Money Management Curriculum

|

|

|

- Nora Melissa Burke

- 5 years ago

- Views:

Transcription

and Stuart T. Nakamoto (University of Hawaii), content.")

and do not")

1 Money Management Module 4: Credit Reports & Credit Scores Money Management Curriculum Module 4: Credit Reports & Credit Scores Project Team: Ruby Ward, Professor, Utah State University Trent Teegerstrom, Associate Director of Tribal Extension, University of Arizona Karli Salisbury, Research Associate, Utah State University Kynda Curtis, Professor, Utah State University Staci Emm, Extension Educator and Professor, University of Nevada Reno Carol Bishop, Extension Educator and Associate Professor, University of Nevada Reno Each university is an affirmative action/equal opportunity institutions Acknowledgments: Vicki Hebb, reviewing content, and Russ Tronstad (University of Arizona) and Stuart T. Nakamoto (University of Hawaii), content. This material is based upon work that is supported by the National Institute of Food and Agriculture, U.S. Department of Agriculture, under award number through the Western Sustainable Agriculture Research and Education program under subaward number EW USDA is an equal opportunity employer and service provider. Any opinions, findings, conclusions, or recommendations expressed in this publication are those of the author(s) and do not necessarily reflect the view of the U.S. Department of Agriculture. Diverseag.org

2 Money Management Module 4: Credit Reports & Credit Scores Teaching Notes: This module explains credit scores and credit reports, accessing and understanding them. Banks and lenders use FICO scores (a specific credit score) to measure the risk of lending to someone. Credit scores indicate the level of borrower risk: higher scores indicate lower risk and lower scores indicate higher risk. If the risk is too high, the lender may not approve the loan. This module covers what FICO scores are, their importance and how they are determined. Credit reports from the three reporting bureaus are used to determine the score. The score can impact whether or not you are able to rent an apartment or are selected for a job. They can also work in your favor: for example, having high scores might mean little to no interest is paid for installment purchases. Understanding your scores and what is on your credit reports BEFORE you apply for a loan, credit card or even a job can help to negotiate rates and terms. The 5 components of a FICO score are: 35% Payment History 30% Total Debt 15% Length of Credit History 10% Credit Mix 10% New Credit Credit reports come from the three major credit bureaus: Experian Equifax TransUnion The only truly free online credit reports are obtained through This site was mandated by the US government and a report from each of the 3 major bureaus is available each year. All three reports can be obtained at once, or they can be spaced out over the 12 months to have more of a running report. These credit reports will not list your actual credit score. They provide the information that is used to calculate your credit score. They should be checked regardless of the FICO score to ensure accuracy and the lack of fraud. There is no quick fix to a bad accurate report. Many fraudulent credit repair companies exist, but reputable help is available. Credit scores are available from many credit card companies. Discover Scorecard is a free source to get your credit score. It will provide your credit score card. Some places offering to provide a free credit score also provide a lot of credit card and loan offers. It might be helpful to pull up the example credit reports and scores Remind your students to keep track of their cash flows and budgets; if they have an accurate budget they may find that they are able to use that to schedule the repayment of any debt. They can also use credit to buy the things they want and pay off the debt monthly to not incur interest expense. If Diverseag.org

3 Money Management Module 4: Credit Reports & Credit Scores applying for a loan is necessary, they already have an idea of where they stand in the eyes of a lender and can negotiate terms. Educational Objectives: Understand what determines a FICO score Understand how to access and correct a credit report Understand how to rebuild credit Discussion Topics: What is a FICO score? What are the benefits and/or drawbacks of a high or low score? What actions can you take that would affect your credit score? How are FICO scores and credit reports related? What should I do if I believe my identity has been compromised? Resources: Worksheets: None Other: Sample credit reports and credit scores for the same person pulled on Outline: 1. Key Concepts 2. FICO Score Background 3. FICO Score Considerations and Requirements 4. FICO Score Components a. Payment History b. Total Debt c. Length of Credit History d. Credit Mix e. New Credit 5. Where to Find Your Score 6. Why Your Score Matters 7. Credit Reports a. Accessing the Repot b. Evaluating the Report 8. Identity Theft 9. Strategies to Improve Credit 10. Reminder to Keep Track of Your Budgeting Exercise Diverseag.org

4 Managing Money Curriculum Module 4: Credit Reports & Credit Scores The importance of keeping track of your information 1 Project Team: Ruby Ward, Professor, Utah State University Trent Teegerstrom, Associate Director of Tribal Extension, University of Arizona Karli Salisbury, Research Associate, Utah State University Kynda Curtis, Professor, Utah State University Staci Emm, Extension Educator and Professor, University of Nevada Reno Carol Bishop, Extension Educator and Associate Professor, University of Nevada Reno Acknowledgments: Vicki Hebb, reviewing content, and Russ Tronstad and Stuart Nakamoto, content. This material is based upon work that is supported by the National Institute of Food and Agriculture, U.S. Department of Agriculture, under award number through the Western Sustainable Agriculture Research and Education program under subaward number EW USDA is an equal opportunity employer and service provider. Any opinions, findings, conclusions, or recommendations expressed in this publication are those of the author(s) and do not necessarily reflect the view of the U.S. Department of Agriculture. Each university is an affirmative action/equal opportunity institution 2 Key Concepts What Is A FICO Score? What Is A Good Credit Score? How Is My Credit Score Calculated? What Is A Credit Report? Getting and Checking My Credit Report What To Do If You Are A Victim Of Identity Theft Strategies To Improve Credit 3

5 FICO Score FICO is an analytics software company that compiles credit data from various credit reporting agencies. They use that data to run math algorithms and create a score. FICO Scores are the credit scores used by 90% of top lenders to determine your credit risk. Lenders want to know the risk they re taking by lending you money. For example: How likely someone is to pay their bills on time? Can they handle a larger line of credit? Slide 4: FICO (Fair Isaac Corporation); FICO is in 90+ countries worldwide; they have been in business since % of the largest financial institutions in the US and all the 100 largest U.S. credit card issuers are FICO Clients. 4 FICO Scores DO NOT Consider Your race, color, religion, national origin, sex, or marital status. Your age. Your salary, occupation, title, employer, date employed, or employment history.(lenders may consider this information, however) Where you live. Any interest rate being charged on a particular credit card or other account. Any items reported as child/family support obligations. Certain types of inquiries (requests for your credit report). Any information not found in your credit report. Any information that is not proven to be predictive of future credit performance. Whether or not you are participating in credit counseling of any kind. 5 Slide 5: US law prohibits credit scoring from considering these facts, as well as any receipt of public assistance, or the exercise of any consumer right under the Consumer Credit Protection Act. Your scores do not count consumer-initiated inquiries requests you have made for your credit report, in order to check it. They also do not count promotional inquiries requests made by lenders in order to make you a preapproved credit offer or administrative inquiries requests made by lenders to review your account with them. Requests that are marked as coming from employers are not counted either. Score Calculation Scores based on data from credit reports Separate FICO score for each of the three credit bureaus Higher is better For valid score, the credit report must have: At least one account opened for six months or more, and At least one account that has been reported to the credit bureau within the past six months, and No indication of deceased on the credit report Slide 6: (Please note, if you share an account with another person this may affect you if the other account holder is reported deceased). The minimum scoring criteria may be satisfied by a single account or by multiple accounts on a credit file. 6

