The PPF s Approach to Risk Management

|

|

|

- Gervais Moore

- 6 years ago

- Views:

Transcription

1 The PPF s Approach to Risk Management Hans den Boer Chief Risk Officer SPP London Evening Meeting 14 October 2015

2 We ve come a long way in ten years PPF established by Pensions Act 2004 Opened our doors in April 2005 Took responsibility for the Financial Assistance Scheme in 2009

3 A reminder. Levy Investment Scheme assets PPF Members Employer recoveries

Liabilities ( m) Surplus (")

4 The first ten years in numbers PPF Balance Sheet 2005 to date / / / / / / / / / Assets ( m) Liabilities ( m) Surplus ( m)

5 Latest status 115% funding level 1.8 billion paid out in compensation 223k members, from ~700 schemes, transferred to PPF [Figures at 31/3/15] PPF SiA Total bn bn bn Net assets Actuarial estimate of liabilities (17.8) (6.2) (24.0) Total net surplus/ (deficit) 4.8 (1.3) 3.6

6 Our Objectives: Deliver excellent customer service to our members, levy payers and other stakeholders. o Over the past year we have made progress on the major project aimed at bringing our PPF member services operations in-house. This initiative will ensure the PPF has the control and flexibility to deliver exceptional service as part of its ambition to be a high performing Customer Focused Financial Institution o The new PPF-specific model (announced last year), developed with Experian following consultation with levy payers and the industry, allows us to offer levy payers greater transparency and certainty Meet our funding target through prudent and effective management of our balance sheets Pursue our mission within a high caliber framework of risk management o to make sure we are always in a position to pay members the compensation they are entitled to

7 Evolving Risk Framework for the PPF 1 GOVERNANCE 2 TOOLS Committees Responsibilities Identify Measure Mitigate Monitor Report Transparency & consistency around properly informed decision making Robust Risk Culture Appropriate Committee Structure Comprehensive Policy framework Clearly articulated Risk Appetite at a PPF and linked to the Taxonomy Effective Training 3 Measure Monitor Report Complete and accurate Risk Taxonomy Comprehensive programme of risk and control self assessments (RCSAs) (Embedded in the business governance) Thematic risk reviews (By Risk Team) Key Risk Indicators with trend analysis Effective process for collecting Incidents & Loss Events Use of Key Risk Scenarios to identify and quantify potential risk and loss events Data collected from all of the above must feed into the management of our reputation and Probability of Success Risk Reporting to support effective decision making USE TEST Demonstrates practical and ongoing utilisation of the Risk Management Framework Tactical and strategic decision making informed by the output from RCSAs, Risk & Loss Events, Key Risk Scenarios and KRIs The output from all of these Tools must be clearly evident in our assessment of our risks and our probability of success Risk assessments of New Business Initiatives driven by the Risk Taxonomy To extract maximum value we must be able to evidence that all three elements are linked, owned and demonstrably employed by the business risk owners 6

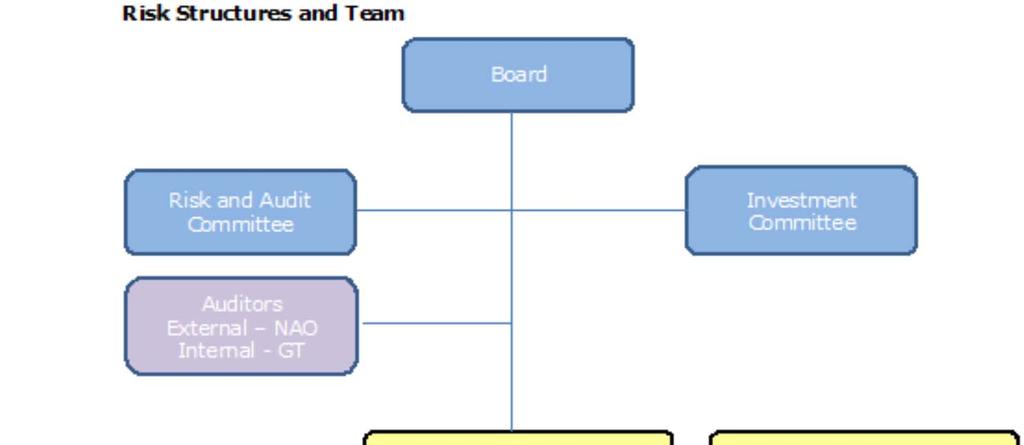

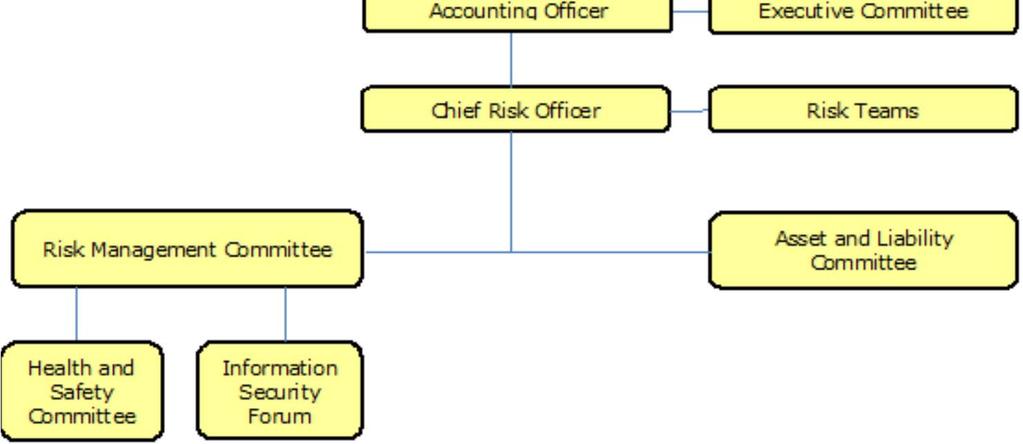

8 PPF Risk Governance

9 Risk Management Function The PPF manages two main areas of risk; operational risk, from member services to the levy collection, and financial risk, executing the Strategic Plan to manage the risks associated with investments Our Risk function consists of 5 small teams: Portfolio & Stress Testing, Market Risk, Credit Risk, Operational Risk and Actuarial Risk & Modelling. One key aspect of the ways we manage financial risk is our risk modelling, using our long-term risk model (LTRM) to inform our Funding Strategy, with the aim of securing self-sufficiency

10 Claims Risk: central to our role as safety net The PPF provides protection to members of 6057 DB schemes. Many of these schemes are in deficit. Monthly, we publish our estimate of the combined deficit through the PPF 7800 index. Large insolvencies have the potential to wipe out the PPF surplus Our estimate is that 36 funds have a deficit greater than 1b, and 90 greater than 500m Through our Top500 model we focus on the credit quality of the 500 largest funds in deficit combination of publicly available ratings and our own Experian model

11 One Key Risk: A worrying trend The TPR shares certain DB scheme data with the PPF This shows that the length of the DB schemes recovery plans is not improving While sponsor contributions are being made, the funding gap is overall not being closed Mainly caused by low interest rates

12 Risk modelling: LTRM +Future levy Current funding position +/-Investment returns -Benefit payments 2,000 economic scenarios PPF 7800 funding position Future claims Insolvencies of sponsors x 500 credit scenarios PPF s future funding position =1,000,000 total scenarios

13 Risk modelling: LTRM LTRM modelling a key part of our funding decisions, to achieve our funding target to be self-sufficient by 2030 While median scenarios look positive, a key risk is that large claims will occur in the future.

