General information document

|

|

|

- Lewis Potter

- 6 years ago

- Views:

Transcription

1 General information document Last updated: January 2018 Natixis, Corporate & Investment Banking Customer Support Department - 40 Avenue des Terroirs de France Paris - BP Paris Cedex 02 mifid_onboarding@natixis.com

2 INTRODUCTION I II III IV V VI VII VIII IX X XI XII Client categorisation and impacts in terms of protection Reclassification process and its consequences Assessment of the clients' knowledge Policy for the management of conflicts of interests Investment advice Fees and benefits Product governance Strengthening of the best order execution policy Recording of communications Information High Frequency Trading ("HFT") and Direct Market Access ( DMA ) Glossary ANNEX: MARKET INFRASTRUCTURE DIAGRAM Page 2

3 INTRODUCTION Following the financial crisis of 2008, in May 2014 the European legislators have adopted a new legal regulatory framework, the so-called MIF 2 framework, in order to take into account the evolution of financial markets and address the weaknesses revealed by the implementation of MIF 1. The MIF 2 pack includes the MiFID 2 Directive 1 and the MiFIR Regulation 2, and will enter into force on the 3rd of January 2018, supplementing the MIF 1 Directive 3. The new regulatory framework amends the conditions governing the activities of investment services providers, and therefore the activities of Natixis 4. The main goals of the MIF 2 framework are to improve the orderly functioning of the market and to increase transparency, while enhancing investor protection. This document aims to present the main innovations of the MIF 2 regulatory framework. All the italicised terms that appear in the text are defined in the Glossary at the end of this document. I - CLIENT CATEGORISATION AND IMPACTS IN TERMS OF PROTECTION Natixis is required to classify the clients to whom it provides investment and ancillary services, according to their aptitude and knowledge in the relevant investment field and service. Pursuant to the regulatory classification criteria, the client is classified within one of the three following categories: a Non-Professional client, a Professional client, an Eligible Counterparty. Natixis is also required to inform the client, in a durable medium, about: their category, any change of category, the possibility of requesting a different category and the consequences involved. The consequence of the classification is that the business protection rules are adapted to each client category and, therefore, to the knowledge and sophistication attached to each category. 1) Non-Professional Clients Non-Professional Clients are those who do not fall within the scope of the definition of a Professional Client or an Eligible Counterparty (cf. the following definitions). Knowing that the regulation does not include any list, clients considered as Non-Professional Clients by Natixis are: Private individuals Organisations under the French 1901 Association Law Local authorities: expressly excluded from the Professional Client category by the MiFID II Directive Unions Cooperatives (such as the French agricultural cooperative AGRALCO) Public health facilities French EARLs (private limited farming companies, whether they be single-member or pluri-partner 1 Directive 2014/65/EU of the European Parliament and Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU. 2 EU Regulation no 600/2014 of the European Parliament and Council of 15 May 2014 on markets in financial instruments and amending EU Regulation no 648/ Directive 2004/39/EC of the European Parliament and Council of 21 April 2004 on markets in financial instruments; Corrigendum to Directive 2004/39/EC of the European Parliament and Council of 21 April 2004 on markets in financial instruments; Commission directive 2006/73/EC of 10 August 2006 implementing Directive 2004/39/EC; Commission regulation (EC) n 1287/2006 of 10 August 2006 implementing Directive 2004/39/EC. 4 Natixis subsidiaries are outside of the scope of this document. Page 3

4 companies) French GAECs (jointly-earned farming companies) French SCEAs (unlimited agricultural development companies) Individual companies Real estate companies IEGs (economic interest groupings) Non-financial corporations (French SAs, public limited companies and equivalents, French SARLs, private corporate entities with limited liability and equivalents, and French SNCs, unlimited partnerships and equivalents...) Regional and local authorities Clients in the Non-Professional Client category benefit from highest level of protection. Therefore, Non-Professional Clients enjoy special protection: - Assessment of their knowledge, their experience in financial investments related to the specific product type or service offered or requested - As well as their financial situation and investment objectives, including their risk tolerance where appropriate. Depending on the offered investment service, this assessment allows for the verification of its appropriateness to the client prior to its provision. The assessment is presented in more detail in section III below. - Provision of specific information on Natixis and its services, financial instruments, investment strategies offered execution venues and the related costs and charges. - Establishment of a legal and regulatory framework listing the rights and obligations of Natixis and its clients through a financial instrument services agreement and an order execution policy which defines transaction execution methods. This policy is updated on an annual and ad hoc basis in order to take into account any changes. 2) Professional Clients; Professional Clients are defined as clients who possess the experience, knowledge and expertise necessary to make their own investment decisions and properly assess the incurred risks. The following shall be regarded as Professionals Clients per se: investment firms, credit institutions, the other authorised or regulated financial institutions; insurance companies, Collective investment schemes and their management companies pension funds and their management companies, commodities and commodity derivatives dealers local firms, and the other institutional investors, national and regional governments, including public bodies that manage public debt at a national or regional level, Central Banks, international and supranational institutions such as the World Bank, the International Monetary Fund, the European Central Bank, the European Investment Bank and other similar international organisations, other institutional investors whose main activity is to invest in financial instruments; including entities operating as securitisation vehicles and carrying out other financial operations, large undertakings meeting two out of the three following size requirements on a company basis: - balance-sheet total equal to or greater than 20 million; - net turnover equal to or greater than 40 million; - capital equal to or greater than 2 million; The level of protection of Professional Clients is lower than that provided to Non-Professional Clients. Page 4

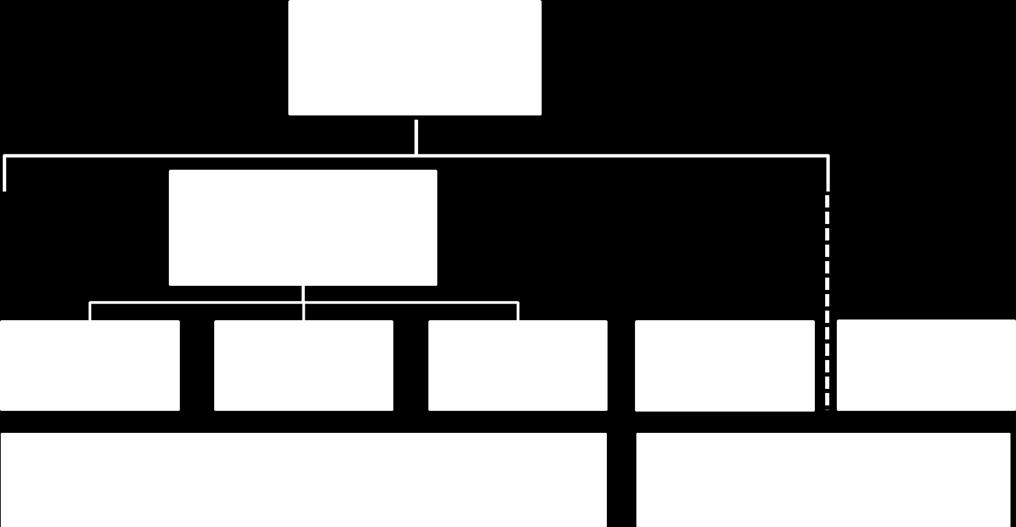

5 Indeed, Professional Clients are presumed to be competent and to have the knowledge of the markets necessary to understand the incurred risks, as well as financially able to bear the losses related to the investment. Takin into account their investment objectives, they only benefit from: an assessment of their investment objectives where Natixis provides them with investment services or a portfolio management services. This assessment according to the investment service provided allows for verification, prior to the provision of the service, that it is appropriate for the concerned client. The assessment is presented in more detail in section III below. a policy for the execution of orders which defines how the transactions are executed. This execution policy is updated annually, and the establishment of a legal and regulatory framework taking into account the rights and obligations of Natixis and its client through a financial instrument services agreement and an order execution policy which defines transaction execution methods. This policy is updated annually and with each modifcation. 3) Eligible Counterparties AN ELIGIBLE COUNTERPARTY CONSTITUTES A CATEGORY OF PROFESSIONAL CLIENTS FOR THE FOLLOWING THREE INVESTMEJNT SERVICES: the reception and transmission of orders on behalf of third parties, the execution of orders on behalf of third parties, own account dealing. Eligible Counterparties remain outside of most business conduct rules concerning these investment services due to their knowledge, competence and financial situation. However, they benefit from some regulatory protection including the requirement for Natixis to act honestly, fairly and professionally in accordance with the best interests of clients, to communicate in a way that is fair, clear and not misleading, and to provide appropriate reports (confirmation of transactions). Natixis provides the Eligible Counterparties with its execution policy for their information. Each of the following is recognised as an Eligible Counterparty: investment firms, credit institutions, insurance companies, UCITS and their management companies, pension funds and their management companies, other financial institutions authorized or regulated under Union law or under the national law of a Member State, national governments and their corresponding offices, including public bodies that deal with public debt at national level, central banks and supranational organisations. Incidentally, Natixis has decided to proceed with the establishment of a legal and regulatory framework listing the rights and obligations of Natixis and its clients through a financial instrument services agreement. II RECLASSIFICATION PROCESS AND ITS CONSEQUENCES Client may request a change in category and opt for a different status within the rules of reclassification illustrated in the diagram below, subject to approval by Natixis (cf. scheme below 5 ). 5 For a Non-Professional Client to opt out of his category and become a Professional Client, at least two of the following criteria shall be met: 1) the client has carried out transactions, in significant size, on the relevant market at an average frequency of 10 per quarter over the previous four quarters; 2) the size the financial instrument portfolio of the person authorised to enter into agreements on behalf of the client, defined as including cash deposits and financial instruments, exceeds EUR 500,000; Page 5