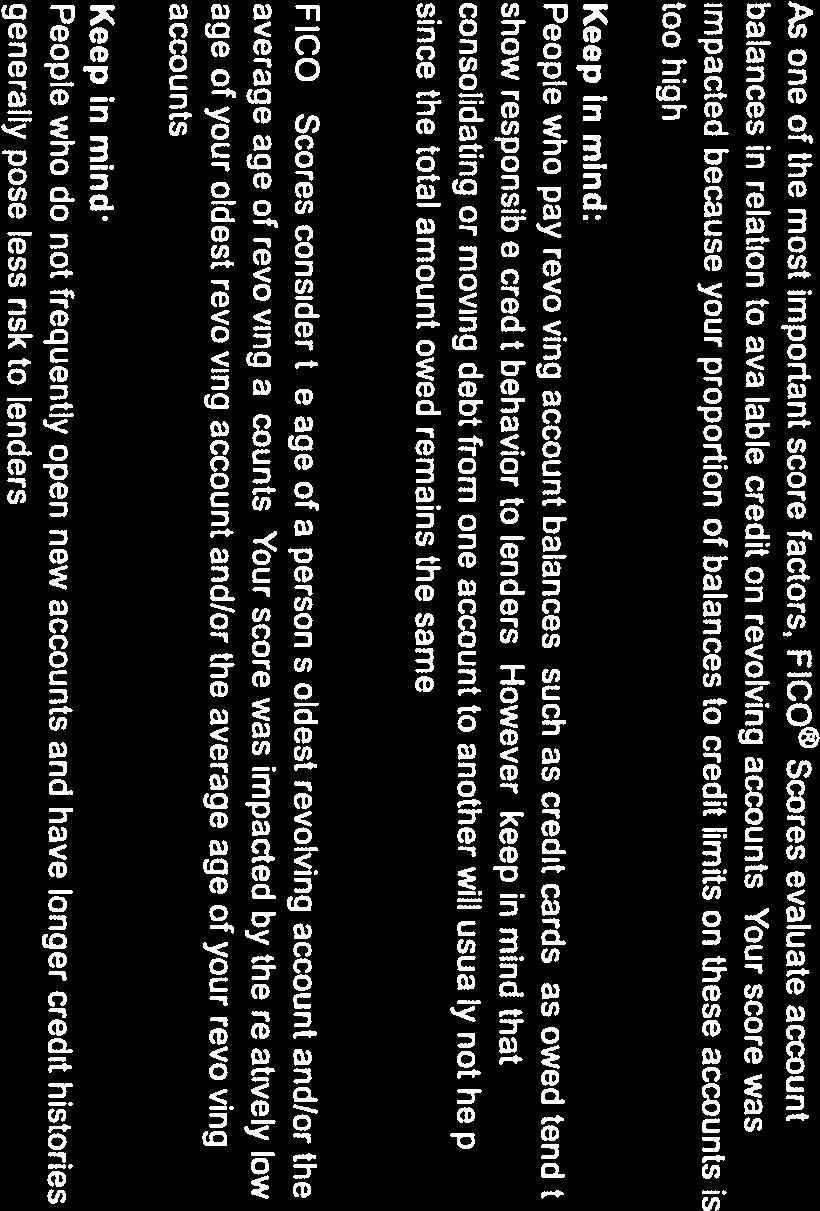

6 FICO Score Components FICO scores based on these 5 categories: 35% Payment History 30% Total Debt 15% Length of Credit History 10% Credit Mix 10% New Credit Slide 7: For some groups, the importance of these categories may vary; for example, people who have not been using credit long will be factored differently than those with a longer credit history. The levels of importance shown in the FICO Scores chart are for the general population, and will be different for different credit profiles. 7 Payment History 35% Paying on time one of the most important factors. Overall good credit more important than missing one or two payments. Payment history includes: credit cards, retail accounts, installment loans and mortgage loans. Negative factors: bankruptcies, foreclosures, lawsuits, wage attachments, liens, and judgements. Late or missed payments: how late, how much owed, how recent, and how many. 8 Slide 8: The first thing any lender wants to know is whether you ve paid past credit accounts on time. A few late payments are not an automatic "score-killer. Payments NOT considered- rent, utilities, etc-unless they go to collections. With collections, older items and items with small amounts will count less than recent items or those with larger amounts. Bankruptcies will stay on your credit report for 7 to 10 years. The FICO scoring formula treats both Chapter 7 and Chapter 13 Bankruptcies similarly in terms of how they affect one's FICO score. Total Debt 30% Amount owed on all accounts Amount owed on different types of accounts Credit utilization on revolving accounts (how much of your available credit you are using) High percentage- negative impacts Low percentage- positive impacts- in some cases, better than not using any of your available credit Someone who is close to "maxing out" several credit cards has a high credit utilization ratio and may have trouble making payments in the future. 9 Slide 9: When a high percentage of a person's available credit is been used, this can indicate that a person is overextended, and is more likely to make late or missed payments. It's also important to note that your current account balance isn't necessarily the balance that shows up on your credit report and factors into your FICO Scores. Your account balance on your credit report will reflect the account balance your lender reported to the credit bureau (typically the balance from your latest monthly statement). So even if you pay your credit card balances in full each month, your account balance won t necessarily show on your credit report as $0. Paying down installment loans is a good sign that you're able and willing to manage and repay debt.

7 Length of Credit History 15% Longer credit history will increase score BUT new users will not necessarily be negatively impacted Age of oldest account Age of newest account Average age of all accounts Use of certain accounts 10 Credit Mix 10% Mix of credit cards, retail accounts, installment loans, finance company accounts, and mortgage loans will be considered. Has your credit experience been only one type? Don t open accounts you won t use. Can raise FICO score by having credit cards and installment loans with a good payment history. Slide 11: It's not necessary to have one of each. The credit mix usually won t be a key factor in determining your FICO Scores but it will be more important if your credit report does not have a lot of other information on which to base a score. People with no credit cards tend to be viewed as a higher risk than people who have managed credit cards responsibly. A closed account still shows on your report. How many is too many will vary depending on your overall credit picture. 11 New Credit 10% Don t open a lot of new accounts quickly Opening several new accounts in short amount of time represents risk How many recent inquiries there are (when a lender makes a request for your credit report or score) Inquiries are on your report for 2 years but only impact your FICO score for 12 months Slide 12: Looking for new credit can equate with higher risk, but most Credit Scores are not affected by loans that commonly involve rate-shopping, such as mortgage, auto and student loan lenders within a short period of time. Typically, these are treated as a single inquiry and will have little impact on your credit scores. If you need a loan, do your rate shopping within a focused period of time, such as 30 days. 12

8 Good, Bad or Ugly? Scores usually range from 300 to Why Should You Care? Compare Costs on a New Vehicle Credit Score of 730+ Car Cost: $30,000 Rate: 2.99% Term: 60 Months Total Cost: $32,335 Credit Score of 679- Car Cost: $30,000 Rate: 7.25% Term: 60 Months Total Cost: $35,855 A 51 Point Difference Will Cost You $3,520! 14 What Would You Do With An Extra $3,500? 15

9 Where s My Score? Most banking institutions offer a free score, especially to those with credit cards Bank of America- select cardholders - Transunion Citibank Citibank branded cardholders- Equifax Chase Chase Slate cardholders- Experian Walmart/Sam s Club- cardholders- Transunion USAA- all credit card holders- Experian Discover- May 20, 2016 new service called Discover Credit Scorecard. You do not need to be a customer of Discover anyone can get their official FICO score for free. This is the first place where anyone, not just a Discover customer, can get their official Experian FICO for free. 16 Slide 17: Identifying factors are not used in credit scoring. Credit accounts are known in the business as trade lines; lenders report on each account you have established with them. When you apply for a loan, you authorize your lender to ask for a copy of your credit report. This is how inquiries appear on your credit report. The inquiries section contains a list of everyone who accessed your credit report within the last two years. The report you see lists both "voluntary" inquiries, spurred by your own requests for credit, and "involuntary" inquires, such as when lenders order your report so as to make you a pre-approved credit offer in the mail. Public record information includes bankruptcies, foreclosures, suits, wage attachments, liens, and judgments. My Credit Report What s in it? Identifying information Name, address, social security, date of birth, etc. Credit accounts reported by lenders Type of account, date opened, credit limit, account balance and payment history Credit inquiries Within last two years- voluntary and involuntary Public record and collections State and county courts, overdue debt from collection agencies Accessing Your Report Three credit reporting agencies: Equifax TransUnion Experian Can get free copy once every 12 months You may order all at the same time, or from each of the companies one at a time. ONLY through annualcreditreport.com or by calling Slide 18: Do not contact the three nationwide credit reporting companies individually. They are providing free annual credit reports only through annualcreditreport.com, or mailing to Annual Credit Report Request Service. Only one website is authorized to fill orders for the free annual credit report you are entitled to under law annualcreditreport.com. Other websites that claim to offer free credit reports, free credit scores, or free credit monitoring are not part of the legally mandated free annual credit report program. Some imposter sites use terms like free report in their names; others have URLs that purposely misspell annualcreditreport.com in the hope that you will mistype the name of the official site. Some of these imposter sites direct you to other sites that try to sell you something or collect your personal information. 18

