Sefa Corporate Plan 2014/ /19 Joint Portfolio Committee Meeting on Economic Development and Small Business Development

|

|

|

- Noel Elmer Stewart

- 5 years ago

- Views:

Transcription

1 Sefa Corporate Plan 2014/ /19 Joint Portfolio Committee Meeting on Economic Development and Small Business Development Thakhani Makhuvha Chief Executive Officer The Small Enterprise Finance Agency 29th July 2014

Wholesale SMME financing via retail financial")

2 Introduction The Small Enterprise Finance Agency (sefa) is a development finance institution established in 2012 with a mandate to provide access to finance to SMMEs sefa is a wholly owned subsidiary of the Industrial Development Corporation (IDC) and provides funding ranging from R500 to R5 million via the following product / channels: Direct lending (50k R5m) Wholesale SMME financing via retail financial intermediaries (RFIs) 50k R3m Wholesale micro finance loans via micro finance institutions (MFIs) ranging from R500 to R50k Dedicated targeted support and lending to cooperative enterprises and support to Financial Services Co-operatives. 2

3 Government Small Business Focus Within the context of NGP, IPAP and NDP, sefa and other development finance institutions are mandated to: Increase and expand the demand for goods and services produced by small businesses Continue to enhance efficiencies on support measures provided to SMMEs and cooperatives Ensure active participation of SMMEs in the industrial development programmes Reduce regulatory burden facing SMMEs and Co-ops Re-establish the Marketing Boards and Export Villages to facilitate linkages (both domestic and international) between suppliers and consumers Sector prioritization and promotion of SMME and Co-ops growth and development Upscale and fast-track the development of youth and women-owned enterprises Specifically sefa is tasked to: Improve its value proposition as the primary provider of financial support to SMMEs, in collaboration with other national agencies with small business activities (e.g. IDC, NEF, Land Bank, DBSA) to particularly address market failure. Increase the uptake of its products and services to improve access to finance for small businesses 3

Mr TR Makhuvha (CEO) Mr M Ferreira Mr IAS Tayob Ms HN Lupuwana Mr SA Molepo Mr VG Mutshekwane Ms BP Calvin Mr GS Gouws Ms K Schumann Mr LB")

4 Governance Structure Board Enterprise Risk Committee Audit Committee HC & Remuneration Committee Wholesale Investment Committee Direct Lending BOARD MEMBERS Dr Magwentshu-Rensburg (Chair) Mr TR Makhuvha (CEO) Mr M Ferreira Mr IAS Tayob Ms HN Lupuwana Mr SA Molepo Mr VG Mutshekwane Ms BP Calvin Mr GS Gouws Ms K Schumann Mr LB Mavundla 4

5 Management Structure sefa Board Company Secretariat CEO Head: Internal Audit Direct Lending EXECUTIVE WHOLESALE EXECUTIVE CHIEF FINANCIAL OFFICER CHIEF RISK OFFICER HR EXECUTIVE Executive in CEO Office 5

6

7 Group Ownership Structure Consolidated entities Consolidated Investment subsidiaries Associates Joint Ventures 100% sefa 100% Khula Emerging Contractors Fund 21% Business Partners 50% Anglo American Khula Mining Fund 100% Khula Credit Guarantee 75% Khula Akwandze Fund 49% Utho Capital SME Fund 50% Awethu 100% New Business Finance 100% Identity Development Fund 82% Small Business Growth Trust Fund 40% 65% Enablis Khula Loan Fund Izibulo 75% Khula- Enablis SME Acceleration Fund 7

8 Financial Position R 000 Group 2014 Group 2013 Total Assets R2,227,194 R2,179,684 Shareholders loan R1,175,521 R944,542 Other liabilities R158,353 R169,941 Equity R893,320 R1,065,201 Total Equity & Liabilities R2,227,194 R2,179,684 8

9 Portfolio of Assets Composition of total assets - group 100% 80% 2% 5% Other assets 36% 31% Investments 60% 40% 20% 0% 22% 14% 8% 8% 32% 42% Loans and advances Investment properties Cash and cash equivalents 9

10 Approvals and Disbursements 2011/ /13 Full Year ex- Khula and ex- samaf Full Year - Actual sefa Approvals R211.1m R439.6m Disbursements R143.0m R198.0m No. of Jobs created No. of SMMEs financed

11 Target Market, Products and distribution channels

with specific focus on: Services (including retailing, wholesaling and tourism); Manufacturing (including agro-processing); Agriculture")

12 Target market sefa s target market consists of survivalist, micro, small and medium businesses as defined in Schedule 1 of the National Small Business Act of 1996 (as amended in 2004) with specific focus on: Services (including retailing, wholesaling and tourism); Manufacturing (including agro-processing); Agriculture (specifically land reform beneficiaries and micro-farming activities); Construction (small construction contractors); Mining (specifically small miners). Survivalists and microenterprises loans of between R500 and R Small enterprises loans between R and R Medium enterprises loans between R and R

13 Products and Services DIRECT LENDING Working capital facilities Revolving loans Bridging Finance Term loans Asset finance WHOLESALE LENDING On-lending Facilities Credit Indemnity Schemes Land Reform Empowerment Loan Equity/Specialised Funds NEW PRODUCTS UNDER CONSIDERATION Performance Guarantees Supplier Guarantees Loan payment facility guarantees INSTITUTIONAL SUPPORT Institutional Strengthening Technical Support Rental Property 13

14 16 Micro-Finance Intermediaries 6 Retail Finance Intermediaries 3 Partnerships * 9 sefa Regional Offices 3 sefa Branch Offices 10 Cooperative Offices Our Footprint * * * * * 8 Specialised Funds * * * 14

15 Co-operatives Products & Services PRODUCTS AND SERVICES Financial Products sefa offers the following products and services: Business Loans/On-lending funds Institutional strengthening to Financial Co-operatives Mentoring to co-operatives funded through direct lending. Direct Lending Business loans up to R5 million to all types of co-operatives except Financial Co-operatives. ( Financing products: bridging loan, term loan, project loan) Non-Financial support sefa does not offer these services but are offered by the following government agencies: CIPC- responsible for registration of co-operatives CBDA- responsible for regulating and supervising Financial Cooperatives including Co-operatives Banks SEDA-responsible for business support and training of co-operatives( this function to be taken over by CDA when it becomes operational) FUNDING MODEL- CHANNELS Wholesale Lending On-lending loans to Financial Co-operatives (FC) subject to 15% cap on external credit but the FC may apply for exemption from CBDA supervisor. R500,000 capacity-grant to start-up Financial Co-operatives to acquire systems,equipment,software and training. The following are not provided for under this scheme: Stipend/ Salaries, Office Furniture and Rental. CIPC Companies and Intellectual Properties Commission, CBDA Co-operative Bank Development Agency, SEDA Small Enterprise Development Agency; CDA Co-operative Development Agency; BOD Board of Directors

16 We do business with: South African citizens and permanent residents owned enterprises Legally registered entities including sole traders with a fixed physical address Applicants must be within the required contractual capacity All business operations must be operated within RSA; The enterprise must be compliant with generally accepted corporate governance practices appropriate to the client s legal status Have a written proposal or business plan that meets the requirements of sefa s loan application criteria Demonstrate the character and ability to repay the loan Have provided personal and/or credit references (if available) Majority shareholder must be owner manager of the business Where available, client provides relevant securities/collateral Businesses with a valid tax clearance certificate 16

up to 12 Months High")

17 What makes sefa different Provision of capital and/or interest moratorium (Payment Holiday) up to 12 Months High appetite for risk in exchange for high development impact Financing SMMEs including start up businesses that are often perceived as high risk Addressing the financing gap for loans below R500k Provision of pre and post loan business support Provision of funding to entrepreneurs with adverse credit records provided they can demonstrate active remedy of their indebtedness Lending not solely based on security backing long term sustainability potential Specific focus on youth owned businesses 17

