Presented by Ed Swanson Lending Solutions Consulting, Inc.

|

|

|

- Noreen Goodman

- 5 years ago

- Views:

Transcription

1 Presented by Ed Swanson Lending Solutions Consulting, Inc.

2 Credit Bureau 101 When to pull a credit report Components of a credit report Key elements on the credit report 2

3 When to Pull a Credit Report Every time a member applies for a loan due to the volatile nature of credit and how quickly it can change When a new member applies for membership in order to cross-sell loan opportunities and preapprove them for loan products In the Collection Department to get an updated snapshot of the member s situation As a pre-screening product in order to approve existing members for a credit card or auto loan to perform a pre-approved mailing campaign 3

4 Components of a Credit Report 1. Identity & Demographic Name/address/date of birth Employment 2. Score & Summary Section Credit score identified Factors contributing to the score Revolving and installment trades added up 3. Trade lines Placement of information on reports Creditors Public Records/Collections 4. Inquiries Voluntary versus involuntary Like inquiries 4

5 1 Identity & Demographic Key Elements to Review Look for discrepancies between what the member has identified vs. what the credit report is reporting. Name Social security number Employment Residence Date of birth 5

6 Identity & Demographic /31/1977 Jane Doe 123 Main Street Elgin, IL ABC Factory 6

7 2 - Credit Score & Summary Section Key Elements to Review Score description Have the score code along with the description print on the credit report Capacity Revolving vs. installment Payment history Number of trade lines: As a guideline, the number of total trade lines versus the member s age should be 40%. When reviewing a credit report with a member, remember to point out positive items before discussing the negative trades. 7

8 Score Description Codes Score reason codes explain the top reasons why a credit score was not higher. These score reasons are more useful in highlighting reason for concern. If you already have a high score (for example, in the mid-700s or higher) some of the reasons may not be very helpful; as they may be marginal factors related to the categories that are weighted the least (length of credit history, new credit, and types of credit in use). The top 10 most frequently given score codes: Serious delinquency Serious delinquency, and public record, or collection filed Derogatory public record or collection filed Time since delinquency is too recent or unknown Level of delinquency on accounts Number of accounts with delinquency Amount owed on accounts Proportion of balances to credit limits on revolving accounts is too high Length of time accounts have been established Too many accounts with balances 8

9 Credit Bureau Score Codes & Definitions EQUIFAX - BEACON Score Codes serious delinquency serious delinquency, and derogatory public record or collection filed amount owed on delinquent accounts proportion of loan balances to loan amounts is too high lack of recent information loan information time since most recent account opening is too short no recent revolving balances number of bank or national revolving accounts with balances length of time since derogatory public record or collection is too short too few accounts currently paid as agreed number of accounts with delinquency lack of recent revolving account information lack of recent bank revolving information length of time accounts have been established time since delinquency is too recent or unknown length of time revolving accounts have been established amount owed on revolving account is too high proportion of balances to credit limits is too high on bank revolving or other revolving accounts too many accounts recently opened too many inquiries last 12 months too many consumer finance company accounts too many accounts with balances level of delinquency on accounts amount owed on accounts is too high O - beacon not available, no recently reported account information FA - number of inquiries adversely affected the score, but not significantly 9

10 TRANSUNION - EMPIRICA Score Codes derogatory public record or collection filed serious delinquency serious delinquency, and public record or collection filed time since most recent account opening is too short no recent bankcard balances number of established accounts too few accounts currently paid as agreed no recent revolving balances amount past due on accounts length of time since derogatory public record or collection is too short number of accounts with delinquency no recent non-mortgage balance information lack of recent revolving account information lack of recent bank revolving information length of time accounts have been established time since delinquency is too recent or unknown length of time revolving accounts have been established proportion of balances to credit limits is too high on bank revolving or other revolving accounts too many accounts recently opened too many inquiries last 12 months too many consumer finance company accounts too many accounts with balances proportion of loan balances to loan amounts is too high level of delinquency on accounts amount owed on accounts too high - file not scored because subject does not have sufficient credit FA - in addition to the factors listed above, the number of inquiries on the consumer's credit file has adversely affected the credit score 10

11 EXPERIAN - FAIR ISAAC Score Codes 40 - derogatory public record or collection field 39 - serious delinquency 38 - serious delinquency and public record or collection filed 33 - proportion of current loan balance to original loan amount 32 - no recent installment loan information 24 - lack of recently reported balances on revolving/open accounts 21 - amount past due to accounts 20 - length of time since legal item filed or collection item reported 18 - number of accounts delinquent 16 - insufficient or lack of revolving account information 15 - insufficient or lack of bank revolving account information 14 - length of time accounts have been established 13 - length of time (or unknown time) since account delinquent 12 - length of revolving account history 10 - proportion of balance to high credit on bank revolving or all revolving accounts 09 - number of accounts opened within the last 12 months 08 - number of recent inquiries 06 - number of finance company accounts 05 - number of accounts with balances 02 - delinquency reported on accounts 01 - current balances on accounts the profile report does not contain any trade line which satisfies both of the following: status date within the last six (6) months or a balance within the last six (6) months. Does not contain disputed information - risk score not calculated due to lack of credit history 11

12 Credit Score Factors A comprehensive list of the information considered by Fair Isaac scoring models when calculating a credit score. 1. Past Payment History -Account payment information on specific types of accounts (credit cards, retail accounts, installment loans, finance company accounts, mortgage, etc.) -Presence of adverse public records (bankruptcy, judgments, suits, liens, wage attachments, etc.), collection items, and/or delinquency (past due items). -Severity of delinquency (how long past due). -Amount past due on delinquent accounts or collection items. -Time since (how recent) past due items (delinquency), adverse public records (if any), or collection items (if any). -Number of past due items on file. -Number of accounts paid as agreed. 2. Amount of Credit Owing -Amount owing on accounts. -Amount owing on specific types of accounts. -Lack of a specific type of balance, in some cases. -Number of accounts with balances. -Proportion of credit lines used (proportion of balances to total credit limits on certain types of revolving accounts). -Proportion of installment loan amounts still owing (proportion of balance to original loan amount on certain types of installment loans).

13 3. Length of Time Credit Established -Time since accounts opened. -Time since accounts opened, by specific type of account. -Time since account activity. 4. Search for and Acquisition of New Credit -Number of recently opened accounts, and proportion of accounts that are recently opened, by type of account. -Number of recent credit inquiries. -Time since recent account opening(s), by type of account -Time since credit inquiry(s). -Re-establishment of positive credit history following past payment problems. 5. Types of Credit Established -Number of (presence, prevalence, and recent information on) various types of accounts (credit cards, retail accounts, installment loans, mortgage, consumer finance accounts, etc.)

14 Credit Score & Summary Section 14

15 Colorful Credit 15

16 3 - Trade lines Key Elements to Review Circle open dates and balances Compare balances to limits Individual, joint, co-signer or authorized user Payment history Current payment status Consumer or Creditor statements 16

17 Understanding Codes R- Revolving (Usually a credit card, no definitive term, payments usually don t go toward principle) I - Installment (Home or auto loan, designated term, payments are amortized to include principle and interest) M Mortgage trade line R1 or I1 = Pays as agreed never late R2 or I2 = 30 days late R3 or I3 = 60 days late R4 or I4 = 90 days late R5 or I5 = 120 days late R7 or I7 = Making regular payments under wage earner plan R8 or I8 = Repossession R9 or I9 = Charge off 17

18 Authorized Users Definition Not responsible for payment but it can affect adversely How is it different than a co-signer? Description Child on a parent s account Spouse on a spouse s account A piece of the puzzle for decision makers Whose account are they on? Why? Do they strengthen or help the member? Opportunity A new member joining the credit union 18

19 Inflated Income Is the member showing signs of living on inflated income? Characteristics of inflated income Escalating debt Opening up numerous accounts Shopping for additional credit Cashing out equity in homes Note: If self employed members are using up their revolving lines and cashing out equity, they may be living off inflated income. 19

20 Trade Lines 20

21 4 - Inquiries Key Elements to Review Who is pulling the member s credit report and what does it tell us? Finance company Typically the member is not worried about rates but whether it fits into their budget. Mortgage company member is looking to refinance their home or purchase a home. Like inquiries (i.e. auto dealers) member is most likely shopping of a vehicle and loan is being sent off to multiple companies. Store credit cards Member likes to take advantage of store promos and less rate focused. Is the member shopping for more credit? General guideline is 2 to 3 inquiries a year If credit is escalating is the income also increasing and/or what is the motivation for the shopping? 21

22 Inquiries 22

23 Credit Score 101 Test your knowledge What it takes to have a credit score Components of the Scoring Models Determining the direction of the score Fragile A credit Bankruptcy vs. credit scores Score enhancement Using the credit report as an opportunity sheet 23

