Office of Student Financial Management

|

|

|

- Deirdre Newton

- 5 years ago

- Views:

Transcription

1 September 2015 Office of Student Financial Management Kasia Palm: Director of Student Financial Management

2 What is Credit? - The ability to obtain goods/services before payment based on the trust that a payment will be made in the future - Borrowed money that you pay back at a specified time - Credit Cards, Overdraft Protection (Line of Credit), Student Loans, Mortgages, Car Loans, Pay Day Loans, etc.

3 What is a Credit Report? - A history of your past credit activities - Including balances and payment history - Includes: - Credit Information (closed and open accounts) - Credit Cards - Loan Accounts - Lines of Credit - Pay Day Loans - Public Record Information - Recent Inquiries (who has obtained your credit report) Hard Inquiries - Doesn t Include - Bank account information - Investments, Retirement Accounts, etc

4 Public Records - Judgment or lawsuit (financially related) - Foreclosure - Bankruptcy - State/Federal Tax Lien - Wage garnishment - Past-due Child Support

5 Inquiries - Hard Inquiries - Occur when a creditor checks your credit report for the purpose of granting you a line of credit - Reported on your credit report for 2 years. Have a small impact on your credit score - Soft Inquiries - Occur when someone checks your credit on your behalf - Employer background check - Identity verification - Pre-approved offers - You check your own credit report - Viewable only by you and have no impact on score - Sometimes, it may not be obvious what kind of inquiry the company is initiating - Apartment rental applications - Opening TV/Cable accounts - Car rentals - Opening a new bank account - You can always ask the company completing the credit check, what type of inquiry they ll initiate

6 Who can see your Credit Report? - Creditors who are considering granting or have granted you credit - Employers considering you for employment, promotion, reassignment or retention - Insurers considering you for an insurance policy or reviewing an existing policy - Government agencies reviewing your financial status or government benefits - Anyone with a legitimate business need for the information, such as a potential landlord, cable company, etc - YOU

7 What is a Negative Account? - Has Late Payments (30, 60, 90 days overdue) - In Collections - Charged-off - Defaulted

8 What is reported and for how long? - Open Accounts - always - Closed Accounts for 7 years - Negative Accounts 7 years from original delinquency - Bankruptcies 10 yrs (Ch 7) or 7yrs (Ch 13/re-org) - Public Records 7 years - Tax Liens 7 years after its paid - Hard Inquiries 2 years

9 Where do Credit Reports Come From? - Credit Bureaus collect and sell credit information - Information these bureaus use comes from the parties that have extended credit to you - A creditor may report your account information to all or none of the credit bureaus - information obtained from the different bureaus may vary - There are 3 major nationwide credit bureaus - Equifax Transunion - Experian

10 Checking your Report It is very important to check your credit reports regularly. - Know where you stand - Helps protect against fraud or identity theft - Credit reports can have ERRORS that hurt your score - Make sure to monitor each of your credit reports as they may have different information

11 How to check your report - You are entitled to 1 free credit report from each of the 3 bureaus annually - AnnualCreditReport.com - NOT FreeCreditReport.com - This website provides a free credit score when you sign up for their credit monitoring service - Go directly to credit bureau s website ($1-$10)

12 Other Websites Providing a Free Credit Report - A number of website services provide you with a free credit report: - Credit Karma TransUnion & Equifax report, once per week. Also provides a score simulator. - Credit Sesame TransUnion report summary, once per month - Quizzle Equifax report, once every 3 months

13 Other Free Ways to get Report - Under Colorado law, you are also entitled to 1 free credit report from each of the credit bureaus each year (so, you could get 2 free reports per year) - If denied credit, insurance or a job due to your credit report, you are entitled to a free report within 60 days - Unemployed and looking for work - Report is inaccurate due to fraud

14 What is a Credit Score? - A numeric rating assigned based on your credit report - Represents your creditworthiness to potential creditors, employers, etc. - The most common score used for this purpose is the FICO score (developed by the Fair Isaac Corporation) - Ranges from Because each bureau has different data, you may have 3 different FICO scores - Another score is the VantageScore - Ranges from for older VantageScores, and for VantageScore Often sold by the 3 credit bureaus to customers - Uses a slightly different calculation than the FICO score

15 Credit Score Details

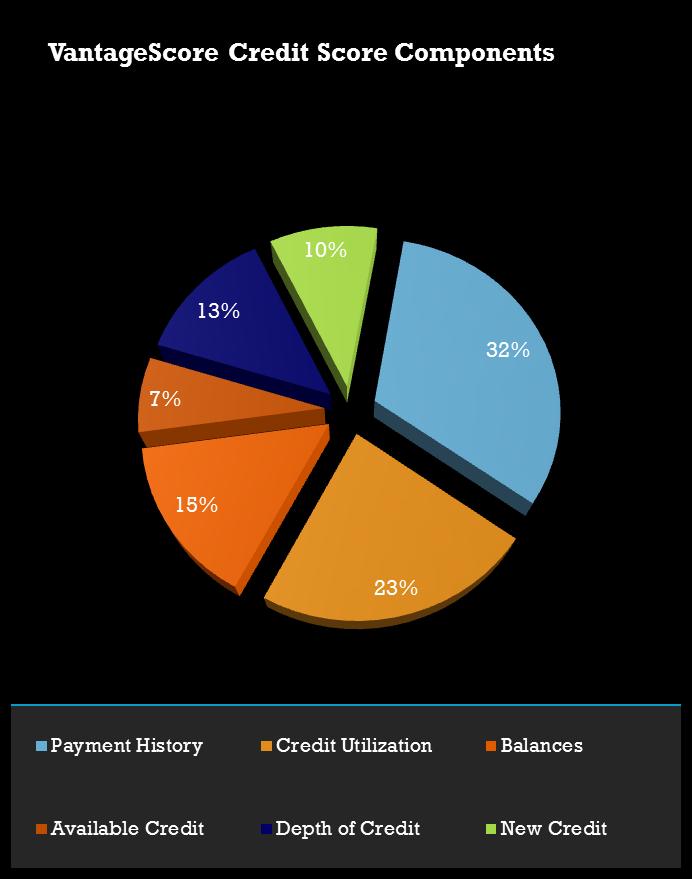

16 Credit Score Components Payment History: 35% FICO or 32% VantageScore - On-time payments help your score - Late payments hurt your score - Payments are reported as 30, 60, 90, or120 days late Credit Utilization: 30% FICO or 45% VantageScore (Utilization 23%, Balances 15% and Available Credit 7%) - The amount of credit you are using compared to how much credit you have available - keeping credit utilization below 30% is good - keeping credit utilization below 10% is excellent

17 Credit Score Components Length of History: 15% FICO - The longer history you have the better - Usually, anything less than 7 years hurts your score Account Diversity: 10% FICO - Having a more diversified credit portfolio helps your score. - Accounts are categorized as: - Revolving (credit cards, lines of credit) - Installment (loans) - Real Estate (mortgage) Depth of Credit: 13% VantageScore - Combination of Length of History and Account Diversity New Credit: 10% - Too many hard inquiries (those where a creditor is checking your credit for the purpose of qualifying you for credit) can hurt your score

18 Understanding your Credit Score FICO : EXCELLENT : GOOD : FAIR : POOR : VERY POOR VantageScore : A, Super Prime : B, Prime Plus : C, Prime : D, Non-Prime : F, High Risk

19 Ways you may be hurting your credit 1 Closing old Credit Card Accounts 2 Missing Payments 3 Settling Past Due Accounts 4 Over-Utilizing Credit 5 Shopping Around Too Much for Credit

20 Qualifying for Credit The following are criteria that creditors use to qualify you for credit: - Character Will you repay your debt? How have you paid your bills in the past? (credit report) - Collateral What will the lender get if you don t repay your debt? - Secured loans (car loans, mortgages) usually have lower interest rates than unsecured loans (personal loans, credit cards) because the lender will get something (car, house) if you default - Capacity Can you repay your debt based on your available income? (debt to income ratio) - Capital What is your net worth? - Again, if you have a higher net worth, the lender is more likely to recoup the money they lent you if you default - Conditions What is the overall economic situation? This will have a high impact on availability of credit and rates.