10 Why Do I Need It? Your credit report has information that affects whether you can get a loan and how much you will have to pay to borrow money. You want a copy of your credit report to: make sure the information is accurate, complete, and up-to-date before you apply for a loan for a major purchase like a house or car, buy insurance, or apply for a job help guard against identity theft. That s when someone uses your personal information like your name, your Social Security number, or your credit card number to commit fraud. 19 Evaluating Your Report To protect the security of your personal information, you may be asked a series of questions that only you would know, like your monthly mortgage payment If you request your report online at annualcreditreport.com, you should be able to access it immediately. Three Things to Look For: Is your information accurate? What are your balances? Are there any creditors on your report that you supposedly owe that you don t remember doing business with? 20 Fixing Errors All 3 credit bureaus accept filing disputes online Contact the bureau and the creditor Sample letter available at: Will be investigated within 30 days Will receive the written results and a free copy of your revised report 21 Slide 21: 1. Tell the credit reporting company, in writing, what information you think is inaccurate. 2. Tell the creditor or other information provider in writing that you dispute an item. When the investigation is complete, the credit reporting company must give you the written results and a free copy of your report if the dispute results in a change. (This free report does not count as your annual free report.) If an investigation doesn t resolve your dispute with the credit reporting company, you can ask that a statement of the dispute be included in your file and in future reports

11 Identity Theft If you know there has been I.D. theft contact: EQUIFAX: ; EXPERIAN: ; TRANSUNION: ; Can t Pay Bills On Time? Slide 23: First bill usually paid is cellphone! Contact the companies that you owe to work out a repayment plan Create a budget and stick to it Pay your home and car loans first If you know you cannot make your car payment, try to sell your car first. DO NOT have it repossessed if you can avoid it. 23 How Long Does A Repo Affect Your Credit? 7 To 10 YEARS! 24

12 Don t feel like this guy the next time you go to apply for a loan. 25 Improving Your Score Fix errors When negative information in your report is accurate, only time can make it go away Beware of any advice that claims to improve your credit score fast. Reputable credit counseling organizations Slide 26: The Credit Repair Organization Act (CROA) makes it illegal for credit repair companies to lie about what they can do for you, and to charge you before they've performed their services. There is help out there to get your credit score on track 26 Tips and Strategies (From myfico.com) Right Now Check your credit report Set up payment reminders Reduce the amount of debt you owe Payment History Tips Pay your bills on time If you have missed payments, get current and stay current. If you are having trouble making ends meet, contact your creditors or see a legitimate credit counselor. 27

13 Tips and Strategies (From myfico.com) Amounts Owed Tips Keep balances low on credit cards and other "revolving credit". Pay off debt rather than moving it around. Don't open a number of new credit cards that you don't need, just to increase your available credit. Length of Credit History Tips If you have been managing credit for a short time, don't open a lot of new accounts too rapidly. 28 Tips and Strategies (From myfico.com) New Credit Tips Do your rate shopping for a given loan within a focused period of time. Re-establish your credit history if you have had problems. Note that it's OK to request and check your own credit report. Types of Credit Use Tips Apply for and open new credit accounts only as needed. Have credit cards but manage them responsibly. Slide 29: Note that closing an account doesn't make it go away. A closed account will still show up on your credit report, and may be considered by a score. 29 Homework Assignments: 1. Use to request and print at least one report from one of the credit bureaus 2. Use Discover Credit Scorecard or your bank website to get your free FICO score 30

14 Questions? 31

15

16

17

18

19

Money Management Curriculum

Module 2: Loans and Credit Cards Money Management Curriculum Module 2: Loans and Credit Cards Project Team: Ruby Ward, Professor, Utah State University Trent Teegerstrom, Associate Director of Tribal Extension,

Module 2: Loans and Credit Cards Money Management Curriculum Module 2: Loans and Credit Cards Project Team: Ruby Ward, Professor, Utah State University Trent Teegerstrom, Associate Director of Tribal Extension,

Understanding Your FICO Score. Understanding FICO Scores

Understanding Your FICO Score Understanding FICO Scores 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Reports

Understanding Your FICO Score Understanding FICO Scores 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Reports

Money Management Curriculum

Money Management Module 5: Savings and Budgeting Money Management Curriculum Module 5: Savings and Budgeting Budgeting Project Team: Ruby Ward, Professor, Utah State University Trent Teegerstrom, Associate

Money Management Module 5: Savings and Budgeting Money Management Curriculum Module 5: Savings and Budgeting Budgeting Project Team: Ruby Ward, Professor, Utah State University Trent Teegerstrom, Associate

Credit Reports 101. Bill Bufkins, November 3, 2011

Credit Reports 101 Bill Bufkins, November 3, 2011 What is a credit report? A credit report is a record of your past borrowing and repayment activity. The information in your credit report helps determine

Credit Reports 101 Bill Bufkins, November 3, 2011 What is a credit report? A credit report is a record of your past borrowing and repayment activity. The information in your credit report helps determine

GREENPATH FINANCIAL WELLNESS SERIES

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Empowering people to lead financially healthy lives. TABLE OF CONTENTS Understanding credit reports...2 What s in a credit

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Empowering people to lead financially healthy lives. TABLE OF CONTENTS Understanding credit reports...2 What s in a credit

UNDERSTANDING YOUR CREDIT REPORT & YOUR CREDIT SCORE

UNDERSTANDING YOUR CREDIT REPORT & YOUR CREDIT SCORE Presented By: Tom Painter Chief Lending Officer WHAT IS A CREDIT SCORE? A credit score is a number that summarizes your credit risk, based on a snapshot

UNDERSTANDING YOUR CREDIT REPORT & YOUR CREDIT SCORE Presented By: Tom Painter Chief Lending Officer WHAT IS A CREDIT SCORE? A credit score is a number that summarizes your credit risk, based on a snapshot

Reviewing C YouR CRedit RepoRt

ChapteR 2 Reviewing C YouR CRedit RepoRt What do your creditors have to say about the way you handle money? Having a good credit score can help you turn your home-buying dream into a reality. There s much

ChapteR 2 Reviewing C YouR CRedit RepoRt What do your creditors have to say about the way you handle money? Having a good credit score can help you turn your home-buying dream into a reality. There s much

UNDERSTANDING CREDIT. KASFAA Conference Manhattan, KS April 21, Robb Cummings Director of Business Development

UNDERSTANDING CREDIT KASFAA Conference Manhattan, KS April 21, 2016 Robb Cummings Director of Business Development FICO Score 2 A FICO Score is a three-digit number calculated from the credit information

UNDERSTANDING CREDIT KASFAA Conference Manhattan, KS April 21, 2016 Robb Cummings Director of Business Development FICO Score 2 A FICO Score is a three-digit number calculated from the credit information

Understanding Your FICO Score

Understanding Your FICO Score Contents Your FICO Score A Vital Part of Your Credit Health............ 1 How FICO Scores Help You................ 2 Your Credit Report The Basis of Your FICO Score..............

Understanding Your FICO Score Contents Your FICO Score A Vital Part of Your Credit Health............ 1 How FICO Scores Help You................ 2 Your Credit Report The Basis of Your FICO Score..............