6 Thus, for example, a Non-Professional Client can only change its category and be treated as a Professional Client under the condition that the client meets the classification criteria* mentioned below but also in accordance with the process defined by the regulation. As a consequence, insofar as the protection measures established by Natixis vary depending on the classification adopted, we draw your attention to the consequences of a change in classification category which implies a modification of Natixis's requirements regarding client protection, as well as an adaptation of our contractual policy, where appropriate. Possible reclassification schemes Likewise, the Professional Client or Eligible Counterparty is responsible for notifying Natixis of any changes liable to modify their classification. Finally, if Natixis notes that a Professional Client or an Eligible Counterparty does not meet the criteria that justify its current classification, Natixis shall take the appropriate measures. III - ASSESSMENT OF THE CLIENT'S KNOWLEDGE In order to strengthen client protection, Natixis is required to gather information on each of its clients, assessing the suitability of the financial service to be provided, as well as its appropriateness for the client. This assessment is also aimed at allowing Natixis to check that the service offered to the client depending on the investment service that is provided. 1) Investment advice services: assessment of the suitability of the service to be provided Where Natixis provides investment advice services to its Clients (Non-Professional and Professional; Eligibel Counterparties being treated as Profession Clients for this type of services), it shall gather detailed information on their experience, their investment knowledge, their financial situation, their capacity to bear losses, their investment objectives and their risk tolerance in order to assess whether the offered service or instrument is appropriate to the situation of the client. This request for information is carried out for and with Non-Professional and Professional Clients alike. If Natixis does not obtain the required information, or is it is not accurate or none of the offered services or investments are appropriate, Natixis shall refrain from offering such investment advice services. 2) Other investment services: assessment of the appropriateness of the service to be provided 3) the client works or has worked in the financial sector for at least one year in a professional position, which requires knowledge of the transactions or services envisaged. Page 6

7 In order to assess the appropriateness of the service to be provided, Natixis assesses its client in order to ensure that the service or product is appropriate for the client. Natixis also assesses each Non-Professional Client. In the framework of this assessment, Natixis shall gather information on the experience and investment knowledge of the client where it provides the following investment services: o Dealing on own account, o Execution of orders on behalf of clients, o Reception and transmission of orders in relation to one or more financial instruments, o Underwriting of financial instruments and/or placing of financial instruments on a firm commitment basis o Placing of financial instruments without a firm commitment basis o Operation of an MTF or an OTF With regard to Professional Clients and Eligible Counterparties, Natixis is authorised to presume that they possess the level of experience and knowledge required to understand the risks incurred with these particular investment services and transactions, or with the type of transaction or product for which the client is classified as a Professional Client or an Eligible Counterparty. If Natixis considers based on the information received, that the product or service is not appropriate to the client or potential client, it shall warn him. In the same way, if a client or a Potential client does not provide the required information, Natixis shall warn him that is not able to determine whether the service or product is appropriate for him. IV - POLICY FOR THE MANAGEMENT OF CONFLICTS OF INTERESTS Natixis has a policy in place, set out in writing, the aim of which is to avoid for potential conflicts of interests to affect its clients' interests, and for the identification and management of conflicts or interests and, where appropriate, mitigate those bearing a risk of affecting clients' interests. This policy applies to conflicts of interests liable to occur during Natixis's or a service provider's provision of investment services and ancillary services, or of a combination of those services, and the existence of which bears a risk of affecting clients' interests Where the provisions made by Natixis to prevent conflicts of interests are not sufficient to ensure that the risks of adversely affecting clients' interests is avoided, Natixis clearly informs such clients, prior to acting on their behalf, on the general nature and/or source of these conflicts of interests, as well as the measures taken to mitigate such risks. A summary of Natixis's conflicts of interest policy is available on the firm's website. You can also directly refer to the conflicts of interest policy for further detail. These documents can also be obtained upon written request sent to the following address: Natixis Pole Support Client 40 Avenue des Terroirs de France Paris BP Paris Cedex 02 V - INVESTMENT ADVICE The MIFID 2 Directive requires for Natixis to inform the client - prior to the provision of the investment service - about whether or not the advice is independent. Natixis has decided it will solely provide non-independent investment advice. Page 7

8 Investment advice is addressed to the client upon his request or at Natixis's initiative. That advice is based on the examination of the client's situation or presented as adapted to his profile, and concerns one or several transactions in financial instruments. Should investment advice be provided, Natixis shall assess the suitability of the service to be provided (cf. section III). VI - FEES AND BENEFITS The framework of MIF 2 strictly restricts the payment or receipt of commissions or benefits. The payment to a third party and the receipt by Natixis of remuneration, commissions or non-monetary benefits related to the provision of an investment service or an ancillary service are subject to the following conditions: the fee or benefit aims at improving the quality of the service provided to the client; such payment or benefit does not impair compliance with Natixis's duty to act honestly, fairly and professionally in the best interests of its clients. the nature and amount of the payment or benefit or the method of calculating that amount, shall be clearly disclosed to the client prior to the provision of a service, and in a manner that is comprehensive, accurate and understandable. This regime is not applicable to Eligible Counterparties VII - PRODUCT GOVERNANCE The regulatory framework of MIF 2 includes new requirements in terms of product governance. Where Natixis acts as the manufacturer of financial products, the framework of MIF 2 states that: the establishment of dedicated organisational arrangements (internal governance, experienced staff); the establishment of an internal validation process for each financial instrument; the determination of an identified target market of end clients; the consideration of the charging structure proposed for each financial instrument; the implementation of a strategy for distribution that is compatible with the identified target market; an obligation to inform distributors on products; the regular review of each financial instrument to ensure that it remains consistent with the needs, characteristics and objectives of the target market. Simultaneously, Natixis shall implement and maintain procedures and measures ensuring that the production of financial instruments is carried out in compliance with the requirements regarding the management of conflicts of interests, including remuneration. Natixis controls that the manufactured financial instruments do not adversely affect market integrity. VIII - STRENGTHENING OF THE BEST ORDER EXECUTION POLICY In order to strengthen the protection of Non-Professional and Professional Clients, the new MIF 2 regulatory framework tends to increase the requirements weighting on service providers regarding the execution and routing of orders towards a trading or execution venue, but also to reinforce their best order execution policy. Natixis establishes an order execution policy in order to ensure the best possible result for clients, and to provide them with information on order execution. Natixis shall abide by this "best execution" requirement where it executes, orders on behalf of Professional or Non-Professional Clients, receives and transmits orders on behalf of clients, or deals on own account. To comply with this best execution requirement, Natixis undertakes, inter alia, to: ensure the best possible result to clients (taking into account the price, cost, speed, likelihood of execution and settlement, the size and nature of the order; Page 8

9 provide information on the order execution policy, especially the manner in which they are executed; monitor the effectiveness of its order execution arrangements in order to identify and, where appropriate, correct shortcomings; notify clients where an important modification of such monitoring systems and evaluation arrangements related to the execution of orders or of the order execution policy has occurred; demonstrate (at the request of the client or the competent authority) the best execution of orders; summarise and make public the top five execution venues in terms of trading volumes on which Natixis has executed client orders during the previous year; Etc Natixis shall obtain the prior consent of its clients on its execution policy. Natixis considers that clients consent has been granted when the first order has been placed by the latter. Natixis shall obtain the express prior consent of its clients where the order is executed outside of a trading venue. IX - RECORDING OF COMMUNICATIONS For the same client protection purposes, the framework of MIF 2 includes the obligation to record communications between Natixis and the client for all services provided, all activities carried out and all sales made in order to reinforce the protection of Natixis's clients. Therefore, Natixis shall be able to record the entirety of the records of phone conversation and electronic communications related to at least: the transactions made within the framework of own-account trading and the provision of services linked with the reception, transmission and execution of client orders, even where these conversations and communications do not lead to the conclusion of such transactions or to the provision of services related to client orders. The content of one-on-one conversations with clients is considered as equivalent to an order placement via the phone as soon as it is recorded in writing within a report or notes. These records must be kept for 5 years (or 7 years upon request by the competent national authorities). The relevant client shall be informed that the communications or phone conversations will be recorded prior to the provision of investment services and activities, where such services are related to the reception, transmission and execution of client orders. The relevant client may request that the records related to him be transmitted to him. X - INFORMATION All the requirements pertaining to the provision of information to clients are strengthened by the framework of MIF 2. When investment advice is provided, Natixis shall, in good time before it provides investment advice, inform the client on: whether the advice is provided on an independent basis; whether it relies on a broad or a more restricted analysis of the various types of financial instruments; whether NATIXIS provides a periodic assessment of the suitability of the financial instruments. Furthermore, Natixis shall give the Non-Professional Client, prior to the execution of the transaction, a statement on suitability in a reliable medium specifying the advice given and in which way it fits the client's needs, objectives, and other characteristics. In the case of a bundled offer, Natixis shall inform the client whether it is possible to buy the different components separately and shall provide for a separate evidence of the costs and charges of each component, as well as a an adequate description of the different components of the agreement or bundled offer. The MIF 2 framework also requires for Natixis to provide the client with comprehensive information about all the costs and charges related to an investment service or a financial instrument, regardless of such client's classification. Page 9