21 Building Your Credit - Get added as an authorized user to another person s account (relative, significant other) - Set up a secured credit card - Obtain a co-signer for loans

22 Debit Card Pros and Cons PROs - Convenient - Secure - Interest free - Can help you track your spending - Can be used to get cash at ATMs or with merchants CONs - Can be declined if you don t have enough money in your account - Overdraft fees can be costly - Using a debit card wisely has no impact on your credit

23 Credit Card Pros and Cons PROs - Convenient - Secure - Interest free, if paid off in full each month - Can help you track your spending - Can give you rewards or cash back - Can provide additional protection for certain purchases - Can be useful in an emergency situation - Help build your credit CONs - Interest charges if you carry a balance from month to month (interest of 10-30%) - Late fees and higher interest rates if not paid on time - May give you the illusion that you have more money than you really have - Can have an annual fee

24 Credit Card Dos and Don ts DOs - Pay your bill on time - Pay your balance in full, if you can - Reduce your credit card use if you can t pay off your card in full - Check your statement/ account activity regularly - Read 0% financing offers carefully - Can cost you A LOT in interest if not paid off by end of promo period - Understand your terms and conditions DON Ts - Max out your credit card - Make purchases you can t afford - Make only minimum payments - Buy things on credit just to get rewards/cash back - If not paying your card of fully next month, how much will that reward cost you.

25 Importance of Budgeting - Ensures you don t spend money that you don t have - Can shed light on some bad spending habits - You may see areas where you are spending money on things you really don t need - Helps you prepare for emergencies - Gives you peace of mind - By following a budget, you ll have control over your financial life, rather than it controlling you. - Helps you meet your financial goals - Paying off loans, taking trips, retirement, etc. - Can help you maintain (or improve) your credit

26 Tracking your Spending - To maintain, and improve, your credit record, you need to monitor your spending and ensure you have enough money to cover your debts. - An easy way of doing this is by creating a Spending Plan or Budget. - There are many tools to help you create a budget you can live on: - Budgeting Worksheets from the Office of Financial Management - Websites such as: Mint.com, BudgetSimple.com, MySpendingPlan.com

27 Creating a Budget - Determine your sources of income - Income from work - Financial Aid (if loans, remember you have to pay those back) - Amount available from savings (for students) - Determine your expenses - Look at your expenses from the previous month or two. - If you don t have a record, make one. Track your spending for a month. - If you have costs that you incur every couple of months or once per year (insurance, car registration); break them down to a per month amount so you can include them in your budget.

28 Creating a Budget - Total your monthly income and expenses - Income > Expenses - Reduce Borrowing (while a student) - Put toward your financial goals: increase savings, save for a larger purchase, pay off credit cards or student loans, etc. - Income < Expenses - Identify areas where you can save money - Cover needs first, wants second - Reduce amount you spend on luxury items eating out, entertainment, cable, etc. - Monitor your Budget regularly

29 Resources General Resources: Budgeting: Getting a Free Credit Score: Credit Bureaus: Questions? Contact Student Financial Management FinancialManagement@law.du.edu Suite 115

GREENPATH FINANCIAL WELLNESS SERIES

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Empowering people to lead financially healthy lives. TABLE OF CONTENTS Understanding credit reports...2 What s in a credit

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Empowering people to lead financially healthy lives. TABLE OF CONTENTS Understanding credit reports...2 What s in a credit

Understanding Credit. Lisa Mitchell, Sallie Mae April 6, Champions of Financial Aid ILASFAA Conference

Understanding Credit Lisa Mitchell, Sallie Mae April 6, 2017 Credit Management Agenda Understanding Your Credit Report Summary: Financial Health Tips Credit Management Credit Basics Credit health plays

Understanding Credit Lisa Mitchell, Sallie Mae April 6, 2017 Credit Management Agenda Understanding Your Credit Report Summary: Financial Health Tips Credit Management Credit Basics Credit health plays

Federal Reserve Bank of Philadelphia

Federal Reserve Bank of Philadelphia 1 When you apply for credit, whether it s a credit card, car loan, or a mortgage, lenders want to know whether you are likely to repay your loan and make the payments

Federal Reserve Bank of Philadelphia 1 When you apply for credit, whether it s a credit card, car loan, or a mortgage, lenders want to know whether you are likely to repay your loan and make the payments

Credit Reports 101. Bill Bufkins, November 3, 2011

Credit Reports 101 Bill Bufkins, November 3, 2011 What is a credit report? A credit report is a record of your past borrowing and repayment activity. The information in your credit report helps determine

Credit Reports 101 Bill Bufkins, November 3, 2011 What is a credit report? A credit report is a record of your past borrowing and repayment activity. The information in your credit report helps determine

Now, let me turn the program over to Jacqueline Cooke, Women s Bureau Regional Administrator in Boston, to introduce our first speaker. Jackie?

Wi$e Up Teleconference Call February 28, 2006 Becoming Credit Smart Speaker 1 Amy Perry Jane Walstedt: Now, let me turn the program over to Jacqueline Cooke, Women s Bureau Regional Administrator in Boston,

Wi$e Up Teleconference Call February 28, 2006 Becoming Credit Smart Speaker 1 Amy Perry Jane Walstedt: Now, let me turn the program over to Jacqueline Cooke, Women s Bureau Regional Administrator in Boston,

Credit and Credit Cards

Credit and Credit Cards What s Next Project Credit Cards They are all around you. Most people have at least one. Some have many. They are credit cards. A credit card allows you to pay for merchandise or

Credit and Credit Cards What s Next Project Credit Cards They are all around you. Most people have at least one. Some have many. They are credit cards. A credit card allows you to pay for merchandise or

Your Credit. Objectives. An Introduction to Personal Credit. By the end of this presentation you will have a understanding of: 1/19/2016.