24 Testing Your Credit Score Knowledge 1. What aspect of the credit history is the most heavily weighted factor in computing the credit score? 2. What aspect of the credit history is the second most heavily weighted factor in computing the score? 3. Is the income a component of the score? 4. Is length of residence a component of the score? 5. Is total-debt-ratio a component of the score? 6. Is length of employment a component of the score? 7. Does the score take into account when good or bad credit occurs? 8. What advice do you presently give members that want to improve their score? 24

25 NEW YORK, July 12, 2010 More Americans' Credit Scores Sink to New Lows About 1 in 4 Consumers With a Credit Account Has a Credit Score of 599 or Lower Americans' credit scores are getting worse. The latest analysis by FICO Inc., based on consumer credit reports as of April, shows that millions more Americans have credit scores that could prevent them from getting credit cards, auto loans or mortgages under the tighter lending standards banks now use. Restricted access to credit is one reason for the slow economic recovery. About a quarter of consumers percent, or nearly 43.4 million people - now have a credit score of 599 or below, marking them as poor risks. That's a big jump over the historical rate of 15 percent of the 170 million consumers with active credit accounts (or 25.5 million people) falling below 599. Yet, the number of consumers who have a top score of 800 or above has also increased in recent years. 25

26 What it Takes to Get a Score Only 1 trade line 6 months of payment history Activity reported in the last 6 months 26

27 How Fast Your Score Can Change The member s score can change whenever the credit report changes. The member s score probably won t change much from one month to the next. Bankruptcies and other public records or collections can have a major impact on credit scores and it takes time to recover. Simply missing a payment can also impact the credit score. However, the score can recover quickly if the payment on the account is current, provided the credit report has substance. 27

28 Components of the Scoring Models Range of Scores 830 = Outstanding 680 = Average 380 = Lowest 10% 10% 35% 15% 30% - Weight of Five Factors That Make Up Scores 35% = How You Pay (payment history) 30% = Capacity (amount owed on revolving) 15% = Length (length of new credit and total credit history) 10% = Accumulation (new credit and inquiries) 10% = Mix (percent of revolving, installment & mortgage) 28

29 Determining The Direction Of The Score Questions? Direction of Score Does the member have recent late payments? Is the member a B or C paper and never missed a payment? Is the member a C paper and claimed bankruptcy in the recent past? Is the member a C paper and has collections in the recent past? Does the member have a lot of recent inquiries? Does the member have recent loans through sub-prime lenders? (Lenders of last resort) Down Down Up Up Down Down Up Down Down Up Down Does the member have low balances on revolving accounts opened in the last 3 yrs? Are the revolving debt maxed out within the last months? Has the member opened up a lot of new accounts in a short time frame? Has the member refinanced revolving debt into installment debt? Does the member have more in revolving debt than installment debt?

30 The credit score on a member s credit report is an average of their credit performance over a number of years, with the most weight being placed on the current year. It is important that you try to determine which direction the score is headed. The member s overall score may look ok, but this can be very misleading and it can encourage you to make a costly mistake. Using the analogy of two college graduates applying for the same job. Reviewing their experience and education they both appear to be equal in every regard. They even had the same cumulative grade point average (GPA) in college. However, their overall cumulative GPA does not reflect how they are currently doing, as demonstrated below: Applicant # 1 GPA Applicant #2 GPA Freshman Year Sophomore Year Junior Year Senior Year Cumulative GPA The point here is that even though both job applicants had a cumulative GPA of 3.00, Applicant #2 has significantly out-performed Applicant #1 over the last two years. Today, Applicant #2 is a 3.80 student, and Applicant #1 is a 2.20 student a huge difference! The exact same can be true of two members applying for credit with the same score. 30

31 How a Credit Score Assigns Weights to Previous Years of Credit History Year Before 2007 Weight Assigned to that Year 40% 30% 20% 10% 0% 31

32 Why the Last 24 Months of History is Crucial Credit scores go from a low of approximately 380 points to a high of approximately 830 points, with an average score around 620 points. Two members can arrive at a 620 score in very different ways: credit Score 2008 (10%) 2009 (20%) 2010 (30%) 2011 (40%) Just as in the example of the two job applicants applying for the same job with the same cumulative GPA, look now at two members applying for credit with the same credit score of 620. They have the following characteristics: Applicant #1 Applicant #2 - Perfect credit - No late pays - No collection accounts - No civil judgments - No repossessions - No bankruptcy - Very colorful credit - Long history of late pays - Several collections - Had a judgment - Previous repossession - Been bankrupt 32

33 Key Conclusions From Example 1. Members with very good credit that score in the low 600 s are a very high risk. They are standing at the edge of a cliff that is about to give way. Their score today is probably more reflective of a score in the low 500 s, but it is their good credit of the past that is propping up their average score. 2. Members with credit reports full of negative information that score in the low 600 s are a much lower credit risk, and should be given serious consideration for a loan approval (especially secured loans). Their score today is probably more reflective of a score in the high 600 s, but their poor credit of the past is dragging down their average score. 33

34 Fragile A Credit One of the real weaknesses of the credit scoring model is that often a member will earn a good score (680+) with little or no credit to base the score upon. We refer to this as the Fragile A. Common characteristics of the Fragile A are: Borrowers are typically young Very few trade lines Credit histories are very limited Dollar amounts of credit they ve had are small You should be cautious of the Fragile A borrower. Any type of hiccup in their credit can result in their score dropping from A to D overnight. This is because there is very little substance to their credit report. The key thing for you to remember is that if you do approve them, you will need to give them the A paper rate today. 34

35 Fragile A Credit Report 35

36 Bankruptcy vs. the Credit Score Score at Time of Loan Grade of Paper A+ A B C D E Approximate Loss of Points Approximate Score After BK Grade of Paper D DE E EE- Note: Members lose a lot of points with high scores and fewer points with low scores (They have already lost them). There is a big difference in the paying habits of an A paper member who filed bankruptcy versus an E paper member. Most A paper members will resume their A paper paying habits, E paper members usually continue to pay like E paper. Note: Member s scores can vary greatly depending on: -How the creditors are reporting -New credit they have established since the bankruptcy -Capacity if available (if they got a new credit card) There is a Bankruptcy Bill of Rights that requires creditors included in the bankruptcy to no longer report them as delinquent or as having a balance. They should report no balance and included in bankruptcy. 36

37 Score Enhancement Techniques That Drive Members' Score Up Score enhancement is a unique competitive advantage credit unions have over all other lenders provided they embrace the concept and put this into practice. Why do we believe this will is very powerful tool? Most members would really appreciate knowing: We believe most members do not know their scores (even though this is changing). What makes up their score? How to improve their score Where to go and get help Members deserve the right to earn a lower rate if they really take the time to clean up their credit. Employees of credit unions must become knowledgeable so they can help members. Any financial institution willing to show their members or customers how to pay less will have tremendous credibility with their members and get all their 37 business.

38 1. What Makes Up your Credit Score? 35% = Based on payment history (i.e. on-time pays or delinquencies) - More weight on current pay history 30% = Capacity (capacity is King) 15% = Length of credit 10% = Accumulation of debt in the last months - # of inquiries - Opening dates 10% = Mix of credit - Installment (can raise) vs. revolving (can lower) - Finance company loans-they can lower your score 2. What Actions Will Hurt Your Score? Missing payments (Regardless of $ amounts, it can take 24 months to restore credit with one late payment) Credit cards at capacity (i.e. maxing out credit cards) Shopping for credit excessively Opening up numerous trades in a short time frame Having more revolving debts in relation to installment debts Closing credit cards out (this could lower available capacity) Borrowing from finance companies

Slow down on opening new accounts Acquire a solid credit history with years of experience 4.")

39 3. How You Can Improve Your Score: Pay off or pay down on your credit cards Do not close credit cards because capacity may decrease Move your revolving debt into installment debt Continue to make payments on time (older late pays will become less significant with time) Slow down on opening new accounts Acquire a solid credit history with years of experience 4. Approximate Credit Weight for Each Year: 40% = Current to 12 months 30% = months 20% = months 10% = 37+ months

40 Savings to Member A Member vs. E Member 542 E Member 681 A Member Loan Amount $25, 000 $25,000 Term 60 months 60 months Rate 16.95% 3.95% Payment $ $ Total Payments $37, $27, $37, , Savings $ 9,

