CREDIT REPORT USER GUIDE

|

|

|

- Mercy Gallagher

- 5 years ago

- Views:

Transcription

1 Page 1 of 17 ABOUT EQUIFAX CREDIT REPORT USER GUIDE Equifax Canada Inc. Box 190 Jean Talon Station Montreal, Quebec H1S 2Z2 Equifax empowers businesses and consumers with information they can trust. A global leader in information solutions, we leverage one of the largest sources of consumer and commercial data, along with advanced analytics and proprietary technology, to create customized insights that enrich both the performance of businesses and the lives of consumers. Customers have trusted Equifax for over 100 years to deliver innovative solutions with the highest integrity and reliability. Businesses -large and small -rely on us for consumer and business credit intelligence, portfolio management, fraud detection, decisioning technology, marketing tools, and much more. We empower individual consumers to manage their personal credit information, protect their identity, and maximize their financial well -being. Headquartered in Atlanta, Georgia, Equifax Inc. employs approximately 6,900 people in 14 countries throughout North America, Latin America and Europe. Equifax is a member of Standard & Poor ' s (S&P) 500 Index. Our common stock is traded on the New York Stock Exchange under the symbol EFX. Equifax is a registered trademark of Equifax Inc., Atlanta, Georgia. All rights reserved. For more information visit

2 Page 2 of 17 CONTENTS: SAMPLE CREDIT REPORT.. 3 DEFINITIONS & DETAILS BY SECTION.. 6 FREQUENTLY ASKED QUESTIONS GLOSSARY OF TERMS..12

3 Page 3 of 17 Your Credit Report is a compilation of information about you and your credit history that has been reported to Equifax by others, mostly by those who granted you credit. Your Credit Report includes personal information such as your name, address, date of birth and Social Insurance Number. It also includes historical data such as current and previous addresses and employers, and public records such as bankruptcies, liens or judgments. Most importantly, your Credit Report contains your account and payment information. Please note that the images below are examples and do not reflect your credit score. SAMPLE CREDIT REPORT

4 Page 4 of 17

5 Page 5 of 17

6 Page 6 of 17 PERSONAL INFORMATION This section contains information about you including: Date: Date on the credit report indicates the date the report was pulled and presented to you. Former Name/Alias: This indicates other names that correspond to your credit file. This may include a maiden name or another name that you used to apply for credit. Address: Includes current and former addresses. Inaccurate information in this section could indicate a mixed file (information from two or more individuals inadvertently combined in one credit file) or possible credit fraud. The last date the address is updated is also noted in this section. Employment: Lists present place of employment. Inaccurate information could indicate a mixed file (information from two or more individuals inadvertently combined in one credit file) or possible credit fraud. Consumer Statement This is a statement that you asked the Credit Reporting agency to add to your file.

7 Page 7 of 17 Credit Information This section provides a summary of your accounts that we have on file. Account Designator indicates if the listed account is joint or individual. Undesignated means it is unknown whether the listed account is joint or individual. Indicator shows that the trade information was updated by an accounts receivable tape. Member Name indicates the name of the company who holds the listed account. Also displayed is the type of credit held with the named company. The member name is often referred to as the account owner. Member Number indicates the reporting member number of the listed creditor.

8 Page 8 of 17 Area represents the area code that precedes the listed phone number. Phone is the phone number reported by the account owner corresponding to the Member name. Ext indicates the extension, if any, associated with the listed account owner phone number. 30/60/90 of days indicates the number of times the listed account was 30/60/90+ days late in receiving payment. Months Reviewed indicates the number of times the listed account owner reported on the account. Last Activity indicates the last time the account was reported as used. Reported indicates the most recent date that the account was reported to Equifax Canada. Opened indicates the date the listed account was opened with the credit grantor. High Credit indicates the high credit on the account or the credit limit. Terms indicates the required payment amount on the listed account. Balance indicates the outstanding amount owed on the listed account at the time it was last reported. Past Due indicates the payment amount past due as of the date of reporting on the listed account. Account Type indicates whether the listed account is revolving, installment, mortgage or line of credit. Rating indicates if the account has been paid per the agreed upon terms of if there are payments in arrears. Account Number is the account number reported to the credit bureau. For your protection not all the information will be displayed. Previous high rate indicates the 3 most recent ratings of the listed account. Previous date indicates the dates of the corresponding rating. Narrative indicates additional information on the listed account.

9 CREDIT HISTORY AND BANKING INFORMATION This section indicates Banking information and whether there are any NSF cheques on file. Page 9 of 17 Chequing/Savings Account(s) indicates any bank account on file and their characteristics. Non Sufficient Funds indicates that a cheque you issued was not honored due to insufficient funds. Public Records and Other information This section indicates the number of public records and includes bankruptcies, judgments, voluntary repayment programs, and secured loans. Most public record items are listed for seven years from the date filed. Bankruptcy indicates whether or not a declaration of bankruptcy is on your credit file. Legal item(s) indicates item(s) and outstanding balances, if any, on credit that resulted in you being taken to court or other legal proceedings. Garnishment of wage indicates whether your earnings have been secured to pay off debt obligations. Secured Loan(s) indicate loan(s) for, and their details, that are secured by an asset.

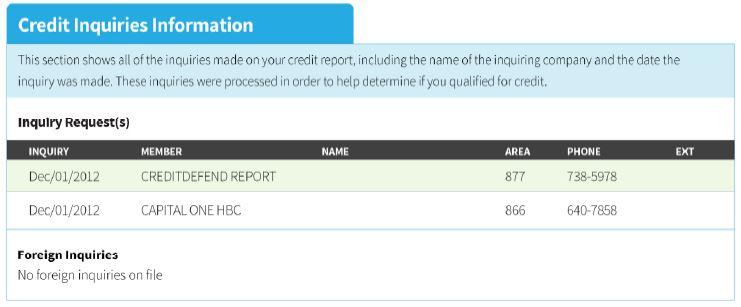

10 Page 10 of 17 COLLECTIONS Collection items indicate accounts sent to a collection agency that you have not paid. This section includes initial amount owing, the outstanding balance, the creditor s name and the date the collections item was reported to Equifax. This section will indicate the creditor s name (i.e. who do you owe this money to). The balance and the amount initially borrowed are also indicated. The balance represents the outstanding debt currently outstanding. Payment of this balance will result in your debt being paid in full. CREDIT INQUIRIES INFORMATION This section will display inquiries made on your credit report. The name of the inquiring company and the date of the inquiry will be displayed for you. These inquiries were processed in order to help determine if you qualified for credit.

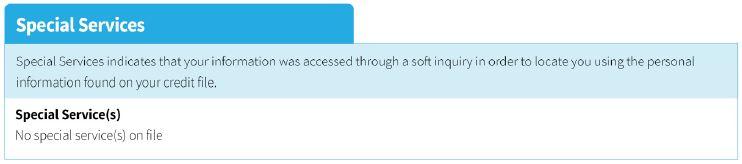

11 Page 11 of 17 SPECIAL SERVICES Special Services indicates that your information was accessed through a soft inquiry in order to locate you using the personal information found on your credit file. FOREIGN INQUIRIES This section will display inquiries by creditors outside of Canada. The name of the inquiring company and the date of the inquiry will be displayed for you. FREQUENTLY ASKED QUESTIONS Why is my Credit Report important? Your Credit Report is a compilation of information about you and your credit history that has been reported to Equifax by others, mostly by those who granted you credit. When you apply for a loan for a home, a car or other major purchase, some lenders will approve your loan and determine the interest rate based upon several factors including your Credit Report. Your Credit Report reflects how well you have been in maintaining credit in the past. How do I change information on my Credit Report? Please completely fill out the form found on the website and follow the steps from there. If this link does not work, go to and scroll to the bottom. Under the OTHER CREDIT SERVICES section, click on the link for correcting inaccuracies and follow the simple steps.

