LIA Credit Union Seminar

|

|

|

- Philippa Nash

- 5 years ago

- Views:

Transcription

1 LIA Credit Union Seminar Designed for you 26 th July

2 Pat O Sullivan LIA Chief Executive

3 Adding Value through Risk Management Justin McCarthy

4 Justin McCarthy Justin McCarthy has worked in roles in many firms, including Bank of America Merrill Lynch, PricewaterhouseCoopers and with the Irish Financial Regulator. This work has allowed him to see the changes in risk management since through and beyond the recent global financial crisis. His work on the PRISM risk based supervision framework with the Irish Regulator included exposure to banking, funds and insurance risk practices as well as the quantitative work done on the related impact models and the challenge in feeding valid financial data to these models. Justin McCarthy mccarthy/ He is Chair of the Global Board of the Professional Risk Managers' International Association (PRMIA). This is a professional body and education organisation for risk managers globally and has a network of over 50,000 around the world. He works as a Strategy, Governance, Risk and Compliance Consultant as well as lecturing and training. He works with a range of credit unions across the country as the risk and / or compliance functions and other work such as writing strategic plans. He also works with other financial services providers such as large banks. In 2017, he spent 6 months working with the Risk Leadership Team at Ulster Bank. Justin has a BSc from University College Cork and an MBA from the Michael Smurfit Graduate School of Business at University College Dublin. He is originally from Schull, west Cork.

5 Risk Management What do you think? Is this a topic worth discussing anymore?

6 Asking another audience What risk is there with this?

7 Actually it wasn t that bad

8 So Let s Try and Keep Risk Interesting

9 Things we all know: Risk Assessment Overview How do we best go about Identifying, Assessing and Monitoring risk? Top-down: E.g. Scenarios Bottom-Up: E.g. Process mapping Top-down: Capture risks that may not be found in a walk-through of processes Cross reference between both approaches Bottom-up: Capture risks as they are seen by the people that are working with the related processes

10 Things we all know: Risk Assessment Overview Questions that should be answered by a well designed risk assessment programme are: What are our top risks in rank order? What is the state of the controls that we have in place to deal with those risks? Are there control gaps? What are we going to do about the gaps? Who will own the action plans to address the gaps? What have we learned that we can apply to the next risk assessment cycle? How do we get people to Buy-in to this approach this is admitting to issues in your business: High level support / sponsorship? Briefing / Education sessions? Applying some kind of capital?

11 Things we all know: Connect the Data Board Management Summary Reports Data in the Credit Union: System Risk Management System Ledgers Spreadsheets

12 Things we all know: The Risk Register? Risk Category Risk Sub Category Risk.. Inherent Risk Credit Risk Credit Risk Credit Risk Credit Risk Credit / Underwriting Risk Credit Concentration Risk Credit / Underwriting Risk Credit / Underwriting Risk Inadequate verification of member's net disposable income Inadequate risk concentration limits on overall lending Loans are made to members who currently have arrears Related party loans are not properly approved Operational Risk IT Risk Risk that a server runs out of warranty Operational Risk IT Risk Disruption to operations and financial loss when a computer virus infects the IT system Operational Risk IT Risk Risk that log-in usernames/ passwords are not sufficiently controlled Is this useful from a Top Down as well as a Bottom Up view of your risks?

13 Things we all know: The Risk Register? These can get really detailed!

14 Collating our Risks IT Risk Cyber Risk IT Resiliance Risk that the Website is Hacked Risk that we are the victim of a "Phishing Attack" Risk that internal / external network is down Risk that the web server fails If we are told IT is one of our main risks, can we drill down into the detail?

15 PRISM already did this in 2011

16 Just Collate it up Get your Top 10 Risks Risk Sub Category Inherent Impact Inherent Probability Business Model Interest Rate Risk Board and Committee Quality Credit Control Anti-Money Laundering Succession Planning Strategic Plan Implementation Strategic Planning Data Protection Internal Fraud

17 Now talk about Risk

18 Make it More Visual if that Helps A picture paints a thousand words

19 Talking the Risk Language? Our Top 5 Risks? I don t know I guess IT is a risk maybe we should get new computers and a website? Have you seen that we have a risk register? It s in there I guess?

20 Talking the Risk Language! Our Top Risk is the business model and thus the viability of the credit union our projections are for a good surplus for the next 3 years. We review the related KPIs at the monthly board meeting. Our top operational risk is cyber risk but we are mitigating this with our IT security programme and the residual risk is within our risk appetite for that area.

21 Talking the Risk Language

22 Example: Operational Risk Taxonomies Much more detail is available to us in the Basel table

23 Example: Operational Risk Taxonomies Level 3 detail can help drive discussion on operational risk

24 Now talk about Risk But wait Have we really been Managing Risk?

25 Our Biggest Risk If we can t show we have a strategy / business model to make a surplus, then the CBI may take action

26 Have That Conversation

27 Questions? Thank you

28 Credit / Underwriting Processes Andrew Donovan Strategus

29 Andrew Donovan Background Summary Extensive financial experience spanning a 30 year career in financial services, Business Development, Debt Recovery, Commercial & Retail Banking with particular experience in process improvement, productivity initiatives and lean processes for financial institutions. Work Experience Worked in AIB Bank, Anglo Irish Bank, Ulster Bank & ACC / Rabo-Bank before commencing consultancy Work in June 2017 Key Skills include: Business Development, Credit Risk Management, Debt Collection, Negotiating, Management, Team Management & Analysis and implementation of Lean Processes.

30 The areas I hope to cover this morning: Lending position as it currently exists PRISM reports and concern & Addressing Central Bank Concerns Lending and underwriting going forward. How to get more from existing resources.

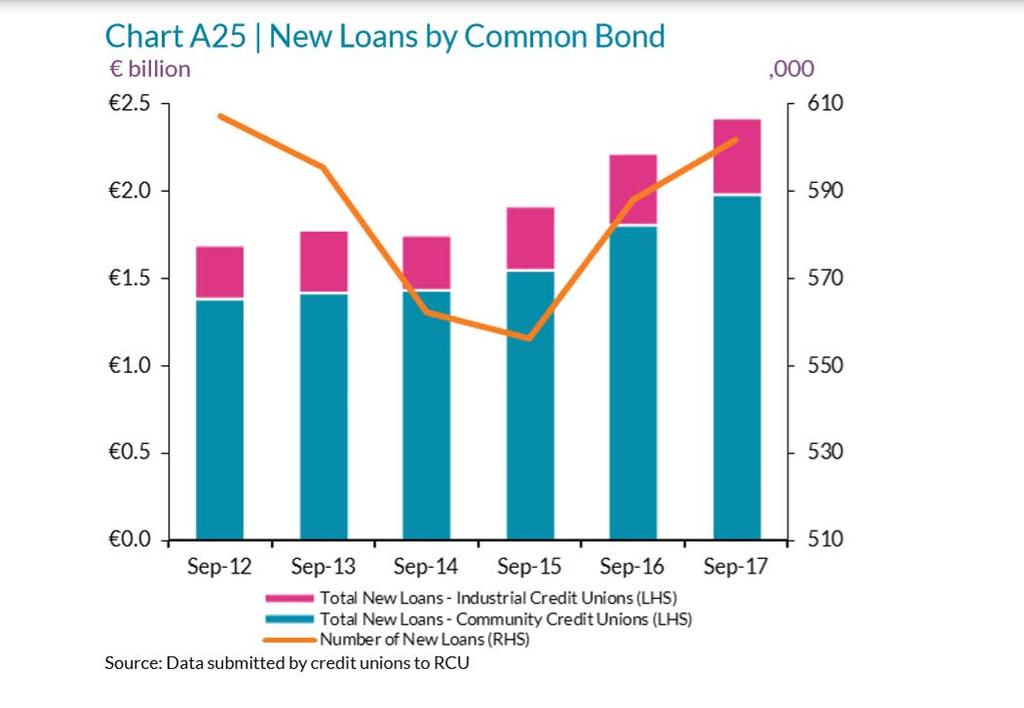

31 Lending position as it currently exists. Want to have a look at a number of charts from the Central Bank

32

33

34

35

36

37

38

39 Looking back over the last 5 years what can we say: Credit Unions have held their share of the personal loan market. The average size of loan has increased slightly & heading in the right direction. The average length of loan is growing slowly but needs to lengthen. Still over 94% of Credit Union loans are personal. The volume and number of new loans has been growing since The excellent work on arrears continues to be evident.