10 For Professional Clients and Eligible Counterparties, the information to be provided are adjusted according to the service provided and the nature of the financial instrument if there are derivatives involved. Where appropriate, Natixis informs the client on all the costs and charges related to the investment services and ancillary services. XI - ALGORITHMIC TRADING, HIGH FREQUENCY TRADING ("HFT") AND DIRECT ACCESS MARKET ( DEA ) In order to take into account the evolution of financial markets, the MIF 2 regulatory framework integrates the recent technological developments in trading such as algorithmic trading, high-frequency trading et and direct access market. MIF 2 also includes a number of provisions to meet a twofold objective, namely to improve the quality of the market by preventing and managing potential or actual risks of market disruption related to technological innovations, including risks stemming from algorithmic trading, especially high-frequency trading but also to prevent the risk of these technological innovations for market manipulation. The use of algorithmic trading now entails the obligation to: have in place effective systems and risk controls suitable to the business it operates (resilience, trading limits, appropriate thresholds and limits, prevention of any kind of market disruption, business continuity arrangements and tests); to notify it to the competent authorities of its Member State of origin and to the trading venue; To provide the competent authorities of its Member State of origin with a description of the nature of its algorithmic trading strategies and detailed information on the trading parameters. MIF 2 also strengthens requirements in terms of high frequency trading by imposing the storage of accurate and time sequenced records (including cancellations of orders, executed orders and quotations on trading venues). Finally, in case of provision of a direct access to a trading venue, Natixis shall: Have in place effective systems and controls: appropriateness of clients, trading and credit limits, risk control function, prevention of market disruptions; Ensure that its clients comply with the directive and market regulations; Monitor transactions; Sign an agreement with clients regarding the rights and obligations arising from the provision of that service; Notify the competent authorities of its Member State and the trading venue; Provide a description of systems and controls upon request. Information gathered by Natixis is subject to data processing in order to comply with regulation for investment service providers as outlined in MiFID II. These data may be communicated to control and audit departments, supervisory authorities and Compliance. This information may be kept for a maximum of five years after the end of the contractual relationship. In accordance with the Data Protection Act of January , amended in 2004, you are entitled to access and correct information that concerns you by contacting the Claims Service6. department. You can also, for legitimate reasons, oppose the processing of your data. 6 Natixis Service de traitement des réclamations - Banque de Grande Clientèle 47 Quai d Austerlitz Paris reclamations-bgc@natixis.com Page 10

11 XII - GLOSSARY DIRECT ELECTRONIC ACCESS Arrangement where a member or participant or client of a trading venue permits a person to use its trading code so the person can electronically transmit orders relating to a financial instrument directly to the trading venue and includes arrangements which involve the use by a person of the infrastructure of the member or participant or client, or any connecting system provided by the member or participant or client, to transmit the orders (direct market access) and arrangements where such an infrastructure is not used by a person (sponsored access); INVESTMENT ADVICE The provision of personal recommendations to a client, either upon the client s request or at the initiative of the investment firm, in respect of one or more transactions relating to financial instruments. Financial instruments Within the meaning of MIF 2, financial instruments include: 1. Transferable securities; 2. Money-market instruments; 3. Units in collective investment undertakings; 4. Options, futures, swaps, forward rate agreements and any other derivative contracts relating to securities, currencies, interest rates or yields, emission allowances or other derivatives instruments, financial indices or financial measures which may be settled physically or in cash; 5. Options, futures, swaps, forwards and any other derivative contracts relating to commodities that must be settled in cash or may be settled in cash at the option of one of the parties other than by reason of default or other termination event; 6. Options, futures, swaps, and any other derivative contract relating to commodities that can be physically settled provided that they are traded on a regulated market, a MTF, or an OTF, except for wholesale energy products traded on an OTF that must be physically settled; 7. Options, futures, swaps, and any other derivative contract relating to commodities that can be physically settled provided that they are traded on a regulated market, a MTF, or an OTF, except for wholesale energy products traded on an OTF that must be physically settled; 8. Derivative instruments for the transfer of credit risk. 9. Financial contracts for differences; 10. Options, futures, swaps, forward rate agreements and any other derivative contracts relating to climatic variables, freight rates or inflation rates or other official economic statistics that must be settled in cash or may be settled in cash at the option of one of the parties other than by reason of default or other termination event, as well as any other derivative contracts relating to assets, rights, obligations, indices and measures not otherwise mentioned in this Section, which have the characteristics of other derivative financial instruments, having regard to whether, inter alia, they are traded on a regulated market, OTF, or an MTF; 11. Emission allowances consisting of any units recognised for compliance with the requirements of Directive 2003/87/EC (Emissions Trading Scheme). REGULATED MARKET Multilateral system, operated by a market operator, which brings together or facilitates the bringing together of multiple experienced third-party buying and selling interests in financial instruments in the system and in accordance with its non-discretionary rules in a way that results in a contract, in respect of the financial instruments admitted to trading under its rules and/or systems, and which is authorised and functions regularly in compliance with title III of the MIF 2 directive; Page 11

12 OPT IN Change in the classification of a client towards a category which provides him with better protection than his initial category (example: from Professional to Non-Professional Client). OPT OUT Change in the classification of a client towards a category which provides him with a lower level of protection than his initial category (example: from Non-Professional to Professional Client). TRADING VENUE Means a Regulated Market (MR), a Multilateral Trading Facility (MTF), or an Organised Trading System (OTF). See the appended market infrastructure diagram. INVESTMENT SERVICES The regulation distinguishes two types of services: investment services and activities and ancillary services. Investment services and activities: Reception and transmission of orders in relation to one or more financial instruments. Execution of orders on behalf of clients. Dealing on own account. Portfolio management. Investment advice. Underwriting of financial instruments and/or placing of financial instruments on a firm commitment basis. Placing of financial instruments without a firm commitment basis. Operation of an MTF. Operation of an OTF. Ancillary services Safekeeping and administration of financial instruments for the account of clients, including custodianship and related services such as cash/collateral management and excluding maintaining securities accounts at the highest level. Granting credits or loans to an investor to allow him to carry out a transaction in one or more financial instrument, where the firm granting the credit or loan is involved in the transaction. Advice to undertakings on capital structure, industrial strategy and related matters and advice and services relating to mergers and the purchase of undertakings. Foreign exchange services where these are connected to the provision of investment services. Investment research and financial analysis or other forms of general recommendation relating to transactions in financial instruments. Services related to underwriting. Investment services and activities as well as ancillary services of the type related to in sections A and B of Annex 1 regarding the underlying market of derivatives included under points (5), (6), (7) and (10) of Section C where these are connected to the provision of investment or ancillary services. DURABLE MEDIUM Any instrument: a) which enables a client to store information addressed personally to that client in a way that affords easy access for future reference for a period of time adequate for the purposes of the information and b) which allows the unchanged reproduction of the information stored; MULTILATERAL TRADING FACILITY ("MTF") A multilateral system, operated by an investment service provider or a market operator, which brings together multiple third-party buying and selling interests in financial instruments in the system and in accordance with its non-discretionary rules in a way that results in a contract in compliance with title II of the MIF 2 directive. ORGANISED TRADING FACILITY ("OTF") A multilateral system operated by an investment service provider which is not a regulated market or an MTF and in which multiple third-party buying and selling interests in bonds, structured finance products, emission allowances or derivatives are able to interact in the system in a way that results in a contract in compliance with title II of the MIF 2 directive. Page 12

13 ALGORITHMIC TRADING Trading system for financial instruments in which where a computer algorithm automatically determines the individual parameters of the orders (such as whether to initiate the order, the timing, price or quantity of the order or how to manage the order after its submission); with minimal or no human intervention. It does not include any system that is only used for the purpose of routing orders to one or more trading venues or for the processing of orders involving no determination of any trading parameters or for the confirmation of orders or the post-trade processing of executed transactions; HIGH-FREQUENCY TRADING Algorithmic trading technique characterised by three criteria: - an infrastructure intended to minimize network and other types of latencies, including at least one of the following facilities for algorithmic order entry: co-location, proximity hosting or high-speed direct electronic access; - determination by the system of order initiation, generation, routing or execution without human intervention for individual trades or orders; and high message intra-day rates which constitute orders, quotes or cancellations. Page 13

14 ANNEX MARKET INFRASTRUCTURE DIAGRAM Page 14

Order Execution Policy

Order Execution Policy Effective 3 January 2018 1 Contents 1. Purpose... 3 2. Scope and Applicability. 3 3. Order Execution. 3 4. Best Execution..... 3 5. Applicability of Best Execution... 3 6. Execution

Order Execution Policy Effective 3 January 2018 1 Contents 1. Purpose... 3 2. Scope and Applicability. 3 3. Order Execution. 3 4. Best Execution..... 3 5. Applicability of Best Execution... 3 6. Execution

Act No. 108/2007 on Securities Transactions

Act No. 108/2007 on Securities Transactions Passage through the Althing. Legislative bill. Entered into force on 1 November 2007. EEA Agreement: Annex IX, Directive 89/298/EEC, 89/592/EEC, 2001/34/EC,

Act No. 108/2007 on Securities Transactions Passage through the Althing. Legislative bill. Entered into force on 1 November 2007. EEA Agreement: Annex IX, Directive 89/298/EEC, 89/592/EEC, 2001/34/EC,

Client Classification Policy

Client Classification Policy Alfa Asset Management (Europe) S.A. 1 P a g e Table of Contents 1. Outlines of MIFID II:... 3 1.1. Aim:... 3 1.2. Scope:... 3 2. Client Classification:... 4 2.1. Eligible counterparties:...

