basic information on the employment of older people in Japan over the last

Monitoring the Performance

Monitoring the Performance of the South African Labour Market An overview of the Sector from 2014 Quarter 1 to 2017 Quarter 1 Factsheet 19 November 2017 South Africa s Sector Government broadly defined

Monitoring the Performance of the South African Labour Market An overview of the Sector from 2014 Quarter 1 to 2017 Quarter 1 Factsheet 19 November 2017 South Africa s Sector Government broadly defined

INTERNATIONAL FINANCE CORPORATION

Management s Discussion and Analysis and Condensed Consolidated Financial Statements September 30, 2013 (Unaudited) Page 2 Management s Discussion and Analysis September 30, 2013 Contents Page I Introduction...

Management s Discussion and Analysis and Condensed Consolidated Financial Statements September 30, 2013 (Unaudited) Page 2 Management s Discussion and Analysis September 30, 2013 Contents Page I Introduction...

PRO-POOR POLICIES FOR ZAMBIA

JCTR & CSPR SUBMISSION TO CSO/PF DIALOGUE 12 th April 2012 PRO-POOR POLICIES FOR ZAMBIA REVIEWING PRO-POOR POLICIES IN LIGHT OF SNDP PRIORITIES By Munyongo Lumba & Mwila Mulumbi 1 PRO-POOR DEVELOPMENT

JCTR & CSPR SUBMISSION TO CSO/PF DIALOGUE 12 th April 2012 PRO-POOR POLICIES FOR ZAMBIA REVIEWING PRO-POOR POLICIES IN LIGHT OF SNDP PRIORITIES By Munyongo Lumba & Mwila Mulumbi 1 PRO-POOR DEVELOPMENT

Module 4: Earnings, Inequality, and Labour Market Segmentation Gender Inequalities and Wage Gaps

Module 4: Earnings, Inequality, and Labour Market Segmentation Gender Inequalities and Wage Gaps Anushree Sinha Email: asinha@ncaer.org Sarnet Labour Economics Training For Young Scholars 1-13 December

Module 4: Earnings, Inequality, and Labour Market Segmentation Gender Inequalities and Wage Gaps Anushree Sinha Email: asinha@ncaer.org Sarnet Labour Economics Training For Young Scholars 1-13 December

Our Expertise. IFC blends investment with advice and resource mobilization to help the private sector advance development.

Our Expertise IFC blends investment with advice and resource mobilization to help the private sector advance development. Where We Work As the largest global development institution focused on the private

Our Expertise IFC blends investment with advice and resource mobilization to help the private sector advance development. Where We Work As the largest global development institution focused on the private

Credit Management. Principles of good lending

Credit Management Principles of good lending Safety Liquidity Profitability Spread Purpose End use Need based finance Viability oriented instead of security oriented lending Own stake National priorities

Credit Management Principles of good lending Safety Liquidity Profitability Spread Purpose End use Need based finance Viability oriented instead of security oriented lending Own stake National priorities

Annual Report 2016 Clarksons Platou Securities Group

Clarksons Platou Securities This Annual Report 2016 for the Clarksons Platou Securities is a translation of the Norwegian Annual Report for 2016. In case of discrepancy between the Norwegian language original

Clarksons Platou Securities This Annual Report 2016 for the Clarksons Platou Securities is a translation of the Norwegian Annual Report for 2016. In case of discrepancy between the Norwegian language original

«FICHE CONTRADICTOIRE» Joint Country Level Evaluation of Bangladesh. (*For details on the recommendations please refer to the main report)

") Ref. Ares(2016)5406779-16/09/2016 «FICHE CONTRADICTOIRE» Joint Country Level Evaluation of Bangladesh (*For details on the recommendations please refer to the main report) Recommendations Response of Commission

Ref. Ares(2016)5406779-16/09/2016 «FICHE CONTRADICTOIRE» Joint Country Level Evaluation of Bangladesh (*For details on the recommendations please refer to the main report) Recommendations Response of Commission

Moving toward. gender balance. in private equity and venture capital

Moving toward gender balance in private equity and venture capital Women are significantly underrepresented among the investment decision-makers at private equity and venture capital firms, as well as

Moving toward gender balance in private equity and venture capital Women are significantly underrepresented among the investment decision-makers at private equity and venture capital firms, as well as

2017 Alberta Labour Force Profiles Youth

2017 Alberta Labour Force Profiles Youth Highlights Population Statistics Labour Force Statistics 4 th highest proportion of youth in the working age population 1. 16.3% MB 2. 15.3% ON 2. 15.2% SK 4. 14.9%