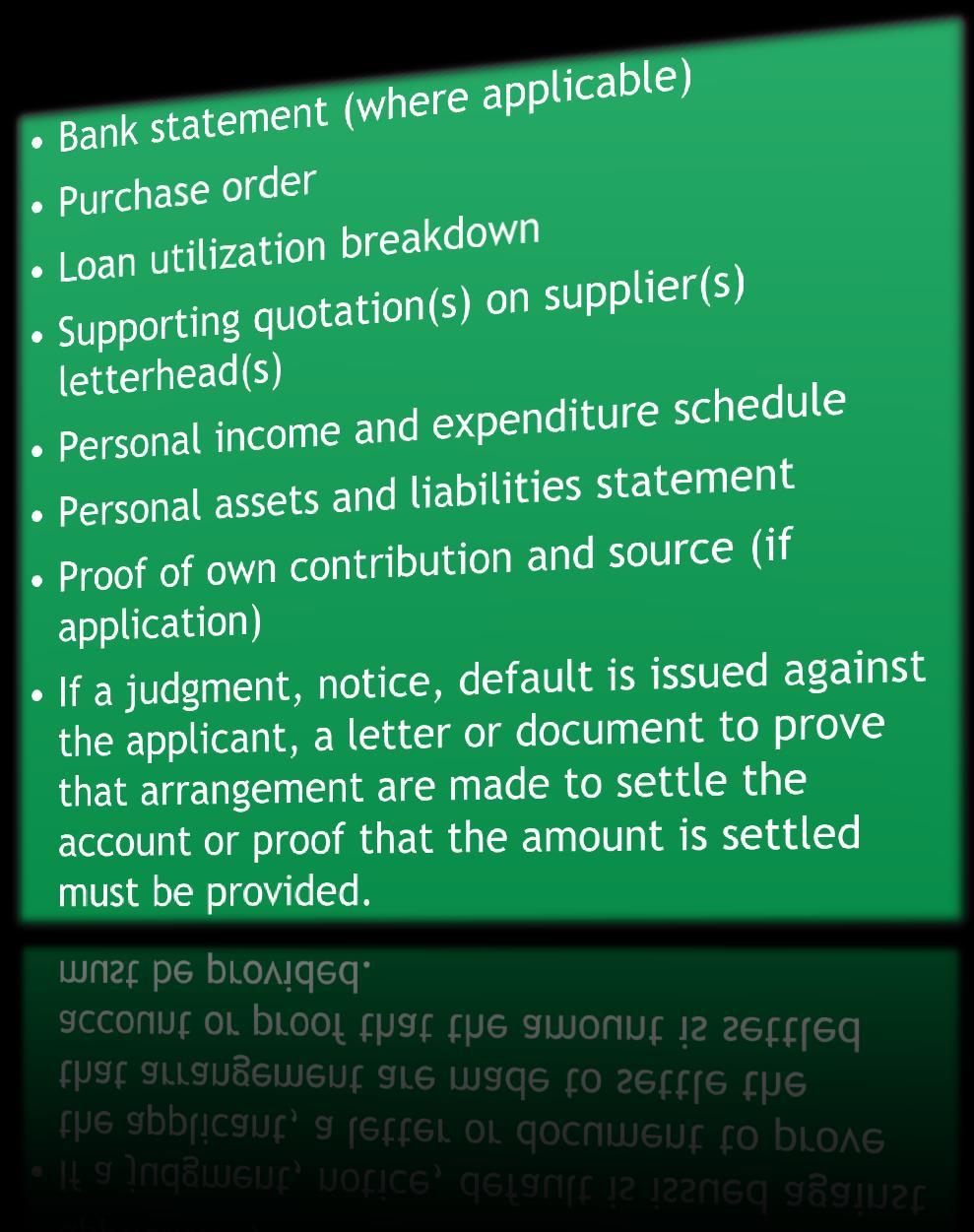

18 What we need when applying 18

19 Pricing Methodology & Model Included in the final price are: A margin to cover the fixed and variable operating costs of the sefa; An unexpected loss charge to provide cushion in the event of unexpected losses and to allow for minimum growth in capital; A loan risk premium to compensate for the risk of default A rebate for desired development Impact. Risk margin (Premium) Development discount Base Rate or Hurdle Rate, which includes the cost of funding and operating costs 19

SME Funding Formal registered financial institutions (e.g. FNB, ABSA, Standard Bank, Nedbank, etc) R500 to R50k R50k to R5m Up to R5m SMMEs can access sefa funding solutions through any of the above channels 20")

20 Our Distribution channels sefa Funding Model sefa Direct Lending sefa Wholesale Lending Credit Guarantee Schemes R50k to R5m Finance Intermediaries: (Cooperatives, Joint Ventures & Funds, Retail Finance Intermediaries) SME Funding Formal registered financial institutions (e.g. FNB, ABSA, Standard Bank, Nedbank, etc) R500 to R50k R50k to R5m Up to R5m SMMEs can access sefa funding solutions through any of the above channels 20

21 Risk Management Strategy 21

22

23 2014/15 Strategic Focus STRATEGIC OBJECTIVE/ ENABLER Increase access & provision of finance to SMMEs through a national footprint & contribute to job creation STRATEGIC GOAL STATEMENT Expand Direct Lending through partnerships Expand access to Micro Enterprise Finance Stronger partnerships with RFIs in SMME wholesale finance Increase utilisation of guarantee indemnity scheme by commercial banks KEY PERFORMANCE AREA Enable SMMEs to access finance & development impact Improve & maintain turnaround times for approvals KEY PERFORMANCE INDICATOR Approvals Disbursements KEY PERFORMA NCE TARGET R974m R800m Development Impact: SMMEs financed Overall jobs created Disbursements to Youth owned 30% Rural provinces 45% Women 45% People with disabilities 2% Black-owned 70% businesses Facilities <R250k 40% Approval in productive 20% industrial Number of day: bridging 10 finance Number of days: term 20 loans 23

24 2014/15 Strategic Focus STRATEGIC OBJECTIVE/ ENABLER Build an effective & efficient sefa that is a sustainable performance drive organisation STRATEGIC GOAL STATEMENT Create, develop & retain a dynamic human capital with values and culture aligned to mandate Build an effective sefa with robust & efficient business processes, systems & infrastructure KEY PERFORMANCE AREA Inculcate a culture of high performance to achieve the mission of sefa Functional, innovative & robust IT infrastructure & reliable MIS to measure performance & development impact KEY PERFORMANCE INDICATOR Formal performance reviews conducted KEY PERFORMANCE TARGET 2 reviews/year Critical systems uptime 99% availability Adequate & reliable 99% compliance reporting Interactive website & Online mobile technology to applications clients e.g. sms alerts streamlined Build a financially sustainable & viable sefa Maintain cost efficiency & profitability FY end profitability ratio %: Cost to income ratio 164% (excl grants) Impairment provision through income statement 25% % of bad debts to book 30% Growth of loan book 122% Growth interest & admin fees 49% 24

25 2014/15 Strategic Focus STRATEGIC OBJECTIVE/ ENABLER STRATEGIC GOAL STATEMENT KEY PERFORMANCE AREA KEY PERFORMANCE INDICATOR KEY PERFORMA NCE TARGET Build a sefa that meets all legislative, regulatory & good governance requirements Ensure an effectively governed and compliant organisation Enterprise-wide Risk Management Risk framework & policies Annual review Quantifiable & defined risk appetite levels Approved by Board of Directors (BOD) Build a strong & effective sefa brand emphasizing accessibility to SMMEs Effective marketing & promotion programme to communicate product offering Improve customer experience Improve outreach to partners, stakeholders & SMMEs CRM system developed System developed % increase in customer satisfaction levels Number of events 3 Number of roadshows 6 60% 25

26 Corporate Targets 2013/ / / / / /19 APPROVALS R815m R974m R1 229m R1 439m R1 708m R1 709m DISBURSEMENT R737.5m R642m R865m R1 011m R1 189m R1 327m NO. OF JOBS CREATED NO. OF SMMES FINANCED

27 Corporate Targets - Approvals PRODUCT 2013/ / / / / /19 DIRECT LENDING R370m R485m R563m R630m R690m R725m RFIS AND FUNDS R285m R330m R415m R470m R590m R698m CO-OPERATIVES R20m R6,4m R8,6m R10,8m R16m R21,2m MICROFINANCE R140m R153m R243m R329m R412m R265m TOTAL R815m R974m R1 229m R1 439m R1 708m R1 709m 27

28 Corporate Targets - Disbursements PRODUCT 2013/ / / / / /19 Direct Lending R348m R388m R450m R522m R586m R616m RFIs and Funds R293m R181m R299m R333m R421m R506m Co-operatives R12m R2,9m R4,3m R5,4 R8m R10,6m Microfinance R84m R71m R112m R151m R174m R195m Total R737m R642m R865m R1 011m R1 189m R1 327m 28

29 Development Impact AREA OF IMPACT Facilities disbursed to youth-owned businesses (Youth between ages of 18 & 35) ANNUAL TARGET 30% Facilities disbursed in priority rural provinces 45% Facilities disbursed to women-owned businesses 45% Facilities disbursed to black-owned businesses 70% Facilities less than R250K disbursed to end-users 40% People Living with Disabilities 2% 29

30 Financial Management 30

31 Budget base and philosophy Budget and projections are based on the Corporate Plan, mainly driven by the targeted disbursements; Business targets per Corporate Plan remain ambitious with an upward trajectory over the Corporate Plan period; Current organisational capability requires a significant investment in human resources for: Shift in Wholesale investment business strategy; Direct Lending business development, due diligence, credit assessment, post investment business support, collections and work out; Business process renewal focused review and enhancement of critical business systems and processes both from a compliance and efficient service delivery perspective Drive cost containment in line with instructions from National Treasury 31

32 Income statement R Revenue R R R R R Impairments and bad debts Operating expenses Loss for the year before taxation Grants capitalised to shareholders 'loan Surplus after subsidies (R47 648) (R ) (R92 805) (R ) (R ) (R ) (R ) (R ) (R ) (R ) (R ) (R ) (R ) (R ) (R95 515)

33 Financial Projections INVESTMENTS NET OF PROVISIONS AND IMPAIRMENTS - R'M SME Retail SME Wholesale Micro Lending Equity related investments Revenue related Interest from lending operations/ total revenue 48% 66% 75% 79% 83% Treasury investment income/ total revenue 24% 13% 9% 7% 5% Indemnity product Indemnity fees/ total revenue 1% 1% 0% 0% 0% Claims and reserve movement/ total expenses 5% 5% 5% 5% 6% Indemnity fees/ Claims and reserve movement 7% 6% 5% 4% 4% 33

