CENTER FOR MICROECONOMIC DATA

|

|

|

- Baldric Clarke

- 5 years ago

- Views:

Transcription

FEDERAL RESERVE BANK of NEW YORK")

1 CENTER FOR MICROECONOMIC DATA QUA RTERL Y REPORT ON HOUSEHOLD DEBT AND CREDIT 20 18:Q4 (RELEASED FEBRUARY 2019 ) FEDERAL RESERVE BANK of NEW YORK RESEARCH AND STATISTICS GROUP ANALYSIS BASED ON NEW YORK FED CONSUMER CREDIT PANEL/EQUIFAX DATA

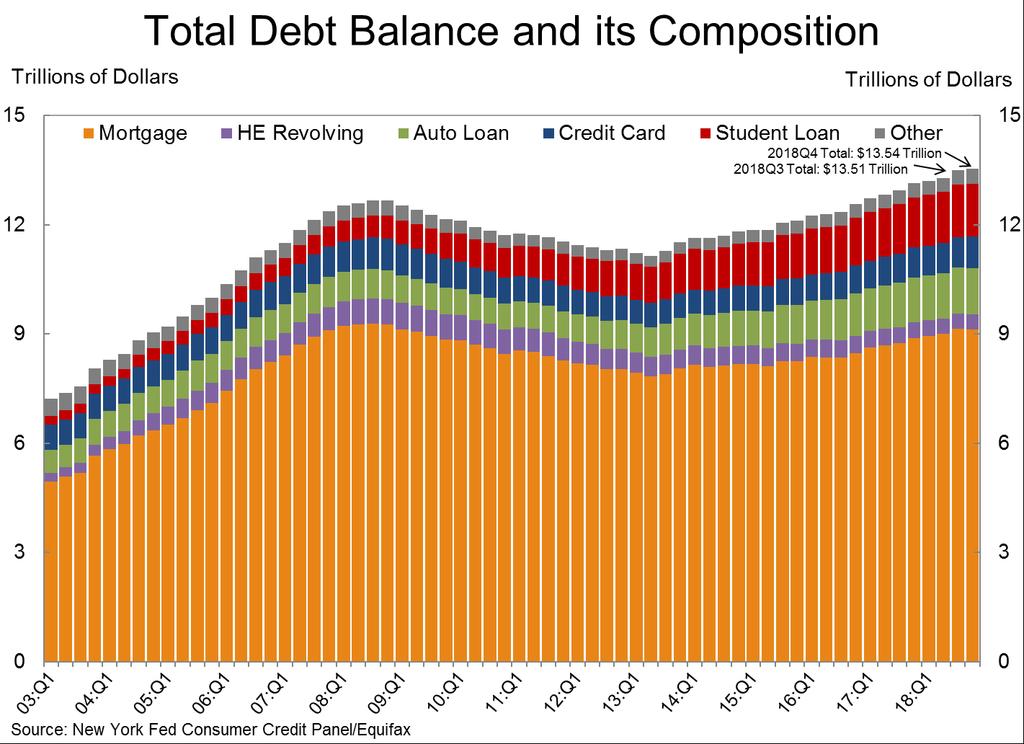

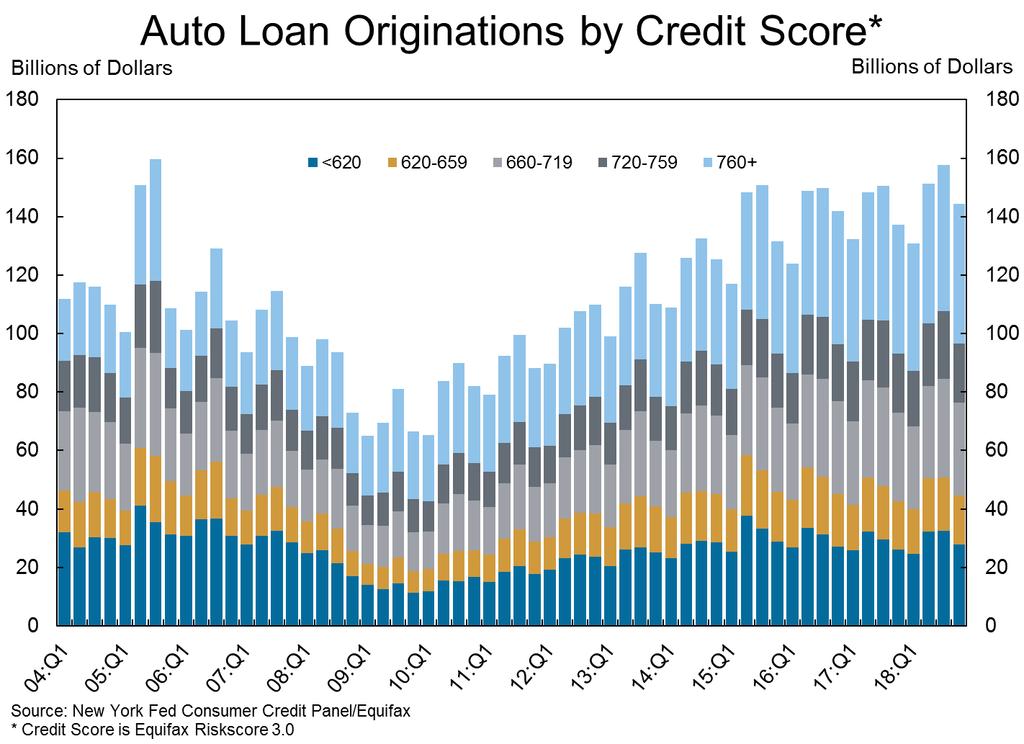

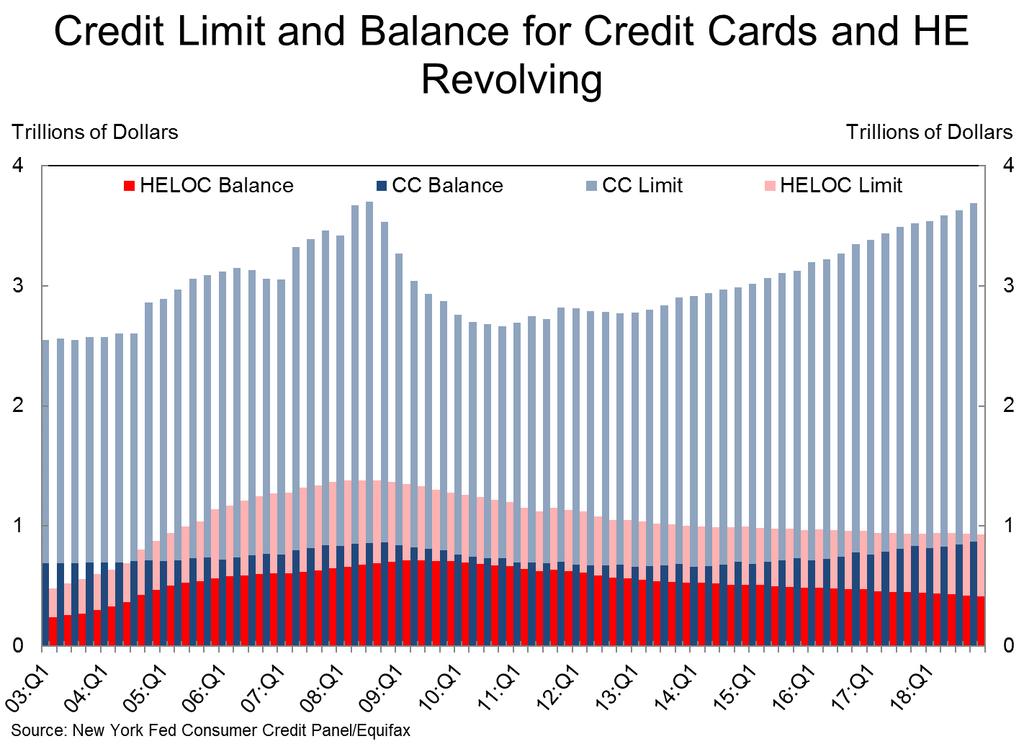

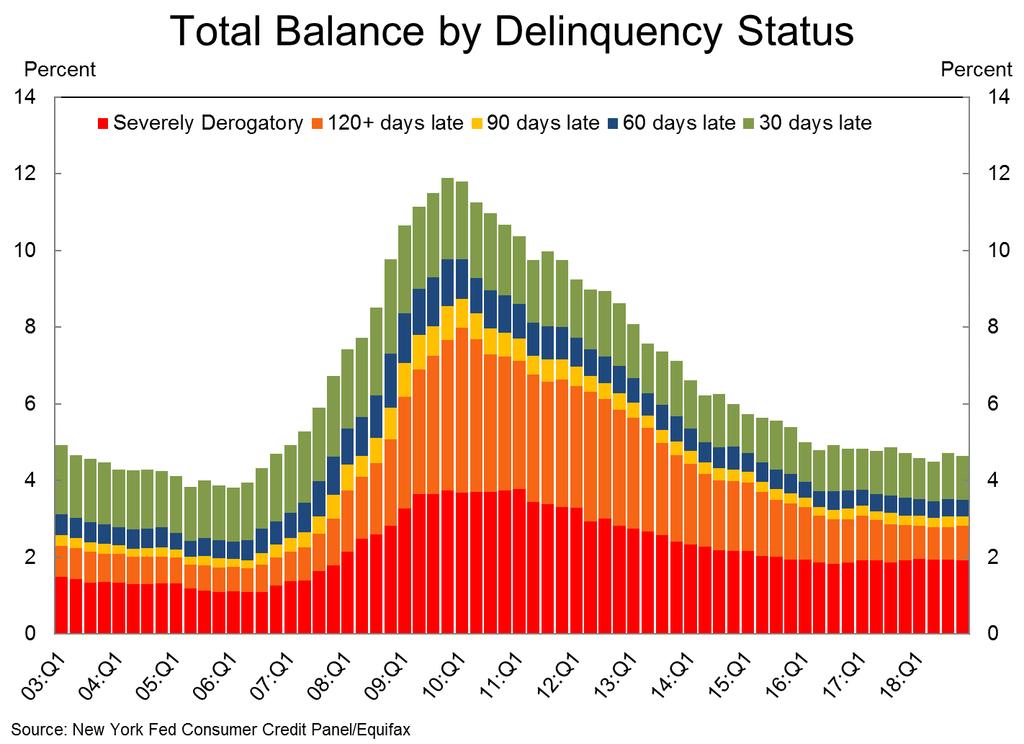

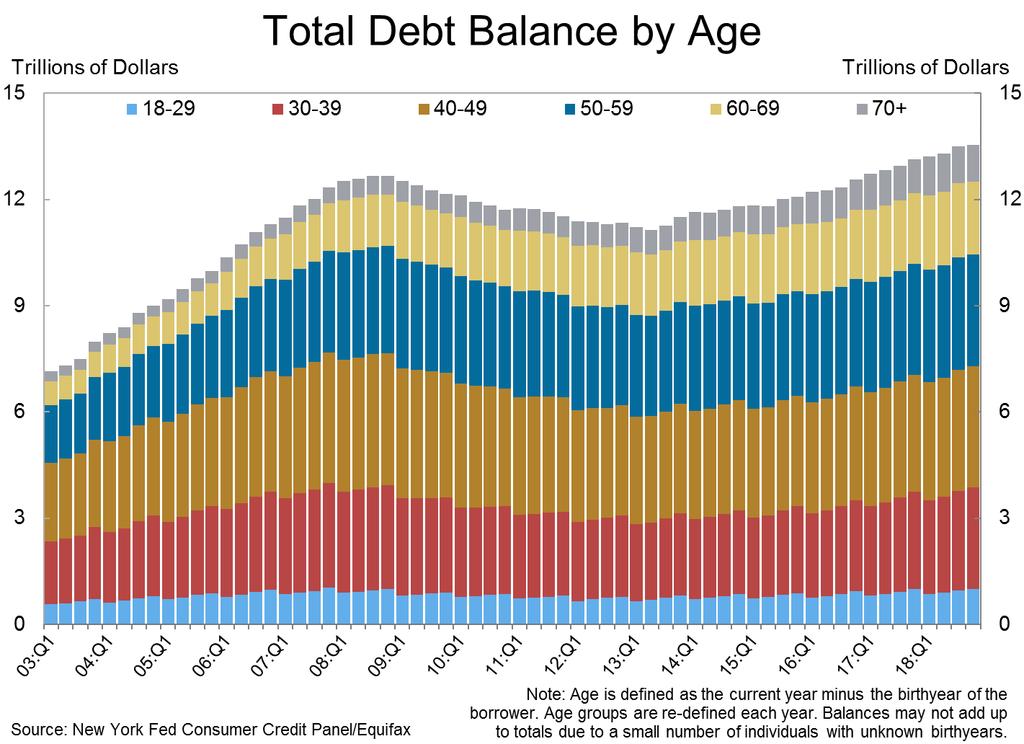

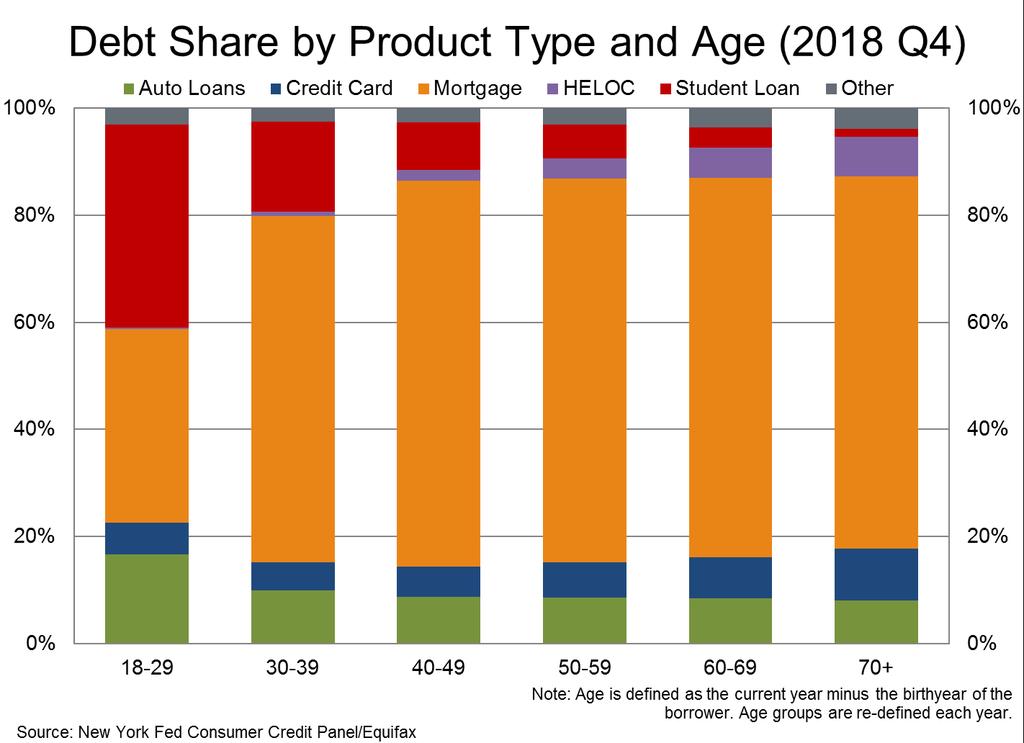

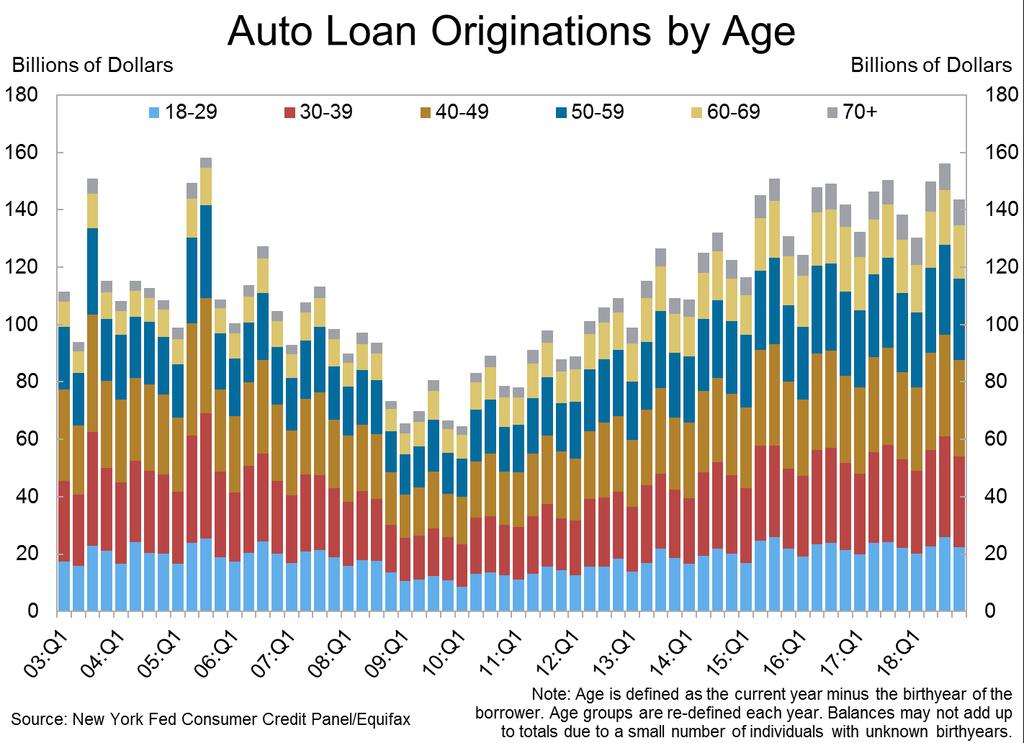

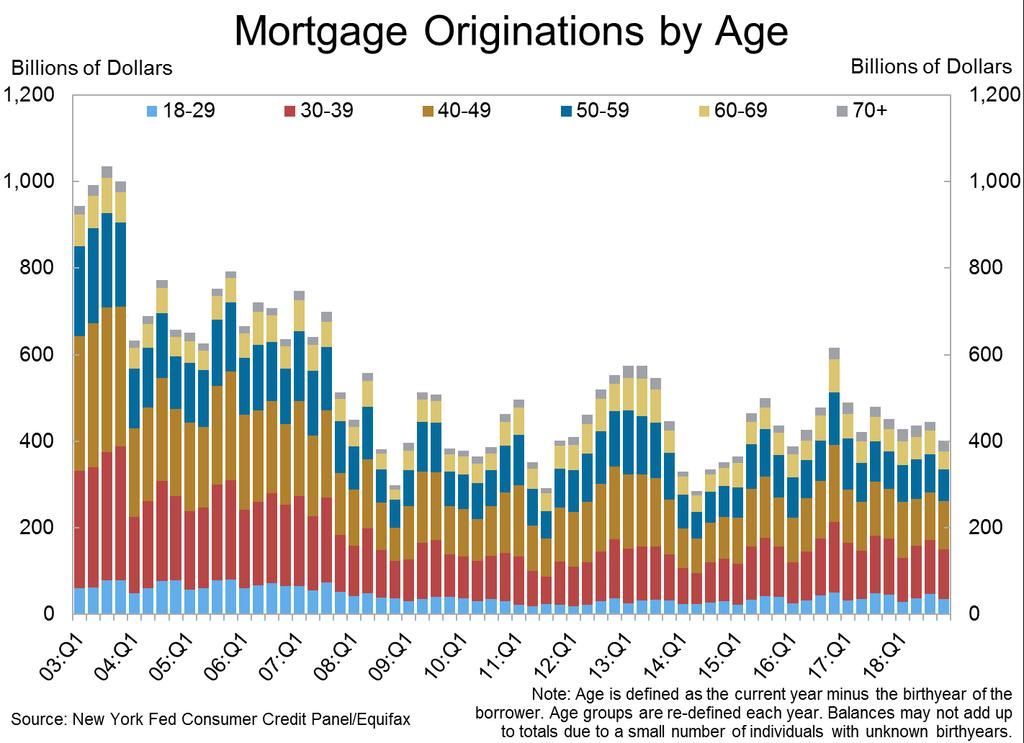

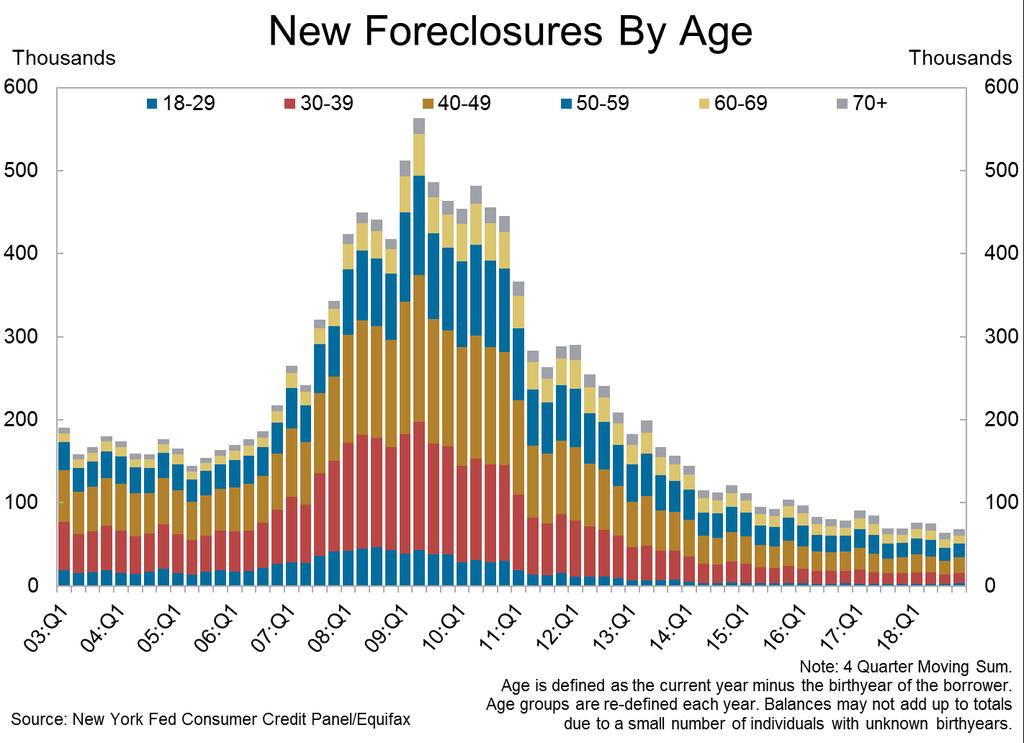

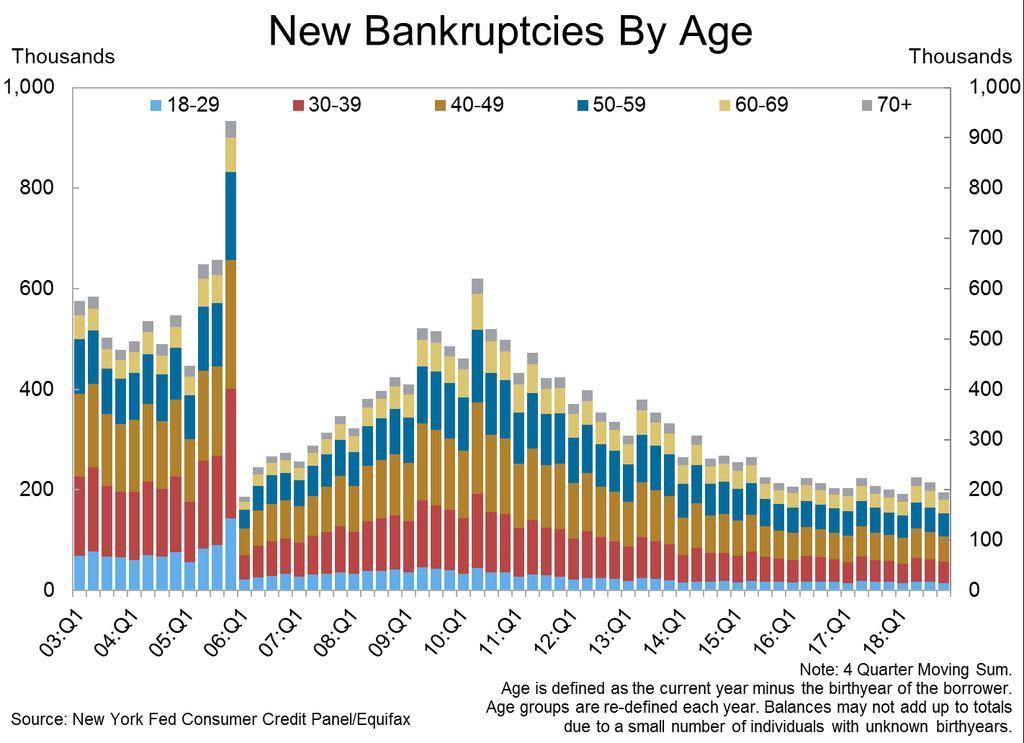

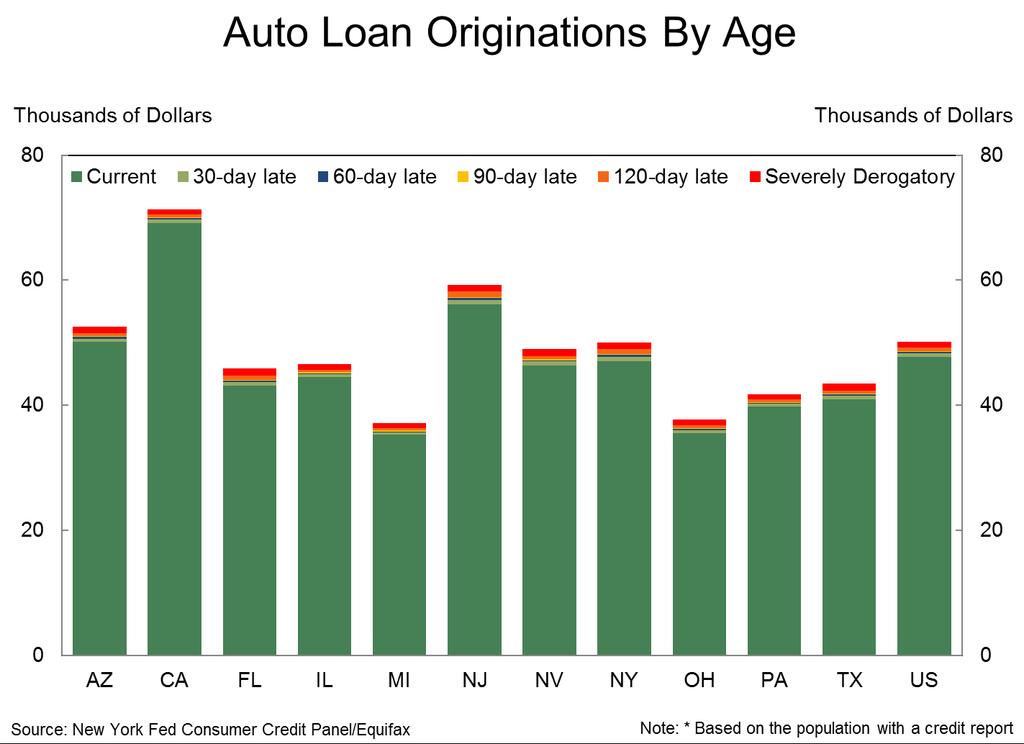

2 Household Debt and Credit Developments in 2018Q4 1 Aggregate household debt balances ticked up in the fourth quarter of 2018 for the 18 th consecutive quarter, and are now $869 billion (6.9%) higher than the previous (2008Q3) peak of $12.68 trillion. As of December 31, 2018, total household indebtedness was $13.54 trillion, a $32 billion (0.2%) increase from the third quarter of Overall household debt is now 21.4% above the 2013Q2 trough. Mortgage balances shown on consumer credit reports on December 31 stood at $9.1 trillion, essentially unchanged from the third quarter of Balances on home equity lines of credit (HELOC) continued their declining trend from 2009 with a drop of $10 billion in the fourth quarter and are now at $412 billion, the lowest level seen in 14 years. Non-housing balances increased by $58 billion in the fourth quarter, with auto loans increasing by $9 billion, credit card balances going up by $26 billion, and student loan balances by $15 billion. The increase in credit card balances is consistent with seasonal patterns but marks the first time credit card balances re-touched the 2008 peak; card balances now stand at $870 billion. New extensions of credit for mortgage and auto loans slowed in the fourth