40 PRISM reports on Lending & Risk Management and concern. Addressing Central Bank Concerns.

41 Given the importance of lending to the overall business model of credit unions of all sizes, we expect high standards of credit risk management from a prudential perspective. In order to satisfactorily manage and mitigate credit risk, credit unions must ensure that credit assessment processes are based on coherent and clearly defined criteria, the process of approving and amending loans is clearly defined and documented in credit policies and that the credit process is consistently implemented

42 CBI expectations of prudent lending include the following: 1. The member s ability to repay shall be the primary consideration in the underwriting process and Credit Unions must satisfy themselves that they are fully appraised of the borrower s financial position before granting a loan. 2. Comprehensive credit policies, reflecting the range of lending undertaken by the credit union. 3. Supporting rationale must be clearly documented with lending decisions. The decision to grant or deny a loan should be supported by a suitably detailed rationale.

43 A number of recurring risk issues were apparent in their engagements: 1. Weaknesses in underwriting practices, including lack of supporting rationale for loan approval. Failure to include such rationale makes it difficult to evidence and understand why certain loans were approved. 2. Failure to accurately assess member repayment capacity / debt-to-income ratios. We noted discrepancies and differences in approach as to how these ratios are calculated, or failure to consider the thresholds for such ratios, as per the approved policy of the credit union. 3. Incomplete or missing documentation on file in relation to the assessment of member s income and outgoings, including examples of missing member account statements, no evidence of income verification or analysis of income and outgoings as part of the underwriting process. 4. Evidence of top-up loans being issued to members, without appropriate consideration of the potential risky nature of this lending and the potential effects on member's overall indebtedness.

44 Supervision Loan Assessment Training Policy Process Procedure People

45 Lending policy, process & procedure Do this we need to understand the difference in the three: Policy vs. Process vs. Procedure A policy is a rule, regulation, or set of guidelines. A process is a high level set of things that must happen outlining what must happen in order to ensure compliance with a policy. A procedure is a specific, detailed series of actions that staff members must take in order to implement a process and comply with a policy.

46 Good Quality Supervision Loan Assessment Training Procedures Processes Policy People

47 Lending and underwriting going forward

48 What are our needs going forward? To increase income Expand offering Better use of IT People

49 What this means for our Business Opportunities Risks

50 Opportunities Increase the amount of our average loan Increase the length of the average loan Increase offering of Loan types Spread risk Widen who we deal with

51 Risks Cost Sectoral Knowledge Underwriting Issues Concentration levels Ongoing Management Staff IT

52 How do we mitigate these risks? Make sure we have a solid core to build on Plan meticulously for whatever expansion we choose Review our performance against the plan on a continuous basis Don t be rigid.

53 Conclusion Increasingly, it is expected that credit unions will proceed with product opportunities that can demonstrably add to earnings, if not immediately, over a reasonable timeframe. It is expected that credit unions boards and management will consider all the risks to which they will be exposed. It is their responsibility to ensure that they can demonstrate they understand the financial and other risks and to have the appropriate systems and processes in place to manage and control those risks, prior to undertaking such business. The Central Bank

54 How to get more from existing resources.

55 First identify then, Eliminate Waste The Lean Concept

56

57 Radical Transformation of Collections Challenge Transform the performance and Management information of the credit arrears process while meeting the Banks KPI s and Central Banks codes. Solution Reviews the efficiency and effectiveness of the current process using lean methods and created a desired future state. Solutions presented where significant Improvements and Efficiencies could be achieved in Reviews Management and Collections. 25% Ensured Reduction in Task Time Highlights Milestone Based Approach Clear Timelines Measurable KPI s Standard Work Improved Collections 100% Compliance Central Bank Requirements 18% Cases Managed on-time 60% Process Time

58 Thank you

59 Networking

60 Credit Union Investments - Regulations, Risks & Returns Padraig O Sullivan

61 Topics to be covered Why are investments important for credit unions? Regulations - what investments can credit unions make? How to assess risk Why are investment returns so low? Outlook for investment returns

62 Why are Investments Important? Total Credit Union Assets: Total Credit Union Investments: 15bn 10bn

63 Why so much in Investments? The excess of shares over loans Since crash, people save more & borrow less Common to all credit unions and banks CU must try earn some return on these funds

64 Investment Regulations Strict regulations covering investments Types of Investments (investment classes) Who to invest with (investment counterparties) How long to invest for

65 Key Factor

66 CU Investment Regulations Permitted investment classes (since March 2018) a) Government Bonds of a euro zone country b) Supranational Bonds c) Bank Deposits d) Bank Bonds (senior bonds only) e) Corporate Bonds f) Approved Housing Bodies (via regulated entity) g) UCITS (i.e. funds) h) Shares/deposits in another credit union i) Shares of a society

67 In Summary 1. Bank Deposits (Approx. 75% of CU investments) 2. Bonds issued by governments, banks & large corporates (25%) Must be capital guaranteed Can t invest for longer than 10 years No more than 20% with any counterparty (less for corporates) Euro investments only

68 Risk Regulations exclude any high-risk investments But all investments carry some risk Obligation on board/investment committee to assess risk Key investment risk for CU s Counterparty Risk A guarantee is only as good as the party providing it Who are you giving our money to? How secure are they? What is their credit rating?

69 Credit Ratings Credit Rating Capacity to Repay Grade AAA Extremely strong Investment AA Very strong Investment A Strong Investment BBB Adequate Investment BB Faces major future uncertainties Speculative B Faces major uncertainties Speculative CCC Currently vulnerable Speculative CC Currently highly vulnerable Speculative C Has filed bankruptcy petition Speculative D In default Speculative

70 Investment Returns Year Rate of Return (sample CU) % % % % % (approx.) All CU s have seen significant fall in investment income

71 Why are interest rates so low? People saving more and borrowing less Too much money in the financial system ECB adding more via Quantitative Easing (QE) i.e. pumping even more money into the system ECB trying to keep rates at rock bottom Encouraging people to save less and spend more

72 3-Month Euribor % Historic & Projected 3 Month Euribor 5.00% 4.00% 3.00% 2.00% July % 1.00% 0.00% -1.00%

73 Are low interest rates here to stay? Euro zone interest rates largely controlled by the ECB Strong economic growth needed before it raises rates In particular, it will want to see higher inflation Target inflation rate 2%, currently only 1% ( core rate) Inflation needs to rise if interest rates are to recover

74 3-Month Euribor % Historic & Projected 3 Month Euribor 5.00% 4.00% 3.00% 2.00% July % 1.00% 0.00% -1.00%

75 3-Month Euribor % Historic & Projected 3 Month Euribor 5.00% 4.00% 3.00% 2.00% July % 1.00% 0.00% -1.00%

76 6.00% Historic & Projected 3-Month Euribor Historic & Projected 3 Month Euribor 5.00% 4.00% 3.00% 2.00% July % Market Projections 1.00% 0.00% -1.00%

77 Summary Interest rates at historic lows Probably not going lower, but recovery will be slow Likely to be several years before any major pickup in CU investment income No quick fix, unfortunately!

78 Questions? Thank you

Risk Management in Regulatory Frameworks Justin McCarthy Chair, Global Board of Directors, Professional Risk Managers' International Association

Risk Management in Regulatory Frameworks Justin McCarthy Chair, Global Board of Directors, Professional Risk Managers' International Association 20-22 February - Meeting of the UNECE GRM Group - Geesthacht

Risk Management in Regulatory Frameworks Justin McCarthy Chair, Global Board of Directors, Professional Risk Managers' International Association 20-22 February - Meeting of the UNECE GRM Group - Geesthacht

PRISM Supervisory Commentary 2018

PRISM Supervisory Commentary 2018 March 2018 Page 2 PRISM Supervisory Commentary 2018 Central Bank of Ireland Table of Contents 1. Foreword... 3 2. Executive Summary... 4 3. Background... 8 4. Overview

PRISM Supervisory Commentary 2018 March 2018 Page 2 PRISM Supervisory Commentary 2018 Central Bank of Ireland Table of Contents 1. Foreword... 3 2. Executive Summary... 4 3. Background... 8 4. Overview

Capital Requirements Directive Pillar 3 Disclosures For the year ended 31 August 2017

Capital Requirements Directive Pillar 3 Disclosures For the year ended 31 August 2017 Contents INTRODUCTION... 2 RISK MANAGEMENT POLICIES AND OBJECTIVES... 3 BOARD & SUB-COMMITTEES... 3 THREE LINES OF

Capital Requirements Directive Pillar 3 Disclosures For the year ended 31 August 2017 Contents INTRODUCTION... 2 RISK MANAGEMENT POLICIES AND OBJECTIVES... 3 BOARD & SUB-COMMITTEES... 3 THREE LINES OF

ULSTER UNIVERSITY TREASURY MANAGEMENT POLICY

ULSTER UNIVERSITY TREASURY MANAGEMENT POLICY DOCUMENT CONTROL Document Title Treasury Management Policy Document Version V2.0 Custodian Chief Finance Officer Author Head of Financial Management Approving

ULSTER UNIVERSITY TREASURY MANAGEMENT POLICY DOCUMENT CONTROL Document Title Treasury Management Policy Document Version V2.0 Custodian Chief Finance Officer Author Head of Financial Management Approving