14 Funding Self Sufficiency A flight-path to self-sufficiency: Zero market risk Zero interest rate and inflation exposure Reserve (10% of liabilities) to hedge future claims and longevity risk Levy only for expected claims Measured as probability of success March % probability that we would reach this target in 2030

15 Other Financial Risks Hedging Strategic Implementation Tactical Active Currency Alternative asset Concentration Credit spread Counterparty Liquidity Model Custody Transition Operational Purple=Risk owned by CIO Blue=Risk owned by another party The embedded risk framework directly impacts daily working life

16 Operational Risks Information Security Key area of focus due to insourcing of member services administration. Training Penetration Testing, Stress scenarios. Preventative & Detective measures Crisis response preparedness Business Continuity Planning What to do in case of major disruption Disaster recovery site Training and regular testing that BCP process works as designed Major Incident Team What-If scenario planning

17 Any Questions?

70 the purple book Charts and Tables

70 the purple book 2017 Charts and Tables Charts and Tables Chapter 2: Figure 2.1 Distribution of schemes excluding those in assessment by number of members as at 31 March 2017 9 Figure 2.2 Distribution

70 the purple book 2017 Charts and Tables Charts and Tables Chapter 2: Figure 2.1 Distribution of schemes excluding those in assessment by number of members as at 31 March 2017 9 Figure 2.2 Distribution

Enterprise Risk Management Policy Adopted by the AMP Limited Board on 2 February 2017

Enterprise Management Policy Adopted by the AMP Limited Board on 2 February 2017 AMP s promise is to help people own tomorrow. To achieve this promise, risks must be managed effectively within the Board

Enterprise Management Policy Adopted by the AMP Limited Board on 2 February 2017 AMP s promise is to help people own tomorrow. To achieve this promise, risks must be managed effectively within the Board

The Purple Book D B P E N S I O N S U N I V E R S E R I S K P R O F I L E

The Purple Book DB PENSIONS UNIVERSE RISK PROFILE 2014 2 t h e p u r p l e b o o k 2 014 The Purple Books give the most comprehensive picture of the risks faced by the PPF-eligible defined benefit pension

The Purple Book DB PENSIONS UNIVERSE RISK PROFILE 2014 2 t h e p u r p l e b o o k 2 014 The Purple Books give the most comprehensive picture of the risks faced by the PPF-eligible defined benefit pension

Glossary t h e p u r p l e b o o k

Glossary 65 Glossary Active member In relation to an occupational pension scheme, a person who is in pensionable service under the scheme. Administration See Company: trading status. Aggregate funding

Glossary 65 Glossary Active member In relation to an occupational pension scheme, a person who is in pensionable service under the scheme. Administration See Company: trading status. Aggregate funding

Coats Group plc. Annual Financial Report 2014

19 March 2015 Coats Group plc Annual Financial Report 2014 Coats Group plc ( Coats or the Company ) has today submitted to the Financial Conduct Authority's national storage mechanism its Annual Financial

19 March 2015 Coats Group plc Annual Financial Report 2014 Coats Group plc ( Coats or the Company ) has today submitted to the Financial Conduct Authority's national storage mechanism its Annual Financial

CYBER REPORT CYBER REPORT 2018

2018 CYBER REPORT CYBER REPORT 2018 Table of Contents 1. Introduction 2 2. Technology Risk Resiliency 3 3. Cyber Underwriting 5 4. Key Statistics 6 5. Cyber Stress Scenarios 7 1. Introduction Technology

2018 CYBER REPORT CYBER REPORT 2018 Table of Contents 1. Introduction 2 2. Technology Risk Resiliency 3 3. Cyber Underwriting 5 4. Key Statistics 6 5. Cyber Stress Scenarios 7 1. Introduction Technology

Solvency and Financial Condition Report 20I6

Solvency and Financial Condition Report 20I6 Contents Contents... 2 Director s Statement... 4 Report of the External Independent Auditor... 5 Summary... 9 Company Information... 9 Purpose of the Solvency

Solvency and Financial Condition Report 20I6 Contents Contents... 2 Director s Statement... 4 Report of the External Independent Auditor... 5 Summary... 9 Company Information... 9 Purpose of the Solvency

STRATEGIC PLAN. Pension Protection Fund

STRATEGIC PLAN 2014 Pension Protection Fund Contents Foreword 3 1. About us 4 1.1 This is what we do 4 1.2 Our strategic framework 5 2. The next three years: 2014 2017 6 2.1 Our vision of the PPF in 2017

STRATEGIC PLAN 2014 Pension Protection Fund Contents Foreword 3 1. About us 4 1.1 This is what we do 4 1.2 Our strategic framework 5 2. The next three years: 2014 2017 6 2.1 Our vision of the PPF in 2017

Joint Forum on Actuarial Regulation: 2016 risk perspective update

Update Professional discipline Financial Reporting Council December 2016 Joint Forum on Actuarial Regulation: 2016 risk perspective update The FRC is responsible for promoting high quality corporate governance

Update Professional discipline Financial Reporting Council December 2016 Joint Forum on Actuarial Regulation: 2016 risk perspective update The FRC is responsible for promoting high quality corporate governance

Pillar 3 Disclosure ICAP Europe Limited

Pillar 3 Disclosure 31 st March 2017 1. INTRODUCTION AND SCOPE The purpose of this report is to meet Pillar 3 requirements laid out by the European Banking Authority (EBA) in Part Eight of the Capital

Pillar 3 Disclosure 31 st March 2017 1. INTRODUCTION AND SCOPE The purpose of this report is to meet Pillar 3 requirements laid out by the European Banking Authority (EBA) in Part Eight of the Capital

Paper 2 Employers Pensions Forum (EPF) USS Town Hall Event USS Mutuality: Flexibility of pension cost and provision an introduction

USS Town Hall Event USS Mutuality: Flexibility of pension cost and provision an introduction") Paper 2 Employers Pensions Forum (EPF) USS Town Hall Event USS Mutuality: Flexibility of pension cost and provision an introduction Contact/s Mary Lambe Senior Policy Lead Pensions and HE Infrastructure

Paper 2 Employers Pensions Forum (EPF) USS Town Hall Event USS Mutuality: Flexibility of pension cost and provision an introduction Contact/s Mary Lambe Senior Policy Lead Pensions and HE Infrastructure

Subject CA1 Actuarial Risk Management

Institute of Actuaries of India Subject CA1 Actuarial Risk Management For 2018 Examinations Subject CA1 Actuarial Risk Management Syllabus Aim The aim of the Actuarial Risk Management subject is that upon

Institute of Actuaries of India Subject CA1 Actuarial Risk Management For 2018 Examinations Subject CA1 Actuarial Risk Management Syllabus Aim The aim of the Actuarial Risk Management subject is that upon

Preparing for an Own Risk & Solvency Assessment

www.pwc.com Preparing for an Own Risk & Solvency Assessment March 2013 Brian Paton Director, Insurance Risk and Capital Practice brian.paton@us.pwc.com Contents 1. ORSA challenges 2. ORSA readiness and

www.pwc.com Preparing for an Own Risk & Solvency Assessment March 2013 Brian Paton Director, Insurance Risk and Capital Practice brian.paton@us.pwc.com Contents 1. ORSA challenges 2. ORSA readiness and

ANNUAL DISCLOSURES FOR 2010 ON AN UNCONSOLIDATED BASIS

ANNUAL DISCLOSURES FOR 2010 ON AN UNCONSOLIDATED BASIS ACCORDING TO THE REQUIREMENTS OF ORDINANCE 8 OF THE BULGARIAN NATIONAL BANK FOR THE CAPITAL ADEQUACY OF CREDIT INSTITUTIONS /ART. 335 OF ORDINANCE