Your Credit An Introduction to Personal Credit Objectives By the end of this presentation you will have a understanding of: Credit Score Where can I find it? What is it? How do I get it? Advantages of

Your Credit An Introduction to Personal Credit Objectives By the end of this presentation you will have a understanding of: Credit Score Where can I find it? What is it? How do I get it? Advantages of

UNDERSTANDING CREDIT. WASFAA Conference Seattle, WA Speakers: Thalassa Naylor, Sallie Mae Anthony Lombardi, Sallie Mae Date: April 10, 2017

UNDERSTANDING CREDIT WASFAA Conference Seattle, WA Speakers: Thalassa Naylor, Sallie Mae Anthony Lombardi, Sallie Mae Date: April 10, 2017 Agenda 2 Credit Management Protect Yourself Understanding Your

UNDERSTANDING CREDIT WASFAA Conference Seattle, WA Speakers: Thalassa Naylor, Sallie Mae Anthony Lombardi, Sallie Mae Date: April 10, 2017 Agenda 2 Credit Management Protect Yourself Understanding Your

Understanding Credit. What it is, why it s important, and how you can maintain it. Brought to you by Sallie Mae and FICO

Understanding Credit What it is, why it s important, and how you can maintain it Brought to you by Sallie Mae and FICO Introduction A student loan may be your first major credit experience. This is a good

Understanding Credit What it is, why it s important, and how you can maintain it Brought to you by Sallie Mae and FICO Introduction A student loan may be your first major credit experience. This is a good

Understanding Credit

Understanding Credit LAURA STEINBECK DIRECTOR OF BUSINESS DEVELOPMENT, SALLIE MAE 2018 MASFAP CONFERENCE Agenda 2 Credit Management Protect Yourself Understanding Credit Reports Summary: Financial Health

Understanding Credit LAURA STEINBECK DIRECTOR OF BUSINESS DEVELOPMENT, SALLIE MAE 2018 MASFAP CONFERENCE Agenda 2 Credit Management Protect Yourself Understanding Credit Reports Summary: Financial Health

UNDERSTANDING YOUR CREDIT REPORT & YOUR CREDIT SCORE

UNDERSTANDING YOUR CREDIT REPORT & YOUR CREDIT SCORE Presented By: Tom Painter Chief Lending Officer WHAT IS A CREDIT SCORE? A credit score is a number that summarizes your credit risk, based on a snapshot

UNDERSTANDING YOUR CREDIT REPORT & YOUR CREDIT SCORE Presented By: Tom Painter Chief Lending Officer WHAT IS A CREDIT SCORE? A credit score is a number that summarizes your credit risk, based on a snapshot

Credit and Debt.notebook August 28, 2014

Credit and Debt What does it mean to have credit? Credit means someone is willing to loan you money in exchange for your promise to repay it, usually with interest. Interest the amount of money you pay

Credit and Debt What does it mean to have credit? Credit means someone is willing to loan you money in exchange for your promise to repay it, usually with interest. Interest the amount of money you pay

Reviewing C YouR CRedit RepoRt

ChapteR 2 Reviewing C YouR CRedit RepoRt What do your creditors have to say about the way you handle money? Having a good credit score can help you turn your home-buying dream into a reality. There s much

ChapteR 2 Reviewing C YouR CRedit RepoRt What do your creditors have to say about the way you handle money? Having a good credit score can help you turn your home-buying dream into a reality. There s much

UNDERSTANDING CREDIT. KASFAA Conference Manhattan, KS April 21, Robb Cummings Director of Business Development

UNDERSTANDING CREDIT KASFAA Conference Manhattan, KS April 21, 2016 Robb Cummings Director of Business Development FICO Score 2 A FICO Score is a three-digit number calculated from the credit information

UNDERSTANDING CREDIT KASFAA Conference Manhattan, KS April 21, 2016 Robb Cummings Director of Business Development FICO Score 2 A FICO Score is a three-digit number calculated from the credit information

Credit Reports & Credit Scores 101. Mary C. Hurlburt Certified Consumer Credit Counselor and Score Volunteer

Credit Reports & Credit Scores 101 Mary C. Hurlburt Certified Consumer Credit Counselor and Score Volunteer mary.hurlburt@scorevolunteer.org Mary Hurlburt Mary Hurlburt is the Financial Counseling and

Credit Reports & Credit Scores 101 Mary C. Hurlburt Certified Consumer Credit Counselor and Score Volunteer mary.hurlburt@scorevolunteer.org Mary Hurlburt Mary Hurlburt is the Financial Counseling and

Does providing FICO Scores influence financial behavior?

Power of Our Past Force of Our Future Does providing FICO Scores influence financial behavior? October 2018 Jeff Johnston, MBA Sallie Mae Ohio Association of Student Financial Aid Administrators 50th Anniversary

Power of Our Past Force of Our Future Does providing FICO Scores influence financial behavior? October 2018 Jeff Johnston, MBA Sallie Mae Ohio Association of Student Financial Aid Administrators 50th Anniversary

Credit Cards. Annual Percentage Rate - What you are paying each month -- unpaid balances calculated as a percentage.

Credit Cards Annual Fee - Amount you pay each year to have a credit card. Annual Percentage Rate - What you are paying each month -- unpaid balances calculated as a percentage. Balance - The total charges

Credit Cards Annual Fee - Amount you pay each year to have a credit card. Annual Percentage Rate - What you are paying each month -- unpaid balances calculated as a percentage. Balance - The total charges

Chapter 26 11/9/2017 1

Chapter 26 11/9/2017 1 Average college students has 3 credit cards Also between $1500 & $2000 in debt Things to know if you re getting a credit card Who accepts it? What amount can you charge to meet your

Chapter 26 11/9/2017 1 Average college students has 3 credit cards Also between $1500 & $2000 in debt Things to know if you re getting a credit card Who accepts it? What amount can you charge to meet your

Justine PETERSEN Building Assets. Changing Lives. Credit Report Basics and Definitions Justine PETERSEN Credit Building Training

Justine PETERSEN Building Assets. Changing Lives Credit Report Basics and Definitions Justine PETERSEN Credit Building Training Included Topics Who reports to the credit bureaus Statute of Limitations

Justine PETERSEN Building Assets. Changing Lives Credit Report Basics and Definitions Justine PETERSEN Credit Building Training Included Topics Who reports to the credit bureaus Statute of Limitations

Budgeting & Debt Basics

Budgeting & Debt Basics Why Have a Budget? Gain control over your finances Get the most out of your money Achieve your financial goals What is a Budget? A plan for saving and spending Allows you to choose

Budgeting & Debt Basics Why Have a Budget? Gain control over your finances Get the most out of your money Achieve your financial goals What is a Budget? A plan for saving and spending Allows you to choose

Loan Exit Counseling & Money Management. Wesleyan University May 2017

Loan Exit Counseling & Money Management Wesleyan University May 2017 Important Things to Know Understand your student loan portfolio Know what types of loans you have Know what your loan terms are: interest

Loan Exit Counseling & Money Management Wesleyan University May 2017 Important Things to Know Understand your student loan portfolio Know what types of loans you have Know what your loan terms are: interest

HOW TO USE CREDIT. Latino Community Credit Union & the Latino Community Development Center.

HOW TO USE CREDIT Latino Community Credit Union & the Latino Community Development Center www.latinoccu.org Copyright 2016 Latino Community Credit Union Made possible by a generous contribution from the

HOW TO USE CREDIT Latino Community Credit Union & the Latino Community Development Center www.latinoccu.org Copyright 2016 Latino Community Credit Union Made possible by a generous contribution from the

Understanding Credit Reports and Scores and How to Improve It!