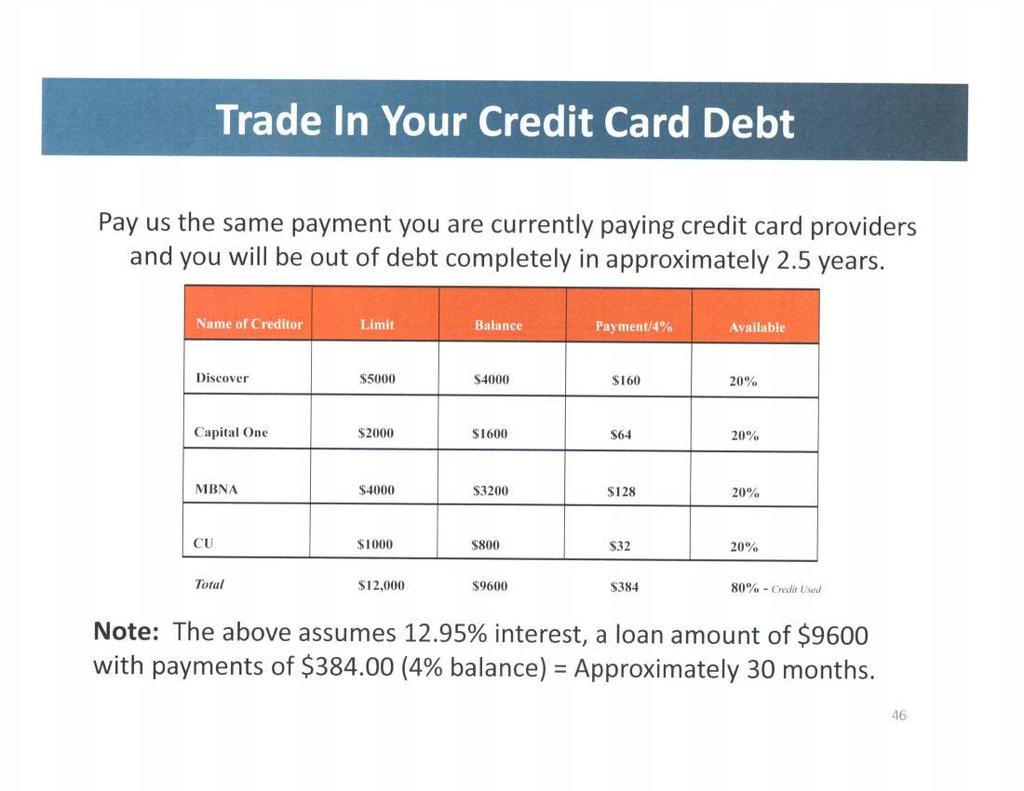

41 Using the Credit Report as an Opportunity Sheet Calculating interest rates of the competition Autos Mortgages Unsecured loans Trade in your credit card debt 41

42 Using the Credit Report as an Opportunity Sheet What rate is your member paying the competition? How much can we save them? $ 950 $

43 NOTE: The credit report must show the following 3 factors: Gross loan amount Monthly payment (On mortgages, if the payment includes taxes and insurance. They must be backed out.) The term (You can only calculate the rate on installment loans.) Step 1: Enter the high credit off the credit reports or original balance = $20,000 Step 2: Press PV (Present Value) PV= Step 3: Enter the number of months on loan = 60 Step 4: Press N N=60.00 Step 5: Enter payment of loan = 444 Step 6: Press +/- (To make the payment negative) If this is not completed, an ERROR 5 will appear when computing interest. Step 7: Press PMT Step 8: Press CPT (Compute) Step 9: Press I/Y to figure the interest the member is paying at your competition.

44 *There may be a slight delay while calculating. I/Y= To compute the savings the member would receive by refinancing with the credit union...*do not erase any of the above* Step 10: Enter your current rate on loan = 5.95 Step 11: Press I/Y I/Y=5.95 Step 12: Press CPT Step 13: Press PMT (To calculate the payment at the credit union) PMT= Step 14: Add old payment to new payment. (This will figure the difference between the credit union & the competition = 149) ( = Step 15: Multiply the number of payments left in the loan = x 53 = $3, $3,063.87

45 What Credit Card Companies are Doing to Your Members Raising interest rates Lowering credit limits (This has a huge impact on capacity) Charging more fees Increasing late fees & over limit fees Increasing minimum monthly payments Taking away perk programs 45

46

47 HYLS High Yield Lending Strategy Number of years as an active member Total dollar amount on deposit with the credit union Number of current & prior satisfactory loans in excess of $1,000 with the CU Highest dollar loan amount the member has had with the credit union Direct deposit Length of residence Length of employment Valid credit score Credit score with no credit flaws Inquiries in the past 24 months Number of open or closed trade lines in the past 24 months Number of Open or Closed Trade Lines as a Percentage of the Member s Age Total dollar amount past due with all creditors Payment history on most recent auto loans Payment History on the Last Prior Vehicle Loan Loan to value on vehicle loan Number of vehicle loans in the past 24 months Loan amount versus term New vehicle loan being purchased vs annual gross income Total secured loan balances outstanding vs annual gross income Debt to income ratio Total outstanding unsecured debt vs annual gross income Total unsecured dollar amount outstanding Total mortgage debt vs annual gross income Number of late payments on mortgage loans Available equity in real estate Cashing out real estate equity 47

48

49 What Have We Learned Today? The credit report is a key tool to assist us in many aspects of our business Analyzing for member s credit worthiness---intent to pay Opening up a new account---big opportunities Collections needs to be pulling credit reports on delinquent accounts and doing their analysis before making that phone call to the member

50 What Have We Learned Today? How to read the 4 codes that the credit bureau provides, to let us know how the score was obtained and which of those codes are warning signs. How vital it is to use capacity as a measuring tool for member s ability to pay are they living off credit cards or the equity in their home? This is known as Inflated Income. How to assist members in reducing capacity and increase their score.

51 What Have We Learned Today? How the credit bureau score is determined: 35% payment history 30% capacity 15% length of credit 10% new credit/inquiries 10% mix of credit Who knew that so few factors were looked at to determine the score? The credit bureau agencies seem to want to keep this information a secret.

52 What Have We Learned Today? The credit report is an Opportunity Sheet the trade lines are screaming at us to pay them off. We must start listening to those screams and pay off the competition on every loan you make for your members. Order filling won t get it done.

53 Thanks for Joining Me Today! You can t build a reputation on what you re going to do. Henry Ford Just Do It! Nike Ed Swanson eswanson@rexcuadvice.com

54 Ed Swanson is a 28-year veteran of the financial services industry and a 25-year veteran of the credit union industry. He has spoken for over 35 Credit Union Leagues throughout the country on a variety of lending and member service related topics. Swanson helps credit unions to strengthen themselves in areas of consumer lending, loan underwriting, risk based lending, mortgage lending, indirect lending, collections, sales development, member service and incentive programs. Swanson was also an annual instructor at the CUNA Consumer Lending Management School for seven years and has been a featured speaker at CU Conference's, 'Focus on Lending' conference for the past twelve years. Ed Specializes In (But not limited to): Lending in Today s Marketplace Underwriting Higher Risk Loans Risk Based Pricing Home Equity Lending Improving Delinquency Numbers Payday Lending Serving Members of Modest Means Sub-Prime Lending Cross-Selling that Actually Works Implementing an Incentive Program Building a Sales Culture Understanding Credit Scoring Auto-Lending Building Member Relations Ed Swanson, Vice President/Consultant Lending Solutions Consulting, Inc Ed Swanson is as well versed in lending, collections, mortgages & sales as anyone you will ever meet. He has spent his entire career in the credit union movement. At Baxter CU, Ed and I worked side by side in all phases of lending, collections, mortgages, & sales & achieved world class results. Delinquencies & charge offs were both below.2% with a 91% loan-to-share ratio. You will absolutely love Ed, we guarantee it! Rex Johnson, LSCI Founder eswanson@rexcuadvice.com

55 Developing a Confident, Engaging and Fearless Sales Force Sales Training Series - Presented by Jack Kelly Webinar Series Topics Webinar 1 - Successful Sales Training in 7 Easy Steps Tuesday, October 11, pm Central Webinar 2-3 Steps for a Successful Sales Culture Tuesday, October 18, pm Central Webinar 3 Seeking Solutions and Overcoming Objections Tuesday, November 1, pm Central Webinar 4 Follow-Up and Follow Through Tuesday, November 8, pm Central

UNDERSTANDING YOUR CREDIT REPORT & YOUR CREDIT SCORE

UNDERSTANDING YOUR CREDIT REPORT & YOUR CREDIT SCORE Presented By: Tom Painter Chief Lending Officer WHAT IS A CREDIT SCORE? A credit score is a number that summarizes your credit risk, based on a snapshot

UNDERSTANDING YOUR CREDIT REPORT & YOUR CREDIT SCORE Presented By: Tom Painter Chief Lending Officer WHAT IS A CREDIT SCORE? A credit score is a number that summarizes your credit risk, based on a snapshot

65 E. Wacker Place Suite 1405, Chicago, IL Ph: Fax: Credit 101

65 E. Wacker Place Suite 1405, Chicago, IL 60601 Ph: 888.895.5145 Fax: 888.895.5146 Credit 101 The subject of credit and what is included on a consumer s credit report can be a source of much debate, confusion

65 E. Wacker Place Suite 1405, Chicago, IL 60601 Ph: 888.895.5145 Fax: 888.895.5146 Credit 101 The subject of credit and what is included on a consumer s credit report can be a source of much debate, confusion

Understanding Your FICO Score. Understanding FICO Scores

Understanding Your FICO Score Understanding FICO Scores 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Reports