ANNUAL DISCLOSURES FOR 2010 ON AN UNCONSOLIDATED BASIS ACCORDING TO THE REQUIREMENTS OF ORDINANCE 8 OF THE BULGARIAN NATIONAL BANK FOR THE CAPITAL ADEQUACY OF CREDIT INSTITUTIONS /ART. 335 OF ORDINANCE

Pension Protection Fund

Pension Protection Fund Protecting people s futures 2017/2018 Annual Report & Accounts HC 1229 Pension Protection Fund Annual Report & Accounts 2017/18 3 Pension Protection Fund Annual Report & Accounts

Pension Protection Fund Protecting people s futures 2017/2018 Annual Report & Accounts HC 1229 Pension Protection Fund Annual Report & Accounts 2017/18 3 Pension Protection Fund Annual Report & Accounts

BAILLIE GIFFORD. Governance, Risk Management and Capital Disclosures ( Pillar 3 ) June 2018

June 2018") BAILLIE GIFFORD Governance, Risk Management and Capital Disclosures ( Pillar 3 ) June 2018 Contents Introduction and Context 3 Purpose of Disclosures Scope Basis of Preparation Governance Arrangements

BAILLIE GIFFORD Governance, Risk Management and Capital Disclosures ( Pillar 3 ) June 2018 Contents Introduction and Context 3 Purpose of Disclosures Scope Basis of Preparation Governance Arrangements

Solvency Assessment and Management: Stress Testing Task Group Discussion Document 96 (v 3) General Stress Testing Guidance for Insurance Companies

General Stress Testing Guidance for Insurance Companies") Solvency Assessment and Management: Stress Testing Task Group Discussion Document 96 (v 3) General Stress Testing Guidance for Insurance Companies 1 INTRODUCTION AND PURPOSE The business of insurance is

Solvency Assessment and Management: Stress Testing Task Group Discussion Document 96 (v 3) General Stress Testing Guidance for Insurance Companies 1 INTRODUCTION AND PURPOSE The business of insurance is

Opinion of the EBA on Good Practices for ETF Risk Management

EBA-Op-2013-01 7 March 2013 Opinion of the EBA on Good Practices for ETF Risk Management Table of contents Table of contents 2 Introduction 4 I. Good Practices for ETF business 6 II. Considerations for

EBA-Op-2013-01 7 March 2013 Opinion of the EBA on Good Practices for ETF Risk Management Table of contents Table of contents 2 Introduction 4 I. Good Practices for ETF business 6 II. Considerations for

RISK APPETITE OVERVIEW

PUBLIC SECTOR PENSION INVESTMENT BOARD ( PSP INVESTMENTS ) RISK APPETITE OVERVIEW February 10, 2017 PSP-Legal 2684702-1 Introduction Maintaining a risk aware culture in which undue risks are avoided and

PUBLIC SECTOR PENSION INVESTMENT BOARD ( PSP INVESTMENTS ) RISK APPETITE OVERVIEW February 10, 2017 PSP-Legal 2684702-1 Introduction Maintaining a risk aware culture in which undue risks are avoided and

Enterprise Risk Management Economic Capital Modleing and the Financial Crisis

Risk Management and The Crisis Enterprise Risk Management Economic Capital Modleing and the Financial Crisis What worked and what did not Insurance Industry Continues to Respond to Risk Dynamics Risk Sources

Risk Management and The Crisis Enterprise Risk Management Economic Capital Modleing and the Financial Crisis What worked and what did not Insurance Industry Continues to Respond to Risk Dynamics Risk Sources

The Pension Protection Fund

The Pension Protection Fund Regulation and Risk Management Partha Dasgupta Chief Executive Pension Protection Fund in Context Mega Trends Climate Change Rise of financial economics International accounting

The Pension Protection Fund Regulation and Risk Management Partha Dasgupta Chief Executive Pension Protection Fund in Context Mega Trends Climate Change Rise of financial economics International accounting

Asset management for insurers A brave new world

Asset management for insurers A brave new world Dirk Jan Klein Essink Chief Financial Officer TVM Verzekeringen Han Rijken Head of Insurance Investments NN Investment Partners Erwin Houbrechts Director

Asset management for insurers A brave new world Dirk Jan Klein Essink Chief Financial Officer TVM Verzekeringen Han Rijken Head of Insurance Investments NN Investment Partners Erwin Houbrechts Director

NAIC ORSA: A Practical Guide to the DOI s First Year Reviews

ZZ NAIC ORSA: A Practical Guide to the DOI s First Year Reviews Eli Russo Sherry Flippo NAIC 2 Attention APIR, PIR, or SPIR Designees This presentation is pre-qualified for NAIC Designation Renewal Credits

ZZ NAIC ORSA: A Practical Guide to the DOI s First Year Reviews Eli Russo Sherry Flippo NAIC 2 Attention APIR, PIR, or SPIR Designees This presentation is pre-qualified for NAIC Designation Renewal Credits

IT Risk in Credit Unions - Thematic Review Findings

IT Risk in Credit Unions - Thematic Review Findings January 2018 Central Bank of Ireland Findings from IT Thematic Review in Credit Unions Page 2 Table of Contents 1. Executive Summary... 3 1.1 Purpose...

IT Risk in Credit Unions - Thematic Review Findings January 2018 Central Bank of Ireland Findings from IT Thematic Review in Credit Unions Page 2 Table of Contents 1. Executive Summary... 3 1.1 Purpose...

Risks and risk management

Strategic report Risks and risk management In 20 we undertook a comprehensive risk review and present our updated findings in this report. Nick Anderson Chairman, Risk Management Committee Board Reports

Strategic report Risks and risk management In 20 we undertook a comprehensive risk review and present our updated findings in this report. Nick Anderson Chairman, Risk Management Committee Board Reports

Financial Review. Volume (case equivalents) 8.4m 8.2m 2% Core revenue 706.7m 663.1m 7% Brand investment expenditure 125.7m 120.

8.4m 8.2m 2% Core revenue 706.7m 663.1m 7% Brand investment expenditure 125.7m 120.") Financial Review MANAGEMENT KEY PERFORMANCE INDICATORS 2018 2017 % movement Volume (case equivalents) 8.4m 8.2m 2% Presented in constant currency rates: Core revenue 706.7m 663.1m 7% Brand investment expenditure

Financial Review MANAGEMENT KEY PERFORMANCE INDICATORS 2018 2017 % movement Volume (case equivalents) 8.4m 8.2m 2% Presented in constant currency rates: Core revenue 706.7m 663.1m 7% Brand investment expenditure

The Pensions Regulator s annual defined benefit funding statement 2015

The Pensions Regulator s annual defined benefit funding statement 2015 The implications for trustees and sponsors Graham McLean, Gareth Connolly and Bina Mistry 28 May 2015 Presenting today Graham McLean

The Pensions Regulator s annual defined benefit funding statement 2015 The implications for trustees and sponsors Graham McLean, Gareth Connolly and Bina Mistry 28 May 2015 Presenting today Graham McLean

17/06/2012. Solvency II: Implementation Challenges & Opportunities. What is Solvency II about?

What is Solvency II about? Solvency II: Implementation Challenges & Opportunities The Solvency II Directive is a regulatory framework for the European insurance industry that adopts a more dynamic and

What is Solvency II about? Solvency II: Implementation Challenges & Opportunities The Solvency II Directive is a regulatory framework for the European insurance industry that adopts a more dynamic and

Guidance Note: Stress Testing Credit Unions with Assets Greater than $500 million. May Ce document est également disponible en français.

