When will this happen? Implementation Date. Applications taken on or after. August 1 st, 2015

|

|

|

- Dylan McBride

- 5 years ago

- Views:

Transcription

1 Let the Fun BEGIN!!

2 When will this happen? Implementation Date Applications taken on or after August 1 st, 2015

3 Closing Disclosure Elizabeth A. Daniel, Continental Title Company David A. Townsend, Esq, NTP Agents National Title Insurance

4 New Form O Closing Disclosure O Replaces current HUD-1 and final TIL O Five pages long

5 What types of transactions are exempt? O Home Equity lines of credit O Reverse Mortgages O Mortgages secured by a mobile home that is not attached to real property O Loans made by a creditor who makes five or fewer mortgages in a year. O Cash Transactions O Commercial Transactions

6

7 Closing Information

8 Loan Terms

9 Page 1 Section: Projected Payments

10 : O Estimated Escrow Includes Taxes and Insurance of $ O Estimated Taxes, Insurance AND Assessments includes Homeowner s Association Dues.

11 Costs at Closing O Provides a quick snap shot of the next two pages of the Closing Disclosure for the borrower ONLY.

12

13 Notable Changes O No longer called a HUD or Settlement Statement O Removal of our 700, 800, 900, etc. sections O O O O Each alphabetical section will have all of the fees alphabetically in order. Fees are now itemized No more rolling up Separate columns for Paid Before Closing fees. No more POCL, POCB, POCS At the TOP of each section the Borrowers total is BOLDED and includes the Before Closing fees in amount.

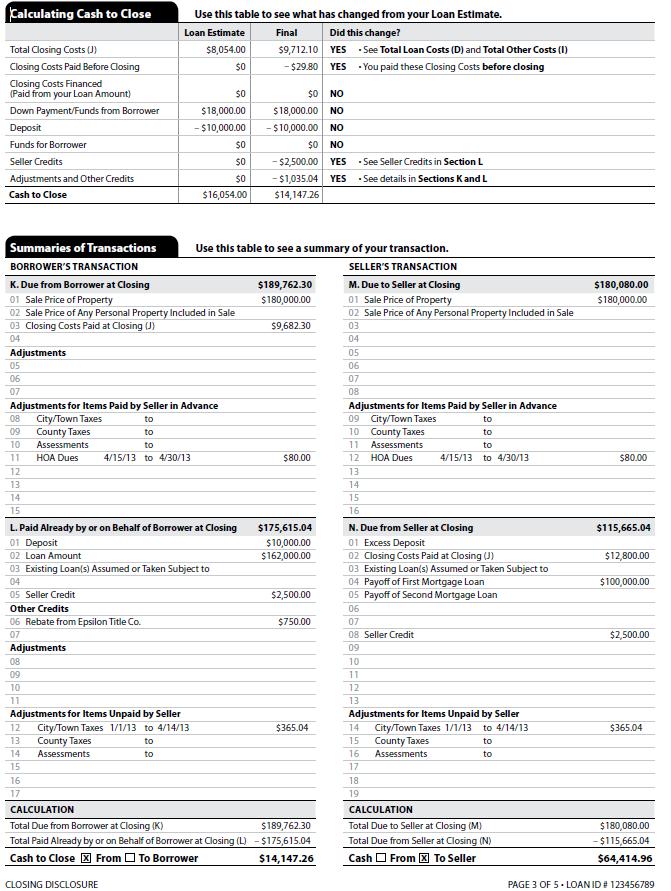

14 Loan Costs CFPB removed the verbiage from Tolerances to Variance A. Origination Charges 0% Variance B. Services Borrower Did Not Shop For 10% Variance C. Services Borrower Did Shop For Costs can change D. Total Loan Costs

15 Other Costs (E-H) E. Recording Fees F. Prepaids O O O O Homeowners Insurance Mortgage Insurance Prepaid Interest Property Taxes G. Initial Escrows H. Other O O O O O HOA/Condo fees Home Inspection Home Warranty Real Estate Commission Title-Owners Title Insurance (Optional)

16 Taxes and Other Government Fees O Per the CFPB Creditors should disclose the name of the entity assessing the transfer tax, even if that is different from the payee of the check cut by the settlement agent. The governing authority assessing the transfer tax must be disclosed, along with the amount paid by consumer, the borrower, seller and others.

17 Owners Title Insurance Optional O The Optional label still applies for buyerpaid insurance O If the seller pays, option phrase is eliminated

18 Other Costs (J) O All of the Borrowers BOLDED amounts are totaled in Section J O Seller Columns are totaled O Paid by Others are totaled

19 Lender Credits

20

21 Calculating Cash to Close O Comparison of the Loan Estimate and Final Closing Disclosure

22 Summaries of Transactions

23

24

25

26

27

28

29

30

31

32 Confirming Receipt O Title software will be adding a FINAL Receipt/Signature line O Currently there is not a final signature line on the Closing Disclosure

33 Who provides the Closing Disclosure 3 days before closing? O According to the final ruling the LENDER/CREDITOR is responsible for delivering the Closing Disclosure form to the consumer O BUT the lender/creditor may USE settlements agents to deliver the Closing Disclosure as well. O Chase, Citi Bank, Wells Fargo and Bank of America have announced they will complete and send the CDF to the consumer.

34 When does the 3 day start? O Timing requirements on different delivery methods O O O O In person: received on the day provided Mail (USPS): received 3 business days after placed in mail unless evidence that consumer received it sooner received 3 business days after sent unless evidence that consumer received it sooner (Read receipt is not enough) UPS or FedEx received 3 days business days after sent unless signed and return receipt signature is received sooner

35 What would trigger a NEW 3 day waiting period before you can close? O If the APR changes above 1/8 of a percent on most loans O Changes in the loan product O The creditor adds a prepayment penalty to the loan

36 How do we show our premium

37 From Page # 1795 of the Final Rule and Interpretation O Section (f)(2) and (3) requires disclosure of the amount the consumer will pay for the lender s title insurance policy.

38 From Page # 1795 of the Final Rule and Interpretation O The amount disclosed for the lender s title insurance policy pursuant to (f)(2) or (3) is the amount of premium without any adjustment that might be made for the simultaneous purchase of the owners policy.

39 From Page # 1802 of the Final Rule and Interpretation O The title insurance premium for a lender s title insurance policy on the full premium rate

40 From Page # 1802 of the Final Rule and Interpretation O The owner s title insurance premium is calculated by taking the full owner s title insurance premium, adding the simultaneous issuance premium for the lender s coverage, and then deducting the full premium for lender s coverage.

41 Owners Title Insurance O Any simultaneous issue discount must be applied to the owner s policy premium (and not the loan policy premium).

42

43 `

Closing Disclosure August 1, CFR

Closing Disclosure August 1, 2015 12 CFR 1026.38 Agent Questions for Lender Clients Who will prepare the Closing Disclosure (CD) Form? How will Agents coordinate with the lender to prepare the Closing

Closing Disclosure August 1, 2015 12 CFR 1026.38 Agent Questions for Lender Clients Who will prepare the Closing Disclosure (CD) Form? How will Agents coordinate with the lender to prepare the Closing

The New Loan Estimate & a. Closing Disclosure Explained. Know before you close.

