8/3/2016. Presented by: John L Crandell EA MBA CTRS

|

|

|

- Ira Hart

- 5 years ago

- Views:

Transcription

1 Presented by: John L Crandell EA MBA CTRS 1 2 1

2 At the end of this webinar, you should be able to: Understand what Clergy means Understand what a Housing Allowance is Be able to calculate Self Employment tax for Clergy Be able to divide income and expenses between Regular and Self-Employment 3 Additional Reading: Publication 517 Social Security For Members of Clergy Publication 17 Your Federal Income Tax Publication 535 Business Expenses Schedule C Profit or Loss from Business (Sole Prop) Form 2106 Employee Business Expenses 4 2

3 5 F _ I C _ A_ S _ E _ C _ A 6 3

4 7 8 4

5 SECA Tax: Citizens Resident Alien Non-Resident not covered unless by treaty 9 Employment Status for Other Tax Purposes. Even though a member of the clergy is considered a self-employed individual in performing his or her ministerial services for social security tax purposes, he or she may be considered an employee for income tax or retirement plan purposes 10 5

6 Employees and FICA: Wages subject to FICA Form 8274 Church doesn t pay FICA Employee can opt out SECA replaces FICA Earnings above $ Minister or Employee? 12 6

7 13 Ministerial Service: The service you perform in the exercise of your ministry, the duties as required by your religious order, or the profession as a Christian Science practitioner or reader. 14 7

8 15 Two Ways to Become Exempt: Form 4361 Form

9 Who: Member of Clergy, Religious Order or Christian Science When: Filed by 2 nd year that: $400 or more Do not have to be consecutive years Retroactive Why: Exempt from FICA/SECA 17 Who: Member of Religious Sect Opposed to accepting public benefits Waive rights to SS & disability payments Commissioner of SS must approve When: Anytime Why: Exempt from FICA/SECA 18 9

10 Overpayments of SE tax: Recovered through 1040X 3 years from due date of return 19 Exempt from SS / SE Taxes if: Timely filed Form nd year made $400 or more Opposed on the basis of religious considerations May still purchase life insurance May participate in nongovernment retirement plan Must be accepted by IRS Decision is irrevocable Must still pay SE tax on self employment 20 10

11 Amounts Included in Gross Income to Figure Net Earnings Salaries and fees for qualified services, Money received for marriages, baptisms, funerals, masses, etc., The value of meals and lodging provided to the taxpayer for the employer s convenience, The fair rental value of a parsonage provided to the taxpayer (including the cost of utilities that are furnished), the rental allowance (including an amount for payment of utilities) paid to the taxpayer, and Any amount a church pays toward the taxpayer s income tax or SE tax, other than withholding from the taxpayer s salary. This amount is also subject to income tax. 21 Housing Allowance: Represents Compensation Does not exceed compensation Represents actual payments Does not exceed agreement Does not exceed FRV + Utilities 22 11

Structural Repairs and Remodeling Yard Maintenance & Improvements")

HOA Fees Down payment if paid after occupied 23 Housing Allowance Housing Costs: FRV Mortgage $15,000 Rent")

12 Housing Expenses: Mortgage Payments Rent for home, storage, garage Real Estate Taxes Property Insurance Utilities Furnishings & Appliances (Purchase & Repair) Structural Repairs and Remodeling Yard Maintenance & Improvements General Maintenance (pest control, etc.) HOA Fees Down payment if paid after occupied 23 Housing Allowance Housing Costs: FRV Mortgage $15,000 Rent $18,000 Utilities $3,000 Utilities $3,000 Maintenance $3,600 $30,000 $21,600 $21,

13 Retired Ministers: May exclude from gross income the fair rental value of a home, plus utilities, furnished by a church as a part of the minister s pay for past services or the part of the minister s pension that was designated as a rental allowance. 25 Salary $30,000 Housing Allowance $10,000 Housing Costs $9,000 Fair Rental Value $12,000 Exclude Lower of the 3 $9,000 Add extra to Income $1,

14

15

16

17 33 Evangelical or Traveling Clergy is: Ordained, Commissioned and/or Licensed Not assigned to any church Is an Independent Contractor 34 17

18 7 Questions Emp./SE status: 1.The degree of control 2.Who has facilities 3.Opportunity for profit / loss 4.Can one party fire other 5.Is work part of regular business 6.How permanent is the relationship 7.Relationship parties believe they have 35 18

19 37 Self Employment Activities: Speaking Weddings Funerals 38 19

20 Item Amount W2 $30,000 Housing $10,000 Self Employment $2,000 Expenses ($3500 / $500) $4, Employee: Accountable Plan Non-Accountable Plan 2106 Self Employed: Schedule C 40 20

21

22 Business Code:

All")

23 It s Not All Deductible! 45 Tax Free Rental or Parsonage Allowance (or other tax free income) All Income (taxable & tax free) earned from the ministry 23

24 47 24

25

26 51 How do they pay their taxes? 52 26

27 Who can help with my taxes? 1. MFJ 2. 2 children 3. TP $76K Salary 4. SP $45K Salary 5. HA $26K 6. SE $ Love Gift $ Excess LI $ Education Costs 10. SE Expenses

28

29

30 59 Any other number will not calculate tax free income After tax free calculation 60 30

31 61 Re-issue Send W2 Send to all agencies Put on Schedule C Enter total as expense Enter on Line

32 IRS audit guide tell examiners to look for: Tax-preparers incorrectly figuring the tax free housing allowance and failing to pay SECA tax on it. Deducting business expenses that are attributed to tax-exempt income

Minister Taxes San Jacinto Baptist Association October 2014

Minister Taxes San Jacinto Baptist Association October 2014 Minister Criteria Credential - Licensed - Commissioned or - Ordained Performance - Conduct of religious worship - Administration & maintenance

Minister Taxes San Jacinto Baptist Association October 2014 Minister Criteria Credential - Licensed - Commissioned or - Ordained Performance - Conduct of religious worship - Administration & maintenance

Taxable income (Federal and Social Security) The following are various types of income commonly found on a priest s tax filing:

The following are various types of income commonly found on a priest s tax filing:") Diocese of Madison Policy for Priest Compensation Taxable income (Federal and Social Security) The following are various types of income commonly found on a priest s tax filing: A. Salary and Supplements

Diocese of Madison Policy for Priest Compensation Taxable income (Federal and Social Security) The following are various types of income commonly found on a priest s tax filing: A. Salary and Supplements

Clergy ************************************************************************

Clergy Contents In this webinar, the student will learn the tax treatment of income received by a minister. Objectives After completing this webinar, the student will be able to: Determine if clergy are

Clergy Contents In this webinar, the student will learn the tax treatment of income received by a minister. Objectives After completing this webinar, the student will be able to: Determine if clergy are

Church and Taxes. San Jacinto Baptist Association October 2014

Church and Taxes San Jacinto Baptist Association October 2014 The Affordable Care Act 1. Health FSA (flexible spending accounts) capped $2,500 2. Modified the itemized deduction for medical expenses increased

Church and Taxes San Jacinto Baptist Association October 2014 The Affordable Care Act 1. Health FSA (flexible spending accounts) capped $2,500 2. Modified the itemized deduction for medical expenses increased

Part 4. Comprehensive Examples and Forms Example One: Active minister

Part 4. Comprehensive Examples and Forms Example One: Active minister Note: This example is based on an illustrated example contained at the end of IRS Publication 517. Rev. John Michaels is the minister

Part 4. Comprehensive Examples and Forms Example One: Active minister Note: This example is based on an illustrated example contained at the end of IRS Publication 517. Rev. John Michaels is the minister

TABLE OF CONTENTS. Overview Who Qualifies for Special Tax Treatment as a Minister Income to Be Reported The Parsonage Allowance...