Client Classification Policy Alfa Asset Management (Europe) S.A. 1 P a g e Table of Contents 1. Outlines of MIFID II:... 3 1.1. Aim:... 3 1.2. Scope:... 3 2. Client Classification:... 4 2.1. Eligible counterparties:...

ING Client Classification Policy

ING Client Classification Policy 1 1. Introduction This Client Classification Policy (Policy) applies to all entities of ING Bank N.V. (ING Bank), (including ING Bank N.V. Hungary Branch based in the European

ING Client Classification Policy 1 1. Introduction This Client Classification Policy (Policy) applies to all entities of ING Bank N.V. (ING Bank), (including ING Bank N.V. Hungary Branch based in the European

MiFID 2/MiFIR Articles relevant to article The top 10 things every commodities firm needs to know about MiFID 2

MiFID 2/MiFIR Articles relevant to article The top 10 things every commodities firm needs to know about MiFID 2 9. At a high level, what else would be different under MiFID 2 and MiFIR for commodity firms?

MiFID 2/MiFIR Articles relevant to article The top 10 things every commodities firm needs to know about MiFID 2 9. At a high level, what else would be different under MiFID 2 and MiFIR for commodity firms?

(Text with EEA relevance) (OJ L 173, , p. 349)

(OJ L 173, , p. 349)") 02014L0065 EN 01.07.2016 002.002 1 This text is meant purely as a documentation tool and has no legal effect. The Union's institutions do not assume any liability for its contents. The authentic versions

02014L0065 EN 01.07.2016 002.002 1 This text is meant purely as a documentation tool and has no legal effect. The Union's institutions do not assume any liability for its contents. The authentic versions

CLIENT CATEGORISATION POLICY

CLIENT CATEGORISATION POLICY 1. General According to the Investment Services and Activities and Regulated Markets Law of 2017 L. 87(I)/2017 ( the Law ), OX Capital Markets Ltd ( the Company ) is required

CLIENT CATEGORISATION POLICY 1. General According to the Investment Services and Activities and Regulated Markets Law of 2017 L. 87(I)/2017 ( the Law ), OX Capital Markets Ltd ( the Company ) is required

7Q Financial Services Ltd. Client Categorization Policy

7Q Financial Services Ltd Client Categorization Policy Headquarters Nicosia Kennedy Business Centre Suite 402 12-14 Kennedy Avenue 1087 Nicosia Cyprus T: +357 22763344 F: +357 22763355 www.7qfs.com September

7Q Financial Services Ltd Client Categorization Policy Headquarters Nicosia Kennedy Business Centre Suite 402 12-14 Kennedy Avenue 1087 Nicosia Cyprus T: +357 22763344 F: +357 22763355 www.7qfs.com September

1.2. It is stressed that different rules and different levels of protection apply to Clients depending on their categorisation.

APPENDIX II. CLIENT CATEGORISATION 1. GENERAL 1.1. In compliance to the Provision of Investment Services, the Exercise of Investment Activities, the Operation of Regulated Markets and Other Related Matters

APPENDIX II. CLIENT CATEGORISATION 1. GENERAL 1.1. In compliance to the Provision of Investment Services, the Exercise of Investment Activities, the Operation of Regulated Markets and Other Related Matters

SKANESTAS INVESTMENTS LIMITED BEST EXECUTION AND ORDER HANDLING POLICY

BEST EXECUTION AND ORDER HANDLING POLICY 1. INTRODUCTION This Policy operates with the following notions: SKANESTAS - ; Execution of orders on behalf of clients means acting to conclude agreements to buy

BEST EXECUTION AND ORDER HANDLING POLICY 1. INTRODUCTION This Policy operates with the following notions: SKANESTAS - ; Execution of orders on behalf of clients means acting to conclude agreements to buy

Markets in Financial Instruments Directive MiFID II

Markets in Financial Instruments Directive MiFID II This fact sheet is prepared by Bank of Ireland Global Markets to give you information on MiFID II, its requirements and the likely impact on you and

Markets in Financial Instruments Directive MiFID II This fact sheet is prepared by Bank of Ireland Global Markets to give you information on MiFID II, its requirements and the likely impact on you and

Order Execution Policy - Corporate & Investment Bank Division - EEA

Level 3 Order Execution Policy - Corporate & Investment Bank Division - EEA Deutsche Bank AG (branches & relevant affiliates within the EEA) Corporate & Investment Banks Division ( The Bank ) 1. Introduction

Level 3 Order Execution Policy - Corporate & Investment Bank Division - EEA Deutsche Bank AG (branches & relevant affiliates within the EEA) Corporate & Investment Banks Division ( The Bank ) 1. Introduction

ORDER EXECUTION POLICY

ORDER EXECUTION POLICY JB CAPITAL MARKETS ORDER EXECUTION POLICY Each of the terms that appear henceforth in bold are defined in the Definitions Section at the end of this document. 1. Purpose In accordance

ORDER EXECUTION POLICY JB CAPITAL MARKETS ORDER EXECUTION POLICY Each of the terms that appear henceforth in bold are defined in the Definitions Section at the end of this document. 1. Purpose In accordance

1. Retail Client is a client who is not a professional client or an eligible counterparty.

Introduction Trading Point of Financial Instruments Ltd operating under the trading name XM.com is a Cypriot Investment Firm ("CIF") registered with the Registrar of Companies in Nicosia under number:

Introduction Trading Point of Financial Instruments Ltd operating under the trading name XM.com is a Cypriot Investment Firm ("CIF") registered with the Registrar of Companies in Nicosia under number:

ORDER EXECUTION POLICY FOR PROFESSIONAL CLIENTS Applicable to ENGIE GLOBAL MARKETS head office and branches in the European Economic Area

ORDER EXECUTION POLICY FOR PROFESSIONAL CLIENTS Applicable to ENGIE GLOBAL MARKETS head office and branches in the European Economic Area Version V.2.0 Last update 15 December 2017 Contents I. PURPOSE

ORDER EXECUTION POLICY FOR PROFESSIONAL CLIENTS Applicable to ENGIE GLOBAL MARKETS head office and branches in the European Economic Area Version V.2.0 Last update 15 December 2017 Contents I. PURPOSE

Client Categorization Policy

Client Categorization Policy The Company is obliged under Applicable Regulations to obtain information about its Clients and such information, inter alia, will help the Company categorize Clients in relation

Client Categorization Policy The Company is obliged under Applicable Regulations to obtain information about its Clients and such information, inter alia, will help the Company categorize Clients in relation

MiFID II Information Note (applicable starting on )

") MiFID II Information Note (applicable starting on 03.01.2018) GARANTI BANK SA (the Bank) offers its clients investment services in connection to the financial instruments subject to Directive 2014/65/EU

MiFID II Information Note (applicable starting on 03.01.2018) GARANTI BANK SA (the Bank) offers its clients investment services in connection to the financial instruments subject to Directive 2014/65/EU

CLIENT CATEGORISATION

CLIENT CATEGORISATION CLIENT CATEGORISATION Notesco Financial Services Limited (the Company ), whose registered office is at 2, Iapetou street, 4101, Limassol, Cyprus is authorised and regulated by Cyprus

CLIENT CATEGORISATION CLIENT CATEGORISATION Notesco Financial Services Limited (the Company ), whose registered office is at 2, Iapetou street, 4101, Limassol, Cyprus is authorised and regulated by Cyprus

Client Categorisation Policy

Client Categorisation Policy Tickmill UK Limited April 2018 1. General Under the auspices of MiFID, Tickmill UK Ltd ( Tickmill, the firm, the company, us ) is required to categorise you as a client under

Client Categorisation Policy Tickmill UK Limited April 2018 1. General Under the auspices of MiFID, Tickmill UK Ltd ( Tickmill, the firm, the company, us ) is required to categorise you as a client under

CLIENT CATEGORIZATION POLICY

CLIENT CATEGORIZATION POLICY This is not a marketing material, but an informative policy for the categorisation of clients and their rights in compliance with Markets in Financial Instruments Directive