CREDIT RATING INFORMATION & SERVICES LIMITED

Rating Methodology INVESTMENT COMPANY CREDIT RATING INFORMATION & SERVICES LIMITED Nakshi Homes (4th & 5th Floor), 6/1A, Segunbagicha, Dhaka 1000, Bangladesh Tel: 717 3700 1, Fax: 956 5783 Email: crisl@bdonline.com

Rating Methodology INVESTMENT COMPANY CREDIT RATING INFORMATION & SERVICES LIMITED Nakshi Homes (4th & 5th Floor), 6/1A, Segunbagicha, Dhaka 1000, Bangladesh Tel: 717 3700 1, Fax: 956 5783 Email: crisl@bdonline.com

Capital Requirements Directive. Pillar 3 Disclosures

Capital Requirements Directive Pillar 3 Disclosures For the year ended 31 August 2016 INDEX Page INTRODUCTION 2 RISK MANAGEMENT POLICIES AND OBJECTIVES 3 CAPITAL ADEQUACY ASSESSMENT, CAPITAL RESOURCES

Capital Requirements Directive Pillar 3 Disclosures For the year ended 31 August 2016 INDEX Page INTRODUCTION 2 RISK MANAGEMENT POLICIES AND OBJECTIVES 3 CAPITAL ADEQUACY ASSESSMENT, CAPITAL RESOURCES

1.1. Low yield environment

1. Key developments The overall macroeconomic environment remains very challenging for the European insurance and pension sector. The yields have been further compressed and are substantially below the

1. Key developments The overall macroeconomic environment remains very challenging for the European insurance and pension sector. The yields have been further compressed and are substantially below the

Sainsbury s Bank plc. Pillar 3 Disclosures for the year ended 31 December 2008

Sainsbury s Bank plc Pillar 3 Disclosures for the year ended 2008 1 Overview 1.1 Background 1 1.2 Scope of Application 1 1.3 Frequency 1 1.4 Medium and Location for Publication 1 1.5 Verification 1 2 Risk

Sainsbury s Bank plc Pillar 3 Disclosures for the year ended 2008 1 Overview 1.1 Background 1 1.2 Scope of Application 1 1.3 Frequency 1 1.4 Medium and Location for Publication 1 1.5 Verification 1 2 Risk

Credit Crunch: Causes, Effects & Implications. Ian Clarke, 29 th May 2008

: Causes, Effects & Implications Ian Clarke, 29 th May 2008 : Causes, Effects and Implications A review of the causal process Impact of the Longer term implications? 2 The : Causal Process Background Sustained

: Causes, Effects & Implications Ian Clarke, 29 th May 2008 : Causes, Effects and Implications A review of the causal process Impact of the Longer term implications? 2 The : Causal Process Background Sustained

CAPITAL REQUIREMENTS DIRECTIVE PILLAR 3 DISCLOSURE DOCUMENT 31 ST MARCH P a g e

CAPITAL REQUIREMENTS DIRECTIVE PILLAR 3 DISCLOSURE DOCUMENT 31 ST MARCH 2017 1 P a g e CONTENTS Page 1. Introduction 3 2. Risk Management Objectives and Policies 3-7 3. Capital Resources 7 4. Capital Adequacy

CAPITAL REQUIREMENTS DIRECTIVE PILLAR 3 DISCLOSURE DOCUMENT 31 ST MARCH 2017 1 P a g e CONTENTS Page 1. Introduction 3 2. Risk Management Objectives and Policies 3-7 3. Capital Resources 7 4. Capital Adequacy

CAPITAL REQUIREMENTS DIRECTIVE PILLAR 3 DISCLOSURE DOCUMENT

CAPITAL REQUIREMENTS DIRECTIVE PILLAR 3 DISCLOSURE DOCUMENT 31 ST MARCH 2014 CONTENTS Paragraph Introduction 1-6 Risk Management Objectives and Policies 7-23 Capital Resources 24-26 Capital Adequacy Assessment

CAPITAL REQUIREMENTS DIRECTIVE PILLAR 3 DISCLOSURE DOCUMENT 31 ST MARCH 2014 CONTENTS Paragraph Introduction 1-6 Risk Management Objectives and Policies 7-23 Capital Resources 24-26 Capital Adequacy Assessment

Capital Requirements Directive. Pillar 3 Disclosures. Vernon Building Society Pillar 3 Disclosures - 31 December 2017 Page 1

+ Capital Requirements Directive Pillar 3 Disclosures 31 December 2017 Vernon Building Society Pillar 3 Disclosures - 31 December 2017 Page 1 Contents 1. Overview... 3 2. Risk Management Objectives and

+ Capital Requirements Directive Pillar 3 Disclosures 31 December 2017 Vernon Building Society Pillar 3 Disclosures - 31 December 2017 Page 1 Contents 1. Overview... 3 2. Risk Management Objectives and

THE BERMUDA MONETARY AUTHORITY BANKS AND DEPOSIT COMPANIES ACT 1999: The Management of Operational Risk

THE BERMUDA MONETARY AUTHORITY BANKS AND DEPOSIT COMPANIES ACT 1999: The Management of Operational Risk May 2007 Introduction 1 This paper sets out the policy of the Bermuda Monetary Authority ( the Authority

THE BERMUDA MONETARY AUTHORITY BANKS AND DEPOSIT COMPANIES ACT 1999: The Management of Operational Risk May 2007 Introduction 1 This paper sets out the policy of the Bermuda Monetary Authority ( the Authority

State Bank of India (Canada)

") State Bank of India (Canada) Basel II Pillar 3 Disclosures December 2012 Note to Readers This document is prepared in accordance with OSFI expectations (OSFI letters dated July 13, 2011 on Implementation

State Bank of India (Canada) Basel II Pillar 3 Disclosures December 2012 Note to Readers This document is prepared in accordance with OSFI expectations (OSFI letters dated July 13, 2011 on Implementation

Rating Methodology Banks and Financial Institutions

CREDIT RATING INFORMATION AND SERVICES LIMITED Rating Methodology Banks and Financial Institutions CREDIT RATING PHILOSOPHY CRISL follows structured rating methodologies for each sectors of the national

CREDIT RATING INFORMATION AND SERVICES LIMITED Rating Methodology Banks and Financial Institutions CREDIT RATING PHILOSOPHY CRISL follows structured rating methodologies for each sectors of the national

Pillar 3 Disclosures. 31 December 2013

Pillar 3 Disclosures 31 December 2013 Contents 1. Overview... 3 1.1 Background... 3 1.2 Scope of application... 3 1.3 Basis and frequency of disclosures... 3 1.4 External audit... 3 2. Risk Management

Pillar 3 Disclosures 31 December 2013 Contents 1. Overview... 3 1.1 Background... 3 1.2 Scope of application... 3 1.3 Basis and frequency of disclosures... 3 1.4 External audit... 3 2. Risk Management

PILLAR III DISCLOSURES

PILLAR III DISCLOSURES 2014 PILLAR III Disclosures - 2014 Page 1 of 21 TABLE OF CONTENT 1 SCOPE OF APPLICATION... 4 1.1 PILLAR I MINIMUM CAPITAL REQUIREMENTS... 4 1.2 PILLAR II INTERNAL CAPITAL ADEQUACY

PILLAR III DISCLOSURES 2014 PILLAR III Disclosures - 2014 Page 1 of 21 TABLE OF CONTENT 1 SCOPE OF APPLICATION... 4 1.1 PILLAR I MINIMUM CAPITAL REQUIREMENTS... 4 1.2 PILLAR II INTERNAL CAPITAL ADEQUACY

Life Insurer Financial Profile

Life Insurer Financial Profile Company New York Life Ins Massachusetts Transamerica Life John Hancock Life & Mutual of Omaha Genworth Life Ins MedAmerica Ins Co Co Mutual Life Ins Ins Co Health Ins Ins

Life Insurer Financial Profile Company New York Life Ins Massachusetts Transamerica Life John Hancock Life & Mutual of Omaha Genworth Life Ins MedAmerica Ins Co Co Mutual Life Ins Ins Co Health Ins Ins

Professional Diploma in Banking Risk Management Practices (including Operational Risk and Conduct Risk)

") Diploma in Banking Risk Management Practices (including Operational Risk and Conduct Risk) 17 18 Who we are The Institute of Banking The Institute of Banking is the largest professional institute in Ireland.

Diploma in Banking Risk Management Practices (including Operational Risk and Conduct Risk) 17 18 Who we are The Institute of Banking The Institute of Banking is the largest professional institute in Ireland.

