Course structure. A. Bank as financial intermediary. B. Banking products and services. C. Banks' Financial Reporting. D. Risk management issues

|

|

|

- Christopher Lucas

- 5 years ago

- Views:

Transcription

1 Course structure 1 A. Bank as financial intermediary B. Banking products and services Course 3 - Banking activities Course 4 - Banking products and their pricing Course 5 - Types of banking C. Banks' Financial Reporting D. Risk management issues

2 Part B. Bank as financial intermediary Lecture 3. Banking activities

3 3 Banking activities

4 Objectives What do banks do? 3.2. Banking services

5 3.1. What do banks do? 5 A simplified bank balance sheet Example (course) for banks, the main source of funding is customer deposits (reported on the liabilities side of the balance sheet); this funding is then invested in loans, other investments and fixed assets (such as buildings for the branch network); the difference between total assets and total liabilities is the bank capital (equity); banks make profits by charging an interest rate on their loans that is higher than the one they pay to depositors;

6 3.1. What do banks do? 6 A simplified bank balance sheet Example (course) as with other companies, banks can raise funds by issuing bonds and equity (shares), and saving from past profits (retained earnings); however, the bulk of their money comes from deposits.!!! It is this ability to collect deposits from the public that distinguishes banks from other financial institutions.

7 3.1. What do banks do? 7 Banks are deposit-taking institutions (DTIs) and are also known as monetary financial institutions (MFIs). Monetary financial institutions play a major role in a country s economy as their deposit liabilities form a major part of a country s money supply and are therefore very relevant to governments and Central Banks for the transmission of monetary policy. Banks deposits function as money; as a consequence, an expansion of bank deposits results in an increase in the stock of money circulating in an economy. All other things being equal, the money supply, that is the total amount of money in the economy, will increase.

8 3.1. What do banks do? 8 The monetary function of bank deposits is often seen as one of the main reasons why deposit-taking institutions (DTIs) are subjected to heavier regulation and supervision than their non-deposit-taking institution (NDTI) counterparts (such as insurance companies, pension funds, investment companies, finance houses).

9 3.1. What do banks do? Classification of financial intermediaries by the nature of financial contracts 9

10 3.1. What do banks do? 10 Discretionary flow of funds savers can make discretionary decisions concerning how much money to hold and for how long depositors are free to decide the frequency and amount of their transactions

11 3.1. What do banks do? 11 Contractual flow of funds holding assets from other financial institutions requires a contract which specifies the amount and frequency of the flow of funds; Example: the monthly contributions to a pension fund or to an insurance provider are normally fixed and predetermined.

12 3.1. What do banks do? 12!!! There is no unique, universally accepted classification of financial intermediaries. Furthermore, regulation; financial conglomeration; advances in information technology and financial innovation; increased competition; and globalisation have all contributed to change the industry in recent years.

13 3.1. What do banks do? 13 All countries have regulations that define what banking business is. EU countries banks have been permitted to perform a broad array of financial services activity since the early 1990s; Since 1999 both US and Japanese banks are also allowed to operate as full service financial firms. Commercial banks can undertake a broad range of financial services, including investment banking and insurance activities; In Romania commercial banks have several restrictions regarding investment activities.

14 3.1. What do banks do? 14 universal banks - banks that engage, directly or through subsidiaries, in other financial activities, such as: financial instruments factoring leasing investment banking

15 3.2. Banking services 15 Modern banks offer a wide range of financial services, including: Payment services Deposit and lending services Investment, pensions and insurance services E-banking

16 Banking services Payment services

17 3.2. Banking services Payment services 17 Banks play a major role in the provision of payment services. transfers between individuals and/or companies transfers between financial institutions (typically high-value transactions)!!! If any of these circulation systems failed, the functioning of large and important parts of the economy would be affected.

18 3.2. Banking services Payment services 18 Types of cashless payments: Cheques Credit transfers Standing orders Direct debits Plastic cards

19 3.2. Banking services Payment services 19 Cheques A document that orders a bank to pay a specific amount of money from a person's account to the person in whose name the cheque has been issued. The person writing the cheque, the drawer, has a transaction banking account (often called a current account) where their money is held. The drawer writes the various details including the monetary amount, date, and a payee on the cheque, and signs it, ordering their bank, known as the drawee, to pay that person or company the amount of money stated.!!! Cheque payments are known as debit transfers because they are written requests to debit the payee s account.

20 Banking services Payment services

21 3.2. Banking services Payment services 21 Cheques Parts of a cheque based on a UK example: 1. drawee (the financial institution where the cheque can be presented for payment) 2. payee (the recipient of the money) 3. date of issue 4. amount of currency 5. drawer, the person or entity making the cheque 6. signature of drawer 7. machine readable routing and account information.

22 3.2. Banking services Payment services 22 Credit transfers (or Bank Giro Credits) payments where the customer instructs their bank to transfer funds directly to the beneficiary's bank account. Examples: pay invoices; send payment in advance for products ordered.

23 Banking services Payment services

24 Banking services Payment services

25 3.2. Banking services Payment services 25 Standing orders are instructions from the customer (account holder) to the bank to pay a fixed amount at regular intervals into the account of another individual or company. The bank has the responsibility for remembering to make these payments. Only the account holder can change the standing order instructions. Example: rents, credit rates.

26 3.2. Banking services Payment services 26 Direct debits are originated by the supplier that supplied the goods/service and the customer has to sign the direct debit; the direct debit instructions are usually of a variable amount and the times at which debiting takes place can also be either fixed or variable (although usually fixed); If a payment is missed, the supplier can request the missed payment on a number of occasions. If the payments are continually missed over a period of time, the customer s bank will cancel the direct debit. Example: utility bills (electricity, gas, water bills)

27 Banking services Payment services Plastic cards include credit cards, debit cards, cheque guarantee cards, travel and entertainment cards, shop cards and smart or chip cards. technically, plastic cards do not act themselves as a payment mechanism they help to identify the customers and assist in creating either a paper or electronic payment.

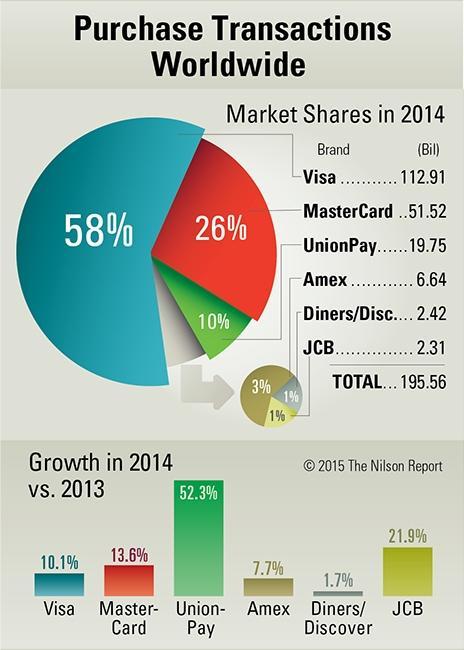

28 3.2. Banking services Payment services 28 Plastic cards: Credit cards provide holders with a pre-arranged credit limit to use for purchases at retail stores and other outlets; the retailer pays the credit card company a commission on every sale made via credit cards; the consumer obtains free credit if the bill is paid off before a certain date; if the bill is not fully paid off then it attracts interest. Visa and MasterCard are the two most important bankowned credit card organizations.