34 Financial Projections (cont.) Personnel costs Personnel expenses/ total expenses 44% 44% 45% 40% 42% Personnel expenses/ investments at carrying value 16% 12% 10% 8% 7% Interest from lending operations/ personnel expenses 46% 71% 102% 131% 164% Bad debt provisions and impairments SME Retail bad debt provision % 24% 24% 25% 25% 25% SME Wholesale bad debt provision % 15% 15% 15% 15% 15% Micro Lending bad debt provision % 5% 5% 5% 5% 5% Equity investments bad debt provision % 63% 57% 52% 48% 44% Total bad debt provision % 25% 23% 22% 21% 21% Net loss Loss per year/total assets -18% -14% -8% -7% -3% Investment growth Growth in investments at cost % 23% 29% 21% 25% 18% Growth in investments at carrying value % 27% 30% 22% 25% 18% 34

35 sefa Contact Details sefa National Call Centre : helpline@sefa.org.za 35

36 36

BPDM Cooperative Summit

BPDM Cooperative Summit Introduction and Background sefa was established on 1 st April 2012 Merger of South African Micro Apex Fund (samaf), Khula Enterprise Finance Limited and the small business activities

BPDM Cooperative Summit Introduction and Background sefa was established on 1 st April 2012 Merger of South African Micro Apex Fund (samaf), Khula Enterprise Finance Limited and the small business activities

SABOA 2013 NATIONAL CONFERENCE 28 FEBRUARY 2013 CSIR CONFERENCE CENTRE

SABOA 2013 NATIONAL CONFERENCE 28 FEBRUARY 2013 CSIR CONFERENCE CENTRE Don Mashele Head of Regions Overview and Background Challenges that led to the establishment of sefa Limited success in fostering

SABOA 2013 NATIONAL CONFERENCE 28 FEBRUARY 2013 CSIR CONFERENCE CENTRE Don Mashele Head of Regions Overview and Background Challenges that led to the establishment of sefa Limited success in fostering

PORTFOLIO COMMITTEE ON TRADE AND INDUSTRY. Mr. Sithembele Mase. CHIEF EXECUTIVE OFFICER: samaf. CONTACT : (Marketing Manager)

") PORTFOLIO COMMITTEE ON TRADE AND INDUSTRY Mr. Sithembele Mase CHIEF EXECUTIVE OFFICER: samaf CONTACT : 012 394 1805 (Marketing Manager) 012 394 1722 (PA Line) 012 394 1116 (Direct Line) 1 CONTENT 1. Rationale

PORTFOLIO COMMITTEE ON TRADE AND INDUSTRY Mr. Sithembele Mase CHIEF EXECUTIVE OFFICER: samaf CONTACT : 012 394 1805 (Marketing Manager) 012 394 1722 (PA Line) 012 394 1116 (Direct Line) 1 CONTENT 1. Rationale

ANNUAL REPORT SMMEs AND COOPERATIVES THE ENGINE FOR ECONOMIC GROWTH

ANNUAL REPORT 2015 SMMEs AND COOPERATIVES THE ENGINE FOR ECONOMIC GROWTH sefa s mandate To be the leading catalyst for the development of sustainable SMMEs and Cooperatives through the provision of finance.

ANNUAL REPORT 2015 SMMEs AND COOPERATIVES THE ENGINE FOR ECONOMIC GROWTH sefa s mandate To be the leading catalyst for the development of sustainable SMMEs and Cooperatives through the provision of finance.

BANK SUPERVISION DIVISION MICROFINANCE SECTOR REPORT FOR QUARTER ENDED 30 SEPTEMBER 2018

BANK SUPERVISION DIVISION MICROFINANCE SECTOR REPORT FOR QUARTER ENDED 30 SEPTEMBER 2018 NOVEMBER 2018 Table of Contents 1. EXECUTIVE SUMMARY... 3 2. ARCHITECTURE OF THE MICROFINANCE SECTOR... 4 3. PERFORMANCE

BANK SUPERVISION DIVISION MICROFINANCE SECTOR REPORT FOR QUARTER ENDED 30 SEPTEMBER 2018 NOVEMBER 2018 Table of Contents 1. EXECUTIVE SUMMARY... 3 2. ARCHITECTURE OF THE MICROFINANCE SECTOR... 4 3. PERFORMANCE

BANK SUPERVISION DIVISION MICROFINANCE INDUSTRY REPORT FOR QUARTER ENDED 31 DECEMBER 2018

BANK SUPERVISION DIVISION MICROFINANCE INDUSTRY REPORT FOR QUARTER ENDED 31 DECEMBER 2018 MARCH 2019 Table of Contents 1. EXECUTIVE SUMMARY... 3 2. ARCHITECTURE OF THE MICROFINANCE INDUSTRY... 4 3. PERFORMANCE

BANK SUPERVISION DIVISION MICROFINANCE INDUSTRY REPORT FOR QUARTER ENDED 31 DECEMBER 2018 MARCH 2019 Table of Contents 1. EXECUTIVE SUMMARY... 3 2. ARCHITECTURE OF THE MICROFINANCE INDUSTRY... 4 3. PERFORMANCE

STRIKING THE RIGHT BALANCE IN REGULATION AND SUPERVISION OF DEVELOPMENT FINANCE INSTITUTIONS

STRIKING THE RIGHT BALANCE IN REGULATION AND SUPERVISION OF DEVELOPMENT FINANCE INSTITUTIONS The South African Experience Global Symposium on Development Finance Institutions Presenter: Anthony Julies,

STRIKING THE RIGHT BALANCE IN REGULATION AND SUPERVISION OF DEVELOPMENT FINANCE INSTITUTIONS The South African Experience Global Symposium on Development Finance Institutions Presenter: Anthony Julies,

Annual Report. 5 years of growing small enterprises

Annual Report 1 Annual Report 5 years of growing small enterprises Reflecting on sefa s 5 Years of Existence "South Africa belongs to all its peoples. Now, in 2030, our story keeps growing as if spring

Annual Report 1 Annual Report 5 years of growing small enterprises Reflecting on sefa s 5 Years of Existence "South Africa belongs to all its peoples. Now, in 2030, our story keeps growing as if spring

Annual Report 2015/16 Presentation. 12 October 2016

Annual Report 2015/16 Presentation 12 October 2016 Presentation outline 1. Economic Environment 2. Operational performance 3. Development impact 4. Performance against predetermined objectives 5. Financial

Annual Report 2015/16 Presentation 12 October 2016 Presentation outline 1. Economic Environment 2. Operational performance 3. Development impact 4. Performance against predetermined objectives 5. Financial

Seda An Overview. Koenie Slabbert Seda COO

Seda An Overview Presented by: Presented by: Koenie Slabbert Seda COO Contents Who is Seda? Legislative Mandate Implications of Mandate Seda s Mission Seda s Goal Operational Network Delivery Model Seda

Seda An Overview Presented by: Presented by: Koenie Slabbert Seda COO Contents Who is Seda? Legislative Mandate Implications of Mandate Seda s Mission Seda s Goal Operational Network Delivery Model Seda

National Development Banks: Improving domestic public resource mobilisation (focusing on South Africa s IDC)

") National Development Banks: Improving domestic public resource mobilisation (focusing on South Africa s IDC) Jorge Maia Head: Research and Information Intergovernmental Group of Experts on Financing for

National Development Banks: Improving domestic public resource mobilisation (focusing on South Africa s IDC) Jorge Maia Head: Research and Information Intergovernmental Group of Experts on Financing for

Introduction to EDD Annual Performance Plan

2014/15 Introduction to EDD Annual Performance Plan June 2014 1 The EDD mandate EDD established in 2009 Core mandates: Identify priorities for job creation, inclusive growth and industrialisation Support

2014/15 Introduction to EDD Annual Performance Plan June 2014 1 The EDD mandate EDD established in 2009 Core mandates: Identify priorities for job creation, inclusive growth and industrialisation Support

PRESENTATION TO PORTFOLIO COMMITTEE ON HUMAN SETTLEMENTS OCTOBER 2017 INTEGRATED ANNUAL REPORT 2017

PRESENTATION TO PORTFOLIO COMMITTEE ON HUMAN SETTLEMENTS OCTOBER 2017 INTEGRATED ANNUAL REPORT 2017 2 0 CONTENTS NHFC Overview Business Model Corporate Governance & Risk Management Business Performance

PRESENTATION TO PORTFOLIO COMMITTEE ON HUMAN SETTLEMENTS OCTOBER 2017 INTEGRATED ANNUAL REPORT 2017 2 0 CONTENTS NHFC Overview Business Model Corporate Governance & Risk Management Business Performance

Annual Performance Plan 2016/ /2019

Annual Performance Plan 2016/2017-2018/2019 Annual Performance Plan 2016/2017-2018/2019 1 CONTENTS Published by Seda, 2016. This document contains confidential and proprietary information. The dissemination,

Annual Performance Plan 2016/2017-2018/2019 Annual Performance Plan 2016/2017-2018/2019 1 CONTENTS Published by Seda, 2016. This document contains confidential and proprietary information. The dissemination,

sefa Finance Solutions

sefa Finance Solutions Get up to R5 million of start-up, expansionary or acquisition finance for your business. Are you an aspiring entrepreneur? Do you have a business idea? Does your business need financial

sefa Finance Solutions Get up to R5 million of start-up, expansionary or acquisition finance for your business. Are you an aspiring entrepreneur? Do you have a business idea? Does your business need financial

Organisational Performance Report

Organisational Performance Report Portfolio Committee Small Business Development 8 November 2017 Table of contents Introduction Loan book performance Approvals Disbursements Development impact SMMEs financed