2017 Alberta Labour Force Profiles Youth Highlights Population Statistics Labour Force Statistics 4 th highest proportion of youth in the working age population 1. 16.3% MB 2. 15.3% ON 2. 15.2% SK 4. 14.9%

Sefa Corporate Plan 2014/ /19 Joint Portfolio Committee Meeting on Economic Development and Small Business Development

Sefa Corporate Plan 2014/15 2018/19 Joint Portfolio Committee Meeting on Economic Development and Small Business Development Thakhani Makhuvha Chief Executive Officer The Small Enterprise Finance Agency

Sefa Corporate Plan 2014/15 2018/19 Joint Portfolio Committee Meeting on Economic Development and Small Business Development Thakhani Makhuvha Chief Executive Officer The Small Enterprise Finance Agency

Financing of the Poverty Reduction Programme

Chapter 15 Financing of the Poverty Reduction Programme 15.1 Underlying Considerations Several underlying considerations are noteworthy when looking at the financial resource requirements for poverty reduction

Chapter 15 Financing of the Poverty Reduction Programme 15.1 Underlying Considerations Several underlying considerations are noteworthy when looking at the financial resource requirements for poverty reduction

General information document

General information document Last updated: January 2018 Natixis, Corporate & Investment Banking Customer Support Department - 40 Avenue des Terroirs de France 75012 Paris - BP 4-75060 Paris Cedex 02 mifid_onboarding@natixis.com

General information document Last updated: January 2018 Natixis, Corporate & Investment Banking Customer Support Department - 40 Avenue des Terroirs de France 75012 Paris - BP 4-75060 Paris Cedex 02 mifid_onboarding@natixis.com

Although Financial Inclusion is higher amongst females in Cambodia, the income distribution shows a disparity favoring males

Although Financial Inclusion is higher amongst females in Cambodia, the income distribution shows a disparity favoring males 66 % 75 % 73 % 79 % 21 % 78 % headed vs. male headed households (Ownership)

Although Financial Inclusion is higher amongst females in Cambodia, the income distribution shows a disparity favoring males 66 % 75 % 73 % 79 % 21 % 78 % headed vs. male headed households (Ownership)

Agriculture and SME Finance

Chapter9 9.1 Bangladesh is on course for middle income country status and its agriculture sector has continued to play a significant role by providing the largest share of employment in the country. Growth

Chapter9 9.1 Bangladesh is on course for middle income country status and its agriculture sector has continued to play a significant role by providing the largest share of employment in the country. Growth

ZAMBIA REVENUE AUTHORITY DIRECT TAXES DIVISION INCOME TAX (AMENDMENT) ACT 2005

ACT 2005") ZAMBIA REVENUE AUTHORITY DIRECT TAXES DIVISION INCOME TAX (AMENDMENT) ACT 2005 PRACTICE NOTE NO. 1/2005 CONTENTS 1. GENERAL 3 PAGE 2. SUMMARY OF THE PRINCIPAL CHANGES 4 IN THE INCOME TAX (AMENDMENT) ACT

ZAMBIA REVENUE AUTHORITY DIRECT TAXES DIVISION INCOME TAX (AMENDMENT) ACT 2005 PRACTICE NOTE NO. 1/2005 CONTENTS 1. GENERAL 3 PAGE 2. SUMMARY OF THE PRINCIPAL CHANGES 4 IN THE INCOME TAX (AMENDMENT) ACT

Component One A Research Report on The Situation of Female Employment and Social Protection Policy in China (Guangdong Province)

") Component One A Research Report on The Situation of Female Employment and Social Protection Policy in China (Guangdong Province) By: King-Lun Ngok (aka Yue Jinglun) School of Government, Sun Yat-sen University

Component One A Research Report on The Situation of Female Employment and Social Protection Policy in China (Guangdong Province) By: King-Lun Ngok (aka Yue Jinglun) School of Government, Sun Yat-sen University

REPORT ON WOMEN S ACCESS TO FINANCIAL SERVICES IN ZAMBIA

REPORT ON WOMEN S ACCESS TO FINANCIAL SERVICES IN ZAMBIA WOMEN S ACCESS TO FINANCIAL SERVICES IN ZAMBIA TABLE OF CONTENTS EXECUTIVE SUMMARY 5 PART I BACKGROUND 9 1 Objectives and methodology 9 2 Overview

REPORT ON WOMEN S ACCESS TO FINANCIAL SERVICES IN ZAMBIA WOMEN S ACCESS TO FINANCIAL SERVICES IN ZAMBIA TABLE OF CONTENTS EXECUTIVE SUMMARY 5 PART I BACKGROUND 9 1 Objectives and methodology 9 2 Overview