Know before you close. The New Loan Estimate & a Closing Disclosure Explained A look at the different sections of each new form and explanations of each page. http://cfpb.fntic.com/ Barry S. Wolfinsohn

Know before you close. The New Loan Estimate & a Closing Disclosure Explained A look at the different sections of each new form and explanations of each page. http://cfpb.fntic.com/ Barry S. Wolfinsohn

TILA / RESPA Integration

The Times, They Are A-Changing (Again)! presented by Jack Konyk Executive Director, Government Affairs OwnOK The Future of Oklahoma Real Estate Feb. 12, 2015 Petroleum Club Oklahoma City, OK 2 Upcoming

The Times, They Are A-Changing (Again)! presented by Jack Konyk Executive Director, Government Affairs OwnOK The Future of Oklahoma Real Estate Feb. 12, 2015 Petroleum Club Oklahoma City, OK 2 Upcoming

TILA-RESPA Integrated Disclosure Rule FAQs for Wholesale Brokers

TILA-RESPA Integrated Disclosure Rule FAQs for Wholesale Brokers DEFINITIONS AND ACRONYMS TRID: TILA-RESPA Integrated Disclosure Know Before You Owe Rule, text of the rule and more information available

TILA-RESPA Integrated Disclosure Rule FAQs for Wholesale Brokers DEFINITIONS AND ACRONYMS TRID: TILA-RESPA Integrated Disclosure Know Before You Owe Rule, text of the rule and more information available

Tips for Implementing the TILA-RESPA Integrated Disclosure rule

Tips for Implementing the TILA-RESPA Integrated Disclosure rule To support your preparation efforts when implementing the TILA-RESPA Integrated Disclosure (TRID) rule effective for applications dated on

Tips for Implementing the TILA-RESPA Integrated Disclosure rule To support your preparation efforts when implementing the TILA-RESPA Integrated Disclosure (TRID) rule effective for applications dated on

What Real Estate Agents/Brokers Need to Know: Know Before You Owe or the TILA RESPA Integrated Disclosure (TRID) Rule.

Rule.") What Real Estate Agents/Brokers Need to Know: Know Before You Owe or the TILA RESPA Integrated Disclosure (TRID) Rule Presented by Overview Know Before You Owe (the TILA RESPA Integrated Disclosure (TRID)

What Real Estate Agents/Brokers Need to Know: Know Before You Owe or the TILA RESPA Integrated Disclosure (TRID) Rule Presented by Overview Know Before You Owe (the TILA RESPA Integrated Disclosure (TRID)

TRID TILA RESPA Integrated Disclosures. Presented by David Luna

TRID TILA RESPA Integrated Disclosures Presented by David Luna Thank you I d like to thank the many sources of information: the Attorney s, Creditors, Title, Credit providers and the CFPB for the information

TRID TILA RESPA Integrated Disclosures Presented by David Luna Thank you I d like to thank the many sources of information: the Attorney s, Creditors, Title, Credit providers and the CFPB for the information

TILA RESPA Integrated Disclosures

TILA RESPA Integrated Disclosures Jimmy Vuong Branch Relations Manager jvuong@afncorp.com Rev. 03/22/2017 American Financial Network, Inc. All Rights Reserved. The Beta is Open Please see Encompass Newsflash

TILA RESPA Integrated Disclosures Jimmy Vuong Branch Relations Manager jvuong@afncorp.com Rev. 03/22/2017 American Financial Network, Inc. All Rights Reserved. The Beta is Open Please see Encompass Newsflash

TILA / RESPA Integrated Disclosures. The Game-changing Impacts and Action Items

TILA / RESPA Integrated Disclosures The Game-changing Impacts and Action Items CUNA Mutual Group Proprietary Reproduction, Adaptation or Distribution Prohibited CUNA Mutual Group 2013 Presenters Jon Bundy

TILA / RESPA Integrated Disclosures The Game-changing Impacts and Action Items CUNA Mutual Group Proprietary Reproduction, Adaptation or Distribution Prohibited CUNA Mutual Group 2013 Presenters Jon Bundy

Compensation paid directly by the consumer and/or the creditor to a loan originator other than an employee of the creditor

This guide to the Closing Disclosure form is not a comprehensive how to guide. Instead, it is intended to highlight certain areas of the form that require some detailed and difficult input. This guide

This guide to the Closing Disclosure form is not a comprehensive how to guide. Instead, it is intended to highlight certain areas of the form that require some detailed and difficult input. This guide

HERE S. TRID. ROBERT E. PINDER (904) ACC Quick Hit -- Truth-in-Lending Act/RESPA Integrated Disclosures Rule June 18, 2015

ACC Quick Hit -- Truth-in-Lending Act/RESPA Integrated Disclosures Rule June 18, 2015") HERE S. TRID ACC Quick Hit -- Truth-in-Lending Act/RESPA Integrated Disclosures Rule June 18, 2015 ROBERT E. PINDER rpinder@rtlaw.com (904) 346-5551 HERE S. TRID 2 COUNTDOWN TO TRID TRID Goes into Effect

HERE S. TRID ACC Quick Hit -- Truth-in-Lending Act/RESPA Integrated Disclosures Rule June 18, 2015 ROBERT E. PINDER rpinder@rtlaw.com (904) 346-5551 HERE S. TRID 2 COUNTDOWN TO TRID TRID Goes into Effect

TILA-RESPA Integrated Disclosure (TRID)

") Section A: General Chase Specific Questions QA1. Will there be any changes to the current lock procedures? No. QA2. Will there be any changes to the fee names or structure of the Purchase Advice? No. QA3.

Section A: General Chase Specific Questions QA1. Will there be any changes to the current lock procedures? No. QA2. Will there be any changes to the fee names or structure of the Purchase Advice? No. QA3.

The TILA-RESPA Integrated Disclosure (TRID) Rule. Compiled by: 110 Title, LLC

Rule. Compiled by: 110 Title, LLC") The TILA-RESPA Integrated Disclosure (TRID) Rule Compiled by: 110 Title, LLC 1 I. Introductory Note The Dodd-Frank Wall Street Reform Act and Consumer Protection Act of 2010 (Dodd-Frank), ushered in the

The TILA-RESPA Integrated Disclosure (TRID) Rule Compiled by: 110 Title, LLC 1 I. Introductory Note The Dodd-Frank Wall Street Reform Act and Consumer Protection Act of 2010 (Dodd-Frank), ushered in the

Integrated Disclosure Vocabulary List. Term Definition as of 8/1/2015 Adjustments and Other Credits

Integrated Disclosure Vocabulary List Term Definition as of 8/1/2015 Adjustments and Other Credits Application (triggering RESPA and TILA early disclosures) Included in this is the total amount of all

Integrated Disclosure Vocabulary List Term Definition as of 8/1/2015 Adjustments and Other Credits Application (triggering RESPA and TILA early disclosures) Included in this is the total amount of all