Organisational Performance Report Portfolio Committee Small Business Development 8 November 2017 Table of contents Introduction Loan book performance Approvals Disbursements Development impact SMMEs financed

The Team. Brigitte Ryder. Bobby Madhav. Sipho Silinda. Lindi Makapela

1 The Team Bobby Madhav Sipho Silinda Brigitte Ryder Lindi Makapela 2 Can Microfinance / Credit be delivered in a sustainable manner to the poor from a South African perspective? 3 Content 1 2 3 4 5 6

1 The Team Bobby Madhav Sipho Silinda Brigitte Ryder Lindi Makapela 2 Can Microfinance / Credit be delivered in a sustainable manner to the poor from a South African perspective? 3 Content 1 2 3 4 5 6

SOLVING FOR SMMEs AND SOLE PROPRIETORS

5 12675-BOOK-2017-07.indb 177 SOLVING FOR SMMEs AND SOLE PROPRIETORS 2017/08/02 11:08 AM SMALL BUSINESS AND ENTREPRENEURSHIP CRITICAL TO EMPLOYMENT AND ECONOMIC GROWTH At the dawn of his second term in

5 12675-BOOK-2017-07.indb 177 SOLVING FOR SMMEs AND SOLE PROPRIETORS 2017/08/02 11:08 AM SMALL BUSINESS AND ENTREPRENEURSHIP CRITICAL TO EMPLOYMENT AND ECONOMIC GROWTH At the dawn of his second term in

Al-Amal Microfinance Bank

Impact Brief Series, Issue 1 Al-Amal Microfinance Bank Yemen The Taqeem ( evaluation in Arabic) Initiative is a technical cooperation programme of the International Labour Organization and regional partners

Impact Brief Series, Issue 1 Al-Amal Microfinance Bank Yemen The Taqeem ( evaluation in Arabic) Initiative is a technical cooperation programme of the International Labour Organization and regional partners

MICROFINANCE QUARTERLY REPORT

MICROFINANCE QUARTERLY REPORT 31 MARCH 2017 Table of Contents Table of Figures... 2 1 EXECUTIVE SUMMARY... 3 ARCHITECTURE OF THE MICROFINANCE INDUSTRY.....3 Branch Network and Outreach... 4 Microfinance

MICROFINANCE QUARTERLY REPORT 31 MARCH 2017 Table of Contents Table of Figures... 2 1 EXECUTIVE SUMMARY... 3 ARCHITECTURE OF THE MICROFINANCE INDUSTRY.....3 Branch Network and Outreach... 4 Microfinance

MICROFINANCE QUARTERLY REPORT 30 JUNE 2017

MICROFINANCE QUARTERLY REPORT 30 JUNE 2017 TABLE OF CONTENTS 1 EXECUTIVE SUMMARY...3 2 ARCHITECTURE OF THE MICROFINANCE INDUSTRY...3 Branch Network and Outreach...4 Microfinance Active Clients...6 3 PERFORMANCE

MICROFINANCE QUARTERLY REPORT 30 JUNE 2017 TABLE OF CONTENTS 1 EXECUTIVE SUMMARY...3 2 ARCHITECTURE OF THE MICROFINANCE INDUSTRY...3 Branch Network and Outreach...4 Microfinance Active Clients...6 3 PERFORMANCE

BROAD-BASED BLACK ECONOMIC EMPOWERMENT TRANSACTION 18 December 2018

KHULA SIZWE BROAD-BASED BLACK ECONOMIC EMPOWERMENT TRANSACTION 18 December 2018 The Circular published on 18 December 2018 is the main source of detailed information on the proposed B-BBEE transaction,

KHULA SIZWE BROAD-BASED BLACK ECONOMIC EMPOWERMENT TRANSACTION 18 December 2018 The Circular published on 18 December 2018 is the main source of detailed information on the proposed B-BBEE transaction,

SEDA STRATEGIC OVERVIEW SABOA 2017 CONFERENCE AND EXHIBITION

SEDA STRATEGIC OVERVIEW SABOA 2017 CONFERENCE AND EXHIBITION COLIN LESHOU Together Advancing Small Enterprise Development 25/05/2017 OUTLINE General Statistics of the South African SMME sector Vision and

SEDA STRATEGIC OVERVIEW SABOA 2017 CONFERENCE AND EXHIBITION COLIN LESHOU Together Advancing Small Enterprise Development 25/05/2017 OUTLINE General Statistics of the South African SMME sector Vision and

CURRICULUM VITAE THABO VAUGHAN SHENXANE

CURRICULUM VITAE THABO VAUGHAN SHENXANE Cell: 084 789 9151 Email: thabo@chumisa.co.za P.O. Box 917 WINGATE PARK, Pretoria East, 0158 PERSONAL INFORMATION Identity Number : 750212 5491 08 2 Driver s Licence

CURRICULUM VITAE THABO VAUGHAN SHENXANE Cell: 084 789 9151 Email: thabo@chumisa.co.za P.O. Box 917 WINGATE PARK, Pretoria East, 0158 PERSONAL INFORMATION Identity Number : 750212 5491 08 2 Driver s Licence

TRANSFORMATION POLICY

SANRAL TRANSFORMATION POLICY DRAFT Policy Reference Number Version Number Effective Date Review Date Policy Owner Signature Policy Sponsor Signature Date of Approval FRAMEWORK 1. INTRODUCTION 2. POLICY

SANRAL TRANSFORMATION POLICY DRAFT Policy Reference Number Version Number Effective Date Review Date Policy Owner Signature Policy Sponsor Signature Date of Approval FRAMEWORK 1. INTRODUCTION 2. POLICY

EUROPEAN COMMISSION Employment, Social Affairs and Equal Opportunities DG DRAFT NOTE ON

EUROPEAN COMMISSION Employment, Social Affairs and Equal Opportunities DG ESF, Monitoring of Corresponding National Policies I, Coordination DRAFT NOTE ON THE EUROPEAN PROGRESS MICROFINANCE FACILITY AND

EUROPEAN COMMISSION Employment, Social Affairs and Equal Opportunities DG ESF, Monitoring of Corresponding National Policies I, Coordination DRAFT NOTE ON THE EUROPEAN PROGRESS MICROFINANCE FACILITY AND

Nedbank Group 2018 ESG INVESTOR BRIEFING. JSE November 2018

Nedbank Group 2018 ESG INVESTOR BRIEFING JSE November 2018 Agenda Nedbank s high-level ESG journey Delivering our purpose & delivering on the SDGs (Environment & Social) Through our businesses Through

Nedbank Group 2018 ESG INVESTOR BRIEFING JSE November 2018 Agenda Nedbank s high-level ESG journey Delivering our purpose & delivering on the SDGs (Environment & Social) Through our businesses Through

Enterprise and Supplier Development (ESD) now counts 40 points on the revised B-BBEE Scorecard

now counts 40 points on the revised B-BBEE Scorecard") Enterprise Development Enterprise and Supplier Development (ESD) now counts 40 points on the revised B-BBEE Scorecard It has become imperative that companies give more thought to investing collectively

Enterprise Development Enterprise and Supplier Development (ESD) now counts 40 points on the revised B-BBEE Scorecard It has become imperative that companies give more thought to investing collectively

SMME Finance Sector Background Paper: A Review of key documents on SMME Finance Client: FinMark Trust. April 2004.

SMME Finance Sector Background Paper: A Review of key documents on SMME Finance 1994-2004 Client: FinMark Trust April 2004 Submitted by: Angela Motsa & Associates strategy, research, training and project

SMME Finance Sector Background Paper: A Review of key documents on SMME Finance 1994-2004 Client: FinMark Trust April 2004 Submitted by: Angela Motsa & Associates strategy, research, training and project

Rural Development Programmes. Financial Instruments: making funding go further

Financial Instruments: making funding go further EU rural development funding provides significant benefits for EU citizens and even more benefits are possible by using Financial Instruments (FIs) to recycle

Financial Instruments: making funding go further EU rural development funding provides significant benefits for EU citizens and even more benefits are possible by using Financial Instruments (FIs) to recycle

Democratic Socialist Republic of Sri Lanka. Smallholder Agribusiness Partnerships (SAP) Programme. Negotiated financing agreement

Programme. Negotiated financing agreement") Document: EB 2017/120/R.13/Sup.1 Agenda: 9(b)(iii) Date: 8 April 2017 Distribution: Public Original: English E Democratic Socialist Republic of Sri Lanka Smallholder Agribusiness Partnerships (SAP) Programme

Document: EB 2017/120/R.13/Sup.1 Agenda: 9(b)(iii) Date: 8 April 2017 Distribution: Public Original: English E Democratic Socialist Republic of Sri Lanka Smallholder Agribusiness Partnerships (SAP) Programme

MicroBank. Facilitating the access to microfinance

MicroBank The Social Bank of la Caixa Facilitating the access to microfinance Conference on Microfinance in Europe Brussels - November 10, 2010 2 la Caixa Savings Bank MicroBank was created in 2007 as

MicroBank The Social Bank of la Caixa Facilitating the access to microfinance Conference on Microfinance in Europe Brussels - November 10, 2010 2 la Caixa Savings Bank MicroBank was created in 2007 as

Strategic Corporate Plan

Strategic Corporate Plan 2012-2017 Dr. Jeffrey Mahachi Acting chief Executive Officer Jeffreym@nhbrc.org.za Click to edit Master subtitle style 13 March 2012 Vision A world class home builders warranty