29 3.2. Banking services Payment services 29 Plastic cards: Debit cards are issued directly by banks and allow customers to withdraw money from their accounts. they can also be used to obtain cash and other information when used through automated teller machines (ATMs).

30 Banking services Payment services

31 31

32 32

33 33

34 34

35 35

36 36

37 37

38 38

39 39

40 3.2. Banking services Deposit and lending services 40 Current or checking accounts Time or savings deposits Consumer loans and mortgages

41 3.2. Banking services Deposit and lending services 41 Current or checking accounts pay no (or low) rates of interest and are used mainly for payments banks offer a broad range of current accounts tailored to various market segments and with various other services attached

42 3.2. Banking services Deposit and lending services 42 Current or checking accounts

43 3.2. Banking services Deposit and lending services 43 Time or savings deposits involve depositing funds for a set period of time for a predetermined or variable rate of interest Banks offer an extensive range of such savings products, from standard fixed term and fixed deposit rate to variable term with variable rates. banks offer deposit facilities that have features that are a combination of time and current accounts whereby customers can withdraw their funds instantly or at short notice. deposits that can be withdrawn on demand pay lower rates than those deposited in the bank for a set period.

44 Banking services Deposit and lending services

45 3.2. Banking services Deposit and lending services 45 Consumer loans and mortgages are commonly offered by banks to their retail customers Consumer loans can be unsecured (no collateral is requested) or secured on property (collateral is requested) interest rates are mainly variable (interest payments vary relative to a benchmark rate such as LIBOR, EURIBOR, ROBOR), but can be also fixed

46 3.2. Banking services Investment, pensions and insurance services 46 Investment products Pensions and insurance services

47 3.2. Banking services Investment, pensions and insurance services 47 Pensions and insurance services provide retirement income (in the form of annuities) to those contributing to pension plans; contributions paid into the pension fund are invested in longterm investments with the individual making contributions receiving a pension on retirement; pension services offered via banks are known as private pensions to distinguish them from public pensions offered by the state; insurance products protect individuals (policyholders) from various adverse events.

48 3.2. Banking services Investment, pensions and insurance services 48 Investment products include various securities-related products including mutual funds (unit trusts), investment in company stocks and various other securities-related products (such as savings bonds); in reality there is a strong overlap between savings and investments products and many banks advertise these services together;

49 3.2. Banking services E-banking 49 E-money includes reloadable electronic money instruments in the form of stored value cards and electronic tokens stored in computer memory. Remote payments payment instruments that allow (remote) access to a customer s account

50 Banking services E-banking

51 Banking services E-banking

52 3.2. Banking services E-banking 52 Major institutions offer traditional remote banking services (ATMs and telephone banking) and have started to offer a growing number of on-line PC banking and internet banking services. Some small-sized specialized banks operate without branches exclusively via remote banking channels. In most cases these banks are subsidiaries of existing banking groups. Innovative new institutions are setting up business on the internet, also covering traditional banking activities. This activity is often promoted by large to medium-sized banks.

Latvijas Banka. 13 March 2014 Regulation No. 131

Latvijas Banka 13 March 2014 Regulation No. 131 Regulation for Compiling Credit Institution, Electronic Money Institution and Payment Institution Payment Statistics Report Note: As amended by Latvijas

Latvijas Banka 13 March 2014 Regulation No. 131 Regulation for Compiling Credit Institution, Electronic Money Institution and Payment Institution Payment Statistics Report Note: As amended by Latvijas

Chapter 10: Money and Banking Section 3

Chapter 10: Money and Banking Section 3 Objectives 1. Explain how the money supply in the United States is measured. 2. Describe the functions of financial institutions. 3. Identify different types of

Chapter 10: Money and Banking Section 3 Objectives 1. Explain how the money supply in the United States is measured. 2. Describe the functions of financial institutions. 3. Identify different types of

Payment & Settelment System in India

All about Payment and Settlement Systems in India A country needs money supply for economic activity to carry out trade and commerce to quench demand and supply of goods and services. For such exchanges

All about Payment and Settlement Systems in India A country needs money supply for economic activity to carry out trade and commerce to quench demand and supply of goods and services. For such exchanges

Authorization Approval of a transaction by the financial institution that issued a paycard or other payment card.

APA Visa Paycard Portal Glossary of Terms Account Number A unique number assigned by a financial institution to a customer s account. The account number for a paycard is embossed or imprinted on the card

APA Visa Paycard Portal Glossary of Terms Account Number A unique number assigned by a financial institution to a customer s account. The account number for a paycard is embossed or imprinted on the card

Schedule of Fees and Charges (Applicable to Retail Customers)

") Schedule of and Charges (Applicable to Retail Customers) Contents 1. Cash withdrawal/deposit 2 2. Certificates 2 3. Accounts 2 4. Cheques 3 5. Cards 3 6. Loans 4 7. Remittances 4 8. Invoices 5 9. Miscellaneous

Schedule of and Charges (Applicable to Retail Customers) Contents 1. Cash withdrawal/deposit 2 2. Certificates 2 3. Accounts 2 4. Cheques 3 5. Cards 3 6. Loans 4 7. Remittances 4 8. Invoices 5 9. Miscellaneous

Business Current Account Cash Tariff

This tariff details the services, rates and charges that are effective from 5 January 2018. We can vary or amend this tariff at any time, but will notify customers when we do so in accordance with account

This tariff details the services, rates and charges that are effective from 5 January 2018. We can vary or amend this tariff at any time, but will notify customers when we do so in accordance with account

UK Plastic Cards 2009 The Way We Pay

UK Plastic Cards 2009 The Way We Pay Plastic cards are the most popular non-cash payment method in the UK. They allow cardholders to pay for goods and services easily and conveniently, and provide a secure

UK Plastic Cards 2009 The Way We Pay Plastic cards are the most popular non-cash payment method in the UK. They allow cardholders to pay for goods and services easily and conveniently, and provide a secure

Saving. Reasons for saving. Future purchases Unforeseen events Children s Education Income for the Future Holidays

Banking Saving Reasons for saving Future purchases Unforeseen events Children s Education Income for the Future Holidays Investing Why would you bother investing your savings? To earn interest For safety

Banking Saving Reasons for saving Future purchases Unforeseen events Children s Education Income for the Future Holidays Investing Why would you bother investing your savings? To earn interest For safety

Settle in faster with RBC Newcomer Advantage. Banking made easy for newcomers to Canada