What is T.R.I.D TILA-RESPA Integrated Disclosure

T.R.I.D. What is T.R.I.D TILA-RESPA Integrated Disclosure The CFPB has issued a rule that is aimed to simplify and improve disclosure forms for mortgage transactions. The rule replaces the current forms

T.R.I.D. What is T.R.I.D TILA-RESPA Integrated Disclosure The CFPB has issued a rule that is aimed to simplify and improve disclosure forms for mortgage transactions. The rule replaces the current forms

RESPA/TILA Integration

RESPA/TILA Integration 1 Presented by: Richard Hogan, Vice President & Associate General Counsel Tracy Pandolfo, Director Agent Services Agenda Basics: Why We re Here Final Rule The New Forms Evaluating

RESPA/TILA Integration 1 Presented by: Richard Hogan, Vice President & Associate General Counsel Tracy Pandolfo, Director Agent Services Agenda Basics: Why We re Here Final Rule The New Forms Evaluating

Introduction to the TILA-RESPA Integrated Disclosure Rule TRID

Introduction to the TILA-RESPA Integrated Disclosure Rule TRID October 3, 2015 Aaron Mason NMLS 54707 Mortgage Loan Officer 859-230-4628 AaronMason@homeserviceslending.com AaronMason.RectorHaydenMortgage.com

Introduction to the TILA-RESPA Integrated Disclosure Rule TRID October 3, 2015 Aaron Mason NMLS 54707 Mortgage Loan Officer 859-230-4628 AaronMason@homeserviceslending.com AaronMason.RectorHaydenMortgage.com

What REALTORS. Should Know About CFPB Changes. Courtesy of:

What REALTORS Should Know About CFPB Changes Courtesy of: CFPB was formed as a result of Dodd-Frank in 2010 CFPB governs all matters consumer finance related CFPB now oversees RESPA CFPB regulates: Credit

What REALTORS Should Know About CFPB Changes Courtesy of: CFPB was formed as a result of Dodd-Frank in 2010 CFPB governs all matters consumer finance related CFPB now oversees RESPA CFPB regulates: Credit

TRID TOPICS Forms The Closing Disclosure (CD)

") TRID TOPICS VIII June 8, 2015 TRID TOPICS Forms The Closing Disclosure (CD) WHAT IS THE CLOSING DISCLOSURE AND HOW DOES IT DIFFER FROM TODAY: The Closing Disclosure, also referenced as the CD, under the

TRID TOPICS VIII June 8, 2015 TRID TOPICS Forms The Closing Disclosure (CD) WHAT IS THE CLOSING DISCLOSURE AND HOW DOES IT DIFFER FROM TODAY: The Closing Disclosure, also referenced as the CD, under the

Closing Disclosure Form

Closing Disclosure Form The Closing Disclosure form is designed to detail all financial particulars of a transaction and it must be delivered to the borrower at least three days before closing. It might

Closing Disclosure Form The Closing Disclosure form is designed to detail all financial particulars of a transaction and it must be delivered to the borrower at least three days before closing. It might

Loan Estimates. with the following requirements: Estimate SMF SMF SMF

Loan Estimates with the following requirements: Estimate SMF SMF SMF Please follow the directions below when completing the Initial Loan Application and Disclosure processes. e e cc e and Locked LE, including

Loan Estimates with the following requirements: Estimate SMF SMF SMF Please follow the directions below when completing the Initial Loan Application and Disclosure processes. e e cc e and Locked LE, including

3. Use the Fee drop-down list to select another fee to add to that same section. The pop-up window changes when the new fee is selected.

How to add, edit and delete fees To create a Closing Disclosure, information is entered in Order Entry, Closing Data Entry, and the Closing Disclosure Details screen. If only a Buyer s or Seller s Settlement

How to add, edit and delete fees To create a Closing Disclosure, information is entered in Order Entry, Closing Data Entry, and the Closing Disclosure Details screen. If only a Buyer s or Seller s Settlement

The WAIT IS OVER. THE ANXIETY BEGINS. New RESPA-TILA Mortgage Disclosure Forms

The WAIT IS OVER. THE ANXIETY BEGINS. New RESPA-TILA Mortgage Disclosure Forms Holly Spencer Bunting K&L Gates LLP 1601 K Street NW Washington, DC 20006 (202) 778-9027 holly.bunting@klgates.com Phillip

The WAIT IS OVER. THE ANXIETY BEGINS. New RESPA-TILA Mortgage Disclosure Forms Holly Spencer Bunting K&L Gates LLP 1601 K Street NW Washington, DC 20006 (202) 778-9027 holly.bunting@klgates.com Phillip

Comparison of 2010 RESPA-TILA Disclosure Rules to TILA RESPA Integrated Disclosure Rules

Comparison of 2010 RESPA-TILA Disclosure Rules to TILA RESPA Integrated Disclosure Rules Covered Transactions Exemptions Title of Instructions for completion of Delivery of Electronic delivery Federally

Comparison of 2010 RESPA-TILA Disclosure Rules to TILA RESPA Integrated Disclosure Rules Covered Transactions Exemptions Title of Instructions for completion of Delivery of Electronic delivery Federally

TILA RESPA Integrated Disclosure ~ Closing Disclosure (CD) ~

~") Click for audio recording of training TILA RESPA Integrated Disclosure ~ Closing Disclosure (CD) ~ Fowler Williams President Crescent Mortgage Company 1 Question and Answers Email fwilliams@crescentmortgage.net

Click for audio recording of training TILA RESPA Integrated Disclosure ~ Closing Disclosure (CD) ~ Fowler Williams President Crescent Mortgage Company 1 Question and Answers Email fwilliams@crescentmortgage.net

Wells Fargo Settlement Agent Communications

Wells Fargo Settlement Agent Communications News for Wells Fargo Settlement Agents September 14, 2015 Wells Fargo says thank-you! When the Consumer Financial Protection Bureau (CFPB) announced the TILA-RESPA

Wells Fargo Settlement Agent Communications News for Wells Fargo Settlement Agents September 14, 2015 Wells Fargo says thank-you! When the Consumer Financial Protection Bureau (CFPB) announced the TILA-RESPA

TILA RESPA Integrated Disclosure (TRID) Closing Disclosure Instructions Page 1 LHFSCorrespondent.com (972)

Closing Disclosure Instructions Page 1 LHFSCorrespondent.com (972)") Page 1 The date this disclosure is delivered to the consumer. The date of consummation. The date when the loan amount will be paid, either to the consumer and seller for purchase loans, or to the consumer

Page 1 The date this disclosure is delivered to the consumer. The date of consummation. The date when the loan amount will be paid, either to the consumer and seller for purchase loans, or to the consumer

TRID. Quick Compliance Guide T I L A-RESPA INTEGRAT E D DISCLOSURES Temenos USA. All rights reserved

TRID T I L A-RESPA INTEGRAT E D DISCLOSURES Quick Compliance Guide 09.01.2015 2015 Temenos USA. All rights reserved w: temenos.com/tricomply p: 205.991.5636 e: usainfo@temenos.com While the publisher and

TRID T I L A-RESPA INTEGRAT E D DISCLOSURES Quick Compliance Guide 09.01.2015 2015 Temenos USA. All rights reserved w: temenos.com/tricomply p: 205.991.5636 e: usainfo@temenos.com While the publisher and

TILA-RESPA Integrated Disclosure (TRID)

") Section A: General Questions QA1. What is Chase s policy for investment loans not subject to Regulation Z (loans exempt from Regulation Z pursuant to the Commentary to section 1026.3 of Regulation Z non-owner

Section A: General Questions QA1. What is Chase s policy for investment loans not subject to Regulation Z (loans exempt from Regulation Z pursuant to the Commentary to section 1026.3 of Regulation Z non-owner

document with your Loan Estimate. Transaction Information X Property Taxes NO X Homeowner's Insurance NO Other: details.