Understanding Your FICO Score Understanding FICO Scores 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Reports

Understanding. What you need to know about the most widely used credit scores

Understanding What you need to know about the most widely used credit scores 300 850 The score lenders use. FICO Scores are the most widely used credit scores according to a recent CEB TowerGroup analyst

Understanding What you need to know about the most widely used credit scores 300 850 The score lenders use. FICO Scores are the most widely used credit scores according to a recent CEB TowerGroup analyst

c» BALANCE C:» Financially Empowering You The World of Credit Reports Podcast [Music plays] Nikki:

![c» BALANCE C:» Financially Empowering You The World of Credit Reports Podcast [Music plays] Nikki:](/thumbs/76/73531259.jpg "c» BALANCE C:» Financially Empowering You The World of Credit Reports Podcast [Music plays] Nikki:") The World of Credit Reports Podcast [Music plays] Nikki: You re listening to world of credit. Hi, I m Nikki, your host for today s podcast. Credit reports and credit scores influence our lives in many

The World of Credit Reports Podcast [Music plays] Nikki: You re listening to world of credit. Hi, I m Nikki, your host for today s podcast. Credit reports and credit scores influence our lives in many

Quick Credit Repair Guide

1 Quick Credit Repair Guide Beacon score? You will most likely have heard of this bizarre term at some point during your home buying process and wondered what they meant and how they affect the mortgage

1 Quick Credit Repair Guide Beacon score? You will most likely have heard of this bizarre term at some point during your home buying process and wondered what they meant and how they affect the mortgage

Understanding Credit Reports

Understanding Credit Reports Family Economics & Financial Education Take Charge of Your Finances Credit Report Detectives Meet Isabella, your new client: About to graduate from college In extreme debt

Understanding Credit Reports Family Economics & Financial Education Take Charge of Your Finances Credit Report Detectives Meet Isabella, your new client: About to graduate from college In extreme debt

GREENPATH FINANCIAL WELLNESS SERIES

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Empowering people to lead financially healthy lives. TABLE OF CONTENTS Understanding credit reports...2 What s in a credit

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Empowering people to lead financially healthy lives. TABLE OF CONTENTS Understanding credit reports...2 What s in a credit

Reviewing C YouR CRedit RepoRt

ChapteR 2 Reviewing C YouR CRedit RepoRt What do your creditors have to say about the way you handle money? Having a good credit score can help you turn your home-buying dream into a reality. There s much

ChapteR 2 Reviewing C YouR CRedit RepoRt What do your creditors have to say about the way you handle money? Having a good credit score can help you turn your home-buying dream into a reality. There s much

Now, let me turn the program over to Jacqueline Cooke, Women s Bureau Regional Administrator in Boston, to introduce our first speaker. Jackie?

Wi$e Up Teleconference Call February 28, 2006 Becoming Credit Smart Speaker 1 Amy Perry Jane Walstedt: Now, let me turn the program over to Jacqueline Cooke, Women s Bureau Regional Administrator in Boston,

Wi$e Up Teleconference Call February 28, 2006 Becoming Credit Smart Speaker 1 Amy Perry Jane Walstedt: Now, let me turn the program over to Jacqueline Cooke, Women s Bureau Regional Administrator in Boston,

Understanding Credit. What it is, why it s important, and how you can maintain it. Brought to you by Sallie Mae and FICO

Understanding Credit What it is, why it s important, and how you can maintain it Brought to you by Sallie Mae and FICO Introduction A student loan may be your first major credit experience. This is a good

Understanding Credit What it is, why it s important, and how you can maintain it Brought to you by Sallie Mae and FICO Introduction A student loan may be your first major credit experience. This is a good

HOW TO USE CREDIT. Latino Community Credit Union & the Latino Community Development Center.

HOW TO USE CREDIT Latino Community Credit Union & the Latino Community Development Center www.latinoccu.org Copyright 2016 Latino Community Credit Union Made possible by a generous contribution from the

HOW TO USE CREDIT Latino Community Credit Union & the Latino Community Development Center www.latinoccu.org Copyright 2016 Latino Community Credit Union Made possible by a generous contribution from the

TABLE OF CONTENTS. Healthier Black Elders Center

TABLE OF CONTENTS What is credit............................................1 The five C s of credit...................................... 2 Types of credit...........................................3

TABLE OF CONTENTS What is credit............................................1 The five C s of credit...................................... 2 Types of credit...........................................3

ves a rue re i Credit Scoring: How it Works and How You Can Improve Your Score What Is Credit Scoring?

ves a Credit Scoring: How it Works and How You Can Improve Your Score rue re i Congratulations! By reading this publication you' ve taken the first step towards understanding and improving your credit

ves a Credit Scoring: How it Works and How You Can Improve Your Score rue re i Congratulations! By reading this publication you' ve taken the first step towards understanding and improving your credit

Improving Your Credit

Teacher Homebuyer Guide to: Improving Your Credit By John Godbey, Founder and Broker of Teacher Homebuyer Real Estate Introduction Thank you for signing up for our E-Guide "Improving Your Credit." We find

Teacher Homebuyer Guide to: Improving Your Credit By John Godbey, Founder and Broker of Teacher Homebuyer Real Estate Introduction Thank you for signing up for our E-Guide "Improving Your Credit." We find

Welcome! Credit Scoring and Sub-Prime Lending

Welcome! Credit Scoring and Sub-Prime Lending What is Credit Scoring? It s the use of a statistical model to objectively evaluate all the credit information available in a single repository What is a repository?

Welcome! Credit Scoring and Sub-Prime Lending What is Credit Scoring? It s the use of a statistical model to objectively evaluate all the credit information available in a single repository What is a repository?

A CONSUMER S GUIDE TO INSURANCE COMPANIES' USE OF CREDIT INFORMATION

A CONSUMER S GUIDE TO INSURANCE COMPANIES' USE OF CREDIT INFORMATION INSURANCE CREDIT SCORING IN NORTH CAROLINA Insurance companies licensed to sell private passenger automobile and residential property

A CONSUMER S GUIDE TO INSURANCE COMPANIES' USE OF CREDIT INFORMATION INSURANCE CREDIT SCORING IN NORTH CAROLINA Insurance companies licensed to sell private passenger automobile and residential property

Introduction. In short- credit is an essential part of our personal and national economic stability.

Table of Contents 2 Introduction 3 The Wait Is Over!. 4 The Five Factors that Determine your FICO Score Are: 5 What is Seasoned Trade Lines?... 7 How Do I Raise My FICO Score with Seasoned Trade Lines.

Table of Contents 2 Introduction 3 The Wait Is Over!. 4 The Five Factors that Determine your FICO Score Are: 5 What is Seasoned Trade Lines?... 7 How Do I Raise My FICO Score with Seasoned Trade Lines.

Your Guide To Better Credit

Your Guide To Better Credit INTRODUCTION Your go-to guide to better credit It seems like every other commercial on television touts some sort of offer around credit. You hear things like, Free credit report,

Your Guide To Better Credit INTRODUCTION Your go-to guide to better credit It seems like every other commercial on television touts some sort of offer around credit. You hear things like, Free credit report,

Improving Your Credit Score

Improving Your Credit Score From my experience working with many potential home buyers looking to improve their credit, they are frustrated! They are frustrated because they receive conflicting information

Improving Your Credit Score From my experience working with many potential home buyers looking to improve their credit, they are frustrated! They are frustrated because they receive conflicting information

5/16/2006 1 of 18 Report for CHRISTINE BAKER on April 30, 2006 Click here to return. 742 CHRISTINE BAKER April 30, 2006 Credit record source: Equifax Your FICO score of 742 summarizes the information on

5/16/2006 1 of 18 Report for CHRISTINE BAKER on April 30, 2006 Click here to return. 742 CHRISTINE BAKER April 30, 2006 Credit record source: Equifax Your FICO score of 742 summarizes the information on

Understanding Credit. Lisa Mitchell, Sallie Mae April 6, Champions of Financial Aid ILASFAA Conference

Understanding Credit Lisa Mitchell, Sallie Mae April 6, 2017 Credit Management Agenda Understanding Your Credit Report Summary: Financial Health Tips Credit Management Credit Basics Credit health plays

Understanding Credit Lisa Mitchell, Sallie Mae April 6, 2017 Credit Management Agenda Understanding Your Credit Report Summary: Financial Health Tips Credit Management Credit Basics Credit health plays

Federal Reserve Bank of Philadelphia

Federal Reserve Bank of Philadelphia 1 When you apply for credit, whether it s a credit card, car loan, or a mortgage, lenders want to know whether you are likely to repay your loan and make the payments

Federal Reserve Bank of Philadelphia 1 When you apply for credit, whether it s a credit card, car loan, or a mortgage, lenders want to know whether you are likely to repay your loan and make the payments

Money Management Curriculum

Money Management Module 4: Credit Reports & Credit Scores Money Management Curriculum Module 4: Credit Reports & Credit Scores Project Team: Ruby Ward, Professor, Utah State University Trent Teegerstrom,

Money Management Module 4: Credit Reports & Credit Scores Money Management Curriculum Module 4: Credit Reports & Credit Scores Project Team: Ruby Ward, Professor, Utah State University Trent Teegerstrom,

Credit Repair Company

6 Business Credit Secrets Every Credit Repair Company Should Know 6 Business Credit Secrets Every Credit Repair Company Should Know About Business Credit is credit that is obtained in a Business Name.