Egan-Jones Ratings Company

Egan-Jones Company 2018 Form NRSRO Annual Certification Exhibit 1 Performance Statistics Attached please find the Transition and Default Rates listed as follows: Financial Institutions, Brokers, or Dealers

Egan-Jones Company 2018 Form NRSRO Annual Certification Exhibit 1 Performance Statistics Attached please find the Transition and Default Rates listed as follows: Financial Institutions, Brokers, or Dealers

Professional Diploma in Banking Risk Management Practices (including Operational Risk and Conduct Risk) 2015/2016

2015/2016") Professional Diploma in Banking Risk Management Practices (including Operational Risk and Conduct Risk) 2015/2016 Who we are THE INSTITUTE OF BANKING The Institute of Banking is the largest professional

Professional Diploma in Banking Risk Management Practices (including Operational Risk and Conduct Risk) 2015/2016 Who we are THE INSTITUTE OF BANKING The Institute of Banking is the largest professional

PILLAR III DISCLOSURES

PILLAR III DISCLOSURES 6102 PILLAR III Disclosures - 6102 Page 1 of 21 TABLE OF CONTENT 1 SCOPE OF APPLICATION... 4 1.1 PILLAR I MINIMUM CAPITAL REQUIREMENTS... 4 1.2 PILLAR II INTERNAL CAPITAL ADEQUACY

PILLAR III DISCLOSURES 6102 PILLAR III Disclosures - 6102 Page 1 of 21 TABLE OF CONTENT 1 SCOPE OF APPLICATION... 4 1.1 PILLAR I MINIMUM CAPITAL REQUIREMENTS... 4 1.2 PILLAR II INTERNAL CAPITAL ADEQUACY

Pillar 3 As at 31st March 2011

Pillar 3 As at 31 st March 2011 Purpose of Disclosure This document sets out the Pillar 3 market disclosures for Threadneedle Asset Management Holdings an authorised and regulated limited license firm

Pillar 3 As at 31 st March 2011 Purpose of Disclosure This document sets out the Pillar 3 market disclosures for Threadneedle Asset Management Holdings an authorised and regulated limited license firm

ALUBAF Arab International Bank B.S.C (c) Basel II -Pillar III disclosures As at 31 December 2013

Basel II -Pillar III disclosures As at 31 December 2013") BASEL II PILLAR III DISCLOSURES 31 DECEMBER 2013 1 ALUBAF Arab International Bank B.S.C (c) Basel II -Pillar III disclosures As at 31 December 2013 Table of Contents 1 Introduction 3 2 Corporate Structure

BASEL II PILLAR III DISCLOSURES 31 DECEMBER 2013 1 ALUBAF Arab International Bank B.S.C (c) Basel II -Pillar III disclosures As at 31 December 2013 Table of Contents 1 Introduction 3 2 Corporate Structure

DARLINGTON BUILDING SOCIETY CAPITAL REQUIREMENTS DIRECTIVE

DARLINGTON BUILDING SOCIETY CAPITAL REQUIREMENTS DIRECTIVE PILLAR 3 DISCLOSURE DOCUMENT AS AT 31 st DECEMBER 2016 CONTENTS Section Title 1 Introduction 2 Risk Management Objectives and Policies 3 Capital

DARLINGTON BUILDING SOCIETY CAPITAL REQUIREMENTS DIRECTIVE PILLAR 3 DISCLOSURE DOCUMENT AS AT 31 st DECEMBER 2016 CONTENTS Section Title 1 Introduction 2 Risk Management Objectives and Policies 3 Capital

Delivering Clarity to Credit Unions Through Expertise and Experience

Jeff Owen, The Rochdale Group September 2012 Delivering Clarity to Credit Unions Through Expertise and Experience Enterprise Risk Management Lending Execution and Risk Management Merger Strategy and Realization

Jeff Owen, The Rochdale Group September 2012 Delivering Clarity to Credit Unions Through Expertise and Experience Enterprise Risk Management Lending Execution and Risk Management Merger Strategy and Realization

Pre Close Statement Year to 31 March Overview. Mid single digit percentage growth in alternative EPS. Robust performance from core businesses.

Pre Close Statement Year to 31 March 2003 Overview Mid single digit percentage growth in alternative EPS. Good earnings growth in the context of economic slowdown and continuing volatility in world stock

Pre Close Statement Year to 31 March 2003 Overview Mid single digit percentage growth in alternative EPS. Good earnings growth in the context of economic slowdown and continuing volatility in world stock

S&P Global Ratings Definitions

S&P Global Ratings s Table Of Contents I. GENERAL-PURPOSE CREDIT RATINGS A. Issue Credit Ratings B. Issuer Credit Ratings II. CREDITWATCH, RATING OUTLOOKS, LOCAL CURRENCY AND FOREIGN CURRENCY RATINGS A.

S&P Global Ratings s Table Of Contents I. GENERAL-PURPOSE CREDIT RATINGS A. Issue Credit Ratings B. Issuer Credit Ratings II. CREDITWATCH, RATING OUTLOOKS, LOCAL CURRENCY AND FOREIGN CURRENCY RATINGS A.

UBS Saudi Arabia (A SAUDI JOINT STOCK COMPANY) Pillar III Disclosure As of 31 December 2014

Pillar III Disclosure As of 31 December 2014") UBS Saudi Arabia King Fahad Road Tatweer Towers Tower 4, 9 th Floor PO Box 75724 Riyadh 11588 Kingdom of Saudi Arabia Tel. +966 (0) 11 203 8000 www.ubs.com UBS Saudi Arabia (A SAUDI JOINT STOCK COMPANY)

UBS Saudi Arabia King Fahad Road Tatweer Towers Tower 4, 9 th Floor PO Box 75724 Riyadh 11588 Kingdom of Saudi Arabia Tel. +966 (0) 11 203 8000 www.ubs.com UBS Saudi Arabia (A SAUDI JOINT STOCK COMPANY)

S&P Global Ratings Definitions

S&P Global Ratings s Table Of Contents I. GENERAL-PURPOSE CREDIT RATINGS A. Issue Credit Ratings B. Issuer Credit Ratings II. CREDITWATCH, RATING OUTLOOK, LOCAL CURRENCY AND FOREIGN CURRENCY RATINGS A.

S&P Global Ratings s Table Of Contents I. GENERAL-PURPOSE CREDIT RATINGS A. Issue Credit Ratings B. Issuer Credit Ratings II. CREDITWATCH, RATING OUTLOOK, LOCAL CURRENCY AND FOREIGN CURRENCY RATINGS A.

Appendix 1C. Treasury Management Policy incorporating Treasury Management Practices

Appendix 1C Treasury Management Policy incorporating Treasury Management Practices 2019-20 CONTENTS Page 1. Background 2 2. Aim 2 3. Scope 2 4. Policy Responsibility 2 5. Review 3 6. Treasury Management

Appendix 1C Treasury Management Policy incorporating Treasury Management Practices 2019-20 CONTENTS Page 1. Background 2 2. Aim 2 3. Scope 2 4. Policy Responsibility 2 5. Review 3 6. Treasury Management

Understanding Credit. What it is, why it s important, and how you can maintain it. Brought to you by Sallie Mae and FICO

Understanding Credit What it is, why it s important, and how you can maintain it Brought to you by Sallie Mae and FICO Introduction A student loan may be your first major credit experience. This is a good

Understanding Credit What it is, why it s important, and how you can maintain it Brought to you by Sallie Mae and FICO Introduction A student loan may be your first major credit experience. This is a good

Investing for income in a time of low interest rates PARTNERS IN MANAGING YOUR WEALTH 1 INVESTING FOR INCOME

Investing for income in a time of low interest rates PARTNERS IN MANAGING YOUR WEALTH 1 Contents 3 Introduction 4 Fixed interest 6 Corporate bonds 9 Gilts 10 Equities 13 Commercial property 14 Risk and

Investing for income in a time of low interest rates PARTNERS IN MANAGING YOUR WEALTH 1 Contents 3 Introduction 4 Fixed interest 6 Corporate bonds 9 Gilts 10 Equities 13 Commercial property 14 Risk and

Northwest Regional Data Center

Northwest Regional Data Center Located in Tallahassee, Florida, NWRDC was founded in 1972 as one of four regional data centers serving State University System of Florida. We have been providing services

Northwest Regional Data Center Located in Tallahassee, Florida, NWRDC was founded in 1972 as one of four regional data centers serving State University System of Florida. We have been providing services

The South African Bank of Athens Limited. PILLAR 3 REGULATORY REPORT December 2016

The South African Bank of Athens Limited PILLAR 3 REGULATORY REPORT December 2016 CONTENTS Page Introduction 2 Capital management 3 Risk Management 7 Credit Risk 9 Market Risk 18 Interest Rate Risk 19

The South African Bank of Athens Limited PILLAR 3 REGULATORY REPORT December 2016 CONTENTS Page Introduction 2 Capital management 3 Risk Management 7 Credit Risk 9 Market Risk 18 Interest Rate Risk 19

UBS Saudi Arabia (A SAUDI JOINT STOCK COMPANY) Pillar III Disclosure As of 31 December 2017