Settle in faster with RBC Newcomer Advantage Banking made easy for newcomers to Canada 1 RBC Royal Bank Banking made easy 2 10newcomers to Canada We know how important it is to choose the right banking

Settle in faster with RBC Newcomer Advantage Banking made easy for newcomers to Canada 1 RBC Royal Bank Banking made easy 2 10newcomers to Canada We know how important it is to choose the right banking

Committee on Payments and Market Infrastructures

Committee on Payments and Market Infrastructures Methodology of the statistics on payments and financial market infrastructures in the CPMI countries (Red Book statistics) August 2017 This publication

Committee on Payments and Market Infrastructures Methodology of the statistics on payments and financial market infrastructures in the CPMI countries (Red Book statistics) August 2017 This publication

The One account Personal Banking Service. We won t charge you a penny for these services. What we charge you for. General banking

the One account services and charges April 2017 The One account Personal Banking Service The One account isn t just about saving money. It s about a great banking service too one that s personal to you.

the One account services and charges April 2017 The One account Personal Banking Service The One account isn t just about saving money. It s about a great banking service too one that s personal to you.

7/27/17. THEME 2 Part 1A Managing Basic Assets

Honors Personal Finance THEME 2 Part 1A Managing Basic Assets Managing Your Cash & Savings Establishing good financial habits involves managing cash as well as other types of assets. Cash Management the

Honors Personal Finance THEME 2 Part 1A Managing Basic Assets Managing Your Cash & Savings Establishing good financial habits involves managing cash as well as other types of assets. Cash Management the

CURRENT ACCOUNT (WADI A/QARD) DEPOSIT

DEPOSIT") DEPOSIT PRODUCTS Mobilization of funds from depositors/savers to borrowers/investors is an important task of a financial intermediary in the economy. Financial intermediaries attempt to achieve this goal

DEPOSIT PRODUCTS Mobilization of funds from depositors/savers to borrowers/investors is an important task of a financial intermediary in the economy. Financial intermediaries attempt to achieve this goal

A banking service allowing a customer s money to be handled and tracked. Common bank accounts are savings and checking accounts.

Kids Glossary Terms Account Account balance Account fee Annual fee Automated teller machine (ATM) Available Balance Bad check Bad credit Balance your checkbook Bank Bank account Bank statement Bounced

Kids Glossary Terms Account Account balance Account fee Annual fee Automated teller machine (ATM) Available Balance Bad check Bad credit Balance your checkbook Bank Bank account Bank statement Bounced

How Does the Banking System Work? (EA)

") How Does the Banking System Work? (EA) What do you notice when you enter a bank? Perhaps you pass an automated teller machine in the lobby. ATMs can dispense cash, accept deposits, and make transfers from

How Does the Banking System Work? (EA) What do you notice when you enter a bank? Perhaps you pass an automated teller machine in the lobby. ATMs can dispense cash, accept deposits, and make transfers from

NEGOTIABLE INSTRUMENTS

NEGOTIABLE INSTRUMENTS 6.1 Types of Negotiable Instruments 6.2 Presenting Checks for Payment 6.3 Processing Checks 6.4 Changing Forms of Payment Slide 1 Cengage/South-Western GOALS 6.1 TYPES OF NEGOTIABLE

NEGOTIABLE INSTRUMENTS 6.1 Types of Negotiable Instruments 6.2 Presenting Checks for Payment 6.3 Processing Checks 6.4 Changing Forms of Payment Slide 1 Cengage/South-Western GOALS 6.1 TYPES OF NEGOTIABLE

Credit Card Conditions of use. Terms and Conditions

Credit Card Conditions of use Terms and Conditions Effective: 20 March 2014 This document does not contain all the terms of this agreement or all of the information we are required by law to give you before

Credit Card Conditions of use Terms and Conditions Effective: 20 March 2014 This document does not contain all the terms of this agreement or all of the information we are required by law to give you before

Credit Card Conditions of Use. Credit Guide.

Credit Card Conditions of Use. Credit Guide. Effective Date: 20 May 2014 This document does not contain all the terms of this agreement or all of the information we are required by law to give you before

Credit Card Conditions of Use. Credit Guide. Effective Date: 20 May 2014 This document does not contain all the terms of this agreement or all of the information we are required by law to give you before

TUTORIAL KIT OMEGA SEMESTER PROGRAMME: BANKING AND FINANCE COURSE: BFN 121

TUTORIAL KIT OMEGA SEMESTER PROGRAMME: BANKING AND FINANCE COURSE: BFN 121 i DISCLAIMER The contents of this document are intended for practice and leaning purposes at the undergraduate level. The materials

TUTORIAL KIT OMEGA SEMESTER PROGRAMME: BANKING AND FINANCE COURSE: BFN 121 i DISCLAIMER The contents of this document are intended for practice and leaning purposes at the undergraduate level. The materials

Business and Agribusiness Account and service fees

Business and Agribusiness Account and service fees April 2018 PARTNERS Account fees Account fees are subject to change at any time. Where applicable, account fees are in addition to all service fees. Business

Business and Agribusiness Account and service fees April 2018 PARTNERS Account fees Account fees are subject to change at any time. Where applicable, account fees are in addition to all service fees. Business

Banking Today. Banks and their uses

Banking Today Banks and their uses Money Supply Money Supply all the money available in the United States (not just dollars and coins) Easy money (liquidity). Dollars Coins Checking Accounts (Demand Deposits)

Banking Today Banks and their uses Money Supply Money Supply all the money available in the United States (not just dollars and coins) Easy money (liquidity). Dollars Coins Checking Accounts (Demand Deposits)

Teens Glossary Terms. (see Bank account)

") Teens Glossary Terms Account Account balance Account fee Annual fee Annual percentage rate (APR) Automated teller machine (ATM) Available Balance Bad check Bad credit Balance your checkbook Bank (see Bank

Teens Glossary Terms Account Account balance Account fee Annual fee Annual percentage rate (APR) Automated teller machine (ATM) Available Balance Bad check Bad credit Balance your checkbook Bank (see Bank

ISLAND PREMIER BANKING INTEREST RATES & CHARGES. Effective from 22 November 2015

ISLAND PREMIER BANKING INTEREST RATES & CHARGES Effective from 22 November 2015 Contents Island Premier rates and charges 1 Island Premier current account 1 Borrowing from us 1 Overdraft buffers 2 Overdraft

ISLAND PREMIER BANKING INTEREST RATES & CHARGES Effective from 22 November 2015 Contents Island Premier rates and charges 1 Island Premier current account 1 Borrowing from us 1 Overdraft buffers 2 Overdraft

Credit Card Conditions of Use and Credit Guide

Credit Card Conditions of Use and Credit Guide Effective Date: 28 October 2016 Your Credit Contract includes this Conditions of Use brochure, the letter which advises both your credit limit and other prescribed

Credit Card Conditions of Use and Credit Guide Effective Date: 28 October 2016 Your Credit Contract includes this Conditions of Use brochure, the letter which advises both your credit limit and other prescribed