quarter. Mortgage originations, which we measure as appearances of new mortgage balances on consumer credit reports and which include refinanced mortgages, were at $401 billion, a decline from the volume seen in 2018Q3 and the lowest level seen in nearly four years. There were $144 billion in newly originated auto loans in the fourth quarter of 2018, continuing the nine year growth trend in new auto loans. Auto loan originations totaled $584 billion in 2018, the highest year in the 19-year history of the data for auto loan originations (in nominal terms) and an increase from 2017 s $567 billion. The aggregate credit card limit rose for the 24th consecutive quarter, with a 1.5% increase. The median credit score of newly originating borrowers was mostly unchanged; the median credit score among newly originating mortgage borrowers was 758, as mortgage underwriting standards remain tight. Only 10% of newly originated mortgages were to borrowers with credit scores under 660, compared to 31% of new auto loans in that category. For auto loan originators, the credit score distribution was flat, and individuals with subprime scores received a substantial share of newly originated auto loans. Aggregate delinquency rates remained steady in the fourth quarter of As of December 31, 4.7% of outstanding debt was in some stage of delinquency, unchanged from the third quarter. Of the $630 billion of debt that is delinquent, $416 billion is seriously delinquent (at least 90 days late or severely derogatory ). The flow into 90+ day delinquency for credit card balances has been rising since 2017, while the flow into 90+ day delinquency for auto loan balances has been slowly trending upward since About 195,000 consumers had a bankruptcy notation added to their credit reports in 2018Q4, five thousand fewer than the 200,000 individuals who filed in the 4 th quarter of New bankruptcy notations have been at historically low levels since Housing Debt There was $401 billion in newly originated mortgage debt in 2018Q4. Mortgage delinquencies were flat again, with 1.1% of