12 Page 12 of 17 GLOSSARY OF TERMS ACCOUNT NUMBER -a reference number assigned to an individual s account by either a creditor or collection agency. ACCOUNT HISTORY -shows payment history on a month-to-month basis for the last 24 months. Abbreviations, which are defined under DEFINITIONS: Account History located at the bottom of each page of your profile, are used to describe your payment status each month including the most recent month reported. ACCOUNT STATUS -shows the current status of your account and may indicate delinquencies that were reported in the past seven years. ACTIVE ACCOUNT -An account for which activity has been reported to a Credit Reporting Agency in the last 90 days. ALIAS -A name reported in your credit file that differs from your primary or given name. This commonly occurs if you've applied for credit or loans under different variations of your name Robert P. Smith and Bob Smith, for example. ALIAS is sometimes referred to as Also Known As (AKA). AMORTIZATION -The reduction of a mortgage loan by regular payments. AMOUNT DUE -Generally, the minimum monthly payment you must make, not the total amount you owe. ANNUAL FEE -The yearly fee charged by a lender to maintain an account. ANNUAL PERCENTAGE RATE (APR) -The cost of credit at a yearly rate. Knowing the APR allows you to effectively compare loans, even when they are structured differently. ASSET -Any holding that has a monetary value or use. Houses, real estate, cars, jewelry, and stocks & bonds are considered assets. AUTHORIZED USER -A person allowed to charge goods and services on a credit card by the primary user of that card. Authorized users --unlike users of a joint account --are not legally responsible for payment. AVAILABLE CREDIT -On a credit account, the credit limit minus the current balance. To many creditors, your total available credit on all your accounts is an important factor. BALANCE AMOUNT -amount due to the creditor at the time account information was last reported.

13 Page 13 of 17 BALANCE -The outstanding amount owed to a creditor on a particular account. BALANCE DATE -the last date the file was updated by the Credit Reporting agency with creditor information. CLOSED ACCOUNT -An account that has been closed by you or your creditor. Such accounts remain on your Credit Report for seven years from the date of last activity. COLLECTION AGENCY -A firm assigned by a creditor to collect overdue amounts. Some creditors have internal collection departments. Like creditors, collection agencies report account information to consumer reporting agencies. CONSOLIDATION LOAN -A loan obtained in order to combine multiple debts into one, typically at a lower interest rate. CONSUMER -An individual who purchases products and services. CONSUMER DEBT -Debt incurred for items that aren't considered tangible investments such as credit card debt, car loans, and personal loans made by family members. CONSUMER STATEMENT -Under the Fair Credit Reporting Act, you have the right to add a consumer statement to your credit file to explain disputed information about your accounts. CREDIT CARD -A card used to make purchases or take out cash loans that require the user to pay some or the entire outstanding amount each month. Credit cards are differentiated mainly by their terms. CREDIT CARD ISSUER -A bank or other institution that extends consumers credit through a credit card. CREDIT FILE -a record of an individual s credit payment history as reported at a Credit Reporting agency. The credit file is a collection of an individual s credit history, indentifying information, and other records maintained by a Credit Reporting agency. Credit File is sometimes used interchangeably with Credit Report, but technically a credit file is the source from which a Credit Report is generated. CREDIT HISTORY -A record of how a consumer has paid credit accounts in the past. It is used as a guide to determine whether or not the consumer is likely to pay future accounts on time. CREDIT LIMIT/CREDIT LINE -The amount of credit issued by a lender. CREDIT PROFILE -a compilation of credit information presented in an easy-to-read format.

14 Page 14 of 17 CREDIT REPORT -A report that a prospective lender or employer obtains from a consumer reporting agency that displays the manner in which a consumer has met his or her past credit obligations. It is used to help determine creditworthiness of the potential borrower or to confirm identity of an individual. CREDIT REPORTING AGENCY -also known as a credit bureau. An organization that compiles information from various financial institutions and courts to create an individual s credit file. CREDIT SCORE -a score based on variables in your credit file that is indicative of your credit worthiness. CREDITOR -a person or business from whom you borrow or to whom you owe money. CURRENT RATINGS - shows total of all account types that are currently delinquent 30, 60, or 90 days. DATE ON FILE -date your credit file was started. DATE OPEN - date account was opened. DATE PAID - date account was satisfied. DATE OF STATUS - date account status was last updated. DELINQUENCY - a debt on which payment is overdue. DISCHARGE - To release a debtor from responsibility for a debt, often as a result of bankruptcy. DISMISSED BANKRUPTCY -An instance in which a judge has ruled against a consumer's petition for bankruptcy, sometimes at the consumer's request. Such cases are recorded in the public records section of the consumer's Credit Report, and the debts covered in the bankruptcy remain outstanding. DISPUTE -to question the accuracy of information in a Credit Report. FILING DATE -date item was filed with the courts. FORECLOSURE: The legal process by which a creditor may sell mortgaged property to recover a defaulted mortgage. FRAUD ALERT -If you suspect that you're the victim of identity theft or credit fraud, you may contact the Credit Reporting agencies and place a fraud alert on your credit file. Such an alert will prevent new credit accounts from being opened without your express permission.

15 HARD INQUIRY -An indication on your credit file that a lender has obtained a copy of the report in order to evaluate your loan or credit application. An excess of hard inquiries within a six-month period may lower your credit rating. HIGH/LIMIT -the highest balance since the account was opened or the limit on the account. Page 15 of 17 HISTORY RATINGS -shows the total of all account types that were delinquent 30, 60, or 90 days in the past seven years. INQUIRY -a request for a copy of your credit file, usually from a bank(s), landlord(s), potential employer(s), mortgage broker(s), or the institution(s) from whom you ve applied for credit. Too many inquiries may be considered a negative factor as it suggests that you are becoming overextended. Inquiries made by companies for marketing purposes have no impact on your credit rating and are not included here. See also hard inquiry and soft inquiry. INQUIRY DATE -date your credit file was requested. INSTALLMENT ACCOUNT -an account with a fixed payment for the term of the loan. INSTALLMENT LOAN -a credit account in which the debt is divided into amounts to be paid successively at specified intervals set by the terms of the loan. INVESTIGATION -The process a Credit Reporting company undertakes in order to verify Credit Report information disputed by a consumer. For more information, see correcting inaccuracies on your Credit Report. JOINT ACCOUNT -A credit or loan account held by two or more people. All account holders assume legal responsibility for the repayment of the account. JOINT CREDIT REPORT -A combined report created by merging the credit files of joint applicants and used by creditors to assess a joint application for credit, usually involving a mortgage. Note that the credit files remain separate. JUDGMENT -A determination by a court of law that, in the case of credit, may require a person to fulfill an obligation to pay a debt, for example. When a judgment has been satisfied (i.e. the debt has been paid or settled), the consumer has fulfilled its requirements and is no longer liable. Information about judgments is recorded in the public records section of a Credit Report. LENDER -A company that lends money to consumers or enables them to make purchases on credit. Sometimes used interchangeably with creditor. LIABILITY -In the context of credit, legal responsibility for the repayment of a debt. LIEN -A legal claim upon real or personal property as security for or payment of a debt.

16 Page 16 of 17 LOAN TYPE -type of loan for which an inquiry was made. MINIMUM PAYMENT -The smallest payment you can make on a revolving credit account to maintain your account status as being paid as agreed. MONTHLY PAYMENT - average monthly payment reported to the Credit Reporting agencymay be estimated by the agency if not reported by the creditor. (This may be indicated by an asterisk * ). MORTGAGE -A loan designed to facilitate the purchase of a home, in which the home itself serves as security for the loan. If the borrower doesn't make the required payments, the lender may through a legal process known as foreclosure, sell the home in order to recover the amount owed on the mortgage. Mortgage can also refer to the legal document detailing the borrower's responsibilities, including the payment schedule and terms. NET 30 ACCOUNT -an account where the balance must be paid in full at the end of 30 days. OPEN ACCOUNT -an account that is currently in use. ORIGINAL CREDITOR -shows the original creditor that turned the account over to the collection agency. OWNERSHIP -designation by a lender of an individual responsible for payment of an account. PAST DUE AMOUNT -amount currently past due. PRIMARY USER -The person under whose name a credit card account is listed. A primary user can authorize other people to use the account, but the primary user is ultimately responsible for repaying all charges. PRIOR DELINQUENCIES -date account was last reported delinquent. PUBLIC RECORD -Information obtained from court records about such things as tax liens, bankruptcy filings and judgments against you in civil actions. REAL ESTATE ACCOUNT -a fixed payment account involving ownership of property (such as mortgage payments). REVOLVING ACCOUNT -an account where a balance can be carried over from month to month. SOCIAL INSURANCE NUMBER (SIN) -The unique nine-digit number assigned to every legal resident of the Canada. Because no two people are assigned the same number, the SIN is usually the main identifying factor in a person's records, including Credit Reports.