Understanding Credit. What it is, why it s important, and how you can maintain it. Brought to you by Sallie Mae and FICO

Understanding Credit What it is, why it s important, and how you can maintain it Brought to you by Sallie Mae and FICO Introduction A student loan may be your first major credit experience. This is a good

Understanding Credit What it is, why it s important, and how you can maintain it Brought to you by Sallie Mae and FICO Introduction A student loan may be your first major credit experience. This is a good

Understanding. What you need to know about the most widely used credit scores

Understanding What you need to know about the most widely used credit scores 300 850 The score lenders use. FICO Scores are the most widely used credit scores according to a recent CEB TowerGroup analyst

Understanding What you need to know about the most widely used credit scores 300 850 The score lenders use. FICO Scores are the most widely used credit scores according to a recent CEB TowerGroup analyst

Federal Reserve Bank of Philadelphia

Federal Reserve Bank of Philadelphia 1 When you apply for credit, whether it s a credit card, car loan, or a mortgage, lenders want to know whether you are likely to repay your loan and make the payments

Federal Reserve Bank of Philadelphia 1 When you apply for credit, whether it s a credit card, car loan, or a mortgage, lenders want to know whether you are likely to repay your loan and make the payments

Your Credit Score 35% 10%

Your Credit Score A credit score is a complex mathematical model that evaluates many types of information in a credit file and displays the results as a number that reflects your credit risk level, typically

Your Credit Score A credit score is a complex mathematical model that evaluates many types of information in a credit file and displays the results as a number that reflects your credit risk level, typically

Understanding Credit. Lisa Mitchell, Sallie Mae April 6, Champions of Financial Aid ILASFAA Conference

Understanding Credit Lisa Mitchell, Sallie Mae April 6, 2017 Credit Management Agenda Understanding Your Credit Report Summary: Financial Health Tips Credit Management Credit Basics Credit health plays

Understanding Credit Lisa Mitchell, Sallie Mae April 6, 2017 Credit Management Agenda Understanding Your Credit Report Summary: Financial Health Tips Credit Management Credit Basics Credit health plays

TABLE OF CONTENTS. Healthier Black Elders Center

TABLE OF CONTENTS What is credit............................................1 The five C s of credit...................................... 2 Types of credit...........................................3

TABLE OF CONTENTS What is credit............................................1 The five C s of credit...................................... 2 Types of credit...........................................3

Understanding Credit

Understanding Credit LAURA STEINBECK DIRECTOR OF BUSINESS DEVELOPMENT, SALLIE MAE 2018 MASFAP CONFERENCE Agenda 2 Credit Management Protect Yourself Understanding Credit Reports Summary: Financial Health

Understanding Credit LAURA STEINBECK DIRECTOR OF BUSINESS DEVELOPMENT, SALLIE MAE 2018 MASFAP CONFERENCE Agenda 2 Credit Management Protect Yourself Understanding Credit Reports Summary: Financial Health

Credit Score: What it Means to your Business

Score: What it Means to your Business Introduction Author Michael K. Swan, Washington State University Reviewers Gary Thome, Riverland Community College Peter Scheffert, Riverland Community College Along

Score: What it Means to your Business Introduction Author Michael K. Swan, Washington State University Reviewers Gary Thome, Riverland Community College Peter Scheffert, Riverland Community College Along

c» BALANCE C:» Financially Empowering You The World of Credit Reports Podcast [Music plays] Nikki:

![c» BALANCE C:» Financially Empowering You The World of Credit Reports Podcast [Music plays] Nikki:](/thumbs/76/73531259.jpg "c» BALANCE C:» Financially Empowering You The World of Credit Reports Podcast [Music plays] Nikki:") The World of Credit Reports Podcast [Music plays] Nikki: You re listening to world of credit. Hi, I m Nikki, your host for today s podcast. Credit reports and credit scores influence our lives in many

The World of Credit Reports Podcast [Music plays] Nikki: You re listening to world of credit. Hi, I m Nikki, your host for today s podcast. Credit reports and credit scores influence our lives in many

UNDERSTANDING CREDIT. WASFAA Conference Seattle, WA Speakers: Thalassa Naylor, Sallie Mae Anthony Lombardi, Sallie Mae Date: April 10, 2017

UNDERSTANDING CREDIT WASFAA Conference Seattle, WA Speakers: Thalassa Naylor, Sallie Mae Anthony Lombardi, Sallie Mae Date: April 10, 2017 Agenda 2 Credit Management Protect Yourself Understanding Your

UNDERSTANDING CREDIT WASFAA Conference Seattle, WA Speakers: Thalassa Naylor, Sallie Mae Anthony Lombardi, Sallie Mae Date: April 10, 2017 Agenda 2 Credit Management Protect Yourself Understanding Your

A CONSUMER S GUIDE TO INSURANCE COMPANIES' USE OF CREDIT INFORMATION

A CONSUMER S GUIDE TO INSURANCE COMPANIES' USE OF CREDIT INFORMATION INSURANCE CREDIT SCORING IN NORTH CAROLINA Insurance companies licensed to sell private passenger automobile and residential property

A CONSUMER S GUIDE TO INSURANCE COMPANIES' USE OF CREDIT INFORMATION INSURANCE CREDIT SCORING IN NORTH CAROLINA Insurance companies licensed to sell private passenger automobile and residential property

Introduction. In short- credit is an essential part of our personal and national economic stability.

Table of Contents 2 Introduction 3 The Wait Is Over!. 4 The Five Factors that Determine your FICO Score Are: 5 What is Seasoned Trade Lines?... 7 How Do I Raise My FICO Score with Seasoned Trade Lines.

Table of Contents 2 Introduction 3 The Wait Is Over!. 4 The Five Factors that Determine your FICO Score Are: 5 What is Seasoned Trade Lines?... 7 How Do I Raise My FICO Score with Seasoned Trade Lines.

ECONOMIC EDUCATION FOR CONSUMERS Chapter 10

WHAT S AHEAD 10.1 What Is Credit? 10.2 How to Qualify for Credit 10.3 Sources of Consumer Credit 10.4 Credit Rights and Responsibilities 10.5 Maintain a Good Credit Rating LESSON 10.1 What Is Credit? GOALS

WHAT S AHEAD 10.1 What Is Credit? 10.2 How to Qualify for Credit 10.3 Sources of Consumer Credit 10.4 Credit Rights and Responsibilities 10.5 Maintain a Good Credit Rating LESSON 10.1 What Is Credit? GOALS

HOW TO USE CREDIT. Latino Community Credit Union & the Latino Community Development Center.

HOW TO USE CREDIT Latino Community Credit Union & the Latino Community Development Center www.latinoccu.org Copyright 2016 Latino Community Credit Union Made possible by a generous contribution from the

HOW TO USE CREDIT Latino Community Credit Union & the Latino Community Development Center www.latinoccu.org Copyright 2016 Latino Community Credit Union Made possible by a generous contribution from the

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook Welcome! This workshop is about credit. Credit is buying something now, but paying for it later. Credit can be useful

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook Welcome! This workshop is about credit. Credit is buying something now, but paying for it later. Credit can be useful

Financial Literacy. Module 4: Workbook Borrowing & Credit. Money Trek Program. AAUW California Financial Literacy Committee

Financial Literacy Money Trek Program Module 4: Workbook Borrowing & Credit AAUW California Financial Literacy Committee 1 Module 4: Borrowing & Credit FICO Score Review ( Fair Isaac Corporation and myfico.com)

Financial Literacy Money Trek Program Module 4: Workbook Borrowing & Credit AAUW California Financial Literacy Committee 1 Module 4: Borrowing & Credit FICO Score Review ( Fair Isaac Corporation and myfico.com)

FICO Scores Decoded Discover How to Easily and Quickly Obtain Excellent FICO Credit Scores Regardless of Your Personal Credit Quality Now

Discover How to Easily and Quickly Obtain Excellent FICO Credit Scores Regardless of Your Personal Credit Quality Now Discover How to Easily and Quickly Obtain Excellent FICO Credit Scores Regardless of

Discover How to Easily and Quickly Obtain Excellent FICO Credit Scores Regardless of Your Personal Credit Quality Now Discover How to Easily and Quickly Obtain Excellent FICO Credit Scores Regardless of

Credit Cards. Annual Percentage Rate - What you are paying each month -- unpaid balances calculated as a percentage.

Credit Cards Annual Fee - Amount you pay each year to have a credit card. Annual Percentage Rate - What you are paying each month -- unpaid balances calculated as a percentage. Balance - The total charges

Credit Cards Annual Fee - Amount you pay each year to have a credit card. Annual Percentage Rate - What you are paying each month -- unpaid balances calculated as a percentage. Balance - The total charges

PRACTICAL MONEY GUIDES. Credit History. Your credit history and how it affects your future.