6 Business Credit Secrets Every Credit Repair Company Should Know 6 Business Credit Secrets Every Credit Repair Company Should Know About Business Credit is credit that is obtained in a Business Name.

FICO Score Open Access Consumer Credit Education US Version. Frequently Asked Questions about FICO Scores

FICO Score Open Access Consumer Credit Education US Version Frequently Asked Questions about Scores 2012 Fair Isaac Corporation. All rights reserved. 1 January 01, 2012 Table of Contents About Scores...

FICO Score Open Access Consumer Credit Education US Version Frequently Asked Questions about Scores 2012 Fair Isaac Corporation. All rights reserved. 1 January 01, 2012 Table of Contents About Scores...

Creditworthiness (UXL)

") Creditworthiness (UXL) Since so much debt is unsecured, it is important for companies to have information on how well their potential borrowers handle money in order to assess their creditworthiness, or

Creditworthiness (UXL) Since so much debt is unsecured, it is important for companies to have information on how well their potential borrowers handle money in order to assess their creditworthiness, or

13.1. Reading a Credit Report EXERCISE. THEME 4 Lesson 13: Applying for Credit NAME: CLASS PERIOD:

13.1 NAME: CLASS PERIOD: Reading a Credit Report Your ability to qualify for a loan depends on a credit report. A credit report is a record of an individual s personal credit history. It is probably a

13.1 NAME: CLASS PERIOD: Reading a Credit Report Your ability to qualify for a loan depends on a credit report. A credit report is a record of an individual s personal credit history. It is probably a

Understanding Credit

Understanding Credit LAURA STEINBECK DIRECTOR OF BUSINESS DEVELOPMENT, SALLIE MAE 2018 MASFAP CONFERENCE Agenda 2 Credit Management Protect Yourself Understanding Credit Reports Summary: Financial Health

Understanding Credit LAURA STEINBECK DIRECTOR OF BUSINESS DEVELOPMENT, SALLIE MAE 2018 MASFAP CONFERENCE Agenda 2 Credit Management Protect Yourself Understanding Credit Reports Summary: Financial Health

Credit Reports 101. Bill Bufkins, November 3, 2011

Credit Reports 101 Bill Bufkins, November 3, 2011 What is a credit report? A credit report is a record of your past borrowing and repayment activity. The information in your credit report helps determine

Credit Reports 101 Bill Bufkins, November 3, 2011 What is a credit report? A credit report is a record of your past borrowing and repayment activity. The information in your credit report helps determine

A Credit Smart Start. Michael Trecek Sr. Risk Analyst Commerce Bank - Retail Lending

A Credit Smart Start Michael Trecek Sr. Risk Analyst Commerce Bank - Retail Lending Agenda Credit Score vs. Credit Report Credit Score Components How Credit Scoring Helps You 10 Things that Hurt Your Credit

A Credit Smart Start Michael Trecek Sr. Risk Analyst Commerce Bank - Retail Lending Agenda Credit Score vs. Credit Report Credit Score Components How Credit Scoring Helps You 10 Things that Hurt Your Credit

A Special Report by Laura Adams, author of Money Girl s Smart Moves to Grow Rich

3 Strategies to Build Credit FAST A Special Report by Laura Adams, author of Money Girl s Smart Moves to Grow Rich 3 Strategies to Build Credit Fast Copyright 2011 SmartMovesToGrowRich.com All rights reserved.

3 Strategies to Build Credit FAST A Special Report by Laura Adams, author of Money Girl s Smart Moves to Grow Rich 3 Strategies to Build Credit Fast Copyright 2011 SmartMovesToGrowRich.com All rights reserved.

Project Pro$per. Credit Reports and Credit Scores

Project Pro$per Presents Credit Reports and Credit Scores Participant Guide www.projectprosper.org www.facebook.com/projectprosper Based on Wells Fargo s Hands on Banking The Hands on Banking program is

Project Pro$per Presents Credit Reports and Credit Scores Participant Guide www.projectprosper.org www.facebook.com/projectprosper Based on Wells Fargo s Hands on Banking The Hands on Banking program is

Module 7 - Credit Reporting HANDOUT 7-1

ParticipantHandbook 1 Module 7 - Credit Reporting HANDOUT 7-1 Credit bureaus Credit bureaus are agencies that collect information about how we use credit. They produce personal credit reports. Credit bureaus

ParticipantHandbook 1 Module 7 - Credit Reporting HANDOUT 7-1 Credit bureaus Credit bureaus are agencies that collect information about how we use credit. They produce personal credit reports. Credit bureaus

Boost Your Credit Score By Yourself! How to get the house or car you want

Boost Your Credit Score By Yourself! How to get the house or car you want TIP 1. STEP-BY-STEP GAME PLAN This is what you have to know to fix your credit in a hurry: You must know your three credit scores

Boost Your Credit Score By Yourself! How to get the house or car you want TIP 1. STEP-BY-STEP GAME PLAN This is what you have to know to fix your credit in a hurry: You must know your three credit scores

Credit Score: What it Means to your Business

Score: What it Means to your Business Introduction Author Michael K. Swan, Washington State University Reviewers Gary Thome, Riverland Community College Peter Scheffert, Riverland Community College Along

Score: What it Means to your Business Introduction Author Michael K. Swan, Washington State University Reviewers Gary Thome, Riverland Community College Peter Scheffert, Riverland Community College Along

Credit Cards. Annual Percentage Rate - What you are paying each month -- unpaid balances calculated as a percentage.

Credit Cards Annual Fee - Amount you pay each year to have a credit card. Annual Percentage Rate - What you are paying each month -- unpaid balances calculated as a percentage. Balance - The total charges

Credit Cards Annual Fee - Amount you pay each year to have a credit card. Annual Percentage Rate - What you are paying each month -- unpaid balances calculated as a percentage. Balance - The total charges

2/10/2015 CREDIT FOR SUCCESS TODAY S NEW RISK FACTORS MOBILE BANKING. The new Consumer Financial Protection Act, the ATR Rule (Ability to Repay Rule)

") CREDIT FOR SUCCESS TODAY S NEW RISK FACTORS Written and Presented by Serge Bevil, Credit Specialist VantagePoint Credit Corp. MOBILE BANKING We have become a social media society that wants information,

CREDIT FOR SUCCESS TODAY S NEW RISK FACTORS Written and Presented by Serge Bevil, Credit Specialist VantagePoint Credit Corp. MOBILE BANKING We have become a social media society that wants information,

DIVORCE AND YOUR C R E D I T

WHAT YOU NEED TO KNOW ABOUT DIVORCE AND YOUR C R E D I T DIVORCE MEDIATION CENTER RHODE ISLAND RHODE ISLAND 1296 Park Avenue, Cranston, RI 02910 401-228-8789 www.ridivorcemediationcenter.com The Truth

WHAT YOU NEED TO KNOW ABOUT DIVORCE AND YOUR C R E D I T DIVORCE MEDIATION CENTER RHODE ISLAND RHODE ISLAND 1296 Park Avenue, Cranston, RI 02910 401-228-8789 www.ridivorcemediationcenter.com The Truth

February 2015 Wednesday Webinar ~ Credit Matters - Resources to Educate Students About Credit and Debt

February 2015 Wednesday Webinar ~ Credit Matters - Resources to Educate Students About Credit and Debt 1 Mike Fagone Jennifer Pincus Jessica Whittier Bernstein Shur US Dept. of Justice FAME 2 About CARE

February 2015 Wednesday Webinar ~ Credit Matters - Resources to Educate Students About Credit and Debt 1 Mike Fagone Jennifer Pincus Jessica Whittier Bernstein Shur US Dept. of Justice FAME 2 About CARE

Homebuyer Guide Presented by:

Homebuyer Guide Presented by: HNB Mortgage 432-683-0081 www.hnbmortgage.com info@hnbmortgage.com Fax:(432)687-2612 NMLS: 205935 The basics What is a mortgage? A mortgage is a loan secured by real estate.

Homebuyer Guide Presented by: HNB Mortgage 432-683-0081 www.hnbmortgage.com info@hnbmortgage.com Fax:(432)687-2612 NMLS: 205935 The basics What is a mortgage? A mortgage is a loan secured by real estate.