mortgage balances 90 or more days delinquent in 2018Q3. Delinquency transition rates were mixed, with about 1.0% of current balances transitioning to delinquency. Transitions from early delinquency were flat, as 14.8% of mortgages in early delinquency (30-60 days late) transitioned to 90+ days delinquent. The share of mortgages in early delinquency that cured was 35.1%. Transitions into serious delinquency for credit card accounts increased again. While this rate is highest for younger borrowers, it has risen sharply among older borrowers over the last two years. About 68,000 individuals had a new foreclosure notation added to their credit reports between October 1 and December 31, up slightly the previous quarter. Foreclosures remain very low by historical standards. Student Loans Outstanding student loan debt stood at 1.46 trillion in the fourth quarter, up $15 billion. 11.4% of aggregate student debt was 90+ days delinquent or in default in 2018Q4, a small improvement from the jump seen in the third quarter of Transition rates into delinquency were unchanged. Account Closings, Credit Inquiries and Collection Accounts The number of credit inquiries within the past six months an indicator of consumer credit demand declined to the lowest level seen in the history of the data. Account closings were at their highest level since This report is based on the New York Fed Consumer Credit Panel, which is constructed from a nationally representative random sample drawn from Equifax credit report data. For details on the data set and the measures reported here, see the data dictionary available at the end of this report. Please contact Joelle Scally with questions at joelle.scally@ny.frb.org. 2 As explained in a 2012 report, delinquency rates for student loans are likely to understate effective delinquency rates because about half of these loans are currently in deferment, in grace periods or in forbearance and therefore temporarily not in the repayment cycle. This implies that among loans in the repayment cycle delinquency rates are roughly twice as high.