Climate shocks and risk attitudes among female and male maize farmers in Kenya

Climate shocks and risk attitudes among female and male maize farmers in Kenya Songporne Tongruksawattana 1, Priscilla Wainaina 2, Nilupa S. Gunaratna 3 and Hugo De Groote 1 1 International Maize and Wheat

Climate shocks and risk attitudes among female and male maize farmers in Kenya Songporne Tongruksawattana 1, Priscilla Wainaina 2, Nilupa S. Gunaratna 3 and Hugo De Groote 1 1 International Maize and Wheat

ZAMBIA REVENUE AUTHORITY DIRECT TAXES DIVISION INCOME TAX (AMENDMENT) ACT 2002

ACT 2002") ZAMBIA REVENUE AUTHORITY DIRECT TAXES DIVISION INCOME TAX (AMENDMENT) ACT 2002 PRACTICE NOTE NO. 1/2002 CONTENTS 1. GENERAL 3 PAGE 2. SUMMARY OF THE PRINCIPAL CHANGES 4 IN THE INCOME TAX (AMENDMENT) ACT

ZAMBIA REVENUE AUTHORITY DIRECT TAXES DIVISION INCOME TAX (AMENDMENT) ACT 2002 PRACTICE NOTE NO. 1/2002 CONTENTS 1. GENERAL 3 PAGE 2. SUMMARY OF THE PRINCIPAL CHANGES 4 IN THE INCOME TAX (AMENDMENT) ACT

Community-Based Savings Groups in Mtwara and Lindi

tanzania Community-Based Savings Groups in Mtwara and Lindi In recent years, stakeholders have increasingly acknowledged that formal financial institutions are not able to address the financial service

tanzania Community-Based Savings Groups in Mtwara and Lindi In recent years, stakeholders have increasingly acknowledged that formal financial institutions are not able to address the financial service

PRODUCTIVE SECTOR COMMERCE PDNA GUIDELINES VOLUME B

PRODUCTIVE SECTOR COMMERCE PDNA GUIDELINES VOLUME B 2 COMMERCE CONTENTS n INTRODUCTION 2 n ASSESSMENT PROCESS 3 n PRE-DISASTER SITUATION 4 n FIELD VISITS FOR POST-DISASTER DATA COLLECTION 5 n ESTIMATION

PRODUCTIVE SECTOR COMMERCE PDNA GUIDELINES VOLUME B 2 COMMERCE CONTENTS n INTRODUCTION 2 n ASSESSMENT PROCESS 3 n PRE-DISASTER SITUATION 4 n FIELD VISITS FOR POST-DISASTER DATA COLLECTION 5 n ESTIMATION

TRANSFORMING THE LIVES OF RURAL WOMEN AND GIRLS THROUGH GENDER AND EQUITY BUDGETING

THE REPUBLIC OF UGANDA TRANSFORMING THE LIVES OF RURAL WOMEN AND GIRLS THROUGH GENDER AND EQUITY BUDGETING A Concept Note for the Side Event by Government of Uganda At the 62 nd Session of the Commission

THE REPUBLIC OF UGANDA TRANSFORMING THE LIVES OF RURAL WOMEN AND GIRLS THROUGH GENDER AND EQUITY BUDGETING A Concept Note for the Side Event by Government of Uganda At the 62 nd Session of the Commission

CONTENTS DIRECTOR S REVIEW INFORMATION ABOUT THE COMPANY OVERVIEW OF THE COMPANY S ACTIVITIES AND DEVELOPMENT

ANNUAL REPORT 2009 CONTENTS DIRECTOR S REVIEW...3 INFORMATION ABOUT THE COMPANY...5 OVERVIEW OF THE COMPANY S ACTIVITIES AND DEVELOPMENT...7 Guarantees Issued to Credit Institutions...7 Volume of Guarantees

ANNUAL REPORT 2009 CONTENTS DIRECTOR S REVIEW...3 INFORMATION ABOUT THE COMPANY...5 OVERVIEW OF THE COMPANY S ACTIVITIES AND DEVELOPMENT...7 Guarantees Issued to Credit Institutions...7 Volume of Guarantees

2017 FIRST QUARTER ECONOMIC REVIEW

2017 FIRST QUARTER ECONOMIC REVIEW MAY 2017 0 P a g e Overview The performance of the economy in the first quarter of 2017 was on a positive trajectory with annual growth projected to be about 3.9 % from

2017 FIRST QUARTER ECONOMIC REVIEW MAY 2017 0 P a g e Overview The performance of the economy in the first quarter of 2017 was on a positive trajectory with annual growth projected to be about 3.9 % from