Closing Disclosure document with your Loan Estimate. Closing Information Date Issued Closing Date Disbursement Date Settlement Agent File # Property Sale Price BLANKTRID Transaction Information Borrower

Closing Disclosure document with your Loan Estimate. Closing Information Date Issued Closing Date Disbursement Date Settlement Agent File # Property Sale Price BLANKTRID Transaction Information Borrower

The new Loan Estimate Form integrates and replaces the existing RESPA Good Faith Estimate and the initial Truth in Lending forms.

The Consumer Financial Protection Bureau s (CFPB) integrated mortgage disclosure rule will be effective August 1, 2015. This rule consolidates four existing disclosures required under Truth-in-Lending

The Consumer Financial Protection Bureau s (CFPB) integrated mortgage disclosure rule will be effective August 1, 2015. This rule consolidates four existing disclosures required under Truth-in-Lending

TRID Quick Reference Guide

TRID General Rules and Definitions New Required Disclosures Loan Estimate (LE) replaces the GFE and Initial TIL Closing Disclosure (CD) replaces the Final TIL and HUD-1 Home Loan Toolkit replaces the HUD

TRID General Rules and Definitions New Required Disclosures Loan Estimate (LE) replaces the GFE and Initial TIL Closing Disclosure (CD) replaces the Final TIL and HUD-1 Home Loan Toolkit replaces the HUD

February 2016 FEBRUARY Sunday Monday Tuesday Wednesday Thursday Friday Saturday. CD is placed in the mail IF DELIVERED BY OVERNIGHT MAIL...

DELIVERY METHODS & TIMING CHEAT SHEET IF DELIVERED BY MAIL... Closing Disclosure (CD) is sent to borrower in the mail 3 day mailing rule applies for the receipt of the disclosure Then 3 day waiting period

DELIVERY METHODS & TIMING CHEAT SHEET IF DELIVERED BY MAIL... Closing Disclosure (CD) is sent to borrower in the mail 3 day mailing rule applies for the receipt of the disclosure Then 3 day waiting period

TILA-RESPA Integrated Disclosure (TRID)

") Section A: General Questions QA1. What is Chase s policy for investment loans not subject to Regulation Z (loans exempt from Regulation Z pursuant to Supplement I of section 1026.3 of Regulation Z non-owner

Section A: General Questions QA1. What is Chase s policy for investment loans not subject to Regulation Z (loans exempt from Regulation Z pursuant to Supplement I of section 1026.3 of Regulation Z non-owner

TRID. Old vs New Comparison of TILA/RESPA Integrated Disclosure Changes for Real Estate Agents. Copyright 2015 Go2Training Consultants, LLC.

TRID Old vs New Comparison of TILA/RESPA Integrated Changes for Real Estate Agents Old vs New Comparison of the TILA/RESPA Integrated Changes Good Faith Estimate Loan Estimate The GFE and Initial TIL are

TRID Old vs New Comparison of TILA/RESPA Integrated Changes for Real Estate Agents Old vs New Comparison of the TILA/RESPA Integrated Changes Good Faith Estimate Loan Estimate The GFE and Initial TIL are

CFPB TRAINING - EXERCISE 6

Overview: Create a Closing Disclosure Form (CDF) form and one HUD where the HUD is for a Home Equity Line of Credit (HELOC). Use the steps and additional information below for help with key items and where

Overview: Create a Closing Disclosure Form (CDF) form and one HUD where the HUD is for a Home Equity Line of Credit (HELOC). Use the steps and additional information below for help with key items and where

The New Mortgage Disclosure Forms: Know the Rule

The New Mortgage Disclosure Forms: Know the Rule 10:15 11:15 a.m. Phillip L. Schulman, Esq., Partner, K&L Gates LLP THE WAIT IS OVER. THE ANXIETY BEGINS. New RESPA-TILA Mortgage Disclosure Forms Phillip

The New Mortgage Disclosure Forms: Know the Rule 10:15 11:15 a.m. Phillip L. Schulman, Esq., Partner, K&L Gates LLP THE WAIT IS OVER. THE ANXIETY BEGINS. New RESPA-TILA Mortgage Disclosure Forms Phillip

The Integrated Disclosures Rule Part A: Introduction to the Integrated Disclosures Rule... 5 Topic 1: Consolidated Disclosures...

SA PL M E Contents The Integrated Disclosures Rule... 4 Part A: Introduction to the Integrated Disclosures Rule... 5 Topic 1: Consolidated Disclosures... 5 Topic 2: Integrated Disclosures Requirements...

SA PL M E Contents The Integrated Disclosures Rule... 4 Part A: Introduction to the Integrated Disclosures Rule... 5 Topic 1: Consolidated Disclosures... 5 Topic 2: Integrated Disclosures Requirements...

The CFPB s New Mortgage Disclosures

The CFPB s New Mortgage Disclosures Benjamin K. Olson March 10, 2015 Key Changes Effective August 1, 2015: GFE and initial TIL replaced with the Loan Estimate The items constituting an application are

The CFPB s New Mortgage Disclosures Benjamin K. Olson March 10, 2015 Key Changes Effective August 1, 2015: GFE and initial TIL replaced with the Loan Estimate The items constituting an application are

Closing Information Transaction Information Loan Information. VA Property Loan ID # Lender MIC # Sale Price $

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Seminar: Closing Disclosure Form Training

Seminar: Date: February 15, 2016 Seminar: Date: February 15, 2016 Presented by: Sandi Allfrey Training and Development Manager Attorneys Title Guaranty Fund, Inc. CDF FAQs Calculating Title Policy Charges

Seminar: Date: February 15, 2016 Seminar: Date: February 15, 2016 Presented by: Sandi Allfrey Training and Development Manager Attorneys Title Guaranty Fund, Inc. CDF FAQs Calculating Title Policy Charges

CFPB Integrated Mortgage Disclosure Final Rule

CFPB Integrated Mortgage Disclosure Final Rule Current Status of the New Rule Mary Schuster Chief Product Officer - RamQuest The Regulatory Reform Ecosystem Meet the CFPB Mission Statement o To make markets

CFPB Integrated Mortgage Disclosure Final Rule Current Status of the New Rule Mary Schuster Chief Product Officer - RamQuest The Regulatory Reform Ecosystem Meet the CFPB Mission Statement o To make markets

The SoftPro Solution

The SoftPro Solution 1 The Final Rule Patrick Hempen SoftPro Corporation SVP Sales & Marketing patrick.hempen@softprocorp.com 2 The Goals of the Final Rule: Improved consumer understanding Risk factors

The SoftPro Solution 1 The Final Rule Patrick Hempen SoftPro Corporation SVP Sales & Marketing patrick.hempen@softprocorp.com 2 The Goals of the Final Rule: Improved consumer understanding Risk factors

Complete Closing Enterprise Closing Disclosure Form

Complete Closing Enterprise Closing Disclosure Form VERSION 8.3 RamQuest.com 2015 RamQuest, Inc. Table of Contents Introduction... 5 Loan Estimate... 5 Closing Disclosure Form... 5 Accessing the CDF...