PRACTICAL MONEY GUIDES Credit History Your credit history and how it affects your future. Learn what a credit history is and how to make the most of yours. What Is a Credit History? To predict your financial

PRACTICAL MONEY GUIDES Credit History Your credit history and how it affects your future. Learn what a credit history is and how to make the most of yours. What Is a Credit History? To predict your financial

Understanding Vehicle Financing

Understanding Vehicle Financing Understanding Vehicle Financing With prices averaging more than $31,000 for a new vehicle and $17,000 for a used model from a dealership, you might consider financing or

Understanding Vehicle Financing Understanding Vehicle Financing With prices averaging more than $31,000 for a new vehicle and $17,000 for a used model from a dealership, you might consider financing or

Credit Education Program

Credit Education Program Course Objectives Identify ways to decrease spending and increase income Read and understand the purpose of your credit report Discuss common debt traps to avoid How lenders evaluate

Credit Education Program Course Objectives Identify ways to decrease spending and increase income Read and understand the purpose of your credit report Discuss common debt traps to avoid How lenders evaluate

Office of Student Financial Management

September 2015 Office of Student Financial Management Kasia Palm: Director of Student Financial Management What is Credit? - The ability to obtain goods/services before payment based on the trust that

September 2015 Office of Student Financial Management Kasia Palm: Director of Student Financial Management What is Credit? - The ability to obtain goods/services before payment based on the trust that

Allstate Foundation Purple Purse Moving Ahead Curriculum

Allstate Foundation Purple Purse Moving Ahead Curriculum A Financial Empowerment Resource MODULE 3 Mastering Credit Basics Reviewing, and Credit MODULE 3 Mastering Credit Basics T his module explains how

Allstate Foundation Purple Purse Moving Ahead Curriculum A Financial Empowerment Resource MODULE 3 Mastering Credit Basics Reviewing, and Credit MODULE 3 Mastering Credit Basics T his module explains how

Credit and Credit Cards

Credit and Credit Cards What s Next Project Credit Cards They are all around you. Most people have at least one. Some have many. They are credit cards. A credit card allows you to pay for merchandise or

Credit and Credit Cards What s Next Project Credit Cards They are all around you. Most people have at least one. Some have many. They are credit cards. A credit card allows you to pay for merchandise or

Fixing Bad Credit and Solving Credit Problems 1

FCS 5049 Fixing Bad Credit and Solving Credit Problems 1 Mary N. Harrison 2 When you want to buy a car, a house, or other expensive items you probably expect to use credit. For smaller purchases, your

FCS 5049 Fixing Bad Credit and Solving Credit Problems 1 Mary N. Harrison 2 When you want to buy a car, a house, or other expensive items you probably expect to use credit. For smaller purchases, your

Project Pro$per. Credit Reports and Credit Scores

Project Pro$per Presents Credit Reports and Credit Scores Participant Guide www.projectprosper.org www.facebook.com/projectprosper Based on Wells Fargo s Hands on Banking The Hands on Banking program is

Project Pro$per Presents Credit Reports and Credit Scores Participant Guide www.projectprosper.org www.facebook.com/projectprosper Based on Wells Fargo s Hands on Banking The Hands on Banking program is

FINANCIAL FOUNDATIONS

FINANCIAL FOUNDATIONS A Financial Beginnings Financial Education Program CREDIT Presenter's Guide Presented by Our Mission Financial Beginnings empowers youth and adults to take control of their financial

FINANCIAL FOUNDATIONS A Financial Beginnings Financial Education Program CREDIT Presenter's Guide Presented by Our Mission Financial Beginnings empowers youth and adults to take control of their financial

Does providing FICO Scores influence financial behavior?

Power of Our Past Force of Our Future Does providing FICO Scores influence financial behavior? October 2018 Jeff Johnston, MBA Sallie Mae Ohio Association of Student Financial Aid Administrators 50th Anniversary

Power of Our Past Force of Our Future Does providing FICO Scores influence financial behavior? October 2018 Jeff Johnston, MBA Sallie Mae Ohio Association of Student Financial Aid Administrators 50th Anniversary

CreditReport.LifeTips.com

CreditReport.LifeTips.com Category: About Credit Reports Subcategory: About Credit Reports Tip: About Credit Reports A credit report is a compilation of information that gives potential creditors a snapshot

CreditReport.LifeTips.com Category: About Credit Reports Subcategory: About Credit Reports Tip: About Credit Reports A credit report is a compilation of information that gives potential creditors a snapshot

Your Guide To Better Credit

Your Guide To Better Credit INTRODUCTION Your go-to guide to better credit It seems like every other commercial on television touts some sort of offer around credit. You hear things like, Free credit report,

Your Guide To Better Credit INTRODUCTION Your go-to guide to better credit It seems like every other commercial on television touts some sort of offer around credit. You hear things like, Free credit report,

2. To encourage consumers to apply for their free credit reports each year from each of the Na onal Credit Repor ng

Credit Reports: A Financial Management Monitoring Tool Grady County OHCE Leader Lesson Leader s Guide January, 2013 Prepared by: Susan Routh, Extension Educator, Family and Consumer Sciences/4 H Youth

Credit Reports: A Financial Management Monitoring Tool Grady County OHCE Leader Lesson Leader s Guide January, 2013 Prepared by: Susan Routh, Extension Educator, Family and Consumer Sciences/4 H Youth

Your Ultimate Guide to DIY Credit Repair. January

Your Ultimate Guide to DIY Credit Repair January 2018 www.upturncredit.com Table of Contents Part 1 - Anatomy of a Credit Report Part 2 - Credit Scores vs Credit Reports Part 3 - Why Your Credit Report

Your Ultimate Guide to DIY Credit Repair January 2018 www.upturncredit.com Table of Contents Part 1 - Anatomy of a Credit Report Part 2 - Credit Scores vs Credit Reports Part 3 - Why Your Credit Report

Module 7 - Credit Reporting HANDOUT 7-1

ParticipantHandbook 1 Module 7 - Credit Reporting HANDOUT 7-1 Credit bureaus Credit bureaus are agencies that collect information about how we use credit. They produce personal credit reports. Credit bureaus

ParticipantHandbook 1 Module 7 - Credit Reporting HANDOUT 7-1 Credit bureaus Credit bureaus are agencies that collect information about how we use credit. They produce personal credit reports. Credit bureaus

FICO Score Open Access Consumer Credit Education US Version. Frequently Asked Questions about FICO Scores

FICO Score Open Access Consumer Credit Education US Version Frequently Asked Questions about Scores 2012 Fair Isaac Corporation. All rights reserved. 1 January 01, 2012 Table of Contents About Scores...

FICO Score Open Access Consumer Credit Education US Version Frequently Asked Questions about Scores 2012 Fair Isaac Corporation. All rights reserved. 1 January 01, 2012 Table of Contents About Scores...

Fact, Fiction & FICOs: Presented by: Vance Edwards, CMB Certified FICO Professional MGIC Marketing Program Director

Fact, Fiction & FICOs: Presented by: Vance Edwards, CMB Certified FICO Professional MGIC Marketing Program Director Agenda What makes up a credit score (and what doesn t) What causes that score to move

Fact, Fiction & FICOs: Presented by: Vance Edwards, CMB Certified FICO Professional MGIC Marketing Program Director Agenda What makes up a credit score (and what doesn t) What causes that score to move

FICO Score Open Access Consumer Credit Education US Version. Frequently Asked Questions about the FICO Score

FICO Score Open Access Consumer Credit Education US Version Frequently Asked Questions about the FICO Score 2012 Fair Isaac Corporation. All rights reserved. 1 January 01, 2012 Table of Contents About

FICO Score Open Access Consumer Credit Education US Version Frequently Asked Questions about the FICO Score 2012 Fair Isaac Corporation. All rights reserved. 1 January 01, 2012 Table of Contents About

Credit Reports & Credit Scores 101. Mary C. Hurlburt Certified Consumer Credit Counselor and Score Volunteer

Credit Reports & Credit Scores 101 Mary C. Hurlburt Certified Consumer Credit Counselor and Score Volunteer mary.hurlburt@scorevolunteer.org Mary Hurlburt Mary Hurlburt is the Financial Counseling and

Credit Reports & Credit Scores 101 Mary C. Hurlburt Certified Consumer Credit Counselor and Score Volunteer mary.hurlburt@scorevolunteer.org Mary Hurlburt Mary Hurlburt is the Financial Counseling and

Take control of your auto loan

Take control of your auto loan A step-by-step guide Consumer Financial Protection Bureau How can this guide help you? While many people shop around for the best deal they can get on their vehicle, not

Take control of your auto loan A step-by-step guide Consumer Financial Protection Bureau How can this guide help you? While many people shop around for the best deal they can get on their vehicle, not

Now, let me turn the program over to Jacqueline Cooke, Women s Bureau Regional Administrator in Boston, to introduce our first speaker. Jackie?