3 Page Left Blank Intentionally 1

4 NATIONAL CHARTS 2

5 3

6 4

7 5

8 6

9 7

10 8

11 9

12 10

13 11

14 12

15 13

16 14

17 15

18 16

19 17

20 18

21 SELECT CHARTS BY AGE 19

22 20

23 21

24 22

25 23

26 24

27 25

28 26

29 27

30 28

31 29

32 30

33 CHARTS BY SELECT STATE 31

34 32

35 33

36 34

37 35

38 36

39 37

40 38

41 39

42 40

43 Data Dictionary The FRBNY Consumer Credit Panel consists of detailed Equifax credit-report data for a unique longitudinal quarterly panel of individuals and households from 1999 to The panel is a nationally representative 5% random sample of all individuals with a social security number and a credit report (usually aged 19 and over). We also sampled all other individuals living at the same address as the primary sample members, allowing us to track household-level credit and debt for a random sample of US households. The resulting database includes approximately 44 million individuals in each quarter. More details regarding the sample design can be found in Lee and van der Klaauw (2010). 2 A comprehensive overview of the specific content of consumer credit reports is provided in Avery, Calem, Canner and Bostic (2003). 3 The credit report data in our panel primarily includes information on accounts that have been reported by the creditor within 3 months of the date that the credit records were drawn each quarter. Thus, accounts that are not currently reported on are excluded. Such accounts may be closed accounts with zero balances, dormant or inactive accounts with no balance, or accounts that when last reported had a positive balance. The latter accounts include accounts that were either subsequently sold, transferred, or paid off as well as accounts, particularly derogatory accounts, that are still outstanding but on which the lender has ceased reporting. According to Avery et al (2003), the latter group of noncurrently reporting accounts, with positive balances when last reported, accounted for approximately 8% of all credit accounts in their sample. For the vast majority of these accounts, and particularly for mortgage and installment loans, additional analysis suggested they had been closed (with zero balance) or transferred. 4 Our exclusion of the latter accounts is comparable to some stale account rules used by credit reporting companies, which treat noncurrently reporting revolving and nonrevolving accounts with positive balances as closed and with zero balance. All figures shown in the tables and graphs are based on the 5% random sample of individuals. To reduce processing costs, we drew a 2% random subsample of these individuals, meaning that the results presented here are for a 0.1% random sample of individuals with credit reports, or approximately 267,000 individuals as of Q In computing several of these statistics, account was taken of the joint or individual nature of various loan accounts. For example, to minimize biases due to double counting, in computing individual-level total balances, 50% of the balance associated with each joint account was attributed to that individual. Per-capita figures are computed by dividing totals for our sample by the total number of people in our sample, so these figures apply to the population of individuals who have a credit report. In comparing aggregate measures of household debt presented in this report to those included in the Board of Governor s Flow Of Funds (FoF) Accounts, there are several important considerations. First, among the different components included in the FoF household debt measure (which also includes debt of nonprofit organizations), our measures are directly comparable to two of its components: home mortgage debt and consumer credit. Total mortgage debt and non-mortgage debt in the third quarter of 2009 were respectively $9.7 and $2.6 trillion, while the comparable amounts in the FoF for the same quarter were 1 Note that reported aggregates, especially in , may reflect some delays in the reporting of student loans by servicers to credit bureaus which could lead to some undercounting of student loan balances. Quarterly data prior to Q1 2003, excluding student loans, will remain available on the Household Credit webpage. 2 Lee, D. and W. van der Klaauw, An introduction to the FRBNY Consumer Credit Panel, [2010]. 3 Avery, R.B., P.S. Calem, G.B. Canner and R.W. Bostic, An Overview of Consumer Data and Credit Reporting, Federal Reserve Bulletin, Feb. 2003, pp Avery et al (2003) found that for many nonreported mortgage accounts a new mortgage account appeared around the time the account stopped being reported, suggesting a refinance or that the servicing was sold. Most revolving and open non-revolving accounts with a positive balance require monthly payments if they remain open, suggesting the accounts had been closed. Noncurrently reporting derogatory accounts can remain unchanged and not requiring updating for a long time when the borrower has stopped paying and the creditor may have stopped trying to collect on the account. Avery et al report that some of these accounts appeared to have been paid off. 5 Due to relatively low occurrence rates we used the full 5% sample for the computation of new foreclosure and bankruptcy rates. Additionally, to capture and account for servicer discrepancies, we used the 1% sample for student loan data. For all other graphs, we found the 0.1% sample to provide a very close representation of the 5% sample.

44 $10.3 and $2.5 trillion, respectively. 6 Second, a detailed accounting for the remaining differences between the debt measures from both data sources will require a more detailed breakdown and documentation of the computation of the FoF measures. 7 Loan types. In our analysis we distinguish between the following types of accounts: mortgage accounts, home equity revolving accounts, auto loans, bank card accounts, student loans and other loan accounts. Mortgage accounts include all mortgage installment loans, including first mortgages and home equity installment loans (HEL), both of which are closed-end loans. Home Equity Revolving accounts (aka Home Equity Line of Credit or HELOC), unlike home equity installment loans, are home equity loans with a revolving line of credit where the borrower can choose when and how often to borrow up to an updated credit limit. Auto Loans are loans taken out to purchase a car, including Auto Bank loans provided by banking institutions (banks, credit unions, savings and loan associations), and Auto Finance loans, provided by automobile dealers and automobile financing companies. Bankcard accounts (or credit card accounts) are revolving accounts for banks, bankcard companies, national credit card companies, credit unions and savings & loan associations. Student Loans include loans to finance educational expenses provided by banks, credit unions and other financial institutions as well as federal and state governments. The Other category includes Consumer Finance (sales financing, personal loans) and Retail (clothing, grocery, department stores, home furnishings, gas etc) loans. Our analysis excludes authorized user trades, disputed trades, lost/stolen trades, medical trades, child/family support trades, commercial trades and, as discussed above, inactive trades (accounts not reported on within the last 3 months). Total debt balance. Total balance across all accounts, excluding those in bankruptcy. Number of open, new and closed accounts. Total number of open accounts, number of accounts opened within the last 12 months. Number of closed accounts is defined as the difference between the number of open accounts 12 months ago plus the number of accounts opened within the last 12 months, minus the total number of open accounts at the current date. Inquiries. Number of credit-related consumer-initiated inquiries reported to the credit reporting agency in the past 6 months. Only hard pulls are included, which are voluntary inquiries generated when a consumer authorizes lenders to request a copy of their credit report. It excludes inquiries made by creditors about existing accounts (for example to determine whether they want to send the customer pre-approved credit applications or to verify the accuracy of customer-provided information) and inquiries made by consumers themselves. Note that inquiries are credit reporting company specific and not all inquiries associated with credit activities are reported to each credit reporting agency. Moreover, the reporting practices for the credit reporting companies may have changed during the period of analysis. High credit and balance for credit cards. Total amount of high credit on all credit cards held by the consumer. High credit is either the credit limit, or highest balance ever reported during history of this loan. As reported by Avery et al (2003) the use of the highest-balance measure for credit limits on accounts in which limits are not reported likely understates the actual credit limits available on those accounts. High credit and balance for HE Revolving. Same as for credit cards, but now applied to HELOCs. Credit utilization rates (for revolving accounts). Computed as proportion of available credit in use (outstanding balance divided by credit limit), and for reasons discussed above are likely to overestimate actual credit utilization. 6 Flow of Funds Accounts of the United States, Flows and Outstandings, Third Quarter 2009, Board of Governors, Table L Our debt totals exclude debt held by individuals without social security numbers. Additional information suggests that total debt held by such individuals is relatively small and accounts for little of the difference.

45 Delinquency status. Varies between current (paid as agreed), 30-day late (between 30 and 59 day late; not more than 2 payments past due), 60-day late (between 60 and 89 days late; not more than 3 payments past due), 90-day late (between 90 and 119 days late; not more than 4 payments past due), 120-day late (at least 120 days past due; 5 or more payments past due) or collections, and severely derogatory (any of the previous states combined with reports of a repossession, charge off to bad debt or foreclosure). Not all creditors provide updated information on payment status, especially after accounts have been derogatory for a longer period of time. Thus the payment performance profiles obtained from our data may to some extent reflect reporting practices of creditors. Percent of balance 90+ days late. Percent of balance that is either 90-day late, 120-day late or severely derogatory. 90+ days late is synonymous to seriously delinquent. New foreclosures. Number of individuals with foreclosures first appearing on their credit report during the past 3 months. Based on foreclosure information provided by lenders (account level foreclosure information) as well as through public records. Note that since borrowers may have multiple real estate loans, this measure is conceptually different from foreclosure rates often reported in the press. For example, a borrower with a mortgage currently in foreclosure would not be counted here if he receives a foreclosure notice on an additional mortgage account. In the case of joint mortgages, both borrowers reports indicate the presence of a foreclosure notice in the last 3 months, and both are counted here. New bankruptcies. New bankruptcies first reported during the past 3 months. Based on bankruptcy information provided by lenders (account level bankruptcy information) as well as through public records. Collections. Number and amount of 3 rd party collections (i.e. collections not being handled by original creditor) on file within the last 12 months. Includes both public record and account level 3 rd party collections information. As reported by Avery et al (2003), only a small proportion of collections are related to credit accounts with the majority of collection actions being associated with medical bills and utility bills. Consumer Credit Score. Credit score is the Equifax Risk Score 3.0. It was developed by Equifax and predicts the likelihood of a consumer becoming seriously delinquent (90+ days past due). The score ranges from , with a higher score being viewed as a better risk than someone with a lower score. New (seriously) delinquent balances and transition rates. New (seriously) delinquent balance reported in each loan category. For mortgages, this is based on the balance of each account at the time it enters (serious) delinquency, while for other loan types it is based on the net increase in the aggregate (seriously) delinquent balance for all accounts of that loan type belonging to an individual. Transition rates. The transition rate is the new (seriously) delinquent balance, expressed as a percent of the previous quarter s balance that was not (seriously) delinquent. Newly originated installment loan balances. We calculate the balance on newly originated mortgage loans as they first appear on an individual s credit report. For auto loans we compare the total balance and number of accounts on an individual credit report in consecutive quarters. New auto loan originations are then defined as increases in the balance accompanied by increases in the number of accounts reported. Cover photo credits clockwise from top right: Andrew Love/flickr.com, The Truth About /flickr.com, Casey Serin/flickr.com, Microsoft.com Federal Reserve Bank of New York. Equifax is a registered trademark of Equifax Inc. All rights reserved.