17 Page 17 of 17 SOFT INQUIRY -An instance in which your Credit Report is accessed without affecting your credit rating. Soft inquiries include your own requests for your Credit Report, promotional inquiries by credit card companies, and checkup inquiries by your existing creditors. Inquiries associated with your credit monitoring service are soft inquiries. TAX LIEN -a charge upon real estate or personal property for the satisfaction of a debt or duty ordinarily arising by operation of law. TERM -The amount of time in which a loan must be repaid in full. TRADELINE NAME -account name. TRADES OPENED -new account(s) opened.

CREDIT SCORE USER GUIDE

Page 1 of 11 ABOUT EQUIFAX Equifax empowers businesses and consumers with information they can trust. A global leader in information solutions, we leverage one of the largest sources of consumer and commercial

Page 1 of 11 ABOUT EQUIFAX Equifax empowers businesses and consumers with information they can trust. A global leader in information solutions, we leverage one of the largest sources of consumer and commercial

Bottom Line. What Do All of These Have in Common? 4/13/2011

4/13/2011 Department of Housing and Consumer Economics What Do All of These Have in Common? 0 Landlords 0 Utility companies 0 Employers (jobs requiring finances or security) 0 card companies 0 Lenders

4/13/2011 Department of Housing and Consumer Economics What Do All of These Have in Common? 0 Landlords 0 Utility companies 0 Employers (jobs requiring finances or security) 0 card companies 0 Lenders

TIP: Make sure this information is correct. A wrong address or phone number could be a mistake or a sign of identity theft.

Reading a Sample Credit Report This sample report shows what kind of information might appear on your own credit report, also called a consumer disclosure statement, from the 3 major Credit Reporting Agencies

Reading a Sample Credit Report This sample report shows what kind of information might appear on your own credit report, also called a consumer disclosure statement, from the 3 major Credit Reporting Agencies

GREENPATH FINANCIAL WELLNESS SERIES

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Empowering people to lead financially healthy lives. TABLE OF CONTENTS Understanding credit reports...2 What s in a credit

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Empowering people to lead financially healthy lives. TABLE OF CONTENTS Understanding credit reports...2 What s in a credit

c» BALANCE C:» Financially Empowering You The World of Credit Reports Podcast [Music plays] Nikki:

![c» BALANCE C:» Financially Empowering You The World of Credit Reports Podcast [Music plays] Nikki:](/thumbs/76/73531259.jpg "c» BALANCE C:» Financially Empowering You The World of Credit Reports Podcast [Music plays] Nikki:") The World of Credit Reports Podcast [Music plays] Nikki: You re listening to world of credit. Hi, I m Nikki, your host for today s podcast. Credit reports and credit scores influence our lives in many

The World of Credit Reports Podcast [Music plays] Nikki: You re listening to world of credit. Hi, I m Nikki, your host for today s podcast. Credit reports and credit scores influence our lives in many

TABLE OF CONTENTS. Healthier Black Elders Center

TABLE OF CONTENTS What is credit............................................1 The five C s of credit...................................... 2 Types of credit...........................................3

TABLE OF CONTENTS What is credit............................................1 The five C s of credit...................................... 2 Types of credit...........................................3

Module 7 - Credit Reporting HANDOUT 7-1

ParticipantHandbook 1 Module 7 - Credit Reporting HANDOUT 7-1 Credit bureaus Credit bureaus are agencies that collect information about how we use credit. They produce personal credit reports. Credit bureaus

ParticipantHandbook 1 Module 7 - Credit Reporting HANDOUT 7-1 Credit bureaus Credit bureaus are agencies that collect information about how we use credit. They produce personal credit reports. Credit bureaus

Advantages & Disadvantages to Using Credit

Advantages & Disadvantages to Using Credit Advantages to Using Credit Able to buy needed items now Don t have to carry cash Creates a record of purchases More convenient than writing cheques Consolidates

Advantages & Disadvantages to Using Credit Advantages to Using Credit Able to buy needed items now Don t have to carry cash Creates a record of purchases More convenient than writing cheques Consolidates

Reviewing C YouR CRedit RepoRt

ChapteR 2 Reviewing C YouR CRedit RepoRt What do your creditors have to say about the way you handle money? Having a good credit score can help you turn your home-buying dream into a reality. There s much

ChapteR 2 Reviewing C YouR CRedit RepoRt What do your creditors have to say about the way you handle money? Having a good credit score can help you turn your home-buying dream into a reality. There s much

Credit Profile Report

Credit Profile Report Unsurpassed data precision and file coverage The best decisions begin with the best information. Experian s Credit Profile Report offers unparalleled accuracy and superior data quality

Credit Profile Report Unsurpassed data precision and file coverage The best decisions begin with the best information. Experian s Credit Profile Report offers unparalleled accuracy and superior data quality

WHOLESALE LENDING AT-A-GLANCE CREDIT

DESCRIPTION STANDARD A borrower s creditworthiness is based on past and present credit history. The credit history must demonstrate the borrower s ability and willingness to handle financial obligations.

DESCRIPTION STANDARD A borrower s creditworthiness is based on past and present credit history. The credit history must demonstrate the borrower s ability and willingness to handle financial obligations.

Federal Reserve Bank of Philadelphia

Federal Reserve Bank of Philadelphia 1 When you apply for credit, whether it s a credit card, car loan, or a mortgage, lenders want to know whether you are likely to repay your loan and make the payments

Federal Reserve Bank of Philadelphia 1 When you apply for credit, whether it s a credit card, car loan, or a mortgage, lenders want to know whether you are likely to repay your loan and make the payments

To collect on a delinquent account, you need to locate the debtor. That s. why the Collection Report from Experian provides the credit and locator

Collection Report The way to maximize your recovery dollars To collect on a delinquent account, you need to locate the debtor. That s why the Collection Report from Experian provides the credit and locator

Collection Report The way to maximize your recovery dollars To collect on a delinquent account, you need to locate the debtor. That s why the Collection Report from Experian provides the credit and locator

Laura Mackie Mortgages. A Guide to Understanding and Rebuilding Your Credit Score

Laura Mackie Mortgages Your Credit Report A Guide to Understanding and Rebuilding Your Credit Score Introduction This guide is intended to help you improve your credit score and provide you with information

Laura Mackie Mortgages Your Credit Report A Guide to Understanding and Rebuilding Your Credit Score Introduction This guide is intended to help you improve your credit score and provide you with information

Understanding Credit. What it is, why it s important, and how you can maintain it. Brought to you by Sallie Mae and FICO

Understanding Credit What it is, why it s important, and how you can maintain it Brought to you by Sallie Mae and FICO Introduction A student loan may be your first major credit experience. This is a good

Understanding Credit What it is, why it s important, and how you can maintain it Brought to you by Sallie Mae and FICO Introduction A student loan may be your first major credit experience. This is a good

13.1. Reading a Credit Report EXERCISE. THEME 4 Lesson 13: Applying for Credit NAME: CLASS PERIOD:

13.1 NAME: CLASS PERIOD: Reading a Credit Report Your ability to qualify for a loan depends on a credit report. A credit report is a record of an individual s personal credit history. It is probably a

13.1 NAME: CLASS PERIOD: Reading a Credit Report Your ability to qualify for a loan depends on a credit report. A credit report is a record of an individual s personal credit history. It is probably a