CLIENT CATEGORIZATION POLICY This is not a marketing material, but an informative policy for the categorisation of clients and their rights in compliance with Markets in Financial Instruments Directive

Summary of the Best Execution Policy

1. Introduction The summary of the Best Execution Policy outlines the key arrangements The Toronto-Dominion Bank (London Branch), TD Securities Limited, TD Bank (Europe) Limited and TD Global Finance Unlimited

1. Introduction The summary of the Best Execution Policy outlines the key arrangements The Toronto-Dominion Bank (London Branch), TD Securities Limited, TD Bank (Europe) Limited and TD Global Finance Unlimited

Best Execution Client Disclosure Statement HSBC UK Bank Plc Global Markets. Dated 1 July 2018 PUBLIC

Best Execution Client Disclosure Statement HSBC UK Bank Plc Global Markets Dated 1 July 2018 PUBLIC Copyright. HSBC UK Bank plc 2018 ALL RIGHTS RESERVED. No part of this publication may be reproduced,

Best Execution Client Disclosure Statement HSBC UK Bank Plc Global Markets Dated 1 July 2018 PUBLIC Copyright. HSBC UK Bank plc 2018 ALL RIGHTS RESERVED. No part of this publication may be reproduced,

CLIENT CATEGORISATION POLICY

CLIENT CATEGORISATION POLICY Version: January,2018 Following the implementation of the Markets in Financial Instruments Directive II (MiFID II) in the European Union and in accordance with the Investment

CLIENT CATEGORISATION POLICY Version: January,2018 Following the implementation of the Markets in Financial Instruments Directive II (MiFID II) in the European Union and in accordance with the Investment

Conduct of Business Rulebook (COBS)

") Conduct of Business Rulebook (COBS) Contents 1. Introduction... 1 2. Client Classification... 1 3. Core Rules Investment Business, Accepting Deposits, Providing Credit and Providing Trust Services... 13

Conduct of Business Rulebook (COBS) Contents 1. Introduction... 1 2. Client Classification... 1 3. Core Rules Investment Business, Accepting Deposits, Providing Credit and Providing Trust Services... 13

Best Execution & Order Handling Policy

Best Execution & Order Handling Policy BGC Brokers LP, Aurel BGC, GFI Brokers Limited, GFI Securities Limited, Sunrise Brokers LLP. Policy Version V 1.1 Effective Date 03/01/2018 Best Execution and Order

Best Execution & Order Handling Policy BGC Brokers LP, Aurel BGC, GFI Brokers Limited, GFI Securities Limited, Sunrise Brokers LLP. Policy Version V 1.1 Effective Date 03/01/2018 Best Execution and Order

Best Execution & Order Handling Policy

Best Execution & Order Handling Policy BGC Brokers LP, GFI Brokers Limited, GFI Securities Limited, Sunrise Brokers LLP. Policy Version V 1.3 Effective Date 20/02/2018 Best Execution and Order Handling

Best Execution & Order Handling Policy BGC Brokers LP, GFI Brokers Limited, GFI Securities Limited, Sunrise Brokers LLP. Policy Version V 1.3 Effective Date 20/02/2018 Best Execution and Order Handling

Mega Equity Securities & Financial Services Public Ltd

MiFID II Information Document on INVESTMENT and ANCILLARY SERVICES in FINANCIAL INSTRUMENTS- BEST EXECUTION POLICY Mega Equity Securities & Financial Services Public Ltd effective 3rd January 2018 1.1

MiFID II Information Document on INVESTMENT and ANCILLARY SERVICES in FINANCIAL INSTRUMENTS- BEST EXECUTION POLICY Mega Equity Securities & Financial Services Public Ltd effective 3rd January 2018 1.1

Best Execution Policy

Best Execution Policy 1. General information about this policy TOBAM manages portfolios of investments on a discretionary basis for investment funds and external segregated client s portfolio (together,

Best Execution Policy 1. General information about this policy TOBAM manages portfolios of investments on a discretionary basis for investment funds and external segregated client s portfolio (together,

Statement on Best Execution Principles of Credit Suisse Asset Management (Switzerland) Ltd.

Ltd.") Statement on Best Execution Principles of Credit Suisse Asset Management (Switzerland) Ltd. Version 1.0 Last updated: 03.01.2018 All rights reserved Credit Suisse Asset Management (Switzerland) Ltd. Table

Statement on Best Execution Principles of Credit Suisse Asset Management (Switzerland) Ltd. Version 1.0 Last updated: 03.01.2018 All rights reserved Credit Suisse Asset Management (Switzerland) Ltd. Table

NAGA Markets Ltd. Client Categorization Policy

NAGA Markets Ltd Client Categorization Policy August 2018 Table of Contents 1. General... 1 2. Professional Clients by Default... 1 3. Non-Professional Clients who may be Treated as Professional on Request...

NAGA Markets Ltd Client Categorization Policy August 2018 Table of Contents 1. General... 1 2. Professional Clients by Default... 1 3. Non-Professional Clients who may be Treated as Professional on Request...

CYPRUS INVESTMENT FIRMS (CIF)

") CYPRUS INVESTMENT FIRMS (CIF) Following the Markets in Financial Instruments Directive (MiFID) of the EU which became effective on 1 November 2007, Cyprus has introduced legislation, Law 144(I)/2007 (

CYPRUS INVESTMENT FIRMS (CIF) Following the Markets in Financial Instruments Directive (MiFID) of the EU which became effective on 1 November 2007, Cyprus has introduced legislation, Law 144(I)/2007 (

Order Execution Policy financial instruments

Order Execution Policy financial instruments Applicable from 3 January 2018 DB0172UK 2017.09 This policy sets out the principles that we follow when executing orders for our retail and professional clients

Order Execution Policy financial instruments Applicable from 3 January 2018 DB0172UK 2017.09 This policy sets out the principles that we follow when executing orders for our retail and professional clients

The Company will automatically categorise all Clients as a Retail Clients as notified to the Client within the Company s Client Agreement.

1 Contents 1. Introduction... 3 2. Categorisation Criteria... 3 2.1 Retail Client... 3 2.2 Professional Client... 3 2.3 Eligible Counterparty... 6 3. Request for Different Categorisation... 7 4. Protection

1 Contents 1. Introduction... 3 2. Categorisation Criteria... 3 2.1 Retail Client... 3 2.2 Professional Client... 3 2.3 Eligible Counterparty... 6 3. Request for Different Categorisation... 7 4. Protection

Best execution policy

Best execution policy 1. Introduction The law of 13 July 2007 that transposes into Luxembourg law the European Markets in Financial Instruments Directive and which is enacted on 1 November (hereafter MiFID)

Best execution policy 1. Introduction The law of 13 July 2007 that transposes into Luxembourg law the European Markets in Financial Instruments Directive and which is enacted on 1 November (hereafter MiFID)

C. EXECUTION POLICY TERMS OF BUSINESS

C. EXECUTION POLICY This policy sets out the principles that the Bank follows when executing orders of retail and professional Clients in financial instruments to ensure that the Bank s Clients obtain

C. EXECUTION POLICY This policy sets out the principles that the Bank follows when executing orders of retail and professional Clients in financial instruments to ensure that the Bank s Clients obtain

Canaccord Genuity Limited Order Execution Policy

Canaccord Genuity Limited Order Execution Policy April 2015 Introduction Under the EU Markets in Financial Instruments Directive 2004/39/EC (MiFID) and the rules of our regulator, the Financial Conduct

Canaccord Genuity Limited Order Execution Policy April 2015 Introduction Under the EU Markets in Financial Instruments Directive 2004/39/EC (MiFID) and the rules of our regulator, the Financial Conduct

Executive Order on Investor Protection in connection with Securities Trading 1)

") While this translation was carried out by a professional translation agency, the text is to be regarded as an unofficial translation based on the latest official Executive Order no. 964 of 30 September

While this translation was carried out by a professional translation agency, the text is to be regarded as an unofficial translation based on the latest official Executive Order no. 964 of 30 September

MARKETS IN FINANCIAL INSTRUMENTS DIRECTIVE (MIFID) INFORMATION TO PRIVATE CLIENTS

INFORMATION TO PRIVATE CLIENTS") MARKETS IN FINANCIAL INSTRUMENTS DIRECTIVE (MIFID) INFORMATION TO PRIVATE CLIENTS Appendix 1 1. Introduction The purpose of this Appendix is to inform you of certain changes with the introduction of the

MARKETS IN FINANCIAL INSTRUMENTS DIRECTIVE (MIFID) INFORMATION TO PRIVATE CLIENTS Appendix 1 1. Introduction The purpose of this Appendix is to inform you of certain changes with the introduction of the

ING Wholesale Banking Best Execution and Order Handling Policy

ING Wholesale Banking Best Execution and Order Handling Policy 1. When do we apply best execution to client transactions? This ING Wholesale Banking Best Execution and Order Handling Policy (the Policy)

ING Wholesale Banking Best Execution and Order Handling Policy 1. When do we apply best execution to client transactions? This ING Wholesale Banking Best Execution and Order Handling Policy (the Policy)