TABLE OF CONTENTS Overview... 1 Who Qualifies for Special Tax Treatment as a Minister... 2 Income to Be Reported... 5 The Parsonage Allowance... 6 Business Expenses... 11 Self-Employment Tax: Exemption...

TABLE OF CONTENTS Overview... 1 Who Qualifies for Special Tax Treatment as a Minister... 2 Income to Be Reported... 5 The Parsonage Allowance... 6 Business Expenses... 11 Self-Employment Tax: Exemption...

CONGREGATIONAL/MINISTERIAL INCOME TAX GUIDELINES

CONGREGATIONAL/MINISTERIAL INCOME TAX GUIDELINES Updated For 2016 Tax Returns By Carl A. Hess The new year brings a reminder that tax season is also here and deserves our attention. This document is to

CONGREGATIONAL/MINISTERIAL INCOME TAX GUIDELINES Updated For 2016 Tax Returns By Carl A. Hess The new year brings a reminder that tax season is also here and deserves our attention. This document is to

Church and Taxes. San Jacinto Baptist Association October 2015

Church and Taxes San Jacinto Baptist Association October 2015 Updates for 2015 1. Standard mileage rate 56 cents per mile, 14 cents charity 2. $18,000 maximum contribution deferral to 403(b) or 401(k)

Church and Taxes San Jacinto Baptist Association October 2015 Updates for 2015 1. Standard mileage rate 56 cents per mile, 14 cents charity 2. $18,000 maximum contribution deferral to 403(b) or 401(k)

Part 4. Comprehensive Example and Sample Forms Example One: Senior Minister

Part 4. Comprehensive Example and Sample Forms Example One: Senior Minister Note: This example is based on an illustrated example contained at the end of IRS Publication 517. Rev. John Michaels is the

Part 4. Comprehensive Example and Sample Forms Example One: Senior Minister Note: This example is based on an illustrated example contained at the end of IRS Publication 517. Rev. John Michaels is the

Bus. Admin: Ministers Tax Issues Course #E913

Bus. Admin: Ministers Tax Issues Course #E913 Presented by: Stephanie Buduhan, CPA PSK LLP 2018 Shelby Systems, Inc. Other brand and product names are trademarks or registered trademarks of the respective

Bus. Admin: Ministers Tax Issues Course #E913 Presented by: Stephanie Buduhan, CPA PSK LLP 2018 Shelby Systems, Inc. Other brand and product names are trademarks or registered trademarks of the respective

TAXATION OF CLERGY & OTHER CALLED WORKERS

TAXATION OF CLERGY & OTHER CALLED WORKERS January 2017 Presented by David Mellem, EA This text is written to provide accurate and authoritative information regarding the subject matter. The information

TAXATION OF CLERGY & OTHER CALLED WORKERS January 2017 Presented by David Mellem, EA This text is written to provide accurate and authoritative information regarding the subject matter. The information

Minister Tax Law. Topics Unique to Ministers. Important Tax Cases and IRS Rulings 8/5/2015

Minister Tax Law Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation August 5, 2015 Topics Unique to Ministers Income Issue: Parsonage/Housing Allowance Gift or Compensation SE Issue:

Minister Tax Law Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation August 5, 2015 Topics Unique to Ministers Income Issue: Parsonage/Housing Allowance Gift or Compensation SE Issue:

Internal Revenue Code Section 1402(a)(5)(A) Definitions.

(5)(A) Definitions.") Internal Revenue Code Section 1402(a)(5)(A) Definitions. CLICK HERE to return to the home page (a) Net earnings from self-employment. The term "net earnings from self-employment" means the gross income

Internal Revenue Code Section 1402(a)(5)(A) Definitions. CLICK HERE to return to the home page (a) Net earnings from self-employment. The term "net earnings from self-employment" means the gross income

CLERGY TAX & BENEFITS SEMINAR. Insight Into the World of Clergy Taxes and Benefits

CLERGY TAX & BENEFITS SEMINAR Insight Into the World of Clergy Taxes and Benefits AGENDA Welcome and Prayer Introductions & Overview Clergy Compensation Clergy Benefits Other Tax Matters Q&A 2 Clergy Tax

CLERGY TAX & BENEFITS SEMINAR Insight Into the World of Clergy Taxes and Benefits AGENDA Welcome and Prayer Introductions & Overview Clergy Compensation Clergy Benefits Other Tax Matters Q&A 2 Clergy Tax

New IRS Audit Guidelines for Ministers

New IRS Audit Guidelines for Ministers In April 2009 the IRS released the new audit guidelines for ministers. Now this doesn t necessarily mean that ministers will be targets of audits in 2010 but it could

New IRS Audit Guidelines for Ministers In April 2009 the IRS released the new audit guidelines for ministers. Now this doesn t necessarily mean that ministers will be targets of audits in 2010 but it could

2017 Minister s Tax Organizer Supplement

Please make a copy of this tax organizer for your records before you send to us. 2017 Minister s Tax Organizer Supplement Peachtree Tax Advisors, LLC 500 East Second Street Rome, GA 30161-3112 706-234-7468

Please make a copy of this tax organizer for your records before you send to us. 2017 Minister s Tax Organizer Supplement Peachtree Tax Advisors, LLC 500 East Second Street Rome, GA 30161-3112 706-234-7468

Tax Guide. for Ministers. Filing Year. The Pension Boards United Church of Christ, Inc.