CENTER FOR MICROECONOMIC DATA

CENTER FOR MICROECONOMIC DATA WWW.NEWYORKFED.ORG/MICROECONOMICS QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT 2018:Q1 (RELEASED MAY 2018 ) FEDERAL RESERVE BANK of NEW YORK RESEARCH AND STATISTICS GROUP

CENTER FOR MICROECONOMIC DATA WWW.NEWYORKFED.ORG/MICROECONOMICS QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT 2018:Q1 (RELEASED MAY 2018 ) FEDERAL RESERVE BANK of NEW YORK RESEARCH AND STATISTICS GROUP

HOUSEHOLD DEBT AND CREDIT

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS GROUP MICROECONOMIC STUDIES FRBNY Analysis Based on FRBNY Consumer Credit Panel / Equifax Data Household

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS GROUP MICROECONOMIC STUDIES FRBNY Analysis Based on FRBNY Consumer Credit Panel / Equifax Data Household

HOUSEHOLD DEBT AND CREDIT

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS GROUP MICROECONOMIC STUDIES Household Debt and Credit Developments in 2015Q2 1 Aggregate household

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS GROUP MICROECONOMIC STUDIES Household Debt and Credit Developments in 2015Q2 1 Aggregate household

HOUSEHOLD DEBT AND CREDIT

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS GROUP MICROECONOMIC STUDIES Household Debt and Credit Developments in 212 Q4 1 Aggregate consumer

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS GROUP MICROECONOMIC STUDIES Household Debt and Credit Developments in 212 Q4 1 Aggregate consumer

HOUSEHOLD DEBT AND CREDIT

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT November 212 FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS GROUP MICROECONOMIC STUDIES Household Debt and Credit Developments in 212 Q3 1 Aggregate

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT November 212 FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS GROUP MICROECONOMIC STUDIES Household Debt and Credit Developments in 212 Q3 1 Aggregate

HOUSEHOLD DEBT AND CREDIT

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT November 21 FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS MICROECONOMIC AND REGIONAL STUDIES Household Debt and Credit Developments in 21Q3 1 Aggregate

QUARTERLY REPORT ON HOUSEHOLD DEBT AND CREDIT November 21 FEDERAL RESERVE BANK OF NEW YORK RESEARCH AND STATISTICS MICROECONOMIC AND REGIONAL STUDIES Household Debt and Credit Developments in 21Q3 1 Aggregate

PRELIMINARY AND INCOMPLETE: PLEASE DO NOT CITE WITHOUT PERMISSION

PRELIMINARY AND INCOMPLETE: PLEASE DO NOT CITE WITHOUT PERMISSION The Financial Crisis at the Kitchen Table: Recent Trends in Household Debt and Credit By Meta Brown, Andrew Haughwout, Donghoon Lee and

PRELIMINARY AND INCOMPLETE: PLEASE DO NOT CITE WITHOUT PERMISSION The Financial Crisis at the Kitchen Table: Recent Trends in Household Debt and Credit By Meta Brown, Andrew Haughwout, Donghoon Lee and

Consumer Credit Conditions June 2016

Consumer Credit Conditions June Prepared by the Federal Reserve Bank of Dallas Community Development Consumer Credit Conditions, June : Auto and Retail Loans Blemish Improved Delinquency Report The Consumer

Consumer Credit Conditions June Prepared by the Federal Reserve Bank of Dallas Community Development Consumer Credit Conditions, June : Auto and Retail Loans Blemish Improved Delinquency Report The Consumer

Student Loan Borrowing and Repayment Trends, 2015 Cleveland Fed 2015 Policy Summit

Student Loan Borrowing and Repayment Trends, 2015 Cleveland Fed 2015 Policy Summit June 18, 2015 Andrew Haughwout, Research Group The views presented here are those of the authors and do not necessarily

Student Loan Borrowing and Repayment Trends, 2015 Cleveland Fed 2015 Policy Summit June 18, 2015 Andrew Haughwout, Research Group The views presented here are those of the authors and do not necessarily

Debt. Consumer Debt Rises for 10th Quarter in a Row. Introduction This is the inaugural edition of the full

VOL. 1, ISSUE 1, COVERING 16:Q1 Debt Consumer Debt Rises for 1th Quarter in a Row By Don E. Schlagenhauf and Lowell R. Ricketts Introduction This is the inaugural edition of the full Quarterly Debt Monitor,

VOL. 1, ISSUE 1, COVERING 16:Q1 Debt Consumer Debt Rises for 1th Quarter in a Row By Don E. Schlagenhauf and Lowell R. Ricketts Introduction This is the inaugural edition of the full Quarterly Debt Monitor,

enth istrict onsumer redit eport

enth istrict onsumer redit eport September 3rd Quarter 20140 Federal Reserve Bank of of Kansas City ummary Tenth District average consumer debt, which for this report includes all outstanding debt other

enth istrict onsumer redit eport September 3rd Quarter 20140 Federal Reserve Bank of of Kansas City ummary Tenth District average consumer debt, which for this report includes all outstanding debt other

Quarterly U.S. Consumer Credit Trends DATA AS OF DECEMBER 2017

Quarterly U.S. Consumer Credit Trends DATA AS OF DECEMBER 2017 March 2, 2018 Quarterly U.S. Consumer Credit Trends Data as of December 2017 Published February 10, 2018 Visit us at www.equifax.com/business/credit-trends

Quarterly U.S. Consumer Credit Trends DATA AS OF DECEMBER 2017 March 2, 2018 Quarterly U.S. Consumer Credit Trends Data as of December 2017 Published February 10, 2018 Visit us at www.equifax.com/business/credit-trends

Understanding Your FICO Score. Understanding FICO Scores

Understanding Your FICO Score Understanding FICO Scores 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Reports

Understanding Your FICO Score Understanding FICO Scores 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Reports

MORTGAGE AND CONSUMER CREDIT TRENDS National Report Q2 2018

HOUSING INDICATORS AND ANALYTICS MORTGAGE AND CONSUMER CREDIT TRENDS National Report Q2 2018 C A N A D A M O R T G A G E A N D H O U S I N G C O R P O R A T I O N December 2018 Executive summary The year-over-year

HOUSING INDICATORS AND ANALYTICS MORTGAGE AND CONSUMER CREDIT TRENDS National Report Q2 2018 C A N A D A M O R T G A G E A N D H O U S I N G C O R P O R A T I O N December 2018 Executive summary The year-over-year

Is Growing Student Loan Debt Impacting Credit Risk?

Is Growing Student Loan Debt Impacting Credit Risk? New research shows that student loan debt has increased dramatically and student loans are riskier than before Number 65 January 2013 As US students

Is Growing Student Loan Debt Impacting Credit Risk? New research shows that student loan debt has increased dramatically and student loans are riskier than before Number 65 January 2013 As US students

The Concentration of Financial Disadvantage: Debt Conditions and Credit Report Data in Massachusetts Cities and Boston Neighborhoods

Regional & Community Outreach Issue Brief 2018-2 June 27, 2018 The Concentration of Financial Disadvantage: Debt Conditions and Credit Report Data in Massachusetts Cities and Boston Neighborhoods Anmol

Regional & Community Outreach Issue Brief 2018-2 June 27, 2018 The Concentration of Financial Disadvantage: Debt Conditions and Credit Report Data in Massachusetts Cities and Boston Neighborhoods Anmol

CFPB Data Point: Becoming Credit Visible

June 2017 CFPB Data Point: Becoming Credit Visible The CFPB Office of Research p Kenneth P. Brevoort p Michelle Kambara This is another in an occasional series of publications from the Consumer Financial

June 2017 CFPB Data Point: Becoming Credit Visible The CFPB Office of Research p Kenneth P. Brevoort p Michelle Kambara This is another in an occasional series of publications from the Consumer Financial

WHOLESALE LENDING AT-A-GLANCE CREDIT

DESCRIPTION STANDARD A borrower s creditworthiness is based on past and present credit history. The credit history must demonstrate the borrower s ability and willingness to handle financial obligations.

DESCRIPTION STANDARD A borrower s creditworthiness is based on past and present credit history. The credit history must demonstrate the borrower s ability and willingness to handle financial obligations.

5/16/2006 1 of 18 Report for CHRISTINE BAKER on April 30, 2006 Click here to return. 742 CHRISTINE BAKER April 30, 2006 Credit record source: Equifax Your FICO score of 742 summarizes the information on

5/16/2006 1 of 18 Report for CHRISTINE BAKER on April 30, 2006 Click here to return. 742 CHRISTINE BAKER April 30, 2006 Credit record source: Equifax Your FICO score of 742 summarizes the information on

Consumer Instalment Credit Expansion

Consumer Instalment Credit Expansion EXPANSION OF instalment credit reached a high in the summer of 1959, and then moderated in the fourth quarter. In early 1960 expansion increased, but at a slower rate

Consumer Instalment Credit Expansion EXPANSION OF instalment credit reached a high in the summer of 1959, and then moderated in the fourth quarter. In early 1960 expansion increased, but at a slower rate

When household incomes are not sufficient to. Economic Edge Lower Debt Benefits Borrowers and Businesses. The Takeaway.

Economic Edge Lower Debt Benefits Borrowers and Businesses Ali Anari February 27, 217 Publication 216 When household incomes are not sufficient to pay cash for big-ticket items such as homes and cars,

Economic Edge Lower Debt Benefits Borrowers and Businesses Ali Anari February 27, 217 Publication 216 When household incomes are not sufficient to pay cash for big-ticket items such as homes and cars,

A Guide to Your Credit Report

Sample for demonstration purposes only. All data is fictitious. A Guide to Your Credit Report John Sample January 20, 2018 Please Note: This packet is provided as is and is meant to give insights into

Sample for demonstration purposes only. All data is fictitious. A Guide to Your Credit Report John Sample January 20, 2018 Please Note: This packet is provided as is and is meant to give insights into

Trends in Household Debt and Credit

Federal Reserve Bank of New York Staff Reports Trends in Household Debt and Credit Andrew Haughwout Donghoon Lee Joelle Scally Lauren Thomas Wilbert van der Klaauw Staff Report No. 882 March 2019 This

Federal Reserve Bank of New York Staff Reports Trends in Household Debt and Credit Andrew Haughwout Donghoon Lee Joelle Scally Lauren Thomas Wilbert van der Klaauw Staff Report No. 882 March 2019 This

Reviewing C YouR CRedit RepoRt

ChapteR 2 Reviewing C YouR CRedit RepoRt What do your creditors have to say about the way you handle money? Having a good credit score can help you turn your home-buying dream into a reality. There s much

ChapteR 2 Reviewing C YouR CRedit RepoRt What do your creditors have to say about the way you handle money? Having a good credit score can help you turn your home-buying dream into a reality. There s much

OCC and OTS Mortgage Metrics Report Disclosure of National Bank and Federal Thrift Mortgage Loan Data

OCC and OTS Mortgage Metrics Report Disclosure of National Bank and Federal Thrift Mortgage Loan Data January June 2008 Office of the Comptroller of the Currency Office of Thrift Supervision Washington,

OCC and OTS Mortgage Metrics Report Disclosure of National Bank and Federal Thrift Mortgage Loan Data January June 2008 Office of the Comptroller of the Currency Office of Thrift Supervision Washington,

How to Stay Relevant in a Disruptive Lending Environment

How to Stay Relevant in a Disruptive Lending Environment Don Arkell CU Lending Advice Friday, June 10, 2016 2:15 p.m. Lending Attitude Check The best lenders learn that lending is both an attitude and

How to Stay Relevant in a Disruptive Lending Environment Don Arkell CU Lending Advice Friday, June 10, 2016 2:15 p.m. Lending Attitude Check The best lenders learn that lending is both an attitude and

Your Credit Score What It Means to You as a Prospective Home Buyer

Rachel Prevost Mortgage Loan Consultant L&G Mortgage Banc BK51263 Phone: (512) 924-3663 Fax: (480) 907-2839 rprevost@lgmortgagebanc.com www.lgmortgagebanc.com Your Credit Score What It Means to You as

Rachel Prevost Mortgage Loan Consultant L&G Mortgage Banc BK51263 Phone: (512) 924-3663 Fax: (480) 907-2839 rprevost@lgmortgagebanc.com www.lgmortgagebanc.com Your Credit Score What It Means to You as