INVESTMENT SERVICES RULES FOR INVESTMENT SERVICES PROVIDERS

INVESTMENT SERVICES RULES FOR INVESTMENT SERVICES PROVIDERS PART BI: STANDARD LICENCE CONDITIONS APPLICABLE TO INVESTMENT SERVICES LICENCE HOLDERS (EXCLUDING UCITS MANAGEMENT COMPANIES) 1. General Requirements

INVESTMENT SERVICES RULES FOR INVESTMENT SERVICES PROVIDERS PART BI: STANDARD LICENCE CONDITIONS APPLICABLE TO INVESTMENT SERVICES LICENCE HOLDERS (EXCLUDING UCITS MANAGEMENT COMPANIES) 1. General Requirements

THE CROATIAN PARLIAMENT

THE CROATIAN PARLIAMENT 2812 Pursuant to Article 88 of the Constitution of the Republic of Croatia, I hereby pass the DECISION PROMULGATING THE CAPITAL MARKET ACT I hereby promulgate the Capital Market

THE CROATIAN PARLIAMENT 2812 Pursuant to Article 88 of the Constitution of the Republic of Croatia, I hereby pass the DECISION PROMULGATING THE CAPITAL MARKET ACT I hereby promulgate the Capital Market

BEST EXECUTION AND CLIENT ORDER HANDLING POLICY FOR PROFESSIONAL AND RETAIL CLIENTS

BEST EXECUTION AND CLIENT ORDER HANDLING POLICY FOR PROFESSIONAL AND RETAIL CLIENTS APPLICABLE TO SOCIÉTÉ GÉNÉRALE ENTITIES IN THE EUROPEAN ECONOMIC AREA (Head office, Branches, and Subsidiaries) Version

BEST EXECUTION AND CLIENT ORDER HANDLING POLICY FOR PROFESSIONAL AND RETAIL CLIENTS APPLICABLE TO SOCIÉTÉ GÉNÉRALE ENTITIES IN THE EUROPEAN ECONOMIC AREA (Head office, Branches, and Subsidiaries) Version

CLIENT CATEGORISATION POLICY

General According the Provision of Investment Services, the Exercise of Investment Activities, the Operation of Regulated Markets and Other Related Matters Law 144(I)/2007, as subsequently amended from

General According the Provision of Investment Services, the Exercise of Investment Activities, the Operation of Regulated Markets and Other Related Matters Law 144(I)/2007, as subsequently amended from

Best Execution Policy Summary For Receipt, Transmission and Execution of orders Business. Fideuram Asset Management (Ireland) Limited ( Fideuram )

Limited ( Fideuram )") Best Execution Policy Summary For Receipt, Transmission and Execution of orders Business Fideuram Asset Management (Ireland) Limited ( Fideuram ) Professional Clients PART ONE: THE BEST EXECUTION REQUIREMENT

Best Execution Policy Summary For Receipt, Transmission and Execution of orders Business Fideuram Asset Management (Ireland) Limited ( Fideuram ) Professional Clients PART ONE: THE BEST EXECUTION REQUIREMENT

Order Execution Policy. January 2018 v1

Order Execution Policy January 2018 v1 Table of Contents Introduction... 2 Scope... 2 Background... 3 Legislation Reference... 3 Business Model... 3 Client Category... 4 Authorised Personnel... 4 Best

Order Execution Policy January 2018 v1 Table of Contents Introduction... 2 Scope... 2 Background... 3 Legislation Reference... 3 Business Model... 3 Client Category... 4 Authorised Personnel... 4 Best

Best Execution Policy. Crossbridge Capital LLP

Best Execution Policy Crossbridge Capital LLP Contents 1 Introduction... 3 1.1 The Best Execution obligation... 3 1.2 Application of FCA and EU regulations... 3 1.3 Direct and indirect execution... 4 1.4

Best Execution Policy Crossbridge Capital LLP Contents 1 Introduction... 3 1.1 The Best Execution obligation... 3 1.2 Application of FCA and EU regulations... 3 1.3 Direct and indirect execution... 4 1.4

CLIENT CATEGORISATION

CLIENT CATEGORISATION Table of Contents 1 CLIENT CATEGORISATION... 3 1.1 Retail Client... 3 2 PROFESSIONAL CLIENT... 3 3 CLIENTS WHO MAY BE TREATED AS PROFESSIONALS ON REQUEST... 4 3.1 Procedure... 5 3.2

CLIENT CATEGORISATION Table of Contents 1 CLIENT CATEGORISATION... 3 1.1 Retail Client... 3 2 PROFESSIONAL CLIENT... 3 3 CLIENTS WHO MAY BE TREATED AS PROFESSIONALS ON REQUEST... 4 3.1 Procedure... 5 3.2

I. Categories of clients who are considered to be professionals by default

CLIENT CATEGORISATION POLICY November 2018 Introduction XTrade Europe Ltd (ex. XFR Financial Ltd.) (hereinafter the Company ) is a Cyprus Investment Firm ( CIF ) registered (Certificate of Incorporation

CLIENT CATEGORISATION POLICY November 2018 Introduction XTrade Europe Ltd (ex. XFR Financial Ltd.) (hereinafter the Company ) is a Cyprus Investment Firm ( CIF ) registered (Certificate of Incorporation

Client Categorization Policy

Client Categorization Policy Note: The English version of this Agreement is the governing version and shall prevail whenever there is any discrepancy between the English version and the other versions.

Client Categorization Policy Note: The English version of this Agreement is the governing version and shall prevail whenever there is any discrepancy between the English version and the other versions.

Order Execution Policy 3 rd January 2018

Nordea Investment Management Order Execution Policy 3 rd January 2018 Contents 1. Purpose... 2 2. Regulatory context... 2 3. Scope... 2 4. Order process... 3 5. Execution decision process... 5 6. Venue

Nordea Investment Management Order Execution Policy 3 rd January 2018 Contents 1. Purpose... 2 2. Regulatory context... 2 3. Scope... 2 4. Order process... 3 5. Execution decision process... 5 6. Venue

SKANESTAS INVESTMENTS LIMITED PRODUCT GOVERNANCE POLICY

PRODUCT GOVERNANCE POLICY Updated on January 3, 2018 1. Definitions CySEC Directive : Directive DI 87-01 of the Cyprus Securities and Exchange Commission for the Safeguarding of Financial Instruments and

PRODUCT GOVERNANCE POLICY Updated on January 3, 2018 1. Definitions CySEC Directive : Directive DI 87-01 of the Cyprus Securities and Exchange Commission for the Safeguarding of Financial Instruments and

Jefferies International Limited

Jefferies International Limited Order Execution Policy January 2018 Issued November 2013 Version 3.0 Supersedes all previous Compliance Policies regarding this subject matter Jefferies International Limited

Jefferies International Limited Order Execution Policy January 2018 Issued November 2013 Version 3.0 Supersedes all previous Compliance Policies regarding this subject matter Jefferies International Limited

RP Martin EXECUTION POLICY

RP Martin EXECUTION POLICY This Execution Policy is applicable to voice broker services provided to you by RP Martin Stockholm AB ( Broker ). This Execution Policy should be read in conjunction with the

RP Martin EXECUTION POLICY This Execution Policy is applicable to voice broker services provided to you by RP Martin Stockholm AB ( Broker ). This Execution Policy should be read in conjunction with the

ORDER AND BEST EXECUTION POLICY

ORDER AND BEST EXECUTION POLICY SUMMARY: This document represents Hottinger Investment Management Limited ( HIM ) - FRN 208737 - Order & Best Execution Policy OWNER: HIM s Board of Directors and Compliance

ORDER AND BEST EXECUTION POLICY SUMMARY: This document represents Hottinger Investment Management Limited ( HIM ) - FRN 208737 - Order & Best Execution Policy OWNER: HIM s Board of Directors and Compliance

THE COMMITTEE OF EUROPEAN SECURITIES REGULATORS

THE COMMITTEE OF EUROPEAN SECURITIES REGULATORS Date : 29 June Ref : CESR/04-323 Formal Request for Technical Advice on Possible Implementing Measures on the Directive on Markets in Financial Instruments

THE COMMITTEE OF EUROPEAN SECURITIES REGULATORS Date : 29 June Ref : CESR/04-323 Formal Request for Technical Advice on Possible Implementing Measures on the Directive on Markets in Financial Instruments

Contents FXORO MCA Intelifunds Ltd,

Contents Client Classification... 2 Retail clients... 2 Professional Clients... 2 Eligible counterparties (ECP)... 3 Opt-down... 4 Opt-up... 4 Changes to professional client / eligible counterparty categorisation...

Contents Client Classification... 2 Retail clients... 2 Professional Clients... 2 Eligible counterparties (ECP)... 3 Opt-down... 4 Opt-up... 4 Changes to professional client / eligible counterparty categorisation...