NATIONAL PAYMENT SYSTEM INFORMATION RETURN

National Payment System Department GUIDELINES TO COMPLETE THE NATIONAL PAYMENT SYSTEM INFORMATION RETURN Revised: June 2012 TABLE OF CONTENTS EXECUTIVE SUMMARY... 3 A. INTRODUCTION... 3 B. COLLECTION AND

National Payment System Department GUIDELINES TO COMPLETE THE NATIONAL PAYMENT SYSTEM INFORMATION RETURN Revised: June 2012 TABLE OF CONTENTS EXECUTIVE SUMMARY... 3 A. INTRODUCTION... 3 B. COLLECTION AND

MULTI CURRENCY CASH PASSPORT PREPAID MASTERCARD

MULTI CURRENCY CASH PASSPORT PREPAID MASTERCARD SEPTEMBER 2017 What is Multi-currency cash passport prepaid Mastercard A reloadable prepaid MasterCard travel currency card Designed to hold up to 11 major

MULTI CURRENCY CASH PASSPORT PREPAID MASTERCARD SEPTEMBER 2017 What is Multi-currency cash passport prepaid Mastercard A reloadable prepaid MasterCard travel currency card Designed to hold up to 11 major

BANKING.

BANKING ana@stikom.edu http://blog.stikom.edu/ana Bank financial institution licensed by a government. Its primary activities include borrowing and lending money. Many other financial activities were allowed

BANKING ana@stikom.edu http://blog.stikom.edu/ana Bank financial institution licensed by a government. Its primary activities include borrowing and lending money. Many other financial activities were allowed

Section 4.1 Banking Systems

Section 4.1 Banking Systems Objectives Identify different types of financial institutions Describe the services of financial institutions Explain special services offered by financial institutions Types

Section 4.1 Banking Systems Objectives Identify different types of financial institutions Describe the services of financial institutions Explain special services offered by financial institutions Types

All the materials and information included in this presentation is provided for educational and illustrative purposes only and is presented with the

Money Wise All the materials and information included in this presentation is provided for educational and illustrative purposes only and is presented with the express understanding that Virginia Credit

Money Wise All the materials and information included in this presentation is provided for educational and illustrative purposes only and is presented with the express understanding that Virginia Credit

Social Enterprise Directplus Tariff

This tariff details the services, rates and charges that are effective from 1 January 2017. We can vary or amend this tariff at any time, but will notify customers when we do so in accordance with account

This tariff details the services, rates and charges that are effective from 1 January 2017. We can vary or amend this tariff at any time, but will notify customers when we do so in accordance with account

Business Vantage Visa Credit Card. Conditions of Use. Effective Date: 4 November 2016

Business Vantage Visa Credit Card Conditions of Use 1 Effective Date: 4 November 2016 Business Vantage Visa Conditions of Use Bank of Melbourne This document does not contain all the terms of this agreement

Business Vantage Visa Credit Card Conditions of Use 1 Effective Date: 4 November 2016 Business Vantage Visa Conditions of Use Bank of Melbourne This document does not contain all the terms of this agreement

KINGDOM OF BAHRAIN VAT FINANCIAL SERVICES GUIDE

KINGDOM OF BAHRAIN VAT FINANCIAL SERVICES GUIDE MARCH 2019 VERSION 1.0 Contents Contents 1. Introduction... 5 1.1. Purpose of this Guide... 5 1.2. About the National Bureau for Revenue (NBR)... 5 1.3.

KINGDOM OF BAHRAIN VAT FINANCIAL SERVICES GUIDE MARCH 2019 VERSION 1.0 Contents Contents 1. Introduction... 5 1.1. Purpose of this Guide... 5 1.2. About the National Bureau for Revenue (NBR)... 5 1.3.

College Accounting. Heintz & Parry. 20 th Edition

Heintz & Parry 20 th Edition College Accounting 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part. Chapter

Heintz & Parry 20 th Edition College Accounting 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part. Chapter

Product Information Document Effective Date: 7 September 2018

Business Accounts Product Information Document Effective Date: 7 September 2018 This document contains information on Suncorp Bank Business Accounts: Business Everyday Accounts, Business Premium Accounts,

Business Accounts Product Information Document Effective Date: 7 September 2018 This document contains information on Suncorp Bank Business Accounts: Business Everyday Accounts, Business Premium Accounts,

BANKING & FINANCE (145)

") Page 1 of 10 Contestant Number: Time: Rank: BANKING & FINANCE (145) REGIONAL 2017 Multiple Choice: (30 @ 2 points each) (60 points) Financial Word Problems: (9 @ 2 points each) (18 points) Endorsements:

Page 1 of 10 Contestant Number: Time: Rank: BANKING & FINANCE (145) REGIONAL 2017 Multiple Choice: (30 @ 2 points each) (60 points) Financial Word Problems: (9 @ 2 points each) (18 points) Endorsements:

Mauritius Commercial Bank Limited Statement of Principal Interest Rates and Service Charges for domestic operations (Last updated

A INTEREST RATES (per annum) 1 Deposits Savings 1.80% Call Term (MUR) 7 days 0.10% 0.10% 03 months 0.30% 0.30% 12 months S + (0.250% - 0.265%) (1) S + (0.250% - 0.265%) (1) 24 months S + (0.375% - 0.425%)

A INTEREST RATES (per annum) 1 Deposits Savings 1.80% Call Term (MUR) 7 days 0.10% 0.10% 03 months 0.30% 0.30% 12 months S + (0.250% - 0.265%) (1) S + (0.250% - 0.265%) (1) 24 months S + (0.375% - 0.425%)

LEGAL ASPECTS OF ELECTRONIC CLEARING AND SETTLEMENT. Payments Clearing and Settlement - Australian Framework PETER SMITH

283 LEGAL ASPECTS OF ELECTRONIC CLEARING AND SETTLEMENT Payments Clearing and Settlement - Australian Framework PETER SMITH Chief Executive Officer Australian Payments Clearing Association Ltd, Sydney

283 LEGAL ASPECTS OF ELECTRONIC CLEARING AND SETTLEMENT Payments Clearing and Settlement - Australian Framework PETER SMITH Chief Executive Officer Australian Payments Clearing Association Ltd, Sydney

BANKING PROCEDURE AND CONTROL OF CASH

BANKING PROCEDURE AND CONTROL OF CASH 6-1 Chapter 6 Learning Objectives 1. Depositing, writing, and endorsing checks for a checking account. 2. Reconciling a bank statement. 3. Establishing and replenishing

BANKING PROCEDURE AND CONTROL OF CASH 6-1 Chapter 6 Learning Objectives 1. Depositing, writing, and endorsing checks for a checking account. 2. Reconciling a bank statement. 3. Establishing and replenishing