The Pension Boards United Church of Christ, Inc. 2017 Filing Year Tax Guide for Ministers Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Tax Guide for

The Pension Boards United Church of Christ, Inc. 2017 Filing Year Tax Guide for Ministers Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Tax Guide for

Tax Status of Deacons Q&As

Tax Status of Deacons Q&As The following questions and answers are intended to assist deacons and local churches in determining the proper tax treatment of deacons in the United Methodist Church. These

Tax Status of Deacons Q&As The following questions and answers are intended to assist deacons and local churches in determining the proper tax treatment of deacons in the United Methodist Church. These

Income Tax Guide and Organizer for 2017

Income Tax Guide and Organizer for 2017 Email: rwa@blueriver.net Web site: www.rwataxservice.com phone: 812.586.0420 Before doing the booklet, please print out or read the informational sheet as it has

Income Tax Guide and Organizer for 2017 Email: rwa@blueriver.net Web site: www.rwataxservice.com phone: 812.586.0420 Before doing the booklet, please print out or read the informational sheet as it has

Letter of Agreement between Clergy and Congregation. Presenter: The Rev. Lee Powers Retired Canon to the Ordinary Diocese of New Jersey

Letter of Agreement between Clergy and Congregation Presenter: The Rev. Lee Powers Retired Canon to the Ordinary Diocese of New Jersey Letters of Agreement Topics explored in this workshop: - Purpose and

Letter of Agreement between Clergy and Congregation Presenter: The Rev. Lee Powers Retired Canon to the Ordinary Diocese of New Jersey Letters of Agreement Topics explored in this workshop: - Purpose and

JANUARY 2017 EMPLOYEE OR INDEPENDENT CONTRACTOR

JANUARY 2017 GUIDELINES TO OBLIGATIONS OF BRANCH CHURCHES AND SOCIETIES TO WITHHOLD FEDERAL INCOME AND SOCIAL SECURITY TAXES AND TO REPORT COMPENSATION; AND OTHER INFORMATION EMPLOYEE OR INDEPENDENT CONTRACTOR

JANUARY 2017 GUIDELINES TO OBLIGATIONS OF BRANCH CHURCHES AND SOCIETIES TO WITHHOLD FEDERAL INCOME AND SOCIAL SECURITY TAXES AND TO REPORT COMPENSATION; AND OTHER INFORMATION EMPLOYEE OR INDEPENDENT CONTRACTOR

Compensation Guidelines

Compensation Guidelines For Rostered Leaders: Ordained Ministers, Associates in Ministry, Deaconesses, and Diaconal Ministers 2016 New England Synod Evangelical Lutheran Church in America Endorsed by Synod

Compensation Guidelines For Rostered Leaders: Ordained Ministers, Associates in Ministry, Deaconesses, and Diaconal Ministers 2016 New England Synod Evangelical Lutheran Church in America Endorsed by Synod

CLERGY TAX LAW SHORT-COURSE Copyright Clergy Financial Resources All Rights Reserved

- 1 - RELIGIOUS EXEMPTIONS Members of religious orders may obtain an exemption from the obligation to pay selfemployment tax if they meet certain requirements. Basically, these requirements are divided

- 1 - RELIGIOUS EXEMPTIONS Members of religious orders may obtain an exemption from the obligation to pay selfemployment tax if they meet certain requirements. Basically, these requirements are divided

The Parsonage Exclusion from Federal Income Tax: Everything You Need to Know

The Parsonage Exclusion from Federal Income Tax: Everything You Need to Know KLR Not-for-Profit Services Group August 2017 www.kahnlitwin.com Boston Newport Providence Shanghai Waltham 888-KLR-8557 TrustedAdvisors@KahnLitwin.com

The Parsonage Exclusion from Federal Income Tax: Everything You Need to Know KLR Not-for-Profit Services Group August 2017 www.kahnlitwin.com Boston Newport Providence Shanghai Waltham 888-KLR-8557 TrustedAdvisors@KahnLitwin.com

Definition of Compensation and Benefits for Rostered Leaders Rocky Mountain Synod Evangelical Lutheran Church in America

Definition of Compensation and Benefits for Rostered Leaders Rocky Mountain Synod Evangelical Lutheran Church in America Now to one who works, wages are not reckoned as a gift but as something due. (Romans

Definition of Compensation and Benefits for Rostered Leaders Rocky Mountain Synod Evangelical Lutheran Church in America Now to one who works, wages are not reckoned as a gift but as something due. (Romans

Ministerial Taxation

Ministerial Taxation Minister s Taxation & Reporting Ministers qualify for four special tax rules: Housing allowance exclusion Self-employed status for social security taxation Exemption from withholding

Ministerial Taxation Minister s Taxation & Reporting Ministers qualify for four special tax rules: Housing allowance exclusion Self-employed status for social security taxation Exemption from withholding

Compensation Guidelines

Compensation Guidelines For Rostered Ministers: Pastors and Deacons 2018 New England Synod Evangelical Lutheran Church in America Proposal to Synod Assembly June 2017 As approved by Synod Council on April

Compensation Guidelines For Rostered Ministers: Pastors and Deacons 2018 New England Synod Evangelical Lutheran Church in America Proposal to Synod Assembly June 2017 As approved by Synod Council on April

Definition of Compensation and Benefits for Rostered Ministers Sierra Pacific Synod Evangelical Lutheran Church in America

Definition of Compensation and Benefits for Rostered Ministers Sierra Pacific Synod Evangelical Lutheran Church in America 1. APPROPRIATE COMPENSATION Rostered ministers (pastors and deacons) are not always

Definition of Compensation and Benefits for Rostered Ministers Sierra Pacific Synod Evangelical Lutheran Church in America 1. APPROPRIATE COMPENSATION Rostered ministers (pastors and deacons) are not always

PART 3 Step-by-Step Tax Return Preparation

PART 3 Step-by-Step Tax Return Preparation TAX FORMS AND SCHEDULES This step-by-step analysis covers these forms and schedules: Form 1040 is the basic document you will use. It summarizes all of your tax

PART 3 Step-by-Step Tax Return Preparation TAX FORMS AND SCHEDULES This step-by-step analysis covers these forms and schedules: Form 1040 is the basic document you will use. It summarizes all of your tax

The Pastor and His Income Tax. For 2015 Tax Year. 38 th

The Pastor and His Income Tax For 2015 Tax Year Our 38 th Year Please Note You must completely fill out the Tax Data Questionnaire (green sheets). Please send your information to us as soon as possible

The Pastor and His Income Tax For 2015 Tax Year Our 38 th Year Please Note You must completely fill out the Tax Data Questionnaire (green sheets). Please send your information to us as soon as possible

Planning Guide. Compensation. V isit. For ministers and church employees. BudgetResources

Compensation Planning Guide V isit www.guidestone.org/ BudgetResources to view this material online along with our other helpful resources. For ministers and church employees Three things you need to know

Compensation Planning Guide V isit www.guidestone.org/ BudgetResources to view this material online along with our other helpful resources. For ministers and church employees Three things you need to know