Pillar III Disclosure As of 31 December 2017") UBS Saudi Arabia King Fahad Road Tatweer Towers Tower 4, 9 th Floor PO Box 75724 Riyadh 11588 Kingdom of Saudi Arabia Tel. +966 (0) 11 203 8000 www.ubs.com UBS Saudi Arabia (A SAUDI JOINT STOCK COMPANY)

UBS Saudi Arabia King Fahad Road Tatweer Towers Tower 4, 9 th Floor PO Box 75724 Riyadh 11588 Kingdom of Saudi Arabia Tel. +966 (0) 11 203 8000 www.ubs.com UBS Saudi Arabia (A SAUDI JOINT STOCK COMPANY)

1.1. Low yield environment

1. Key developments Overall, the macroeconomic outlook has deteriorated since June 215. Although many European countries continue to recover, economic growth still remains fragile reflecting high public

1. Key developments Overall, the macroeconomic outlook has deteriorated since June 215. Although many European countries continue to recover, economic growth still remains fragile reflecting high public

BASEL III PILLAR III DISCLOSURES

BASEL III PILLAR III DISCLOSURES 31 DECEMBER 2016 1 ALUBAF Arab International Bank B.S.C (c) Basel III -Pillar III disclosures As at 31 December 2016 Table of Contents 1 Introduction 3 2 Corporate Structure

BASEL III PILLAR III DISCLOSURES 31 DECEMBER 2016 1 ALUBAF Arab International Bank B.S.C (c) Basel III -Pillar III disclosures As at 31 December 2016 Table of Contents 1 Introduction 3 2 Corporate Structure

Treasury Policy. Purpose of this policy:

Purpose of this policy: The purpose of this policy is to set out appropriate parameters as deemed fit by the Board for ELEXON s banking arrangements, in order to minimise counterparty risk, while delivering

Purpose of this policy: The purpose of this policy is to set out appropriate parameters as deemed fit by the Board for ELEXON s banking arrangements, in order to minimise counterparty risk, while delivering

BASEL III PILLAR III DISCLOSURES

BASEL III PILLAR III DISCLOSURES 31 DECEMBER 2017 1 ALUBAF Arab International Bank B.S.C (c) Basel III -Pillar III disclosures As at 31 December 2017 Table of Contents 1 Introduction 3 2 Corporate Structure

BASEL III PILLAR III DISCLOSURES 31 DECEMBER 2017 1 ALUBAF Arab International Bank B.S.C (c) Basel III -Pillar III disclosures As at 31 December 2017 Table of Contents 1 Introduction 3 2 Corporate Structure

Response of St Anthony s & Claddagh Credit Union To Consultation paper CP109 Potential Changes to the Investment Framework for Credit Unions

Response of St Anthony s & Claddagh Credit Union To Consultation paper CP109 Potential Changes to the Investment Framework for Credit Unions 8/9 Mainguard St, Galway Tel: 091 537200 Fax: 091 537250 8 Westside

Response of St Anthony s & Claddagh Credit Union To Consultation paper CP109 Potential Changes to the Investment Framework for Credit Unions 8/9 Mainguard St, Galway Tel: 091 537200 Fax: 091 537250 8 Westside

CARRIER FINANCIAL STRENGTH RATINGS Financial ratings reflect an insurance company's claims paying ability

CARRIER FINANCIAL STRENGTH RATINGS Financial ratings reflect an insurance company's claims paying ability Source Carrier A.M. Best Standard & Poor s Moody s Fitch 1 Unum A A A2 A 2 John Hancock A+ AA-

CARRIER FINANCIAL STRENGTH RATINGS Financial ratings reflect an insurance company's claims paying ability Source Carrier A.M. Best Standard & Poor s Moody s Fitch 1 Unum A A A2 A 2 John Hancock A+ AA-

European Investment Grade Credit Market Outlook Q Introduction

MARKET REVIEW European Investment Grade Credit Market Outlook Q4 2014 Garrett Walsh, Head of Credit Research, Europe September 2014 Introduction European Investment Grade Credit continued to perform well

MARKET REVIEW European Investment Grade Credit Market Outlook Q4 2014 Garrett Walsh, Head of Credit Research, Europe September 2014 Introduction European Investment Grade Credit continued to perform well

The PPF s Approach to Risk Management

The PPF s Approach to Risk Management Hans den Boer Chief Risk Officer SPP London Evening Meeting 14 October 2015 We ve come a long way in ten years PPF established by Pensions Act 2004 Opened our doors

The PPF s Approach to Risk Management Hans den Boer Chief Risk Officer SPP London Evening Meeting 14 October 2015 We ve come a long way in ten years PPF established by Pensions Act 2004 Opened our doors

Standard & Poor's Ratings Definitions

Table Of Contents I. GENERAL-PURPOSE CREDIT RATINGS A. Issue Credit Ratings B. Issuer Credit Ratings II. CREDITWATCH, RATING OUTLOOK, LOCAL CURRENCY AND FOREIGN CURRENCY RATINGS A. CreditWatch B. Rating

Table Of Contents I. GENERAL-PURPOSE CREDIT RATINGS A. Issue Credit Ratings B. Issuer Credit Ratings II. CREDITWATCH, RATING OUTLOOK, LOCAL CURRENCY AND FOREIGN CURRENCY RATINGS A. CreditWatch B. Rating

Nottingham Building Society. Pillar 3 Disclosures

Nottingham Building Society Pillar 3 Disclosures 31 December 2017 Contents 1. Overview...4 1.1. Background...4 1.2. Basis and Frequency of Disclosures...4 1.3. Location and Verification...4 1.4. Scope

Nottingham Building Society Pillar 3 Disclosures 31 December 2017 Contents 1. Overview...4 1.1. Background...4 1.2. Basis and Frequency of Disclosures...4 1.3. Location and Verification...4 1.4. Scope

TWG. Toronto Wealth Group. My Conversations with: Peter J. Frost & Tristan Sones. Investments, Retirement Planning, Insurance.

I attended the AGF Think Income, Think Equities, Investment Insights from Peter Frost event on January 22 nd, 2013 and the AGF Open House & Investment Forum on March 7 th, 2013 featuring Tristan Sones.

I attended the AGF Think Income, Think Equities, Investment Insights from Peter Frost event on January 22 nd, 2013 and the AGF Open House & Investment Forum on March 7 th, 2013 featuring Tristan Sones.

Step 2: Decide Who Might be Harmed and How. Step 3: Evaluate the Risks and Decide on Precautions. Step 4: Record Your Findings and Implement Them

r o f t n e m e g a n a M s p k i s r i T R d n a s e r u t x i F y Awa Ris y g e t a r t ks CONTENTS Section 1: Section 2: Section 3: Introduction The Risk Management Process The Types of Risks Faced

r o f t n e m e g a n a M s p k i s r i T R d n a s e r u t x i F y Awa Ris y g e t a r t ks CONTENTS Section 1: Section 2: Section 3: Introduction The Risk Management Process The Types of Risks Faced

Outline Capital Investment Strategy

Outline Capital Investment Strategy INDEX FOREWORD 1. INTRODUCTION 2. PURPOSE 3. SUMMARY 4. INFLUENCES ON CAPITAL INVESTMENT 5. CURRENT CAPITAL EXPENDITURE 6. COMMERCIAL PROPERTY INVESTMENT STRATEGY 7.

Outline Capital Investment Strategy INDEX FOREWORD 1. INTRODUCTION 2. PURPOSE 3. SUMMARY 4. INFLUENCES ON CAPITAL INVESTMENT 5. CURRENT CAPITAL EXPENDITURE 6. COMMERCIAL PROPERTY INVESTMENT STRATEGY 7.

Analytic measures of credit capacity can help bankcard lenders build strategies that go beyond compliance to deliver business advantage

How Much Credit Is Too Much? Analytic measures of credit capacity can help bankcard lenders build strategies that go beyond compliance to deliver business advantage Number 35 April 2010 On a portfolio

How Much Credit Is Too Much? Analytic measures of credit capacity can help bankcard lenders build strategies that go beyond compliance to deliver business advantage Number 35 April 2010 On a portfolio

Rynda Property Investors LLP (the Firm )

") Rynda Property Investors LLP (the Firm ) Disclosure Statement under Pillar III as at 30 th June 2018 Contents 1. Overview 2. Risk Management Objectives and Policies 3. Capital Resources 4. Capital Adequacy

Rynda Property Investors LLP (the Firm ) Disclosure Statement under Pillar III as at 30 th June 2018 Contents 1. Overview 2. Risk Management Objectives and Policies 3. Capital Resources 4. Capital Adequacy

CREDIT RATING INFORMATION & SERVICES LIMITED

Rating Methodology BANKS AND FINANCIAL INSTITUTIONS CREDIT RATING INFORMATION & SERVICES LIMITED Nakshi Homes (4th & 5th Floor), 6/1A, Segunbagicha, Dhaka 1000, Bangladesh Tel: 717 3700 1, Fax: 956 5783