Your account charges explained COMMERCIAL BANKING

Your account charges explained COMMERCIAL BANKING Contents Help with queries 2 Keeping your charges low 2 Electronic Business Tariff 4 Business Extra Tariff 4 Other service charges for all tariffs 8 Business

Your account charges explained COMMERCIAL BANKING Contents Help with queries 2 Keeping your charges low 2 Electronic Business Tariff 4 Business Extra Tariff 4 Other service charges for all tariffs 8 Business

Platinum Balance Transfer

Platinum Balance Transfer Terms and Conditions These are the conditions of an agreement between us, TSB Bank plc of PO Box,16591, Birmingham B25 9GR, and: Name of customer: Address: ( you ) The credit

Platinum Balance Transfer Terms and Conditions These are the conditions of an agreement between us, TSB Bank plc of PO Box,16591, Birmingham B25 9GR, and: Name of customer: Address: ( you ) The credit

CREDIT CARD AGREEMENT REGULATED BY THE CONSUMER CREDIT ACT 1974

CREDIT CARD AGREEMENT REGULATED BY THE CONSUMER CREDIT ACT 1974 Between us, Creation Financial Services Limited, Chadwick House, Blenheim Court, Solihull B91 2AA and you, the Customer. KEY FINANCIAL INFORMATION

CREDIT CARD AGREEMENT REGULATED BY THE CONSUMER CREDIT ACT 1974 Between us, Creation Financial Services Limited, Chadwick House, Blenheim Court, Solihull B91 2AA and you, the Customer. KEY FINANCIAL INFORMATION

Business Current Account Price Plan Charges

Business Banking Business Current Account Price Plan Charges Details of business current account fees and charges, our Price Plan Guarantee and Loyalty Reward Price Plans to suit the way you do business

Business Banking Business Current Account Price Plan Charges Details of business current account fees and charges, our Price Plan Guarantee and Loyalty Reward Price Plans to suit the way you do business

Banking & Finance (145)

") Page 1 of 7 Contestant Number: Time: Rank: Banking & Finance (145) REGIONAL 2016 Multiple Choice: Multiple Choice (30 @ 2 points each) (60 points) Production Portion: Job 1: Complete a budget (30 @ 1 point

Page 1 of 7 Contestant Number: Time: Rank: Banking & Finance (145) REGIONAL 2016 Multiple Choice: Multiple Choice (30 @ 2 points each) (60 points) Production Portion: Job 1: Complete a budget (30 @ 1 point

Introduction to Depository Institutions

Introduction to Depository Institutions Advanced Level What is a Depository Institution? Depository institution businesses that provide financial services What is the name of one depository institution

Introduction to Depository Institutions Advanced Level What is a Depository Institution? Depository institution businesses that provide financial services What is the name of one depository institution

Using Banking Services

Presentation Slides $ Lesson Six Using Banking Services 04/09 banking terms you should know Account ATM Bank Checking account Credit union Interest Joint account Minimum deposit Savings account Teller

Presentation Slides $ Lesson Six Using Banking Services 04/09 banking terms you should know Account ATM Bank Checking account Credit union Interest Joint account Minimum deposit Savings account Teller

Business Activities Definitions

Business Activities s Mortgage First mortgage brokering Second mortgage brokering First mortgage lending Second mortgage lending First mortgage servicing Third party first mortgage servicing Subordinate

Business Activities s Mortgage First mortgage brokering Second mortgage brokering First mortgage lending Second mortgage lending First mortgage servicing Third party first mortgage servicing Subordinate

TERMS AND CONDITIONS

GREATER BUILDING SOCIETY LTD TERMS AND CONDITIONS PART 2 SCHEDULE OF FEES, CHARGES, TRANSACTIONAL LIMITS AND CONTACT DETAILS Dated: 1 October 2015 This document is Part 2 of the Terms and Conditions. The

GREATER BUILDING SOCIETY LTD TERMS AND CONDITIONS PART 2 SCHEDULE OF FEES, CHARGES, TRANSACTIONAL LIMITS AND CONTACT DETAILS Dated: 1 October 2015 This document is Part 2 of the Terms and Conditions. The

AMPLIFY CREDIT CARD. Business Conditions of Use.

AMPLIFY BUSINESS CREDIT CARD Business Conditions of Use. Effective Date: 30 May 2018 Your Credit Contract includes this Conditions of Use brochure, the letter which advises both your credit limit and other

AMPLIFY BUSINESS CREDIT CARD Business Conditions of Use. Effective Date: 30 May 2018 Your Credit Contract includes this Conditions of Use brochure, the letter which advises both your credit limit and other

BANKING & FINANCE (145)

") Page 1 of 10 Contestant Number: Time: Rank: BANKING & FINANCE (145) REGIONAL 2017 Multiple Choice: (30 @ 2 points each) (60 points) Financial Word Problems: (9 @ 2 points each) (18 points) Endorsements:

Page 1 of 10 Contestant Number: Time: Rank: BANKING & FINANCE (145) REGIONAL 2017 Multiple Choice: (30 @ 2 points each) (60 points) Financial Word Problems: (9 @ 2 points each) (18 points) Endorsements:

A bankers bank is an institution satisfying all of the following criteria:

Glossary This section provides definitions for terms in sections 1 and 2. These definitions are used for purposes of the FR 2900. They may differ from definitions that appear in other rules, regulations,

Glossary This section provides definitions for terms in sections 1 and 2. These definitions are used for purposes of the FR 2900. They may differ from definitions that appear in other rules, regulations,

Suncorp Bank Freedom Access Account

Suncorp Bank Freedom Access Account Product Information Document This document contains information on Suncorp Bank Freedom Access Account and related fees and charges. This document must be read in conjunction

Suncorp Bank Freedom Access Account Product Information Document This document contains information on Suncorp Bank Freedom Access Account and related fees and charges. This document must be read in conjunction

Welcome. 1. Agenda. 2. Ground Rules. 3. Introductions. Bank On It 2

Bank On It Welcome 1. Agenda 2. Ground Rules 3. Introductions Bank On It 2 Objectives Identify the major types of insured financial institutions Identify five reasons to use a bank Describe the steps involved

Bank On It Welcome 1. Agenda 2. Ground Rules 3. Introductions Bank On It 2 Objectives Identify the major types of insured financial institutions Identify five reasons to use a bank Describe the steps involved

Your account charges explained COMMERCIAL BANKING

Your account charges explained COMMERCIAL BANKING To ensure you have everything you need to know about our charges, this brochure has been designed to let you know when and how they will be applied. The

Your account charges explained COMMERCIAL BANKING To ensure you have everything you need to know about our charges, this brochure has been designed to let you know when and how they will be applied. The

Your account charges explained.

Your account charges explained. To ensure you have everything you need to know about our charges, this brochure has been designed to let you know when and how they will be applied. The charges and tariffs

Your account charges explained. To ensure you have everything you need to know about our charges, this brochure has been designed to let you know when and how they will be applied. The charges and tariffs

Experience business banking with more control.