UNDERSTAND & PREDICT CONSUMER BEHAVIOUR WITH TRENDED DATA SOLUTIONS

UNDERSTAND & PREDICT CONSUMER BEHAVIOUR WITH TRENDED DATA SOLUTIONS PREDICT RISK AND REVENUE POTENTIAL WITH PRECISE, TARGETED INSIGHTS The best predictor of future behaviour is often past behaviour. That

UNDERSTAND & PREDICT CONSUMER BEHAVIOUR WITH TRENDED DATA SOLUTIONS PREDICT RISK AND REVENUE POTENTIAL WITH PRECISE, TARGETED INSIGHTS The best predictor of future behaviour is often past behaviour. That

Glossary of Terms. Accounts Receivable: Additional Payment Experiences: Aged Trades: Alert s: Background: Balance: Bank Accounts:

Glossary of Terms Accounts Receivable: Is one of a series of accounting transactions dealing with the billing of customers which owe money to a person, company or organization for goods and services that

Glossary of Terms Accounts Receivable: Is one of a series of accounting transactions dealing with the billing of customers which owe money to a person, company or organization for goods and services that

Justine PETERSEN Building Assets. Changing Lives. Credit Report Basics and Definitions Justine PETERSEN Credit Building Training

Justine PETERSEN Building Assets. Changing Lives Credit Report Basics and Definitions Justine PETERSEN Credit Building Training Included Topics Who reports to the credit bureaus Statute of Limitations

Justine PETERSEN Building Assets. Changing Lives Credit Report Basics and Definitions Justine PETERSEN Credit Building Training Included Topics Who reports to the credit bureaus Statute of Limitations

2/10/2015 CREDIT FOR SUCCESS TODAY S NEW RISK FACTORS MOBILE BANKING. The new Consumer Financial Protection Act, the ATR Rule (Ability to Repay Rule)

") CREDIT FOR SUCCESS TODAY S NEW RISK FACTORS Written and Presented by Serge Bevil, Credit Specialist VantagePoint Credit Corp. MOBILE BANKING We have become a social media society that wants information,

CREDIT FOR SUCCESS TODAY S NEW RISK FACTORS Written and Presented by Serge Bevil, Credit Specialist VantagePoint Credit Corp. MOBILE BANKING We have become a social media society that wants information,

Understanding Your FICO Score. Understanding FICO Scores

Understanding Your FICO Score Understanding FICO Scores 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Reports

Understanding Your FICO Score Understanding FICO Scores 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Reports

Part 2 Understanding Credit. And Your Credit Report

Part 2 Understanding Credit And Your Credit Report What Is Credit? (Developed by Z. Omarali, Toronto District School Board) 50% of Canadians do not know what factors contribute to a credit rating. The

Part 2 Understanding Credit And Your Credit Report What Is Credit? (Developed by Z. Omarali, Toronto District School Board) 50% of Canadians do not know what factors contribute to a credit rating. The

Now, let me turn the program over to Jacqueline Cooke, Women s Bureau Regional Administrator in Boston, to introduce our first speaker. Jackie?

Wi$e Up Teleconference Call February 28, 2006 Becoming Credit Smart Speaker 1 Amy Perry Jane Walstedt: Now, let me turn the program over to Jacqueline Cooke, Women s Bureau Regional Administrator in Boston,

Wi$e Up Teleconference Call February 28, 2006 Becoming Credit Smart Speaker 1 Amy Perry Jane Walstedt: Now, let me turn the program over to Jacqueline Cooke, Women s Bureau Regional Administrator in Boston,

Rescore Guidelines. Please read. If proper documentation is not received it will delay the processing time and may result in unnecessary charges.

Contact: Sydni Woolley Phone: (800)275-7398 ext 123 Email: swoolley@nacmint.com RESCORE PACKET Page 1: Rescore Guidelines and Required Documents Page 2: Rescore Pricing Page 3: Rescore order form Page

Contact: Sydni Woolley Phone: (800)275-7398 ext 123 Email: swoolley@nacmint.com RESCORE PACKET Page 1: Rescore Guidelines and Required Documents Page 2: Rescore Pricing Page 3: Rescore order form Page

Chapter 26 11/9/2017 1

Chapter 26 11/9/2017 1 Average college students has 3 credit cards Also between $1500 & $2000 in debt Things to know if you re getting a credit card Who accepts it? What amount can you charge to meet your

Chapter 26 11/9/2017 1 Average college students has 3 credit cards Also between $1500 & $2000 in debt Things to know if you re getting a credit card Who accepts it? What amount can you charge to meet your

Twelve common questions. About consumer credit and direct marketing

Twelve common questions About consumer credit and direct marketing Twelve common questions Most of us don t think about credit until a specific event sparks our interest. Maybe we want to buy a car or

Twelve common questions About consumer credit and direct marketing Twelve common questions Most of us don t think about credit until a specific event sparks our interest. Maybe we want to buy a car or

Project Pro$per. Credit Reports and Credit Scores

Project Pro$per Presents Credit Reports and Credit Scores Participant Guide www.projectprosper.org www.facebook.com/projectprosper Based on Wells Fargo s Hands on Banking The Hands on Banking program is

Project Pro$per Presents Credit Reports and Credit Scores Participant Guide www.projectprosper.org www.facebook.com/projectprosper Based on Wells Fargo s Hands on Banking The Hands on Banking program is

12 common questions. About consumer credit and direct marketing

12 common questions About consumer credit and direct marketing Most of us don t think about credit until a specific event sparks our interest. Maybe we want to buy a car or home. Or perhaps we receive

12 common questions About consumer credit and direct marketing Most of us don t think about credit until a specific event sparks our interest. Maybe we want to buy a car or home. Or perhaps we receive

Consumer Credit Report User Guide

Consumer Credit Report User Guide sample report (Please see format specific user guides for system-to-system outputs). 1 CONSUMER CREDIT FILE 7 2 3 4 5 6 [1] 1-800-465-7166 [2] /DD [3] File Requested by:

Consumer Credit Report User Guide sample report (Please see format specific user guides for system-to-system outputs). 1 CONSUMER CREDIT FILE 7 2 3 4 5 6 [1] 1-800-465-7166 [2] /DD [3] File Requested by:

UNDERSTANDING YOUR CREDIT REPORT AND CREDIT SCORE CREDIT AND LOANS

UNDERSTANDING YOUR CREDIT REPORT AND CREDIT SCORE CREDIT AND LOANS June 2015 Cat. No.: FC5-8/25-2015E-PDF ISBN: 978-0-660-02844-6 Her Majesty the Queen in Right of Canada (Financial Consumer Agency of

UNDERSTANDING YOUR CREDIT REPORT AND CREDIT SCORE CREDIT AND LOANS June 2015 Cat. No.: FC5-8/25-2015E-PDF ISBN: 978-0-660-02844-6 Her Majesty the Queen in Right of Canada (Financial Consumer Agency of

Written by Credit Doctor, author of Credit-Aid Software the Award-winning Credit Repair Software Kit. Table of Contents (Click to view)

") Boost your FICO Score in 7 Easy Steps! Tricks of the trade the Pro s use to Boost your Credit Score FAST! These are the Credit Repair Secrets the banks don t want you to know Written by Credit Doctor,

Boost your FICO Score in 7 Easy Steps! Tricks of the trade the Pro s use to Boost your Credit Score FAST! These are the Credit Repair Secrets the banks don t want you to know Written by Credit Doctor,

65 E. Wacker Place Suite 1405, Chicago, IL Ph: Fax: Credit 101

65 E. Wacker Place Suite 1405, Chicago, IL 60601 Ph: 888.895.5145 Fax: 888.895.5146 Credit 101 The subject of credit and what is included on a consumer s credit report can be a source of much debate, confusion

65 E. Wacker Place Suite 1405, Chicago, IL 60601 Ph: 888.895.5145 Fax: 888.895.5146 Credit 101 The subject of credit and what is included on a consumer s credit report can be a source of much debate, confusion

Consumer FAQs Comprehensive Credit Reporting. January 2016

Consumer FAQs Comprehensive Credit Reporting January 2016 CONTENTS 03 Credit Report FAQs 03 Why is there new information in my report? 03 How can I tell which lenders are providing CCR information to Equifax