Complete Closing Enterprise Closing Disclosure Form VERSION 8.3 RamQuest.com 2015 RamQuest, Inc. Table of Contents Introduction... 5 Loan Estimate... 5 Closing Disclosure Form... 5 Accessing the CDF...

TILA/RESPA Integrated Disclosure Rule

TILA/RESPA Integrated Disclosure Rule Solving the Puzzle July 22, 2015 Presented by: Gary D. Clark, CMB Chief Operating Officer Sierra Pacific Mortgage Webinar All lines will be muted You can type your

TILA/RESPA Integrated Disclosure Rule Solving the Puzzle July 22, 2015 Presented by: Gary D. Clark, CMB Chief Operating Officer Sierra Pacific Mortgage Webinar All lines will be muted You can type your

TILA-RESPA Integrated Disclosures (TRID) FAQs

FAQs") TILA-RESPA Integrated Disclosures (TRID) FAQs On July 21, 2015, the Consumer Financial Protection Bureau (CFPB) published the final rule to delay the effective date of the TILA-RESPA Integrated Disclosure

TILA-RESPA Integrated Disclosures (TRID) FAQs On July 21, 2015, the Consumer Financial Protection Bureau (CFPB) published the final rule to delay the effective date of the TILA-RESPA Integrated Disclosure

TILA / RESPA Integrated Disclosures Roll-Out. CUNA Lending Council November 4th, 2014

TILA / RESPA Integrated Disclosures Roll-Out CUNA Lending Council November 4th, 2014 Presenter Jon Bundy Regulatory Compliance Manager LOANLINER Documents CUNA Mutual Group Agenda Overview of Integrated

TILA / RESPA Integrated Disclosures Roll-Out CUNA Lending Council November 4th, 2014 Presenter Jon Bundy Regulatory Compliance Manager LOANLINER Documents CUNA Mutual Group Agenda Overview of Integrated

The New Loan Estimate & Closing Disclosure Explained. Know before you close.

Know before you close. The New Loan Estimate & a Closing Disclosure Explained A look at the different sections of each new form and explanations of each page. 2015 Chicago Title Know before you close.

Know before you close. The New Loan Estimate & a Closing Disclosure Explained A look at the different sections of each new form and explanations of each page. 2015 Chicago Title Know before you close.

THE CLOSING DISCLOSURE

THE CLOSING DISCLOSURE Coverage: Most Closed-End Consumer Mortgages Not HELOCs, reverse mortgages or mobile home loans not attached to real property Agency/Citation: Consumer Financial Protection Bureau

THE CLOSING DISCLOSURE Coverage: Most Closed-End Consumer Mortgages Not HELOCs, reverse mortgages or mobile home loans not attached to real property Agency/Citation: Consumer Financial Protection Bureau

WELCOME! Are You Ready for TRID?

1 WELCOME! www.grantsimon.com Are You Ready for TRID? 2 Dodd Frank the CFPB & You Featuring TRID TRID TILA-RESPA INTEGRATED DISCLOSURE 3 Ready For It New Jargon Lender Borrower Closing GFE & TIL HUD 1

1 WELCOME! www.grantsimon.com Are You Ready for TRID? 2 Dodd Frank the CFPB & You Featuring TRID TRID TILA-RESPA INTEGRATED DISCLOSURE 3 Ready For It New Jargon Lender Borrower Closing GFE & TIL HUD 1

Closing Information Transaction Information Loan Information. VA Property Lender Loan ID # MIC #

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Consumer Financial Protection Bureau Rule

Consumer Financial Protection Bureau Rule Presented by Jerry T. Gorman Attorneys Title Guaranty Fund, Inc. Champaign CFPB Rule Consumer Financial Protection Bureau (CFPB) Came into being July 2011 Created

Consumer Financial Protection Bureau Rule Presented by Jerry T. Gorman Attorneys Title Guaranty Fund, Inc. Champaign CFPB Rule Consumer Financial Protection Bureau (CFPB) Came into being July 2011 Created

WELCOME!

WELCOME! www.grantsimon.com Are You Ready for TRID? Dodd Frank the CFPB & You Featuring TRID TRID TILA-RESPA INTEGRATED DISCLOSURE Ready For It New Jargon Lender Borrower Closing GFE & TIL HUD 1 & TIL

WELCOME! www.grantsimon.com Are You Ready for TRID? Dodd Frank the CFPB & You Featuring TRID TRID TILA-RESPA INTEGRATED DISCLOSURE Ready For It New Jargon Lender Borrower Closing GFE & TIL HUD 1 & TIL

TILA RESPA Integrated Disclosure (TRID) Doing Business with NewLeaf

Doing Business with NewLeaf") TILA RESPA Integrated Disclosure (TRID) Doing Business with NewLeaf Presented By Marti Tromley EVP, Chief Risk Officer mtromley@newleafwholesale.com The information contained herein is intended as informational

TILA RESPA Integrated Disclosure (TRID) Doing Business with NewLeaf Presented By Marti Tromley EVP, Chief Risk Officer mtromley@newleafwholesale.com The information contained herein is intended as informational

Presentation by Janet M. Bonnefin Aldrich & Bonnefin, PLC

Washington Bankers Association 2015 Northwest Compliance Conference TRID We re Down to the Wire! Presentation by Janet M. Bonnefin Aldrich & Bonnefin, PLC Agenda Creditor s duty to give Loan Estimate Restrictions

Washington Bankers Association 2015 Northwest Compliance Conference TRID We re Down to the Wire! Presentation by Janet M. Bonnefin Aldrich & Bonnefin, PLC Agenda Creditor s duty to give Loan Estimate Restrictions

TRID (TILA-RESPA Integrated Disclosures) Presented by:

Presented by:") TRID (TILA-RESPA Integrated Disclosures) Presented by: What is TRID? TRID will eliminate the use of the good faith estimate, truth in lending disclosures, and HUD-1 Settlement Statement. They will now

TRID (TILA-RESPA Integrated Disclosures) Presented by: What is TRID? TRID will eliminate the use of the good faith estimate, truth in lending disclosures, and HUD-1 Settlement Statement. They will now

CFPB: The New Closing Process

CFPB: The New Closing Process Course Objective: Relate the new CFPB Rules to what the real estate transaction process could look like after August 1, 2015 (CFPB revised date: October 3, 2015) INTRODUCTION