Guidance Note: Stress Testing Credit Unions with Assets Greater than $500 million May 2017 Ce document est également disponible en français. Applicability This Guidance Note is for use by all credit unions

Guidance Note: Stress Testing Credit Unions with Assets Greater than $500 million May 2017 Ce document est également disponible en français. Applicability This Guidance Note is for use by all credit unions

BAILLIE GIFFORD. Governance, Risk Management and Capital Disclosures ( Pillar 3 ) June 2017

June 2017") BAILLIE GIFFORD Governance, Risk Management and Capital Disclosures ( Pillar 3 ) June 2017 Contents Introduction and Context 3 Purpose of Disclosures Scope Basis of Preparation Governance Arrangements

BAILLIE GIFFORD Governance, Risk Management and Capital Disclosures ( Pillar 3 ) June 2017 Contents Introduction and Context 3 Purpose of Disclosures Scope Basis of Preparation Governance Arrangements

By way of background, Carillion (DB) Pension Trustee limited became trustee of the 6 schemes on 1 April I have been chairman since that date.

Pension Trustee limited became trustee of the 6 schemes on 1 April I have been chairman since that date.") Rt Hon Frank Field MP Chair Work and Pensions Committee House of Commons London SW1A 0AA workpencom@parliament.uk By email 26 January 2018 Dear Mr Field Carillion (DB) Pension Trustee Many thanks for your

Rt Hon Frank Field MP Chair Work and Pensions Committee House of Commons London SW1A 0AA workpencom@parliament.uk By email 26 January 2018 Dear Mr Field Carillion (DB) Pension Trustee Many thanks for your

Ashmore Group plc Pillar 3 Disclosures as at 30 June 2018

Ashmore Group plc Pillar 3 Disclosures as at 30 June 2018 Table of Contents 1. OVERVIEW 3 1.1 BASIS OF DISCLOSURES 1.2 FREQUENCY OF DISCLOSURES 1.3 MEDIA AND LOCATION OF DISCLOSURES 2. CORPORATE GOVERNANCE

Ashmore Group plc Pillar 3 Disclosures as at 30 June 2018 Table of Contents 1. OVERVIEW 3 1.1 BASIS OF DISCLOSURES 1.2 FREQUENCY OF DISCLOSURES 1.3 MEDIA AND LOCATION OF DISCLOSURES 2. CORPORATE GOVERNANCE

Strategic Report Risk and risk management ENGINEERING SUSTAINABLE VALUE BY MANAGING RISK

Strategic Report Risk and risk management ENGINEERING SUSTAINABLE VALUE BY MANAGING RISK In 2016 we undertook a risk appetite assessment and in 2017 we will be reviewing the structure of our internal audit

Strategic Report Risk and risk management ENGINEERING SUSTAINABLE VALUE BY MANAGING RISK In 2016 we undertook a risk appetite assessment and in 2017 we will be reviewing the structure of our internal audit

Merchant Navy Officers Pension Fund (MNOPF) Statement of Investment Principles

Statement of Investment Principles") Merchant Navy Officers Pension Fund (MNOPF) Statement of Investment Principles Introduction The main purpose of the MNOPF is to provide pensions on retirement at normal pension age for Officers in the

Merchant Navy Officers Pension Fund (MNOPF) Statement of Investment Principles Introduction The main purpose of the MNOPF is to provide pensions on retirement at normal pension age for Officers in the

Capital Requirements Directive Pillar 3 Disclosure

Capital Requirements Directive Pillar 3 Disclosure Contents: Contents 1. Introduction... 2 2. Scope and Application of Directive Requirements... 2 3. Risk Management Objectives and Policy... 4 4. Key Risk

Capital Requirements Directive Pillar 3 Disclosure Contents: Contents 1. Introduction... 2 2. Scope and Application of Directive Requirements... 2 3. Risk Management Objectives and Policy... 4 4. Key Risk

Trustee Statement of Investment Principles

Trustee Statement of Investment Principles Reviewed by the Investment Committee: June 2017 Approved by the Trustee Board: September 2017 1. Introduction 1.1. The Pensions Trust is an occupational pension

Trustee Statement of Investment Principles Reviewed by the Investment Committee: June 2017 Approved by the Trustee Board: September 2017 1. Introduction 1.1. The Pensions Trust is an occupational pension

BANKING CONVENTIONAL. Overview

CONVENTIONAL BANKING Overview Is the Bank s Board spending enough time and resources on making sure the Bank is developing the desired culture and is it strong enough to be sustainable for the long run?

CONVENTIONAL BANKING Overview Is the Bank s Board spending enough time and resources on making sure the Bank is developing the desired culture and is it strong enough to be sustainable for the long run?

It s safe to say that over the past 10

BEST PRACTICES CalPERS A Plan for Reigning in Risk By Cheryl Eason The California Public Employees Retirement System developed a funding risk-mitigation policy that will lower the discount rate in years

BEST PRACTICES CalPERS A Plan for Reigning in Risk By Cheryl Eason The California Public Employees Retirement System developed a funding risk-mitigation policy that will lower the discount rate in years

Subject SP9 Enterprise Risk Management Specialist Principles Syllabus

Subject SP9 Enterprise Risk Management Specialist Principles Syllabus for the 2019 exams 1 June 2018 Enterprise Risk Management Specialist Principles Aim The aim of the Enterprise Risk Management (ERM)

Subject SP9 Enterprise Risk Management Specialist Principles Syllabus for the 2019 exams 1 June 2018 Enterprise Risk Management Specialist Principles Aim The aim of the Enterprise Risk Management (ERM)

COLUMBIA THREADNEEDLE Threadneedle Pensions Limited Solvency and Financial Condition Report

COLUMBIA THREADNEEDLE Threadneedle Pensions Limited Solvency and Financial Condition Report 31 December 2016 Report date: 19 May 2017 Contents 1. Summary... 3 1.1 Business and performance... 3 1.2 System

COLUMBIA THREADNEEDLE Threadneedle Pensions Limited Solvency and Financial Condition Report 31 December 2016 Report date: 19 May 2017 Contents 1. Summary... 3 1.1 Business and performance... 3 1.2 System

Capital and Risk Management Pillar 3 Disclosures

Capital and Risk Management Pillar 3 Disclosures For Year Ended 31 st December 2016 Contents 1. Introduction... 3 1.1 Background... 3 1.2 Scope... 3 1.3 Frequency of Disclosure... 4 2. Key Measures & Ratios...

Capital and Risk Management Pillar 3 Disclosures For Year Ended 31 st December 2016 Contents 1. Introduction... 3 1.1 Background... 3 1.2 Scope... 3 1.3 Frequency of Disclosure... 4 2. Key Measures & Ratios...

Key Risk Indicators (KRI) Survey September 2011

Survey September 2011") Key Risk Indicators (KRI) Survey September 2011 KRI Survey September 2011 This RMA Survey was intended to capture the current status of key risk indicators (KRIs) across a range of institutions and also

Key Risk Indicators (KRI) Survey September 2011 KRI Survey September 2011 This RMA Survey was intended to capture the current status of key risk indicators (KRIs) across a range of institutions and also

Annual Report & Accounts 2013/14

Annual Report & Accounts 2013/14 Protecting people s futures Annual Report & Accounts 2013/14 Annual report presented to Parliament pursuant to Section 119(5) of the Pensions Act 2004 and Accounts presented

Annual Report & Accounts 2013/14 Protecting people s futures Annual Report & Accounts 2013/14 Annual report presented to Parliament pursuant to Section 119(5) of the Pensions Act 2004 and Accounts presented

Keeping Pace With Solvency II

Keeping Pace With Solvency II Challenges and Opportunities Facing Insurers By Gerard L Aimable, Colin Murray and Naren Persad Scheduled for 2013, Solvency II will introduce a risk-based regulatory framework

Keeping Pace With Solvency II Challenges and Opportunities Facing Insurers By Gerard L Aimable, Colin Murray and Naren Persad Scheduled for 2013, Solvency II will introduce a risk-based regulatory framework

Statement of Investment Principles

Statement of Investment Principles Cheshire Pension Fund November 2014 Page 1 of 15 Introduction The Cheshire Pension Fund ( The Fund ) is required to publish a Statement of Investment Principles (SIP)

Statement of Investment Principles Cheshire Pension Fund November 2014 Page 1 of 15 Introduction The Cheshire Pension Fund ( The Fund ) is required to publish a Statement of Investment Principles (SIP)

REGULATORY GUIDELINE Liquidity Risk Management Principles TABLE OF CONTENTS. I. Introduction II. Purpose and Scope III. Principles...