Consumer FAQs Comprehensive Credit Reporting January 2016 CONTENTS 03 Credit Report FAQs 03 Why is there new information in my report? 03 How can I tell which lenders are providing CCR information to Equifax

Table of Contents. Money Smart for Small Business Page 2 of 19

Table of Contents Welcome... 4 What Do You Know? Credit Reporting for a Small Business... 5 Pre-Test... 6 Credit Reporting... 7 Credit Report Impact... 7 Business Credit Reports... 7 Discussion Point #1:

Table of Contents Welcome... 4 What Do You Know? Credit Reporting for a Small Business... 5 Pre-Test... 6 Credit Reporting... 7 Credit Report Impact... 7 Business Credit Reports... 7 Discussion Point #1:

5/16/2006 1 of 18 Report for CHRISTINE BAKER on April 30, 2006 Click here to return. 742 CHRISTINE BAKER April 30, 2006 Credit record source: Equifax Your FICO score of 742 summarizes the information on

5/16/2006 1 of 18 Report for CHRISTINE BAKER on April 30, 2006 Click here to return. 742 CHRISTINE BAKER April 30, 2006 Credit record source: Equifax Your FICO score of 742 summarizes the information on

Your Credit. Objectives. An Introduction to Personal Credit. By the end of this presentation you will have a understanding of: 1/19/2016.

Your Credit An Introduction to Personal Credit Objectives By the end of this presentation you will have a understanding of: Credit Score Where can I find it? What is it? How do I get it? Advantages of

Your Credit An Introduction to Personal Credit Objectives By the end of this presentation you will have a understanding of: Credit Score Where can I find it? What is it? How do I get it? Advantages of

Equifax Credit Report Personal Information Since xx/xx/xx FAD xx/xx/xx SSN Information Employment Beacon

PO Box 1386, Columbia, SC 29202 www.icscredit.com This document is provided only to assist new users in reading an Equifax Credit Report. It is not intended to be authoritative, and may not reflect the

PO Box 1386, Columbia, SC 29202 www.icscredit.com This document is provided only to assist new users in reading an Equifax Credit Report. It is not intended to be authoritative, and may not reflect the

Business Identity Report PlusTM

COMMERCIAL INFORMATION SOLUTIONS >Training Guide Business Identity Report PlusTM 1 COMMERCIAL INFORMATION SOLUTIONS March 1, 1 1:7 p.m. EDT Customer Ref: SW1 EFX ID: Company Profile: Telephone: Tax ID/SSN:

COMMERCIAL INFORMATION SOLUTIONS >Training Guide Business Identity Report PlusTM 1 COMMERCIAL INFORMATION SOLUTIONS March 1, 1 1:7 p.m. EDT Customer Ref: SW1 EFX ID: Company Profile: Telephone: Tax ID/SSN:

UNDERSTANDING CREDIT. KASFAA Conference Manhattan, KS April 21, Robb Cummings Director of Business Development

UNDERSTANDING CREDIT KASFAA Conference Manhattan, KS April 21, 2016 Robb Cummings Director of Business Development FICO Score 2 A FICO Score is a three-digit number calculated from the credit information

UNDERSTANDING CREDIT KASFAA Conference Manhattan, KS April 21, 2016 Robb Cummings Director of Business Development FICO Score 2 A FICO Score is a three-digit number calculated from the credit information

EasterSeal/Freddie Mac CreditSmart Training Credit Questions & Answers

Bankruptcy What Is Bankruptcy? Bankruptcy is a legal proceeding in which a person who cannot pay his or her bills can get a fresh financial start. The right to file for bankruptcy is provided by federal

Bankruptcy What Is Bankruptcy? Bankruptcy is a legal proceeding in which a person who cannot pay his or her bills can get a fresh financial start. The right to file for bankruptcy is provided by federal

Identifying High Spend Consumers with Equifax Dimensions

Identifying High Spend Consumers with Equifax Dimensions April 2014 Table of Contents 1 Executive summary 2 Know more about consumers by understanding their past behavior 3 Optimize business performance

Identifying High Spend Consumers with Equifax Dimensions April 2014 Table of Contents 1 Executive summary 2 Know more about consumers by understanding their past behavior 3 Optimize business performance

A Glossary of Loan Terms

A Glossary of Loan Terms Link to Online Glossary of Loan Terms: http://www.gdrc.org/icm/loan-glossary.html Assets Anything of value. Any interest in real or personal property which can be appropriated

A Glossary of Loan Terms Link to Online Glossary of Loan Terms: http://www.gdrc.org/icm/loan-glossary.html Assets Anything of value. Any interest in real or personal property which can be appropriated

Chapter 6 - Credit. Section 6.1

Chapter 6 - Credit Section 6.1 Credit is a medium of exchange which allows individuals to buy goods or services now and pay for them later The creditor supplies money, goods, or services in a credit agreement

Chapter 6 - Credit Section 6.1 Credit is a medium of exchange which allows individuals to buy goods or services now and pay for them later The creditor supplies money, goods, or services in a credit agreement

Understanding Credit. Lisa Mitchell, Sallie Mae April 6, Champions of Financial Aid ILASFAA Conference

Understanding Credit Lisa Mitchell, Sallie Mae April 6, 2017 Credit Management Agenda Understanding Your Credit Report Summary: Financial Health Tips Credit Management Credit Basics Credit health plays

Understanding Credit Lisa Mitchell, Sallie Mae April 6, 2017 Credit Management Agenda Understanding Your Credit Report Summary: Financial Health Tips Credit Management Credit Basics Credit health plays

ALTLOAN CREDIT GUIDELINES

ALTLOAN CREDIT GUIDELINES BRIDGE AND FIX & FLIP LOANS PRIMARY RESIDENCE & SECOND HOME TERM LOANS INVESTOR TERM LOANS BRIDGE AND FIX & FLIP Use the lower of two credit scores or middle of three for each

ALTLOAN CREDIT GUIDELINES BRIDGE AND FIX & FLIP LOANS PRIMARY RESIDENCE & SECOND HOME TERM LOANS INVESTOR TERM LOANS BRIDGE AND FIX & FLIP Use the lower of two credit scores or middle of three for each

HOW TO USE CREDIT. Latino Community Credit Union & the Latino Community Development Center.

HOW TO USE CREDIT Latino Community Credit Union & the Latino Community Development Center www.latinoccu.org Copyright 2016 Latino Community Credit Union Made possible by a generous contribution from the

HOW TO USE CREDIT Latino Community Credit Union & the Latino Community Development Center www.latinoccu.org Copyright 2016 Latino Community Credit Union Made possible by a generous contribution from the

Understanding. What you need to know about the most widely used credit scores

Understanding What you need to know about the most widely used credit scores 300 850 The score lenders use. FICO Scores are the most widely used credit scores according to a recent CEB TowerGroup analyst

Understanding What you need to know about the most widely used credit scores 300 850 The score lenders use. FICO Scores are the most widely used credit scores according to a recent CEB TowerGroup analyst

Money Management Curriculum

Money Management Module 4: Credit Reports & Credit Scores Money Management Curriculum Module 4: Credit Reports & Credit Scores Project Team: Ruby Ward, Professor, Utah State University Trent Teegerstrom,

Money Management Module 4: Credit Reports & Credit Scores Money Management Curriculum Module 4: Credit Reports & Credit Scores Project Team: Ruby Ward, Professor, Utah State University Trent Teegerstrom,

Attract and retain more high-quality customers while reducing your risks.