CFPB: The New Closing Process Course Objective: Relate the new CFPB Rules to what the real estate transaction process could look like after August 1, 2015 (CFPB revised date: October 3, 2015) INTRODUCTION

TRID. Acceptable Broker Submissions Booklet WHSL EQUAL HOUSING LENDER MEMBER FDIC NMLS #478471

TRID Acceptable Broker Submissions Booklet EQUAL HOUSING LENDER MEMBER FDIC NMLS #478471 WHSL-0022-1015 As Fremont Bank transitions to the new Rule, our goal is to make the submission of your loan applications

TRID Acceptable Broker Submissions Booklet EQUAL HOUSING LENDER MEMBER FDIC NMLS #478471 WHSL-0022-1015 As Fremont Bank transitions to the new Rule, our goal is to make the submission of your loan applications

Closing Disclosure. Loan Terms. Projected Payments. Costs at Closing

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued Closing Date Disbursement Date Settlement

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued Closing Date Disbursement Date Settlement

TILA-RESPA Integrated Disclosure (TRID) Rule a.k.a. Know Before You Owe. with New Haven Middlesex Association of REALTORS

Rule a.k.a. Know Before You Owe. with New Haven Middlesex Association of REALTORS") TILA-RESPA Integrated Disclosure (TRID) Rule a.k.a. Know Before You Owe with New Haven Middlesex Association of REALTORS July 16, 2015 Jeremy Potter, General Counsel and Chief Compliance Officer, Norcom

TILA-RESPA Integrated Disclosure (TRID) Rule a.k.a. Know Before You Owe with New Haven Middlesex Association of REALTORS July 16, 2015 Jeremy Potter, General Counsel and Chief Compliance Officer, Norcom

TRID October 3, 2015!

TRID October 3, 2015! Purpose This announcement includes the following topics: Consumer Financial Protection Bureau (CFPB), Truth-in-Lending and RESPA Integrated Disclosures (TRID). Policy It is MSI Policy

TRID October 3, 2015! Purpose This announcement includes the following topics: Consumer Financial Protection Bureau (CFPB), Truth-in-Lending and RESPA Integrated Disclosures (TRID). Policy It is MSI Policy

Understanding CFPB Rules CONSUMER FINANCIAL PROTECTION BUREAU

Understanding CFPB Rules CONSUMER FINANCIAL PROTECTION BUREAU The Consumer Financial Protection Bureau The CFPB is a new federal agency Created by Dodd Frank Wall Street and Consumer Protection Act Dodd

Understanding CFPB Rules CONSUMER FINANCIAL PROTECTION BUREAU The Consumer Financial Protection Bureau The CFPB is a new federal agency Created by Dodd Frank Wall Street and Consumer Protection Act Dodd

TILA RESPA Integrated Disclosure

FEBRUARY 7, 2014 TILA RESPA Integrated Disclosure H-24(G) Mortgage Loan Transaction Loan Estimate Modification to Loan Estimate for Transaction Not Involving Seller Model Form This is a blank model Loan

FEBRUARY 7, 2014 TILA RESPA Integrated Disclosure H-24(G) Mortgage Loan Transaction Loan Estimate Modification to Loan Estimate for Transaction Not Involving Seller Model Form This is a blank model Loan

TIL/RESPA Final Rules on Integrated Mortgage Disclosures

TIL/RESPA Final Rules on Integrated Mortgage Disclosures CLAconnect.com Disclaimers The information contained herein is general in nature and is not intended, and should not be construed, as legal, accounting,

TIL/RESPA Final Rules on Integrated Mortgage Disclosures CLAconnect.com Disclaimers The information contained herein is general in nature and is not intended, and should not be construed, as legal, accounting,

The TRID Process for Wholesale Lending

The TRID Process for Wholesale Lending Michelle McLaughlin 2015 CMG Financial, All Rights Reserved. CMG Financial is a registered trade name of CMG Mortgage, Inc., NMLS #1820 in most, but not all states.

The TRID Process for Wholesale Lending Michelle McLaughlin 2015 CMG Financial, All Rights Reserved. CMG Financial is a registered trade name of CMG Mortgage, Inc., NMLS #1820 in most, but not all states.

FINALLY HERE TILA-RESPA INTEGRATED DISCLOSURE FORMS

TRIPLE PLAY CONVENTION FINALLY HERE TILA-RESPA INTEGRATED DISCLOSURE FORMS December 7, 2015 Phillip L. Schulman K&L Gates LLP 1601 K Street NW Washington, DC 20006 (202) 778-9027 phil.schulman@klgates.com

TRIPLE PLAY CONVENTION FINALLY HERE TILA-RESPA INTEGRATED DISCLOSURE FORMS December 7, 2015 Phillip L. Schulman K&L Gates LLP 1601 K Street NW Washington, DC 20006 (202) 778-9027 phil.schulman@klgates.com

Closing Disclosure $0 NO. $0 a month. Loan Terms. Projected Payments. Costs at Closing

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued Closing Date Disbursement Date Settlement

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued Closing Date Disbursement Date Settlement

Closing Disclosure $ % $ $ $ $ Loan Terms. Projected Payments. Costs at Closing

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Issued Borrower

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Issued Borrower

The CFPB s TILA-RESPA Integrated Disclosure Rule: What You Need to Know for October 3rd. Paul Bugoni, Esq. Stewart Title Guaranty Company New York, NY

The CFPB s TILA-RESPA Integrated Disclosure Rule: What You Need to Know for October 3rd by Paul Bugoni, Esq. Stewart Title Guaranty Company New York, NY 1 2 The CFPB s TILA-RESPA Integrated Disclosure

The CFPB s TILA-RESPA Integrated Disclosure Rule: What You Need to Know for October 3rd by Paul Bugoni, Esq. Stewart Title Guaranty Company New York, NY 1 2 The CFPB s TILA-RESPA Integrated Disclosure

Closing Disclosure (CD) Communicating with Creditors Owner s Title Insurance Premium

Communicating with Creditors Owner s Title Insurance Premium") Frequently Asked Questions CFPB s TILA-RESPA Integrated Disclosure (TRID) Rule To use the index, click on a topic below to be taken to that topic location in the document. Section 1: Section 2: Section

Frequently Asked Questions CFPB s TILA-RESPA Integrated Disclosure (TRID) Rule To use the index, click on a topic below to be taken to that topic location in the document. Section 1: Section 2: Section

TRID TILA RESPA Integrated Disclosures

Experience Extraordinary TRID TILA RESPA Integrated Disclosures May 13, 2015 Loan Estimate Completion Kara Lamphere Loan Estimate Breakdown The GFE and Initial TIL combined = the Loan Estimate ( LE ) http://files.consumerfinance.gov/f/201403_cfpb_loan-estimate_model-form-h24.pdf

Experience Extraordinary TRID TILA RESPA Integrated Disclosures May 13, 2015 Loan Estimate Completion Kara Lamphere Loan Estimate Breakdown The GFE and Initial TIL combined = the Loan Estimate ( LE ) http://files.consumerfinance.gov/f/201403_cfpb_loan-estimate_model-form-h24.pdf

CUNA Mutual Group Discovery Conference logo

CUNA Mutual Group Discovery Conference logo It s a Whole New World TILA/RESPA Integrated Disclosures Theresa Reinke, LOANLINER Compliance Consultant, CUNA Mutual Group Download the Slides Need Some Help??