2/10/2015 CREDIT FOR SUCCESS TODAY S NEW RISK FACTORS MOBILE BANKING. The new Consumer Financial Protection Act, the ATR Rule (Ability to Repay Rule)

") CREDIT FOR SUCCESS TODAY S NEW RISK FACTORS Written and Presented by Serge Bevil, Credit Specialist VantagePoint Credit Corp. MOBILE BANKING We have become a social media society that wants information,

CREDIT FOR SUCCESS TODAY S NEW RISK FACTORS Written and Presented by Serge Bevil, Credit Specialist VantagePoint Credit Corp. MOBILE BANKING We have become a social media society that wants information,

GREENPATH FINANCIAL WELLNESS SERIES

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Empowering people to lead financially healthy lives. TABLE OF CONTENTS Understanding credit reports...2 What s in a credit

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Empowering people to lead financially healthy lives. TABLE OF CONTENTS Understanding credit reports...2 What s in a credit

CONSUMER CREDIT STARTER GUIDE

Atlantic Bay Mortgage Group CONSUMER CREDIT STARTER GUIDE Atlantic Bay Mortgage Group s Consumer Guide To Credit Scores & Home Financing Atlantic Bay Mortgage Is A Mortgage Lender Where The Genuine Care

Atlantic Bay Mortgage Group CONSUMER CREDIT STARTER GUIDE Atlantic Bay Mortgage Group s Consumer Guide To Credit Scores & Home Financing Atlantic Bay Mortgage Is A Mortgage Lender Where The Genuine Care

You re a Mean One, Mr. Grinch

You re a Mean One, Mr. Grinch Debt Is Haunting the American Consumer and Harming the Economy Christian E. Weller Senior Fellow Amanda Logan Special Assistant for Economic Policy Center for American Progress

You re a Mean One, Mr. Grinch Debt Is Haunting the American Consumer and Harming the Economy Christian E. Weller Senior Fellow Amanda Logan Special Assistant for Economic Policy Center for American Progress

The Bubble, the Burst and Now What Happened to the Consumer? Joe Mellman Vice President, Financial Services TransUnion

The Bubble, the Burst and Now What Happened to the Consumer? Joe Mellman Vice President, Financial Services TransUnion How did the financial crisis affect consumers and how have they fared since? 1 2 3

The Bubble, the Burst and Now What Happened to the Consumer? Joe Mellman Vice President, Financial Services TransUnion How did the financial crisis affect consumers and how have they fared since? 1 2 3

Ivan Gjaja (212) Natalia Nekipelova (212)

Natalia Nekipelova (212)") Ivan Gjaja (212) 816-8320 ivan.m.gjaja@ssmb.com Natalia Nekipelova (212) 816-8075 natalia.nekipelova@ssmb.com In a departure from seasonal patterns, January speeds were 1% CPR higher than December speeds.

Ivan Gjaja (212) 816-8320 ivan.m.gjaja@ssmb.com Natalia Nekipelova (212) 816-8075 natalia.nekipelova@ssmb.com In a departure from seasonal patterns, January speeds were 1% CPR higher than December speeds.

Understanding. What you need to know about the most widely used credit scores

Understanding What you need to know about the most widely used credit scores 300 850 The score lenders use. FICO Scores are the most widely used credit scores according to a recent CEB TowerGroup analyst

Understanding What you need to know about the most widely used credit scores 300 850 The score lenders use. FICO Scores are the most widely used credit scores according to a recent CEB TowerGroup analyst

Using alternative data, millions more consumers qualify for credit and go on to improve their credit standing

NO. 89 90 New FICO research shows how to score millions more creditworthy consumers Using alternative data, millions more consumers qualify for credit and go on to improve their credit standing Widespread

NO. 89 90 New FICO research shows how to score millions more creditworthy consumers Using alternative data, millions more consumers qualify for credit and go on to improve their credit standing Widespread

Understanding Credit. What it is, why it s important, and how you can maintain it. Brought to you by Sallie Mae and FICO

Understanding Credit What it is, why it s important, and how you can maintain it Brought to you by Sallie Mae and FICO Introduction A student loan may be your first major credit experience. This is a good

Understanding Credit What it is, why it s important, and how you can maintain it Brought to you by Sallie Mae and FICO Introduction A student loan may be your first major credit experience. This is a good

Greek household indebtedness and financial stress: results from household survey data

Greek household indebtedness and financial stress: results from household survey data George T Simigiannis and Panagiota Tzamourani 1 1. Introduction During the three-year period 2003-2005, bank loans

Greek household indebtedness and financial stress: results from household survey data George T Simigiannis and Panagiota Tzamourani 1 1. Introduction During the three-year period 2003-2005, bank loans

The Office of Economic Policy HOUSING DASHBOARD. March 16, 2016

The Office of Economic Policy HOUSING DASHBOARD March 16, 216 Recent housing market indicators suggest that housing activity continues to strengthen. Solid residential investment in 215Q4 contributed.3

The Office of Economic Policy HOUSING DASHBOARD March 16, 216 Recent housing market indicators suggest that housing activity continues to strengthen. Solid residential investment in 215Q4 contributed.3

How Are Credit Line Decreases Impacting Consumer Credit Risk?

How Are Credit Line Decreases Impacting Consumer Credit Risk? As lenders reduce or close credit lines to mitigate exposure, new research explores its impact on FICO scores Number 22 August 2009 With recent

How Are Credit Line Decreases Impacting Consumer Credit Risk? As lenders reduce or close credit lines to mitigate exposure, new research explores its impact on FICO scores Number 22 August 2009 With recent

TABLE OF CONTENTS. Healthier Black Elders Center

TABLE OF CONTENTS What is credit............................................1 The five C s of credit...................................... 2 Types of credit...........................................3

TABLE OF CONTENTS What is credit............................................1 The five C s of credit...................................... 2 Types of credit...........................................3

Federal Reserve Bank of Philadelphia

Federal Reserve Bank of Philadelphia 1 When you apply for credit, whether it s a credit card, car loan, or a mortgage, lenders want to know whether you are likely to repay your loan and make the payments

Federal Reserve Bank of Philadelphia 1 When you apply for credit, whether it s a credit card, car loan, or a mortgage, lenders want to know whether you are likely to repay your loan and make the payments

A LOOK BEHIND THE NUMBERS

KEY FINDINGS A LOOK BEHIND THE NUMBERS Home Lending in Cuyahoga County Neighborhoods Lisa Nelson Community Development Advisor Federal Reserve Bank of Cleveland Prior to the Great Recession, home mortgage

KEY FINDINGS A LOOK BEHIND THE NUMBERS Home Lending in Cuyahoga County Neighborhoods Lisa Nelson Community Development Advisor Federal Reserve Bank of Cleveland Prior to the Great Recession, home mortgage

Creditworthiness (UXL)

") Creditworthiness (UXL) Since so much debt is unsecured, it is important for companies to have information on how well their potential borrowers handle money in order to assess their creditworthiness, or

Creditworthiness (UXL) Since so much debt is unsecured, it is important for companies to have information on how well their potential borrowers handle money in order to assess their creditworthiness, or

TIP: Make sure this information is correct. A wrong address or phone number could be a mistake or a sign of identity theft.

Reading a Sample Credit Report This sample report shows what kind of information might appear on your own credit report, also called a consumer disclosure statement, from the 3 major Credit Reporting Agencies

Reading a Sample Credit Report This sample report shows what kind of information might appear on your own credit report, also called a consumer disclosure statement, from the 3 major Credit Reporting Agencies

Your Credit Score 35% 10%

Your Credit Score A credit score is a complex mathematical model that evaluates many types of information in a credit file and displays the results as a number that reflects your credit risk level, typically

Your Credit Score A credit score is a complex mathematical model that evaluates many types of information in a credit file and displays the results as a number that reflects your credit risk level, typically

National Housing Market Summary

1st 2017 June 2017 HUD PD&R National Housing Market Summary The Housing Market Recovery Showed Progress in the First The housing market improved in the first quarter of 2017. Construction starts rose for

1st 2017 June 2017 HUD PD&R National Housing Market Summary The Housing Market Recovery Showed Progress in the First The housing market improved in the first quarter of 2017. Construction starts rose for

CREDIT SCORE USER GUIDE

Page 1 of 11 ABOUT EQUIFAX Equifax empowers businesses and consumers with information they can trust. A global leader in information solutions, we leverage one of the largest sources of consumer and commercial

Page 1 of 11 ABOUT EQUIFAX Equifax empowers businesses and consumers with information they can trust. A global leader in information solutions, we leverage one of the largest sources of consumer and commercial

Consumer Credit Data not Supportive of Management Decisions in the U.S. Apartment Industry

Consumer Credit Data not Supportive of Management Decisions in the U.S. Apartment Industry Michael Furick, Assistant Professor of Marketing, Georgia Gwinnett College, USA ABSTRACT Purpose: Credit scoring

Consumer Credit Data not Supportive of Management Decisions in the U.S. Apartment Industry Michael Furick, Assistant Professor of Marketing, Georgia Gwinnett College, USA ABSTRACT Purpose: Credit scoring

TRENDS IN DELINQUENCIES AND FORECLOSURES IN NEVADA

TRENDS IN DELINQUENCIES AND FORECLOSURES IN NEVADA January 2011 Community Development Research Federal Reserve Bank of San Francisco National Trends Even though NBER officially announced the recession

TRENDS IN DELINQUENCIES AND FORECLOSURES IN NEVADA January 2011 Community Development Research Federal Reserve Bank of San Francisco National Trends Even though NBER officially announced the recession

HOUSING OBSERVER. An Examination of Household Indebtedness. Article 2 March 2016

HOUSING OBSERVER 2016 Article 2 March 2016 Table of Contents 1 Overview of Canadians financial health....4 2 Changes in household borrowing....7 3 Looking ahead: implications of the changing composition

HOUSING OBSERVER 2016 Article 2 March 2016 Table of Contents 1 Overview of Canadians financial health....4 2 Changes in household borrowing....7 3 Looking ahead: implications of the changing composition

A new highly predictive FICO Score for an uncertain world

A new highly predictive FICO Score for an uncertain world Lenders gain a 5% 15% predictive boost to manage business and control losses Number 12 January 2009 As delinquency levels increase and consumer

A new highly predictive FICO Score for an uncertain world Lenders gain a 5% 15% predictive boost to manage business and control losses Number 12 January 2009 As delinquency levels increase and consumer

Recent Changes to a Measure of U.S. Household Debt Service

Recent Changes to a Measure of U.S. Household Debt Service Karen Dynan, Kathleen Johnson, and Karen Pence, of the Board s Division of Research and Statistics, prepared this article. David Brown provided

Recent Changes to a Measure of U.S. Household Debt Service Karen Dynan, Kathleen Johnson, and Karen Pence, of the Board s Division of Research and Statistics, prepared this article. David Brown provided

NYFed s Center for Microeconomic Data currently houses two major data collection efforts:

Presentation Outline NYFed s Center for Microeconomic Data currently houses two major data collection efforts: Survey of Consumer Expectations (SCE) NYFed Consumer Credit Panel (CCP) For each: Brief description