Understanding Credit Reports and Scores and How to Improve It! Ryan Chatterton, CCCC What Will We Cover? When we are finished, you will understand: Credit Reports and Credit Scores - What they are and

Understanding Credit Reports and Scores and How to Improve It! Ryan Chatterton, CCCC What Will We Cover? When we are finished, you will understand: Credit Reports and Credit Scores - What they are and

Understanding Your FICO Score. Understanding FICO Scores

Understanding Your FICO Score Understanding FICO Scores 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Reports

Understanding Your FICO Score Understanding FICO Scores 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Reports

Introduction. In short- credit is an essential part of our personal and national economic stability.

Table of Contents 2 Introduction 3 The Wait Is Over!. 4 The Five Factors that Determine your FICO Score Are: 5 What is Seasoned Trade Lines?... 7 How Do I Raise My FICO Score with Seasoned Trade Lines.

Table of Contents 2 Introduction 3 The Wait Is Over!. 4 The Five Factors that Determine your FICO Score Are: 5 What is Seasoned Trade Lines?... 7 How Do I Raise My FICO Score with Seasoned Trade Lines.

Welcome. 1. Agenda. 2. Ground Rules. 3. Introductions. Charge It Right 2

Charge It Right Welcome 1. Agenda 2. Ground Rules 3. Introductions Charge It Right 2 Objectives Define credit Explain why credit is important Identify the factors creditors look for when making credit

Charge It Right Welcome 1. Agenda 2. Ground Rules 3. Introductions Charge It Right 2 Objectives Define credit Explain why credit is important Identify the factors creditors look for when making credit

Chapter 6 - Credit. Section 6.1

Chapter 6 - Credit Section 6.1 Credit is a medium of exchange which allows individuals to buy goods or services now and pay for them later The creditor supplies money, goods, or services in a credit agreement

Chapter 6 - Credit Section 6.1 Credit is a medium of exchange which allows individuals to buy goods or services now and pay for them later The creditor supplies money, goods, or services in a credit agreement

A Special Report by Laura Adams, author of Money Girl s Smart Moves to Grow Rich

3 Strategies to Build Credit FAST A Special Report by Laura Adams, author of Money Girl s Smart Moves to Grow Rich 3 Strategies to Build Credit Fast Copyright 2011 SmartMovesToGrowRich.com All rights reserved.

3 Strategies to Build Credit FAST A Special Report by Laura Adams, author of Money Girl s Smart Moves to Grow Rich 3 Strategies to Build Credit Fast Copyright 2011 SmartMovesToGrowRich.com All rights reserved.

How Students Use Credit and What You Need to Know. Deb Gossman College Ave Student Loans

How Students Use Credit and What You Need to Know Deb Gossman College Ave Student Loans 3-19-2019 Agenda Private credit within the student loan ecosystem & compared to other consumer assets Credit Reports

How Students Use Credit and What You Need to Know Deb Gossman College Ave Student Loans 3-19-2019 Agenda Private credit within the student loan ecosystem & compared to other consumer assets Credit Reports

February 2015 Wednesday Webinar ~ Credit Matters - Resources to Educate Students About Credit and Debt

February 2015 Wednesday Webinar ~ Credit Matters - Resources to Educate Students About Credit and Debt 1 Mike Fagone Jennifer Pincus Jessica Whittier Bernstein Shur US Dept. of Justice FAME 2 About CARE

February 2015 Wednesday Webinar ~ Credit Matters - Resources to Educate Students About Credit and Debt 1 Mike Fagone Jennifer Pincus Jessica Whittier Bernstein Shur US Dept. of Justice FAME 2 About CARE

Introduction. Purpose. Student Introductions. Objectives (Continued) Objectives

Objectives") Introduction Instructor and student introductions. Module overview. 1 2 Your name. Student Introductions Your expectations, questions and concerns about credit cards. Purpose will teach you about credit

Introduction Instructor and student introductions. Module overview. 1 2 Your name. Student Introductions Your expectations, questions and concerns about credit cards. Purpose will teach you about credit

Project Pro$per. Credit Reports and Credit Scores

Project Pro$per Presents Credit Reports and Credit Scores Participant Guide www.projectprosper.org www.facebook.com/projectprosper Based on Wells Fargo s Hands on Banking The Hands on Banking program is

Project Pro$per Presents Credit Reports and Credit Scores Participant Guide www.projectprosper.org www.facebook.com/projectprosper Based on Wells Fargo s Hands on Banking The Hands on Banking program is

FICO Score Open Access Consumer Credit Education US Version. Frequently Asked Questions about FICO Scores

FICO Score Open Access Consumer Credit Education US Version Frequently Asked Questions about Scores 2012 Fair Isaac Corporation. All rights reserved. 1 January 01, 2012 Table of Contents About Scores...

FICO Score Open Access Consumer Credit Education US Version Frequently Asked Questions about Scores 2012 Fair Isaac Corporation. All rights reserved. 1 January 01, 2012 Table of Contents About Scores...

Money Management Curriculum

Money Management Module 4: Credit Reports & Credit Scores Money Management Curriculum Module 4: Credit Reports & Credit Scores Project Team: Ruby Ward, Professor, Utah State University Trent Teegerstrom,

Money Management Module 4: Credit Reports & Credit Scores Money Management Curriculum Module 4: Credit Reports & Credit Scores Project Team: Ruby Ward, Professor, Utah State University Trent Teegerstrom,

Secrets to Success: Personal Finance Management

Secrets to Success: Personal Finance Management Harvard University Employees Credit Union (HUECU) A financial institution exclusively serving the Harvard University students, alumni, faculty, staff, and

Secrets to Success: Personal Finance Management Harvard University Employees Credit Union (HUECU) A financial institution exclusively serving the Harvard University students, alumni, faculty, staff, and

TABLE OF CONTENTS. Healthier Black Elders Center

TABLE OF CONTENTS What is credit............................................1 The five C s of credit...................................... 2 Types of credit...........................................3

TABLE OF CONTENTS What is credit............................................1 The five C s of credit...................................... 2 Types of credit...........................................3

CREDIT: HELPFUL OR HURTFUL? Ch 13 Section 1

CREDIT: HELPFUL OR HURTFUL? Ch 13 Section 1 DO NOW: T/F? 1. Using credit can lead to serious problems. 2. When you charge a purchase with a credit card, you can withhold payment if the product is defective.

CREDIT: HELPFUL OR HURTFUL? Ch 13 Section 1 DO NOW: T/F? 1. Using credit can lead to serious problems. 2. When you charge a purchase with a credit card, you can withhold payment if the product is defective.