Rating Methodology BANKS AND FINANCIAL INSTITUTIONS CREDIT RATING INFORMATION & SERVICES LIMITED Nakshi Homes (4th & 5th Floor), 6/1A, Segunbagicha, Dhaka 1000, Bangladesh Tel: 717 3700 1, Fax: 956 5783

Jeff Davies. Group Chief Financial Officer

Jeff Davies Group Chief Financial Officer AIM: DEMONSTRATE THAT LEGAL & GENERAL S EARNINGS AND BALANCE SHEET ARE RESILIENT TO CREDIT STRESS EVENTS 1. Financial results (Jeff Davies) 2. Legal & General

Jeff Davies Group Chief Financial Officer AIM: DEMONSTRATE THAT LEGAL & GENERAL S EARNINGS AND BALANCE SHEET ARE RESILIENT TO CREDIT STRESS EVENTS 1. Financial results (Jeff Davies) 2. Legal & General

The case for lower rated corporate bonds

The case for lower rated corporate bonds Marcus Pakenham Fixed income product specialist December 3 Introduction Where should fixed income investors be positioned over the medium term? We expect that government

The case for lower rated corporate bonds Marcus Pakenham Fixed income product specialist December 3 Introduction Where should fixed income investors be positioned over the medium term? We expect that government

PEOPLES TRUST COMPANY. PUBLIC DISCLOSURES (BASEL III PILLAR 3) As at December 31, 2013

As at December 31, 2013") PEOPLES TRUST COMPANY PUBLIC DISCLOSURES (BASEL III PILLAR 3) As at December 31, 2013 TABLE OF CONTENTS Disclosure Policy... 1 Location and Verification... 1 Background... 1 Statement of Risk Appetite...

PEOPLES TRUST COMPANY PUBLIC DISCLOSURES (BASEL III PILLAR 3) As at December 31, 2013 TABLE OF CONTENTS Disclosure Policy... 1 Location and Verification... 1 Background... 1 Statement of Risk Appetite...

National Ratings Definitions

National Ratings Definitions AM Best Rating Descriptor Definition A++ Superior Assigned to companies that have, in our opinion, a superior ability to meet their ongoing insurance obligations. A++ Superior

National Ratings Definitions AM Best Rating Descriptor Definition A++ Superior Assigned to companies that have, in our opinion, a superior ability to meet their ongoing insurance obligations. A++ Superior

Hypo Investor Update Debt Investor Presentation

Hypo Investor Update 2019 Debt Investor Presentation Hypo Covered Bond Roadshow February March, 2019 Secure Way for Better Living Hypo Group Overview Founded in 1860 The oldest private credit institution

Hypo Investor Update 2019 Debt Investor Presentation Hypo Covered Bond Roadshow February March, 2019 Secure Way for Better Living Hypo Group Overview Founded in 1860 The oldest private credit institution

CATTOLICA LIFE DAC SOLVENCY AND FINANCIAL CONDITION REPORT 31 ST DECEMBER 2017

CATTOLICA LIFE DAC SOLVENCY AND FINANCIAL CONDITION REPORT 31 ST DECEMBER 2017 May 3, 2018 TABLE OF CONTENTS EXECUTIVE SUMMARY 3 A. BUSINESS AND PEFORMANCE 5 A.1 Business A.2 Underwriting Performance 5

CATTOLICA LIFE DAC SOLVENCY AND FINANCIAL CONDITION REPORT 31 ST DECEMBER 2017 May 3, 2018 TABLE OF CONTENTS EXECUTIVE SUMMARY 3 A. BUSINESS AND PEFORMANCE 5 A.1 Business A.2 Underwriting Performance 5

Feedback Statement on CP109 Consultation on Potential Changes to the Investment Framework for Credit Unions

Feedback Statement on CP109 Consultation on Potential Changes to the Investment Framework for Credit Unions 1 Table of Contents Foreword... 2 1. Introduction... 4 2. Executive Summary... 6 3. Responses

Feedback Statement on CP109 Consultation on Potential Changes to the Investment Framework for Credit Unions 1 Table of Contents Foreword... 2 1. Introduction... 4 2. Executive Summary... 6 3. Responses

BASEL II - PILLAR III

BASEL II - PILLAR III DISCLOSURES 2009 ARESBANK PILAR III DISCLOSURES (December 31 st 2009) TABLE OF CONTENTS 1. INTRODUCTION... 2 2. INTERNAL GOVERNANCE STRUCTURE... 3 3. RISK GOVERNANCE... 5 4. CAPITAL

BASEL II - PILLAR III DISCLOSURES 2009 ARESBANK PILAR III DISCLOSURES (December 31 st 2009) TABLE OF CONTENTS 1. INTRODUCTION... 2 2. INTERNAL GOVERNANCE STRUCTURE... 3 3. RISK GOVERNANCE... 5 4. CAPITAL

Disclosure Prudential Disclosure Report. 12/31/2017 Derayah Financial

Derayah - Pillar III Disclosure -2017 Prudential Disclosure Report 12/31/2017 Derayah Financial Table of Contents 1. OVERVIEW... 2 2. CAPITAL STRUCTURE... 2 2.1. Disclosure on Capital Base... 3 3. CAPITAL

Derayah - Pillar III Disclosure -2017 Prudential Disclosure Report 12/31/2017 Derayah Financial Table of Contents 1. OVERVIEW... 2 2. CAPITAL STRUCTURE... 2 2.1. Disclosure on Capital Base... 3 3. CAPITAL

PANAFRICAN CREDIT RATING AGENCY. Tel: +(225) (225) Fax:+(225)

(225) Fax:+(225)") PANAFRICAN CREDIT RATING AGENCY Public Limited Company with a Board of Directors with a share capital of CFAF 100,000,000 Accredited by the Capital Market authority (CMA) of Rwanda Ref/CMA/July/3047/2015

PANAFRICAN CREDIT RATING AGENCY Public Limited Company with a Board of Directors with a share capital of CFAF 100,000,000 Accredited by the Capital Market authority (CMA) of Rwanda Ref/CMA/July/3047/2015

INVESTMENT DEALERS ASSOCIATION

INVESTMENT DEALERS ASSOCIATION IN THE MATTER OF: THE BY-LAWS OF THE INVESTMENT DEALERS ASSOCIATION OF CANADA AND KYLE KAI KEE WONG SETTLEMENT AGREEMENT I. INTRODUCTION 1. The Enforcement Department Staff

INVESTMENT DEALERS ASSOCIATION IN THE MATTER OF: THE BY-LAWS OF THE INVESTMENT DEALERS ASSOCIATION OF CANADA AND KYLE KAI KEE WONG SETTLEMENT AGREEMENT I. INTRODUCTION 1. The Enforcement Department Staff

Governor's Statement No. 16 October 10, Statement by the Hon. PATRICK HONOHAN, Alternate Governor of the Fund for IRELAND

Governor's Statement No. 16 October 10, 2014 Statement by the Hon. PATRICK HONOHAN, Alternate Governor of the Fund for IRELAND Statement by Mr. Patrick Honohan, Alternate Governor for Ireland of the International

Governor's Statement No. 16 October 10, 2014 Statement by the Hon. PATRICK HONOHAN, Alternate Governor of the Fund for IRELAND Statement by Mr. Patrick Honohan, Alternate Governor for Ireland of the International

DECEMBER 2010 BASEL II - PILLAR 3 DISCLOSURES. JPMorgan Chase Bank, National Association, Madrid Branch INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS

DECEMBER 2010 BASEL II - PILLAR 3 DISCLOSURES INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS JPMorgan Chase Bank, National Association, Madrid Branch Financial year ending December 31, 2010 Disclosures under

DECEMBER 2010 BASEL II - PILLAR 3 DISCLOSURES INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS JPMorgan Chase Bank, National Association, Madrid Branch Financial year ending December 31, 2010 Disclosures under

June Implementation of the Credit Union Act 1997 (Regulatory Requirements) Regulations 2016 for Credit Unions Frequently Asked Questions

Regulations 2016 for Credit Unions Frequently Asked Questions") June 2016 Implementation of the Credit Union Act 1997 (Regulatory Requirements) Regulations 2016 for Credit Unions Frequently Asked Questions [Type text] 1 Contents Introduction... 3 Application of the

June 2016 Implementation of the Credit Union Act 1997 (Regulatory Requirements) Regulations 2016 for Credit Unions Frequently Asked Questions [Type text] 1 Contents Introduction... 3 Application of the

GL ON COMMON PROCEDURES AND METHODOLOGIES FOR SREP EBA/CP/2014/14. 7 July Consultation Paper

EBA/CP/2014/14 7 July 2014 Consultation Paper Draft Guidelines for common procedures and methodologies for the supervisory review and evaluation process under Article 107 (3) of Directive 2013/36/EU Contents

EBA/CP/2014/14 7 July 2014 Consultation Paper Draft Guidelines for common procedures and methodologies for the supervisory review and evaluation process under Article 107 (3) of Directive 2013/36/EU Contents

Relevance of Operational Risk to the FCA Jill Savager Manager, Operational Risk, Financial Conduct Authority

Relevance of Operational Risk to the FCA Jill Savager Manager, Operational Risk, Financial Conduct Authority IOR Scottish Chapter Annual Conference Glasgow Caledonian University 01/11/13 1 What we will

Relevance of Operational Risk to the FCA Jill Savager Manager, Operational Risk, Financial Conduct Authority IOR Scottish Chapter Annual Conference Glasgow Caledonian University 01/11/13 1 What we will

Guidance Note: Stress Testing Credit Unions with Assets Greater than $500 million. May Ce document est également disponible en français.