Lombard Odier Group Markets in financial instruments directive (MiFID) Conflict of interest policy and Order Execution Policy

Conflict of interest policy and Order Execution Policy") Lombard Odier Group Markets in financial instruments directive (MiFID) Conflict of interest policy and Order Execution Policy Markets in financial instruments directive (MiFID) conflict of interest policy

Lombard Odier Group Markets in financial instruments directive (MiFID) Conflict of interest policy and Order Execution Policy Markets in financial instruments directive (MiFID) conflict of interest policy

SCOPE OF SECTION C(10) CONTRACTS WHICH ARE "COMMODITY DERIVATIVES" FOR THE PURPOSES OF MIFID II

CONTRACTS WHICH ARE COMMODITY DERIVATIVES FOR THE PURPOSES OF MIFID II") 22 February 2017 SCOPE OF SECTION C(10) CONTRACTS WHICH ARE "COMMODITY DERIVATIVES" FOR THE PURPOSES OF MIFID II We write further to our letter of 22 September 2016 1 and the meeting between ESMA and our

22 February 2017 SCOPE OF SECTION C(10) CONTRACTS WHICH ARE "COMMODITY DERIVATIVES" FOR THE PURPOSES OF MIFID II We write further to our letter of 22 September 2016 1 and the meeting between ESMA and our

Transposition of Directive 2004/39/EC on Markets in Financial Instruments

Transposition of Directive 2004/39/EC on Markets in Financial Instruments Draft amendments to Book III of the AMF General on Investment Services Providers Consultation document INTRODUCTION This document

Transposition of Directive 2004/39/EC on Markets in Financial Instruments Draft amendments to Book III of the AMF General on Investment Services Providers Consultation document INTRODUCTION This document

PVM Execution and Order Handling Policy

PVM Execution and Order Handling Policy November 2017 This Execution and Order Handling Policy (the Policy ) is applicable to execution services provided to you by any of the following entities and any

PVM Execution and Order Handling Policy November 2017 This Execution and Order Handling Policy (the Policy ) is applicable to execution services provided to you by any of the following entities and any

Order Handling and Best Execution Policy

Order Handling and Best Execution Policy Effective 3 January 2018 TABLE OF CONTENTS 1 INTRODUCTION... 4 2 PURPOSE OF THIS POLICY... 4 3 ABBREVIATIONS... 5 4 DEFINITIONS... 6 5 POLICY APPLICATION... 8 6

Order Handling and Best Execution Policy Effective 3 January 2018 TABLE OF CONTENTS 1 INTRODUCTION... 4 2 PURPOSE OF THIS POLICY... 4 3 ABBREVIATIONS... 5 4 DEFINITIONS... 6 5 POLICY APPLICATION... 8 6

Important Information about. Bank of Ireland Private Banking

Important Information about Bank of Ireland Private Banking January 2018 1 1 Contents 01 Client Agreement 4 02 Definitions 5 03 About Us 8 04 Client Classification 11 05 Our Services 14 06 Investment Products

Important Information about Bank of Ireland Private Banking January 2018 1 1 Contents 01 Client Agreement 4 02 Definitions 5 03 About Us 8 04 Client Classification 11 05 Our Services 14 06 Investment Products

Notification of Intention To Provide Cross-Border Services The Financial Services (Banking) Act

Act") 2BCD2 Notification of Intention To Provide Cross-Border Services The Financial Services (Banking) Act All Gibraltar incorporated licensed institutions and Gibraltar subsidiary institutions that wish to

2BCD2 Notification of Intention To Provide Cross-Border Services The Financial Services (Banking) Act All Gibraltar incorporated licensed institutions and Gibraltar subsidiary institutions that wish to

Christos Gortsos Associate Professor of International Economic Law, Panteion University of Athens

ERA Conference The MIFID II Legislative Proposal Crucial changes in the reform of MiFID: : distinction between MiFID obligations and MiFIR requirements Christos Gortsos Associate Professor of International

ERA Conference The MIFID II Legislative Proposal Crucial changes in the reform of MiFID: : distinction between MiFID obligations and MiFIR requirements Christos Gortsos Associate Professor of International

Order Execution Policy

(ATFX) Order Execution Policy ORDER EXECUTION POLICY Introduction In accordance with the rules of the Financial Conduct Authority (the FCA ) and the requirements of the Markets in Financial Instruments

(ATFX) Order Execution Policy ORDER EXECUTION POLICY Introduction In accordance with the rules of the Financial Conduct Authority (the FCA ) and the requirements of the Markets in Financial Instruments

Powernext Commodities Market Rules Consolidated texts on 19/12//2017. Powernext Commodities Market Rules. Consolidated texts

Powernext Commodities Market Rules Consolidated texts on 19/12//2017 Powernext Commodities Market Rules Consolidated texts December 19. 2017 CONTENTS TITLE 1 - POWERNEXT COMMODITIES GENERAL REQUIREMENTS...

Powernext Commodities Market Rules Consolidated texts on 19/12//2017 Powernext Commodities Market Rules Consolidated texts December 19. 2017 CONTENTS TITLE 1 - POWERNEXT COMMODITIES GENERAL REQUIREMENTS...

BofAML EMEA Order Execution Policy Summary

1. Order Execution Policy This document provides a summary of Bank of America Merrill Lynch s ( BofAML ) Order Execution Policy ( Policy ), which BofAML will adopt when executing orders on behalf of clients.

1. Order Execution Policy This document provides a summary of Bank of America Merrill Lynch s ( BofAML ) Order Execution Policy ( Policy ), which BofAML will adopt when executing orders on behalf of clients.

OCTOBER 2017 MIFID II GUIDE FOR FINANCIAL INVESTMENT ADVISORS

OCTOBER 2017 MIFID II GUIDE FOR FINANCIAL INVESTMENT ADVISORS amf-france.org PREAMBLE Financial investment advisors (FIAs), which are governed by the regime introduced in the Financial Security Act of

OCTOBER 2017 MIFID II GUIDE FOR FINANCIAL INVESTMENT ADVISORS amf-france.org PREAMBLE Financial investment advisors (FIAs), which are governed by the regime introduced in the Financial Security Act of

MIFID II LEAFLET CORPORATE INVESTMENT BANKING (SGCIB)

") Since its implementation in November 2007, the Markets in Financial Instruments Directive ( MiFID I ) has been the cornerstone of capital markets regulation in Europe. MiFID I was recast by the Markets

Since its implementation in November 2007, the Markets in Financial Instruments Directive ( MiFID I ) has been the cornerstone of capital markets regulation in Europe. MiFID I was recast by the Markets

Jefferies International Limited

Jefferies International Limited Order Execution Policy August 2015 Issued November 2013 Version 2.0 Supersedes all previous Compliance Policies regarding this subject matter Jefferies International Limited

Jefferies International Limited Order Execution Policy August 2015 Issued November 2013 Version 2.0 Supersedes all previous Compliance Policies regarding this subject matter Jefferies International Limited

Questions and Answers On MiFID II and MiFIR market structures topics

Questions and Answers On MiFID II and MiFIR market structures topics 31 May 2017 ESMA70-872942901-38 Date: 31 May 2017 ESMA70-872942901-38 ESMA CS 60747 103 rue de Grenelle 75345 Paris Cedex 07 France

Questions and Answers On MiFID II and MiFIR market structures topics 31 May 2017 ESMA70-872942901-38 Date: 31 May 2017 ESMA70-872942901-38 ESMA CS 60747 103 rue de Grenelle 75345 Paris Cedex 07 France

MIFID II LEAFLET CORPORATE INVESTMENT BANKING (SGCIB)

") Since its implementation in November 2007, the Markets in Financial Instruments Directive ( MiFID I ) has been the cornerstone of capital markets regulation in Europe. MiFID I was recast by the Markets

Since its implementation in November 2007, the Markets in Financial Instruments Directive ( MiFID I ) has been the cornerstone of capital markets regulation in Europe. MiFID I was recast by the Markets

CITI SECURITIES SERVICES EXECUTION POLICY

CITI SECURITIES SERVICES EXECUTION POLICY ISSUE DATE: JANUARY 2018 VERSION: 1.0 2017 Citigroup Inc. TABLE OF CONTENTS 1 POLICY 3 ANNEX A: PRODUCT SPECIFIC POLICIES 10 2017 Citigroup Inc. POLICY 1 PURPOSE

CITI SECURITIES SERVICES EXECUTION POLICY ISSUE DATE: JANUARY 2018 VERSION: 1.0 2017 Citigroup Inc. TABLE OF CONTENTS 1 POLICY 3 ANNEX A: PRODUCT SPECIFIC POLICIES 10 2017 Citigroup Inc. POLICY 1 PURPOSE

INFINOX Capital Ltd Best Execution Policy

INFINOX Capital Ltd Best Execution Policy July Page 12018 INFINOX Capital Ltd 20 Birchin Lane London EC3V 9DU www.infinox.com 1. Introduction 1.1 This Best Execution Policy (the Policy ) summarises the

INFINOX Capital Ltd Best Execution Policy July Page 12018 INFINOX Capital Ltd 20 Birchin Lane London EC3V 9DU www.infinox.com 1. Introduction 1.1 This Best Execution Policy (the Policy ) summarises the

MiFID 2/MiFIR Articles relevant to article The top 10 things every investment banker should know about MiFID 2. EU Council MiFID 2 general approach

MiFID 2/MiFIR Articles relevant to article The top 10 things every investment banker should know about MiFID 2 3. What is an organised trading facility? EU Commission MiFID 2 legislative proposal Article