Strategic Corporate Plan 2012-2017 Dr. Jeffrey Mahachi Acting chief Executive Officer Jeffreym@nhbrc.org.za Click to edit Master subtitle style 13 March 2012 Vision A world class home builders warranty

FY2018 ANNUAL RESULTS RETIREMENTS WEALTH INVESTMENTS INSURANCE. Twelve months to 31 March 2018

FY2018 ANNUAL RESULTS Twelve months to 31 March 2018 Andrew A. Darfoor Group Chief Executive Naidene Ford-Hoon Group Chief Financial Officer RETIREMENTS WEALTH INVESTMENTS INSURANCE Presentation agenda

FY2018 ANNUAL RESULTS Twelve months to 31 March 2018 Andrew A. Darfoor Group Chief Executive Naidene Ford-Hoon Group Chief Financial Officer RETIREMENTS WEALTH INVESTMENTS INSURANCE Presentation agenda

NATIONAL TREASURY STRATEGIC PLAN 2013/17 PRESENTATION TO PARLIAMENTARY FINANCE COMMITTEES

NATIONAL TREASURY STRATEGIC PLAN 2013/17 PRESENTATION TO PARLIAMENTARY FINANCE COMMITTEES 14 May 2013 TREASURY AIMS AND OBJECTIVES Chapter 13 of the Constitution of the Republic of South Africa. According

NATIONAL TREASURY STRATEGIC PLAN 2013/17 PRESENTATION TO PARLIAMENTARY FINANCE COMMITTEES 14 May 2013 TREASURY AIMS AND OBJECTIVES Chapter 13 of the Constitution of the Republic of South Africa. According

3. The Macro Framework

3. The Macro Framework 3.1 Introduction T he aim of this section is to cover the broad policy and institutional framework in place to support business development and development of the financial sector

3. The Macro Framework 3.1 Introduction T he aim of this section is to cover the broad policy and institutional framework in place to support business development and development of the financial sector

ANNUAL REPORT AND FINANCIAL RESULTS 31 MARCH 2011

ANNUAL REPORT AND FINANCIAL RESULTS 31 MARCH 2011 Standing Committee on Finance 18 October 2011 Delegation Name Mr. Nhlanhla Nene Mr. Jabu Moleketi Mr Paul Baloyi Mr. Paul Kibuuka Mr. Luther Mashaba Mr.

ANNUAL REPORT AND FINANCIAL RESULTS 31 MARCH 2011 Standing Committee on Finance 18 October 2011 Delegation Name Mr. Nhlanhla Nene Mr. Jabu Moleketi Mr Paul Baloyi Mr. Paul Kibuuka Mr. Luther Mashaba Mr.

Job creation: Progress Microfinance implementation report frequently asked questions

EUROPEAN COMMISSION MEMO Brussels, 17 July 2012 Job creation: Progress Microfinance implementation report 2011 - frequently asked questions The European Progress Microfinance Facility (Progress Microfinance)

EUROPEAN COMMISSION MEMO Brussels, 17 July 2012 Job creation: Progress Microfinance implementation report 2011 - frequently asked questions The European Progress Microfinance Facility (Progress Microfinance)

Enterprise Development Fund- Concept Idea. March 2014

- Concept Idea March 2014 Enterprise Development Enterprise and Supplier Development (ESD) now counts 40 points on the revised B-BBEE Scorecard It has become imperative that companies give more thought

- Concept Idea March 2014 Enterprise Development Enterprise and Supplier Development (ESD) now counts 40 points on the revised B-BBEE Scorecard It has become imperative that companies give more thought

Momentum Consult Intermediary Value Proposition

Momentum Consult Intermediary Value Proposition Why - how - what Why How What What How Why Why How What What Why How What How Why How What What How Why Financial Wellness What is our purpose? What is our

Momentum Consult Intermediary Value Proposition Why - how - what Why How What What How Why Why How What What Why How What How Why How What What How Why Financial Wellness What is our purpose? What is our

LAND BANK ANNUAL REPORT FY2017

LAND BANK ANNUAL REPORT FY2017 LAUNCH: 3 AUGUST 2017 CONTENT 1. Opening Remarks by Programme Director, Mrs. Konehali Gugushe 2. Remarks by Land Bank Board Member, Mrs. Sue Lund 3. Presentation by The CEO,

LAND BANK ANNUAL REPORT FY2017 LAUNCH: 3 AUGUST 2017 CONTENT 1. Opening Remarks by Programme Director, Mrs. Konehali Gugushe 2. Remarks by Land Bank Board Member, Mrs. Sue Lund 3. Presentation by The CEO,

DEPARTMENT OF SMALL BUSINESS DEVELOPMENT PRESENTATION ON THE APP FOR QUARTER 3 AND QUARTER 4 OF 2014/15 FINANCIAL YEAR

DEPARTMENT OF SMALL BUSINESS DEVELOPMENT PRESENTATION ON THE APP FOR QUARTER 3 AND QUARTER 4 OF 2014/15 FINANCIAL YEAR QUARTER 3 OF 2014/15 FINANCIAL YEAR Presentation Outline Purpose Challenges Programmes

DEPARTMENT OF SMALL BUSINESS DEVELOPMENT PRESENTATION ON THE APP FOR QUARTER 3 AND QUARTER 4 OF 2014/15 FINANCIAL YEAR QUARTER 3 OF 2014/15 FINANCIAL YEAR Presentation Outline Purpose Challenges Programmes

BANK SUPERVISION DIVISION MICROFINANCE INDUSTRY REPORT FOR

BANK SUPERVISION DIVISION MICROFINANCE INDUSTRY REPORT FOR QUARTER ENDED 30 SEPTEMBER 2017 1. Executive Summary 1.1. The microfinance sector continues to contribute towards the financial emancipation and

BANK SUPERVISION DIVISION MICROFINANCE INDUSTRY REPORT FOR QUARTER ENDED 30 SEPTEMBER 2017 1. Executive Summary 1.1. The microfinance sector continues to contribute towards the financial emancipation and

OPERATIONS MANUAL BANK POLICIES (BP) These policies were prepared for use by ADB staff and are not necessarily a complete treatment of the subject.

These policies were prepared for use by ADB staff and are not necessarily a complete treatment of the subject.") Page 1 of 1 OPERATIONS MANUAL BANK POLICIES (BP) These policies were prepared for use by ADB staff and are not necessarily a complete treatment of the subject. A. Introduction FINANCIAL INTERMEDIATION

Page 1 of 1 OPERATIONS MANUAL BANK POLICIES (BP) These policies were prepared for use by ADB staff and are not necessarily a complete treatment of the subject. A. Introduction FINANCIAL INTERMEDIATION

Understanding Rural Finance Issues and the Macro and Micro Operating Environment. Module 2 Rural Finance & Microfinance Actors and approaches

Understanding Rural Finance Issues and the Macro and Micro Operating Environment Module 2 Rural Finance & Microfinance Actors and approaches Rural and Agricultural Finance Module 2 Agenda Block 1 Introductions

Understanding Rural Finance Issues and the Macro and Micro Operating Environment Module 2 Rural Finance & Microfinance Actors and approaches Rural and Agricultural Finance Module 2 Agenda Block 1 Introductions

Entrepreneurship-Based Development Capital Sources

Entrepreneurship-Based Development Capital Sources Kyle Arganbright, Chief Operating Officer and Co-Founder - Sandhills State Bank Glennis McClure, Program Manager Nebraska Enterprise Fund How do Banks

Entrepreneurship-Based Development Capital Sources Kyle Arganbright, Chief Operating Officer and Co-Founder - Sandhills State Bank Glennis McClure, Program Manager Nebraska Enterprise Fund How do Banks

SAFCOL s Annual Financial Statements and Report For the year ended 31 March 2011

SAFCOL s Annual Financial Statements and Report For the year ended 31 March 2011 Presented by Maureen Manyama-Matome Acting Chief Executive Officer 1 November 2011 Presentation GROWTH to the Portfolio

SAFCOL s Annual Financial Statements and Report For the year ended 31 March 2011 Presented by Maureen Manyama-Matome Acting Chief Executive Officer 1 November 2011 Presentation GROWTH to the Portfolio

Paul A. Chin Acting General Manager Microfinance Services Division MONEY TALKS: CAPITAL FUNDING

Paul A. Chin Acting General Manager Microfinance Services Division MONEY TALKS: CAPITAL FUNDING Presented at Jampro s #DoBizJA Agriculture Investment Forum November 15, 2016 INCREASING ACCESS TO FINANCING

Paul A. Chin Acting General Manager Microfinance Services Division MONEY TALKS: CAPITAL FUNDING Presented at Jampro s #DoBizJA Agriculture Investment Forum November 15, 2016 INCREASING ACCESS TO FINANCING

FNB PROGRESS FUND APPLICATION FOR BUSINESS FINANCING

FNB POGESS FUND APPLICATION FO BUSINESS FINANCING BUSINESS INFOMATION FO FNB USE ONLY FNB branch elationship Manager (M) receipt date M name E-mail Details of applicant Name of applicant Trading name Physical

FNB POGESS FUND APPLICATION FO BUSINESS FINANCING BUSINESS INFOMATION FO FNB USE ONLY FNB branch elationship Manager (M) receipt date M name E-mail Details of applicant Name of applicant Trading name Physical

EDD Annual Performance Plan

2013/14 EDD Annual Performance Plan 13 March 2013 Economic Development Department 1 2 1 Table of Contents FOREWORD PART A: STRATEGIC OVERVIEW 1. Updated Situational Analysis Performance Environment Organisational

2013/14 EDD Annual Performance Plan 13 March 2013 Economic Development Department 1 2 1 Table of Contents FOREWORD PART A: STRATEGIC OVERVIEW 1. Updated Situational Analysis Performance Environment Organisational

The Status of Agricultural and Rural Financial Services in Southern Africa Zambia Country Report

The Status of Agricultural and Rural Financial Services in Southern Africa Zambia Country Report Lemmy Manje, Melanie Newman Wilkinson Taj Pomodzi Hotel Friday, 13 th December 2013 Making financial markets

The Status of Agricultural and Rural Financial Services in Southern Africa Zambia Country Report Lemmy Manje, Melanie Newman Wilkinson Taj Pomodzi Hotel Friday, 13 th December 2013 Making financial markets

Presentation of the Strategic Plan and APP April 2015

The Presidency: Department of Planning, Monitoring and Evaluation Presentation of the Strategic Plan 2015-2020 and APP 2015-2016 15 April 2015 Structure of the Presentation 1. Background to the DPME 2.