Experience business banking with more control. Business Visa Debit Card User Guide. Welcome to an easier way of doing business, with the HSBC Business Visa Debit Card. Now you re in control of your business

Experience business banking with more control. Business Visa Debit Card User Guide. Welcome to an easier way of doing business, with the HSBC Business Visa Debit Card. Now you re in control of your business

General guidelines on payment statistics

Payment statistics Deutsche Bundesbank Statistics Guidelines February 2016 General guidelines on payment statistics I Focus of the data collection and definitions This collection of payment statistics

Payment statistics Deutsche Bundesbank Statistics Guidelines February 2016 General guidelines on payment statistics I Focus of the data collection and definitions This collection of payment statistics

ELECTRONIC FUND TRANSFERS DISCLOSURE. and MOBILE BANKING AGREEMENT YOUR RIGHTS AND RESPONSIBILITIES IMPORTANT! IF YOU DISCOVER YOUR

ELECTRONIC FUND TRANSFERS DISCLOSURE and MOBILE BANKING AGREEMENT YOUR RIGHTS AND RESPONSIBILITIES IMPORTANT! IF YOU DISCOVER YOUR VISA DEBIT CARD OR MAC CARD IS LOST OR STOLEN, PLEASE REPORT IT IMMEDIATELY

ELECTRONIC FUND TRANSFERS DISCLOSURE and MOBILE BANKING AGREEMENT YOUR RIGHTS AND RESPONSIBILITIES IMPORTANT! IF YOU DISCOVER YOUR VISA DEBIT CARD OR MAC CARD IS LOST OR STOLEN, PLEASE REPORT IT IMMEDIATELY

Freedom Access Account

Freedom Access Account Product Information Document Effective Date: 01 March 2018 This document contains information on Suncorp Bank Freedom Access Account and related fees and charges. This document must

Freedom Access Account Product Information Document Effective Date: 01 March 2018 This document contains information on Suncorp Bank Freedom Access Account and related fees and charges. This document must

BMW Credit (Malaysia) Sdn. Bhd. (Company No D)

Sdn. Bhd. (Company No D)") BMW Credit (Malaysia) Sdn. Bhd. (Company No. 75342-D) Dear Valued Customer, This document illustrates the payment options and guide in servicing your loan payments with BMW Credit (Malaysia) Sdn. Bhd.

BMW Credit (Malaysia) Sdn. Bhd. (Company No. 75342-D) Dear Valued Customer, This document illustrates the payment options and guide in servicing your loan payments with BMW Credit (Malaysia) Sdn. Bhd.

ACCOUNT CHARGES. Your account charges explained

ACCOUNT CHARGES Your account charges explained June 2017 Account charges To put your business in greater control we d like to fully explain your business banking fees. Here we ll outline how our charges

ACCOUNT CHARGES Your account charges explained June 2017 Account charges To put your business in greater control we d like to fully explain your business banking fees. Here we ll outline how our charges

Important Information. Changes to our Terms

Important Information Changes to our Terms Important changes at a glance From 1 June 2013 we ll be making some changes to our Terms. We ve highlighted some of the changes below and you ll find more detailed

Important Information Changes to our Terms Important changes at a glance From 1 June 2013 we ll be making some changes to our Terms. We ve highlighted some of the changes below and you ll find more detailed

THE METHODOLOGY OF REPORTING PAYMENT INSTRUMENTS

THE METHODOLOGY OF REPORTING PAYMENT INSTRUMENTS I. INTRODUCTION Based on the Law on Payment System, Article 8, and on the Regulation on Payment Instruments Statistics, and in order to fullfill its public

THE METHODOLOGY OF REPORTING PAYMENT INSTRUMENTS I. INTRODUCTION Based on the Law on Payment System, Article 8, and on the Regulation on Payment Instruments Statistics, and in order to fullfill its public

Welcome to Money Essentials SM!

Money Essentials SM Welcome to Money Essentials SM! Money Essentials provides you with a valuable, easy to understand introduction to financial services and is designed to give you realistic choices in

Money Essentials SM Welcome to Money Essentials SM! Money Essentials provides you with a valuable, easy to understand introduction to financial services and is designed to give you realistic choices in

List of Terms and Conditions for Corporate Banking Page 1

Deutsche Bank Page 1 Accounts, Information Service Charging Terms Price Account Terms HUF/ Account Opening Per Free of charge Account Maintenance (incl. electronic reporting - Per month, per 25,00* MT940

Deutsche Bank Page 1 Accounts, Information Service Charging Terms Price Account Terms HUF/ Account Opening Per Free of charge Account Maintenance (incl. electronic reporting - Per month, per 25,00* MT940

Checking 101 Checking Out Checking Accounts

Checking 101 Checking Out Checking Accounts Checking 101 Checking Account Basics A check is a written order that represents cash Credit Union checking accounts are also called SHARE DRAFT accounts A share

Checking 101 Checking Out Checking Accounts Checking 101 Checking Account Basics A check is a written order that represents cash Credit Union checking accounts are also called SHARE DRAFT accounts A share

Chapter 12 Consumption Credit

Consumption Credit CCP-CC 12-1 Chapter 12 Consumption Credit Content Outline 1. Personal Loan... 12-2 2. Personal Overdraft... 12-4 3. Credit Cards... 12-6 Practice Questions... 12-11 Learning Objectives

Consumption Credit CCP-CC 12-1 Chapter 12 Consumption Credit Content Outline 1. Personal Loan... 12-2 2. Personal Overdraft... 12-4 3. Credit Cards... 12-6 Practice Questions... 12-11 Learning Objectives

Banking & Finance (145)

") Page 1 of 7 Contestant Number: Time: Rank: Banking & Finance (145) REGIONAL 2016 Multiple Choice: Multiple Choice (30 @ 2 points each) (60 points) Production Portion: Job 1: Complete a budget (30 @ 1 point

Page 1 of 7 Contestant Number: Time: Rank: Banking & Finance (145) REGIONAL 2016 Multiple Choice: Multiple Choice (30 @ 2 points each) (60 points) Production Portion: Job 1: Complete a budget (30 @ 1 point

Business Current Account FSB Tariff

Business Current Account FSB Tariff This tariff details the services, rates and charges that are effective from 19 July 2017. We can vary or amend this tariff at any time, but will notify customers when

Business Current Account FSB Tariff This tariff details the services, rates and charges that are effective from 19 July 2017. We can vary or amend this tariff at any time, but will notify customers when

General Tariff for Fusion Customers Issue Date: August 2018

General Tariff for Fusion Customers Issue Date: August 2018 Tariff applies on accounts, facilities, services and transactions used/made for business purposes only. 2 Issue Date: August 2018 Contents General

General Tariff for Fusion Customers Issue Date: August 2018 Tariff applies on accounts, facilities, services and transactions used/made for business purposes only. 2 Issue Date: August 2018 Contents General