HOW TO ASSESS THE CREDIT RISK OF NEW IMMIGRANTS Attract and retain more high-quality customers while reducing your risks. EXECUTIVE SUMMARY With approximately 250, new immigrants arriving in Canada every

HOW TO ASSESS THE CREDIT RISK OF NEW IMMIGRANTS Attract and retain more high-quality customers while reducing your risks. EXECUTIVE SUMMARY With approximately 250, new immigrants arriving in Canada every

DEFINITION OF COMMON TERMS

DEFINITION OF COMMON TERMS Actual Cash Value: An amount equal to the replacement value of damaged property minus depreciation. Adjustable-Rate Mortgage (ARM): Also known as a variable-rate loan, an ARM

DEFINITION OF COMMON TERMS Actual Cash Value: An amount equal to the replacement value of damaged property minus depreciation. Adjustable-Rate Mortgage (ARM): Also known as a variable-rate loan, an ARM

COMMERCIAL INFORMATION SOLUTIONS. >Training Guide. Power PackTM. for Telco and Utility

COMMERCIAL INFORMATION SOLUTIONS >Training Guide Power PackTM for Telco and Utility COMMERCIAL INFORMATION SOLUTIONS September 3, 200 2:27 p.m. EDT 2 Customer Ref: SW224 EFX ID: Company Profile: Telephone:

COMMERCIAL INFORMATION SOLUTIONS >Training Guide Power PackTM for Telco and Utility COMMERCIAL INFORMATION SOLUTIONS September 3, 200 2:27 p.m. EDT 2 Customer Ref: SW224 EFX ID: Company Profile: Telephone:

Credit Reports 101. Bill Bufkins, November 3, 2011

Credit Reports 101 Bill Bufkins, November 3, 2011 What is a credit report? A credit report is a record of your past borrowing and repayment activity. The information in your credit report helps determine

Credit Reports 101 Bill Bufkins, November 3, 2011 What is a credit report? A credit report is a record of your past borrowing and repayment activity. The information in your credit report helps determine

PRACTICAL MONEY GUIDES. Credit History. Your credit history and how it affects your future.

PRACTICAL MONEY GUIDES Credit History Your credit history and how it affects your future. Learn what a credit history is and how to make the most of yours. What Is a Credit History? To predict your financial

PRACTICAL MONEY GUIDES Credit History Your credit history and how it affects your future. Learn what a credit history is and how to make the most of yours. What Is a Credit History? To predict your financial

An Overview of Credit Report/Credit Score Models and a Proposal for Vietnam

VNU Journal of Science: Policy and Management Studies, Vol. 33, No. 2 (2017) 36-45 An Overview of Credit Report/Credit Score Models and a Proposal for Vietnam Le Duc Thinh * VNU International School, Building

VNU Journal of Science: Policy and Management Studies, Vol. 33, No. 2 (2017) 36-45 An Overview of Credit Report/Credit Score Models and a Proposal for Vietnam Le Duc Thinh * VNU International School, Building

TransUnion Credit Report. Training Guide

TransUnion Credit Report Training Guide Sample TransUnion Credit Report 1 1A This sample report is intended for education purposes. 2 2A 2B 2C The actual Credit Report you receive will be customized to

TransUnion Credit Report Training Guide Sample TransUnion Credit Report 1 1A This sample report is intended for education purposes. 2 2A 2B 2C The actual Credit Report you receive will be customized to

Fixed Sum Loan Agreement Regulated by the Consumer Credit Act 1974

Fixed Sum Loan Agreement Regulated by the Consumer Credit Act 1974 This is your Loan Agreement, which we enter into with you. It sets out the details of your loan and should be read with the Terms and

Fixed Sum Loan Agreement Regulated by the Consumer Credit Act 1974 This is your Loan Agreement, which we enter into with you. It sets out the details of your loan and should be read with the Terms and

Business Owner Profile

Business Owner Profile Make sound credit decisions about small business owners Extending credit to small businesses can be risky. Don t take chances. Use Experian s Business Owner Profile and extend credit

Business Owner Profile Make sound credit decisions about small business owners Extending credit to small businesses can be risky. Don t take chances. Use Experian s Business Owner Profile and extend credit

FTC Facts. For Consumers Federal Trade Commission. Credit Scoring Ever wonder how a creditor decides

FTC Facts For Consumers Federal Trade Commission For The Consumer May 2006 Credit Scoring www.ftc.gov 1-877-ftc-help Ever wonder how a creditor decides whether to grant you credit? For years, creditors

FTC Facts For Consumers Federal Trade Commission For The Consumer May 2006 Credit Scoring www.ftc.gov 1-877-ftc-help Ever wonder how a creditor decides whether to grant you credit? For years, creditors

Secrets to Success: Personal Finance Management

Secrets to Success: Personal Finance Management Harvard University Employees Credit Union (HUECU) A financial institution exclusively serving the Harvard University students, alumni, faculty, staff, and

Secrets to Success: Personal Finance Management Harvard University Employees Credit Union (HUECU) A financial institution exclusively serving the Harvard University students, alumni, faculty, staff, and

ACF Administration for Children and Families

ACF Administration for Children and Families U.S. DEPARTMENT OF HEALTH AND HUMAN SERVICES Administration on Children, Youth and Families 1. Log No: ACYF-CB-PI-12-07 2. Issuance Date: May 8, 2012 3. Originating

ACF Administration for Children and Families U.S. DEPARTMENT OF HEALTH AND HUMAN SERVICES Administration on Children, Youth and Families 1. Log No: ACYF-CB-PI-12-07 2. Issuance Date: May 8, 2012 3. Originating

Understanding credit reports and scores

MODULE 7: Understanding credit reports and scores If you have a 10 -minute session... If you have a 30 -minute session... If you have multiple sessions... Tool 1: Getting your credit reports and scores

MODULE 7: Understanding credit reports and scores If you have a 10 -minute session... If you have a 30 -minute session... If you have multiple sessions... Tool 1: Getting your credit reports and scores

Your Guide To Better Credit

Your Guide To Better Credit INTRODUCTION Your go-to guide to better credit It seems like every other commercial on television touts some sort of offer around credit. You hear things like, Free credit report,

Your Guide To Better Credit INTRODUCTION Your go-to guide to better credit It seems like every other commercial on television touts some sort of offer around credit. You hear things like, Free credit report,

INSTALLATION AND USE OF CREDIT-AID SOFTWARE

1 TABLE OF CONTENTS INSTALLATION AND USE OF CREDIT-AID SOFTWARE... 3 INTRODUCTION FROM THE CREDIT DOCTOR... 4 YOUR CREDIT REPORTS... 7 CREDIT SCORING... 8 ORDERING COPIES OF YOUR CREDIT REPORTS... 9 REVIEWING

1 TABLE OF CONTENTS INSTALLATION AND USE OF CREDIT-AID SOFTWARE... 3 INTRODUCTION FROM THE CREDIT DOCTOR... 4 YOUR CREDIT REPORTS... 7 CREDIT SCORING... 8 ORDERING COPIES OF YOUR CREDIT REPORTS... 9 REVIEWING

TRANS UNION OF CANADA Consumer Credit Report 16OCT98

Page 1 of 6 TRANS UNION OF CANADA Consumer Credit Report 16OCT98 1 Surname Given Name(s) Soc. Ins. No. Birth Subject CONSUMER JOHN/B 11OCT61 Spouse CONSUMER JEANNE/ 22JAN63 X-Ref AKA CONSUMER JOHN ROBERT/

Page 1 of 6 TRANS UNION OF CANADA Consumer Credit Report 16OCT98 1 Surname Given Name(s) Soc. Ins. No. Birth Subject CONSUMER JOHN/B 11OCT61 Spouse CONSUMER JEANNE/ 22JAN63 X-Ref AKA CONSUMER JOHN ROBERT/

RESCORE EXPRESS SERVICES

RESCORE EXPRESS SERVICES Thank you for your recent inquiry regarding our Rescore Express service. Rescore Express is an expedited process of correction of dispute, through which Advantage Credit will attempt,

RESCORE EXPRESS SERVICES Thank you for your recent inquiry regarding our Rescore Express service. Rescore Express is an expedited process of correction of dispute, through which Advantage Credit will attempt,

Understanding Credit

Understanding Credit LAURA STEINBECK DIRECTOR OF BUSINESS DEVELOPMENT, SALLIE MAE 2018 MASFAP CONFERENCE Agenda 2 Credit Management Protect Yourself Understanding Credit Reports Summary: Financial Health