Guidance Note: Stress Testing Credit Unions with Assets Greater than $500 million May 2017 Ce document est également disponible en français. Applicability This Guidance Note is for use by all credit unions

Guidance Note: Stress Testing Credit Unions with Assets Greater than $500 million May 2017 Ce document est également disponible en français. Applicability This Guidance Note is for use by all credit unions

SHARE DEALING. Income GeneratoR. Halifax Structured Products

SHARE DEALING Income GeneratoR Halifax Structured Products Contents Page 1. Who is involved in the Income Generator? 3 2. Product Overview 4 3. How does the Income Generator work? 6 4. Is the Income Generator

SHARE DEALING Income GeneratoR Halifax Structured Products Contents Page 1. Who is involved in the Income Generator? 3 2. Product Overview 4 3. How does the Income Generator work? 6 4. Is the Income Generator

Disclosure Prudential Disclosure Report. 12/31/2016 Derayah Financial

Derayah - Pillar III Disclosure -2016 Prudential Disclosure Report 12/31/2016 Derayah Financial Table of Contents 1. OVERVIEW... 2 2. CAPITAL STRUCTURE... 2 2.1. Disclosure on Capital Base... 3 3. CAPITAL

Derayah - Pillar III Disclosure -2016 Prudential Disclosure Report 12/31/2016 Derayah Financial Table of Contents 1. OVERVIEW... 2 2. CAPITAL STRUCTURE... 2 2.1. Disclosure on Capital Base... 3 3. CAPITAL

Regulatory Disclosures March 31, 2018

Regulatory Disclosures March 31, 2018 SCOPE of DISCLOSURE... 3 CORPORATE PROFILE... 3 CAPITAL... 3 Capital structure... 4 Common shares... 4 Subordinated debt... 4 RISK MANAGEMENT... 4 Risk management

Regulatory Disclosures March 31, 2018 SCOPE of DISCLOSURE... 3 CORPORATE PROFILE... 3 CAPITAL... 3 Capital structure... 4 Common shares... 4 Subordinated debt... 4 RISK MANAGEMENT... 4 Risk management

BATH BUILDING SOCIETY

BATH BUILDING SOCIETY Pillar 3 Disclosure Document Index Page 1. Introduction 3 2. Risk management policies and objectives 5 3. Main Board and committee structure 10 4. Capital resources and capital ratios

BATH BUILDING SOCIETY Pillar 3 Disclosure Document Index Page 1. Introduction 3 2. Risk management policies and objectives 5 3. Main Board and committee structure 10 4. Capital resources and capital ratios

Mapping of Egan-Jones Ratings Company s credit assessments under the Standardised Approach

18/07/2017 Mapping of Egan-Jones Ratings Company s credit assessments under the Standardised Approach 1. Executive summary 1. This report describes the mapping exercise carried out by the Joint Committee

18/07/2017 Mapping of Egan-Jones Ratings Company s credit assessments under the Standardised Approach 1. Executive summary 1. This report describes the mapping exercise carried out by the Joint Committee

LEGAL & GENERAL GROUP PLC risk management supplement

LEGAL & GENERAL GROUP PLC 2017 risk management supplement Supplement contents Within this supplement we set out descriptions of the risks we face, how our risk management framework operates, as well as

LEGAL & GENERAL GROUP PLC 2017 risk management supplement Supplement contents Within this supplement we set out descriptions of the risks we face, how our risk management framework operates, as well as

HONG LEONG INVESTMENT BANK BERHAD Company no: P (Incorporated in Malaysia)

") BASEL II PILLAR 3 DISCLOSURES FOR THE FINANCIAL PERIOD ENDED 31 DECEMBER 2011 BASEL II PILLAR 3 DISCLOSURES FOR THE FINANCIAL PERIOD ENDED 31 DECEMBER 2011 Content Page INTRODUCTION 1 SCOPE OF APPLICATION

BASEL II PILLAR 3 DISCLOSURES FOR THE FINANCIAL PERIOD ENDED 31 DECEMBER 2011 BASEL II PILLAR 3 DISCLOSURES FOR THE FINANCIAL PERIOD ENDED 31 DECEMBER 2011 Content Page INTRODUCTION 1 SCOPE OF APPLICATION

Taiwan Ratings. An Introduction to CDOs and Standard & Poor's Global CDO Ratings. Analysis. 1. What is a CDO? 2. Are CDOs similar to mutual funds?

An Introduction to CDOs and Standard & Poor's Global CDO Ratings Analysts: Thomas Upton, New York Standard & Poor's Ratings Services has been rating collateralized debt obligation (CDO) transactions since

An Introduction to CDOs and Standard & Poor's Global CDO Ratings Analysts: Thomas Upton, New York Standard & Poor's Ratings Services has been rating collateralized debt obligation (CDO) transactions since

What makes bonds marketable... or not! And - a program that can help. Patrick Rutledge, AVP / Public Finance Relationship Manager FHLBank Atlanta

What makes bonds marketable... or not! And - a program that can help. Patrick Rutledge, AVP / Public Finance Relationship Manager FHLBank Atlanta 1 Disclaimer Certain information contained herein has been

What makes bonds marketable... or not! And - a program that can help. Patrick Rutledge, AVP / Public Finance Relationship Manager FHLBank Atlanta 1 Disclaimer Certain information contained herein has been

Integrating budgets and entity strategy. ICAZ CFO Forum

Integrating budgets and entity strategy ICAZ CFO Forum 14.11.13 How we shall move to the promised land Introduction and Background Challenges faced in practice Around budgeting Link with strategy 8 Best

Integrating budgets and entity strategy ICAZ CFO Forum 14.11.13 How we shall move to the promised land Introduction and Background Challenges faced in practice Around budgeting Link with strategy 8 Best

THE INVESTOR FOR SECURITIES COMPANY. PILLAR III DISCLOSURE As of 31 December 2017

THE INVESTOR FOR SECURITIES COMPANY PILLAR III DISCLOSURE As of 31 December 2017 Table of Contents 1. Scope of Application... 3 1.1. Basis of Disclosure... 4 1.2. Frequency of Disclosures... 4 1.3. Material

THE INVESTOR FOR SECURITIES COMPANY PILLAR III DISCLOSURE As of 31 December 2017 Table of Contents 1. Scope of Application... 3 1.1. Basis of Disclosure... 4 1.2. Frequency of Disclosures... 4 1.3. Material

PROTECTING PROFITS WITH POWERFUL INSIGHT

PROTECTING PROFITS WITH POWERFUL INSIGHT A cash management strategy that powers success moving money for better CASH MANAGEMENT Safely navigate currency markets, smooth out cash flow and grow business.

PROTECTING PROFITS WITH POWERFUL INSIGHT A cash management strategy that powers success moving money for better CASH MANAGEMENT Safely navigate currency markets, smooth out cash flow and grow business.

Default rates for Low and Medium-rated Japanese Issuers: Objective Approach to Calculating the Gap between BBB and BB

Default rates for Low and Medium-rated Japanese Issuers: Objective Approach to Calculating the Gap between BBB and BB Issued February 20, 2015 The Japanese corporate bond market lacks sufficient data on

Default rates for Low and Medium-rated Japanese Issuers: Objective Approach to Calculating the Gap between BBB and BB Issued February 20, 2015 The Japanese corporate bond market lacks sufficient data on

House Loans in Credit Unions Thematic Review Findings

House Loans in Credit Unions Thematic Review Findings January 2018 Page 2 House Loans in Credit Unions - Thematic Review Findings Central Bank of Ireland Table of Contents 1. Executive Summary... 3 2.

House Loans in Credit Unions Thematic Review Findings January 2018 Page 2 House Loans in Credit Unions - Thematic Review Findings Central Bank of Ireland Table of Contents 1. Executive Summary... 3 2.