Wi$e Up Teleconference Call February 28, 2006 Becoming Credit Smart Speaker 1 Amy Perry Jane Walstedt: Now, let me turn the program over to Jacqueline Cooke, Women s Bureau Regional Administrator in Boston,

Wi$e Up Teleconference Call February 28, 2006 Becoming Credit Smart Speaker 1 Amy Perry Jane Walstedt: Now, let me turn the program over to Jacqueline Cooke, Women s Bureau Regional Administrator in Boston,

Improving Your Credit

Teacher Homebuyer Guide to: Improving Your Credit By John Godbey, Founder and Broker of Teacher Homebuyer Real Estate Introduction Thank you for signing up for our E-Guide "Improving Your Credit." We find

Teacher Homebuyer Guide to: Improving Your Credit By John Godbey, Founder and Broker of Teacher Homebuyer Real Estate Introduction Thank you for signing up for our E-Guide "Improving Your Credit." We find

Building Credit. Inside this issue:

CCCS of Rochester/RethinkingDebt Headquarters: 1000 University Ave, Rochester, NY 14607 **Fall 2018** Inside this issue: Building Credit Building Credit 1 Retail Credit Cards 2 By: CCCS of Rochester Student

CCCS of Rochester/RethinkingDebt Headquarters: 1000 University Ave, Rochester, NY 14607 **Fall 2018** Inside this issue: Building Credit Building Credit 1 Retail Credit Cards 2 By: CCCS of Rochester Student

Credit info changes likely to get Bush OK

NET GAIN Scoring points for your financial future AS SEEN IN USA TODAY NOVEMBER 24, 2003 Credit info changes likely to get Bush OK House, Senate approve revisions to reporting law By Thomas A. Fogarty

NET GAIN Scoring points for your financial future AS SEEN IN USA TODAY NOVEMBER 24, 2003 Credit info changes likely to get Bush OK House, Senate approve revisions to reporting law By Thomas A. Fogarty

Volume 2 Your Credit Report and Your Rights

Volume 2 Your Credit Report and Your Rights Your Credit Report and Your Rights Take the first step in changing your financial future. Call InCharge Debt Solutions today at 1.877.544.7772 or visit www.incharge.org

Volume 2 Your Credit Report and Your Rights Your Credit Report and Your Rights Take the first step in changing your financial future. Call InCharge Debt Solutions today at 1.877.544.7772 or visit www.incharge.org

A Special Report by Laura Adams, author of Money Girl s Smart Moves to Grow Rich

3 Strategies to Build Credit FAST A Special Report by Laura Adams, author of Money Girl s Smart Moves to Grow Rich 3 Strategies to Build Credit Fast Copyright 2011 SmartMovesToGrowRich.com All rights reserved.

3 Strategies to Build Credit FAST A Special Report by Laura Adams, author of Money Girl s Smart Moves to Grow Rich 3 Strategies to Build Credit Fast Copyright 2011 SmartMovesToGrowRich.com All rights reserved.

What is credit and why does it matter to me?

Understanding Credit 1 Money Matters The BIG Idea What is credit and why does it matter to me? AGENDA Approx. 45 minutes I. Warm Up: What Do You Know About Credit? (10 minutes) II. Credit: The Good, The

Understanding Credit 1 Money Matters The BIG Idea What is credit and why does it matter to me? AGENDA Approx. 45 minutes I. Warm Up: What Do You Know About Credit? (10 minutes) II. Credit: The Good, The

Creditworthiness (UXL)

") Creditworthiness (UXL) Since so much debt is unsecured, it is important for companies to have information on how well their potential borrowers handle money in order to assess their creditworthiness, or

Creditworthiness (UXL) Since so much debt is unsecured, it is important for companies to have information on how well their potential borrowers handle money in order to assess their creditworthiness, or

Your Credit. Objectives. An Introduction to Personal Credit. By the end of this presentation you will have a understanding of: 1/19/2016.

Your Credit An Introduction to Personal Credit Objectives By the end of this presentation you will have a understanding of: Credit Score Where can I find it? What is it? How do I get it? Advantages of

Your Credit An Introduction to Personal Credit Objectives By the end of this presentation you will have a understanding of: Credit Score Where can I find it? What is it? How do I get it? Advantages of

13.1. Reading a Credit Report EXERCISE. THEME 4 Lesson 13: Applying for Credit NAME: CLASS PERIOD:

13.1 NAME: CLASS PERIOD: Reading a Credit Report Your ability to qualify for a loan depends on a credit report. A credit report is a record of an individual s personal credit history. It is probably a

13.1 NAME: CLASS PERIOD: Reading a Credit Report Your ability to qualify for a loan depends on a credit report. A credit report is a record of an individual s personal credit history. It is probably a

What You Can Do to Improve Your Credit, Now

What You Can Do to Improve Your Credit, Now Provided compliments of: 1 What You Can Do to Improve Your Credit, Now Steps to Raise Your Score Now we re going to focus on certain steps that you can take,

What You Can Do to Improve Your Credit, Now Provided compliments of: 1 What You Can Do to Improve Your Credit, Now Steps to Raise Your Score Now we re going to focus on certain steps that you can take,

February 2015 Wednesday Webinar ~ Credit Matters - Resources to Educate Students About Credit and Debt

February 2015 Wednesday Webinar ~ Credit Matters - Resources to Educate Students About Credit and Debt 1 Mike Fagone Jennifer Pincus Jessica Whittier Bernstein Shur US Dept. of Justice FAME 2 About CARE

February 2015 Wednesday Webinar ~ Credit Matters - Resources to Educate Students About Credit and Debt 1 Mike Fagone Jennifer Pincus Jessica Whittier Bernstein Shur US Dept. of Justice FAME 2 About CARE

Introduction Slide SET. Host Organization s Name July 30, Business Smart is a business education series developed by

Introduction Slide Business Smart is a business education series developed by SET Host Organization s Name July 30, 2015 1 Business Smart Workshop 3 Modules READY SET GO 2 Today s Presenter Add Name of

Introduction Slide Business Smart is a business education series developed by SET Host Organization s Name July 30, 2015 1 Business Smart Workshop 3 Modules READY SET GO 2 Today s Presenter Add Name of

Building a U.S. credit score

Building a U.S. credit score A strong credit history could help improve many aspects of your life in the U.S. Here s our guide for new-to-country residents. Together We Thrive When moving overseas, it

Building a U.S. credit score A strong credit history could help improve many aspects of your life in the U.S. Here s our guide for new-to-country residents. Together We Thrive When moving overseas, it

Credit Building Apps

Credit Building Apps Apps that Can Help Build and Repair Credit Webinar of September 27, 2018 Sponsored by Community Development and the Payments, Standards, and Outreach Group of the Federal Reserve Bank

Credit Building Apps Apps that Can Help Build and Repair Credit Webinar of September 27, 2018 Sponsored by Community Development and the Payments, Standards, and Outreach Group of the Federal Reserve Bank

PERSONAL FINANCIAL LITERACY EVENT PARTICIPANT INSTRUCTIONS

CAREER CLUSTER Financial Literacy INSTRUCTIONAL AREA Credit and Debt PERSONAL FINANCIAL LITERACY EVENT PARTICIPANT INSTRUCTIONS PROCEDURES 1. The event will be presented to you through your reading of

CAREER CLUSTER Financial Literacy INSTRUCTIONAL AREA Credit and Debt PERSONAL FINANCIAL LITERACY EVENT PARTICIPANT INSTRUCTIONS PROCEDURES 1. The event will be presented to you through your reading of

A Credit Smart Start. Michael Trecek Sr. Risk Analyst Commerce Bank - Retail Lending

A Credit Smart Start Michael Trecek Sr. Risk Analyst Commerce Bank - Retail Lending Agenda Credit Score vs. Credit Report Credit Score Components How Credit Scoring Helps You 10 Things that Hurt Your Credit

A Credit Smart Start Michael Trecek Sr. Risk Analyst Commerce Bank - Retail Lending Agenda Credit Score vs. Credit Report Credit Score Components How Credit Scoring Helps You 10 Things that Hurt Your Credit

Credit and Debt.notebook August 28, 2014

Credit and Debt What does it mean to have credit? Credit means someone is willing to loan you money in exchange for your promise to repay it, usually with interest. Interest the amount of money you pay