UNDERSTANDING CREDIT. KASFAA Conference Manhattan, KS April 21, Robb Cummings Director of Business Development

UNDERSTANDING CREDIT KASFAA Conference Manhattan, KS April 21, 2016 Robb Cummings Director of Business Development FICO Score 2 A FICO Score is a three-digit number calculated from the credit information

UNDERSTANDING CREDIT KASFAA Conference Manhattan, KS April 21, 2016 Robb Cummings Director of Business Development FICO Score 2 A FICO Score is a three-digit number calculated from the credit information

UNDERSTANDING CREDIT. WASFAA Conference Seattle, WA Speakers: Thalassa Naylor, Sallie Mae Anthony Lombardi, Sallie Mae Date: April 10, 2017

UNDERSTANDING CREDIT WASFAA Conference Seattle, WA Speakers: Thalassa Naylor, Sallie Mae Anthony Lombardi, Sallie Mae Date: April 10, 2017 Agenda 2 Credit Management Protect Yourself Understanding Your

UNDERSTANDING CREDIT WASFAA Conference Seattle, WA Speakers: Thalassa Naylor, Sallie Mae Anthony Lombardi, Sallie Mae Date: April 10, 2017 Agenda 2 Credit Management Protect Yourself Understanding Your

What is credit and why does it matter to me?

Understanding Credit 1 Money Matters The BIG Idea What is credit and why does it matter to me? AGENDA Approx. 45 minutes I. Warm Up: What Do You Know About Credit? (10 minutes) II. Credit: The Good, The

Understanding Credit 1 Money Matters The BIG Idea What is credit and why does it matter to me? AGENDA Approx. 45 minutes I. Warm Up: What Do You Know About Credit? (10 minutes) II. Credit: The Good, The

Laura Mackie Mortgages. A Guide to Understanding and Rebuilding Your Credit Score

Laura Mackie Mortgages Your Credit Report A Guide to Understanding and Rebuilding Your Credit Score Introduction This guide is intended to help you improve your credit score and provide you with information

Laura Mackie Mortgages Your Credit Report A Guide to Understanding and Rebuilding Your Credit Score Introduction This guide is intended to help you improve your credit score and provide you with information

How to Stay Relevant in a Disruptive Lending Environment

How to Stay Relevant in a Disruptive Lending Environment Don Arkell CU Lending Advice Friday, June 10, 2016 2:15 p.m. Lending Attitude Check The best lenders learn that lending is both an attitude and

How to Stay Relevant in a Disruptive Lending Environment Don Arkell CU Lending Advice Friday, June 10, 2016 2:15 p.m. Lending Attitude Check The best lenders learn that lending is both an attitude and

How Much House Can You Afford?

03 4580 CH02 4/4/06 4:11 PM Page 15 How Much House Can You Afford? 2 Chapter In This Chapter Calculating your total income and monthly expenses Finding your appropriate price range or knowing how much

03 4580 CH02 4/4/06 4:11 PM Page 15 How Much House Can You Afford? 2 Chapter In This Chapter Calculating your total income and monthly expenses Finding your appropriate price range or knowing how much

Beyond the Classroom. Blaise P. Johnson Gate City Bank

Beyond the Classroom Blaise P. Johnson Gate City Bank 1 Topics To Be Discussed 1. Credit Reports & Credit Scores 2. Repayment/Consolidation of Student Loans 3. Obtaining A Personal or Home Loan 4. Open

Beyond the Classroom Blaise P. Johnson Gate City Bank 1 Topics To Be Discussed 1. Credit Reports & Credit Scores 2. Repayment/Consolidation of Student Loans 3. Obtaining A Personal or Home Loan 4. Open

TIP: Make sure this information is correct. A wrong address or phone number could be a mistake or a sign of identity theft.

Reading a Sample Credit Report This sample report shows what kind of information might appear on your own credit report, also called a consumer disclosure statement, from the 3 major Credit Reporting Agencies

Reading a Sample Credit Report This sample report shows what kind of information might appear on your own credit report, also called a consumer disclosure statement, from the 3 major Credit Reporting Agencies

Chapter 6 - Credit. Section 6.1

Chapter 6 - Credit Section 6.1 Credit is a medium of exchange which allows individuals to buy goods or services now and pay for them later The creditor supplies money, goods, or services in a credit agreement

Chapter 6 - Credit Section 6.1 Credit is a medium of exchange which allows individuals to buy goods or services now and pay for them later The creditor supplies money, goods, or services in a credit agreement

FICO Scores Decoded Discover How to Easily and Quickly Obtain Excellent FICO Credit Scores Regardless of Your Personal Credit Quality Now

Discover How to Easily and Quickly Obtain Excellent FICO Credit Scores Regardless of Your Personal Credit Quality Now Discover How to Easily and Quickly Obtain Excellent FICO Credit Scores Regardless of

Discover How to Easily and Quickly Obtain Excellent FICO Credit Scores Regardless of Your Personal Credit Quality Now Discover How to Easily and Quickly Obtain Excellent FICO Credit Scores Regardless of

Office of Student Financial Management

September 2015 Office of Student Financial Management Kasia Palm: Director of Student Financial Management What is Credit? - The ability to obtain goods/services before payment based on the trust that

September 2015 Office of Student Financial Management Kasia Palm: Director of Student Financial Management What is Credit? - The ability to obtain goods/services before payment based on the trust that

Chapter 26 11/9/2017 1

Chapter 26 11/9/2017 1 Average college students has 3 credit cards Also between $1500 & $2000 in debt Things to know if you re getting a credit card Who accepts it? What amount can you charge to meet your

Chapter 26 11/9/2017 1 Average college students has 3 credit cards Also between $1500 & $2000 in debt Things to know if you re getting a credit card Who accepts it? What amount can you charge to meet your

FICO Score Open Access Consumer Credit Education US Version. Frequently Asked Questions about the FICO Score

FICO Score Open Access Consumer Credit Education US Version Frequently Asked Questions about the FICO Score 2012 Fair Isaac Corporation. All rights reserved. 1 January 01, 2012 Table of Contents About

FICO Score Open Access Consumer Credit Education US Version Frequently Asked Questions about the FICO Score 2012 Fair Isaac Corporation. All rights reserved. 1 January 01, 2012 Table of Contents About

Your Credit Score 35% 10%

Your Credit Score A credit score is a complex mathematical model that evaluates many types of information in a credit file and displays the results as a number that reflects your credit risk level, typically

Your Credit Score A credit score is a complex mathematical model that evaluates many types of information in a credit file and displays the results as a number that reflects your credit risk level, typically

FINANCIAL FITNESS EDUCATION

(Agency s Name & Logo) FINANCIAL FITNESS EDUCATION Sponsored by BETTER FORTUNES Control Your Money Control Your Life Knowing the difference can make all the difference Chapter One ECONOMIC WAY OF THINKING

(Agency s Name & Logo) FINANCIAL FITNESS EDUCATION Sponsored by BETTER FORTUNES Control Your Money Control Your Life Knowing the difference can make all the difference Chapter One ECONOMIC WAY OF THINKING

Equifax Credit Report Personal Information Since xx/xx/xx FAD xx/xx/xx SSN Information Employment Beacon

PO Box 1386, Columbia, SC 29202 www.icscredit.com This document is provided only to assist new users in reading an Equifax Credit Report. It is not intended to be authoritative, and may not reflect the

PO Box 1386, Columbia, SC 29202 www.icscredit.com This document is provided only to assist new users in reading an Equifax Credit Report. It is not intended to be authoritative, and may not reflect the

What You Can Do to Improve Your Credit, Now

What You Can Do to Improve Your Credit, Now Provided compliments of: 1 What You Can Do to Improve Your Credit, Now Steps to Raise Your Score Now we re going to focus on certain steps that you can take,

What You Can Do to Improve Your Credit, Now Provided compliments of: 1 What You Can Do to Improve Your Credit, Now Steps to Raise Your Score Now we re going to focus on certain steps that you can take,

Understanding Your FICO Score

Understanding Your FICO Score Contents Your FICO Score A Vital Part of Your Credit Health............ 1 How FICO Scores Help You................ 2 Your Credit Report The Basis of Your FICO Score..............

Understanding Your FICO Score Contents Your FICO Score A Vital Part of Your Credit Health............ 1 How FICO Scores Help You................ 2 Your Credit Report The Basis of Your FICO Score..............