REGULATORY GUIDELINE Liquidity Risk Management Principles SYSTEM COMMUNICATION NUMBER Guideline 2015-02 ISSUE DATE June 2015 TABLE OF CONTENTS I. Introduction... 1 II. Purpose and Scope... 1 III. Principles...

REGULATORY GUIDELINE Liquidity Risk Management Principles SYSTEM COMMUNICATION NUMBER Guideline 2015-02 ISSUE DATE June 2015 TABLE OF CONTENTS I. Introduction... 1 II. Purpose and Scope... 1 III. Principles...

Risk Appetite Survey Current state of the Insurance Industry

Risk Appetite Survey Current state of the Insurance Industry Deloitte Belgium and The Netherlands Financial Services Industry The survey was conducted during July 2013 till December 2013 Introduction The

Risk Appetite Survey Current state of the Insurance Industry Deloitte Belgium and The Netherlands Financial Services Industry The survey was conducted during July 2013 till December 2013 Introduction The

Society of Actuaries - ERM Forum, 10 May 2016 A regulatory perspective on consumer risk

Society of Actuaries - ERM Forum, 10 May 2016 A regulatory perspective on consumer risk Helena Mitchell Head of Consumer Protection: Supervision Division Contents What is conduct risk and consumer risk?

Society of Actuaries - ERM Forum, 10 May 2016 A regulatory perspective on consumer risk Helena Mitchell Head of Consumer Protection: Supervision Division Contents What is conduct risk and consumer risk?

Glossary. Active member. Acronyms. Administration. Aggregate funding position. Assessment period. Buy-out basis. Closed (to new members)

") Glossary Active member In relation to an occupational pension scheme, a person who is in pensionable service under the scheme. Acronyms LDI Liability-driven investment ONS Office for National Statistics

Glossary Active member In relation to an occupational pension scheme, a person who is in pensionable service under the scheme. Acronyms LDI Liability-driven investment ONS Office for National Statistics

Proposed Approach to the Methodology for the 2017 Actuarial Valuation. Response to the Valuation Discussion Forum (VDF)

") Proposed Approach to the Methodology for the 2017 Actuarial Valuation Response to the Valuation Discussion Forum (VDF) 22 November 2016 Summary This paper addresses the methodology to be used in the 2017

Proposed Approach to the Methodology for the 2017 Actuarial Valuation Response to the Valuation Discussion Forum (VDF) 22 November 2016 Summary This paper addresses the methodology to be used in the 2017

Security and Sustainability in Defined Benefit Pension Schemes Green Paper Questions and NFOP Responses

Security and Sustainability in Defined Benefit Pension Schemes Green Paper Questions and NFOP Responses OVERVIEW NFOP represents 65,000 individual pensioners predominantly in three Defined Benefit Pension

Security and Sustainability in Defined Benefit Pension Schemes Green Paper Questions and NFOP Responses OVERVIEW NFOP represents 65,000 individual pensioners predominantly in three Defined Benefit Pension

Solvency II Detailed guidance notes for dry run process. March 2010

Solvency II Detailed guidance notes for dry run process March 2010 Introduction The successful implementation of Solvency II at Lloyd s is critical to maintain the competitive position and capital advantages

Solvency II Detailed guidance notes for dry run process March 2010 Introduction The successful implementation of Solvency II at Lloyd s is critical to maintain the competitive position and capital advantages

Capital Requirements Directive Pillar 3 Disclosures For the year ended 31 August 2017

Capital Requirements Directive Pillar 3 Disclosures For the year ended 31 August 2017 Contents INTRODUCTION... 2 RISK MANAGEMENT POLICIES AND OBJECTIVES... 3 BOARD & SUB-COMMITTEES... 3 THREE LINES OF

Capital Requirements Directive Pillar 3 Disclosures For the year ended 31 August 2017 Contents INTRODUCTION... 2 RISK MANAGEMENT POLICIES AND OBJECTIVES... 3 BOARD & SUB-COMMITTEES... 3 THREE LINES OF

2014 Own Risk and Solvency Assessment (ORSA) Feedback Pilot Project Observations of the Group Solvency Issues (E) Working Group

Feedback Pilot Project Observations of the Group Solvency Issues (E) Working Group") 2014 Own Risk and Solvency Assessment (ORSA) Feedback Pilot Project Observations of the Group Solvency Issues (E) Working Group During October 2014 through June 2015, a third ORSA Feedback Pilot Project

2014 Own Risk and Solvency Assessment (ORSA) Feedback Pilot Project Observations of the Group Solvency Issues (E) Working Group During October 2014 through June 2015, a third ORSA Feedback Pilot Project

The Purple Book DB PENSIONS UNIVERSE RISK PROFILE

The Purple Book DB PENSIONS UNIVERSE RISK PROFILE 2017 2 the purple book 2017 The Purple Books give the most comprehensive picture of the risks faced by the PPF-eligible defined benefit pension schemes.

The Purple Book DB PENSIONS UNIVERSE RISK PROFILE 2017 2 the purple book 2017 The Purple Books give the most comprehensive picture of the risks faced by the PPF-eligible defined benefit pension schemes.

Own Risk and Solvency Assessment

Own Risk and Solvency Assessment Acumen Conference 2015 Elaine Hultzer, Insurance Audit & Advisory Partner, Deloitte Sati MacLean, Senior P&C Actuarial Manager, Deloitte June 10 th, 2015 Agenda Introduction

Own Risk and Solvency Assessment Acumen Conference 2015 Elaine Hultzer, Insurance Audit & Advisory Partner, Deloitte Sati MacLean, Senior P&C Actuarial Manager, Deloitte June 10 th, 2015 Agenda Introduction

Agenda. Agenda (cont.) Risk Management Association. Loss Data in an Organization s DNA

Risk Management Association. Loss Data in an Organization s DNA") Risk Management Association Internal Loss Events: Embedding Internal Loss Data in an Organization s DNA Agenda Overview and Context Background on Loss Data Defining the Objectives Objectives of Collecting

Risk Management Association Internal Loss Events: Embedding Internal Loss Data in an Organization s DNA Agenda Overview and Context Background on Loss Data Defining the Objectives Objectives of Collecting

KRUNG THAI BANK PUBLIC COMPANY LIMITED

KRUNG THAI BANK PUBLIC COMPANY LIMITED Basel II Pillar III Disclosure Risk Management & Compliance Group Page 1 of 24 Basel II Pillar III Disclosures Krung Thai Bank PCL has applied the Basel II Standardised

KRUNG THAI BANK PUBLIC COMPANY LIMITED Basel II Pillar III Disclosure Risk Management & Compliance Group Page 1 of 24 Basel II Pillar III Disclosures Krung Thai Bank PCL has applied the Basel II Standardised