MiFID 2/MiFIR Articles relevant to article The top 10 things every investment banker should know about MiFID 2 3. What is an organised trading facility? EU Commission MiFID 2 legislative proposal Article

ORDER EXECUTION POLICY

ORDER EXECUTION POLICY Last Reviewed on 23 February 2016 Last Updated on 23 February 2016 Terms that appear in Capital Case typeset are defined at the end of this document. 1. INTRODUCTION / LEGAL BACKGROUND

ORDER EXECUTION POLICY Last Reviewed on 23 February 2016 Last Updated on 23 February 2016 Terms that appear in Capital Case typeset are defined at the end of this document. 1. INTRODUCTION / LEGAL BACKGROUND

CITIBANK EUROPE PLC CUSTOMER INFORMATION FOR THE PURPOSE OF PROVIDING THE INVESTMENT SERVICES

CITIBANK EUROPE PLC CUSTOMER INFORMATION FOR THE PURPOSE OF PROVIDING THE INVESTMENT SERVICES Valid and effective from 3 January 2018 Citibank Europe plc, organizační složka PRAGUE CZECH REPUBLIC Citibank

CITIBANK EUROPE PLC CUSTOMER INFORMATION FOR THE PURPOSE OF PROVIDING THE INVESTMENT SERVICES Valid and effective from 3 January 2018 Citibank Europe plc, organizační složka PRAGUE CZECH REPUBLIC Citibank

Order Execution Policy for clients of the SEB

Order Execution Policy for clients of the SEB Effective from 03.01.2018 Table of Contents 1. Introduction 3 2. Scope 4 2.1 Clients covered 4 2.2 Geographies covered 4 2.3 Financial Instruments covered

Order Execution Policy for clients of the SEB Effective from 03.01.2018 Table of Contents 1. Introduction 3 2. Scope 4 2.1 Clients covered 4 2.2 Geographies covered 4 2.3 Financial Instruments covered

Appendix 1. In this appendix underlining indicates new text and striking through indicates deleted text.

Appendix 1 In this appendix underlining indicates new text and striking through indicates deleted text. As a significant number of enhancements are being made to chapter 2 of the current COB Rules, this

Appendix 1 In this appendix underlining indicates new text and striking through indicates deleted text. As a significant number of enhancements are being made to chapter 2 of the current COB Rules, this

Citco Bank Nederland N.V. Order Execution Policy

Citco Bank Nederland N.V. Order Execution Policy January 2018 Table of Contents 1. Introduction... 3 1.1 Purpose... 3 1.2 Scope... 3 1.3 Client Consent... 4 1.4 Treatment and Violation of this policy...

Citco Bank Nederland N.V. Order Execution Policy January 2018 Table of Contents 1. Introduction... 3 1.1 Purpose... 3 1.2 Scope... 3 1.3 Client Consent... 4 1.4 Treatment and Violation of this policy...

MIFID. Client Pre-Contractual Info Pack

MIFID Client Pre-Contractual Info Pack CONTENTS 1 OBJECTIVES AND SCOPE OF NEW LEGISLATION... 2 2 EUROBANK EQUITIES AND ITS SERVICES... 3 2.1 EUROBANK EQUITIES... 3 2.2 INVESTMENT SERVICES OFFERED... 3

MIFID Client Pre-Contractual Info Pack CONTENTS 1 OBJECTIVES AND SCOPE OF NEW LEGISLATION... 2 2 EUROBANK EQUITIES AND ITS SERVICES... 3 2.1 EUROBANK EQUITIES... 3 2.2 INVESTMENT SERVICES OFFERED... 3

(Text with EEA relevance) (OJ L 173, , p. 84)

(OJ L 173, , p. 84)") 02014R0600 EN 01.07.2016 001.002 1 This text is meant purely as a documentation tool and has no legal effect. The Union's institutions do not assume any liability for its contents. The authentic versions

02014R0600 EN 01.07.2016 001.002 1 This text is meant purely as a documentation tool and has no legal effect. The Union's institutions do not assume any liability for its contents. The authentic versions

Canada Life Investments

Canada Life Investments Order Execution Policy Owner Delegated Owner/s Last Approved 23 February 2018 Next Review Due Q1 2019 Version Number V1 2018 David Marchant, Managing Director & Chief Investment

Canada Life Investments Order Execution Policy Owner Delegated Owner/s Last Approved 23 February 2018 Next Review Due Q1 2019 Version Number V1 2018 David Marchant, Managing Director & Chief Investment

Powernext Commodities Market Rules Consolidated texts on 28/05/2017. Powernext Commodities Market Rules. Consolidated texts

Powernext Commodities Market Rules Consolidated texts on 28/05/2017 Powernext Commodities Market Rules Consolidated texts May 28. 2018 CONTENTS TITLE 1 - POWERNEXT COMMODITIES GENERAL REQUIREMENTS... 4

Powernext Commodities Market Rules Consolidated texts on 28/05/2017 Powernext Commodities Market Rules Consolidated texts May 28. 2018 CONTENTS TITLE 1 - POWERNEXT COMMODITIES GENERAL REQUIREMENTS... 4

- Regulation 600/2014 of 15 May 2014 on markets in financial instruments and amending Regulation 648/2012 (EMIR) EUOJ L 173/84 12/6/2014

EUOJ L 173/84 12/6/2014") MIFID II /MIFIR Reference documents: - Directive 2014/65/EU of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC (insurance mediation) and directive 2011/61/EU (AIFMD) EUOJ

MIFID II /MIFIR Reference documents: - Directive 2014/65/EU of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC (insurance mediation) and directive 2011/61/EU (AIFMD) EUOJ

PRODUCT GOVERNANCE POLICY V X Spot Markets (EU) Ltd.

Ltd.") PRODUCT GOVERNANCE POLICY V1.0 2018 X Spot Markets (EU) Ltd. Table of Contents A. Introduction & Purpose... 3 B. Legal Framework... 3 C. Definitions... 3 D. Requirements and procedures for manufacturers...

PRODUCT GOVERNANCE POLICY V1.0 2018 X Spot Markets (EU) Ltd. Table of Contents A. Introduction & Purpose... 3 B. Legal Framework... 3 C. Definitions... 3 D. Requirements and procedures for manufacturers...

MiFID II Academy: proprietary trading and trading venues. Floortje Nagelkerke 7 December 2017

MiFID II Academy: proprietary trading and trading venues Floortje Nagelkerke 7 December 2017 The countdown to MiFID II / MiFIR implementation as of 8:30am this morning 27 DAYS 15 Hours 30 Minutes But if

MiFID II Academy: proprietary trading and trading venues Floortje Nagelkerke 7 December 2017 The countdown to MiFID II / MiFIR implementation as of 8:30am this morning 27 DAYS 15 Hours 30 Minutes But if

General information on MiFID II. December 2017 edition

December 2017 edition Introduction Since November 2007, investment business in Europe has been governed by the Markets in Financial Instruments Directive (MiFID). The European Union (EU) amended this Directive

December 2017 edition Introduction Since November 2007, investment business in Europe has been governed by the Markets in Financial Instruments Directive (MiFID). The European Union (EU) amended this Directive

INVESTMENT SERVICES RULES FOR INVESTMENT SERVICES PROVIDERS

INVESTMENT SERVICES RULES FOR INVESTMENT SERVICES PROVIDERS PART A: THE APPLICATION PROCESS Title 1 Investment Services Act, 1994 Section 1 Scope 1.1 Regulation of Investment Services The Investment Services

INVESTMENT SERVICES RULES FOR INVESTMENT SERVICES PROVIDERS PART A: THE APPLICATION PROCESS Title 1 Investment Services Act, 1994 Section 1 Scope 1.1 Regulation of Investment Services The Investment Services

Nordea Execution Policy

Nordea Execution Policy January 2017 The President of Nordea Bank AB (publ) and Chief Executive Officer (CEO) in Group Executive Management has approved this execution policy ( Execution Policy ), which

Nordea Execution Policy January 2017 The President of Nordea Bank AB (publ) and Chief Executive Officer (CEO) in Group Executive Management has approved this execution policy ( Execution Policy ), which

COMMISSION DELEGATED REGULATION (EU) /... of

/... of") EUROPEAN COMMISSION Brussels, 25.4.2016 C(2016) 2398 final COMMISSION DELEGATED REGULATION (EU) /... of 25.4.2016 supplementing Directive 2014/65/EU of the European Parliament and of the Council as regards

EUROPEAN COMMISSION Brussels, 25.4.2016 C(2016) 2398 final COMMISSION DELEGATED REGULATION (EU) /... of 25.4.2016 supplementing Directive 2014/65/EU of the European Parliament and of the Council as regards

LEVERAGE AND MARGIN POLICY Maxiflex Ltd

LEVERAGE AND MARGIN POLICY Maxiflex Ltd Proprietary Restriction: This controlled document is property of Maxiflex Ltd, any disclosure, reproduction or transmission to unauthorized parties without the prior

LEVERAGE AND MARGIN POLICY Maxiflex Ltd Proprietary Restriction: This controlled document is property of Maxiflex Ltd, any disclosure, reproduction or transmission to unauthorized parties without the prior

Sberbank CIB (UK) Limited