How to Find and Qualify for the Best Loan for Your Business

How to Find and Qualify for the Best Loan for Your Business With so many business loans available to you these days, where do you get started? What loan product is right for you, and how do you qualify

How to Find and Qualify for the Best Loan for Your Business With so many business loans available to you these days, where do you get started? What loan product is right for you, and how do you qualify

12 Steps to Improved Credit Steven K. Shapiro

12 Steps to Improved Credit Steven K. Shapiro 2009 2018 sks@skscci.com In my previous article, I wrote about becoming debt-free and buying everything with cash. Even while I was writing the article, I

12 Steps to Improved Credit Steven K. Shapiro 2009 2018 sks@skscci.com In my previous article, I wrote about becoming debt-free and buying everything with cash. Even while I was writing the article, I

Credit and Credit Cards

Credit and Credit Cards What s Next Project Credit Cards They are all around you. Most people have at least one. Some have many. They are credit cards. A credit card allows you to pay for merchandise or

Credit and Credit Cards What s Next Project Credit Cards They are all around you. Most people have at least one. Some have many. They are credit cards. A credit card allows you to pay for merchandise or

An Overview of Credit Report/Credit Score Models and a Proposal for Vietnam

VNU Journal of Science: Policy and Management Studies, Vol. 33, No. 2 (2017) 36-45 An Overview of Credit Report/Credit Score Models and a Proposal for Vietnam Le Duc Thinh * VNU International School, Building

VNU Journal of Science: Policy and Management Studies, Vol. 33, No. 2 (2017) 36-45 An Overview of Credit Report/Credit Score Models and a Proposal for Vietnam Le Duc Thinh * VNU International School, Building

Get Your Credit Mortgage Ready

Special Report Get Your Credit Mortgage Ready Compliments of: HowtoFixMyCredit.com Tel: 1-888-262-2123 Dear Home Buyer, If you re considering buying a home, then now would be a good time to check your

Special Report Get Your Credit Mortgage Ready Compliments of: HowtoFixMyCredit.com Tel: 1-888-262-2123 Dear Home Buyer, If you re considering buying a home, then now would be a good time to check your

Understanding Vehicle Financing

Understanding Vehicle Financing Understanding Vehicle Financing With prices averaging more than $31,000 for a new vehicle and $17,000 for a used model from a dealership, you might consider financing or

Understanding Vehicle Financing Understanding Vehicle Financing With prices averaging more than $31,000 for a new vehicle and $17,000 for a used model from a dealership, you might consider financing or

Twelve common questions. About consumer credit and direct marketing

Twelve common questions About consumer credit and direct marketing Twelve common questions Most of us don t think about credit until a specific event sparks our interest. Maybe we want to buy a car or

Twelve common questions About consumer credit and direct marketing Twelve common questions Most of us don t think about credit until a specific event sparks our interest. Maybe we want to buy a car or

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook Welcome! This workshop is about credit. Credit is buying something now, but paying for it later. Credit can be useful

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook Welcome! This workshop is about credit. Credit is buying something now, but paying for it later. Credit can be useful

c» BALANCE c» Financially Empowering You Credit Matters Podcast

Credit Matters Podcast [Music plays] Nikki: You re listening to Credit Matters. Hi. I m Nikki, your host for today s podcast. In today s world credit does matter. In fact, getting and using credit is part

Credit Matters Podcast [Music plays] Nikki: You re listening to Credit Matters. Hi. I m Nikki, your host for today s podcast. In today s world credit does matter. In fact, getting and using credit is part

12 common questions. About consumer credit and direct marketing

12 common questions About consumer credit and direct marketing Most of us don t think about credit until a specific event sparks our interest. Maybe we want to buy a car or home. Or perhaps we receive

12 common questions About consumer credit and direct marketing Most of us don t think about credit until a specific event sparks our interest. Maybe we want to buy a car or home. Or perhaps we receive

Asset Lending. Hard Money ASSET LENDING OR HARD MONEY

Asset Lending OR Hard Money ASSET LENDING OR HARD MONEY Asset Lending or Hard Money The purpose of this chapter is to introduce you to one of the most lucrative and least understood aspects of real estate

Asset Lending OR Hard Money ASSET LENDING OR HARD MONEY Asset Lending or Hard Money The purpose of this chapter is to introduce you to one of the most lucrative and least understood aspects of real estate

You re listening to rebuilding after a financial crisis. Hi, I m Niki, your host for today s Podcast.

Rebuilding After a Financial Crisis Podcast [Music plays] Nikki: You re listening to rebuilding after a financial crisis. Hi, I m Niki, your host for today s Podcast. There are many things in life that

Rebuilding After a Financial Crisis Podcast [Music plays] Nikki: You re listening to rebuilding after a financial crisis. Hi, I m Niki, your host for today s Podcast. There are many things in life that

Secrets to Success: Personal Finance Management

Secrets to Success: Personal Finance Management Harvard University Employees Credit Union (HUECU) A financial institution exclusively serving the Harvard University students, alumni, faculty, staff, and

Secrets to Success: Personal Finance Management Harvard University Employees Credit Union (HUECU) A financial institution exclusively serving the Harvard University students, alumni, faculty, staff, and

Credit Education Program

Credit Education Program Course Objectives Identify ways to decrease spending and increase income Read and understand the purpose of your credit report Discuss common debt traps to avoid How lenders evaluate

Credit Education Program Course Objectives Identify ways to decrease spending and increase income Read and understand the purpose of your credit report Discuss common debt traps to avoid How lenders evaluate

Making Money & Maximizing Opportunities in the Loan Application

Making Money & Maximizing Opportunities in the Loan Application USING THE CU*BASE LOAN ORIGINATION SYSTEM TO PROCESS LOAN APPLICATIONS CU*BASE LENDING TOOLS WEBINAR SERIES #3 OF 8 Today s Agenda 2 Intro

Making Money & Maximizing Opportunities in the Loan Application USING THE CU*BASE LOAN ORIGINATION SYSTEM TO PROCESS LOAN APPLICATIONS CU*BASE LENDING TOOLS WEBINAR SERIES #3 OF 8 Today s Agenda 2 Intro

Money Management Financial Survivor: Understanding Credit and Banking

Money Management Financial Survivor: Understanding Credit and Banking In this workshop, youth will learn about credit, the importance of maintaining good credit, and how to access their credit report.

Money Management Financial Survivor: Understanding Credit and Banking In this workshop, youth will learn about credit, the importance of maintaining good credit, and how to access their credit report.

Your Credit Score What It Means to You as a Prospective Home Buyer

Rachel Prevost Mortgage Loan Consultant L&G Mortgage Banc BK51263 Phone: (512) 924-3663 Fax: (480) 907-2839 rprevost@lgmortgagebanc.com www.lgmortgagebanc.com Your Credit Score What It Means to You as

Rachel Prevost Mortgage Loan Consultant L&G Mortgage Banc BK51263 Phone: (512) 924-3663 Fax: (480) 907-2839 rprevost@lgmortgagebanc.com www.lgmortgagebanc.com Your Credit Score What It Means to You as

Your Credit. Objectives. An Introduction to Personal Credit. By the end of this presentation you will have a understanding of: 1/19/2016.

Your Credit An Introduction to Personal Credit Objectives By the end of this presentation you will have a understanding of: Credit Score Where can I find it? What is it? How do I get it? Advantages of

Your Credit An Introduction to Personal Credit Objectives By the end of this presentation you will have a understanding of: Credit Score Where can I find it? What is it? How do I get it? Advantages of

The Newfi First-Time Homebuyer s Guide

The Newfi First-Time Homebuyer s Guide Newfi is a licensed tradename of Nexera Holding LLC. NMLS No. 1231327; HUD Lender ID 0038900004. Newfi is an Equal Housing Lender. The basics What is a mortgage?

The Newfi First-Time Homebuyer s Guide Newfi is a licensed tradename of Nexera Holding LLC. NMLS No. 1231327; HUD Lender ID 0038900004. Newfi is an Equal Housing Lender. The basics What is a mortgage?

Money 101 Presenter s Guide

For College Students Money 101 Presenter s Guide A Crash Course in Better Money Management For College Students Getting Started The What s My Score Money 101 presentation features six topics that should

For College Students Money 101 Presenter s Guide A Crash Course in Better Money Management For College Students Getting Started The What s My Score Money 101 presentation features six topics that should

FINANCIAL FOUNDATIONS

FINANCIAL FOUNDATIONS A Financial Beginnings Financial Education Program CREDIT Presenter's Guide Presented by Our Mission Financial Beginnings empowers youth and adults to take control of their financial

FINANCIAL FOUNDATIONS A Financial Beginnings Financial Education Program CREDIT Presenter's Guide Presented by Our Mission Financial Beginnings empowers youth and adults to take control of their financial

Keeping Finances Under Control. How to Manage Debt so it Doesn t Manage You

Keeping Finances Under Control How to Manage Debt so it Doesn t Manage You Seminar Objectives What is DEBT? What are the types of debt? What is good debt? What is bad debt? What are the benefits and costs?

Keeping Finances Under Control How to Manage Debt so it Doesn t Manage You Seminar Objectives What is DEBT? What are the types of debt? What is good debt? What is bad debt? What are the benefits and costs?

4 BIG REASONS YOU CAN T AFFORD TO IGNORE BUSINESS CREDIT!

SPECIAL REPORT: 4 BIG REASONS YOU CAN T AFFORD TO IGNORE BUSINESS CREDIT! Provided compliments of: 4 Big Reasons You Can t Afford To Ignore Business Credit Copyright 2012 All rights reserved. No part of

SPECIAL REPORT: 4 BIG REASONS YOU CAN T AFFORD TO IGNORE BUSINESS CREDIT! Provided compliments of: 4 Big Reasons You Can t Afford To Ignore Business Credit Copyright 2012 All rights reserved. No part of

Frequently Asked Questions For Rescore Express. You can update your report through the bureaus or.