Swedish Bankers Association 15 April 2003 Debit Advice. Business Transaction DEBIT ADVICE. Rev

Business Transaction DEBIT ADVICE Rev 2003-04-15 Swedish Bankers Association Svenska Bankföreningen aftdeb-e.xxx 16 December 1997, Ver 2.0 Page 1 1. Functional Definition A Debit Advice is used to advise

Business Transaction DEBIT ADVICE Rev 2003-04-15 Swedish Bankers Association Svenska Bankföreningen aftdeb-e.xxx 16 December 1997, Ver 2.0 Page 1 1. Functional Definition A Debit Advice is used to advise

Expenses made easy with Visa Business cards

Expenses made easy with Visa Business cards Visa Business card and Gold Visa Business card This document is important and should be read Guidance on our credit card facilities We apply lending criteria

Expenses made easy with Visa Business cards Visa Business card and Gold Visa Business card This document is important and should be read Guidance on our credit card facilities We apply lending criteria

The Consumer Protection Regulations

1 The Consumer Protection Regulations Repealed by Chapter C-30.1 Reg 2 (effective October 15, 2007). Formerly Chapter C-30.1 Reg 1 (effective January 1, 1997) as amended by Saskatchewan Regulations 65/2005.

1 The Consumer Protection Regulations Repealed by Chapter C-30.1 Reg 2 (effective October 15, 2007). Formerly Chapter C-30.1 Reg 1 (effective January 1, 1997) as amended by Saskatchewan Regulations 65/2005.

Fees. A guide to personal account fees

Fees A guide to personal account fees We re committed to helping you get the most out of your account which includes making you aware of the charges and rates of interest that apply to your account. It

Fees A guide to personal account fees We re committed to helping you get the most out of your account which includes making you aware of the charges and rates of interest that apply to your account. It

Chapter 12. Banking Procedures and Services Pearson Education, Inc. All rights reserved

Chapter 12 Banking Procedures and Services 2010 Pearson Education, Inc. All rights reserved Learning Objectives Explain the difference between different types of financial institutions Learn the basics

Chapter 12 Banking Procedures and Services 2010 Pearson Education, Inc. All rights reserved Learning Objectives Explain the difference between different types of financial institutions Learn the basics

Business Banking Fees and Limits

Business Banking Fees and Limits Effective 1 March 2018 What s Inside Here. 1 Our fees 2 Transaction account, savings accounts and investments 9 International accounts and services 11 Business lending

Business Banking Fees and Limits Effective 1 March 2018 What s Inside Here. 1 Our fees 2 Transaction account, savings accounts and investments 9 International accounts and services 11 Business lending

Effective Date: 1 March Corporate MasterCard. Conditions of Use

Effective Date: 1 March 2010 Corporate MasterCard Conditions of Use Corporate MasterCard Card account Conditions of Use St.George Bank This document does not contain all the terms of the agreement applicable

Effective Date: 1 March 2010 Corporate MasterCard Conditions of Use Corporate MasterCard Card account Conditions of Use St.George Bank This document does not contain all the terms of the agreement applicable

General Service Fees. Withdrawal Transaction Fees

Withdrawal Transaction Fees Agency Cash Withdrawal Payable whenever a cash withdrawal is processed at a PCU agency. $2.50 rediatm Cash Withdrawal Including NAB ATMS. Payable whenever a cash withdrawal

Withdrawal Transaction Fees Agency Cash Withdrawal Payable whenever a cash withdrawal is processed at a PCU agency. $2.50 rediatm Cash Withdrawal Including NAB ATMS. Payable whenever a cash withdrawal

FNB Global Accounts. Terms & Conditions

FNB Global Accounts Terms & Conditions These Terms and Conditions must be read in conjunction with FNB Forex Terms and Conditions and FNB General Terms and Conditions that apply to your banking relationship

FNB Global Accounts Terms & Conditions These Terms and Conditions must be read in conjunction with FNB Forex Terms and Conditions and FNB General Terms and Conditions that apply to your banking relationship

Lending Fees and Charges. Effective from 12 November 2016

Lending Fees and Charges Effective from 12 November 2016 2 Suncorp Bank About this brochure These fees and charges are applicable at the time of printing and are subject to change. We recommend you confirm

Lending Fees and Charges Effective from 12 November 2016 2 Suncorp Bank About this brochure These fees and charges are applicable at the time of printing and are subject to change. We recommend you confirm

Decree No. 21/2006 (XI. 24.) of the Governor of the MNB. on carrying out payment transactions

of the Governor of the MNB. on carrying out payment transactions") Decree No. 21/2006 (XI. 24.) of the Governor of the MNB on carrying out payment transactions Pursuant to the authorisation defined in Article 60 (1) ha) of Act LVIII of 2001 on the Magyar Nemzeti Bank,

Decree No. 21/2006 (XI. 24.) of the Governor of the MNB on carrying out payment transactions Pursuant to the authorisation defined in Article 60 (1) ha) of Act LVIII of 2001 on the Magyar Nemzeti Bank,

General Tariff. Issue Date: April 2017

Current and Savings Accounts Cheques returned unpaid by us Refer to Drawer 25.00 per cheque Any other reason 5.00 per cheque Stopped Cheques (applicable whether stop instructions are for one cheque or

Current and Savings Accounts Cheques returned unpaid by us Refer to Drawer 25.00 per cheque Any other reason 5.00 per cheque Stopped Cheques (applicable whether stop instructions are for one cheque or

Cardholder Agreement for Mastercard Business Cards issued by National Bank of Canada

Cardholder Agreement for Mastercard Business Cards issued by National Bank of Canada Table of contents 1. Definitions 2. Your acceptance of this agreement 3. Use of credit card account 4. Credit limit

Cardholder Agreement for Mastercard Business Cards issued by National Bank of Canada Table of contents 1. Definitions 2. Your acceptance of this agreement 3. Use of credit card account 4. Credit limit

ACCOUNT CHARGES. Your account charges explained

ACCOUNT CHARGES Your account charges explained June 2018 Account charges To put your business in greater control we d like to fully explain your business banking fees. Here we ll outline how our charges

ACCOUNT CHARGES Your account charges explained June 2018 Account charges To put your business in greater control we d like to fully explain your business banking fees. Here we ll outline how our charges

Personal Financial Services Fees and Charges. with effect from 1 December 2008

Personal Financial Services Fees and Charges with effect from 1 December 2008 About this Guide At HSBC we want to make it easy for you to know what fees and charges apply to the HSBC financial services

Personal Financial Services Fees and Charges with effect from 1 December 2008 About this Guide At HSBC we want to make it easy for you to know what fees and charges apply to the HSBC financial services

FarmHouse International Fraternity New Member Education Program Topic Summary: Personal Finance

FarmHouse International Fraternity New Member Education Program Topic Summary: Personal Finance 11 College is a challenging time both in and out of class. As a student you are coping with a new environment