Understanding Credit LAURA STEINBECK DIRECTOR OF BUSINESS DEVELOPMENT, SALLIE MAE 2018 MASFAP CONFERENCE Agenda 2 Credit Management Protect Yourself Understanding Credit Reports Summary: Financial Health

Fixing Bad Credit and Solving Credit Problems 1

FCS 5049 Fixing Bad Credit and Solving Credit Problems 1 Mary N. Harrison 2 When you want to buy a car, a house, or other expensive items you probably expect to use credit. For smaller purchases, your

FCS 5049 Fixing Bad Credit and Solving Credit Problems 1 Mary N. Harrison 2 When you want to buy a car, a house, or other expensive items you probably expect to use credit. For smaller purchases, your

Playing Membership Application

Prior TG&CC membership number, if any: Date membership ended: New membership number if accepted: Date membership began: 10532 Golf Link Road, Turlock, CA 95380 Telephone (209) 634-5471 Playing Membership

Prior TG&CC membership number, if any: Date membership ended: New membership number if accepted: Date membership began: 10532 Golf Link Road, Turlock, CA 95380 Telephone (209) 634-5471 Playing Membership

CREDIT-REBUILDING LETTERS. Index of Credit-Rebuilding Letters. Letter # Letter Should Be Sent to Reason to Send Letter (Letter Name)

") CREDIT-REBUILDING LETTERS Index of Credit-Rebuilding Letters Letter # Letter Should Be Sent to Reason to Send Letter (Letter Name) 1 Credit Reporting Agency/Bureau Request for Credit Report 2 Credit Reporting

CREDIT-REBUILDING LETTERS Index of Credit-Rebuilding Letters Letter # Letter Should Be Sent to Reason to Send Letter (Letter Name) 1 Credit Reporting Agency/Bureau Request for Credit Report 2 Credit Reporting

Understanding Credit Reports and Scores and How to Improve It!

Understanding Credit Reports and Scores and How to Improve It! Ryan Chatterton, CCCC What Will We Cover? When we are finished, you will understand: Credit Reports and Credit Scores - What they are and

Understanding Credit Reports and Scores and How to Improve It! Ryan Chatterton, CCCC What Will We Cover? When we are finished, you will understand: Credit Reports and Credit Scores - What they are and

FAQ. What is trended credit data? Why is this change coming?

FAQ What is trended credit data? Trended credit data provides an expanded, more granular view of the consumer by leveraging 24 months of a consumer s past balance, payment, and credit utilization history.

FAQ What is trended credit data? Trended credit data provides an expanded, more granular view of the consumer by leveraging 24 months of a consumer s past balance, payment, and credit utilization history.

Your Money, Your Goals Spotlight Series. Understanding credit reports and scores: An in-depth look

Your Money, Your Goals Spotlight Series Understanding credit reports and scores: An in-depth look DISCLAIMER This presentation is being made by a Consumer Financial Protection Bureau representative on

Your Money, Your Goals Spotlight Series Understanding credit reports and scores: An in-depth look DISCLAIMER This presentation is being made by a Consumer Financial Protection Bureau representative on

Understanding Credit Reports

Understanding Credit Reports Family Economics & Financial Education Take Charge of Your Finances Credit Report Detectives Meet Isabella, your new client: About to graduate from college In extreme debt

Understanding Credit Reports Family Economics & Financial Education Take Charge of Your Finances Credit Report Detectives Meet Isabella, your new client: About to graduate from college In extreme debt

This helpful resource translates some commonly used financial terms into plain English.

FINANCIAL JARGON This helpful resource translates some commonly used financial terms into plain English. One of the things that can make the world of personal finance so confusing is that it seems to come

FINANCIAL JARGON This helpful resource translates some commonly used financial terms into plain English. One of the things that can make the world of personal finance so confusing is that it seems to come

Product User Guide It s Your Credit. Keep It That Way with 5LINX Safe Score.

Product User Guide It s Your Credit. Keep It That Way with 5LINX Safe Score. Features & Benefits Identity Verification Credit Monitoring Score Simulator Full Access to Credit Reports Score Tracker Resource

Product User Guide It s Your Credit. Keep It That Way with 5LINX Safe Score. Features & Benefits Identity Verification Credit Monitoring Score Simulator Full Access to Credit Reports Score Tracker Resource

Welcome. 1. Agenda. 2. Ground Rules. 3. Introductions. Charge It Right 2

Charge It Right Welcome 1. Agenda 2. Ground Rules 3. Introductions Charge It Right 2 Objectives Define credit Explain why credit is important Identify the factors creditors look for when making credit

Charge It Right Welcome 1. Agenda 2. Ground Rules 3. Introductions Charge It Right 2 Objectives Define credit Explain why credit is important Identify the factors creditors look for when making credit

Profiles in Credit is designed to be flexible and meet the needs of learners in different educational settings. Examples include:

Profiles in Credit Educator Resource Guide Module Summary Profiles in Credit is a self-paced, interactive learning module in which students visit the social media profiles of three young people facing

Profiles in Credit Educator Resource Guide Module Summary Profiles in Credit is a self-paced, interactive learning module in which students visit the social media profiles of three young people facing

Office of Student Financial Management

September 2015 Office of Student Financial Management Kasia Palm: Director of Student Financial Management What is Credit? - The ability to obtain goods/services before payment based on the trust that

September 2015 Office of Student Financial Management Kasia Palm: Director of Student Financial Management What is Credit? - The ability to obtain goods/services before payment based on the trust that

WHAT ARE CREDITORS LOOKING FOR?

THEME 4 SPENDING AND USING CREDIT IIX ERe I' E 3.1 Reading a Credit Report depends on a credit report. A Your credit ability report tois qualify a record forof a loan individual's personal credit history.

THEME 4 SPENDING AND USING CREDIT IIX ERe I' E 3.1 Reading a Credit Report depends on a credit report. A Your credit ability report tois qualify a record forof a loan individual's personal credit history.

FICO Score Open Access Consumer Credit Education US Version. Frequently Asked Questions about FICO Scores

FICO Score Open Access Consumer Credit Education US Version Frequently Asked Questions about Scores 2012 Fair Isaac Corporation. All rights reserved. 1 January 01, 2012 Table of Contents About Scores...

FICO Score Open Access Consumer Credit Education US Version Frequently Asked Questions about Scores 2012 Fair Isaac Corporation. All rights reserved. 1 January 01, 2012 Table of Contents About Scores...

GLOSSARY OF LOAN TERMS

GLOSSARY OF LOAN TERMS Accrued Interest Interest that accumulates on the unpaid principal balance of a loan. Accrual Date The date on which interest charges on an educational loan begin to accrue. Amortization

GLOSSARY OF LOAN TERMS Accrued Interest Interest that accumulates on the unpaid principal balance of a loan. Accrual Date The date on which interest charges on an educational loan begin to accrue. Amortization

The information that follows includes important information about the cost of credit and the interest rates that apply to your account.

Terms and Conditions of the Bill Me Later Payment System Bill Me Later is an open-end credit plan offered by WebBank, Salt Lake City, Utah ( the Lender ). IF YOU DO NOT HAVE A BILL ME LATER ACCOUNT, by

Terms and Conditions of the Bill Me Later Payment System Bill Me Later is an open-end credit plan offered by WebBank, Salt Lake City, Utah ( the Lender ). IF YOU DO NOT HAVE A BILL ME LATER ACCOUNT, by

How Students Use Credit and What You Need to Know. Deb Gossman College Ave Student Loans

How Students Use Credit and What You Need to Know Deb Gossman College Ave Student Loans 3-19-2019 Agenda Private credit within the student loan ecosystem & compared to other consumer assets Credit Reports

How Students Use Credit and What You Need to Know Deb Gossman College Ave Student Loans 3-19-2019 Agenda Private credit within the student loan ecosystem & compared to other consumer assets Credit Reports

Creditworthiness (UXL)

") Creditworthiness (UXL) Since so much debt is unsecured, it is important for companies to have information on how well their potential borrowers handle money in order to assess their creditworthiness, or

Creditworthiness (UXL) Since so much debt is unsecured, it is important for companies to have information on how well their potential borrowers handle money in order to assess their creditworthiness, or

AUTHORIZATION AND PAYMENT

In this Choice Rewards World MasterCard Card ( Agreement and Disclosure Statement ) the words: I, me, my and mine mean any and all of those who apply for or use the First Technology Federal Credit Union

In this Choice Rewards World MasterCard Card ( Agreement and Disclosure Statement ) the words: I, me, my and mine mean any and all of those who apply for or use the First Technology Federal Credit Union

Understanding Credit Reports & Credit Scoring

Understanding Credit Reports & Credit Scoring April 2017 2012 Genworth Financial, Inc. All rights reserved. Overview & Course Objectives Credit Reports & Scoring Credit Reports & Scoring are designed to

Understanding Credit Reports & Credit Scoring April 2017 2012 Genworth Financial, Inc. All rights reserved. Overview & Course Objectives Credit Reports & Scoring Credit Reports & Scoring are designed to

Terms. Asset - Assets are everything you own that has any monetary value, plus any money you are owed.