Presentation Outline NYFed s Center for Microeconomic Data currently houses two major data collection efforts: Survey of Consumer Expectations (SCE) NYFed Consumer Credit Panel (CCP) For each: Brief description

SOCIAL SECURITY OFFSETS. Improvements to Program Design Could Better Assist Older Student Loan Borrowers with Obtaining Permitted Relief

United States Government Accountability Office Report to Congressional Requesters December 2016 SOCIAL SECURITY OFFSETS Improvements to Program Design Could Better Assist Older Student Loan Borrowers with

United States Government Accountability Office Report to Congressional Requesters December 2016 SOCIAL SECURITY OFFSETS Improvements to Program Design Could Better Assist Older Student Loan Borrowers with

Loan Exit Counseling & Money Management. Wesleyan University May 2017

Loan Exit Counseling & Money Management Wesleyan University May 2017 Important Things to Know Understand your student loan portfolio Know what types of loans you have Know what your loan terms are: interest

Loan Exit Counseling & Money Management Wesleyan University May 2017 Important Things to Know Understand your student loan portfolio Know what types of loans you have Know what your loan terms are: interest

Debt. In the third quarter of 2016, the upward. Consumer Debt Growth Stalls Despite Strong Sectors. Executive Summary

VOL., ISSUE 3, COVERING 6:Q3 Debt Consumer Debt Growth Stalls Despite Strong Sectors By Lowell R. Ricketts and Don E. Schlagenhauf In the third quarter of 6, the upward trend in per capita consumer debt

VOL., ISSUE 3, COVERING 6:Q3 Debt Consumer Debt Growth Stalls Despite Strong Sectors By Lowell R. Ricketts and Don E. Schlagenhauf In the third quarter of 6, the upward trend in per capita consumer debt

Understanding Debt Problems & Solutions

Understanding Debt Problems & Solutions The Debt Landscape 40% of Americans live on 110% of their income Total U.S. household debt = $11.2 trillion Finances are one of the top five causes of divorce Money

Understanding Debt Problems & Solutions The Debt Landscape 40% of Americans live on 110% of their income Total U.S. household debt = $11.2 trillion Finances are one of the top five causes of divorce Money

Credit Card Debt in New York State

Credit Card Debt in New York State OFFICE OF THE NEW YORK STATE COMPTROLLER Thomas P. DiNapoli, State Comptroller MAY 2018 Introduction Credit cards are the most commonly used vehicle for consumer borrowing,

Credit Card Debt in New York State OFFICE OF THE NEW YORK STATE COMPTROLLER Thomas P. DiNapoli, State Comptroller MAY 2018 Introduction Credit cards are the most commonly used vehicle for consumer borrowing,

TRENDS IN DELINQUENCIES AND FORECLOSURES IN ARIZONA

TRENDS IN DELINQUENCIES AND FORECLOSURES IN ARIZONA January 2011 Community Development Research Federal Reserve Bank of San Francisco National Trends Even though NBER officially announced the recession

TRENDS IN DELINQUENCIES AND FORECLOSURES IN ARIZONA January 2011 Community Development Research Federal Reserve Bank of San Francisco National Trends Even though NBER officially announced the recession

ECONOMIC COMMENTARY. Americans Cut Their Debt Yuliya Demyanyk and Matthew Koepke

ECONOMIC COMMENTARY Number 2012-11 August 8, 2012 Americans Cut Their Debt Yuliya Demyanyk and Matthew Koepke The Great Recession brought an end to a 20-year expansion of consumer debt. In its wake is

ECONOMIC COMMENTARY Number 2012-11 August 8, 2012 Americans Cut Their Debt Yuliya Demyanyk and Matthew Koepke The Great Recession brought an end to a 20-year expansion of consumer debt. In its wake is

FICO Score Open Access Consumer Credit Education US Version. Frequently Asked Questions about FICO Scores

FICO Score Open Access Consumer Credit Education US Version Frequently Asked Questions about Scores 2012 Fair Isaac Corporation. All rights reserved. 1 January 01, 2012 Table of Contents About Scores...

FICO Score Open Access Consumer Credit Education US Version Frequently Asked Questions about Scores 2012 Fair Isaac Corporation. All rights reserved. 1 January 01, 2012 Table of Contents About Scores...

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners February 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners February 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research

Quarterly overview of consumer credit trends released by TransUnion CIBIL

TransUnion CIBIL Industry Insights Report Quarterly overview of consumer credit trends released by TransUnion CIBIL FIRST QUARTER 2018 Executive Summary For purposes of this report, retail lending includes

TransUnion CIBIL Industry Insights Report Quarterly overview of consumer credit trends released by TransUnion CIBIL FIRST QUARTER 2018 Executive Summary For purposes of this report, retail lending includes

FICO s analysis indicates:

FICO s analysis indicates: No observed material impact to the FICO Score due to expected NCAP changes. Minimal impact to risk prediction, odds-to-score relationship, and score distributions. No impact

FICO s analysis indicates: No observed material impact to the FICO Score due to expected NCAP changes. Minimal impact to risk prediction, odds-to-score relationship, and score distributions. No impact

ECONOMIC COMMENTARY. Three Myths about Peer-to-Peer Loans. Yuliya Demyanyk, Elena Loutskina, and Daniel Kolliner

ECONOMIC COMMENTARY Number 2017-18 November 9, 2017 Three Myths about Peer-to-Peer Loans Yuliya Demyanyk, Elena Loutskina, and Daniel Kolliner Peer-to-peer lending platforms, which provide a way for individuals

ECONOMIC COMMENTARY Number 2017-18 November 9, 2017 Three Myths about Peer-to-Peer Loans Yuliya Demyanyk, Elena Loutskina, and Daniel Kolliner Peer-to-peer lending platforms, which provide a way for individuals

Desktop Underwriter/Desktop Originator Release Notes

Desktop Underwriter/Desktop Originator Release Notes DU Version 10.3 Oct. 23, 2018 Updated Oct. 31, 2018 During the weekend of Dec. 8, 2018, Fannie Mae will implement Desktop Underwriter (DU ) Version

Desktop Underwriter/Desktop Originator Release Notes DU Version 10.3 Oct. 23, 2018 Updated Oct. 31, 2018 During the weekend of Dec. 8, 2018, Fannie Mae will implement Desktop Underwriter (DU ) Version

ECONOMIC AND FINANCIAL HIGHLIGHTS

ECONOMIC AND FINANCIAL HIGHLIGHTS FEDERAL RESERVE BALANCE SHEET Assets and Liabilities 2-3 REAL ESTATE Construction Spending 4 CoreLogic Home Price Index 5 Mortgage Rates and Applications 6-7 CONSUMER

ECONOMIC AND FINANCIAL HIGHLIGHTS FEDERAL RESERVE BALANCE SHEET Assets and Liabilities 2-3 REAL ESTATE Construction Spending 4 CoreLogic Home Price Index 5 Mortgage Rates and Applications 6-7 CONSUMER

12/14/2015. What it is

The topics of this class apply to the underwriting of FHA Title II Forward mortgages for the purchase or non-streamline refinance of 1-4 unit Single Family Residences. This information correlates to FHA

The topics of this class apply to the underwriting of FHA Title II Forward mortgages for the purchase or non-streamline refinance of 1-4 unit Single Family Residences. This information correlates to FHA

DEFINITION OF COMMON TERMS

DEFINITION OF COMMON TERMS Actual Cash Value: An amount equal to the replacement value of damaged property minus depreciation. Adjustable-Rate Mortgage (ARM): Also known as a variable-rate loan, an ARM

DEFINITION OF COMMON TERMS Actual Cash Value: An amount equal to the replacement value of damaged property minus depreciation. Adjustable-Rate Mortgage (ARM): Also known as a variable-rate loan, an ARM

Out of the Shadows: Projected Levels for Future REO Inventory

ECONOMIC COMMENTARY Number 2010-14 October 19, 2010 Out of the Shadows: Projected Levels for Future REO Inventory Guhan Venkatu Nearly one homeowner in ten is more than 90 days delinquent on his mortgage

ECONOMIC COMMENTARY Number 2010-14 October 19, 2010 Out of the Shadows: Projected Levels for Future REO Inventory Guhan Venkatu Nearly one homeowner in ten is more than 90 days delinquent on his mortgage

Tennessee Housing Market Brief

3rd quarter Housing ket Brief Business and Economic Research Center David A. Penn, Director Jennings A. Jones College of Business Middle State University his is the first in a series of quarterly reports

3rd quarter Housing ket Brief Business and Economic Research Center David A. Penn, Director Jennings A. Jones College of Business Middle State University his is the first in a series of quarterly reports

Making More Informed Decisions

December 8, 2008 TRANSUNION BANKRUPTCY SCORE Making More Informed Decisions Thomas Higgins Director, Analytic Decision Services thiggins@transunion.ca 416-332-2438 National Bankruptcy Trends Consumer bankruptcies

December 8, 2008 TRANSUNION BANKRUPTCY SCORE Making More Informed Decisions Thomas Higgins Director, Analytic Decision Services thiggins@transunion.ca 416-332-2438 National Bankruptcy Trends Consumer bankruptcies

MBA Forecast Commentary Joel Kan

MBA Forecast Commentary Joel Kan Economy & Labor Markets Strong Enough, First Rate Hike Expected in December MBA Economic and Mortgage Finance Commentary: November 2015 This month s outlook largely mirrors

MBA Forecast Commentary Joel Kan Economy & Labor Markets Strong Enough, First Rate Hike Expected in December MBA Economic and Mortgage Finance Commentary: November 2015 This month s outlook largely mirrors

Welcome! Credit Scoring and Sub-Prime Lending

Welcome! Credit Scoring and Sub-Prime Lending What is Credit Scoring? It s the use of a statistical model to objectively evaluate all the credit information available in a single repository What is a repository?

Welcome! Credit Scoring and Sub-Prime Lending What is Credit Scoring? It s the use of a statistical model to objectively evaluate all the credit information available in a single repository What is a repository?

CREDIT REPORT USER GUIDE

Page 1 of 17 ABOUT EQUIFAX CREDIT REPORT USER GUIDE Equifax Canada Inc. Box 190 Jean Talon Station Montreal, Quebec H1S 2Z2 Equifax empowers businesses and consumers with information they can trust. A

Page 1 of 17 ABOUT EQUIFAX CREDIT REPORT USER GUIDE Equifax Canada Inc. Box 190 Jean Talon Station Montreal, Quebec H1S 2Z2 Equifax empowers businesses and consumers with information they can trust. A

Financing Residential Real Estate. Qualifying the Buyer

Financing Residential Real Estate Lesson 8: Qualifying the Buyer Introduction In this lesson we will cover: the underwriting process, qualifying the buyer, and factors taken into account when a buyer s

Financing Residential Real Estate Lesson 8: Qualifying the Buyer Introduction In this lesson we will cover: the underwriting process, qualifying the buyer, and factors taken into account when a buyer s

GUIDELINES FOR THE AVERAGE MORTGAGE

GUIDELINES FOR THE AVERAGE MORTGAGE A mortgage lender reviews a loan applicant s financial history to determine the likelihood of receiving on-time payments. The primary items reviewed are: * Income *

GUIDELINES FOR THE AVERAGE MORTGAGE A mortgage lender reviews a loan applicant s financial history to determine the likelihood of receiving on-time payments. The primary items reviewed are: * Income *

UNDERSTANDING CREDIT. KASFAA Conference Manhattan, KS April 21, Robb Cummings Director of Business Development

UNDERSTANDING CREDIT KASFAA Conference Manhattan, KS April 21, 2016 Robb Cummings Director of Business Development FICO Score 2 A FICO Score is a three-digit number calculated from the credit information

UNDERSTANDING CREDIT KASFAA Conference Manhattan, KS April 21, 2016 Robb Cummings Director of Business Development FICO Score 2 A FICO Score is a three-digit number calculated from the credit information

Presented by Ed Swanson Lending Solutions Consulting, Inc.