FarmHouse International Fraternity New Member Education Program Topic Summary: Personal Finance 11 College is a challenging time both in and out of class. As a student you are coping with a new environment

List of Fees ENTREPRENEURS AND SMALL COMPANIES. Turnover up to CZK 25 Million

List of Fees ENTREPRENEURS AND SMALL COMPANIES Turnover up to 25 Million Valid from 7/7/2016 Table of Contents 1. Day-to-Day Banking 02 1.1 Current Accounts 02 1.2 Escrow Accounts 02 1.3 Professional accounts

List of Fees ENTREPRENEURS AND SMALL COMPANIES Turnover up to 25 Million Valid from 7/7/2016 Table of Contents 1. Day-to-Day Banking 02 1.1 Current Accounts 02 1.2 Escrow Accounts 02 1.3 Professional accounts

Topic 2: Compare different types of payment card

Topic 2: Compare different types of payment card After completing this topic, you will be able to: define, understand the purpose of, and compare the features of debit and credit cards; define, understand

Topic 2: Compare different types of payment card After completing this topic, you will be able to: define, understand the purpose of, and compare the features of debit and credit cards; define, understand

Rs 10 + VAT per month, i.e. Rs per month 4Debit interest on unauthorised overdrawn balances

Account Access Services Internet Banking 4Subscription fee 4Security Token - First acquisition/ replaced device per device 4Dispatch charges Rs 550 Mobile Banking 4Mobile Internet Banking 4SMS ReFill service

Account Access Services Internet Banking 4Subscription fee 4Security Token - First acquisition/ replaced device per device 4Dispatch charges Rs 550 Mobile Banking 4Mobile Internet Banking 4SMS ReFill service

ANZ PERSONAL BANKING

ANZ PERSONAL BANKING ACCOUNT FEES AND CHARGES 06.02.2018 Thank you for banking with ANZ. We are proud of our products, and believe they are amongst the best in the industry. Many have received industry

ANZ PERSONAL BANKING ACCOUNT FEES AND CHARGES 06.02.2018 Thank you for banking with ANZ. We are proud of our products, and believe they are amongst the best in the industry. Many have received industry

ACCOUNT CHARGES. Your account charges explained

ACCOUNT CHARGES Your account charges explained March 2018 Account charges To put your business in greater control we d like to fully explain your business banking fees. Here we ll outline how our charges

ACCOUNT CHARGES Your account charges explained March 2018 Account charges To put your business in greater control we d like to fully explain your business banking fees. Here we ll outline how our charges

BULLETIN ON PAYMENT SERVICE

1 st. May 2018 This bulletin contains general advance information on payment services which the Bank must provide to a consumer customer before entering into a master agreement (hereinafter the "Bulletin

1 st. May 2018 This bulletin contains general advance information on payment services which the Bank must provide to a consumer customer before entering into a master agreement (hereinafter the "Bulletin

Personal Banking. Account Fees

Personal Banking Account Fees Contents 1. Introduction 1 2. Monthly account fees 1 3. Arranged overdraft interest 2 4. Arranged overdraft, unarranged overdraft and unpaid transaction fees 3 5. Debit card

Personal Banking Account Fees Contents 1. Introduction 1 2. Monthly account fees 1 3. Arranged overdraft interest 2 4. Arranged overdraft, unarranged overdraft and unpaid transaction fees 3 5. Debit card

Conditions of Use and Credit Guide

Conditions of Use and Credit Guide Effective December 2017 Credit Guide Latitude Finance Australia ABN 42 008 583 588 ( Latitude ), Australian Credit Licence Number 392145. This credit guide gives you

Conditions of Use and Credit Guide Effective December 2017 Credit Guide Latitude Finance Australia ABN 42 008 583 588 ( Latitude ), Australian Credit Licence Number 392145. This credit guide gives you

PRICE LIST OF PRODUCTS AND SERVICES FOR ENTREPRENEURS AND LEGAL ENTITIES PART 1

PRICE LIST OF PRODUCTS AND SERVICES FOR ENTREPRENEURS AND LEGAL ENTITIES PART 1 We are continuously developing our services. Thus, for better orientation, our price list is split into two parts. The first

PRICE LIST OF PRODUCTS AND SERVICES FOR ENTREPRENEURS AND LEGAL ENTITIES PART 1 We are continuously developing our services. Thus, for better orientation, our price list is split into two parts. The first

Business Banking/Savings application form

Business Banking Page 1 of 12 Business Banking/Savings application form For use by Sole Traders, Partnerships, LLP s, Limited Companies, Charities, Clubs, Societies and Unincorporated Associations This

Business Banking Page 1 of 12 Business Banking/Savings application form For use by Sole Traders, Partnerships, LLP s, Limited Companies, Charities, Clubs, Societies and Unincorporated Associations This

Report S 3.2 «Non-balance sheet information» Banque centrale du Luxembourg

In case of discrepancies between the French and the English text, the French text shall prevail Report S 3.2 «Non-balance sheet information» Banque centrale du Luxembourg Contents 1 Introduction...3 1.1

In case of discrepancies between the French and the English text, the French text shall prevail Report S 3.2 «Non-balance sheet information» Banque centrale du Luxembourg Contents 1 Introduction...3 1.1

Schedule of Charges for Business Customers

Schedule of Charges for Business Customers Northern Ireland Effective December 2018 1. Transaction Fees on Business Accounts Transaction and account maintenance fees are payable on all business current

Schedule of Charges for Business Customers Northern Ireland Effective December 2018 1. Transaction Fees on Business Accounts Transaction and account maintenance fees are payable on all business current

Effective from: 30 th April 2014 (1404) Published on 30 th April 2014

Published on 30 th April 2014") Effective from: 30 th April 2014 (1404) Published on 30 th April 2014 For a company group s 1 employees 2 if at least 1500 employees of the group open an account with the bank within 1.5 years if the group

Effective from: 30 th April 2014 (1404) Published on 30 th April 2014 For a company group s 1 employees 2 if at least 1500 employees of the group open an account with the bank within 1.5 years if the group

DEFINITIONS. An authorized charge can be made over the telephone, in person, on the Internet, or in any other way that your account can be used.

DEFINITIONS Address on file Your address on file is the address that you provided on your application to open this credit card account, unless: (1) we have received and processed your written notice of

DEFINITIONS Address on file Your address on file is the address that you provided on your application to open this credit card account, unless: (1) we have received and processed your written notice of

Guidelines for the issue of Smart / Debit Cards by banks

Guidelines for the issue of Smart / Debit Cards by banks FSC.BC. 123 /24.01.019/99-2000 November 12,1999 All Scheduled Commercial Banks (excluding RRBs) Dear Sir, Guidelines for the issue of Smart / Debit

Guidelines for the issue of Smart / Debit Cards by banks FSC.BC. 123 /24.01.019/99-2000 November 12,1999 All Scheduled Commercial Banks (excluding RRBs) Dear Sir, Guidelines for the issue of Smart / Debit