Chapter 2: Housing Allowance and Parsonage

Chapter 2: Housing Allowance and Parsonage INTRODUCTION...100 ELIGIBILITY...200 HOUSING ALLOWANCE...300 Housing Allowance Income Tax Aspects...310 Tax-free Limits...320 The Designated Amount...321 Use

Chapter 2: Housing Allowance and Parsonage INTRODUCTION...100 ELIGIBILITY...200 HOUSING ALLOWANCE...300 Housing Allowance Income Tax Aspects...310 Tax-free Limits...320 The Designated Amount...321 Use

Housing Allowance and Other Clergy Tax Issues Revised December 2015

By Dennis R. Walsh, CPA Housing Allowance and Other Clergy Tax Issues Revised December 2015 This is a summary of special income tax issues applicable to clergy employed by units of government and serving

By Dennis R. Walsh, CPA Housing Allowance and Other Clergy Tax Issues Revised December 2015 This is a summary of special income tax issues applicable to clergy employed by units of government and serving

PAYROLL AND THE CHURCH 5 THINGS THAT MINISTRIES GET WRONG

PAYROLL AND THE CHURCH 5 THINGS THAT MINISTRIES GET WRONG 1 MINISTRY PAYROLL: IT S COMPLICATED PAYROLL CAN BE COMPLICATED. FOR THAT, THERE S MINISTRYWORKS. Whether you re a small church using a volunteer

PAYROLL AND THE CHURCH 5 THINGS THAT MINISTRIES GET WRONG 1 MINISTRY PAYROLL: IT S COMPLICATED PAYROLL CAN BE COMPLICATED. FOR THAT, THERE S MINISTRYWORKS. Whether you re a small church using a volunteer

Compensation Guidelines

Compensation Guidelines For Rostered Ministers: Pasrs and Deacons 2019 New England Synod Evangelical Lutheran Church in America Approved by Synod Assembly June 2018 Introduction Let the elders who rule

Compensation Guidelines For Rostered Ministers: Pasrs and Deacons 2019 New England Synod Evangelical Lutheran Church in America Approved by Synod Assembly June 2018 Introduction Let the elders who rule

Clergy Compensation Archdiocese of Baltimore Parish/School Management Training April/May 2008

Clergy Compensation Archdiocese of Baltimore Parish/School Management Training April/May 2008 Archdiocese of Baltimore ~ Parish/School Management Training Agenda 1. Tax Treatment 2. Taxable Income 3. Administrative

Clergy Compensation Archdiocese of Baltimore Parish/School Management Training April/May 2008 Archdiocese of Baltimore ~ Parish/School Management Training Agenda 1. Tax Treatment 2. Taxable Income 3. Administrative

2014 COMPENSATION WORKSHEET THE PRESBYTERY OF NEW COVENANT

THE PRESBYTERY OF NEW COVENANT The 2013 Compensation Worksheet is intended to assist clerks, treasurers and pastors as they define and report income to Presbytery, the Board of Pensions and, of course,

THE PRESBYTERY OF NEW COVENANT The 2013 Compensation Worksheet is intended to assist clerks, treasurers and pastors as they define and report income to Presbytery, the Board of Pensions and, of course,

Frequently asked Questions: Donations. General Council of the Assemblies of God Division of the Treasury

Frequently asked Questions: Donations General Council of the Assemblies of God Division of the Treasury 1 FREQUENTLY ASKED QUESTIONS CONCERNING DONATIONS QUESTIONS ADDRESSED IN THIS PAMPHLET What are appropriate

Frequently asked Questions: Donations General Council of the Assemblies of God Division of the Treasury 1 FREQUENTLY ASKED QUESTIONS CONCERNING DONATIONS QUESTIONS ADDRESSED IN THIS PAMPHLET What are appropriate

MEMO #3. Tax and Reporting Procedures for Congregations. Pensions and Benefits USA. Caution! Determine employee classifications accurately.

MEMO #3 Tax and Reporting Procedures for Congregations Pensions and Benefits USA The tax and reporting requirements with which churches must comply often seem to complicate the task of the local church

MEMO #3 Tax and Reporting Procedures for Congregations Pensions and Benefits USA The tax and reporting requirements with which churches must comply often seem to complicate the task of the local church

Accounting for Churches. Jerry L Walker, CPA

Accounting for Churches By Jerry L Walker, CPA TABLE OF CONTENTS Worker Classifications... 1 Do ministers receive special tax treatment?... 1 Who is considered a minister for tax purposes?... 1 Is a part-time

Accounting for Churches By Jerry L Walker, CPA TABLE OF CONTENTS Worker Classifications... 1 Do ministers receive special tax treatment?... 1 Who is considered a minister for tax purposes?... 1 Is a part-time

Orthodox Church in America Tax Help for Parish Treasurers

Orthodox Church in America Tax Help for Parish Treasurers INTRODUCTION Taxes in the United States are complex and consequences for noncompliance can be significant. Furthermore, there are nuances in the

Orthodox Church in America Tax Help for Parish Treasurers INTRODUCTION Taxes in the United States are complex and consequences for noncompliance can be significant. Furthermore, there are nuances in the

Church Tax Issues II: The Church as an Employer E921

Church Tax Issues II: The Church as an Employer E921 Presented by: Stephanie Buduhan PSK 2018 Shelby Systems, Inc. Other brand and product names are trademarks or registered trademarks of the respective

Church Tax Issues II: The Church as an Employer E921 Presented by: Stephanie Buduhan PSK 2018 Shelby Systems, Inc. Other brand and product names are trademarks or registered trademarks of the respective

1 of 14 8/10/ :45 PM

1 of 14 8/10/2016 11:45 PM Publication 503 - Main Content Table of Contents Tests To Claim the Credit Qualifying Person Test Earned Income Test Work-Related Expense Test Joint Return Test Provider Identification

1 of 14 8/10/2016 11:45 PM Publication 503 - Main Content Table of Contents Tests To Claim the Credit Qualifying Person Test Earned Income Test Work-Related Expense Test Joint Return Test Provider Identification

Iowa Annual Conference of the United Methodist Church Table II, Part A Church Assets Report Assets/Liabilities from January 1, to December 31,

Table II, Part A Church Assets Report Assets/Liabilities from January 1, to December 31, District Church Church # Pastor Email: Read the instructions with each line item. Round all figures to the nearest

Table II, Part A Church Assets Report Assets/Liabilities from January 1, to December 31, District Church Church # Pastor Email: Read the instructions with each line item. Round all figures to the nearest

Moving Expenses. Unreimbursed Business Expenses. Became effective January 1, 2018

Became effective January 1, 2018 Moving Expenses Prior law generally deductible, or a non-taxable reimbursement by an employer New law No longer deductible and taxable if paid for or reimbursed by an employer

Became effective January 1, 2018 Moving Expenses Prior law generally deductible, or a non-taxable reimbursement by an employer New law No longer deductible and taxable if paid for or reimbursed by an employer