Finance and Asset Management for Long Term Delivery

Finance and Asset Management for Long Term Delivery Financing Social Housing John O Connor PwC Agenda UK Experience AHB Funding Options UK Market Evolution Pre 1988 mostly grant funded Since 1988 grants

Finance and Asset Management for Long Term Delivery Financing Social Housing John O Connor PwC Agenda UK Experience AHB Funding Options UK Market Evolution Pre 1988 mostly grant funded Since 1988 grants

WHITE PAPER. Solvency II Compliance and beyond: Title The essential steps for insurance firms

WHITE PAPER Solvency II Compliance and beyond: Title The essential steps for insurance firms ii Contents Introduction... 1 Step 1 Data Management... 1 Step 2 Risk Calculations... 3 Solvency Capital Requirement

WHITE PAPER Solvency II Compliance and beyond: Title The essential steps for insurance firms ii Contents Introduction... 1 Step 1 Data Management... 1 Step 2 Risk Calculations... 3 Solvency Capital Requirement

A value-based approach to the redesign of US state pension plans

A value-based approach to the redesign of US state pension plans Zina Lekniūtė, Roel Beetsma, Eduard Ponds May 28, 2014 Are state pensions in trouble? The practice is to downplay the problem. Expected

A value-based approach to the redesign of US state pension plans Zina Lekniūtė, Roel Beetsma, Eduard Ponds May 28, 2014 Are state pensions in trouble? The practice is to downplay the problem. Expected

Continuing the journey

Continuing the journey Risk and ICAAP Benchmarking Survey 2016 Insights into evolving risk management practices for investment firms. November 2016 kpmg.com/uk Introduction David Yim Partner I m delighted

Continuing the journey Risk and ICAAP Benchmarking Survey 2016 Insights into evolving risk management practices for investment firms. November 2016 kpmg.com/uk Introduction David Yim Partner I m delighted

LLOYDS BANKING GROUP PLC ANNUAL REPORT AND ACCOUNTS FOR THE YEAR ENDED 31 DECEMBER 2017

21 February 2018 LLOYDS BANKING GROUP PLC ANNUAL REPORT AND ACCOUNTS FOR THE YEAR ENDED 31 DECEMBER In accordance with Listing Rule 9.6.1, Lloyds Banking Group plc has submitted today the following document

21 February 2018 LLOYDS BANKING GROUP PLC ANNUAL REPORT AND ACCOUNTS FOR THE YEAR ENDED 31 DECEMBER In accordance with Listing Rule 9.6.1, Lloyds Banking Group plc has submitted today the following document

An Introduction to the Buy-Out Market. Mark Wood, Paternoster P A T E R N O S T E R. Cass Business School 13 September 2006

An Introduction to the Buy-Out Market Mark Wood, Paternoster Cass Business School 13 September 2006 Development of a new market The traditional buy-out market for schemes in wind-up is changing as a new

An Introduction to the Buy-Out Market Mark Wood, Paternoster Cass Business School 13 September 2006 Development of a new market The traditional buy-out market for schemes in wind-up is changing as a new

Rolling Up Operational Risk

Rolling Up Operational Risk SHARI BREITEN Director, Operational Risk September 17, 2015 Historical Perspective Goals & Objectives Industry Challenges Solutions HISTORICAL PERSPECTIVE: Regulatory Environment

Rolling Up Operational Risk SHARI BREITEN Director, Operational Risk September 17, 2015 Historical Perspective Goals & Objectives Industry Challenges Solutions HISTORICAL PERSPECTIVE: Regulatory Environment

ICBC LONDON Tax Strategy

ICBC LONDON Tax Strategy This document details the strategic tax objectives of the Industrial and Commercial Bank of China Limited London Branch and ICBC (London) plc, known collectively as ICBC London

ICBC LONDON Tax Strategy This document details the strategic tax objectives of the Industrial and Commercial Bank of China Limited London Branch and ICBC (London) plc, known collectively as ICBC London

Academy Presentation to NAIC ORSA Implementation (E) Subgroup

Subgroup") Academy Presentation to NAIC ORSA Implementation (E) Subgroup Tricia Matson, MAAA, FSA Chairperson, Enterprise Risk Management (ERM) and Own Risk and Solvency Assessment (ORSA) Committee August 10, 2016

Academy Presentation to NAIC ORSA Implementation (E) Subgroup Tricia Matson, MAAA, FSA Chairperson, Enterprise Risk Management (ERM) and Own Risk and Solvency Assessment (ORSA) Committee August 10, 2016

Relevance of Operational Risk to the FCA Jill Savager Manager, Operational Risk, Financial Conduct Authority

Relevance of Operational Risk to the FCA Jill Savager Manager, Operational Risk, Financial Conduct Authority IOR Scottish Chapter Annual Conference Glasgow Caledonian University 01/11/13 1 What we will

Relevance of Operational Risk to the FCA Jill Savager Manager, Operational Risk, Financial Conduct Authority IOR Scottish Chapter Annual Conference Glasgow Caledonian University 01/11/13 1 What we will

Finance and Asset Management for Long Term Delivery. ICSH National Social Housing Conference, Limerick. 27 September 2017

Finance and Asset Management for Long Term Delivery ICSH National Social Housing Conference, Limerick 27 September 2017 Susanna Lyons Head Of Regulation Regulatory Focus Our mission is to protect AHB assets

Finance and Asset Management for Long Term Delivery ICSH National Social Housing Conference, Limerick 27 September 2017 Susanna Lyons Head Of Regulation Regulatory Focus Our mission is to protect AHB assets

Operational Risk Management: How Emerging Best Practices Can Improve Performance

Operational Risk Management: Enter Presentation Title Here How Emerging Best Practices Can Improve Performance Charles Taylor Director, Operational Risk RMA 1 BBC Photograph 2 Controls Failures New Business

Operational Risk Management: Enter Presentation Title Here How Emerging Best Practices Can Improve Performance Charles Taylor Director, Operational Risk RMA 1 BBC Photograph 2 Controls Failures New Business

Disclosure Prudential Disclosure Report. 12/31/2017 Derayah Financial

Derayah - Pillar III Disclosure -2017 Prudential Disclosure Report 12/31/2017 Derayah Financial Table of Contents 1. OVERVIEW... 2 2. CAPITAL STRUCTURE... 2 2.1. Disclosure on Capital Base... 3 3. CAPITAL

Derayah - Pillar III Disclosure -2017 Prudential Disclosure Report 12/31/2017 Derayah Financial Table of Contents 1. OVERVIEW... 2 2. CAPITAL STRUCTURE... 2 2.1. Disclosure on Capital Base... 3 3. CAPITAL

BERMUDA MONETARY AUTHORITY BANKS AND DEPOSIT COMPANIES ACT 1999: PRINCIPLES FOR SOUND LIQUIDITY RISK MANAGEMENT AND SUPERVISION

BERMUDA MONETARY AUTHORITY BANKS AND DEPOSIT COMPANIES ACT 1999: PRINCIPLES FOR SOUND LIQUIDITY RISK MANAGEMENT AND SUPERVISION DECEMBER 2010 Table of Contents Introduction... 3 1. Approach to liquidity

BERMUDA MONETARY AUTHORITY BANKS AND DEPOSIT COMPANIES ACT 1999: PRINCIPLES FOR SOUND LIQUIDITY RISK MANAGEMENT AND SUPERVISION DECEMBER 2010 Table of Contents Introduction... 3 1. Approach to liquidity