The Presidency: Department of Planning, Monitoring and Evaluation Presentation of the Strategic Plan 2015-2020 and APP 2015-2016 15 April 2015 Structure of the Presentation 1. Background to the DPME 2.

QUARTERLY PERFORMANCE REPORT OF THE MICROFINANCE SECTOR. as at 31 March 2017 ZAMFI CREDIT ONLY MFI MEMBERS

Zimbabwe Association of Microfinance Institutions creating sustainable microfinance QUARTERLY PERFORMANCE REPORT OF THE MICROFINANCE SECTOR as at 31 March 2017 ZAMFI CREDIT ONLY MFI MEMBERS 1 PERFORMANCE

Zimbabwe Association of Microfinance Institutions creating sustainable microfinance QUARTERLY PERFORMANCE REPORT OF THE MICROFINANCE SECTOR as at 31 March 2017 ZAMFI CREDIT ONLY MFI MEMBERS 1 PERFORMANCE

SOUTH AFRICAN BANKING SECTOR OVERVIEW

1 SOUTH AFRICAN BANKING SECTOR OVERVIEW TABLE OF CONTENTS Sections Page 1 Background 1 2. Total Assets 1 3. Total liabilities 3 4. Credit extension 4 5. Branches and ATMs 5 6. Usage of payment systems

1 SOUTH AFRICAN BANKING SECTOR OVERVIEW TABLE OF CONTENTS Sections Page 1 Background 1 2. Total Assets 1 3. Total liabilities 3 4. Credit extension 4 5. Branches and ATMs 5 6. Usage of payment systems

CODES OF GOOD PRACTICE FOR THE SOUTH AFRICAN MINERALS INDUSTRY

(15 June 2017 to date) MINERAL AND PETROLEUM RESOURCES DEVELOPMENT ACT 28 OF 2002 (Gazette No. 23922, Notice No. 1273 dated 10 October 2002. Commencement date: 1 May 2004 [Proc. No. R25, Gazette No. 26264])

(15 June 2017 to date) MINERAL AND PETROLEUM RESOURCES DEVELOPMENT ACT 28 OF 2002 (Gazette No. 23922, Notice No. 1273 dated 10 October 2002. Commencement date: 1 May 2004 [Proc. No. R25, Gazette No. 26264])

An EMPOWERDEX Guide. The Codes of Good Practice. Codes Definitions

An EMPOWERDEX Guide The Codes of Good Practice Codes Definitions ABET: Means Adult Basic Education and Training as determined by the National Qualifications Authority Accreditation Body: Means the South

An EMPOWERDEX Guide The Codes of Good Practice Codes Definitions ABET: Means Adult Basic Education and Training as determined by the National Qualifications Authority Accreditation Body: Means the South

AUSTRALIA INTERMEDIATED (CGU) INVESTOR BRIEFING

INVESTOR BRIEFING") 9 March 2012 ABN 60 090 739 923 AUSTRALIA INTERMEDIATED (CGU) INVESTOR BRIEFING Mike Wilkins Managing Director and Chief Executive Officer Peter Harmer Chief Executive Officer Australia Intermediated (CGU)

9 March 2012 ABN 60 090 739 923 AUSTRALIA INTERMEDIATED (CGU) INVESTOR BRIEFING Mike Wilkins Managing Director and Chief Executive Officer Peter Harmer Chief Executive Officer Australia Intermediated (CGU)

Public Disclosure Copy. Implementation Status & Results Report FATA Rural Livelihoods and Community Infrastructure Project (RLCIP) (P126833)

(P126833)") SOUTH ASIA Pakistan Agriculture and Rural Development Global Practice Recipient Executed Activities Specific Investment Loan FY 2012 Seq No: 7 ARCHIVED on 08-May-2015 ISR19105 Implementing Agencies: FATA

SOUTH ASIA Pakistan Agriculture and Rural Development Global Practice Recipient Executed Activities Specific Investment Loan FY 2012 Seq No: 7 ARCHIVED on 08-May-2015 ISR19105 Implementing Agencies: FATA

Financing Agriculture Forum 2013: Profitable Agricultural Banking Colombo, Sri Lanka. Florence Kariuki August 2013

Financing Agriculture Forum 2013: Profitable Agricultural Banking Colombo, Sri Lanka Florence Kariuki August 2013 Introduction Equity Bank was founded as Equity Building Society (EBS) in October 1984 and

Financing Agriculture Forum 2013: Profitable Agricultural Banking Colombo, Sri Lanka Florence Kariuki August 2013 Introduction Equity Bank was founded as Equity Building Society (EBS) in October 1984 and

Reviewing the Role of Namibia Post Savings Bank (NSB) in Broadening Access to Financial Services to the Poor. Problem Statement Background...

in Broadening Access to Financial Services to the Poor. Problem Statement Background...") Reviewing the Role of Namibia Post Savings Bank (NSB) in Broadening Access to Financial Services to the Poor Table of Contents Problem Statement... 3 Background... 3 Analysis... 4 The Status Quo of Nampost

Reviewing the Role of Namibia Post Savings Bank (NSB) in Broadening Access to Financial Services to the Poor Table of Contents Problem Statement... 3 Background... 3 Analysis... 4 The Status Quo of Nampost

OLD MUTUAL INVESTMENT GROUP RESPONSIBLE OWNERSHIP GUIDELINES

RESPONSIBLE INVESTMENT POSITIVE FUTURES OLD MUTUAL INVESTMENT GROUP RESPONSIBLE OWNERSHIP GUIDELINES First published: JULY 2012 Latest update: JANUARY 2016 1 TABLE OF CONTENTS 1. INTRODUCTION 1 2. OLD

RESPONSIBLE INVESTMENT POSITIVE FUTURES OLD MUTUAL INVESTMENT GROUP RESPONSIBLE OWNERSHIP GUIDELINES First published: JULY 2012 Latest update: JANUARY 2016 1 TABLE OF CONTENTS 1. INTRODUCTION 1 2. OLD

SECTION SIX: Labour Demand Forecasting Model

PAGE 115 SECTION SIX: Labour Demand Forecasting Model 6.1. INTRODUCTION The demand for labour up to 2010 according to the SIC sectors have been estimated through the development of a labour demand model.

PAGE 115 SECTION SIX: Labour Demand Forecasting Model 6.1. INTRODUCTION The demand for labour up to 2010 according to the SIC sectors have been estimated through the development of a labour demand model.

TRANSFORMATION POLICY OF THE SOUTH AFRICAN NATIONAL ROADS AGENCY SOC LIMITED

TRANSFORMATION POLICY OF THE SOUTH AFRICAN NATIONAL ROADS AGENCY SOC LIMITED South African National Roads Agency SOC Limited (SANRAL) Transformation Policy Policy Reference Number Version Number Effective

TRANSFORMATION POLICY OF THE SOUTH AFRICAN NATIONAL ROADS AGENCY SOC LIMITED South African National Roads Agency SOC Limited (SANRAL) Transformation Policy Policy Reference Number Version Number Effective

RURAL HOUSING LOAN FUND

RURAL HOUSING LOAN FUND Presentation at the : ANNUAL WORKSHOP 23 MARCH 2017 JABULANI FAKAZI, CEO 1 Outline 2 RHLF mandate Howe we create value for people in our mandate Business model RHLF Pricing Policy

RURAL HOUSING LOAN FUND Presentation at the : ANNUAL WORKSHOP 23 MARCH 2017 JABULANI FAKAZI, CEO 1 Outline 2 RHLF mandate Howe we create value for people in our mandate Business model RHLF Pricing Policy

A Perspective of ASEAN Financial Sector under the Global Financial Crisis: Assisting SMEs Through Financial Sector Intervention in Asia

International Conference on A Perspective of Asian Financial Sector under the Global Financial Crisis January 21, 2010 A Perspective of ASEAN Financial Sector under the Global Financial Crisis: Assisting

International Conference on A Perspective of Asian Financial Sector under the Global Financial Crisis January 21, 2010 A Perspective of ASEAN Financial Sector under the Global Financial Crisis: Assisting

PROGRAM-FOR-RESULTS INFORMATION DOCUMENT (PID) CONCEPT STAGE Report No.:

CONCEPT STAGE Report No.:") Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized PROGRAM-FOR-RESULTS INFORMATION DOCUMENT (PID) CONCEPT STAGE Report No.: 113653 Program