Credit and Debt What does it mean to have credit? Credit means someone is willing to loan you money in exchange for your promise to repay it, usually with interest. Interest the amount of money you pay

4-Step Guide to Rebuilding Your Credit

4-Step Guide to Rebuilding Your Credit Bankruptcy Solutions 1 800.435.9138 StartFreshToday.com 1 Contents 3 4 5 8 12 16 Rebuilding Your Credit Step 1: Obtain Your Records Step 2: Identify Errors Step 3:

4-Step Guide to Rebuilding Your Credit Bankruptcy Solutions 1 800.435.9138 StartFreshToday.com 1 Contents 3 4 5 8 12 16 Rebuilding Your Credit Step 1: Obtain Your Records Step 2: Identify Errors Step 3:

FTC Facts. For Consumers Federal Trade Commission. Credit Scoring Ever wonder how a creditor decides

FTC Facts For Consumers Federal Trade Commission For The Consumer May 2006 Credit Scoring www.ftc.gov 1-877-ftc-help Ever wonder how a creditor decides whether to grant you credit? For years, creditors

FTC Facts For Consumers Federal Trade Commission For The Consumer May 2006 Credit Scoring www.ftc.gov 1-877-ftc-help Ever wonder how a creditor decides whether to grant you credit? For years, creditors

65 E. Wacker Place Suite 1405, Chicago, IL Ph: Fax: Credit 101

65 E. Wacker Place Suite 1405, Chicago, IL 60601 Ph: 888.895.5145 Fax: 888.895.5146 Credit 101 The subject of credit and what is included on a consumer s credit report can be a source of much debate, confusion

65 E. Wacker Place Suite 1405, Chicago, IL 60601 Ph: 888.895.5145 Fax: 888.895.5146 Credit 101 The subject of credit and what is included on a consumer s credit report can be a source of much debate, confusion

Twelve common questions. About consumer credit and direct marketing

Twelve common questions About consumer credit and direct marketing Twelve common questions Most of us don t think about credit until a specific event sparks our interest. Maybe we want to buy a car or

Twelve common questions About consumer credit and direct marketing Twelve common questions Most of us don t think about credit until a specific event sparks our interest. Maybe we want to buy a car or

Understanding Credit Reports

Understanding Credit Reports Family Economics & Financial Education Take Charge of Your Finances Credit Report Detectives Meet Isabella, your new client: About to graduate from college In extreme debt

Understanding Credit Reports Family Economics & Financial Education Take Charge of Your Finances Credit Report Detectives Meet Isabella, your new client: About to graduate from college In extreme debt

UNDERSTANDING CREDIT REPORTS AND SCORES

UNDERSTANDING CREDIT REPORTS AND SCORES 1-888-282-5811 www.myfinancialgoals.org THE NEED FOR GOOD CREDIT Some financial goals cannot be accomplished in one payment for example, an automobile or a house

UNDERSTANDING CREDIT REPORTS AND SCORES 1-888-282-5811 www.myfinancialgoals.org THE NEED FOR GOOD CREDIT Some financial goals cannot be accomplished in one payment for example, an automobile or a house

Financial Well-being. Debt and Credit

Financial Well-being Debt and Credit Debt and Credit When evaluating financial wellness, debt has a real impact on your ability to reach your goals. Debt feels like a four letter word. However, it can

Financial Well-being Debt and Credit Debt and Credit When evaluating financial wellness, debt has a real impact on your ability to reach your goals. Debt feels like a four letter word. However, it can

12 common questions. About consumer credit and direct marketing

12 common questions About consumer credit and direct marketing Most of us don t think about credit until a specific event sparks our interest. Maybe we want to buy a car or home. Or perhaps we receive

12 common questions About consumer credit and direct marketing Most of us don t think about credit until a specific event sparks our interest. Maybe we want to buy a car or home. Or perhaps we receive

Chapter 26 11/9/2017 1

Chapter 26 11/9/2017 1 Average college students has 3 credit cards Also between $1500 & $2000 in debt Things to know if you re getting a credit card Who accepts it? What amount can you charge to meet your

Chapter 26 11/9/2017 1 Average college students has 3 credit cards Also between $1500 & $2000 in debt Things to know if you re getting a credit card Who accepts it? What amount can you charge to meet your

Beyond the Classroom. Blaise P. Johnson Gate City Bank

Beyond the Classroom Blaise P. Johnson Gate City Bank 1 Topics To Be Discussed 1. Credit Reports & Credit Scores 2. Repayment/Consolidation of Student Loans 3. Obtaining A Personal or Home Loan 4. Open

Beyond the Classroom Blaise P. Johnson Gate City Bank 1 Topics To Be Discussed 1. Credit Reports & Credit Scores 2. Repayment/Consolidation of Student Loans 3. Obtaining A Personal or Home Loan 4. Open

Chapter 6 - Credit. Section 6.1

Chapter 6 - Credit Section 6.1 Credit is a medium of exchange which allows individuals to buy goods or services now and pay for them later The creditor supplies money, goods, or services in a credit agreement

Chapter 6 - Credit Section 6.1 Credit is a medium of exchange which allows individuals to buy goods or services now and pay for them later The creditor supplies money, goods, or services in a credit agreement

ves a rue re i Credit Scoring: How it Works and How You Can Improve Your Score What Is Credit Scoring?

ves a Credit Scoring: How it Works and How You Can Improve Your Score rue re i Congratulations! By reading this publication you' ve taken the first step towards understanding and improving your credit

ves a Credit Scoring: How it Works and How You Can Improve Your Score rue re i Congratulations! By reading this publication you' ve taken the first step towards understanding and improving your credit

2/10/2015 CREDIT FOR SUCCESS TODAY S NEW RISK FACTORS MOBILE BANKING. The new Consumer Financial Protection Act, the ATR Rule (Ability to Repay Rule)

") CREDIT FOR SUCCESS TODAY S NEW RISK FACTORS Written and Presented by Serge Bevil, Credit Specialist VantagePoint Credit Corp. MOBILE BANKING We have become a social media society that wants information,

CREDIT FOR SUCCESS TODAY S NEW RISK FACTORS Written and Presented by Serge Bevil, Credit Specialist VantagePoint Credit Corp. MOBILE BANKING We have become a social media society that wants information,

Credit score ratings chart 2017

Credit score ratings chart 2017 By 2009 the worldwide bond market (total debt outstanding) reached an estimated $82.2 trillion, in 2009 dollars. [26]. As the influence and profitability of CRAs expanded,

Credit score ratings chart 2017 By 2009 the worldwide bond market (total debt outstanding) reached an estimated $82.2 trillion, in 2009 dollars. [26]. As the influence and profitability of CRAs expanded,

Secrets to Success: Personal Finance Management

Secrets to Success: Personal Finance Management Harvard University Employees Credit Union (HUECU) A financial institution exclusively serving the Harvard University students, alumni, faculty, staff, and

Secrets to Success: Personal Finance Management Harvard University Employees Credit Union (HUECU) A financial institution exclusively serving the Harvard University students, alumni, faculty, staff, and

Credit Cards. The Language of Credit. Student Loans. Installment Loans 12/14/2016

Quick Response Explain how you think credit cards work. How much do you have to pay every month? What happens if you pay late? What kinds of fees are involved? Unit 4 - Good Debt, Bad Debt: Using Credit

Quick Response Explain how you think credit cards work. How much do you have to pay every month? What happens if you pay late? What kinds of fees are involved? Unit 4 - Good Debt, Bad Debt: Using Credit

Credit Reports and Scores

Credit Reports and Scores Advanced Level The Importance of a Credit History for Obtaining Credit Credit refers to borrowing. You have used credit if you receive money, goods, or services in exchange for

Credit Reports and Scores Advanced Level The Importance of a Credit History for Obtaining Credit Credit refers to borrowing. You have used credit if you receive money, goods, or services in exchange for

Rebuilding YOUR CREDIT. Leader s Guide

Rebuilding YOUR CREDIT Leader s Guide C CONTENTS Table of contents Page Topic 1 Introduction 2 Damaged credit 2 Credit reports 5 Mistakes on your credit report 6 Credit scoring 8 Credit repair offers 8

Rebuilding YOUR CREDIT Leader s Guide C CONTENTS Table of contents Page Topic 1 Introduction 2 Damaged credit 2 Credit reports 5 Mistakes on your credit report 6 Credit scoring 8 Credit repair offers 8

20 STEPS TO IMPROVE YOUR CREDIT SCORE APPROVED CREDIT SCORE SUPER FAST CREDIT RANKINGS

20 STEPS TO IMPROVE YOUR CREDIT SCORE APPROVED CREDIT SCORE SUPER FAST CREDIT RANKINGS 2 Approved Credit Score info@approvedcreditscore.com www.approvedcreditscore.com APPROVED CREDIT SCORE CONGRATULATIONS!