Presented by Ed Swanson Lending Solutions Consulting, Inc. Credit Bureau 101 When to pull a credit report Components of a credit report Key elements on the credit report 2 When to Pull a Credit Report

Presented by Ed Swanson Lending Solutions Consulting, Inc. Credit Bureau 101 When to pull a credit report Components of a credit report Key elements on the credit report 2 When to Pull a Credit Report

FICO Scores Decoded Discover How to Easily and Quickly Obtain Excellent FICO Credit Scores Regardless of Your Personal Credit Quality Now

Discover How to Easily and Quickly Obtain Excellent FICO Credit Scores Regardless of Your Personal Credit Quality Now Discover How to Easily and Quickly Obtain Excellent FICO Credit Scores Regardless of

Discover How to Easily and Quickly Obtain Excellent FICO Credit Scores Regardless of Your Personal Credit Quality Now Discover How to Easily and Quickly Obtain Excellent FICO Credit Scores Regardless of

Laura Mackie Mortgages. A Guide to Understanding and Rebuilding Your Credit Score

Laura Mackie Mortgages Your Credit Report A Guide to Understanding and Rebuilding Your Credit Score Introduction This guide is intended to help you improve your credit score and provide you with information

Laura Mackie Mortgages Your Credit Report A Guide to Understanding and Rebuilding Your Credit Score Introduction This guide is intended to help you improve your credit score and provide you with information

M E M O R A N D U M Financial Crisis Inquiry Commission

M E M O R A N D U M Financial Crisis Inquiry Commission To: From: Commissioners Ron Borzekowski Wendy Edelberg Date: July 7, 2010 Re: Analysis of housing data As is well known, the rate of serious delinquency

M E M O R A N D U M Financial Crisis Inquiry Commission To: From: Commissioners Ron Borzekowski Wendy Edelberg Date: July 7, 2010 Re: Analysis of housing data As is well known, the rate of serious delinquency

Credit Score: What it Means to your Business

Score: What it Means to your Business Introduction Author Michael K. Swan, Washington State University Reviewers Gary Thome, Riverland Community College Peter Scheffert, Riverland Community College Along

Score: What it Means to your Business Introduction Author Michael K. Swan, Washington State University Reviewers Gary Thome, Riverland Community College Peter Scheffert, Riverland Community College Along

Memorandum. Sizing Total Exposure to Subprime and Alt-A Loans in U.S. First Mortgage Market as of

Memorandum Sizing Total Exposure to Subprime and Alt-A Loans in U.S. First Mortgage Market as of 6.30.08 Edward Pinto Consultant to mortgage-finance industry and chief credit officer at Fannie Mae in the

Memorandum Sizing Total Exposure to Subprime and Alt-A Loans in U.S. First Mortgage Market as of 6.30.08 Edward Pinto Consultant to mortgage-finance industry and chief credit officer at Fannie Mae in the

Dollars of Lines Originated (Billions) Dollars of Lines Originated Billions)

Dollars of Lines Originated Billions)") Lending Trends Crissy Wallace Lead Analytics Consultant 1 Experian Agenda Macroeconomic Trends Auto Trends Mortgage Trends Personal Loan Trends Student Loan Trends Alternative Data 2 Experian 1 Since the

Lending Trends Crissy Wallace Lead Analytics Consultant 1 Experian Agenda Macroeconomic Trends Auto Trends Mortgage Trends Personal Loan Trends Student Loan Trends Alternative Data 2 Experian 1 Since the

Fixing Bad Credit and Solving Credit Problems 1

FCS 5049 Fixing Bad Credit and Solving Credit Problems 1 Mary N. Harrison 2 When you want to buy a car, a house, or other expensive items you probably expect to use credit. For smaller purchases, your

FCS 5049 Fixing Bad Credit and Solving Credit Problems 1 Mary N. Harrison 2 When you want to buy a car, a house, or other expensive items you probably expect to use credit. For smaller purchases, your

GET SOCIAL WITH US. #vision2016. Tweet, follow, share throughout the session.

GET SOCIAL WITH US Tweet, follow, share throughout the session. 2015 Experian Information Solutions, Inc. All rights reserved. 1 Alternative methods to validate with low portfolio volumes Experian and

GET SOCIAL WITH US Tweet, follow, share throughout the session. 2015 Experian Information Solutions, Inc. All rights reserved. 1 Alternative methods to validate with low portfolio volumes Experian and

Credit and Credit Cards

Credit and Credit Cards What s Next Project Credit Cards They are all around you. Most people have at least one. Some have many. They are credit cards. A credit card allows you to pay for merchandise or

Credit and Credit Cards What s Next Project Credit Cards They are all around you. Most people have at least one. Some have many. They are credit cards. A credit card allows you to pay for merchandise or

Improving Your Credit

Teacher Homebuyer Guide to: Improving Your Credit By John Godbey, Founder and Broker of Teacher Homebuyer Real Estate Introduction Thank you for signing up for our E-Guide "Improving Your Credit." We find

Teacher Homebuyer Guide to: Improving Your Credit By John Godbey, Founder and Broker of Teacher Homebuyer Real Estate Introduction Thank you for signing up for our E-Guide "Improving Your Credit." We find

What You Can Do to Improve Your Credit, Now

What You Can Do to Improve Your Credit, Now Provided compliments of: 1 What You Can Do to Improve Your Credit, Now Steps to Raise Your Score Now we re going to focus on certain steps that you can take,

What You Can Do to Improve Your Credit, Now Provided compliments of: 1 What You Can Do to Improve Your Credit, Now Steps to Raise Your Score Now we re going to focus on certain steps that you can take,

SEGMENTATION FOR CREDIT-BASED DELINQUENCY MODELS. May 2006

SEGMENTATION FOR CREDIT-BASED DELINQUENCY MODELS May 006 Overview The objective of segmentation is to define a set of sub-populations that, when modeled individually and then combined, rank risk more effectively

SEGMENTATION FOR CREDIT-BASED DELINQUENCY MODELS May 006 Overview The objective of segmentation is to define a set of sub-populations that, when modeled individually and then combined, rank risk more effectively

ves a rue re i Credit Scoring: How it Works and How You Can Improve Your Score What Is Credit Scoring?

ves a Credit Scoring: How it Works and How You Can Improve Your Score rue re i Congratulations! By reading this publication you' ve taken the first step towards understanding and improving your credit

ves a Credit Scoring: How it Works and How You Can Improve Your Score rue re i Congratulations! By reading this publication you' ve taken the first step towards understanding and improving your credit

Twelve common questions. About consumer credit and direct marketing

Twelve common questions About consumer credit and direct marketing Twelve common questions Most of us don t think about credit until a specific event sparks our interest. Maybe we want to buy a car or

Twelve common questions About consumer credit and direct marketing Twelve common questions Most of us don t think about credit until a specific event sparks our interest. Maybe we want to buy a car or

Fact, Fiction & FICOs: Presented by: Vance Edwards, CMB Certified FICO Professional MGIC Marketing Program Director

Fact, Fiction & FICOs: Presented by: Vance Edwards, CMB Certified FICO Professional MGIC Marketing Program Director Agenda What makes up a credit score (and what doesn t) What causes that score to move

Fact, Fiction & FICOs: Presented by: Vance Edwards, CMB Certified FICO Professional MGIC Marketing Program Director Agenda What makes up a credit score (and what doesn t) What causes that score to move

Get Your Credit Mortgage Ready

Special Report Get Your Credit Mortgage Ready Compliments of: HowtoFixMyCredit.com Tel: 1-888-262-2123 Dear Home Buyer, If you re considering buying a home, then now would be a good time to check your

Special Report Get Your Credit Mortgage Ready Compliments of: HowtoFixMyCredit.com Tel: 1-888-262-2123 Dear Home Buyer, If you re considering buying a home, then now would be a good time to check your

12 common questions. About consumer credit and direct marketing

12 common questions About consumer credit and direct marketing Most of us don t think about credit until a specific event sparks our interest. Maybe we want to buy a car or home. Or perhaps we receive

12 common questions About consumer credit and direct marketing Most of us don t think about credit until a specific event sparks our interest. Maybe we want to buy a car or home. Or perhaps we receive

RETAIL BANKING. Consumer Lending. David Kemp President Bankers Management, Inc. McDonough, GA

RETAIL BANKING Consumer Lending David Kemp President McDonough, GA bankers3@inbox.com 770-909-6004 August 7, 2018 Graduate School of Banking 2018 Presented By: David L. Kemp: BMI 2016 2015 2014 2013 2012

RETAIL BANKING Consumer Lending David Kemp President McDonough, GA bankers3@inbox.com 770-909-6004 August 7, 2018 Graduate School of Banking 2018 Presented By: David L. Kemp: BMI 2016 2015 2014 2013 2012

SLUGGISH HOUSEHOLD GROWTH

3 Demographic Drivers Household growth has yet to rebound fully as the weak economic recovery continues to prevent many young adults from living independently. As the economy strengthens, though, millions

3 Demographic Drivers Household growth has yet to rebound fully as the weak economic recovery continues to prevent many young adults from living independently. As the economy strengthens, though, millions

Money & Credit: FRB-NY Household Debt & Credit Report

Money & Credit: FRB-NY Household Debt & Credit Report May 17, 21 Dr. Edward Yardeni 51-972-73 eyardeni@ Please visit our sites at www. blog. thinking outside the box Table Of Contents Table Of Contents

Money & Credit: FRB-NY Household Debt & Credit Report May 17, 21 Dr. Edward Yardeni 51-972-73 eyardeni@ Please visit our sites at www. blog. thinking outside the box Table Of Contents Table Of Contents

The Unique Credit Characteristics of Healthcare Patients. An Equifax Predictive Sciences Research Paper December 2003

The Unique Credit Characteristics of Healthcare Patients An Equifax Predictive Sciences Research Paper December 2003 Executive Summary As today s healthcare payment trends shift toward an ever increasing

The Unique Credit Characteristics of Healthcare Patients An Equifax Predictive Sciences Research Paper December 2003 Executive Summary As today s healthcare payment trends shift toward an ever increasing