CUNA Mutual Group Discovery Conference logo It s a Whole New World TILA/RESPA Integrated Disclosures Theresa Reinke, LOANLINER Compliance Consultant, CUNA Mutual Group Download the Slides Need Some Help??

A GFE must be issued when the originator receives an application OR six minimum pieces of information sufficient to complete an application including:

PROVIDENT BANK MORTGAGE RESPA REFORM Effective January 1, 2010 RESPA OVERVIEW The goal of RESPA Reform is to provide consumers with the information needed to readily understand loan terms and total settlement

PROVIDENT BANK MORTGAGE RESPA REFORM Effective January 1, 2010 RESPA OVERVIEW The goal of RESPA Reform is to provide consumers with the information needed to readily understand loan terms and total settlement

TRID: TILA-RESPA Integrated Disclosures Rules and Procedures Overview

TRID: TILA-RESPA Integrated Disclosures Rules and Procedures Overview Disclaimer Information included is intended for general information purposes only and is current as October 2, 2015. It should not

TRID: TILA-RESPA Integrated Disclosures Rules and Procedures Overview Disclaimer Information included is intended for general information purposes only and is current as October 2, 2015. It should not

Executive Summary of the 2017 TILA- RESPA Rule

1700 G Street NW, Washington, DC 20552 July 7, 2017 Executive Summary of the 2017 TILA- RESPA Rule On July 7, 2017, the Consumer Financial Protection Bureau (Bureau) issued a final rule (2017 TILA-RESPA

1700 G Street NW, Washington, DC 20552 July 7, 2017 Executive Summary of the 2017 TILA- RESPA Rule On July 7, 2017, the Consumer Financial Protection Bureau (Bureau) issued a final rule (2017 TILA-RESPA

Guidance for Completing the 2010 Good Faith Estimate

Guidance for Completing the 2010 Good Faith Estimate Please use this information for assistance when completing the 2010 GFE. Initial accuracy is imperative as it is binding and inaccuracy may result in

Guidance for Completing the 2010 Good Faith Estimate Please use this information for assistance when completing the 2010 GFE. Initial accuracy is imperative as it is binding and inaccuracy may result in

Contents. Basics of the Integrated Mortgage Disclosures Rule...3. Closing Disclosure Sample...4. Closing Disclosure Delivery Calendar Examples...

Contents Basics of the Integrated Mortgage Disclosures Rule...3 Closing Disclosure Sample...4 Closing Disclosure Delivery Calendar Examples...9 Basics of the Integrated Mortgage Disclosures Rule What

Contents Basics of the Integrated Mortgage Disclosures Rule...3 Closing Disclosure Sample...4 Closing Disclosure Delivery Calendar Examples...9 Basics of the Integrated Mortgage Disclosures Rule What

TRID TILA RESPA Integrated Disclosures

Experience Extraordinary TRID TILA RESPA Integrated Disclosures July 16, 2015 Changed Circumstances: Revised Loan Estimates and Revised Closing Disclosures Kara Lamphere Changed Circumstances The reasons

Experience Extraordinary TRID TILA RESPA Integrated Disclosures July 16, 2015 Changed Circumstances: Revised Loan Estimates and Revised Closing Disclosures Kara Lamphere Changed Circumstances The reasons

CFPB- Getting Ready for NEW Real Estate Closing Procedures. Ruth Dillingham, Special Counsel First American Title Insurance Company April 17, 2014

CFPB- Getting Ready for NEW Real Estate Closing Procedures Ruth Dillingham, Special Counsel First American Title Insurance Company April 17, 2014 1 Supervision of Third Party Vendors CFPB Bulletin April

CFPB- Getting Ready for NEW Real Estate Closing Procedures Ruth Dillingham, Special Counsel First American Title Insurance Company April 17, 2014 1 Supervision of Third Party Vendors CFPB Bulletin April

PPDocs, Inc. Compliance Certificate

PPDocs, Inc. Lender: Peirson & Patterson Borrower(s): Webinar Demo, a single man Property: 2310 W Interstate 20, Arlington, TX 76017 Loan Type: First Lien Fixed Rate Conventional Loan Loan Purpose: Purchase

PPDocs, Inc. Lender: Peirson & Patterson Borrower(s): Webinar Demo, a single man Property: 2310 W Interstate 20, Arlington, TX 76017 Loan Type: First Lien Fixed Rate Conventional Loan Loan Purpose: Purchase

Good Faith Estimate (GFE)

") OMB pproval No. 2502-0265 Good Faith Estimate (GFE) Name of Originator Originator ddress Borrower Property ddress Originator Phone Number Originator Email Date of GFE Purpose Shopping for your loan Important

OMB pproval No. 2502-0265 Good Faith Estimate (GFE) Name of Originator Originator ddress Borrower Property ddress Originator Phone Number Originator Email Date of GFE Purpose Shopping for your loan Important

Display the questions that impact the date through which the interest rate is available with a left click on the control.

New Standardized Good Faith Estimate On November 17, 2008, the Department of Housing and Urban Development published its final rule regarding RESPA Reform. The final rule requires mortgage lenders and

New Standardized Good Faith Estimate On November 17, 2008, the Department of Housing and Urban Development published its final rule regarding RESPA Reform. The final rule requires mortgage lenders and

The TILA-RESPA Integrated Disclosures Rule consolidates. Estimate (GFE) into the Loan Estimate and. the Closing Disclosure

into the Loan Estimate and. the Closing Disclosure") Agenda This training consists of three parts explaining the general requirements of the law that consolidated multiple disclosures into two separate forms; the Loan Estimate and the Closing Disclosure:

Agenda This training consists of three parts explaining the general requirements of the law that consolidated multiple disclosures into two separate forms; the Loan Estimate and the Closing Disclosure:

New RESPA Rule FAQs. (New items are in bold)

") New RESPA Rule FAQs (New items are in bold) General 1) Q: When does the new RESPA Rule take effect? A: The November 2008 RESPA Rule was effective January 16, 2009. Implementation of the provisions are

New RESPA Rule FAQs (New items are in bold) General 1) Q: When does the new RESPA Rule take effect? A: The November 2008 RESPA Rule was effective January 16, 2009. Implementation of the provisions are

Correspondent Procedures. rev. 8/3/16

Correspondent Procedures rev. 8/3/16 1 Website www.mmcitpo.com AUS Run Requests Definition of an application Fees Registration/Rate Lock The Loan Estimate Submission Checklists TBDs LE/CD Revision Requests

Correspondent Procedures rev. 8/3/16 1 Website www.mmcitpo.com AUS Run Requests Definition of an application Fees Registration/Rate Lock The Loan Estimate Submission Checklists TBDs LE/CD Revision Requests