Beyond the Classroom. Blaise P. Johnson Gate City Bank

Beyond the Classroom Blaise P. Johnson Gate City Bank 1 Topics To Be Discussed 1. Credit Reports & Credit Scores 2. Repayment/Consolidation of Student Loans 3. Obtaining A Personal or Home Loan 4. Open

Beyond the Classroom Blaise P. Johnson Gate City Bank 1 Topics To Be Discussed 1. Credit Reports & Credit Scores 2. Repayment/Consolidation of Student Loans 3. Obtaining A Personal or Home Loan 4. Open

Building a U.S. credit score

Building a U.S. credit score A strong credit history could help improve many aspects of your life in the U.S. Here s our guide for new-to-country residents. Together We Thrive When moving overseas, it

Building a U.S. credit score A strong credit history could help improve many aspects of your life in the U.S. Here s our guide for new-to-country residents. Together We Thrive When moving overseas, it

Credit Building Apps

Credit Building Apps Apps that Can Help Build and Repair Credit Webinar of September 27, 2018 Sponsored by Community Development and the Payments, Standards, and Outreach Group of the Federal Reserve Bank

Credit Building Apps Apps that Can Help Build and Repair Credit Webinar of September 27, 2018 Sponsored by Community Development and the Payments, Standards, and Outreach Group of the Federal Reserve Bank

in Head Start Credit and Debt: Make it work for you!

in Head Start Credit and Debt: Make it work for you! Annual Credit Report Request Form You have the right to get a free copy of your credit file disclosure, commonly called a credit report, once every

in Head Start Credit and Debt: Make it work for you! Annual Credit Report Request Form You have the right to get a free copy of your credit file disclosure, commonly called a credit report, once every

13.1. Reading a Credit Report EXERCISE. THEME 4 Lesson 13: Applying for Credit NAME: CLASS PERIOD:

13.1 NAME: CLASS PERIOD: Reading a Credit Report Your ability to qualify for a loan depends on a credit report. A credit report is a record of an individual s personal credit history. It is probably a

13.1 NAME: CLASS PERIOD: Reading a Credit Report Your ability to qualify for a loan depends on a credit report. A credit report is a record of an individual s personal credit history. It is probably a

12/5/2013. Cash Management: Overview. More Month Than Money and Extra Credit. Why are you here? Benefits of developing a budget

12/5/2013 Cash Management: Overview More Month Than Money and Extra Credit Sean L. Mabey smabey@neamb.com Understanding cash management Age old questions: Where oh where does our money go? Making a budget

12/5/2013 Cash Management: Overview More Month Than Money and Extra Credit Sean L. Mabey smabey@neamb.com Understanding cash management Age old questions: Where oh where does our money go? Making a budget

TIP: Make sure this information is correct. A wrong address or phone number could be a mistake or a sign of identity theft.

Reading a Sample Credit Report This sample report shows what kind of information might appear on your own credit report, also called a consumer disclosure statement, from the 3 major Credit Reporting Agencies

Reading a Sample Credit Report This sample report shows what kind of information might appear on your own credit report, also called a consumer disclosure statement, from the 3 major Credit Reporting Agencies

CHAPTER 8. Personal Finance. Copyright 2015, 2011, 2007 Pearson Education, Inc. Section 8.7, Slide 1

CHAPTER 8 Personal Finance Copyright 2015, 2011, 2007 Pearson Education, Inc. Section 8.7, Slide 1 8.8 Credit Cards Copyright 2015, 2011, 2007 Pearson Education, Inc. Section 8.7, Slide 2 Objectives 1.

CHAPTER 8 Personal Finance Copyright 2015, 2011, 2007 Pearson Education, Inc. Section 8.7, Slide 1 8.8 Credit Cards Copyright 2015, 2011, 2007 Pearson Education, Inc. Section 8.7, Slide 2 Objectives 1.

Understanding. What you need to know about the most widely used credit scores

Understanding What you need to know about the most widely used credit scores 300 850 The score lenders use. FICO Scores are the most widely used credit scores according to a recent CEB TowerGroup analyst

Understanding What you need to know about the most widely used credit scores 300 850 The score lenders use. FICO Scores are the most widely used credit scores according to a recent CEB TowerGroup analyst

Understanding Vehicle Financing

Understanding Vehicle Financing Understanding Vehicle Financing With prices averaging more than $31,000 for a new vehicle and $17,000 for a used model from a dealership, you might consider financing or

Understanding Vehicle Financing Understanding Vehicle Financing With prices averaging more than $31,000 for a new vehicle and $17,000 for a used model from a dealership, you might consider financing or

FarmHouse International Fraternity New Member Education Program Topic Summary: Personal Finance

FarmHouse International Fraternity New Member Education Program Topic Summary: Personal Finance 11 College is a challenging time both in and out of class. As a student you are coping with a new environment

FarmHouse International Fraternity New Member Education Program Topic Summary: Personal Finance 11 College is a challenging time both in and out of class. As a student you are coping with a new environment

Take Charge: Wise Use of Credit Cards. Brought to you by ALEC

Take Charge: Wise Use of Credit Cards Brought to you by ALEC Seminar Objectives LEARN: Advantages/pitfalls of credit cards How CARD Act affects you How to build solid credit foundation Warning signs: too

Take Charge: Wise Use of Credit Cards Brought to you by ALEC Seminar Objectives LEARN: Advantages/pitfalls of credit cards How CARD Act affects you How to build solid credit foundation Warning signs: too

Personal Credit Fundamentals &

Personal Credit Fundamentals & Your Credit Score Presented by: Harvard University Employees Credit Union Harvard Student Sources of Financial Education Sources of consumer finance education Formal Program

Personal Credit Fundamentals & Your Credit Score Presented by: Harvard University Employees Credit Union Harvard Student Sources of Financial Education Sources of consumer finance education Formal Program

Fact, Fiction & FICOs: Presented by: Vance Edwards, CMB Certified FICO Professional MGIC Marketing Program Director

Fact, Fiction & FICOs: Presented by: Vance Edwards, CMB Certified FICO Professional MGIC Marketing Program Director Agenda What makes up a credit score (and what doesn t) What causes that score to move

Fact, Fiction & FICOs: Presented by: Vance Edwards, CMB Certified FICO Professional MGIC Marketing Program Director Agenda What makes up a credit score (and what doesn t) What causes that score to move

Keeping Finances Under Control. How to Manage Debt so it Doesn t Manage You

Keeping Finances Under Control How to Manage Debt so it Doesn t Manage You Seminar Objectives What is DEBT? What are the types of debt? What is good debt? What is bad debt? What are the benefits and costs?

Keeping Finances Under Control How to Manage Debt so it Doesn t Manage You Seminar Objectives What is DEBT? What are the types of debt? What is good debt? What is bad debt? What are the benefits and costs?

Credit Education Program

Credit Education Program Course Objectives Identify ways to decrease spending and increase income Read and understand the purpose of your credit report Discuss common debt traps to avoid How lenders evaluate

Credit Education Program Course Objectives Identify ways to decrease spending and increase income Read and understand the purpose of your credit report Discuss common debt traps to avoid How lenders evaluate

Financial Fitness: MONEY Matters

Financial Fitness: MONEY Matters Financial Literacy and Education University of Colorado Denver Spring 2015 Presenter: M. Lesa Briggs After this presentation, you will be able to: Evaluate your student

Financial Fitness: MONEY Matters Financial Literacy and Education University of Colorado Denver Spring 2015 Presenter: M. Lesa Briggs After this presentation, you will be able to: Evaluate your student

What is credit and why does it matter to me?