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized PROGRAM-FOR-RESULTS INFORMATION DOCUMENT (PID) CONCEPT STAGE Report No.: 113653 Program

Deep and Comprehensive Free Trade Area (DCFTA) Initiative East

Initiative East") Deep and Comprehensive Free Trade Area (DCFTA) Initiative East Chisinau 4 July 2017 European Investment Bank European Investment Fund 1 DCFTA Initiative East Deep and Comprehensive Free Trade Area (DCFTA)

Deep and Comprehensive Free Trade Area (DCFTA) Initiative East Chisinau 4 July 2017 European Investment Bank European Investment Fund 1 DCFTA Initiative East Deep and Comprehensive Free Trade Area (DCFTA)

Parliament Standing Committee of Finance. CEO Goolam Aboobaker

Parliament Standing Committee of Finance CEO Goolam Aboobaker 1 Agenda LEGISLATIVE MANDATE GOVERNMENT COMPONENT FUNDS ADMINISTERED VISION / MISSION / GOALS / VALUES BUDGET CORE OPERATIONS THE NDP AND GPAA

Parliament Standing Committee of Finance CEO Goolam Aboobaker 1 Agenda LEGISLATIVE MANDATE GOVERNMENT COMPONENT FUNDS ADMINISTERED VISION / MISSION / GOALS / VALUES BUDGET CORE OPERATIONS THE NDP AND GPAA

POSTAL FINANCIAL INCLUSION

POSTAL FINANCIAL INCLUSION Dr. Vuyo Mahlati Chairperson of Board, South African Post Office UPU Workshop Berne, Switzerland 31 October 1 November 2011 Postbank central to SAPO Mandate, Growth and Sustainability

POSTAL FINANCIAL INCLUSION Dr. Vuyo Mahlati Chairperson of Board, South African Post Office UPU Workshop Berne, Switzerland 31 October 1 November 2011 Postbank central to SAPO Mandate, Growth and Sustainability

Microfinance for Agriculture: Perspectives from India

Microfinance for Agriculture: Perspectives from India SATISH PILLARISETTI National Bank for Agriculture and Rural Development (NABARD) INDIA 11 December 2007 1 PROLOGUE State interventions in rural finance

Microfinance for Agriculture: Perspectives from India SATISH PILLARISETTI National Bank for Agriculture and Rural Development (NABARD) INDIA 11 December 2007 1 PROLOGUE State interventions in rural finance

Southern African-German Chamber of Commerce and Industry Enterprise and Supplier Development Fund

Southern African-German Chamber of Commerce and Industry Enterprise and Supplier Development Fund 1 2 NEF MANDATE Grow black economic participation Financial & non-financial support Culture of savings

Southern African-German Chamber of Commerce and Industry Enterprise and Supplier Development Fund 1 2 NEF MANDATE Grow black economic participation Financial & non-financial support Culture of savings

Microfinance and Energy Clients Win with Partnership Model in Uganda

FIELD BRIEF No. 9 Microfinance and Energy Clients Win with Partnership Model in Uganda A Case Study of FINCA s Microfinance and Renewable Energy Pilot Activity This FIELD Brief is the ninth in a series

FIELD BRIEF No. 9 Microfinance and Energy Clients Win with Partnership Model in Uganda A Case Study of FINCA s Microfinance and Renewable Energy Pilot Activity This FIELD Brief is the ninth in a series

Private Sector Facility: Working with Local Private Entities, Including Small and Medium-Sized Enterprises

Private Sector Facility: Working with Local Private Entities, Including Small and Medium-Sized Enterprises GCF/B.09/12 5 March 2015 Meeting of the Board 24-26 March 2015 Songdo, Republic of Korea Agenda

Private Sector Facility: Working with Local Private Entities, Including Small and Medium-Sized Enterprises GCF/B.09/12 5 March 2015 Meeting of the Board 24-26 March 2015 Songdo, Republic of Korea Agenda

NATIONAL YOUTH DEVELOPMENT AGENCY QUARTER 3 PERFORMANCE AND FINANCIAL ANALYSIS 2012/2013 PRESENTATION TO PARLIAMENT DATE: 26 MARCH 2013

NATIONAL YOUTH DEVELOPMENT AGENCY QUARTER 3 PERFORMANCE AND FINANCIAL ANALYSIS 2012/2013 PRESENTATION TO PARLIAMENT DATE: 26 MARCH 2013 PRESENTATION OUTLINE SECTION PART A CONTENTS NYDA Q3 Performance

NATIONAL YOUTH DEVELOPMENT AGENCY QUARTER 3 PERFORMANCE AND FINANCIAL ANALYSIS 2012/2013 PRESENTATION TO PARLIAMENT DATE: 26 MARCH 2013 PRESENTATION OUTLINE SECTION PART A CONTENTS NYDA Q3 Performance

CONFERENCE ON OVER- INDEBTEDNESS AN OVERVIEW OF THE NCR S RESEARCH,AWARENESS & EDUCATION ACTIVITIES AS PART OF EXECUTING ITS MANDATE

CONFERENCE ON OVER- INDEBTEDNESS AN OVERVIEW OF THE NCR S RESEARCH,AWARENESS & EDUCATION ACTIVITIES AS PART OF EXECUTING ITS MANDATE Nomsa Motshegare AUGUST 2010 Reckless lending National Credit Act became

CONFERENCE ON OVER- INDEBTEDNESS AN OVERVIEW OF THE NCR S RESEARCH,AWARENESS & EDUCATION ACTIVITIES AS PART OF EXECUTING ITS MANDATE Nomsa Motshegare AUGUST 2010 Reckless lending National Credit Act became

Ola Busari. Acting CEO, TCTA. 18 April 2018

Ola Busari Acting CEO, TCTA 1 18 April 2018 Strategic Overview Pre-determined Objectives Current TCTA Directives Balanced Scorecard Budget Funding Program Discussion & Clarifications 2 3 Vision To be the

Ola Busari Acting CEO, TCTA 1 18 April 2018 Strategic Overview Pre-determined Objectives Current TCTA Directives Balanced Scorecard Budget Funding Program Discussion & Clarifications 2 3 Vision To be the

AMFI SECTOR REPORT DECEMBER 2017

AMFI SECTOR REPORT DECEMBER 2017 1.1.0: INTRODUCTION 1.1.1: BACKGROUND INFORMATION The Association for Microfinance Institutions (AMFI) is a member-based organization that was established and registered

AMFI SECTOR REPORT DECEMBER 2017 1.1.0: INTRODUCTION 1.1.1: BACKGROUND INFORMATION The Association for Microfinance Institutions (AMFI) is a member-based organization that was established and registered

Microinsurance Technical Advisory Group. MICROINSURANCE LANDSCAPE - ZAMBIA MICROINSURANCE FOCUS NOTE No. 9 JUNE Funded by

Microinsurance Technical Advisory Group FOCUS NOTE No. 9 JUNE 2018 Funded by ABOUT THIS FOCUS NOTE Since 2009, the Technical Advisory Group for Microinsurance (TAG) has been spearheading the development

Microinsurance Technical Advisory Group FOCUS NOTE No. 9 JUNE 2018 Funded by ABOUT THIS FOCUS NOTE Since 2009, the Technical Advisory Group for Microinsurance (TAG) has been spearheading the development

Welcome to the FinCoNet newsletter

Issue 1 March 2019 201420140142014 CONTENTS Welcome 1 In focus 2 Current issues forum 4 Microfinance: new caps for marginal debt value and daily interest rate Conduct of Business Returns for the South

Issue 1 March 2019 201420140142014 CONTENTS Welcome 1 In focus 2 Current issues forum 4 Microfinance: new caps for marginal debt value and daily interest rate Conduct of Business Returns for the South

Statement of Performance Expectations

B: 34 Statement of Performance Expectations 2016-2017 Start up capital for New Zealand tech companies NZVIF OVERVIEW HOW NZVIF OPERATES NZVIF is the Crown s lead equity investment agency addressing the

B: 34 Statement of Performance Expectations 2016-2017 Start up capital for New Zealand tech companies NZVIF OVERVIEW HOW NZVIF OPERATES NZVIF is the Crown s lead equity investment agency addressing the

Ghana : Financial services for women entrepreneurs in the informal sector

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized No. 136 June 1999 Findings occasionally reports on development initiatives not assisted

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized No. 136 June 1999 Findings occasionally reports on development initiatives not assisted

3 1 M a y TECHNOLOGY AND HUMAN RESOURCES FOR INDUSTRY PROGRAMME MCDM GUIDE FOR THE EVALUATION AND PRIORITISATION OF THRIP PROJECTS

3 1 M a y 2 0 1 2 MCDM GUIDE FOR THE EVALUATION AND PRIORITISATION OF THRIP PROJECTS NOTE: Applicants are strongly advised to read this MCDM document in conjunction with the THRIP GUIDE MISSION STATEMENT

3 1 M a y 2 0 1 2 MCDM GUIDE FOR THE EVALUATION AND PRIORITISATION OF THRIP PROJECTS NOTE: Applicants are strongly advised to read this MCDM document in conjunction with the THRIP GUIDE MISSION STATEMENT