An Introduction to Solvency II

An Introduction to Solvency II Peter Withey KPMG Agenda 1. Background to Solvency II 2. Pillar 1: Quantitative Pillar Basic building blocks Assets Technical Reserves Solvency Capital Requirement Internal

An Introduction to Solvency II Peter Withey KPMG Agenda 1. Background to Solvency II 2. Pillar 1: Quantitative Pillar Basic building blocks Assets Technical Reserves Solvency Capital Requirement Internal

Introducing the 2016 Summary Funding Statement to all defined benefit (DB) members and beneficiaries of the Capgemini UK Pension Plan ( the Plan )

members and beneficiaries of the Capgemini UK Pension Plan ( the Plan )") Introducing the 2016 Summary Funding Statement to all defined benefit (DB) members and beneficiaries of the Capgemini UK Pension Plan ( the Plan ) As the Trustees of the Plan, we are required to send you

Introducing the 2016 Summary Funding Statement to all defined benefit (DB) members and beneficiaries of the Capgemini UK Pension Plan ( the Plan ) As the Trustees of the Plan, we are required to send you

Outline Capital Investment Strategy

Outline Capital Investment Strategy INDEX FOREWORD 1. INTRODUCTION 2. PURPOSE 3. SUMMARY 4. INFLUENCES ON CAPITAL INVESTMENT 5. CURRENT CAPITAL EXPENDITURE 6. COMMERCIAL PROPERTY INVESTMENT STRATEGY 7.

Outline Capital Investment Strategy INDEX FOREWORD 1. INTRODUCTION 2. PURPOSE 3. SUMMARY 4. INFLUENCES ON CAPITAL INVESTMENT 5. CURRENT CAPITAL EXPENDITURE 6. COMMERCIAL PROPERTY INVESTMENT STRATEGY 7.

Foundations of Risk Management

Foundations of Risk Management Introduction Level 1 Foundations of Risk Management Topics 1. 2. CORPORATE RISK MANAGEMENT: A PRIMER 3. CORPORATE GOVERNANCE AND RISK MANAGEMENT 4. WHAT IS ERM? 5. RISK-TAKING

Foundations of Risk Management Introduction Level 1 Foundations of Risk Management Topics 1. 2. CORPORATE RISK MANAGEMENT: A PRIMER 3. CORPORATE GOVERNANCE AND RISK MANAGEMENT 4. WHAT IS ERM? 5. RISK-TAKING

A summary of changes to the PPF Levy for 2015/16

A summary of changes to the PPF Levy for 2015/16 Executive summary The PPF has confirmed that a number of changes will be made to the levy it charges to all eligible DB schemes. The key changes have already

A summary of changes to the PPF Levy for 2015/16 Executive summary The PPF has confirmed that a number of changes will be made to the levy it charges to all eligible DB schemes. The key changes have already

WORK AND PENSIONS SELECT COMMITTEE INQUIRY INTO DEFINED BENEFIT PENSION SCHEMES

The Financial Inclusion Centre Financial markets that work for society WORK AND PENSIONS SELECT COMMITTEE INQUIRY INTO DEFINED BENEFIT PENSION SCHEMES Introduction 1. The Financial Inclusion Centre is

The Financial Inclusion Centre Financial markets that work for society WORK AND PENSIONS SELECT COMMITTEE INQUIRY INTO DEFINED BENEFIT PENSION SCHEMES Introduction 1. The Financial Inclusion Centre is

BB&T Corporation. Dodd-Frank Act Company-run Mid-cycle Stress Test Disclosure BB&T Severely Adverse Scenario

BB&T Corporation Dodd-Frank Act Company-run Mid-cycle Stress Test Disclosure BB&T Severely Adverse Scenario October 19, 2017 1 Introduction BB&T Corporation (BB&T) is one of the largest financial services

BB&T Corporation Dodd-Frank Act Company-run Mid-cycle Stress Test Disclosure BB&T Severely Adverse Scenario October 19, 2017 1 Introduction BB&T Corporation (BB&T) is one of the largest financial services

BERMUDA MONETARY AUTHORITY GUIDELINES ON STRESS TESTING FOR THE BERMUDA BANKING SECTOR

GUIDELINES ON STRESS TESTING FOR THE BERMUDA BANKING SECTOR TABLE OF CONTENTS 1. EXECUTIVE SUMMARY...2 2. GUIDANCE ON STRESS TESTING AND SCENARIO ANALYSIS...3 3. RISK APPETITE...6 4. MANAGEMENT ACTION...6

GUIDELINES ON STRESS TESTING FOR THE BERMUDA BANKING SECTOR TABLE OF CONTENTS 1. EXECUTIVE SUMMARY...2 2. GUIDANCE ON STRESS TESTING AND SCENARIO ANALYSIS...3 3. RISK APPETITE...6 4. MANAGEMENT ACTION...6

CAPITAL REQUIREMENTS DIRECTIVE PILLAR 3 DISCLOSURE DOCUMENT 31 ST MARCH P a g e

CAPITAL REQUIREMENTS DIRECTIVE PILLAR 3 DISCLOSURE DOCUMENT 31 ST MARCH 2017 1 P a g e CONTENTS Page 1. Introduction 3 2. Risk Management Objectives and Policies 3-7 3. Capital Resources 7 4. Capital Adequacy

CAPITAL REQUIREMENTS DIRECTIVE PILLAR 3 DISCLOSURE DOCUMENT 31 ST MARCH 2017 1 P a g e CONTENTS Page 1. Introduction 3 2. Risk Management Objectives and Policies 3-7 3. Capital Resources 7 4. Capital Adequacy

Pillar 3 Disclosure Statement

Pillar 3 Disclosure Statement Last Updated: December, 2017 Disclosure Statement This Pillar 3 Disclosure as at September 30, 2017 contains statements that are considered "forwardlooking statements," including

Pillar 3 Disclosure Statement Last Updated: December, 2017 Disclosure Statement This Pillar 3 Disclosure as at September 30, 2017 contains statements that are considered "forwardlooking statements," including

Operational Risk Management

Operational Risk Management An Iceberg but Icebergs can melt DMF Stakeholders Forum Berlin, May 2013 Mike Williams mike.williams@mj-w.net Operational risk is: The risk of loss (financial or nonfinancial)

Operational Risk Management An Iceberg but Icebergs can melt DMF Stakeholders Forum Berlin, May 2013 Mike Williams mike.williams@mj-w.net Operational risk is: The risk of loss (financial or nonfinancial)

COMMUNIQUE. Page 1 of 13

COMMUNIQUE 16-COM-001 Feb. 1, 2016 Release of Liquidity Risk Management Guiding Principles The Credit Union Prudential Supervisors Association (CUPSA) has released guiding principles for Liquidity Risk

COMMUNIQUE 16-COM-001 Feb. 1, 2016 Release of Liquidity Risk Management Guiding Principles The Credit Union Prudential Supervisors Association (CUPSA) has released guiding principles for Liquidity Risk

LEGAL & GENERAL GROUP PLC risk management supplement

LEGAL & GENERAL GROUP PLC 2017 risk management supplement Supplement contents Within this supplement we set out descriptions of the risks we face, how our risk management framework operates, as well as

LEGAL & GENERAL GROUP PLC 2017 risk management supplement Supplement contents Within this supplement we set out descriptions of the risks we face, how our risk management framework operates, as well as

Skip to the content Skip to the menu Skip to the search. Home News EPF News. + Share. Latest Q&As on the USS 11 August 2014

Skip to the content Skip to the menu Skip to the search Home News EPF News + Share Latest Q&As on the USS 11 August 2014 Employers are aware that the triennial valuation of the USS as at 31 March 2014