Understanding Credit 1 Money Matters The BIG Idea What is credit and why does it matter to me? AGENDA Approx. 45 minutes I. Warm Up: What Do You Know About Credit? (10 minutes) II. Credit: The Good, The

Understanding Credit 1 Money Matters The BIG Idea What is credit and why does it matter to me? AGENDA Approx. 45 minutes I. Warm Up: What Do You Know About Credit? (10 minutes) II. Credit: The Good, The

Be Credit Wise Credit is a way of having something now and paying for it later. Many

Be Credit Wise Credit is a way of having something now and paying for it later. Many of us want to take advantage of flexibility in our spending plans by using credit. Credit isn t free; it s paid for

Be Credit Wise Credit is a way of having something now and paying for it later. Many of us want to take advantage of flexibility in our spending plans by using credit. Credit isn t free; it s paid for

Financial Well-being. Debt and Credit

Financial Well-being Debt and Credit Debt and Credit When evaluating financial wellness, debt has a real impact on your ability to reach your goals. Debt feels like a four letter word. However, it can

Financial Well-being Debt and Credit Debt and Credit When evaluating financial wellness, debt has a real impact on your ability to reach your goals. Debt feels like a four letter word. However, it can

Module 2 Good. Your score in the game of life

Module 2 Good Credit Your score in the game of life Keys to Your Financial Future 1 Module 2: Good Credit Your Score in the Game of Life Keys to Your Financial Future is designed to help you plan how

Module 2 Good Credit Your score in the game of life Keys to Your Financial Future 1 Module 2: Good Credit Your Score in the Game of Life Keys to Your Financial Future is designed to help you plan how

Charge It Right. FDIC Money Smart for Young Adults. Building: Knowledge, Security, Confidence

Charge It Right FDIC Money Smart for Young Adults PNC is proud to work with the FDIC to offer their Money Smart program to our customers, to support lifelong learning in Financial Education. Building:

Charge It Right FDIC Money Smart for Young Adults PNC is proud to work with the FDIC to offer their Money Smart program to our customers, to support lifelong learning in Financial Education. Building:

Credit score ratings chart 2017

Credit score ratings chart 2017 By 2009 the worldwide bond market (total debt outstanding) reached an estimated $82.2 trillion, in 2009 dollars. [26]. As the influence and profitability of CRAs expanded,

Credit score ratings chart 2017 By 2009 the worldwide bond market (total debt outstanding) reached an estimated $82.2 trillion, in 2009 dollars. [26]. As the influence and profitability of CRAs expanded,

A CONSUMER S GUIDE TO INSURANCE COMPANIES' USE OF CREDIT INFORMATION

A CONSUMER S GUIDE TO INSURANCE COMPANIES' USE OF CREDIT INFORMATION INSURANCE CREDIT SCORING IN NORTH CAROLINA Insurance companies licensed to sell private passenger automobile and residential property

A CONSUMER S GUIDE TO INSURANCE COMPANIES' USE OF CREDIT INFORMATION INSURANCE CREDIT SCORING IN NORTH CAROLINA Insurance companies licensed to sell private passenger automobile and residential property

Understanding Credit Reports

Understanding Credit Reports Family Economics & Financial Education Take Charge of Your Finances Credit Report Detectives Meet Isabella, your new client: About to graduate from college In extreme debt

Understanding Credit Reports Family Economics & Financial Education Take Charge of Your Finances Credit Report Detectives Meet Isabella, your new client: About to graduate from college In extreme debt

Question of the Day. What percent of year olds have a credit card?

Chapter 6.1 Credit Objectives Explain the advantages and disadvantages of using credit Identify the different types of consumer credit Describe secured and unsecured loans Describe how to establish a sound

Chapter 6.1 Credit Objectives Explain the advantages and disadvantages of using credit Identify the different types of consumer credit Describe secured and unsecured loans Describe how to establish a sound

FINANCIAL FITNESS EDUCATION

(Agency s Name & Logo) FINANCIAL FITNESS EDUCATION Sponsored by BETTER FORTUNES Control Your Money Control Your Life Knowing the difference can make all the difference Chapter One ECONOMIC WAY OF THINKING

(Agency s Name & Logo) FINANCIAL FITNESS EDUCATION Sponsored by BETTER FORTUNES Control Your Money Control Your Life Knowing the difference can make all the difference Chapter One ECONOMIC WAY OF THINKING

Your Guide To Better Credit

Your Guide To Better Credit INTRODUCTION Your go-to guide to better credit It seems like every other commercial on television touts some sort of offer around credit. You hear things like, Free credit report,

Your Guide To Better Credit INTRODUCTION Your go-to guide to better credit It seems like every other commercial on television touts some sort of offer around credit. You hear things like, Free credit report,

BASIC FINANCIAL LITERACY. Economics Marshall High School Mr. Cline Unit Three DD

BASIC FINANCIAL LITERACY Economics Marshall High School Mr. Cline Unit Three DD * Nothing So Simple Has Ever Been So Hard Reconciling their account on a regular basis could have helped prevent this! Credit

BASIC FINANCIAL LITERACY Economics Marshall High School Mr. Cline Unit Three DD * Nothing So Simple Has Ever Been So Hard Reconciling their account on a regular basis could have helped prevent this! Credit

Smart Credit Strategies for Small Business Owners

Smart Credit Strategies for Small Business Owners Why Credit Matters When it comes to growing your business, strong credit scores can give you a significant advantage. Access to credit at good terms when

Smart Credit Strategies for Small Business Owners Why Credit Matters When it comes to growing your business, strong credit scores can give you a significant advantage. Access to credit at good terms when

Profiles in Credit is designed to be flexible and meet the needs of learners in different educational settings. Examples include:

Profiles in Credit Educator Resource Guide Module Summary Profiles in Credit is a self-paced, interactive learning module in which students visit the social media profiles of three young people facing

Profiles in Credit Educator Resource Guide Module Summary Profiles in Credit is a self-paced, interactive learning module in which students visit the social media profiles of three young people facing

Using Credit. services but do not require payments in full when the service is performed.

Using Credit How would you like to pay for this, cash or charge? Chances are you have heard this question asked. Cash or charge? is really asking you, the buyer, if you want to use the cash or the money

Using Credit How would you like to pay for this, cash or charge? Chances are you have heard this question asked. Cash or charge? is really asking you, the buyer, if you want to use the cash or the money

12 common questions. About consumer credit and direct marketing

12 common questions About consumer credit and direct marketing Most of us don t think about credit until a specific event sparks our interest. Maybe we want to buy a car or home. Or perhaps we receive

12 common questions About consumer credit and direct marketing Most of us don t think about credit until a specific event sparks our interest. Maybe we want to buy a car or home. Or perhaps we receive

Module 7 - Credit Reporting HANDOUT 7-1

ParticipantHandbook 1 Module 7 - Credit Reporting HANDOUT 7-1 Credit bureaus Credit bureaus are agencies that collect information about how we use credit. They produce personal credit reports. Credit bureaus

ParticipantHandbook 1 Module 7 - Credit Reporting HANDOUT 7-1 Credit bureaus Credit bureaus are agencies that collect information about how we use credit. They produce personal credit reports. Credit bureaus