2018 Compensation Policy

Summary 2018 Compensation Policy It is the policy of Newark Presbytery that its member churches shall provide equitable compensation of pastors and shall meet or exceed the minimum amounts specified for

Summary 2018 Compensation Policy It is the policy of Newark Presbytery that its member churches shall provide equitable compensation of pastors and shall meet or exceed the minimum amounts specified for

Ministerial Compensation:

Ministerial Compensation: Unraveling the Complexities for Lay Leaders UUA Office of Church Staff Finances Rev. Richard Nugent, Director Jan Gartner, Compensation and Staffing Practices Manager March 2017

Ministerial Compensation: Unraveling the Complexities for Lay Leaders UUA Office of Church Staff Finances Rev. Richard Nugent, Director Jan Gartner, Compensation and Staffing Practices Manager March 2017

Church Administration Matters

Church Administration Matters Greg Hickle Minnesota District Secretary/Treasurer Housing Allowances Housing Allowances are perhaps the most common and sometimes the least understood of the benefits that

Church Administration Matters Greg Hickle Minnesota District Secretary/Treasurer Housing Allowances Housing Allowances are perhaps the most common and sometimes the least understood of the benefits that

Part 3. Step-by-Step Tax Return Preparation

Part 3. Step-by-Step Tax Return Preparation TAX FORMS AND SCHEDULES This step-by-step analysis covers these forms and schedules: Form 1040 is the basic document you will use. It summarizes all of your

Part 3. Step-by-Step Tax Return Preparation TAX FORMS AND SCHEDULES This step-by-step analysis covers these forms and schedules: Form 1040 is the basic document you will use. It summarizes all of your

Top 10 Questions that Ministers, Missionaries, and Church Treasurers Ask Tax Preparers (Updated: December 11, 2014)

") Based on our experience, the following are frequent questions asked by ministers, missionaries, church treasurers, and others serving in ministry positions as licensed or ordained ministers. Our answers

Based on our experience, the following are frequent questions asked by ministers, missionaries, church treasurers, and others serving in ministry positions as licensed or ordained ministers. Our answers

Northwestern Pennsylvania Synod, ELCA Compensation Guidelines Compensation Standards for Rostered Leaders

Northwestern Pennsylvania Synod, ELCA Compensation Guidelines Compensation Standards for Rostered Leaders -- 2018 Rostered Leader compensation is to be revisited and renegotiated annually. Compensation

Northwestern Pennsylvania Synod, ELCA Compensation Guidelines Compensation Standards for Rostered Leaders -- 2018 Rostered Leader compensation is to be revisited and renegotiated annually. Compensation

Planning Financial Support. Planning Financial Support. For ministers and church employees. Visit

Planning Financial Support Visit www.guidestone.org for an online version of this workbook or view the Planning Financial Support presentation. For ministers and church employees Well done... M A T T H

Planning Financial Support Visit www.guidestone.org for an online version of this workbook or view the Planning Financial Support presentation. For ministers and church employees Well done... M A T T H

The Arkansas-Oklahoma Synod of the Evangelical Lutheran Church in America August 29, 2016 Guidelines for Pastor s Compensation for the Year 2017

The Arkansas-Oklahoma Synod of the Evangelical Lutheran Church in America August 29, 2016 Guidelines for Pastor s Compensation for the Year 2017 Special points of interest: Recommendation for at least

The Arkansas-Oklahoma Synod of the Evangelical Lutheran Church in America August 29, 2016 Guidelines for Pastor s Compensation for the Year 2017 Special points of interest: Recommendation for at least

P&B. Memo #3. The tax and reporting requirements with which churches must comply. Tax and Reporting Procedures for Congregations

P&B Memo #3 Pensions and Benefits USA, Church of the Nazarene Tax and Reporting Procedures for Congregations The tax and reporting requirements with which churches must comply often seem to complicate

P&B Memo #3 Pensions and Benefits USA, Church of the Nazarene Tax and Reporting Procedures for Congregations The tax and reporting requirements with which churches must comply often seem to complicate

Taxes and Ministers TOPICS: 2011 edition (rev. 10/11) The IRS s definition of minister. Employment status: W-2 or Housing/Parsonage allowance

The IRS s definition of minister. Employment status: W-2 or Housing/Parsonage allowance") Taxes and Ministers 2011 edition (rev. ) TOPICS: The IRS s definition of minister Employment status: W-2 or 1099 Housing/Parsonage allowance Reporting income and expenses Paying federal and state taxes

Taxes and Ministers 2011 edition (rev. ) TOPICS: The IRS s definition of minister Employment status: W-2 or 1099 Housing/Parsonage allowance Reporting income and expenses Paying federal and state taxes

Tax Guide. for Ministers. Filing Year. The Pension Boards United Church of Christ, Inc.

The Pension Boards United Church of Christ, Inc. 2012 Filing Year Tax Guide for Ministers Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Tax Guide for

The Pension Boards United Church of Christ, Inc. 2012 Filing Year Tax Guide for Ministers Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Tax Guide for

Minister Audit Technique Guide

This Guide has been reproduced from the IRS website and is provided here as a convenience. Please refer to the IRS website before relying on the information contained in this Guide, as the IRS may have

This Guide has been reproduced from the IRS website and is provided here as a convenience. Please refer to the IRS website before relying on the information contained in this Guide, as the IRS may have

Legal and Business Issues Pertaining to Church Life

Legal and Business Issues Pertaining to Church Life There are various government entities and businesses with whom an established church will transact business on a regular basis and with whom a new church

Legal and Business Issues Pertaining to Church Life There are various government entities and businesses with whom an established church will transact business on a regular basis and with whom a new church

2011 Tax Return Preparation

2011 Tax Return Preparation and Federal Reporting Guide Tax Guide for 2010 Returns for Ministers Prepared by Richard R. Hammar, J.D., LL.M., CPA Edited by GuideStone Financial Resources of the Southern

2011 Tax Return Preparation and Federal Reporting Guide Tax Guide for 2010 Returns for Ministers Prepared by Richard R. Hammar, J.D., LL.M., CPA Edited by GuideStone Financial Resources of the Southern

Taxes and Ministers 2012 edition (rev. 10/12)

") Taxes and Ministers 2012 edition (rev. ) TOPICS: The IRS s definition of minister Employment status: W-2 or 1099 Housing/Parsonage allowance Reporting income and expenses Paying federal and state taxes

Taxes and Ministers 2012 edition (rev. ) TOPICS: The IRS s definition of minister Employment status: W-2 or 1099 Housing/Parsonage allowance Reporting income and expenses Paying federal and state taxes