GUIDELINES FOR THE OPERATION OF MICRO, SMALL AND MEDIUM ENTERPRISES DEVELOPMENT FUND FOR NIGERIA

GUIDELINES FOR THE OPERATION OF MICRO, SMALL AND MEDIUM ENTERPRISES DEVELOPMENT FUND FOR NIGERIA 1. Background Chapter One A large number of un-served and under-served clients exist in the Nigerian MSME

GUIDELINES FOR THE OPERATION OF MICRO, SMALL AND MEDIUM ENTERPRISES DEVELOPMENT FUND FOR NIGERIA 1. Background Chapter One A large number of un-served and under-served clients exist in the Nigerian MSME

BancoEstado. Social Bond Framework

BancoEstado Social Bond Framework TABLE OF CONTENTS 1. Introduction 3 2. Rationale for BancoEstado to issue a Social Bond 3 3. BancoEstado Social Bond Framework 4 3.1 Use of Proceeds 4 3.2 Project Evaluation

BancoEstado Social Bond Framework TABLE OF CONTENTS 1. Introduction 3 2. Rationale for BancoEstado to issue a Social Bond 3 3. BancoEstado Social Bond Framework 4 3.1 Use of Proceeds 4 3.2 Project Evaluation

Chief Executive s Review. Delivering our Strategic Objectives

2014 saw AIB successfully execute its three year plan to deliver a bank that is sustainably profitable, adequately capitalised and appropriately funded. We have a strong momentum in our business and are

2014 saw AIB successfully execute its three year plan to deliver a bank that is sustainably profitable, adequately capitalised and appropriately funded. We have a strong momentum in our business and are

EU financial engineering instruments for revitalization of degraded urban areas BGK experiences

EU financial engineering instruments for revitalization of degraded urban areas BGK experiences Ewa Kołodziej Mateusz Andrzejewski Bank Gospodarstwa Krajowego Brussels 7th March 2016 BANK GOSPODARSTWA

EU financial engineering instruments for revitalization of degraded urban areas BGK experiences Ewa Kołodziej Mateusz Andrzejewski Bank Gospodarstwa Krajowego Brussels 7th March 2016 BANK GOSPODARSTWA

SCOPE OF WORK AND APPLICATION GUIDELINES

SCOPE OF WORK AND APPLICATION GUIDELINES Investment Promotion Expert Ethiopia Investment Commission Dated: Wednesday, December 1, 2016 Deadline for submission of applications: by Sunday, December 11, 2016,

SCOPE OF WORK AND APPLICATION GUIDELINES Investment Promotion Expert Ethiopia Investment Commission Dated: Wednesday, December 1, 2016 Deadline for submission of applications: by Sunday, December 11, 2016,

Annual Report Presentation to the Human Settlements Portfolio Committee. Mr. Samson Moraba CEO 02 September 2011

Annual Report Presentation to the Human Settlements Portfolio Committee Mr. Samson Moraba CEO 02 September 2011 Mandate, Vision, Mission Strategic Objectives NHFC Values NHFC Outcomes NHFC Past Performance

Annual Report Presentation to the Human Settlements Portfolio Committee Mr. Samson Moraba CEO 02 September 2011 Mandate, Vision, Mission Strategic Objectives NHFC Values NHFC Outcomes NHFC Past Performance

SAMRUDHI Micro Fin Society (SMS) Brief Profile

Brief Profile") SAMRUDHI Micro Fin Society (SMS) Brief Profile 1 The Problem Sixty percent of the population in India lives below poverty line and they suffers from high rates of hunger and malnutrition. To cope with

SAMRUDHI Micro Fin Society (SMS) Brief Profile 1 The Problem Sixty percent of the population in India lives below poverty line and they suffers from high rates of hunger and malnutrition. To cope with

INVESTOR BRIEFING SESSION (hosted by Avior Capital)

") INVESTOR BRIEFING SESSION (hosted by Avior Capital) 22 March 2018 Andrew A. Darfoor Group Chief Executive RETIREMENTS WEALTH INVESTMENTS INSURANCE Disclaimer 2 The views expressed here may contain information

INVESTOR BRIEFING SESSION (hosted by Avior Capital) 22 March 2018 Andrew A. Darfoor Group Chief Executive RETIREMENTS WEALTH INVESTMENTS INSURANCE Disclaimer 2 The views expressed here may contain information

Housing Microfinance in South Africa: Status, Problems and Prospects. Based on literature review, interviews, workshop inputs & peer inputs

A Mouse That Roared? Housing Microfinance in South Africa: Status, Problems and Prospects FinMark Forum Sandton David Gardner 18 September, 2008 Study Background Finmark Trust & HIVOS-funded Based on literature

A Mouse That Roared? Housing Microfinance in South Africa: Status, Problems and Prospects FinMark Forum Sandton David Gardner 18 September, 2008 Study Background Finmark Trust & HIVOS-funded Based on literature

ARIES. FINCA Program Brief No. 4 AFGHANISTAN. Agriculture, Rural Investment and Enterprise Strengthening Program in Afghanistan

ARIES Agriculture, Rural Investment and Enterprise Strengthening Program in Afghanistan FINCA Program Brief No. 4 AFGHANISTAN The Financial Integration, Economic Leveraging, Broad-Based Dissemination Leader

ARIES Agriculture, Rural Investment and Enterprise Strengthening Program in Afghanistan FINCA Program Brief No. 4 AFGHANISTAN The Financial Integration, Economic Leveraging, Broad-Based Dissemination Leader

M2i s Experience in Microfinance

M2i s Experience in Microfinance Title Duration Client Page Implementation of Risk Management International Finance June 2012-May 2015 Framework in 5 MFIs Corporation 3 Adaptation of Global Risk International

M2i s Experience in Microfinance Title Duration Client Page Implementation of Risk Management International Finance June 2012-May 2015 Framework in 5 MFIs Corporation 3 Adaptation of Global Risk International

Results Presentation. For the financial year ended 30 September 2017 AFRICAN BANK HOLDINGS LIMITED 1 DECEMBER

Results Presentation For the financial year ended 30 September 2017 AFRICAN BANK HOLDINGS LIMITED 1 DECEMBER 2017 www.africanbank.co.za Contents CEO review Financial review Outlook 2 Introduction Good

Results Presentation For the financial year ended 30 September 2017 AFRICAN BANK HOLDINGS LIMITED 1 DECEMBER 2017 www.africanbank.co.za Contents CEO review Financial review Outlook 2 Introduction Good

Technical Cooperation s Contribution to Transition in Early Transition Countries: Evidence from Micro, Small and Medium Enterprises Lending 1

WORKING DRAFT Technical Cooperation s Contribution to Transition in Early Transition Countries: Evidence from Micro, Small and Medium Enterprises Lending 1 Office of Chief Economist, the European Bank

WORKING DRAFT Technical Cooperation s Contribution to Transition in Early Transition Countries: Evidence from Micro, Small and Medium Enterprises Lending 1 Office of Chief Economist, the European Bank

QUARTERLY PERFORMANCE REPORT OF THE MICROFINANCE SECTOR. As at 31 March 2018 ZAMFI CREDIT ONLY MFI MEMBERS

Zimbabwe Association of Microfinance Institutions creating sustainable microfinance QUARTERLY PERFORMANCE REPORT OF THE MICROFINANCE SECTOR As at 31 March 2018 ZAMFI CREDIT ONLY MFI MEMBERS 1 Below is

Zimbabwe Association of Microfinance Institutions creating sustainable microfinance QUARTERLY PERFORMANCE REPORT OF THE MICROFINANCE SECTOR As at 31 March 2018 ZAMFI CREDIT ONLY MFI MEMBERS 1 Below is

Investor Briefing & H Performance Presentation Outline

Investor Briefing & Performance August Presentation Outline 1. Macro-economic overview 2. Governance & leadership structure 3. Regional expansion and diversification 4. Innovation & digital banking 5.

Investor Briefing & Performance August Presentation Outline 1. Macro-economic overview 2. Governance & leadership structure 3. Regional expansion and diversification 4. Innovation & digital banking 5.

Supply/Availability of Wholesale Funds for MFIs in Nepal: Challenges and Problems

Supply/Availability of Wholesale Funds for MFIs in Nepal: Challenges and Problems A draft paper prepared for the Microfinance Summit Nepal 2010 (14-16 February, 2010) Kathmandu, Nepal By Nirdhan Utthan

Supply/Availability of Wholesale Funds for MFIs in Nepal: Challenges and Problems A draft paper prepared for the Microfinance Summit Nepal 2010 (14-16 February, 2010) Kathmandu, Nepal By Nirdhan Utthan

The contribution of British American Tobacco South Africa to the Western Cape economy

The contribution of British American Tobacco South Africa to the Western Cape economy A study conducted by Quantec Research, 2016 Contents 2 The contribution of British American Tobacco South Africa to

The contribution of British American Tobacco South Africa to the Western Cape economy A study conducted by Quantec Research, 2016 Contents 2 The contribution of British American Tobacco South Africa to

Myanmar Global Leaders Programme 2018 THE FUTURE OF FINANCE FOR MYANMAR S UNBANKED. Executive Summary

Myanmar Global Leaders Programme 2018 THE FUTURE OF FINANCE FOR MYANMAR S UNBANKED Executive Summary FINANCIAL INCLUSION An estimated 2 billion adults worldwide do not have a basic financial account.

Myanmar Global Leaders Programme 2018 THE FUTURE OF FINANCE FOR MYANMAR S UNBANKED Executive Summary FINANCIAL INCLUSION An estimated 2 billion adults worldwide do not have a basic financial account.