Improving Your Credit

Teacher Homebuyer Guide to: Improving Your Credit By John Godbey, Founder and Broker of Teacher Homebuyer Real Estate Introduction Thank you for signing up for our E-Guide "Improving Your Credit." We find

Teacher Homebuyer Guide to: Improving Your Credit By John Godbey, Founder and Broker of Teacher Homebuyer Real Estate Introduction Thank you for signing up for our E-Guide "Improving Your Credit." We find

Credit Reports and Scores

Credit Reports and Scores Advanced Level The Importance of a Credit History for Obtaining Credit Credit refers to borrowing. You have used credit if you receive money, goods, or services in exchange for

Credit Reports and Scores Advanced Level The Importance of a Credit History for Obtaining Credit Credit refers to borrowing. You have used credit if you receive money, goods, or services in exchange for

c» BALANCE C:» Financially Empowering You The World of Credit Reports Podcast [Music plays] Nikki:

![c» BALANCE C:» Financially Empowering You The World of Credit Reports Podcast [Music plays] Nikki:](/thumbs/76/73531259.jpg "c» BALANCE C:» Financially Empowering You The World of Credit Reports Podcast [Music plays] Nikki:") The World of Credit Reports Podcast [Music plays] Nikki: You re listening to world of credit. Hi, I m Nikki, your host for today s podcast. Credit reports and credit scores influence our lives in many

The World of Credit Reports Podcast [Music plays] Nikki: You re listening to world of credit. Hi, I m Nikki, your host for today s podcast. Credit reports and credit scores influence our lives in many

Credit Score: What it Means to your Business

Score: What it Means to your Business Introduction Author Michael K. Swan, Washington State University Reviewers Gary Thome, Riverland Community College Peter Scheffert, Riverland Community College Along

Score: What it Means to your Business Introduction Author Michael K. Swan, Washington State University Reviewers Gary Thome, Riverland Community College Peter Scheffert, Riverland Community College Along

Lesson 5: Credit and Debt

Lesson 5: Credit and Debt debt: something owed to a person or an organization credit: the privilege granted to approved clients to receive goods or services and to pay for them in the future In February

Lesson 5: Credit and Debt debt: something owed to a person or an organization credit: the privilege granted to approved clients to receive goods or services and to pay for them in the future In February

SEVEN LIFE-DEFINING FINANCIAL DECISIONS

SEVEN LIFE-DEFINING FINANCIAL DECISIONS A Joint Project of The Actuarial Foundation and WISER, the Women's Institute for a Secure Retirement 4 HOME OWNERSHIP, DEBT, AND CREDIT Buying a home is one of the

SEVEN LIFE-DEFINING FINANCIAL DECISIONS A Joint Project of The Actuarial Foundation and WISER, the Women's Institute for a Secure Retirement 4 HOME OWNERSHIP, DEBT, AND CREDIT Buying a home is one of the

Your Money, Your Goals Spotlight Series. Understanding credit reports and scores: An in-depth look

Your Money, Your Goals Spotlight Series Understanding credit reports and scores: An in-depth look DISCLAIMER This presentation is being made by a Consumer Financial Protection Bureau representative on

Your Money, Your Goals Spotlight Series Understanding credit reports and scores: An in-depth look DISCLAIMER This presentation is being made by a Consumer Financial Protection Bureau representative on

FICO Score Open Access Consumer Credit Education US Version. Frequently Asked Questions about the FICO Score

FICO Score Open Access Consumer Credit Education US Version Frequently Asked Questions about the FICO Score 2012 Fair Isaac Corporation. All rights reserved. 1 January 01, 2012 Table of Contents About

FICO Score Open Access Consumer Credit Education US Version Frequently Asked Questions about the FICO Score 2012 Fair Isaac Corporation. All rights reserved. 1 January 01, 2012 Table of Contents About

FINANCIAL LITERACY WHAT YOU NEED TO KNOW TO SURVIVE IN TODAY S ECONOMY

FINANCIAL LITERACY WHAT YOU NEED TO KNOW TO SURVIVE IN TODAY S ECONOMY Presented by: Terry Lawson Lawson Law Center 700 E. 8 th St. Kansas City, MO 64106 www.llckc.com LAWSON LAW CENTER LLC WWW. LLCKC.COM

FINANCIAL LITERACY WHAT YOU NEED TO KNOW TO SURVIVE IN TODAY S ECONOMY Presented by: Terry Lawson Lawson Law Center 700 E. 8 th St. Kansas City, MO 64106 www.llckc.com LAWSON LAW CENTER LLC WWW. LLCKC.COM

12 Steps to Improved Credit Steven K. Shapiro

12 Steps to Improved Credit Steven K. Shapiro 2009 2018 sks@skscci.com In my previous article, I wrote about becoming debt-free and buying everything with cash. Even while I was writing the article, I

12 Steps to Improved Credit Steven K. Shapiro 2009 2018 sks@skscci.com In my previous article, I wrote about becoming debt-free and buying everything with cash. Even while I was writing the article, I

Your Ultimate Guide to DIY Credit Repair. January

Your Ultimate Guide to DIY Credit Repair January 2018 www.upturncredit.com Table of Contents Part 1 - Anatomy of a Credit Report Part 2 - Credit Scores vs Credit Reports Part 3 - Why Your Credit Report

Your Ultimate Guide to DIY Credit Repair January 2018 www.upturncredit.com Table of Contents Part 1 - Anatomy of a Credit Report Part 2 - Credit Scores vs Credit Reports Part 3 - Why Your Credit Report

UNDERSTANDING BUSINESS CREDIT

YOUR GUIDE TO UNDERSTANDING BUSINESS CREDIT POOR YOUR BUSINESS CREDIT PROFILE GOOD SPONSORED BY UNDERSTANDING YOUR PERSONAL CREDIT PROFILE Every small business owner has two credit profiles: 1. Your personal

YOUR GUIDE TO UNDERSTANDING BUSINESS CREDIT POOR YOUR BUSINESS CREDIT PROFILE GOOD SPONSORED BY UNDERSTANDING YOUR PERSONAL CREDIT PROFILE Every small business owner has two credit profiles: 1. Your personal

ECONOMIC EDUCATION FOR CONSUMERS Chapter 10

WHAT S AHEAD 10.1 What Is Credit? 10.2 How to Qualify for Credit 10.3 Sources of Consumer Credit 10.4 Credit Rights and Responsibilities 10.5 Maintain a Good Credit Rating LESSON 10.1 What Is Credit? GOALS

WHAT S AHEAD 10.1 What Is Credit? 10.2 How to Qualify for Credit 10.3 Sources of Consumer Credit 10.4 Credit Rights and Responsibilities 10.5 Maintain a Good Credit Rating LESSON 10.1 What Is Credit? GOALS

FICO Scores Decoded Discover How to Easily and Quickly Obtain Excellent FICO Credit Scores Regardless of Your Personal Credit Quality Now

Discover How to Easily and Quickly Obtain Excellent FICO Credit Scores Regardless of Your Personal Credit Quality Now Discover How to Easily and Quickly Obtain Excellent FICO Credit Scores Regardless of