The New CFPB Mortgage Disclosures: What You Need to Know. William A. Anderson Vice President, Best Practices and Legislative Affairs

The New CFPB Mortgage Disclosures: What You Need to Know William A. Anderson Vice President, Best Practices and Legislative Affairs Poll Question Tell us about yourself: o This is my first NSA Webinar

The New CFPB Mortgage Disclosures: What You Need to Know William A. Anderson Vice President, Best Practices and Legislative Affairs Poll Question Tell us about yourself: o This is my first NSA Webinar

CFPB: The New Closing Process

CFPB: The New Closing Process Course Objective: Relate the new CFPB Rules to what the real estate transaction process could look like after August 1, 2015 INTRODUCTION (10-12 minute segment) TEACHING OBJECTIVE:

CFPB: The New Closing Process Course Objective: Relate the new CFPB Rules to what the real estate transaction process could look like after August 1, 2015 INTRODUCTION (10-12 minute segment) TEACHING OBJECTIVE:

Uniform Closing Dataset (UCD) Specification Issued by Fannie Mae and Freddie Mac Appendix C: Sample Closing Disclosures with Reference Numbers

Specification Issued by Fannie Mae and Freddie Mac Appendix C: Sample Closing Disclosures with Reference Numbers") Uniform Closing Dataset (UCD) Specification Issued by Fannie Mae and Freddie Mac Appendix C: Sample Closing Disclosures with Numbers Document Version 1.5 June 06, 2017 In support of the Integrated Mortgage

Uniform Closing Dataset (UCD) Specification Issued by Fannie Mae and Freddie Mac Appendix C: Sample Closing Disclosures with Numbers Document Version 1.5 June 06, 2017 In support of the Integrated Mortgage

Loan Estimate $ NO. Loan Terms. Loan Amount $ NO. Interest Rate 1.75% NO

Pennsylvania Housing Finance Agency 211 N. Front Street Harrisburg, PA 17101 Save this Loan Estimate to compare with your Closing Disclosure. Loan Estimate DATE ISSUED APPLICANTS PROPERTY PROP. VALUE LOAN

Pennsylvania Housing Finance Agency 211 N. Front Street Harrisburg, PA 17101 Save this Loan Estimate to compare with your Closing Disclosure. Loan Estimate DATE ISSUED APPLICANTS PROPERTY PROP. VALUE LOAN

Closing Information Transaction Information Loan Information KRISTINE GERMOLAI 132 PHILIP STREET HOLBROOK, NY PLAZA HOME MORTGAGE INC NO NO + -

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

RESPA REFORM TRAINING Effective January 1, FOR MORTGAGE PROFESSIONALS ONLY Rev 1, 12/29/09

RESPA REFORM TRAINING Effective January 1, 2010 OVERVIEW In November 2008, HUD published its final rule amending Regulation X of the Real Estate Settlement Procedures Act (RESPA). The final rule includes

RESPA REFORM TRAINING Effective January 1, 2010 OVERVIEW In November 2008, HUD published its final rule amending Regulation X of the Real Estate Settlement Procedures Act (RESPA). The final rule includes

Know Before You Owe Mortgage Disclosure Rule: Post-Effective Date Questions & Guidance

Know Before You Owe Mortgage Disclosure Rule: Post-Effective Date Questions & Guidance Outlook Live Webinar April 12, 2016 Dania Ayoubi Seth Caffrey Kristin Switzer Alexa Reimelt Chelsea Peter Counsel

Know Before You Owe Mortgage Disclosure Rule: Post-Effective Date Questions & Guidance Outlook Live Webinar April 12, 2016 Dania Ayoubi Seth Caffrey Kristin Switzer Alexa Reimelt Chelsea Peter Counsel

2014 Freddie Mac and Fannie Mae. All Rights Reserved. MISMO is a registered trademark of the Mortgage Industry Standards Maintenance Organization.

Uniform Closing Dataset (UCD) Specification Issued by Fannie Mae and Freddie Mac Appendix C: Closing Disclosure with Numbers Non-Seller Transaction Document Version 1.1 July 15, 2014 In support of the

Uniform Closing Dataset (UCD) Specification Issued by Fannie Mae and Freddie Mac Appendix C: Closing Disclosure with Numbers Non-Seller Transaction Document Version 1.1 July 15, 2014 In support of the

Presented by Powered by Investors Title

CFPB and the Changing Landscape of Real Estate Closings Presented by Powered by Investors Title The only thing constant in life is change. - François de la Rochefoucauld And the CFPB is proof positive!

CFPB and the Changing Landscape of Real Estate Closings Presented by Powered by Investors Title The only thing constant in life is change. - François de la Rochefoucauld And the CFPB is proof positive!

Guidance for Completing the 2010 Good Faith Estimate

Guidance for Completing the 2010 Good Faith Estimate Please use this information for assistance when completing the 2010 GFE. Initial accuracy is imperative as it is binding and inaccuracy may result in

Guidance for Completing the 2010 Good Faith Estimate Please use this information for assistance when completing the 2010 GFE. Initial accuracy is imperative as it is binding and inaccuracy may result in

FREQUENTLY ASKED QUESTIONS (FAQ) FOR IMPLEMENTING THE TILA-RESPA INTEGRATED DISCLOSURE RULE (TRID)

FOR IMPLEMENTING THE TILA-RESPA INTEGRATED DISCLOSURE RULE (TRID)") Best Practices FREQUENTLY ASKED QUESTIONS (FAQ) FOR IMPLEMENTING THE TILA-RESPA INTEGRATED DISCLOSURE RULE (TRID) SUMMARY With the upcoming implementation of the Truth in Lending (TILA)/Real Estate Settlement

Best Practices FREQUENTLY ASKED QUESTIONS (FAQ) FOR IMPLEMENTING THE TILA-RESPA INTEGRATED DISCLOSURE RULE (TRID) SUMMARY With the upcoming implementation of the Truth in Lending (TILA)/Real Estate Settlement

Closing Disclosure $ NO $1, $ a month. Loan Terms. Projected Payments. Costs at Closing

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued 8/15/2015 Closing Date 8/31/2015 Disbursement

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued 8/15/2015 Closing Date 8/31/2015 Disbursement

Closing Disclosure $ $ Loan Terms. Projected Payments. Costs at Closing

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Issued Borrower

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Issued Borrower

Settlement Disclosure

Settlement Disclosure This form is a statement of final loan terms and closing costs. Compare this document to your Loan Estimate. Settlement information Date 1/24/2012 Agent ABC Settlement File # 01234

Settlement Disclosure This form is a statement of final loan terms and closing costs. Compare this document to your Loan Estimate. Settlement information Date 1/24/2012 Agent ABC Settlement File # 01234

Transaction Information. Johnathan James Doe and Jennifer Jane Doe 1234 Riverside Drive Grand Prairie, TX ABC Mortgage Company

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued 10/31/2016 Closing Date /30/2016 Disbursement

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued 10/31/2016 Closing Date /30/2016 Disbursement