20 STEPS TO IMPROVE YOUR CREDIT SCORE APPROVED CREDIT SCORE SUPER FAST CREDIT RANKINGS 2 Approved Credit Score info@approvedcreditscore.com www.approvedcreditscore.com APPROVED CREDIT SCORE CONGRATULATIONS!

YOUR MONEY, YOUR GOALS. A financial empowerment toolkit

YOUR MONEY, YOUR GOALS A financial empowerment toolkit Consumer Financial Protection Bureau December 2016 About the Consumer Financial Protection Bureau The Consumer Financial Protection Bureau (CFPB)

YOUR MONEY, YOUR GOALS A financial empowerment toolkit Consumer Financial Protection Bureau December 2016 About the Consumer Financial Protection Bureau The Consumer Financial Protection Bureau (CFPB)

Budgeting & Debt Basics

Budgeting & Debt Basics Why Have a Budget? Gain control over your finances Get the most out of your money Achieve your financial goals What is a Budget? A plan for saving and spending Allows you to choose

Budgeting & Debt Basics Why Have a Budget? Gain control over your finances Get the most out of your money Achieve your financial goals What is a Budget? A plan for saving and spending Allows you to choose

An Overview of Credit Report/Credit Score Models and a Proposal for Vietnam

VNU Journal of Science: Policy and Management Studies, Vol. 33, No. 2 (2017) 36-45 An Overview of Credit Report/Credit Score Models and a Proposal for Vietnam Le Duc Thinh * VNU International School, Building

VNU Journal of Science: Policy and Management Studies, Vol. 33, No. 2 (2017) 36-45 An Overview of Credit Report/Credit Score Models and a Proposal for Vietnam Le Duc Thinh * VNU International School, Building

You re listening to rebuilding after a financial crisis. Hi, I m Niki, your host for today s Podcast.

Rebuilding After a Financial Crisis Podcast [Music plays] Nikki: You re listening to rebuilding after a financial crisis. Hi, I m Niki, your host for today s Podcast. There are many things in life that

Rebuilding After a Financial Crisis Podcast [Music plays] Nikki: You re listening to rebuilding after a financial crisis. Hi, I m Niki, your host for today s Podcast. There are many things in life that

5/16/2006 1 of 18 Report for CHRISTINE BAKER on April 30, 2006 Click here to return. 742 CHRISTINE BAKER April 30, 2006 Credit record source: Equifax Your FICO score of 742 summarizes the information on

5/16/2006 1 of 18 Report for CHRISTINE BAKER on April 30, 2006 Click here to return. 742 CHRISTINE BAKER April 30, 2006 Credit record source: Equifax Your FICO score of 742 summarizes the information on

Profiles in Credit is designed to be flexible and meet the needs of learners in different educational settings. Examples include:

Profiles in Credit Educator Resource Guide Module Summary Profiles in Credit is a self-paced, interactive learning module in which students visit the social media profiles of three young people facing

Profiles in Credit Educator Resource Guide Module Summary Profiles in Credit is a self-paced, interactive learning module in which students visit the social media profiles of three young people facing

FINANCIAL FITNESS EDUCATION

(Agency s Name & Logo) FINANCIAL FITNESS EDUCATION Sponsored by BETTER FORTUNES Control Your Money Control Your Life Knowing the difference can make all the difference Chapter One ECONOMIC WAY OF THINKING

(Agency s Name & Logo) FINANCIAL FITNESS EDUCATION Sponsored by BETTER FORTUNES Control Your Money Control Your Life Knowing the difference can make all the difference Chapter One ECONOMIC WAY OF THINKING

Table of Contents. Money Smart for Small Business Page 2 of 19

Table of Contents Welcome... 4 What Do You Know? Credit Reporting for a Small Business... 5 Pre-Test... 6 Credit Reporting... 7 Credit Report Impact... 7 Business Credit Reports... 7 Discussion Point #1:

Table of Contents Welcome... 4 What Do You Know? Credit Reporting for a Small Business... 5 Pre-Test... 6 Credit Reporting... 7 Credit Report Impact... 7 Business Credit Reports... 7 Discussion Point #1:

TIP: Make sure this information is correct. A wrong address or phone number could be a mistake or a sign of identity theft.

Reading a Sample Credit Report This sample report shows what kind of information might appear on your own credit report, also called a consumer disclosure statement, from the 3 major Credit Reporting Agencies

Reading a Sample Credit Report This sample report shows what kind of information might appear on your own credit report, also called a consumer disclosure statement, from the 3 major Credit Reporting Agencies

How Much House Can You Afford?

03 4580 CH02 4/4/06 4:11 PM Page 15 How Much House Can You Afford? 2 Chapter In This Chapter Calculating your total income and monthly expenses Finding your appropriate price range or knowing how much

03 4580 CH02 4/4/06 4:11 PM Page 15 How Much House Can You Afford? 2 Chapter In This Chapter Calculating your total income and monthly expenses Finding your appropriate price range or knowing how much

Table of Contents. Introduction. The History of Credit Scoring. What Is a Good Credit Score? The 5 Factors of Credit Scoring

Table of Contents Introduction The History of Credit Scoring What Is a Good Credit Score? The 5 Factors of Credit Scoring 3 Ways to Get Your Credit Score Get Your FREE Credit Report What If There Are Errors

Table of Contents Introduction The History of Credit Scoring What Is a Good Credit Score? The 5 Factors of Credit Scoring 3 Ways to Get Your Credit Score Get Your FREE Credit Report What If There Are Errors

GENERAL FINANCING QUESTIONS

GENERAL FINANCING QUESTIONS 1. What is a Mortgage? Tips for Homebuyers Generally speaking, a mortgage is a loan obtained to purchase real estate. The "mortgage" itself is a lien (a legal claim) on the

GENERAL FINANCING QUESTIONS 1. What is a Mortgage? Tips for Homebuyers Generally speaking, a mortgage is a loan obtained to purchase real estate. The "mortgage" itself is a lien (a legal claim) on the

in Head Start Credit and Debt: Make it work for you!

in Head Start Credit and Debt: Make it work for you! Annual Credit Report Request Form You have the right to get a free copy of your credit file disclosure, commonly called a credit report, once every

in Head Start Credit and Debt: Make it work for you! Annual Credit Report Request Form You have the right to get a free copy of your credit file disclosure, commonly called a credit report, once every

12/5/2013. Cash Management: Overview. More Month Than Money and Extra Credit. Why are you here? Benefits of developing a budget

12/5/2013 Cash Management: Overview More Month Than Money and Extra Credit Sean L. Mabey smabey@neamb.com Understanding cash management Age old questions: Where oh where does our money go? Making a budget

12/5/2013 Cash Management: Overview More Month Than Money and Extra Credit Sean L. Mabey smabey@neamb.com Understanding cash management Age old questions: Where oh where does our money go? Making a budget

Quick Credit Repair Guide

1 Quick Credit Repair Guide Beacon score? You will most likely have heard of this bizarre term at some point during your home buying process and wondered what they meant and how they affect the mortgage

1 Quick Credit Repair Guide Beacon score? You will most likely have heard of this bizarre term at some point during your home buying process and wondered what they meant and how they affect the mortgage

MODULE J: SMART CHOICES FOR MANAGING CREDIT

MODULE J: SMART CHOICES FOR MANAGING CREDIT 1 Common Sense Economics ~ What Everyone Should Know About Wealth and Prosperity http://commonsenseeconomics.com/ Turn on the learning light! CREDIT, FINANCIAL

MODULE J: SMART CHOICES FOR MANAGING CREDIT 1 Common Sense Economics ~ What Everyone Should Know About Wealth and Prosperity http://commonsenseeconomics.com/ Turn on the learning light! CREDIT, FINANCIAL