Discover How to Easily and Quickly Obtain Excellent FICO Credit Scores Regardless of Your Personal Credit Quality Now Discover How to Easily and Quickly Obtain Excellent FICO Credit Scores Regardless of

UNDERSTANDING CREDIT REPORTS AND SCORES

UNDERSTANDING CREDIT REPORTS AND SCORES 1-888-282-5811 www.myfinancialgoals.org THE NEED FOR GOOD CREDIT Some financial goals cannot be accomplished in one payment for example, an automobile or a house

UNDERSTANDING CREDIT REPORTS AND SCORES 1-888-282-5811 www.myfinancialgoals.org THE NEED FOR GOOD CREDIT Some financial goals cannot be accomplished in one payment for example, an automobile or a house

Your Guide to Cars, Insurance and Identity Theft

Ignition Your Guide to Cars, Insurance and Identity Theft Each step toward independence comes with questions about finances that may affect your future. We ve got you covered; this booklet can answer some

Ignition Your Guide to Cars, Insurance and Identity Theft Each step toward independence comes with questions about finances that may affect your future. We ve got you covered; this booklet can answer some

Understanding Your FICO Score

Understanding Your FICO Score Contents Your FICO Score A Vital Part of Your Credit Health............ 1 How FICO Scores Help You................ 2 Your Credit Report The Basis of Your FICO Score..............

Understanding Your FICO Score Contents Your FICO Score A Vital Part of Your Credit Health............ 1 How FICO Scores Help You................ 2 Your Credit Report The Basis of Your FICO Score..............

Rebuilding YOUR CREDIT. Leader s Guide

Rebuilding YOUR CREDIT Leader s Guide C CONTENTS Table of contents Page Topic 1 Introduction 2 Damaged credit 2 Credit reports 5 Mistakes on your credit report 6 Credit scoring 8 Credit repair offers 8

Rebuilding YOUR CREDIT Leader s Guide C CONTENTS Table of contents Page Topic 1 Introduction 2 Damaged credit 2 Credit reports 5 Mistakes on your credit report 6 Credit scoring 8 Credit repair offers 8

CREDIT SESSION OBJECTIVES SUBJECT INDEX

CREDIT SESSION OBJECTIVES In today s economy, it would be rare not to use credit to pay for large purchases, such as car repairs or any type of emergency situation. Credit can be an overwhelming topic,

CREDIT SESSION OBJECTIVES In today s economy, it would be rare not to use credit to pay for large purchases, such as car repairs or any type of emergency situation. Credit can be an overwhelming topic,

Twelve common questions. About consumer credit and direct marketing

Twelve common questions About consumer credit and direct marketing Twelve common questions Most of us don t think about credit until a specific event sparks our interest. Maybe we want to buy a car or

Twelve common questions About consumer credit and direct marketing Twelve common questions Most of us don t think about credit until a specific event sparks our interest. Maybe we want to buy a car or

How Much House Can You Afford?

03 4580 CH02 4/4/06 4:11 PM Page 15 How Much House Can You Afford? 2 Chapter In This Chapter Calculating your total income and monthly expenses Finding your appropriate price range or knowing how much

03 4580 CH02 4/4/06 4:11 PM Page 15 How Much House Can You Afford? 2 Chapter In This Chapter Calculating your total income and monthly expenses Finding your appropriate price range or knowing how much

Managing Credit & Debt. Presenter: [William Cheeks, ABBA Associates Inc.] Jump$tart Teacher Training Program Managing Credit & Debt

![Managing Credit & Debt. Presenter: [William Cheeks, ABBA Associates Inc.] Jump$tart Teacher Training Program Managing Credit & Debt](/thumbs/81/82773138.jpg "Managing Credit & Debt. Presenter: [William Cheeks, ABBA Associates Inc.] Jump$tart Teacher Training Program Managing Credit & Debt") Managing Credit & Debt Presenter: [William Cheeks, ABBA Associates Inc.] Jump$tart Teacher Training Program Managing Credit & Debt EIGHT TOP FINANCIAL WORRIES OF AMERICANS Affording Retirement Affording

Managing Credit & Debt Presenter: [William Cheeks, ABBA Associates Inc.] Jump$tart Teacher Training Program Managing Credit & Debt EIGHT TOP FINANCIAL WORRIES OF AMERICANS Affording Retirement Affording

Credit Reports and Scores

Credit Reports and Scores Advanced Level The Credit Process Credit goods, services, and/or money received in exchange for a promise to pay back a definite sum of money at a future date Borrower Someone

Credit Reports and Scores Advanced Level The Credit Process Credit goods, services, and/or money received in exchange for a promise to pay back a definite sum of money at a future date Borrower Someone

Understanding Debt Problems & Solutions

Understanding Debt Problems & Solutions The Debt Landscape 40% of Americans live on 110% of their income Total U.S. household debt = $11.2 trillion Finances are one of the top five causes of divorce Money

Understanding Debt Problems & Solutions The Debt Landscape 40% of Americans live on 110% of their income Total U.S. household debt = $11.2 trillion Finances are one of the top five causes of divorce Money

money management managing credit and debt

money management managing credit and debt our mission The mission of The USAA Educational Foundation is to help consumers make informed decisions by providing information on financial management, safety

money management managing credit and debt our mission The mission of The USAA Educational Foundation is to help consumers make informed decisions by providing information on financial management, safety

12-Step Guide to Financial Success

12-Step Guide to Financial Success Step 1: Be accountable and responsible The first step on the path to financial success is accepting responsibility. You are in control of your financial future, and every

12-Step Guide to Financial Success Step 1: Be accountable and responsible The first step on the path to financial success is accepting responsibility. You are in control of your financial future, and every

CreditReport.LifeTips.com

CreditReport.LifeTips.com Category: About Credit Reports Subcategory: About Credit Reports Tip: About Credit Reports A credit report is a compilation of information that gives potential creditors a snapshot

CreditReport.LifeTips.com Category: About Credit Reports Subcategory: About Credit Reports Tip: About Credit Reports A credit report is a compilation of information that gives potential creditors a snapshot

4-Step Guide to Rebuilding Your Credit

4-Step Guide to Rebuilding Your Credit Bankruptcy Solutions 1 800.435.9138 StartFreshToday.com 1 Contents 3 4 5 8 12 16 Rebuilding Your Credit Step 1: Obtain Your Records Step 2: Identify Errors Step 3:

4-Step Guide to Rebuilding Your Credit Bankruptcy Solutions 1 800.435.9138 StartFreshToday.com 1 Contents 3 4 5 8 12 16 Rebuilding Your Credit Step 1: Obtain Your Records Step 2: Identify Errors Step 3:

Name Period. Finance charge Loan term Grace period Late fee Cash Advance Fee Prepayment Penalty Origination Fee Amortization Collateral Capital

Name Period GOOD DEBT, BAD DEBT: USING CREDIT WISELY ACCELERATED Say you dream of buying a $15,000 car. Even if you saved $200 a month, it would still take you seven years to save what you needed to buy

Name Period GOOD DEBT, BAD DEBT: USING CREDIT WISELY ACCELERATED Say you dream of buying a $15,000 car. Even if you saved $200 a month, it would still take you seven years to save what you needed to buy