Terms Asset - Assets are everything you own that has any monetary value, plus any money you are owed. Award Letter - The award letter is sent by the Office of Financial Aid and provides information on

Terms Asset - Assets are everything you own that has any monetary value, plus any money you are owed. Award Letter - The award letter is sent by the Office of Financial Aid and provides information on

UNDERSTANDING CREDIT. WASFAA Conference Seattle, WA Speakers: Thalassa Naylor, Sallie Mae Anthony Lombardi, Sallie Mae Date: April 10, 2017

UNDERSTANDING CREDIT WASFAA Conference Seattle, WA Speakers: Thalassa Naylor, Sallie Mae Anthony Lombardi, Sallie Mae Date: April 10, 2017 Agenda 2 Credit Management Protect Yourself Understanding Your

UNDERSTANDING CREDIT WASFAA Conference Seattle, WA Speakers: Thalassa Naylor, Sallie Mae Anthony Lombardi, Sallie Mae Date: April 10, 2017 Agenda 2 Credit Management Protect Yourself Understanding Your

When sending a Dispute Letter, McCarthy Law requires the following items in a Dispute Letter for Litigation ready files:

DISPUTE LETTERS TABLE OF CONTENTS Dispute Letter Requirements........ 1 Dispute Letter Tips.. 1 Additional Documentation... 1 SAMPLE LETTERS 1099... 2 Account Settled directly with Bank.. 3 Account Settled

DISPUTE LETTERS TABLE OF CONTENTS Dispute Letter Requirements........ 1 Dispute Letter Tips.. 1 Additional Documentation... 1 SAMPLE LETTERS 1099... 2 Account Settled directly with Bank.. 3 Account Settled

Annual Interest Rates. Standard Rates: Purchases: 11.99% Cash advances (including balance transfers and access cheques):11.

:11.") Annual Interest Rates Standard Rates: Purchases: 11.99% Cash advances (including balance transfers and access cheques):11.99% Default Rates: If your Minimum Payment is late more than once within 12consecutive

Annual Interest Rates Standard Rates: Purchases: 11.99% Cash advances (including balance transfers and access cheques):11.99% Default Rates: If your Minimum Payment is late more than once within 12consecutive

VISA PERKS CREDIT CARD. Apply Now! of rewards points with every purchase! Enjoy the PERKS midcoastfcu.me.

186 Lower Main Street Freeport, Maine 207.865.4443 831 Middle Street Bath, Maine 207.443.5531 6 Station Avenue Brunswick, Maine 207.729.8737 41 Route One Edgecomb, Maine 207.882.7919 209 New County Road

186 Lower Main Street Freeport, Maine 207.865.4443 831 Middle Street Bath, Maine 207.443.5531 6 Station Avenue Brunswick, Maine 207.729.8737 41 Route One Edgecomb, Maine 207.882.7919 209 New County Road

Count Balance $0.00 $0.00 $0.00 Current Delinquent Other 0 0 0

COLLECTION ACCOUNTS: Count 0 0 0 Balance $0.00 $0.00 $0.00 Current 0 0 0 Delinquent 0 0 0 Other 0 0 0 TOTAL ACCOUNTS: Count 5 5 5 Balance $0.00 $0.00 $0.00 Current 5 5 5 Delinquent 0 0 0 Other 0 0 0 ACCOUNTS

COLLECTION ACCOUNTS: Count 0 0 0 Balance $0.00 $0.00 $0.00 Current 0 0 0 Delinquent 0 0 0 Other 0 0 0 TOTAL ACCOUNTS: Count 5 5 5 Balance $0.00 $0.00 $0.00 Current 5 5 5 Delinquent 0 0 0 Other 0 0 0 ACCOUNTS

Bankruptcy and Foreclosure Policy Changes

August 13, 2008 Announcement 08-16: Bankruptcy, Foreclosure, and Conversion of Principal Residence Policy Changes; and Revised Property Value Representation and Warranty Requirements Frequently Asked Questions

August 13, 2008 Announcement 08-16: Bankruptcy, Foreclosure, and Conversion of Principal Residence Policy Changes; and Revised Property Value Representation and Warranty Requirements Frequently Asked Questions

CARDMEMBER AGREEMENT AND DISCLOSURE STATEMENT Part 1 of 2: Agreement ABOUT THIS AGREEMENT

CARDMEMBER AGREEMENT AND DISCLOSURE STATEMENT Part 1 of 2: Agreement ABOUT THIS AGREEMENT Part 1 and 2 together make your Cardmember Agreement and Disclosure Statement ( Agreement ) and govern your Credit

CARDMEMBER AGREEMENT AND DISCLOSURE STATEMENT Part 1 of 2: Agreement ABOUT THIS AGREEMENT Part 1 and 2 together make your Cardmember Agreement and Disclosure Statement ( Agreement ) and govern your Credit

How to Dispute Credit Report Errors

FTC Facts For Consumers Federal Trade Commission For The Consumer May 2006 www.ftc.gov 1-877-ftc-help How to Dispute Credit Report Errors Y our credit report contains information about where you live,

FTC Facts For Consumers Federal Trade Commission For The Consumer May 2006 www.ftc.gov 1-877-ftc-help How to Dispute Credit Report Errors Y our credit report contains information about where you live,

VISA Credit Card Application

VISA Credit Card Application An individual may apply for individual credit. Two co-applicants may apply for joint credit Complete Applicant sections if only the applicant s income is considered for loan

VISA Credit Card Application An individual may apply for individual credit. Two co-applicants may apply for joint credit Complete Applicant sections if only the applicant s income is considered for loan

Mortgage Terms Glossary

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

BUSINESS CREDIT REPORT

COMMERCIAL INFORMATION SOLUTIONS BUSINESS CREDIT REPORT Business information Company name BUSINESS CREDIT REPORT TEST FILE Legal name BUSINESS CREDIT REPORT TEST FILE Address MONTREAL QUEBEC CANADA H3H1H5

COMMERCIAL INFORMATION SOLUTIONS BUSINESS CREDIT REPORT Business information Company name BUSINESS CREDIT REPORT TEST FILE Legal name BUSINESS CREDIT REPORT TEST FILE Address MONTREAL QUEBEC CANADA H3H1H5

Money Matters: Making Cents of It All

Slide 1 Money Matters: Making Cents of It All Dollars and Sense Page1 Slide 2 Copyright Copyright Texas Education Agency, 2014. These Materials are copyrighted and trademarked as the property of the Texas

Slide 1 Money Matters: Making Cents of It All Dollars and Sense Page1 Slide 2 Copyright Copyright Texas Education Agency, 2014. These Materials are copyrighted and trademarked as the property of the Texas

Credit and Credit Cards

Credit and Credit Cards What s Next Project Credit Cards They are all around you. Most people have at least one. Some have many. They are credit cards. A credit card allows you to pay for merchandise or

Credit and Credit Cards What s Next Project Credit Cards They are all around you. Most people have at least one. Some have many. They are credit cards. A credit card allows you to pay for merchandise or