TAX RETURN PREPARATION & FEDERAL REPORTING. Ministers Tax Guide for 2015 Returns

Ministers Tax Guide for 2015 Returns 2016 TAX RETURN PREPARATION & FEDERAL REPORTING G U I D E Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2016 Christianity Today

Ministers Tax Guide for 2015 Returns 2016 TAX RETURN PREPARATION & FEDERAL REPORTING G U I D E Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2016 Christianity Today

The Arkansas-Oklahoma Synod of the Evangelical Lutheran Church in America August 24, 2014 Guidelines for Pastor s Compensation for the Year 2014

The Arkansas-Oklahoma Synod of the Evangelical Lutheran Church in America August 24, 2014 Guidelines for Pastor s Compensation for the Year 2014 Special points of interest: Recommendation for at least

The Arkansas-Oklahoma Synod of the Evangelical Lutheran Church in America August 24, 2014 Guidelines for Pastor s Compensation for the Year 2014 Special points of interest: Recommendation for at least

TAX ORGANIZER Tax Year THINGS TO BRING (or send to us if no appointment)

") TAX ORGANIZER - 2018 Tax Year THINGS TO BRING (or send to us if no appointment) NEW CLIENTS ONLY: Copy of prior year tax return. Please provide birthdates and social security numbers for all taxpayers

TAX ORGANIZER - 2018 Tax Year THINGS TO BRING (or send to us if no appointment) NEW CLIENTS ONLY: Copy of prior year tax return. Please provide birthdates and social security numbers for all taxpayers

See separate instructions. Your social security number GREEN BEAN If a joint return, spouse's first name and initial

Form Department of the Treasury - Internal Revenue Service (99) 1040 U.S. Individual Income Tax Return OMB. 1545-0074 For the year Jan. 1-Dec. 31,, or other tax year beginning,, ending, 0 Your first name

Form Department of the Treasury - Internal Revenue Service (99) 1040 U.S. Individual Income Tax Return OMB. 1545-0074 For the year Jan. 1-Dec. 31,, or other tax year beginning,, ending, 0 Your first name

Missio Nexus - Missions Finance and Accounting Boot Camp. Orlando, FL

Missio Nexus - Missions Finance and Accounting Boot Camp Orlando, FL Dave Meldrum-Green Tim Sims September 20, 2018 Introductions Missions Finance & Accounting Boot Camp Workshop Description and Objective:

Missio Nexus - Missions Finance and Accounting Boot Camp Orlando, FL Dave Meldrum-Green Tim Sims September 20, 2018 Introductions Missions Finance & Accounting Boot Camp Workshop Description and Objective:

Frequently Asked Questions (FAQs) and Personnel Policies for {Church Name}

and Personnel Policies for {Church Name}") Frequently Asked Questions (FAQs) and Personnel Policies for {Church Name} Purpose: To provide a consolidated and easy to understand set of frequently asked questions and approved personnel policies for

Frequently Asked Questions (FAQs) and Personnel Policies for {Church Name} Purpose: To provide a consolidated and easy to understand set of frequently asked questions and approved personnel policies for

Tax Issues From Volume 2005, Issue Proper treatment of fringe benefits

Tax Issues From Volume 2005, Issue 5-5 2005 Proper treatment of fringe benefits

Tax Issues From Volume 2005, Issue 5-5 2005 Proper treatment of fringe benefits

Pension Plan Member Resource Book

Pension Plan Member Resource Book Issued May 2017 TABLE OF CONTENTS INTRODUCTION... 1 A. Our Common Mission: Caring and Support... 1 B. Caution.... 1 WHAT KEY DEFINITIONS DO I NEED TO KNOW?... 1 PARTICIPATION...

Pension Plan Member Resource Book Issued May 2017 TABLE OF CONTENTS INTRODUCTION... 1 A. Our Common Mission: Caring and Support... 1 B. Caution.... 1 WHAT KEY DEFINITIONS DO I NEED TO KNOW?... 1 PARTICIPATION...

Tax Guide Appendix

ThePe ns i onboa r ds Uni t e dchur c hofchr i s t,i nc. 2 0 1 8 F i l i ngye a r T a xg u i d e f ormi ni s t e r s Pr e pa r e dbychur c hl a w &T a xre por t Publ i s he dbythepe ns i onboa r ds Uni

ThePe ns i onboa r ds Uni t e dchur c hofchr i s t,i nc. 2 0 1 8 F i l i ngye a r T a xg u i d e f ormi ni s t e r s Pr e pa r e dbychur c hl a w &T a xre por t Publ i s he dbythepe ns i onboa r ds Uni

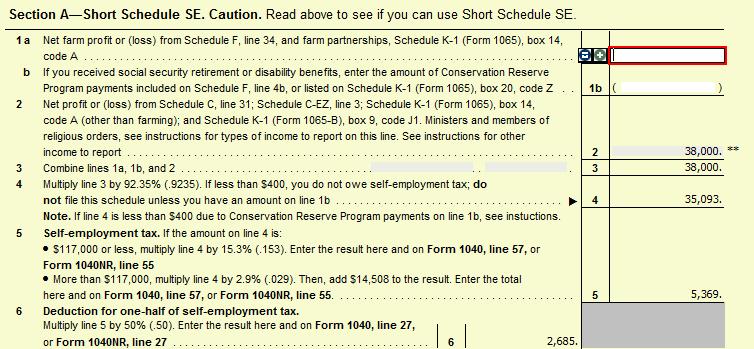

2018 Instructions for Schedule SE (Form 1040)

") Department of the Treasury Internal Revenue Service 2018 Instructions for Schedule SE (Form 1040) Self-Employment Tax Use Schedule SE (Form 1040) to figure the tax due on net earnings from self-employment.

Department of the Treasury Internal Revenue Service 2018 Instructions for Schedule SE (Form 1040) Self-Employment Tax Use Schedule SE (Form 1040) to figure the tax due on net earnings from self-employment.