Frequently Asked Questions For Rescore Express You can update your report through the bureaus or. USE OUR RESCORE EXPRESS PROGRAM TO QUICKLY AND ACCURATELY IMPROVE YOUR BORROWERS CREDIT SCORES! What is

Frequently Asked Questions For Rescore Express You can update your report through the bureaus or. USE OUR RESCORE EXPRESS PROGRAM TO QUICKLY AND ACCURATELY IMPROVE YOUR BORROWERS CREDIT SCORES! What is

Maximizing Purchasing Power: Make the Most of Your Credit Score

When life happens... Maximizing Purchasing Power: Make the Most of Your Credit Score Consolidated Credit Counseling Services, Inc. 5701 West Sunrise Boulevard Fort Lauderdale, FL 33313 1-800-210-3481 How

When life happens... Maximizing Purchasing Power: Make the Most of Your Credit Score Consolidated Credit Counseling Services, Inc. 5701 West Sunrise Boulevard Fort Lauderdale, FL 33313 1-800-210-3481 How

Does providing FICO Scores influence financial behavior?

Power of Our Past Force of Our Future Does providing FICO Scores influence financial behavior? October 2018 Jeff Johnston, MBA Sallie Mae Ohio Association of Student Financial Aid Administrators 50th Anniversary

Power of Our Past Force of Our Future Does providing FICO Scores influence financial behavior? October 2018 Jeff Johnston, MBA Sallie Mae Ohio Association of Student Financial Aid Administrators 50th Anniversary

Product Guide. What is the Platinum Discount Network? FIVE STAR PASS. TheCreditPros Services. Advantages: Selling Platinum Discount Network

Product Guide What is the Platinum Discount Network? The Platinum Discount Network is an exclusive member s only savings program that offers discounts on travel, retail, dining, personal services, free

Product Guide What is the Platinum Discount Network? The Platinum Discount Network is an exclusive member s only savings program that offers discounts on travel, retail, dining, personal services, free

Welcome. 1. Agenda. 2. Ground Rules. 3. Introductions. Charge It Right 2

Charge It Right Welcome 1. Agenda 2. Ground Rules 3. Introductions Charge It Right 2 Objectives Define credit Explain why credit is important Identify the factors creditors look for when making credit

Charge It Right Welcome 1. Agenda 2. Ground Rules 3. Introductions Charge It Right 2 Objectives Define credit Explain why credit is important Identify the factors creditors look for when making credit

How to Strategically Manage Your Debt

Debt. Funny how four little letters can feel so dirty. Most of us have it in one shape or another, but none of us like to talk about it. Debt can get us into trouble, especially if it is unplanned and

Debt. Funny how four little letters can feel so dirty. Most of us have it in one shape or another, but none of us like to talk about it. Debt can get us into trouble, especially if it is unplanned and

CREDIT SESSION OBJECTIVES SUBJECT INDEX

CREDIT SESSION OBJECTIVES In today s economy, it would be rare not to use credit to pay for large purchases, such as car repairs or any type of emergency situation. Credit can be an overwhelming topic,

CREDIT SESSION OBJECTIVES In today s economy, it would be rare not to use credit to pay for large purchases, such as car repairs or any type of emergency situation. Credit can be an overwhelming topic,

FarmHouse International Fraternity New Member Education Program Topic Summary: Personal Finance

FarmHouse International Fraternity New Member Education Program Topic Summary: Personal Finance 11 College is a challenging time both in and out of class. As a student you are coping with a new environment

FarmHouse International Fraternity New Member Education Program Topic Summary: Personal Finance 11 College is a challenging time both in and out of class. As a student you are coping with a new environment

Essential Facts for Students Carol A. Carolan, Ph.D.

The ABCs of Credit Card Finance Essential Facts for Students Carol A. Carolan, Ph.D. HOW LONG AND HOW MUCH DO I HAVE TO PAY? By using the following chart you can find out your total payoff time and total

The ABCs of Credit Card Finance Essential Facts for Students Carol A. Carolan, Ph.D. HOW LONG AND HOW MUCH DO I HAVE TO PAY? By using the following chart you can find out your total payoff time and total

Drive Away Happy: Car Buying Decisions

Drive Away Happy: Car Buying Decisions Buy new, buy used, or lease? These are just a few of the many decisions you ll need to make before happily driving away with a vehicle. While shopping for a car or

Drive Away Happy: Car Buying Decisions Buy new, buy used, or lease? These are just a few of the many decisions you ll need to make before happily driving away with a vehicle. While shopping for a car or

MODULE 4 // HOW CREDITWORTHY ARE YOU? WORLD CLASS: AGES 18+

MODULE 4 // HOW CREDITWORTHY ARE YOU? WORLD CLASS: AGES 18+ MODULE 4 // FINANCIAL SOCCER PROGRAM Financial Soccer is an educational video game designed to help students learn more about the fundamentals

MODULE 4 // HOW CREDITWORTHY ARE YOU? WORLD CLASS: AGES 18+ MODULE 4 // FINANCIAL SOCCER PROGRAM Financial Soccer is an educational video game designed to help students learn more about the fundamentals

RETAIL BANKING. Consumer Lending. David Kemp President Bankers Management, Inc. McDonough, GA

RETAIL BANKING Consumer Lending David Kemp President McDonough, GA bankers3@inbox.com 770-909-6004 August 7, 2018 Graduate School of Banking 2018 Presented By: David L. Kemp: BMI 2016 2015 2014 2013 2012

RETAIL BANKING Consumer Lending David Kemp President McDonough, GA bankers3@inbox.com 770-909-6004 August 7, 2018 Graduate School of Banking 2018 Presented By: David L. Kemp: BMI 2016 2015 2014 2013 2012

Fixing Bad Credit and Solving Credit Problems 1

FCS 5049 Fixing Bad Credit and Solving Credit Problems 1 Mary N. Harrison 2 When you want to buy a car, a house, or other expensive items you probably expect to use credit. For smaller purchases, your

FCS 5049 Fixing Bad Credit and Solving Credit Problems 1 Mary N. Harrison 2 When you want to buy a car, a house, or other expensive items you probably expect to use credit. For smaller purchases, your

Be Credit Wise Credit is a way of having something now and paying for it later. Many

Be Credit Wise Credit is a way of having something now and paying for it later. Many of us want to take advantage of flexibility in our spending plans by using credit. Credit isn t free; it s paid for

Be Credit Wise Credit is a way of having something now and paying for it later. Many of us want to take advantage of flexibility in our spending plans by using credit. Credit isn t free; it s paid for

Financial Well-being. Debt and Credit

Financial Well-being Debt and Credit Debt and Credit When evaluating financial wellness, debt has a real impact on your ability to reach your goals. Debt feels like a four letter word. However, it can

Financial Well-being Debt and Credit Debt and Credit When evaluating financial wellness, debt has a real impact on your ability to reach your goals. Debt feels like a four letter word. However, it can

UNDERSTANDING BUSINESS CREDIT

YOUR GUIDE TO UNDERSTANDING BUSINESS CREDIT POOR YOUR BUSINESS CREDIT PROFILE GOOD SPONSORED BY UNDERSTANDING YOUR PERSONAL CREDIT PROFILE Every small business owner has two credit profiles: 1. Your personal

YOUR GUIDE TO UNDERSTANDING BUSINESS CREDIT POOR YOUR BUSINESS CREDIT PROFILE GOOD SPONSORED BY UNDERSTANDING YOUR PERSONAL CREDIT PROFILE Every small business owner has two credit profiles: 1. Your personal

Count Balance $0.00 $0.00 $0.00 Current Delinquent Other 0 0 0

COLLECTION ACCOUNTS: Count 0 0 0 Balance $0.00 $0.00 $0.00 Current 0 0 0 Delinquent 0 0 0 Other 0 0 0 TOTAL ACCOUNTS: Count 5 5 5 Balance $0.00 $0.00 $0.00 Current 5 5 5 Delinquent 0 0 0 Other 0 0 0 ACCOUNTS

COLLECTION ACCOUNTS: Count 0 0 0 Balance $0.00 $0.00 $0.00 Current 0 0 0 Delinquent 0 0 0 Other 0 0 0 TOTAL ACCOUNTS: Count 5 5 5 Balance $0.00 $0.00 $0.00 Current 5 5 5 Delinquent 0 0 0 Other 0 0 0 ACCOUNTS

Fact, Fiction & FICOs: Presented by: Vance Edwards, CMB Certified FICO Professional MGIC Marketing Program Director

Fact, Fiction & FICOs: Presented by: Vance Edwards, CMB Certified FICO Professional MGIC Marketing Program Director Agenda What makes up a credit score (and what doesn t) What causes that score to move

Fact, Fiction & FICOs: Presented by: Vance Edwards, CMB Certified FICO Professional MGIC Marketing Program Director Agenda What makes up a credit score (and what doesn t) What causes that score to move