Skip to the content Skip to the menu Skip to the search Home News EPF News + Share Latest Q&As on the USS 11 August 2014 Employers are aware that the triennial valuation of the USS as at 31 March 2014

Basel II Briefing: Pillar 2 Preparations. Considerations on Pillar 2 for Subsidiary Banks

Basel II Briefing: Pillar 2 Preparations Considerations on Pillar 2 for Subsidiary Banks November 2006 Preamble Those studying this document should be aware that because of the nature of the technical

Basel II Briefing: Pillar 2 Preparations Considerations on Pillar 2 for Subsidiary Banks November 2006 Preamble Those studying this document should be aware that because of the nature of the technical

Pension Scheme Cyber Resilence Workshop

Pension Scheme Cyber Resilence Workshop Cyber Resilience Workshop Pension schemes hold substantial amounts of personal data, have regular financial transactions, and are managed by trustees who often

Pension Scheme Cyber Resilence Workshop Cyber Resilience Workshop Pension schemes hold substantial amounts of personal data, have regular financial transactions, and are managed by trustees who often

Telefónica UK Pension Plan. Statement of Investment Principles

Telefónica UK Pension Plan Statement of Investment Principles Introduction Under the Pensions Act 1995 (as updated by the Pensions Act 2004), the Telefónica UK Pension Trustee ( the Trustee ) is required

Telefónica UK Pension Plan Statement of Investment Principles Introduction Under the Pensions Act 1995 (as updated by the Pensions Act 2004), the Telefónica UK Pension Trustee ( the Trustee ) is required

Back to the Future What yesterday can tell us about tomorrow s pensions

Back to the Future What yesterday can tell us about tomorrow s pensions Mark Rowlinson FIA 18 June 2013 Opening comments Defined contribution benefit pensions Current Good efficient funding framework outcomes

Back to the Future What yesterday can tell us about tomorrow s pensions Mark Rowlinson FIA 18 June 2013 Opening comments Defined contribution benefit pensions Current Good efficient funding framework outcomes

PRINCIPLES FOR RISK MANAGEMENT IN NORGES BANK INVESTMENT MANAGEMENT

PRINCIPLES FOR RISK MANAGEMENT IN NORGES BANK INVESTMENT MANAGEMENT LAID DOWN BY THE EXECUTIVE BOARD 10 JUNE 2009 LAST AMENDED 18 MARCH 2015 1. PURPOSE AND OBJECTIVES The Executive Board recognises that

PRINCIPLES FOR RISK MANAGEMENT IN NORGES BANK INVESTMENT MANAGEMENT LAID DOWN BY THE EXECUTIVE BOARD 10 JUNE 2009 LAST AMENDED 18 MARCH 2015 1. PURPOSE AND OBJECTIVES The Executive Board recognises that

PRINCIPLES FOR RISK MANAGEMENT IN NORGES BANK INVESTMENT MANAGEMENT LAID DOWN BY THE EXECUTIVE BOARD 10 JUNE 2009, LAST AMENDED 21 NOVEMBER 2018

PRINCIPLES FOR RISK MANAGEMENT IN NORGES BANK INVESTMENT MANAGEMENT LAID DOWN BY THE EXECUTIVE BOARD 10 JUNE 2009, LAST AMENDED 21 NOVEMBER 2018 1. Purpose and objective These principles represent our

PRINCIPLES FOR RISK MANAGEMENT IN NORGES BANK INVESTMENT MANAGEMENT LAID DOWN BY THE EXECUTIVE BOARD 10 JUNE 2009, LAST AMENDED 21 NOVEMBER 2018 1. Purpose and objective These principles represent our

Risk category Category description Risk appetite

V. RISK MANAGEMENT Doing business inherently involves taking risks. By managing these risks, TNT strives to secure a sustainable performance. Therefore, TNT operates a risk management framework that allows

V. RISK MANAGEMENT Doing business inherently involves taking risks. By managing these risks, TNT strives to secure a sustainable performance. Therefore, TNT operates a risk management framework that allows

Capital Requirements Directive Pillar 3 Disclosure. June 2017

Capital Requirements Directive Pillar 3 Disclosure June 2017 1. Background The purpose of this document is to outline the Pillar 3 disclosures for BlueBay Asset Management LLP ( LLP ). LLP is a subsidiary

Capital Requirements Directive Pillar 3 Disclosure June 2017 1. Background The purpose of this document is to outline the Pillar 3 disclosures for BlueBay Asset Management LLP ( LLP ). LLP is a subsidiary

Enterprise Risk Management (ERM) Module 3.0 (CERA/FSA)

Module 3.0 (CERA/FSA)") FSA QFI, INDIVIDUAL LIFE AND ANNUITIES, RETIRMEMENT BENEFITS, GENERAL INSURANCE TRACKS CERA ALL TRACKS Enterprise Risk Management (ERM) Module 3.0 (CERA/FSA) SECTION 1: MODULE OVERVIEW Quick! Try to name

FSA QFI, INDIVIDUAL LIFE AND ANNUITIES, RETIRMEMENT BENEFITS, GENERAL INSURANCE TRACKS CERA ALL TRACKS Enterprise Risk Management (ERM) Module 3.0 (CERA/FSA) SECTION 1: MODULE OVERVIEW Quick! Try to name

World Bank / IFC Global Insurance Conference. Challenging aspects of Solvency II and the Own Risk Solvency Assessment (ORSA)

") World Bank / IFC Global Insurance Conference Challenging aspects of Solvency II and the Own Risk Solvency Assessment (ORSA) Mehmet Ogut 1 June 2011 Challenging aspects of Solvency II Disagreements over

World Bank / IFC Global Insurance Conference Challenging aspects of Solvency II and the Own Risk Solvency Assessment (ORSA) Mehmet Ogut 1 June 2011 Challenging aspects of Solvency II Disagreements over

Quantitative and Qualitative Disclosures about Market Risk.

Item 7A. Quantitative and Qualitative Disclosures about Market Risk. Risk Management. Risk Management Policy and Control Structure. Risk is an inherent part of the Company s business and activities. The

Item 7A. Quantitative and Qualitative Disclosures about Market Risk. Risk Management. Risk Management Policy and Control Structure. Risk is an inherent part of the Company s business and activities. The

Implementation of Basel II in Guernsey. This paper summarizes the key points in the first year (Year 1) of the implementation of Basel II in Guernsey.

of the implementation of Basel II in Guernsey.") Implementation of Basel II in Guernsey Introduction This paper summarizes the key points in the first year (Year 1) of the implementation of Basel II in Guernsey. Section I considers the impact of regulatory

Implementation of Basel II in Guernsey Introduction This paper summarizes the key points in the first year (Year 1) of the implementation of Basel II in Guernsey. Section I considers the impact of regulatory

Recommendation 1 trustees power to demand timely information

Rt Hon Frank Field MP Chair of Work & Pensions Select Committee House of Commons London SW1A 0AA 20 February 2017 Dear Mr Field, This letter is The Pensions Regulator s (TPR) response to the Work & Pensions

Rt Hon Frank Field MP Chair of Work & Pensions Select Committee House of Commons London SW1A 0AA 20 February 2017 Dear Mr Field, This letter is The Pensions Regulator s (TPR) response to the Work & Pensions

USS Valuation Questions and Answers

USS Valuation Questions and Answers Contents Understanding USS... 3 What kind of pension scheme is USS?... 3 USS currently offers defined benefit pensions, what does this mean?... 3 Who funds USS?... 3

USS Valuation Questions and Answers Contents Understanding USS... 3 What kind of pension scheme is USS?... 3 USS currently offers defined benefit pensions, what does this mean?... 3 Who funds USS?... 3