Example Two: Retired Minister

Example Two: Retired Minister Form 1040 Rev. William K. Green is a retired minister. He is 69 years old. He is married to Sarah J. Green. She is 65 years old and is also retired. For 2010, Rev. Green received

Example Two: Retired Minister Form 1040 Rev. William K. Green is a retired minister. He is 69 years old. He is married to Sarah J. Green. She is 65 years old and is also retired. For 2010, Rev. Green received

Authorized Ministers Compensation Guidelines for a Part-Time Call

Authorized Ministers Compensation Guidelines for a Part-Time Call 2017-2018 1 INTRODUCTION 3 FAITH FOUNDATIONS 3 CONSIDERATIONS 3 THREE MODELS OF PART-TIME MINISTRY 4 DEFINITIONS (MESA CALL AGREEMENT PP.4-6)

Authorized Ministers Compensation Guidelines for a Part-Time Call 2017-2018 1 INTRODUCTION 3 FAITH FOUNDATIONS 3 CONSIDERATIONS 3 THREE MODELS OF PART-TIME MINISTRY 4 DEFINITIONS (MESA CALL AGREEMENT PP.4-6)

Alien Tax Home Representation Form

Alien Tax Home Representation Form I have reviewed the attached tax home information for aliens and/or have consulted with my tax advisor and make the following good faith representation (please check

Alien Tax Home Representation Form I have reviewed the attached tax home information for aliens and/or have consulted with my tax advisor and make the following good faith representation (please check

MINISTER'S INCOME TAX INFORMATION

MINISTER'S INCOME TAX INFORMATION Introduction The Gospel of Matthew records two episodes where Jesus addresses the issue of paying taxes. The first reference is Matthew 17:24-27. The tax collectors asked

MINISTER'S INCOME TAX INFORMATION Introduction The Gospel of Matthew records two episodes where Jesus addresses the issue of paying taxes. The first reference is Matthew 17:24-27. The tax collectors asked

Congregational Treasurers and Bookkeepers Financial and Accounting Guide

Congregational Treasurers and Bookkeepers Financial and Accounting Guide A resource provided by the Office of the Treasurer of the Evangelical Lutheran Church in America Preface These resources for congregational

Congregational Treasurers and Bookkeepers Financial and Accounting Guide A resource provided by the Office of the Treasurer of the Evangelical Lutheran Church in America Preface These resources for congregational

Benefits. and Expenses. Your Home

Recommended IRS Publication Reading Listt for Part 1: Individuals Publication 17, Your Federal Income Tax Publication 501, Exemptions, Standard Deduction, and Filing Information Publication 971, Innocent

Recommended IRS Publication Reading Listt for Part 1: Individuals Publication 17, Your Federal Income Tax Publication 501, Exemptions, Standard Deduction, and Filing Information Publication 971, Innocent

LOCAL CHURCH REPORT TO THE ANNUAL CONFERENCE

Instructions for Table 1 1 Enter here the figure reported on Line 9 of last year s Local Church Report. Do not use this line to correct the previous year s report. Corrections, if necessary, may be made

Instructions for Table 1 1 Enter here the figure reported on Line 9 of last year s Local Church Report. Do not use this line to correct the previous year s report. Corrections, if necessary, may be made

Tax & Money S E R I E S PREPARING TAX RETURNS FOR CLERGY. Federal, state, and other reporting made easy. by Dan Busby, CPA John Van Drunen, JD, CPA

2 0 1 2 Tax & Money S E R I E S E D I T I O N PREPARING TAX RETURNS FOR CLERGY Federal, state, and other reporting made easy. by Dan Busby, CPA John Van Drunen, JD, CPA The federal tax laws offer you special

2 0 1 2 Tax & Money S E R I E S E D I T I O N PREPARING TAX RETURNS FOR CLERGY Federal, state, and other reporting made easy. by Dan Busby, CPA John Van Drunen, JD, CPA The federal tax laws offer you special

2017 Agricultural Tax Issues. Greg Bouchard for The Ohio State University

2017 Agricultural Tax Issues Greg Bouchard for The Ohio State University A. Income and Deductions p. 1 1. Ag. Income and Expenses 2. NOLs 3. Rental Property 4. Demolition of Structures 5. Marijuana and

2017 Agricultural Tax Issues Greg Bouchard for The Ohio State University A. Income and Deductions p. 1 1. Ag. Income and Expenses 2. NOLs 3. Rental Property 4. Demolition of Structures 5. Marijuana and

Compensation and Benefits Guidelines for Lay and Clergy Employees. Revised October 2014

2015 Compensation and Benefits Guidelines for Lay and Clergy Employees Revised October 2014 Page 2 Page 3 Table of Contents INTRODUCTION... 5 COMPENSATION... 6 COMPENSATION FOR PRIESTS AND TRANSITIONAL

2015 Compensation and Benefits Guidelines for Lay and Clergy Employees Revised October 2014 Page 2 Page 3 Table of Contents INTRODUCTION... 5 COMPENSATION... 6 COMPENSATION FOR PRIESTS AND TRANSITIONAL

2013 Clergy Compensation Guidelines

2013 Clergy Compensation Guidelines Southwestern Washington Synod Evangelical Lutheran Church in America Find this document on the synod website http://www.lutheranssw.org/wp-content/uploads/definition-of-compensation-for-pastor-form1.pdf

2013 Clergy Compensation Guidelines Southwestern Washington Synod Evangelical Lutheran Church in America Find this document on the synod website http://www.lutheranssw.org/wp-content/uploads/definition-of-compensation-for-pastor-form1.pdf

Tax-Deferred Retirement Account Member Resource Book

Tax-Deferred Retirement Account Member Resource Book A benefit under the Issued May 2017 Defined Contribution Retirement Accounts of the Pension Fund of the Christian Church (Disciples of Christ) ("DCRA")

Tax-Deferred Retirement Account Member Resource Book A benefit under the Issued May 2017 Defined Contribution Retirement Accounts of the Pension Fund of the Christian Church (Disciples of Christ) ("DCRA")

LOCAL CHURCH REPORT TO THE ANNUAL CONFERENCE

Instructions for Table 1 1 Enter here the figure reported on Line 9 of last year s Local Church Report. Do not use this line to correct the previous year s report. If possible, this line should be provided

Instructions for Table 1 1 Enter here the figure reported on Line 9 of last year s Local Church Report. Do not use this line to correct the previous year s report. If possible, this line should be provided

Child and Dependent Care Credit. Basics. Form /13/2016. Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation October 12, 2016

Child and Dependent Care Credit Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation October 12, 2016 Basics The client may be able to claim the child and dependent care credit if they

Child and Dependent Care Credit Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation October 12, 2016 Basics The client may be able to claim the child and dependent care credit if they

Ministers Tax Guide for 2017 Returns TAX RETURN PREPARATION. Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report

Ministers Tax Guide for 2017 Returns 2018 TAX RETURN PREPARATION G U I D E Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2018 Christianity Today International. Clergy

Ministers Tax Guide for 2017 Returns 2018 TAX RETURN PREPARATION G U I D E Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2018 Christianity Today International. Clergy

Table of Contents. Introduction... 1 Worker Classification Hobby Loss Rules Specialty Occupations... 33

Table of Contents Introduction... 1 Worker Classification.... 3 Employee vs. Independent Contractor... 3 Factors...4 Misclassified Employees...9 Worker Classification Review Questions...11 Worker Classification

Table of Contents Introduction... 1 Worker Classification.... 3 Employee vs. Independent Contractor... 3 Factors...4 Misclassified Employees...9 Worker Classification Review Questions...11 Worker Classification