Musharaka Capital Company Pillar III Disclosure Report

Musharaka Capital Company Pillar III Disclosure Report 31.12.2017 Table of Contents Overview:... 2 Capital structure... 4 Capital adequacy... 5 Risk management... 6 Market risk... 6 Credit risk... 7 Operational

Musharaka Capital Company Pillar III Disclosure Report 31.12.2017 Table of Contents Overview:... 2 Capital structure... 4 Capital adequacy... 5 Risk management... 6 Market risk... 6 Credit risk... 7 Operational

Tungsten Corporation plc Tungsten Bank plc. Pillar 3 Disclosures. 8 July / 20

Tungsten Corporation plc Tungsten Bank plc Pillar 3 Disclosures 8 July 2014 1 / 20 Table of Contents 1 Overview... 4 Introduction... 4 Basis and Frequency of Disclosures... 4 Published Information... 4

Tungsten Corporation plc Tungsten Bank plc Pillar 3 Disclosures 8 July 2014 1 / 20 Table of Contents 1 Overview... 4 Introduction... 4 Basis and Frequency of Disclosures... 4 Published Information... 4

PILLAR 3 DISCLOSURES MERCER UK AUGUST 2016

PILLAR 3 DISCLOSURES MERCER UK AUGUST 2016 CONTENTS 1. Background... 1 1.1 Basis of Disclosures... 2 1.2 Frequency of Publication... 2 1.3 Verification... 2 1.4 Media & Location of Publication... 2 2.

PILLAR 3 DISCLOSURES MERCER UK AUGUST 2016 CONTENTS 1. Background... 1 1.1 Basis of Disclosures... 2 1.2 Frequency of Publication... 2 1.3 Verification... 2 1.4 Media & Location of Publication... 2 2.

DEBT 101: FUNDAMENTALS OF DEBT ISSUANCE

DEBT 101: FUNDAMENTALS OF DEBT ISSUANCE Debby Cherney Deputy General Manager Eastern Municipal Water District Tyler Old Director PFM Financial Advisors LLC Cyrus Torabi Shareholder Stradling Yocca Carlson

DEBT 101: FUNDAMENTALS OF DEBT ISSUANCE Debby Cherney Deputy General Manager Eastern Municipal Water District Tyler Old Director PFM Financial Advisors LLC Cyrus Torabi Shareholder Stradling Yocca Carlson

Nottingham Building Society. Basel II - Pillar 3 Disclosures 2012

Nottingham Building Society Basel II - Pillar 3 Disclosures 2012 1 Contents 1. Overview 1.1 Background 1.2 Basis and Frequency of Disclosures 1.3 Location and Verification 1.4 Scope of Application Page

Nottingham Building Society Basel II - Pillar 3 Disclosures 2012 1 Contents 1. Overview 1.1 Background 1.2 Basis and Frequency of Disclosures 1.3 Location and Verification 1.4 Scope of Application Page

USER GUIDE. How To Get The Most Out Of Your Daily Cryptocurrency Trading Signals

USER GUIDE How To Get The Most Out Of Your Daily Cryptocurrency Trading Signals Getting Started Thank you for subscribing to Signal Profits daily crypto trading signals. If you haven t already, make sure

USER GUIDE How To Get The Most Out Of Your Daily Cryptocurrency Trading Signals Getting Started Thank you for subscribing to Signal Profits daily crypto trading signals. If you haven t already, make sure

Financial Crime Governance, Risk and Compliance Fund Managers & Fund Administrators. Thematic Review 2017

Financial Crime Governance, Risk and Compliance Fund Managers & Fund Administrators Thematic Review 2017 Foreword During late 2016 a thematic review of fund managers and fund administrators governance,

Financial Crime Governance, Risk and Compliance Fund Managers & Fund Administrators Thematic Review 2017 Foreword During late 2016 a thematic review of fund managers and fund administrators governance,

Statement of Guidance for Licensees seeking approval to use an Internal Capital Model ( ICM ) to calculate the Prescribed Capital Requirement ( PCR )

to calculate the Prescribed Capital Requirement ( PCR )") MAY 2016 Statement of Guidance for Licensees seeking approval to use an Internal Capital Model ( ICM ) to calculate the Prescribed Capital Requirement ( PCR ) 1 Table of Contents 1 STATEMENT OF OBJECTIVES...

MAY 2016 Statement of Guidance for Licensees seeking approval to use an Internal Capital Model ( ICM ) to calculate the Prescribed Capital Requirement ( PCR ) 1 Table of Contents 1 STATEMENT OF OBJECTIVES...

Consumer Risk Index. An annual survey of the risks Americans believe are most prevalent in their lives

Consumer Risk Index An annual survey of the risks Americans believe are most prevalent in their lives October 2015 Contents Executive summary 1 Key findings 2 Top risks 3 Demographic and regional highlights

Consumer Risk Index An annual survey of the risks Americans believe are most prevalent in their lives October 2015 Contents Executive summary 1 Key findings 2 Top risks 3 Demographic and regional highlights

Exploding the myths Insurance under Basel II and the CRD

Exploding the myths Insurance under Basel II and the CRD John Thirlwell LMA, London, 9 July 2008 Agenda Basel basics CRD criteria specifics mapping Comments on some market solutions Coverage A short history

Exploding the myths Insurance under Basel II and the CRD John Thirlwell LMA, London, 9 July 2008 Agenda Basel basics CRD criteria specifics mapping Comments on some market solutions Coverage A short history

REINSURANCE RISK MANAGEMENT GUIDELINE

DRAFT DRAFT REINSURANCE RISK MANAGEMENT GUIDELINE Initial publication: April 2010 Update: July 2013 Table of Contents Preamble... 2 Introduction... 3 Scope... 5 Coming into effect and updating... 6 1.

DRAFT DRAFT REINSURANCE RISK MANAGEMENT GUIDELINE Initial publication: April 2010 Update: July 2013 Table of Contents Preamble... 2 Introduction... 3 Scope... 5 Coming into effect and updating... 6 1.

EARLY WARNING SIGNALS IN INSURANCE COMPANIES

EARLY WARNING SIGNALS IN INSURANCE COMPANIES Leading Excellence in Insurance Global Reach BIBF plays a vital role in the training and development of human capital in the Middle East and North Africa. Our

EARLY WARNING SIGNALS IN INSURANCE COMPANIES Leading Excellence in Insurance Global Reach BIBF plays a vital role in the training and development of human capital in the Middle East and North Africa. Our

Introduction to the Gann Analysis Techniques

Introduction to the Gann Analysis Techniques A Member of the Investment Data Services group of companies Bank House Chambers 44 Stockport Road Romiley Stockport SK6 3AG Telephone: 0161 285 4488 Fax: 0161

Introduction to the Gann Analysis Techniques A Member of the Investment Data Services group of companies Bank House Chambers 44 Stockport Road Romiley Stockport SK6 3AG Telephone: 0161 285 4488 Fax: 0161

TD BANK INTERNATIONAL S.A.

TD BANK INTERNATIONAL S.A. Pillar 3 Disclosures Year Ended October 31, 2013 1 Contents 1. Overview... 3 1.1 Purpose...3 1.2 Frequency and Location...3 2. Governance and Risk Management Framework... 4 2.1

TD BANK INTERNATIONAL S.A. Pillar 3 Disclosures Year Ended October 31, 2013 1 Contents 1. Overview... 3 1.1 Purpose...3 1.2 Frequency and Location...3 2. Governance and Risk Management Framework... 4 2.1

Interest Rate Swaps Product Disclosure Statement. Issued by Westpac Banking Corporation ABN AFSL

Interest Rate Swaps Product Disclosure Statement Issued by Westpac Banking Corporation ABN 33 007 457 141 AFSL 233714 Dated: 22 September 2017. This is a replacement product disclosure statement. It replaces

Interest Rate Swaps Product Disclosure Statement Issued by Westpac Banking Corporation ABN 33 007 457 141 AFSL 233714 Dated: 22 September 2017. This is a replacement product disclosure statement. It replaces

GOLDMAN SACHS BANK (EUROPE) PLC

PLC") AS AT 31 DECEMBER 2009 GOLDMAN SACHS BANK (EUROPE) PLC PILLAR 3 DISCLOSURES Table of Contents 1. Overview 1 2. Basel II and Pillar 3 1 3. Scope of Pillar 3 1 4. Capital Resources and Capital Requirements

AS AT 31 DECEMBER 2009 GOLDMAN SACHS BANK (EUROPE) PLC PILLAR 3 DISCLOSURES Table of Contents 1. Overview 1 2. Basel II and Pillar 3 1 3. Scope of Pillar 3 1 4. Capital Resources and Capital Requirements

Pillar 3 Disclosures Year ended 31 st December 2017

Pillar 3 Disclosures Year ended 31 st December 2017 1 Contents 1. Introduction 3 2. Board and Committee structure 3 3. Capital resources 4 4. Capital requirements 4 5. Key risks 5 6. Directors 9 2 1. Introduction

Pillar 3 Disclosures Year ended 31 st December 2017 1 Contents 1. Introduction 3 2. Board and Committee structure 3 3. Capital resources 4 4. Capital requirements 4 5. Key risks 5 6. Directors 9 2 1. Introduction