[Type here] PRESBYTERY of EASTERN VIRGINIA

![[Type here] PRESBYTERY of EASTERN VIRGINIA](/thumbs/92/110259386.jpg "[Type here] PRESBYTERY of EASTERN VIRGINIA") [Type here] PRESBYTERY of EASTERN VIRGINIA GUIDELINES for FAIR COMPENSATION for INSTALLED PASTORS, COMMISSIONED RULING ELDERS and CERTIFIED CHRISTIAN EDUCATORS 2019 This document was approved by COM on

[Type here] PRESBYTERY of EASTERN VIRGINIA GUIDELINES for FAIR COMPENSATION for INSTALLED PASTORS, COMMISSIONED RULING ELDERS and CERTIFIED CHRISTIAN EDUCATORS 2019 This document was approved by COM on

Filing status: Single Married filing jointly Married filing separately Head of household Qualifying widow(er)

") -Internal Revenue Service (99) 1040 U.S. Individual Income Tax Return 018 IRS Use Only-Do not write or staple in this space. Filing status: Single Married filing jointly Married filing separately Head

-Internal Revenue Service (99) 1040 U.S. Individual Income Tax Return 018 IRS Use Only-Do not write or staple in this space. Filing status: Single Married filing jointly Married filing separately Head

Payment Options. Disability

Payment Options Disability Choosing your payment option Information in this brochure is provided to assist you in understanding your pay ment options and the Disability Retirement Income Estimate(s).

Payment Options Disability Choosing your payment option Information in this brochure is provided to assist you in understanding your pay ment options and the Disability Retirement Income Estimate(s).

PERSONNEL POLICIES FOR CLERGY

PERSONNEL POLICIES FOR CLERGY PRESBYTERY OF LOS RANCHOS These policies have been developed as a means of providing for the Sessions of the Los Ranchos Presbytery, a uniform set of personnel policies to

PERSONNEL POLICIES FOR CLERGY PRESBYTERY OF LOS RANCHOS These policies have been developed as a means of providing for the Sessions of the Los Ranchos Presbytery, a uniform set of personnel policies to

UNITED STATES DISTRICT COURT WESTERN DISTRICT OF WISCONSIN. V. Case No. 11-CV-626 COMPLAINT

UNITED STATES DISTRICT COURT WESTERN DISTRICT OF WISCONSIN FREEDOM FROM RELIGION FOUNDATION, INC.; ANNIE LAURIE GAYLOR; ANNE NICOL GAYLOR; and DAN BARKER, Plaintiffs, V. Case No. 11-CV-626 TIMOTHY GEITHNER,

UNITED STATES DISTRICT COURT WESTERN DISTRICT OF WISCONSIN FREEDOM FROM RELIGION FOUNDATION, INC.; ANNIE LAURIE GAYLOR; ANNE NICOL GAYLOR; and DAN BARKER, Plaintiffs, V. Case No. 11-CV-626 TIMOTHY GEITHNER,

Central/Southern Illinois Synod, ELCA Compensation Guidelines for Rostered Leaders 2018

Central/Southern Illinois Synod, ELCA Compensation Guidelines for Rostered Leaders 2018 Contents: Presented by the Leadership Support Subcommittee of the Professional and Lay Ministry Committee and approved

Central/Southern Illinois Synod, ELCA Compensation Guidelines for Rostered Leaders 2018 Contents: Presented by the Leadership Support Subcommittee of the Professional and Lay Ministry Committee and approved

Penn West Conference 2019 Pastoral Compensation Guidelines

Penn West Conference 2019 Pastoral Compensation Guidelines In accordance with action taken by delegates to the 33 rd Annual Meeting of the Penn West Conference, the Conference Church and Ministry Committee

Penn West Conference 2019 Pastoral Compensation Guidelines In accordance with action taken by delegates to the 33 rd Annual Meeting of the Penn West Conference, the Conference Church and Ministry Committee

Federal Reporting Requirements for Churches

Federal Reporting Requirements for Churches Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, CHURCH LAW & TAX REPORT Copyright 2013 Christianity Today International. Federal Reporting Requirements

Federal Reporting Requirements for Churches Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, CHURCH LAW & TAX REPORT Copyright 2013 Christianity Today International. Federal Reporting Requirements

LEADERSHIP SUPPORT GUIDELINES 2018

LEADERSHIP SUPPORT GUIDELINES 2018 FOR ELCA CLERGY FOR USE WITHIN THE NORTHEASTERN PENNSYLVANIA SYNOD 2354 GROVE ROAD ALLENTOWN, PA 18109 PHONE: 610.266.5101 We are pleased to share with you the 2018 recommended

LEADERSHIP SUPPORT GUIDELINES 2018 FOR ELCA CLERGY FOR USE WITHIN THE NORTHEASTERN PENNSYLVANIA SYNOD 2354 GROVE ROAD ALLENTOWN, PA 18109 PHONE: 610.266.5101 We are pleased to share with you the 2018 recommended

PARISH BUDGET GUIDELINES

INTRODUCTION Please read all guidelines before completing your budget. These budget guidelines are to help you in preparing your 2018-19 Budget Certification Form. Every Parish and Mission MUST complete

INTRODUCTION Please read all guidelines before completing your budget. These budget guidelines are to help you in preparing your 2018-19 Budget Certification Form. Every Parish and Mission MUST complete

Federal Reporting Requirements for Churches

Federal Reporting Requirements for Churches Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2014 Christianity Today International. Federal Reporting Requirements

Federal Reporting Requirements for Churches Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2014 Christianity Today International. Federal Reporting Requirements

LOCAL CHURCH REPORT TO THE ANNUAL CONFERENCE

Instructions for Table 1 1 Enter here the figure reported on Line 9 of last year s Local Church Report. Do not use this line to correct the previous year s report. If possible, this line should be provided

Instructions for Table 1 1 Enter here the figure reported on Line 9 of last year s Local Church Report. Do not use this line to correct the previous year s report. If possible, this line should be provided

Penn West Conference 2018 Pastoral Compensation Guidelines

Penn West Conference 2018 Pastoral Compensation Guidelines In accordance with action taken by delegates to the 33 rd Annual Meeting of the Penn West Conference, the Conference Church and Ministry Committee

Penn West Conference 2018 Pastoral Compensation Guidelines In accordance with action taken by delegates to the 33 rd Annual Meeting of the Penn West Conference, the Conference Church and Ministry Committee

CHURCH ASSETS & EXPENSES WORKSHEET

Table 2 of the Local Church Report to the Annual Conference CHURCH ASSETS & EXPENSES WORKSHEET The General Council on Finance and Administration of The United Methodist Church 2013-2016 Quadrennium Revised

Table 2 of the Local Church Report to the Annual Conference CHURCH ASSETS & EXPENSES WORKSHEET The General Council on Finance and Administration of The United Methodist Church 2013-2016 Quadrennium Revised